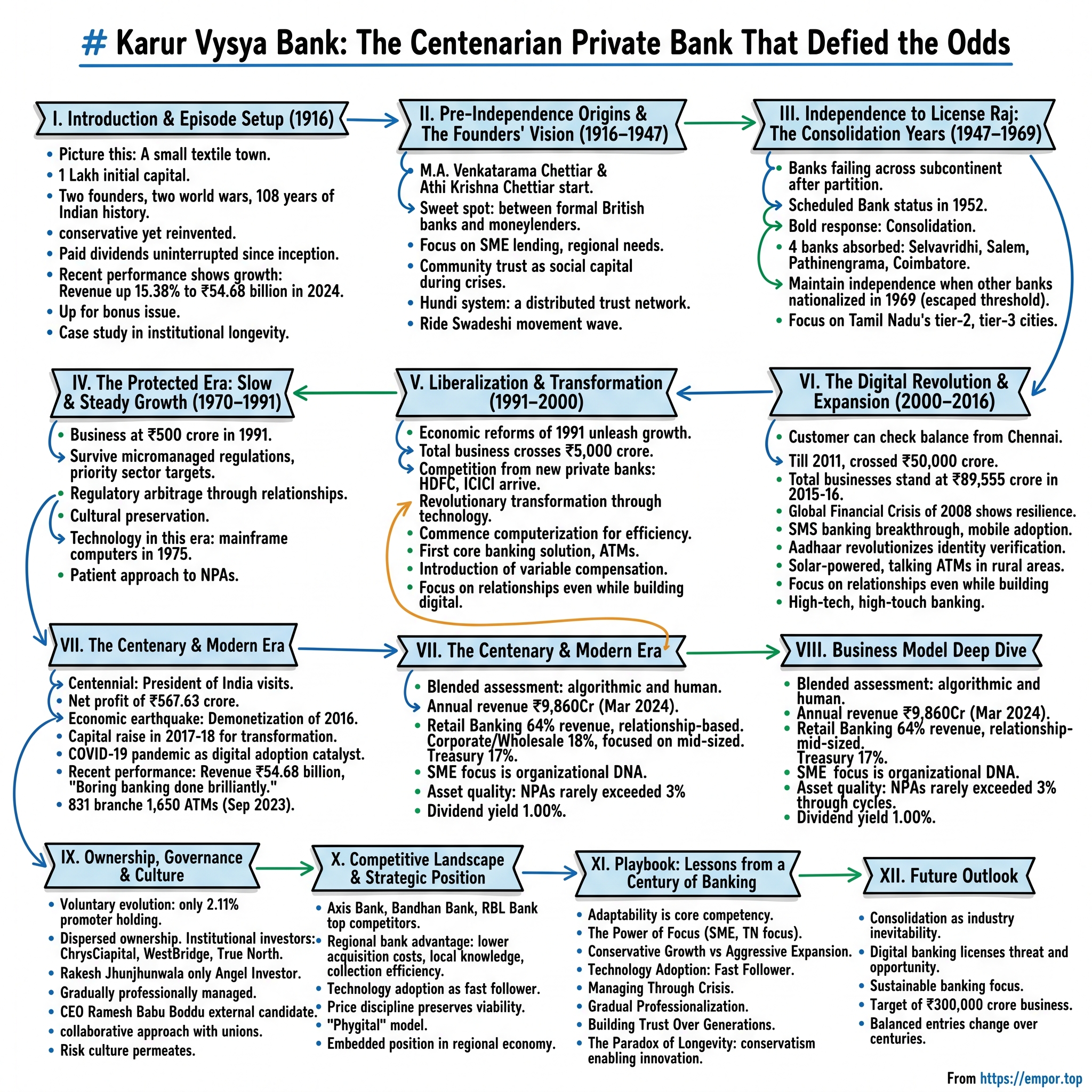

Karur Vysya Bank: The Centenarian Private Bank That Defied the Odds

I. Introduction & Episode Setup

Picture this: In the bustling textile town of Karur, Tamil Nadu, where the Amaravathi River meets ancient trade routes, a bank opened its doors on July 1, 1916, with just one lakh rupees in capital. Today, that same institution—Karur Vysya Bank—commands ₹186,564 crore in total business, operates 831 branches across India, and serves millions of customers through cutting-edge digital platforms. The journey from a community lender in a small town to a tech-forward regional powerhouse spans 108 years of Indian history, encompassing two world wars, independence, partition, the license raj, liberalization, the 2008 financial crisis, and a global pandemic.

The puzzle that fascinates us isn't just survival—plenty of Indian institutions have endured through sheer inertia. What's remarkable about KVB is how a conservative, regional bank repeatedly reinvented itself while maintaining its cultural DNA. When nationalization waves swept through Indian banking in 1969 and 1980, KVB remained private. When new-age banks like HDFC and ICICI burst onto the scene in the 1990s with aggressive growth strategies, KVB stuck to its knitting—SME lending and regional focus—yet somehow thrived. When fintech disruption threatened traditional banking, this centenarian embraced WhatsApp banking and digital transformation with surprising agility.

The numbers tell a story of consistent execution: the bank has paid dividends without interruption since inception, a feat virtually unmatched in Indian corporate history. Its recent performance—revenue up 15.38% to ₹54.68 billion in 2024, earnings up 20.99% to ₹19.42 billion—suggests the old dog has plenty of new tricks. With 86.67% of analysts recommending 'BUY' and an upcoming bonus issue scheduled for August 26, 2025, the market clearly believes there's more to come.

This episode explores how a small-town bank built by textile traders became a case study in institutional longevity, examining the strategic decisions, cultural factors, and market dynamics that enabled KVB to navigate India's tumultuous economic history. We'll dissect the business model that generates 64% of revenue from retail banking while maintaining asset quality through multiple credit cycles. We'll analyze how professional management took over from founding families without losing the institution's soul. And we'll evaluate whether this regional champion can compete in an era of digital banking, consolidation, and global capital flows.

The roadmap ahead takes us from pre-independence India, where indigenous banking meant community trust and handshake deals, through the maze of socialist-era regulations, into the crucible of liberalization, and finally to today's digital battlefield. Along the way, we'll uncover lessons about patient capital, the power of focus, and why sometimes the tortoise really does beat the hare. Because understanding KVB isn't just about one bank's history—it's about understanding how institutions adapt, endure, and occasionally, against all odds, flourish.

II. Pre-Independence Origins & The Founders' Vision (1916–1947)

The monsoon rains of June 1916 were particularly heavy in Karur that year, turning the red earth into rivers of mud, but inside the small office on Jawahar Bazaar, two men sat hunched over ledgers, their white veshtis pristine despite the chaos outside. M.A. Venkatarama Chettiar and Athi Krishna Chettiar, two illustrious sons of Karur, were putting the final touches on what would become the Karur Vysya Bank. The timing seemed almost absurd—Europe was tearing itself apart in the Great War, Indian soldiers were dying in Mesopotamian trenches, and the British Raj was squeezing every rupee from the subcontinent to fund its imperial ambitions. Yet these two visionaries saw opportunity where others saw only turbulence.

Karur was a small town with a predominantly agricultural background, nestled along ancient trade routes where bullock carts laden with textiles crossed paths with farmers bringing their harvest to market. The Amaravathi River, when not flooding, provided water for the fields and power for the handlooms that would make the region famous. But what truly distinguished Karur wasn't its geography—it was its people, particularly the merchant communities who had perfected the art of converting trust into capital over centuries.

The Chettiars weren't just any merchants. The Nattukottai Chettiar caste had organized themselves into a complex, segmentary network of interdependent family merchant-banking firms, each trading individually in commodities, money lending, and banking operations, while operating as commercial banks by taking deposits and drafting hundis for transferring capital. They had established a sophisticated banking system, introducing financial instruments like the hundi (promissory note) and developing credit networks that extended from colonial India to Burma, Malaysia, and Singapore, earning them a reputation as the "bankers of the East" during the British Raj.

The founders mopped up the initial capital of Rs. 1 Lakh to begin business on 1st July, 1916—a modest sum even by the standards of that era. To put this in perspective, the Imperial Bank of India, formed just five years earlier through amalgamation, commanded capital of Rs. 11.5 crores. Yet what KVB lacked in capital, it compensated with something far more valuable: deep roots in the community and an intimate understanding of local credit needs.

The bank was set up to provide financial support to the traders and agriculturists in and around Karur, filling a crucial gap in the colonial financial architecture. The British banking system, represented by exchange banks and presidency banks, catered primarily to European trade and large-scale commerce. Indigenous moneylenders, on the other hand, often charged usurious rates that trapped borrowers in cycles of debt. KVB positioned itself in the sweet spot between these extremes—formal enough to be trusted with deposits, local enough to understand the seasonal rhythms of agriculture and the credit needs of small traders.

The founders brought complementary strengths to the enterprise. Venkatarama Chettiar came from a family of successful traders who understood the pulse of local commerce. Athi Krishna Chettiar brought connections to the broader Chettiar network, with its sophisticated understanding of banking practices. Together, they represented a fusion of local knowledge and cosmopolitan financial acumen that would become KVB's defining characteristic. The early years weren't easy. The First World War, which initially sparked the bank's founding, also created unprecedented volatility in Indian financial markets. Cotton prices soared as Bombay merchants rushed to fill the void left by disrupted American supplies to European markets. Credit expanded recklessly. Then came the inevitable crash. Between 1913 and 1948, there was stagnation in India's banking space as growth was slow. Multiple banks encountered periodic failures. The 1920s were particularly brutal—Bank frauds and banking crises were an integral part of the financial history of India under British rule. In 1913, John Maynard Keynes, after studying the state of the banking sector characterised "(the) country as dangerous for banks".

Yet KVB not only survived but prospered. The business was robust right from the beginning, with the bank earning profits and paying dividend without interruption right from inception. This remarkable streak—maintaining profitability and dividend payments through world wars, economic depressions, and political upheavals—speaks to something deeper than mere financial prudence. It reflected a fundamental understanding of risk that came from being embedded in the community rather than imposed upon it from above.

The bank's early growth strategy was deliberately conservative yet opportunistic. While larger banks chased the glamorous business of financing international trade or courting European firms, KVB focused on the mundane but essential work of financing local commerce. They understood the credit cycles of textile merchants, the seasonal cash flows of farmers, and the working capital needs of small traders. This wasn't sophisticated banking by Lombard Street standards, but it was exactly what Karur needed.

The founders also recognized that trust in banking isn't just about capital adequacy or regulatory compliance—it's about cultural resonance. The bank conducted business in Tamil as well as English, employed locals who understood the social dynamics of credit, and structured loans around agricultural seasons rather than arbitrary calendar quarters. When a farmer needed credit for seeds, he didn't have to explain the monsoon patterns to a clerk trained in Bombay; the clerk's family probably farmed the neighboring village.

This cultural embedding gave KVB a crucial advantage during the periodic runs and panics that plagued Indian banking in this era. The lack of confidence in the country's banking system played a part in the slow mobilisation of funds and the growth of this sector. But KVB's depositors knew the founders personally, saw them in temples and markets, and understood that their money wasn't being gambled on indigo futures or remitted to London but was being lent to their neighbors and relatives. This social capital proved more durable than financial capital during crises.

The Chettiar heritage brought another crucial element: sophisticated financial technology wrapped in traditional forms. The hundi system they had perfected over centuries was essentially a distributed ledger technology avant la lettre—bills of exchange that could move money across vast distances without physical transfer, backed not by government guarantee but by community trust and reputation. KVB inherited this DNA, understanding that banking was fundamentally about information and trust networks, not just capital allocation.

By the 1930s, as India stirred with independence movements and Gandhi's call for swadeshi resonated across the subcontinent, KVB had already established itself as authentically Indian institution. The period between 1906 and 1911 saw the establishment of banks inspired by the Swadeshi movement. The Swadeshi movement inspired local businessmen and political figures to found banks of and for the Indian community. A number of banks established then have survived to the present such as Catholic Syrian Bank, The South Indian Bank, Bank of India, Corporation Bank, Indian Bank, Bank of Baroda, Canara Bank and Central Bank of India. KVB, founded in 1916, rode this wave perfectly—Indian-owned, locally focused, yet professionally managed.

The founders' vision extended beyond mere profitability. They saw the bank as an instrument of economic development for the region, a means of channeling savings into productive investment, and a bridge between traditional financial practices and modern banking. This philosophy would guide the institution through the tumultuous decades ahead, as India moved from colonial subjugation toward independence, and KVB evolved from a small-town lender into something far more ambitious. The foundation was set; now came the test of whether it could withstand the seismic shifts that independence would bring.

III. Independence to License Raj: The Consolidation Years (1947–1969)

The midnight hour of August 15, 1947, brought freedom to India, but for KVB's board of directors gathered in their Karur headquarters, it brought uncertainty. Partition had triggered the largest human migration in history, communal violence had torn the social fabric, and the integration of 562 princely states threatened economic chaos. Banks were failing across the subcontinent—of the 566 banks that existed in 1951, only 92 would survive the decade. Yet in this maelstrom, KVB's leadership saw opportunity where others saw only risk.

The transformation began with a piece of paper that arrived in 1952: Schedule Bank status from the Reserve Bank of India. KVB has consistently maintained strong fundamentals, generating profits and rewarding its stakeholders with handsome dividends since inception. This wasn't just bureaucratic recognition—it was a license to play in the big leagues. Scheduled banks could borrow from the RBI, participate in the clearing house, and most importantly, inspire confidence among depositors who had watched too many banks vanish with their savings.

The board's response was bold: consolidation through acquisition. Between 1952 and 1965, KVB absorbed four banks in rapid succession. Its finances were sound enough for it to acquire four banks by 1965 – the Selvavridhi Bank, Salem Shri Kannika Parameswari Bank, Pathinengrama Arya Vysya Bank and Coimbatore Bhagyalakshmi Bank. Each acquisition told a story of strategic expansion. The Selvavridhi Bank brought a network in Salem's textile markets. The Salem Shri Kannika Parameswari Bank added depositor trust from the merchant community. The Pathinengrama Arya Vysya Bank opened doors to the Vysya trading networks. The Coimbatore Bhagyalakshmi Bank provided entry into Tamil Nadu's Manchester—Coimbatore's booming textile industry.

These weren't distressed asset purchases or hostile takeovers. Each merger was negotiated with the delicacy of marriage alliances, preserving staff, honoring local relationships, and maintaining the acquired banks' community connections. The Pathinengrama acquisition was particularly instructive: rather than impose Karur's systems wholesale, KVB retained the acquired bank's traditional thalayadi (head office) system of maintaining customer relationships, recognizing that banking in India was as much about social capital as financial capital.

The political economy of the 1950s and 60s created a peculiar operating environment. Nehru's socialist vision manifested in the Industries Development and Regulation Act of 1951, which required licenses for everything from opening a factory to importing machinery. Banks became instruments of state policy, directed to lend to priority sectors, maintain statutory liquidity ratios, and submit to interest rate controls that often made lending unprofitable. The cash reserve ratio could be changed at the RBI's whim, freezing lending capacity overnight.

Yet KVB thrived in this controlled environment through what can only be called regulatory arbitrage through relationships. While nationalized banks struggled with bureaucratic oversight and private banks chafed at restrictions, KVB occupied a sweet spot. Small enough to avoid political attention, large enough to matter locally, and embedded enough to understand which rules could be bent without breaking. When the government mandated agricultural lending, KVB was already financing farmers. When priority sector norms came, their SME focus naturally qualified.

The 1960s brought new challenges. The Indo-China war of 1962 triggered economic controls. The Indo-Pak wars of 1965 stretched resources. Gold control orders banned private gold holdings, disrupting traditional savings patterns. Foreign exchange crises led to devaluation. Through it all, KVB maintained its unbroken record of profitability and dividends—a feat that fewer than a dozen Indian banks could claim.

Then came 1969, the year that changed Indian banking forever. On July 19, Prime Minister Indira Gandhi, in a dramatic midnight broadcast, announced the nationalization of 14 major commercial banks. The criteria was simple: any bank with deposits over Rs. 50 crores would be taken over by the state. KVB, with deposits just under the threshold, escaped by the narrowest of margins. Whether this was fortuitous or carefully managed remains a matter of speculation among banking historians.

With an aim to solve this problem, the then Government decided to nationalise the Banks. These banks were nationalised under the Banking Regulation Act, 1949. The banks that were nationalized included powerhouses like Central Bank of India, Bank of India, and Punjab National Bank. Overnight, 91% of banking business came under government control. Private banks like KVB became an endangered species, viewed with suspicion by socialist ideologues and protected only by their size—too small to threaten the commanding heights of the economy.

The post-nationalization period tested KVB's adaptability. Competition from nationalized banks, with their government backing and subsidized operations, was fierce. These banks could afford to lend at rates that would bankrupt private players. They had implicit sovereign guarantees that made depositors feel secure. They had political backing that opened doors KVB couldn't access.

KVB's response was to double down on what it did best: relationship banking in Tamil Nadu's tier-2 and tier-3 cities. While nationalized banks built grand branches in metropolises, KVB opened modest offices in towns like Namakkal, Erode, and Tirupur. While public sector banks rotated managers every three years, KVB's branch managers spent decades in the same town, becoming fixtures in local business communities.

The bank also pioneered what would later be called "financial inclusion," though they simply called it good business. They introduced pigmy deposit schemes, where agents would collect small daily savings from households—sometimes as little as one rupee. They created chit fund-like products that appealed to traditional savings groups. They offered gold loans that respected cultural preferences for the metal as security. These innovations weren't driven by regulatory mandates but by deep understanding of customer needs.

By 1969's end, KVB had grown from that single office in Karur to a network spanning Tamil Nadu. Total business crossed Rs. 100 crores—modest by national standards but remarkable for a private bank operating without government support. More importantly, they had survived the first great winnowing of Indian banking. Of the 566 banks that existed at independence, fewer than 100 remained. KVB wasn't just among the survivors; it was among the few still paying dividends, still expanding, still confident about the future.

The irony wasn't lost on observers: in an era designed to eliminate private banking, KVB had found ways to grow. While the government promoted bank nationalization as a way to democratize credit, KVB was already doing it—one small loan, one rural branch, one relationship at a time. The consolidation years had transformed KVB from a local bank into a regional presence, setting the stage for the next phase of growth in the byzantine world of the License Raj. The question now was whether they could maintain their independence and identity in an increasingly state-controlled financial system.

IV. The Protected Era: Slow & Steady Growth (1970–1991)

The 1970s opened with KVB's senior management huddled in their Karur boardroom, studying a map of Tamil Nadu marked with red pins for nationalized bank branches and blue for their own. The red pins clustered in cities; the blue ones dotted the countryside. This wasn't coincidence—it was strategy. In an India where the state controlled the commanding heights of the economy, KVB had found its niche in the valleys below.

The numbers told a story of patient accumulation. Total business, which was at Rs500 crore in 1991 represented twenty years of compound growth in an economy where GDP growth rarely exceeded 3.5%—the infamous "Hindu rate of growth." But these aggregate figures obscured the granular reality of KVB's operations: thousands of small loans to power loom operators in Erode, working capital for turmeric traders in Salem, crop loans for farmers in Thanjavur's rice bowl.

The regulatory environment of this era would make modern compliance officers weep. Interest rates weren't just regulated; they were micromanaged. The RBI dictated rates for loans below Rs. 7,500 (10%), between Rs. 7,500 and Rs. 25,000 (11%), and so on through a byzantine structure that changed frequently. Priority sector lending targets climbed from 33% to 40% of net bank credit. Sub-targets proliferated: 18% for agriculture, 10% for weaker sections, specific percentages for small-scale industries, cottage industries, tiny industries—categories that multiplied like fractals of bureaucratic imagination.

KVB's response was characteristically pragmatic. Rather than fight these constraints, they embraced them. Their SME focus naturally aligned with priority sector requirements. When the government introduced the Lead Bank Scheme in 1969, assigning districts to banks for coordinated development, KVB volunteered for rural areas others avoided. They understood something the planners in Delhi missed: these weren't just regulatory burdens but competitive moats. Every complex rule that frustrated large banks created opportunities for those who could navigate them.

Technology in this era meant something different than Silicon Valley imagined. KVB's first computer, installed in 1975, was a room-sized ICL 1901 that required its own air-conditioning plant and dedicated power supply. It could process the entire bank's daily transactions in just eight hours—revolutionary compared to the weeks of manual ledger reconciliation it replaced. But the real innovation wasn't the hardware; it was convincing traditionalist staff that machines wouldn't replace them and training rural branch managers to prepare data in formats the computer could digest.

The cultural preservation during this period deserves special attention. As nationalized banks adopted the bureaucratic culture of government departments—with their emphasis on procedure over performance, seniority over merit—KVB maintained its merchant-banking ethos. Loan decisions still involved personal assessment, not just financial ratios. Branch managers still attended customers' family functions. The chairman still knew major borrowers by name. This wasn't mere nostalgia; it was competitive advantage. When a textile mill needed emergency working capital, they came to KVB because decisions took days, not months.

The Emergency of 1975-77 tested every institution in India, and banks were no exception. When Indira Gandhi suspended civil liberties and ruled by decree, banks became instruments of political power. Loans could be directed to supporters, denied to opponents. Yet KVB navigated these treacherous waters by maintaining studied apolitical stance. They lent based on creditworthiness, not party affiliation. They avoided high-profile clients who might attract political attention. They stayed, as one director put it, "below the radar of Delhi."

The 1980s brought new challenges and opportunities. Indira Gandhi's return to power in 1980 triggered another wave of nationalization—six more banks were taken over. KVB again escaped, but the message was clear: private banks existed at political sufferance. The assassination of Indira Gandhi in 1984, the anti-Sikh riots, the Bhopal gas tragedy—each crisis tested the banking system's resilience. Through it all, KVB maintained its steady course, growing deliberately rather than dramatically.

Rajiv Gandhi's modernization drive from 1985 offered glimpses of liberalization to come. Computers were no longer licensed items. Foreign exchange regulations eased slightly. The long-distance telecom monopoly cracked. KVB responded by accelerating its own modernization. By 1990, they had computerized all major branches, introduced magnetic ink character recognition for check processing, and even experimented with early automated teller machines—though customers remained skeptical about trusting machines with their money.

The focus on SME lending during this period wasn't just business strategy; it was economic philosophy. While nationalized banks channeled credit to large public sector undertakings—often at political direction and regardless of viability—KVB funded the actual engines of employment. A typical KVB loan might finance a small rice mill employing 20 people, a transport company with 10 trucks, or a textile unit with 50 power looms. These weren't glamorous borrowers, but they repaid their loans and created jobs.

The bank's approach to non-performing assets revealed institutional character. When borrowers struggled—and in an economy growing at 3% annually, many did—KVB's first response wasn't legal action but restructuring. They understood that a functioning business, even if financially stressed, was worth more than seized collateral. This patient approach meant their gross NPAs never exceeded 3% during the entire License Raj period, while some nationalized banks saw double-digit default rates.

By 1991, as P.V. Narasimha Rao prepared to announce economic reforms that would transform India, KVB had quietly built something remarkable. From a single branch in 1916, they now operated 89 branches. From initial capital of Rs. 1 lakh, they managed Rs. 500 crores in business. From two founders, they employed over 2,000 people. Most remarkably, they had maintained their unbroken record of profitability and dividend payments through 75 years that included two world wars, independence, partition, multiple wars with neighbors, political upheavals, and economic stagnation.

The protected era was ending, but it had served its purpose for KVB. While sheltered from foreign competition and constrained by socialist controls, they had built deep roots in Tamil Nadu's economy. They had developed systems and culture that could function despite, not because of, government policy. They had accumulated capital, both financial and social, that would prove crucial in the liberal era ahead. As India prepared to open its economy to the world, KVB was ready to prove that a 75-year-old regional bank could learn new tricks. The question was whether their conservative, relationship-based model could survive in a world about to be transformed by technology, competition, and globalization.

V. Liberalization & Transformation (1991–2000)

July 24, 1991: Finance Minister Manmohan Singh stood before Parliament, his soft voice carrying words that would shatter India's economic orthodoxy: "No power on earth can stop an idea whose time has come." Within hours, industrial licensing was abolished, foreign investment welcomed, and the rupee devalued. For KVB's management watching from Karur, it felt like someone had suddenly changed the rules of a game they'd been playing for 75 years.

The numbers tell the story of explosive growth: Total business, which was at Rs500 crore in 1991, crossed Rs5,000 crore by the turn of the millennium. A ten-fold increase in nine years—after taking seven decades to reach the first Rs. 500 crores. But raw numbers don't capture the organizational transformation required to achieve this growth while the entire competitive landscape shifted beneath their feet.

The new private banks arrived like conquistadors in virgin territory. HDFC Bank, launched in 1994, brought Wall Street sophistication to Indian banking. ICICI, transforming from a development financial institution to a commercial bank, deployed technology and aggression in equal measure. These weren't banks in the traditional sense KVB understood—they were financial services companies that happened to have banking licenses. They poached talent with salaries KVB couldn't match, promised customers services KVB hadn't imagined, and deployed technology KVB was only beginning to understand.

The Karur Vysya Bank Limited, popularly known as KVB, was set up in 1916 by two great visionaries and illustrious sons of Karur—but by 1995, those visionaries' descendants faced an existential question: Could a traditional bank survive in this brave new world?

The answer came through technology, but not in the way Silicon Valley mythology suggests. In 1995 landmark: Commencing computerization for operational efficiency wasn't about installing servers or writing code—it was about convincing a 70-year-old branch manager in Gobichettipalayam that a computer wouldn't make him redundant, training a teller in Kumbakonam to trust a screen more than her handwritten ledger, and explaining to customers why their passbooks would be replaced by printed statements.

The core banking solution KVB chose—a domestically developed system rather than expensive foreign software—reflected both financial pragmatism and cultural sensitivity. The interface could switch between English and Tamil. The software understood Indian naming conventions (where father's names, caste names, and given names created endless permutations). It could handle the complexity of Indian joint families where single accounts might have multiple operators with different signing authorities. This wasn't technological leadership; it was technological appropriateness.

Competition from new private banks forced KVB to confront uncomfortable truths. Their branches looked dated—more like government offices than modern retail spaces. Their products were generic—savings accounts, fixed deposits, loans. Their processes were slow—loan approvals took weeks while HDFC promised 48 hours. Their staff was aging—the average employee age exceeded 45. Their brand was unknown outside Tamil Nadu—while new banks advertised on cricket matches watched by millions.

The response was measured revolution. Branch renovation began with customer-facing areas—air conditioning, comfortable seating, electronic displays. But the back offices remained spartan, reflecting KVB's cost consciousness. New products emerged, but built on existing strengths: gold loans leveraging Tamil Nadu's affinity for the metal, agricultural loans using their rural network, SME loans exploiting decades of relationships. The bank began recruiting MBAs, but paired them with veteran bankers for cultural transmission.

The Asian Financial Crisis of 1997 provided unexpected validation of KVB's conservative approach. While aggressive banks that had rushed into foreign exchange derivatives and international exposure faced losses, KVB's domestic focus insulated them. Their lack of sophistication, once seen as weakness, appeared prescient. The crisis reminded markets that boring banking had virtues—a lesson that would be forgotten and relearned repeatedly.

Y2K—the millennium bug that threatened to crash computer systems—became an unexpected catalyst for modernization. The fear that date-dependent software would fail when calendars rolled from 1999 to 2000 forced every bank to audit and upgrade their technology. For KVB, this external pressure provided cover for massive internal change. Legacy systems were replaced, processes documented, disaster recovery procedures established. The bank that entered 1999 running on patched-together technology emerged in 2000 with infrastructure comparable to any modern bank.

The human dimension of this transformation deserves emphasis. In 1991, KVB employees were essentially guaranteed lifetime employment—the concept of performance management was alien. By 2000, variable compensation, performance reviews, and voluntary retirement schemes had been introduced. Yet this wasn't slash-and-burn restructuring. The bank offered generous retraining programs, helping clerks become computer operators, tellers become relationship managers. The message was clear: change was mandatory, but abandonment wasn't.

Customer behavior evolved dramatically during this decade. In 1991, a typical KVB customer visited the branch weekly, maintained handwritten accounts, and viewed banking as a necessary evil. By 2000, that same customer expected ATM access, telephone banking, and quarterly statements. The introduction of debit cards was particularly revealing—initial skepticism ("Why do I need plastic when I have cash?") gave way to enthusiasm once customers discovered they could withdraw money anywhere, anytime.

The regulatory environment, while liberalized, remained complex. The RBI introduced prudential norms aligned with international standards—capital adequacy ratios, asset classification criteria, provisioning requirements. KVB's traditional conservative accounting actually helped here; they discovered their informal provisioning often exceeded new regulatory requirements. What had been seen as over-cautious now appeared as regulatory compliance.

Product innovation accelerated in the decade's final years. Housing loans, virtually unknown in 1991, became a major business line as middle-class aspirations expanded. Credit cards, initially resisted by KVB's conservative culture, were reluctantly introduced through a partnership with Visa. Internet banking launched in 1999 to exactly 47 customers—within a year, thousands had signed up, surprised by their own embrace of technology.

The decade ended with symbolic and substantive milestones. Crossing Rs. 5,000 crores in business validated the transformation strategy. Successfully managing Y2K transition demonstrated technological capability. Surviving competition from new private banks proved the viability of their model. Most importantly, maintaining the unbroken profit and dividend record through revolutionary change showed that tradition and transformation weren't mutually exclusive.

As the new millennium dawned, KVB was a different institution than the one that entered the 1990s. Still rooted in Tamil Nadu but now looking beyond, still focused on SMEs but serving diverse segments, still conservative but selectively aggressive, still traditional but increasingly digital. The liberalization decade had forced evolution at unprecedented speed. The question now was whether this momentum could be sustained as India entered the digital age and global integration accelerated. The next phase would test whether a bank born in the age of bullock carts could thrive in the age of the internet.

VI. The Digital Revolution & Expansion (2000–2016)

The millennium opened with KVB's IT head demonstrating something revolutionary to the board: a customer in Chennai could now check his account balance from a computer in California. The directors, several of whom had never used email, watched with mixture of wonder and worry as he clicked through the bank's newly launched internet banking portal. "But who will go to California to check their balance?" one director asked, missing the point entirely. Within a decade, millions would check their balances from mobile phones that didn't yet exist, through apps that hadn't been invented, using networks that hadn't been built.

The transformation numbers stagger: Within a decade, till 2011, it also crossed the Rs50,000 crore mark. Now, in 2015-16, the bank's total businesses stand at Rs89,555 crore. But these figures only hint at the fundamental reimagining of banking that occurred. With over 4.5 million debit card holders, its branch network has crossed 667, with the ATM network expanding to 1,652; cash deposit machines, to 389—infrastructure that would have seemed like science fiction to the bank's founders.

The 2008 Global Financial Crisis arrived in India like a delayed monsoon—expected but still devastating when it hit. Lehman Brothers collapsed in September; by October, Indian markets had crashed 60%. Foreign institutional investors pulled out $13 billion. Credit markets froze. Companies that had borrowed assuming eternal growth suddenly couldn't service their debts. Yet KVB not only survived but grew, their conservative lending practices and domestic focus providing insulation from global contagion.

The crisis revealed something profound about KVB's business model. While banks exposed to real estate speculation and derivative products bled, KVB's portfolio of small textile units, rice mills, and transport companies proved remarkably resilient. These businesses might not have been sexy enough for investment bankers, but they produced real goods for real customers who paid real money. When global supply chains fractured, local suppliers thrived. When export markets collapsed, domestic consumption continued. KVB's boring banking looked brilliant in hindsight.

Digital transformation accelerated post-crisis, but with distinctly Indian characteristics. The bank's mobile banking adoption tells the story: initial apps were designed for smartphones that few customers owned. The breakthrough came when they introduced SMS banking—suddenly, anyone with a basic Nokia phone could check balances and transfer funds. By 2010, more transactions happened via SMS than internet banking. Technology adoption wasn't about having the latest gadgets; it was about understanding customer reality.

The introduction of Aadhaar, India's biometric identity system, revolutionized KVB's operations in ways that weren't immediately obvious. Suddenly, verifying customer identity—previously involving multiple documents, witnesses, and weeks of processing—took seconds. A farmer from a remote village could open an account with fingerprint authentication. This wasn't just efficiency; it was inclusion. KVB could now profitably serve customers previously deemed unviable.

Branch expansion during this period followed a counterintuitive strategy. While new-age banks focused on metros and digital channels, KVB continued opening physical branches in tier-3 and tier-4 towns. The logic was simple: trust in banking remained tactile for most Indians. They wanted to see where their money was kept, shake hands with their banker, have somewhere to go if something went wrong. Each new branch was an investment in relationship infrastructure that digital channels could supplement but not replace.

The ATM network expansion revealed operational excellence hidden beneath traditional exterior. KVB pioneered the deployment of solar-powered ATMs in rural areas lacking reliable electricity. They introduced talking ATMs for illiterate customers. They placed machines in unconventional locations—textile markets, agricultural mandis, transport hubs—where their customers actually were rather than where banking convention suggested they should be.

Competition intensified from unexpected directions. Telecom companies launched mobile wallets. E-commerce giants offered credit. Payment banks promised to make traditional banking obsolete. Yet KVB's response was partnership rather than panic. They integrated with payment wallets, enabled e-commerce transactions, and viewed fintech as opportunity rather than threat. The same bank that took 75 years to embrace computers adapted to digital disruption in months.

The human story of this period centers on generational transition. The employees who joined in the 1970s were retiring, taking with them institutional memory and relationship capital. The new recruits—engineers, MBAs, data scientists—brought different skills but lacked the intuitive understanding of credit that came from decades of experience. KVB's solution was systematic knowledge transfer: retiring managers spent their final years training successors, documenting unwritten rules, explaining why certain exceptions were made and others weren't.

Risk management evolved from art to science, though both remained important. Credit scoring models supplemented but didn't replace personal assessment. Data analytics identified patterns but branch managers' local knowledge remained crucial. The bank developed what they called "high-tech, high-touch" banking—using technology to enhance rather than replace human judgment.

Product innovation accelerated dramatically. Education loans supported Tamil Nadu's engineering college boom. Microfinance products served self-help groups. Bancassurance generated fee income. Foreign exchange services capitalized on increasing overseas travel and education. Each product emerged from observed customer needs rather than copying competitors—a bottom-up innovation model that proved remarkably effective.

The period's most significant strategic decision might have been what KVB didn't do. They didn't pursue aggressive international expansion like some peers. They didn't bet heavily on investment banking or capital markets. They didn't chase size for its own sake through expensive acquisitions. Instead, they deepened existing strengths, expanded gradually into adjacent areas, and maintained focus on core constituencies.

Regulatory changes during this period—Basel II implementation, financial inclusion mandates, know-your-customer requirements—were met with characteristic pragmatism. Rather than viewing compliance as burden, KVB treated it as operational discipline. Their traditionally conservative practices often exceeded regulatory requirements, turning compliance into competitive advantage when competitors struggled with remediation.

By 2016, as the bank prepared for its centenary celebrations, the digital revolution had transformed every aspect of operations. Yet fundamental character remained unchanged: conservative in risk, progressive in technology adoption, focused on relationships even while building digital channels, regional in presence but modern in outlook. The upcoming centenary would celebrate not just survival but successful adaptation—proof that institutional DNA could evolve without mutating beyond recognition. The stage was set for the next phase: navigating India's dramatic economic experiments while positioning for a digital-first future that was arriving faster than anyone anticipated.

VII. The Centenary & Modern Era (2016–Present)

The President of India's helicopter descended onto the makeshift helipad in Karur on July 1, 2016, kicking up dust that had settled on this ancient trading town for centuries. Pranab Mukherjee had come to mark something remarkable: a private sector bank reaching its hundredth birthday in a country where most businesses didn't survive their founders. As he walked through the exhibition showcasing KVB's journey from ledger books to artificial intelligence, from one branch to hundreds, from Rs. 1 lakh to approaching Rs. 1 lakh crore, he remarked, "This is not just a bank's history; this is India's economic biography."

The centenary celebrations, however, were overshadowed by an economic earthquake. On November 8, 2016, Prime Minister Modi announced demonetization—86% of India's currency would cease to be legal tender overnight. For a bank with deep rural presence where cash was king, this was potential catastrophe. Yet KVB's response revealed institutional resilience built over a century. Branches stayed open late, staff was mobilized from headquarters, temporary cash deposit points were established at agricultural mandis. While customers queued at other banks faced harassment and delays, KVB's relationship-based approach meant they knew their customers, could quickly verify deposits, and maintained trust during chaos.

Now, in 2015-16, the bank's total businesses stand at Rs89,555 crore, with a net profit of Rs567.63 crore. But the modern era would demand more than incremental growth. Digital disruption was accelerating, demographic shifts were creating new customer segments, and regulatory expectations were evolving rapidly.

The capital raise of 2017-18 marked a pivotal moment. Successfully raising capital through a Rights Issue demonstrated market confidence, but more importantly, it showed that a century-old institution could still attract growth capital. The funds weren't just for regulatory compliance—they were for transformation. The Bank has spread its wings across the country with 782 branches in 20 States and 3 Union Territories. Opening 79 new branches in a single year might seem anachronistic in the digital age, but KVB understood something that Silicon Valley often missed: India's digital divide meant physical presence remained crucial for financial inclusion.

The DLite app launch represented more than technological advancement—it was cultural revolution. For an institution where decisions traditionally required multiple approvals and physical documentation, offering instant digital loans required reimagining risk management. The app used artificial intelligence to assess creditworthiness, but incorporated KVB's century of lending experience into its algorithms. A small business owner in Tirupur could now get working capital approved in minutes, not weeks.

WhatsApp banking introduction in 2019 showed KVB's ability to leapfrog technological generations. Rather than forcing customers through multiple digital transitions, they went straight to where customers already were. With over 400 million Indians using WhatsApp daily, it became the most democratic banking channel—accessible to anyone with a basic smartphone and data connection. Customers could check balances, request statements, and even block cards through simple messages.

The COVID-19 pandemic of 2020 tested every assumption about banking. Branches shut during lockdowns. Staff worked from home—itself a revolutionary concept for traditional banking. Customer behavior changed overnight—digital adoption that might have taken years happened in weeks. KVB's response combined high-tech solutions with high-touch sensitivity. Video KYC enabled account opening without branch visits. Loan moratoriums helped struggling borrowers. Emergency credit lines supported SMEs facing existential threats.

Recent performance validates the transformation strategy. Revenue grew from ₹54.68 billion in 2024, marking 15.38% growth, while earnings jumped 20.99% to ₹19.42 billion. These aren't just numbers—they represent thousands of small businesses funded, millions of transactions processed, and continued relevance in a rapidly evolving financial landscape. The upcoming bonus issue in ratio 1:5 with ex-date August 26, 2025, signals confidence in continued growth.

Ramesh Babu Boddu is the CEO of Karur Vysya Bank. Under his leadership, the bank has navigated the paradox of being simultaneously conservative and innovative. The strategy focuses on "boring banking done brilliantly"—no cryptocurrency speculation or complex derivatives, just consistent execution of core banking with modern tools.

The current scale—831 branches and 1,650 ATMs as of September 2023—might seem modest compared to banking giants. Yet this footprint generates remarkable efficiency. Revenue per employee exceeds many larger banks. Cost-to-income ratios remain competitive. Asset quality metrics consistently outperform peers. This isn't about being biggest; it's about being best at chosen segments.

Digital transformation continues accelerating. Artificial intelligence now screens loan applications, identifying patterns human underwriters might miss. Blockchain experiments promise to revolutionize trade finance. Cloud computing enables scalability without proportional infrastructure investment. Yet each innovation is filtered through KVB's conservative lens—proven technology over bleeding edge, practical application over technological showcasing.

The management transition from family leadership to professional management, completed over recent decades, proved crucial for modern era success. While founding families remain shareholders, operational control rests with professional managers selected for competence rather than connections. This meritocracy enables rapid decision-making and strategic flexibility impossible in family-dominated institutions.

Recent strategic initiatives reveal forward-thinking approach. Partnership with fintech companies provides technological capabilities without massive investment. Focus on supply chain financing capitalizes on GST-driven formalization of Indian economy. Emphasis on sustainable finance aligns with global ESG trends while supporting traditional customer base's evolution toward environmental consciousness.

The modern era also brought unprecedented scrutiny. Regulatory requirements—from Basel III implementation to data protection regulations—demand sophisticated compliance infrastructure. Cyber security threats require constant vigilance. Customer expectations, shaped by global technology giants, demand seamless service. Competition comes not just from banks but from every company with digital payments capability.

Yet KVB's response isn't defensive but adaptive. They've embraced open banking, sharing data through APIs to enable customer choice. They've invested in cybersecurity not as compliance burden but as trust infrastructure. They've reimagined customer service, with AI chatbots handling routine queries while human bankers focus on complex relationship management.

As KVB moves beyond its centenary toward an uncertain but exciting future, the modern era has proven that age need not mean obsolescence. The same institution that once recorded transactions in handwritten ledgers now processes millions digitally. The same culture that valued relationships over transactions now uses technology to deepen those relationships at scale. The upcoming bonus issue and analyst optimism suggest markets believe this 108-year-old bank has plenty of growth ahead. The question isn't whether KVB can survive another century—it's what banking itself will look like when they celebrate their bicentennial.

VIII. Business Model Deep Dive

Step inside KVB's credit committee meeting on any Tuesday morning, and you'll witness a fascinating collision of old and new. A loan officer presents a textile manufacturer's application on a digital dashboard showing real-time GST filings, bank statement analytics, and bureau scores. But the discussion that follows sounds like it could have happened in 1950: "What's his father's reputation?" "How did he handle the 2018 cotton price spike?" "Is his daughter's wedding this year?" This blend of algorithmic assessment and anthropological understanding defines KVB's business model—modern tools applied to timeless banking principles.

The numbers reveal a carefully orchestrated portfolio: Annual revenue of Karur Vysya Bank is ₹9,860Cr as on Mar 31, 2024. Retail Banking dominates at 64% of revenue, but this isn't mass-market consumer lending. It's granular, relationship-based banking to individuals whose needs span from education loans for engineering aspirants to gold loans for wedding expenses. Corporate/Wholesale Banking contributes 18%, focused on mid-sized companies too small for large banks' attention but too sophisticated for microfinance. Treasury operations at 17% provide stability through government securities and inter-bank markets. The remaining 1% from other operations might seem negligible but includes fee income from distribution and advisory services that require no capital deployment.

The SME focus isn't just marketing rhetoric—it's organizational DNA. Consider a typical KVB corporate client: a spinning mill in Coimbatore with Rs. 50 crore turnover, employing 200 workers, owned by second-generation entrepreneurs who inherited the business from their fathers. Large banks consider them too small; microfinance institutions can't handle their complexity. KVB understands their seasonal working capital needs, their investment cycles tied to textile demand, their family dynamics affecting business decisions. This isn't relationship banking as buzzword—it's deep, multi-generational understanding that algorithms can't replicate.

Asset quality management reveals institutional discipline. Through multiple credit cycles—the 2008 global crisis, 2016 demonetization, COVID-19 pandemic—gross NPAs rarely exceeded 3%. This isn't luck; it's systematic risk management. Every loan officer maintains a "watch list" of accounts showing stress signals: delayed interest payments, inventory buildup, family disputes, health issues. Early intervention—restructuring before default, additional collateral when needed, partial payments when cash flow is stressed—prevents problems from festering.

Recent metrics paint a picture of profitable growth. Revenue reached ₹55.97 billion with earnings of ₹20.04 billion, generating EPS of ₹24.89. The efficiency is remarkable: ₹78.07 billion in cash provides liquidity buffer while ₹12.17 billion in debt remains manageable. The dividend policy—annual dividend of ₹2.60 yielding 1.00%—balances growth retention with shareholder returns. These aren't aggressive metrics designed to impress quarterly earnings calls; they're sustainable returns from boring banking done well.

The retail banking strategy deserves deeper examination. Unlike new-age banks chasing urban millennials with lifestyle products, KVB's retail focus remains utilitarian. The average savings account holder maintains Rs. 50,000 balance—not high-net-worth by metropolitan standards but substantial for a small-town teacher or shopkeeper. Fixed deposits dominate liabilities, providing stable, low-cost funding. The depositor profile—risk-averse, relationship-oriented, geographically stable—perfectly matches KVB's conservative lending approach.

Corporate banking operates through specialized verticals. The textile vertical understands ginning, spinning, weaving, and garmenting cycles. The agriculture vertical knows monsoon patterns, minimum support prices, and mandi dynamics. The transport vertical grasps fleet utilization, route economics, and regulatory changes. This specialization enables quick decision-making—a transport company needing to buy trucks before the festive season can get approval in days, not weeks.

Treasury operations, often seen as casino capitalism in banking, remain boringly conservative at KVB. The portfolio heavily weights government securities and highly-rated corporate bonds. Derivative exposure is minimal, mostly plain-vanilla hedging for customer needs. Trading profits are steady but unspectacular. This isn't where KVB makes its money—it's where they park surplus funds safely while maintaining regulatory ratios.

Fee income streams have evolved significantly. Bancassurance generates steady commissions without balance sheet risk. Cash management services for SMEs provide transaction fees. Government business—pension distribution, subsidy disbursement—brings float income. Trade finance—letters of credit, guarantees—leverages corporate relationships. These aren't headline-grabbing businesses but provide stable, capital-light revenue.

The cost structure reflects operational efficiency born from necessity. With net interest margins compressed by competition, cost control becomes survival skill. Branch designs are functional, not luxurious. Technology spending focuses on automation rather than innovation theater. Marketing emphasizes word-of-mouth over mass media. The cost-to-income ratio consistently below 50% isn't achieved through dramatic restructuring but through thousands of small economies.

Risk management philosophy permeates the organization. Credit risk is managed through diversification—no single borrower exceeds regulatory limits, no sector dominates the portfolio. Operational risk is minimized through standardized processes and regular audits. Market risk is limited by conservative treasury policies. Reputation risk—perhaps most important for a relationship-based bank—is guarded zealously through transparent communication and fair dealing.

The capital allocation strategy balances growth with stability. Tier-1 capital ratios exceed regulatory requirements, providing buffer for expansion. But growth isn't pursued at any cost—return on equity targets are realistic, not aspirational. Branch expansion follows customer migration, not empire-building ambition. Technology investment focuses on capability building rather than headline-grabbing announcements.

Digital integration enhances rather than replaces traditional banking. The loan origination system speeds processing but doesn't eliminate human judgment. Customer relationship management software systematizes what branch managers always did—remembering birthdays, tracking life events, understanding family dynamics. Data analytics identifies cross-selling opportunities, but relationship managers still make the pitch. Technology is tool, not master.

The sustainable banking initiatives reflect pragmatic environmentalism. Financing solar pumps for farmers makes business sense—reduced power costs improve repayment capacity. Funding electric three-wheelers serves urban transport needs while meeting emission norms. Supporting organic farming responds to market demand rather than ideological commitment. ESG isn't separate from business strategy; it's integrated into credit assessment and product development.

Looking ahead, the business model faces challenges and opportunities. The formalization of India's economy through GST creates new SME lending opportunities. Digital public infrastructure like UPI and ONDC enables cost-effective service delivery. Demographic shifts—urbanization, rising incomes, financial inclusion—expand addressable markets. Yet competition intensifies from both traditional banks and new-age financial services providers. Regulatory requirements grow more complex. Customer expectations, shaped by global technology companies, demand continuous innovation.

The response isn't transformation but evolution. KVB won't become a fintech company or universal bank. They'll remain focused on chosen segments, leveraging deep understanding and relationships while adopting technology that enhances these strengths. The business model that survived a century of disruption—from independence to liberalization, from ledger books to artificial intelligence—continues adapting while maintaining its essential character: conservative in risk, progressive in service, profitable in execution. This isn't just business model resilience; it's institutional wisdom accumulated over 108 years and still generating returns.

IX. Ownership, Governance & Culture

The most striking number in KVB's shareholding pattern isn't what you'd expect—it's 2.11%. That's the promoter holding in a bank founded 108 years ago by two families who could have maintained control through pyramidal structures, cross-holdings, or differential voting rights. Instead, Karur Vysya Bank has 6 institutional investors including ChrysCapital, WestBridge Capital and True North. Rakesh Jhunjhunwala is only Angel Investor in Karur Vysya Bank. This ownership structure—widely dispersed, professionally managed, institutionally monitored—tells a story of voluntary evolution from family enterprise to public institution.

The current ownership breakdown reads like a democracy: FII at 15.41%, Mutual Funds at 31.46%, Retail at 43%. No single entity controls the bank. No family patriarch makes decisions at dinner tables. No political power broker pulls strings from behind. This isn't ownership by accident but by design—a conscious choice made over decades to prioritize institutional strength over family control.

The journey from family to professional management wasn't sudden rupture but gradual transition. Through the 1970s and 80s, founding family members gradually ceded operational control while remaining board members. Professional managers were recruited from nationalized banks and given real authority. The message was clear: competence over kinship, merit over birthright. By the time fourth-generation family members reached working age, joining KVB meant competing with MBAs from IIMs, not inheriting corner offices.

The institutional investors who emerged as significant shareholders brought more than capital—they brought governance expectations. ChrysCapital, one of India's oldest private equity firms, doesn't just seek returns; they demand transparency, professional management, and strategic clarity. WestBridge Capital, with its track record of backing mid-sized companies, provides patient capital and strategic guidance. True North (formerly India Value Fund) brings operational expertise from transforming dozens of Indian companies.

The Rakesh Jhunjhunwala investment deserves special mention. India's most celebrated investor, often called the "Warren Buffett of India," rarely invested in old private sector banks. His KVB stake signaled confidence in the transformation story—a bet that traditional banking done well could compete with flashy new-age banks. Though Jhunjhunwala passed away in 2022, his investment philosophy lives on in KVB's approach: focus on fundamentals, ignore short-term noise, and compound returns over time.

Mutual fund ownership at 31.46% represents thousands of systematic investment plan investors, retirement funds, and institutional allocations. These aren't hot money flows chasing quarterly earnings but patient capital from funds like HDFC Mutual Fund, ICICI Prudential, and SBI Mutual Fund. Their presence provides daily liquidity, market discipline, and constant scrutiny—every quarter's results are dissected, every strategic decision evaluated, every management change analyzed.

The retail shareholding at 43% might be the most interesting component. These aren't day traders flipping stocks but longtime shareholders, many from Tamil Nadu, who inherited shares from parents or bought them decades ago. Walk into any KVB branch in Karur, and you'll meet shareholders—retired teachers holding 100 shares bought in the 1980s, small businessmen who received shares as loan collateral never reclaimed, employees who participated in stock option plans. This distributed ownership creates natural brand ambassadors—every shareholder is potential customer and vice versa.

Board composition reflects governance evolution. Independent directors dominate, bringing expertise from banking, technology, law, and accounting. The Chairman role separated from CEO position ensures oversight without interference. Board committees—audit, risk, nomination, remuneration—function with real authority rather than rubber-stamp compliance. Meeting minutes reveal substantive discussions, dissenting opinions, and decisions reversed after debate—signs of genuine governance rather than theatrical compliance.

Ramesh Babu Boddu is the CEO of Karur Vysya Bank. His appointment itself tells the governance story—an external candidate selected through professional search process, not internal promotion or family connection. His background—extensive experience in retail banking, technology transformation, and risk management—matched strategic needs rather than cultural comfort. The board's willingness to look outside for leadership demonstrated maturity rare in traditional Indian businesses.

The professional management culture extends beyond the corner office. Department heads are domain experts recruited from competitors or cultivated internally through decades of training. The credit chief understands risk modeling and regulatory requirements but also knows textile industry cycles and agricultural patterns. The technology head speaks both COBOL and Python, bridging legacy systems with modern architecture. The human resources leader balances union relations with talent management, maintaining harmony while driving performance.

Cultural DNA remains distinctly KVB despite professional management. The emphasis on relationships over transactions, long-term thinking over quarterly targets, and conservative growth over aggressive expansion reflects foundational values. New employees undergo cultural orientation that includes bank history, founder philosophy, and customer service principles. The message is clear: you're joining an institution, not just a company.

The decision-making process balances empowerment with control. Branch managers have lending authority within limits, but unusual requests escalate quickly. Credit decisions involve multiple stakeholders—relationship manager who knows the customer, credit analyst who evaluates numbers, risk officer who stress-tests assumptions, and senior management who provides oversight. This multi-layered approach slows decision-making but prevents concentration risk and ensures institutional memory influences individual judgment.

Performance management evolved from seniority-based promotion to merit-based advancement, though transition wasn't without friction. Variable compensation now forms significant portion of total remuneration, aligned with individual, departmental, and bank-wide metrics. Stock options for senior management align long-term interests. Yet the culture resists Wall Street-style bonus culture—compensation differentials remain modest, team performance matters alongside individual achievement, and loyalty is still valued even if not determinative.

The union dynamics deserve attention. Unlike public sector banks where unions often resist change, KVB's employee unions maintain collaborative approach. This isn't because workers lack bargaining power but because management maintains open communication, shares financial performance transparently, and involves unions in strategic discussions. When technology threatens jobs, retraining is offered. When branches close, redeployment is arranged. The social contract—job security in exchange for flexibility—remains intact even as terms evolve.

Risk culture permeates the organization from board to branch. Every employee understands that one bad loan can erase profits from hundred good ones. Credit officers who prevent losses receive recognition alongside those who generate income. Whistleblower policies protect employees reporting malfeasance. Regular training reinforces that reputation accumulated over century can be destroyed in moments. This isn't fear-based culture but responsibility-based consciousness.

The governance framework extends to stakeholder management. Annual general meetings aren't perfunctory affairs but genuine forums for shareholder queries. Analyst calls provide detailed operational metrics beyond regulatory requirements. Customer grievance systems function effectively—complaints reaching senior management trigger investigations, not cover-ups. Regulatory relationships remain professional—neither adversarial nor obsequious, but collaborative within boundaries.

Looking forward, governance challenges include maintaining independence as ownership consolidates in Indian banking, preserving culture while professionalizing further, and balancing stakeholder interests as expectations diverge. The response requires continuous evolution—strengthening independent oversight, investing in leadership development, and maintaining transparency even when it reveals problems. The ownership structure that emerged from historical accident—family dilution, institutional investment, retail participation—created governance advantage that conscious design might not have achieved. KVB's story suggests that sometimes the best governance comes not from controlling ownership but from its absence, forcing institutions to earn trust rather than inherit it.

X. Competitive Landscape & Strategic Position

Stand at the intersection of Cathedral Road and Dr. Radhakrishnan Salai in Chennai, and within 500 meters you'll find branches of HDFC Bank, ICICI Bank, Axis Bank, Kotak Mahindra Bank, and yes, Karur Vysya Bank. This single street corner embodies Indian banking's competitive intensity—global giants, new-age tigers, and century-old warriors competing for the same customers, same deposits, same loans. KVB's ability to maintain relevance at this intersection, replicated across hundreds of Indian cities, reveals strategic positioning that transcends simple David versus Goliath narratives.

Its top competitors include companies like Axis Bank, Bandhan Bank and RBL Bank. But this list obscures competitive reality. Axis Bank, with assets exceeding ₹11 lakh crore, operates at different scale—their treasury operations alone exceed KVB's total balance sheet. Bandhan Bank, born from microfinance roots, serves different segments with different economics. RBL Bank, aggressive in retail and credit cards, pursues growth at costs KVB wouldn't accept. The real competition comes from dozens of banks, hundreds of NBFCs, and increasingly, thousands of fintech companies nibbling at traditional banking's edges.

Market capitalization tells part of the story: ₹21,168 crore positions KVB as mid-sized player in Indian banking universe. HDFC Bank's market cap exceeds ₹12 lakh crore—nearly 60 times larger. Yet market cap per branch reveals different picture: KVB generates roughly ₹25 crore market value per branch, comparable to many larger banks. This isn't about absolute size but efficiency of capital deployment, depth of relationships, and quality of earnings.

The regional bank advantage manifests in multiple ways. Customer acquisition costs remain fraction of national banks—word-of-mouth in close-knit communities beats expensive marketing campaigns. Credit assessment benefits from local knowledge—knowing which businesses struggle during local festivals, which families have marriage expenses coming, which areas face water scarcity. Collection efficiency improves when borrowers know their banker attends same temples, shops at same markets, children study in same schools. This social capital can't be replicated by banks parachuting into markets with standardized products.

Yet regional concentration creates vulnerabilities. Tamil Nadu's economic cycles directly impact KVB's performance—textile industry downturns, agricultural distress from failed monsoons, political instability affecting business sentiment. Larger banks diversify across geographies, industries, and customer segments. When Tirupur's textile exports slump, HDFC Bank barely notices; KVB feels immediate impact. This concentration risk explains why rating agencies assign lower ratings despite strong operational metrics.

Technology disruption presents existential questions. Fintech companies unbundle banking—payments companies like PhonePe and Google Pay intermediate transactions, lending platforms like Lendingkart serve SMEs, wealth-tech apps manage investments. Each nibble seems small, but collectively they threaten traditional banking's integrated model. KVB's response—partnering rather than competing—shows pragmatic adaptation. They white-label products through fintech platforms, use their balance sheet while fintechs provide customer interface, sharing economics rather than fighting over them.

The competitive moat analysis reveals surprising strengths. Regulatory licenses, while not exclusive, create barriers—new banks need RBI approval, demonstrated capital, proven management. The branch network, expensive to maintain, provides physical presence that digital-only players lack. The deposit franchise, built over decades, provides low-cost funding that fintech lenders accessing capital markets can't match. SME relationships, cultivated across generations, resist poaching because switching costs include losing institutional memory of business cycles, family dynamics, and informal credit arrangements.

Cost structures reveal competitive dynamics. Large private banks spend heavily on technology and marketing but achieve scale economies. Small finance banks operate with lower costs but accept higher risks. Public sector banks enjoy government support but carry legacy burdens. KVB occupies middle ground—higher costs than small finance banks, lower than large private banks, but with risk profile and operational efficiency that generates sustainable returns. The key isn't lowest cost but appropriate cost for value delivered.

Pricing power remains limited in commoditized products. Savings account rates are regulated. Loan rates face competition from banks willing to accept lower margins for growth. Fee income faces pressure from digital players offering free services. Yet KVB maintains pricing discipline—they'd rather lose customer than accept uneconomical terms. This discipline frustrates growth-oriented analysts but preserves long-term viability.

The talent war intensifies annually. Large private banks poach KVB's trained staff with 50% salary increases. Fintech companies lure technology talent with stock options. Public sector banks, despite perceptions, attract candidates seeking stability. KVB's retention strategy combines cultural appeal (work-life balance, familiar environment), career development (faster progression in smaller organization), and selective matching of critical talent compensation. They can't win every battle but focus on keeping core team intact.

Strategic partnerships reveal competitive pragmatism. Rather than building everything internally, KVB partners selectively—technology with established vendors, bancassurance with insurance companies, wealth management with mutual funds. These partnerships provide capabilities without capital investment, speed without development time, and risk sharing without full exposure. Critics call this dependence; KVB calls it capital efficiency.

Customer segment focus sharpens competitive edge. While universal banks chase every customer from daily wage earners to billionaires, KVB maintains focus on core segments—SMEs, professionals, and affluent rural/semi-urban households. This focus enables specialized products, dedicated service, and deep understanding that generalists can't match. A Tirupur textile exporter values KVB's understanding of letter of credit nuances more than HDFC Bank's global presence.

The competitive response to market changes shows institutional agility. When JAM trinity (Jan Dhan-Aadhaar-Mobile) revolutionized financial inclusion, KVB quickly adapted systems for direct benefit transfers. When GST formalized economy, they modified credit assessment to incorporate GST returns. When COVID accelerated digital adoption, they fast-tracked digital initiatives planned for years. This isn't industry leadership but fast followership—letting others prove concepts then executing better.

Competitive advantages compound over time. Reputation builds slowly but pays dividends forever—customers choose KVB because their grandfathers banked there. Relationships deepen with each interaction—solving problems creates loyalty that rate differences can't break. Local knowledge accumulates—understanding which industries thrive, which struggle, which transform. These advantages can't be bought, only earned through patient presence.

Looking ahead, competitive dynamics will intensify. Digital public infrastructure like Account Aggregator framework levels playing fields. Open banking enables customers to access services from multiple providers seamlessly. Embedded finance puts banking inside non-banking apps. Yet KVB's strategic position—trusted regional player with national capabilities, traditional values with modern delivery, conservative risk with selective innovation—remains defensible. The question isn't whether they can compete with everyone but whether they can serve chosen segments better than anyone. Evidence suggests they can, though success requires continuous evolution without abandoning core strengths that enabled century-long survival.

XI. Playbook: Lessons from a Century of Banking

Inside KVB's headquarters, there's a conference room where management training sessions begin with a simple question: "How do you survive 108 years in a business where most fail within 10?" The answers that emerge—documented in training manuals, embedded in credit policies, encoded in cultural DNA—constitute a playbook for institutional longevity that transcends banking. These aren't abstract principles but battle-tested practices refined through world wars, economic crises, technological revolutions, and political upheavals.

Lesson 1: Adaptability as Core Competency

KVB survived three different Indias—colonial, socialist, and liberalized—by treating adaptability not as reactive scrambling but as proactive capability. When independence brought upheaval, they consolidated through acquisitions. When nationalization threatened existence, they stayed small enough to avoid attention. When liberalization introduced competition, they embraced technology. When digitalization disrupted banking, they partnered with disruptors. This isn't pivoting—the core business remained unchanged—but evolutionary adaptation, like a tree growing around obstacles while roots remain planted.

The adaptability mechanism operates through systematic environmental scanning. Every quarter, senior management reviews not just financial metrics but contextual changes—regulatory shifts, technological emergence, competitive moves, customer behavior evolution. These reviews generate strategic initiatives, pilot programs, and policy adjustments. More importantly, they create organizational comfort with change. Employees expect evolution, prepare for transformation, and view stability as stagnation rather than security.

Lesson 2: The Power of Focus

While competitors pursued universal banking—everything for everyone everywhere—KVB maintained laser focus on SME lending in Tamil Nadu and adjacent states. This wasn't limitation but liberation. Deep focus enabled expertise competitors couldn't match. A textile mill owner in Coimbatore gets better service from KVB than from banks hundred times larger because KVB understands his business, knows his industry, speaks his language—literally and figuratively.

Focus compounds advantages over time. Each SME loan teaches something about sector dynamics. Each cycle reveals patterns. Each relationship deepens understanding. After decades, this accumulated knowledge becomes unmarketable competitive advantage. New entrants can copy products, match rates, and replicate technology, but they can't compress decades of learning into quarters. Focus isn't about doing less—it's about doing specific things so well that competition becomes irrelevant.

Lesson 3: Conservative Growth vs Aggressive Expansion

KVB's growth trajectory—steady, sustainable, unspectacular—contrasts sharply with boom-bust cycles plaguing aggressive expanders. They never had hockey-stick growth that impresses stock markets, but they also never had near-death experiences that destroy shareholder value. This conservatism isn't timidity but prudence born from witnessing dozens of aggressive banks fail.

The conservative growth philosophy manifests in multiple practices. Credit growth targets are based on deposit growth, not ambitious projections. Geographic expansion follows existing customer migration, not map-coloring exercises. Product launches emerge from observed needs, not competitor copying. Technology investments prioritize reliability over innovation. This measured approach frustrates growth-hungry investors but delights risk-conscious depositors—and in banking, depositors matter more than investors because without deposits, there's nothing to invest.

Lesson 4: Technology Adoption—Fast Follower Strategy

KVB was never first to adopt new technology but rarely last. They let pioneers debug systems, prove concepts, and educate markets, then implemented proven solutions better than pioneers. This fast-follower strategy avoided bleeding-edge risks while capturing technology benefits. When core banking emerged, they watched early adopters struggle with implementation, learned from mistakes, then chose systems that worked. When mobile banking arrived, they studied user behavior on competitors' apps before launching their own.