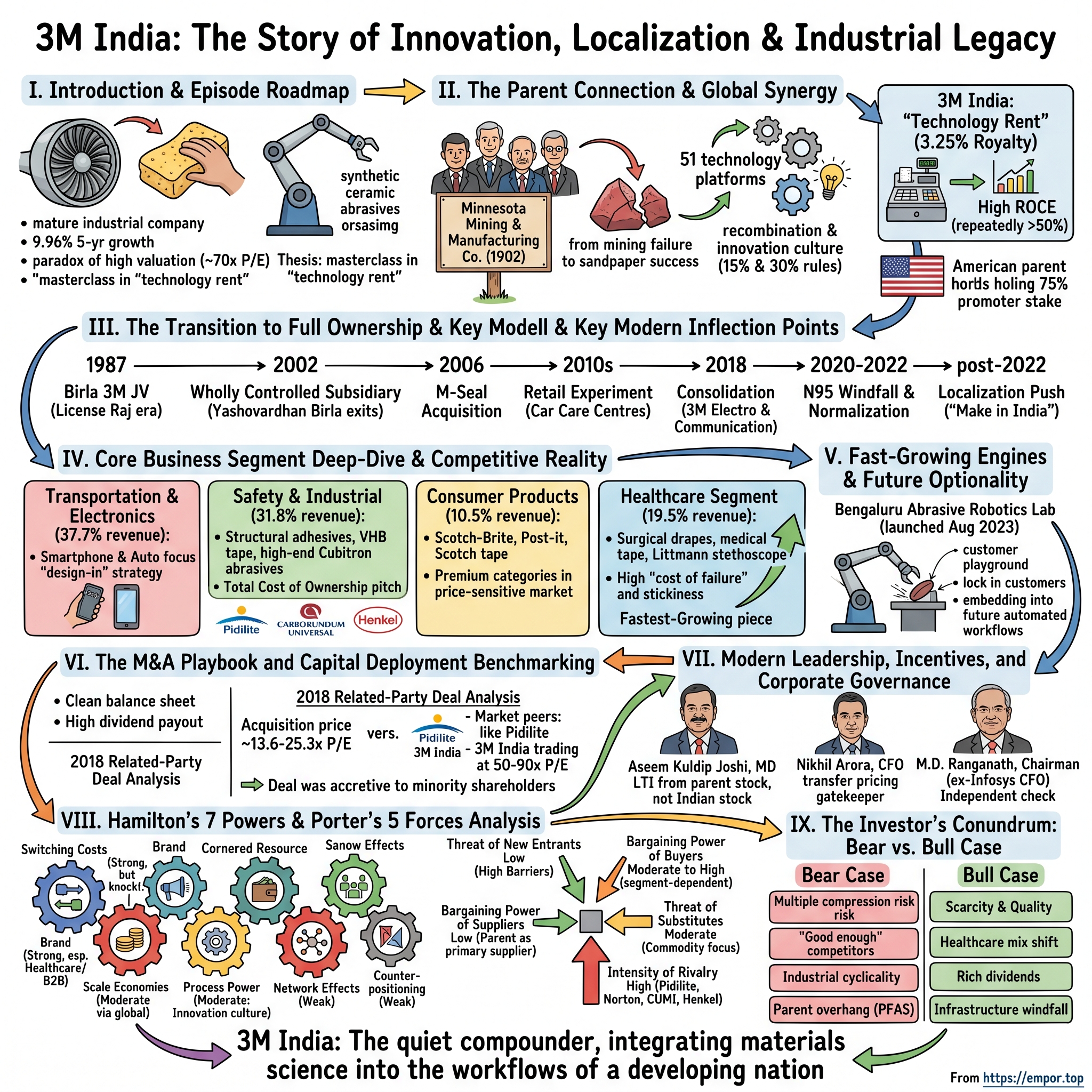

3M India: The Story of Innovation, Localization & Industrial Legacy

I. Introduction & Episode Roadmap

Picture two scenes happening at the same moment somewhere in India.

In a temperature-controlled lab in Bengaluru, a robotic arm swings toward an aircraft turbine blade. It presses an abrasive belt against the metal with a force calibrated to the micron, grinding away imperfections you could never see with the naked eye. The remarkable thing is the sandpaper itself. As it wears, it does not go dull and useless the way the stuff in your garage does. Its synthetic ceramic grains fracture in a controlled, predictable way, exposing fresh cutting edges. The abrasive, in effect, sharpens itself as it works.

Now picture a kitchen in a middle-class apartment in Pune. A homemaker scrubs a stubborn patch of burnt dal off a steel pot with a green-and-yellow sponge. She paid five times what a fistful of steel wool would have cost, and she did it gladly, because the steel wool scratches her non-stick pan and the sponge does not.

The turbine blade and the burnt pot share a secret. Both are being cleaned by the same body of material science — the chemistry of abrasives, adhesives, and surface coatings perfected over more than a century by a company born from a mining failure on the shores of Lake Superior. In India, that science is delivered by a single listed entity: 3M India Limited, ticker 3MINDIA on the National Stock Exchange.

And here is where the story gets interesting for investors. This is a mature industrial company. It sells tape, sponges, masks, sandpaper, and stethoscopes. Its five-year sales growth has been a workmanlike ~9.96%.7 Yet the market values it like a software company on a tear — a market capitalization north of ₹37,000 crore and a price-to-earnings multiple hovering around 70 times earnings.7

That is the central paradox of this episode. Why does a company selling sandpaper command the valuation of a hypergrowth SaaS startup? How does a business that is, at its core, a technology importer throw off some of the highest returns on capital in all of India — a return on capital employed that has repeatedly crossed 50%?7

Our thesis is this: 3M India is not really a tape-and-sponge story. It is a masterclass in the economics of what we'll call "technology rent." It is the story of how a global parent's deep portfolio of material-science platforms gets localized, paid for through a clean royalty arrangement, and turned into some of the most defensible cash flows in the Indian market. The company spends almost nothing on primary research, carries no meaningful debt, and converts its inventions into pricing power in a price-sensitive economy.

Here's where we're headed. We'll start with the parent — the Minnesota company whose DNA defines everything the Indian subsidiary does. We'll trace the transition from a license-era joint venture into a wholly controlled American subsidiary. We'll walk segment by segment through the actual business — the electronics and automotive films that are the biggest revenue line, the industrial backbone of adhesives and abrasives, the consumer brands that are the public face, and the quietly compounding healthcare engine. We'll dig into capital allocation and whether management overpaid on its big internal acquisition. We'll meet the new managing director taking the wheel in 2026 and examine how his incentives are wired. We'll war-game the competition — Pidilite, Grindwell Norton, Carborundum Universal, Henkel, Avery Dennison. And we'll run the whole thing through Hamilton Helmer's 7 Powers and Porter's Five Forces before laying out the bull and bear cases. Let's get into it.

II. The Parent Connection & Global Synergy

To understand 3M India, you have to understand that its parent company was, at the very beginning, a flop.

In 1902, five businessmen in Two Harbors, Minnesota — a butcher, a lawyer, a doctor, and two railroad executives — pooled their money to mine a mineral called corundum on the shores of Lake Superior. Corundum is an extremely hard abrasive, and the plan was to dig it out and sell it to grinding-wheel manufacturers. They named their venture Minnesota Mining and Manufacturing Company. The problem was that the deposit they had staked turned out not to be corundum at all. It was a low-grade, nearly worthless mineral called anorthosite. The founding premise of the company was, quite literally, a geological mistake.

What happened next is the origin myth of one of the great innovation cultures in industrial history. Unable to mine good abrasive, the company pivoted to making sandpaper instead — buying better minerals and gluing them onto paper backing. That forced a question that would define the company forever: what makes a good abrasive product is not just the grit, but the adhesive that holds the grit, and the backing the adhesive sits on, and the coating that keeps it all from clogging. Minnesota Mining stumbled into the realization that it was not really in the mining business at all. It was in the business of putting precisely engineered particles onto precisely engineered surfaces. From that single insight grew masking tape, cellophane tape, reflective road signs, surgical drapes, Post-it Notes, and N95 respirators.

Over the following century, 3M codified this into what it calls its technology platforms — roughly 51 distinct families of materials-science capability, from microreplication (stamping microscopic structures onto film) to non-woven fibers, fluorochemicals, advanced adhesives, light management, and nanotechnology. The genius of the platform model is recombination. A single adhesive chemistry developed for one industry can be redeployed into a dozen others. The microreplication technology that brightens a laptop screen is a cousin of the technology that makes a road sign glow in headlights. 3M's competitive advantage is not any one product; it is the library, and the institutional habit of cross-pollinating it.

Now, here is the part that matters for the Indian listed company and for anyone trying to value it. 3M India does not own that library. It rents it.

The financial architecture of the subsidiary is built on a royalty. 3M India pays its American parent a royalty of roughly 3.25% on its manufactured sales for access to the global technology, the brands, and the trademarks.[^2] In exchange, it gets to pull, more or less off the shelf, from one of the deepest catalogs of industrial products on earth, without spending billions of its own rupees on basic research. The American parent, 3M Company, in turn holds a 75.0% promoter equity stake in the Indian entity — the maximum a promoter is permitted to hold under Indian listing rules before it must either delist or dilute.7

This is the engine of those extraordinary returns on capital. A normal industrial company of this caliber would have to sink enormous sums into R&D laboratories and accept the risk that most of that research leads nowhere. 3M India skips that entire line item. Its "R&D" is a variable royalty cost — a small, predictable percentage that scales with sales and never threatens the balance sheet. The heavy, speculative capital is borne in St. Paul, Minnesota; the rupee profits are harvested in Bengaluru.

The parent also exports something less tangible than chemistry: a culture of systematic invention. Two numbers define 3M's global DNA. The first is the famous "15% rule" — the long-standing principle that technical staff may spend up to 15% of their time on projects of their own choosing, the policy that famously birthed the Post-it Note. The second, and the one investors should care about more, is the "30% rule" — the goal that a meaningful share of sales should come from products introduced in the last few years. It is a discipline designed to keep a hundred-year-old company from coasting on legacy products. In India, that DNA is grounded in physical plants — the manufacturing and technical facilities in Bengaluru's Peenya Industrial Area and Electronic City, where global formulations are adapted to Indian raw materials, Indian climate, and Indian price points.

That localization — taking a global platform and bending it to fit India — is what the next chapter is all about, because it began with a very Indian institution: the license-era joint venture.

III. The Transition to Full Ownership & Key Modern Inflection Points

In the late 1980s, a foreign company could not simply walk into India and set up shop. The License Raj — the dense thicket of permits, quotas, and foreign-ownership caps that governed Indian industry until the 1991 liberalization — made a local partner all but mandatory. So in 1987, 3M did what nearly every multinational did: it found an Indian house to hold its hand. The result was Birla 3M Limited, a joint venture with the Birla Group, one of India's storied industrial families.

For fifteen years, that was the arrangement. Then the world changed. Liberalization had torn down the ownership caps, and a foreign parent no longer needed an Indian partner to operate. In 2002, Yashovardhan Birla exited, selling the family's stake, and the American parent stepped up its ownership and renamed the company 3M India Limited.[^2] The "Birla" came off the door, and what had been a hedged, halfway presence in India became a full-throated subsidiary of the Minnesota giant. This is the pivot worth holding onto: everything that makes 3M India a high-return compounder today — the royalty model, the unfettered access to the global catalog, the 75% promoter alignment — flows from that 2002 decision to go from partnership to control.

From there, the modern story is a series of inflection points, each one revealing something about how the company thinks.

The M-Seal moment (2006). In 2006, 3M India acquired the cable-accessories and electrical-jointing business associated with Mahindra Engineering & Chemical Products, bringing the now-iconic M-Seal epoxy compound and a portfolio of electrical jointing kits into the 3M fold.[^10] This mattered because it was not a glamorous technology play; it was a distribution and brand play. M-Seal is the kind of product an electrician or a plumber reaches for without thinking — a multipurpose sealant with deep, sticky reach into the Indian repair economy. Acquiring it gave 3M instant credibility and shelf space in a market it could never have built from scratch at that speed.

The retail experiment (2010s). Somewhere in the next decade, 3M tried something genuinely un-3M-like. It opened 3M Car Care Centres — branded automotive detailing outlets where customers could get their cars washed, polished, ceramic-coated, and wrapped in 3M's paint-protection film. For a company whose entire identity was business-to-business — selling abrasives to factories and films to manufacturers — this was a leap into consumer-facing, experiential retail. It was an attempt to capture the full margin of the value chain rather than selling a component to someone else who captured it. The lesson the company took from it was about brand: a 3M-branded service experience could pull through 3M-branded products at premium prices.

The consolidation (2018). This is the one that matters most for the balance sheet, and we'll dissect the economics later. In 2018, the listed 3M India entity acquired 100% of an unlisted sister company, 3M Electro & Communication India Private Limited, for ₹590 crore.2 That sister company housed the highly profitable M-Seal and electrical-markets business. The effect was to pull a high-margin, cash-generative business out of a private affiliate and fully onto the listed company's balance sheet — directly to the benefit of the minority shareholders who own the other 25%. For now, hold the thought that this was an internal, related-party deal, exactly the kind of transaction where a 75%-owner could quietly shortchange the minority. We'll examine whether it did.

The N95 windfall (2020–2022). Then came the pandemic, and 3M found itself sitting on the single most demanded product in the country: the N95 respirator. As COVID-19 swept India, 3M India was a primary supplier of respiratory protection to hospitals, frontline workers, and a terrified public. Revenue and profit in the safety business spiked. But the crucial investor lesson here is about the morning after. The N95 boom was a one-time event, not a new baseline. As the pandemic receded, that demand evaporated, and FY23 saw a sharp normalization. Anyone who extrapolated the COVID-era numbers into the future learned a hard lesson about distinguishing a structural trend from a spike. Good analysts mentally strip the pandemic years out of the safety segment's growth line.

The localization push (post-2022). The most recent inflection is quieter but strategically deep. Rising import duties and the global supply-chain chaos of the early 2020s exposed the weakness in 3M India's traditional model — importing finished or semi-finished product from the global network and distributing it. When ships stopped and tariffs rose, that model strained. So the company has been steadily deepening local manufacturing, including commencing local production of specialized coatings for aviation fuel pipelines at its Ahmedabad unit. The shift from "import and distribute" toward "make in India" is both a margin story (cutting out import duty and freight) and a resilience story (insulating the business from the next supply shock).

Each of these moves localized a piece of the global parent's capability into the Indian market. But to really understand where the value sits, we have to open the hood and look at the segments — because they are wildly different businesses wearing the same logo.

IV. Core Business Segment Deep-Dive & Competitive Reality

If you think of 3M India as one company, you'll misjudge it. It is really four companies stapled together, each facing different customers, different competitors, and different economics. The segment reporting from FY25 tells the story, and the proportions are revealing.1

Transportation & Electronics — the quiet giant (37.7% of FY25 revenue, ₹1,676.6 crore)

The single largest slice of 3M India is the one the public never sees. This is the segment that puts optical films inside your smartphone to make the screen brighter while sipping less battery, manages the heat inside electronic devices so they don't cook themselves, and wraps cars and commercial vehicles in graphics and paint-protection film.1

Think about what's happening in India right now. The country has become one of the world's great smartphone assembly hubs, with global brands building handsets by the tens of millions on Indian lines. Every one of those screens is a candidate for a display-enhancement film. The automotive sector is similarly booming. 3M's strategy here is to embed itself into the manufacturing ecosystem early, so that when a phone maker or a carmaker designs a product, a 3M material is already specified into the bill of materials. Once you're designed in, you're hard to design out.

The competition here is real but specialized. The most direct global rival is Avery Dennison — a leader in pressure-sensitive materials, labels, and vehicle graphics — along with a long tail of unlisted Tier-1 automotive component suppliers. This is a war fought in engineering specs and qualification cycles, not on retail shelves. It's a knife fight nobody outside the industry ever notices, and it generates more than a third of 3M India's revenue.

Safety & Industrial — the backbone (31.8% of FY25 revenue, ₹1,413.9 crore)

This is the segment closest to 3M's mining-and-sandpaper roots: structural adhesives, personal protective equipment, and industrial abrasives.1 The crown jewel here is the abrasive technology — including the high-end ceramic-grain products marketed under the Cubitron line, the self-sharpening abrasive we described in the opening. To understand why a factory pays a premium for it, you have to understand the pitch, which is not really about the sandpaper at all.

3M sells this segment on "total cost of ownership." The classic example is structural adhesive tape. When a manufacturer builds the body of a commercial bus, the traditional method is welding — slow, labor-intensive, requiring skilled welders and creating points of stress and corrosion. 3M's high-bond VHB tape can replace many of those welds. The tape itself is far more expensive than a weld, and a naive purchasing manager would reject it on unit cost. But the right comparison is the system cost: faster assembly, less labor, no welding equipment, a cleaner finish, better distribution of stress across the joint. When you sell the savings on the whole line rather than the price of the tape, the premium evaporates. That is the entire art of 3M's industrial salesmanship — reframing a "expensive consumable" as a "cheaper process."

But this segment also faces the most credible competition in the whole company, and two of those competitors are formidable Indian institutions in their own right.

The first is Grindwell Norton, a subsidiary of the French materials giant Saint-Gobain. Grindwell carries a market capitalization of roughly ₹23,300 crore on annual revenue of about ₹3,073 crore.4 The second is Carborundum Universal, known universally as CUMI, part of the storied Murugappa Group of Chennai, with a market cap around ₹21,500 crore and revenue near ₹4,900 crore.5 Together, Grindwell and CUMI dominate the bread-and-butter abrasives market in India. CUMI in particular is vertically integrated all the way back to the source — it mines bauxite and processes its own raw minerals, the very thing 3M's founders failed to do in 1902.

So how does 3M coexist with two larger, cheaper, more integrated abrasive players? By refusing to fight on their turf. 3M does not try to win the commodity grinding-wheel market. It carves out the high-end, technologically superior niche — the precision ceramic abrasives where performance, consistency, and self-sharpening behavior justify a price the commodity players can't match. It is the classic premium-niche posture: cede the volume, capture the margin. And in industrial adhesives specifically, it also contends with Henkel, the German chemicals group whose Loctite-led adhesives business competes hard in B2B structural bonding.

Consumer Products — the public face (10.5% of FY25 revenue, ₹465.7 crore)

Here, finally, are the products you actually recognize: Scotch-Brite scrubbers and mops, Post-it Notes, Scotch tape, and Command damage-free hanging strips.1 This is the smallest of the four engines by revenue, but it carries the brand into millions of homes and offices, doing the quiet work of making "3M" a name a consumer trusts.

The strategic challenge in this segment is building premium categories in a fiercely price-sensitive market. The Scotch-Brite sponge is the perfect case study. It costs roughly five times what a wad of steel wool costs. On a price tag, that's a loser. But it wins on the things that don't fit on a price tag: it lasts far longer, it doesn't shed metal slivers, and — crucially in the age of non-stick cookware — it doesn't scratch the pan you spent good money on. 3M has spent decades teaching the Indian consumer that the right comparison is cost-per-month-of-use and pan-not-ruined, not cost-at-checkout. It's the same "total cost of ownership" argument as the bus-body tape, just translated into kitchen language.

The competition here is twofold and asymmetric. At the top sits Pidilite Industries — the colossus of Indian adhesives, owner of Fevicol, Fevikwik, Dr. Fixit, and, notably, a competing M-Seal-style product line. Pidilite is in a different weight class entirely: a market capitalization around ₹1,60,900 crore on revenue near ₹14,600 crore, with something like a 70% share of India's organized consumer-adhesives market — an effective near-monopoly.6 3M does not try to out-Fevicol Fevicol. It competes at the premium and stationery end — Scotch tape, Post-it, Command — where Pidilite is weaker and where brand and design matter more than rural distribution muscle.

At the bottom sits the other competitor: the unorganized sector. Walk through any Indian market and you'll find sponges in the exact green-and-yellow livery of Scotch-Brite, made by manufacturers nobody has heard of, selling at a fraction of the price. This knockoff pressure is a permanent tax on the consumer margin and a reminder that brand trust, while real, is not impregnable.

Notice the pattern across all three of these segments: 3M wins not by being cheapest, but by selling the cost of failure or the cost of the whole system. That logic reaches its purest, most powerful form in the fourth segment — the one growing fastest of all.

V. Fast-Growing Engines & Future Optionality

The Healthcare Segment — the real growth engine (19.5% of FY25 revenue, ₹865.2 crore)

Walk into any modern Indian operating theater and you will find 3M everywhere, mostly in places you'd never think to look. The clear plastic film draped over the surgical site, sealing the skin against bacteria — that's an incise drape. The tape holding the IV line and the dressing in place — medical tape engineered not to tear fragile skin. The indicator strips that confirm an instrument has actually been sterilized. The stethoscope around the surgeon's neck — quite likely a Littmann, the gold-standard brand 3M owns.1

This is the segment that should make a long-term investor sit up. Healthcare grew from ₹632.6 crore in FY24 to ₹865.2 crore in FY25 — the fastest-growing piece of the entire portfolio, expanding while the cyclical industrial segments wheezed.1 And the economics are the best in the company.

Why? Because this is where the "cost of failure" logic reaches its extreme. A surgical drape costs a few hundred rupees. A post-operative infection costs the hospital a fortune — in extended stays, in additional treatment, in reputational damage, and increasingly in litigation. No hospital administrator in their right mind switches to an unproven, cheaper surgical drape to save a rounding error, because the downside of that drape failing is catastrophic and the upside of the saving is trivial. The product is a tiny fraction of the procedure's cost but stands between the hospital and a ruinous risk. That asymmetry is the source of immense pricing power and switching costs. Once a hospital's protocols, its surgeons' habits, and its procurement systems are built around 3M's healthcare products, dislodging them is enormously difficult. This is the most defensive, highest-margin, stickiest revenue 3M India has — and it's compounding faster than anything else.

The Bengaluru Abrasive Robotics Lab — the call option (launched August 2023)

In August 2023, 3M India opened something with no immediate revenue line but a great deal of strategic intrigue: an Abrasive Robotics Lab in Bengaluru — its 17th such lab globally and the first in India.3 To understand why this matters, you have to think about where Indian manufacturing is heading.

For decades, India's manufacturing edge has been cheap manual labor. A worker holds a grinding tool and finishes a metal part by hand. But as wages rise and quality demands tighten, Indian factories are beginning the same shift to robotic automation that transformed Japanese, Korean, and German manufacturing before them. When you automate grinding and finishing, you have to teach a robot arm exactly how to hold the abrasive, how much pressure to apply, at what angle, for how long. That programming and calibration is painstaking — and it is built around the specific physical and cutting properties of a specific abrasive.

That is the chess move. The lab is a customer playground. Automotive and aerospace clients bring their actual parts — a turbine blade, an engine casting, a car panel — and 3M's engineers help them design an automated grinding routine using 3M's proprietary abrasive geometry. The lab gives away expertise for free. But here's the trap that springs shut: once a manufacturer has spent months programming a robotic cell calibrated precisely to the cutting behavior of a 3M abrasive, switching to a rival abrasive means re-engineering the whole automated routine. The switching cost goes from "buy a different box of sandpaper" to "re-validate an entire production line." For a few rupees of abrasive, no plant manager will take that on. 3M is buying its way into the workflow of Indian manufacturing's automated future, one robot cell at a time. It is a small bet today and a potentially enormous moat tomorrow.

These growth engines — defensive healthcare and embedded automation — are what justify part of the premium valuation. But the other half of the value story is what management does with all the cash these businesses throw off. That's a question of capital allocation, and it's where the 2018 acquisition becomes a fascinating test case.

VI. The M&A Playbook and Capital Deployment Benchmarking

Most industrial companies have a capital-allocation problem: they generate cash and feel compelled to spend it, often on empire-building acquisitions that destroy value — the phenomenon Peter Lynch immortalized as "diworsification." 3M India has the opposite posture, and it flows directly from the royalty model we described earlier.

Because the parent funds the heavy, speculative research, 3M India doesn't need to hoard capital for a giant R&D budget or a risky new-technology bet. Its capital needs are modest — working capital, some plant expansion, localization projects. The result is a company that is essentially debt-free and generates large free cash flows it cannot productively reinvest at its sky-high returns. So it does the rational thing: it gives much of the cash back. The dividend payout ratio has, in recent years, run extraordinarily high — at one point exceeding 170% of earnings, funded by accumulated reserves, with per-share dividends declared as high as ₹535.71 A payout above 100% is a deliberate statement: management is telling you it would rather return surplus capital than chase growth for growth's sake.

But the company has done M&A, and its single most scrutinized deal is the perfect lens on how disciplined that capital allocation really is — because it was a related-party transaction, the kind most ripe for abuse.

Recall the 2018 acquisition: the listed 3M India bought 100% of its unlisted sister company, 3M Electro & Communication India, for ₹590 crore.2 The seller and the buyer were, ultimately, controlled by the same American parent. When a 75%-owner sells an asset from its private pocket into the public company it controls, minority shareholders have every reason to be nervous. The parent could, in principle, jack up the price and effectively transfer wealth from the minority into its own private affiliate.

So did 3M overpay? Let's run the numbers the way an analyst would have at the time.

First, the process. The deal was supported by independent valuation reports from Deloitte and Bansi Mehta & Co. — outside firms whose job was to set a defensible fair value rather than a sponsor-friendly one.2 Governance box ticked, but governance theater is cheap, so let's check the math.

The acquired business, 3M E&C, was generating profit after tax of roughly ₹43.19 crore in FY19 and about ₹23.30 crore in FY20.7 Against a ₹590 crore price, that implies an acquisition price-to-earnings multiple of somewhere between about 13.6 times and 25.3 times, depending on which year's earnings you anchor to. Hold that range in your mind: call it the mid-teens to mid-twenties.

Now the comparison. What was the market paying for similar businesses at that time? Pidilite — the closest comparable consumer-and-industrial adhesives play — traded somewhere between 50 and 90 times earnings. The listed 3M India parent itself traded at roughly 55 to 75 times earnings.76 In other words, the public market was valuing comparable adhesives and sealant businesses at three to five times the multiple that 3M India paid for 3M E&C.

The verdict writes itself. Far from overpaying, 3M India acquired a high-margin electrical-sealant and jointing business at a fraction of the prevailing market multiple. The deal was accretive to the minority shareholders on day one — they got a cash-generative business folded onto their balance sheet at mid-teens earnings while their own stock traded at sixty-plus. This is exactly the discipline you want to see from a controlled subsidiary, and it's a meaningful data point in the governance column. When the controlling shareholder had the opportunity and the means to squeeze the minority, it chose restraint and benchmarked below market.

That restraint, it turns out, is partly a function of how the people running the company are paid and overseen — which brings us to the team steering 3M India in 2026.

VII. The Modern Leadership, Incentives, and Corporate Governance

Leadership at a 75%-owned multinational subsidiary is a peculiar job. You are not the founder. You are not the ultimate owner. You are a steward, running an Indian listed company according to the standards and strategy of an American parent, while answerable to Indian minority shareholders and Indian regulators. The people who do this well share a trait: their incentives are wired to the global enterprise, not to short-term local games. The 2026 leadership team is a study in exactly that wiring.

Aseem Kuldip Joshi — the new Managing Director

The headline change is at the very top. Effective April 1, 2026, Aseem Kuldip Joshi took over as Managing Director for a five-year term, succeeding the retiring Ramesh Ramadurai.[^3][^12] Joshi's background is instructive. He came not from inside the 3M lifer track but from running the India business of GMM Pfaudler, a leading manufacturer of glass-lined process equipment, where he served as CEO of the India operation from 2021 to 2025.[^12] That's a man who has spent his recent career selling sophisticated, mission-critical industrial equipment to demanding process industries — chemicals, pharma, specialty manufacturing. He understands the "cost of failure" sale in his bones. Putting an outsider with deep Indian industrial credibility in the MD chair, rather than parachuting in an expatriate, signals a continued commitment to local market knowledge.

Now look at how he's paid, because this is where the incentive architecture reveals itself. Joshi's cash compensation is capped at ₹45 lakhs per month — roughly ₹5.4 crore per annum.[^4] By the standards of an Indian CEO running a ₹37,000-crore-market-cap company, that is a notably restrained cash package. But cash is not where his real wealth is meant to come from. Critically, he holds no direct personal equity in 3M India itself. Instead, his long-term incentives — restricted stock units, stock options, and performance shares — are granted by the parent, 3M Company in the United States.[^4]

Sit with the implications of that, because it's elegant. By tying the MD's wealth to the global parent's stock rather than to the Indian subsidiary's stock, the parent aligns his incentives with global 3M's standards of capital allocation, technology compliance, and ethics. He has no personal incentive to pump the Indian share price with short-term financial engineering, because he doesn't own Indian shares. His payoff comes from advancing the whole 3M enterprise correctly. For minority shareholders, this is double-edged — his loyalty is structurally to St. Paul — but it also means he is not playing games with the local stock, and his interests run with the long-term health of the technology platform that the whole edifice depends on.

Nikhil Arora — the Chief Financial Officer

The financial gatekeeper is Nikhil Arora, appointed CFO effective May 5, 2025.1 His job is more delicate than a typical CFO's because of one word: royalty. Recall that 3M India pays its parent that ~3.25% royalty and buys materials from the global network. Every one of those related-party flows is a transfer-pricing question under Indian tax law — the regulator's standing concern is that multinationals use inflated royalties and intercompany prices to siphon profit out of India and dodge Indian tax. Arora's mandate includes managing the company's tight working-capital cycle and cash conversion while ensuring every related-party price can withstand scrutiny under India's transfer-pricing regime. He sits at the seam between the parent's interest in extracting value and the minority's and the regulator's interest in keeping it in India.

M.D. Ranganath — the Chairman

Guarding that seam from the board is the Non-Executive Independent Chairman, M.D. Ranganath. His résumé is a reassurance in itself: he served as Chief Financial Officer of Infosys during its high-growth years — a tour of duty at one of India's most governance-conscious companies, in the very role that demands financial integrity. Having an independent chairman of that caliber overseeing a 75%-controlled subsidiary is precisely the kind of structural protection a minority investor should want. His presence is a check against the two great risks of a controlled multinational: an excessive royalty hike or transfer-pricing manipulation that would quietly drain value from the Indian shareholders toward the American parent.

Strong governance and aligned incentives are necessary but not sufficient. The question of whether 3M India is a great business in the end comes down to its competitive position — and that's best examined through the formal lenses of strategy.

VIII. Hamilton's 7 Powers and Porter's 5 Forces Analysis

We've described 3M India's advantages in narrative terms throughout this episode. Now let's be disciplined about it and run the business through two of the standard frameworks for assessing durable competitive advantage. The point is not to assign grades but to locate, precisely, where the moat is deep and where it is shallow.

Hamilton Helmer's 7 Powers

Switching costs — strong. This is 3M India's deepest power, and we've seen it in two places. In healthcare, a hospital's protocols, surgeon habits, and procurement systems are built around specific sterile drapes and tapes, and the cost of switching is measured in the risk of infection, not the price of the product. In B2B industrial, the VHB tape designed into a bus body and the abrasive programmed into a robotic finishing cell both lock the customer in at the level of the production line. In every case, the product is cheap relative to the catastrophe of getting it wrong — the textbook condition for high switching costs.

Brand — strong. Scotch-Brite and Post-it function as category creators; in many Indian households, "Scotch-Brite" is simply what you call the sponge. That linguistic ownership lets the brand command a large premium over unbranded local alternatives, and it pulls 3M product through retail on trust alone. It is a genuine power, though, as we noted, the green-and-yellow knockoffs constantly nibble at its edges.

Cornered resource — strong. This is the structural heart of the whole story: 3M India's exclusive, royalty-based access to the parent's roughly 51 global technology platforms and its vast active patent estate. No Indian competitor can replicate this pipeline of materials science, because it represents a century of cumulative, cross-pollinated research. The Indian entity rents a cornered resource it could never build.

Scale economies — moderate. The relevant scale is global, not local. The parent amortizes its enormous R&D and platform development across operations in dozens of countries, which lets 3M India deploy world-class products with minimal domestic R&D spend. The Indian subsidiary borrows the scale economics of the whole enterprise.

Process power — moderate. The embedded culture of systematic innovation — the 15% rule, the customer technical centers, the habit of reframing price as total cost of ownership — is a process advantage that survives individual management transitions. It is harder to copy than a product because it lives in institutional habit.

Network effects — weak. This is largely absent. There is a faint ecosystem effect in the network of certified installers for paint-protection film, but nothing resembling a true network effect where each user makes the product more valuable to the next.

Counter-positioning — weak. 3M is the incumbent industrial conglomerate, not the agile disruptor exploiting a business model the incumbent can't copy. If anything, 3M is the one that must watch for counter-positioning from cheaper, "good enough" challengers.

Porter's Five Forces

Threat of new entrants — low. To replicate 3M, a newcomer would need both a century of materials science and decades of distributor and customer relationships. The combination of technological depth and entrenched distribution is a formidable barrier.

Bargaining power of buyers — moderate to high, and segment-dependent. This is the crucial nuance. In commoditized industrial tapes and abrasives, buyers have real power — Chinese manufacturers give them a credible cheaper alternative, so they can push back hard on price. But in critical medical products, automotive graphics designed into a vehicle, and premium branded consumer goods, buyer power collapses, because the alternatives carry unacceptable risk or lack the brand. The blended picture depends entirely on the mix, which is why the shift toward healthcare matters so much.

Bargaining power of suppliers — low. Here 3M India enjoys a structural quirk: its most important "supplier" of technology and key materials is its own 75%-owning parent. The supplier and the controlling shareholder are the same entity, so their incentives are aligned rather than adversarial — the parent has no interest in squeezing a subsidiary it owns three-quarters of.

Threat of substitutes — moderate. For non-critical applications, substitutes are very real — Pidilite's adhesives, low-cost Chinese imports, local chemical formulations. The threat is concentrated at the commodity end and fades as you move toward mission-critical uses.

Intensity of rivalry — high. In every arena 3M competes, it faces serious, well-capitalized rivals: Pidilite in consumer adhesives, Grindwell Norton and CUMI in abrasives, Henkel in industrial bonding, Avery Dennison in graphics. 3M survives this intensity not by winning everywhere but by retreating to the premium, mission-critical niches where its powers actually bite.

The frameworks converge on a clear picture: a fortress in healthcare and mission-critical B2B, an exposed flank in commodity industrial and mass consumer. Which of those pictures dominates is precisely the argument between the bulls and the bears.

IX. The Investor's Conundrum: Bear vs. Bull Case

Here is where a sophisticated investor earns their keep, because 3M India is a genuinely contested stock. The same set of facts supports two very different conclusions depending on which weight you assign to them. Let's steelman both.

The Bear Case

It starts, inevitably, with the valuation. A stock trading near 70 times earnings is making an implicit promise of growth, and 3M India's five-year sales growth of roughly 9.96% does not obviously keep that promise.7 The bear's sharpest point is multiple compression: if the market ever decides to value 3M India like the mature industrial company it largely is — say, at a more typical 40 times earnings — the stock could lose a large fraction of its value even if earnings keep growing. You'd be right about the business and still lose money, because you overpaid for it. That is the most dangerous kind of loss.

The second worry is the "good enough" competitor. Across the commodity end of the industrial and consumer portfolio, Chinese and local manufacturers increasingly offer products that are, say, 80% as good at 50% of the price. In a price-sensitive economy, "good enough and half the price" is a powerful proposition, and it steadily squeezes 3M's margins in any application where failure is not catastrophic. The green-and-yellow sponge knockoffs are the visible tip of a much larger pressure.

Third is industrial cyclicality. The classic Safety & Industrial segment is tethered to Indian manufacturing capital expenditure, which is famously lumpy. The segment's historical performance has been bumpy precisely because factory investment turns on and off with the economic cycle. A buyer paying a smooth-growth multiple for a cyclical earnings stream is taking on risk they may not have priced.

Finally, there's the parent overhang. 3M Company globally has faced multibillion-dollar liabilities related to PFAS — the so-called "forever chemicals" — and earplug litigation. While 3M India is a legally separate entity insulated from those direct liabilities, the bear argues that a parent fighting expensive global battles is a distracted, financially strained parent, potentially less able to invest in and support its subsidiaries, and a drag on overall sentiment toward the 3M name.

The Bull Case

The bull doesn't dispute the valuation is rich; the bull argues it is deserved, and starts with scarcity. 3M India is one of a small handful of high-quality, debt-free, cash-generating multinational engineering subsidiaries available on the Indian market, with promoter holding locked at the regulatory maximum of 75%.7 In a market where investors prize governance and consistency, that scarcity commands — and arguably deserves — a premium. There simply aren't many other ways to own a business of this quality and this lineage on an Indian exchange.

Then comes the mix shift, which is the bull's most important quantitative argument. The high-margin, fast-growing healthcare segment (19.5% of FY25 revenue) and the premium consumer segment (10.5%) are growing faster than the cyclical industrial businesses.1 If that continues, the blended margin and the blended quality of the whole company rises over time, and the headline "9.96% sales growth" understates the improving quality of those sales. The company is quietly becoming more of a healthcare-and-premium-consumer business and less of a cyclical-industrial one, and the market may pay up for that transition.

The bull also leans on the balance sheet and returns. Debt-free, with returns on capital employed above 50%, 3M India can weather any downturn without stress and keep returning rich dividends throughout.7 This is a company that does not blow up. For a long-term compounder, the absence of ruin risk is itself worth a great deal.

And finally, the infrastructure windfall. India's structural buildout — new airports, expanded highways, semiconductor fabs, specialized pipelines — is a multi-year tailwind for exactly the products 3M sells: retroreflective sheeting for road signs, electronic materials for fabs, specialized coatings for pipelines. The bull sees a long runway where India's physical development pulls 3M's catalog along with it.

The honest synthesis is that both cases are partly right. The bear is right about the price and the commodity flank; the bull is right about the quality, the mix shift, and the balance sheet. Which is why the most useful exercise is not to pick a side but to ask: what would we do if we were running the place?

X. If We Were CEOs

Sitting in the MD's chair in Bengaluru in 2026, with a fortress balance sheet and a contested valuation, here is where we'd place our strategic bets. Three moves, each designed to lean into the powers that actually work and retreat from the fights that don't.

One: turn the robotics lab into a business model, not a showroom. The Abrasive Robotics Lab is currently a marketing asset — a place to impress customers and lock them in. We'd push it further and change what 3M actually sells. Instead of selling sandpaper and grinding belts as consumables, sell "automated finishing subscriptions." Bundle the 3M abrasive, the robotic end-effector, and the finishing software into a single contract priced on outcomes — parts finished, throughput, quality — for India's scaling automotive and defense manufacturing lines. This converts a transactional consumable into a recurring, embedded service, deepens the switching costs we described, and captures more of the value 3M creates rather than leaving it on the table for the customer. It plays directly to 3M's process power and its workflow lock-in, the two places its moat is real.

Two: stop fighting Pidilite head-on and go around it. Pidilite's distribution into rural and small-town India is, for practical purposes, unassailable. Trying to out-distribute Fevicol in a million kirana shops is a war 3M cannot win and should stop fighting. Instead, we'd spin the consumer business toward where 3M's brand actually commands a premium: a digital-first, direct-to-consumer premium proposition built on Command hooks, specialized Scotch-Brite cleaning systems, and high-end DIY adhesives, sold through quick-commerce platforms — Blinkit, Zepto, Swiggy Instamart — where affluent urban consumers value convenience and design over a small price saving. Cede the rural mass market; own the urban premium shelf, which increasingly lives on a phone screen rather than a store shelf.

Three: weaponize the Bengaluru talent base. 3M operates a large Global Capability Center in Bengaluru, staffed with thousands of skilled professionals, currently doing substantial back-office and analytical work for the global enterprise. We'd transition that center from a cost-saving support function into a co-development engine — using Indian software and engineering talent to build connected, smart-safety products for the entire global 3M network: IoT-enabled respiratory equipment, sensor-equipped electrical joints that report their own health, smart PPE. This would turn India from a place where 3M saves money into a place where 3M invents products, marrying the parent's materials science with India's software depth. It is the kind of move that, over a decade, could change what 3M India is — from a localizer of foreign technology into a contributor of new technology back to the parent.

Each of these doubles down on what we've learned actually drives value at this company. Which is a fitting place to step back and extract the broader lessons.

XI. Epilogue & Key Playbook Lessons

Strip away the segments and the financials, and 3M India leaves the long-term investor with a few durable lessons that travel well beyond this one stock.

Technology renting can beat technology building. The most counterintuitive lesson is that 3M India's refusal to do its own primary research is a feature, not a bug. By licensing proven global technology through a clean, predictable royalty rather than gambling capital on basic research in an emerging market, the company achieves capital efficiency a self-funded innovator never could. The returns on capital that so impress the market are, in large part, the arithmetic of not having to fund a laboratory. For investors, it's a reminder that the question is not "does this company innovate?" but "who pays for the innovation, and who keeps the profit?"

Moats live in process, not just product. It is tempting to think 3M's advantage is the chemical formula of its adhesive. But a formula can be reverse-engineered, and the green-and-yellow knockoffs prove that even a brand can be cloned. The more durable moat is the localized process of teaching a customer exactly how to apply a product to their specific production line — the engineering relationship, the qualification, the workflow integration. That knowledge can't be copied off a shelf, and it walks back out the door very slowly.

Price premiums survive when the cost of failure is high. This is the single most portable investing lesson in the whole story. Look for businesses where the product is a tiny share of the customer's total budget but its failure represents an outsized share of the customer's risk — the surgical drape against the infection, the VHB tape against the bus body, the abrasive against the re-validated robotic line. That asymmetry is the engine of sustainable pricing power, and it is the thread connecting 3M's best businesses. Where that asymmetry is absent — in commodity tape and mass-market sponges — the premium erodes and the bears are right.

3M India, in the end, is the quiet compounder of India's industrial era. It will never have the meteoric arc of a consumer-tech rocket ship. What it has instead is a century of accumulated material science, rented cheaply; a balance sheet that cannot break; and a slow, patient integration into the workflows of Indian factories, hospitals, and homes. That integration — the trust of a surgeon, the calibration of a robot, the habit of a homemaker reaching for the green-and-yellow sponge — is the kind of asset that compounds invisibly and lasts a very long time. It is a permanent fixture of India's manufacturing backbone, hiding in plain sight inside the tape, the mask, and the stethoscope.

XII. Recent News & Financial Pulse

To close, the current scoreboard, and the small number of things actually worth tracking.

For FY25, 3M India reported total revenue from operations of ₹4,445.6 crore, up about 6.1% year-on-year from ₹4,189.4 crore in FY24 — solid but unspectacular top-line growth that the bears will note sits well below what a 70x multiple implies.1 Net profit, however, fell roughly 18.4% to ₹476.1 crore.1 The profit drop deserves a footnote of context rather than alarm: it was driven substantially by a one-time tax settlement under the government's Vivad Se Vishwas dispute-resolution scheme and higher tax outlays, rather than by an operating deterioration.1 An investor should mentally normalize for that one-off when judging the underlying earnings power.

Beneath the headline, the segment story confirmed the thesis of this episode. Healthcare led the charge, climbing to ₹865.2 crore, while the consumer segment proved resilient at ₹465.7 crore; Safety & Industrial remained stable but cyclically sensitive, and Transportation & Electronics held its place as the largest revenue line.1 And true to form, the company confirmed a stellar dividend — ₹535 per share for the fiscal year — maintaining its standing as one of the premier cash-returning assets on the Indian market.17

So what should a long-term investor actually watch from here? Resist the temptation to track everything. Two or three indicators carry most of the signal. The first is the healthcare segment's growth rate — it is the fastest-growing, highest-quality, stickiest business, and its trajectory is the clearest read on whether the bull's mix-shift thesis is playing out. The second is the blended segment margin and revenue mix — specifically, whether the high-margin healthcare and premium consumer slices keep gaining share against the cyclical industrial businesses, because that mix shift is what would justify the premium multiple over time. And the third, for the governance-minded, is the royalty rate and related-party transaction trend — any creep upward in that ~3.25% royalty or in intercompany pricing would be the earliest warning that value is being quietly redirected from the minority toward the parent. Track those three, and you are tracking the real 3M India.

References

-

3M India Financial Facts Local — 3M India Investor Relations ↩↩↩↩↩↩↩↩↩↩↩↩↩↩

-

3M India Acquires remaining stake in 3M Electro & Communication India for Rs 590 crore — Business Standard, 2018-08-09 ↩↩↩

-

3M India Launches its first Abrasive Robotics Lab in Bengaluru — ProMFG Media, 2023-08-17 ↩

-

Grindwell Norton Consolidated Financial Results — Grindwell Norton IR, 2025-05-15 ↩

-

Carborundum Universal Financial Highlights — CUMI Murugappa IR, 2025-05-18 ↩

-

Pidilite Industries Annual Financial Reports — Pidilite IR, 2025-05-22 ↩↩

-

3M India Stock Screener & Ratios — Screener India, 2026-06-19 ↩↩↩↩↩↩↩↩↩↩↩

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube