Morgan Stanley: From White Shoes to Wall Street Survivor

I. Introduction & Episode Roadmap

Picture this: September 19, 2008. Morgan Stanley's stock has cratered 57% in four days. The firm that had survived the Great Depression, thrived through wars, and built empires for America's corporate titans is 48 hours from extinction. In a conference room at Wachtell Lipton, a Japanese banker named Nobuyuki Hirano is about to hand over something extraordinary—a physical check for $9 billion, the largest ever written. It's Columbus Day, the banks are closed, and this piece of paper represents the difference between survival and becoming the next Lehman Brothers.

How did we get here? How did a firm born from regulatory dismemberment in 1935 become one of only two major investment banks to survive the 2008 financial crisis? And perhaps more intriguingly—how did it transform from that near-death experience into a $180 billion market cap financial conglomerate managing over $6 trillion in client assets?

This is the story of Morgan Stanley—a tale of aristocratic origins, brutal meritocracy, catastrophic mergers, existential crises, and ultimately, reinvention. It's about how a white-shoe partnership evolved into a three-legged stool of institutional securities, wealth management, and investment management. It's about culture clashes that nearly destroyed the firm from within before markets could do it from without. And it's about the fundamental question facing every Wall Street firm: in finance, is bigger actually better, or does diversification dilute what makes you special?

We'll trace the journey from Henry Morgan and Harold Stanley's Depression-era startup through the go-go years of investment banking supremacy, the disastrous Dean Witter merger, the 2008 crisis that almost ended everything, and James Gorman's decade-long transformation that turned Morgan Stanley from a volatile trading house into something approaching a utility—albeit one that still mints money.

Along the way, we'll unpack the strategic decisions, the power struggles, the near-misses, and the calculated bets that shaped not just Morgan Stanley, but modern Wall Street itself. We'll explore how a firm's DNA—that original "first-class business done in a first-class way" ethos—can be both its greatest strength and its most dangerous blind spot.

This isn't just a story about investment banking. It's about American capitalism's evolution, the price of survival, and what happens when tradition collides with transformation. So let's start where all great Wall Street stories begin: with a regulatory hammer, a forced breakup, and two men with a famous name who decided to build something new from the pieces.

II. The House of Morgan: Origins & Glass-Steagall

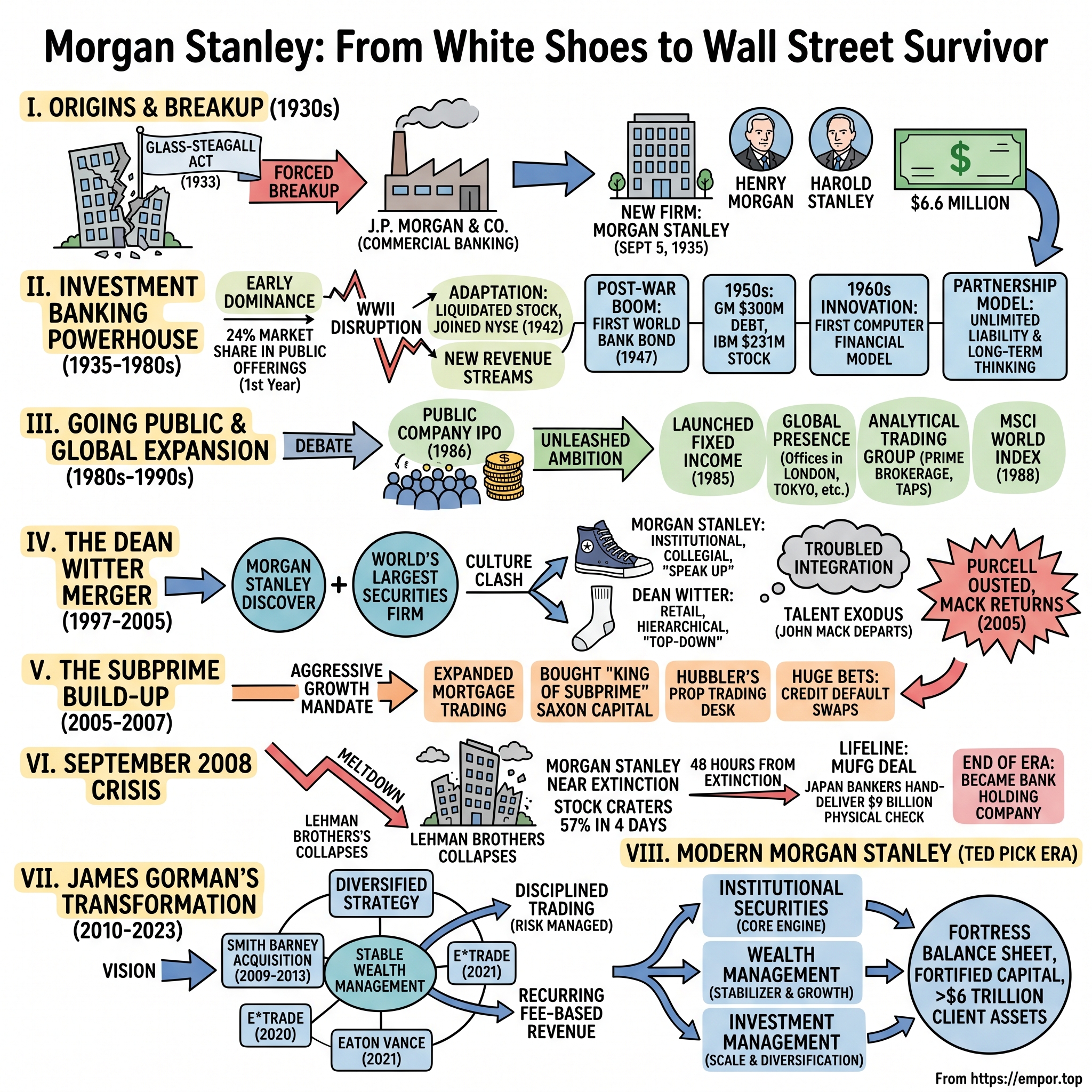

The year is 1933. Franklin Roosevelt has just taken office, banks are failing by the hundreds, and Congress is hunting for villains. In their crosshairs sits the most powerful financial institution in America: J.P. Morgan & Co. For decades, the House of Morgan had been American capitalism's unofficial central bank—financing railroads, steel companies, and even bailing out the U.S. government itself during the Panic of 1907. But now, in the depths of the Depression, that concentrated power looked less like stability and more like systemic risk.

The Glass-Steagall Act of 1933 was Congress's sledgehammer solution: commercial banks could no longer underwrite securities. Investment banks couldn't take deposits. Pick a side. For J.P. Morgan & Co., this meant choosing between its lucrative securities business and its prestigious commercial banking franchise. The firm chose commercial banking, keeping the deposits and the lending relationships but abandoning the high-margin world of underwriting and trading.

This is where our story truly begins. On September 5, 1935, in a wood-paneled conference room at 23 Wall Street, J.P. Morgan & Co. announced that several partners would leave to form a new securities firm. Among them: Henry Sturgis Morgan, grandson of J. Pierpont Morgan himself, and Harold Stanley, a Harvard-educated dealmaker who'd run the securities business. They weren't being cast out—this was a carefully orchestrated spin-off, blessed by the Morgan partnership and backed by $6.6 million in nonvoting preferred stock from J.P. Morgan partners. The name itself tells you everything. Morgan Stanley wasn't just another investment bank—it was the legitimate heir to the House of Morgan, carrying both the bloodline and the culture into the new world of separated banking. The new company was incorporated on September 16, 1935, with $6.6 million of nonvoting preferred stock from J.P. Morgan partners, a financial blessing that signaled continuity rather than rupture.

What's remarkable is the speed at which the new firm established dominance. Morgan Stanley advised on initial public offerings and private placements of securities worth $1.1 billion in its first year—a substantial figure at the time. In Depression-era America, when capital markets were still traumatized and public trust in Wall Street had evaporated, Morgan Stanley managed to capture a 24% market share in public offerings within twelve months.

This wasn't luck—it was legacy. The firm inherited not just the Morgan name but its client relationships, its syndicate partners, and most importantly, its culture. That famous phrase—"first-class business done in a first-class way"—wasn't just marketing copy. It was the firm's operating system, a set of unwritten rules about how to conduct oneself, whom to do business with, and what standards to maintain.

Founded in 1935 as a partnership with a staff of just 13, the firm started small but elite. The firm began its operations with 24 employees and a clear focus on corporate finance and securities. Harold Stanley, at 42, brought operational expertise and a network cultivated at Guaranty Trust. Henry Morgan, J.P.'s grandson, provided the dynastic connection and the implicit guarantee that this was still, in essence, the House of Morgan.

The timing was both terrible and perfect. Terrible because the capital markets were moribund, public faith in Wall Street had collapsed, and new regulations constrained every move. Perfect because the destruction created opportunity for those with capital, connections, and credibility. Morgan Stanley had all three. While other firms struggled to adapt to the new regulatory reality, Morgan Stanley was purpose-built for it—a pure-play investment bank designed from inception to operate within Glass-Steagall's constraints.

As we'll see, this origin story—born from regulation, blessed by legacy, built for a new era—would define Morgan Stanley's trajectory for the next seven decades, through boom and bust, transformation and near-death, until it faced its ultimate test in September 2008.

III. Building the Investment Banking Powerhouse (1935–1980s)

The morning of December 7, 1941, changed everything. Within hours of Pearl Harbor, America was at war, and Morgan Stanley's business model—underwriting securities for corporate America—essentially evaporated. Capital markets froze. Companies stopped expanding. The government commandeered the economy. For a firm not even seven years old, this could have been fatal.

Instead, Morgan Stanley adapted with aristocratic pragmatism. In 1941, Morgan Stanley liquidated its stock and reorganized to qualify for membership on the New York Stock Exchange (NYSE), which it joined in 1942. The move seems technical, even mundane, but it represented a fundamental shift—from pure investment banking toward a more diversified model that included brokerage commissions. When your traditional business disappears, you find new revenue streams or you die.

Henry Morgan himself exemplified this adaptability, joining the navy, where he served on the Joint Army and Navy Munitions Board and as a commander attached to the Naval Command Office of Strategic Services. While the firm survived on consulting fees and the occasional private placement, its leaders were literally helping run the war effort. This wasn't just patriotic duty—it was relationship building at the highest levels of government, connections that would prove invaluable in the post-war boom.

And what a boom it was. In 1947, the firm issued the first bond on behalf of the World Bank to fund post-war reconstruction in Europe. Think about the symbolism: Morgan Stanley, barely a decade old, was chosen to finance the rebuilding of Europe. This wasn't just a deal—it was an anointment as America's premier international investment bank.

The 1950s brought scale that would have seemed fantastical during the Depression. During the 1950s, the firm managed General Motors' $300 million debt issuance—at the time, the largest securities issue ever underwritten. Other major deals during this period included a $231 million IBM stock offering and a $250 million debt offering for AT&T. These weren't just big numbers; they were the financial architecture of American corporate dominance. GM was reshaping transportation, IBM was birthing the computer age, AT&T was wiring the nation. Morgan Stanley was their banker.

But the firm understood that dominance required innovation, not just relationships. In the 1960s, Morgan Stanley developed the first computer model to deal with the increasing complexity of financial analysis. While other white-shoe firms clung to paper and intuition, Morgan Stanley was quantifying risk, modeling scenarios, turning finance into science. This early embrace of technology would become a defining characteristic—the ability to maintain elite culture while adopting cutting-edge tools.

The partnership structure during this period was both strength and constraint. Partners had unlimited liability—their personal fortunes were on the line with every deal. This created extraordinary discipline and alignment. Bad deals didn't just hurt the firm; they could bankrupt the decision-makers. The result was a culture of extreme diligence, careful risk management, and long-term thinking.

Compensation reflected this ethos. Partners didn't just earn salaries or bonuses—they earned partnership points, a share of the firm's profits that could only be realized over time. Leaving meant forfeiting unvested interests. This golden handcuff system created remarkable stability. People joined Morgan Stanley for careers, not jobs. They thought in decades, not quarters.

The "white shoe" mystique wasn't just about breeding or education, though the firm certainly recruited heavily from Harvard, Yale, and Princeton. It was about a particular way of doing business—understated, relationship-driven, with an almost British sense of propriety. Morgan Stanley bankers didn't hustle for deals; clients came to them. They didn't advertise their successes; discretion was assumed. They didn't just execute transactions; they provided counsel to CEOs and boards.

This culture created enormous competitive advantages. In an era before standardized disclosure and modern regulation, trust was everything. When a Morgan Stanley banker said a company was worth $X, the market believed it. When Morgan Stanley led a syndicate, other banks followed. The firm's imprimatur was itself valuable—companies would accept lower valuations to have Morgan Stanley's name on their prospectus.

By the 1970s, Morgan Stanley had become what it set out to be: the premier investment bank in America, perhaps the world. But the ground was shifting. Fixed commissions were ending. Global markets were integrating. New competitors—aggressive, hungry, without the burden of tradition—were emerging. The partnership model that had created the firm's culture was becoming a competitive disadvantage in a world that required ever more capital.

The question facing Morgan Stanley's partners was existential: Could you maintain first-class culture while adopting joint-stock capitalism? Could you stay elite while going public? As we'll see, the answer would prove more complicated than anyone imagined.

IV. Going Public & Global Expansion (1986–1996)

March 1986. The partners of Morgan Stanley gather for what would be the most consequential vote in the firm's history. The question on the table: Should they abandon the partnership structure that had defined them for fifty years and become a public company? The debate was fierce. Old-timers argued it would destroy the culture, turn long-term thinking into quarterly earnings management, transform partners into employees. The younger generation countered that without access to public capital markets, Morgan Stanley would be left behind by Merrill Lynch, Salomon Brothers, and the commercial banks now encroaching on their territory.

Morgan Stanley became a public company in 1986. The decision wasn't just about money—it was about survival in a rapidly changing financial landscape. Fixed commissions had ended in 1975. The globalization of markets demanded enormous capital for trading operations. Clients wanted firms that could commit billions, not millions, to transactions. The partnership model, elegant as it was, simply couldn't generate enough capital to compete.

The IPO itself was a cultural earthquake. Perhaps the biggest shocker was the March IPO of Morgan Stanley, one of the clubbiest of firms since its founding by Henry S. Morgan and five partners For the first time, outsiders could buy a piece of the House of Morgan's legacy. The offering was modest by today's standards, but the symbolism was profound: Morgan Stanley was no longer a private club but a public corporation, answerable to shareholders, subject to quarterly scrutiny, forced to disclose what had always been secret.

But going public also unleashed Morgan Stanley's ambitions. In 1985, Morgan Stanley launched its Fixed Income Division. In 1986, the firm established Morgan Stanley and Co. International Plc, a financial services company operating in Europe, the Middle East, Africa, the Americas and Asia. Over the course of the next few decades, the firm opened offices in Frankfurt, Hong Kong, Luxembourg, Melbourne, Milan, São Paulo, Sydney and Zurich, as well as expanding in London and Tokyo.

The global expansion wasn't just about planting flags. Each office represented a bet on the globalization of capital markets. Morgan Stanley opened its first international office in 1967, launching Morgan & Cie. International in Paris with Morgan Guaranty Trust Co., to pursue the growing European securities market. In 1970, Morgan Stanley was among the first global investment banks to establish a presence in Japan. By the 1980s, these early investments were paying off as cross-border M&A exploded and companies sought global capital.

Technology became another differentiator. Morgan Stanley created its analytical proprietary trading group in 1986, bringing together traders, technical analysts and computer engineers to create and deploy new trading technologies. While other firms saw technology as a cost center, Morgan Stanley saw it as a weapon. The firm that had invented financial modeling in the 1960s was now using computers to find arbitrage opportunities, price derivatives, and manage risk in ways that would have been impossible just years earlier.

In 1984, Morgan Stanley developed the first Trade Analysis Processing System (TAPS), which boosted the volume of accuracy of trades, and formed its Prime Brokerage group to service hedge fund clients. This wasn't just operational efficiency—it was strategic positioning. Prime brokerage would become one of Wall Street's most profitable businesses, and Morgan Stanley was there at the beginning.

But perhaps the most prescient move was seemingly minor at the time. The firm launched the MSCI World Index in 1988, the first comprehensive index of equity markets in developing countries. This wasn't just a data product—it was infrastructure for the coming explosion in emerging markets investing. Today, trillions are benchmarked to MSCI indices, generating steady, high-margin revenue that most investment banks can only dream of.

In 1995, Morgan Stanley moved its global headquarters to its current location at 1585 Broadway in New York. The move from Wall Street to Times Square was both practical and symbolic. The new building offered modern trading floors, advanced technology infrastructure, and room to grow. But it also signaled that Morgan Stanley was no longer defined by proximity to the old financial district. The firm was creating its own center of gravity.

By 1996, Morgan Stanley seemed to have solved the partnership paradox. It had maintained its elite culture while accessing public markets. It had gone global without losing its identity. It had embraced technology without abandoning relationships. Revenue and profits were at record highs. The firm was regularly ranked #1 or #2 in global M&A and equity underwriting.

But success bred hubris. The firm's leaders looked at rivals—particularly Merrill Lynch with its massive retail network and Dean Witter with its credit card business—and saw opportunity. Why shouldn't Morgan Stanley have multiple revenue streams? Why shouldn't it serve Main Street as well as Wall Street? The answer to those questions would nearly destroy everything they had built.

V. The Dean Witter Merger: Culture Clash of the Century (1997–2005)

February 5, 1997. Two press releases hit the wires simultaneously. Morgan Stanley and Dean Witter Discover & Co. would merge in a $10 billion stock swap, creating the world's largest securities firm. Wall Street was stunned. Not because of the size—everyone knew consolidation was coming. But because of the pairing. Morgan Stanley, the ultimate white-shoe investment bank, was marrying Dean Witter, a retail brokerage that had been owned by Sears—yes, the department store—and still carried the Discover Card in its portfolio. As one wag put it: "white shoes and white socks".

The numbers looked compelling. Dean Witter's focus on retail investors, mutual funds and credit cards which were seen by the stock market as generating more stable cash flows than Morgan Stanley's investment banking business had by the time of the merger made it the more valuable partner in terms of market capitalization. Dean Witter brought 9,000 retail brokers, $90 billion in mutual fund assets, and the Discover Card with its steady fee income. Morgan Stanley brought prestige, global reach, and dominance in M&A and trading. Together, they would have a market capitalization of $23 billion, surpassing Merrill Lynch.

But numbers don't capture culture, and culture, as Peter Drucker allegedly said, eats strategy for breakfast. Dean Witter's CEO, Philip Purcell, the main architect of the merger, became chairman and chief executive officer of the merged group. John Mack, Morgan Stanley's president and heir apparent, became president and COO with what was reportedly a handshake agreement to succeed Purcell by 2002. This arrangement—Dean Witter's CEO running Morgan Stanley—would prove toxic.

The cultural divide was immediate and visceral. Morgan Stanley bankers, who saw themselves as advisors to Fortune 500 CEOs, suddenly found themselves in the same company as Dean Witter brokers who sold mutual funds in strip malls. The Morgan Stanley side called it "white shoes meets white socks"—and they didn't mean it as a compliment. Dean Witter employees, meanwhile, resented the arrogance of their new colleagues who acted as if retail brokerage was beneath them.

But the real problem was management philosophy. Dean Witter had a significantly more hierarchical culture than Morgan Stanley. "Dean Witter had a very control from the top culture. No one would go into Phil's office and say, you know, you can't do that. That doesn't make sense. No one challenging — whatever he said they did," said Mack, who was president of Morgan Stanley at the time of the merger. "The Morgan Stanley culture was you speak up if you think it can be done in a more efficient way, a better way, more profitable way. You would speak up".

This wasn't just about corporate democracy—it was about risk management and innovation. Morgan Stanley's culture of challenge and debate had been crucial to its success. Partners argued fiercely behind closed doors, then presented a united front. Ideas were stress-tested through confrontation. Purcell's top-down approach stifled this dynamic. Decisions came from the executive suite with no input, no pushback, no refinement through debate.

The business integration was equally troubled. The promise of cross-selling—Morgan Stanley's investment banking clients using Dean Witter's retail distribution, Dean Witter's retail clients buying Morgan Stanley's sophisticated products—largely failed to materialize. Corporate CEOs didn't want their M&A advisors to also be their employees' retail brokers. Retail investors weren't interested in complex derivatives. The supposed synergies were mostly fantasy.

By 2001, the situation had become untenable. Mack, who was supposed to succeed Purcell, was instead forced out after a power struggle. His departure triggered an exodus of talent. Star bankers and traders left for competitors. Entire teams decamped to Credit Suisse, Deutsche Bank, and other rivals. Morgan Stanley's league table rankings in M&A and equity underwriting began to slip.

By 2005, Morgan Stanley was embroiled in governance and legal problems, which affected its business performance and financial position. The stock price lagged peers. Return on equity trailed Goldman Sachs by wide margins. Perhaps most damaging was a $1.45 billion jury verdict in a fraud case—a verdict directed by the judge as a sanction after Morgan Stanley's attorneys failed to produce documents and allegedly misled the court.

The revolt, when it came, was unprecedented in Wall Street history. A "Group of Eight" former Morgan Stanley executives, including former president Robert Scott and former chairman Parker Gilbert, launched a public campaign to oust Purcell. They took out full-page newspaper ads. They gave interviews. They essentially staged a hostile takeover of their own former firm—from the outside.

Purcell resigned as CEO of Morgan Stanley in June 2005 when a highly public campaign by former Morgan Stanley partners threatened to damage the firm and challenged his refusal to aggressively increase leverage, increase risk, enter the sub-prime mortgage business and make expensive acquisitions. The irony is palpable in hindsight—Purcell was ousted partly for being too conservative, for not taking enough risk, for not diving into subprime mortgages. Within three years, those criticisms would look like virtues.

John Mack returned as CEO on June 30, 2005, to widespread celebration. "Mack is Back" read the internal emails. The stock jumped 8% on the news. But Mack inherited a broken institution. The culture was poisoned. Talent had fled. Market share had eroded. And most dangerously, to prove the firm could still compete, Mack would embark on exactly the aggressive risk-taking his predecessors had been criticized for avoiding. As we'll see, that decision would nearly destroy Morgan Stanley.

VI. The Subprime Build-Up & Risk Taking (2005–2007)

John Mack returned to Morgan Stanley on June 30, 2005, with a mandate to restore the firm's glory. The stock had jumped 8% on news of his return. "Mack is Back" banners hung in the trading floor. But Mack faced a brutal reality: Morgan Stanley had fallen behind Goldman Sachs in nearly every metric that mattered—league tables, trading revenue, return on equity, stock performance. To catch up, he believed, required aggression.

Mack was committed to a more aggressive investment strategy that included increased involvement in the mortgage market. He committed the firm to doubling its revenues in five years and to take bigger, bolder gambles. This wasn't recklessness—it was calculation. Every Wall Street firm was printing money in mortgages. The housing market hadn't had a nationwide decline since the Great Depression. Risk models showed that diversification across geographies made catastrophic losses nearly impossible.

The centerpiece of this strategy was the mortgage trading desk. Under John Mack's leadership, Morgan Stanley made what was described as "a poorly timed push into the mortgage market at the end of 2006." The bank bought Saxon Capital, dubbed the "King of Subprime", for $706 million in December 2006. Saxon was a subprime originator, giving Morgan Stanley direct access to the raw material of the mortgage boom—loans to borrowers with poor credit that could be packaged, sliced, and sold at enormous profit.

But the real money was in proprietary trading—using the firm's own capital to bet on markets. One of Morgan Stanley's own internal proprietary trading units, Process Driven Trading, earned about one quarter of all the firm's net income until the financial meltdown. In the decade up to 2006, this unit made $4 billion and paid the small group of traders staffing it $1 billion, exceeding the pay of Morgan Stanley's chief executives. According to Scott Patterson, few in the firm knew what this unit actually did, and for CEO John Mack all that mattered was that it was profitable most of the time.

Then there was Howie Hubler and his Global Proprietary Credit group. Hubler was Morgan Stanley's point person in the subprime mortgage bond game, as well as the manager of side bets through credit default swaps. Through Hubler's desk, Morgan Stanley was effectively selling worthless triple-B mortgage bonds to investors (often German land banks and pension funds), then betting on those very same bonds to fail through the swaps. Hubler's team became a bank-within-a-bank: by April 2006, they alone were generating an estimated 20 percent of Morgan Stanley's profits.

For the bank's leadership, Hubler was the goose that laid the golden eggs. They didn't understand how he did what he did, they only knew that it continued to make them rich. And they were always afraid that he'd leave to start his own fund. To keep him happy, Morgan Stanley set Hubler up with his own proprietary trading desk (on his own private floor), where he would keep a chunk of the profits he generated.

The crucial decision—the one that would nearly destroy Morgan Stanley—came in late 2006. Hubler had been shorting subprime mortgages through credit default swaps, betting they would fail. But the premiums on these swaps were expensive, eating into profits. So Hubler made what seemed like a clever trade: he sold credit default swaps on higher-rated mortgage securities (AA and AAA tranches) to finance his shorts on the lower-rated ones. The logic was seductive—the AAA securities would never fail, so collecting premiums on them was free money to fund the real bet.

This is where Morgan Stanley got more heavily invested in the housing market when it decided to sell credit default swaps, which were new for the housing market at the time. This move would directly lead the Morgan Stanley's 2008 financial crisis, and the financial crisis more broadly. The firm was now massively long the housing market through these AAA positions, even as it thought it was short through the lower-rated bets.

The warning signs emerged in 2007. In 2007 the quantitative models used by PDT failed, with spectacular losses. For example, on one day alone PDT lost $300 million. The quant models that had worked for years suddenly stopped functioning. A PDT trader, commenting on the huge losses suffered during the crisis from computerized trading, pointed out a basic flaw in the system: "The types of volatility we were seeing had no historical basis. If your model is based on historical patterns and you're seeing something you've never seen before, you can't expect your model to perform."

But the real catastrophe was in Hubler's mortgage book. As subprime loans started defaulting in waves, the AAA securities that were supposed to be bulletproof began to crack. The trade that was supposed to hedge Morgan Stanley's risk had instead concentrated it. When Morgan Stanley finally admitted defeat and exited the trade, they had lost a net $9 billion, the single largest trading loss in Wall Street history. By the end of 2007, the bank lost over $37 billion through the subprime mortgage bond and related derivatives market.

Years later, the government would document the firm's deceptions during this period. In particular, Morgan Stanley told investors that it did not securitize underwater loans (loans that exceeded the value of the property). However, Morgan Stanley did not disclose to investors that in April 2006 it had expanded its "risk tolerance" in evaluating loans in order to purchase and securitize "everything possible." As Morgan Stanley's manager of valuation due diligence told an employee in 2006, "please do not mention the 'slightly higher risk tolerance' in these communications. We are running under the radar and do not want to document these types of things."

By December 2007, Morgan Stanley was hemorrhaging money and credibility. The firm took a $5 billion investment from China Investment Corporation in exchange for securities convertible to 9.9% of its shares. Mack, who had returned to restore the firm's glory, had instead presided over the largest losses in its history. But this was just the prelude. The real test would come nine months later, when Lehman Brothers collapsed and Morgan Stanley found itself 48 hours from extinction.

VII. September 2008: 48 Hours from Extinction

Sunday, September 14, 2008. Lehman Brothers files for bankruptcy. By Monday morning, the contagion has spread. AIG is collapsing. Merrill Lynch has sold itself to Bank of America. And Morgan Stanley, which had seemed relatively healthy just days earlier, is watching its lifeblood—confidence—evaporate by the hour.

The mechanics of an investment bank's death are brutally simple. Unlike commercial banks with sticky deposits, investment banks fund themselves in the wholesale markets—commercial paper, repo agreements, prime brokerage balances. These funding sources can disappear in hours if counterparties lose faith. And faith, once lost, becomes self-fulfilling prophecy. If everyone believes you're going to fail, they pull their money, and you fail.

By Tuesday, September 16, Morgan Stanley's stock had fallen 25%. Hedge funds were pulling prime brokerage assets. Counterparties were demanding more collateral. CEO John J. Mack wrote in a memo to staff "we're in the midst of a market controlled by fear and rumours and short-sellers are driving our stock down." By September 19, 2008, the share price had slid 57% in four days, and the company was said to have explored merger possibilities with CITIC, Wachovia, HSBC, Standard Chartered, Banco Santander and Nomura.

Inside Morgan Stanley's headquarters at 1585 Broadway, Mack was fighting a three-front war. First, keep the firm liquid—ensure enough cash to meet obligations. Second, find capital—a large investment that would restore confidence. Third, fend off the vultures—particularly the U.S. government, which seemed determined to force a merger.

The government's position was stark. Timothy Geithner, president of the New York Fed, and Hank Paulson, Treasury Secretary, believed Morgan Stanley couldn't survive independently. Their solution: merge with JPMorgan Chase. At one point, Hank Paulson offered Morgan Stanley to JPMorgan Chase at no cost, but JPMorgan's Jamie Dimon refused the offer. Even for free, Dimon didn't want the risk.

Mack saw this as a death sentence. A forced merger would wipe out shareholders, destroy jobs, and end Morgan Stanley's 73-year history. He had watched Bear Stearns get sold for $2 per share (later revised to $10) in a government-orchestrated fire sale. He was determined to find another way.

The lifeline came from an unexpected source: Mitsubishi UFJ Financial Group (MUFG), Japan's largest bank. MUFG had been watching the crisis unfold and saw opportunity where others saw disaster. Morgan Stanley had a premier franchise, global reach, and capabilities MUFG couldn't build organically. At the right price, it was worth the risk.

The negotiations were surreal. Teams from both firms held an emergency meeting over Columbus Day weekend in October 2008. After 48 straight hours of negotiations, the two sides had a deal worked out and a final price tag. MUFG is investing $9 billion in equity in Morgan Stanley for a 21 percent interest in the Company on a fully diluted basis. MUFG will acquire 9.9 percent of Morgan Stanley's common stock on a primary basis at a price of $25.25 per share, for a total of $3 billion. MUFG will also acquire $6 billion of perpetual non-cumulative convertible preferred stock with a 10 percent dividend and a conversion price of $31.25 per share.

But then came the final crisis. The deal was done Sunday night. Markets would open Tuesday. Morgan Stanley needed to announce the investment Monday morning to stop the death spiral. But it was Columbus Day in the U.S. and a holiday in Japan. Banks were closed. A wire transfer would take days.

The payment from MUFG was supposed to be wired electronically; however, because it needed to be made on an emergency basis on Columbus Day when banks were closed in the US, MUFG cut a US$9 billion physical check, the largest amount written via physical check at the time. The physical check was accepted by Robert A. Kindler, Global Head of Mergers and Acquisitions and Vice Chairman of Morgan Stanley, at the offices of Wachtell Lipton.

The image is almost absurd: Japanese bankers walking through Manhattan with a piece of paper worth $9 billion, hand-delivering it to save one of Wall Street's most storied firms. Top-level executives from Mitsubishi UFJ reportedly hand-delivered the check to Morgan Stanley on Monday, October 13th, 2008, and also took a few pictures to remember the occasion.

The announcement changed everything. Morgan Stanley immediately announced to the world that they had a done deal. On Tuesday, their stock surged 85% from $9.68 to $17.92. The death spiral stopped. Confidence began to return.

But Morgan Stanley wasn't done transforming. Morgan Stanley and Goldman Sachs, the last two major investment banks in the US, both announced on September 22, 2008, that they would become traditional bank holding companies regulated by the Federal Reserve. This was the end of an era. The independent investment bank model, which had dominated Wall Street since Glass-Steagall, was dead. Morgan Stanley would now be a bank—with all the regulations, capital requirements, and restrictions that entailed.

The government also forced Morgan Stanley to take $10 billion in TARP funds, which the firm would repay with interest by June 2009. Morgan Stanley borrowed $107.3 billion from the Fed during the 2008 crisis, the most of any bank, according to data compiled by Bloomberg News Service—a number that shows just how close the firm came to collapse.

Looking back, Morgan Stanley's survival seems almost miraculous. The firm that had advised on $1.1 billion in deals in its first year in 1935 had nearly died with trillions under management in 2008. It survived not through strength but through desperation, foreign capital, and a physical check that arrived just in time. The Morgan Stanley that emerged would be fundamentally different—less profitable, more regulated, but ultimately more stable. The transformation from investment bank to diversified financial services firm was about to begin.

VIII. The Transformation: From Investment Bank to Diversified Financial Services (2009–2020)

January 1, 2010. James Gorman takes the helm as CEO of Morgan Stanley. An Australian-born lawyer who'd run wealth management at Merrill Lynch, Gorman was an unlikely choice to lead Wall Street royalty. But the board saw something others missed: Gorman understood that the age of pure investment banking was over. The future belonged to diversified financial services firms with multiple, stable revenue streams.

Gorman's vision was deceptively simple: transform Morgan Stanley from a volatile trading house dependent on market conditions into a balanced financial services firm with predictable earnings. The centerpiece would be wealth management—boring, steady, fee-based revenue that didn't disappear when markets crashed.

The opportunity had emerged from crisis. Citigroup, decimated by the financial meltdown, needed capital desperately. Among its assets was Smith Barney, one of America's largest retail brokerages with 18,000 financial advisors and nearly $2 trillion in client assets. For Gorman, this was the deal of a lifetime.

On January 13, 2009, the Global Wealth Management Group was merged with Citi's Smith Barney to form Morgan Stanley Smith Barney. Morgan Stanley owned 51% of the entity, and Citi held 49%. The structure was clever—Morgan Stanley could buy additional stakes over time at pre-negotiated prices, spreading out the capital requirements while immediately gaining scale.

On May 31, 2012, Morgan Stanley exercised its option to purchase an additional 14% of the joint venture from Citi. In June 2013, Morgan Stanley stated it had secured all regulatory approvals to buy Citigroup's remaining 35% stake in Smith Barney and would proceed to finalize the deal. The staggered acquisition meant Morgan Stanley ultimately paid about $13.5 billion for a business that would become the crown jewel of its transformation.

But integration was brutal. In 2011, margins in the wealth business were only 7%. Press headlines were calling Gorman's strategy a failure. Smith Barney financial advisers were enraged by the poor technology platform that Morgan Stanley provided. Plenty were leaving what they thought was a sinking ship, taking their clients with them. One advisor even accused wealth management head Greg Fleming of being "the captain of the Titanic" at a town hall meeting.

Gorman's response revealed his management philosophy. When he'd first arrived at Morgan Stanley in 2006, he'd inherited 10,000 advisors and massive legal problems. Analysis showed most issues came from low-producing advisors. His solution was ruthless: he fired 2,000 of them. "People saw it as us losing 2,000 advisers," Gorman told Euromoney. "We saw it as firing several hundred million dollars of legal problems."

With Smith Barney, he took a different approach—massive investment in technology and patient integration. The firm essentially rebuilt its wealth management technology platform from scratch, spending billions to create systems that could compete with Charles Schwab and Fidelity. By 2013, the bleeding had stopped. By 2015, wealth management was generating consistent profits.

But Gorman didn't stop there. He understood that wealth management was evolving from stockbroking to holistic financial services. Clients didn't just want investment advice—they wanted banking, lending, cash management. Morgan Stanley needed to become their clients' primary financial relationship.

In February 2019, the company announced the acquisition of Solium Capital, a manager of employee stock plans, for $900 million. This gave Morgan Stanley access to corporate employees at the moment they received equity compensation—a prime opportunity to capture new wealth management clients.

The masterstroke came in 2020. In October 2020, the company completed its acquisition of ETrade, a deal announced in February 2020 for $13 billion, the biggest acquisition by a U.S. bank since the 2008 financial crisis. ETrade brought 5.2 million client accounts and $360 billion in assets, but more importantly, it brought digital capabilities and self-directed investors who could eventually be upgraded to full-service wealth management.

In March 2021, Morgan Stanley completed its acquisition of Eaton Vance, a deal announced in October 2020. With the addition of Eaton Vance, Morgan Stanley now had $5.4 trillion of client assets across its Wealth Management and Investment Management segments. Eaton Vance added scale in asset management and crucial capabilities in customized separately managed accounts.

The transformation's impact was staggering. When Gorman became CEO, wealth management generated single-digit margins and volatile revenues. By 2023, wealth management had brought in $19.6 billion of revenues over the first nine months of this year – up 10% on the same period in 2022 – with a return on average tangible common equity of 35% and, perhaps most remarkable, a pre-tax profit margin of 26%.

Meanwhile, Gorman was quietly revolutionizing the institutional securities business as well. Rather than abandon investment banking and trading, he made them more disciplined. Risk limits were enforced ruthlessly. Compensation was tied to multi-year performance. The casino culture that nearly destroyed the firm was replaced with careful risk management.

The results spoke for themselves. Morgan Stanley's stock price rose from under $20 in 2010 to over $100 by the time Gorman stepped down as CEO in December 2023. Return on equity stabilized in the mid-teens. The firm that had borrowed $107 billion from the Fed in 2008 was now one of the best-capitalized banks in America.

In May 2023, Gorman announced his forthcoming retirement as CEO of Morgan Stanley. He was succeeded as CEO by Ted Pick on January 1, 2024, while remaining executive chairman of the firm's board. Unlike many Wall Street successions, this one was smooth, planned, and drama-free—itself a testament to the cultural transformation Gorman had achieved.

The Morgan Stanley that Gorman handed to his successor bore little resemblance to the firm he'd inherited. It was no longer just an investment bank that happened to have some retail brokers. It was a balanced financial services firm where wealth management generated nearly half of revenues, where technology was a competitive advantage, and where culture emphasized long-term client relationships over short-term trading profits. The transformation from Wall Street casino to Main Street advisor was complete.

IX. The Modern Morgan Stanley: Three Pillars Strategy

Standing at 1585 Broadway today, Morgan Stanley operates as a fundamentally different institution than at any point in its 89-year history. The company operates in three business segments: Institutional Securities, Wealth Management, and Investment Management. Each pillar supports the others, creating what executives call an "integrated firm" where the whole exceeds the sum of its parts.

The numbers tell the story of transformation. Morgan Stanley now manages over $6 trillion in client assets. It employs over 80,000 people across 42 countries. Market capitalization exceeds $180 billion. But the real change is in the business mix—wealth management, which barely existed in the original Morgan Stanley, now generates roughly 45% of revenues and an even higher percentage of profits.

Institutional Securities: The Evolved Engine

The institutional securities division—investment banking, sales and trading, research—remains the firm's historical core, but it operates under fundamentally different principles than during the go-go years. Risk limits are sacrosanct. Proprietary trading is minimal. The focus has shifted from betting the firm's capital to facilitating client transactions.

Investment banking still commands premium fees for blue-chip advisory work. Morgan Stanley consistently ranks in the top three globally for M&A advisory, equity underwriting, and debt capital markets. But the cowboy culture is gone. Bankers talk about "connectivity"—leveraging the firm's wealth management relationships to win corporate mandates, using investment banking relationships to capture wealth management assets when executives liquidate stock.

The trading business has been similarly transformed. The days of Howie Hubler betting billions on mortgage derivatives are ancient history. Today's trading is primarily client-driven—market-making, hedging, facilitating transactions. Technology and quantitative strategies dominate, but within strict risk parameters. The Process Driven Trading unit that once lost $300 million in a day has been replaced by disciplined, systematic approaches with multiple fail-safes.

Wealth Management: The Stabilizer and Growth Driver

The wealth management transformation that Gorman engineered has created what is arguably the premier wealth management franchise globally. With over 16,000 financial advisors and $4.5 trillion in client assets, Morgan Stanley Wealth Management serves everyone from mass affluent to ultra-high-net-worth individuals.

But the real innovation isn't size—it's integration. A Morgan Stanley wealth management client can access investment banking deals, structured products from the institutional side, alternative investments from the asset management division, lending from the commercial bank, even workplace financial services through the Solium platform. No other firm offers this breadth under one roof.

Technology has become a massive differentiator. The E*Trade acquisition brought not just assets but digital capabilities that Morgan Stanley is deploying across its platform. Artificial intelligence helps advisors identify opportunities and risks in client portfolios. Robo-advisory services handle simple transactions, freeing human advisors for complex planning.

The business model has evolved from transaction-based commissions to fee-based advisory relationships. This creates predictable, recurring revenue that doesn't evaporate in market downturns. Average household wealth management client assets exceed $250,000, but the firm serves segments from workplace stock plan participants to billionaires.

Investment Management: Scale Through Acquisition

The investment management division, managing over $1.5 trillion, represents Morgan Stanley's quietest transformation. Built through acquisitions like Van Kampen, Eaton Vance, and Calvert, it provides asset management services to institutions and individuals globally.

The strategy here is diversification—traditional active management, passive indexing, alternatives, ESG strategies, customized solutions. The MSCI indices, that prescient 1988 innovation, remain a crown jewel, with trillions benchmarked to them globally and generating steady licensing revenue.

But investment management also feeds the other divisions. Wealth management clients buy investment management products. Institutional clients use both traditional asset management and alternatives. The division provides stable, fee-based revenue while supporting the integrated firm model.

The Technology Arms Race

Across all three pillars, technology has become existential. Morgan Stanley spends over $4 billion annually on technology—not just for efficiency but for competitive advantage. AI and machine learning identify trading opportunities, predict client needs, detect fraud, optimize capital allocation.

The firm's approach to technology reflects its cultural evolution. Where once it might have tried to build everything internally, Morgan Stanley now partners aggressively—with fintechs, with cloud providers, with data analytics firms. The Solium and E*Trade acquisitions were as much about acquiring technology capabilities as client assets.

Cybersecurity has become paramount. The firm employs thousands of cybersecurity professionals and conducts constant threat assessments. A major breach could destroy client trust instantly—the one asset no amount of capital can replace.

Ted Pick Era: Continuity or Change?

Ted Pick is Chairman and Chief Executive Officer of Morgan Stanley. Before becoming CEO in January 2024 and Chairman in January 2025, Pick represented internal continuity. A 34-year Morgan Stanley veteran who'd run equities, fixed income, and the entire institutional securities group, Pick understood both the firm's heritage and its transformation.

Pick's early moves suggest evolution rather than revolution. He's emphasized the "integrated firm" model, pushing for more collaboration between divisions. Wealth management continues to expand, with plans to grow deposits from $130 billion to $400 billion. The institutional business focuses on gaining share in areas like prime brokerage and equity derivatives.

But Pick faces new challenges. Regional banks' failures in 2023 raised questions about financial stability. Regulatory scrutiny has increased, particularly around wealth management practices. Competition has intensified—JPMorgan and Bank of America have built formidable wealth management franchises, while Goldman Sachs is attempting its own transformation.

The competitive landscape has fundamentally shifted. JPMorgan, with its massive balance sheet and diversified revenue streams, has become the undisputed king of Wall Street. Bank of America leverages its retail banking base to feed wealth management. Goldman Sachs, Morgan Stanley's historical rival, is attempting its own pivot toward stable revenues, though with mixed results.

Meanwhile, new competitors emerge constantly. Private equity firms like Apollo and Blackstone compete for alternative investment mandates. Fintechs like Robinhood and Betterment challenge traditional wealth management models. Chinese banks expand globally. The competitive moat that once protected Morgan Stanley has narrowed.

Yet Morgan Stanley's position remains formidable. The integrated model creates genuine synergies. The brand still carries prestige that opens doors globally. The culture, painfully transformed through crisis and renewal, emphasizes long-term client relationships over short-term profits. In a world where trust is increasingly scarce, Morgan Stanley has rebuilt its reputation as a firm that survives, adapts, and ultimately thrives.

X. Playbook: Business & Investing Lessons

Morgan Stanley's journey from Depression-era spinoff to modern financial conglomerate offers a masterclass in organizational resilience, strategic transformation, and the price of survival. The lessons extend far beyond banking—they're applicable to any business facing existential change.

Lesson 1: Culture Can Be Both Moat and Trap

Morgan Stanley's "first-class business done in a first-class way" culture was its greatest asset for decades. It attracted the best talent, won the most prestigious clients, and maintained standards that competitors couldn't match. But that same culture nearly destroyed the firm twice—first during the Dean Witter merger when cultural arrogance prevented integration, then in 2005-2007 when the need to maintain "first-class" returns drove catastrophic risk-taking.

The lesson: Cultural strengths become weaknesses when contexts change. The partnership culture that created Morgan Stanley couldn't generate enough capital for global competition. The relationship-banking culture couldn't integrate with retail brokerage. The risk-taking culture that drove innovation nearly caused collapse. Successful organizations must be willing to evolve their cultures while maintaining core values—a delicate balance Morgan Stanley only achieved through near-death experience.

Lesson 2: Diversification Requires Conviction Through the Painful Middle

Gorman's wealth management transformation took over a decade. For years, margins were terrible, advisors were leaving, technology was failing, and critics called the strategy a disaster. Many CEOs would have reversed course. Gorman doubled down, investing billions in technology and patiently integrating acquisitions.

The pattern repeats throughout Morgan Stanley's history. The international expansion of the 1970s-80s took decades to pay off. The building of trading capabilities required massive upfront investment. The transformation to bank holding company status meant accepting lower returns for years.

The lesson: True diversification is painful and slow. The temptation to retreat to core competencies is overwhelming, especially when activists and analysts demand immediate returns. But concentration risk—whether in business lines, geographies, or revenue models—is ultimately existential. Morgan Stanley survived 2008 partly because it had diversified beyond pure investment banking. It thrives today because Gorman had conviction through the painful middle of transformation.

Lesson 3: M&A Culture Fit Matters More Than Strategic Fit

The Dean Witter merger made perfect strategic sense—investment banking plus retail brokerage equals diversified financial services. It was a disaster because the cultures were incompatible. Dean Witter's hierarchical, retail-focused culture clashed violently with Morgan Stanley's collegial, institutional culture. The result was a decade of infighting that weakened both businesses.

Contrast this with the Smith Barney acquisition. Gorman understood the cultural challenges and addressed them systematically—investing in technology to win over advisors, maintaining separate brands during transition, gradually integrating systems and processes. The E*Trade and Eaton Vance acquisitions followed similar patterns—patient, thoughtful integration that preserved what made each business successful.

The lesson: In M&A, culture eats strategy for breakfast, lunch, and dinner. Strategic fit means nothing if the organizations can't work together. Successful acquirers either buy businesses with compatible cultures or invest heavily in cultural integration. Morgan Stanley learned this lesson at enormous cost.

Lesson 4: Capital Allocation in Cyclical Businesses Requires Counter-Cyclical Thinking

Investment banking and trading are inherently cyclical—enormous profits in good times, massive losses in bad times. Most firms amplify these cycles through their capital allocation, investing aggressively at peaks (like Morgan Stanley in 2006-2007) and retrenching in troughs.

Gorman's genius was counter-cyclical thinking. He bought Smith Barney when Citi was desperate in 2009. He acquired E*Trade during COVID uncertainty in 2020. He invested billions in technology during the European debt crisis when competitors were cutting costs. This patient, contrarian capital allocation created enormous value.

The lesson: In cyclical businesses, the best investments are made when things look worst. This requires not just financial capacity but organizational confidence—the ability to invest for the long term when everyone else is fighting for survival. Morgan Stanley's transformation succeeded because it had both the capital (thanks to MUFG) and leadership willing to deploy it counter-cyclically.

Lesson 5: Regulatory Relationships Are Strategic Assets

Morgan Stanley's survival in 2008 hinged partly on regulatory relationships. The Fed's willingness to let it become a bank holding company, access to emergency lending facilities, the government's blessing of the MUFG investment—all required regulatory trust built over decades.

But the firm also learned that regulatory antagonism is destructive. The Perelman case, where Morgan Stanley's lawyers allegedly misled the court, resulted in a $1.45 billion verdict. Poor compliance in wealth management led to massive fines. Regulatory violations in trading caused reputational damage beyond any financial penalty.

Today, Morgan Stanley invests heavily in compliance and maintains deep regulatory relationships. Senior executives regularly engage with regulators. The firm often leads industry initiatives on new regulations. This isn't just defense—it's offense. Good regulatory relationships provide flexibility in crisis and competitive advantage in normal times.

Lesson 6: Technology Is Never Just About Efficiency

Every major Morgan Stanley transformation involved technology. The 1960s computer models for financial analysis. The 1980s Trade Analysis Processing System. The 2010s wealth management platform rebuild. The current AI and cloud investments. But the lesson isn't about being first—it's about understanding technology's strategic value.

Morgan Stanley succeeded when it used technology to enable new business models, not just improve existing ones. MSCI indices created an entirely new revenue stream. Electronic trading platforms captured market share. Digital wealth management tools attracted new client segments. The failures came when technology was seen as just cost reduction—the initial Smith Barney integration failed partly because Morgan Stanley underinvested in technology.

The lesson: Technology investments should be evaluated not on ROI but on strategic optionality. What new businesses does this enable? What competitive advantages does it create? What risks does it mitigate? Morgan Stanley's survivors understood that technology shapes strategy, not the reverse.

Lesson 7: Building Recurring Revenue in Transaction Businesses

Investment banking and trading are inherently transactional—you're only as good as your last deal. This creates enormous volatility. Morgan Stanley's evolution has been about building recurring revenue streams within these transactional businesses.

Wealth management fees recur annually. Asset management charges ongoing management fees. MSCI indices generate subscription revenue. Prime brokerage creates sticky client relationships. Even in investment banking, Morgan Stanley focuses on retainer relationships and multi-year advisory mandates.

The result: more predictable revenues, higher valuations, lower cost of capital. The market values recurring revenue streams at higher multiples than transactional revenue. Morgan Stanley trades at premium valuations partly because nearly 60% of revenues are now relatively stable.

The lesson: Every business, no matter how transactional, can build recurring elements. It requires different metrics (client lifetime value vs. transaction profit), different incentives (relationship rewards vs. deal bonuses), and different capabilities (service excellence vs. execution excellence). But the stability created is worth the investment.

These lessons—about culture, diversification, M&A, capital allocation, regulation, technology, and revenue models—explain not just Morgan Stanley's survival but its transformation. They're applicable far beyond banking. Any organization facing disruption, seeking transformation, or simply trying to build lasting value can learn from Morgan Stanley's journey from white shoes to Wall Street survivor.

XI. Analysis & Bear vs. Bull Case

After nearly 90 years, multiple near-death experiences, and fundamental transformations, where does Morgan Stanley stand today? The answer depends on your perspective. Bulls see a transformed financial services giant with diversified revenue streams and competitive moats. Bears see a complex conglomerate with lower returns than pure-plays and facing structural headwinds. Both have compelling arguments.

The Bull Case: A Transformed Powerhouse

Bulls start with the wealth management franchise. At $4.5 trillion in client assets with 16,000 advisors, Morgan Stanley has achieved unprecedented scale in the most attractive segment of financial services. Wealth management generates predictable, capital-light, high-margin revenues that grow with markets and demographics. As baby boomers transfer $70 trillion to millennials over the next two decades, Morgan Stanley is perfectly positioned to capture this intergenerational wealth transfer.

The integrated model creates genuine competitive advantages. A tech founder can work with Morgan Stanley investment bankers on an IPO, wealth managers on personal finances, and the private bank on lending—all with seamless coordination. This "one firm" approach is difficult for competitors to replicate and creates sticky client relationships that compound over time.

Technology investments are finally paying dividends. The rebuilt wealth management platform rivals any competitor. AI-driven insights help advisors serve clients better. Digital capabilities from E*Trade attract younger clients who will eventually need full-service wealth management. Morgan Stanley has successfully bridged the analog-digital divide that threatens traditional financial services.

The balance sheet is fortress-strong. Tier 1 capital ratios exceed 15%, well above regulatory requirements. The firm weathered the 2023 regional banking crisis without stress. Deposit growth in wealth management provides stable, low-cost funding. Morgan Stanley can invest through cycles, acquire opportunistically, and return capital to shareholders consistently.

Management execution has been exceptional. The smooth CEO transition from Gorman to Pick demonstrates operational excellence. The successful integration of multiple large acquisitions shows execution capability. The cultural transformation from trading house to client-focused firm, while maintaining performance, is genuinely remarkable.

Valuation remains reasonable despite the transformation. Morgan Stanley trades at roughly 12-13x forward earnings and 1.5x tangible book value—not demanding for a business generating mid-teens ROE with significant growth potential. As the business mix continues shifting toward wealth management, multiple expansion seems likely.

The Bear Case: Structural Challenges and Declining Returns

Bears counter that Morgan Stanley's transformation, while impressive, has come at the cost of returns. ROE in the mid-teens is respectable but hardly exceptional. Pure-play investment banks like Goldman Sachs can generate 20%+ returns in good years. Focused wealth managers like Charles Schwab have higher margins. Morgan Stanley's conglomerate structure creates complexity without commensurate returns.

The wealth management business faces structural headwinds. Fee compression continues as passive investing grows and robo-advisors proliferate. Younger investors prefer self-directed platforms to traditional advisors. The $250,000 average account size seems substantial, but it's unclear if millennials will ever embrace the full-service model their parents used.

Technology disruption threatens every business line. Cryptocurrency and DeFi could disintermediate traditional banking. AI might replace junior bankers and traders. Fintech companies unbundle financial services, cherry-picking profitable segments. Morgan Stanley's massive technology investments might be just running to stand still against disruption.

Regulatory constraints limit profitability. As a systemically important financial institution, Morgan Stanley faces higher capital requirements, more compliance costs, and greater scrutiny than smaller competitors. The bank holding company structure, while providing stability, permanently reduces returns compared to the pre-2008 model.

Competition has intensified across all segments. JPMorgan's scale advantages seem insurmountable. Bank of America leverages its retail base more effectively. Goldman Sachs remains dominant in high-margin advisory. International banks compete aggressively in wealth management. Private equity firms take market share in alternatives. Morgan Stanley is strong everywhere but dominant nowhere.

The economic cycle poses risks. Investment banking and trading remain cyclical despite diversification. A serious recession would hit all three business segments simultaneously. Market declines reduce wealth management fees, investment banking deal flow, and trading volumes. The supposedly stable business model hasn't been tested in a prolonged downturn.

Integration complexity creates hidden risks. Managing three distinct businesses with different cultures, compensation models, and regulatory requirements is inherently difficult. The promise of synergies often disappoints. Cybersecurity risks multiply with complexity. One serious operational failure could damage the entire franchise.

Competitive Positioning: Strong but Not Dominant

Morgan Stanley occupies an interesting competitive position—clearly in the top tier of global financial institutions but not dominant in any single business. This creates both stability and challenge.

Versus JPMorgan: JPM's scale advantages are overwhelming—$4 trillion in assets, $2 trillion in deposits, dominant in every business line. But Morgan Stanley's focused wealth management strategy and superior technology integration give it advantages in specific segments. The David vs. Goliath dynamic forces Morgan Stanley to be more innovative and client-focused.

Versus Goldman Sachs: The historical rivalry continues but in different directions. Goldman remains the premier pure-play investment bank with higher returns but more volatility. Morgan Stanley's diversified model provides more stability but lower peaks. Interestingly, Goldman is now attempting its own wealth management transformation, validating Morgan Stanley's strategy.

Versus Bank of America: BofA's Merrill Lynch wealth management division competes directly with Morgan Stanley, leveraging the retail bank's 66 million customers. But Morgan Stanley's independent platform and superior technology arguably serve ultra-high-net-worth clients better. The competition is segment-specific rather than head-to-head.

Versus Boutiques and Fintechs: Boutique investment banks take share in specialized advisory. Fintech wealth managers attract younger clients. But Morgan Stanley's integrated model and global reach provide advantages in complex, cross-border transactions and comprehensive wealth management. The firm competes by moving upmarket rather than fighting on price.

The Next Decade Outlook

Looking forward, Morgan Stanley faces fascinating strategic questions. Can it maintain wealth management margins as competition intensifies? Will investment banking consolidation create opportunities or threats? How will AI and blockchain reshape financial services? Can the integrated model survive increasing regulatory complexity?

The bull case sees Morgan Stanley continuing its transformation, perhaps acquiring additional wealth management assets, expanding internationally, and leveraging technology to serve clients better. Wealth management grows to 60% of revenues, ROE expands to high teens, and the stock re-rates to premium multiples.

The bear case envisions margin compression across all businesses, integration challenges from complexity, and disruption from new technologies and business models. The conglomerate structure proves unwieldy, returns decline to low teens, and the stock trades at a persistent discount.

The reality will likely fall between these extremes. Morgan Stanley has proven remarkably adaptable—surviving the Depression, thriving post-war, navigating deregulation, surviving 2008, and transforming its business model. This adaptability, more than any specific strategy, may be its greatest asset.

The firm's journey from white-shoe partnership to global financial conglomerate reflects broader changes in American capitalism. The questions facing Morgan Stanley—about technology, regulation, globalization, and purpose—are questions facing all major corporations. How it answers them will determine not just its own future but provide lessons for business transformation in the 21st century.

XII. Epilogue & Reflections

Standing in the Morgan Stanley lobby at 1585 Broadway today, you're surrounded by the ghosts of multiple firms. The aristocratic investment bank that opened at 2 Wall Street in 1935 with 13 employees. The go-go trading house that bet billions on mortgages. The desperate institution saved by a $9 billion check. The transformed wealth manager serving millions of Americans. Each incarnation seems impossible from the perspective of the previous one.

This is perhaps the most profound lesson from Morgan Stanley's story: organizational identity is more fluid than we imagine. The firm that once refused to work with any company below investment grade now serves retail investors with $50,000 accounts. The partnership that made decisions over brandy and cigars now uses artificial intelligence to analyze millions of data points. The institution that nearly collapsed from concentrated risk now preaches diversification as gospel.

Yet something essential persists through these transformations. Call it DNA, culture, or organizational memory—Morgan Stanley retains an identity distinct from JPMorgan's imperial ambition or Goldman's trader swagger. It's visible in the emphasis on advisory over trading, the preference for long-term relationships over quick profits, the careful balance between innovation and tradition. The phrase "first-class business done in a first-class way" may seem anachronistic, but its spirit endures in modernized form.

The transformation also illustrates a broader truth about American capitalism. The separation of commercial and investment banking that created Morgan Stanley has been reversed. The independent investment bank model that defined Wall Street for decades is extinct. The distinction between retail and institutional financial services has blurred beyond recognition. Morgan Stanley's evolution mirrors these systemic changes while also driving them.

For founders and leaders, Morgan Stanley offers both inspiration and caution. The inspiration comes from its resilience—the ability to survive existential crises, transform business models, and emerge stronger. Few organizations navigate one fundamental transformation successfully; Morgan Stanley has managed several. This requires not just strategic vision but organizational courage—the willingness to abandon what made you successful when context changes.

The caution comes from the price of survival. Morgan Stanley exists today because it accepted lower returns, embraced regulation, and abandoned the freewheeling culture that defined it for decades. The firm that exists today is safer, more stable, and more socially responsible than its predecessors—but also less profitable, less innovative, and less distinctive. Whether this trade-off was worth it depends on your perspective on capitalism's purpose.

The ongoing question—is bigger better in banking?—remains unresolved. Morgan Stanley's journey suggests size provides stability and resources for transformation but reduces returns and increases complexity. The firm is too big to fail but perhaps also too big to excel. It can weather any crisis but struggles to dominate any market. This tension between resilience and excellence defines modern banking and, increasingly, modern business.

What would Henry Morgan and Harold Stanley think of the firm bearing their names? They'd likely be astonished by the scale—managing trillions rather than millions, operating globally rather than from a single office, serving millions rather than dozens of blue-chip clients. They might be disturbed by the democratization—their exclusive partnership now serves retail investors, their private deliberations now subject to quarterly earnings calls, their handshake deals replaced by thousand-page contracts.

But they'd probably recognize the essential mission: channeling capital from those who have it to those who need it, advising organizations through transformation, helping individuals preserve and grow wealth. The mechanisms have changed dramatically—algorithms replace intuition, regulations replace relationships, diversification replaces concentration. But the fundamental purpose endures.

Morgan Stanley's story is far from over. New challenges emerge constantly—climate change, cryptocurrency, artificial intelligence, geopolitical fragmentation. Each could trigger another transformation as profound as Glass-Steagall or the 2008 crisis. The firm's history suggests it will adapt, though at what cost remains unknown.

For investors, Morgan Stanley represents a fascinating study in value creation through transformation. The stock has generated enormous returns for those who bought during crises and held through transformations. But it's also destroyed value for those who bought at peaks expecting continuation of trends. The lesson: in transforming organizations, timing and patience matter more than analysis.

For competitors, Morgan Stanley demonstrates both the possibility and difficulty of fundamental change. Many firms attempt transformation; few succeed. The difference often comes down to leadership willing to accept short-term pain for long-term gain, cultures capable of evolution while maintaining coherence, and balance sheets strong enough to invest through cycles.

For regulators and policymakers, Morgan Stanley embodies the complexities of modern finance. It's more stable than before 2008 but also more complex. It serves more stakeholders but with potential conflicts of interest. It's safer individually but contributes to systemic concentration. These tensions have no easy resolution.

Ultimately, Morgan Stanley's journey from white shoes to Wall Street survivor is about adaptation—the most essential organizational capability. In a world of accelerating change, the ability to transform while maintaining identity, to diversify while preserving focus, to modernize while respecting tradition, becomes existential. Morgan Stanley has mastered this balance better than most, though at considerable cost.

The firm that started as a regulatory accident has become a case study in organizational evolution. Its story continues to unfold, shaped by forces beyond any institution's control—technology, regulation, competition, society's expectations. How it navigates these forces will determine not just its own future but provide lessons for any organization seeking to survive and thrive through fundamental change.

As we reflect on nearly nine decades of history, one thing seems certain: the Morgan Stanley of 2034 will be as different from today's firm as today's is from 1935's. The only constant is change, and the only sustainable advantage is the ability to adapt. In this, Morgan Stanley has proven remarkably, sometimes painfully, but ultimately successfully capable. The white shoes may be gone, but the survivor endures.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube