MPLX: The Pipeline Empire Marathon Built

I. Introduction & Episode Setup

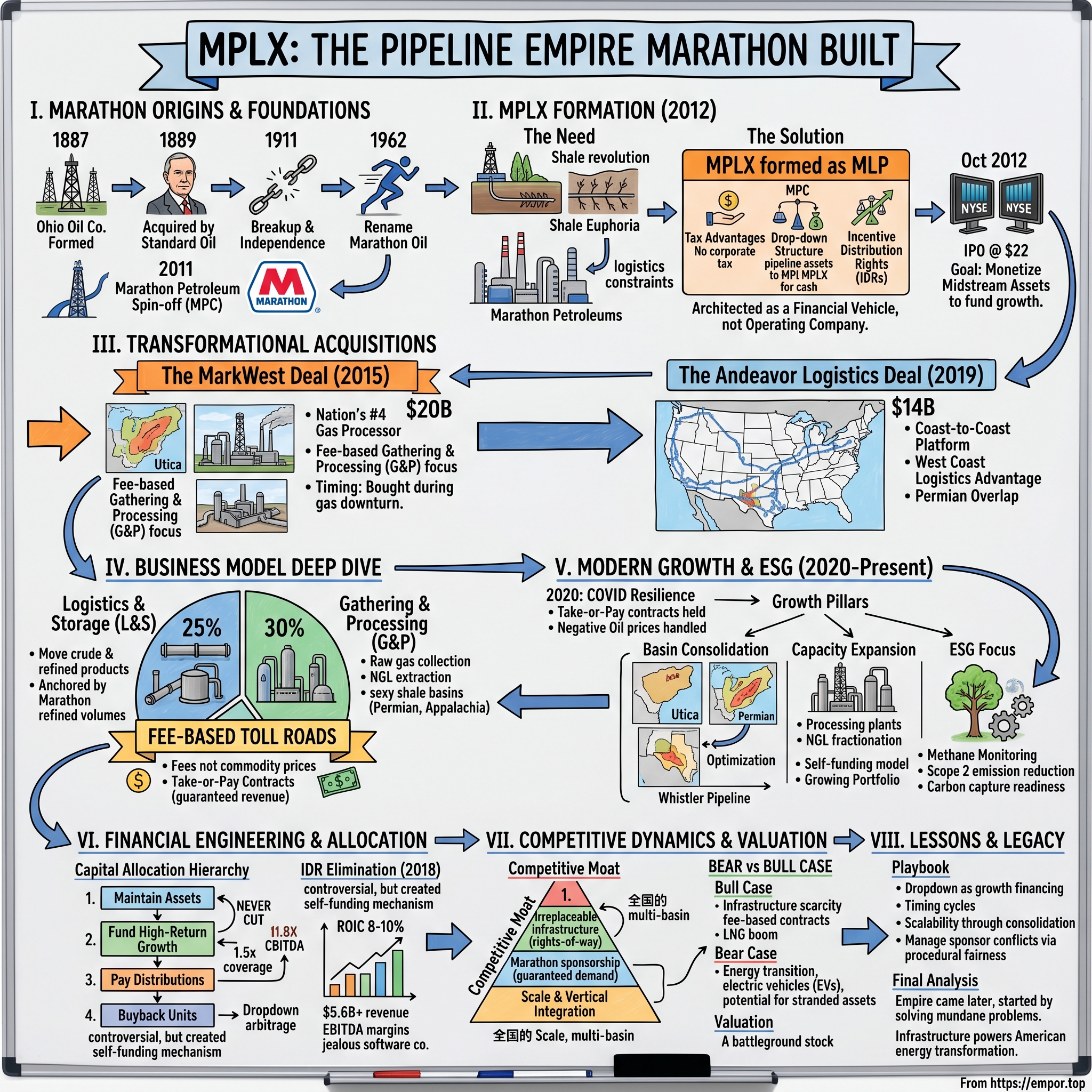

Picture this: It's a crisp October morning in 2012, and a new ticker symbol flashes across the NYSE screens—MPLX. To most observers, it's just another energy IPO in a frothy market drunk on shale euphoria. But for the executives at Marathon Petroleum's Findlay, Ohio headquarters, this three-letter symbol represents something far more strategic: the financial engineering blueprint that would transform a collection of rusty pipelines into a $50 billion midstream colossus.

The story of MPLX isn't just about pipes and terminals—it's about mastering the dark arts of MLP structuring, executing perfectly-timed mega-acquisitions, and building what amounts to America's energy toll roads at precisely the moment the shale revolution demanded them. While Tesla captures headlines and solar panels multiply on rooftops, MPLX quietly moves 5.9 million barrels of crude daily through its arteries, processes enough natural gas to heat millions of homes, and generates the kind of predictable cash flows that make dividend investors swoon.

But here's what makes this story particularly fascinating: MPLX was architected from day one as a financial vehicle, not an operating company. Marathon Petroleum didn't just want to own midstream assets—they wanted to monetize them through an elegant dropdown structure that would fund billions in growth while maintaining control. Think of it as the energy sector's version of a REIT, but instead of shopping malls, you're collecting tolls on the hydrocarbons that keep America running.

The master limited partnership structure itself deserves unpacking. MLPs don't pay corporate taxes—they pass through income directly to unitholders, creating a tax-efficient vehicle for capital-intensive infrastructure. For Marathon Petroleum, this meant they could transfer assets to MPLX at attractive valuations, MPLX could raise cheap capital from yield-hungry investors, and Marathon could redeploy that capital into higher-return projects. It's financial engineering at its finest—or most controversial, depending on your perspective.

Today, MPLX operates across two massive segments that touch nearly every molecule of hydrocarbon moving through America's heartland. Their Logistics and Storage segment runs the pipelines, terminals, and marine vessels that move crude oil and refined products. Meanwhile, their Gathering and Processing segment operates in the sexy shale basins—Marcellus, Utica, Permian—where natural gas gets pulled from wellheads, processed, fractionated, and shipped to market. Combined, these operations generated $5.6 billion in revenue over the past twelve months, with EBITDA margins that would make a software company jealous.

The timing of MPLX's creation couldn't have been more prescient. In 2012, the Bakken was booming, the Eagle Ford was accelerating, and the Marcellus was just revealing its true potential. America needed pipelines, processing plants, and storage terminals—fast. Traditional financing was too slow, too expensive. The MLP structure offered a solution: patient capital from income investors funding the infrastructure build-out that would enable American energy independence.

Yet the MPLX story is also one of consolidation and simplification. What began as a small dropdown vehicle has absorbed multiple MLPs, simplified Marathon's corporate structure, and emerged as one of the few midstream giants with true nationwide scale. The path from that $300 million IPO to today's $50 billion enterprise value runs through two transformative acquisitions—MarkWest in 2015 and Andeavor Logistics in 2019—each perfectly timed to capture value and expand capabilities.

As we dive deep into this eight-decade saga that spans from Ohio oil fields to nationwide pipeline networks, we'll explore how Marathon Petroleum built one of America's most essential—and profitable—energy infrastructure platforms. We'll examine the financial engineering, dissect the mega-deals, and ultimately answer the question: In an era of energy transition and ESG mandates, what is the enduring value of owning America's hydrocarbon highways?

II. Marathon Petroleum Origins & The Energy Landscape

The year was 1887, and Lima, Ohio was experiencing the kind of boom that would make modern-day Austin or Miami look quaint. Oil had been discovered just two years earlier, and suddenly this sleepy railroad town was the epicenter of American crude production. Into this chaos stepped a group of fourteen independent oil producers who pooled their resources to form The Ohio Oil Company—not out of ambition for empire-building, but from pure survival instinct against the predatory pricing of Standard Oil.

The Ohio Oil Company's early days read like a David and Goliath tale, except David eventually joined Goliath's army. By 1889, just two years after formation, The Ohio Oil Company had become the largest oil producer in Ohio, controlling an astounding 90% of the state's production. This caught the attention of John D. Rockefeller, who absorbed the company into his Standard Oil Trust that same year. For the next two decades, Ohio Oil operated as Standard's crucial Midwest subsidiary, learning the dark arts of vertical integration and market control from the master monopolist himself.

The 1911 Supreme Court decision that shattered Standard Oil into 34 pieces gave Ohio Oil its independence—and its future. Reborn as an independent entity with substantial production assets but limited refining capacity, the company embarked on a decades-long transformation. They moved their headquarters from Findlay to Houston in 1959, signaling a shift from Midwest producer to national player. The real identity change came in 1962 when they adopted the Marathon name—inspired by the ancient Greek battle that symbolized endurance against overwhelming odds.

Fast forward through decades of international expansion, upstream focus, and the creation of one of America's most successful integrated oil companies. By 2011, Marathon Oil had become a $30 billion enterprise, but management faced a classic conglomerate discount problem. Their upstream exploration and production business required different capital allocation than their downstream refining and marketing operations. Activist investors smelled blood. The solution? Split the company in two.

On July 1, 2011, Marathon Petroleum Corporation emerged as a standalone downstream company—America's fifth-largest refiner with 1.2 million barrels per day of capacity across six refineries. CEO Gary Heminger, a Marathon lifer who started as a co-op student in 1975, suddenly found himself running a pure-play refining and marketing company in the midst of the shale revolution. The timing was exquisite: domestic crude production was surging, refining margins were expanding, and infrastructure bottlenecks were creating massive arbitrage opportunities.

But Heminger and his team recognized a problem that would define MPLX's creation. Marathon Petroleum owned valuable midstream assets—pipelines connecting their refineries, terminals storing their products, marine vessels moving their crude. These assets generated steady, fee-based cash flows that the market valued differently than volatile refining margins. Moreover, Marathon needed capital to expand these logistics assets to capture the shale opportunity, but didn't want to dilute shareholders or lever up the parent company.

The MLP boom of the early 2010s offered a solution. Master limited partnerships had emerged as the preferred structure for midstream assets, offering tax advantages to investors and cheap capital to sponsors. The playbook was elegant: contribute assets to an MLP at attractive multiples, sell units to yield-seeking investors, use proceeds to fund growth, maintain control through general partner interests and incentive distribution rights. Peers like Phillips 66, Valero, and Tesoro were all launching MLPs. Marathon needed its own.

The broader energy landscape in 2012 was undergoing a tectonic shift that made midstream infrastructure suddenly sexy. Horizontal drilling and hydraulic fracturing had unlocked resources previously thought uneconomical. The Bakken in North Dakota was producing 600,000 barrels per day and climbing. The Eagle Ford in South Texas was ramping toward a million barrels daily. The Marcellus in Pennsylvania was revealing itself as one of the world's largest natural gas fields.

This production surge created massive infrastructure deficits. Crude oil from North Dakota was moving by rail—expensive and dangerous—because pipeline capacity didn't exist. Natural gas in Pennsylvania was selling for negative prices because processing plants couldn't handle the volume. The arbitrage opportunities were staggering: Bakken crude traded at a $20 discount to Gulf Coast pricing simply due to transportation constraints.

For Marathon Petroleum, with refineries in the Midwest perfectly positioned to process discounted shale crude, the opportunity was obvious. They needed to control the logistics chain—to ensure reliable supply to their refineries while capturing the infrastructure margins themselves. But building pipelines and processing plants requires massive upfront capital with long payback periods. Traditional corporate financing would constrain their flexibility and increase their cost of capital.

Enter the master limited partnership structure—a distinctly American financial innovation that would enable the infrastructure buildout of the shale revolution. MLPs don't pay corporate taxes; they pass through income directly to unitholders who pay taxes at individual rates. This tax efficiency, combined with America's deep appetite for yield in a zero-interest-rate environment, created a nearly perfect capital recycling machine.

The regulatory environment also favored midstream expansion. The Federal Energy Regulatory Commission maintained a light touch on interstate pipelines. Environmental permitting, while complex, hadn't yet reached the weaponized opposition levels of the late 2010s. States like Texas, Oklahoma, and North Dakota actively courted pipeline development. The stars were aligning for a midstream infrastructure boom.

Marathon's strategic positioning was particularly advantageous. Unlike pure-play midstream companies that relied entirely on third-party volumes, Marathon Petroleum provided a guaranteed anchor customer for any assets dropped into an MLP. Their refineries needed crude supply and product distribution—volumes that could underpin long-term contracts and provide stable cash flows to support distributions.

The competitive landscape was fragmenting in interesting ways. Integrated majors like ExxonMobil and Chevron showed little interest in the MLP game, viewing it as financial engineering that distracted from operations. Independent refiners were all racing to create MLPs, but most lacked Marathon's scale and geographic diversity. Pure-play midstream companies like Enterprise Products and Kinder Morgan were consolidating smaller players but faced pressure to maintain distribution growth without a corporate parent to drop down assets.

As Marathon Petroleum's board approved the formation of MPLX in early 2012, they weren't just creating another MLP—they were architecting a financial vehicle that would become the funding mechanism for one of the largest infrastructure buildouts in American history. The initial public offering would be modest, the initial assets unremarkable. But the dropdown pipeline—pun intended—that Marathon controlled would fuel decades of growth.

The shale revolution needed infrastructure. Marathon needed capital efficiency. Investors needed yield. MPLX would sit at the intersection of all three needs, collecting tolls on America's energy transformation while building an empire one pipeline at a time.

III. MPLX Formation & IPO (2012)

Gary Heminger stood before a packed conference room at Marathon Petroleum's Findlay headquarters on a humid July morning in 2012. The PowerPoint slide behind him showed a simple corporate structure diagram, but what it represented was anything but simple: the financial architecture that would unlock billions in value from Marathon's midstream assets. "Gentlemen," he began, "we're not just launching an MLP. We're creating a perpetual funding mechanism for the infrastructure America desperately needs."

The formation of MPLX had been months in the making, orchestrated by Marathon's finance team with the precision of a Swiss watchmaker. The initial portfolio wasn't meant to impress—it was meant to prove the concept. Marathon would contribute a 51% interest in its pipeline network connecting the Robinson, Illinois refinery to various terminals, plus a 100% interest in two butane caverns in Neal, West Virginia. Total asset value: roughly $400 million. Modest by design, executable by necessity.

The choice of initial assets revealed Marathon's strategic thinking. The pipeline network generated about $100 million in annual revenue through long-term contracts with Marathon Petroleum itself—providing the stable, predictable cash flows that MLP investors craved. The butane caverns added diversity and growth potential. Together, they formed a foundation solid enough to support distributions but small enough to leave massive runway for growth. The IPO roadshow in October 2012 was a masterclass in expectation management. Heminger and CFO Don Templin traveled from Boston to Houston, meeting with institutional investors who were simultaneously hungry for yield and skeptical of yet another refiner MLP. The pitch was straightforward: unlike peers who promised growth through risky acquisitions, MPLX would grow through dropdown transactions with Marathon Petroleum at pre-negotiated, formulaic valuations. No bidding wars, no integration risks, just steady, predictable growth.

The market responded enthusiastically. On October 25, 2012, MPLX priced its IPO at $22 per unit, above the $19-$21 range, raising $381 million by offering 17.3 million units—the company had originally planned just 15 million units. The oversubscription sent a clear message: investors believed in the Marathon dropdown story.

The financial engineering behind the IPO structure deserves attention. Marathon retained an 81% limited partner interest plus a 2% general partner interest through MPLX GP LLC. This gave Marathon effective control while allowing public unitholders to participate in the cash flow growth. The incentive distribution rights (IDRs) were the secret sauce—as distributions grew, Marathon's share of incremental cash flows would increase from 2% to 15%, 25%, and ultimately 50% above certain thresholds.

Think of IDRs as a carried interest on steroids. At low distribution levels, nearly all cash flows go to limited partners. But as distributions grow—funded by dropdown acquisitions—the general partner captures an increasing share of marginal cash flows. For Marathon, this created a powerful incentive to grow MPLX distributions, which they could accomplish by dropping down assets at attractive multiples.

The initial quarterly distribution was set at $0.2625 per unit, implying an annualized yield of about 4.8% at the IPO price. Conservative by design—management wanted to under-promise and over-deliver. The distribution coverage ratio exceeded 1.5x, providing a substantial cushion that would allow for steady increases even if market conditions deteriorated.

Wall Street's analyst community initially struggled to value MPLX. Was it a pipeline company? A logistics play? A Marathon Petroleum subsidiary in disguise? The answer was all three, which made comparable analysis challenging. Enterprise Products Partners traded at 11x EBITDA, but had third-party customer diversity. Plains All American Pipeline traded at 9x, but faced commodity exposure. MPLX's initial valuation of roughly 10x forward EBITDA split the difference.

The dropdown pipeline—Marathon's inventory of assets that could be sold to MPLX—was the real prize. Marathon owned or leased approximately 8,300 miles of pipeline, 60 terminals, 120 light product trucks, and a 1,100-vessel barge fleet. Only a tiny fraction had been contributed to MPLX at IPO. The remaining assets represented a decade-plus of dropdown inventory, each transaction potentially accretive to MPLX distributions and valuable to Marathon's capital recycling.

The first dropdown came quickly. In December 2012, just two months post-IPO, MPLX acquired additional pipeline interests from Marathon for $45 million. Small, but it proved the model worked. The transaction was immediately accretive to distributable cash flow, funded entirely with debt at attractive rates, and executed at a pre-negotiated multiple based on EBITDA.

Behind the scenes, Marathon's finance team had built a sophisticated model for optimizing dropdown timing and pricing. They analyzed MPLX's cost of capital, distribution coverage, leverage metrics, and market conditions to determine the optimal pace of dropdowns. Too fast, and MPLX might over-lever or dilute returns. Too slow, and distribution growth would lag, depressing unit prices and raising capital costs.

The governance structure, while standard for MLPs, created inherent conflicts of interest that would define MPLX's evolution. Marathon Petroleum controlled the general partner, set the dropdown prices, and decided which assets to sell and when. The conflicts committee—independent directors tasked with protecting public unitholders—provided oversight, but everyone understood the game. As long as dropdowns were accretive and distributions grew, everyone won.

Early operational performance validated the model. The Robinson pipeline system maintained 99% uptime. The butane caverns operated at near-full capacity. Customer contracts renewed at favorable rates. Most importantly, Marathon Petroleum's refining volumes provided steady, guaranteed demand that underpinned MPLX's cash flows.

The cultural dynamics between Marathon and MPLX were fascinating. MPLX had no employees—all operations were conducted by Marathon personnel under an omnibus agreement. This created efficiency but also dependence. MPLX was less a company than a financial vehicle, a structure for monetizing Marathon's infrastructure while maintaining operational control.

By year-end 2012, MPLX units had risen to $27, a 23% gain from the IPO price. The first distribution increase came in Q1 2013—a 4.8% bump that signaled management's confidence. The dropdown pipeline was valued at roughly $2 billion in potential acquisitions. The MLP structure was working exactly as designed.

Yet even in these early days, shrewd observers noted the model's inherent limitations. MPLX's growth depended entirely on Marathon's willingness to sell assets. Its cost of capital relied on maintaining distribution growth. Its value proposition assumed that yield-seeking investors would continue accepting limited partner governance rights in exchange for tax-advantaged income. These assumptions would be tested, but in late 2012, with WTI crude at $90 and natural gas production booming, the future looked bright.

The IPO had established MPLX as a viable funding vehicle for Marathon's infrastructure ambitions. The real test would come with scale—could this model support not just millions, but billions in acquisitions? The answer would reshape American energy infrastructure.

IV. The MarkWest Mega-Deal (2015)

Frank Semple, CEO of MarkWest Energy Partners, stared at the offer sheet in his Denver office on a February morning in 2015. The number was staggering: $15.8 billion in enterprise value, representing a 32% premium to MarkWest's unit price. After building MarkWest from a small Appalachian gatherer into the nation's fourth-largest processor of natural gas, Semple knew this was the exit his unitholders deserved. But for Gary Heminger and the MPLX team, this wasn't an exit—it was the transformation that would define their company's next decade. The strategic rationale for the MarkWest acquisition was compelling enough to make investment bankers salivate. MarkWest controlled the gathering and processing infrastructure in the Marcellus and Utica shales—the most prolific natural gas basins in America. They processed 5.5 billion cubic feet of natural gas daily, operated 13 processing complexes, and had locked up long-term dedications from producers who had no other viable options for getting their gas to market. The transaction would combine "the nation's second-largest processor of natural gas and the largest processor and fractionator in the Marcellus and Utica shale plays with a rapidly growing crude oil and refined products logistics master limited partnership."

The deal structure revealed sophisticated financial engineering. MarkWest unitholders would receive 1.09 MPLX units plus approximately $5.21 in cash per MarkWest unit. The total transaction valued at approximately $20 billion included the assumption of debt and other liabilities of approximately $4.2 billion. Marathon Petroleum sweetened the pot by contributing $1.075 billion in cash to fund the payment—up from an initial $675 million—after MarkWest unitholders balked at the original terms.

What made MarkWest so attractive wasn't just its assets—it was the irreplaceability of those assets. In the Marcellus and Utica, geography is destiny. The processing plants sit in valleys where producers have no alternative but to flow their gas. The gathering lines snake through Pennsylvania and Ohio farmland where obtaining new rights-of-way would take years and face fierce opposition. MarkWest had built its infrastructure when landowners welcomed pipelines; by 2015, that window had largely closed.

The timing of the acquisition was either brilliant or lucky, depending on your perspective. Natural gas prices had collapsed from $4.50 to $2.50 per thousand cubic feet, crushing MarkWest's unit price and making the 32% premium palatable to MPLX investors. Yet Marcellus production continued growing, driven by associated gas from liquids-rich drilling. Producers had to move their gas regardless of price, and MarkWest collected fees on every molecule.

Frank Semple's integration into the MPLX organization was seamless—he became vice chairman and joined the board, bringing decades of midstream expertise and crucial producer relationships. His team had built MarkWest through the cowboy days of Marcellus development, when handshake deals and rapid execution mattered more than corporate governance. That entrepreneurial DNA would prove invaluable as MPLX navigated the complexities of serving both third-party producers and its sponsor's refineries.

The operational synergies emerged quickly. MPLX's crude pipelines could now connect to MarkWest's NGL infrastructure, creating integrated value chains from wellhead to refinery. MarkWest's processing plants produced NGLs that Marathon's refineries could consume. The combined entity could offer producers comprehensive midstream solutions—gathering, processing, fractionation, transportation—capturing more margin at each step.

By December 4, 2015, the deal closed successfully, with approximately 80% of MarkWest unitholders voting in favor. The integration proceeded with military precision. IT systems merged within six months. Commercial teams cross-sold services to existing customers. Most importantly, the MarkWest field operations continued without disruption—critical given that any downtime would cascade through producer operations and destroy hard-won trust.

The financial impact was immediate and dramatic. Fourth-quarter 2015 adjusted EBITDA jumped to $286 million, with the MarkWest assets contributing significant cash flow despite being consolidated for less than a month. Distribution coverage remained healthy at 1.27x, providing confidence that the acquisition wouldn't imperil the payout that investors cherished.

But the real value of MarkWest went beyond current cash flows—it was about positioning for the next decade of American energy development. The Marcellus and Utica weren't just big; they were permanent. Unlike shale oil plays that might exhaust in decades, these gas fields contained centuries of reserves. Whoever controlled the processing and transportation infrastructure would collect tolls for generations.

The cultural integration challenges were real but manageable. MarkWest's Denver-based team had operated with significant autonomy, making quick decisions to capture opportunities. MPLX's Findlay culture was more deliberate, shaped by decades of refinery operations where safety and reliability trumped speed. The solution was elegant: maintain MarkWest as a semi-autonomous division, preserving its entrepreneurial spirit while imposing Marathon's operational discipline where it mattered.

Wall Street's reaction was mixed but ultimately positive. Some analysts questioned paying a 32% premium in a collapsing commodity environment. Others worried about MPLX's increased exposure to natural gas prices and producer creditworthiness. But the strategic logic was undeniable: MPLX had transformed from a simple logistics MLP into a full-service midstream powerhouse with irreplaceable assets in America's most important gas basins.

The leverage metrics told the story of disciplined execution. Despite adding $4.2 billion in debt, MPLX maintained its investment-grade credit profile. The combined entity's EBITDA could support the enlarged debt load with comfortable coverage. Marathon Petroleum's implicit support—both as primary customer and equity sponsor—provided additional comfort to creditors.

For Marathon Petroleum, the MarkWest acquisition through MPLX was a masterstroke of capital allocation. They gained exposure to high-growth gathering and processing without diluting their refining-focused equity story. The enhanced IDR payments from MPLX's enlarged distribution base created a growing annuity stream. Most importantly, they now controlled critical infrastructure linking Appalachian gas production to Midwest refining and petrochemical demand.

The integration playbook would become the template for future acquisitions. Focus on operational continuity first, financial optimization second. Preserve local relationships while imposing corporate standards. Invest in connecting assets to create network effects. And always, always maintain the distribution—the sacred covenant with MLP investors that enabled access to capital markets.

By early 2016, the transformation was complete. MPLX had evolved from Marathon's dropdown vehicle into one of America's largest midstream companies, with assets spanning from Appalachian hillsides to Gulf Coast terminals. The MarkWest acquisition proved that MPLX could execute large-scale M&A, integrate complex operations, and create value beyond simple financial engineering. The stage was set for the next act: nationwide consolidation.

V. The Andeavor Era & Creating Scale (2018-2019)

The phone call that would reshape American energy infrastructure came on a Sunday evening in April 2018. Gary Heminger had just agreed to Marathon Petroleum's $23 billion acquisition of Andeavor, creating America's largest refiner. But as he reviewed the deal terms with his CFO, another opportunity crystallized: Andeavor owned its own MLP—Andeavor Logistics—with West Coast pipelines and terminals that would perfectly complement MPLX's Midwest and Gulf Coast footprint. Why stop at combining the refineries when they could create the first truly nationwide midstream platform? The Andeavor Logistics acquisition, announced in May 2019 and completed on July 30, represented a different beast entirely from MarkWest. The companies entered into a definitive merger agreement whereby MPLX would acquire ANDX in a unit-for-unit transaction at a blended exchange ratio of 1.07x, representing an equity value of approximately $9 billion and an enterprise value of $14 billion for the acquired entity. This wasn't about entering new markets or capabilities—it was about simplification, scale, and creating the first coast-to-coast midstream platform.

The backstory made the deal almost inevitable. When Marathon acquired Andeavor's refining assets in 2018, they inherited a parallel MLP structure that duplicated costs and confused investors. Two MLPs, two management teams, two sets of public unitholders, competing for the same dropdown assets from the same sponsor. The inefficiency was obvious, the solution elegant: combine them into a single, simplified vehicle.

Andeavor Logistics brought assets Marathon couldn't have built or bought independently: West Coast pipelines connecting California refineries to Nevada and Arizona markets, terminals in Los Angeles and Seattle, crude gathering systems in the Bakken. These weren't just pipes—they were irreplaceable rights-of-way through some of America's most regulated and litigious states. Try building a new pipeline from Los Angeles to Las Vegas today; you'll understand why these assets trade at astronomical multiples.

The integration challenge was fundamentally different from MarkWest. While MarkWest required melding entrepreneurial cultures, Andeavor Logistics was already running on Marathon's operating system—same safety protocols, similar commercial practices, compatible IT infrastructure. The real complexity lay in harmonizing contracts, optimizing overlapping assets, and managing the delicate dance of serving both legacy Marathon and legacy Andeavor refineries without favoritism.

Gary Heminger captured the strategic vision: "This transaction allows MPLX to further progress its strategic vision of creating a leading, large-scale, diversified midstream company anchored by fee-based cash flows." The emphasis on "fee-based" wasn't accidental—in a world where investors increasingly questioned commodity exposure, MPLX was doubling down on its toll-road model.

The financial engineering of the deal showcased sophisticated structuring. Under the terms of the merger agreement, ANDX public unitholders would receive 1.135x MPLX common units for each ANDX common unit held, representing a premium of 7.3%, while MPC would receive 1.0328x MPLX common units for each ANDX common unit held, representing a 2.4% [premium]. This differential pricing elegantly balanced the interests of public unitholders who needed incentive to approve the deal with Marathon's desire to maintain its economic interest.

The West Coast assets transformed MPLX's strategic positioning. California's unique fuel specifications—essentially a closed market—meant whoever controlled the logistics infrastructure could extract premium margins. The Los Angeles refinery-to-terminal connections were particularly valuable, moving millions of barrels through some of America's most congested and regulated corridors. These weren't just assets; they were licenses to print money in markets where new competition was practically impossible.

The Permian Basin overlap created immediate synergies. Both MPLX and Andeavor Logistics had been building gathering systems in the Delaware and Midland basins, sometimes competing for the same producer dedications. Combined, they could optimize gathering routes, share processing capacity, and offer producers comprehensive wellhead-to-market solutions. The commercial teams identified $50 million in annual synergies just from eliminating redundant infrastructure projects.

But the real genius of the Andeavor combination was what it meant for Marathon Petroleum's dropdown strategy. Instead of choosing which MLP should receive each asset, Marathon now had a single, scaled vehicle with access to cheaper capital. The simplified structure reduced governance complexity, eliminated conflicts between competing MLPs, and created a clearer story for investors: one sponsor, one MLP, one nationwide platform.

The market initially struggled to digest the combination. Some investors worried about increased leverage—MPLX was assuming approximately $5 billion of Andeavor Logistics debt. Others questioned whether the promised synergies would materialize. The unit price reflected this skepticism, trading sideways despite the strategic logic of the combination.

Yet operational performance quickly validated the strategy. The combined entity generated immediate cost savings from eliminating duplicate management structures, consolidating insurance programs, and optimizing capital allocation. More importantly, the nationwide footprint enabled new commercial opportunities: long-haul crude movements from the Permian to West Coast refineries, product backhauls from California to Nevada, integrated NGL logistics from wellhead to export terminal.

The governance simplification was perhaps the most underappreciated benefit. Instead of managing conflicts between two MLPs competing for the same dropdown assets, Marathon could now execute a streamlined capital recycling strategy. Assets could be dropped down based on MPLX's capital availability and cost of capital, not artificial competition between sister MLPs. This efficiency would prove crucial as Marathon evaluated its next wave of infrastructure investments.

The technology integration proceeded smoothly—both MLPs had already been operating on Marathon's systems, making the combination more like merging databases than integrating companies. Commercial contracts were harmonized within six months. Field operations barely noticed the change, except their scheduling and dispatch suddenly had more options for routing molecules.

For the broader MLP sector, the Andeavor combination sent a clear message: the era of sponsor-owned MLP proliferation was ending. Simplification was the new growth strategy. Rather than financial engineering through multiple vehicles, sponsors would focus on operational excellence through single, scaled platforms. The market rewarded this maturation—MPLX's cost of capital improved as investors appreciated the simplified structure.

By the end of 2019, MPLX had emerged as something unique in the midstream landscape: a truly nationwide platform with assets in every major basin, serving America's largest refining system, generating over $5 billion in annual EBITDA. The combination of organic growth, MarkWest's gathering and processing, and Andeavor's logistics had created a midstream giant that touched nearly every molecule of hydrocarbon moving through America.

The transformation from a $300 million IPO to a $50 billion enterprise had taken just seven years. But the real accomplishment wasn't size—it was the creation of an integrated platform that could capture value from wellhead to rack, from Appalachian gas fields to California terminals. As America entered 2020, MPLX was positioned to weather whatever storms lay ahead. Little did anyone know how soon that positioning would be tested.

VI. Business Model Deep Dive

Inside MPLX's Houston control room, dozens of screens display real-time flows across 10,000 miles of pipelines. A controller notices pressure dropping at a Permian gathering point—likely a well coming offline for maintenance. Within seconds, she reroutes flow through alternative lines, maintaining steady deliveries to the downstream processing plant. This operational ballet happens thousands of times daily, but the beauty of MPLX's business model isn't in the complexity of operations—it's in the simplicity of the economics: every molecule that moves generates a fee, regardless of commodity prices.

MPLX operates through two distinct but synergistic segments that together form an integrated midstream platform. The Logistics and Storage segment generated $3.2 billion in revenue over the last twelve months, operating the pipelines, terminals, and marine assets that move crude oil and refined products across America. Meanwhile, the Gathering and Processing segment contributed $2.4 billion, running the infrastructure that collects raw natural gas from wellheads, strips out valuable liquids, and delivers processed gas to market.

The genius of the fee-based model becomes clear when you examine a typical contract. A producer in the Marcellus commits to deliver 100 million cubic feet of gas daily to MPLX's processing plant for ten years. MPLX charges $0.50 per thousand cubic feet for gathering, $0.30 for processing, and keeps 15% of the extracted natural gas liquids. Crucially, these fees are largely fixed—whether natural gas sells for $2 or $10, MPLX collects the same tolls. Even better, most contracts include annual escalators tied to inflation and minimum volume commitments that ensure payment even if wells underperform.

The contract architecture deserves careful attention. Take-or-pay provisions require customers to pay for reserved capacity whether they use it or not—think of it as paying rent on a storage unit you might not fill. These commitments typically cover 70-80% of facility capacity, providing MPLX with guaranteed revenue that underpins distributions. The remaining 20-30% captures spot volumes at higher rates, providing upside during periods of high production.

Consider the economics of a typical processing plant in the Utica Shale. MPLX invests $300 million to build a 200 million cubic feet per day facility. Anchor producers commit to 150 MMcf/d under 10-year contracts at $0.80 per Mcf, generating $44 million in annual revenue before MPLX processes a single molecule. Add NGL retention revenues and spot volumes, and the plant generates $65 million in annual EBITDA—a 4.6-year payback that would make any industrial investor envious.

The marine business offers a fascinating case study in competitive moats. MPLX operates 18 towboats and 280 barges on inland waterways, moving refined products from Gulf Coast refineries to Midwest terminals. A single barge holds 30,000 barrels—equivalent to 120 rail cars or 144 trucks. The capital intensity is staggering: a new towboat costs $30 million, a barge $3 million. But once deployed, these assets generate steady returns for decades. The Ohio River isn't getting any wider, and environmental permits for new marine facilities are essentially impossible to obtain.

Marathon Petroleum's role as anchor customer provides ballast that pure-play midstream companies lack. Roughly 55% of MPLX's revenues come from Marathon, primarily through long-term contracts at market rates validated by regulatory filings. This isn't problematic dependence—it's strategic symbiosis. Marathon needs reliable logistics for its 3 million barrels per day of refining capacity. MPLX needs stable volumes to support growth investments. The relationship is governed by commercial agreements that ensure arm's-length pricing while providing both parties with operational flexibility.

The crude oil pipeline network showcases the value of strategic positioning. The Bakken Pipeline system, jointly owned with Energy Transfer, moves 570,000 barrels daily from North Dakota to Illinois. Shippers commit to capacity years in advance, paying whether they ship or not. During 2020's production collapse, MPLX continued collecting fees on contracted capacity even as actual flows dropped 30%. This resilience in the face of volume destruction demonstrates why midstream assets deserve utility-like valuations.

Natural gas processing adds a commodity overlay to the fee structure, but with important hedges. When MPLX strips NGLs from raw gas, they typically keep 10-20% of the liquids as payment. This creates commodity exposure, but MPLX hedges 80% of expected NGL production two years forward, locking in margins and protecting distributions. The remaining unhedged exposure provides upside when NGL prices spike, as they did in 2022 when European petrochemical demand surged.

The fractionation facilities at Mont Belvieu represent midstream infrastructure at its most essential. These plants separate mixed NGLs into purity products—ethane for chemicals, propane for heating, butane for gasoline blending. MPLX charges fixed fees per gallon fractionated, regardless of commodity spreads. With 850,000 barrels per day of fractionation capacity and 95% utilization rates, these facilities are essentially printing presses, generating $400 million in annual EBITDA with minimal capital investment.

Storage assets provide the ballast in MPLX's portfolio. The 35 million barrels of crude and product storage generate $300 million in annual revenue through fixed monthly fees. Customers pay for the option value of storage—the ability to arbitrage price differentials across time or locations. For MPLX, it's pure annuity income. Tanks don't require feed gas, they don't face production declines, and their contracts renew at 95% rates because the switching costs of moving to alternative storage are prohibitive.

The distribution strategy reflects classic MLP economics. MPLX targets a 1.4-1.6x coverage ratio, meaning they generate 40-60% more cash than they distribute. This cushion provides safety during downturns while funding growth capital without constant equity issuance. The quarterly distribution of $0.775 per unit implies a 6.2% yield at current prices—attractive in any rate environment but particularly compelling when investment-grade corporate bonds yield 4%.

Capital allocation follows a clear hierarchy: maintain the assets, fund high-return growth projects, pay distributions, buy back units if they trade below intrinsic value. This disciplined approach means passing on acquisitions that might boost EBITDA but would dilute returns. It means investing in boring reliability projects that prevent outages rather than sexy expansions that grab headlines. It's the operational equivalent of compound interest—steady, predictable, powerful over time.

The technology investments, while unglamorous, drive meaningful efficiency gains. Automated pig launchers clean pipelines without manual intervention. Predictive analytics identify equipment failures before they occur. Digital twins simulate system operations to optimize flow patterns. These investments typically generate 20-30% returns through reduced maintenance costs and improved utilization—far exceeding the returns from building new infrastructure.

Risk management extends beyond commodity hedging to operational resilience. MPLX maintains diverse supply sources for critical equipment. They cross-train operators across facilities. They invest in cybersecurity with the paranoia of a defense contractor. When Colonial Pipeline suffered a ransomware attack in 2021, MPLX's systems remained unaffected because they had air-gapped critical control systems and maintained analog backups for essential operations.

The regulatory framework provides both protection and obligation. FERC-regulated interstate pipelines can earn regulated returns but face rate cases and shipper challenges. State-regulated gathering systems enjoy more pricing flexibility but face environmental scrutiny. MPLX navigates this complex landscape through dedicated regulatory teams that maintain relationships with agencies from the EPA to the Texas Railroad Commission.

Looking at returns on invested capital, MPLX consistently generates 8-10% ROIC, impressive for such a capital-intensive business. The key is the multiplier effect: a dollar invested in gathering pipelines enables processing plant construction, which justifies fractionation expansion, which supports storage development. Each investment makes the network more valuable, creating what economists call "increasing returns to scale"—the rich getting richer, but through operational excellence rather than financial engineering.

The business model's resilience was battle-tested during COVID-19's demand destruction. While volumes dropped 20-30% across some systems, EBITDA declined less than 10% thanks to take-or-pay contracts and fee structures. MPLX maintained its distribution when peers cut theirs, continued growth investments when competitors retreated, and emerged from the pandemic with increased market share. This wasn't luck—it was the business model working exactly as designed.

VII. Modern Operations & Growth Strategy (2020-Present)

March 2020 began like any other month in MPLX's Findlay headquarters—until oil prices went negative for the first time in history. Gary Heminger watched WTI crude trade at minus $37 per barrel on April 20, a moment that would have destroyed a commodity-exposed company. But in MPLX's conference room, the mood was surprisingly calm. "Gentlemen," Heminger told his leadership team, "this is exactly why we built a fee-based model. While others panic, we execute."

COVID-19's impact on energy markets was unprecedented. Demand collapsed 30% overnight as lockdowns grounded flights and emptied highways. Storage tanks filled to capacity. Producers shut in wells. Yet MPLX's first-quarter 2020 results told a different story: EBITDA of $1.2 billion, down just 5% from the prior year. The resilience came from those take-or-pay contracts—producers paid for pipeline capacity whether they used it or not.

The pandemic response revealed MPLX's operational DNA. Within days of lockdown orders, they implemented split operations—control room teams isolated in hotels to prevent COVID spread, maintenance crews segregated into pods, executive teams running scenarios from home offices. The technology investments of previous years paid dividends: remote monitoring systems allowed engineers to manage facilities from living rooms, predictive maintenance algorithms identified issues before they required field visits, automated systems reduced the need for on-site personnel.

While competitors slashed capital budgets, MPLX made a contrarian bet. They accelerated maintenance during the low-volume period, completing five-year turnarounds in months. They locked in construction contracts at distressed prices. Most boldly, they continued expanding in the Permian and Appalachian basins, betting that production would recover faster than consensus expected. The $1.2 billion growth capital program in 2020 looked reckless to some, prescient in hindsight. The recovery from COVID proved swifter than even optimists anticipated. By 2021, MPLX was firing on all cylinders—EBITDA exceeded $5 billion as volumes recovered and commodity prices surged. The contrarian investments during the downturn paid off handsomely. Processing plants commissioned in 2020 caught the production rebound. Pipeline expansions completed during lockdowns captured market share from competitors who had retreated.

The 2024 Utica expansion exemplified MPLX's modern growth strategy: consolidate positions in core basins rather than chase new frontiers. In March 2024, MPLX acquired Summit Midstream Utica, LLC, which includes its approximately 36% interest in Ohio Gathering Company, LLC, approximately 38% interest in Ohio Condensate Company, LLC and wholly owned Utica assets for $625 million in cash. This wasn't about entering the Utica—MPLX had operated there since the MarkWest acquisition. It was about achieving critical mass, eliminating joint venture complexity, and capturing synergies from integrated operations.

The strategic logic was compelling. Since partnering with Summit in the Utica Shale in 2014, MPLX's acquisitions of OGC and OCC assets strengthen its regional foothold. By consolidating ownership, MPLX could optimize gathering routes, eliminate redundant compression, and offer producers seamless service from wellhead to interstate pipelines. The $625 million price tag looked steep to some, but MPLX saw it differently: they were buying irreplaceable gathering positions in America's most prolific gas basin at a fraction of replacement cost.

The Permian Basin buildout showcased MPLX's ability to execute massive projects in challenging environments. The Whistler Pipeline, a joint venture with WhiteWater Midstream, required threading 450 miles of 42-inch pipe from the Permian to the Gulf Coast. Environmental protests, regulatory delays, and COVID complications pushed the timeline, but MPLX's project management expertise—honed over decades of refinery turnarounds—kept the project on track. When Whistler entered service in 2021, it immediately filled to capacity, validating the investment thesis.

Processing plant expansions in the Northeast revealed the power of MPLX's integrated model. It's building three more natural gas processing plants that should come online through the second half of next year. These weren't speculative builds—Marathon Petroleum's petrochemical operations provided guaranteed demand for the NGLs, while long-term producer dedications ensured feed gas supply. The plants incorporated the latest technology: automated pigging systems, AI-driven optimization, carbon capture readiness. Each represented not just capacity addition but capability enhancement.

The ESG transformation at MPLX reflects broader industry evolution. What began as defensive positioning against activist investors has become offensive strategy. Methane monitoring systems using satellite imagery and ground sensors detect leaks before they become material. Electric compression powered by renewable energy reduces Scope 2 emissions. Water recycling systems minimize freshwater consumption. These investments generate returns—reduced regulatory risk, lower operating costs, improved social license—that don't appear in traditional ROIC calculations but create long-term value nonetheless.

The 2024 financial performance validated the strategy. Last year, the MLP generated $5.4 billion in net cash from operating activities. It distributed $3.3 billion to investors and spent $1.3 billion on capital projects to maintain and expand its operations. The 1.5x distribution coverage provided ample cushion for growth investments while maintaining the sacred distribution. Leverage of 3.4x remained comfortably below the 4.0x target, providing dry powder for opportunistic acquisitions. The Q3 2024 results demonstrated the strategy's effectiveness: net income attributable to MPLX of $1,037 million, compared with $918 million for the third quarter of 2023. For the first nine months of the year, net income attributable to MPLX was $3,218 million, compared with $2,794 million in the first nine months of 2023. More impressively, Gathered volumes averaged 6.7 billion cubic feet per day (bcf/d), an 8% increase from the third quarter of 2023. Processed volumes averaged 9.8 bcf/d, a 9% increase versus the third quarter of 2023. Fractionated volumes averaged 635 thousand bpd, a 4% increase versus the third quarter of 2023.

The Northeast processing expansion represents MPLX betting on natural gas as a transition fuel. Harmon Creek II, a 200 mmcf/d processing plant, was placed into operation in February. Harmon Creek III, a 300 mmcf/d processing plant and 40 thousand bpd de-ethanizer, is expected online in the second half of 2026. These aren't speculative builds—producers have committed volumes under 10-year contracts, and petrochemical demand for NGLs continues growing as plastics consumption rises globally.

Capital allocation discipline remains paramount. As of September 30, 2024, MPLX had $2.4 billion in cash, $2.0 billion available on its bank revolving credit facility, and $1.5 billion available through its intercompany loan agreement with Marathon Petroleum Corp. MPLX's leverage ratio was 3.4x, while the stability of cash flows supports leverage in the range of 4.0x. This financial fortress provides optionality—MPLX can pursue acquisitions, accelerate organic growth, or return capital to unitholders as opportunities arise.

The distribution strategy evolution reflects management's confidence. MPLX announced a third-quarter 2024 distribution of $0.9565 per common unit, resulting in distribution coverage of 1.5x for the quarter... "The durability of our cash flows drove the decision to increase the distribution 12.5% this quarter and our growing portfolio is expected to support this level of annual distribution increases in the future", noted CEO Maryann Mannen.

Looking ahead, MPLX's growth strategy focuses on three pillars: consolidating positions in core basins, expanding processing and fractionation capacity ahead of demand, and optimizing the existing asset base through technology and operational excellence. The Permian natural gas value chain expansions, Northeast processing plants, and continued Utica optimization represent billions in committed growth capital that will drive cash flow expansion through 2027.

The technology investments accelerating through 2024 reveal MPLX's vision for the future of midstream operations. AI-powered predictive maintenance reduces unplanned outages by 30%. Digital twins optimize flow patterns in real-time, increasing throughput without new steel. Automated pig launchers clean pipelines without manual intervention. These aren't Silicon Valley buzzwords—they're operational improvements that drop straight to the bottom line.

Environmental initiatives have evolved from compliance to competitive advantage. Methane detection systems using satellite imagery identify leaks within hours, not days. Electric compression powered by renewable energy reduces emissions while lowering operating costs when grid power is cheaper than gas-fired alternatives. Carbon capture readiness at new facilities positions MPLX for potential future revenue streams as carbon markets develop.

The regulatory landscape continues evolving, but MPLX's proactive engagement positions them well. They're working with FERC on streamlined permitting for system expansions. They're collaborating with EPA on methane regulations that balance environmental protection with operational reality. They're engaging with state regulators on hydrogen blending standards that could open new revenue opportunities. This isn't lobbying—it's shaping the future regulatory framework in partnership with agencies.

Risk management has become increasingly sophisticated. MPLX maintains multiple scenario plans for everything from hurricane disruptions to cyber attacks. They hedge commodity exposure two years forward while maintaining upside optionality. They diversify customer concentration while preserving the Marathon Petroleum anchor relationship. They invest in redundancy and resilience rather than chasing the last dollar of optimization.

The human capital strategy deserves recognition. MPLX has invested heavily in training programs that convert refinery workers into midstream operators, addressing the industry's skilled labor shortage. They've implemented flexible work arrangements that attract younger talent without compromising operational excellence. They've created career paths that retain institutional knowledge while bringing in fresh perspectives.

As MPLX enters 2025, the company stands at an inflection point. The infrastructure built over the past decade generates predictable cash flows. The growth projects underway will expand capacity in the highest-return basins. The financial flexibility enables opportunistic capital allocation. The operational excellence culture drives continuous improvement. The strategic positioning captures value across the hydrocarbon value chain.

The modern MPLX is far removed from the simple dropdown vehicle created in 2012. It's become a sophisticated infrastructure platform that connects American energy production to global markets, generates substantial cash returns for investors, and adapts to an evolving energy landscape. Whether natural gas serves as a bridge fuel for decades or hydrogen economy infrastructure needs emerge, MPLX's assets, capabilities, and financial strength position it to capture value across multiple scenarios.

VIII. Capital Allocation & Financial Engineering

In MPLX's treasury department, spreadsheets glow with the intricate mathematics of MLP finance. The team manages a Rubik's cube of variables: distribution coverage ratios, leverage targets, IDR thresholds, dropdown valuations, hedge ratios, and cost of capital calculations. Each decision ripples through the structure—raise the distribution too fast and coverage shrinks; take on too much debt and credit spreads widen; price dropdowns too aggressively and conflicts committees balk. This is financial engineering at its most complex, where pennies per unit compound into billions of market value.

The MLP structure itself is a masterpiece of tax efficiency wrapped in governance complexity. MPLX pays no corporate taxes—all income flows through to unitholders who pay at their individual rates. For tax-exempt institutions and retirement accounts, this creates phantom income problems. For high-net-worth individuals, it generates tax-advantaged income through depreciation shields and depletion allowances. The K-1 tax forms are notoriously complex, but the after-tax returns justify the accounting headaches for many investors.

Distribution coverage philosophy reveals management's risk tolerance. MPLX targets 1.4-1.6x coverage, meaning they retain 40-60% of distributable cash flow for growth and safety. This contrasts with aggressive MLPs that distributed everything during the boom years, then slashed payouts when markets turned. The retained cash funds growth capex without dilutive equity issuances, maintains financial flexibility during downturns, and provides a buffer against operational disruptions. It's the financial equivalent of wearing both belt and suspenders.

The leverage target of 4.0x EBITDA represents a careful balance. Too much debt and credit ratings fall, increasing borrowing costs and limiting access to capital markets. Too little leverage and returns on equity suffer, making the distribution yield uncompetitive. MPLX's leverage ratio was 3.4x, while the stability of cash flows supports leverage in the range of 4.0x. This cushion provides dry powder for acquisitions while maintaining investment-grade ratings from Moody's and S&P.

Dropdown economics deserve detailed examination. When Marathon Petroleum sells assets to MPLX, the valuation typically ranges from 8-12x EBITDA depending on asset quality, growth prospects, and market conditions. Marathon receives MPLX units or cash, recycling capital while maintaining economic exposure through its LP and GP interests. MPLX funds the acquisition through a combination of debt, retained cash, and occasionally equity issuance. The key is ensuring each dropdown is accretive to distributable cash flow per unit after accounting for financing costs.

Consider a typical dropdown transaction: Marathon sells a $500 million pipeline system generating $50 million in annual EBITDA to MPLX at 10x multiple. MPLX funds it with $200 million in retained cash and $300 million in debt at 5% interest. The asset contributes $50 million in EBITDA but costs $15 million in interest, netting $35 million to distributable cash flow. Spread across 430 million units, that's $0.08 per unit annually—immediately accretive to distributions. Meanwhile, Marathon receives $500 million to redeploy into higher-return refining projects.

The incentive distribution rights (IDRs) created powerful alignment—until they didn't. As originally structured, Marathon's GP received increasing percentages of incremental cash flows as distributions grew: 2% up to $0.2875 per unit quarterly, 15% from $0.2875 to $0.3125, 25% from $0.3125 to $0.375, and 50% above $0.375. By 2018, with quarterly distributions at $0.6025, Marathon was capturing nearly 50% of marginal cash flows. This created a ceiling on distribution growth and made MPLX's cost of equity capital prohibitively expensive. The 2018 IDR elimination transaction was controversial but necessary. Immediately following the dropdown, MPC is exchanging its general partner (GP) economic interests in MPLX, including incentive distribution rights (IDRs), for 275 million newly issued MPLX common (LP) units valued at $10.1 billion as of the announcement date. John Fox, co-founder of MarkWest, publicly criticized the valuation, arguing the IDR elimination will be executed at a multiple of 17x the pro forma value of the GP's IDRs, well above market precedents.

Despite the controversy, IDR elimination transformed MPLX's cost of capital. Without IDRs siphoning off 50% of marginal cash flows, MPLX could retain more cash for growth, access cheaper equity capital when needed, and compete more effectively for third-party acquisitions. The market eventually recognized this value—MPLX units outperformed the Alerian MLP Index by 15% in the two years following IDR elimination.

Debt capital markets access represents another crucial component of financial strategy. MPLX maintains investment-grade ratings from both Moody's (Baa3) and S&P (BBB), enabling access to unsecured bond markets at attractive spreads. The May 2024 $1.65 billion bond issuance priced at Treasury plus 145 basis points for 10-year notes—remarkable for a capital-intensive partnership. This access provides flexibility to fund growth without dilutive equity issuances or expensive bank debt.

The capital structure optimization continues evolving. MPLX maintains a $2 billion revolving credit facility for working capital needs, a $1.5 billion intercompany loan agreement with Marathon for strategic flexibility, and long-dated bonds laddered across maturities to minimize refinancing risk. The weighted average cost of debt hovers around 4.5%, while the distribution yield implies an equity cost near 8%—suggesting an optimal capital structure around 40% debt, 60% equity.

Growth capital allocation follows a disciplined framework. Projects must clear a 15% unlevered IRR hurdle, have contracted cash flows covering at least 70% of capacity, and enhance system connectivity or customer relationships. The $950 million 2024 growth budget focuses on high-return debottlenecking projects, strategic system expansions, and technology investments that reduce operating costs. Each project undergoes rigorous stage-gate review, with post-investment audits ensuring projected returns materialize.

The unit buyback authorization, while rarely used, provides another capital allocation tool. When units trade below intrinsic value—which management estimates around $45 based on comparable transactions and DCF analysis—buybacks become accretive to remaining unitholders. The authorization also signals management confidence and provides support during market dislocations.

Distribution policy evolution reflects changing investor preferences. During the growth phase (2012-2018), aggressive distribution increases attracted yield-seeking investors. Post-IDR elimination (2018-2020), moderate growth with higher coverage appealed to total return investors. Today's 10-12% annual increases balance income and growth, attracting both yield and appreciation seekers. The sacred nature of the distribution—never cut, even during COVID—provides the foundation for this investor trust.

The conflicts of interest inherent in the MLP structure require careful navigation. Every dropdown, every commercial contract with Marathon, every capital allocation decision faces scrutiny from the conflicts committee of independent directors. These directors, typically former energy executives or financial experts, review fairness opinions, negotiate terms, and ensure public unitholders aren't disadvantaged. It's corporate governance theater, but necessary theater that maintains market confidence.

Tax considerations drive numerous structural decisions. The partnership structure's pass-through taxation creates complexity but saves approximately $500 million annually versus C-corp taxation. The depreciation and depletion deductions shelter much of the distribution from current taxation, creating tax-deferred income for investors. The Section 754 election allows buyers of units to step up their basis, enhancing the secondary market liquidity.

Looking forward, MPLX's financial strategy focuses on self-funding growth. With $5+ billion in annual EBITDA, $1.5 billion in maintenance capex, and $3.3 billion in distributions, roughly $200-400 million remains for growth investments without accessing capital markets. This self-funding model insulates MPLX from market volatility while maintaining distribution growth—the holy grail of MLP finance.

The sophistication of MPLX's financial engineering extends to risk management. Interest rate swaps fix 70% of floating rate debt. Commodity hedges lock in NGL margins two years forward. Credit insurance protects against customer defaults. These aren't speculative positions but systematic risk reduction that protects the distribution during volatile periods.

As interest rates normalize and energy markets evolve, MPLX's financial flexibility becomes increasingly valuable. The ability to access multiple capital sources, optimize between debt and equity, time the market for dropdowns and acquisitions, and maintain distribution growth regardless of market conditions—this is the financial engineering that transforms a collection of pipes into a wealth-compounding machine.

IX. Competitive Dynamics & Industry Position

At the annual Barclays CEO Energy Conference, the midstream panel resembles a gathering of infrastructure royalty. The CEOs of Enterprise Products, Energy Transfer, Kinder Morgan, and MPLX share the stage, each running enterprises worth tens of billions, collectively controlling the arteries through which American energy flows. Yet beneath the cordial panel discussion lies fierce competition for producer dedications, acquisition targets, and investor capital. In this game of pipeline poker, scale matters, but so do sponsor relationships, operational excellence, and financial flexibility.

Enterprise Products Partners stands as the industry's undisputed heavyweight—$150 billion enterprise value, 50,000 miles of pipelines, operations from wellhead to export terminal. Their fully integrated model and conservative financial management make them the industry's gold standard. Yet Enterprise lacks what MPLX possesses: a captive refining customer providing guaranteed demand. While Enterprise must compete for every barrel and molecule, MPLX starts with Marathon's 3 million barrels per day of refining capacity as baseload demand.

Energy Transfer represents MPLX's most direct competitor in scale and scope. With $100 billion in enterprise value and assets spanning every major basin, Energy Transfer matches MPLX's geographic reach. But Energy Transfer's history of aggressive acquisitions, complex structure changes, and distribution cuts during downturns creates investor skepticism that MPLX has avoided. Where Energy Transfer pursues transformational deals, MPLX focuses on strategic bolt-ons. Where Energy Transfer leverages aggressively, MPLX maintains conservative metrics.

Kinder Morgan offers an interesting contrast—a C-corporation rather than an MLP, having consolidated its partnership structure in 2014. This simplification eliminated IDR complications and broadened their investor base to include index funds and international institutions that can't own MLPs. Yet Kinder Morgan's 2015 distribution cut to fund growth internally scarred investor trust. MPLX learned from this cautionary tale: maintain the distribution at all costs, even if it means slower growth.

The regional competitors present different challenges. In the Permian, Plains All American Pipeline and Magellan Midstream Partners control legacy crude oil systems with irreplaceable rights-of-way. In the Marcellus, Williams Companies and TC Energy dominate interstate gas transmission. In the Bakken, Oneok and Crestwood Equity Partners compete for gathering and processing volumes. MPLX must navigate these entrenched positions while leveraging its multi-basin presence for competitive advantage.

Marathon Petroleum's sponsorship provides MPLX's crucial differentiator. As America's largest refiner, Marathon offers guaranteed demand that pure-play midstream competitors lack. This anchor load enables MPLX to justify infrastructure investments that might be marginal on third-party volumes alone. The Bakken pipeline system, for instance, makes economic sense primarily because Marathon's refineries in Illinois and Michigan provide committed demand for North Dakota crude.

The infrastructure moat deserves careful analysis. Replacing MPLX's asset base would cost an estimated $30-40 billion in today's construction environment—if permits could even be obtained. A new interstate pipeline faces 5-7 years of regulatory approval, environmental challenges, and landowner negotiations. A new processing plant in the Marcellus requires air permits that Pennsylvania rarely grants. These barriers to entry make existing infrastructure increasingly valuable as production grows but new construction becomes nearly impossible.

Customer relationships reveal competitive positioning. While Marathon provides 55% of revenues, the remaining 45% comes from diverse third-party customers including major oil companies (ExxonMobil, Chevron), large independents (EOG, Continental), and hundreds of smaller producers. These relationships, many spanning decades, create switching costs beyond simple economics. Producers dedicate acreage to MPLX gathering systems, integrate their production scheduling with MPLX operations, and rely on MPLX's reliability for their own operational planning.

The contract renewal patterns tell a story of competitive strength. MPLX maintains 95%+ renewal rates on expiring contracts, often extending terms and increasing rates. This pricing power stems from the lack of alternatives—a producer can't simply switch gathering systems like changing cell phone providers. The physical connections, operational integration, and capital invested in connecting to MPLX's system create powerful lock-in effects.

Technology is becoming a competitive differentiator. While pipes and plants look similar across companies, the operational technology varies significantly. MPLX's investment in automation, predictive maintenance, and digital optimization provides cost advantages that compound over time. Their ability to remotely operate facilities, predict equipment failures, and optimize system flows reduces operating costs by an estimated 10-15% versus industry averages.

The ESG competition represents a new battlefield. As investors increasingly focus on environmental performance, midstream companies compete on methane emissions, renewable power usage, and carbon intensity. MPLX's methane intensity of 0.05% matches industry leaders, while their investment in renewable-powered compression and carbon capture readiness positions them for evolving regulations. This isn't just about social license—it's about access to capital as ESG-focused funds control trillions in assets.

Scale economics increasingly favor the largest players. MPLX can spread corporate costs across a larger asset base, negotiate better rates with suppliers, and invest in technology that smaller competitors can't afford. The industry is consolidating toward a handful of mega-players who can provide integrated services from wellhead to water. MPLX's $50 billion enterprise value places them firmly in this top tier.

The regional market dynamics create interesting competitive patterns. In the Marcellus, MPLX (through MarkWest) dominates processing but depends on interstate pipelines owned by others for market access. This creates both competition and forced cooperation—MPLX needs Williams' Transco pipeline to move gas to market, while Williams needs MPLX's processing to prepare gas for pipeline transport. These interdependencies create stable competitive equilibriums.

International competition is minimal but growing. Canadian midstream companies like TC Energy and Pembina Pipeline compete for Bakken and Rockies volumes. Mexican infrastructure development by IEnova and others could eventually compete for Permian gas flows. But the complexity of cross-border operations, regulatory differences, and currency risks limit international competition to border regions.

The competitive response to energy transition varies across players. Enterprise is investing heavily in petrochemical infrastructure, betting on growing plastics demand. Kinder Morgan is exploring renewable natural gas and hydrogen transport. Energy Transfer focuses on NGL exports to meet global petrochemical demand. MPLX's strategy balances traditional hydrocarbon infrastructure with optionality for alternative fuels, avoiding big bets while maintaining flexibility.

Acquisition competition has intensified as attractive assets become scarce. The 2024 Utica acquisition from Summit Midstream saw multiple bidders, with MPLX winning through a combination of strategic fit, operational synergies, and financial capacity. As the universe of available assets shrinks, the competition for remaining independents intensifies. MPLX's strong balance sheet and Marathon's support provide advantages, but they must compete with private equity buyers willing to pay premium valuations.

Market share analysis reveals MPLX's strong but not dominant position. In Marcellus processing, they control approximately 35% of capacity. In Midwest refined products logistics, they move about 25% of volumes. In Permian gathering, they have roughly 10% share. This diversified position provides stability—they're not overly dependent on any single region or commodity—while leaving room for growth through market share gains.

The customer satisfaction metrics, while not publicly disclosed, can be inferred from operational data. MPLX maintains 99%+ system reliability, processes gas within 0.1% of specification requirements, and resolves commercial disputes without litigation in nearly all cases. These operational metrics translate to customer loyalty that provides competitive insulation.

Competitive threats evolve constantly. Electric vehicles threaten long-term refined product demand. Renewable energy challenges natural gas power generation. Distributed energy resources could reduce pipeline requirements. Environmental opposition makes new infrastructure nearly impossible. Yet MPLX's diversified asset base, strong sponsor relationship, and financial flexibility position them to adapt better than most competitors.

The competitive moat ultimately rests on three pillars: irreplaceable infrastructure in core basins, Marathon Petroleum's anchor demand, and operational excellence that keeps customers loyal. While competitors may match one or two pillars, none combine all three as effectively as MPLX. This competitive position doesn't guarantee success, but it provides sustainable advantages that should compound over time.

X. Bear vs. Bull Case & Valuation

The investment committee room at a major pension fund crackles with tension. The energy analyst is defending her recommendation to initiate a position in MPLX, while the ESG officer challenges the wisdom of investing in fossil fuel infrastructure. The value investor sees a 7.7% yield trading at 10x EBITDA—classic deep value. The growth investor worries about stranded assets in an electrifying world. This debate, playing out in investment committees globally, captures the fundamental tension in valuing MPLX: Is it an essential infrastructure play generating utility-like returns, or a melting ice cube in an warming world?

The Bull Case: Infrastructure Scarcity Meets Energy Reality

The bullish thesis starts with a simple observation: America runs on hydrocarbons, and MPLX owns the toll roads. Despite decades of renewable investment, fossil fuels still provide 80% of U.S. energy. Natural gas generates 40% of electricity. Petroleum fuels 95% of transportation. Petrochemicals—derived from NGLs that MPLX processes—are essential for everything from medical devices to wind turbine blades. This isn't changing overnight.

The fee-based model provides remarkable stability in a volatile world. With 85% of revenues from take-or-pay contracts, MPLX collects tolls regardless of commodity prices. During 2020's negative oil prices, MPLX maintained EBITDA margins above 60%. This isn't a cyclical commodity play—it's an infrastructure business with utility-like characteristics but without regulatory rate restrictions.

Marathon Petroleum's sponsorship strength cannot be overstated. As America's largest refiner with 3 million barrels per day of capacity, Marathon provides guaranteed demand that underpins MPLX's economics. Marathon needs MPLX's logistics to operate efficiently. MPLX needs Marathon's volumes to justify infrastructure investments. This symbiotic relationship creates stability that pure-play midstream companies lack.

The infrastructure scarcity value continues appreciating. Building a new interstate pipeline today takes 5-7 years and faces fierce environmental opposition. Constructing processing plants requires air permits that are increasingly difficult to obtain. The replacement cost of MPLX's assets exceeds $40 billion—assuming you could even get permits. This scarcity premium only grows as existing infrastructure ages and new construction becomes impossible.

Natural gas demand growth remains robust despite energy transition narratives. In the Marcellus, new plants will bring MPLX gas processing capacity in the Northeast to 8.1 bcf/d and total fractionation capacity to 800 thousand bpd: Harmon Creek II, a 200 mmcf/d processing plant, was placed into operation in February. Harmon Creek III, a 300 mmcf/d processing plant and 40 thousand bpd de-ethanizer, is expected online in the second half of 2026. In the Utica basin, we are increasing utilization of existing capacity, with gas processing volumes up 50% year to date versus the same period in 2023. Gas displaces coal in power generation, supports renewable intermittency, and enables industrial reshoring. LNG exports are booming. Petrochemical demand for NGLs continues growing. MPLX is positioned to capture this growth.

The valuation remains compelling on both absolute and relative basis. At 10x EV/EBITDA, MPLX trades at a 20% discount to pipeline peers and a 30% discount to utility companies with similar business models. The 7.7% distribution yield exceeds high-yield bonds while offering tax advantages and growth potential. The 1.5x coverage ratio provides substantial safety margin. On a DCF basis, assuming just 3% annual growth, MPLX is worth $55-60 per unit.

The self-funding model eliminates capital markets dependence. With $5.4 billion in operating cash flow, MPLX can fund both distributions and growth without issuing equity or excessive debt. This self-sufficiency insulates the company from market volatility while enabling steady distribution growth—a rare combination in the MLP space.

The Bear Case: Energy Transition Meets Structural Challenges