Ameriprise Financial: From Midwest Roots to Wall Street Heights

I. Introduction & Episode Framing

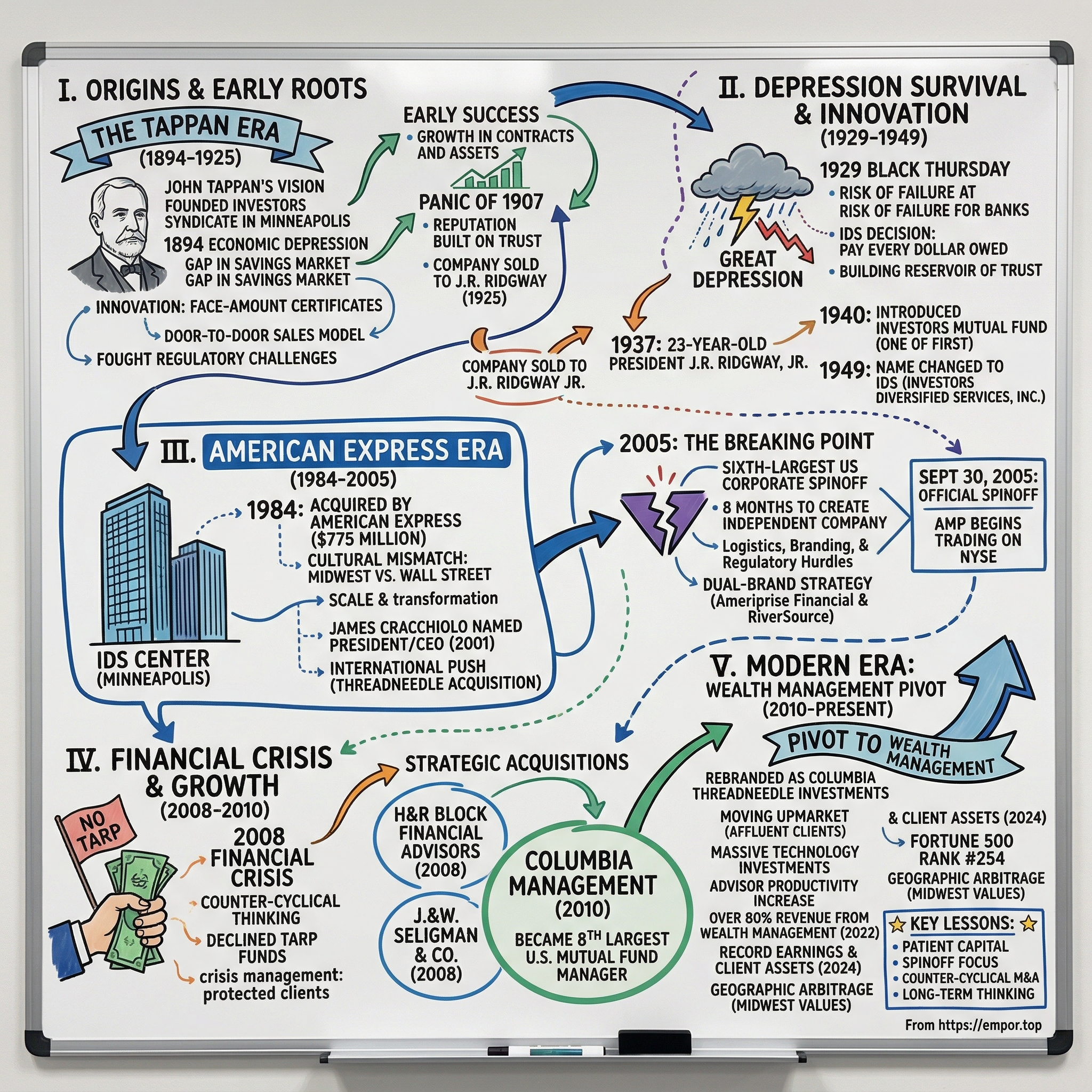

Picture this: October 3, 2005. The opening bell rings at the New York Stock Exchange, and a new ticker symbol—AMP—begins trading. But this isn't your typical IPO story. This is the sixth-largest corporate spinoff in U.S. history, a $7.6 billion financial services giant breaking free from American Express after two decades under its wing. The man at the helm? Jim Cracchiolo, a Brooklyn-born executive who'd spent his entire career climbing the ranks, now suddenly tasked with steering an independent ship through uncharted waters.

Here's the paradox that makes this story remarkable: Ameriprise Financial was simultaneously brand new and 111 years old. While the name was freshly minted in a Minneapolis conference room just months earlier, the company's DNA traced back to 1894, when a 24-year-old entrepreneur named John Tappan knocked on doors in the Twin Cities, selling something called "face-amount certificates" with nothing but $2,500 in assets and an audacious dream.

The central question driving this narrative isn't just how a door-to-door savings certificate company survived the Great Depression, two world wars, and countless economic cycles. It's how this Midwestern financial institution—through multiple identities, ownership changes, and strategic pivots—emerged as one of the most successful wealth management platforms in America, now overseeing $1.4 trillion in client assets and delivering returns that have crushed both the S&P 500 and its financial sector peers.

This is a story about patient capital meeting opportunistic execution. About Midwest values colliding with Wall Street ambitions. About a company that paid every single dollar owed during the darkest days of the 1930s, building a reservoir of trust that would compound for a century. It's about transformation—from selling certificates to farmers, to pioneering mutual funds, to becoming a wealth management powerhouse serving everyone from Main Street to Park Avenue.

What we're about to unpack is how a Minneapolis-based face certificate company became Investors Syndicate, morphed into IDS, got swallowed by American Express, and ultimately emerged as Ameriprise—a Fortune 500 company that turned a messy divorce into one of the great wealth creation stories of the 21st century. Along the way, we'll see how counter-cyclical thinking, strategic acquisitions during crises, and an almost religious devotion to client service created a financial services juggernaut that most people have never heard of, yet millions depend on.

The roadmap ahead takes us from those first door-to-door sales calls in 1894 to today's digital wealth management platforms. We'll witness the company's near-death experiences and its phoenix-like rebirths. We'll explore how Jim Cracchiolo transformed a cultural misfit within American Express into a focused, high-performing standalone enterprise. And we'll examine whether this 130-year-old startup can maintain its momentum in an era of robo-advisors, fee compression, and generational wealth transfer.

So let's rewind to 1894, to a young man with a radical idea about helping ordinary Americans save money, and trace how that simple concept evolved into one of the most compelling turnaround stories in modern finance.

II. Origins: John Tappan's Vision (1894-1925)

The year was 1894, and America was in the grip of one of its worst economic depressions. Banks were failing at an alarming rate—over 500 would collapse that year alone. Unemployment soared past 18%. In this unlikely moment, with the economy in ruins and public trust in financial institutions evaporating, 24-year-old John Tappan decided to start a savings company in Minneapolis.

Tappan wasn't a banker or a Wall Street financier. He was a salesman who'd spent years observing how ordinary Americans—farmers, shopkeepers, factory workers—struggled to save money. Banks were for the wealthy; they required minimum deposits that working families couldn't meet. Life insurance was expensive and complicated. There was a massive gap in the market, and Tappan thought he'd found a way to fill it.

His innovation was elegantly simple: the face-amount certificate. Think of it as a forced savings plan with a twist. Customers would commit to making regular monthly payments—as little as $5—over a fixed period, typically 10 years. At maturity, they'd receive the face amount of the certificate, say $1,000, which included their principal plus accumulated interest. If they needed money before maturity, they could borrow against the certificate's value. It was savings, investment, and emergency fund rolled into one. But what made Tappan's approach revolutionary wasn't just the product—it was the distribution model and the underlying philosophy. Tappan and local Minneapolis attorney Henry Farnham submitted articles of incorporation for Investors Syndicate, which was organized under the general incorporation statute of Minnesota in July 1894 with $50,000 in capital. Instead of waiting for customers to come to him, Tappan recruited salesmen to go door-to-door, bringing financial services directly to people's homes. Tappan applied the smalltown and rural door-to-door sales techniques of life insurance to agricultural banking and eventually branched out into other investment products.

The early days were brutal. By the end of 1894, Investors Syndicate had assets of just $2,500. Tappan faced immediate regulatory challenges that nearly killed the company in its infancy. In January 1897, the postmaster general of Washington State accused Investors Syndicate of "being engaged in a lottery for the distribution of money," and the company was accused of fraud and lost its mailing privileges. After various appeals, Tappan and Farnham managed to successfully appeal to their congressman and have their mailing privileges restored.

The regulatory battles revealed a crucial insight: Tappan wasn't just fighting for his business—he was fighting to create an entirely new category of financial services. Tappan's certificates paid around 6 percent, which was several points above what banks could offer and well above the 2 percent on government bonds or 3 percent on railroad bonds. This higher return naturally attracted scrutiny from regulators who suspected fraud or gambling schemes.

Personal tragedy and triumph intertwined with the company's growth. In November 1896, Tappan married Winifred Gallagher, a secretary and Irish immigrant. That January, Tappan graduated from the University of Minnesota College of Law. Winnie typed company letters and ran the office, becoming an integral part of the Investors Syndicate team. This partnership—both personal and professional—would prove essential as the company navigated its early crises.

By the end of 1899, Investors Syndicate had written over 300 contracts, done $100,000 in business, and paid out over $11,000 in returns to its early investors. The growth was slow but steady. Investors Syndicate reached $1 million in assets in the early 1900s, a psychological milestone that validated Tappan's vision.

Then came the Panic of 1907, the first major test of Investors Syndicate's resilience. The Panic of 1907 spread through the country, bankrupted brokerage firms and prompted investors to pull their money out of banks. This was the moment that would define the company's character for the next century. While banks failed and trust companies collapsed, Investors Syndicate met every obligation. Every certificate holder who came due received their money. This wasn't just good business—it was the foundation of a reputation that would carry the company through even darker days ahead.

The success through the 1907 panic attracted attention from a new breed of entrepreneur. In 1925, West Coast entrepreneur J.R. Ridgway purchased Investors Syndicate from founder John Tappan and his partners, merging his investment firm with Investors Syndicate and taking over as president. Tappan, after three decades of building his vision from nothing, stepped aside.

What Tappan had created wasn't just a company—it was a template for democratizing finance. He'd proven that ordinary Americans, given the right tools and trustworthy intermediaries, could participate in wealth creation previously reserved for the elite. The face-amount certificate might seem quaint today, but in 1894, it was as innovative as any fintech startup. And unlike many financial innovations that would follow, it was built on a simple principle: help regular people save money safely and earn a fair return.

As Ridgway took the helm in 1925, Investors Syndicate stood at a crossroads. The Roaring Twenties were in full swing, speculation was rampant, and the financial world was about to face its greatest test. The company that Tappan built on Minnesota values and door-to-door sales was about to discover whether those foundations were strong enough to weather the storm that nobody saw coming.

III. Depression Era Survival & Mutual Fund Innovation (1929-1949)

The telegram arrived at Investors Syndicate headquarters in Minneapolis on October 24, 1929—Black Thursday. The New York Stock Exchange had just witnessed the most devastating selling in its history. Sixteen million shares traded hands. Fortunes evaporated. By Tuesday, October 29, the market had lost $14 billion in value. For a company whose entire business model depended on Americans having money to save and confidence in financial institutions, this should have been a death sentence.

J.R. Ridgway, who'd taken over from Tappan just four years earlier, gathered his executives in the boardroom. The question wasn't whether they'd survive—it was how many of their certificate holders they could protect while everything around them burned. What happened next would become the stuff of company legend and establish a trust that would compound for generations. While 744 U.S. banks failed during the first 10 months of 1930, with 9,000 banks failing during the 1930s, Investors Syndicate made a decision that would define its reputation for the next century: They would pay every dollar owed, on time, no matter what. This wasn't just a business decision—it was a moral stand that would echo through generations. The mantle of leadership during the Depression fell to an unlikely figure. In 1937, upon the death of then 50-year-old J. R. Ridgway from leukemia, 23-year-old J. R. Ridgway, Jr. was appointed president. Picture this: a 23-year-old inheriting control of a financial services company in the middle of the worst economic crisis in American history. Most board members would have sought experienced hands. Instead, they bet on youth, family continuity, and the Ridgway name.

The company's performance during this period reads like financial fiction. During the decade of the Great Depression, Investors Syndicate paid every dollar on its due date to certificate owners. Think about what that meant: While 744 U.S. banks failed during the first 10 months of 1930, with 9,000 banks failing during the 1930s, and by April 1933, around $7 billion in deposits had been frozen in failed banks, every single Investors Syndicate certificate holder who came due received their money. Not 98%. Not 99%. One hundred percent.

This wasn't luck or conservative investing alone—it was a philosophy baked into the company's DNA from Tappan's earliest days. The face-amount certificates, by design, were backed by diversified, conservative investments, primarily in real estate mortgages and high-grade bonds. When everyone else was chasing returns in the stock market during the Roaring Twenties, Investors Syndicate stayed boring. Boring saved them.

By 1937, company assets reached $100 million, a remarkable achievement considering the economic devastation around them. To put this in perspective: unemployment peaked at nearly 25%, farm prices had collapsed by 60%, and industrial production had fallen by half. Yet here was a Minneapolis financial company not just surviving but growing.

The real genius move came in 1940, at the tail end of the Depression. Investors Syndicate introduced one of the first mutual funds, the Investors Mutual Fund, giving clients new investing options and two advantages: diversification and professional management. This wasn't just product innovation—it was democratization of investment management. Before mutual funds, diversified professional management was available only to the wealthy. Now, someone with $100 could access the same diversification principles that protected large fortunes.

The timing was counterintuitive but brilliant. Launching an equity product after the worst stock market crash in history required either stupidity or profound conviction about the future. Young Ridgway bet on the latter. By the 1960s, Investors Mutual Fund would become the largest balanced mutual fund in the world.

Investors Stock Fund and Investors Selective Fund followed in 1945. Ruth Abrahamson joined the company in 1946 and later became the number one female sales representative in the country. Abrahamson's success was particularly remarkable in an era when women were largely excluded from financial services. She didn't just break the glass ceiling—she shattered sales records, proving that the company's door-to-door model could work with anyone who had the drive and integrity to execute it.

The cultural transformation during this period was as important as the financial one. The Depression had fundamentally changed Americans' relationship with money. The get-rich-quick mentality of the 1920s was replaced by a desperate desire for security. Investors Syndicate, having never betrayed that trust, found itself perfectly positioned. Their salesforce could knock on doors and truthfully say: "We paid every dollar through the Depression."

In 1949, recognizing that the company had evolved far beyond its original face-amount certificate business, Investors Syndicate changed its name to Investors Diversified Services, Inc. (IDS). The new name reflected a new reality: this was no longer just a savings certificate company but a diversified financial services firm offering mutual funds, insurance, and financial planning.

What's remarkable about this period is what didn't happen. There was no government bailout. No emergency capital raise. No dramatic restructuring. Just steady, conservative management and an absolute commitment to meeting obligations. In an era when cash-strapped corporations and municipal governments defaulted on their debts, IDS's record stood as a beacon of reliability.

The company emerged from the Depression with something more valuable than assets: trust that had been tested in the crucible of the worst economic disaster in American history and found unbreakable. That trust would become the foundation for everything that followed—expansion into insurance, the American Express acquisition, and eventually, the transformation into Ameriprise.

As America entered the 1950s and the post-war boom began, IDS wasn't just another financial services company that had survived the Depression. It was the company that had kept every promise when keeping promises seemed impossible. That reputation, earned dollar by dollar through the darkest decade, would propel the company into its next chapter of explosive growth.

IV. The American Express Era: Scale & Transformation (1984-2005)

Harvey Golub sat across from the IDS board in the Minneapolis boardroom in 1984, outlining American Express's vision. The financial services giant, flush with cash from its charge card empire and hungry for diversification, saw IDS as the perfect acquisition—a Midwest gem with deep client relationships, a proven distribution model, and most importantly, a culture of trust that money couldn't buy. The price: $775 million for a company that had grown from those humble $2,500 beginnings into a financial services powerhouse. The acquisition wasn't straightforward. IDS had become a wholly owned subsidiary of Alleghany Corporation pursuant to a merger in 1979, and in 1984, American Express acquired IDS Financial Services from Alleghany Corporation. The original deal to acquire all of Alleghany was a stock purchase involving 22.875 million American Express shares then worth $1.01 billion, and through a sales force of about 4,500 agents, IDS managed $16.6 billion in assets.

The cultural mismatch was evident from day one. IDS, with its Midwest roots and focus on middle-class Americans, suddenly found itself owned by a company synonymous with Wall Street prestige and "Don't Leave Home Without It" exclusivity. American Express officials saw the purchase as a way to bring the financial services concern into a middle market that neither its Shearson brokerage arm nor its travel and entertainment card operation generally served.

For IDS employees in Minneapolis, the acquisition brought both opportunity and anxiety. The company maintained its headquarters in the iconic IDS Center—the tallest building in Minneapolis that Mary Tyler Moore had made famous—but now reported to New York executives who didn't always understand or appreciate the door-to-door, relationship-based model that had built IDS.

Effective January 1, 1995, IDS changed its name to American Express Financial Corporation, doing business as American Express Financial Advisors (AEFA). The rebranding was more than cosmetic—it represented American Express's attempt to leverage its prestigious brand across the entire financial services spectrum. Suddenly, the advisors who had been selling mutual funds in Iowa farmhouses were carrying American Express business cards.

The transformation accelerated under a rising star named Jim Cracchiolo. James Cracchiolo was named President and CEO of American Express Financial Advisors in 2001, after serving in various leadership roles since joining the company as a young CPA. Cracchiolo, a Brooklyn native with degrees from Hunter College and NYU, understood both worlds—the scrappy, entrepreneurial spirit of IDS and the sophisticated, global ambitions of American Express.

Under Cracchiolo's leadership, AEFA began expanding beyond its traditional domestic market. In October 2003, AEFA acquired London-based Threadneedle Asset Management Holdings, marking a significant push into international asset management. This wasn't just geographic expansion—it was a strategic bet that the wealth management principles that worked in Minneapolis could scale globally.

The integration period revealed fundamental tensions. American Express wanted synergies—cross-selling credit cards to AEFA clients, pushing AEFA products through Amex channels. But the cultures clashed. AEFA's advisors built their business on long-term relationships and comprehensive financial planning. The American Express card business was transactional, focused on spending and rewards. Trying to merge these models often felt like forcing a square peg into a round hole.

By 2000, Cracchiolo had risen to Group President of American Express Global Financial Services, overseeing not just AEFA but American Express's entire financial services portfolio. He was building something unique: a platform that combined financial planning, insurance, asset management, and banking under one roof. But he was doing it within a larger organization that increasingly saw financial advisory as a non-core business.

The numbers told a story of growth despite the tensions. By 2005, AEFA had grown to more than 12,000 advisors and registered representatives serving more than 2.7 million individual, business, and institutional clients. Assets under management had exploded from that $16.6 billion at acquisition to hundreds of billions. The business was profitable, growing, and by most metrics, successful.

But success within American Express came with constraints. Investment decisions required approval from New York. Technology investments competed with credit card systems for priority. Most frustratingly for Cracchiolo and his team, American Express's regulatory issues in other divisions created reputational challenges for AEFA. In July 2005, New Hampshire reached a $7.4 million settlement with Ameriprise Financial Advisors, alleging the company had violated the law by rewarding their financial advisers for recommending underperforming in-house mutual funds to clients.

The breaking point came gradually, then suddenly. Kenneth Chenault, American Express's CEO, was focused on the card business and saw financial advisory as increasingly peripheral. Wall Street analysts complained that American Express was too complex, that the financial advisory business deserved a different multiple than the card business. Activist investors began pushing for a breakup.

By early 2005, the decision was made: American Express would spin off AEFA as an independent company. The announcement sent shockwaves through the Minneapolis headquarters. After 21 years as part of American Express, they were being set free—or cut loose, depending on your perspective.

The spinoff represented one of the most complex corporate divorces in history. Ameriprise Financial became an independent, publicly-owned company through the 6th largest spin-off in U.S. history. Eight months—that's all the time they had to create a public company from scratch. New brand, new systems, new everything.

The transformation challenges were immense. AEFA shared technology systems with American Express that had to be separated. Client contracts had to be rewritten. Regulatory approvals were needed from every state. A new brand had to be created that could stand on its own while maintaining client trust. And all of this had to happen while continuing to serve millions of clients without disruption.

Cracchiolo later described the period as "People comfortably ensconced in Fortune 50 company told to build a ship and sail on their own". The relationship with American Express during the transition was "less than positive," with former mentors suddenly treating AEFA as a competitor rather than a colleague.

As September 30, 2005 approached—the date of the official spinoff—the questions mounted. Could a Minneapolis-based financial services firm compete independently in a world dominated by Wall Street giants? Would clients trust a brand they'd never heard of? Could Cracchiolo transform a division into a standalone company?

The American Express era had given IDS scale, sophistication, and global reach. But it had also constrained its entrepreneurial spirit and created cultural tensions that never fully resolved. Now, as Ameriprise Financial prepared to debut on the NYSE, the company founded in 1894 on Minnesota values was about to discover whether those values could still compete in the 21st century.

V. The Great Spinoff: Creating Ameriprise (2005)

The conference room on the 47th floor of the IDS Center was packed with lawyers, bankers, and brand consultants on a humid July evening in 2005. Jim Cracchiolo stood at the whiteboard, crossing off rejected names. "IDS" couldn't be used—American Express owned it. "American Express Financial Advisors" was obviously out. They'd been through hundreds of options: Archstone, Luminous, Broadridge. Nothing felt right. Then someone suggested combining "American" with "Enterprise." Ameriprise. It wasn't perfect, but it was available, trademarkable, and suggested both heritage and ambition. With less than two months until the spinoff, they had their name.

In September 2005, American Express completed the corporate spin-off of AEFA as Ameriprise Financial, Inc., a public company. The creation of Ameriprise represented something unprecedented in financial services: taking a 111-year-old company that had been folded into a Fortune 50 corporation and spinning it out as a standalone entity in just eight months.

The logistics alone were staggering. Ameriprise needed to establish 67 new legal entities, obtain regulatory approvals in all 50 states, separate IT systems that had been integrated for two decades, create new financial reporting systems, establish independent credit facilities, and build a brand from scratch—all while continuing to serve 2.7 million clients without missing a beat.

Cracchiolo assembled a war room of 200 executives who worked around the clock. The technology separation was particularly brutal. American Express and AEFA shared customer databases, trading systems, and back-office operations that had been intertwined for 21 years. They had to build parallel systems, test them exhaustively, and execute a cutover without losing a single client record or transaction.

The brand challenge was equally daunting. Research showed that clients trusted their individual advisors but had little attachment to the American Express Financial Advisors brand. The new identity needed to maintain advisor relationships while establishing corporate credibility. The solution: a dual-brand strategy. The company would be Ameriprise Financial, while the insurance and annuity products would carry the RiverSource brand—a nod to the Mississippi River that flows through Minneapolis.

The regulatory gauntlet was relentless. Each state insurance department needed to approve the new entities. The SEC required extensive documentation. NASD (now FINRA) had to approve the new broker-dealer. One delayed approval could derail the entire timeline. Ameriprise's legal team, led by general counsel Walter Berman, essentially lived in conference rooms for six months, managing multiple parallel approval processes.

Then came the employee challenge. Jim Cracchiolo became Chairman and Chief Executive Officer of Ameriprise Financial, but he needed to convince 10,000 employees and 12,000 advisors to bet their careers on an unknown brand. The message was carefully crafted: "We're not starting over; we're starting out—with 111 years of experience, strong financials, and the freedom to control our destiny."

The financial engineering of the spinoff was complex. American Express distributed one share of Ameriprise for every five shares of American Express stock. The new company would start with approximately $420 million in capital, a AA- credit rating, and no debt to American Express. But the separation agreement contained landmines—Ameriprise had to indemnify American Express for various pre-spinoff liabilities, including ongoing regulatory investigations.

September 30, 2005, the spinoff became official. That weekend, one of the largest technology migrations in corporate history took place. Every client account, every transaction, every piece of data had to be moved from American Express systems to Ameriprise systems. Teams worked in shifts through 72 straight hours. By Monday morning, October 3, when AMP began trading on NYSE, the migration was complete. Not a single client transaction was lost.

The first day of trading was nerve-wracking. AMP opened at $37 per share, giving the company a market cap of approximately $9 billion. By day's end, over 13 million shares had traded hands. The market's verdict: cautious optimism. Analysts praised the company's strong advisor force and client relationships but worried about regulatory overhangs and competition from larger players.

The cultural transformation was immediate and profound. For two decades, Minneapolis employees had existed in the shadow of New York headquarters. Now, suddenly, they were the headquarters. Decisions that used to take months of corporate approval could be made in days. Investments in technology and marketing no longer competed with credit card priorities.

But freedom came with challenges. The regulatory issues inherited from the American Express era immediately surfaced. In December 2005, Ameriprise agreed to pay $12.3 million to settle NASD charges relating to favorable treatment allegedly given to some mutual funds in exchange for brokerage business. These settlements, while related to pre-spinoff activities, damaged the new brand before it could establish itself.

Cracchiolo's response was swift and decisive. He instituted new compliance procedures, invested heavily in ethics training, and made it clear that regulatory infractions would not be tolerated. The message to advisors was blunt: "We will compete on service and performance, not on pushing proprietary products."

The spinoff also revealed operational challenges. Without American Express's purchasing power, vendor contracts were more expensive. Credit facilities had to be renegotiated. The company's debt rating was lower as a standalone entity, increasing borrowing costs. Health insurance and other employee benefits became more expensive without American Express's scale.

Yet there were unexpected benefits. Freed from American Express's constraints, Ameriprise could make acquisitions that would have been impossible before. The company could enter new markets, launch new products, and most importantly, create compensation structures that aligned with long-term wealth management rather than short-term transaction fees.

The advisor force responded enthusiastically to independence. Retention, which many analysts expected to plummet, actually increased. Advisors who had considered leaving for independent firms stayed, energized by the entrepreneurial spirit and improved technology investments. Recruiting improved as Ameriprise could offer equity compensation in a pure-play wealth management firm rather than a diversified financial conglomerate.

By the end of 2005, just three months after the spinoff, the transformation was evident. Employee satisfaction scores increased. Advisor productivity improved. Client retention remained strong. The company that many Wall Street analysts had written off as "American Express's unwanted stepchild" was proving it could stand on its own.

The spinoff's success challenged conventional wisdom about corporate separations. Typically, spinoffs involved unwinding failed acquisitions or divesting underperforming divisions. Ameriprise was neither—it was a profitable, growing business that simply didn't fit its parent's strategy. The execution proved that with the right leadership, clear vision, and flawless execution, even the most complex corporate divorces could create value for all parties.

As 2006 dawned, Ameriprise faced a critical test. The easy part—if any of it could be called easy—was complete. The company existed, the systems worked, the brand was established. Now came the hard part: proving that a Minneapolis-based financial services firm with Midwest values could compete against Wall Street giants, Silicon Valley disruptors, and everything in between. The financial crisis that no one saw coming would soon provide that test in ways no one could have imagined.

VI. Financial Crisis & Strategic Acquisitions (2008-2010)

Jim Cracchiolo's phone rang at 2 AM on September 15, 2008. Lehman Brothers had just filed for bankruptcy. AIG was teetering. Reserve Primary Fund, a money market fund where Ameriprise clients had parked $775 million they thought was as safe as cash, had "broken the buck"—its net asset value had fallen below $1 per share. By dawn, Cracchiolo had made a decision that would define Ameriprise's reputation for the next decade: the company would advance $700 million of its own capital to make clients whole, immediately, no questions asked. The scene in Ameriprise's crisis management center that September morning was controlled chaos. While other financial institutions were lining up for government bailouts—with 12 of the nation's 13 largest banks "at the risk of failure within a week or two" according to Fed Chairman Ben Bernanke—Cracchiolo made a contrarian decision. Ameriprise would not only decline government assistance but would use the crisis as an opportunity to grow. The Reserve Primary Fund crisis perfectly illustrated Ameriprise's approach to the financial crisis. In September 2008, the company volunteered to pay as much as $33 million to cover investor losses in the Reserve Primary Fund when it became the first major money market mutual fund ever to "break the buck." But the actual exposure was much larger—when the Reserve Fund froze assets, the company responded by advancing its clients approximately $700 million to help them meet immediate cash needs during a period of extreme market volatility. This wasn't required. It wasn't expected. It was simply the right thing to do.

During the Great Recession, the company declined an investment by the United States Department of the Treasury under the Troubled Asset Relief Program. While Congress authorized $700 billion for TARP and Treasury invested $204.9 billion in 707 financial institutions, Ameriprise stood apart. Cracchiolo was confident that the company's capital position "is more than adequate" without federal assistance. This decision wasn't just about financial strength—it was about sending a message to clients, advisors, and competitors: Ameriprise didn't need a bailout because it hadn't taken the risks that necessitated one.

The contrast with competitors was stark. Of the nation's 13 largest banks, "12 were at the risk of failure within a week or two" of the initial bailout period, in late September and October of 2008. Every single one of those banks took huge bailout payments. Meanwhile, Ameriprise was shopping.

The financial crisis created what Cracchiolo called "a once-in-a-generation opportunity to acquire quality franchises at attractive prices." While others were selling assets to survive, Ameriprise was buying assets to thrive. The strategy was simple: identify strong businesses temporarily weakened by market conditions, acquire them at distressed prices, and integrate them into Ameriprise's platform.

In November 2008, the company acquired H&R Block Financial Advisors for $315 million, and the asset management firm J. & W. Seligman & Co. for $440 million. During the Great Recession while others took bailouts, Ameriprise acquired H&R Block Financial Advisors—growing their advisor force by 30% and extending national reach and visibility.

The H&R Block acquisition was particularly strategic. It brought 4,000 financial advisors and $27 billion in client assets, instantly expanding Ameriprise's geographic footprint into markets where it had limited presence. These advisors served mass affluent clients—exactly Ameriprise's sweet spot—through H&R Block's extensive tax preparation network. The price was a fraction of what it would have been two years earlier.

J. & W. Seligman brought something different: investment management expertise dating back to 1864 and $18 billion in assets under management. The firm's expertise in growth equity investing complemented Ameriprise's existing capabilities. Again, the price reflected distressed market conditions rather than fundamental business value.

The integration challenges were immense. Bringing on 4,000 new advisors meant converting technology platforms, retraining staff, and managing cultural differences—all while markets remained volatile and clients remained nervous. Ameriprise created dedicated integration teams, invested heavily in training, and most importantly, assured new advisors that they'd have the same autonomy and support they'd enjoyed before.

In May 2010, Ameriprise Financial acquired Columbia Management, the long-term asset management business of Bank of America, for $1 billion. This was the crown jewel of crisis-era acquisitions. Columbia brought $170 billion in assets under management, making Ameriprise the eighth-largest manager of long-term U.S. mutual fund assets overnight. Bank of America, forced to raise capital to repay TARP funds and meet new regulatory requirements, sold a business it would never have parted with under normal circumstances.

The Columbia acquisition transformed Ameriprise from primarily a distribution company into a serious asset management player. It brought institutional capabilities, international reach through the Threadneedle brand, and most importantly, scale in an industry where scale drives profitability.

Throughout this acquisition spree, Ameriprise maintained discipline. Every deal had to meet strict financial criteria: immediate earnings accretion, strategic fit with existing businesses, and achievable cost synergies. Cracchiolo personally reviewed every major integration decision, ensuring that client service never faltered during transitions.

The counter-cyclical strategy extended beyond acquisitions. While competitors cut advisor compensation and reduced technology spending, Ameriprise invested. The company enhanced its wealth management platform, improved digital capabilities, and maintained advisor payout ratios. The message was clear: while others retreated, Ameriprise advanced.

By 2010, the transformation was complete. Ameriprise had emerged from the financial crisis not just unscathed but fundamentally stronger. Assets under management had grown from $456 billion in 2007 to $675 billion in 2010. The advisor force had expanded by 40%. Most importantly, the company had proven that patient capital and strategic courage could turn crisis into opportunity.

The financial crisis period also revealed the depth of Ameriprise's cultural transformation since the spinoff. The company that had once been criticized for pushing proprietary products now advanced $700 million of its own money to protect clients. The firm that had struggled with regulatory issues now operated with such conservative principles that it didn't need government assistance. The Minneapolis-based outsider had become one of the winners of Wall Street's darkest hour.

As markets recovered and normalcy returned, Ameriprise faced a new challenge: proving that its crisis-era gains were sustainable. The acquisitions needed to deliver promised synergies. The expanded advisor force needed to grow organically. And most critically, the company needed to demonstrate that its newfound scale could translate into superior returns for shareholders. The next decade would answer these questions decisively.

VII. Modern Era: Wealth Management Pivot (2010-Present)

The war room on the 50th floor of Ameriprise's new Minneapolis headquarters buzzed with activity in early 2015. Jim Cracchiolo stood before a wall-sized display showing the company's business mix: insurance and annuities still generated 35% of earnings, asset management contributed 28%, and wealth management delivered 37%. "By 2020," he declared to his leadership team, "wealth management will be over half our earnings. That's where the future is." It was a bold prediction that would require dismantling parts of the business that had sustained the company for decades.

With the Columbia Management acquisition, Ameriprise Financial became the eighth-largest manager of long-term U.S. mutual fund assets. But Cracchiolo saw beyond the immediate benefits of scale. The entire financial services industry was undergoing a secular shift. Baby boomers were entering their peak wealth accumulation years. Fee compression was crushing traditional asset management margins. Robo-advisors were threatening to commoditize basic investment advice. The companies that would win weren't those clinging to yesterday's business models but those building tomorrow's.

The pivot began with rebranding. In 2015, the asset management arm begins operating under the Columbia Threadneedle Investments name, unifying the Columbia and Threadneedle brands globally. This wasn't just administrative tidiness—it was a strategic decision to separate manufacturing from distribution, allowing each business to optimize independently.

The real transformation happened in the wealth management division. Ameriprise began systematically moving upmarket, focusing on clients with $500,000 to $5 million in investable assets—the "mass affluent" and "affluent" segments that offered the best combination of scale and profitability. The company invested heavily in technology platforms that allowed advisors to deliver institutional-quality portfolio management to individual clients.

The results were dramatic. By 2018, 48% of pretax operating earnings came from the advice and wealth management division, up from 37% just three years earlier. The business model evolution from insurance/annuities to wealth management focus was accelerating faster than even Cracchiolo had predicted.

As of April 2022, more than 80% of the company's revenue came from wealth management. This wasn't just a shift in revenue mix—it was a fundamental reimagining of what Ameriprise was. The company that had started selling face-amount certificates door-to-door was now competing with Goldman Sachs and Morgan Stanley for high-net-worth clients.

The technology investments were massive and transformative. Ameriprise built a proprietary wealth management platform that integrated financial planning, portfolio management, and client reporting into a seamless digital experience. Advisors could model complex scenarios in real-time, showing clients how market changes, tax law modifications, or life events would impact their long-term plans.

But technology was just an enabler. The real competitive advantage was the advisor force. By 2024, Ameriprise had approximately 10,000 financial advisors, down from the peak of 12,000 but far more productive. Average advisor productivity increased by over 50% between 2015 and 2024, driven by better technology, more affluent clients, and improved practice management support.

The company's approach to advisor recruitment and retention became a case study in the industry. While competitors fought over established advisors with astronomical signing bonuses, Ameriprise focused on organic growth and advisor development. The firm created sophisticated succession planning programs, helping aging advisors transition their practices to younger partners while maintaining client relationships.

The regulatory environment post-financial crisis actually helped Ameriprise's pivot. The Department of Labor's fiduciary rule (though later vacated) accelerated the industry's shift from commission-based to fee-based advice. Ameriprise, which had been moving in this direction already, was better positioned than competitors still dependent on transaction fees. The financial performance validated the strategy decisively. Q4 2024 results revealed the transformation's success: Advice & Wealth Management pretax adjusted operating earnings of $823 million, up 18%, with a 29% margin. The adjusted operating EPS of $9.36 excluding unlocking represented a ROE ex-AOCI of 52.7%—numbers that would make any Wall Street bank envious.

The 2024 annual results were even more impressive: Annual net income of $3.401 billion, up 33% from 2023. This wasn't just growth—it was acceleration. The company that had struggled to find its identity within American Express was now generating returns that exceeded most pure-play investment banks.

The international expansion through Columbia Threadneedle provided unexpected benefits. While U.S. wealth management drove profits, the global asset management platform provided diversification and scale. Columbia Threadneedle managed over $600 billion in assets across multiple continents, giving Ameriprise credibility with institutional investors and high-net-worth individuals globally.

Digital transformation accelerated during the COVID-19 pandemic. What might have taken five years of gradual evolution happened in five months. Virtual client meetings became the norm. Digital onboarding eliminated paperwork. Automated rebalancing and tax-loss harvesting became table stakes. Ameriprise's technology investments from the previous decade suddenly looked prescient.

The company's approach to ESG (Environmental, Social, and Governance) investing exemplified its balanced strategy. While some competitors went all-in on ESG products and others dismissed them entirely, Ameriprise took a pragmatic approach: offer ESG options for clients who want them, but don't force them on anyone. This middle path reflected the company's Midwest roots—practical, client-focused, non-ideological.

Competition intensified from unexpected quarters. Morgan Stanley's acquisition of E*Trade and Schwab's purchase of TD Ameritrade created vertically integrated giants. Meanwhile, private equity firms began rolling up independent advisory firms, creating new scaled competitors. Ameriprise's response was to double down on its unique value proposition: the combination of employee and franchise advisors, proprietary and third-party products, and technology-enabled personal service.

The succession challenge loomed large. Jim Cracchiolo, who'd led the company since before the spinoff, was approaching traditional retirement age. Yet his leadership had been so central to Ameriprise's success that finding a successor seemed almost impossible. The board's solution was elegant: extend Cracchiolo's tenure while grooming internal candidates, ensuring continuity while preparing for transition.

By 2024, the transformation was complete but the evolution continued. Client inflows into fee-based investment advisory accounts grew to an all-time high. Total client assets reached record levels. The company ranked 254th on the Fortune 500, was the 9th largest independent broker-dealer, and stood among the 25 largest asset managers in the world.

The regulatory environment remained challenging but manageable. Unlike the crisis-era settlements, recent regulatory issues were minor—routine matters for a firm of Ameriprise's size. The company had built robust compliance systems and, more importantly, a culture that prioritized client interests over short-term profits.

The demographic tailwinds were undeniable. Baby boomers controlled $75 trillion in assets and were entering their peak distribution years. The great wealth transfer to millennials was beginning. Both trends favored companies like Ameriprise that could serve multiple generations with comprehensive financial planning rather than just investment products.

Technology disruption remained a constant threat and opportunity. Robo-advisors had commoditized basic portfolio management, but Ameriprise's response—combining digital tools with human advisors—proved more resilient than pure digital or pure human models. Clients wanted technology for convenience but human advisors for complex decisions and emotional support during market volatility.

The modern Ameriprise bore little resemblance to the company that had spun off from American Express in 2005, and even less to the Investors Syndicate of 1894. Yet the core values remained: help ordinary Americans achieve financial security, maintain trust through all market conditions, and adapt to changing times while staying true to foundational principles.

As 2025 began, Ameriprise faced new challenges: potential recession, continued fee pressure, and evolving client expectations. But the company that had survived the Great Depression, navigated the American Express years, executed a complex spinoff, and thrived through the financial crisis seemed well-positioned for whatever came next. The pivot to wealth management wasn't just a strategic shift—it was a return to the company's roots, updated for the 21st century.

VIII. Financial Performance & Capital Allocation

Walter Berman, Ameriprise's CFO, pulled up a chart during the 2024 investor day that told the entire story in one image. Two lines: Ameriprise's total return since the 2005 spinoff versus the S&P 500. The Ameriprise line soared above, showing a total return over 2,000% versus the S&P 500's 600% and S&P Financials' 200%. "This isn't luck," Berman said. "This is disciplined capital allocation meeting operational excellence."

The numbers were staggering. From a market cap of $9 billion at spinoff, Ameriprise had grown to over $50 billion by 2024. But the real story wasn't just growth—it was the consistency and quality of that growth. While many financial services companies lurched between boom and bust, Ameriprise delivered steady, compounding returns.

The 2024 results exemplified this performance: Annual net income of $3.401 billion, up 33% from 2023. The adjusted operating EPS of $35.07 for the full year represented the kind of earnings growth typically associated with high-flying tech companies, not 130-year-old financial services firms. The ROE ex-AOCI of 52.7% in Q4 2024 was almost unheard of in financial services—most banks would kill for half that return.

The capital allocation strategy was deceptively simple but ruthlessly executed. Reduced share count by 22% over the past five years while steadily increasing the dividend. This wasn't financial engineering—it was returning excess capital to shareholders while simultaneously investing in organic growth. The company generated so much cash that it could do both aggressively.

The secret sauce was the business mix evolution. Wealth management, with its recurring fee-based revenue and minimal capital requirements, generated returns on equity that dwarfed traditional banking or insurance. As the mix shifted toward wealth management—reaching over 80% of revenue by 2022—the company's return metrics soared.

Consider the unit economics of the wealth management business. A typical advisor managing $150 million in client assets generated roughly $1.5 million in annual revenue (assuming a 1% fee). After paying the advisor (typically 40-50% of revenue), covering support costs, and technology expenses, the company netted 25-30% operating margins. With minimal capital requirements, these margins translated directly to extraordinary returns on equity.

The asset management division, while facing fee pressure, still contributed meaningfully. Columbia Threadneedle's $600 billion in AUM generated steady management fees, even as margins compressed. The key was scale—spreading fixed costs across a larger asset base maintained profitability despite fee pressure.

The company's approach to share buybacks was particularly shrewd. Rather than announcing massive buyback authorizations for headlines, Ameriprise bought consistently and opportunistically. During market selloffs, buybacks accelerated. During peaks, they slowed. This disciplined approach meant the company retired shares at attractive prices, enhancing per-share value for remaining shareholders.

Dividend growth told another story. From $0.19 quarterly in 2005 to $1.51 in 2024—nearly an 8x increase. But the payout ratio remained conservative at around 20-25% of earnings, leaving plenty of capital for growth investments and buybacks. This wasn't a dividend aristocrat strategy—it was balanced capital return that preserved flexibility.

The acquisition track record validated management's capital allocation skills. The crisis-era acquisitions of H&R Block Financial Advisors, J.&W. Seligman, and Columbia Management all proved accretive to earnings within the first year. More importantly, they provided strategic capabilities that would have taken decades to build organically.

Current position metrics were impressive: Fortune 500 rank #254, 9th largest independent broker-dealer, 27th in global AUM. But these rankings understated Ameriprise's true position. In the wealth management sweet spot—clients with $500,000 to $5 million—Ameriprise was arguably the market leader, with deeper penetration than firms focused on ultra-high-net-worth clients.

The efficiency metrics were equally impressive. Adjusted annual operating net revenue per advisor jumped 13% year-over-year in 2024, reflecting not just market appreciation but genuine productivity gains. Technology investments were paying off in advisor efficiency and client satisfaction.

Executive compensation had become a flashpoint. Jim Cracchiolo's pay package, exceeding $30 million in some years, drew shareholder pushback and negative say-on-pay votes. Critics argued it was excessive for a company of Ameriprise's size. Defenders pointed to the stock performance—shareholders who'd held since the spinoff had seen 20x returns. In that context, paying for performance seemed reasonable.

The balance sheet remained fortress-like. Despite aggressive capital returns, Ameriprise maintained AA- credit ratings and excess capital well above regulatory requirements. This wasn't conservatism for its own sake—it was strategic flexibility. When the next crisis hit, Ameriprise would again be shopping while competitors were selling.

The international contribution through Columbia Threadneedle added diversification without diluting returns. While U.S. wealth management drove the highest returns, having 30% of assets managed outside the U.S. provided currency diversification and access to international distribution channels.

Tax efficiency was another hidden advantage. The shift to fee-based revenue meant more predictable income that could be managed for tax efficiency. The company's effective tax rate of around 20% was several points below the statutory rate, reflecting sophisticated tax planning and the benefits of international operations.

The technology spending, while substantial at over $500 million annually, generated measurable returns. Digital client acquisition costs were 40% lower than traditional channels. Automated rebalancing reduced operational costs by 25%. These weren't venture capital-style bets on unproven technology—they were pragmatic investments in proven tools that enhanced productivity.

Looking forward, the financial model appeared sustainable. The demographic tailwinds of baby boomer retirement and millennial wealth accumulation would drive organic growth for decades. Fee pressure in asset management was offset by scale and efficiency gains. The wealth management margins, while high, reflected genuine value creation rather than regulatory arbitrage or excessive risk-taking.

The risk factors were real but manageable. Market downturns would impact AUM-based fees, but the diversified revenue streams provided cushioning. Regulatory changes could compress margins, but Ameriprise had proven its ability to adapt. Competition would intensify, but the company's scale and advisor productivity provided competitive moats.

The ultimate validation came from the market itself. At a forward P/E of around 12-14x, Ameriprise traded at a discount to pure-play wealth managers like Charles Schwab or Raymond James, despite superior returns and growth. This valuation disconnect suggested either the market didn't fully appreciate Ameriprise's transformation, or there was skepticism about sustainability.

For long-term investors, the financial performance told a compelling story: a company that had successfully transformed its business model, delivered exceptional returns through multiple cycles, and positioned itself to capitalize on secular growth trends. The capital allocation track record suggested management would continue creating value regardless of market conditions. The numbers didn't lie—this was one of the great untold success stories in financial services.

IX. Playbook: Key Business Lessons

The conference room at Harvard Business School was packed with MBA students in November 2024. Jim Cracchiolo stood at the podium, having just finished a two-hour case discussion on Ameriprise's transformation. A student raised her hand: "Mr. Cracchiolo, if you had to distill Ameriprise's success into key lessons for future leaders, what would they be?" Cracchiolo smiled. "I'd need another two hours, but let me try to give you the highlights."

The Power of Patient Capital

"First," Cracchiolo began, "understand that trust compounds slower than interest but lasts longer than any financial asset." During the Great Depression, Investors Syndicate paid every dollar on its due date to certificate owners—a total of $101 million when banks were failing left and right. That decision, made 90 years ago, still resonates today. When advisors sit with clients, they can point to that track record.

During the 2008 crisis, advancing $700 million to clients affected by the Reserve Fund collapse wasn't legally required. But it was the right thing to do. That single decision probably generated more client loyalty than $100 million in marketing could have bought. Patient capital isn't just about having money to invest during downturns—it's about building reservoirs of trust that pay dividends for generations.

Spinoff Success Factors

The Ameriprise spinoff should be taught as a masterclass in corporate separation. Three factors made it work: strong leadership, clear cultural identity, and strategic focus. Cracchiolo wasn't brought in as a turnaround CEO—he'd grown up in the business, understood its DNA, and had the credibility to lead through uncertainty.

Cultural identity mattered more than anyone expected. American Express never really understood the Minneapolis-based, Main Street-focused culture of IDS. The spinoff allowed that suppressed identity to flourish. Suddenly, decisions could be made based on what was right for the business, not what fit American Express's strategy.

Strategic focus was ruthless. Post-spinoff, every decision was filtered through one question: "Does this help us become the premier wealth management firm in America?" If the answer was no, they didn't do it. This clarity enabled rapid decision-making and resource allocation.

Counter-cyclical M&A

The best deals are made when nobody else is buying. The 2008-2010 acquisition spree—H&R Block Financial Advisors for $315 million, J.&W. Seligman for $440 million, Columbia Management for $1 billion—transformed Ameriprise's capabilities at fraction of normal valuations.

But counter-cyclical M&A requires three things: balance sheet strength to act when others can't, operational excellence to integrate during chaos, and courage to move when conventional wisdom says wait. Ameriprise had all three. While competitors were taking TARP funds, Ameriprise was writing checks.

The discipline was as important as the opportunism. Each acquisition had to be immediately accretive, strategically coherent, and culturally compatible. No empire building, no ego deals, no "strategic options" that might pay off someday. Every deal had to make sense on day one.

Business Model Evolution

The shift from insurance to wealth management wasn't a sudden pivot—it was a 15-year evolution that required cannibalizing profitable legacy businesses to build the future. Insurance and annuities were profitable, generated float, and had been the company's bread and butter for decades. Walking away from that required vision and courage.

The key insight: wealth management scales better than insurance. Insurance requires capital reserves, complex risk management, and regulatory oversight that limits returns. Wealth management is capital-light, scales elegantly, and generates recurring fees. As one senior executive put it: "Insurance is about managing risk; wealth management is about managing relationships."

The transition wasn't just strategic—it was operational. Systems built for insurance had to be rebuilt for wealth management. Advisors trained to sell products had to learn financial planning. Compliance frameworks designed for insurance regulations had to adapt to securities laws. It was like rebuilding the plane while flying it.

Geographic Arbitrage

"Focus on average citizens, not the wealthy"—this Midwest value became a competitive advantage. While New York firms fought over ultra-high-net-worth clients in Manhattan and Silicon Valley, Ameriprise built dominant positions in Minneapolis, Des Moines, and Dallas.

The mass affluent market—clients with $500,000 to $5 million—was underserved by Wall Street firms that considered them too small and robo-advisors that couldn't handle their complexity. Ameriprise found the sweet spot: clients wealthy enough to need sophisticated planning but not so wealthy they demanded white-glove service.

Geographic arbitrage extended to talent. Ameriprise could hire top talent in Minneapolis for 60% of what they'd cost in New York. Lower cost of living meant employees stayed longer, reducing turnover costs. The headquarters location, initially seen as a disadvantage, became a strategic asset.

Long-term Thinking

"Serving the client well and doing what makes sense for the next 5, 10, and 20 years" wasn't just a slogan—it was embedded in every major decision. When regulatory pressure mounted to eliminate proprietary products, many firms fought back. Ameriprise embraced open architecture, betting that giving advisors choice would drive long-term growth even if it reduced short-term margins.

Technology investments were made with 10-year horizons. The wealth management platform built in 2015 was designed for capabilities that wouldn't be needed until 2020. The cost was painful upfront, but the competitive advantage proved durable.

Executive compensation reflected long-term thinking. While Cracchiolo's pay drew criticism, the majority was tied to long-term performance metrics. Senior executives were required to hold significant equity stakes, aligning their interests with long-term shareholders rather than quarterly earnings.

The Compound Effect

Every lesson reinforced the others. Patient capital enabled counter-cyclical acquisitions. Geographic arbitrage supported business model evolution. Long-term thinking justified strategic focus. The playbook wasn't a collection of independent tactics—it was an integrated strategy where each element amplified the others.

The most powerful lesson might be the simplest: consistency compounds. Ameriprise didn't have the most innovative products, the highest-paid advisors, or the flashiest brand. But they showed up every day for 130 years, kept their promises, and adapted to changing times while staying true to core values.

As Cracchiolo concluded his Harvard talk: "We're not the smartest people in financial services. We're probably not the hardest working. But we might be the most consistent. In a business built on trust, where relationships span generations, consistency isn't just a virtue—it's the whole game."

The students scribbled notes, trying to capture strategies they could apply to their own careers. But the real lesson was simpler: build something worth trusting, and then never, ever break that trust. Everything else—the returns, the growth, the success—follows from that foundation.

X. Bear & Bull Case Analysis

The Ameriprise boardroom was tense during the annual strategy session in September 2024. On one wall, the bull case: soaring stock charts, record earnings, industry-leading margins. On the opposite wall, the bear case: fee compression graphs, regulatory heat maps, competitive threats. "We need to see both clearly," Cracchiolo said, "because our competitors certainly do."

Bull Case: The Optimist's View

The bull case for Ameriprise starts with mathematics. Baby boomers control $75 trillion in wealth and are moving into their distribution years at a rate of 10,000 per day. This isn't a trend—it's a demographic tsunami that will drive demand for wealth management services for the next two decades. Ameriprise, with its focus on the mass affluent and affluent segments, sits directly in the path of this wave.

Best-in-class wealth management margins and organic growth validate the business model. The 29% operating margins in wealth management aren't a temporary phenomenon—they reflect structural advantages. The combination of scale, technology efficiency, and advisor productivity creates a competitive moat that's widening, not narrowing.

The $1.4 trillion in assets under management and administration provides enormous operating leverage. Every 10% market increase adds roughly $140 billion to AUM, generating approximately $1.4 billion in additional annual revenue at minimal incremental cost. This is the beauty of asset-based fee models—market appreciation is pure margin expansion.

The demographic tailwind extends beyond baby boomers. The great wealth transfer—estimated at $70 trillion over the next 20 years—will move assets from elderly parents to middle-aged children, exactly Ameriprise's target demographic. Meanwhile, millennials are beginning their wealth accumulation phase, providing a pipeline of future clients.

Proven capital allocation track record suggests value creation will continue. Management has reduced share count by 22% over five years while growing the dividend and investing in the business. This isn't financial engineering—it's disciplined capital deployment that compounds shareholder value.

Strong advisor retention and productivity metrics indicate competitive strength. While competitors fight expensive recruiting wars, Ameriprise maintains 95%+ advisor retention rates and generates industry-leading revenue per advisor. The advisor value proposition—technology tools, brand support, and practice autonomy—creates switching costs that protect market share.

The business model has proven resilient through multiple cycles. Survived the Great Depression, thrived post-2008 crisis, navigated COVID-19 seamlessly. Each crisis validated the model rather than exposing weaknesses. This isn't luck—it's structural resilience built on diversified revenue streams and conservative risk management.

International expansion through Columbia Threadneedle provides untapped growth potential. While 70% of revenue comes from the U.S., global wealth creation offers decades of growth runway. The platform and capabilities exist; execution will drive the opportunity.

Technology investments are yielding measurable returns. Digital client acquisition, automated portfolio management, and AI-driven financial planning aren't just buzzwords—they're driving real efficiency gains and client satisfaction improvements. The company that started with door-to-door sales in 1894 has successfully evolved into a digital-first, advisor-enabled model.

Regulatory moats, paradoxically, protect incumbents. While compliance costs are painful, they're more painful for smaller competitors. The resources required to maintain licenses across 50 states, comply with SEC/FINRA requirements, and manage fiduciary obligations create barriers to entry that protect Ameriprise's position.

Bear Case: The Skeptic's Concerns

The bear case begins with fee compression, the industry's existential threat. Wealth management fees have fallen from 1.5% to under 1% over the past decade, and the pressure continues. Robo-advisors offer portfolio management for 0.25%. Vanguard's Personal Advisor Services charges 0.30%. How long can Ameriprise maintain premium pricing?

Rising competition from every direction threatens market share. Morgan Stanley and Bank of America are moving downmarket into Ameriprise's sweet spot. Charles Schwab and Fidelity are moving upmarket with enhanced advisor services. Private equity is rolling up independent advisors into scaled competitors. Big tech companies are eyeing financial services. The competitive moat might be narrower than it appears.

Regulatory risks in wealth management are escalating. The SEC's focus on conflicts of interest, fee disclosure, and best execution standards could compress margins and increase compliance costs. One major regulatory violation could damage the brand that took 130 years to build.

Key person risk with long-tenured CEO is real and growing. Jim Cracchiolo has led the company since before the spinoff. His vision, relationships, and credibility have been central to success. Succession planning remains opaque, and leadership transitions in financial services often disappoint.

Market dependency for earnings growth creates vulnerability. With 80% of revenue tied to AUM-based fees, a 20% market correction would directly hit revenue by similar magnitude. Unlike banks with net interest income or insurers with premiums, Ameriprise's revenue is extraordinarily market-sensitive.

Technology disruption accelerates faster than incumbents adapt. While Ameriprise has invested heavily in technology, Silicon Valley moves faster. Could a well-funded fintech startup build a better wealth management platform from scratch? Could AI make human advisors obsolete? The innovator's dilemma is real.

Generational preferences might not favor traditional models. Millennials and Gen Z grew up with smartphones, expect free services, and trust algorithms more than advisors. Will they pay 1% fees for services their parents valued? The industry assumption that younger clients will evolve into traditional wealth management clients might be wrong.

Concentration risk in U.S. wealth management is significant. Unlike globally diversified banks, Ameriprise generates 70% of profits from U.S. wealth management. A recession, bear market, or regulatory change in this single geography and business line would disproportionately impact results.

Talent acquisition challenges in a competitive market are intensifying. The best advisors have unprecedented options—independent platforms, competing firms, or starting their own RIAs. Maintaining advisor quality while growing headcount becomes harder and more expensive each year.

ESG and social pressures could impact business model. Growing scrutiny of wealth inequality, executive compensation, and financial services' societal role could lead to regulatory or social backlash. The industry that survived 2008's anger might not escape the next populist wave.

The Balanced View

Neither the bull nor bear case tells the complete story. The truth, as always, lies somewhere between. Ameriprise faces real challenges—fee compression, competition, and regulatory pressure aren't going away. But the company has structural advantages—scale, brand, advisor relationships—that provide resilience.

The key question isn't whether challenges exist, but whether management can navigate them. The track record suggests they can. Every previous challenge—the Depression, the American Express years, the spinoff, the financial crisis—has been overcome. But past performance, as every disclaimer notes, doesn't guarantee future results.

For investors, the risk-reward calculus depends on time horizon and risk tolerance. Short-term investors should worry about market volatility and quarterly earnings. Long-term investors might see a company with secular tailwinds, proven execution, and valuation support.

The bear case is real enough to keep management paranoid and focused. The bull case is compelling enough to justify investment. Perhaps that balance—between confidence and concern, between optimism and realism—is exactly where a well-managed company should be.

XI. Epilogue: What's Next?

The Minneapolis skyline gleamed in the fading winter light as Jim Cracchiolo stood in his 50th-floor office, gazing at the city that had been home to this remarkable company for 130 years. On his desk sat two items: a framed photo of John Tappan from 1894 and a holographic display showing real-time client portfolio performance across the globe. The juxtaposition captured everything—how far they'd come, how much had changed, yet how the core mission remained the same.

Succession Planning Questions Post-Cracchiolo Era

The elephant in every room at Ameriprise is succession. Cracchiolo, now in his mid-60s, has led the company through its most transformative period. But even the best leaders must eventually pass the torch. The board has been quietly evaluating internal candidates, with several executives emerging as potential successors.

The challenge isn't finding someone competent—Ameriprise has deep bench strength. It's finding someone with Cracchiolo's unique combination of strategic vision, operational excellence, and cultural authenticity. The next CEO must understand both Minneapolis Main Street and Wall Street, both 70-year-old retirees and 30-year-old tech workers, both traditional advisory and digital disruption.

The succession plan, when revealed, will likely emphasize continuity over revolution. Ameriprise doesn't need reinvention—it needs evolution. The next leader will inherit a strong hand: market-leading positions, robust financials, and clear strategic direction. Their job will be to play that hand wisely in an increasingly complex game.

Artificial Intelligence and Wealth Management Disruption

AI isn't coming to wealth management—it's already here. But not in the way techno-optimists predicted. Rather than replacing human advisors, AI is augmenting them. Ameriprise's approach—using AI for portfolio optimization, risk assessment, and operational efficiency while maintaining human relationships for complex planning and emotional support—appears prescient.

The next frontier is hyper-personalization. AI can analyze millions of data points to customize advice for each client's unique situation. Imagine an AI that knows a client's spending patterns, anticipates life changes, and proactively suggests planning adjustments. The advisor remains the trusted guide, but armed with superhuman analytical capabilities.

The risk is that a tech giant—Google, Apple, or Amazon—enters wealth management with AI capabilities that leapfrog traditional firms. But the moat might be trust, not technology. Would you rather have your wealth managed by an algorithm from a tech company or by a human advisor backed by 130 years of keeping promises? The answer might be generational.

International Expansion Opportunities

The U.S. wealth management market, while enormous, is mature. The real growth lies abroad. Asian wealth creation, European pension reform, and emerging market affluence represent trillions in potential AUM. Ameriprise, through Columbia Threadneedle, has the platform but hasn't fully exploited the opportunity.

The challenge is that wealth management is inherently local. Tax laws, regulatory requirements, and cultural attitudes toward money vary dramatically by country. The model that works in Minneapolis might fail in Mumbai. Success requires local partnerships, cultural adaptation, and patient investment—not exactly Silicon Valley's "move fast and break things" approach.

The opportunity is particularly compelling in Asia, where wealth is growing fastest but financial advice infrastructure lags. A hybrid model—combining Ameriprise's planning expertise with local partners' relationships—could unlock enormous value. But execution risk is high, and many Western firms have stumbled trying to crack Asian markets.

The Next Generation of Financial Planning

Financial planning is evolving from episodic to continuous, from reactive to proactive, from financial to holistic. The next generation won't just want investment advice—they'll want life optimization. How do I balance financial success with personal fulfillment? How do I align my money with my values? How do I navigate career changes, relationship dynamics, and existential questions about meaning and purpose?

This expanded scope represents both opportunity and challenge. Ameriprise advisors might need to become more like life coaches than stock pickers. The training, tools, and regulatory framework for this expanded role don't yet exist. But the firms that figure it out will own the next generation of wealth management.

Technology will enable this evolution. Imagine continuous financial monitoring that alerts advisors to significant changes—a spending spike that might indicate stress, a savings pattern that suggests a life change, a risk tolerance shift that reflects evolving priorities. The advisor's role evolves from periodic check-ins to continuous partnership.

Reflections on Building a Century-Spanning Financial Institution

What does it take to build a financial institution that survives 130 years and multiple existential crises? The Ameriprise story suggests several timeless principles.

First, trust is the only currency that matters in financial services. You can lose money and recover. You can lose market share and regain it. But lose trust, and you're finished. Every decision—from paying Depression-era certificates to advancing money during the Reserve Fund crisis—must be filtered through trust impact.

Second, culture eats strategy for breakfast, lunch, and dinner. The Minneapolis culture that seemed provincial to New York bankers turned out to be Ameriprise's greatest asset. Values, not valuations, drive long-term success.

Third, evolution beats revolution. Ameriprise didn't suddenly pivot from insurance to wealth management—it evolved over 15 years. Sustainable transformation requires patience, persistence, and pragmatism.

Fourth, timing matters more than most admit. The spinoff succeeded partly because of execution but also because of timing—just before the financial crisis created acquisition opportunities. The wealth management pivot worked because demographics aligned perfectly. Success requires both skill and luck.

Finally, the paradox of financial services: you must change everything while changing nothing. The technology, products, and delivery mechanisms are unrecognizable from 1894. But the core promise—help people achieve financial security—remains unchanged. Companies that honor that paradox survive. Those that don't disappear.

The View Forward

As 2025 unfolds, Ameriprise faces a future both promising and perilous. The demographic tailwinds are real and powerful. The competitive threats are serious and multiplying. The technological changes are accelerating beyond anyone's ability to fully predict.

But perhaps that's always been true. John Tappan faced the Panic of 1907 with no idea the Great Depression was coming. The company that survived the 1930s couldn't have imagined being acquired by American Express. The executives who executed the spinoff didn't foresee the 2008 crisis that would create unprecedented opportunities.

The constant through all these changes has been adaptability grounded in unchanging principles. Serve clients well. Keep promises. Evolve with the times. Don't get too fancy. Remember your roots. These aren't sophisticated strategies—they're simple truths that compound over time.

As Cracchiolo often says, "We're not trying to be the biggest or the fastest or the most innovative. We're trying to be the most trusted. In financial services, over the long term, trust wins."

The next chapter of the Ameriprise story remains unwritten. Will AI transform wealth management beyond recognition? Will new competitors disrupt the industry's economics? Will regulatory changes reshape the business model? Will the next generation embrace or reject traditional financial advice?