M&T Bank: Building a Regional Banking Empire Through Prudence and Partnership

I. Introduction & Cold Open

The year is 2008. Lehman Brothers has collapsed. Bear Stearns is gone. Washington Mutual—dead. Wachovia—acquired in distress. Even the mighty Citigroup and Bank of America are on government life support. In boardrooms across America, bank CEOs are making the same grim phone call to their boards: "We need to cut the dividend."

But in a limestone and granite tower in downtown Buffalo, New York, Robert Wilmers is having a different conversation. The 74-year-old CEO of M&T Bank—a regional player most Wall Street analysts couldn't locate on a map—is reviewing his bank's quarterly numbers. They're profitable. Again. Just like they have been every single quarter since Gerald Ford was president.

"We're not cutting the dividend," Wilmers tells his board. In fact, other than Northern Trust in Chicago, M&T would emerge as the only bank in the entire S&P 500 to maintain its dividend throughout the financial crisis. While trillion-dollar banks were being nationalized, this Buffalo institution with working-class roots was quietly proving that boring, relationship-based banking wasn't just alive—it was antifragile.

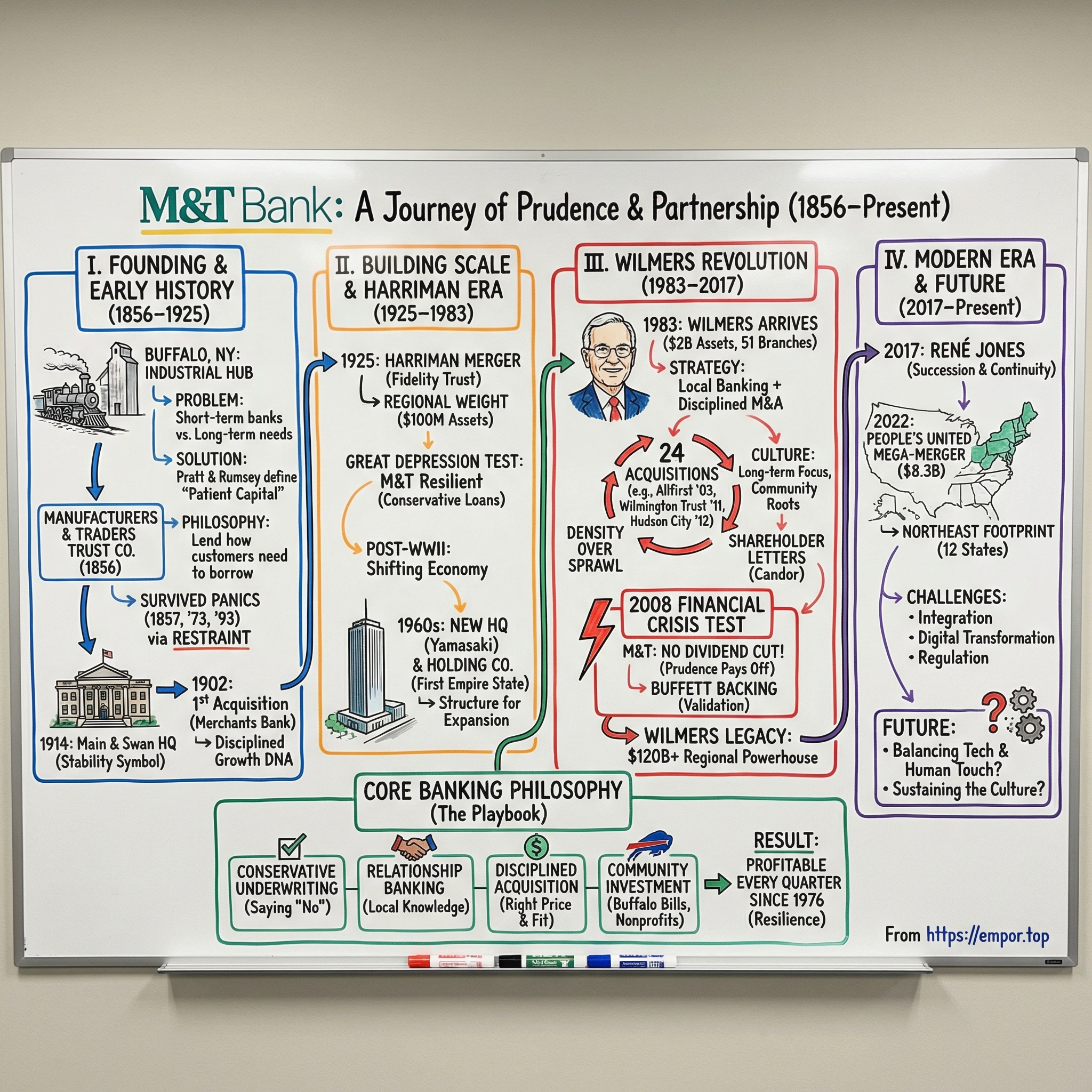

How did we get here? How did a bank founded in 1856 with $200,000 in capital by two Buffalo businessmen—Pascal Paoli Pratt and Bronson Case Rumsey—become one of America's most resilient financial institutions? Today, M&T Bank operates over 950 branches across 12 states and Washington D.C., managing assets north of $200 billion. But the numbers only tell part of the story.

The real story is about culture, patience, and a radical idea: that a bank could actually serve its community while generating superior returns for shareholders. It's about rejecting the siren song of subprime mortgages and synthetic CDOs in favor of knowing your borrowers by name. It's about building a regional empire through 24 carefully orchestrated acquisitions while never losing the soul of a community bank.

This is the story of how manufacturing trust—both the institution and the concept—built one of American banking's great franchises. And it starts, as all great American business stories do, with a problem that needed solving.

II. Founding & Early History: Manufacturing Trust (1856-1925)

Buffalo in 1856 was a city on the make. The Erie Canal had transformed it from a frontier outpost into the gateway between the Great Lakes and the Eastern seaboard. Grain elevators lined the waterfront. Steel mills belched smoke into the sky. The city's population had exploded from 8,000 in 1830 to over 74,000 by the mid-1850s.

But Buffalo's manufacturers had a problem. The existing banks—traditional institutions focused on short-term commercial paper—wouldn't make the long-term loans needed to finance durable manufacturing equipment. A steel press or grain elevator required years to pay for itself, not the 90-day notes that banks preferred. Pascal Paoli Pratt, a prominent local businessman, and Bronson Case Rumsey, from one of Buffalo's founding families, saw opportunity in this financing gap.

On April 2, 1856, they founded Manufacturers and Traders Trust Company with $200,000 in capital. The name itself was a statement of purpose: this would be a bank for the makers and merchants who were building Buffalo's industrial economy. While other banks focused on wealthy depositors and government bonds, M&T would specialize in commercial and industrial lending to Buffalo's growing manufacturing base.

The early decades established patterns that would define M&T for the next century and a half. In 1902, just 46 years after its founding, the bank completed its first acquisition—Merchants Bank of Buffalo. This wasn't a distressed takeover or hostile raid. It was a friendly combination of two institutions with aligned values and overlapping customer bases. The DNA for thoughtful, accretive M&A was being encoded early.

By 1914, M&T had grown substantial enough to require grander quarters. The bank moved into a massive white marble building at the corner of Main and Swan Streets, a Beaux-Arts monument to Buffalo's industrial prosperity. Robert Livingston Fryer had taken the helm as president, steering the institution through the turbulent waters of World War I.

The war years revealed another M&T trait: civic patriotism married to commercial opportunity. Harry T. Ramsdell, a senior executive, served as district chairman for the Liberty Loan program, helping coordinate the sale of war bonds across Western New York. Meanwhile, M&T financed local companies manufacturing everything from aircraft engines to ammunition. The bank wasn't just in Buffalo; it was of Buffalo, its fortunes intertwined with the city's industrial base.

By 1925, Manufacturers and Traders Trust had grown to $50 million in assets—a 250-fold increase from its founding capital. But the real transformation was about to begin. A 36-year-old banker with Ivy League credentials and Wall Street connections was about to arrive in Buffalo with plans to build something much bigger.

III. The Harriman Era & Building Scale (1925-1969)

Lewis Gawtry Harriman didn't look like a Buffalo banker. Yale-educated, impeccably dressed, with the bearing of a diplomat rather than a back-slapping local businessman, the 36-year-old seemed an unlikely choice to lead a regional industrial bank. But Harriman brought something M&T desperately needed: vision backed by capital.

In 1925, Harriman orchestrated a transformative merger between M&T and Fidelity Trust Company, creating a $100 million institution—massive by Buffalo standards. But the deal's structure was as important as its size. Harriman had assembled an investor group that read like a Who's Who of American power: A. H. Schoellkopf from the Niagara Mohawk founding family controlled local hydroelectric power; James V. Forrestal, who would later become America's first Secretary of Defense, brought Wall Street connections; and various Buffalo industrialists provided local credibility.

The merger timing seemed perfect—until it wasn't. Four years later, the stock market crashed. Banks failed by the thousands. Between 1930 and 1933, nearly 10,000 American banks closed their doors forever. Harriman faced the first great test of his leadership.

His response defined M&T's culture for generations: conservative underwriting, high capital reserves, and a focus on borrowers' character over collateral. While other banks chased hot money and speculative loans during the Roaring Twenties, M&T had stuck to financing Buffalo's factories and merchants. The strategy seemed boring during the boom, but it proved brilliant during the bust. M&T not only survived the Depression—it emerged stronger, absorbing weaker competitors and gaining market share.

Harriman's conservatism extended beyond lending. In an era when bank executives lived like nobility, he maintained modest offices and drove himself to work. He instituted a culture of "patient capital"—the idea that a bank should think in decades, not quarters. This wasn't just philosophy; it was strategy. By maintaining strong reserves and avoiding fashionable risks, M&T could lend aggressively during downturns when competitors were retrenching.

The post-war boom of the 1950s tested this patience. Buffalo's industrial economy was roaring. Bethlehem Steel employed 20,000 workers at its Lackawanna plant. General Mills, Bell Aircraft, and dozens of other manufacturers needed constant financing for expansion. M&T could have grown explosively by loosening standards. Harriman refused.

Instead, he focused on physical expansion and modernization. In 1961, M&T acquired an entire city block on Main Street for $12 million to build a new headquarters. The choice of architect revealed Harriman's ambitions: Minoru Yamasaki, who would later design the World Trade Center, was retained in 1963 to create a modernist tower that would announce M&T as a serious financial institution.

By 1969, as Harriman prepared to step back from active management, M&T had grown to nearly $1 billion in assets. The bank reorganized that year under a new holding company structure called First Empire State Corporation—a name that suggested grander ambitions than just serving Buffalo. The pieces were in place for expansion beyond Western New York. All that was needed was the right leader to execute the vision.

That leader was already in the building, though nobody knew it yet. He was a young executive who had joined M&T just a few years earlier, after stints at Morgan Guaranty and Bankers Trust. His name was Robert Wilmers, and he was about to transform M&T from a successful regional bank into one of American banking's great success stories.

IV. The Wilmers Revolution: From Local to Regional Power (1983-2017)

Robert George Wilmers arrived at M&T's headquarters on a gray March morning in 1983 carrying a single briefcase and a reputation for turning around troubled banks. At 48, he had already rescued banks in New York City and knew the playbook: cut costs, clean up bad loans, and find a buyer. The M&T board had hired him to do exactly that. The bank was struggling with bad real estate loans, and many directors assumed Wilmers would pretty it up for sale.

They had hired the right doctor but diagnosed the wrong disease. Wilmers saw something in M&T that others missed—not a dying institution but a sleeping giant. With $2 billion in assets, 51 branches in one state, and 2,000 employees, M&T had the infrastructure of a major regional bank but the mindset of a local savings and loan. Wilmers didn't come to bury M&T; he came to build an empire.

His first moves were surgical. Bad loans were written off immediately—no hoping for miraculous recoveries. Underperforming branches were closed. Sacred cow executives who had grown comfortable were shown the door. But this wasn't slash-and-burn cost-cutting. For every cut, Wilmers made a strategic investment: new technology systems, better training programs, and most importantly, aggressive recruitment of commercial lending talent.

The strategy crystallized in 1987 when Wilmers penned his first annual letter to shareholders—a tradition he would maintain for three decades. In dense, thoughtful prose that channeled his hero Warren Buffett, Wilmers laid out a simple philosophy: "A bank is not a technology company that happens to take deposits. It's not a trading floor with a consumer division attached. A bank is a relationship business, and relationships are built on trust."

This wasn't just rhetoric. While competitors were consolidating back-office operations and replacing loan officers with algorithms, M&T was hiring more relationship managers. While other banks were standardizing products, M&T gave its loan officers unprecedented autonomy to structure deals that made sense for specific customers. The approach seemed anachronistic in the go-go 1980s, but Wilmers was playing a longer game.

The acquisition spree began modestly. In 1990-1991, as the savings and loan crisis devastated weaker institutions, M&T acquired Monroe Savings, Empire of America, and Goldome Bank deposits—all distressed S&Ls that expanded M&T's footprint across upstate New York. The pattern was always the same: buy troubled institutions at discounts to book value, integrate their operations meticulously, keep the best people and the best customers, and move on to the next deal.

By 1992, M&T was acquiring healthy banks too: Central Trust of Rochester and Endicott Trust joined the fold. Each deal was different, but the integration playbook never varied. Day one: senior M&T executives would visit every acquired branch. Week one: all employees would receive offers to stay, with better benefits packages than they had before. Month one: customers would notice nothing had changed except the sign on the door.

In 1998, recognizing that "First Empire State Corporation" sounded like either a real estate trust or a Star Wars villain, Wilmers renamed the holding company to M&T Bank Corporation. The change was more than cosmetic—it signaled that M&T was ready to expand beyond New York's borders.

The transformation was staggering. By 2005, when Wilmers briefly retired (only to return 18 months later when his hand-picked successor Robert Sadler unexpectedly stepped down), M&T had grown to $55 billion in assets. The bank operated across multiple states, employed thousands, and had completed a dozen major acquisitions. But Wilmers was just getting started.

His return in 2006 marked a new phase of ambition. The financial crisis was brewing—though few saw it coming—and Wilmers sensed opportunity in chaos. As he wrote in his 2007 letter: "Banking is a cyclical business. The key is not to avoid cycles but to be positioned to take advantage of them."

The financial crisis would prove him devastatingly right. While competitors were failing or begging for bailouts, M&T was shopping. The bank emerged from 2008 not weakened but strengthened, with a reputation for prudence that money couldn't buy and acquisition opportunities that seemed almost unfair.

By 2011, American Banker named Wilmers "Banker of the Year"—a recognition that seemed overdue. Stephen Steinour, CEO of Huntington Bancshares, was more direct in his assessment: "Bob Wilmers might be the most successful banker in half a century." The numbers backed it up: under Wilmers' leadership, M&T had grown from $2 billion to over $120 billion in assets, expanded from one state to eight plus D.C., and completed 24 acquisitions while never losing money in a single quarter.

But perhaps Wilmers' greatest achievement wasn't what he built—it was what he preserved. In an era of homogenized, too-big-to-fail mega-banks, M&T remained stubbornly local. Loan decisions were still made by bankers who lived in the communities they served. The Buffalo Bills stadium still bore M&T's name, a partnership dating back to 1985. And every year, Wilmers would write his letter, explaining in plain English why boring banking was beautiful banking.

When Wilmers died in December 2017 at age 83, he left behind more than a bank. He left a philosophy, a culture, and a question: Could M&T maintain its community banking soul while competing in an increasingly digital, consolidated industry? The answer would depend on the next generation of leadership and their ability to execute one more transformative deal.

V. Major Strategic Acquisitions & Geographic Expansion (2000-2015)

The morning of September 26, 2002, should have been triumphant for Robert Wilmers. M&T was about to announce its largest acquisition ever—Baltimore-based Allfirst Financial for $3.1 billion. But the deal came with baggage. Allfirst had just lost $691 million in a rogue trading scandal involving a single currency trader named John Rusnak who had hidden losses for five years. Allied Irish Banks, Allfirst's parent, was desperate to exit.

Wilmers saw opportunity where others saw disaster. The deal structure was complex: AIB would receive 26.7 million shares of M&T common stock plus approximately $886 million in cash in exchange for all of Allfirst's outstanding stock. The merger would create a strong mid-Atlantic banking franchise with more than 700 branches in six states and the District of Columbia and approximately $50 billion in assets.

The Allfirst acquisition wasn't just about size—it was about transformation. For the first time, M&T would have a major presence outside New York State. Baltimore, Washington D.C., and Northern Virginia represented some of the country's most attractive banking markets. The deal would make M&T the 18th largest commercial bank headquartered in the U.S.

But the real story of M&T's expansion era wasn't Allfirst—it was what came after. In 2009, as the financial crisis raged, M&T acquired Provident Bank of Maryland, adding density to its Mid-Atlantic footprint. Then in 2011, another opportunistic deal: Wilmington Trust, the venerable Delaware institution founded by the du Pont family in 1903, was struggling with bad loans. M&T acquired it for just $351 million in stock, gaining not just branches but a premier trust and wealth management platform. The Irish banking crisis of 2010 provided an unexpected twist to the Allfirst story. Allied Irish Banks, under pressure from Irish regulators to raise capital during their sovereign debt crisis, sold its 22.5% stake in M&T (26.7 million shares) in November 2010 for $77.50 per share, generating $2.1 billion. The sale freed M&T from its largest shareholder and gave Wilmers even more flexibility to pursue his vision.

But the deal that would define M&T's modern footprint—and test its operational excellence—was Hudson City Bancorp. Announced on August 27, 2012, M&T agreed to acquire Hudson City for approximately $3.7 billion. Hudson City was a New Jersey thrift with $50 billion in assets and a remarkable history—Forbes had named it the "best managed bank of 2007" for avoiding subprime mortgages entirely.

The Hudson City acquisition should have closed in months. It took three years. The Federal Reserve had identified weaknesses in M&T's anti-money-laundering compliance program, forcing a massive remediation effort before approval could be granted. The delay was embarrassing and expensive, but it revealed something important about M&T's culture: the bank would do things right, even if it meant waiting.

When the deal finally closed on November 1, 2015, it added approximately $19 billion in loans and expanded M&T's franchise by 135 branches located in New Jersey (97 branches), downstate New York (29 branches) and Fairfield County, Connecticut (9 branches), along with 123 ATMs. More importantly, it gave M&T critical mass in the New York metropolitan area, completing the transformation from upstate regional bank to Mid-Atlantic powerhouse.

Each acquisition followed the same playbook: conservative valuation, meticulous integration, retention of key talent, and preservation of local relationships. M&T wasn't just buying banks; it was collecting franchises, each with its own customer base and community ties that could be enhanced but never erased. By 2015, Wilmers had orchestrated 24 acquisitions, building M&T into one of America's premier regional banking franchises through patience, discipline, and an unwavering focus on relationship banking.

VI. The Financial Crisis Test: Strength Through Adversity (2007-2010)

The conference room at One M&T Plaza was silent except for the hum of the air conditioning. It was September 15, 2008—Lehman Brothers had just filed for bankruptcy. Robert Wilmers sat at the head of the table, surrounded by his senior team, all watching CNBC on mute as the ticker showed bank stocks in freefall.

"How much exposure do we have to Lehman?" Wilmers asked quietly.

"Minimal, Bob. Less than $10 million total," his chief risk officer replied.

"And our mortgage book?"

"No subprime to speak of. Some Alt-A, but nothing like what Wachovia or WaMu are sitting on."

Wilmers nodded slowly. For years, Wall Street had mocked M&T's conservative lending standards. The bank had largely sat out the mortgage boom, refusing to lower underwriting standards or chase yield with exotic securities. Now, as the financial system collapsed around them, that conservatism looked like genius.

The numbers tell the story: while Bank of America was absorbing Countrywide's toxic mortgage portfolio and Citigroup was accepting $45 billion in government bailouts, M&T remained profitable every single quarter of the crisis. The bank did participate in TARP—taking $600 million more as a sign of systemic solidarity than necessity—but paid it back with interest by 2009.

But the real test wasn't avoiding losses; it was maintaining the dividend. For a bank, cutting the dividend is an admission of distress, a signal to the market that management has lost control. By late 2008, virtually every major bank had slashed or eliminated their dividends. Wells Fargo cut theirs by 85%. Bank of America went from $0.64 per share to $0.01. Even the mighty JPMorgan cut its dividend by 87%.

At M&T, the board meeting in February 2009 was tense. The dividend question was on everyone's mind. Some directors argued for a symbolic cut—better to be prudent than proud. But Wilmers was adamant: "We've been profitable for 33 straight years. We're profitable now. We'll be profitable next quarter. The dividend stays."

And it did. Other than Northern Trust, M&T was the only bank in the S&P 500 to maintain its dividend throughout the crisis. It was more than a financial decision—it was a statement of identity. M&T wasn't a trading floor that happened to take deposits. It was a bank, and banks honor their obligations.

Wilmers used the crisis as a teaching moment, both internally and externally. His 2008 shareholder letter was a masterpiece of controlled fury, excoriating Wall Street's excesses while defending the honor of traditional banking. "The financial crisis was not caused by banking," he wrote. "It was caused by gambling dressed up as banking."

The crisis also deepened M&T's relationship with Warren Buffett. Berkshire Hathaway had been an M&T shareholder since the 1990s, but during the crisis, Buffett became more vocal in his support. At Berkshire's 2009 annual meeting, he singled out M&T as one of the few banks that had maintained its underwriting discipline. "Bob Wilmers understands that a bank is a utility, not a casino," Buffett said.

But perhaps the most important outcome of the crisis was what M&T did while others were retrenching. As competitors pulled back from lending, M&T expanded. Commercial loan originations actually increased in 2009. The bank hired talented bankers from failed competitors. And most importantly, it began planning for acquisitions that would transform its footprint once the crisis passed.

In his 2010 letter, as the crisis finally began to ebb, Wilmers reflected on what M&T had learned: "Crises reveal character. They show who was swimming naked when the tide goes out, to borrow from our largest shareholder. But they also show who was wearing a sensible bathing suit all along. We're proud to have kept ours on."

The financial crisis of 2008 didn't make M&T's reputation—decades of conservative banking had already done that. But it cemented it. In an industry that had lost the public's trust, M&T stood as proof that banks could still be boring, profitable, and honorable all at the same time.

VII. Post-Wilmers Era & People's United Mega-Merger (2017-Present)

The December evening in 2017 was unseasonably warm for Buffalo. René Jones, M&T's chief operating officer, was driving home when his phone rang. It was Robert Brady, the board chairman. "Bob's gone," Brady said simply. Robert Wilmers, the titan who had led M&T for 34 years, had died of a heart attack at his Manhattan home. He was 83.

The boardroom at One M&T Plaza the next morning was somber. Wilmers hadn't just been the CEO; he had been M&T's philosopher-king, its public face, and the guardian of its culture. The question wasn't just who would replace him—it was whether anyone could.

The board's solution was elegant: divide and conquer. Robert Brady would serve as non-executive chairman. Three vice chairmen—Richard Gold, René Jones, and Kevin Pearson—would collectively manage operations. But everyone knew this was temporary. The real succession plan would play out over months, not days.

René Jones emerged as the natural successor. A Buffalo native who had joined M&T in 1992, Jones had spent his entire career in Wilmers' shadow, learning the master's philosophy while developing his own vision for the digital age. When he officially became CEO in December 2017, Jones faced an immediate challenge: prove that M&T's community banking model could survive without its legendary leader.

Jones' answer came in February 2021, when M&T announced its largest acquisition ever: People's United Financial for $8.3 billion. The deal was vintage M&T in strategy but modern in execution. People's United, based in Bridgeport, Connecticut, operated nearly 400 branches across New England—markets where M&T had minimal presence. The combined company would employ more than 22,000 people and have a network of over 1,000 branches and 2,200 ATMs spanning 12 states from Maine to Virginia and Washington, D.C.

But Jones understood that simply replicating Wilmers' playbook wasn't enough. The banking industry of 2021 was fundamentally different from the one Wilmers had conquered. Digital banking was no longer optional. Fintech competitors were attacking traditional banks' most profitable products. And a new generation of customers expected their bank to be as technologically sophisticated as their smartphone.

The People's United integration would be the most complex in M&T's history, not just because of its size but because of its ambition. Jones committed to maintaining both banks' systems in parallel until a complete technology overhaul could be implemented—a process that took until the third quarter of 2022. For all of 2022, the bank recorded $580 million in merger-related expenses, a staggering sum that reflected the true cost of doing integration right.

The cultural integration was equally deliberate. People's United's headquarters in Bridgeport became M&T's New England regional headquarters, signaling that this wasn't a conquest but a partnership. Key People's United executives were retained and given significant roles in the combined organization. The message was clear: M&T might be bigger, but it hadn't forgotten Wilmers' lesson that all banking is local.

Jones also brought a new transparency to M&T's operations. While maintaining the tradition of the annual shareholder letter, he embraced earnings calls, investor conferences, and digital communications in ways Wilmers never had. The hermit kingdom of Buffalo was opening its doors, if only slightly.

The numbers validated Jones' approach. Despite the massive integration costs, M&T remained profitable throughout the merger process. The bank's stock price, which had traded around $160 when Wilmers died, climbed above $180 by 2023. More importantly, M&T had successfully expanded into New England—one of the few remaining growth markets for regional banking—while maintaining its community banking ethos.

But perhaps the most important achievement of the post-Wilmers era was what didn't change. M&T still made lending decisions locally. It still sponsored the Buffalo Bills (the naming rights partnership was now approaching its 40th year). And it still hadn't lost money in a single quarter—a streak now extending back 47 years.

In his 2022 shareholder letter, Jones reflected on the transition: "Bob Wilmers taught us that banking is about relationships, not transactions. That wisdom doesn't become obsolete because customers can now deposit checks with their phones. If anything, as banking becomes more digital, the human element becomes more valuable, not less."

The post-Wilmers era at M&T is still being written. But the early chapters suggest that the bank's culture was stronger than any single leader, its strategy more durable than any single generation. In an industry obsessed with disruption, M&T had achieved something even more difficult: succession.

VIII. Culture & Community Banking Philosophy

Every August since 1985, something unusual happens at the Buffalo Bills' stadium. The bank executives arrive not in luxury boxes but in the parking lot, hours before kickoff. They're not there to schmooze clients or close deals. They're there to tailgate with customers, grill hot dogs with small business owners, and talk football with tellers and branch managers. This is M&T Bank's way—no velvet ropes, no VIP sections, just banking as community service with a side of chicken wings.

The Bills partnership itself tells the story of M&T's culture. When the team was threatening to leave Buffalo in the 1990s, M&T didn't just write a sponsorship check—it helped organize the local business community to keep the team in town. When the Bills finally made the playoffs in 2017 after a 17-year drought, M&T branches stayed open late so fans could withdraw cash for the spontaneous celebrations. The bank donated $170,000 to Andy Dalton's foundation after the Cincinnati quarterback's touchdown pass clinched Buffalo's playoff spot—$17 for each year of the drought.

This isn't corporate PR; it's corporate DNA. Over the past decade, M&T and its charitable foundation have contributed over $279 million to more than 7,600 nonprofits. But the numbers only hint at the depth of involvement. M&T executives serve on dozens of local boards. Bank employees get paid time off for volunteer work. Branch managers have discretionary budgets for local sponsorships without requiring headquarters approval.

The philosophy traces directly back to the bank's manufacturing roots. Buffalo's industrialists didn't build factories and leave; they built communities. They understood that a bank's health was inseparable from its community's health. This wasn't altruism—it was enlightened self-interest. Healthy communities produce creditworthy borrowers. Stable neighborhoods protect collateral values. Civic pride reduces brain drain.

Robert Wilmers institutionalized this philosophy through what he called "the covenant of community banking." In his view, a bank had three constituencies: shareholders, customers, and communities. Serve all three, and the bank thrives. Neglect any one, and the bank ultimately fails. Wall Street might optimize for shareholders at the expense of the other two, but that was a recipe for long-term decline.

The conservative lending philosophy was another cultural cornerstone. M&T loan officers were taught to ask three questions: Can the borrower repay? Will the borrower repay? What happens if they can't? The first question was about cash flow, the second about character, the third about collateral. But here's the key: character mattered most. A borrower with perfect financials but questionable ethics would be rejected. A borrower with imperfect financials but impeccable character might get approved with the right structure.

This approach required something most banks had abandoned: local decision-making. A loan officer in Buffalo couldn't possibly judge the character of a borrower in Baltimore. So M&T maintained local credit committees with real authority. Yes, large loans required headquarters approval, but local teams had meaningful input. This slowed decision-making compared to algorithmic lending, but it produced better outcomes—not just fewer defaults, but deeper relationships.

Employee tenure reflected this cultural stability. While Wall Street banks churned through talent, M&T lifers were common. The average branch manager had been with the bank for over 15 years. Senior executives often started as tellers or credit analysts. Promotion from within wasn't just preferred; it was expected. This created institutional memory—the kind that prevented repeating past mistakes.

The annual shareholder letter tradition, inherited from Wilmers and continued by Jones, embodied M&T's cultural transparency. These weren't glossy marketing documents but dense, thoughtful essays on banking, economics, and corporate responsibility. Wilmers would quote everyone from Adam Smith to Mark Twain, building arguments about interest rate policy or regulatory reform with the precision of a legal brief. The letters assumed readers were intelligent adults who deserved honest analysis, not corporate speak.

Even M&T's headquarters embodied its cultural values. While peer banks built gleaming towers with executive floors and private elevators, M&T's offices were functional rather than luxurious. The executive suite was on the same floor as regular meeting rooms. The cafeteria served everyone from the CEO to the newest teller trainee. The message was clear: we're all in this together.

The culture faced tests, of course. Each acquisition brought employees with different values and practices. The digital transformation required new skills and mindsets. Younger employees expected different things from their careers than their predecessors. But M&T's solution was always the same: evolution, not revolution. New ideas were welcome, but core values were non-negotiable.

In 2019, American Banker published a survey of the best banks to work for. M&T ranked third, with employees citing the family atmosphere and community involvement as key factors. One employee's comment captured it perfectly: "This doesn't feel like a bank. It feels like a family business that happens to have $140 billion in assets."

That's the paradox of M&T's culture: it's simultaneously deeply traditional and surprisingly progressive. Traditional in its commitment to relationship banking and community service. Progressive in its willingness to empower employees and invest in communities others had written off. It's a culture that values both continuity and change, both local roots and regional ambition.

As René Jones wrote in his 2021 letter: "Culture isn't what you say; it's what you do when no one's watching. It's the loan you don't make because something feels wrong. It's the customer you help even though they're too small to be profitable. It's the community you support even when you could deploy capital elsewhere for higher returns. That's not just good banking—that's good business."

IX. Playbook: M&T's Banking Strategy

If you wanted to build a regional banking powerhouse from scratch, the M&T playbook would seem almost contradictory. Be aggressive in acquisitions but conservative in lending. Centralize strategy but decentralize decisions. Embrace technology but never forget that banking is about people. These aren't contradictions, though—they're complementary principles that create a resilient competitive advantage.

The serial acquirer model is perhaps M&T's most visible strategy. Twenty-four acquisitions under Wilmers alone, with People's United marking number 25. But calling M&T a "serial acquirer" misses the nuance. This isn't growth for growth's sake. Each acquisition follows strict criteria: the target must be in or adjacent to existing markets, culturally compatible, available at a reasonable price, and immediately accretive to earnings after conservative integration costs.

The discipline shows in what M&T doesn't buy. No cross-country deals to enter hot markets. No transformational acquisitions that would fundamentally change the bank's character. No bidding wars that drive prices to irrational levels. When Bank of America was selling branches during its post-crisis retrenchment, M&T looked but passed—the locations were scattered, making integration expensive and market density impossible.

Integration excellence separates M&T from banks that struggle with mergers. The playbook is methodical: Day one, senior executives visit every acquired branch. Week one, all employees receive retention offers. Month one, systems integration begins but customer-facing changes are minimal. Month three, the brands converge but local management remains. Year one, back-office integration completes but credit decisions stay local.

This patient approach costs more upfront but pays dividends long-term. Customer retention rates in M&T acquisitions consistently exceed 90%, compared to industry averages around 80%. Employee retention is similarly high. The acquired bank's best practices are studied and often adopted system-wide. It's not conquest; it's combination.

Market density over geographic sprawl represents another strategic pillar. While some regional banks pride themselves on operating in 20 or 30 states, M&T focuses on dominating its chosen markets. In Buffalo, Rochester, and Syracuse, M&T has over 30% deposit market share. In Baltimore, following the Allfirst acquisition, it's the number two bank. This density creates economies of scale in marketing, operations, and brand awareness that scattered branches never could.

Relationship banking in an algorithmic age might seem anachronistic, but M&T has turned it into a competitive moat. While fintech companies can offer better rates or slicker apps, they can't offer a loan officer who knows your business, understands your industry, and can structure a solution for your specific situation. M&T's commercial loan officers average over 15 years of experience and maintain portfolios of 30-50 clients—small enough to provide personal service, large enough to be profitable.

The risk management philosophy—profitable every quarter since 1976—isn't about avoiding risk but about understanding it. M&T takes plenty of risks: lending to small businesses, financing real estate development, acquiring troubled banks. But these are risks the bank understands, can price appropriately, and can manage through downturns. The risks M&T avoids are the ones it doesn't understand: complex derivatives, subprime mortgages, cryptocurrency, or whatever the latest financial innovation might be.

Capital allocation discipline undergirds everything. M&T maintains capital ratios well above regulatory minimums—not because regulators require it but because financial strength creates strategic flexibility. During crises, when weak banks are selling assets at distressed prices, M&T is buying. When competitors are retrenching, M&T is extending credit to their abandoned customers. When regulators are forcing mergers, M&T is the acquirer of choice.

The technology strategy is pragmatic rather than pioneering. M&T will never be confused with a fintech startup, but it doesn't need to be. The bank invests heavily in core systems—the People's United integration included a complete technology overhaul—but focuses on reliability over innovation. The mobile app might not have the latest features, but it works every time. The online banking platform might look dated, but it's secure and stable.

Building moats in regional banking requires recognizing what's defensible and what isn't. M&T can't compete with JPMorgan's technology budget or Bank of America's national scale. But it can offer something the mega-banks can't: local decision-making, personal relationships, and deep community roots. These aren't just nice-to-haves for certain customers—they're essential.

The small business segment illustrates this perfectly. A small manufacturer in Buffalo doesn't need a sophisticated cash management system; it needs a credit line that flexes with seasonal demand. A family-owned restaurant in Baltimore doesn't need investment banking services; it needs a banker who understands that February is always slow but March makes up for it. M&T can provide this because its bankers live in these communities, understand these businesses, and have the authority to make decisions.

The succession planning embedded in M&T's strategy ensures continuity beyond any individual leader. The bank develops talent internally, rotating high-performers through different divisions and geographies. The three-headed leadership structure after Wilmers' death wasn't a panic response—it was a planned transition that had been discussed for years. Every senior executive has a designated successor, and probably a successor to the successor.

The playbook's ultimate test is replicability. Can M&T's model work in new markets? Can it scale beyond its current footprint? Can it survive the digital transformation of banking? The People's United acquisition suggests yes—M&T is successfully exporting its model to New England. But the real test will come during the next crisis, when we'll learn whether Jones and his team have truly internalized Wilmers' lessons or were just following his playbook.

As one longtime M&T executive put it: "Our strategy isn't complicated. We take deposits from our communities, lend that money back to our communities, and try not to do anything stupid in between. The hard part isn't understanding the strategy—it's having the discipline to stick with it when everyone else is chasing the latest fad."

X. Analysis: Bear vs. Bull Case

Bull Case: The Berkshire of Banking

The bull case for M&T starts with a simple observation: for 47 years, through recessions, banking crises, and pandemic, this bank has made money every single quarter. In an industry where earnings volatility is the norm, M&T's consistency is almost unnatural. This isn't luck—it's evidence of a sustainable competitive advantage.

Start with the acquisition track record. Twenty-five bank acquisitions over four decades, and not a single material failure. Each deal has been accretive to earnings within 12 months. The integration playbook is so refined that M&T can accurately predict cost savings and revenue synergies to within 5% accuracy. In an industry where 70% of mergers fail to deliver promised value, M&T's success rate approaches 100%.

The People's United acquisition demonstrates that M&T's model scales. Despite being the largest deal in company history, integration is proceeding on schedule and under budget. The financial benefits are "consistent to slightly better than expectations at announcement," according to CFO Darren King. The combined franchise now has critical mass in some of America's most attractive banking markets—from Boston's biotech corridor to Virginia's government contractors.

The deposit franchise is particularly valuable in a rising rate environment. M&T's deposits are sticky—customers stay for decades, not quarters. The bank's deposit costs are consistently below peer averages because customers value the relationship more than an extra 10 basis points of interest. This isn't the hot money that flees at the first sign of trouble; it's core funding that provides stability through cycles.

Conservative underwriting culture creates a hidden asset: reserve releases during recoveries. While aggressive lenders are still provisioning for yesterday's bad loans, M&T is releasing reserves from loans that performed better than expected. This creates a earnings tailwind that can last years after a crisis ends.

Scale advantages post-People's United are just beginning to manifest. The combined bank can spread technology investments across a much larger base. It has the heft to negotiate better terms with vendors. It can attract talent that wouldn't consider a smaller regional bank. Yet it's still small enough to maintain local decision-making and community focus.

Warren Buffett's continued ownership—Berkshire Hathaway remains a top-10 shareholder—provides the ultimate endorsement. Buffett doesn't just buy banks; he buys banks with sustainable competitive advantages. His multi-decade holding period suggests he sees something in M&T that transcends quarterly earnings.

Bear Case: The Last of the Mohicans

The bear case starts with an uncomfortable truth: regional banking is a dying business model. The industry is consolidating relentlessly. In 1984, there were 14,000 banks in America. Today, fewer than 4,000 remain. The economics are brutal: massive technology investments, crushing regulatory costs, and competition from both mega-banks and fintech startups. M&T might be executing the regional banking model perfectly, but that's like being the world's best typewriter manufacturer.

Interest rate sensitivity poses immediate risks. M&T's balance sheet is asset-sensitive—it benefits from rising rates. But if rates fall or stay low, net interest margins compress. The bank's heavy commercial real estate exposure (about 40% of the loan portfolio) looks particularly vulnerable if remote work permanently reduces office demand.

Technology investment needs are staggering and never-ending. JPMorgan spends $12 billion annually on technology—more than M&T's entire annual revenue. How can a regional bank compete when the technology arms race requires nation-scale resources? M&T's pragmatic approach to technology might be prudent, but it risks falling too far behind to catch up.

Regulatory burden falls disproportionately on regional banks. They face similar compliance requirements to mega-banks but without the scale to spread costs. The Hudson City acquisition delay—three years due to compliance issues—shows how regulatory problems can derail strategic plans. As M&T approaches $250 billion in assets, it will face even more stringent requirements.

Competition from both ends is intensifying. From above, mega-banks are using technology to compete for M&T's commercial clients. JPMorgan's digital wholesale banking platform offers services M&T can't match. From below, fintech companies are cherry-picking the most profitable products. Square is taking small business payments. Rocket Mortgage is taking home loans. What's left for regional banks?

The community banking mission, while admirable, might be economically obsolete. Younger customers don't value branch networks or personal relationships. They want seamless digital experiences, instant decisions, and the lowest price. M&T's strength—local market knowledge and relationship banking—might be solving yesterday's problem.

Succession risk remains material. René Jones has performed admirably, but he's no Robert Wilmers. The cult of personality that Wilmers cultivated can't be easily replaced. The next recession will test whether M&T's culture is truly institutionalized or was dependent on a single leader's vision.

Geographic concentration is a double-edged sword. Yes, M&T dominates upstate New York, but these are slow-growth markets with declining populations. Buffalo's population has fallen by half since 1950. Syracuse and Rochester face similar demographic challenges. Even M&T's expansion markets—Baltimore, Hartford—aren't exactly economic dynamos.

The Verdict

The truth, as always, lies somewhere between the extremes. M&T is neither invincible nor obsolete. It's a exceptionally well-run regional bank facing structural industry challenges. The bull case assumes execution can overcome industry headwinds. The bear case assumes industry dynamics will overwhelm even the best operators.

The most likely scenario: M&T continues to consolidate smaller banks, maintaining profitability through scale and efficiency. But growth slows, returns compress, and the stock becomes a value trap—cheap for good reasons. The bank might remain independent for another decade, maybe two. But eventually, economics will force a sale to a mega-bank. M&T will command a premium price, shareholders will do fine, and another regional banking franchise will disappear into the oligopoly.

Unless, of course, M&T can pull off one more transformation. The pieces are there: strong deposit franchise, proven acquisition capabilities, and genuine competitive advantages in certain segments. If Jones and his team can successfully navigate the digital transition while maintaining M&T's relationship banking edge, the bank might have another chapter to write. But that's a big if in an industry littered with formerly great regional banks that couldn't adapt fast enough.

XI. Epilogue: The Future of Regional Banking

There's a photograph in M&T Bank's archives from 1856, the year of its founding. It shows a small wooden building on Buffalo's waterfront, surrounded by grain elevators and canal boats. The bank's entire staff—all six of them—stand proudly in front of their new office. They're wearing top hats and morning coats, the uniform of 19th-century American capitalism. But their faces show something more modern: the nervous excitement of entrepreneurs betting everything on an idea.

One hundred and sixty-eight years later, M&T Bank employs 22,000 people across 12 states. The wooden shack has become a billion-dollar enterprise. The canal boats have given way to wire transfers. But the fundamental bet remains the same: that a bank can serve its community and shareholders simultaneously, that local knowledge matters, that relationships transcend transactions.

The question isn't whether M&T's story has been successful—by any measure, it has been extraordinarily so. The question is whether this story has a future. Can regional banking survive in an age of global finance, algorithmic lending, and digital disruption? M&T's journey offers clues, if not definitive answers.

First, the consolidation imperative is real but not absolute. Yes, the number of banks continues declining. But the pace has slowed, and a sustainable equilibrium might emerge. America probably doesn't need 4,000 banks, but it probably needs more than four. The sweet spot might be 50-100 regional champions, each dominating their geography while the mega-banks handle global corporations and capital markets. M&T is positioned to be one of these survivors.

Second, technology is a tool, not a destiny. The banks that died weren't killed by technology—they were killed by their failure to adapt technology to their business model. M&T's pragmatic approach—using technology to enhance rather than replace relationship banking—might prove more sustainable than either digital-only models or Luddite resistance.

Third, culture compounds like interest. M&T's 47-year streak of profitable quarters didn't happen because of any single decision or leader. It happened because thousands of employees making millions of decisions were guided by consistent principles. This cultural capital can't be replicated by algorithms or acquired through mergers. It must be built, maintained, and transmitted across generations.

The community banking mission isn't anachronistic—it's just misunderstood. Yes, young consumers want digital convenience. But they also want their banks to share their values, support their communities, and treat them as humans rather than account numbers. M&T's challenge isn't abandoning community banking but translating it for a digital generation.

What would Robert Wilmers make of today's banking landscape? He'd probably be appalled by negative interest rates, cryptocurrency speculation, and trillion-dollar balance sheets. But he'd also recognize the opportunity. When everyone else is zigging toward complexity, there's value in zagging toward simplicity. When competitors are automating everything, there's differentiation in human touch. When the industry is consolidating, there are acquisitions to be made.

The leadership transition from Wilmers to Jones represents more than a generational change—it's an evolutionary adaptation. Wilmers built M&T for the 20th century: branch networks, paper checks, and face-to-face relationships. Jones must rebuild it for the 21st: mobile apps, instant payments, and omnichannel engagement. But the core mission remains unchanged: help customers and communities prosper.

The recent history of American banking is littered with regional champions that lost their way. Wachovia, once the pride of North Carolina, destroyed itself chasing growth. Washington Mutual, the nation's largest thrift, collapsed under bad mortgages. National City, Fleet, First Union—all gone, absorbed into the mega-bank blob. M&T has survived where others failed not through luck but through discipline.

Yet survival isn't enough. M&T must prove that regional banking can thrive, not just endure. This requires threading an impossibly narrow needle: being big enough to afford technology and compliance but small enough to maintain local relationships; being aggressive enough to grow but conservative enough to survive downturns; being traditional enough to maintain trust but innovative enough to attract new customers.

The verdict on regional banking's future won't be rendered in quarters or even years—it will take decades. But M&T's story suggests reasons for optimism. Every banking crisis creates opportunities for the prepared. Every wave of consolidation leaves gaps for focused competitors. Every technological disruption creates customers who value human expertise even more.

In his final shareholder letter before his death, Robert Wilmers wrote: "Banking is not about products or technology or even money. It's about trust. And trust isn't built in a quarter or a year. It's built over generations, one relationship at a time, one kept promise at a time. That's why M&T has survived for 161 years, and that's why we'll survive for 161 more."

Perhaps he's right. Or perhaps M&T is the last of a dying breed, executing a obsolete strategy with exceptional skill. Time will tell. But for now, in Buffalo and Baltimore, in Hartford and Harrisburg, M&T bankers are still making loans to local businesses, still sponsoring Little League teams, still proving that banking can be both boring and beautiful.

The photograph from 1856 hangs in René Jones' office now, a reminder of how far M&T has come and how much further it still must go. Those six founders in their top hats couldn't have imagined smartphones or credit default swaps or banks with trillion-dollar balance sheets. But they would recognize the fundamental promise that M&T still makes to its communities: We're here to help you build something. We'll be here tomorrow. And we'll be here the day after that.

In banking, as in life, that's really all that matters.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube