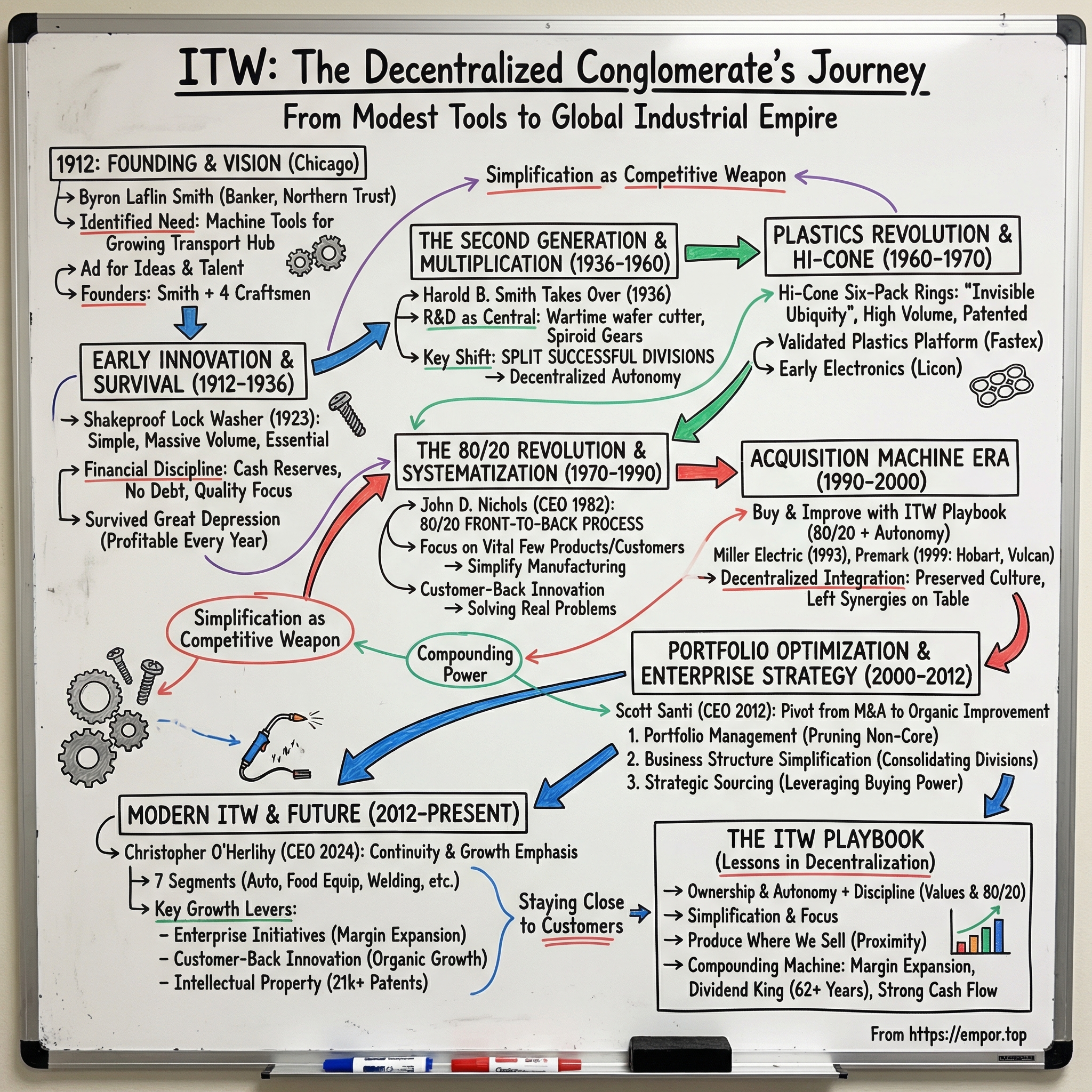

Illinois Tool Works: The Decentralized Conglomerate

I. Introduction & Episode Setup

Picture this: A Fortune 300 company with 44,000 employees spread across 51 countries, holding 20,900 patents, generating $15.9 billion in revenue—yet most people have never heard of it. Illinois Tool Works doesn't make consumer products you'd recognize on store shelves. Instead, ITW makes the machines that make everything else: the plastic rings holding your six-pack together, the welding equipment building skyscrapers, the food service equipment in restaurant kitchens, the fasteners in your car's engine. They're everywhere and nowhere, omnipresent yet invisible.

The company's story defies conventional business wisdom. While management consultants preach focus and simplification, ITW operates through hundreds of semi-autonomous business units. While Wall Street demands quarterly growth, ITW thinks in decades. While competitors chase scale through centralization, ITW deliberately breaks successful divisions into smaller pieces. The result? A sprawling industrial conglomerate that somehow maintains operating margins above 26%—nearly double the industry average.

At the heart of this paradox lies a question that has fascinated business scholars for decades: How did a small metal-cutting tool company founded in 1912 transform into one of the world's most successful decentralized empires? The answer involves three generations of the Smith family, a radical management philosophy developed over 30 years, and an acquisition machine that consumed over 100 companies in a single decade—only to break them apart again.

This is the story of ITW's century-long experiment in organized chaos, a masterclass in turning complexity into competitive advantage. It's about trusting factory floor workers more than headquarters executives, about finding fortune in the mundane corners of industry, and about building a $60 billion market cap company by thinking small. As we'll discover, ITW's greatest innovation wasn't any single product—it was the business model itself.

II. Byron Smith's Vision & The Founding Years (1912-1936)

The year was 1912, and Byron L. Smith had a problem. As president of the Northern Trust Company in Chicago, he watched the city transform into America's industrial heartland—railroads converging, stockyards expanding, factories sprouting along the lakefront. Capital was flooding into manufacturing ventures, but Smith, ever the cautious banker, wanted to invest his own money wisely. So he did something unusual for a financier of his stature: he placed a classified ad in the Chicago newspapers, seeking partners for a manufacturing venture.

The responses poured in—dreamers, schemers, legitimate businessmen. Smith meticulously interviewed candidates, applied his banker's scrutiny to their proposals, and selected four respondents whose ideas showed promise. With an initial capital investment of $22,500 (roughly $700,000 in today's dollars), Illinois Tool Works was born. The company would manufacture metal-cutting tools for the booming Chicago industrial complex—unglamorous products for an unglamorous market, but essential to every factory floor.

Smith's timing proved both fortunate and tragic. Chicago's emergence as the nation's transportation hub created insatiable demand for machine tools. Orders flooded in from meatpackers needing equipment for their processing lines, from railroad companies maintaining their rolling stock, from the nascent automobile industry establishing Midwest operations. But in 1914, just two years after founding ITW, Byron Smith died unexpectedly, leaving behind a profitable but precarious young company.

Enter Harold C. Smith, Byron's brother, who assumed the presidency in 1915. Where Byron had been the visionary financier, Harold proved to be the operational architect. He recognized that ITW's initial success stemmed not from making the cheapest tools, but from making tools that lasted longer and performed better under Chicago's brutal industrial conditions. "Quality at a fair price," became his mantra—a philosophy that sounds quaint today but was revolutionary in an era of planned obsolescence and corner-cutting.

Harold expanded ITW's portfolio methodically. Pumps for the oil industry. Compressors for manufacturing plants. Truck transmissions for the growing logistics sector. Each product line followed the same pattern: identify a specific industrial pain point, engineer a superior solution, then price it fairly rather than extracting maximum profit. He invested heavily in modern equipment—unusual for a company of ITW's size—believing that better machinery would create better products, which would create loyal customers, which would generate steady cash flow.

But Harold's most enduring contribution wasn't any particular product—it was ITW's conservative financial philosophy. Having witnessed the banking panics of 1907 and the market gyrations of the 1920s, Harold insisted on maintaining substantial cash reserves and avoiding debt whenever possible. "A company that owes nothing fears nothing," he reportedly told his board. This wasn't just fiscal prudence; it was strategic positioning. When competitors overleveraged themselves chasing growth, ITW could weather downturns and even acquire distressed assets at favorable prices.

By the mid-1920s, ITW had established itself as a reliable, if unremarkable, industrial supplier. Annual revenues reached $2 million. The company employed 400 workers in its Chicago facilities. Patents began accumulating—not breakthrough innovations, but incremental improvements that made customers' operations slightly more efficient. It was precisely the kind of steady, profitable, boring business that Wall Street ignored and customers depended upon.

The true test came in 1929. As the stock market crashed and the Great Depression gripped America, ITW's conservative balance sheet became its salvation. While competitors shuttered factories and defaulted on loans, ITW maintained operations, kept its workforce largely intact, and even continued investing in research and development. Harold Smith's caution had positioned the company not just to survive the economic catastrophe, but to emerge stronger.

By 1936, as Harold prepared to step down, ITW stood at a crossroads. The company had proven its resilience, established its reputation for quality, and accumulated the financial resources for expansion. But it remained essentially a regional player in a handful of industrial markets. The next generation would need to decide: remain a solid but limited Chicago manufacturer, or pursue a more ambitious vision? That decision would fall to Harold's son, Harold Byron Smith—and his answer would transform American manufacturing.

III. The Second Generation & Early Innovations (1936-1960)

Harold Byron Smith—grandson of founder Byron, son of Harold—assumed ITW's presidency in 1936 at age 35, carrying both the weight of family legacy and radical ideas about corporate structure. Where his predecessors built through steady expansion, the younger Smith envisioned something unprecedented: a company that would grow by dividing itself.

His first major move revealed this philosophy in action. ITW acquired Shakeproof Screw and Nut Lock Company, a small firm that had developed an ingenious solution to a maddening problem plaguing the automotive industry. Car manufacturers in Detroit were discovering that vibration from increasingly powerful engines would gradually loosen screws and bolts, causing everything from annoying rattles to catastrophic failures. Shakeproof's patented lock washers—twisted metal rings that maintained tension even under constant vibration—offered elegant simplicity.

But rather than folding Shakeproof into ITW's existing operations, Harold Byron Smith did something counterintuitive: he kept it separate. Shakeproof would maintain its own management, its own facilities, its own profit-and-loss responsibility. This wasn't neglect or lack of integration strategy—it was the birth of ITW's decentralized structure. Smith believed that keeping business units small and autonomous would preserve entrepreneurial energy while preventing bureaucratic bloat.

The approach proved prescient during World War II. When military contracts flooded in, ITW's autonomous divisions could pivot quickly without waiting for corporate approval. The company's engineers developed a revolutionary wafer cutter for artillery barrels that reduced production time by 60%—innovation born not from a central R&D lab but from factory floor workers closest to the problem. One division manufactured specialized fasteners for aircraft assembly; another produced components for naval vessels; a third developed tools for munitions factories. Each operated like a small, agile company while benefiting from ITW's financial strength and reputation.

The post-war boom presented both opportunity and challenge. Returning veterans fueled suburban expansion and automobile purchases. Consumer goods manufacturers needed increasingly sophisticated production equipment. But Smith recognized that ITW's growing portfolio of products and markets risked creating exactly the kind of unwieldy corporation he sought to avoid. His solution was radical: when a division grew beyond a certain size—typically $25-30 million in revenue—he would split it in two.

Critics called it corporate mitosis, unnecessary complexity. Why create two management teams where one sufficed? Why duplicate overhead costs? Smith's answer was that smaller units stayed closer to customers, made decisions faster, and maintained the hunger of a startup. A division president managing a $25 million business felt like an entrepreneur; one managing a $100 million business felt like a bureaucrat. The math seemed to support him—ITW's return on invested capital consistently exceeded larger, more centralized competitors.

By the late 1950s, the company had grown far beyond its tool-making origins. Employees increasingly referred to it simply as "ITW"—acknowledging that "Illinois Tool Works" no longer captured the breadth of its operations. The company now manufactured products for industries that didn't exist when Byron Smith placed his newspaper ad: jet engine components, television manufacturing equipment, early computer peripherals.

Two initiatives from this period would prove particularly significant for ITW's future. In 1958, the company established the Illinois Tools Division Gear School, bringing customers' engineers to Chicago for intensive training on gear design and application. This wasn't altruism—it was strategic customer lock-in. Engineers trained on ITW equipment specified ITW products in their designs. The following year, ITW founded Spiroid, dedicated to right-angle gear units. These gears, which transferred power through 90-degree turns with minimal friction, found applications everywhere from food mixers to industrial robots.

As 1960 approached, ITW stood as a testament to unconventional thinking. Revenue had grown to $60 million across dozens of autonomous divisions. The company held over 1,000 patents. Most remarkably, it had achieved this growth while maintaining the financial conservatism inherited from the founding generation—minimal debt, substantial cash reserves, steady dividend payments.

Harold Byron Smith had proven that a company could grow by dividing, could innovate through decentralization, could maintain entrepreneurial energy at industrial scale. But the next decade would bring ITW's most famous innovation—a simple piece of plastic that would generate billions in revenue and demonstrate the power of solving mundane problems brilliantly.

IV. The Plastic Revolution & Six-Pack Innovation (1960-1970)

The breakthrough came from an unlikely source: a frustrated ITW engineer drinking beer after work, annoyed by the cardboard carriers that kept tearing in his refrigerator. It was 1960, and Americans were buying more packaged beverages than ever—beer, soda, juice—but the packaging technology hadn't evolved since Prohibition's end. Cardboard carriers absorbed moisture, wooden crates were expensive to ship and store, and metal holders added significant cost. The engineer sketched an idea on a napkin: what if plastic rings could hold cans together?

That napkin sketch would become Hi-Cone, one of the most profitable patents in industrial history. The innovation seems obvious in retrospect—flexible plastic rings that grip can tops, allowing six or eight cans to be carried as a unit. But the engineering challenges were formidable. The plastic needed to be strong enough to support weight, flexible enough to stretch over cans, cheap enough for mass production, and stable enough to withstand temperature extremes from freezers to delivery trucks.

ITW's engineers spent two years perfecting the formulation and manufacturing process. They developed specialized equipment that could extrude, cut, and package the carriers at speeds matching modern canning lines. When they presented the finished product to brewery executives, the response was immediate: this would save 40-60% versus traditional packaging. Lighter weight meant lower shipping costs. Elimination of cardboard meant no more weather damage. Transparent plastic meant better product visibility. Customers could grab a six-pack with one hand while shopping.

But Harold Byron Smith, still leading ITW as it entered the 1960s, recognized that Hi-Cone represented more than just a successful product—it was a gateway into an entirely new material technology. Plastic was transforming American industry, and ITW's expertise in precision manufacturing positioned it perfectly for this revolution. Rather than simply licensing Hi-Cone technology, Smith created Fastex, a new division focused entirely on plastic fasteners and components.

Fastex embodied ITW's innovation philosophy: start with a customer problem, design backward to a solution, then find adjacent applications. The same engineers who developed Hi-Cone began creating plastic fasteners for automotive interiors—clips, rivets, and anchors that replaced metal components at a fraction of the cost and weight. Detroit's Big Three, locked in fierce competition and seeking any efficiency gain, became eager customers. A plastic clip might save only pennies per car, but multiplied across millions of vehicles, the savings reached tens of millions of dollars.

The division's growth trajectory was staggering. By 1965, Fastex had spawned three separate units, each focused on different market segments. One served the automotive industry, another targeted consumer goods manufacturers, a third developed specialized applications for aerospace and defense contractors. True to ITW tradition, each operated autonomously, maintaining its own customer relationships and innovation priorities.

The defense market proved particularly lucrative as Vietnam War spending accelerated. ITW developed specialized switches for military communications equipment, precision gears for helicopter transmissions, and plastic components for infantry equipment. These weren't commodity products but highly engineered solutions requiring extensive testing and certification. The military's exacting standards forced ITW to develop quality control processes that would later benefit its commercial customers.

Meanwhile, the computer industry's emergence created demand for entirely new component categories. ITW engineers developed anti-static plastic housings for sensitive electronics, precision gears for tape drives, and specialized fasteners for rapidly assembled computer cases. IBM alone became a multimillion-dollar customer, specifying ITW components across its product line.

By decade's end, ITW had transformed from a Midwest tool manufacturer into something unprecedented: a decentralized conglomerate unified by material science expertise and customer-focused innovation. The company now operated 50 divisions generating $150 million in annual revenue. Its patent portfolio had grown to 3,000, with Hi-Cone alone generating licensing fees from producers worldwide.

In 1970, Harold Byron Smith stepped down as CEO after 34 years of leadership, leaving behind a radically different company than he had inherited. ITW was now internationally recognized, with operations in Europe and Asia. Its products touched virtually every industrial sector. Most importantly, it had developed a replicable innovation process: identify a specific customer frustration, develop a narrowly targeted solution, then systematically explore adjacent applications.

The Hi-Cone story became ITW legend, told to every new engineer as inspiration and instruction. A simple observation—cardboard carriers tear when wet—had generated hundreds of millions in revenue. The lesson was clear: fortune lay not in revolutionary breakthroughs but in solving the mundane problems that customers faced every day. This philosophy would guide ITW's next phase of growth, as it codified its approach into something even more powerful—a comprehensive business model that would become the envy of industrial companies worldwide.

V. The 80/20 Revolution & Decentralization (1970-1990)

The insight came from Vilfredo Pareto, the Italian economist who observed that 80% of Italy's land was owned by 20% of the population. But at ITW in the early 1970s, a group of division presidents realized this principle explained something profound about their own businesses: roughly 80% of their sales came from 20% of their products, sold to 20% of their customers. This wasn't just an interesting observation—it was a revelation that would reshape American manufacturing.

Under new CEO John Nichols, who took the helm in 1970, ITW began developing what would become its legendary business model—a system so effective that Harvard Business School would later teach it as a case study, yet so culturally specific that competitors struggled to replicate it. The model rested on three pillars that seemed simple individually but proved transformative in combination: the 80/20 Front-to-Back Process, Customer-Back Innovation, and Decentralized Entrepreneurial Culture.

The 80/20 process started with brutal honesty. Division managers were instructed to analyze every product, every customer, every transaction. Which products generated the most profit? Which customers created the most complexity? Which activities added value versus mere motion? The results were often shocking. One division discovered that 50% of its SKUs generated less than 5% of profits. Another found that its largest customer by revenue was actually unprofitable after accounting for service costs and payment terms.

But unlike traditional cost-cutting exercises, ITW's 80/20 wasn't about abandonment—it was about focus. Rather than eliminating the unprofitable 80%, divisions would either find ways to make these products profitable (through price increases or process improvements) or transition customers to better alternatives. The goal wasn't to shrink but to simplify, not to retreat but to redeploy resources toward higher-value activities.

The implementation required unusual courage. In 1975, one division president walked away from a $10 million contract with a major automotive manufacturer because the terms would have required dedicated equipment and inventory that violated 80/20 principles. Wall Street analysts called it insane. Five years later, that same division was generating 30% operating margins by focusing on smaller, more profitable customers who valued ITW's technical expertise over rock-bottom pricing. The transformation accelerated when ITW became a public company, listing on the New York Stock Exchange in the mid-1970s. This access to capital markets coincided with another strategic milestone: the 1976 acquisition of Devcon, solidifying ITW's industrial polymer offerings. Devcon brought expertise in wear-resistant coatings and maintenance/repair/operations (MRO) solutions—products that epitomized the 80/20 philosophy. A small tube of epoxy might cost $20 but save thousands in equipment downtime. Customers didn't care about price; they cared about reliability.

Customer-Back Innovation, the second pillar, reversed traditional R&D thinking. Instead of engineers in labs dreaming up products to push onto markets, ITW's approach started with a customer's specific problem and worked backward to a solution. Division presidents were expected to spend at least 30% of their time with customers, not reviewing spreadsheets but walking factory floors, understanding pain points, observing workarounds.

This customer intimacy led to unexpected innovations. A packaging division noticed brewery workers struggling with condensation on bottle-filling lines. Within six months, ITW had developed a moisture-resistant adhesive that became an industry standard. A fastener division observed automotive workers using multiple tools for a single assembly task. The solution: a revolutionary clip system that reduced assembly time by 40%. None of these innovations would have emerged from a centralized R&D facility.

The third pillar—Decentralized Entrepreneurial Culture—was perhaps most radical. By 1980, ITW operated through nearly 100 separate business units, each with its own P&L responsibility. Division presidents had extraordinary autonomy: they could approve capital expenditures, set pricing, hire and fire, even pursue small acquisitions without corporate approval. The only requirements: maintain ITW's ethical standards, achieve target returns on invested capital, and share best practices with sister divisions.

This extreme decentralization created fascinating dynamics. Division presidents competed fiercely for resources and recognition, yet collaborated when customers needed integrated solutions. The company developed an internal "technology transfer" process where innovations from one division could be licensed to others—creating internal markets for intellectual property. A breakthrough in automotive fasteners might find applications in construction or aerospace, with the originating division receiving royalties from internal transfers.

The 1980s saw ITW embark on an aggressive acquisition strategy, with 32 acquisitions doubling the company's size to $1.5 billion while leadership further decentralized by handing control to individual businesses. But unlike traditional conglomerate builders who sought synergies through integration, ITW typically left acquired companies alone, applying 80/20 principles to simplify their operations while preserving their entrepreneurial culture.

The approach confounded Wall Street analysts accustomed to economies of scale and centralized efficiency. How could a company with hundreds of small divisions possibly compete with focused, integrated competitors? The answer lay in what ITW called "the power of smallness." Small divisions stayed hungry, innovative, responsive. They couldn't hide poor performance in consolidated results. They couldn't blame corporate headquarters for strategic mistakes. Success or failure rested entirely on division management—creating an ownership mentality rare in large corporations.

By 1990, ITW had grown to $1.5 billion in revenue across 200 autonomous divisions. Operating margins consistently exceeded 15%, extraordinary for industrial manufacturing. Return on invested capital approached 20%, nearly double the industry average. The company held over 5,000 patents, most generated by engineers working directly with customers rather than in isolated R&D centers.

Critics argued this complexity was unsustainable, that ITW would eventually collapse under its own weight. But as the company entered the 1990s, it was about to prove that its unconventional model could scale even further—through an acquisition spree that would shock even its supporters.

VI. The Acquisition Machine Era (1990-2000)

The Berlin Wall had just fallen, globalization was accelerating, and ITW's new CEO James Farrell inherited a company at an inflection point in 1990. Where his predecessors had made selective acquisitions, Farrell would transform ITW into perhaps the most prolific acquirer in industrial history—completing over 200 deals in a single decade, expanding from $1.5 billion to over $9 billion in revenue. Yet remarkably, this wasn't empire building for its own sake. It was 80/20 philosophy applied to M&A itself.

Farrell's acquisition strategy defied conventional wisdom from the start. While competitors sought "transformational" mega-deals that would reshape their companies overnight, ITW pursued dozens of small, bolt-on acquisitions—typically $50-200 million companies that dominated narrow niches. The logic was compelling: smaller deals meant lower risk, faster integration, and preservation of entrepreneurial culture. A $100 million acquisition that failed might sting; a $3 billion bet that went wrong could destroy the company.

The 1993 acquisition of Miller Group Ltd., a maker of arc welding equipment with $250 million in revenues, exemplified the approach. Miller wasn't just a welding company—it was the technology leader in specific welding applications for shipbuilding and heavy construction. ITW didn't try to merge Miller with existing operations or extract cost synergies through consolidation. Instead, following its decentralization philosophy, Miller was broken into five separate divisions, each focused on distinct customer segments. Within three years, the former Miller operations were generating 25% operating margins, far exceeding pre-acquisition performance.

The pace of acquisitions accelerated through the mid-1990s, sometimes closing multiple deals per month. ITW developed an acquisition machine as sophisticated as its operational model. A dedicated team of former division presidents—operators who understood the business, not just financial engineers—identified targets. Due diligence focused less on synergies and integration plans, more on fundamental questions: Does this company solve real customer problems? Can 80/20 principles improve its operations? Will current management thrive in ITW's decentralized culture?

In late 1995, ITW made its first hostile takeover bid in company history, a $134 million offer for fastener maker Elco Industries, though the venture failed after being outbid by Textron. During this period, revenues were growing at about 20% annually, with profits increasing even faster—40% in 1995 alone. The failed Elco bid revealed something important about ITW's acquisition philosophy: they would compete aggressively but never overpay. Walking away from deals became as important as closing them.

The discipline paid off spectacularly. By 1998, ITW was generating $5.6 billion in revenue with operating margins approaching 18%. The company now operated over 400 business units across 40 countries. But Farrell wasn't satisfied. He believed ITW's decentralized model and acquisition expertise could handle something bigger—much bigger.

In November 1999, ITW completed the biggest acquisition in its history, a $3.4 billion deal for Premark International, Inc. Premark was itself a conglomerate, owning Hobart commercial food equipment, Vulcan cooking equipment, Wilsonart decorative laminates, and several other businesses generating $2.5 billion in combined revenue. The acquisition nearly doubled ITW's size overnight and sent shockwaves through the business community. Had ITW finally abandoned its small-deal discipline for the allure of transformational M&A?

The answer came quickly: no. Within months of closing, ITW began dissecting Premark into dozens of focused business units. Hobart's massive food equipment division was split into separate units for cooking equipment, refrigeration, dishwashers, and food preparation. Wilsonart was divided by customer segment—commercial construction, residential remodeling, furniture manufacturers. Non-core assets like West Bend small appliances, Precor fitness equipment, and Florida Tile were divested entirely. What looked like a massive consolidation play was actually ITW's decentralization philosophy applied at unprecedented scale.

The integration—or rather, dis-integration—of Premark demonstrated ITW's organizational genius. Each new division received an experienced ITW executive as mentor, not to manage but to teach 80/20 principles and cultural values. Corporate headquarters provided financial resources and best practices but no mandates. Division presidents were told: "You know your business better than we do. Apply these tools, achieve these returns, maintain these values. How you do it is up to you."

By 2000, ITW had grown to nearly 600 separate business units generating $9.3 billion in revenue. The company employed 60,000 people across 45 countries. Its patent portfolio exceeded 10,000. Most remarkably, despite this explosive growth through acquisition, operating margins had actually increased to 18.5%, and return on invested capital exceeded 20%. The acquisition machine hadn't diluted ITW's performance—it had enhanced it.

Wall Street remained skeptical. Analysts questioned how long ITW could maintain control over such a sprawling empire. The dot-com bubble was bursting, recession loomed, and industrial companies were struggling. Surely ITW's complexity would become a liability in tough times? But as the new millennium dawned, ITW would prove that its decentralized model wasn't just suited for growth—it was equally powerful for optimization and value creation.

VII. Portfolio Optimization & Enterprise Strategy (2000-2012)

The dot-com crash of 2000 hit industrial America hard. Orders evaporated, customers delayed capital expenditures, and overcapacity plagued every sector. For ITW, now a $9 billion colossus with 600 business units, the recession became an unexpected laboratory for testing whether extreme decentralization could handle adversity as well as it had handled growth.

The answer emerged through thousands of micro-decisions rather than grand corporate strategy. Each division president, managing their small slice of ITW, made brutal but surgical cuts. Unprofitable product lines were eliminated. Marginal customers were fired or charged more. Manufacturing footprints were optimized. Because decisions were made locally by managers who knew their businesses intimately, ITW avoided the across-the-board cuts that devastated competitors. A fastener division serving aerospace might be investing and hiring while an automotive division two buildings away was restructuring.

By the early 2000s, ITW's presence expanded dramatically in global emerging markets, with businesses operating in Brazil, Russia, India and China as revenue generated outside North America increased significantly. But this wasn't traditional international expansion through exported products or massive new facilities. Instead, ITW acquired small local companies in each market, applied 80/20 principles to improve their operations, then let local management run the business. A Chinese fastener company understood Chinese customers better than any American executive ever could.

The recovery from the dot-com recession revealed something profound: ITW had become too complex even for its own decentralized model. With 600 business units, best practice sharing was breaking down. Division presidents couldn't possibly know what innovations were happening elsewhere in the company. Customers complained about dealing with multiple ITW divisions for related products. The company that had grown through division was now being constrained by it.

Enter David Speer, who became CEO in 2005 with a mandate to rationalize ITW's portfolio without destroying its entrepreneurial culture. Speer's solution was elegant: Portfolio Management, a systematic process for evaluating every business unit against consistent criteria. Was the division growing? Were margins improving? Did it have sustainable competitive advantages? Could 80/20 principles drive further improvement? If the answer to any was "no," the division faced three options: fix, merge, or divest.

The Premark assets became the proving ground for Portfolio Management. West Bend small appliances—profitable but strategically irrelevant—was sold. Precor fitness equipment, despite strong brand recognition, didn't fit ITW's industrial focus and was divested. Florida Tile faced consolidation in a commoditizing industry and was sold to private equity. These weren't fire sales but strategic exits, often at premium valuations to buyers who valued the assets more highly.

But Portfolio Management wasn't just about divestiture—it was about focus and investment. Divisions that passed the strategic filters received increased resources. The food equipment businesses from Premark, initially viewed skeptically, proved to be gems. Restaurants needed equipment that could withstand 18-hour daily use in harsh conditions—exactly the kind of engineered durability ITW excelled at providing. The company doubled down, acquiring complementary food equipment businesses and expanding globally.

The 2008 financial crisis provided the ultimate test of Portfolio Management. As credit markets froze and industrial production plummeted, ITW's revenues fell 23% from peak to trough. Yet the company remained solidly profitable throughout the crisis, never cut its dividend, and emerged stronger than most competitors. The secret: Portfolio Management had already eliminated marginal businesses, 80/20 had reduced complexity, and decentralization allowed rapid response to changing conditions.

In 2012, ITW celebrated its 100-year anniversary while launching a company-wide Enterprise Strategy, centered on generating maximum performance through ITW's differentiated business model. This wasn't a departure from ITW's traditional approach but rather its codification and intensification. The Enterprise Strategy formalized what had been cultural knowledge into teachable processes.

The strategy set ambitious targets: organic growth above GDP, operating margins expanding 200 basis points, returns on invested capital exceeding 20%, and free cash flow consistently above net income. These weren't aspirational goals but mathematical outcomes of properly applied 80/20 principles and portfolio optimization. Every business unit received training, tools, and clear expectations. Underperformers faced rapid intervention or exit.

By 2012's end, ITW had transformed from 800 business units at the peak to approximately 500, yet revenues had recovered to $11.8 billion. Operating margins reached 17.8%, up from 13% a decade earlier. Return on invested capital hit 16.5%. The company had proven that you could shrink to grow, that less complexity meant more value, that discipline trumped diversification.

As ITW entered its second century, it faced new questions. Could a company built on industrial manufacturing thrive in an increasingly digital economy? Could decentralization work when customers demanded integrated solutions? Could the 80/20 philosophy remain relevant as data analytics promised to optimize everything? The next phase of ITW's evolution would need to answer these challenges while preserving the entrepreneurial spirit that had driven a century of success.

VIII. Modern ITW: The Next Phase (2012-Present)

Scott Santi assumed ITW's leadership in 2012 with a paradoxical mandate: simplify the complex company without losing its entrepreneurial soul. The Enterprise Strategy was working—margins were expanding, returns increasing—but organic growth had stagnated. ITW had become brilliant at optimizing existing businesses but struggled to create new ones. The company that had invented the six-pack carrier and revolutionized industrial fasteners hadn't launched a breakthrough product in years.

Santi's diagnosis was counterintuitive: ITW had become too decentralized. With 500 business units, innovation was trapped in silos. A breakthrough in automotive might have applications in food equipment, but division presidents, focused on their own P&Ls, had little incentive to share. Customers increasingly wanted integrated solutions, not products from a dozen different ITW divisions. The structure that had enabled growth was now constraining it.

The solution was radical simplification. Over the next five years, ITW reorganized from 500 business units into 84 divisions within seven strategic segments. The new structure included Automotive OEM, Food Equipment, Test & Measurement/Electronics, Construction Products, Welding, Polymers & Fluids, and Specialty Products segments. This wasn't centralization—divisions maintained P&L responsibility and operational autonomy—but rather intelligent grouping that enabled collaboration while preserving accountability.

The impact was immediate and profound. Engineers from different divisions within the same segment began collaborating on customer solutions. The automotive segment could now offer integrated fastening systems, adhesives, and polymers as a complete solution rather than individual products. Food equipment divisions jointly developed IoT-enabled kitchen systems that connected previously standalone appliances. What had been impossible under extreme decentralization became natural under thoughtful organization. The financial results vindicated the new structure. In 2024, ITW generated $15.9 billion in revenue with operating income of $4.3 billion growing six percent, and operating margin increasing 170 basis points to a record 26.8%—with enterprise initiatives contributing 130 basis points. Six of seven segments expanded margins in 2024 with two segments achieving margins above 30 percent.

The seven-segment portfolio revealed ITW's strategic positioning. Automotive OEM (approximately 20% of revenue) supplied critical components as vehicles became increasingly complex. Food Equipment (17%) dominated commercial kitchen technology as restaurants demanded efficiency and reliability. Test & Measurement/Electronics (18%) provided precision instruments for quality control and product development. Construction Products (12%) offered engineered fastening systems for residential and commercial building. Welding (11%) served industrial fabrication and infrastructure projects. Polymers & Fluids (11%) supplied adhesives and specialty chemicals. Specialty Products (11%) included everything from beverage packaging to appliance components.

Each segment operated with remarkable autonomy while benefiting from shared expertise. The Construction Products segment, for instance, could leverage adhesive innovations from Polymers & Fluids while maintaining its own customer relationships and go-to-market strategy. This balance—independence with selective collaboration—proved optimal for both innovation and efficiency.

Customer-Back Innovation evolved significantly under the new structure. Rather than pushing technology for technology's sake, ITW divisions embedded engineers with customers to understand unmet needs. A food equipment team spent months in commercial kitchens, observing pain points that chefs didn't even recognize as problems. The result: a revolutionary ventless cooking system that eliminated the need for expensive exhaust hoods, opening new locations for restaurants previously constrained by building codes.

The automotive segment exemplified this evolution. As electric vehicles proliferated, ITW engineers recognized that EVs required entirely different fastening solutions—lighter weight, better thermal management, enhanced electrical insulation. Rather than adapting existing products, they developed new material formulations and designs specifically for EV applications. By 2024, ITW held critical content positions in most major EV platforms globally.

Digital transformation, often challenging for industrial companies, proceeded smoothly through ITW's decentralized model. Rather than imposing a top-down digital strategy, each division adopted technologies suited to their specific markets. A test equipment division developed cloud-based analytics for remote monitoring. A welding division created augmented reality training systems. Food equipment integrated IoT sensors for predictive maintenance. The diversity of approaches accelerated learning and reduced implementation risk.

In 2024, ITW launched what leadership called "The Next Phase," with organic growth as the highest priority after years of margin expansion. This wasn't abandonment of operational excellence but recognition that sustainable value creation required both growth and efficiency. The company set ambitious targets: outperform end markets by 100-200 basis points annually while continuing to expand margins through enterprise initiatives.

The strategy emphasized three growth vectors. First, geographic expansion in underserved markets, particularly Asia and Latin America, through targeted acquisitions and organic investment. Second, innovation acceleration through increased R&D spending and faster product development cycles. Third, market share gains through superior service and technical support—leveraging ITW's decentralized presence to stay closer to customers than larger, more centralized competitors.

As CEO Christopher O'Herlihy noted, "Throughout 2024, the ITW team delivered a year of solid operational and financial performance, achieving record financial results by consistently exceeding market growth and significantly improving profitability and margins. Building on this momentum, we will continue to outperform our key end markets in 2025 as we build above-market organic growth, driven by continuous improvement in Customer-Back Innovation, into a core ITW strength".

The modern ITW stands as validation of principles established over a century ago: customer focus, operational excellence, financial discipline, and decentralized decision-making. But it also represents continuous evolution—the company that began making metal-cutting tools now develops IoT-enabled systems and advanced materials. The challenge ahead is maintaining this balance between tradition and transformation.

IX. The ITW Playbook: Lessons in Decentralization

After a century of refinement, ITW's management system represents one of the most sophisticated approaches to industrial conglomerate management ever developed. It's a playbook that seems to violate every rule taught in business schools, yet consistently generates superior returns. Understanding how it works—and why competitors struggle to replicate it—reveals profound lessons about organizational design, human motivation, and value creation.

The foundation is deceptively simple: empowering teams to think like owners within a clear framework. Every division president at ITW essentially runs their own company. They control pricing, can approve capital expenditures up to predetermined limits, hire their own teams, and make strategic decisions about products and markets. This isn't delegation—it's genuine autonomy. A division president in Shanghai has as much authority over their business as one in Chicago.

But autonomy without accountability breeds chaos. ITW's framework provides the essential boundaries. Every division must achieve specific return on invested capital targets—typically above 20%. They must apply 80/20 principles to continuously simplify operations. They must maintain ITW's ethical standards without exception. They must share innovations and best practices with sister divisions. Within these guardrails, creativity flourishes.

The operational philosophy extends to manufacturing itself. ITW factories don't chase scale economies through massive, centralized production. Instead, they dedicate production lines to small product families—often just 3-4 products per line—enabling long, uninterrupted runs. This reduces changeover time, minimizes inventory, and improves quality. A fastener plant might have ten small lines each optimized for specific products rather than one large, "flexible" line trying to make everything.

Geographic strategy follows similar logic: manufacture where you sell. ITW operates hundreds of small factories close to customers rather than a few mega-facilities serving global markets. This increases costs by traditional measures—duplicated equipment, smaller purchasing volumes, more facilities to maintain. But it dramatically improves customer responsiveness, reduces logistics complexity, and creates resilience against disruptions. When COVID-19 shut down global supply chains, ITW's distributed manufacturing network proved remarkably robust.

The acquisition integration playbook has been refined through hundreds of transactions. Day one after closing, the acquired company's leadership meets with an ITW mentor—always an experienced operator, never a corporate staff member. The mentor doesn't impose changes but teaches tools: how to apply 80/20 analysis, how to identify value-creating versus value-destroying complexity, how to strengthen customer relationships. Integration isn't about synergy capture but capability transfer.

Most acquisitions are broken into smaller units within 12-18 months. A $200 million acquisition might become four $50 million divisions, each with focused market positions. This prevents the bureaucratic creep that afflicts most growing companies. It also multiplies leadership development opportunities—instead of one president and several vice presidents, ITW creates four presidents who learn by doing.

Talent development is perhaps ITW's most underappreciated advantage. The company promotes almost exclusively from within, viewing external hires at senior levels as failure of development. Young engineers and managers are given significant responsibility early—running a $30 million division at age 35 isn't unusual. Mistakes are tolerated if lessons are learned. Success is rewarded with larger divisions or new challenges, not corporate staff positions.

The company maintains unusual practices that reinforce its culture. There's no corporate jet—executives fly commercial, staying connected to the real economy. Headquarters remains deliberately small, under 200 people for a $16 billion company. Corporate approval requirements are minimal—a division president has more signing authority than many Fortune 500 CEOs. These aren't cost-saving measures but cultural statements: value creation happens in the divisions, not at headquarters.

Risk management through diversification is built into ITW's DNA. With seven major segments and dozens of end markets, no single customer, product, or geography can threaten the enterprise. This isn't the false diversification of unrelated conglomerates but thoughtful portfolio construction. Every business shares common characteristics: they solve specific customer problems through engineered products, generate recurring revenue through consumables or replacement cycles, and operate in markets with rational competition.

The financial philosophy remains remarkably consistent with founder Byron Smith's conservative approach. ITW maintains strong cash generation, with free cash flow consistently exceeding net income. Capital allocation follows clear priorities: organic growth investments first, then dividends (raised annually for decades), then share buybacks, and finally acquisitions—but only at reasonable valuations. The company has never pursued a "transformational" deal that would require significant leverage or distract from operations.

Core values—integrity, respect, trust, shared risk, and simplicity—aren't just wall posters but operating principles. Integrity means walking away from business that requires ethical compromise. Respect means treating the smallest supplier or customer with the same consideration as the largest. Trust means believing division presidents know their business better than headquarters ever could. Shared risk means everyone from factory workers to executives has skin in the game through profit sharing and equity ownership. Simplicity means constantly fighting complexity even when complexity seems profitable.

The power of this model compounds over time. Each year, hundreds of division presidents make thousands of decisions optimized for their specific situations. Most are small improvements—a slightly better product design, a more efficient process, a stronger customer relationship. But collectively, these micro-optimizations create macro advantages that no centralized organization could achieve. It's evolution through variation and selection rather than intelligent design.

Yet replication remains nearly impossible for competitors. The model requires not just processes but deeply embedded culture. It demands leaders willing to give up control, middle managers who think like owners, and front-line employees who take pride in continuous improvement. It needs patient shareholders who value long-term compounding over quarterly earnings beats. These elements take decades to develop and can be destroyed in quarters by wrong leadership.

X. Analysis & Investment Case

Understanding ITW as an investment requires looking beyond traditional metrics to appreciate how the company's unique model creates sustainable competitive advantages. While the stock has never been cheap by conventional measures—typically trading at premium multiples—long-term shareholders have been richly rewarded through consistent execution and compounding returns.

The competitive moat starts with market position. Across its segments, ITW typically holds #1 or #2 positions in narrow niches. These aren't commodity markets but specialized applications where switching costs are high and price is secondary to performance. When a beverage company has designed its entire canning line around Hi-Cone carriers, switching to save pennies per unit risks millions in retrofitting and downtime. When an automotive manufacturer has qualified ITW fasteners through extensive testing, changing suppliers for marginal savings makes no sense.

The 80/20 model creates economic advantages beyond market position. By focusing on the most profitable customers and products, ITW achieves structurally higher margins than competitors serving entire markets. A competitor matching ITW's prices for key accounts would destroy profitability on their broader portfolio. This selective service model is nearly impossible to replicate without abandoning existing customers—a decision few management teams will make.

Financial performance validates the strategy. In 2024, operating income of $4.3 billion grew six percent, and operating margin increased 170 basis points to 26.8 percent with enterprise initiatives contributing 130 basis points. These aren't cyclical peaks but sustainable improvements driven by operational excellence. The company consistently converts over 100% of net income to free cash flow, providing tremendous flexibility for capital allocation.

Capital allocation itself deserves recognition. Over the past decade, ITW has returned over $20 billion to shareholders through dividends and buybacks while maintaining a strong balance sheet and investing in organic growth. The discipline to avoid large, risky acquisitions—despite pressure from investment bankers and activists—has preserved value that many industrial conglomerates have destroyed through empire building.

The bear case centers on several concerns. First, cyclical exposure: while diversified across end markets, ITW remains sensitive to industrial production cycles. A global recession would impact most segments simultaneously, though the company's variable cost structure and operational flexibility provide cushioning. The 2008-2009 experience, where ITW remained profitable despite a 23% revenue decline, demonstrates this resilience.

Second, market maturity: many of ITW's end markets are mature, with growth tied to GDP rather than secular expansion. Electric vehicles provide opportunity in automotive, but also disruption risk to existing content. Construction faces long-term headwinds from high interest rates and affordability challenges. Food equipment depends on restaurant formation, which may be structurally challenged post-pandemic. These aren't existential threats but do limit organic growth potential.

Third, management execution: ITW's model depends heavily on cultural continuity and operational discipline. New leadership could be tempted to pursue more aggressive growth strategies, larger acquisitions, or organizational centralization—all of which could destroy long-term value. The company's history of internal promotion provides comfort, but leadership transitions always carry risk.

Foreign exchange represents ongoing headwind with approximately 40% of revenues generated internationally. Dollar strength reduces reported results, though natural hedging through local production mitigates operational impact. The company doesn't hedge translation exposure, accepting FX volatility as a cost of global diversification.

The bull case rests on ITW's proven ability to generate value through any economic environment. The Enterprise Strategy has consistently delivered 100+ basis points of annual margin improvement through operational excellence. Even with revenues flat, margin expansion and capital returns can drive high-single-digit EPS growth. This is not a company dependent on favorable markets but one that creates its own favorable economics.

The innovation pipeline, while not flashy, addresses real customer needs. EV content opportunities could offset traditional automotive headwinds. Automation and labor shortages drive demand for ITW's food equipment solutions. Infrastructure investment supports construction and welding segments. Sustainability requirements create opportunities for ITW's materials expertise. None of these are home runs, but collectively they support steady growth.

Valuation requires nuanced analysis. On trailing P/E, ITW typically screens as expensive. But adjusting for quality—consistent free cash flow generation, minimal capital intensity, strong returns on capital—the premium appears justified. The company's ability to compound value through cycles, rather than despite them, warrants a higher multiple than cyclical industrials.

For long-term investors, ITW offers a rare combination: the stability of a diversified industrial conglomerate with the growth dynamics of focused businesses, the operational excellence of lean manufacturing with the innovation culture of entrepreneurship, the financial strength of a century-old company with the agility of much smaller competitors. It's not a thrilling investment—no breakthrough products, transformational acquisitions, or restructuring stories—but rather a compound wealth creation machine that has delivered for generations of shareholders.

XI. Future Outlook & Closing Thoughts

Looking ahead to 2025, ITW's guidance reflects both confidence and realism: above-market organic growth of 0 to 2% based on current demand levels, with enterprise initiatives contributing approximately 100 basis points to margin improvement. These targets might seem modest compared to high-flying technology companies or restructuring stories, but they represent the sustainable value creation that has defined ITW for over a century.

The electric vehicle transition presents both opportunity and challenge. ITW's content per vehicle could increase as EVs require more sophisticated thermal management, electrical insulation, and lightweight materials—all areas where ITW excels. However, the transition also disrupts established supply chains and customer relationships. The company's approach—working directly with EV manufacturers to develop custom solutions rather than adapting existing products—reflects the customer-back innovation philosophy that has driven success for decades.

Sustainability initiatives are becoming growth drivers rather than compliance costs. ITW's equipment enables customers to reduce energy consumption, minimize waste, and meet environmental regulations. A new generation of welding equipment reduces power consumption by 40%. Food equipment innovations cut water usage in commercial kitchens by half. These aren't marketed as "green" products but as economic solutions that happen to be environmentally beneficial—a positioning that resonates with pragmatic industrial customers.

Geographic expansion remains a significant opportunity. Despite global presence, ITW is underpenetrated in many emerging markets. The company's localized manufacturing model—small factories serving regional customers—is particularly suited for markets where infrastructure, regulations, and customer needs vary significantly. Rather than exporting Western products, ITW acquires local companies and enhances their capabilities, creating solutions tailored to specific market needs.

Digital transformation continues, but at ITW's characteristic measured pace. The company isn't chasing buzzwords like "Industry 4.0" or "digital twins" but implementing practical technologies that solve real problems. Predictive maintenance algorithms reduce equipment downtime. Cloud-based monitoring enables remote service. Augmented reality assists with complex installations. These innovations emerge from divisions working with customers, not from corporate innovation labs.

Leadership succession planning reflects ITW's commitment to cultural continuity. The company maintains deep bench strength through systematic development of internal talent. Future leaders are groomed through progressive division management roles, ensuring they understand ITW's unique model before reaching senior positions. This isn't just about maintaining the status quo but ensuring leaders who can evolve the model while preserving its essential elements.

The broader lessons from ITW's century-long experiment in decentralized management remain highly relevant. In an era of increasing centralization—driven by technology platforms, data analytics, and global scale—ITW proves that pushing decision-making closer to customers can create superior value. The company's success challenges conventional wisdom about economies of scale, synergy capture, and strategic planning.

For operators, ITW demonstrates that sustainable competitive advantage comes not from any single innovation or strategy but from a coherent system of mutually reinforcing practices. The 80/20 philosophy only works with decentralized decision-making. Decentralization only works with strong cultural values. Values only matter with accountability for results. Remove any element and the system fails.

For investors, ITW illustrates the power of long-term compounding through consistent execution. The company has never delivered a spectacular year—no doubling of earnings, breakthrough products, or transformational deals. Instead, it has delivered dozens of good years, each building on the last, creating enormous value for patient shareholders. In a market increasingly focused on disruption and transformation, ITW proves that operational excellence and incremental improvement remain powerful wealth creation strategies.

The challenges ahead are real. Global supply chains are fragmenting. Labor markets remain tight. Geopolitical tensions threaten global trade. Technology is accelerating change across every industry. Yet ITW has navigated world wars, depressions, technological revolutions, and countless predictions of obsolescence. Each challenge has strengthened rather than weakened the company, forcing adaptation while reinforcing core principles.

As ITW enters its second century, the question isn't whether the model will survive but how it will evolve. The company that started making metal-cutting tools for Chicago factories now produces sophisticated electronics, advanced materials, and IoT-enabled equipment for global markets. The constant has been the approach: understand customer problems, develop focused solutions, operate with minimal complexity, and trust people closest to the market to make decisions.

Perhaps the most remarkable aspect of ITW's story is its reproducibility—not the specific practices but the underlying principles. Any organization can choose to focus on profitable customers rather than chasing volume. Any company can push decision-making closer to markets rather than centralizing control. Any management team can choose simplification over complexity, even when complexity seems profitable. The barrier isn't knowledge but courage—the courage to trust people, to say no to marginal business, to think long-term when markets demand immediate results.

Illinois Tool Works stands as a testament to the power of patient capital, operational excellence, and organizational design. It's a company that has created enormous value not by being brilliant but by being consistently good, not by revolutionary breakthroughs but by evolutionary improvement, not by grand strategies but by millions of small decisions optimized for local conditions. In a business world obsessed with disruption and transformation, ITW proves that there's still room for companies that simply execute better than everyone else, every day, for decades.

The story continues, written daily by thousands of employees solving customer problems, improving processes, and building businesses within the framework of a century-old model that remains as relevant today as when Byron Smith placed his newspaper ad in 1912. For those willing to look beyond the mundane products and boring markets, ITW offers profound lessons about value creation, organizational design, and the enduring power of decentralized entrepreneurship within large organizations.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube