Viavi Solutions: From Dot-Com Supernova to Quiet Compounder

I. Introduction & Episode Roadmap

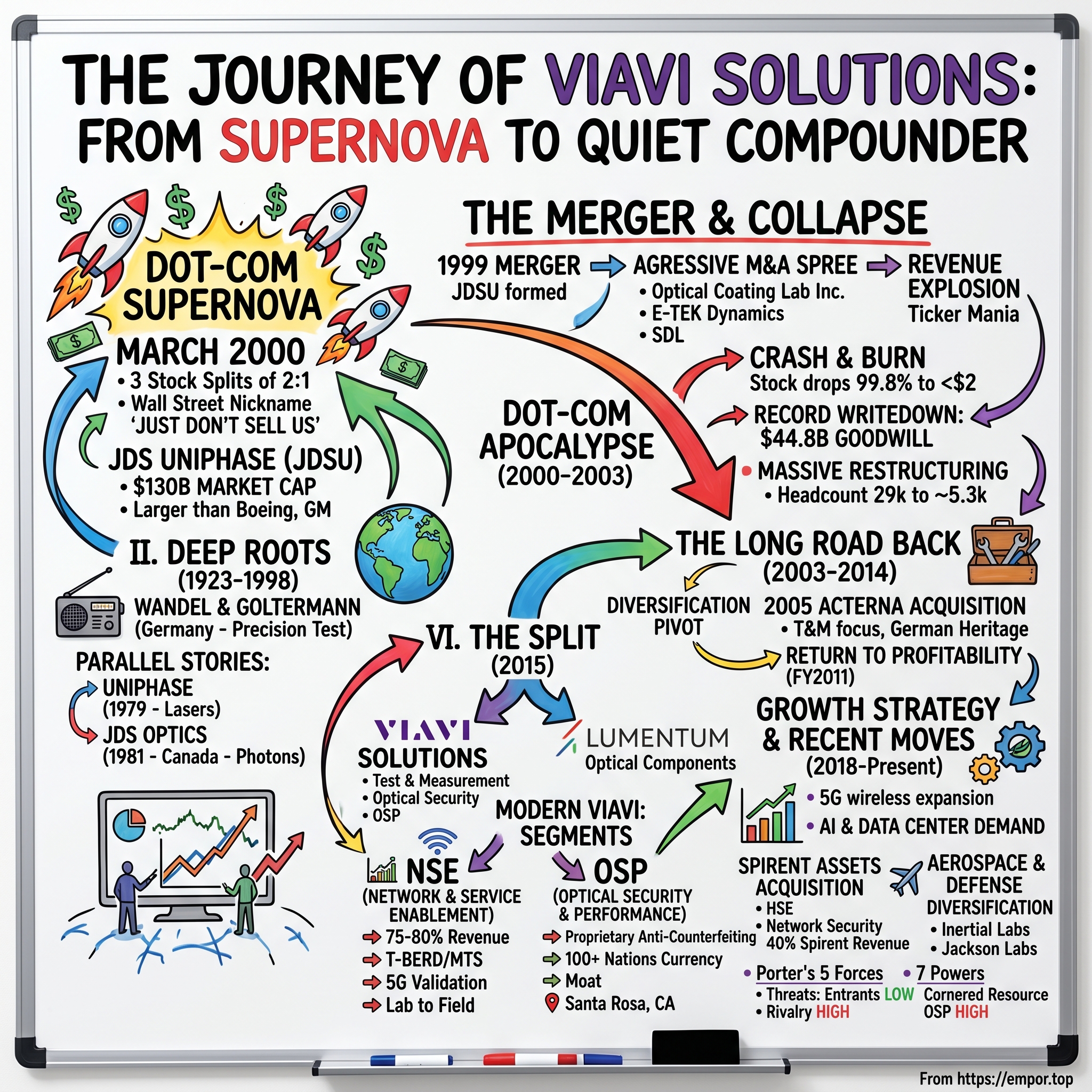

Picture this: It's March 2000, and on trading floors across America, a company called JDS Uniphase has become the most electrifying ticker symbol on the NASDAQ. The stock has just completed its third two-for-one split in six months. Traders who bought shares the previous autumn are up 600%. The company's market capitalization has ballooned to approximately $130 billion—larger than Boeing, larger than General Motors, larger than many nations' entire GDP. Its stock price doubled three times and three stock splits of 2:1 occurred roughly every 90 days during the last half of 1999 through early 2000, making millionaires of many employees who were stock option holders.

The nickname on Wall Street? "Just Don't Sell Us."

Fast forward twenty-five years. That $130 billion company is gone—obliterated in one of the most spectacular crashes in market history. The stock, then known as JDS Uniphase, was one of the highest of the high-flyers at the turn of the century, soaring past $1000 before cratering fast with the dot com crash in 2000. Yet from its ashes emerged something unexpected: two distinct, profitable companies that continue operating today.

One of those successors is Viavi Solutions, headquartered in Chandler, Arizona, with a current market cap of approximately $3 billion. As of late October 2024, Viavi's stock price was around $13.75, with a market cap of $3.07 billion and 223 million shares outstanding. The company operates as a provider of network test, monitoring, and assurance solutions, serving telecommunications operators, enterprises, military organizations, and aerospace companies worldwide.

The central question of this deep dive is perhaps the most fascinating in business history: How does a company survive losing 99.8% of its value and emerge as a quietly profitable niche leader a quarter century later?

This is a powerful story of ambition, collapse, and ultimate reinvention—from the ashes of JDSU to two distinct and successful companies that continue to innovate today: Viavi Solutions and Lumentum.

The answer reveals important lessons about the difference between momentum and fundamentals, about how bubble-era excess creates opportunities for patient capital, and about the underappreciated power of corporate restructuring. This is not a glamorous tech story of hockey-stick growth—it's something more valuable: a study in corporate survival, disciplined reinvention, and the long game of compounding in specialized markets.

II. The Deep Roots: A Century of Telecom Testing (1923–1998)

Long before fiber optics became household terminology, before the internet was even a concept, a small company in Germany was laying the foundation for what would eventually become part of Viavi's DNA. Viavi Solutions traces its roots back to its founding in 1923 as Wandel and Goltermann, a German manufacturer of electronic testing equipment.

The Wandel & Goltermann Legacy

Wandel & Goltermann, an internationally operating manufacturer of test solutions for global communications, was founded in 1923. In an era when radio was the cutting-edge technology transforming society, the company started by manufacturing radios and electronic components. Over the following decades, as telecommunications evolved from simple voice transmission to increasingly complex data networks, Wandel & Goltermann evolved alongside it.

The company built a reputation for German engineering precision—meticulous attention to measurement accuracy that would prove invaluable in the telecommunications industry. By the 1990s, Wandel & Goltermann had become a respected name in telecom testing, with market-oriented test solutions covering all areas of voice, video and data communications.

The merger between Wandel & Goltermann and Wavetek took place September 30, 1998, combining Wandel & Goltermann's leading position in the field of datacoms and telecoms test equipment with Wavetek's strength in test solutions for Cable TV and mobile communications systems. This combination created Wavetek Wandel Goltermann (WWG), a company that would later be absorbed into the telecom testing empire that became part of Viavi.

Parallel Founding Stories: Uniphase & JDS Optics

While the German testing tradition was evolving, two other companies were developing the optical technologies that would form JDSU's core identity. Uniphase was started in 1979 in a San Jose, California garage, and made lasers for chip makers and scanners. Like many legendary tech companies, it began with a simple vision and garage-level resources, capitalizing on the emerging demand for precision lasers in manufacturing applications.

Meanwhile, across the border in Canada, in 1981, JDS Optics was founded in Ottawa, Ontario by Philip Garel-Jones, Gary Duck, Jozef Straus, and Bill Sinclair. The "JDS" is short for Jones, Duck and Straus/Sinclair. These were engineers who had worked at Bell-Northern Research, Canada's premier telecommunications R&D facility, and they understood something critical: the future of communications lay in photons, not electrons.

The company became JDS Fitel when it formed a partnership with Fitel, a fiber optic and optical connector company. This partnership gave JDS access to crucial connector technology and manufacturing capabilities, positioning it at the heart of the emerging fiber-optic revolution.

The Foundational Technology

Understanding JDSU's rise requires understanding why fiber optics mattered so much in the late 1990s. JDSU designed and manufactured critical components—everything from optical amplifiers and modulators to reconfigurable optical add/drop multiplexers (ROADMs)—that were essential for transmitting vast amounts of data over fiber-optic networks. In essence, they built the intricate plumbing that enabled the internet to flow at unimaginable speeds.

These weren't commodity products. Dense wavelength division multiplexing (DWDM) components required precision manufacturing at the nanometer scale. The companies that could produce reliable, high-performance optical components controlled the chokepoint of the entire internet infrastructure buildout.

As the 1990s progressed and internet adoption accelerated, the demand for these components exploded. The late 1990s witnessed an unprecedented surge in internet adoption, creating a market condition that was nothing short of a gold rush for companies involved in networking infrastructure.

The stage was set for a merger that would create the dominant player in optical networking—and one of the most dramatic stock market stories ever told.

III. The Merger That Created a Monster: JDS Uniphase (1999)

The 1999 merger between JDS Fitel and Uniphase wasn't just a business combination—it was the creation of a market phenomenon. In 1999, JDSU was formed by the merger between JDS Fitel and Uniphase, and it became known as JDS Uniphase subsequent to the merger. Kevin Kalkhoven became co-chairman and CEO, while Jozef Straus—one of the original Ottawa founders—became co-chairman, president, and chief operating officer.

The Strategic Logic

The merger made perfect strategic sense. Uniphase brought expertise in active optical components—the lasers and amplifiers that generated and boosted optical signals. JDS Fitel contributed passive components—the filters, switches, and multiplexers that directed and managed those signals. Together, they could offer customers a complete optical networking solution from a single vendor.

Fueled by its core technological leadership and the explosive market demand, JDS Uniphase embarked on a hyper-growth phase, largely driven by an aggressive and audacious Mergers and Acquisitions (M&A) strategy.

The Acquisition Spree

What followed was one of the most aggressive acquisition campaigns in corporate history. Three other major fiber companies were acquired by JDS Uniphase during the telecom boom—Optical Coating Laboratory Inc. (OCLI), bought for $6.2 billion and based in Santa Rosa, California, E-TEK Dynamics, bought for $15 billion, and SDL, bought for $45 billion, both based in San Jose, California.

Consider those numbers for a moment. SDL alone—a company that manufactured pump lasers for optical amplifiers—cost $45 billion. That's more than the market capitalization of many major corporations today. E-TEK Dynamics, which made passive fiber-optic components, went for $15 billion. These weren't leveraged buyouts funded with debt—they were all-stock transactions, paid for with JDSU's stratospheric share price.

The strategic rationale was sound on paper: vertical integration would allow JDSU to control more of the value chain, reduce dependency on outside suppliers, and offer customers integrated solutions. But the prices paid assumed a future of unlimited growth that would never materialize.

Revenue Explosion and Stock Mania

The numbers from this period seem almost fictional today. JDSU's revenue rocketed from $282.8 million in fiscal 1999 to $3.23 billion in fiscal 2001—an eleven-fold increase in just two years. The company became the world's largest supplier of optical components, serving the network equipment giants that were building out global fiber infrastructure.

Its stock price doubled three times and three stock splits of 2:1 occurred roughly every 90 days during the last half of 1999 through early 2000, making millionaires of many employees who were stock option holders, and further enabling JDS Uniphase to go on an acquisition and merger binge.

The momentum became self-reinforcing. Higher stock prices enabled larger acquisitions. Larger acquisitions promised higher growth. Higher growth drove the stock higher still. Professional money managers who didn't own JDSU risked underperforming their benchmarks. Retail investors piled in, convinced they'd found the ticket to early retirement.

At its peak, JDSU's market capitalization reached approximately $130 billion—making it, briefly, one of the most valuable companies on Earth. The Jim Cramer joke among traders was that JDSU stood for "Just Don't Sell Us."

The Canadian Anomaly

Perhaps the most remarkable statistic of all: at its peak, this single Canadian-connected company accounted for roughly 35% of the entire Canadian stock market index, dwarfing the Big Six banks and the oil and gas giants that had traditionally dominated Canadian equities. Fund managers running Canadian equity portfolios had no choice but to own massive positions—diversification became mathematically impossible.

This level of index concentration would become a textbook example of why index-hugging strategies can create systemic risks. When the company fell, it would drag down portfolios across the country.

What investors failed to understand—or chose to ignore—was that JDSU's apparent success was built on two assumptions that would both prove catastrophically wrong: that demand for fiber-optic capacity would continue growing exponentially, and that the stock prices used to make acquisitions reflected sustainable values rather than speculative mania.

IV. The Dot-Com Apocalypse: Crash & Burn (2000–2003)

The collapse came with stunning speed. Employment soon dropped as part of the Global Realignment Program from nearly 29,000 to approximately 5,300, many of its factories and facilities were closed around the world, and the stock price dropped from $153 per share to less than $2 per share.

The Bubble Bursts

The telecom bust of 2000-2002 was uniquely devastating because it exposed the fundamental lie at the heart of the fiber buildout: there was vastly more capacity being installed than demand could possibly fill for years to come. The so-called "dark fiber" problem—miles of fiber-optic cable lying dormant underground—became a symbol of the era's excess.

The turn of the millennium marked a dramatic shift in the global economy, as the euphoria surrounding internet-based companies reached its breaking point.

JDSU's customers—the Nortels and Lucents building fiber networks—found themselves with massive overcapacity and vanishing demand. Orders evaporated. Companies that had been begging for more product suddenly stopped calling. The entire premise underlying JDSU's growth—unlimited bandwidth demand—collapsed.

The Record-Breaking Goodwill Write-Down

What followed was one of the most staggering accounting events in corporate history. In 2001, after the dot-com bubble burst, JDSU wrote $38.7 billion off its books—the entire value of the handful of companies it had purchased over the previous two years.

JDS Uniphase announced a record-breaking goodwill write-down of $44.8 billion. To put this in perspective, that single write-down was roughly equivalent to California's annual K-12 education budget at the time.

The accounting reality was brutal but understandable. When JDSU purchased SDL for $45 billion in stock, it created massive goodwill on its balance sheet—the difference between what it paid and the fair value of SDL's identifiable assets. At the end of its fiscal third quarter on March 31, JDS had $56.2 billion in goodwill, thanks to its acquisition of E-Tek Dynamics, SDL and other companies with lots of intangible assets. Goodwill accounted for a staggering 86 percent of total assets.

When JDSU's own stock collapsed, the company was forced to confront reality: the market no longer believed those acquisitions were worth anywhere close to what had been paid. The company would go back and take a $38.7 billion write-down for the third quarter, plus a $6.1 billion charge for the fourth quarter to reflect a continued fall in its stock price.

The Accounting Perspective

JDSU's management offered a nuanced defense that illuminates an important accounting reality. The company argued that since it used highly valued stock to acquire other companies whose stock was also highly valued, and since both values subsequently collapsed together, the write-down was essentially a paper loss that didn't reflect actual cash destruction.

Their argument goes like this: Since JDS used its highly valued stock to acquire another company whose stock was highly valued, and the value of both companies subsequently collapsed, the write-down should be viewed as a paper loss that, by itself, did not hurt shareholders.

The company maintained that "we have $1.6 billion in cash, and essentially no debt." In other words, the company wasn't going bankrupt—it had simply been forced to acknowledge that acquisitions made during the bubble weren't worth what bubble-era prices suggested.

This is an important distinction. Unlike companies that leveraged themselves to make acquisitions and then faced creditors when values collapsed, JDSU's primarily stock-based acquisition strategy meant the company survived the crash intact, if humiliated.

Massive Restructuring

The human cost was enormous. From nearly 29,000 employees at the peak, headcount plummeted to approximately 5,300 as facilities worldwide were shuttered. In 2003, CEO Straus retired, and the company moved its headquarters to San Jose, California, to consolidate its business.

Investors embraced JDS Uniphase during the dot-com boom but soured on it in 2001 as business spending on telecommunications gear stalled. The company rang up a staggering $50.6 billion net loss in fiscal 2001 and its shares dropped 99 percent.

The stock would continue languishing for years. By November 2008, during the depths of the financial crisis, shares traded just above $2—representing a decline of over 99.8% from the peak. The nickname "Just Don't Sell Us" had transformed into bitter irony: "Just Don't Sue Us."

The company even faced legal challenges. After the 2001 crash of the telecommunications industry, the state of Connecticut filed a lawsuit against the company and four key executives, claiming that they had misled and hid from company shareholders advance knowledge of the company's impending downturn. Unlike most similar lawsuits, which are dismissed or settled before trial, Connecticut's lawsuit went to trial in October 2007. JDSU was acquitted of all charges in November 2007.

The acquittal was meaningful—it vindicated the management team of allegations that they had engaged in fraud. But it couldn't restore the lost billions or the shattered portfolios of investors who had believed in the "new economy" dream.

V. The Long Road Back: Diversification & Acterna (2003–2014)

The decade following the crash was a period of quiet, unglamorous rebuilding. The company that emerged from the wreckage was fundamentally different from the high-flying optical components maker of the bubble era. Rather than trying to recapture past glories, new leadership made a strategic pivot that would ultimately define Viavi's identity.

The Pivotal Acterna Acquisition (2005)

On August 3, 2005, the company acquired test and measurement equipment company Acterna for $760 million, which became part of JDSU's Test and Measurement Group.

The Acterna deal was transformational for several reasons. First, $760 million was a fraction of the bubble-era prices—a realistic valuation that could generate actual returns. Second, it brought JDSU into the test and measurement business, which has fundamentally different economics than component manufacturing.

Acterna had been formed by the May 2000 merger of network test solutions developer Wavetek Wandel Goltermann (WWG) and hand-held test equipment developer TTC. This brought the company full circle back to the German Wandel & Goltermann heritage in precision measurement.

Test and measurement equipment serves a different customer need than optical components. While component sales depend on new network buildouts, test equipment is needed throughout the network lifecycle—during construction, for ongoing maintenance, and for troubleshooting. This creates more stable, recurring revenue streams less dependent on capital spending cycles.

Building a Diversified Portfolio

Throughout the post-crash years, JDSU management methodically built a more diversified business model. Communication products like optical components enable the transmission and transport of video, audio and test data over high-capacity fiber-optic lines. JDSU also makes 3-D glasses, and the company makes lasers, medical and aerospace gear and even helps fight currency counterfeiters.

This diversification strategy was unglamorous but wise. Rather than betting everything on a single technology or market, JDSU spread its risk across multiple segments that had different cyclical patterns.

In December 2013, the company announced it was acquiring fellow network performance management company Network Instruments, for $200 million. This acquisition enhanced software capabilities for enterprise network monitoring—another step away from pure hardware dependency.

Return to Profitability

The company achieved profitability in fiscal 2011, reporting net revenue of $1.8 billion and net income of $217 million, a significant turnaround from prior years' losses driven by cost controls and renewed demand for optical products.

That $217 million profit wasn't spectacular, but it represented something important: proof that a sustainable business existed underneath all the bubble-era wreckage. The company had become what value investors call a "compounder"—not a high-growth rocket ship, but a profitable enterprise generating cash that could be reinvested or returned to shareholders.

By fiscal 2014, pre-split revenue stood at approximately $1.7 billion, with non-GAAP net income reflecting operational improvements of $133 million.

The transformation was real, but Wall Street largely ignored it. The JDSU ticker still carried the stigma of dot-com excess. Institutional investors who'd been burned once weren't eager to return. The stock remained deeply depressed relative to the company's underlying earning power.

This created an opportunity—and management eventually recognized that unlocking value would require a more dramatic restructuring than organic growth could provide.

VI. The Split: Birth of Viavi Solutions (2015)

The decision to split JDSU into two separate companies represents arguably the most transformative event in the company's post-crash history. JDSU announced the division in September 2014. The split ends JDSU's reign as one of the top companies in optical communications technology and test and measurement. The company was extremely aggressive in mergers and acquisitions during the bubble era.

The Strategic Rationale

Why split a company that was finally profitable and stable? The logic reflected a sophisticated understanding of how capital markets value different business types.

Tom Waechter, president and chief executive officer of JDSU, commented, "By operating as two independent companies, we believe Lumentum and Viavi Solutions will each be able to leverage a strong history while being more flexible and better positioned to capitalize on new opportunities in their respective markets."

The reality was that JDSU had become a conglomerate holding two fundamentally different businesses. The optical components business (Lumentum) was capital-intensive, cyclical, and exposed to commodity-like competition. The test and measurement business (Viavi) was lower-capital, more recurring in nature, and served a fragmented market with higher barriers to entry.

Combining them in one company created what's known as a "conglomerate discount"—investors couldn't properly value either business because the financial statements blended them together.

The Separation

The special dividend distribution was effective at 12:01 am on Saturday, August 1, 2015. The distribution was paid on the first trading day thereafter, Monday, August 3, 2015, to JDSU shareholders of record.

Viavi comprises JDSU's test and measurement as well as its Optical Security and Performance (OSP) operations, under the leadership of President and CEO Thomas Waechter. Lumentum's core is the former Communications and Commercial Optical Products (CCOP) business unit. CCOP head Alan Lowe became that company's president and CEO.

For every five shares of JDSU common stock held, shareholders received one share of Lumentum common stock. JDSU was renamed Viavi Solutions Inc. and, at the time of the distribution, retained ownership of approximately 19.9% of Lumentum's outstanding shares. Based on approximately 235.3 million shares of JDSU common stock outstanding as of June 27, 2015, approximately 47.1 million shares of Lumentum common stock were distributed to shareholders.

New Leadership

The newly independent Viavi didn't remain under its initial leadership for long. Interim president and CEO Richard E. Belluzzo stepped in after former chief executive Thomas Waechter departed in August 2015, less than two weeks after Viavi was formed by the separation of JDSU into two separate entities.

Oleg Khaykin joined VIAVI in February 2016 as President and CEO, bringing more than 28 years of industry experience to VIAVI. Khaykin's background was particularly relevant to Viavi's needs. Before VIAVI, Khaykin was President and CEO of International Rectifier from 2008 until its acquisition by Infineon AG in January of 2015.

During his tenure at International Rectifier, he successfully turned around the company and transformed it into the world leader in power semiconductors. This track record of operational improvement and eventual strategic exit made Khaykin an ideal choice for Viavi's next chapter.

Khaykin has also served as Chief Operating Officer of Amkor Technology and Vice President of Strategy & Business Development at Conexant Systems. Earlier in his career he spent eight years with The Boston Consulting Group and prior to that, he was an engineer at Motorola. He holds an MBA from Kellogg School of Management at Northwestern University and a B.S. in Electrical and Computer Engineering with honors from Carnegie-Mellon University.

The combination of engineering depth, strategic consulting experience, and turnaround credentials made Khaykin a CEO who understood both the technical and financial dimensions of Viavi's challenge.

Waechter said in an interview that Viavi would look toward opportunities in the evolution of carrier and data center/enterprise networks toward software-defined networking (SDN) and network functions virtualization (NFV), particularly in enabling network operators to monetize the data they collect.

VII. The Modern Viavi: Business Segments Deep Dive

Understanding Viavi's investment thesis requires understanding its two primary business segments and how they generate value differently.

Business Model Overview

The company operates in two segments, Network and Service Enablement (NSE) and Optical Security and Performance Products (OSP). The NSE segment accounts for roughly 75-80% of revenue, with OSP contributing the remainder.

Network and Service Enablement (NSE)

The NSE segment provides testing, monitoring, assurance, and security solutions that address lab and production environments, network management, service assurance, and AIOps for wireless, wireline, cloud, satellite, public safety, military, and infrastructure networks.

The Network Enablement segment develops testing products for broadband/IP network operators to build and maintain their networks. The products are used in lab and production environments as well as in the field. NE products are divided into wireline, wireless and lab groups.

The company's T-BERD and MTS product families have become industry standards for field testing. A modular design allows migration of fiber test capabilities across VIAVI platforms, including T-BERD/MTS, OneAdvisor and CellAdvisor 5G. This solution offers the most comprehensive range of fiber and service layer tests, from basic fiber certification to automated bi-directional characterization.

What makes this business attractive is its recurring nature. Telecom operators and network equipment manufacturers need test equipment throughout the network lifecycle—during construction for validation, during operation for maintenance, and during troubleshooting for problem resolution. Unlike one-time capital equipment sales, this creates multiple touchpoints and upgrade opportunities.

Optical Security and Performance (OSP)

The OSP segment is genuinely unique and represents an underappreciated competitive moat. The OSP segment utilizes optical coating technology for anti-counterfeiting products, and other optics. The anti-counterfeiting products are Optically Variable Pigment (OVP) and the newer Optically Variable Magnetic Pigment (OVMP).

The OSP overt technology platform is built around expertise in the use of optical and material technologies and decades of experience in authentication to manage light and color to create unique overt and covert effects that cannot be easily replicated or simulated using conventional technologies.

Using proprietary processes, the company manufactures optically variable pigments that are widely used as a strong overt security component to protect the currency of more than 100 nations around the world. The anti-counterfeiting pigments are used on the currency of more than 100 nations.

Think about that for a moment: when you handle paper currency from over 100 countries, you're likely touching Viavi technology. The color-shifting effects you see on modern banknotes—those security features that make counterfeiting difficult—often come from Viavi's Santa Rosa, California facility.

This business traces its lineage back to the Optical Coating Laboratory Inc. (OCLI) acquisition during the bubble era. While most bubble-era acquisitions were disastrous, OCLI has proven to be genuinely valuable, providing decades of stable cash generation.

Key Products & Brands

Beyond the core segments, Viavi offers products under brands including ChromaFlair and SpectraFlair—unique, multi-layer pigment flakes that give paints, coatings, plastics, textiles and packaging the ability to change color when viewed from different angles.

The company also develops optical technology used for a range of applications including material quality control, currency anti-counterfeiting and 3D motion sensing, including Microsoft's Kinect video game controller.

This diversity—from testing fiber networks to preventing currency counterfeiting to enabling 3D sensing—is part of what makes Viavi difficult to categorize but also difficult to disrupt. The company occupies multiple specialized niches rather than competing head-to-head in commoditized markets.

VIII. The 5G Opportunity & Growth Strategy (2018–Present)

The emergence of 5G wireless networks has provided Viavi with its most significant growth catalyst since the post-crash recovery. Unlike the bubble-era fiber buildout, which collapsed under the weight of overcapacity, 5G represents a more sustainable expansion driven by genuine consumer demand for mobile data.

5G as a Growth Driver

Viavi's lab validation includes RANtoCore functional, performance, and conformance testing solutions for interoperable 4G, 5G, and O-RAN wireless communication network elements. Users can emulate thousands of users and different services to exercise and validate the RAN and Core.

Field solutions include antenna alignment, fiber and coax verification, real-time spectrum analysis, X-haul validation, timing & synchronization, EMF analysis and uplink interference detection.

The 5G opportunity is particularly attractive because it requires testing at multiple levels—from laboratory validation of new equipment to field deployment verification to ongoing network monitoring. Viavi's comprehensive portfolio addresses all these needs.

5G is not just wireless—there is fiber in the front-haul, fiber in the back-haul, and then several layers. Viavi addresses layer one through layer seven, and RAN to core, from lab to field, and validation to optimization.

Recent Fiscal Performance

"Fiscal 2024 was a challenging year for VIAVI, as the end market spend environment continued to be anemic throughout the year. For the fourth quarter, revenue came at the mid-point of guidance, with slightly stronger OSP revenues offsetting softer NSE demand. We believe the decline in NSE demand is bottoming out and expect to see gradual recovery in the second half of fiscal 2025," said Oleg Khaykin.

The company's Q1 fiscal 2025 results showed early signs of that recovery. "On a positive side, we are starting to see a pickup in the NSE order momentum with advanced fiber products such as 800G and recently announced 1.6Tb, being particularly strong. This aligns with our expectations for the beginning of NSE demand recovery in second half of FY25," said Khaykin.

Second quarter fiscal 2025 net revenue reached $270.8 million, up $16.3 million or 6.4% year-over-year, with GAAP operating margin of 8.2% and Non-GAAP operating margin of 14.9%, up 170 basis points year-over-year.

"VIAVI's financial performance exceeded expectations, largely driven by recovering NSE demand. We expect that the recovery in our traditional service provider end markets together with our diversification and growth opportunities in new end markets such as the data center ecosystem and aerospace and defense applications will position us favorably for a long term growth cycle," said Khaykin.

Recent Strategic Moves

Viavi has been actively pursuing acquisitions to strengthen its market position. The most significant recent development involved Spirent Communications.

VIAVI Solutions extended an all-cash proposal in March 2024 to acquire Spirent for about $1.3 billion. However, Keysight Technologies made an offer for Spirent Communications, exceeding the earlier bid from Viavi Solutions.

While Viavi lost the bidding war for Spirent's entirety, it gained something valuable through the regulatory process. The proposed settlement required Keysight to divest Spirent's high-speed ethernet testing, network security testing, and RF channel emulation businesses to Viavi, including all tangible and intangible assets necessary to produce and sell these products. Together, these three business lines account for about 40% of Spirent's total revenues.

VIAVI acquired the HSE, Network Security and CE Business for all-cash consideration of $425 million, subject to certain customary closing adjustments. The transaction is expected to add approximately $180 million to VIAVI's Network Service Enablement revenue in the first 12 months after closing and is expected to be accretive to non-GAAP EPS 12 months after closing.

The company also expanded into aerospace and defense through the Inertial Labs acquisition. VIAVI signed a definitive agreement to acquire Inertial Labs, Inc. for initial consideration of $150 million at closing and up to $175 million of contingent consideration over four years. VIAVI intends to fund the transaction through cash on hand.

Headquartered in Leesburg, Virginia, Inertial Labs is a leading developer, producer and supplier of high-performance orientation, positioning and navigation solutions for aerospace, defense and industrial applications. The company offers Inertial Measurement Units (IMU), Inertial Navigation Systems (INS), Assured Position Navigation and Timing (APNT), GNSS Tracking, LiDAR Scanning, Alternative Navigation (ALTNAV) and Visual Navigation solutions.

This marks VIAVI's second major PNT acquisition, following its 2022 purchase of Jackson Labs Technologies. That acquisition brought key technologies such as front-end GNSS receivers, transcoders, and retrofit solutions—along with a strong military customer base—into the VIAVI ecosystem.

VIAVI completed the acquisition of Inertial Labs, Inc. on January 28, 2025.

IX. Recent Financial Performance & Current Position

FY2024-2025 Performance

The most recent fiscal results show a company navigating industry headwinds while maintaining profitability and positioning for recovery. Fourth quarter of fiscal 2024 net revenue was $252.0 million.

As of June 29, 2024, the Company held $496.2 million in total cash, short-term investments and short-term restricted cash. This strong cash position provides significant flexibility for acquisitions and weathering downturns.

The company's fiscal year 2024 revenue declined from the prior year, with full-year revenue of $1 billion, down 9.6% year-over-year, primarily due to conservative spending by service providers and NEMs.

However, recent quarters show improvement. VIAVI reported fiscal Q1 2026 results for the quarter ended September 27, 2025: net revenue of $299.1 million (+25.6% YoY) and non-GAAP operating margin of 15.7% (up 570 bps YoY).

"VIAVI's first quarter financial performance exceeded expectations. Strong demand from the data center ecosystem and aerospace & defense customers was the primary driver behind strong performance. We expect the strong momentum in these end markets to continue through the fiscal year. Additionally, the acquisition of highly complementary Spirent product lines from Keysight is expected to further strengthen our position in the data center ecosystem and significantly increase our business footprint in this high growth market segment," said Khaykin.

Competitive Positioning

VIAVI's primary competitors include Keysight, EXFO, Netscout and others. Viavi's main competitors include Keysight Technologies, Anritsu Corporation, Tektronix, EXFO Inc., and Rohde & Schwarz.

In the rapidly growing 5G test equipment market, Viavi is among the top players alongside Keysight, Anritsu, and Rohde & Schwarz, with particular strength in field testing solutions. The company's diversified portfolio across multiple network technologies and its strong relationships with major service providers and equipment manufacturers provide competitive advantages in a fragmented market.

In the fiber optic test equipment market, EXFO Inc., Anritsu Corporation, VIAVI Solutions Inc, VeEX Inc. and Yokogawa Electric Corporation are the major companies operating in the market.

X. Competitive Analysis & Investment Thesis

Porter's Five Forces Analysis

Threat of New Entrants: LOW The test and measurement industry has significant barriers to entry. Developing reliable, accurate testing equipment requires decades of accumulated expertise and extensive patent portfolios. Customer relationships with major service providers take years to build. Certification and regulatory compliance add additional hurdles.

Bargaining Power of Suppliers: MODERATE Viavi relies on specialized components and manufacturing capabilities, but its technical expertise provides some leverage. The company's vertical integration in optical coatings (OSP segment) reduces supplier dependency in that area.

Bargaining Power of Customers: MODERATE to HIGH Major telecom carriers and network equipment manufacturers are large, sophisticated buyers with significant purchasing power. However, the specialized nature of testing equipment and the cost of switching creates some stickiness.

Threat of Substitutes: LOW There are few substitutes for precision network testing equipment. Software-based solutions can complement but not fully replace physical test instruments for many applications.

Competitive Rivalry: HIGH Competition from Keysight, EXFO, Rohde & Schwarz, and others is intense. However, the market is fragmented enough that multiple players can maintain profitable positions in different niches.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: MODERATE Viavi benefits from scale in manufacturing and R&D amortization, but this advantage is limited compared to larger competitors like Keysight.

Network Effects: LOW Testing equipment doesn't exhibit significant network effects.

Counter-Positioning: MODERATE Viavi's focus on field testing and service provider relationships provides differentiation that larger competitors may be less motivated to match.

Switching Costs: MODERATE to HIGH Customers invest significantly in training, integration, and workflow development around specific testing platforms. Switching involves substantial retraining and workflow disruption.

Branding: MODERATE The T-BERD and MTS brands carry significant recognition in the industry, representing decades of reliability.

Cornered Resource: HIGH (OSP segment) The optical coating expertise and customer relationships in currency authentication represent a genuine cornered resource. This business is protected by decades of accumulated expertise, proprietary processes, and long-term government relationships.

Process Power: MODERATE Manufacturing processes for precision optical equipment require significant accumulated expertise and process refinement.

Bull Case

-

5G and Fiber Everywhere: The ongoing buildout of 5G networks and fiber-to-the-home deployments creates sustained demand for testing equipment. Unlike the bubble-era buildout, this expansion is driven by genuine consumer demand.

-

Data Center Opportunity: Data center operators are increasingly leasing fiber and requiring high-performance standards, which benefits Viavi. The demand for fiber is growing faster than anticipated, driven by the need for high-quality performance and quick activation.

-

AI Infrastructure: AI and data center investments are driving demand for higher-speed fiber interconnects. Data centers are leading the transition to 1.6 terabits, which is expected to boost demand for Viavi's fiber lab and production equipment.

-

Aerospace & Defense Diversification: The Inertial Labs and Jackson Labs acquisitions position Viavi for growth in military and aerospace markets, which have different cyclical patterns than telecom.

-

Spirent Asset Acquisition: The $425 million acquisition of Spirent's high-speed ethernet and network security testing businesses strengthens Viavi's data center portfolio.

Bear Case

-

Telecom CapEx Cyclicality: Service provider capital spending is notoriously cyclical. Downturns in telecom investment directly impact Viavi's core NSE business.

-

Larger Competitors: Keysight Technologies has significantly greater scale and R&D resources. The failed Spirent bid illustrates Viavi's limitations in competing for major acquisitions.

-

Customer Concentration Risk: Major telecom carriers represent significant revenue concentration. Spending decisions by a few large customers can materially impact results.

-

OSP Dependency on Government Contracts: The anti-counterfeiting business depends on long-term government relationships that could shift.

-

Technology Transitions: Shifts toward software-defined networking and cloud-based testing could reduce demand for traditional hardware test equipment.

Key Metrics to Watch

For investors tracking Viavi's ongoing performance, two KPIs are most critical:

-

NSE Segment Revenue Growth: This metric reflects underlying telecom and data center capital spending trends. Positive organic growth indicates healthy end-market demand; declining revenue signals industry headwinds.

-

Non-GAAP Operating Margin: Given the company's history and mix of product and service revenues, operating margin reflects both pricing power and operational efficiency. Management targets mid-teens margins in healthy environments.

XI. Myth vs. Reality

| Myth | Reality |

|---|---|

| "JDSU was a fraud that destroyed shareholder value" | While bubble-era acquisitions were wildly overpriced, the company was acquitted of all securities fraud charges. Management used inflated stock as currency, but didn't engage in accounting manipulation. |

| "The dot-com crash killed JDSU" | The company survived, restructured, and eventually returned to profitability. The split into Viavi and Lumentum has created two viable businesses. |

| "Viavi is just a commodity test equipment maker" | The OSP segment provides genuinely differentiated anti-counterfeiting technology used in currencies of 100+ nations—a business with high barriers to entry. |

| "5G testing is a one-time opportunity" | Network testing is required throughout the lifecycle—deployment, operation, and maintenance—creating recurring demand rather than one-time sales. |

XII. Conclusion

Viavi Solutions represents one of the most remarkable corporate survival stories in technology history. From a peak market capitalization of approximately $130 billion to a crash of 99.8%, and from there to a rebuilt, profitable company worth roughly $3 billion, the journey offers profound lessons about market cycles, corporate resilience, and the value of patient restructuring.

The company today is fundamentally different from the bubble-era JDSU. Rather than a momentum-driven fiber components maker dependent on telecom capital spending booms, Viavi is a diversified provider of test, measurement, and optical security solutions serving multiple end markets with different cyclical patterns.

Viavi Solutions is firmly established as a key player within the telecommunications test and measurement sector and a leader in specific optical technology niches. Its strengths lie in its comprehensive product suite addressing network deployment, monitoring, and optimization, particularly strong in fiber optics testing. The OSP segment provides diversification through anti-counterfeiting solutions and advanced optical filters.

The company's near-term trajectory depends on the pace of 5G and data center infrastructure buildout. Long-term success will require continued innovation in testing technologies as networks evolve toward software-defined architectures and AI-driven operations.

For investors, Viavi represents a case study in how corporate restructuring can unlock value from troubled assets. The bubble-era excess created both the catastrophic collapse and, ultimately, the opportunity to build something durable from the wreckage. Twenty-five years after "Just Don't Sell Us" became the hottest ticker on Wall Street, Viavi quietly persists—not as a rocket ship, but as a specialized technology company generating real profits from real products serving real market needs.

That may not be as exciting as a 600% rally in six months. But for long-term investors, it might be something more valuable: a sustainable business with defensible niches, competent management, and exposure to durable technology trends. In a market obsessed with the next JDSU, there's something to be said for the company that learned from being the original.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube