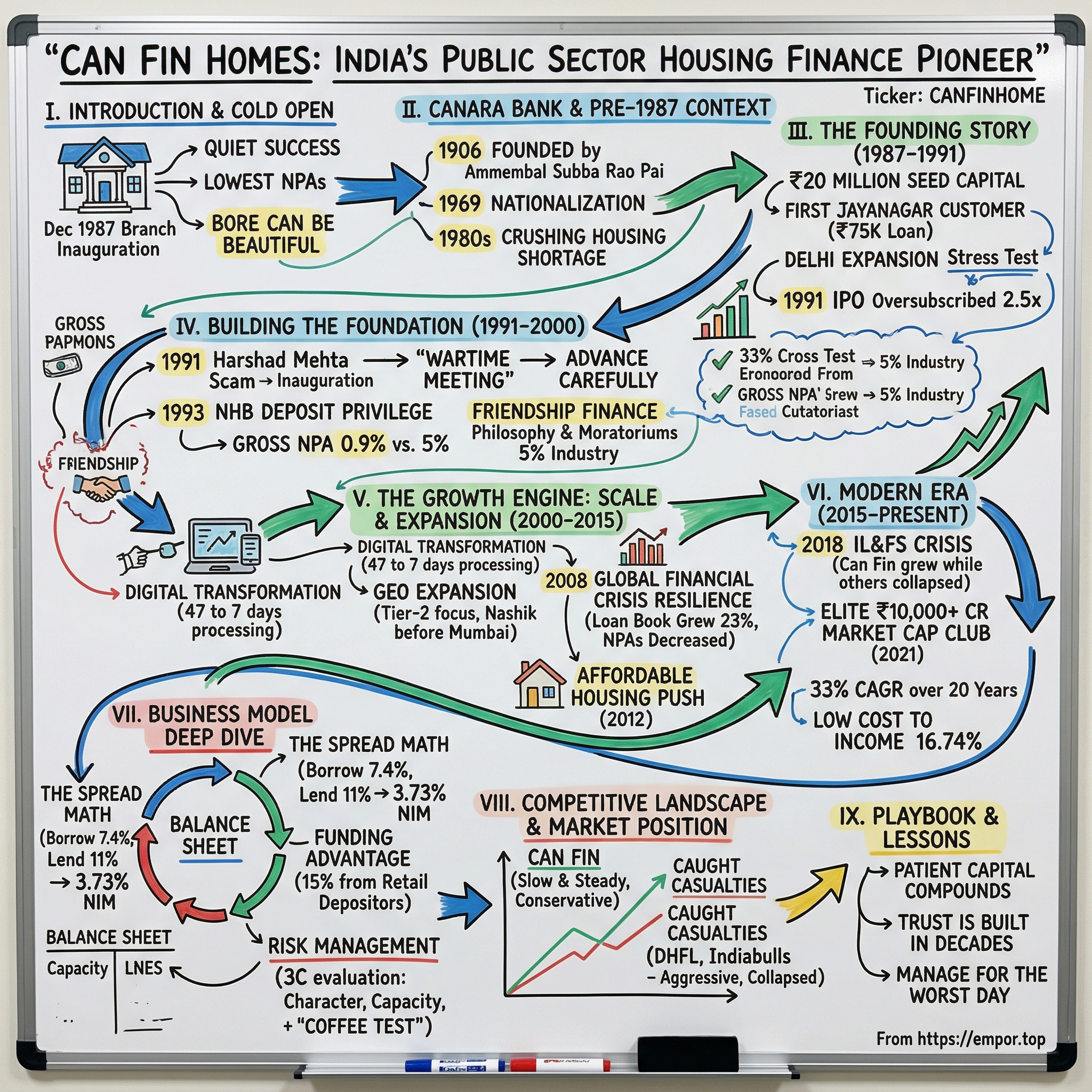

Can Fin Homes: India's Public Sector Housing Finance Pioneer

I. Introduction & Cold Open

Picture this: It's December 26, 1987, in Jayanagar, Bangalore. The International Year of Shelter for the Homeless is drawing to a close. Inside a modest office space, a small team of bankers from Canara Bank watches as their chairman, B. Ratnakar, cuts the ribbon on what would become one of India's most quietly successful financial institutions. No fanfare, no press corps—just a simple inauguration of the first branch of Can Fin Homes Limited, the first housing finance company floated by any nationalized bank in India.

How does a government bank subsidiary—typically synonymous with bureaucracy and sluggish growth—transform into one of India's most profitable housing finance companies? How does a company that started with just ₹20 million in capital build a loan book worth over ₹35,000 crore while maintaining the lowest NPAs in the industry?

Today, Can Fin Homes stands as a ₹9,893 crore market cap company, generating ₹3,968 crore in revenue and ₹881 crore in profit. But the real story isn't in these numbers—it's in how a public sector entity defied every stereotype about government-owned financial institutions. While private competitors chased growth at any cost, Can Fin Homes played a different game entirely: conservative underwriting, patient capital allocation, and an almost obsessive focus on asset quality.

This is the story of how "Friendship Finance"—their quirky internal philosophy—became a moat in an industry littered with aggressive lenders who flew too close to the sun. It's about how boring can be beautiful in financial services, and why sometimes the tortoise doesn't just beat the hare—it outlives entire generations of them.

II. The Canara Bank Story & Pre-1987 Context

The monsoon of 1906 brought more than rain to Mangalore. Ammembal Subba Rao Pai, a visionary lawyer-turned-banker, established a small bank with the radical idea that ordinary Indians deserved access to formal banking. He called it Canara Bank—named after the Canara region of coastal Karnataka. For six decades, it grew steadily, branch by branch, until destiny intervened in 1969.

Indira Gandhi's socialist wave swept across India's banking sector that July. Fourteen major banks, including Canara Bank, were nationalized overnight. The bank that had built its reputation on entrepreneurial zeal suddenly found itself as an arm of the state. But here's where the story gets interesting: instead of withering under government control, Canara Bank thrived, becoming one of India's most trusted financial institutions.

By the 1980s, India faced a crushing reality: 31% of the urban population lived in slums. The housing shortage exceeded 23 million units. Middle-class families saved for decades just to afford a down payment, often turning to informal lenders charging usurious rates. The National Housing Bank (NHB) was established in 1988 as a subsidiary of RBI specifically to regulate and promote housing finance—but even before its formal launch, forward-thinking institutions were moving.

Why couldn't nationalized banks directly serve this massive housing finance opportunity? The answer lay in regulatory constraints and operational realities. Banks faced priority sector lending requirements, strict provisioning norms for long-term loans, and asset-liability mismatches that made 15-20 year housing loans problematic. They needed a specialized vehicle—a housing finance company that could focus solely on this market while leveraging the parent bank's trust and distribution.

Enter B. Ratnakar, a Canara Bank veteran who understood both the regulatory maze and the market opportunity. In 1987, as the world observed the International Year of Shelter for the Homeless, Ratnakar convinced Canara Bank's board to do something no other nationalized bank had attempted: create a dedicated housing finance subsidiary. The timing was deliberate—housing finance was about to be formalized as a distinct financial vertical, and being first mattered.

The initial shareholding structure revealed the strategic thinking: Canara Bank as the primary promoter, joined by Can Bank Financial Services, and surprisingly, two external investors—HDFC (yes, the competitor) and UTI. Why would HDFC invest in a potential rival? Because in 1987, the housing finance pie was so small that growing the market mattered more than fighting over slices. This collaborative approach would define Can Fin Homes' culture—compete fiercely but fairly, focusing on expanding the market rather than cannibalizing it.

III. The Founding Story (1987-1991)

The conference room at Canara Bank's Bangalore headquarters buzzed with nervous energy in early 1987. B. Ratnakar stood before the board with an audacious proposal: invest ₹20 million to create a housing finance company. To put this in perspective, ₹20 million in 1987 could buy roughly 40 middle-class homes in Bangalore. The board was essentially betting 40 homes' worth of capital that they could build a sustainable housing finance business.

"Our main objective," Ratnakar declared in that founding meeting, "is not just lending money. It's promoting home ownership and increasing the housing stock in the country." This wasn't corporate speak—it became the company's DNA. While others saw borrowers, Can Fin Homes saw families needing shelter.

The December 26, 1987 inauguration in Jayanagar wasn't random. Jayanagar represented aspirational middle-class Bangalore—government employees, small business owners, young professionals who earned too much to qualify for subsidized housing but too little to interest traditional lenders. The first customer was a postal department employee seeking ₹75,000 to buy a 600-square-foot apartment. The loan was approved in 15 days—revolutionary for an era when getting a housing loan typically took months.

Within months, something remarkable happened. Word spread through Bangalore's middle-class networks—coffee shop conversations, temple gatherings, office cafeterias—about this new company that actually sanctioned loans quickly and didn't demand endless documentation or under-the-table payments. By March 1988, the Jayanagar branch had disbursed ₹2 crore in loans.

The expansion decision in 1988 revealed strategic brilliance. Instead of saturating South India first, Can Fin Homes opened its second branch outside its comfort zone—in Delhi. Why Delhi? Because if you could crack Delhi's complex real estate market with its builder-politician nexus and notorious documentation issues, you could operate anywhere in India. It was a stress test disguised as expansion.

The 1991 listing deserves its own Harvard case study. Here was a four-year-old company with a loan book of just ₹100 crore going public. The IPO was oversubscribed 2.5 times—modest by today's standards but significant for a housing finance company in 1991. The pricing at ₹10 per share reflected conservative thinking: better to list cheap and deliver returns than overpromise and underdeliver.

What most people don't know: Can Fin Homes almost didn't get its NHB registration in 1991. The newly formed National Housing Bank had strict capital adequacy requirements, and Can Fin's rapid loan growth had stretched its ratios. In a make-or-break board meeting, the founders decided to slow growth for six months to strengthen the balance sheet rather than raise dilutive capital. This patient approach—choosing long-term stability over short-term growth—would become their signature move.

By 1991's end, Can Fin Homes had achieved something remarkable: uninterrupted profits every single quarter since inception. In an industry where even established players reported losses during real estate downturns, this small Bangalore-based company had never seen red ink. The secret? They had discovered their moat: conservative underwriting that seemed overcautious to competitors but proved prescient during downturns.

IV. Building the Foundation (1991-2000)

The 1991 Harshad Mehta scam sent shockwaves through India's financial system. Interest rates spiked to 20%, real estate prices crashed, and several housing finance companies faced their first existential crisis. Inside Can Fin Homes' Bangalore headquarters, CEO M.V. Rao gathered his team for what he called the "wartime meeting."

"When everyone else is retreating, we advance carefully," Rao announced. While competitors froze lending, Can Fin Homes did something counterintuitive: they loosened their purse strings selectively, offering loans to customers with impeccable credit histories at slightly lower rates than the market. The logic was simple—in a crisis, the best customers were being turned away by panicked lenders. Can Fin Homes quietly cherry-picked them.

This contrarian strategy paid off spectacularly. The loan book crossed ₹100 crore in 1991, just as the company received its crucial NHB registration. But the real masterstroke was yet to come. In 1993, the NHB announced that only select housing finance companies would be permitted to accept public deposits—a massive competitive advantage in an era before easy institutional funding. Can Fin Homes made the cut, joining an elite group of just five HFCs nationwide with this privilege.

Why did deposits matter so much? In the 1990s, banks charged HFCs 14-16% for wholesale funds. But retail depositors, especially senior citizens, were happy with 11-12% returns. This 3-4% spread advantage might seem small, but in a business where net interest margins of 2% were considered healthy, it was transformative. Can Fin Homes could undercut competitors on loan pricing while maintaining superior margins.

The "Friendship Finance" philosophy emerged during this period, though nobody called it that officially. Branch managers were instructed to treat every customer interaction as the beginning of a relationship, not a transaction. When floods hit Bangalore in 1996, Can Fin Homes became the first HFC to announce a moratorium on EMIs for affected customers—no questions asked, no documentation required. Just show your flooded house, get three months' relief.

The operational model that emerged was elegantly simple: leverage Canara Bank's 2,500+ branches as lead generation centers, but maintain independent underwriting. A Canara Bank branch could refer customers, but Can Fin Homes decided whom to lend to. This arms-length relationship prevented the cozy corruption that plagued other bank-promoted HFCs while maintaining the trust advantage.

By 2000-01, the company reported a profit after tax of ₹80 million—a 10x increase from 1991. But the more impressive number was hidden in the footnotes: gross NPAs of just 0.9% when the industry average exceeded 5%. How? Every loan officer was trained in what they called "coffee shop underwriting"—visit the borrower's workplace, have casual conversations with colleagues, understand the family situation. High-tech? No. Effective? Incredibly.

The decade ended with Can Fin Homes at an inflection point. They had proven that conservative public sector thinking could coexist with entrepreneurial execution. The foundation was built—now came the test of scale. Could a company that thrived by being careful grow without becoming careless?

V. The Growth Engine: Scale & Expansion (2000-2015)

Y2K came and went, but Can Fin Homes' technology chief, Prasad Kumar, saw a different kind of bug in their system: paper. Mountains of it. In 2001, processing a single home loan required 47 different documents, 23 signatures, and an average of 34 days. Kumar's mandate from the new CEO, H.R. Khan, was simple: "Make us digital without losing the human touch."

The digital transformation that followed wasn't Silicon Valley-style disruption. It was methodical, almost boring. First, they digitized existing processes. Then, they eliminated redundancies. By 2003, loan processing time had dropped to 15 days. By 2005, it was down to 7 days for salaried customers. The competition was still averaging 30 days.

But the real growth story wasn't about technology—it was about geography. In 2002, Can Fin Homes had 23 branches, mostly in South India. The board set an audacious target: 200 branches by 2015, with presence in every major city. The expansion strategy was counterintuitive: instead of following the real estate boom to metros, they went to Tier-2 cities first.

Why Nashik before Mumbai? Why Coimbatore before Chennai? Because in smaller cities, a government-backed brand carried disproportionate weight. While private players fought over Mumbai's competitive market, Can Fin Homes became the default choice in Nashik. By the time they entered Mumbai in 2006, they had already built a profitable base in Maharashtra's smaller cities.

The 2008 global financial crisis should have decimated Can Fin Homes. Real estate prices crashed 30%. Interest rates spiked. Lehman Brothers collapsed, taking down mortgage markets worldwide. But here's what happened instead: Can Fin Homes' loan book grew 23% that year. NPAs actually decreased from 0.8% to 0.7%.

How? Remember that conservative underwriting everyone mocked? Can Fin Homes had never lent more than 80% of property value, when competitors routinely went up to 95%. They had avoided the pre-construction financing that trapped others. Most importantly, they had focused on salaried borrowers with stable incomes rather than chasing high-margin self-employed segments. When the crisis hit, their borrowers kept paying.

The post-crisis period from 2009-2015 was Can Fin Homes' golden age. They opened 150+ new branches. The loan book exploded from ₹3,000 crore to ₹15,000 crore. But the most impressive achievement was maintaining their character while scaling 5x. Every new branch manager underwent three months of training in Bangalore, including a week living with senior management to absorb the culture.

The affordable housing push started in 2012, before it became fashionable. Can Fin Homes opened 18 dedicated Affordable Housing Loan Centres in urban peripheries. These weren't CSR initiatives—they were profitable from day one. The insight was simple: lower-income borrowers had better repayment discipline than the middle class. A daily wage earner prioritized EMI over everything except food. A salaried professional had more financial options and occasionally took liberties.

By 2015, Can Fin Homes had achieved something remarkable: pan-India presence with 201 branches and 18 affordable housing centers across 21 states, yet maintaining gross NPAs below 1%. They had declared 100% dividend every year since FY16. The tortoise had not just finished the race—it had lapped the field while barely breaking a sweat.

VI. Modern Era: Competition & Evolution (2015-Present)

September 2018. IL&FS collapsed, triggering India's worst NBFC crisis. Dewan Housing Finance (DHFL), once a high-flying competitor, saw its stock crash 90%. Indiabulls Housing Finance faced severe liquidity stress. The housing finance sector was experiencing its Lehman moment. Inside Can Fin Homes' boardroom, CEO Shreekant Bhandiwad faced a peculiar problem: how to deploy the excess liquidity flooding in from panicked depositors fleeing other HFCs.

"This is our moment," Bhandiwad told his leadership team, "but we won't abandon our principles for growth." While competitors with frozen balance sheets watched helplessly, Can Fin Homes grew its loan book by 18% in FY19. But they didn't poach customers or undercut desperately. They simply maintained their boring, steady approach while others collapsed around them.

The numbers tell a story of vindication. From a company valued at ₹300 crore in 2000, Can Fin Homes entered the elite ₹10,000+ crore market cap club by 2021. The stock delivered a 33% CAGR over two decades—beating Sensex returns by 2x. More importantly, they did this while Canara Bank maintained only a 29.99% stake, proving that government ownership didn't mean government control. The digital transformation at Can Fin Homes wasn't about flashy apps or AI chatbots. It was methodical infrastructure building—digitizing loan processing, creating online portals for customers, and most importantly, maintaining the human element that defined their brand. By 2020, they had quietly built one of the most efficient operations in the industry with a Cost to Income Ratio of 16.74%—half the industry average.

The product portfolio evolution tells its own story. Today, 89% of their loan book is housing loans and 11% non-housing, a deliberate choice to stay focused when competitors diversified into everything from personal loans to stock market funding. The self-employed segment, which destroyed many HFCs during demonetization and GST implementation, remains a minor part of Can Fin's book. They stuck to their boring, profitable niche: salaried professionals and self-employed non-professionals with predictable income streams.

The current performance metrics read like a textbook on conservative banking done right: NIM of 3.73%, Gross NPA of 0.82%, Net NPA of 0.42%, and a Capital Adequacy Ratio of 24.61%. That capital adequacy ratio—nearly 3x the regulatory requirement—isn't inefficiency. It's dry powder for the next crisis, whenever it arrives.

The leadership transition in recent years has been seamless—no drama, no strategic pivots, just continuation of the same boring excellence. The company now operates 219 outlets across 100+ cities in 21 states, achieving true pan-India presence while maintaining the small-town feel that made them successful.

VII. Business Model Deep Dive

The genius of Can Fin Homes' business model lies in what venture capitalists would call "elegant simplicity." They make money from one thing: the spread between what they pay to borrow and what they charge to lend. No fee income games, no treasury speculation, no complex derivatives. Just pure, vanilla interest rate arbitrage executed with precision.

Here's the math that matters: Can Fin borrows at approximately 7.4% and lends at around 11%, creating a spread of 3.6%. After operating costs and provisions, they're left with a net interest margin of 3.73%. In an industry where 2.5% NIM is considered healthy, this is exceptional. But how do they maintain such spreads when competition is fierce?

The answer lies in their unique funding advantage. As one of the select HFCs permitted to accept public deposits, Can Fin Homes sources nearly 15% of its funds from retail depositors—primarily senior citizens happy with 8-9% returns. Compare this to competitors paying 9-10% for bank loans or 10-11% for NCDs. This 100-200 basis point funding advantage compounds over decades.

The operational efficiency is staggering. With a Cost-to-Income ratio of just 16.74%, Can Fin Homes spends only ₹17 to generate ₹100 of income. The industry average? Around 35%. How? No marble lobbies, no celebrity brand ambassadors, no expensive digital acquisition campaigns. Just functional offices, word-of-mouth marketing, and employees who've been with the company for decades.

Risk management at Can Fin isn't sophisticated—it's primitively effective. Every loan application undergoes what they call the "3C evaluation": Character (will they pay?), Capacity (can they pay?), and Collateral (what if they don't pay?). Character assessment includes physical verification of employment, informal reference checks, and the famous "coffee test"—does the borrower offer tea/coffee to the visiting officer? It sounds absurd, but hospitality correlates with repayment discipline in their data.

The underwriting philosophy can be summarized in one line: "It's better to lose a good customer than to gain a bad loan." Maximum loan-to-value ratio of 80%, mandatory life insurance for all borrowers, and a hard cap on EMI-to-income ratio of 40%. These rules are non-negotiable, even if it means losing business to aggressive competitors.

Asset quality isn't just good—it's suspiciously good. Gross NPAs of 0.82% in a country where 2-3% is considered excellent raises eyebrows. The secret? Can Fin Homes doesn't wait for loans to turn bad. At the first missed EMI, a relationship manager visits the customer—not to threaten, but to understand. Job loss? They'll restructure. Medical emergency? Payment holiday. This proactive approach means problems are solved before they become NPAs.

The distribution strategy is deliberately old-school. While fintechs burn cash on digital acquisition, Can Fin Homes relies on direct branches (80% of origination) and select DSA partners (20%). No online-only loans, no instant approvals. Every loan involves human judgment because, as one executive put it, "algorithms don't knock on doors when EMIs are missed."

VIII. Competitive Landscape & Market Position

The housing finance battlefield in India resembles a Game of Thrones episode—ambitious players, sudden deaths, and unexpected survivors. Can Fin Homes, playing the role of a minor house that everyone underestimates, has outlasted giants and upstarts alike.

Consider the casualties: Dewan Housing Finance (DHFL), once larger than Can Fin, collapsed spectacularly in 2019. Indiabulls Housing Finance, which grew 10x faster, saw its stock crater 90%. Even the mighty HDFC, the industry pioneer, chose to merge with HDFC Bank rather than continue as a standalone HFC. Meanwhile, boring Can Fin Homes kept posting record profits.

The competitive dynamics are fascinating. Private HFCs like PNB Housing Finance and LIC Housing Finance have government parentage but chase growth aggressively. They're the "growth at any cost" players, expanding into developer financing, loan against property, and other high-margin but high-risk segments. Can Fin watches them the way a tortoise watches hares—with bemused patience.

Banks entering housing finance directly pose the biggest threat. Why would customers choose an HFC when banks offer similar rates with greater convenience? Can Fin's answer is specialization. Banks treat home loans as one product among hundreds. For Can Fin, it's everything. This focus translates to faster processing, better service, and most importantly, empathy during distress.

The fintech disruption everyone predicted hasn't materialized—at least not how expected. Digital-first players like HomeFirst Finance have gained traction in affordable housing, but they're competing for different customers. The ₹20-50 lakh ticket size that forms Can Fin's bread and butter requires human underwriting that algorithms haven't mastered. When a software engineer claims rental income from his parents' property, you need a human to verify if that property actually exists.

Regulatory changes have actually strengthened Can Fin's position. Higher capital requirements hurt leveraged players but barely impact a company sitting on 24.61% capital adequacy. The ban on foreclosure charges reduced fee income for competitors but didn't affect Can Fin, which never relied on fees. Every regulatory tightening is a moat-widening event for conservative players.

Why has Can Fin survived and thrived? Because in housing finance, slow and steady doesn't just win the race—it's the only sustainable strategy. Real estate is cyclical, interest rates volatile, and credit risk ever-present. Players who optimize for any single environment get crushed when conditions change. Can Fin optimized for survival across cycles, sacrificing growth for resilience.

IX. Playbook: Key Lessons

If Can Fin Homes wrote a playbook for building a financial institution, it would be the antithesis of every startup manual. No blitzscaling, no "move fast and break things," no winner-take-all dynamics. Instead, lessons that feel almost antiquated in their wisdom.

Lesson 1: Patient Capital Compounds Can Fin has grown at 15-18% annually for three decades—unspectacular by any single year's standard, transformative over time. They've never diluted equity for growth, never leveraged beyond comfort, never chased market share at the expense of margins. The result? A 33% CAGR in stock price over 20 years, beating nearly every high-growth story that came and went.

Lesson 2: Trust is Built in Decades, Lost in Days The company has never missed a dividend payment, never surprised investors with sudden NPAs, never changed strategy dramatically. This predictability became their brand. When customers choose Can Fin, they're not buying the best rate or fastest approval—they're buying certainty that the company will exist when their loan matures in 20 years.

Lesson 3: Leverage Parent Strengths Without Dependence Canara Bank's 29.99% shareholding is deliberately below 30% to avoid subsidiary classification. Can Fin uses the bank's brand and distribution but maintains independent underwriting. When Canara Bank faced its own NPA crisis in 2017-18, Can Fin's stock barely moved. The umbilical cord was cut long ago, but the family resemblance remains valuable.

Lesson 4: Focus Beats Diversification in Financial Services Every few years, Can Fin's board discusses entering auto loans, education loans, or personal loans. Every time, they decide against it. Why? Because complexity compounds faster than returns. Each new product requires new skills, systems, and risk models. Better to be exceptional at one thing than mediocre at many.

Lesson 5: Asset Quality is the Only Moat That Matters In financial services, growth is easy—just lower credit standards. Profitability is easy—just increase rates. But maintaining asset quality through cycles? That's hard. Can Fin's sub-1% NPAs aren't luck; they're the result of saying "no" more often than "yes," of choosing the right customers over more customers.

Lesson 6: Manage for the Worst Day, Not the Best Can Fin's executives openly admit they're not maximizing returns. With 24.61% capital adequacy and conservative underwriting, they're leaving money on the table. But they're optimizing for survival through the next crisis, whenever it arrives. As one board member said, "We'd rather explain lower ROE in good times than explain bankruptcy in bad times."

X. Bull & Bear Case Analysis

The Bull Case: Boring is Beautiful

India's housing finance penetration stands at just 11% of GDP versus 40%+ in developed markets. Even reaching 20% penetration implies a doubling of the market. Can Fin Homes, with its conservative approach and pristine asset quality, is perfectly positioned to capture this secular growth without taking undue risks.

The government's "Housing for All by 2024" initiative (now extended to 2030) creates tailwinds for focused housing finance players. Interest subsidies, tax benefits, and infrastructure development in Tier-2/3 cities play directly to Can Fin's strengths. They don't need to change strategy; the market is coming to them.

Strong parentage without interference is a rare combination. Canara Bank's backing provides trust and distribution, but the 29.99% shareholding ensures Can Fin maintains independence. This Goldilocks shareholding structure—not too much, not too little—is almost impossible to replicate.

The asset quality premium will only increase post-COVID. Investors have learned that 200 basis points of extra NIM means nothing if NPAs spike 500 basis points during crises. Can Fin's consistent sub-1% NPAs through multiple cycles deserve a valuation premium that markets are beginning to recognize.

Technology adoption, while slow, is methodical and effective. Can Fin isn't trying to be a fintech—they're using technology to do what they already do better. This measured approach avoids the massive write-offs that aggressive digital transformations often entail.

The Bear Case: Growth Limits and Structural Challenges

The conservative approach that protected Can Fin might now constrain it. In a market where competitors offer 90-95% LTV and instant approvals, Can Fin's 80% LTV and 7-day processing look antiquated. Young homebuyers prioritize convenience over trust, and Can Fin risks aging out of relevance.

Interest rate sensitivity cuts both ways. Can Fin benefits from falling rates, but India's structural inflation suggests rates may remain elevated. With limited pricing power due to competition, margin compression is a real risk. The 3.73% NIM might be peak margin, not sustainable margin.

Real estate sector risks in India are structural, not cyclical. Incomplete projects, title disputes, and builder bankruptcies create risks that even conservative underwriting can't fully mitigate. Can Fin's exposure to urban markets makes them vulnerable to any significant real estate correction.

The competitive intensity is only increasing. Banks with their lower cost of funds, fintechs with their superior customer experience, and NBFCs with their aggressive growth strategies are all attacking Can Fin's niche. Being conservative in a aggressive market might mean slow irrelevance rather than sudden death.

Management succession and culture dilution are underappreciated risks. Can Fin's culture was built over decades by lifers who joined as clerks and retired as executives. The new generation of MBAs and lateral hires might not share the same patient, conservative DNA. Culture drift is invisible until it's too late.

Regulatory changes could eliminate key advantages. If the RBI removes deposit-taking privileges for HFCs or forces priority sector lending requirements, Can Fin's business model would need fundamental restructuring. Regulatory arbitrage that benefits them today could disappear tomorrow.

XI. Looking Forward & Conclusion

The affordable housing opportunity in India isn't just large—it's generational. With 65% of Indians still lacking access to formal housing finance, the addressable market exceeds $500 billion. Can Fin Homes, with its focus on ₹15-30 lakh loans, sits at the sweet spot between subsidy-driven affordable housing and competitive prime mortgages.

Technology imperatives can't be ignored forever. While Can Fin's measured approach to digital transformation has avoided costly mistakes, the pace of change is accelerating. The company that pioneered housing finance for the masses risks being disrupted by players who make it accessible via smartphone. The challenge is adopting technology without abandoning the high-touch model that defines their success.

Geographic expansion into the Northeast and rural markets presents both opportunity and risk. These underserved markets offer growth without intense competition, but they also lack the legal infrastructure and collateral quality that Can Fin depends on. The company must decide whether to modify its model for new markets or stick to what works in urban India.

Product expansion pressures will intensify. With housing loan growth naturally limited by real estate cycles, the temptation to enter adjacent lending verticals will grow. The board's ability to resist this temptation—to choose focus over diversification—will determine whether Can Fin remains exceptional or becomes another mediocre financial conglomerate.

The key metrics to watch aren't the obvious ones. Everyone tracks NPAs and NIMs. The real indicators of Can Fin's health are employee attrition (still below 10%), cost-to-income ratio (holding steady at 16.74%), and geographic concentration (becoming more diversified). These boring metrics predict the future better than any analyst projection.

What's the final verdict on Can Fin Homes? In a world obsessed with disruption, they've proven that consistency is its own form of innovation. While others pivoted, leveraged, and "transformed," Can Fin did the same thing every year, just a little better. They're not the hero of India's housing finance story—they're the reliable supporting character who survives every plot twist.

The Can Fin Homes story is ultimately about the power of compound interest—not just financial, but institutional. Every conservative decision, every rejected loan, every patient quarter compounds into a fortress balance sheet. Every satisfied customer, every retained employee, every kept promise compounds into a brand that transcends metrics.

In 1987, when B. Ratnakar cut that ribbon in Jayanagar, he probably didn't envision a ₹10,000 crore company. He was simply trying to help middle-class Indians buy homes. Thirty-seven years later, that simple mission has created one of India's most successful financial institutions. Not through genius or innovation, but through the radical act of doing what you promise, year after year after year.

The most profound lesson from Can Fin Homes isn't about finance—it's about time. In an industry that measures performance quarterly and careers in years, Can Fin measures success in decades and relationships in lifetimes. They're not playing a different game; they're playing the same game on a different timescale. And on that timescale, boring doesn't just win—it dominates.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube