Franklin Electric: The Hidden Giant of the Water Economy

The Essential Infrastructure Play on Global Water Scarcity

Somewhere in the American heartland, in a modest Indiana facility that most investors have never heard of, approximately 20,000 pumps, motors, and controls roll off production lines every single day. These machines will help move 3 trillion gallons of fresh water and 1 billion gallons of fuel worldwide—before the sun sets again tomorrow. The company responsible for this staggering output carries a name that might evoke the 18th century's most famous polymath rather than a modern industrial powerhouse, yet Franklin Electric has quietly built itself into what it proudly calls "the world's largest manufacturer of submersible electric motors."

Franklin Electric (NASDAQ: FELE) is a global manufacturer and distributor of systems and technologies for moving and protecting the world's most critical resources: water, fuel, and electricity. The company serves customers in residential, commercial, agricultural, industrial, municipal, and energy applications.

The question that should animate any serious investor is deceptively simple: How did a company that started making backpack generators for World War II paratroopers transform itself into a $4.4 billion infrastructure essential with a global manufacturing footprint spanning eleven countries?

In 2024, the company made revenue of $2.02 billion, a decrease over revenue in 2023 of $2.06 billion. GAAP diluted earnings per share for the year was $3.86, versus $4.11 in 2023. While the topline modestly contracted, what lies beneath these figures tells a far more compelling story about disciplined capital allocation, strategic vertical integration, and positioning for what may be the defining infrastructure challenge of the 21st century: global water scarcity.

The Energy Systems segment achieved notable growth, prompting a name change from Fueling Systems to better reflect its market strategy. The company ended the year with a strong cash position and anticipates increased sales in 2025, projecting revenues between $2.09 billion and $2.15 billion.

The Founding Story: From War to Water (1944-1950)

A Backpack Generator and a Bold Pivot

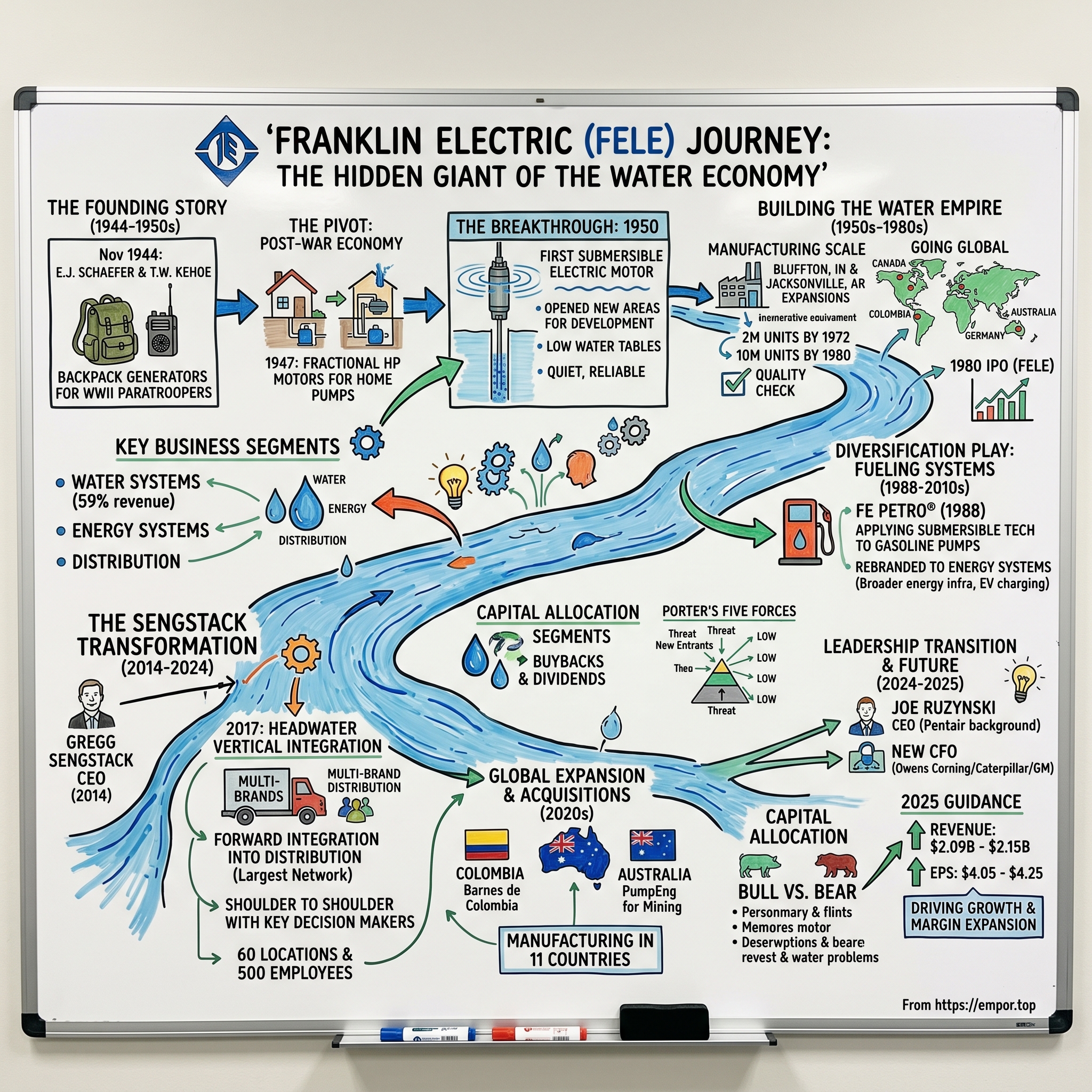

Picture November 1944. The Allies are pushing through Europe. In the small town of Bluffton, Indiana—population barely 6,000—two electrical engineers in their forties are placing a bet on American manufacturing. The Franklin Electric Company was founded in Bluffton, Indiana, by E.J. (Ed) Schaefer and T.W. (Wayne) Kehoe. Schaefer and Kehoe were already successful electrical engineers who believed they could make a go of manufacturing small electric motors on a mass scale.

The founding capital? With their wives as their business partners, and less than $20,000 in start-up capital, Schaefer and Kehoe started the company in November 1944. In today's dollars, that's roughly equivalent to an angel round of under $350,000—modest even by bootstrapped standards.

Why "Franklin Electric"? From the very beginning the two engineers had their sights set on serving a nation-wide market, and hence they were reluctant to name the new firm after themselves. Instead they christened the concern after Benjamin Franklin, whom they considered the country's first electrical engineer, because of his early experiments with electromagnetism.

The company's first product was a backpack generator to power the radio equipment paratroopers used during WWII. It was a solid government contract, but Schaefer and Kehoe were engineers, not defense contractors. They understood that war economies are temporary.

The Post-War Pivot That Made the Company

When WWII concluded, Franklin experienced a reduction in orders. Schaefer and Kehoe began designing and manufacturing fractional horsepower motors to pump water into homes or out of flooded basements to adjust to the peacetime economy.

This pivot proved spectacularly well-timed. This new product hit the market coinciding with the home building boom that occurred as G.I.s returned from war. The motors performed well and led to nearly $1.7 million in sales in 1947. From government contracts to consumer products in under three years—the kind of strategic agility that would characterize Franklin Electric's evolution for decades to come.

But the true breakthrough came in 1950. In 1950, Franklin introduced the first electric motor that was fully submersible. The new pump motors were quiet, resistant to freezing, smaller, easy to install, and had a high pumping capacity. The new motors could recover water from much deeper in the earth, making it possible for the first time to develop areas with low water tables.

Consider what this meant for post-war America. Vast swaths of the Southwest, Great Plains, and rural America had limited access to municipal water systems. Low water tables made traditional pump technology impractical. Franklin's submersible motor literally opened new territories for development—a piece of enabling technology that's easy to overlook from our modern vantage point.

The motors also proved extremely versatile. Eventually, they would be used for gasoline pumps, commercial air conditioning units, crude oil recovery, and deep-sea use.

For investors, this origin story illuminates a pattern that persists today: Franklin Electric builds essential infrastructure technology, positions itself as the technical leader in a niche, then extends that expertise into adjacent markets. The $20,000 startup became a diversified industrial with $2 billion in annual sales by following this playbook repeatedly across eight decades.

Building the Water Empire (1950s-1980s)

Scaling Through Innovation and Manufacturing Excellence

The 1950s through the 1980s were Franklin Electric's empire-building phase—a period of relentless capacity expansion, manufacturing excellence, and geographic reach that established the competitive moat the company still enjoys today.

The company expanded its Bluffton, Indiana, plant by 74,000 square feet and acquired a 200,000-square-foot manufacturing facility in Jacksonville, Arkansas, to meet growing demand for submersible motors, with production surpassing 2 million units by 1972. Sales reached $64 million that year, reflecting robust growth driven by innovations in water pumping systems.

Two million units. Consider the manufacturing discipline required: each submersible motor must function flawlessly while fully submerged, often for years or decades, in well depths that make field repair impractical. The company was building its reputation on reliability in applications where failure meant expensive service calls or complete system replacement.

Further expansions included a 50,000-square-foot addition to the Bluffton plant in 1975 and the introduction of the four-inch Super Stainless motor, enhancing durability for groundwater applications. In 1980, Franklin Electric acquired a factory in Wilburton, Oklahoma, and achieved the production of its 10 millionth fractional horsepower motor, solidifying its position as a leader in electric motor manufacturing.

Ten million motors by 1980—this milestone speaks to the cumulative manufacturing know-how that becomes extraordinarily difficult for competitors to replicate. Each motor produced generates insights about failure modes, materials performance, and process optimization that feed forward into improved designs and lower defect rates.

Going Global

The 1970s also saw an expansion of Franklin's overseas activities. The company had established its first foreign presence as early as 1962 when it set up a plant in Dandenong, Victoria, Australia, a venture in which Franklin had a 50 percent holding. A year afterwards it established its first wholly-owned subsidiary, Franklin Electric of Canada; in 1965 Franklin Electric Europa GmbH, a wholly-owned subsidiary located in Wittlich, West Germany, was formed. In the early-1960s foreign sales accounted for barely three percent of Franklin's total business.

The international expansion reflected a strategic insight: water pumping is a global need, but local presence matters for service, distribution, and regulatory compliance. Rather than simply exporting from Indiana, Franklin built manufacturing capabilities close to key markets—a strategy that has compounded over decades.

As a publicly traded company on the NASDAQ stock exchange under the ticker symbol FELE since its initial public offering in 1980, Franklin Electric employs approximately 6,300 people globally as of the end of 2024.

The 1980 IPO marked Franklin's transition from a regional manufacturer to a publicly accountable enterprise with obligations to outside shareholders. It also provided growth capital that would fuel the next phase of expansion.

The Diversification Play: Fueling Systems (1988-2010s)

Applying Motor Expertise to New Markets

By the mid-60s, it was clear that Franklin motors could pump more than just water. The company began designing and producing motors to pump oil, as well as motors for undersea use. Eventually, Franklin developed a motor to move gasoline and founded FE Petro in 1988 (which would later be called Franklin Fueling Systems).

The creation of FE Petro (later Franklin Fueling Systems, now rebranded as Energy Systems) demonstrated Franklin's ability to leverage core motor competencies into entirely new market segments. The strategic logic was compelling: the same submersible motor technology that reliably pumped water from wells could pump gasoline from underground storage tanks at retail fuel stations.

In 1988, Charles "Chuck" C. Franklin founded FE PETRO® with a vision to provide an innovative submersible turbine pump for the safe transfer of petroleum from underground tanks to aboveground fuel dispensers. Chuck partnered with Franklin Electric to provide the motors that would drive FE PETRO® submersible turbine pumps.

FE Petro introduced devices such as variable length pumps and the Mag Shell pump. Through organic innovation and acquisitions, Franklin Fueling Systems built out a complete portfolio of petroleum equipment products.

Recognizing the Company's diverse portfolio and growth strategy, it renamed its Fueling Systems segment to Energy Systems to better reflect the markets and customers served by this business. The rebranding reflects the segment's evolution beyond petroleum into broader energy infrastructure—including EV charging applications and critical power monitoring.

The fueling systems business provides Franklin with diversification benefits during cyclical water equipment demand. More importantly, it demonstrates the company's capacity to transfer technical expertise across industry boundaries—a trait that distinguishes truly innovative industrial companies from commodity manufacturers.

The Sengstack Transformation (2014-2024)

A Decade of Strategic Evolution

Gregg Sengstack, who has served as CEO since 2014 and chairperson since 2015, will continue as executive chairperson.

Gregg Sengstack's decade-long tenure as CEO represents one of the most consequential leadership periods in Franklin Electric's history. Gregg C. Sengstack first joined Franklin Electric in 1988 and has been President and Chief Operating Officer since 2011. He had previously been Senior Vice President and President, Franklin Fueling Systems and International Water Group and has held numerous positions in the Company's Finance organization before becoming Chief Financial Officer in 1999.

Mr. Sengstack holds a bachelor's degree from Bucknell University and masters in business administration from the University of Chicago. The Chicago Booth training shows in his approach—rigorous, analytical, and focused on capital allocation.

The board's assessment of his tenure speaks volumes: "He has been instrumental in transforming the company from a submersible motor manufacturer to a global leader in water and energy systems, with a diversified portfolio of products and services. Under his leadership, the company has achieved record revenues, earnings, and cash flows, while expanding its global footprint and enhancing its innovation capabilities."

As CEO, Gregg led a strategic transformation at Franklin Electric, which included the rapid expansion of the company's energy systems business, forward integration into distribution in the U.S., portfolio extensions into the adjacent water treatment market and the introduction of connected solutions across a range of the company's products.

This transformation wasn't a single strategic initiative but a sustained campaign across multiple fronts: vertical integration (Headwater), geographic expansion (global manufacturing footprint), product adjacencies (water treatment), and digital capabilities (connected solutions).

When assessing management quality, it's worth noting that Sengstack spent 26 years at Franklin before becoming CEO. He understood the business, the culture, and the competitive dynamics intimately before taking the helm. This "promote from within" pattern distinguishes companies with genuine institutional knowledge from those where CEOs arrive, make dramatic changes, and depart before consequences become clear.

The Headwater Vertical Integration (2017)

A Bold Forward Integration Into Distribution

In April 2017, Franklin Electric made a strategic move that fundamentally altered its position in the value chain. Franklin Electric announced today that it has reached agreement to acquire controlling interests in three distributors in the U.S. professional groundwater market. Franklin Electric will acquire 2M Company Inc. of Billings, Montana; Western Hydro Holding Corporation of Hayward, California and Drillers Service, Inc. (DSI) of Hickory, North Carolina for approximately $89 million in the aggregate, which includes assumed debt.

The $89 million deal created a distributor network — with 60 locations and nearly 500 employees — that Franklin Chairman and CEO Gregg Sengstack calls "the largest in the industry."

CEO Sengstack articulated the strategic rationale: "By forward integrating into distribution in the U.S., Franklin Electric is taking a logical next step in our evolution as a groundwater pumping systems company. This action places Franklin Electric shoulder to shoulder with the key decision makers in this end market—distributors and the installing contractors. The Headwater companies will continue to operate as full line wholesale distributors with a focus on total water systems support, including products from all industry manufacturers."

This last point deserves emphasis: Headwater wasn't designed as a captive distribution channel for Franklin products only. The Headwater companies will continue to operate as full line wholesale distributors with a focus on total water systems support, including products from all industry manufacturers.

The new segment is expected to have operating income margins of approximately 4 to 6 percent and pre-tax return on capital measures consistent with historical Franklin Electric returns after certain integration actions are complete. The new segment will have approximately $275 million of consolidated annual sales.

The initial projections proved conservative. Headwater has continued expanding through subsequent acquisitions. DeLancey Davis, President of Headwater Companies, commented: "We are pleased to add Blake to the Headwater family. Blake has served the pump industry and related water resource markets for over 40 years and has an outstanding reputation within the industry for quality service and technical depth. The acquisition of Blake adds to Headwater's commitment to the critical groundwater channel, provides geographic expansion in the New York and New England markets and furthers our objective of being the leading source of distribution for water systems solutions in the U.S."

This strategic move marks Headwater's inaugural venture into the Missouri market, aligning with our overarching goal of becoming the leading distributor of water systems solutions in the United States.

For investors, Headwater represents a structural competitive advantage. Distribution networks in specialized industrial segments are extraordinarily difficult to build from scratch—they require decades of contractor relationships, technical expertise, and geographic density. Franklin essentially bought its way past those barriers while ensuring that its own products receive preferential positioning without overtly alienating other manufacturers.

Global Expansion and Recent Acquisitions (2020s)

Strategic M&A With Discipline

Franklin Electric's acquisition activity has intensified in recent years, reflecting both available capital and strategic opportunity. The company's 2025 acquisitions demonstrate the geographic and capability expansion that characterizes its M&A approach.

Fort Wayne, IN – February 14, 2025 – Franklin Electric Co., Inc. announced it has signed a definitive agreement to acquire Barnes de Colombia S.A., a leading manufacturer and distributor of industrial and commercial pumps based in Cota, Cundinamarca, Colombia. This acquisition aligns with Franklin Electric's long-term growth and diversification goals, providing significant opportunities for expansion in Latin America. Barnes de Colombia, also operating under the WDM brand in certain countries including the US, is headquartered near Bogotá, Colombia. It has two manufacturing facilities and over eight stocking locations in Colombia, as well as assembly facilities in Mexico, Brazil, and Argentina, and local warehouses in Guatemala, Panama, Ecuador, Peru, and Chile. The acquisition enhances Franklin Electric's product portfolio and market presence in key Latin American regions.

Electricity, water and fuel systems and technologies distributor and manufacturer Franklin Electric agreed to acquire Barnes de Colombia and acquired Australian-based PumpEng. Terms of the transactions were not disclosed.

Perth, Australia-based PumpENG is an original equipment manufacturer of submersible pumps, serving customers in the mining industry. The company operates in Australia with locations in Kalgoorlie, Townsville and Adelaide, as well as in Twin Falls, ID. PumpENG, valued at $7.97 million, offers a range of dewatering pumps under brands like JetGuard, Guardian and Raptor, with products assembled in Australia.

CEO Joe Ruzynski explained the Latin American acquisition: "This acquisition not only strengthens our presence in the high-growth Latin American markets but also enhances our ability to serve our customers with an expanded portfolio of innovative and high-quality products. Barnes' approximately 400 team members and manufacturing and foundry capabilities will enhance our operating footprint materially."

The company also operates manufacturing facilities in the United States, Germany, Czech Republic, Italy, Turkey, Mexico, Brazil, Australia, South Africa, China, and Japan.

This global manufacturing footprint provides operational flexibility—the ability to serve regional markets with locally manufactured products while optimizing for tariffs, logistics, and supply chain resilience.

Leadership Transition (2024-2025)

New CEO, Fresh Perspectives

Franklin Electric Co., Inc. (NASDAQ: FELE), a global leader in water and energy systems, announced today that its Board of Directors has appointed Joe Ruzynski as Chief Executive Officer and a member of the Board, effective July 1, 2024.

Ruzynski, 49, joins Franklin Electric from nVent Electric plc (NYSE: NVT), a global leader in electrical connection and protection solutions, where he served as President of the Enclosures Segment since 2018. Prior to that, he held various leadership roles at Pentair plc, a global water technology company, including President of Technical Solutions and President of Flow and Filtration Solutions. He has over 25 years of experience in the industrial and electrical sectors, with a track record of driving growth, innovation, and operational excellence.

The Pentair background is particularly relevant—Pentair is a direct competitor in water technology, meaning Ruzynski understands Franklin's competitive landscape intimately. This industry experience contrasts with the "outsider CEO" trend that has sometimes produced value-destructive results at industrial companies.

Mrs. Wolfenbarger joined Franklin Electric in July 2025 as the Chief Financial Officer. Prior to joining Franklin Electric, she served as Vice President and Chief Financial Officer of the Insulation business for Owens Corning, a global leader in building materials. She previously held divisional CFO roles for Stryker, Caterpillar and General Motors. She has a proven track record of strategic growth, transformation and manufacturing excellence.

The new CFO's manufacturing company pedigree (Caterpillar, General Motors, Owens Corning) suggests Franklin is prioritizing operational finance expertise over purely financial engineering backgrounds—appropriate for a company whose competitive advantage depends on manufacturing excellence.

CEO Ruzynski commented: "Our resiliency is supported by the breadth of our global portfolio, which has proven to be a strategic asset as we closed out a year shaped by macroeconomic pressures. Order trends have improved, and with the support of a very healthy balance sheet, we are well-positioned to capitalize on opportunities in the year ahead. In 2025, our focus turns to driving revenue growth and margin expansion as we accelerate innovation and growth."

Business Model Deep Dive

The Three-Segment Structure

Franklin Electric operates through three distinct but complementary business segments:

Water Systems (approximately 59% of revenue): The primary driver behind last 12 months revenue was the Water Systems segment contributing a total revenue of US$1.18b (59% of total revenue). This segment designs, manufactures, and distributes water pumping systems, including submersible motors, drives, and controls for residential, agricultural, and industrial applications.

Energy Systems (formerly Fueling Systems): Provides fuel pumping, containment, and monitoring systems for retail and commercial fueling applications. The segment has evolved beyond pure petroleum to encompass broader energy infrastructure including EV charging support and critical power monitoring.

Distribution (Headwater): Distribution net sales were $157.2 million, an increase of $9.2 million or 6 percent compared to the fourth quarter 2023. Sales increases were driven by higher volumes and the incremental impact from a recent acquisition.

Manufacturing Scale and Breadth

Every day, Franklin Electric manufactures approximately 20,000 pumps, motors, drives, and controls to move the 3 trillion gallons of fresh water used worldwide and 1 billion gallons of fuel used worldwide on a daily basis. Together, we assure their reliability and availability to our millions of customers around the world.

Long recognized as the world's largest manufacturer of submersible electric motors, Franklin Electric has been able to leverage its expertise in motor applications to grow and serve several different markets. Franklin offers pumps, motors, drives, and controls for use in a wide variety of residential, commercial, agricultural, industrial, and municipal installations, for both clean and grey water applications.

Competitive Landscape

Established Global Players

Franklin Electric's top competitors include Pentair, Xylem and Grundfos. Franklin Electric's top 20 competitors are Pentair, Xylem, Grundfos, Brehnor Pumps, KSB SE Co KGaA, Sulzer, Wilo, Evoqua, Flowserve, Ebara, United Rentals, Danaher, JWCE, Gardner Denver, Pfannenberg Group Holding GmbH, SPX Technologies, Chromalox, John Crane, Urecon and Heat Trace Products.

According to Xylem's 10-K: "Our key competitors in the Applied Water segment include Franklin Electric Co., Inc, Grundfos, Pentair plc, and Wilo SE."

The competitive dynamics differ significantly by segment and geography:

Grundfos (Denmark-based, private) generates approximately $4.6 billion in revenue, making it roughly twice Franklin's size. Grundfos generates $2.6B more revenue vs. Franklin Electric.

Pentair operates in similar water technology segments and generates 199% of Franklin Electric's revenue.

Xylem is substantially larger with a broader technology portfolio spanning water infrastructure, applied water, and measurement/control solutions.

However, Franklin's competitive position in submersible motors specifically remains dominant. Long recognized as the world's largest manufacturer of submersible electric motors, Franklin Electric has been able to leverage its expertise in motor applications to grow and serve several different markets.

Strategic Analysis: Porter's Five Forces

Threat of New Entrants: LOW

The barriers to entry in submersible motor manufacturing are formidable. Franklin achieved its 10 millionth motor milestone in 1980—forty-five years of accumulated manufacturing expertise create technical barriers that capital alone cannot quickly overcome. The company's global manufacturing footprint (facilities in 11+ countries) provides supply chain advantages that regional newcomers cannot match. Regulatory certifications, particularly for drinking water applications, create additional compliance barriers. The Headwater distribution network compounds entry barriers by controlling access to the installing contractor base that specifies equipment.

Bargaining Power of Suppliers: MODERATE

Franklin Electric sources multiple input materials (steel, copper, electronic components) from diverse global suppliers. The company's manufacturing scale provides purchasing leverage, though certain specialized components may have limited supplier options. Raw material cost fluctuations—particularly copper pricing—can impact margins, as noted in management commentary about commodity pricing pressures on the Distribution segment.

Bargaining Power of Buyers: MODERATE

The customer base is highly fragmented across residential, agricultural, commercial, and industrial applications. No single customer dominates Franklin's revenue mix. The Headwater vertical integration specifically addressed buyer power by positioning Franklin "shoulder to shoulder with the key decision makers"—distributors and installing contractors. Products sold through wholesale and retail distributors, specialty distributors, and OEMs dilute individual buyer leverage. Technical specifications and contractor familiarity create meaningful switching costs.

Threat of Substitutes: LOW

Water pumping represents essential infrastructure with no viable technological substitutes—gravity-fed systems work in limited applications, and alternative pumping technologies (pneumatic, hydraulic) serve different niches rather than competing directly. Replacement of diesel water pumps with electric water pumps is further driving the expansion of the water pump market size. Use of electric pumps typically leads to lower operational costs than diesel pumps as they rely on electricity, which is often more cost-effective than diesel fuel. Electric pumps generally demand less maintenance and boast longer lifespans, thereby reducing overall maintenance and replacement expenses. The diesel-to-electric transition creates a tailwind for Franklin rather than a substitution threat.

Competitive Rivalry: MODERATE-HIGH

The water pump and motor market includes well-capitalized global players (Xylem, Grundfos, Pentair, KSB, Wilo) with significant R&D resources and geographic reach. However, The submersible pumps market share is highly fragmented, with several players including EBARA CORPORATION, Franklin Electric Co., Inc., Grundfos Pumps India Private Ltd., KIRLOSKAR BROTHERS LIMITED, KSB Limited, Pentair, Sulzer Ltd. Competition occurs primarily on quality, availability, service, and technical support rather than pure price—a dynamic that favors Franklin's brand reputation and service infrastructure.

Strategic Analysis: Hamilton's 7 Powers Framework

1. Scale Economies: STRONG

Manufacturing approximately 20,000 units daily creates significant unit cost advantages impossible for smaller competitors to match. The historical scaling from 2 million units (1972) to current production levels demonstrates decades of manufacturing learning curve benefits. Global manufacturing footprint enables regional cost optimization while maintaining quality standards.

2. Network Economies: MODERATE

Headwater is a focused groundwater distribution organization that delivers quality products and leading brands to the industry, providing contractors with the availability and service they demand to meet their application challenges. The Headwater distribution network creates value through geographic density—more locations serving more contractors increases contractor switching costs and generates market intelligence. This isn't a pure network effect (each additional contractor doesn't directly benefit other contractors), but distribution density does create local advantages.

3. Counter-Positioning: MODERATE

Franklin's vertical integration into distribution represents counter-positioning versus pure manufacturers. Traditional pump manufacturers sell through independent distributors and may be reluctant to compete directly with their own distribution customers. Franklin's approach—operating Headwater as a full-line distributor carrying multiple brands—allows it to benefit from channel control while maintaining relationships with other manufacturers whose products Headwater distributes.

4. Switching Costs: MODERATE-HIGH

Installed motor bases create replacement demand with existing brand familiarity. Contractors develop technical expertise with specific product lines and may resist switching to unfamiliar products. Training, specifications, and parts availability create practical switching costs. However, in commodity applications, price sensitivity can override brand loyalty.

5. Branding: MODERATE

Franklin Electric is a respected and trusted brand with a strong heritage and a bright future. I have admired the company's culture, values, and commitment to excellence for many years. The brand carries recognition for quality and reliability particularly among installing contractors. Franklin Electric is proud to be named in Newsweek's lists of America's Most Responsible Companies and Most Trustworthy Companies for 2024. The multiple brand portfolio (Franklin, Little Giant, Red Lion, Pioneer Pump) serves different market segments and price points.

6. Cornered Resource: MODERATE

Eighty-plus years of submersible motor expertise represents accumulated intellectual property and engineering know-how. In 1950, Franklin introduced the first electric motor that was fully submersible—this first-mover advantage in submersible technology created decades of manufacturing and application engineering insights. Specialized talent familiar with Franklin's systems represents a human capital cornered resource.

7. Process Power: STRONG

Franklin's manufacturing processes—developed over eight decades—represent institutionalized operational excellence. The company's consistent quality enables reliability-critical applications (municipal water systems, agricultural irrigation, industrial processes) where pump failure carries significant consequences. New product development capabilities (launching approximately 30 new products in 2024 alone) demonstrate sustained process innovation.

Financial Analysis and Current State

Profitability Profile

Operating income was $243.6 million with operating margin of 12.1%. Despite macroeconomic challenges affecting full-year sales, the company maintained a strong gross profit margin of 35.5% over the last twelve months.

Franklin Electric's return on equity is 14.3%, and it has net margins of 8.9%.

The gross profit margin of 35.5% reflects Franklin's positioning as a technical leader rather than a commodity manufacturer—commodity motor manufacturers would struggle to achieve such margins. The operating margin of approximately 12% leaves room for improvement through productivity initiatives and scale leverage on fixed costs.

Balance Sheet Strength

The company operates with moderate debt levels and maintains liquid assets that exceed short-term obligations, with a healthy current ratio of 2.4.

The Company ended 2024 with a cash balance of $220.5 million, an increase of $135.5 million compared to the end of 2023. Net cash flows from operating activities for 2024 were $261.4 million versus $315.7 million in the same period in 2023.

The $220.5 million cash position provides substantial dry powder for acquisitions and capital investments. Operating cash flow of $261.4 million provides the recurring capital generation that enables sustained M&A activity and shareholder returns.

2025 Guidance

Franklin Electric expects full year 2025 sales to range between $2.09 billion and $2.15 billion, with EPS between $4.05 and $4.25.

The guidance implies 3-7% revenue growth and 5-10% EPS growth, suggesting management expects margin improvement alongside modest top-line expansion. This combination of revenue growth and margin expansion is the traditional formula for industrial outperformance.

Capital Allocation

The company increased capital returned to shareholders, with $129.3 million in share repurchases and $25.3 million in dividends in the first six months of 2025, compared to $47.9 million and $24.0 million, respectively, in the same period of 2024.

This represents a $1.06 annualized dividend and a dividend yield of 1.1%. Franklin Electric's payout ratio is presently 27.39%.

The 27% payout ratio provides substantial retained earnings for reinvestment while maintaining a consistent dividend—the traditional approach for growth-oriented industrials.

Playbook: Business and Investing Lessons

Lesson 1: Master the Art of the Pivot

Franklin's transformation from military backpack generators to civilian water pumps illustrates how technical capabilities can be redirected when market conditions change. The founders didn't cling to a declining defense market; they identified adjacent civilian applications for their motor manufacturing expertise. This pattern—maintaining technical core competencies while shifting end markets—recurs throughout Franklin's history (water to fuel, motors to complete systems, manufacturing to distribution).

Lesson 2: Dominate the Boring

Submersible motors aren't glamorous. They're invisible infrastructure, literally buried underground or submerged in wells. But they're essential and technically demanding. Franklin's strategy of achieving technical leadership in unglamorous but critical applications creates sustainable competitive advantages—competitors find it difficult to generate investor excitement for "boring" industrial niches, reducing competitive intensity.

Lesson 3: Vertical Integration Done Right

The Headwater acquisition demonstrates thoughtful vertical integration. Rather than creating a captive distribution channel (which would alienate other manufacturers whose products provide inventory depth), Franklin structured Headwater as a full-line distributor while gaining preferential positioning and market intelligence. The integration captured value without destroying the distributor ecosystem that serves installing contractors.

Lesson 4: Disciplined M&A

Franklin's acquisition approach follows clear financial discipline—management has indicated that acquisitions must be accretive within two years and achieve target ROIC within three years. This contrasts with "growth at any price" acquisition strategies that often destroy shareholder value. The relatively small deal sizes (the Barnes de Colombia and PumpEng acquisitions didn't even warrant disclosed transaction values) suggest preference for tuck-in acquisitions over transformational mega-deals.

Lesson 5: The Global-Local Balance

Manufacturing presence in 11+ countries enables Franklin to serve regional markets with locally manufactured products while maintaining global scale advantages in engineering, purchasing, and brand development. This isn't purely a cost optimization play—local manufacturing provides supply chain resilience, tariff flexibility, and customer proximity for service and support.

Lesson 6: Long-Term Institutional Thinking

The trajectory from $20,000 startup to $4+ billion market cap required 81 years of compounding. The leadership continuity (Sengstack spent 35 years at Franklin before becoming CEO) suggests genuine institutional memory and long-term thinking. This contrasts with companies where short CEO tenures produce strategic discontinuity and value destruction.

Bull vs. Bear Case

The Bull Case

1. Essential Infrastructure with Secular Tailwinds

Global water scarcity is intensifying. Water scarcity is a major issue plaguing various regions across the globe. Governments of various countries are implementing regulations mandating water recycling and reuse, especially in industries. Thus, these factors are expected to drive the growth of the submersible pumps market during the forecast period.

The global water and wastewater pumps market size is projected to grow from $18.81 billion in 2025 and is expected to reach $30.61 billion by 2032. This represents a 63% market expansion over seven years—a substantial tailwind for well-positioned participants.

2. Electric Pump Transition Creating Market Expansion

Replacement of diesel water pumps with electric water pumps is further driving the expansion of the water pump market size. Use of electric pumps typically leads to lower operational costs than diesel pumps as they rely on electricity, which is often more cost-effective than diesel fuel.

Electric drives hold a 78.31% share because grid reliability, renewable power integration and variable-speed electronics lower operating costs relative to hydraulic or diesel alternatives.

This diesel-to-electric transition plays directly to Franklin's strengths as the world's largest submersible electric motor manufacturer.

3. Strong Balance Sheet for Opportunistic M&A

With $220 million in cash and strong operating cash generation, Franklin can pursue accretive acquisitions without overleveraging. The Barnes de Colombia and PumpEng deals demonstrate continued deal activity even in a challenging macro environment.

4. Vertical Integration Benefits

The Headwater distribution network provides customer intelligence, channel control, and recurring revenue that pure manufacturers lack. As Headwater continues geographic expansion, these advantages compound.

5. Valuation Relative to Peers

Franklin's smaller market capitalization relative to Xylem, Grundfos, and Pentair may attract M&A interest from larger players seeking to consolidate the submersible motor segment.

The Bear Case

1. Macroeconomic Sensitivity

Macro trends such as low housing starts and existing home sales as well as unfavorable weather patterns, particularly in the US and movements in commodities have pressured our sales.

Residential water systems demand correlates with housing activity. A prolonged housing downturn would pressure the Water Systems segment's largest market.

2. Competitive Intensity

Larger competitors (Xylem, Grundfos) have greater R&D resources and could potentially close technology gaps. Chinese manufacturers offer lower-cost alternatives in less demanding applications.

3. Margin Pressure in Distribution

The Distribution segment operates at lower margins (4-6% operating income) than manufacturing. If Distribution grows faster than manufacturing, blended company margins could compress. Additionally, the trend in price decline lasted longer than the historical norm and we expect to see stabilization in the coming year. While we have little control over commodity pricing environment, we will focus on streamlining our operations.

4. Integration and Execution Risk

The leadership transition (new CEO, new CFO, new CHRO all within 12-18 months) creates integration risk. Multiple acquisitions require successful integration to achieve projected synergies.

5. Currency and Geopolitical Exposure

Global manufacturing footprint creates currency translation effects. Operations in emerging markets (Latin America, Turkey, South Africa) expose the company to geopolitical and currency devaluation risks.

Key Performance Indicators to Monitor

For long-term investors tracking Franklin Electric's ongoing performance, three metrics deserve particular attention:

1. Water Systems Operating Margin

The Water Systems segment represents the company's manufacturing core and generates the highest margins. Current segment operating margin trends indicate manufacturing efficiency and pricing power. Management expects productivity initiatives to drive 40-50 basis points of margin improvement—investors should verify this shows up in reported results.

2. Organic Revenue Growth by Segment

Distinguishing organic growth from acquisition-driven growth reveals the underlying business momentum. Management guidance of 1-4% organic growth in 2025 provides a benchmark. Sustainable organic growth indicates market share gains and product innovation traction.

3. Operating Cash Flow Conversion

Operating cash flow relative to net income demonstrates earnings quality and working capital management. The company's strong cash generation ($261 million in 2024) supports M&A, dividends, and buybacks. Deterioration in cash conversion would warrant investigation into inventory, receivables, or accounting quality.

Conclusion

Franklin Electric represents a distinctive investment proposition: a company that has achieved category dominance (world's largest submersible motor manufacturer) in essential infrastructure (water and energy systems) with demonstrated strategic evolution (manufacturing to systems to distribution) and disciplined capital allocation (consistent M&A, returning capital to shareholders).

The risks are real—macroeconomic sensitivity, competitive intensity, execution challenges. But the company's 81-year track record, global manufacturing footprint, vertical distribution integration, and positioning for water scarcity tailwinds create a foundation for continued value creation.

For investors seeking exposure to essential infrastructure with less volatility than pure-play technology and more growth potential than traditional utilities, Franklin Electric merits serious consideration. The stock won't double next quarter on a meme-driven frenzy. But Ed Schaefer and Wayne Kehoe's $20,000 bet in 1944 has compounded into a $4+ billion enterprise—and the fundamental drivers of that compounding remain intact.

As one analyst framed it: to be a Franklin Electric shareholder is to believe in the continued global need for water systems and infrastructure solutions, supported by resilient demand and technological innovation. In a world where water scarcity is intensifying, that seems like a reasonable bet.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube