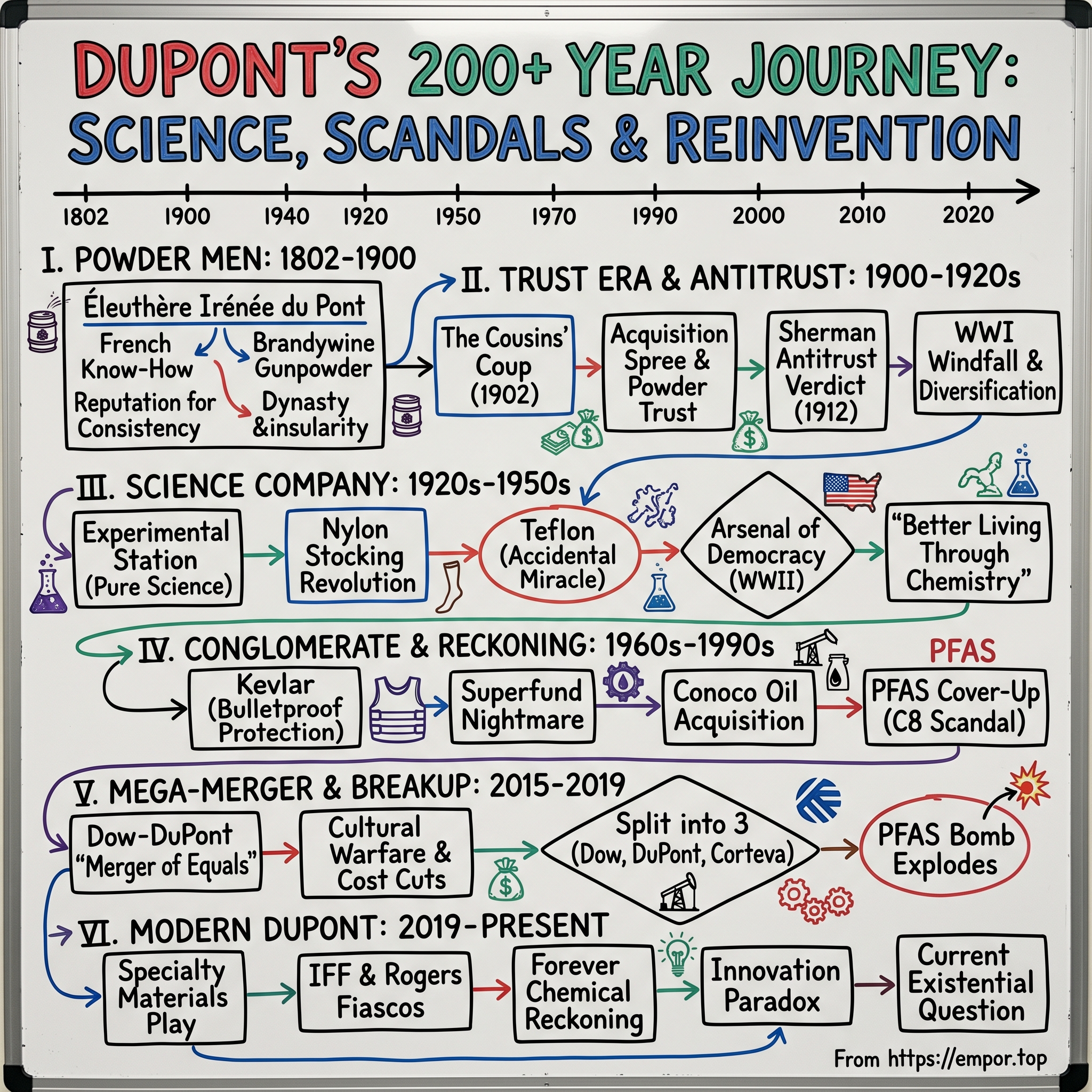

DuPont: Two Centuries of Science, Scandals, and Shareholder Returns

I. Introduction & Episode Roadmap

The explosion rattled windows five miles away. On March 29, 1818, forty workers at the DuPont powder mills scrambled for cover as fire reached the granulating house. Within seconds, 10,000 pounds of black powder detonated, killing forty people and leaving a crater where the building once stood. Éleuthère Irénée du Pont, the company's founder, rushed from his mansion on the hill—close enough to feel the heat, far enough to survive—and began directing rescue efforts. This wouldn't be the last explosion. Over the next century, DuPont facilities would detonate with grim regularity, each blast teaching the company another lesson about chemistry, safety, and the brutal economics of innovation.

That peculiar mix of danger, science, and profit would define DuPont for the next two centuries. From those early powder mills on Delaware's Brandywine Creek, the company would evolve into something far stranger and more significant than its founder could have imagined. This is the story of how a French aristocrat's gunpowder operation became the company that gave us nylon stockings and bulletproof vests, Teflon pans and genetically modified corn, miracle materials and environmental disasters that would haunt communities for generations.

Today's DuPont—trading at around $80 per share with a market cap near $35 billion—is actually the fourth or fifth incarnation of itself, depending on how you count. It's been broken up by antitrust authorities, rebuilt through acquisitions, merged with equals, and split apart again. Along the way, it created the modern industrial research lab, pioneered management techniques that would reshape corporate America, and discovered materials that fundamentally changed how humans dress, cook, communicate, and kill each other.

But here's what makes DuPont truly fascinating for investors and business historians: it's a company that has survived and often thrived through every major economic era in American history. Agricultural age? DuPont supplied the explosives that cleared the land. Industrial revolution? DuPont chemicals and materials enabled it. Information age? DuPont materials insulate the cables and protect the chips. Each transformation required the company to essentially destroy and rebuild itself, a corporate Ouroboros that somehow emerged stronger from each cycle.

The journey ahead takes us through three wars, multiple antitrust battles, Nobel Prize-winning science, and environmental scandals that would inspire Hollywood films. We'll meet brilliant scientists who revolutionized materials science before taking their own lives, executives who ran two of America's largest companies simultaneously, and lawyers who spent decades fighting to expose chemical cover-ups. We'll explore how a company founded on making things that explode became a company obsessed with safety, how "Better Living Through Chemistry" became a bitter punchline, and how the ultimate American industrial conglomerate keeps reinventing itself for each new century.

This is not just a business story—it's the story of American capitalism itself, with all its promise and peril, innovation and exploitation, creative destruction and actual destruction. So buckle up. This is going to be explosive.

II. The Powder Men: Founding & Early Dynasty (1802–1900)

The Aristocrat's Escape

In the summer of 1799, a small group of French refugees huddled on a ship bound for America, their conversation a mixture of relief and trepidation. Among them sat Éleuthère Irénée du Pont, age 28, clutching architectural drawings and chemical formulas—the only wealth he managed to salvage from revolutionary France. His father, Pierre Samuel du Pont de Nemours, had been an economist and minor noble who barely escaped the guillotine. Now they were sailing toward an uncertain future in a country they'd never seen.

Young Irénée had trained under Antoine Lavoisier, the father of modern chemistry, learning the secrets of gunpowder manufacture at the French royal powder works. Lavoisier hadn't been as fortunate—the Revolution claimed his head in 1794. But his knowledge lived on in his student's careful notes, formulas that would soon transform American industry.

The du Ponts initially planned to create a utopian colony in Virginia, a sort of French intellectual commune. That fantasy collapsed within months. Reality hit hard when Irénée went hunting with a former French naval officer and discovered American gunpowder was garbage—expensive garbage. It burned inconsistently, misfired frequently, and cost far more than superior French powder. Here was opportunity wrapped in black granules.

Building the Brandywine Empire

By 1802, Irénée had raised $36,000 from French investors and purchased 95 acres along Delaware's Brandywine Creek, chosen for its steep banks (natural blast walls) and reliable water power. He brought over French powder makers, men who understood that making explosives was equal parts chemistry and choreography—every movement calculated to minimize friction, every building designed to channel explosions upward rather than outward.

The early years nearly killed the company multiple times—literally. The first major explosion in 1815 leveled a building and killed several workers. Irénée rebuilt. Another blast in 1818 killed forty. He rebuilt again, this time spreading buildings further apart, limiting powder quantities in each structure, and instituting safety rules that seemed paranoid to outsiders: no metal tools, no running, no smoking within a quarter-mile.

But Irénée understood something his competitors didn't: in the powder business, reputation meant everything. The U.S. government and mining companies needed reliable suppliers. One bad batch could collapse a mine shaft or lose a battle. DuPont powder gained a reputation for consistency—it exploded when it should, with predictable force. By 1810, DuPont was selling 45,000 pounds annually. By 1820, after proving themselves during the War of 1812, they were moving 500,000 pounds.

The Family System

When Irénée died in 1834, he left behind seven children and a unique corporate structure. Rather than primogeniture or outside management, the DuPont company would be run by the family collectively, with leadership passing to the most capable son or son-in-law. This created a bizarre but effective dynamic: fierce internal competition coupled with absolute loyalty against outsiders.

The family lived in mansions built within earshot of the mills—close enough that explosions rattled their china, a constant reminder that their wealth came wrapped in danger. They intermarried obsessively. When Alfred Victor du Pont married his cousin Marguerite in 1837, it started a pattern that would see first cousins marrying first cousins for generations. By 1900, the family tree looked less like a tree and more like a Celtic knot.

This insularity had purpose. Gunpowder recipes were trade secrets. Manufacturing techniques were proprietary. Every marriage kept knowledge within the family. Every child raised on the Brandywine absorbed the business through dinner conversations and explosion drills.

The Civil War Windfall

When Confederate guns opened fire on Fort Sumter in April 1861, Henry du Pont—Irénée's son and current family leader—faced a defining moment. The company could have supplied both sides, as some competitors attempted. Instead, Henry chose the Union, partly from principle (the du Ponts opposed slavery) but mostly from pragmatism (the North had more money and would likely win).

The decision transformed DuPont from successful regional supplier to national powerhouse. Orders flooded in: 4 million pounds in 1861, 8 million in 1862, peaking at nearly 9 million pounds in 1864. The company built new mills, hired hundreds of workers, and ran production twenty-four hours a day. Profit margins expanded from around 15% to over 40% as demand overwhelmed supply.

But the war extracted its price. Three major explosions between 1863 and 1865 killed dozens of workers. Henry's own son, Lammot, barely escaped an 1863 blast that killed twelve men. The family began paying death benefits to workers' families—unusual for the era—partly from guilt, partly to maintain workforce loyalty in dangerous conditions.

Post-War Evolution

After Appomattox, military orders evaporated. DuPont faced the classic wartime supplier's dilemma: massive capacity, minimal demand. Henry and his nephew Lammot engineered a remarkable pivot. They'd noticed something during the war—military contracts had forced them to innovate constantly, developing specialized powders for different purposes: coarse grain for cannons, fine grain for rifles, specific formulations for mining.

Lammot, who'd studied chemistry at Penn, became obsessed with nitroglycerin and dynamite—Alfred Nobel's new inventions that promised to revolutionize blasting. Despite family skepticism (nitroglycerin was even more dangerous than black powder), Lammot pushed DuPont into high explosives. When he died in 1884—not from an explosion but from a disgruntled worker's bullet—he'd positioned DuPont for the next era.

By 1900, three generations of du Ponts had built something remarkable: America's largest explosives manufacturer, controlling about 36% of the national market. They'd survived fifty major explosions, killing over 230 workers. They'd developed a corporate culture obsessing over safety while manufacturing death. They'd created a family dynasty that was simultaneously insular and innovative, conservative and risk-taking.

The company's DNA was set: technical excellence, family control, strategic patience, and a willingness to destroy and rebuild when markets shifted. That DNA would soon be tested by three young cousins with radical ideas about corporate structure, market control, and the future of American business. The powder men were about to become power men.

III. The Trust Era & Antitrust Reckoning (1900–1920s)

The Orphans' Coup

Eugene du Pont's funeral in January 1902 should have been a somber transition of power. The DuPont Company patriarch was dead, and the family elders gathered to discuss selling the company to their largest competitor, Laflin & Rand, for $12 million. The business had grown too complex, they argued. None of Eugene's generation wanted the crushing responsibility. Better to cash out honorably than watch the family empire crumble.

Then Alfred I. du Pont stood up. At 37, he was considered something of a family embarrassment—a tinkerer who preferred the powder yards to the boardroom, who'd scandalized society by divorcing his first wife (also his cousin) to marry another cousin. "I'll take it," he announced. The room erupted. Alfred had no money, no backing, and no business running anything beyond a powder line.

But Alfred had two cousins: Thomas Coleman du Pont and Pierre S. du Pont. Coleman, at 39, was the entrepreneur who'd made a fortune in coal and steel ventures in Kentucky. Pierre, just 32, was the MIT-trained engineer with a head for numbers. Within weeks, the three cousins had engineered one of the most audacious takeovers in American business history.

They bought the company for $12 million—$2.4 million in cash and $9.6 million in bonds, using the company's own assets as collateral. The elders got their money. The cousins got an industrial empire. They'd essentially purchased DuPont with DuPont's own future earnings, a leveraged buyout decades before private equity made it fashionable.

Building the Powder Trust

Coleman du Pont had studied the great trusts—Standard Oil, U.S. Steel, American Tobacco. He understood that in the new industrial economy, controlling 36% of a market meant nothing if competitors could undercut prices. You needed 60%, 70%, ideally more. Between 1902 and 1907, the cousins went on an acquisition spree that would make modern tech giants jealous.

They bought Laflin & Rand, the would-be acquirer, in 1902. Then Hazard Powder Company. International Smokeless Powder. California Powder Works. Eastern Dynamite. Over 100 smaller firms. Some they bought with cash, others with DuPont stock, many with promises of future payments. Coleman's genius was understanding that most powder company owners were old, tired, and scared—scared of labor unrest, scared of explosions, scared of being crushed by larger competitors. DuPont offered them graceful exits.

Pierre revolutionized how they integrated acquisitions. Rather than maintaining separate companies, he centralized operations: purchasing, research, accounting, sales. He created departments—a novel concept in 1903. He instituted uniform cost accounting across all facilities, allowing headquarters to spot inefficiencies instantly. He developed return-on-investment calculations for every product line, every facility, every major decision. This wasn't just buying competitors; it was building the first modern industrial corporation.

By 1905, DuPont controlled between 70% and 75% of American explosives production. They set prices, allocated territories, and essentially decided who could blast and who couldn't. Mining companies, construction firms, and the military had one supplier that mattered: DuPont.

The Government Strikes Back

Theodore Roosevelt had been watching. The trust-busting president who'd taken on Standard Oil and Northern Securities couldn't ignore a monopoly that controlled the nation's explosives. In 1907, the Department of Justice filed suit under the Sherman Antitrust Act. The charge was simple: DuPont had created an illegal monopoly through predatory acquisitions and anti-competitive practices.

The trial revealed fascinating details about DuPont's methods. They'd created fake independent companies to give the illusion of competition. They'd threatened suppliers who sold to competitors. They'd used their size to negotiate exclusive contracts with railroads. Coleman's correspondence, subpoenaed by prosecutors, showed a man who understood exactly what he was doing: "We want to control absolutely," he'd written to Pierre.

The 1912 verdict was devastating but not unexpected: guilty of monopolization. The remedy was radical: DuPont had to divest enough assets to create two viable competitors. But Pierre, now running the company after Coleman's departure due to illness, turned disaster into advantage. Rather than spinning off random assets, he carefully crafted two new companies—Hercules Powder and Atlas Powder—keeping the best facilities, newest technologies, and key personnel for DuPont.

The War to End All Wars

When Archduke Franz Ferdinand was assassinated in June 1914, Pierre du Pont was more concerned with General Motors stock prices than European politics. By August, as Europe erupted, he understood: this war would consume explosives at unprecedented rates. DuPont received its first Allied orders before America entered the war—$100 million from France, $50 million from Britain, $36 million from Russia.

The numbers were staggering. DuPont's military powder production increased from 14 million pounds in 1914 to 455 million pounds in 1917. Employment surged from 5,300 to 85,000. The company built the world's largest smokeless powder plant in three months, entire cities sprouting around new facilities. Hopewell, Virginia, went from farmland to a city of 40,000 in less than a year, all to feed DuPont's powder plants.

But Pierre understood something his critics didn't: this windfall was temporary. While newspapers branded DuPont "merchants of death," Pierre was already planning the post-war transition. He poured war profits into research, into diversification, into acquiring a 23% stake in General Motors. When the November 1918 armistice came, DuPont had $90 million in cash and securities, minimal debt, and ambitious plans for peacetime.

The Management Revolution

Pierre's greatest innovation wasn't making powder—it was making the modern corporation. By 1920, DuPont had pioneered concepts that would define American business for the next century. The multidivisional structure, where autonomous units reported to central headquarters. The DuPont formula for return on investment: ROI = (Earnings/Sales) × (Sales/Assets). The systematic approach to capital allocation, comparing opportunities across divisions using standardized metrics.

He institutionalized strategic planning, creating committees that looked five, ten years ahead. He separated operational management from ownership, bringing in professional managers regardless of surname. He created one of America's first corporate research laboratories, understanding that future growth required innovation, not just acquisition.

Most remarkably, Pierre served simultaneously as president of DuPont and chairman of General Motors from 1915 to 1920, cross-pollinating management techniques between the chemical and automotive giants. His protégé, Alfred P. Sloan Jr., would take these ideas and build GM into the world's largest corporation. The DuPont management model became the template for industrial America.

The Transformation Begins

By 1920, the three cousins' coup was complete, though only Pierre remained in power. Coleman had moved on to politics and real estate, building New York's McAlpin Hotel. Alfred, forced out in a bitter family feud over his scandalous divorces, had retreated to Florida to build his own empire. Pierre stood alone atop a transformed company.

DuPont was no longer the Powder Company but the Chemical Company. War profits had funded new research into nitrocellulose, synthetic materials, and industrial chemicals. The antitrust breakup had paradoxically strengthened DuPont by forcing efficiency and innovation. The management revolution had created an organization capable of managing complexity at scale.

As the 1920s dawned, Pierre looked at his research laboratories and saw the future: synthetic fibers stronger than silk, plastics that could replace metal, chemicals that could transform agriculture. The powder men had built the foundation. Now it was time for the scientists to build the future. The age of "Better Living Through Chemistry" was about to begin.

IV. The Science Company Transformation (1920s–1950s)

The Experimental Station

In 1926, Charles Stine stood before DuPont's executive committee with an audacious request: $300,000 annually for "pure science" research with no guaranteed commercial application. The executives, accustomed to funding research tied to specific products, were skeptical. Pierre du Pont leaned forward: "What exactly would we be buying?" Stine's answer would transform American industry: "We'd be buying the future before anyone knows what it looks like."

The Experimental Station, built on 142 acres along the Brandywine near the original powder mills, became something unprecedented in American industry: a corporate research facility pursuing fundamental science. Bell Labs existed, but focused on telecommunications. GE researched electrical applications. DuPont's station would chase knowledge itself, betting that understanding would eventually yield products.

Stine recruited academics with promises unheard of in corporate America: publish freely, pursue curiosity, fail without consequence. He landed Wallace Carothers from Harvard, Julian Hill from MIT, dozens of PhDs who might have stayed in academia. The station's buildings, designed with movable walls and excess electrical capacity, assumed experiments would constantly evolve. The library subscribed to every major scientific journal in five languages. The machine shop could fabricate equipment that didn't exist anywhere else.

By 1929, the station employed over 850 people, making it larger than most university chemistry departments. The culture was deliberately academic—seminars, visiting speakers, publication in peer-reviewed journals. But with a difference: when someone discovered something interesting, armies of engineers would descend to scale it up.

The Miracle Worker's Tragedy

Wallace Carothers arrived at DuPont in February 1928, a brilliant, troubled 31-year-old who'd rather be teaching at Harvard but couldn't refuse DuPont's offer: complete freedom, unlimited resources, and a salary double what Harvard paid. Tall, thin, chronically anxious, Carothers carried cyanide capsules in his watch pocket—a chemist's security blanket against unbearable depression.

His assignment was magnificently vague: explore polymer chemistry. Scientists knew small molecules could link into chains, but nobody understood how to control the process. Carothers began with a simple question: what determines how molecules connect? Within months, his team was creating substances that had never existed—long chains of carbon and hydrogen, synthetic materials with properties nobody had imagined.

April 1930 brought the first breakthrough. Julian Hill, stretching a sample of polymer goo, discovered it formed strong, lustrous fibers. They called it "fiber 66" for its molecular structure. Years of refinement followed—learning to spin it, strengthen it, dye it. By 1935, they had something remarkable: synthetic silk, stronger than the natural material, capable of being molded, woven, or stretched into any shape.

But Carothers was unraveling as his polymers strengthened. The pressure of success, the depression he'd battled since childhood, the imposter syndrome despite global recognition—it all compounded. His notebooks from 1936 show increasingly frantic calculations interspersed with personal doubts. On April 29, 1937, two days after his 41st birthday, Carothers checked into a Philadelphia hotel and drank lemon juice laced with potassium cyanide. He left no note, only thousands of pages of research that would transform the world.

Nylon's Revolution

DuPont announced nylon to the public on October 27, 1938, with typical corporate understatement: "a new synthetic fiber with remarkable properties." The first demonstration was theatrical—a DuPont executive's wife wearing nylon stockings that could be stretched, crushed, and washed while maintaining their shape. Newspapers went wild. Here was American science defeating Japanese silk, modern chemistry improving on nature.

The numbers tell the real story. When nylon stockings went on sale May 15, 1940, DuPont had produced 4 million pairs. They sold out in four days. By December, the company was producing 12 million pounds of nylon annually. Women lined up for blocks when shipments arrived. The Japanese silk industry, which had supplied 90% of American hosiery thread, collapsed within two years.

Then Pearl Harbor changed everything. The War Production Board commandeered nylon for parachutes, rope, and tire cord. DuPont built new plants in West Virginia and Tennessee, scaling production to 50 million pounds by 1945. The company developed 20 different military applications: bomber tires that lasted longer, parachute cord stronger than silk, fuel tanks that didn't leak. One internal report calculated that nylon helped save 100,000 Allied lives through improved equipment.

The Accidental Miracle

Not every breakthrough came from planning. In 1938, Roy Plunkett was trying to create a new refrigerant when his gas cylinder seemed empty but weighed too much. Rather than discarding it, he sawed it open. Inside was a white, waxy substance that nothing would stick to—not water, not oil, not acid. Even concentrated sulfuric acid just beaded up and rolled off.

Polytetrafluoroethylene—PTFE, later branded Teflon—seemed useless at first. Too expensive for consumer products, too slippery for industrial applications. Then the Manhattan Project needed a material that could resist uranium hexafluoride's corrosion. Teflon was the only substance that worked. DuPont produced it in absolute secrecy, with workers unaware they were enabling atomic weapons.

Post-war applications exploded in unexpected directions. NASA used Teflon for spacesuits and heat shields. Surgeons implanted it as artificial arteries. By 1960, the "Happy Pan" coated with Teflon revolutionized cooking. The accidental discovery generated over $1 billion in revenue by 1970.

Building the Arsenal of Democracy

World War II transformed DuPont from chemical company to national strategic asset. Beyond nylon and Teflon, the company operated the Hanford Site, producing plutonium for the Manhattan Project. They synthesized RDX explosive, 50% more powerful than TNT. They created Neoprene synthetic rubber when Japanese conquest cut off natural supplies.

The scale was breathtaking. DuPont's employment peaked at 115,000 in 1943. The company operated 54 plants across 26 states. Revenue increased from $214 million in 1939 to $961 million in 1943. But unlike WWI, Pierre's successors had learned from history. They took most military contracts at cost-plus-one-dollar, avoiding war profiteering charges while building capabilities for peacetime.

The research never stopped. Even while producing for war, the Experimental Station developed Orlon (synthetic wool), Mylar (polyester film), and Dacron (polyester fiber). They created Freon refrigerants, Lucite acrylic, and hundreds of specialty chemicals. By 1945, DuPont held over 1,000 patents with another 500 pending.

"Better Living Through Chemistry"

The slogan appeared in 1935, but it captured the post-war zeitgeist perfectly. Americans who'd survived Depression and war wanted progress, convenience, modernity. DuPont delivered. Nylon carpets that never wore out. Orlon sweaters that moths ignored. Vinyl car interiors that looked like leather but cost pennies. Tupperware (using DuPont polyethylene) that kept food fresh for weeks.

The company's advertising sold not just products but a vision: science solving human problems. TV commercials showed happy families in synthetic-filled homes, everything clean, bright, maintenance-free. The Wonderful World of Chemistry exhibit at the 1964 World's Fair drew 10 million visitors, all marveling at DuPont's future—plastic hearts, synthetic food, materials that would last forever.

That last promise would prove ironic. "Forever" sounds wonderful until you realize some chemicals really do last forever, accumulating in water, soil, and human tissue. But in the 1950s, as DuPont's stock price quadrupled and American living standards soared, nobody worried about forever. They were too busy enjoying the miracles of modern chemistry.

By 1950, less than 10% of DuPont's revenue came from explosives. The company that began with black powder now produced thousands of products from hundreds of facilities. The Experimental Station had spawned satellite laboratories in Michigan, Texas, and Delaware. The company employed more PhDs than most universities.

The transformation was complete: DuPont had become the world's premier science company, turning fundamental research into commercial reality with unmatched efficiency. But success bred new challenges. How do you manage such diversity? How do you maintain innovation at scale? And what happens when your miracles turn out to have hidden costs? The next phase would test whether DuPont could adapt as successfully to social change as it had to scientific opportunity.

V. The Conglomerate Years & Environmental Reckoning (1960s–1990s)

The Empire Expands

Irving Shapiro's appointment as CEO in 1973 broke two centuries of tradition—he was neither a du Pont nor an engineer but a lawyer from Minneapolis, son of Lithuanian Jewish immigrants. His predecessor had chosen him precisely because DuPont needed an outsider's perspective. The company controlled dominant positions in dozens of chemical markets but faced new threats: environmentalists, regulators, and foreign competitors who'd rebuilt from WWII's ashes with newer technology.

Shapiro's strategy was audacious: if chemicals faced regulatory headwinds, buy businesses that didn't. In 1981, DuPont shocked Wall Street by acquiring Conoco Oil for $7.8 billion, the largest merger in history at that time. The logic seemed compelling—Conoco provided hydrocarbon feedstocks for chemicals while diversifying into energy. Critics called it desperation, a chemical company admitting its core business had peaked.

The acquisition binge continued through the 1980s. Consolidation Coal for $1.2 billion. New England Nuclear for $380 million. Dozens of smaller pharmaceutical and agricultural companies. By 1985, DuPont operated in industries Éleuthère Irénée couldn't have imagined: oil drilling, uranium enrichment, pharmaceutical manufacturing, seed genetics. Revenue hit $35 billion, making DuPont one of America's ten largest corporations.

But complexity bred dysfunction. The company's famous central research model fractured as divisions pursued different technologies. A Conoco executive complained he spent more time in Wilmington board meetings than Texas oil fields. Agricultural scientists fought chemical engineers for resources. The clear mission—"Better Living Through Chemistry"—dissolved into corporate alphabet soup of divisions, subsidiaries, and joint ventures.

The Kevlar Revolution

Sometimes innovation still broke through bureaucracy. Stephanie Kwolek, one of the few female chemists DuPont hired in the 1940s, had spent decades experimenting with polymer solutions. In 1965, she created a cloudy, thin liquid that should have been discarded—it looked nothing like the clear, viscous solutions that produced good fibers. But Kwolek insisted on spinning it. The resulting fiber was five times stronger than steel by weight.

It took DuPont fifteen years and $500 million to commercialize what became Kevlar. The molecular structure was unprecedented—rigid chains that lined up parallel, creating extraordinary tensile strength. Early applications disappointed. Tire manufacturers found it too expensive. The military was skeptical that fabric could stop bullets.

The breakthrough came from an unexpected source: pizza. In 1975, a DuPont sales representative noticed pizza delivery drivers were being robbed and sometimes shot. He convinced a small company to create Kevlar-lined delivery bags that could double as shields. Word spread to police departments. By 1980, DuPont was selling Kevlar vests that had saved hundreds of officers' lives.

Applications exploded: racing tires, spacecraft shielding, hurricane panels, firefighter gear, bulletproof helmets. By 1990, Kevlar generated $500 million annually with 90% gross margins. The fiber that almost got thrown away became DuPont's most profitable material per pound.

Silent Spring's Revenge

Rachel Carson's 1962 book "Silent Spring" had named DuPont directly, criticizing the company's pesticides and chemicals. Initially, executives dismissed her as hysterical. But public opinion was shifting. The Cuyahoga River caught fire in 1969. The Environmental Protection Agency formed in 1970. Suddenly, the chemicals that built American prosperity were suspected of destroying it.

The first major reckoning came with chlorofluorocarbons (CFCs). DuPont had commercialized Freon refrigerants in the 1930s, revolutionary for their safety—non-toxic, non-flammable, stable. By 1974, the company produced 50% of global CFCs, worth $600 million annually. Then scientists discovered CFCs were destroying atmospheric ozone, the layer protecting Earth from ultraviolet radiation.

DuPont's response revealed corporate schizophrenia. The company funded research confirming ozone depletion while simultaneously lobbying against regulations. Internal memos from 1978 show executives understood the science but feared losing market share. Only when the Antarctic ozone hole appeared in 1985—visual proof of catastrophe—did DuPont reverse course, pledging to phase out CFCs by 2000.

The pattern repeated with other chemicals. Benzene, a key feedstock, caused leukemia in workers. Lead additives, highly profitable, damaged children's brains. Asbestos, used in construction materials, triggered lung disease decades later. Each revelation followed the same arc: initial denial, grudging acceptance, expensive remediation.

The Superfund Nightmare

In 1980, Congress passed the Comprehensive Environmental Response, Compensation, and Liability Act—Superfund—requiring companies to clean up toxic waste sites. DuPont's name appeared on site after site. The company had operated for 180 years, often dumping waste by practices legal at the time but devastating in retrospect.

The Pompton Lakes facility in New Jersey became a case study in industrial contamination. DuPont had manufactured explosives there since 1902, leaving 570 acres contaminated with lead, mercury, and solvents. Cleanup costs exceeded $100 million. Residents filed lawsuits claiming birth defects and cancers. The work continues today, forty years later.

By 1990, DuPont faced environmental liabilities exceeding $1 billion. The company that had marketed itself as improving life through chemistry was spending fortunes proving it hadn't destroyed life through chemistry. The irony was bitter—many contaminated sites produced materials for safety equipment or life-saving medicines.

Innovation Never Stopped

Despite distractions, DuPont's laboratories kept producing breakthroughs. Tyvek, introduced in 1967, created a new category—synthetic material that breathed like fabric but repelled water like plastic. Construction companies wrapped buildings in it. Medical companies made sterile packaging. The postal service used it for envelopes that couldn't tear.

Corian solid surface, launched in 1971, let designers create seamless countertops and sinks. Lycra spandex revolutionized athletic wear—every yoga pant and swimsuit contained DuPont technology. Nomex fireproof fiber protected race car drivers and astronauts. SentryGlas made hurricane windows that could stop flying debris.

The pharmaceutical division developed breakthrough HIV drugs, cholesterol medications, and agricultural chemicals that increased crop yields 30%. The company pioneered biotechnology, genetically engineering bacteria to produce materials previously extracted from petroleum. By 1990, DuPont held 23,000 patents with 2,000 new applications annually.

The Seagram Scare

In April 1995, Edgar Bronfman Jr.'s Seagram Company announced it had acquired 24% of DuPont's shares, becoming the largest stockholder. Bronfman, heir to a liquor fortune, claimed he wanted to "unlock value" through breakups and spinoffs. DuPont's stock jumped 15% as arbitrageurs bet on a hostile takeover.

CEO Jack Krol mobilized defense. Delaware's legislature passed anti-takeover laws. The du Pont family, still controlling 15% of shares through trusts, rallied against the interloper. Institutional investors were courted with promises of higher dividends and share buybacks. The board authorized a poison pill that would dilute Bronfman's stake if he crossed 25%.

The standoff lasted three years. Bronfman pushed for board seats, demanded strategic reviews, and threatened proxy fights. But he never gained allies—institutional investors preferred DuPont management's steady returns to Bronfman's financial engineering. In 1998, Seagram sold its stake for $8.8 billion, a 50% profit but far less than a successful takeover would have yielded.

The episode forced introspection. DuPont had survived but looked bloated—a conglomerate pretending coherence. New CEO Chad Holliday arrived in 1998 with a mandate: focus on life sciences and specialty materials, exit everything else. The unwinding would take a decade and culminate in the most dramatic transformation in DuPont history.

By 1999, DuPont generated $45 billion in revenue from businesses ranging from nylon to pharmaceuticals, seeds to oil. The company employed 125,000 people across 70 countries. It remained highly profitable—$2.8 billion in net income—but growth had stalled. The stock traded at the same price as 1997 despite bull markets everywhere else.

The 20th century was ending with DuPont at a crossroads. The conglomerate model that had provided stability was now preventing growth. Environmental liabilities clouded the future. Biotechnology promised revolution but required capabilities DuPont lacked. Something had to give. The company that had reinvented itself from explosives to chemicals would need to transform again. This time, the solution would be more radical than anyone imagined: DuPont would essentially destroy itself to survive.

VI. The Dow-DuPont Mega-Merger & Breakup (2015–2019)

The December Surprise

On December 11, 2015, two titans of American industry announced the unthinkable: DuPont and Dow Chemical would merge in a $130 billion "merger of equals," creating the world's largest chemical company before immediately splitting into three. The announcement came at 6 AM, timed to hit markets before trading opened. Within minutes, both stocks surged 10%.

The architects were unlikely partners. Ed Breen, DuPont's CEO for barely two months, was a corporate breakup artist who'd dismantled Tyco International. Andrew Liveris, Dow's CEO since 2004, was a chemical lifer who'd spent decades building Dow's global empire. They'd been secretly meeting since October, sometimes in Midland, Michigan, sometimes in Wilmington, Delaware, always in unmarked conference rooms.

The pitch to shareholders was elegant in its simplicity: combine two bloated conglomerates, cut $3 billion in costs, then divide into three focused companies—agriculture, materials science, and specialty products. Each piece would be worth more than the muddled whole. Financial engineering would accomplish what decades of strategic planning hadn't: clarity, focus, and growth.

But the real driver was desperation disguised as strategy. Both companies faced existential threats. Activist investor Nelson Peltz's Trian Fund had acquired $1.8 billion of DuPont stock, demanding breakups and board seats. Dow confronted Chinese competitors selling commodities at losses, destroying margins. Agriculture units at both companies struggled with collapsed crop prices. Merging wasn't visionary—it was survival.

The Integration Nightmare

The deal required 18 months of regulatory approval across 30 countries. China demanded divestiture of rice herbicides. Brazil worried about corn seed monopolies. The European Commission conducted a 15-month investigation, ultimately requiring $15 billion in asset sales. DuPont sold chunks of its crop protection business to FMC Corporation. Dow divested petrochemical plants across Europe.

Behind the regulatory drama, cultural warfare erupted. DuPont employees, proud of 200 years of history, bristled at Dow's aggressive commercial culture. Dow workers resented DuPont's bureaucracy and East Coast elitism. Integration meetings devolved into turf battles. A Dow executive later described it as "trying to merge Harvard and a Big Ten school—everyone thought they were smarter."

The companies maintained separate headquarters 700 miles apart, a logistical nightmare. Executives shuttled between Midland and Wilmington weekly, burning millions on private jets. IT systems wouldn't communicate—DuPont ran SAP while Dow used Oracle. Even email required workarounds. Simple decisions like unified expense policies took months.

The promised $3 billion in cost synergies translated to human carnage. 10,000 jobs disappeared—8% of combined workforce. Research facilities closed in Michigan, Delaware, and Switzerland. The Experimental Station, birthplace of nylon and Teflon, saw its workforce halved. Scientists with decades of experience were offered retirement packages or severance. Institutional knowledge evaporated.

Three-Way Split Execution

The separation began before integration finished—a corporate mitosis conducted at breakneck speed. Teams worked on three contradictory goals simultaneously: merging operations, cutting costs, and preparing for divorce. Project managers used military terminology: "Day One" for merger close, "Day Two" for separation launch, "End State" for final structure.

Corteva Agriscience, the agriculture spinoff, combined DuPont's Pioneer seeds with Dow's crop protection chemicals. The portfolio looked powerful: leading positions in corn and soybean seeds, broad-spectrum herbicides, new digital farming platforms. But timing was terrible. Farm income had declined 50% since 2013. Bayer had just acquired Monsanto for $63 billion, creating a larger competitor. Chinese companies were pirating seed genetics.

New Dow inherited commodity chemicals—ethylene, polyethylene, caustic soda. These were Dow's historical businesses, steady but unexciting, with returns tied to oil prices and global GDP. The company would focus on plastics, industrial intermediates, and infrastructure chemicals. Steady cash flow but limited growth, a dividend aristocrat in waiting.

New DuPont got the sexy stuff: Kevlar, Tyvek, Corian, Nomex, plus electronic materials, water filtration, and automotive applications. High margins, technological differentiation, growth potential. But also the liabilities—environmental lawsuits, asbestos claims, and a devastating revelation about PFAS "forever chemicals" that would haunt the company.

The Unraveling

Separation occurred in stages throughout 2019. Corteva spun off first on June 1, trading at $26 per share. New Dow followed on April 1. DuPont emerged last, keeping the historic name but little else. Each company received one-third of synergies but all of their specific problems.

The financial results were immediately disappointing. Combined market value of the three companies in December 2019: $120 billion, less than the merger value four years earlier despite broader market gains. Corteva struggled with agricultural headwinds. Dow faced petrochemical overcapacity. DuPont discovered integration had destroyed more value than expected. Ed Breen later called it "the deal from hell." The integration consumed $4 billion in costs—$1 billion more than projected synergies. Consulting fees alone exceeded $500 million. Executive compensation packages for retention and separation totaled $800 million. The human toll was worse: employee satisfaction scores plummeted 40%, institutional knowledge worth decades vanished, and research productivity declined measurably.

The PFAS Bomb Explodes

In May 2019, just as the three companies were finalizing separation, the Environmental Working Group released a map showing PFAS contamination at 610 sites across 43 states. DuPont facilities dominated the list. PFAS—per- and polyfluoroalkyl substances—were the miracle molecules that made Teflon non-stick and Scotchgard water-repellent. They were also "forever chemicals" that accumulated in human blood and never degraded.

The timing couldn't have been worse. The separated companies were fighting over who inherited PFAS liability. Chemours, spun off from DuPont in 2015 specifically to isolate Teflon liabilities, sued its former parent claiming fraudulent conveyance. Corteva argued agricultural operations never used PFAS. New DuPont claimed it was a different legal entity than historical DuPont. The legal battle escalated quickly. Chemours sued DuPont in 2019, claiming that DuPont's liability estimates were "spectacularly wrong." When it spun off Chemours in 2015, DuPont had pegged the maximum liability in the multidistrict litigation involving the 3,500-plus PFOA cases at $128 million. The company settled 19 months later for $671 million. The discrepancy was stunning—DuPont had understated liabilities by over 400%.

By January 2021, the three companies reached a $4 billion cost-sharing agreement. DuPont and Corteva together, on one hand, and Chemours, on the other hand, agree to a 50-50 split of certain qualified expenses incurred over a term not to exceed twenty years or $4 billion. The settlement revealed the merger's hidden catastrophe: companies that had just spent four years integrating and separating were now bound together for two decades by environmental liabilities nobody wanted to own.

Was It Worth It?

The numbers tell a damning story. The DowDuPont merger promised $3 billion in cost synergies but delivered $4 billion in integration costs, $4 billion in PFAS liabilities, and destroyed approximately $50 billion in market value. Thousands of jobs vanished, research capabilities degraded, and three weakened companies emerged where two strong ones had existed.

The transaction took nearly four years from announcement in December 2015 to final spinoff in 2019. During that period, the S&P 500 gained 40% while the combined entities lost value. Competitors like BASF and Shin-Etsu strengthened market positions while DowDuPont was distracted by internal reorganization.

The human cost was immeasurable. Scientists with decades of experience left or were pushed out. The Experimental Station, which had produced Nylon and Kevlar, became a shadow of itself. Corporate cultures that had evolved over centuries were dismantled in months. Institutional knowledge that money couldn't buy disappeared forever.

Ed Breen, reflecting years later, admitted the execution was flawed but defended the strategy: "The individual pieces are stronger than the muddled whole we started with." Andrew Liveris was less diplomatic, calling the regulatory delays and cultural clashes "unnecessary destruction of value." Industry analysts were harsher—one called it "the worst mega-merger in chemical industry history."

The only clear winners were the investment bankers who collected $500 million in fees, the consultants who billed hundreds of millions, and the lawyers who managed the regulatory maze. Nelson Peltz's Trian Fund, which had agitated for the breakup, made modest gains but far less than if DuPont had simply improved operations without the merger drama.

For investors, the lesson was sobering: financial engineering is no substitute for operational excellence. The companies that emerged from DowDuPont were neither the focused champions promised nor the integrated powerhouse they might have been. They were compromised entities, carrying pieces of history they didn't want and missing capabilities they needed.

The merger that was supposed to unlock value had instead revealed a fundamental truth about American industrial companies: sometimes the inefficiencies and redundancies that consultants hate are actually the resilience and capabilities that ensure survival. DowDuPont had performed the ultimate corporate experiment—complete integration followed by complete separation—and proved that some things, once broken, can't be properly rebuilt.

As the three companies entered the 2020s as independent entities, each faced its own challenges. But they shared one common burden: the ghost of DowDuPont, a four-year fever dream that had promised transformation and delivered trauma. The question now wasn't whether the merger was worth it—clearly it wasn't—but whether the surviving companies could recover from it.

VII. Modern DuPont: The Specialty Materials Play (2019–Present)

Rising from the Ashes

On June 1, 2019, Ed Breen stood before employees at DuPont's Wilmington headquarters with a message that was equal parts confession and rallying cry: "We've been through hell. Now let's build something worth the journey." The new DuPont that emerged from the DowDuPont breakup was neither the diversified giant of old nor the agricultural powerhouse some had envisioned. It was something deliberately narrower—a $21 billion specialty materials company betting everything on higher margins and technological differentiation.

The portfolio Breen inherited looked impressive on paper: Kevlar body armor, Tyvek building wrap, Corian countertops, Nomex fireproof suits, plus thousands of specialty chemicals for electronics, automotive, and industrial applications. These weren't commodity products competing on price but engineered materials where DuPont's intellectual property commanded premiums. Operating margins averaged 23%, well above the chemical industry's 15% standard.

But beneath the surface, problems festered. The DowDuPont merger had scrambled reporting systems so badly that managers couldn't accurately track inventory for months. Customer relationships, some dating back decades, had frayed during the chaos. The sales force, reorganized three times in four years, barely knew their own product lines. Most critically, R&D spending had been slashed from 4.5% of revenue to 2.8% to fund merger costs, crippling innovation pipelines.

The IFF Debacle

Breen's first major move as CEO seemed brilliant. In December 2019, DuPont announced the sale of its Nutrition & Biosciences division to International Flavors & Fragrances (IFF) for $26.2 billion—$7.3 billion in cash plus 55.4% ownership of the combined company. The division, which made food ingredients, probiotics, and enzymes, generated solid profits but didn't fit DuPont's materials focus.

The deal structure was elegant financial engineering. DuPont would receive immediate cash to pay down debt, maintain majority control of a growing business, and eventually monetize IFF shares at premium valuations. Analysts praised the transaction as "transformative value creation."

Reality proved messier. IFF's integration of the nutrition business stumbled badly. IT systems didn't mesh, causing order fulfillment delays. Key customers defected to competitors. Synergy targets were missed by 40%. IFF's stock price, which had reached $145 before the merger, collapsed to $75 by 2022. DuPont's stake, valued at $18 billion at closing, was worth barely $10 billion two years later. Worse, Breen had miscalculated the tax implications. The Reverse Morris Trust structure was supposed to be tax-free, but technicalities triggered unexpected capital gains. DuPont stockholders who exchanged shares for IFF faced surprise tax bills. The final exchange ratio for the exchange offer was set at 0.7180 shares of N&B common stock for each share of DuPont common stock validly tendered, diluting value further than expected.

By late 2022, Breen quietly began selling DuPont's IFF stake in blocks, accepting massive losses to raise cash. The $26.2 billion crown jewel had become an $8 billion albatross. One board member privately called it "the worst major transaction in DuPont's 220-year history."

The Rogers Acquisition Fiasco

Seeking redemption, Breen announced in November 2021 that DuPont would acquire Rogers Corporation for $5.2 billion, a 50% premium to market price. Rogers made specialized materials for 5G telecommunications, electric vehicles, and advanced electronics—exactly the high-growth markets DuPont needed. The deal would add $800 million in revenue with 30% EBITDA margins.

But Breen had misread the regulatory environment. Chinese authorities, reviewing the deal for antitrust concerns, slow-walked approval. The Committee on Foreign Investment in the United States (CFIUS) raised national security concerns about Chinese access to Rogers' defense technologies through DuPont's global operations. European regulators worried about concentration in specialty polymers.

For 18 months, DuPont's executives shuttled between Washington, Brussels, and Beijing, offering increasingly desperate concessions. Legal fees exceeded $50 million. The distraction paralyzed other strategic initiatives. Rogers' customers, uncertain about ownership, began qualifying alternative suppliers.

In November 2022, DuPont terminated the merger, paying Rogers a $162.5 million breakup fee. The failure wasn't just financial—it signaled that DuPont lacked the political capital and regulatory expertise to execute major acquisitions. Competitors noted the weakness. Within months, activist investors began circling.

The Forever Chemical Reckoning

While Breen focused on deals, PFAS litigation metastasized into existential threat. The companies will collectively establish and contribute a total of $1.185 billion to a settlement fund announced in June 2023, covering water utility claims. But personal injury lawsuits kept multiplying.

The science was damning. PFAS chemicals, used to make Teflon and hundreds of other products, accumulated in human blood and never degraded. Studies linked them to kidney cancer, testicular cancer, thyroid disease, and pregnancy complications. DuPont had known about health risks since the 1960s but continued production for decades. The C8 Science Panel, formed as part of a class action settlement, had concluded PFOA was "more probably than not" linked to kidney cancer, testicular cancer, ulcerative colitis, thyroid disease, hypercholesterolemia, and pregnancy-induced hypertension. Documents revealed through litigation showed industry had multiple studies showing adverse health effects at least 21 years before they were reported in public findings.

The financial exposure kept growing. Beyond the $1.185 billion water utility settlement, personal injury claims proliferated. Analysts estimated total PFAS liability could exceed $10 billion. Every quarter brought new lawsuits, new scientific studies linking PFAS to diseases, new communities discovering contamination. DuPont's insurance carriers began denying coverage, arguing the company knew about dangers and continued production.

Current Strategy: The Narrow Path

By 2023, Lori Koch had replaced Ed Breen as CEO, inheriting a company worth less than when DowDuPont merger was announced eight years earlier. Her strategy was deliberately modest: focus on existing specialty materials, improve operations, manage liabilities. No grand visions, no transformative acquisitions, just blocking and tackling.

The portfolio had been pruned to four segments: Electronics & Industrial (semiconductor materials, industrial films), Water & Protection (filtration membranes, Tyvek, Kevlar), Corporate & Other (legacy businesses being wound down), and the disastrous IFF stake being liquidated. Revenue had shrunk to approximately $12 billion annually, less than a third of pre-merger DuPont.

But margins were improving. The electronics business benefited from semiconductor shortages, with customers accepting 20% price increases for critical materials. Tyvek demand surged during COVID for medical packaging. Kevlar sales grew as global conflicts increased demand for body armor. Operating margins reached 25% in core businesses, generating substantial cash despite smaller scale.

Koch's masterstroke was settling with activist investor Third Point, which had accumulated a significant stake demanding further breakups. Rather than fight, she negotiated board seats and strategic review, essentially admitting DuPont might need to split again. The market responded positively—admission of problems beat denial.

The Innovation Paradox

DuPont still possessed remarkable technology. The company held over 15,000 active patents, employed 3,000 scientists, and operated research facilities globally. Recent innovations included membranes that could desalinate seawater using 30% less energy, materials enabling flexible electronic displays, and biodegradable polymers replacing traditional plastics.

But innovation had become defensive rather than offensive. Research focused on incremental improvements to existing products, not breakthrough discoveries. The budget—$400 million annually—was substantial in absolute terms but tiny relative to history. The Experimental Station that once employed 850 researchers now had fewer than 200.

The company faced a cruel paradox: it needed innovation to grow but couldn't afford the patient capital required for fundamental research. Every dollar spent on speculative science was a dollar not available for PFAS settlements or share buybacks. The quarterly earnings cycle that public markets demanded was incompatible with the decade-long development cycles that materials science required.

Financial Engineering Redux

By late 2024, DuPont's financial position had stabilized but remained precarious. Net debt of $6 billion seemed manageable against $2.5 billion in annual EBITDA, but PFAS liabilities lurked off-balance-sheet. The company generated roughly $1 billion in free cash flow annually, but most went to dividends and litigation settlements rather than growth investments. The latest results showed the pattern: Fourth Quarter 2024 net sales of $3.1 billion increased 7% with operating EBITDA of $807 million, up 13% year-over-year. For the full year 2024, net sales rose by 3% to $12.4 billion, with a GAAP income of $778 million and an adjusted EPS of $4.07. The numbers looked healthy until you remembered this was a company that once generated $35 billion in revenue.

The board's solution was predictable: another spinoff. In 2024, DuPont announced plans to separate its Electronics business by November 2025, creating yet another independent company. The electronics division, generating roughly half of DuPont's profits, would become a pure-play semiconductor materials company. What remained would be an even smaller DuPont focused on water, protection, and industrial applications.

The market shrugged. DuPont stock traded around $80-85 per share, essentially flat for five years while the S&P 500 had nearly doubled. The company that had once been a Dow Jones Industrial Average component for 82 years was now barely noticed by investors, too small for index funds, too complex for retail investors, too troubled for growth funds.

The Existential Question

As 2025 began, DuPont faced an existential question: what was it for? The company that had armed the Union Army, enabled the automobile age, dressed the world in synthetic fibers, and put men on the moon now seemed to lack purpose beyond managing decline and liabilities.

The irony was crushing. DuPont possessed technologies the world desperately needed—materials for renewable energy, water purification for climate adaptation, lightweight composites for electric vehicles. But it lacked the scale to commercialize them effectively, the capital to develop them fully, and the credibility to lead after decades of environmental damage.

Some board members quietly discussed the ultimate solution: selling DuPont entirely. Private equity firms circled, calculating how much value could be extracted by breaking up the company and selling the pieces. Strategic buyers from Europe and Asia evaluated which technologies they wanted. The du Pont family, their ownership diluted to insignificance, could only watch.

Yet DuPont endured, as it always had. The company that survived the War of 1812, the Civil War, two World Wars, the Great Depression, countless explosions, antitrust breakups, and environmental disasters would likely survive this crisis too. But survival and success are different things.

The question for investors wasn't whether DuPont would exist in five years—it probably would. The question was whether it would matter. In an economy increasingly dominated by software and services, was there still room for a company that made physical things, even miraculous physical things? In a world traumatized by environmental damage, could a chemical company ever be trusted again?

As Koch prepared for another earnings call, another round of questions about PFAS litigation and margin improvements, she might have reflected on how far DuPont had fallen from its motto: "Better Living Through Chemistry." The chemistry continued, remarkable as ever. But better living? That promise had been broken, perhaps irreparably. What remained was a company rich in history and technology but poor in trust and vision, searching for a future it might never find.

VIII. Innovation Legacy & Technological Impact

The Pantheon of Discoveries

Walk through any American home and you're surrounded by DuPont's ghosts. The non-stick pan in the kitchen—Teflon, 1938. The stretch in yoga pants—Lycra, 1959. The bulletproof vest hanging in a police officer's locker—Kevlar, 1965. The building wrap keeping moisture out of walls—Tyvek, 1967. These weren't just products; they were revolutions disguised as materials, each one rewriting the rules of what matter could do.

The numbers alone stagger the imagination. Between 1920 and 1990, DuPont scientists filed over 50,000 patents. They published 15,000 peer-reviewed papers. Nine DuPont researchers won Nobel Prizes, though only one—Charles Pedersen for crown ethers in 1987—won for work done at the company. The Experimental Station and its satellite laboratories employed over 10,000 PhDs across seven decades, making it the largest concentration of industrial scientists outside the Soviet Union.

But the real legacy wasn't in numbers—it was in transformation. Before DuPont, clothing came from plants and animals. After DuPont, it could be designed molecule by molecule. Before DuPont, armor meant heavy metal plates. After DuPont, a vest weighing five pounds could stop a bullet. Before DuPont, chemistry was something that happened in universities. After DuPont, it was the engine of American industrial supremacy.

The R&D Model That Changed Everything

In 1927, when Charles Stine convinced DuPont to fund "pure research" with no immediate commercial application, he invented something more important than any chemical: the modern corporate research laboratory. Not the Edison model of directed invention, not the German model of university-industry collaboration, but something uniquely American—massive resources directed at fundamental understanding, betting that knowledge would eventually yield profit.

The model had four revolutionary elements. First, patience—researchers could work on problems for years without producing revenue. Wallace Carothers spent six years on polymer chemistry before creating nylon. Stephanie Kwolek worked on aramid fibers for over a decade before Kevlar emerged. Second, scale—when something showed promise, DuPont could throw hundreds of researchers and millions of dollars at commercialization. Third, integration—discoveries moved seamlessly from laboratory to pilot plant to full production, all within one company. Fourth, protection—ironclad patents and trade secrets that could defend innovations for decades.

This model influenced every major American corporation. IBM Research, Bell Labs, Xerox PARC, Microsoft Research—all borrowed from DuPont's playbook. The idea that companies should fund basic science, that patient capital could yield extraordinary returns, that industrial research could match or exceed academic research—these concepts emerged from the Brandywine and spread across the economy.

The Polymer Revolution

To understand DuPont's impact, you must understand what polymers meant. Before the 1930s, humans were limited to materials nature provided—wood, metal, stone, natural fibers. Chemistry could modify these materials but not fundamentally transcend their limitations. Polymers changed everything. Suddenly humans could design materials atom by atom, creating substances with properties that had never existed.

Nylon was the breakthrough that proved the concept. Here was a fiber stronger than silk, more uniform than wool, capable of being drawn into threads a fraction of a human hair's width or molded into gears that could replace metal. When DuPont's pavilion at the 1939 World's Fair displayed nylon stockings, visitors literally couldn't believe what they were seeing—synthetic silk seemed like alchemy.

The cascade of innovations that followed rewrote material science. Neoprene (1930) created synthetic rubber when natural supplies were threatened. Lucite (1936) made transparent plastics practical. Teflon (1938) created the most slippery substance known. Mylar (1952) enabled magnetic recording tape. Nomex (1961) provided fireproof fabric. Kevlar (1965) stopped bullets with fiber. Corian (1967) created seamless countertops. Each breakthrough spawned entire industries.

Patents, Secrets, and Monopoly Power

DuPont's approach to intellectual property was as innovative as its chemistry. The company didn't just patent products—it patented processes, intermediates, applications, even potential uses it had no intention of pursuing. A successful material might be protected by hundreds of patents, creating thickets competitors couldn't navigate.

Trade secrets mattered even more than patents. The exact process for making Kevlar remained secret for decades after the patent expired. DuPont would license technologies selectively, maintaining control while extracting maximum value. Competitors might know what DuPont made but not how they made it profitably.

This strategy created virtual monopolies lasting decades. DuPont controlled 90% of the U.S. nylon market through the 1960s. They maintained 80% market share in aramid fibers (Kevlar and Nomex) into the 2000s. Teflon dominance persisted until PFOA health concerns destroyed the brand. These monopolies funded further research, creating virtuous cycles of innovation and profit.

The Failures That Taught

Not every breakthrough succeeded commercially. Corfam, synthetic leather introduced in 1963, was technically superior to natural leather—it didn't stretch, stain, or wear out. DuPont spent $100 million developing it, built dedicated factories, and launched with massive marketing. By 1971, they'd abandoned the product entirely. Consumers didn't want shoes that didn't break in, that felt artificial despite technical superiority.

The biotech pivot of the 1990s largely failed. DuPont spent billions acquiring seed companies and developing genetically modified crops, but could never match Monsanto's ruthlessness or agricultural expertise. The pharmaceutical ventures of the 1990s and 2000s produced few blockbusters despite massive investment. The company that could make any material struggled with anything biological.

These failures taught harsh lessons. Technical superiority didn't guarantee market success. Core competencies didn't automatically transfer to adjacent fields. Being early to a technology (like GMOs) meant nothing without the right business model. The very capabilities that made DuPont great at materials—patience, perfectionism, engineering excellence—became liabilities in faster-moving markets.

The Digital Age Disconnect

As the economy digitized, DuPont's innovations seemed increasingly peripheral. The company made materials for semiconductors but not the chips themselves. They created films for displays but not the software that ran on them. They enabled the physical infrastructure of the internet age while missing the value creation happening in bits rather than atoms.

Recent innovations reflected this disconnect. DuPont's latest breakthroughs—membranes for water filtration, materials for electric vehicle batteries, films for solar panels—were impressive but invisible, embedded in other companies' products. A consumer might use dozens of DuPont innovations daily without knowing the company existed.

The research model that had worked for a century was breaking down. Modern innovation happened in networks, not isolated corporate labs. Open source, not trade secrets. Software iterations in weeks, not materials development over decades. The company that had invented corporate R&D couldn't adapt to distributed innovation.

Current Pipeline: Incremental Excellence

Today's DuPont still innovates, but differently. The company files 500-600 patents annually, respectable but not revolutionary. Research focuses on incremental improvements—making Kevlar 10% stronger, Tyvek 15% more breathable, semiconductor materials 20% purer. These improvements matter enormously to customers but lack the transformative impact of past breakthroughs.

AI-related sales grew by about 30% this year, reaching over $300 million, showing DuPont materials enabling the artificial intelligence revolution. But again, DuPont provided ingredients, not leadership. The company that had once defined the future now served those who were defining it.

The innovation legacy endures in unexpected ways. DuPont alumni populated the chemical industry, bringing the company's methods and mindset to competitors. The Experimental Station model influenced Chinese state-owned enterprises building massive research facilities. Indian conglomerates studied DuPont's patent strategies. The company's innovations continued shaping the world, even as DuPont itself shrank.

The Ultimate Judgment

How should history judge DuPont's innovation legacy? The company gave humanity materials that saved millions of lives—bulletproof vests, safer automobiles, medical devices. But it also created substances that poisoned waterways and accumulated in every living organism on Earth. It democratized products once reserved for the wealthy—stockings, raincoats, carpeting—while generating environmental costs that fell disproportionately on the poor.

Perhaps the judgment is simpler: DuPont proved that organized industrial research could transform civilization. Between 1920 and 1990, the company demonstrated that patient capital plus brilliant scientists could create miracles. The materials DuPont invented will outlast the company itself—Kevlar will still be stopping bullets long after the last DuPont factory closes.

But the model that created these miracles is dying. The age of the great corporate laboratory has passed, replaced by venture capital, startups, and distributed innovation. DuPont's greatest invention—the industrial research laboratory—has become obsolete, a victim of its own success in making innovation routine rather than revolutionary.

The tragedy isn't that DuPont stopped innovating—it hasn't. The tragedy is that innovation stopped being enough. In a world demanding not just new materials but new business models, not just patents but platforms, not just chemistry but code, DuPont's miracles became commodities. The company that taught America how to innovate never learned how to innovate innovation itself.

IX. The Dark Side: Environmental & Legal Battles

The Devil They Knew

In 1961, DuPont's Polymer Products Division received a report that should have changed everything. Rats exposed to PFOA—the chemical that made Teflon possible—showed enlarged livers, kidney damage, and testicular atrophy. The report recommended "extreme care" in handling. Instead of extreme care, DuPont chose extreme production. Over the next forty years, the company would manufacture millions of pounds of PFOA, knowing from the very beginning that it was poison.

Industry had multiple studies showing adverse health effects at least 21 years before they were reported in public findings. The documents, uncovered through decades of litigation, revealed a pattern so damning that they inspired a Hollywood film, "Dark Waters," portraying attorney Robert Bilott's twenty-year battle against DuPont. But the movie only scratched the surface of a contamination story that would make Love Canal look like a minor spill.

The Washington Works facility in Parkersburg, West Virginia, became ground zero for one of the worst environmental crimes in American history. The settlement stemmed from the perfluorooctanoic acid (PFOA, or C8) contamination of drinking water in six water districts in two states near the DuPont Washington Works facility near Parkersburg, West Virginia. Between 1951 and 2003, DuPont dumped, pumped, and released 1.7 million pounds of PFOA into the Ohio River, another 7.5 million pounds into the air, and untold quantities into unlined landfills.

The C8 Cover-Up

The code name was innocuous: C8, for the eight-carbon chain that formed PFOA's backbone. But inside DuPont, C8 meant something else—a secret so valuable that protecting it justified any cost, including human lives. By 1978, DuPont knew that workers exposed to C8 had elevated cancer rates. By 1981, they knew it caused birth defects—two of seven pregnant workers in the Teflon division gave birth to children with facial deformities. The company's response? Transfer the women and buy their silence.

The most damning evidence came from DuPont's own scientists. In 1984, Gerald Kennedy, a DuPont veterinarian, reported that cattle drinking from streams near Washington Works were dying with grotesque tumors, blackened teeth, and fluorescent green organs. His supervisors told him to stop documenting his findings. When he persisted, he was reassigned. His final report was locked in a corporate archive, not to surface for twenty years.

By 1991, DuPont's internal documents showed they knew C8 was in the blood of the general population—not just workers, not just neighbors, but everyone. The chemical designed never to break down was doing exactly that, accumulating in every human on Earth. The National Institutes of Health concluded in a 2019 analysis that PFAS are in the blood of 97 percent of Americans. DuPont's response was to set an internal "community exposure guideline" at 150 parts per billion—3,750 times higher than the level their own scientists considered safe.

The Wilbur Tennant Case

The unraveling began with dead cows. Wilbur Tennant, a West Virginia cattle farmer, watched his herd of 200 die horrible deaths after DuPont began dumping waste on adjacent property. The cows' eyes turned eerie blue, their teeth black, their behavior aggressive and erratic. Tennant videotaped the evidence, performed amateur necropsies, kept samples in his freezer. When he couldn't get help locally—DuPont was the region's largest employer—he called a Cincinnati attorney named Robert Bilott.

Bilott was an unlikely crusader. He'd spent his career defending chemical companies, including DuPont. But Tennant's evidence was undeniable. During discovery, Bilott requested documents about something called "PFOA" mentioned in passing. DuPont delivered 110,000 documents, assuming no attorney would read them all. Bilott did, spending years piecing together the cover-up.

What he found was corporate malfeasance on an almost incomprehensible scale. A 2003 cohort study by DuPont, also filed with the EPA but not published elsewhere, shows that standardized mortality ratios were elevated and significant for bladder and kidney cancer. The company had conducted secret medical studies on workers, finding elevated cancer rates. They'd tested local water supplies, finding contamination at thousands of times safe levels. They'd even tested pregnant employees' blood, finding C8 in umbilical cord blood. And they'd hidden it all.

The Class Action and C8 Science Panel

The Tennant case led to something unprecedented: a class action lawsuit on behalf of 70,000 people whose water had been contaminated with C8. A multicomponent $107 million pretrial settlement between the Class and DuPont was reached. Complete settlement terms are part of the public record. Key provisions included the following: a $70 million award for Class members, of which $20 million was required to be used for health and education projects; provision of water treatment technologies to remove PFOA from the water supply of the six affected water districts; and formation of an independent panel of three scientific experts to carry out a community study and determine if there is a "probable link".

The C8 Science Panel, composed of three independent epidemiologists, conducted one of the largest health studies in history. The C8 Science Panel studied 55 health outcomes and, between 2011 and 2012, delivered four reports to the court concluding that PFOA was probably linked to six outcomes: kidney cancer, testicular cancer, ulcerative colitis, thyroid disease, hypercholesterolemia, and pregnancy-induced hypertension.

The findings were devastating for DuPont. Not only had C8 caused disease, but the company had known the risks for decades. In 2017, a settlement was reached involving about 3,500 claims made against DuPont involving water contamination of its chemical C8. A Chemours Teflon plant in Parkersburg, West Virginia released millions of pounds of the C8 chemical into the Ohio River and into the surrounding air, causing thousands of injuries, including kidney and testicular cancer, and ulcerative colitis.

The Chemours Shell Game

Facing mounting liabilities, DuPont executed a maneuver of breathtaking cynicism. In 2015, they spun off their Performance Chemicals division into a new company called Chemours, transferring not just the Teflon business but the environmental liabilities. While Chemours' shareholders received 19 percent of DuPont's total business operations under the deal, they received roughly two-thirds of DuPont's environmental liabilities and 90 percent of DuPont's pending litigation.

It was a corporate magic trick—make the liabilities disappear by giving them to someone else. Except Chemours immediately began drowning. The company DuPont claimed would thrive independently lost 90% of its stock value within months. When it spun off Chemours in 2015, DuPont had pegged the maximum liability in the multidistrict litigation involving the 3,500-plus PFOA cases at $128 million. The company settled 19 months later for $671 million, agreeing to pay half the settlement amount, and up to $125 million more toward costs of other PFOA-related litigation.

Chemours sued its former parent, claiming fraudulent conveyance. The litigation revealed DuPont's internal estimates had deliberately lowballed liabilities by factors of five or more. Eventually, the companies reached the settlement described earlier, but the damage to both companies' reputations was irreversible. DuPont had tried to wash its hands of PFAS, only to discover the chemicals were as persistent in courtrooms as in groundwater.

Superfund Sites and Forever Contamination

Beyond PFAS, DuPont's environmental legacy reads like a toxic atlas of America. The company operates or is responsible for over 170 Superfund sites—locations so contaminated they require federal intervention. The Pompton Lakes facility in New Jersey, mentioned earlier, is still being cleaned up after forty years and $100 million. The Newport, Delaware, pigment plant left behind lead and arsenic that will require remediation for generations.

Each site tells a story of expedience over safety. At the Necco Park site in Niagara Falls, DuPont dumped chemical waste directly into the ground from 1930 to 1970, creating a plume of contamination that reached the Niagara River. At the Edge Moor, Delaware facility, mercury contamination from chlorine production poisoned soil so thoroughly that it must be excavated and shipped to specialized disposal sites, one truckload at a time.

The true cost is incalculable. Communities near DuPont facilities show elevated rates of rare cancers, birth defects, and autoimmune diseases. Property values collapse when contamination is discovered. Entire watersheds become unusable. The economic impact runs to hundreds of billions; the human cost can't be quantified.