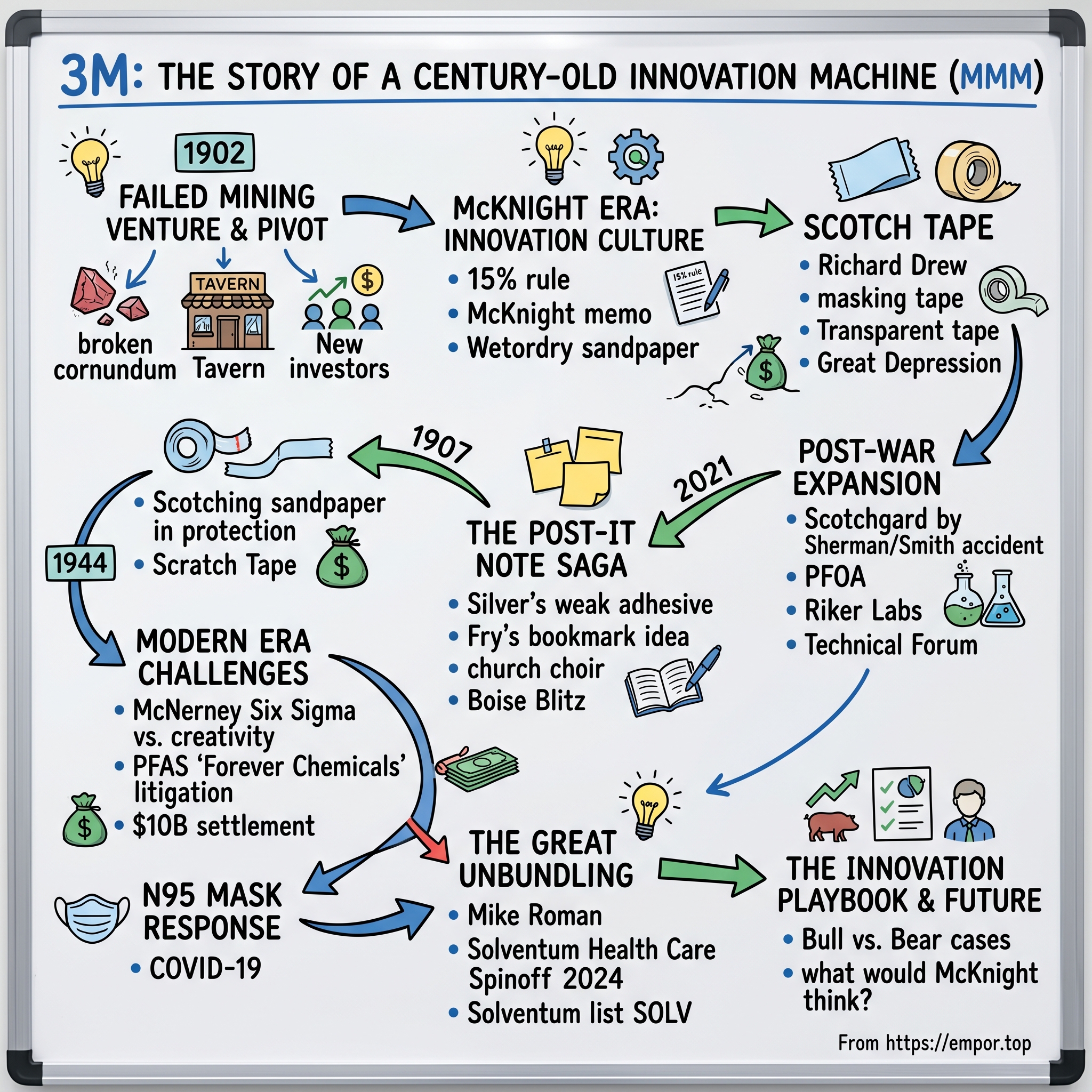

3M: The Story of a Century-Old Innovation Machine

I. Introduction & Episode Roadmap

Picture this: A worker in a 3M laboratory accidentally spills a fluorochemical compound on her tennis shoes in 1952. Instead of ruining them, the liquid beads up and rolls off, leaving no stain. That accident would become Scotchgard, generating billions in revenue over seven decades. This is the 3M story—where mistakes become markets, and failures forge fortunes.

In 2021, 3M generated $35.4 billion in total sales, producing over 60,000 products that touch nearly every aspect of modern life. From the Post-it Notes cluttering your desk to the N95 masks that protected healthcare workers during COVID-19, from the reflective sheeting on highway signs to the adhesives holding your smartphone together—3M's innovations are so ubiquitous they've become invisible.

But here's the extraordinary part: This global innovation powerhouse began as a spectacular failure. Five Minnesota businessmen set out to mine corundum for grinding wheels. They got the geology wrong. The "corundum" was worthless anorthosite. The company should have died in 1902.

Instead, that failed mining venture in Two Harbors, Minnesota, would transform into one of history's most prolific innovation machines. How did a company that couldn't identify the right minerals become synonymous with scientific breakthroughs? How did an organization built on a geological mistake create a culture that turned accidents into billion-dollar businesses?

This is a story about patient capital triumphing over quarterly capitalism. About giving researchers permission to fail. About a management philosophy so radical for its time that it still feels progressive today. It's about William McKnight's 15% rule—decades before Google made "20% time" famous. About Spencer Silver spending five years evangelizing a "solution looking for a problem" that would become Post-it Notes.

But it's also a darker tale. Of knowing about "forever chemicals" contaminating water supplies yet continuing to produce them. Of Six Sigma efficiency culture nearly strangling the creative chaos that built the company. Of $10 billion in environmental settlements that would have bankrupted most corporations.

We'll explore how 3M navigated each existential crisis—from the Great Depression to globalization, from environmental disasters to pandemic demands. We'll examine the recent Solventum healthcare spinoff, the largest restructuring in company history. And we'll ask whether a 122-year-old innovation culture can survive modern pressures for efficiency, sustainability, and quarterly earnings.

This journey takes us from Minnesota mine shafts to Shanghai skyscrapers, from sandpaper to semiconductors, from a five-person startup to a Dow 30 component. We'll meet the inventors, the leaders, and the accidents that built an empire. Welcome to 3M—where innovation isn't a department, it's a diagnosis.

II. The Failed Mining Venture & Early Pivot (1902–1916)

The Two Harbors Tavern was buzzing with speculation on a June evening in 1902. Five Minnesota businessmen—Henry Bryan, Hermon Cable, John Dwan, William McGonagle, and Dr. J. Danley Budd—huddled over geological surveys and financial projections. They'd discovered what they believed was a mountain of corundum on the North Shore of Lake Superior. Corundum, crystalline aluminum oxide, was the industrial diamond of its era—essential for grinding wheels that shaped America's industrial revolution. The five men founded the Minnesota Mining and Manufacturing Company, making their first sale on June 13, 1902.

There was just one catastrophic problem: They were wrong about literally everything.

The "corundum" wasn't corundum at all. It was anorthosite, a type of feldspar with the commercial value of decorative rock. Imagine building a gold mine, then discovering you'd been mining pyrite. The company's entire premise—its geology, its market, its future—evaporated with a single assay report.

By 1903, the company was hemorrhaging money. The Crystal Bay mine had consumed their initial $200,000 investment with nothing to show but worthless rock and broken dreams. Co-founder John Dwan, refusing to accept defeat, embarked on a desperate fundraising tour. He traveled to every major city within reach, soliciting funds in exchange for stock. Most doors slammed in his face.

But in 1905, two men changed everything. Edgar Ober, a Duluth railroad executive, and Lucius Ordway, a St. Paul plumbing supplier, saw something others missed. Not in the mine—that was obviously worthless—but in the determination of these failed miners. Ordway would eventually invest $250,000 (roughly $8 million today), essentially buying the company. His one condition: Stop mining. Start manufacturing.

The pivot was born of pure desperation. If they couldn't mine abrasives, maybe they could make them. The company limped to Duluth and began producing sandpaper. Even this was a disaster at first. Their inaugural product used Spanish garnet that fell off the paper. Customers returned it by the truckload. The company's sandpaper was so inferior that they had to sell it at a loss just to maintain any market presence.

Enter William L. McKnight in 1907. A 20-year-old bookkeeper hired at $11.55 per week, McKnight would reshape not just 3M but the entire concept of corporate innovation. But in 1907, he was just trying to keep accurate records of a company bleeding cash. He watched as the company struggled with quality control, with angry customers, with products that literally fell apart in users' hands.

The breakthrough came from failure analysis. Instead of blaming suppliers or customers, McKnight insisted on understanding why products failed. He discovered that the Spanish garnet was contaminated with olive oil from the shipping process. This insight led to the company developing its own quality control processes—revolutionary for a small manufacturer in 1908.

By 1910, the company had stabilized enough to move to St. Paul, where land was cheaper and rail connections better. McKnight, promoted to sales, pioneered a radical approach: He visited actual users in factories and workshops, watching them work, understanding their frustrations. This wasn't market research—that concept didn't exist yet. This was survival instinct crystallized into methodology.

The transformation accelerated when the company purchased a waterproof sandpaper patent from inventor Francis Okie. The "Wetordry" sandpaper, launched in 1914, could be used with water or oil, lasting longer and producing smoother finishes. For the first time, 3M had a product that was genuinely superior to competitors. Auto manufacturers, desperate for better finishing solutions for the booming car industry, became eager customers.

Finally, in 1916—fourteen years after its founding—3M achieved consistent profitability and paid its first dividend: six cents per share. The failed mining company had become a successful manufacturer. More importantly, it had developed a philosophy that would guide it for the next century: Listen to customers obsessively. Turn failures into data. Give inventors room to experiment.

The foundation was set, but nobody could have imagined what McKnight would build upon it. The failed corundum mine had inadvertently unearthed something far more valuable than minerals—a methodology for innovation that would generate thousands of patents and billions in revenue.

III. McKnight Era: Building the Innovation Culture (1916–1966)

William McKnight stood before 3M's salesforce in 1921 with a radical proposition: "Listen to anyone with an idea." This wasn't feel-good management speak. McKnight, now vice president, was encoding DNA into 3M's corporate genome that would mutate the company from a sandpaper maker into an innovation machine. His philosophy was deceptively simple yet revolutionary for its time: Hire good people, give them room to fail, and get out of their way.

The first test of this philosophy came from Richard Drew, a 23-year-old lab assistant with barely two years at the company. In 1923, Drew was delivering sandpaper samples to auto body shops when he noticed painters struggling with the two-tone paint jobs that had become fashionable. They used newspapers, butcher paper, and heavy adhesive tape to mask off sections, but removing these materials often pulled off fresh paint, forcing complete repaints.

Drew promised to invent a solution. He had no authorization. No budget. No relevant expertise. Under traditional management, he would have been fired for overstepping. McKnight told him to proceed.

For two years, Drew experimented with different adhesives, backing materials, and coating techniques. His superiors repeatedly ordered him to return to sandpaper work. Drew nodded politely and kept experimenting. This was "bootlegging"—using company resources for unauthorized projects—and McKnight deliberately turned a blind eye. In 1925, Drew delivered masking tape, 3M's first non-abrasive product. Auto painters called it "Scotch tape" because it originally had adhesive only on the edges (the full coating was deemed too expensive). The name stuck, though 3M quickly added adhesive across the entire width when customers complained.

The real breakthrough came in 1930. Drew, now emboldened, created transparent cellophane tape—what we know as Scotch tape. The timing seemed catastrophic. The Great Depression had begun. Families were struggling to eat. Who would buy transparent tape?

Everyone, it turned out. In an era when nothing could be wasted, transparent tape let people repair everything—torn books, cracked windows, ripped clothing. It was the perfect Depression product: cheap, versatile, essential. During the 1930s, 3M funneled some 45 percent of its profits into new product research; consequently, the company tripled in size during the worst decade American business had ever endured.

McKnight established what would become known as the "15% rule"—researchers could spend 15% of their work time on projects of their own choosing, no questions asked, no approval needed. This wasn't corporate benevolence; it was calculated strategy. McKnight understood that innovation couldn't be scheduled or commanded. It had to be cultivated.

The rule had teeth. When Drew's supervisor ordered him to stop working on tape and return to sandpaper improvements, Drew ignored the order. When confronted, McKnight backed Drew, not the supervisor. The message rippled through 3M: Bootlegging wasn't just tolerated; it was protected.

In 1940, McKnight codified his philosophy in a memo that would guide 3M for decades: "Mistakes will be made, but if a person is essentially right, the mistakes he or she makes are not as serious in the long run as the mistakes management will make if it is dictatorial and undertakes to tell those under its authority exactly how they must do their job."

This wasn't Silicon Valley in 2010. This was industrial Minnesota in 1940. While competitors focused on efficiency and standardization, McKnight built a company where a lab assistant could ignore direct orders and become a hero for it.

The results spoke volumes. Between 1916 and 1929, 3M's sales grew from $264,000 to $5.4 million. Even during the Depression, when industrial production fell by half nationwide, 3M's sales grew from $5.5 million in 1930 to $22 million by 1939. The company had found a formula: patient capital plus creative freedom equals exponential growth.

The company moved to Saint Paul in 1910, where it remained for 52 years before outgrowing the campus and moving to its current headquarters at 3M Center in Maplewood, Minnesota, in 1962. The new headquarters wasn't just bigger; it was designed as an innovation campus, with laboratories intentionally placed near each other to encourage the cross-pollination of ideas.

McKnight stepped down as CEO in 1966 but remained chairman until 1970. By then, 3M had become exactly what he'd envisioned: not a company that made products, but a company that solved problems. The culture he built—where failure was data, where curiosity trumped hierarchy, where patience beat pressure—had become 3M's greatest competitive advantage.

The mining company that couldn't identify minerals had transformed into a technology company that turned accidents into industries. McKnight didn't just save 3M; he invented a new way to run a corporation. Decades before "innovation culture" became a buzzword, he'd built one that actually worked.

IV. Post-War Expansion & Diversification (1945–1980)

The C-47 transport plane descended through German flak over Normandy in June 1944, its fuselage riddled with holes. But the aircraft kept flying. The secret: 3M's pressure-sensitive aluminum tape, hastily applied over battle damage, held the plane together long enough to complete its mission. This wasn't what Richard Drew had envisioned when he invented adhesive tape, but war has a way of revealing unexpected applications.

World War II transformed 3M from a clever manufacturer into a strategic asset. The company's researchers, freed from commercial constraints by military contracts, pushed into territories they'd never imagined. They developed reflective materials for road signs that helped convoys navigate in blackouts. They created sound-dampening materials for submarines. They produced sandpaper so precise it could polish optical lenses for bombsights.

The war taught 3M a crucial lesson: Their core competence wasn't making specific products—it was manipulating materials at the molecular level. They were platform technologists before anyone used that term.

In 1947, 3M began producing perfluorooctanoic acid (PFOA), an industrial surfactant and chemical feedstock, by electrochemical fluorination. At the time, fluorochemistry seemed like magic—compounds that repelled both water and oil, that could make anything stain-proof. Nobody questioned what happened when magic leaked into groundwater.

The real breakthrough came by accident in 1952. Patsy Sherman, one of the few female chemists at 3M, was working on a new rubber for jet fuel hoses when her lab assistant spilled a fluorochemical compound on her tennis shoes. The original formula for Scotchgard, a water repellent applied to fabrics, was discovered accidentally in 1952 by 3M chemists Patsy Sherman and Samuel Smith. Sales began in 1956.

Sherman noticed something odd: The spill wouldn't come off, but neither would anything stick to it. Water beaded up. Oil rolled off. Dirt wouldn't adhere. Her ruined shoes had become unstainable. Where others saw a mess, Sherman saw a market.

But turning laboratory accident into commercial product took four years. The chemistry was complex—creating a spray that would bond permanently to fabric while repelling everything else required innovations in both molecular design and application technology. Sherman and her team had to invent new testing methods, new production processes, new quality controls.

Scotchgard launched in 1956 into a market that didn't know it needed fabric protection. 3M's marketers positioned it as insurance for an aspirational lifestyle—protecting the wall-to-wall carpeting and upholstered furniture that defined suburban success. By 1960, Scotchgard was generating tens of millions in revenue.

The post-war era saw 3M systematically expanding through both innovation and acquisition. In the late 1950s, 3M produced the first asthma inhaler, but the company did not enter the pharmaceutical industry until the mid-1960s with the acquisition of Riker Laboratories. The Riker acquisition in 1970 marked 3M's entry into pharmaceuticals, bringing both drug development capabilities and FDA expertise.

But the company's most important post-war innovation might have been organizational. In 1948, 3M created its Technical Forum, where researchers from different divisions presented their work to colleagues. This wasn't typical corporate knowledge-sharing—it was designed serendipity. A researcher working on surgical tapes might learn about adhesive innovations from the automotive division. A fluorochemist might discover applications in electronics manufacturing.

The international expansion strategy reflected similar thinking. Rather than simply exporting products, 3M established local research centers in major markets. The philosophy: Japanese customers had different problems than American ones, requiring different solutions. By 1970, international sales exceeded $500 million, with manufacturing in 40 countries.

The numbers told the story of transformation. Revenue grew from $163 million in 1950 to $1.3 billion in 1970. The product catalog expanded from hundreds to thousands of items. But the real change was strategic. 3M had evolved from solving specific problems to creating technology platforms that could address entire categories of challenges.

As of 2012, 3M was one of the 30 companies included in the Dow Jones Industrial Average, added on August 9, 1976. The Dow inclusion marked Wall Street's recognition that 3M had become essential infrastructure for the global economy.

Yet this golden age contained seeds of future crisis. Those miraculous fluorochemicals that made Scotchgard possible? They didn't break down. Ever. They accumulated in water supplies, in wildlife, in human bloodstreams. The company that prided itself on solving problems had inadvertently created one that would cost billions to address.

By 1980, 3M stood at the apex of American industrial innovation. But the company built on patient experimentation was about to face a world demanding quarterly results. The culture that turned accidents into breakthroughs would soon meet an efficiency revolution that viewed accidents as waste. The stage was set for the Post-it Note—3M's last great accident—and the cultural collision that would follow.

V. The Post-it Note Saga: Silver & Fry's Serendipity (1968–1980)

Spencer Silver stood before yet another unreceptive audience in 1973, holding up a small yellow square. "Imagine," he said, "a note that sticks to anything but can be removed without damage." The 3M executives stared blankly. After five years of evangelizing his failed adhesive, Silver was used to the silence.

In 1968, Spencer Silver was a senior scientist working to develop new classes of adhesives at 3M when he discovered an acrylic adhesive with unique properties. It was formed of tiny spheres that provided a pressure-sensitive adhesive with a high level of tack but a low degree of adhesion. Silver had been trying to create a super-strong adhesive for aircraft construction. Instead, he'd invented an adhesive that barely stuck at all.

Under normal circumstances, this would have been filed away as another failed experiment. But Silver saw something others didn't. His adhesive was reusable—it could stick, unstick, and stick again hundreds of times. It left no residue. It didn't damage surfaces. This wasn't a failed strong adhesive; it was a successful weak one.

The problem: Nobody knew what to do with it. Silver spent years giving seminars within 3M, demonstrating his adhesive to anyone who would listen. He coated bulletin boards with it, creating surfaces where papers could be temporarily attached. He proposed spray-on adhesive for photo albums. Marketing killed every idea. Who would buy an adhesive that didn't really stick?

Enter Art Fry, a chemical engineer in 3M's tape division laboratory and a member of his church choir. Fry was frustrated by the fact that when he stood and opened his hymnal to sing, the paper bookmarks that he used in his hymnal to mark the songs on the program would slip out of sight or even onto the floor. In a moment of insight that has become legendary in the realm of contemporary invention, Fry, musing during a rather boring sermon, realized that Silver's reusable adhesive would provide his bookmarks with precisely the temporary anchoring he required.

That Sunday morning epiphany in 1974 launched a six-year journey that would test every principle of 3M's innovation culture. Fry didn't just need Silver's adhesive; he needed to engineer an entirely new product category. The adhesive had to be applied to paper in exactly the right amount—too much and it would tear when removed, too little and it wouldn't stick at all.

Years of perfecting design and production followed. Major challenges involved creating equipment and processes to manufacture the notes, as well as the problem of getting the adhesive to stay in place and maintain a consistent range of adhesion. The manufacturing challenge was enormous. No equipment existed to apply adhesive to just one edge of paper squares. Fry had to invent it, literally building machinery in his basement that he later had to knock out walls to remove.

But the biggest challenge was conceptual. 3M's marketing department couldn't figure out how to sell Post-it Notes. Their first attempt in 1977, marketed as "Press 'n Peel," failed spectacularly in four test cities. The problem wasn't the product—it was that customers couldn't imagine why they needed it.

The breakthrough came from desperation disguised as genius. In 1978, 3M's Joe Ramey flew to Richmond, Virginia, one of the failed test markets, with boxes of free samples. He walked into offices and handed out Post-it Notes to secretaries, executives, anyone who would take them. "Just try them," he said. "Use them for a week."

The Boise Blitz, as it became known when repeated in Boise, Idaho, achieved 90% reorder rates from customers who tried the product. People who couldn't imagine needing Post-it Notes suddenly couldn't imagine living without them. They used them for reminders, for bookmarks, for routing notes on documents, for a thousand applications nobody had anticipated.

Post-it Notes were introduced nationally in the United States in 1980. Within two years, they were named 3M's Outstanding New Product. Within four years, they were generating over $100 million in revenue. The product that nobody wanted became the product nobody could live without.

The Post-it Note success contained profound lessons about innovation. First, breakthrough products often create their own markets—customers can't want what they can't imagine. Second, patient capital matters—twelve years elapsed between Silver's discovery and national launch. Third, failure is data—the adhesive that failed at its intended purpose succeeded beyond imagination at an unexpected one.

But the Post-it saga also marked an ending. It was 3M's last great serendipitous innovation, the final triumph of McKnight's patient, experimental culture. By 1980, Wall Street was demanding efficiency, not experimentation. Management consultants were preaching Six Sigma, not serendipity. The company that turned accidents into billions was about to meet leaders who viewed accidents as defects to be eliminated.

Art Fry retired in 1993, and Spencer Silver in 1996. Both watched as 3M transformed from a laboratory that happened to have factories into a factory that happened to have laboratories. The Post-it Note remained 3M's most recognizable product, a billion-dollar business built on failure. But it was also a monument to a way of innovating that the company would struggle to recapture.

VI. Modern Era Challenges: Innovation vs. Litigation (1990s–2020s)

James McNerney strode into 3M headquarters in January 2001 with a mandate to fix what Wall Street saw as broken: a sprawling conglomerate with declining margins and unfocused research. The former General Electric executive, trained in Jack Welch's school of ruthless efficiency, looked at 3M's chaotic innovation process and saw waste. Researchers spending 15% of their time on pet projects? Inefficient. Thousand of SKUs with tiny market shares? Irrational. A culture that celebrated productive failure? Unacceptable.

2001: GE veteran W. James McNerney, Jr., takes over as chairman and CEO, becoming the first outsider at the helm in the company's history. McNerney introduced Six Sigma with evangelical fervor. Every process would be measured, mapped, and optimized. Variation would be eliminated. Defects would approach zero.

The efficiency gains were immediate and impressive. Operating margins improved from 17% to 23% within three years. Inventory turns accelerated. Capital allocation tightened. Wall Street loved it—3M's stock rose 20% in McNerney's first year.

But something else happened. Patent applications began declining. The pace of breakthrough innovations slowed. Researchers complained that Six Sigma's emphasis on predictable outcomes was antithetical to experimental research. How do you Six Sigma your way to an accident that becomes a billion-dollar business?

One researcher, speaking anonymously to BusinessWeek in 2007, captured the cultural collision: "You can't schedule innovation. You can't tell researchers, 'I need a breakthrough by Q3.' McNerney brought discipline, but he almost killed the patient to cure the disease."

McNerney left for Boeing in 2005, but his efficiency revolution had lasting impact. His successor, George Buckley, tried to restore balance, famously declaring, "Invention is by its very nature a disorderly process." But the damage to 3M's free-wheeling culture was hard to reverse. The company that once gave researchers unlimited time to pursue hunches now demanded detailed project justifications and ROI projections.

Meanwhile, a darker challenge was emerging from 3M's past. Those miracle fluorochemicals that created Scotchgard and dozens of other products? Scientists were discovering they were everywhere—in Arctic ice, in eagle eggs, in human blood samples from around the world. PFAS (per- and polyfluoroalkyl substances) didn't break down. Ever. They accumulated in organisms and ecosystems, earning the nickname "forever chemicals."

Internal 3M documents revealed through litigation showed the company knew about PFAS persistence and toxicity concerns as early as the 1970s. A 1978 internal memo noted PFAS in workers' blood. A 1983 study found PFAS in fish downstream from 3M plants. By the 1990s, internal research showed potential links to cancer and developmental problems.

In June 2023, 3M reached a settlement to pay more than $10 billion to US public water systems to resolve claims over the company's contamination of water with PFASs (so-called forever chemicals). It has been revealed that the company knew of the health harms of PFAS in the 1990s, yet concealed these harms and continues to sell contaminated products.

The PFAS crisis represented an existential challenge. This wasn't a defective batch of products or a single environmental incident. This was decades of manufacturing and selling chemicals that 3M knew were accumulating in the environment and human bodies. The company that prided itself on solving problems had created one that might take centuries to resolve.

The COVID-19 pandemic briefly restored 3M's reputation as an essential innovator. When N95 mask shortages threatened healthcare systems in 2020, 3M ramped production from 50 million to 95 million masks per month within weeks. The company's Aberdeen, South Dakota plant ran 24/7, with workers volunteering for extra shifts. President Trump invoked the Defense Production Act to prevent 3M from exporting masks, leading to a public confrontation over global supply chains and humanitarian obligations.

But even this heroic effort couldn't escape controversy. Price gouging accusations flew as N95 masks that typically sold for $1 reached $7 on secondary markets. 3M insisted it hadn't raised prices, but the reputational damage was done. The company that invented the N95 in 1972 was accused of profiteering from a pandemic.

By 2022, 3M faced a stark reality. Environmental liabilities potentially exceeding $100 billion. Growth rates lagging competitors. A bloated structure with 95,000 employees across dozens of business units. The innovation culture that created Post-it Notes and thousands of other products had been suffocated by efficiency metrics and risk management.

CEO Mike Roman announced the solution: Break up the company. The healthcare division, responsible for $8.6 billion in revenue, would be spun off as Solventum. It was an admission that 3M's conglomerate model—where innovations in one division sparked breakthroughs in another—no longer worked in an era demanding focused expertise and predictable returns.

The modern 3M faced an impossible balancing act: Restore innovation culture while managing massive environmental liabilities. Generate growth while eliminating risk. Create breakthroughs while meeting quarterly targets. The company that once turned mining failure into manufacturing triumph now struggled to turn its own history into a viable future.

VII. The Great Unbundling: Solventum Spinoff (2022–2024)

Mike Roman faced 3M's board of directors on a gray November morning in 2022 with a proposal that would have been heresy to William McKnight: Dismember the company. After 120 years of growth through diversification, 3M would split itself apart. The healthcare division—the crown jewel that generated 27% of profits—would become an independent company called Solventum.

The logic was compelling yet painful. Healthcare operated in a fundamentally different universe than industrial adhesives or consumer products. It required specialized regulatory expertise, distinct R&D cycles, and dedicated sales channels. While a Post-it Note could go from concept to market in months, a new surgical product might take a decade of clinical trials.

3M (NYSE: MMM) today announced that its Board of Directors has approved the planned spin-off of its Health Care business, which will be known as Solventum Corporation. The company is anticipated to spin off from 3M on April 1, 2024, and has applied to list on the New York Stock Exchange as "SOLV."

The numbers behind Solventum were substantial. A leading global healthcare company innovating at the intersection of health, material, and data science, with $8.2 billion in revenue in 2023. Solventum will serve an approximate $93 billion global addressable market anticipated to grow at 4-6% through 2026. The company would instantly become a major player in medical technology, with 23,000 employees across four divisions: MedSurg, Dental Solutions, Health Information Systems, and Purification and Filtration.

But the spinoff wasn't just about operational efficiency. It was about financial engineering in the face of existential threats. 3M's environmental liabilities—those PFAS settlements—created a $10+ billion overhang that depressed the company's valuation. By spinning off healthcare, 3M could create value through division. Solventum would be free from PFAS liability, while 3M could focus resources on managing its environmental challenges.

3M's Board of Directors approved the distribution to 3M shareholders of 80.1% of the outstanding shares of Solventum. 3M will retain 19.9% of the outstanding shares of Solventum common stock, which will be monetized within five years following the spin-off. This structure allowed 3M to capture immediate value while maintaining future upside.

The separation process revealed just how intertwined 3M's businesses had become over decades. Solventum products relied on 3M's adhesive technologies. 3M's manufacturing expertise supported Solventum's production. The companies shared research facilities, IT systems, supply chains, even cafeterias. Untangling this took 18 months and cost hundreds of millions.

Bryan Hanson, appointed CEO of Solventum, embodied the cultural shift. A healthcare industry veteran from Medtronic and Zimmer Biomet, Hanson had never worked at 3M. His mandate: Build a pure-play healthcare company focused on predictable growth, not serendipitous innovation. No 15% time. No patient capital for indefinite research. Just disciplined execution in defined markets.

The employee reaction was mixed. Healthcare division workers welcomed independence from 3M's industrial legacy and environmental baggage. But many mourned the loss of 3M's innovation ecosystem. A Solventum researcher wouldn't stumble upon adhesive innovations from the automotive division that might revolutionize wound care. The cross-pollination that created unexpected breakthroughs would end.

Wall Street's initial response was positive but measured. On April 1, 2024, Solventum began trading at $28 per share, giving it a market capitalization of approximately $13 billion. Analysts praised the focused strategy but questioned whether Solventum could maintain 3M's innovation pace without its parent's vast R&D resources.

For 3M, the spinoff represented both liberation and loss. Liberation from the complexity of healthcare regulation and the need to compete with specialized medical technology companies. Loss of stable, high-margin revenue that had cushioned volatility in industrial markets.

Post-spinoff, 3M announced aggressive restructuring. Six thousand jobs would be eliminated. Dozens of facilities would close. R&D spending would focus on core industrial technologies. The company that once celebrated productive failure would now optimize for predictable returns.

The strategic rationale was clear: Create two stronger companies from one struggling conglomerate. Solventum would pursue growth in healthcare without industrial distractions. 3M would restore focus on materials science without healthcare complexity. Both would have cleaner equity stories for investors.

But something ineffable was lost in the division. The 3M that emerged from the spinoff was smaller, more focused, but also less ambitious. The company that once turned accidents in one division into breakthroughs in another had chosen efficiency over serendipity. The great unbundling wasn't just a corporate restructuring—it was an admission that 3M's model of innovation through integration no longer worked in modern capital markets.

As Solventum began its independent journey and 3M faced its environmental reckoning, a question lingered: Had 3M saved itself by splitting apart, or had it destroyed the very connections that once made it great? The answer would only come with time, but the century-old experiment in corporate innovation had fundamentally changed course.

VIII. The Innovation Playbook: How 3M Creates

Picture a 3M researcher in 1975, spending her Friday afternoons experimenting with microspheres that nobody asked for, using equipment nobody authorized, pursuing a goal nobody defined. Now picture her explaining this to a Six Sigma black belt in 2005, complete with control charts and ROI projections. The tension between these two images explains both 3M's historic success and its modern struggles.

The 15% rule, instituted by McKnight and still officially in place today, represents something more profound than time allocation. It's a philosophical statement: Not all value can be planned. When Spencer Silver spent years developing his repositionable adhesive, he wasn't filling a market need or solving a customer problem. He was following curiosity. The fact that this curiosity eventually generated billions in Post-it Note revenue was unforeseeable and unplannable.

But here's what made 3M's innovation system truly distinctive: It wasn't just about individual creativity. It was about institutional patience. When Silver's adhesive found no immediate application, 3M didn't kill the project or reassign him. The company maintained his research for five years before Art Fry's hymnal problem created an application. Most companies can't hold their breath that long.

The cross-pollination between divisions was deliberate architecture, not happy accident. 3M's Technical Forum, established in 1951, required researchers to present their work to colleagues from other divisions. A chemist working on dental adhesives might learn about innovations in automotive tape that could revolutionize tooth bonding. This wasn't efficiency—hauling researchers away from their labs for presentations—but it was effective.

Consider how Scotchgard emerged. Sherman was working on rubber for jet fuel hoses when the spill occurred. The fluorochemistry expertise came from 3M's work on industrial coatings. The application technology borrowed from the tape division. The marketing insights came from consumer products. No single division could have created Scotchgard, but 3M's structure made the combination possible.

The company also mastered the art of patient capital. When 3M entered a new market, it expected to lose money for five to seven years. The pharmaceutical division lost money for a decade before becoming profitable. The electronics materials business took fifteen years to generate meaningful returns. This wasn't poor management—it was strategic patience.

Technology platforms, not single products, drove 3M's expansion. The company didn't just make tape; it mastered adhesion science. It didn't just make sandpaper; it understood abrasion at the molecular level. These platforms could spawn hundreds of products across dozens of markets. When 3M developed fluorochemistry capabilities, it yielded products from fabric protection to semiconductor manufacturing.

The role of failure at 3M deserves special attention. Failure wasn't just tolerated; it was data. The adhesive that failed to be super-strong became Post-it Notes. The surgical tape that didn't stick well enough became gentle-removal products for sensitive skin. The waterproofing that was too expensive became a premium automotive coating. 3M turned more failures into fortunes than perhaps any company in history.

Compare this with modern innovation models. Google's famous 20% time was inspired by 3M but lacks the institutional support structure. Employees get time for projects but not patient capital for five-year development cycles. Bell Labs produced remarkable innovations but struggled to commercialize them. Xerox PARC invented the future but gave it away. 3M uniquely combined invention with commercialization, patience with profits.

The company's approach to acquisitions also reflected its innovation philosophy. 3M didn't buy companies for their products but for their capabilities. The Riker Laboratories acquisition brought pharmaceutical expertise that enhanced 3M's medical adhesives. The Imation spinoff shed commodity businesses while preserving innovation capabilities. Each transaction was evaluated not just for financial return but for innovation potential.

Yet the innovation playbook that worked for a century began failing in the 2000s. Markets demanded predictability. Shareholders wanted efficiency. Regulators required documentation. The freewheeling culture that produced breakthroughs also produced environmental disasters. The same patient capital that enabled Post-it Notes also allowed PFAS accumulation.

Modern 3M faces an existential question: Can programmatic innovation replace serendipitous discovery? The company now uses artificial intelligence to predict molecular behaviors, data analytics to identify market opportunities, and stage-gate processes to manage development. These tools are powerful but mechanistic. They can optimize known pathways but struggle to imagine unknown ones.

The deeper challenge is cultural. The researchers who spent decades at 3M, accumulating deep expertise while pursuing patient experiments, are retiring. Their replacements, trained in lean startup methodologies and agile development, expect faster cycles and clearer metrics. The institutional memory of how to turn accidents into industries is fading.

Some argue 3M's innovation model was a historical artifact, possible only in an era of patient capital and limited competition. Others contend the company abandoned its model too quickly, sacrificing long-term breakthrough potential for short-term efficiency gains. The truth likely lies between: 3M's innovation playbook was brilliant for its time but requires fundamental reimagination for the current era.

What remains clear is that 3M wrote the definitive playbook for corporate innovation in the 20th century. Whether anyone—including 3M itself—can write an equally effective playbook for the 21st century remains an open question.

IX. Business Model & Financial Architecture

3M's financial architecture resembles a Victorian mansion—built over generations, with countless additions, hidden passages, and load-bearing walls that can't be removed without risking collapse. Understanding how this $48 billion revenue machine operates requires examining both its elegant design and its structural vulnerabilities.

3M's stock ticker symbol is MMM and is listed on the New York Stock Exchange, Inc. (NYSE), the Chicago Stock Exchange, Inc., and the SIX Swiss Exchange. The MMM ticker has become synonymous with industrial aristocracy—a dividend aristocrat that increased its payout for 64 consecutive years before finally holding flat in 2024 amid PFAS settlements.

The revenue diversification that McNerney tried to eliminate turned out to be 3M's greatest strength. In 2023, no single customer represented more than 10% of sales. The company served everything from aerospace (premium margins) to consumer products (volume scale). When automotive production crashed during chip shortages, medical technology compensated. When healthcare faced pandemic disruption, industrial adhesives boomed from e-commerce packaging demand.

Consider the margin architecture. 3M's gross margins historically ranged from 45-50%, extraordinary for an industrial company. The secret: proprietary technology commanding premium prices. A roll of Scotch tape might cost pennies to produce but sells for dollars because customers trust the brand. An automotive adhesive might carry 70% margins because switching costs are prohibitive—no automaker risks production lines to save basis points on tape.

But this margin structure depends on innovation moats. When 3M's new product vitality index (percentage of sales from products introduced in the last five years) fell from 35% to 25% during the McNerney era, margins compressed. Commoditization is death for a company built on proprietary technology.

The R&D spending philosophy reveals strategic tensions. 3M invests approximately 5.5% of sales in R&D, about $2.6 billion annually. This seems substantial until compared with pharmaceutical companies (15-20%) or software companies (20-30%). The challenge: 3M competes in hundreds of markets, each requiring specialized research. That $2.6 billion gets spread thin—perhaps too thin to maintain leadership everywhere.

Capital efficiency metrics tell a mixed story. Return on invested capital (ROIC) averaged 20% during the growth years but declined to 13% by 2023. The culprit: accumulated acquisitions and expanding asset base without proportional profit growth. 3M owns 125 manufacturing facilities globally—massive fixed costs that provide scale advantages but limit flexibility.

The global distribution strategy reflects both strength and complexity. 3M products reach customers through multiple channels: direct sales to large accounts, distributors for fragmented markets, retail for consumer products, and e-commerce for specialty items. This omnichannel approach provides resilience but requires enormous coordination. A single product might have different prices, packages, and specifications across dozens of markets.

Channel strategy varies by division. Industrial products rely on technical sales engineers who embed with customers, solving problems that create switching costs. Consumer products depend on retail relationships and brand pull. Healthcare products require navigating complex reimbursement systems. Each channel demands different capabilities, investments, and metrics.

The pricing power that underpinned 3M's model faces new pressures. Amazon enables instant price comparison. Chinese competitors offer adequate quality at fraction of 3M's prices. Industrial customers consolidate purchasing to negotiate harder. The premium pricing that funded patient R&D becomes harder to sustain.

Working capital management reveals operational excellence despite strategic challenges. 3M turns inventory 4.5 times annually—impressive for a company making 60,000 products. Days sales outstanding average 54 days, reflecting strong collection despite global complexity. The company generates over $5 billion in free cash flow annually, though PFAS settlements will consume much of this for years.

The dividend aristocrat status carries both pride and burden. 3M paid $3.3 billion in dividends in 2023, yielding approximately 6%—attractive but reflecting market skepticism about growth. The 64-year streak of increases created expectation that constrains capital allocation. Management can't cut the dividend without triggering institutional exodus, even if reinvestment might generate better returns.

Geographic revenue distribution shows both opportunity and challenge. International sales represent 53% of total revenue, with Asia-Pacific growing fastest. But this exposes 3M to currency fluctuations, trade tensions, and regulatory variations. A product approved in the US might require years of additional testing for Chinese markets. Brexit disrupted European supply chains. Taiwan tensions threaten semiconductor materials business.

The financial architecture reveals a fundamental tension: 3M operates like a portfolio of businesses that occasionally benefit from shared technology, rather than an integrated innovation engine where breakthroughs in one area catalyze advances in others. The Solventum spinoff acknowledged this reality—financial markets value focus over synergy.

Post-spinoff, 3M's financial profile clarifies but doesn't necessarily improve. Revenue drops to roughly $40 billion. Margins might expand from eliminated complexity, but innovation investment capacity shrinks. The company becomes easier to understand but not necessarily better positioned to compete.

The financial model that worked for a century—patient capital funding long-term research, generating proprietary products commanding premium prices—faces structural headwinds. Markets demand predictability. Competitors copy innovations faster. Customers resist pricing power. Environmental liabilities consume cash. The elegant Victorian mansion needs renovation, but its residents can't agree whether to restore or rebuild.

X. Analysis & Bear vs. Bull Case

The investment case for 3M resembles a Rorschach test—bulls and bears look at identical facts and reach opposite conclusions. Is this a wounded giant poised for recovery or a declining empire managing retreat? The answer depends on which version of 3M you believe will emerge from current challenges.

The Bull Case: Reinvention and Focus

Bulls argue 3M is executing the most significant transformation in its history, shedding bureaucracy while preserving innovation DNA. The Solventum spinoff isn't retreat—it's strategic focus. By separating healthcare, 3M eliminates complexity that obscured value. The remaining company can concentrate resources on core industrial technologies where competitive advantages remain strong.

The PFAS settlement, while painful, provides closure. The $10+ billion payment is manageable given 3M's cash generation, and it removes an existential uncertainty. Markets hate unknown liabilities more than known costs. With PFAS largely resolved, management can focus on operations rather than litigation.

The innovation pipeline, though diminished from glory days, still produces. Recent breakthroughs in automotive electrification materials, renewable energy adhesives, and sustainable packaging solutions address massive growth markets. The company's 125,000 patents provide a deep reservoir of potentially monetizable technology.

Valuation metrics support the bull case. At 10x forward earnings, 3M trades at historic lows relative to industrial peers. The 6% dividend yield provides income while waiting for recovery. If management achieves targeted 4-6% organic growth and margin expansion, the stock could double from current levels.

China recovery presents enormous opportunity. As the world's largest manufacturing economy reopens post-COVID, demand for 3M's industrial products should surge. The company's established presence and relationships in Asia provide competitive advantages that new entrants can't replicate.

The restructuring plan shows serious intent. Cutting 6,000 jobs and closing facilities isn't cosmetic—it's structural change. Management targets $900 million in annual savings, which could add $0.75 to earnings per share. Combined with share buybacks enabled by improved cash flow, EPS could grow double-digits even with modest revenue growth.

The Bear Case: Structural Decline

Bears see a company whose best days are permanently behind it. The innovation culture that created 3M's moat has been irreversibly damaged. You can't Six Sigma your way to breakthrough innovation, then suddenly rediscover serendipity. The researchers who understood patient experimentation have retired, replaced by efficiency experts.

Environmental liabilities extend beyond PFAS. 3M faces ongoing litigation over combat earplugs, respirator defects, and other product liability claims. The $10 billion PFAS settlement might be just the beginning. As environmental standards tighten globally, cleanup costs could escalate beyond current reserves.

Competition intensifies across every segment. Chinese manufacturers offer adequate quality at 30-50% lower prices. Specialized competitors target 3M's most profitable niches. Amazon enables instant price comparison that erodes pricing power. The moats that protected 3M's margins are draining.

The Solventum spinoff removed the fastest-growing, highest-margin business. Healthcare generated 27% of profits despite being 23% of revenue. Without it, 3M becomes more cyclical, more commodity-exposed, more vulnerable to industrial downturns. The company kept the challenging businesses and spun off the gem.

Growth prospects appear limited. Organic revenue growth averaged 1-2% over the past decade, below inflation. The company operates in mature markets with limited expansion potential. Electric vehicles might reduce demand for traditional automotive products. Digitalization threatens physical office supplies. Where does growth come from?

Management credibility suffers from repeated disappointments. Guidance cuts, restructuring charges, and strategic reversals have become routine. The board that hired McNerney to impose efficiency, then Buckley to restore innovation, then Roman to split the company shows no consistent vision. Why believe this transformation succeeds when others failed?

The Verdict: A Value Trap or Opportunity?

The truth likely lies between extremes. 3M isn't disappearing—its products remain essential to global industry. But neither will it recapture the innovation magic that created Post-it Notes and thousand other breakthroughs. The company faces a long, grinding transformation from innovation aristocrat to efficient operator.

For investors, timeframe matters enormously. Short-term traders might profit from volatility around earnings and settlement announcements. Income investors can collect attractive dividends while waiting. But growth investors seeking the next innovation breakthrough should look elsewhere.

The fundamental question isn't whether 3M survives—it will. It's whether 3M can generate returns exceeding its cost of capital while managing environmental liabilities and competitive pressures. The answer depends on execution quality, market conditions, and whether management can balance efficiency with innovation.

The bull-bear debate ultimately reflects different beliefs about corporate regeneration. Can a 122-year-old company fundamentally reinvent itself? Can innovation culture be restored once destroyed? Can patient capital coexist with quarterly capitalism? 3M's next decade will answer these questions, not just for itself but for industrial America.

XI. Lessons for Founders & Investors

The 3M story reads like a business school curriculum compressed into a single company: pivoting from failure, building innovation culture, managing complexity, navigating disruption, and confronting unintended consequences. For founders building the next century-long enterprise and investors evaluating them, 3M offers lessons both inspiring and cautionary.

Building Culture That Survives Leadership Changes

William McKnight didn't just create policies; he encoded DNA. The 15% rule survived because it became identity, not just practice. Employees didn't follow the rule because management mandated it—they followed it because "that's how 3M works." This cultural embedding requires decades of consistent reinforcement and stories that become mythology.

Consider how differently 3M might have evolved if McKnight had optimized for his tenure rather than institutional permanence. He stepped aside as CEO at 60 but remained chairman, ensuring cultural continuity. He promoted from within, choosing successors who'd absorbed 3M values through decades of experience. The culture survived McKnight because McKnight designed it to survive him.

For founders, the lesson is profound: The companies that outlive their creators are those whose cultures become self-reinforcing. Netflix's "freedom and responsibility" culture, Amazon's "Day 1" mentality, and Bridgewater's "radical transparency" represent modern attempts at cultural encoding. But will they survive their founders? The jury's out.

The Power of Patient Capital and Long-Term Thinking

3M held Spencer Silver's "failed" adhesive for five years before Post-it Notes emerged. The company lost money in pharmaceuticals for a decade before profitability. This patience wasn't stupidity—it was strategy. By accepting longer development cycles, 3M could pursue opportunities competitors abandoned as too uncertain or too distant.

Modern venture capital has inverted this philosophy. The pressure for 10x returns in 7 years forces startups to pursue rapid scaling over patient development. The result: many billion-dollar valuations but few billion-dollar sustainable businesses. WeWork, Theranos, and countless others represent the pathology of impatient capital.

Yet some modern companies embrace 3M's patience. Amazon famously lost money for years while building infrastructure. Tesla burned billions before achieving profitability. SpaceX spent a decade perfecting reusable rockets. These companies succeeded not despite patient capital but because of it.

For investors, the lesson challenges conventional wisdom. The best returns might come not from rapid exits but from decades-long commitments. Berkshire Hathaway's 50+ year holding periods, Sequoia's perpetual funds, and Naspers's 20-year Tencent investment show patient capital's potential. But executing requires conviction that transcends quarterly pressures.

When to Pivot vs. Persevere

3M's founding pivot from mining to manufacturing saved the company. But equally important were the pivots not taken. When sandpaper struggled, 3M didn't pivot to lumber or textiles—they persevered in abrasives while improving quality. When Scotch tape faced competition, they didn't pivot to paper products—they innovated within adhesives.

The framework: Pivot on "what" but persevere on "how." 3M pivoted from mining corundum to making sandpaper (the "what") but persevered in materials science expertise (the "how"). Post-it Notes pivoted from super-strong to repositionable adhesive (the "what") but persevered in adhesion technology (the "how").

Modern founders often confuse these. They pivot core capabilities while persevering on specific products. A social media company becomes a crypto platform becomes an AI startup—pivoting capabilities while chasing markets. This rarely works because competitive advantage comes from accumulated expertise, not market timing.

Creating Platforms, Not Just Products

3M didn't make tape; they mastered adhesion science that yielded thousands of products. They didn't make sandpaper; they understood abrasion physics that spawned entire industries. This platform approach created compound advantages—each innovation strengthened the foundation for future breakthroughs.

Contemporary platform thinking often focuses on digital networks—iOS, AWS, Salesforce. But 3M shows physical and chemical platforms can be equally powerful. Gore-Tex built a empire on expanded PTFE. Corning created successive businesses from glass science. Materials platforms might lack software's network effects but offer patent protection and manufacturing moats.

For founders, the lesson suggests focusing on fundamental capabilities rather than specific applications. What underlying technology or expertise could yield multiple products across multiple markets? For investors, it means evaluating companies not just on current products but on platform potential.

Managing Innovation at Scale

3M's Technical Forum, where researchers from different divisions shared discoveries, represents organizational innovation as important as any product. The company understood that innovation doesn't scale linearly—it scales through connections. The forum created collision points where unexpected combinations sparked breakthroughs.

Google's 20% time, Facebook's hackathons, and Amazon's "working backwards" process represent modern attempts at scaling innovation. But most fail because they copy practices without understanding principles. It's not about time allocation—it's about permission to fail, patience for development, and mechanisms for cross-pollination.

The deeper challenge: innovation antibodies. As organizations grow, they develop immune systems that reject deviation. Procurement processes, legal reviews, brand guidelines, and financial controls all serve important purposes but collectively suffocate experimentation. 3M managed this tension for decades through cultural counterweights—celebrating productive failures, promoting innovators, and protecting bootleggers.

The Role of Serendipity in Breakthrough Innovation

Post-it Notes, Scotchgard, and countless 3M breakthroughs emerged from accidents. This wasn't luck—it was prepared minds recognizing unexpected value. 3M created conditions where serendipity could flourish: diverse expertise, experimental freedom, and patience for applications to emerge.

Modern innovation processes often eliminate serendipity through over-planning. OKRs, sprint goals, and product roadmaps create efficiency but reduce randomness. The most valuable discoveries might be those nobody thought to look for. Penicillin, microwave ovens, and Viagra all emerged from accidents recognized by prepared observers.

For organizations seeking breakthrough innovation, the lesson isn't to abandon planning but to reserve space for unplanned discovery. Google's founding PageRank algorithm emerged from a side project. Slack started as an internal tool for a gaming company. The highest-return innovations often aren't on any roadmap.

The 3M story ultimately teaches that building a century-long innovation machine requires more than good ideas or smart people. It requires patient capital, cultural encoding, platform thinking, and comfort with productive failure. These lessons feel almost antiquated in an era of rapid iteration and quarterly earnings. Perhaps that's precisely why they're valuable.

XII. Epilogue: What Would McKnight Think?

William McKnight died in 1978 at age 90, having watched his sandpaper company transform into a global innovation empire. He lived long enough to see early computer systems but not the internet. He witnessed the moon landing but not smartphones. He knew about environmental regulations but not PFAS settlements. If McKnight could observe today's 3M, what would he recognize, and what would mystify him?

He'd recognize the fundamental tension between efficiency and innovation. Even in his era, McKnight fought board members who wanted faster returns and more predictable results. His famous quote—"If you put fences around people, you get sheep"—was directed at executives demanding tighter controls. The Six Sigma revolution would likely appall him, not because he opposed measurement but because he understood that innovation requires inefficiency.

The Solventum spinoff might surprise but not shock him. McKnight believed in focus but also in unexpected connections. He'd probably ask: "How will medical researchers learn from automotive innovations if they're in different companies?" But he'd also appreciate the strategic clarity. McKnight was, above all, pragmatic. If division creates more value than integration, divide.

The PFAS crisis would deeply trouble him, not just financially but philosophically. McKnight built 3M on solving problems, not creating them. The idea that 3M's innovations poisoned water supplies would challenge his fundamental belief in business as a force for good. Yet he'd probably focus on solutions rather than blame—how can 3M's expertise fix what it broke?

Modern 3M's global scale would astound him. When McKnight retired as chairman in 1966, international sales were meaningful but not dominant. Today's 3M, with 95,000 employees across 70 countries, would seem almost incomprehensible. Yet he'd recognize the principle: Go where customers need solutions.

The pace of modern competition would concern him. McKnight built 3M in an era when patents provided decades of protection and relationships lasted generations. Today's instant price comparison, rapid reverse-engineering, and fleeting customer loyalty would challenge every assumption of his patient capital model. How do you invest in 10-year development cycles when competitors copy products in 10 months?

He'd be fascinated by modern innovation tools—artificial intelligence designing molecules, quantum computers modeling materials, robots automating experimentation. But he'd probably warn against over-dependence on technology. Innovation, in McKnight's view, came from human creativity, not computational power. Tools enable but don't replace insight.

The quarterly earnings pressure would perplex and frustrate him. McKnight thought in decades, not quarters. He'd question how companies can pursue breakthrough innovation while satisfying Wall Street's demand for predictable growth. The financialization of business—where moving numbers matters more than making products—would seem like a fundamental corruption of capitalism's purpose.

Yet McKnight would find hope in unexpected places. The startup ecosystem's experimentation ethos echoes his bootlegging culture. Open-source collaboration resembles his Technical Forum. The maker movement's hands-on innovation mirrors 3M's early laboratory culture. The principles he championed persist, even if institutions struggle to maintain them.

Looking forward, McKnight might argue that 3M's challenges aren't unique but universal. Every successful company eventually faces the innovator's dilemma—how to disrupt yourself before others disrupt you. Every innovation culture eventually calcifies into bureaucracy. Every competitive advantage eventually erodes. The question isn't whether these challenges arise but how organizations respond.

His prescription would likely be simple but difficult: Return to first principles. What problems need solving? What expertise can we contribute? How can we create conditions for unexpected discovery? The specific answers would differ from his era, but the questions remain constant.

McKnight might also challenge modern assumptions about corporate purpose. He believed companies existed to solve problems profitably, with emphasis on both words. Pure profit maximization without problem-solving creates Enron. Pure problem-solving without profit creates bankruptcy. The balance point shifts with context, but balance is essential.

The environmental and social responsibilities that dominate modern corporate discourse would resonate with McKnight's Minnesota values but challenge his methods. He believed in treating employees and communities well because it was both right and smart. But stakeholder capitalism's complexity—balancing shareholders, employees, customers, communities, and environment—would require new frameworks beyond his experience.

Ultimately, McKnight would probably view modern 3M with mixed emotions. Pride in the company's global impact and technological sophistication. Concern about its innovation struggles and cultural drift. Frustration with short-term pressures and bureaucratic complexity. Hope that patient capital and creative freedom might somehow resurge.

His final observation might be this: 3M succeeded not because it had better strategies or smarter people but because it created conditions where ordinary people could do extraordinary things. Those conditions—patience, permission, and persistence—remain as relevant today as in 1902. The challenge isn't understanding these principles but implementing them in a world that seems designed to prevent them.

What would McKnight think? He'd think what he always thought: Stop talking about innovation and start experimenting. Stop optimizing existing products and start imagining impossible ones. Stop managing quarterly earnings and start building century-long value. Easy to say, difficult to do, essential to try.

The 3M story isn't finished. Whether the company recaptures its innovation magic or becomes another industrial has-been remains unwritten. But McKnight's ghost haunts the headquarters in Maplewood, whispering a simple question to anyone who'll listen: "What accident will you turn into the next billion-dollar business?" The answer will determine whether 3M's next century resembles its first or whether the innovation machine finally stops.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube