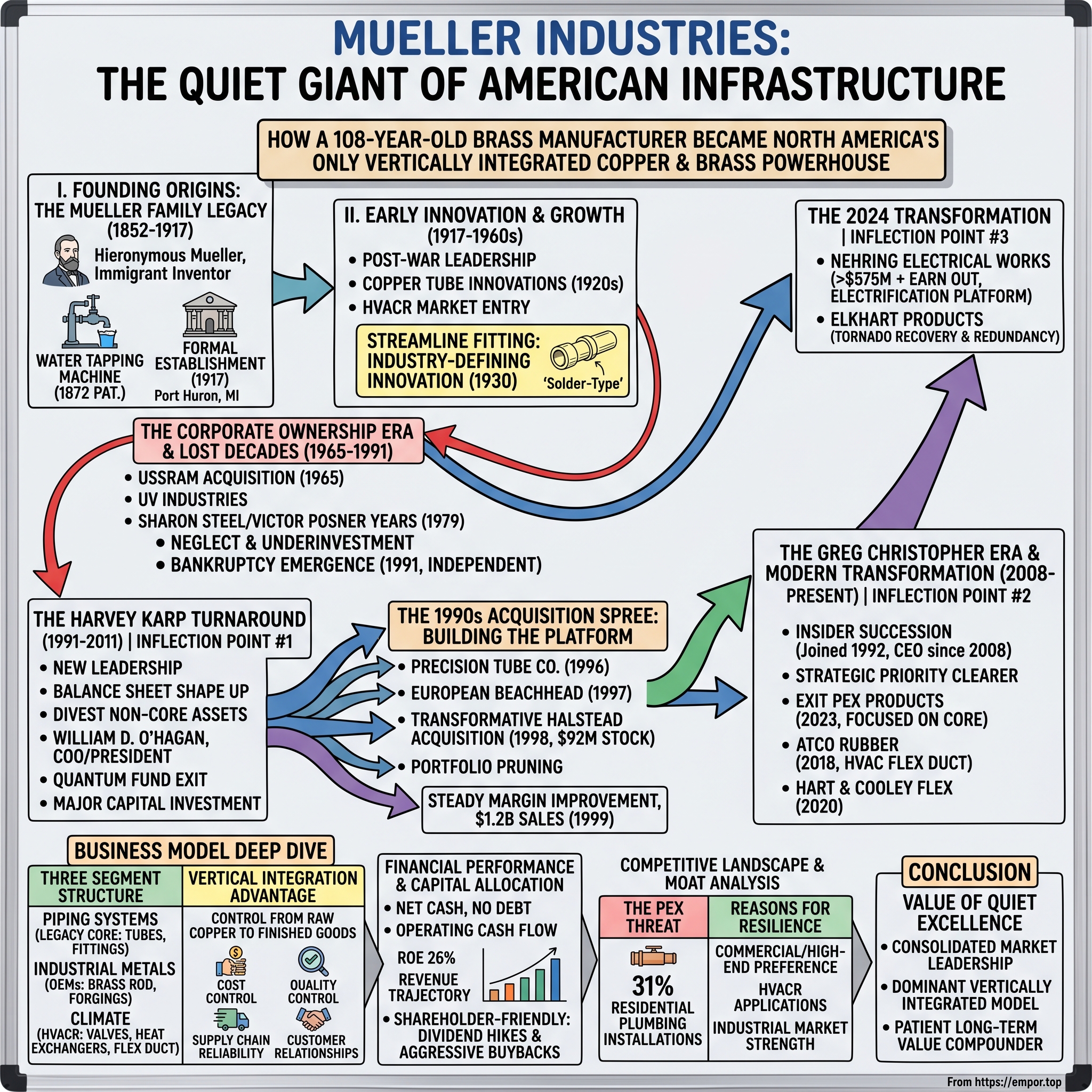

Mueller Industries: The Quiet Giant of American Infrastructure

I. Introduction: The Plumbing of Prosperity

Somewhere in the walls of your home, beneath the floors of a hospital, inside the condenser coil of your air conditioner, and coursing through the veins of power grids across America, there runs a silent network of copper and brass products that most people never think about. These tubes, fittings, valves, and forgings do not make headlines. They do not attract the attention of consumer brands or tech investors. Yet without them, modern life would come to a grinding halt.

Mueller Industries, Inc. (NYSE: MLI) is a global industrial corporation whose holdings are leading manufacturers and distributors of highly technical and essential products. Those products support critical infrastructure and serve a broad range of industries including plumbing, heating, ventilation, air conditioning and refrigeration (HVACR), industrial manufacturing, appliance, transportation, medical, military and defense and electrical.

With a market capitalization of approximately $11.6 billion, trailing twelve-month revenue of $4.14 billion, and an ROE of 26%, Mueller represents one of those rare industrial compounders that generates exceptional returns while operating in what most would consider a "boring" industry.

The central question that animates this story: How did a company founded by a German immigrant inventor in the 1850s survive the chaos of World War I, the Great Depression, serial acquisitions by corporate raiders, and a decade of bankruptcy-adjacent neglect—only to emerge in the 21st century as the dominant force in North American copper and brass manufacturing?

Mueller is the only vertically integrated manufacturer of copper tube and fittings, brass rod and forgings in North America, with operations in Europe, Asia and the Middle East. This unique positioning—the ability to control the manufacturing process from raw copper to finished products—creates a durable competitive moat that has proven remarkably difficult for competitors to replicate.

The story of Mueller Industries offers several key themes that will emerge throughout this analysis: the power of vertical integration as a moat in commodity-adjacent businesses; the crucial importance of capital allocation discipline; the surprising resilience of "boring" industrial companies that serve essential needs; and the value that competent management can unlock after decades of corporate neglect.

For investors, the Mueller story is a masterclass in what happens when an essential business, deeply embedded in critical infrastructure, falls into the hands of operators who understand its true potential.

II. Founding Origins: The Mueller Family Legacy (1852-1917)

The Immigrant Inventor

The Mueller story begins not with a corporate founding, but with a young man's curiosity about how water flows through buildings.

Mueller Industries traces its history back to 1852 when 20-year-old Hieronymous Mueller migrated to the United States. Mueller was an inventor with an interest in plumbing—particularly plumbing using copper.

This was a transformative era in American infrastructure. Indoor plumbing was still a luxury in most homes, and the technologies that would eventually bring running water to millions were just being developed. Hieronymous Mueller recognized early that copper's natural properties—its resistance to corrosion, its malleability, its antimicrobial qualities—made it the ideal material for conveying water safely.

He patented an improved water tapping machine in 1872. Mueller was the first to pour castings using brass in 1877. The business was incorporated as H. Mueller Manufacturing Company in Michigan in 1893 with $68,000 in capital.

That initial capital stake—roughly $2.4 million in today's dollars—seems almost quaint for a business that would eventually become a multi-billion dollar enterprise. But Hieronymous Mueller had identified something fundamental: as America urbanized and modernized, the demand for copper plumbing products would only grow.

The significance of brass and copper in America's plumbing revolution cannot be overstated. Before copper plumbing became standard, lead pipes were common—with all the health consequences we now understand. Mueller's innovations helped establish safer, more durable water systems that would become the backbone of American homes and commercial buildings.

Formal Company Establishment

The formal inception of the company, under the name Mueller Metals Company, occurred in 1917 in Port Huron, Michigan. This transition coincided with the construction of the U.S.'s first commercial forging facility for munitions during World War I.

The timing was not coincidental. With America's entry into World War I, industrial capacity became a matter of national survival. Mueller, like many industrial companies, participated in a general increase in manufacturing. The Port Huron facility was built specifically to produce munitions, and it represented the first commercial forging facility of its kind in the United States.

This wartime expansion established a pattern that would repeat throughout Mueller's history: the company's core competencies in metalworking proved valuable not only for civilian plumbing applications but also for military and defense purposes. The ability to precision-manufacture brass and copper components would later support both world wars, and Mueller's manufacturing strength played a key role in producing vital materials for both efforts.

Later, in 1927, Oscar Mueller established an independent brass tubing and fitting manufacturing business, known as Mueller Brass Company, by exchanging his interest in Mueller Co. for the Port Huron plant.

The corporate family tree can be confusing here—there would eventually be separate Mueller companies focused on different aspects of the plumbing business. But the Port Huron operation, focused on brass tubing and fittings, would become the direct ancestor of today's Mueller Industries. The foundation had been laid for a century of copper and brass manufacturing.

III. Early Innovation & Growth (1917-1960s)

Post-War Technological Leadership

Following World War I, Mueller did not simply rest on its wartime success. Instead, the company continued to make technological advances that would prove key to the growth of significant industries.

In 1923 the company introduced soft copper tube for underground water supplies and, in 1924, hard copper tube for indoor water supplies. By 1927, Mueller Brass Company (the new name having been adopted in 1925) was firmly established in the plumbing business and was producing a full line of fittings and valves produced in its own foundry.

The distinction between soft and hard copper tube may seem technical, but it was crucial. Soft copper could be bent and shaped to navigate underground obstacles, while hard copper provided the rigidity needed for indoor plumbing systems. Mueller's ability to produce both types—along with the fittings needed to connect them—established the company as a one-stop supplier for plumbing applications.

For the nascent mechanical refrigeration industry, the company provided brass forging that did not leak refrigeration gas like the porous castings previously in use. This innovation opened an entirely new market that would eventually become massive: heating, ventilation, air conditioning, and refrigeration (HVACR) would grow to represent a significant portion of Mueller's business over the following century.

The Streamline Fitting: Industry-Defining Innovation

Perhaps the company's most important innovation came in 1930 when the company introduced the revolutionary Streamline solder-type fitting. Previously, fittings—which joined pieces of tube—had been the weakest sections of pipes. The new solder-joined fittings, however, were actually stronger than the tubes they connected. It was because of this development that all-copper plumbing and heating systems were established as industry standards.

This is worth pausing on. Before the Streamline fitting, fittings were the weak point in any plumbing system—the place where leaks were most likely to occur, where maintenance was most frequently required. Mueller's innovation flipped this dynamic entirely. The fitting became stronger than the tube itself, creating a reliable, leak-proof connection that could last for decades.

Introduced in 1930, this fitting was a groundbreaking innovation that dramatically improved the efficiency and reliability of plumbing and HVACR systems.

The Streamline brand, born in 1930, continues to this day. It remains one of Mueller's most recognized product lines, a testament to the durability of genuine product innovation. The brand has evolved to become a world leader in piping systems, serving applications from residential plumbing to complex commercial and industrial installations.

Mid-Century Performance

Mueller continued to grow, reporting profits of $2.35 million on sales of $80.8 million in 1963.

By the early 1960s, Mueller had established itself as a diversified manufacturer of brass and copper products serving multiple end markets. The company was producing rods, forgings, tubes, and castings made from aluminum, copper, brass, bronze, and other alloys. The product range included refrigeration valves and fittings, chromium- and nickel-plated fabricated items, and the copper pipes, tubes, and fittings that remained the company's bread and butter.

Defense subcontracting had become a larger proportion of the business mix, demonstrating Mueller's ability to serve demanding, specification-heavy customers. Sales continued to expand through the 1960s, reaching $170 million in 1969 alongside record income of $12 million.

Yet even as the company prospered, management was not clinging to the idea of an independent Mueller with an indefinite future. Forces were gathering that would reshape the company's trajectory for the next quarter century.

IV. The Corporate Ownership Era & Lost Decades (1965-1991)

The USSRAM Acquisition

Having previously amassed a 72 percent share of Mueller, U.S. Smelting Refining and Mining (USSRAM) acquired the remaining shares and took full control in 1965.

U.S. Smelting Refining and Mining was a mining company whose primary products were gold, silver, lead, and zinc. The acquisition made strategic sense on paper: USSRAM could secure a vertically integrated supply chain, ensuring that the metals it mined would flow into value-added manufacturing. But in practice, Mueller became a subsidiary within a larger conglomerate whose primary focus lay elsewhere.

USSRAM changed its name to UV Industries, Inc. in 1970.

For Mueller, the transition to subsidiary status marked the beginning of a long period during which capital investment and strategic attention would be directed elsewhere. The company continued to operate, but the entrepreneurial energy that had driven innovation in earlier decades began to dissipate.

The Sharon Steel/Victor Posner Years

Sharon Steel Corporation acquired UV Industries in 1979. Sharon Steel filed for bankruptcy in 1987; Mueller remained a viable enterprise and does not file for Chapter 11.

The acquisition by Sharon Steel brought Mueller under the control of Victor Posner, one of the era's most notorious corporate raiders. Posner's approach to corporate management was extractive: he acquired companies through leveraged buyouts, minimized capital investment, and extracted cash through management fees and dividends.

For Mueller, this meant years of underinvestment and neglect of the core manufacturing business. Plant equipment aged without replacement. Product development slowed. The company continued to function—copper and brass products remained essential to American construction—but it was operating far below its potential.

When Sharon Steel filed for bankruptcy in 1987, Mueller remained a viable enterprise and did not file for Chapter 11. This speaks to the durability of the underlying business: even after years of neglect, Mueller's essential products and established customer relationships kept the company afloat when its parent collapsed.

The Bankruptcy Emergence

The issues surrounding Sharon were finally resolved on December 28, 1990, when negotiators, headed by Raymond Wechsler, an advisor to the Quantum Fund, hammered out a plan to divide up the company. After 25 years as a subsidiary, Mueller reemerged as an independent company called Mueller Industries, Inc. The new Mueller was an industrial concern that held its traditional plumbing and flow control equipment operation as well as natural resource holdings centered around a division called Arava Natural Resources Company, Inc. This new sector of the business included the Utah Railway Company—a short-line that carried coal to Provo, Utah, for transshipment by major rail carriers—Alaskan gold mining operations, and a variety of mining interests in Canada and the West.

The Quantum Fund connection is noteworthy. George Soros's famous hedge fund emerged as a significant stakeholder in the restructuring, seeing value in the manufacturing operations that had been neglected under Sharon Steel's ownership.

In its first year as an independent company, Mueller announced a loss of $43.7 million on sales of $441 million. Almost all of the 1991 loss was due to a revaluation of assets, coupled with costs related to the bankruptcy proceeding and restructuring of the business following the reorganization.

The company had survived, but it was battered. Plants needed upgrading. Management needed rebuilding. And the accumulated problems of 25 years of corporate neglect needed addressing. Mueller Industries, newly independent, stood at an inflection point.

V. The Harvey Karp Turnaround (1991-2011): Inflection Point #1

New Leadership & Immediate Actions

Harvey L. Karp, who became chairman and CEO on October 8, 1991, moved quickly to shape up the company. He enhanced the balance sheet by selling $25 million worth of investment grade notes and negotiated for expanded borrowing capabilities that provided $40 million.

Karp's arrival marked the beginning of Mueller's modern era. Unlike the absentee ownership of the Sharon Steel years, Karp brought an operator's sensibility and a clear focus on rebuilding the core manufacturing business.

His initial actions were textbook turnaround management. First, shore up the balance sheet to provide financial stability. Second, divest non-core assets to focus resources. Third, invest in the manufacturing operations that had been starved of capital for years.

In an effort to focus on the company's core manufacturing business, the sale of the malleable iron business—which had not been profitable for Mueller—was arranged in 1992. To help upgrade operations neglected for many years, Karp made a commitment to allocate more capital and undertake improvement projects.

He also negotiated settlements of litigation which asserted a $16.5 million guarantee obligation for the Sharon Steel business. This settlement turned out to be very favorable when Sharon filed Chapter 9 in the fourth quarter of 1992.

This legal maneuvering proved prescient: by settling before Sharon's final bankruptcy, Mueller avoided being dragged into prolonged litigation that could have hampered the recovery.

Building the Management Team

Finally, among other key executives, Karp recruited William D. O'Hagan, who had 32 years experience in the industry, to be Mueller's chief operating officer and president. Karp's efforts paid off handsomely—for the year ended 1992, earnings were up significantly, reaching $16.6 million on sales of $517.3 million.

O'Hagan brought the deep industry knowledge necessary to run day-to-day operations while Karp focused on strategy and capital allocation. This division of labor would prove effective: earnings rose dramatically even as the company invested in modernizing its manufacturing base.

The Quantum Fund Connection & Independence

After Mueller emerged from Sharon Steel's shadow, the Quantum Fund held about 46 percent of the common stock, with the remainder owned by Sharon Steel's creditors. The stock initially traded on the NASDAQ exchange, but the company gained a listing on the New York Stock Exchange in February 1991. During 1993 the Quantum Fund sold the bulk of its stake to the public through a secondary offering. Then in 1994 Mueller bought Quantum's remaining 9.6 percent stake for $25.9 million. Also in 1994, O'Hagan was promoted to president and CEO, with Karp remaining chairman.

The Quantum Fund's exit marked Mueller's transition to a truly independent public company with a dispersed shareholder base. The buyback of Quantum's remaining stake in 1994 demonstrated management's confidence in the company's prospects—and began what would become a long track record of shareholder-friendly capital allocation.

Capital Investment & Growth

The mid-1990s were marked by major capital outlays in which Mueller invested about $100 million in plant improvements that increased product capacity and efficiency. This was the anti-thesis of the Sharon Steel approach: instead of extracting cash, management was reinvesting in the business.

The steadily expanding economy in the mid-1990s fueled growth in housing starts, which was the key economic indicator for Mueller given the large portion of sales that were generated from the construction industry. Both revenues and earnings advanced steadily during this period, culminating in the 1996 figures of $61.2 million in net income on net sales of $729.9 million.

During 1995 the company declared a two-for-one stock split and also announced that the headquarters would be moved from Wichita to Memphis, Tennessee. The move, completed in May 1996, was taken in order to place the head office closer to Mueller's core manufacturing operations in Tennessee and Mississippi.

The Karp era had transformed Mueller from a bankruptcy-adjacent orphan into a growing, profitable manufacturer with a clear strategy and a modernizing manufacturing base. But the real growth spurt was still to come.

VI. The 1990s Acquisition Spree: Building the Platform

Strategic M&A Strategy

During the late 1990s, as Mueller continued to enjoy annual increases in revenues and profits, the company stepped up its growth efforts by completing a string of significant acquisitions.

The first came in late December 1996 when Precision Tube Company, Inc. of North Wales, Pennsylvania, was purchased for $6.6 million. Founded in 1948, Precision Tube produced copper, copper alloy, and aluminum tubing and fabricated tubular products, with its main product line being copper tubing for the baseboard heating industry. A second plant in Salisbury, Maryland, manufactured semirigid and flexible coaxial cables and assemblies used in the defense industry and in microwave technology.

The acquisition pattern revealed Mueller's strategy: bolt on companies that served adjacent markets, brought complementary capabilities, or expanded geographic reach—all while staying close to the core competency of nonferrous metal manufacturing.

European Expansion

In the first half of 1997, Mueller established its first significant European beachhead through the acquisition of two copper tube manufacturers. This marked an important step toward geographic diversification, reducing dependence on the North American construction cycle.

The Halstead Acquisition

In November 1998 Mueller completed the acquisition of Halstead Industries, Inc. for about $92 million in stock. The privately held Halstead, which was founded in Pittsburgh in 1936 and which had sales in 1997 of approximately $250 million, produced copper tubing for plumbing, air conditioning, and refrigeration applications at plants in Wynne, Arkansas, and Clinton, Tennessee. Following the acquisition, Halstead was renamed Mueller Copper Tube Products, Inc.

This was the transformative deal. Halstead's scale and capabilities significantly expanded Mueller's copper tube business, strengthening the vertical integration that would become the company's defining competitive advantage.

Focused Portfolio Management

In addition to its series of acquisitions and its continued investment of tens of millions of dollars to modernize and update existing plants, Mueller during the late 1990s also divested a number of its natural resources operations as these businesses were increasingly viewed as noncore. At the end of 1997 the company sold off a coal mining business whose operations had been shut down earlier in the decade.

This portfolio pruning reflected management's clarity about what Mueller should be: a manufacturer of copper, brass, and related products serving construction and industrial markets—not a diversified conglomerate with mining and railroad operations.

Results of the Strategy

The results spoke for themselves. In the late 1990s, Mueller Industries marked significant milestones in earnings growth, with 1999 representing the eighth consecutive year of increases, as net income rose 32% to $99.3 million on net sales of $1.2 billion.

Profit margins during this period improved steadily, supported by cost controls and market positioning in copper and brass products. The company had grown from a bankruptcy emergence at $517 million in sales to over $1.2 billion in less than a decade, while dramatically improving profitability.

By the early 2000s, Mueller had established the platform that would support continued growth for the next two decades. The question was whether the company could find leadership capable of taking it to the next level.

VII. The Greg Christopher Era & Modern Transformation (2008-Present): Inflection Point #2

Leadership Transition

The announcement coincided with the naming of Gregory Christopher to the company's newly created COO position. Christopher, who has been with Mueller since 1992, most recently served as president of the company's standard products division.

Greg Christopher's rise to leadership represents the quintessential insider succession. Mr. Christopher has served as Chief Executive Officer since October 2008 and Chairman of the Board of Directors since January 2016. He joined Mueller Industries in 1992 and previously held various Company and industry leadership roles in sales, manufacturing, distribution, and supply chain management.

This is the profile of a leader who knows every corner of the business: someone who worked his way up through operations, who understands the manufacturing processes intimately, and who has survived multiple cycles of the construction industry. Christopher's tenure now exceeds 17 years as CEO—a remarkable run that has produced exceptional results.

Gregory Christopher, Chief Executive Officer commented at the time of Karp's retirement, "While we are saddened to lose Harvey as Chairman of our Company, we are excited that he will consult with us for at least the next six years. Harvey has been critical in building Mueller and his determination and contributions cannot be overstated."

Strategic Evolution Under Christopher

The company's evolution accelerated under Christopher's leadership. The strategic priorities became clearer: sell off non-core businesses, acquire companies that expand into higher-margin niches, and double down on the vertical integration that provides competitive advantage.

Mueller ventured into PEX products via its Heatlink acquisition, exploring the plastic piping market that was gaining share in residential plumbing. But the company eventually exited that business in 2023, recognizing that its core strengths lay in copper and metal systems rather than competing directly in plastics.

This willingness to experiment—and the discipline to exit when experiments don't work—reflects sophisticated capital allocation. Too many companies double down on mistakes; Mueller cut its losses and refocused on strengths.

Key Modern Acquisitions

Mueller Industries announced that it has acquired ATCO Rubber Products, Inc. (ATCO) for approximately $162.8 million. ATCO is an industry leader in the manufacturing and distribution of insulated HVAC flexible duct systems and will support the Company's strategy to grow its Climate Products businesses to become a more valuable resource to its HVAC customers.

The 2018 ATCO acquisition bolstered Mueller's Climate segment, expanding beyond pure copper products into the broader HVAC ecosystem. ATCO had revenues of approximately $166 million with 800 employees in its fiscal year ending December 31, 2017.

In 2020, Mueller announced that it had signed a definitive agreement to purchase the Hart & Cooley Flexible Duct business. The acquisition was scheduled to close in late January 2021.

These deals reflected a strategic push to become a more comprehensive supplier to HVAC customers, expanding the relationship beyond just copper components.

The 2024 Transformation: Inflection Point #3

2024 proved to be a transformative year for Mueller's acquisition strategy.

Mueller Industries announced that it had entered into a definitive agreement to acquire Nehring Electrical Works Company and certain of its affiliated companies for approximately $575 million, subject to customary purchase price adjustments, plus an additional $25 million earn out. Founded in 1912 and headquartered in DeKalb, Illinois, Nehring produces high-quality wire and cable solutions for the utility, telecommunication, electrical distribution, and OEM markets.

The acquisition of Nehring provides a substantial platform for long-term growth in the electrical and power infrastructure space, and complements the other critical infrastructure sectors already supported by Mueller. This transaction aligns with Mueller's acquisition strategy to target high-quality businesses with leading market positions, attractive margin and cash flow profiles and strong management teams.

The Nehring acquisition represented Mueller's most significant expansion in years, moving the company into the electrical wire and cable business that serves utility and telecom markets. With power grid upgrades and data center construction driving demand for electrical infrastructure, this positions Mueller to benefit from the growing electrification trend.

Mueller Industries completed the acquisition of Elkhart Products Corporation for approximately $38.2 million on August 2, 2024.

The acquisition is expected to accelerate the recovery of Mueller's tornado-impacted Covington copper fittings business, expand and complement current operations, and provide redundant manufacturing capabilities for solder fittings.

The Elkhart acquisition addressed a specific operational challenge: Mueller's Covington, Tennessee copper fittings facility had been substantially impacted by a tornado in March 2023. Rather than simply rebuilding, Mueller acquired a competitor that could both accelerate recovery and provide redundant manufacturing capabilities.

VIII. Business Model Deep Dive

The Three Segment Structure

Mueller Industries manufactures and sells copper, brass, and aluminum products in the United States, the United Kingdom, Canada, Asia and the Middle East, and Mexico. It operates through three segments: Piping Systems, Industrial Metals, and Climate. The Piping Systems segment offers copper tubes, fittings, line sets, and pipe nipples; resells steel pipe, brass and plastic plumbing valves, malleable iron fittings, faucets, and plumbing specialties. This segment sells its products to wholesalers in the plumbing and refrigeration markets, distributors to the manufactured housing and recreational vehicle industries, building material retailers, and air-conditioning original equipment manufacturers (OEMs).

Piping Systems represents the legacy core of the business: copper tubes, fittings, and related products for plumbing and HVACR applications. This segment serves wholesalers and OEMs, supplying the essential components that connect water, refrigerant, and heating systems throughout North America and beyond.

The Industrial Metals segment offers brass, bronze, and copper alloy rods; cold-form aluminum and copper products; high-volume machining of aluminum, steel, brass, and cast-iron impacts and castings for automotive applications; brass and aluminum forgings; brass, aluminum, and stainless steel valves; fluid control solutions; and gas train assembles; specialty copper, copper alloy, and aluminum tube to OEMs in the industrial, construction, plumbing, refrigeration, utility, telecommunication, and electrical distribution markets.

Industrial Metals serves original equipment manufacturers with higher-value-added products: brass rod, forgings, impact extrusions, and specialty components for automotive, industrial, and increasingly, electrical applications.

The Climate segment provides valves, protection devices, and brass fittings; and coaxial heat exchangers and twisted tubes to wholesalers and OEMs in the HVAC and refrigeration markets. This segment also manufactures and distributes high-pressure components and accessories, as well as insulated HVAC flexible duct systems.

Climate encompasses components specifically designed for HVACR applications, including the flexible duct systems acquired through ATCO and Hart & Cooley, as well as specialized heat exchangers and refrigeration components.

The Vertical Integration Advantage

Mueller Industries stands as the sole vertically integrated manufacturer of copper tube and fittings, as well as brass rod and forgings, in North America. This unique operational structure provides a distinct competitive advantage.

This is the core of Mueller's moat. The company controls the manufacturing process from raw copper to finished products. It does not rely on outside suppliers for critical intermediate steps. This vertical integration provides several advantages:

Cost Control: By controlling multiple stages of production, Mueller can capture margin at each step rather than paying it to suppliers. When a competitor buys copper tube from one company, fittings from another, and distributes through yet another channel, margin leaks at each interface. Mueller captures that margin internally.

Quality Control: Vertical integration allows Mueller to maintain consistent quality standards throughout the manufacturing process. In industries where product failures can cause water damage, refrigerant leaks, or safety hazards, quality assurance matters.

Supply Chain Reliability: When supply chains are disrupted—as they were during COVID-19 and continue to be due to geopolitical tensions—vertically integrated companies can continue operating while competitors scramble for components.

Customer Relationships: The ability to supply a complete package of products (tubes plus fittings plus valves) makes Mueller a more valuable supplier to wholesalers and OEMs than competitors who can only provide partial solutions.

Market Position

The company holds substantial market penetration in critical sectors. As of January 2024, it commanded 27% of the HVAC market, 24% in plumbing applications, and 19% in the industrial segment.

Mueller Industries leads North America via its Streamline and LinesetsPlus brands and generated 75% of 2025 sales domestically under tariff protection.

This domestic concentration, combined with tariff protection for copper products, creates a degree of insulation from international competition. While Chinese and other international producers can compete on price, the cost of shipping heavy copper products combined with import duties often eliminates their advantage.

IX. Financial Performance & Capital Allocation

Recent Financial Strength

Full-year 2024 performance showed net sales of $3.8 billion (up 10.2%), with operating income at $770.4 million (up 1.9%). The company generated $645.9 million in operating cash flow for the year, ending with $1.06 billion in cash and short-term investments.

Mueller Industries revenue for the twelve months ending September 30, 2025 was $4.140B, a 15.71% increase year-over-year.

The revenue trajectory demonstrates consistent growth even amid challenging macroeconomic conditions. More importantly, this growth has been accompanied by exceptional profitability and cash generation.

In its third-quarter 2025 earnings report, the company reported a net income of $208.1 million, an increase from $168.7 million, and net sales of $1.08 billion, up from $997.8 million. The diluted earnings per share also rose to $1.88 from $1.48, highlighting a robust financial performance. Key financial metrics for the quarter included an operating income of $276.1 million, compared to $206.7 million in the previous year.

"Softness in residential construction, combined with an influx of imported products ahead of escalating tariffs, exerted downward pressure on unit volumes in several of our businesses. Amidst these challenges, our team once again delivered an excellent quarter," said Greg Christopher, Mueller's CEO.

Balance Sheet Fortress

The Company generated $140.1 million of cash from operations in the fourth quarter, and $645.9 million for the year. Year-end cash and short-term investments totaled $1.06 billion, and our current ratio is 5.1 to 1.

The company reported a net cash generation from operations of $310.1 million, with a strong cash balance of $1.3 billion and no debt. The current ratio remains robust at 4.8 to 1.

Mueller carries effectively zero net debt and has accumulated over $1 billion in cash. This is remarkable for an industrial company—most peers carry significant debt to finance operations and acquisitions. The fortress balance sheet provides multiple advantages:

Acquisition Optionality: Mueller can move quickly on attractive acquisitions, paying cash without the delays of debt financing or the dilution of equity issuance.

Cycle Resilience: In cyclical downturns, cash-rich companies can not only survive but often acquire distressed competitors at attractive prices.

Dividend and Buyback Flexibility: The company can return cash to shareholders even during difficult periods.

Capital Allocation Philosophy

In early 2021, Mueller hiked its quarterly dividend from 10 cents to 13 cents and has since kept increasing it. It's not a massive yield (~1%). More impactful, they leaned hard into buybacks. For years, the share count hovered around 114 million, drifting only modestly. But in early 2025, management took a big swing. Shares outstanding fell sharply to about 110.7 million, a drop of more than 3 million shares in just a few quarters. That's nearly a 3% reduction in under a year, a meaningful cut for a company of this size.

The industrial manufacturer, currently valued at nearly $12 billion, has maintained dividend payments for 22 consecutive years and has raised its dividend for 4 consecutive years, according to InvestingPro data.

For the fifth consecutive year, Mueller Industries has announced a double digit increase to its quarterly dividend. The Board of Directors declared a regular quarterly cash dividend of $.25 per share, to be paid on March 28, 2025 to stockholders of record as of the close of business on March 14, 2025. This represents a 25 percent increase over the 2024 quarterly dividend.

Management has demonstrated itself to be rational and disciplined capital allocators. The pattern is clear: maintain the fortress balance sheet, invest in core operations and strategic acquisitions, return excess cash through dividends and opportunistic buybacks.

X. Competitive Landscape & Moat Analysis

The Competitive Threat from PEX

The Copper Pipes & Tubes Industry Analysis identifies increasing competition from substitutes such as aluminum, plastic (PEX), and stainless steel. PEX piping currently represents 31% of residential plumbing installations due to lower cost and easier installation.

This is the elephant in the room for copper tube manufacturers. PEX (cross-linked polyethylene) has been steadily gaining market share in residential plumbing applications for decades. It's cheaper than copper, easier to install (no soldering required), and flexible enough to snake through walls and around obstacles.

Competition from Alternative Materials: The copper pipes market faces increasing competition from alternative materials such as PEX and PVC, which are often cheaper and easier to install. In future, the market share of PEX is expected to reach 30%, challenging copper's traditional dominance. This shift may lead to reduced demand for copper pipes, compelling manufacturers to innovate and differentiate their products to retain market share.

Although copper pipe market has reduced by 50% in the past 10 years, it remains a primary choice for plumbing applications across the U.S.

However, the threat is not as existential as it might appear:

Commercial and High-End Applications: Copper remains preferred in commercial buildings, high-end residential construction, and applications requiring maximum durability. PEX is primarily taking share in budget-conscious residential installations.

HVACR Applications: PEX cannot replace copper in refrigerant lines, high-pressure systems, or applications requiring copper's thermal conductivity. Mueller's substantial HVACR business is relatively insulated from PEX competition.

Industrial Applications: Brass rod, forgings, and specialized components serve industrial markets where plastic alternatives do not exist.

Porter's Five Forces Analysis

Threat of New Entrants (Low): Vertical integration creates massive barriers to entry. A new entrant would need to replicate Mueller's entire manufacturing chain—from copper melting to tube drawing to fitting production—to compete effectively. The capital requirements are substantial, and the learning curve is steep.

Bargaining Power of Suppliers (Moderate): Mueller buys raw copper, which is a globally-traded commodity with transparent pricing. While copper price volatility affects margins, Mueller generally passes through raw material costs to customers.

Bargaining Power of Buyers (Moderate): Mueller's customers include wholesalers, distributors, and OEMs. No single customer dominates, and Mueller's vertical integration and brand recognition provide some pricing power. However, in commodity-like products, price competition is real.

Threat of Substitutes (Moderate-High): PEX and other plastics represent genuine substitutes in some applications, though copper maintains advantages in commercial, HVACR, and high-performance applications.

Competitive Rivalry (Moderate): In copper tubes and fittings, Mueller's main U.S. competitors are private or foreign-owned players like Cerro Flow and Cambridge-Lee (Mexican-owned). There are also importers from Asia and Europe. The presence of multiple competitors prevents monopoly pricing, but Mueller's vertical integration provides cost advantages that are difficult to replicate.

Hamilton Helmer's 7 Powers Framework

Scale Economies: Mueller's size allows it to spread fixed manufacturing costs across larger production volumes than smaller competitors.

Network Effects: Limited in this industry—Mueller's products don't become more valuable as more customers use them.

Counter-Positioning: Mueller's vertical integration represents a business model that competitors cannot easily replicate without dismantling their existing operations.

Switching Costs: Moderate—wholesalers have established relationships and systems, but switching to an alternative supplier is possible.

Branding: The Streamline brand carries significant recognition in the industry, though this provides less pricing power than consumer brands.

Cornered Resource: Mueller's manufacturing facilities, customer relationships, and operational know-how represent accumulated assets that competitors cannot easily replicate.

Process Power: Decades of manufacturing optimization have created institutional knowledge that drives efficiency advantages.

Overall, Mueller's competitive position rests primarily on counter-positioning (vertical integration that competitors cannot easily match), scale economies, and process power accumulated through over a century of manufacturing experience.

XI. Risks, Opportunities, and the Path Forward

Key Risks

PEX Substitution: The continued adoption of PEX in residential plumbing represents a structural headwind for copper tube demand. Management has addressed this by diversifying into HVACR, industrial, and now electrical markets where plastic substitution is not feasible.

Copper Price Volatility: COMEX copper averaged $4.57 per pound in Q1 2025, an 18.4% increase from Q1 2024, impacting cost structures. While Mueller generally passes through commodity costs, rapid price swings can create margin pressure and demand uncertainty.

Construction Cycle Exposure: Mueller's business remains highly correlated with housing starts and commercial construction activity. Prolonged construction downturns would impact revenue and profitability.

Key Person Risk: CEO Greg Christopher has led the company exceptionally well for 17+ years, but succession planning becomes increasingly important as key executives age.

Key Opportunities

Electrification Tailwinds: Nehring plugs Mueller into the utility and telecom markets, giving it a toehold in the growing electrification trend (think power grid upgrades and data centers). Power grid modernization and data center construction are multi-decade tailwinds that the Nehring acquisition positions Mueller to capitalize on.

Infrastructure Investment: Federal infrastructure programs are driving investment in water systems, buildings, and industrial facilities—all of which require Mueller's products.

Acquisition Opportunities: The fortress balance sheet positions Mueller to acquire attractive businesses as opportunities arise.

Market Share Gains: As smaller competitors face cost pressures, Mueller's scale and integration advantages should enable continued market share gains.

XII. Key Performance Indicators to Track

For investors following Mueller Industries, three metrics provide the most insight into the company's ongoing performance:

1. Operating Margin

Mueller's operating margins have expanded dramatically over the past two decades, reflecting operational leverage and vertical integration benefits. With an EBITDA of $962.8 million on trailing revenue of $4.14 billion, Mueller is generating approximately 23% EBITDA margins—exceptional for a manufacturing business. Tracking this metric reveals whether the company is maintaining pricing power and operational efficiency.

2. Cash Generation vs. Capital Deployment

Mueller's ability to generate cash in excess of maintenance capital expenditure is the foundation of its shareholder returns. The balance between reinvestment in operations, acquisitions, dividends, and buybacks reflects management's capital allocation discipline. A sustained deterioration in cash conversion or unwise acquisition spending would be warning signs.

3. Revenue Mix by Segment and End Market

As Mueller diversifies beyond pure residential plumbing—into HVACR, industrial applications, and now electrical infrastructure—tracking the revenue contribution from each segment reveals whether the strategic evolution is succeeding. Increasing contributions from higher-growth markets like electrical transmission would validate the Nehring acquisition thesis.

XIII. Conclusion: The Value of Quiet Excellence

Mueller Industries offers a case study in what happens when a genuinely excellent business falls into the hands of operators who understand its potential. After decades of neglect under conglomerate ownership, the company emerged from bankruptcy in 1991 as a damaged but fundamentally sound enterprise. Harvey Karp's turnaround, followed by Greg Christopher's continued stewardship, transformed Mueller into North America's dominant copper and brass manufacturer.

Mueller's track record of over 30 years of profitable growth through all industry cycles demonstrates the resilience and sustainability of our business model.

The company's competitive advantage rests on vertical integration that competitors cannot easily replicate, manufacturing excellence accumulated over a century, and disciplined capital allocation that generates consistent shareholder returns. While the threat of PEX substitution in residential plumbing is real, Mueller has diversified into markets—HVACR, industrial, and electrical—where copper and brass remain essential.

Mueller ended 2024 on a very positive note, and in terms of quarter over quarter operating income performance, the fourth quarter was the strongest of the year. Mueller's concentration in the U.S. and status as a leading manufacturer positions it well, as the U.S. remains one of the most secure end markets. The company maintains a positive outlook for 2025 and beyond.

For long-term fundamental investors, Mueller Industries represents the kind of enterprise that rarely makes headlines but consistently compounds shareholder value. The pipes in your walls, the fittings in your HVAC system, the brass components in industrial machinery—these products will be needed as long as buildings are constructed and maintained. Mueller's position as the dominant supplier, with unmatched vertical integration and a fortress balance sheet, positions the company to capture value from that essential demand for decades to come.

The quiet giant of American infrastructure continues to build wealth for those patient enough to appreciate its merits.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube