Williams Companies: From Pipeline Builders to America's Energy Infrastructure Backbone

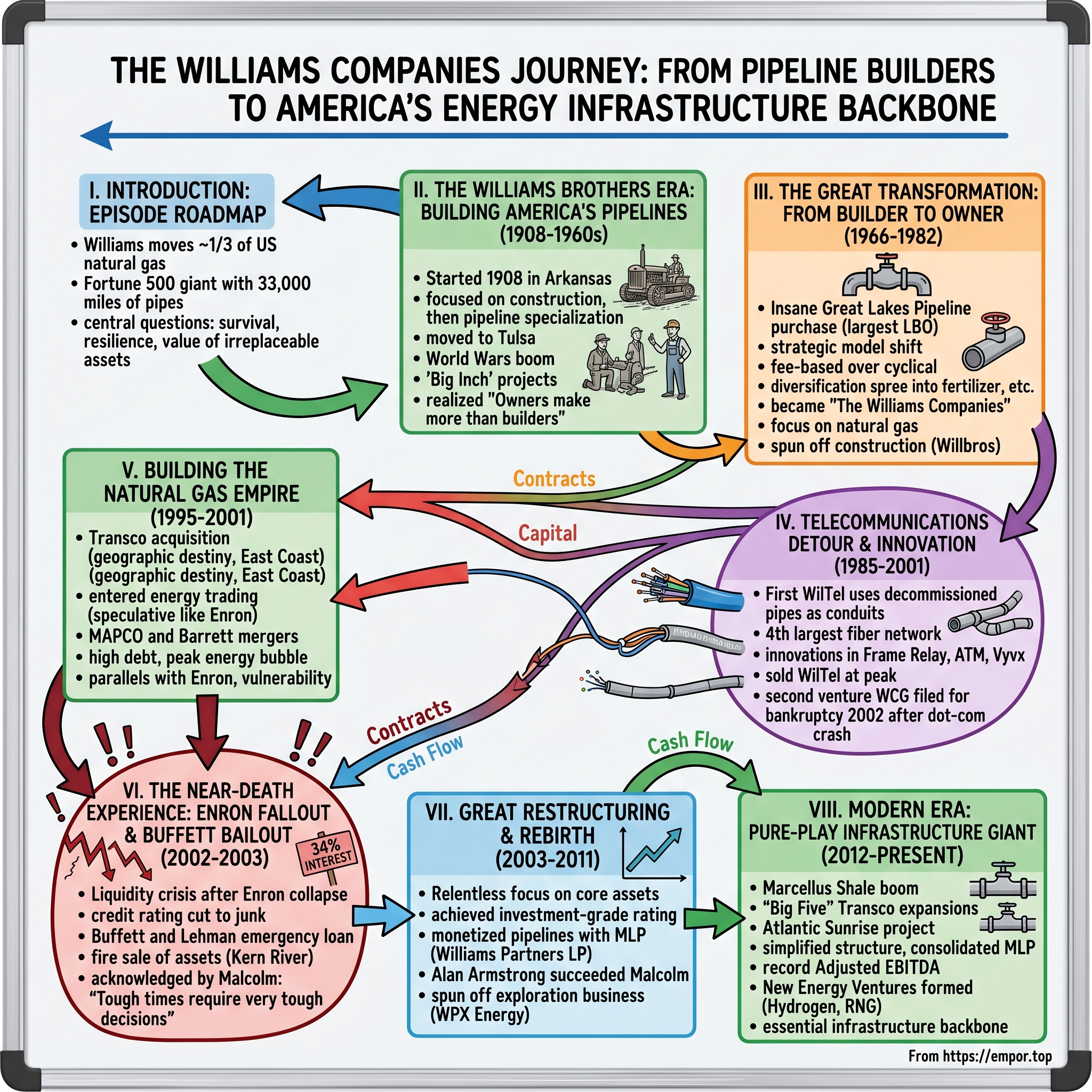

I. Introduction & Episode Roadmap

Picture this: It's 1908 in Fort Smith, Arkansas, and two brothers with calloused hands and construction equipment are about to unknowingly lay the foundation for what would become one of America's most critical energy infrastructure companies. Miller and David Williams couldn't have imagined that their modest construction business would evolve into a Fortune 500 giant operating 33,000 miles of pipelines—veins through which flows the lifeblood of American energy.

Today, Williams Companies moves about a third of the nation's natural gas, delivering half of what New York City consumes. From its headquarters in Tulsa, Oklahoma, the company has survived near-death experiences, pivoted through multiple industries, and emerged as an infrastructure backbone that powers everything from your morning coffee to the data centers running artificial intelligence models.

The central question isn't just how two brothers built a pipeline empire—it's how their company survived when it should have died, why it succeeded where giants like Enron failed, and what makes infrastructure businesses so enduringly valuable despite their capital intensity and regulatory burdens.

This is a story about family business evolution, where three generations of Williams leadership gave way to professional management. It's about infrastructure as destiny—how owning the pipes matters more than what flows through them. It's about corporate resilience, featuring one of the most expensive bailouts in American business history. And ultimately, it's about the transition from builder to owner, a strategic shift that transformed a construction contractor into an irreplaceable asset holder.

What you'll learn goes beyond Williams itself. This is a masterclass in building generational infrastructure businesses, navigating commodity cycles without getting crushed, and the art of corporate survival when the walls are closing in. We'll explore why some businesses can charge 34% interest rates in crisis (hello, Warren Buffett), why telecommunications and pipelines made strange bedfellows, and how a company can lose billions yet emerge stronger.

The themes that emerge—focus versus diversification, fee-based models versus commodity exposure, the value of irreplaceable assets—offer a playbook for understanding not just energy infrastructure, but any business built on networks, rights-of-way, and regulatory moats. Whether you're an investor evaluating infrastructure plays or an operator building for the long term, Williams' century-spanning journey offers lessons in both triumph and near-tragedy.

II. The Williams Brothers Era: Building America's Pipelines (1908–1960s)

The summer heat in Fort Smith, Arkansas, was brutal in 1908, but Miller and David Williams didn't mind. They were too busy hauling lumber, pouring concrete, and building whatever the growing frontier town needed. Their construction company started with simple projects—foundations for buildings, small bridges, local infrastructure. But within a few years, something transformative happened: oil was booming across Oklahoma and Texas, and someone needed to build the steel arteries to move it.

The Williams brothers earned a reputation that would define the company for decades: they delivered on time and on budget, no matter how challenging the terrain or weather. In an era when handshake deals mattered more than contracts, this reliability became their calling card. By 1915, they were laying pipelines across multiple states, their crews becoming experts at welding steel pipes in trenches that stretched to the horizon.

The early pivot from general construction to pipeline specialization wasn't strategic planning—it was following the money. But the brothers recognized something others missed: as America industrialized, energy transportation would become as critical as energy production. While wildcatters chased oil strikes, the Williams brothers chased the certainty of construction contracts. They weren't gambling on where oil would be found; they were betting that wherever it was found, it would need to move.

In 1919, the company made a decision that telegraphed its ambitions: relocating from Fort Smith to Tulsa, Oklahoma. Tulsa wasn't just another oil town—it was becoming the self-proclaimed "Oil Capital of the World." The move placed Williams at the epicenter of American energy development, where pipeline routes were planned, deals were struck, and fortunes were made. The brothers weren't just following their customers; they were positioning themselves at the industry's nerve center.

World War I created the first major pipeline boom. The war effort demanded massive fuel supplies, and the government contracted for coast-to-coast pipeline construction. Williams crews worked around the clock, laying what were then considered engineering marvels—pipelines that could move oil from Texas fields to East Coast refineries. The work was dangerous—welding accidents, trench collapses, equipment failures—but profitable. Each completed mile meant more reputation, more contracts, more growth.

The interwar years brought a different challenge: pipeline technology was evolving rapidly. Larger diameter pipes, better welding techniques, improved pumping stations—staying competitive meant constant investment in equipment and training. The Williams brothers proved adaptable, often being first to adopt new construction methods. They pioneered techniques for crossing rivers and mountains that competitors considered impossible. One legendary project involved laying pipe across the Arkansas River during flood season—Williams crews worked from barges, welding underwater sections while battling currents that had stopped three previous contractors.

World War II triggered an even larger boom. The government's "Big Inch" and "Little Big Inch" pipelines—emergency projects to move oil from Texas to the Northeast after German U-boats threatened tanker routes—became the largest pipeline project in history. Williams won major segments of these contracts, their crews working in shifts that never stopped, laying pipe through swamps, across mountains, under rivers. The company's ability to maintain quality while working at unprecedented speed earned commendations from the War Department.

But here's what made the Williams brothers different from their competitors: they studied every pipeline they built. While other contractors moved from job to job, Williams kept detailed records of routes, capacity, operational challenges. They were building an intellectual property database before that term existed. David Williams reportedly kept notebooks filled with observations about which routes had expansion potential, which operators ran efficient systems, which pipelines would need replacement first. They were contractors thinking like owners, even though ownership seemed impossibly capital-intensive.

The family dynamics added another layer of complexity. Miller handled operations—he could calculate pipe stress tolerances in his head and knew every foreman by name. David managed finances and relationships, charming bankers in Tulsa while negotiating with oil executives. Their complementary skills created a balanced leadership that avoided the power struggles that destroyed many family businesses. When Miller's son John joined in the 1930s, he brought engineering expertise from Oklahoma University. When David's son David Jr. arrived in the 1940s, he added financial sophistication from his time on Wall Street.

By the 1950s, Williams Brothers Company (as it was then known) had built thousands of miles of pipelines across America. They'd worked for every major oil company, constructed pipelines that became industrial landmarks, and accumulated knowledge that money couldn't buy. But the brothers faced a strategic crossroads: construction was profitable but cyclical. When oil prices dropped or pipeline building slowed, revenues evaporated. They needed steadier cash flows, better margins, something more sustainable than project-based work.

The 1957 decision to go public under the Williams Brothers name wasn't just about raising capital—it was about institutional permanence. The brothers were aging, the next generation needed resources to compete with larger contractors, and public markets offered both capital and discipline. The IPO valued the company at $15 million, modest by today's standards but substantial for a regional contractor. More importantly, it forced professionalization: formal board meetings, audited financials, strategic planning beyond the next contract.

The late 1950s brought a revelation that would reshape Williams' future. During a pipeline project for Great Lakes Pipeline Company, David Jr. studied the owner's financials. The pipeline owner earned steady fees regardless of oil prices, maintenance was predictable, and the asset would generate cash for decades. Meanwhile, Williams Brothers had built the pipeline for a one-time payment, shouldered all construction risk, then moved on. The math was clear: owners made more than builders, and their returns were more predictable.

This realization coincided with industry consolidation. Major oil companies were buying their contractors or squeezing margins through competitive bidding. Smaller contractors were failing. Williams needed a new model, and the leadership—now including second-generation family members—began planning a transformation that would have seemed impossible to those two brothers sweating in Fort Smith fifty years earlier. They would stop just building pipelines and start owning them.

III. The Great Transformation: From Builder to Owner (1966–1982)

The boardroom in Tulsa was thick with cigarette smoke in early 1966 when John Williams, now president, laid out what seemed like an insane proposition. Williams Brothers would buy Great Lakes Pipeline Company—the very pipeline system they'd helped build—for $287 million. The room went silent. The company's entire market value was barely $50 million. This wasn't just ambitious; it was betting the entire company on a single transaction. What made this deal revolutionary wasn't just its size—it was the largest leveraged buyout that Wall Street had ever seen. Williams Brothers' net worth in 1965 was $27 million, and the company had to borrow almost the entire amount, paying only $1.6 million of its own cash for Great Lakes Pipe Line. The debt-to-equity ratio would reach an eye-watering 160% by 1970, numbers that would make modern private equity firms nervous.

But John Williams saw what others missed. Great Lakes had been founded in 1930 by a consortium of eight major oil companies to service the Midwest, but a recent federal consent decree limiting profit to seven percent convinced the owners their resources were better spent elsewhere. For the oil majors, a 7% regulated return was pocket change. For Williams, it was predictable gold.

The strategic brilliance lay in the business model transformation. As contractors, Williams faced feast-or-famine cycles—in 1963 the company lost $4 million on domestic operations, with only strong overseas business limiting the overall net loss to $500,000. But pipeline ownership offered something revolutionary: customers paid whether they shipped product or not through take-or-pay contracts, maintenance was predictable, and the asset would generate cash for decades.

The integration challenges were immense. Williams went from managing construction crews to operating 6,228 miles of pipe and 20 terminals—the longest petroleum products pipeline network in America. They had to learn dispatch operations, terminal management, regulatory compliance. John Williams reportedly spent months traveling the pipeline route, meeting with terminal managers, understanding bottlenecks, learning the operational intricacies that construction never revealed.

But success bred ambition—and this is where the story gets complicated. Rather than focusing solely on pipeline operations, Williams embarked on a diversification spree that would have made 1960s conglomerates proud. By 1970, the company was manufacturing fertilizer through Gulf Oil's former agrichemical operations. By 1972, they'd acquired Agrico Chemical Company, becoming one of America's largest fertilizer producers. They bought steel companies, developed commercial real estate, even operated retail stores.

The logic seemed sound: vertical integration and countercyclical hedging. When energy was down, chemicals might be up. When pipelines needed steel, why not own the supplier? But each acquisition brought complexity, management challenges, and more debt. The company that had been laser-focused on pipeline construction was now managing disparate businesses with different economics, cultures, and capital needs.

The company changed its name to "The Williams Companies" in 1971 to reflect this new diversity—plural "Companies" signaling the conglomerate ambition. But by the late 1970s, cracks were showing. The fertilizer business was brutally cyclical, real estate development consumed capital, retail operations distracted management. Interest rates were rising, making the debt burden heavier.

The company's salvation came from an unlikely source: deregulation of natural gas markets. The Natural Gas Policy Act of 1978 began opening opportunities for pipeline companies to expand beyond their traditional regulated utility model. Williams' leadership, now including third-generation family members and professional managers, recognized that natural gas—not petroleum products—represented the future.

In 1982, Williams expanded into natural gas transportation with the purchase of Northwest Energy Company, marking the beginning of what would become a nationwide natural gas pipeline system. This wasn't just adding another pipeline; it was a fundamental strategic pivot. Natural gas was cleaner than oil, demand was growing from power generation and industrial users, and the regulatory environment was becoming more favorable.

The Northwest Energy acquisition brought 7,000 miles of natural gas pipelines serving the Pacific Northwest and Rocky Mountain regions. More importantly, it brought expertise in natural gas operations, which differed significantly from petroleum products. Gas required compression stations instead of pump stations, different safety protocols, and complex balancing of supply and demand in real-time.

Williams also made a prescient decision in 1975: spinning off the pipeline construction business as Willbros. The company's last construction project included sections of the Trans Alaska Pipeline—a fitting capstone to nearly seven decades of building America's energy infrastructure. But the message was clear: Williams was no longer a builder. It was an owner, an operator, an infrastructure company.

The transformation from builder to owner fundamentally changed Williams' economics. Construction revenues were lumpy and unpredictable—a big project one year, drought the next. But pipeline ownership generated steady cash flows through long-term contracts. Shippers committed to pay for capacity whether they used it or not. The assets, once built, required maintenance but not constant capital investment. And most importantly, the barriers to entry were enormous—nobody was going to build competing pipelines along the same routes.

By 1982, Williams had completed its metamorphosis. The company that started with two brothers and some construction equipment now owned critical energy infrastructure spanning the continent. The diversification into chemicals and retail would eventually be unwound, but the core insight—that owning infrastructure beats building it—would guide Williams for the next four decades. The stage was set for the next chapter: an unlikely detour into telecommunications that would showcase both the opportunities and dangers of infrastructure ownership.

IV. The Telecommunications Detour & Innovation (1985–2001)

The conference room at Williams headquarters in 1985 was filled with skeptical faces as an engineer explained his crazy idea: what if we ran fiber optic cables through our decommissioned pipelines? The board members exchanged glances—they were an energy company, not AT&T. But the engineer persisted, pulling out maps showing Williams' pipeline routes connecting major cities. "We already have the hardest part," he argued. "The rights-of-way. "The idea came from Roy Wilkens, then president of Williams Pipeline Co., who after attending a Harvard University program for mid-career executives, was inspired to start the new subsidiary. The Williams Companies committed $50 million to the project and within four years, through construction projects and acquisitions, WilTel had built approximately 11,000 miles of network to become the fourth largest digital fiber optic network in the United States.

"We really knew nothing about the telecommunications industry," Wilkens later confided. It was a stunning admission for someone who'd just convinced his board to invest millions in fiber optics. But Williams had something more valuable than telecom expertise: thousands of miles of decommissioned pipelines sitting idle, already possessing the most expensive component of any telecommunications network—the rights-of-way.

The genius was in the simplicity. Obtaining permits to dig trenches across the country for fiber optic cables could take years and cost billions. Williams already had the trenches, the permits, the easements. In 1985, the company began turning decommissioned petroleum pipelines into conduits for fiber optic cable. The steel pipes that once carried oil now protected fragile glass fibers carrying data at the speed of light.

WilTel was able to exploit two key industry drivers: fiber technology had just entered the scene commercially, and deregulation had led to the breakup of AT&T, creating opportunities for other long-distance carriers. The timing was perfect. Corporate America was hungry for alternatives to AT&T's monopoly pricing, and WilTel's network offered both redundancy and competitive rates.

WilTel early on provided a surprising challenge to industry giants AT&T, MCI, and Sprint. WilTel Network Services, set up in 1990, geared its fiber optic network to medium- and high-end business customers, providing reliable, highly secure private lines and data network solutions. The company wasn't trying to serve residential customers—it was cherry-picking the most profitable corporate accounts with dedicated, high-bandwidth connections.

The innovation didn't stop at repurposing pipelines. WilTel was the first carrier to put traffic on a public network frame relay overlay in early 1991 and offered limited ATM service by fall 1993, ahead of both AT&T and MCI. These weren't incremental improvements—they were generational leaps in how data moved across networks. Frame relay and ATM (Asynchronous Transfer Mode) enabled the kind of high-speed, reliable data transmission that would eventually make the internet explosion possible.

Williams also pioneered another breakthrough that revolutionized broadcasting. In 1990, a WilTel business unit, Vyvx, broke ground by using fiber optics to transmit video of Super Bowl XXIV from New Orleans to CBS. Before this, live television relied on satellites, which were expensive, weather-dependent, and introduced noticeable delays. Fiber optic transmission was instantaneous, crystal-clear, and reliable. Within years, every major sporting event and news broadcast would rely on fiber networks Williams had helped pioneer.

But success attracted attention, and not all of it was welcome. Long Distance Discount Service (LDDS) made a move to buy the company for $2 billion, but WilTel initially staved off the takeover, then agreed to sell in January 1995 for $2.5 billion in cash—about 28 times WilTel's earnings. The sale price represented a staggering return on Williams' $700 million total investment in building WilTel.

The deal came with a catch: Williams signed a three-year non-compete agreement with LDDS (which later became WorldCom, then MCI WorldCom), restricting WilTel from providing any tariff-based pure voice and data services. But Williams was clever. They retained a single strand of the 24-strand optical fiber through the 11,000-mile network, which they turned over to their newly created WilTech Group.

This single strand became the seed of Williams' second telecommunications venture. When the non-compete expired in 1998, Williams was ready. They'd spent three years planning, and by 1999 had rebuilt a network spanning 19,500 miles, with plans to reach 125 cities by 2000. The company created Williams Communications Group, combining various telecom assets and positioning for another run at the telecommunications market.

The timing seemed perfect—again. The dot-com boom was creating insatiable demand for bandwidth. Internet traffic was doubling every few months. Williams Communications went public in October 1999, with the parent company retaining 86% ownership. The IPO valued the communications unit at billions, and Williams looked like a genius for getting back into telecom.

But this second act would end in tears. Williams Communications was spun off in 2001, filed for bankruptcy the following year with $7.15 billion in debt, adopted the name WilTel Communications, and ultimately was acquired by Level 3 Communications. The dot-com crash had eviscerated demand for bandwidth, turning what seemed like valuable fiber networks into stranded assets.

The telecommunications detour offers a case study in both innovation and timing. Williams showed remarkable foresight in recognizing that decommissioned pipelines could house fiber optics—a insight that helped launch America's digital infrastructure. The first WilTel venture, sold at the peak of telecom optimism, generated extraordinary returns. But the second venture, launched into the teeth of the dot-com bubble, became a cautionary tale about the dangers of chasing yesterday's success.

The irony is striking: Williams helped build the physical infrastructure that enabled the internet revolution, generated billions in value, yet ultimately couldn't sustain a telecommunications business. The lesson was clear—being an infrastructure innovator didn't guarantee success as an infrastructure operator, especially in an industry as volatile as telecommunications. Williams would return to its roots in energy, but the scars from the telecom implosion would contribute to the near-death experience that was just around the corner.

V. Building the Natural Gas Empire (1995–2001)

While Williams was making headlines with fiber optics in the mid-1990s, a quieter revolution was happening in the company's core energy business. In a Houston boardroom in 1995, Williams executives were finalizing what would become the company's most important acquisition since Great Lakes Pipeline three decades earlier. Transco Energy Company was on the block, and its 10,000-mile pipeline system represented the missing piece in Williams' continental puzzle. The acquisition of Transco Energy Company expanded Williams' natural gas transportation system to the East Coast and established the company as one of the nation's largest-volume transporters of natural gas, now delivering about half of the natural gas consumed in New York City. The deal wasn't just about adding miles of pipeline—it was about geographic destiny. The Transco pipeline safely and reliably delivers natural gas through a 10,000-mile interstate transmission pipeline system extending from south Texas to New York City.

Transco represented the crown jewel of natural gas pipelines, a system that had been built over decades to connect the prolific gas fields of the Gulf Coast with the energy-hungry markets of the Eastern seaboard. For Williams, which had strong positions in the West and Midwest through Northwest Pipeline and other assets, Transco filled the critical gap in their continental coverage. The combined system would touch every major natural gas market in America.

The strategic timing was impeccable. Natural gas was becoming the fuel of choice for new power generation—cleaner than coal, more flexible than nuclear, cheaper to build than renewables. The Clean Air Act amendments of 1990 had tightened emissions standards, making gas-fired power plants increasingly attractive. Williams was positioning itself to benefit from a generational shift in America's energy mix.

But the late 1990s also marked Williams' entry into a dangerous new arena: energy trading. Enron's spectacular success had convinced Wall Street that energy companies needed trading desks to complement their physical assets. Williams Energy Marketing & Trading was born, initially focused on optimizing the company's pipeline capacity but quickly expanding into speculative trading.

The trading floor in Tulsa grew from a handful of schedulers to hundreds of traders. Williams wasn't content to just move gas through pipes—they wanted to arbitrage price differentials, trade derivatives, create structured products. The profits were intoxicating. In good quarters, trading income rivaled or exceeded income from the physical assets that had taken decades to build.

In 1998, Williams merged with MAPCO for $3 billion, adding refineries, convenience stores, and more pipelines. The deal epitomized the era's thinking: bigger was better, diversification reduced risk, synergies would materialize. But it also added complexity and debt at exactly the wrong moment. The company was becoming unwieldy, with businesses ranging from pipelines to telecommunications to retail gasoline sales.

In 2001, the company narrowed its focus back to energy, exited the telecommunications business, and acquired Barrett Resources, adding significant natural gas reserves, primarily in the western United States. The Barrett acquisition for $2.8 billion seemed to complete Williams' transformation into a fully integrated natural gas company—production, gathering, processing, transportation, and marketing. On paper, it was a powerful combination.

But the Barrett deal was funded primarily with debt, coming at the peak of the energy bubble. Natural gas prices were near historic highs, making Barrett's reserves look incredibly valuable. Williams was essentially making a massive bet on continued high gas prices, using borrowed money, while simultaneously ramping up its trading operations to Enron-like proportions.

The parallels with Enron were becoming uncomfortable. Both companies had started as pipeline operators. Both had diversified into trading. Both were using increasingly complex financial structures to fund growth. Both were beloved by Wall Street analysts who saw trading profits as evidence of management brilliance rather than elevated risk-taking.

By late 2001, Williams looked unstoppable. The company operated one of America's largest natural gas pipeline networks, owned significant production assets, had a booming trading operation, and still maintained its stake in Williams Communications (though that was becoming problematic as the telecom bubble burst). Revenue had grown from $6 billion in 1997 to over $10 billion in 2001.

But beneath the surface, cracks were forming. The trading operation was taking increasingly large positions. Debt levels were climbing toward dangerous territory. The company's credit rating was under pressure. And most ominously, Enron—the company Williams had been trying to emulate—was beginning its death spiral. The collapse of Enron in December 2001 would trigger a crisis of confidence in energy trading that would nearly destroy Williams.

The irony was cruel: Williams had spent the 1990s building exactly the kind of integrated natural gas empire that should have thrived in the 21st century. The Transco acquisition was strategically brilliant. The focus on natural gas was prescient. But the company's ambitions in trading and its appetite for debt-funded growth had created vulnerabilities that would soon be ruthlessly exposed. The stage was set for one of the most dramatic near-death experiences in American corporate history.

VI. The Near-Death Experience: Enron Fallout & The Buffett Bailout (2002–2003)

The call came at 2 AM on a Sunday morning in July 2002. Williams' CFO was being told that the company's commercial paper—short-term debt that funded daily operations—couldn't be rolled over. Without that funding, Williams couldn't pay its bills. A company that had survived nearly a century, that operated critical American infrastructure, was days away from bankruptcy. The collapse began with Enron's December 2001 bankruptcy, which sent shockwaves through energy markets. Williams' trading desk, which had been generating hundreds of millions in profits, suddenly faced massive losses as counterparties disappeared and liquidity evaporated. The company found itself in financial distress due to changed market conditions, its competition with Enron Corp., and the large debt of its subsidiary Williams Communications Group.

By spring 2002, the situation was desperate. Williams' credit rating had been slashed to junk status. The commercial paper market—where companies borrow for 30-90 days to fund operations—was closed to them. Banks that had eagerly lent billions were now demanding repayment. The stock price, which had peaked above $40 in 2001, crashed below $5.

The numbers were staggering: Williams had $15 billion in debt, its telecom subsidiary was hemorrhaging cash, energy trading losses were mounting, and credit markets had completely lost faith. Rating agencies were threatening further downgrades. Without immediate cash, the company would default on bond payments, triggering cross-default provisions that would bring down the entire enterprise.

Troubled energy firm Williams Cos. received $3.4 billion in financing to help stave off bankruptcy, but the terms were brutal. The centerpiece was a whopping 30 percent interest rate on a $900 million loan from Warren Buffett's Berkshire Hathaway Inc. and investment bank Lehman Brothers—actually, the effective rate was even higher.

The actual terms were even more punishing than the headline suggested. Buffett's firm would walk away with a final $1.17 billion payment on a $900 million loan that carried a 34% interest rate, plus additional fees and collateral. The one-year loan carried an interest rate of 19.824 percent, plus a "deferred set up fee" of at least 15 percent ($135 million), totaling nearly 35 percent in interest and charges for a one-year loan.

But Buffett wanted more than just interest. Williams agreed to pay 34% interest and pledge its valuable Rocky Mountain energy assets as collateral for an emergency 364-day loan. These weren't just any assets—they were Williams' crown jewels, including interests in producing gas fields and gathering systems that generated steady cash flow.

The negotiations were humiliating. Williams executives flew to Omaha, essentially begging for mercy. Buffett, sitting in his modest office, knew he held all the cards. The company needed cash immediately or would face bankruptcy within days. At the time, the Tulsa-based energy giant was desperate for cash to pay its debts and was flirting with bankruptcy. The high interest rate was unavoidable. "Despite the cost, this was clearly a necessary step. Tough times require very tough decisions. This financing came at a critical time in the life of our company."

Williams also had to accept crushing covenants: minimum liquidity requirements, restrictions on dividends, limitations on capital expenditures, and prohibitions on asset sales without lender approval. The company essentially handed control to its creditors. Every major decision would require permission. Management was reduced to caretakers of assets that creditors effectively owned.

The broader financing package included $2 billion in bank credit facilities, but even these came with onerous terms. Banks that had once competed to lend to Williams now demanded security interests, tight covenants, and regular financial reporting. The company had to provide weekly liquidity reports, monthly financial statements, and submit to lender inspections.

Meanwhile, Williams was conducting a fire sale of assets. The company sold its interest in Northern Border Partners for just $12 million—a fraction of what it had been worth years earlier. Canadian natural gas plants went for $540 million. Every sale was at distressed prices, with buyers knowing Williams had no negotiating leverage.

The human cost was enormous. Williams employed 12,000 people worldwide, including 3,000 in Tulsa. Asset sales would eliminate 4,000 jobs. Employees who had built careers at Williams, who held company stock in retirement accounts, watched their futures evaporate. The Tulsa community, where Williams had been a pillar for decades, faced the potential loss of a headquarters and major employer.

What made the crisis particularly painful was that Williams' core assets—its pipelines—remained valuable and profitable. Natural gas was still flowing, customers were still paying. But the company had borrowed too much, diversified too broadly, and when confidence evaporated, even good assets couldn't save them from a liquidity crisis.

Williams CEO Steve Malcolm acknowledged the severity: "This group's demonstrated faith in Williams' fundamental strengths and, importantly, our future, helped us weather a severe financial crisis." One money manager noted, "Last July, Williams had to make a trip to the emergency room."

The lesson was brutal but clear: in a liquidity crisis, asset quality doesn't matter if you can't access cash. Williams owned irreplaceable infrastructure worth tens of billions, but nearly went bankrupt because it couldn't roll over short-term debt. The company that had survived the Great Depression, two world wars, and multiple energy crises almost died because of a confidence crisis triggered by association with Enron's collapse.

Buffett, meanwhile, demonstrated his famous principle of being "greedy when others are fearful." His loan to Williams wasn't charity—it was opportunistic investing at its most aggressive. He walked away with $1.17 billion on a $900 million loan, plus the valuable Kern River pipeline that was snatched up for a song in early 2002. For Williams, it was expensive survival. For Buffett, it was exactly the kind of distressed opportunity that builds fortunes.

VII. The Great Restructuring & Rebirth (2003–2011)

Steve Malcolm stood before employees in Williams' Tulsa auditorium in late 2003, his message simple but powerful: "We survived. Now we rebuild." The company had just paid off Buffett's usurious loan, using proceeds from asset sales and new financing at merely painful rather than catastrophic rates. The near-death experience was over, but Williams was a shadow of its former self—stripped of assets, burdened with debt, its reputation in tatters. The restructuring strategy was clear: focus relentlessly on natural gas infrastructure, sell everything else, pay down debt, and earn back Wall Street's trust. Malcolm and his team executed with discipline that would have made military commanders proud. Every asset was evaluated through a simple lens: Is it core to natural gas transportation and processing? If not, it was for sale.

The company executed a plan to rebuild its financial strength by focusing on core world-class natural gas assets, selling billions in assets and reducing long-term debt. But what made this restructuring remarkable was what Williams didn't do—they continued to pay quarterly dividends without interruption since 1974. Even at the depths of the crisis, when every dollar mattered, the board maintained the dividend. It was a signal: Williams would survive and thrive again.

The asset sales were surgical. Gone were the refineries acquired with MAPCO. Sold were the convenience stores, the electricity generation assets, the remaining international operations. Each sale brought cash to pay down debt, but also simplified the business. Williams was returning to what it knew best: moving natural gas through pipes.

By 2007, after four years of grinding restructuring, Williams achieved something that seemed impossible during the dark days of 2002: return to investment-grade credit rating. The psychological impact was enormous. Investment-grade status meant access to capital markets at reasonable rates, the ability to compete for major projects, and validation that the turnaround was real.

The financial engineering during this period was sophisticated. In 2010, the company underwent a major restructuring that included reorganization of its extensive pipeline holdings in Williams Partners LP. This master limited partnership (MLP) structure was brilliant: it allowed Williams to monetize its stable, fee-based assets while maintaining control. The MLP paid high distributions to investors seeking yield, while Williams retained the general partner interest and operational control.

The MLP structure also created a powerful growth vehicle. Williams could "drop down" assets from the parent company to the MLP at attractive valuations, generating cash for the parent while growing distributions at the MLP. It was financial engineering that actually made operational sense, unlike the complex derivatives that had nearly destroyed the company.

Leadership transition marked the end of this era. In October 2010, Williams and Williams Partners LP announced that chairman and chief executive officer Steve Malcolm would retire at the end of the year. Malcolm had saved the company, but it was time for new leadership to drive growth. The board elected Alan Armstrong to succeed Malcolm as CEO effective January 3, 2011.

Armstrong wasn't an outsider brought in to shake things up—he had served as senior vice president of Williams since 2002, living through the crisis and restructuring. He joined Williams in 1986 as an engineer, working his way up through operations. This was someone who understood pipelines, compressor stations, and gas processing plants at a technical level, but who had also proven himself as a strategic thinker during the turnaround.

His appointment signaled continuity but also ambition. Armstrong had led the company's North American midstream businesses through a period of growth, even during the restructuring. He understood that Williams had spent years playing defense—now it was time to play offense.

Almost immediately, Armstrong faced a strategic decision that would define his early tenure. On February 16, 2011, Williams' board approved pursuing a plan to separate the company's businesses into two stand-alone, publicly traded corporations. The exploration and production business would be spun off as WPX Energy, allowing Williams to become a pure-play midstream company.

The spinoff logic was compelling. The E&P business had different capital needs, risk profiles, and investor bases than the midstream business. E&P was volatile, dependent on commodity prices, capital-intensive. Midstream was stable, fee-based, infrastructure-focused. By separating them, each could pursue optimal strategies and attract appropriate investors.

The separation was completed December 31, 2011, with the distribution of one share of WPX Energy common stock for every three shares of Williams common stock. Williams retained no interest in WPX, making a clean break. The company that had spent decades diversifying was now more focused than ever: a pure-play natural gas infrastructure company.

The numbers told the story of successful restructuring. Debt had been reduced from crisis peaks. The company had investment-grade ratings from all major agencies. Cash flow was growing steadily. The dividend, never cut even in crisis, was increasing. Williams had not just survived—it had been transformed.

The cultural transformation was equally important. The company that had chased Enron's trading profits was now proudly boring. Steady cash flows from long-term contracts were celebrated. Disciplined capital allocation replaced aggressive expansion. Risk management became paramount. The scars from 2002 created an institutional memory that valued stability over growth at any cost.

But Armstrong and his team weren't content with mere stability. They saw massive opportunity ahead. The shale revolution was transforming American energy, creating need for new infrastructure. Natural gas was replacing coal in power generation. LNG exports were becoming reality. Williams, with its continental pipeline network and hard-won financial strength, was perfectly positioned for the next chapter.

The lesson from this period was profound: sometimes near-death experiences create stronger companies. Williams emerged from restructuring with better assets (focused on natural gas), better structure (the MLP provided growth capital), better management (battle-tested and disciplined), and better strategy (fee-based, long-term contracts). The company that Buffett had charged 34% interest was now investment-grade. The company that almost went bankrupt was now paying growing dividends. The resurrection was complete.

VIII. Modern Era: Pure-Play Infrastructure Giant (2012–Present)

Alan Armstrong looked out at the Marcellus Shale from a helicopter in 2012, seeing not just wells and rigs but the future of American energy. Below him, the landscape of Pennsylvania was being transformed by the shale revolution, and Williams was building the infrastructure to connect this bounty to markets across the continent. "We're not betting on gas prices," he told his team. "We're betting that America will need to move gas from where it's produced to where it's consumed. "Williams became an infrastructure company with many pipeline assets held through master limited partnership Williams Partners LP, but the structure would evolve. In 2014, Williams placed Transco's "Big Five" expansion projects into service, increasing capacity on the pipeline by 25%. These weren't just maintenance projects—they were transformative expansions that positioned Transco as the superhighway of American natural gas.

The Atlantic Sunrise project epitomized Williams' modern strategy. This nearly $3 billion expansion of the existing Transco natural gas pipeline connected abundant Marcellus gas supplies with markets in the Mid-Atlantic and Southeastern U.S., placed into full service in 2018. The historic project increased the design capacity of the Transco pipeline by 1.7 billion cubic feet per day (approximately 12 percent) to 15.8 billion cubic feet per day, further strengthening and extending the bi-directional flow of the Transco system.

What made Atlantic Sunrise remarkable wasn't just its scale but its strategic importance. The project created a superhighway from the Marcellus—America's most prolific gas field—to demand centers along the Eastern seaboard. It connected supply with the Cove Point LNG facility, enabling American gas to reach global markets. During peak construction, the project directly employed approximately 2,300 people in 10 Pennsylvania counties and supported an additional 6,000 jobs in related industries, generating up to $1.6 billion in economic activity.

In 2018, Williams made another pivotal decision: acquiring the remaining interest in Williams Partners. The MLP structure had served its purpose during recovery, but market conditions had changed. MLP valuations had collapsed, and the complexity of the structure was becoming a hindrance rather than help. By simplifying to a single entity, Williams eliminated conflicts of interest, reduced costs, and made the company easier for investors to understand.

Recent major Transco pipeline expansions demonstrate the company's continued growth: Southeast Energy Connector in Alabama (150 MMcf/d) and Texas to Louisiana Energy Pathway (364 MMcf/d) to support Gulf Coast energy infrastructure and LNG exports. The Transco pipeline system achieved record-breaking transmission volumes with system-design capacity now exceeding 20 Bcf/d, transporting approximately 20% of U.S. natural gas production.

The modern Williams runs a 33,000-mile pipeline network that moves about a third of the country's natural gas. The business is built on long-term, take-or-pay contracts that provide stable, predictable cash flows regardless of commodity price volatility. Record Adjusted EBITDA of $7.08 billion in 2024, with 2025 guidance of $7.45–7.85 billion, reflects EBITDA growing at an 8% annual clip.

The company's four business segments reflect its comprehensive approach: Transmission & Gulf of America (including Transco, Northwest Pipeline, and MountainWest pipelines), Northeast G&P (serving Marcellus/Utica), West (Rocky Mountain, Barnett, Eagle Ford, Haynesville, Anadarko, Permian), and Gas & NGL Marketing Services. Each segment benefits from irreplaceable assets, long-term contracts, and strategic positioning in growing markets.

Growth drivers are compelling and multiplying. Surging U.S. natural gas demand from LNG exports has transformed America from gas importer to one of the world's largest exporters. The growing need for gas-powered electricity, driven by data centers, AI computing, and electrification of transportation, creates decades of demand growth. Natural gas's role as the transition fuel—cleaner than coal, more reliable than renewables, faster to build than nuclear—positions Williams perfectly.

In 2020, Williams formed the New Energy Ventures team, focusing on advancing innovative technologies, markets, and business models. This isn't abandoning natural gas but preparing for its evolution. Hydrogen production, renewable natural gas from landfills and agricultural waste, carbon capture and sequestration—all leverage Williams' existing infrastructure and expertise.

Recent acquisitions show strategic focus. In 2021, the company acquired Sequent Energy Management, accelerating natural gas pipeline and storage optimization. In 2024, Williams acquired a portfolio of natural gas storage assets from Hartree Partners for $1.95 billion, including six underground storage facilities in Louisiana and Mississippi with 115 Bcf capacity—critical for managing the intermittency of renewable power and serving LNG export facilities.

The transformation from near-bankruptcy to infrastructure giant is complete. Williams shares jumped 34.6% from July 2024 to July 2025, easily outpacing the S&P 500's 18.4% gain. Wall Street is generally optimistic: 8 out of 15 recent analyst ratings are Buys with average price targets suggesting further upside. Institutional ownership at 86.4% reflects confidence from sophisticated investors.

The company that Buffett nearly left for dead has become essential infrastructure for American energy. The fee-based model provides recession-resistant cash flows. The growth projects are visible and contracted. The balance sheet, while leveraged, is manageable with investment-grade ratings. Williams has transformed from a company trying everything to a company doing one thing exceptionally well: moving natural gas from where it's produced to where it's needed.

The lesson from this modern era is profound: sometimes the best strategy is the simplest. Williams doesn't drill for gas, doesn't bet on prices, doesn't trade derivatives. It owns pipes, compressors, and processing plants. It charges fees for moving molecules. It invests in expansions backed by long-term contracts. This boring, predictable model has created extraordinary value. The company that chased Enron's complexity has found success in simplicity.

IX. Business Model & Competitive Position

Walking through Williams' operations center in Houston, you see dozens of screens showing real-time gas flows, pressure readings, and system alerts across 33,000 miles of pipeline. Controllers can redirect gas flows with a few keystrokes, balancing supply and demand across a continental network. But the real power isn't in the technology—it's in the business model that turns steel pipes into profit machines. The business is built on long-term, take-or-pay contracts that generate predictable cash flows regardless of throughput. When a customer signs a contract for pipeline capacity, they pay whether they use it or not. This transforms volatile commodity businesses into stable infrastructure returns. Record Adjusted EBITDA of $7.08 billion in 2024, with 2025 guidance of $7.45–7.85 billion, demonstrates the model's power.

Williams operates through four distinct but complementary segments. Transmission & Gulf of America, anchored by the Transco, Northwest Pipeline, and MountainWest systems, generates the majority of earnings through firm transportation contracts. These are typically 10-20 year agreements with creditworthy utilities and LNG exporters. The segment benefits from FERC-regulated returns that provide inflation protection and recovery of capital investments.

Northeast G&P focuses on the Marcellus and Utica shale regions, operating gathering systems that collect gas from wellheads and processing plants that separate natural gas liquids. This segment uses a mix of fee-based and commodity-based contracts, with increasing emphasis on fixed-fee arrangements to reduce volatility. The strategic positioning in America's most prolific gas basin provides decades of growth visibility.

The West segment operates across Rocky Mountain, Barnett, Eagle Ford, Haynesville, Anadarko, and Permian basins. These assets benefit from diverse geology and multiple commodity streams—dry gas, NGLs, and oil-related gas. The geographic diversity reduces dependence on any single basin's production trends.

Gas & NGL Marketing Services provides optimization around Williams' physical assets. This isn't the speculative trading that nearly destroyed the company in 2002—it's using market knowledge and storage capacity to capture seasonal spreads and location differentials. The segment contributes modest but stable earnings while enhancing the value of physical assets.

The competitive moats are formidable and growing stronger. Rights-of-way across private and public lands would be nearly impossible to replicate today. Environmental opposition makes new pipeline construction increasingly difficult, enhancing the value of existing infrastructure. FERC certificates for interstate pipelines create regulatory barriers that protect incumbent operators.

Network effects multiply value. Each new connection—whether a power plant, LNG terminal, or industrial facility—makes the entire system more valuable. The ability to redirect gas flows, balance supply and demand, and provide reliability creates switching costs that lock in customers. A utility connected to Transco won't easily switch to another pipeline—the physical connection, operational integration, and reliability record create powerful retention.

The fee-based model provides remarkable stability. Approximately 90% of earnings come from fixed fees or regulated cost-of-service rates. Commodity price exposure is limited and often hedged. During the COVID-19 pandemic, when energy demand collapsed, Williams' earnings remained stable because customers still paid for contracted capacity.

Capital allocation follows clear priorities. Growth capital focuses on contracted expansion projects with typical returns of 5-7x EBITDA. These aren't speculative builds—projects don't proceed without long-term contracts covering the majority of capacity. Maintenance capital of approximately $600-700 million annually keeps assets operating safely and efficiently. The dividend, growing at 5-6% annually, returns cash to shareholders while maintaining financial flexibility.

The growth algorithm is compelling: GDP growth drives baseline energy demand, coal-to-gas switching adds 2-3% annual demand growth, LNG exports are growing at double-digit rates, and data center proliferation creates new power demand. Williams captures this growth through expansion projects that leverage existing corridors and systems, generating high returns on incremental capital.

Financial metrics reflect the model's strength. EBITDA margins exceed 60%, among the highest in the energy sector. Return on invested capital consistently exceeds cost of capital. Free cash flow funds both growth investments and rising dividends. The balance sheet, while leveraged at approximately 3.8x debt/EBITDA, is appropriate for stable, contracted cash flows.

Competition exists but is limited by geography and regulation. Other interstate pipelines compete for new connections, but rarely for existing customers given switching costs. Gathering and processing faces more competition, but Williams' scale and integrated systems provide advantages. The real competition isn't other pipelines—it's alternative energy sources, and natural gas's role as a transition fuel provides decades of runway.

The business model's elegance lies in its simplicity. Williams doesn't bet on commodity prices, doesn't need technological breakthroughs, doesn't face disruption from digital competitors. It owns pipes that move molecules from Point A to Point B, charging tolls regardless of the molecules' value. It's a business model that has worked for centuries—from Roman aqueducts to modern highways—and will likely work for centuries more.

Risk management is embedded in the model. Long-term contracts reduce volume risk. Investment-grade customers reduce credit risk. Geographic diversity reduces regional exposure. Multiple commodity streams reduce dependence on any single product. Regulatory frameworks provide cost recovery mechanisms. The company that nearly died from excessive risk-taking has become a case study in risk mitigation.

X. Playbook: Business & Investing Lessons

Sitting in Williams' boardroom, where crisis meetings in 2002 determined the company's survival, you can still feel the weight of those decisions. The mahogany table bears invisible scars from fists pounded in frustration, tears shed in desperation, and ultimately, agreements signed that saved the company. The lessons learned here, paid for with near-bankruptcy and 34% interest rates, offer a masterclass in business survival and transformation.

The Value of Owning vs. Building Infrastructure

Williams spent six decades building pipelines for others before discovering the superior economics of ownership. As builders, they faced feast-or-famine cycles, competitive bidding that squeezed margins, and zero residual value after project completion. As owners, they collect predictable fees for decades, benefit from inflation escalation, and hold irreplaceable assets that appreciate over time.

The math is compelling: building a pipeline might generate 10-15% margins on construction costs, paid once. Owning that same pipeline generates 8-10% annual returns on invested capital for 40+ years. The present value difference is staggering. Williams Brothers the contractor was worth tens of millions; Williams the infrastructure owner is worth tens of billions.

Surviving Existential Crises: When to Take Expensive Capital

The Buffett bailout teaches a brutal lesson: in a liquidity crisis, any capital that lets you survive is cheap capital. Williams paid effectively 34% for one-year money, terms that would make loan sharks blush. But the alternative was bankruptcy, which would have wiped out all equity value. The $270 million in excess interest paid to Buffett preserved billions in enterprise value.

The key insight: companies die from lack of liquidity, not lack of profitability. Williams had valuable assets generating positive cash flow, but couldn't access short-term funding. The lesson? Maintain multiple funding sources, extend maturities before markets close, and never assume capital markets will remain open. Pride is expensive when survival is at stake.

The Importance of Focus After Diversification Fails

Williams' journey from focused pipeline builder to conglomerate (fertilizer, retail, telecommunications) to focused midstream company illustrates the siren song of diversification. Each expansion seemed logical—vertical integration, countercyclical hedging, leveraging existing assets. But complexity compounds faster than synergies materialize.

The post-crisis focus on natural gas infrastructure wasn't just about selling non-core assets—it was about building expertise, relationships, and competitive advantages in a single domain. Depth beats breadth. A company excellent at one thing beats a company good at many things. The focused Williams generates higher returns on capital than the diversified Williams ever achieved.

Long-Term Contracts and Fee-Based Models in Commodity Businesses

The transformation from commodity exposure to fee-based revenue streams represents a fundamental risk reduction. Williams learned that commodity volatility can generate spectacular profits in good times but existential losses in bad times. The fee-based model sacrifices upside for stability—a trade-off that's created tremendous value.

The contract structure matters enormously. Take-or-pay provisions ensure payment regardless of usage. Minimum volume commitments protect against demand destruction. Escalation clauses preserve real returns. Credit requirements protect against counterparty failure. These provisions, learned through painful experience, transform volatile businesses into bond-like cash flows.

Why Infrastructure Assets Are Irreplaceable

Williams' 33,000-mile pipeline network couldn't be rebuilt today at any price. Environmental opposition, regulatory complexity, and landowner resistance make new construction nearly impossible. This isn't just about replacement cost—it's about genuine irreplaceability. The rights-of-way, permits, and social license accumulated over a century cannot be replicated.

This irreplaceability creates pricing power, competitive advantages, and terminal value that financial models struggle to capture. It's why infrastructure assets trade at premium multiples despite capital intensity. The moat isn't just wide—it's getting wider as construction becomes harder. Williams' existing assets become more valuable every time a new pipeline project fails to get permitted.

Capital Allocation Through Cycles

Williams' capital allocation history reads like a textbook of what to do and what not to do. During booms, the company often overpaid for acquisitions (Barrett Resources at the peak) and overinvested in speculative projects. During busts, it sold assets at distressed prices and underinvested in maintenance.

The lesson: countercyclical capital allocation creates enormous value but requires discipline when markets reward the opposite behavior. Buying when others are selling, investing when others are retrenching, and maintaining strategic patience when others panic—these behaviors separate great companies from merely good ones. Williams now follows strict return hurdles, requires contracted revenue before building, and maintains consistent maintenance spending regardless of market conditions.

The Power of Geographic and Customer Diversification

Williams' continental footprint provides resilience that regional operators lack. When Marcellus production disappoints, Permian volumes compensate. When industrial demand weakens, power generation fills the gap. When domestic markets soften, LNG exports provide growth. This diversification isn't about spreading bets—it's about creating a portfolio of options that ensures stability while maintaining upside exposure.

Customer diversification is equally important. Williams serves utilities, industrials, producers, marketers, and exporters. No single customer represents existential risk. This contrasts with gathering systems dependent on a single producer or pipelines serving a single power plant. Concentration risk, as Williams learned during the Enron collapse, can transform good assets into stranded assets overnight.

The Governance Revolution

The transformation from family control to professional management, accelerated by the 2002 crisis, fundamentally changed Williams' trajectory. Independent directors, separated CEO/Chairman roles, and robust risk management weren't just governance theater—they prevented the empire-building and risk-taking that nearly destroyed the company.

The board that approved 34% interest rates to Buffett had learned humility. The management that rebuilt Williams had scars from the crisis. This institutional memory, embedded in processes and culture, provides discipline that financial incentives alone cannot create. Sometimes the best governance comes from people who remember what bad governance costs.

When Infrastructure Beats Technology

Williams' telecommunications ventures offer a cautionary tale about confusing enablement with participation. Yes, decommissioned pipelines could house fiber optic cables. Yes, rights-of-way had value for telecommunications. But owning the pipes didn't mean Williams could compete with specialized telecom operators.

The lesson: stick to your core competency. Infrastructure companies should own and operate infrastructure, not try to become technology companies. The skills, culture, and capital requirements differ fundamentally. Williams' failed telecom ventures lost billions; its pipeline operations generate billions. The difference isn't luck—it's alignment between capabilities and strategy.

The Permanent Value of Temporary Advantages

Many of Williams' advantages seemed temporary. The shale revolution would end. LNG exports would plateau. Coal-to-gas switching would complete. Yet each "temporary" driver has lasted longer than expected, and new drivers emerge. Data centers need power. Hydrogen requires transport. Carbon capture needs infrastructure.

The lesson: infrastructure positioned at critical nodes captures value from multiple waves of change. Williams doesn't need to predict which energy transition scenario occurs—it benefits from any scenario requiring molecule movement. This optionality, embedded in physical assets, provides growth beyond any single trend.

The playbook that emerges from Williams' century-long journey is clear: Own irreplaceable assets. Generate contracted cash flows. Maintain financial flexibility. Focus relentlessly. Diversify strategically. Govern professionally. Allocate countercyclically. And remember—always remember—that survival trumps optimization. The company that nearly died from complexity and leverage has been reborn through simplicity and discipline. These lessons, earned through corporate near-death, offer a roadmap for building enduring value in any infrastructure business.

XI. Analysis & Investment Case

The investment case for Williams Companies presents a fascinating paradox: a company with 19th-century assets competing in a 21st-century energy transition. Yet from July 2024 to July 2025, WMB shares jumped 34.6%, easily outpacing the S&P 500's 18.4% gain. Wall Street is generally optimistic, with 8 out of 15 recent analyst ratings as Buys and an average price target of $61.77, while institutional ownership at 86.4% signals confidence from sophisticated investors.

Bull Case: Essential Infrastructure in an Energy-Hungry World

The bull thesis rests on irreplaceable assets meeting insatiable demand. Williams' 33,000-mile pipeline network cannot be replicated—environmental opposition and regulatory barriers make new construction nearly impossible. This scarcity value increases every year as permitting becomes harder and opposition grows stronger.

Natural gas demand growth appears unstoppable. LNG exports are transforming America from importer to global supplier, with export capacity expected to double by 2030. Data centers, driven by AI computing, are projected to consume 8% of U.S. power by 2030 versus 3% today. Each new data center needs reliable, 24/7 power that renewables alone cannot provide. Natural gas, providing both baseload and peaking power, becomes essential infrastructure for the digital economy.

The energy transition paradoxically benefits natural gas. Coal plant retirements require replacement baseload capacity. Renewable intermittency requires fast-ramping backup power. Hydrogen production may use natural gas as feedstock. Carbon capture could extend gas plants' useful lives. Williams wins in multiple transition scenarios.

The financial trajectory supports optimism. EBITDA growing at 8% annually from a base of $7+ billion provides visible cash flow growth. Contracted revenues with investment-grade counterparties ensure stability. The dividend, yielding approximately 3.5% and growing 5-6% annually, offers attractive total returns. With 90% of revenues fee-based, earnings remain stable regardless of commodity volatility.

Bear Case: Regulatory Risks and Transition Uncertainties

The bear thesis acknowledges current strength but questions long-term sustainability. Regulatory risk looms large—pipeline expansions depend on FERC approval, which has become increasingly difficult. State-level opposition, especially in blue states, can delay or kill projects regardless of federal approval. Environmental litigation adds years and millions in costs to any expansion.

The energy transition timeline remains uncertain. Aggressive electrification could reduce direct natural gas consumption. Renewable costs continue declining, potentially making gas-fired power uneconomic. Battery storage improvements could eliminate gas's peaking advantage. Green hydrogen could replace natural gas in industrial applications. While these transitions will take decades, market valuations could reprice much sooner.

High debt levels concern conservative investors. At approximately 3.8x debt/EBITDA, Williams carries more leverage than pipeline peers. Rising interest rates increase refinancing costs. Rating downgrades would trigger higher borrowing costs and potentially covenant violations. While manageable in normal conditions, leverage limits financial flexibility during downturns.

Execution risks on expansion projects multiply with scale. Williams has 14 major projects in development, requiring precise execution across permitting, construction, and commissioning. Delays are common, cost overruns endemic. Each stumble erodes investor confidence and returns. The company's ambitious growth plans assume flawless execution in an increasingly difficult environment.

Valuation: Premium Justified or Priced for Perfection?

Williams trades at premium valuations reflecting its quality and growth. At approximately 11x forward EBITDA, it commands multiples above slower-growing peers but below high-growth MLPs. The premium seems justified given contracted growth, strategic positioning, and execution track record. However, premium valuations leave little room for disappointment.

The DCF analysis supports current valuations assuming mid-single-digit growth and stable multiples. But sensitivity to terminal assumptions is high—small changes in long-term growth rates or discount rates significantly impact fair value. This sensitivity reflects the long-duration nature of infrastructure assets and uncertainty about energy transition timing.

Relative valuation suggests fair pricing. Williams trades in line with high-quality midstream peers on EV/EBITDA basis but at premium on P/E given higher leverage. The dividend yield matches peer averages while growth exceeds them. The market is paying for quality and growth but not excessively.

Risk-Reward: Asymmetric but Favorable

The risk-reward appears favorable for long-term investors. Downside seems limited given essential infrastructure, contracted cash flows, and dividend support. Even in recession, natural gas demand for heating and power generation remains stable. The 2020 pandemic proved the model's resilience.

Upside potential remains significant if execution continues. Data center demand could exceed expectations. LNG exports could accelerate further. Hydrogen economy could create new demand. Multiple expansion is possible if interest rates decline or energy infrastructure regains favor. A 20-30% annual return over the next 3-5 years seems achievable.

The key risks are more gradual than acute. Regulatory tightening could slow growth. Energy transition could accelerate. Competition could intensify. But these risks unfold over years, not quarters, allowing management time to adapt. Williams survived near-bankruptcy in 2002—gradual challenges seem manageable by comparison.

Catalysts and Signposts

Near-term catalysts favor bulls. Major projects coming online in 2025-2026 will drive earnings growth. LNG export facilities under construction ensure demand growth. Data center announcements continue accelerating. Natural gas prices remaining low supports demand growth while Williams' fee-based model protects margins.

Longer-term signposts require monitoring. Permitting reform could unlock growth or create barriers. Renewable deployment rates indicate transition pace. Battery storage costs determine gas plant competitiveness. Carbon pricing could help or hurt depending on design. Infrastructure legislation could provide funding or impose restrictions.

The Verdict: Quality Infrastructure at Fair Prices

Williams represents a high-quality infrastructure investment at reasonable valuations. The company owns irreplaceable assets, generates predictable cash flows, and operates in growing markets. Management has proven execution capability and capital discipline. The balance sheet, while leveraged, remains manageable.

For income-focused investors, Williams offers an attractive dividend with growth potential. For growth investors, the expansion project pipeline provides visible earnings acceleration. For ESG-conscious investors, natural gas as transition fuel offers a pragmatic approach to emissions reduction.

The investment case ultimately depends on time horizon and risk tolerance. Short-term traders face commodity volatility and regulatory headlines. Long-term investors own essential infrastructure with decades of useful life. Patient capital willing to withstand volatility should be rewarded as America's energy infrastructure needs continue growing.

Williams isn't a risk-free investment—no equity is. But it offers a compelling combination of stability and growth, income and appreciation, defensive characteristics and offensive potential. For investors seeking exposure to America's energy infrastructure transformation, Williams provides a battle-tested operator with proven assets and promising prospects. The company that nearly died in 2002 has been reborn as an infrastructure giant for the next generation.

XII. The Future & Conclusion

Standing atop Compressor Station 515 in Pennsylvania, you can hear the rhythmic pulse of turbines pushing natural gas toward markets hundreds of miles away. This mechanical heartbeat has echoed across Williams' infrastructure for over a century, but the molecules flowing through these pipes are beginning to tell a different story. The company that built its fortune moving fossil fuels is quietly positioning itself for an energy system that might look radically different in 2050.

In 2020, Williams formed the New Energy Ventures team, focusing on advancing innovative technologies, markets, and business models. This isn't a desperate pivot away from natural gas—it's a recognition that the molecules moving through pipelines will evolve. Today it's methane from shale wells. Tomorrow it might be renewable natural gas from landfills. By 2040, it could be hydrogen from electrolysis.

The beauty of Williams' position is that pipes don't care what molecules flow through them. With modifications, natural gas pipelines can transport hydrogen. Processing plants can be retrofitted for carbon capture. Storage caverns can hold hydrogen or compressed air for energy storage. The infrastructure built for fossil fuels becomes the backbone for cleaner alternatives.

Williams' low-carbon strategy isn't about abandoning natural gas—it's about extending its useful life while preparing for evolution. The company is investing in renewable natural gas projects, capturing methane from dairy farms and landfills. These projects generate premium-priced gas that counts as carbon-negative under many regulatory frameworks. It's a small business today but growing rapidly as carbon pricing and renewable fuel standards create economic incentives.

The hydrogen opportunity is more speculative but potentially transformative. Williams' pipelines could transport hydrogen blended with natural gas, initially at 5-10% concentrations, eventually at higher levels. The company's storage assets could hold hydrogen for seasonal balancing of renewable electricity. The technical challenges are significant—hydrogen embrittles steel, requires different compression ratios, and has different energy density. But Williams' engineering expertise and existing rights-of-way provide advantages in solving these challenges.

Carbon capture and sequestration represent another growth vector. Williams' Louisiana Energy Gateway project includes carbon capture infrastructure, positioning the company to transport and store CO2 from industrial facilities. The geology beneath Williams' Gulf Coast pipelines is ideal for CO2 sequestration. As carbon prices rise and capture technology improves, this could become a significant business.

The data center opportunity deserves special attention. AI's exponential growth requires massive computing power, which requires reliable electricity, which currently requires natural gas. A single large data center can consume as much power as a small city. Williams is positioning infrastructure near data center clusters, providing direct gas supply that ensures reliability. Some facilities are exploring on-site power generation, with Williams providing both gas supply and potentially handling carbon capture.

But the future isn't just about new molecules and technologies—it's about new business models. Williams is exploring energy-as-a-service offerings, providing integrated solutions rather than just transportation. Virtual pipeline services using compressed natural gas and liquefied natural gas provide energy to locations without pipeline access. Digital twins and predictive analytics optimize system operations and prevent failures before they occur.

The regulatory landscape will shape Williams' future as much as technology. Pipeline expansions depend on FERC approval, which has become increasingly politicized. State-level opposition can delay projects for years. Environmental regulations continue tightening. Carbon pricing, if implemented, could fundamentally alter energy economics. Williams' lobbying efforts and regulatory expertise become as important as engineering capability.

The geopolitical dimension adds complexity and opportunity. American LNG exports strengthen allies' energy security while generating massive demand for pipeline capacity. The Russia-Ukraine conflict highlighted the strategic importance of energy infrastructure. Williams' assets aren't just commercial infrastructure—they're components of national security. This strategic importance could provide regulatory tailwinds even as environmental pressures increase.

Climate change itself creates infrastructure challenges and opportunities. Extreme weather events stress energy systems, requiring more robust infrastructure. Hurricanes threaten Gulf Coast facilities. Drought affects hydroelectric generation, increasing gas demand. Williams must harden assets against climate impacts while benefiting from increased demand for reliable energy.

The talent challenge looms large. Williams' workforce averages over 50 years old, with critical expertise approaching retirement. Attracting young talent to fossil fuel infrastructure becomes harder as ESG concerns influence career choices. The company must balance maintaining traditional expertise while building capabilities in new technologies. The culture that rebuilt Williams after 2002 must evolve without losing hard-won discipline.

Financial evolution continues as well. The MLP structure that served Williams during recovery has been simplified. Future capital structures might include green bonds for renewable projects, sustainability-linked loans with ESG targets, or joint ventures for new technologies. The capital markets that nearly destroyed Williams in 2002 now provide multiple funding avenues for different risk profiles.

Looking ahead to 2030 and beyond, Williams faces fundamental questions. Will natural gas remain a bridge fuel or become a destination fuel? Will hydrogen economics ever compete with electrification? Will carbon capture extend fossil fuel use or prove too expensive? Will data center demand continue exponential growth or plateau? Will regulatory support or opposition determine infrastructure development?

The answers matter less than Williams' positioning to benefit from multiple scenarios. The company doesn't need to predict the future perfectly—it needs to maintain flexibility, operational excellence, and financial strength to adapt as the future unfolds. The infrastructure built for yesterday's energy system can serve tomorrow's if managed wisely.

Final Thoughts: A Century of Resilience

Williams' story, from two brothers with a construction company to a Fortune 500 infrastructure giant, embodies American industrial evolution. The company has survived world wars, depressions, boom-bust cycles, technological disruption, and near-bankruptcy. Each crisis taught lessons that strengthened the company for the next challenge.

The transformation from builder to owner created permanent value. The focus on natural gas positioned Williams for decades of growth. The fee-based model provides stability through volatility. The continental footprint offers resilience and optionality. These strategic choices, some deliberate and others forced by crisis, created today's Williams.

But past success doesn't guarantee future prosperity. The energy transition represents an existential challenge different from previous crises. This isn't about surviving a financial crisis or commodity collapse—it's about remaining relevant as the entire energy system transforms. Williams must evolve without abandoning strengths, innovate without losing focus, grow without overleveraging.

The investment case for Williams ultimately depends on believing that America will need energy infrastructure for decades to come, that natural gas will play a crucial transition role, that existing infrastructure has irreplaceable value, and that Williams' management can navigate an uncertain future. These aren't unreasonable beliefs, but they require faith in both continuity and change.