TechnipFMC: The Story of the Subsea Architects

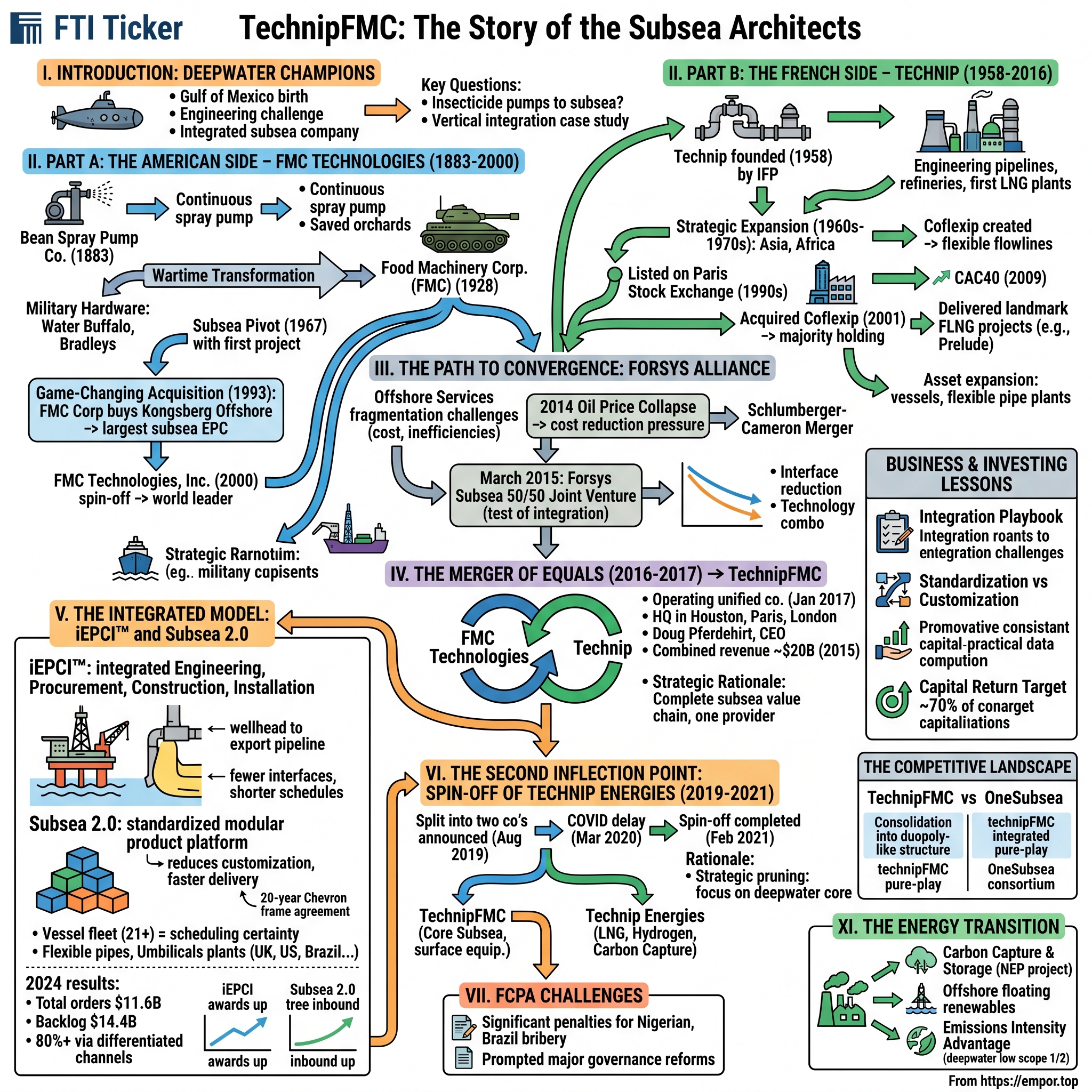

I. Introduction: The Unlikely Deepwater Champions

Two thousand feet beneath the churning waters of the Gulf of Mexico, where sunlight cannot penetrate and pressures crush most materials, a different kind of oil industry was being born. The equipment that makes deepwater oil extraction possible—the Christmas trees, manifolds, umbilicals, and flowlines that form the central nervous system of modern offshore production—represents one of the most demanding engineering challenges humans have ever undertaken. And at the center of this specialized universe sits a company whose origin story stretches back not to oil fields, but to California orchards.

TechnipFMC plc is a French-American, UK-domiciled global oil and gas company that provides services for the energy industry. The company was formed by the merger of FMC Technologies of the United States and Technip of France that was announced in 2016 and completed in 2017.

TechnipFMC annual revenue for 2024 was $9.083B, a 16.09% increase from 2023. At year-end 2024, the company achieved total inbound orders of $11.6 billion, driving year-over-year growth in backlog to $14.4 billion. The company has about 23,000 employees from 126 nationalities and operates in 48 countries.

The central question that animates this story is deceptively simple: How did a California insecticide pump company and a French post-war engineering firm become the most integrated deepwater subsea company in the world? The answer involves world wars, oil shocks, bribery scandals, a merger of equals, a subsequent spin-off, and the relentless march of engineering innovation into ever-deeper waters.

For investors, TechnipFMC represents a fascinating case study in vertical integration, cyclical industry management, and the strategic use of M&A. The company occupies an unusual position in the oilfield services landscape: it designs, manufactures, and installs the complete subsea production system. In an industry where specialization is the norm, TechnipFMC chose integration. Understanding why—and whether that strategy will continue to pay off—requires diving deep into the company's unusual dual heritage.

II. The Origin Stories: Two Companies, Two Continents

Part A: The American Side – From Orchards to Oceans (1883-2000)

The story begins not in Houston's energy corridor, but in the Santa Clara Valley of California in 1883. Founded in 1883 as the Bean Spray Pump Company in Los Gatos, California, by chemist John Bean. The company's first product was a piston pump. Bean invented the pump to spray insecticide on the many fruit orchards in the area.

The problem Bean was trying to solve was a tree disease known locally as "San Jose Scale" that threatened thousands of acres of orchards. His solution—a continuous spray pump—would set the company on a trajectory no one could have predicted. Bean Avenue in downtown Los Gatos still honors the inventor whose pumps saved the valley's fruit industry.

In 1928, Bean Spray Pump purchased two companies: the Anderson-Barngrover Co. and Sprague-Sells Co. The Anderson-Barngrover Co. manufactured a sealed can rotary pressure sterilizer and the Sprague-Sells Co. manufactured canning machinery. At this time the company changed its name to Food Machinery Corporation, and began using the initials FMC.

The transformation from orchard equipment to military hardware came with World War II. Food Machinery's equipment division prospered in the 1940s due to the Second World War. Some months before the United States entered the war, Food Machinery began producing the "Water Buffalo," an amphibious tank which provided important troop mobility over the next crucial years. Other products were adapted for wartime uses as well, such as the orchard sprayer, which was to be used for decontamination purposes if necessary, and nailing machines which produced ammunition boxes at an exceedingly high rate.

During World War II, FMC produced more than 10,000 armored vehicles. The company's transformation from food machinery to military contractor was complete, and defense would remain a significant business line for decades. FMC later built the M113 Armored Personnel Carrier (APC), the Bradley Fighting Vehicle, and the XR311 at its former facility in Santa Clara, California. FMC also became the primary contractor for an advanced armed personnel carrier called the Bradley Fighting Vehicle, developed during the 1970s to counter the introduction of a similar but less sophisticated Soviet model called the BMP. In the early 1980s, the Bradley was criticized for a lack of battlefield survivability. FMC and Pentagon officials responded that even the most heavily armored tanks were not impervious to attack, but nonetheless began to investigate ways to improve the Bradley. About 3,000 Bradleys were delivered, each capable of defeating enemy tanks and other fighting vehicles while moving at high speeds in any kind of weather.

The subsea pivot came in 1967, when FMC's Oil Center Tool subsidiary received its first subsea project. In 1967, Placid awarded OCT its first subsea project at Ship Shoal Block 204 in the Gulf of Mexico. This modest beginning would eventually eclipse both the food machinery and defense businesses.

The game-changing acquisition occurred in 1993. FMC Corp purchased Kongsberg Offshore from Siemens, making FMC the world's largest subsea engineering, procurement, and construction company. In 1986 Kongsberg Oil was renamed Kongsberg Offshore. In 1987, the Norwegian state divested itself of all Kongsberg industries not related to weapons manufacture, selling Kongsberg Offshore to Siemens A.S. In 1993, FMC Corp purchased Kongsberg Offshore from Siemens.

The Norwegian acquisition brought critical subsea controls expertise that would prove invaluable in the deep waters where FMC was heading. Norway's North Sea expertise—developed in the harsh conditions of the North Atlantic—gave FMC a technology base that competitors couldn't easily replicate.

FMC Technologies, Inc. was a North American company that produced equipment for the exploration and production of hydrocarbons. FMC Technologies was incorporated in 2000 when FMC Corporation divested its machinery businesses. It exists today as a part of TechnipFMC, after a merge with Technip in 2017.

By the time of its spin-off from FMC Corporation, FMC Technologies had evolved from pumps to defense to subsea—each transition driven by opportunistic responses to changing market conditions. The company entered the 2000s as the world leader in subsea systems, a position it would hold for the next two decades.

Part B: The French Side – Technip (1958-2016)

Across the Atlantic, Technip's story begins in post-war France, where the government was determined to build an independent energy industry. Technip was founded on April 21, 1958, in Paris by the Institut Français du Pétrole (IFP) as Compagnie Française d'Etudes et de Construction Technip, starting with 100 employees to address engineering shortages in pipeline construction and refining amid France's post-war oil sector development.

The IFP, France's national petroleum research institute, created Technip to translate its laboratory innovations into commercial reality. Technip was established in 1958 by IFP, Institut Français du Pétrole, as Compagnie Française d'Etudes et de Construction Technip. Tasked with engineering refineries and petrochemical plants in France and its territories, Technip was building a liquefied natural gas (LNG) facility in Algeria in 1962. A second such plant followed ten years later.

The company grew through strategic geographic expansion. In the 1960s, the company completed its first international projects in Africa and Asia. In the 1970s Technip became an international group with the acquisition of an office in Rome and the creation of Technip Geoproduction, a subsidiary specialized in hydrocarbon field equipment.

During this period, Coflexip – a firm specialized in the design, manufacture, and supply of flexible subsea flowlines – was created by the IFP (French Petroleum Institute) and opened a flexible flowline manufacturing plant in Le Trait, France, as well as offices in Houston, Aberdeen and Rio de Janeiro. In the 1980s Technip opened operating centers in Kuala Lumpur and Abu Dhabi. Coflexip opened a second flowline manufacturing plant in Brazil and branched out into the manufacture of umbilicals with the establishment of the Duco plant in Newcastle, UK.

The 1990s brought public markets. In the 1990s Technip was listed on the Paris Stock Exchange and Coflexip on the New York Stock Exchange. Technip was included in the CAC40 French benchmark index in September 2009.

In April, Technip acquired an initial 29.7 percent investment in Coflexip, an offshore construction specialist. In October 2001, Technip acquired a majority (98.36 percent) holding in Coflexip as well as a controlling interest in ISIS, a holding company that formerly had been owned by the national oil institute IFP.

Technip achieved prominence as a world leader in floating liquefied natural gas (FLNG) facilities, delivering landmark projects such as Shell's Prelude FLNG and Petronas' PFLNG Satu. The Prelude FLNG facility, moored off Australia's northwest coast, became the largest floating structure ever built—a 488-meter vessel designed to liquefy natural gas at sea. Technip's ability to execute such mega-projects established its reputation as an engineering powerhouse.

In 2010 three major assets came into operation: the Technip fleet expanded to 17 vessels with the addition of the Apache II, one of the most advanced pipelay vessels in the industry, and the Skandi Vitoria, a Brazilian-flagged vessel dedicated to the pre-salt market. Asiaflex Products, the Group's third flexible pipe production plant, located in Tanjung Langsat, Malaysia was inaugurated.

By the mid-2010s, Technip and FMC Technologies were the two dominant players in the subsea space—but with different specializations. FMC excelled at manufacturing the subsea production systems (SPS)—the trees, manifolds, and controls that sit on the seabed. Technip's strength lay in SURF (subsea umbilicals, risers, and flowlines) and installation—connecting everything and putting it in place. Together, they represented the complete subsea value chain. Separately, they were increasingly competing for the same customers' attention.

III. The Path to Convergence: Industry Consolidation & The Forsys Alliance

The offshore services industry had long maintained a structural separation between equipment makers and installers. Oil companies would hire one contractor to manufacture the subsea production equipment and another to lay the pipelines and install the system. This fragmentation created inefficiencies: interfaces between systems, coordination challenges, and finger-pointing when problems arose.

The 2014 oil price collapse changed the calculus. As crude fell from over $100 to below $30 per barrel, offshore projects—with their long lead times and high capital requirements—became increasingly difficult to sanction. Oil companies demanded cost reductions of 30-40% just to keep projects viable.

In this environment, FMC Technologies and Technip saw an opportunity. On March 22, 2015, FMC Technologies, Inc. and Technip signed an agreement to form an exclusive alliance and to launch Forsys Subsea, a 50/50 joint venture that will unite the skills and capabilities of two subsea industry leaders. This alliance will redefine the way subsea fields are designed, delivered and maintained.

In June 2015, Forsys Subsea, a 50/50 joint venture, received all regulatory approvals. The parties closed the transaction making Forsys Subsea operational on June 1, 2015.

Bringing the industry's most talented subsea professionals together early in the project concept phase, Forsys Subsea will have the technical capabilities, products and systems to significantly reduce the cost of subsea field development and provide the technology to maximize well performance over the life of the field. By combining the industry-leading technologies of the parent companies, Forsys Subsea will reduce the interfaces of the subsea umbilical, riser and flowline systems (SURF) and subsea production and processing systems (SPS).

The Forsys alliance was a laboratory experiment—a way for the two companies to test whether integration could actually deliver on its promise. The results were encouraging enough to prompt a more radical step.

Meanwhile, the competitive landscape was shifting. In 2015, Schlumberger announced its acquisition of Cameron International, a leading subsea equipment manufacturer, for $12.7 billion. The deal created a formidable competitor with combined capabilities in drilling, production, and subsea systems. The message was clear: scale and integration were the future of offshore services.

For FMC Technologies and Technip, the Schlumberger-Cameron combination forced a strategic response. They could continue as independent companies, facing an increasingly powerful competitor, or they could combine their complementary strengths to create something new. They chose the latter.

IV. The Merger of Equals (2016-2017): Creating TechnipFMC

On May 19, 2016, it was announced that FMC Technologies would team up with French Technip to create a new company called TechnipFMC.

On January 17, 2017, TechnipFMC announced that it is operating as a unified company after completion of the merger, which created a significant new player in an energy industry wracked by a nearly two-year slump in crude prices.

The deal structure reflected the "merger of equals" framing. Under the terms of the merger, Technip shareholders received 2.0 shares of the combined company for each share of Technip; FMC Technologies shareholders received 1.0 share of the combined company for each share of FMC Technologies. The resulting company was listed on both the New York Stock Exchange and Euronext Paris.

In 2017, FMC Technologies Inc. and Technip agreed to merge, forming a significant new player in an energy industry racked by a nearly two-year slump in crude prices. The all-share deal would result in a new company named TechnipFMC with a market value of about $13 billion.

TechnipFMC has three headquarters in Houston, Paris, and London under new Houston-based CEO Doug Pferdehirt, who worked as FMC's chief operating officer. Former Technip chairman and CEO Thierry Pilenko is the new executive chairman.

Doug Pferdehirt, the man chosen to lead the combined entity, brought a distinctive background to the role. After a successful 26-year career with Schlumberger Limited, Pferdehirt joined FMC Technologies. In the almost four years he had been with the company, he had helped lead and execute many strategic shifts, including industry-changing alliances with leading service providers, such as Technip. His Schlumberger experience gave him deep knowledge of the competitive dynamics in oilfield services, while his time at FMC had familiarized him with the unique challenges of subsea systems.

Thierry Pilenko led Technip as Chairman and CEO from 2007, and over the next 10 years grew Technip into an industry leader with exemplary project execution. In January 2017, he assumed the role of Executive Chairman of TechnipFMC providing continuity and leadership during the integration period.

The strategic rationale centered on the integration thesis. The transaction brings together two market leaders and their talented employees, building on the proven success of their existing alliance and joint venture, Forsys Subsea, uniting innovative technologies, common cultures and values, enabling rapid integration. The combined company will offer a new generation of comprehensive solutions in Subsea, Surface and Onshore/Offshore to reduce the cost of producing and transforming hydrocarbons.

With more than 49,000 employees operating in over 45 countries, TechnipFMC generated 2015 combined revenue of approximately $20 billion and combined 2015 EBITDA of approximately $2.4 billion.

The value proposition to customers was straightforward: hire TechnipFMC at the beginning of a project, and the company could deliver the complete subsea development—from wellhead to export pipeline—with fewer interfaces, shorter schedules, and lower costs than the traditional fragmented approach.

V. The Integrated Model: iEPCI™ and Subsea 2.0

The centerpiece of TechnipFMC's strategy is its iEPCI™ model—integrated Engineering, Procurement, Construction, and Installation. On January 17, 2017, FMC Technologies, Inc. and Technip S.A. combined through a merger of equals to create a global subsea leader, TechnipFMC, that would drive change by redefining the development of the subsea infrastructure used in the production of oil and natural gas through a new integrated commercial model. By integrating the complementary work scopes of the subsea production system ("SPS") with the subsea umbilicals, risers, and flowlines ("SURF") and installation vessels, we can more efficiently deliver an entire subsea development utilizing iEPCI™. As the only subsea provider to integrate these work scopes, we successfully created a new market and helped expand the deepwater opportunity set for our clients during a challenging market environment.

The industry's first fully integrated EPCI subsea project, Equinor's Trestakk field offshore Norway, enters production, underscoring the importance of early engagement and collaboration as part of our iEPCI™ offering.

The second pillar of TechnipFMC's technology strategy is Subsea 2.0, a standardized, modular product platform designed to reduce customization and accelerate delivery. Traditional subsea production systems were engineered to order—each project required unique designs, lengthy engineering cycles, and custom manufacturing. Subsea 2.0 flipped this model by creating configurable products that could be assembled from standard modules.

Jonathan Landes, President, Subsea at TechnipFMC, commented: "Subsea 2.0™ is field-proven technology, which reduces engineering complexity and shortens lead times. We are delighted to have the opportunity to support Chevron's gas production needs under this long-term agreement."

The vessel fleet represents another critical competitive advantage. TechnipFMC owns and operates 21 vessels and 4 are under construction. These large vessels are used for installation of subsea oil extraction systems on the seabed. In an industry where vessel availability can determine project timelines, owning a fleet provides scheduling certainty that vessel charters cannot match.

TechnipFMC designs and manufactures Umbilical cable and flexible pipes. It has flexible pipe manufacturing plants in France, Brazil and Malaysia. It operates umbilical production facilities in UK, United States, Angola, Singapore, Brazil and Malaysia.

The 2024 results demonstrated the power of the integrated model. Our unique combination of direct awards, iEPCI™, and Subsea Services continues to represent an even greater share of our business—growing to more than 80% of total Subsea inbound in 2024 and underpinning the quality of our expanding backlog. Both iEPCI™ and Subsea 2.0® orders reached new records in 2024. The value of iEPCI™ awards grew nearly 25%, with Subsea 2.0® tree inbound increasing more than 50% versus the prior year.

iEPCI™ has since grown to represent nearly one-third of the addressable subsea market, validating the benefits of our unique business model aimed at improving project economics by accelerating the delivery schedule of hydrocarbon production.

TechnipFMC has signed a 20-year framework agreement with Chevron Australia Pty Ltd, under which TechnipFMC may provide Subsea 2.0™ configure-to-order subsea production systems for gas field developments off Australia's northwest coast. The agreement covers the supply of wellheads, tree systems, manifolds, controls, flexible jumpers, and flying leads.

A twenty-year frame agreement represents extraordinary customer commitment in an industry where contract horizons typically measured in months or single-digit years. Such agreements provide visibility into future revenue while validating the technology platform's value proposition.

VI. The Second Inflection Point: The Spin-off of Technip Energies (2019-2021)

Just two years after completing the merger, TechnipFMC announced another dramatic transformation. In August 2019, Doug Pferdehirt announces that TechnipFMC will be split into two independent engineering companies. The separation is expected to be completed by the end of the first semester of 2020.

The separation would enhance TechnipFMC's and Technip Energies' focus on their respective strategies and provide both improved flexibility and growth opportunities, with each company uniquely positioned to capitalize on the energy transition. Post spin-off the two companies would have: Distinct and expanding market opportunities and specific customer bases; Enhanced focus of management, resources and capital.

The COVID-19 pandemic disrupted the timeline. On March 15, 2020, the group announced the suspension of the spin-off due to market conditions in the context of the COVID-19 pandemic. In February 2021, the spin-off was completed.

The Spin-off is the method by which Technip Energies will separate from TechnipFMC and become a separate publicly traded company on February 16, 2021. In the Spin-off, TechnipFMC will distribute to holders of TechnipFMC shares at 17:00 New York time, on February 17, 2021 (the "Record Date"), approximately 50.1% of the Technip Energies shares. TechnipFMC retains a 49.9% ownership interest in Technip Energies, but intends to significantly reduce its shareholding in Technip Energies over the 18 months following the Spin-off.

On February 16, 2021, TechnipFMC will distribute to each TechnipFMC shareholder one Technip Energies share for every five TechnipFMC shares held on the Record Date.

The spin-off created two focused companies: TechnipFMC concentrated on subsea systems, surface equipment, and integrated solutions for upstream energy projects. Technip Energies became an independent publicly traded company focused on process technologies for liquefied natural gas (LNG), hydrogen, and carbon capture initiatives.

Doug Pferdehirt, chairman and CEO of TechnipFMC, said: "As the market leader and industry's only fully integrated pure-play, we are uniquely positioned to transform our clients' project economics, helping them to unlock traditional and new energy resources while reducing carbon intensity and supporting their energy transition ambitions."

The merger-then-split strategy might seem contradictory, but the logic was coherent. The 2017 merger brought together subsea capabilities and achieved the integration benefits that remained with TechnipFMC. The 2021 spin-off separated the onshore/offshore engineering business (Technip Energies) that served different customers, operated under different competitive dynamics, and faced different energy transition opportunities. The post-spin TechnipFMC emerged as a more focused, higher-margin business concentrated on deepwater subsea—arguably the most defensible part of the original Technip franchise.

VII. Controversies: The FCPA Challenges

No examination of TechnipFMC's history would be complete without addressing the serious compliance failures that preceded the merger. Both legacy companies faced significant Foreign Corrupt Practices Act (FCPA) investigations.

Technip S.A., a global engineering, construction and services company based in Paris, has agreed to pay a $240 million criminal penalty to resolve charges related to the Foreign Corrupt Practices Act (FCPA) for its participation in a decade-long scheme to bribe Nigerian government officials to obtain engineering, procurement and construction (EPC) contracts. The EPC contracts to build liquefied natural gas (LNG) facilities on Bonny Island, Nigeria, were valued at more than $6 billion. The department filed a deferred prosecution agreement and a criminal information against Technip in the U.S. District Court for the Southern District of Texas.

Technip also reached a settlement of a related civil complaint filed by the Securities and Exchange Commission (SEC) charging Technip with violating the FCPA's anti-bribery, books and records, and internal controls provisions. As part of that settlement, Technip agreed to pay $98 million in disgorgement of profits relating to those violations. Including today's resolutions, a total of $917 million in criminal and civil penalties have been obtained to date as a result of the ongoing Department of Justice and SEC investigations of the scheme to bribe Nigerian government officials in order to win the Bonny Island EPC contracts.

TSKJ was comprised of Technip S.A., Snamprogetti Netherlands B.V., Kellogg Brown & Root Inc. (KBR) and JGC Corporation. Between 1995 and 2004, TSKJ was awarded four EPC contracts, valued at more than $6 billion, by Nigeria LNG Ltd.

The Bonny Island case became one of the largest FCPA enforcement actions in history, with the joint venture participants collectively paying over $1.7 billion in penalties. Technip's $338 million share reflected both the severity of the violations and the company's cooperation with investigators.

Post-merger, additional issues emerged. In June 2019, TechnipFMC agreed to pay around US$300 million to resolve allegations it bribed government officials in Iraq (FMC) and Brazil, including at the country's state-controlled oil-and-gas company Petróleo Brasileiro S.A., also known as Petrobras.

London-based TechnipFMC plc said in an SEC filing Wednesday that it has set aside $280 million for a settlement of bribery-related offenses with authorities in the United States, Brazil, and France. The company said the investigation relates to "potential violations of anticorruption laws relating to historical projects in Brazil, Equatorial Guinea, and Ghana, and Unaoil contracts."

These enforcement actions, while costly and reputationally damaging, prompted significant governance reforms. The company implemented enhanced compliance programs, retained independent monitors, and restructured its approach to third-party agents and consultants. For investors, the FCPA history represents both a legacy risk and a demonstration that the company has paid the price for past transgressions and implemented reforms to prevent recurrence.

VIII. Today's TechnipFMC & The Competitive Landscape

TechnipFMC revenue for the twelve months ending September 30, 2025 was $9.783B, a 11.25% increase year-over-year.

Doug Pferdehirt, Chair and CEO of TechnipFMC, stated, "This was another year of tremendous success for the TechnipFMC team, and I am proud to report our strong quarterly and full-year results. We achieved total Company inbound of $11.6 billion for the full year—driving year-over-year growth in backlog to $14.4 billion. Subsea inbound orders increased to $10.4 billion, representing our fourth consecutive year with a book-to-bill greater than one. This inbound was characterized by growth in iEPCI™, Subsea 2.0®, and Subsea Services, and benefited from a significant level of direct awards."

Total Company revenue for the year grew 16% to $9.1 billion. Adjusted EBITDA improved to $1.4 billion, an increase of 47% when compared to the prior year, excluding the impact of foreign exchange. Cash flow from operations for the full year increased 39% to $961 million, driving growth in free cash flow of 45% to $679 million.

Recent contract wins demonstrate the technology platform's market acceptance. TechnipFMC has been awarded a major integrated Engineering, Procurement, Construction, and Installation (iEPCI™) contract by TotalEnergies for its GranMorgu project on Block 58, the first oil and gas development offshore Suriname. This iEPCI™ award supports the development of an emerging frontier and is enabled by the Company's vessel ecosystem. The project will combine TechnipFMC's leading subsea architecture with Saipem's EPCI solutions and best-in-class pipelay capabilities. TechnipFMC's contracted scope for the project includes Subsea 2.0® tree systems, manifolds, connectors, and topside control equipment.

For TechnipFMC, a "major" contract is more than $1 billion, and this represents the value of the contracted scope awarded to the Company.

TechnipFMC has been awarded a significant integrated Engineering, Procurement, Construction and Installation (iEPCI) contract by Eni SpA for the deepwater Maha project offshore Indonesia. The project represents Eni's first deployment of TechnipFMC's Subsea 2.0® configure-to-order (CTO) technology in the country. The award builds on TechnipFMC's prior experience with Eni in the region, including the Jangkrik and Merakes projects, and will tie back to the existing Jangkrik Floating Production Unit.

The Competitive Landscape

The subsea market has undergone significant consolidation. SLB, Aker Solutions and Subsea7 announced today the final closing of their previously announced joint venture. The new business, which will adopt the OneSubsea name, will drive innovation and efficiency in subsea production by helping customers unlock reserves and reduce cycle time. OneSubsea now comprises SLB's and Aker Solutions' subsea businesses, which include an extensive complementary subsea production and processing technology portfolio, world-class manufacturing scale and capacity, access to industry-leading reservoir and digital domain expertise, unique pore-to-process integration capabilities and strengthened R&D capabilities.

Aker Solutions is a 20 percent owner in the joint venture, with SLB holding 70 percent and Subsea7 holding 10 percent. OneSubsea will be headquartered in Oslo, Norway, and Houston, Texas, with 11,000 people working in all key operating regions around the world.

SLB, Aker Solutions, and Subsea7 have come together to create the world's leading subsea technology and solutions provider. We are focused on accelerating innovation to create a step change in subsea production economics and reduce emissions in subsea operations. The joint venture brings together deep reservoir domain expertise, broad front-end and system design knowledge. We provide an extensive field-proven subsea production and processing technology portfolio, world-class manufacturing scale and capacity, and unique pore-to-process integration capabilities.

Further consolidation may be coming. ExxonMobil, Petrobras raise Saipem/Subsea7 merger red flags, citing deepwater competition risks. This potential combination between two major players (with Subsea7 being a minority owner in OneSubsea) has drawn regulatory scrutiny, suggesting that competition authorities are closely watching industry concentration.

The market structure has effectively consolidated into two major camps: TechnipFMC as the vertically integrated pure-play, and OneSubsea as the SLB-backed consortium approach. Baker Hughes maintains a presence in subsea production systems but lacks the same integration as the two leaders. This duopoly-like structure could provide pricing power and stable market shares, but also attracts regulatory attention.

IX. Playbook: Business & Investing Lessons

The Integration Playbook: TechnipFMC's strategy demonstrates that vertical integration can create value even in cyclical industries—but only when executed with specific conditions. The combination of equipment manufacturing (SPS) and installation services (SURF) eliminated the interface that had long created cost overruns and delays. The key insight: integration works when it reduces transaction costs, eliminates adversarial relationships, and creates new solutions impossible under fragmented structures. TechnipFMC didn't just bolt two companies together; they created iEPCI™, a new service category that neither predecessor could offer alone.

Cyclical Industry Management: The offshore services industry is notoriously volatile, driven by oil prices, exploration budgets, and project sanctioning cycles. TechnipFMC's approach centers on technology differentiation—Subsea 2.0's standardization reduces costs enough to make projects viable even at lower oil prices. The backlog business model also provides visibility; at $14.4 billion of backlog against $9 billion in revenue, the company has roughly 18 months of visibility, cushioning against cyclical downturns.

The Merger-Then-Split Strategy: The 2017 merger followed by the 2021 spin-off may appear contradictory but reflects evolving strategic understanding. The merger achieved the subsea integration benefits, while the spin-off recognized that the onshore/offshore engineering business (Technip Energies) had different customers, competitive dynamics, and energy transition exposures. This willingness to revisit major strategic decisions—even recent ones—demonstrates intellectual honesty about what combinations actually create value.

Standardization vs. Customization: Subsea 2.0 represents a fundamental shift from engineer-to-order to configure-to-order. In industries where customization is the default, standardization can seem like retreat. But when standardization delivers faster delivery, lower costs, and proven reliability, customers reward it with long-term frame agreements like Chevron's 20-year deal. The lesson: standardization succeeds when it solves real customer problems, not when it merely reduces supplier costs.

Fleet Ownership: TechnipFMC's ownership of 21 installation vessels provides scheduling certainty and quality control that vessel charters cannot match. In a tight vessel market, fleet ownership becomes increasingly valuable. The capital intensity is significant, but the strategic benefit—being able to promise customers a complete integrated solution with controlled delivery—justifies the investment for a company pursuing the iEPCI™ model.

Capital Discipline: The company has increased shareholder distributions significantly, targeting 70% of free cash flow for 2025. "We are committed to sharing the benefits of our improving financial results and growing cash flow through shareholder distributions—with our 2025 target now being increased to at least 70% of free cash flow—driving year-over-year growth in distributions of at least 30%." This capital return discipline, combined with share repurchase authorizations, signals confidence in the business while returning excess cash rather than empire-building.

X. Strategic Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Porter's Five Forces Analysis

| Force | Assessment | Analysis |

|---|---|---|

| Threat of New Entrants | LOW | Extremely high barriers: specialized vessels costing hundreds of millions, decades of deepwater engineering expertise, FCPA compliance track records, long-standing customer relationships, and track records on complex projects. The subsea market requires certifications and proven reliability that take decades to establish. |

| Bargaining Power of Suppliers | MODERATE | Specialized steel, components, and materials can be sourced from multiple vendors, but some critical technologies (sensors, control systems) have limited suppliers. Vertical integration into flexible pipe manufacturing reduces supplier power. |

| Bargaining Power of Buyers | MODERATE-HIGH | Major IOCs (ExxonMobil, Shell, Chevron, Petrobras) and NOCs have significant negotiating power, especially during industry downturns. However, switching costs are high once a project begins, and multi-decade frame agreements demonstrate customer lock-in. |

| Threat of Substitutes | MODERATE | Onshore shale production competes for E&P capital. Offshore deepwater and tight oil projects remain the most economical new supply sources, with oil sands still the most expensive. Energy transition could reduce long-term oil demand, though deepwater's low emissions intensity may prove advantageous. |

| Competitive Rivalry | HIGH | The market has consolidated to two dominant integrated players (TechnipFMC and OneSubsea), creating intense competition for major projects. The project-based business creates bidding wars, though differentiation through iEPCI™ enables direct awards that bypass competitive tenders. |

Hamilton's 7 Powers Analysis

| Power | Present? | Analysis |

|---|---|---|

| Scale Economies | ✓ Strong | Fleet amortization across projects, manufacturing plants for flexible pipes and umbilicals spread costs globally. The 21-vessel fleet creates per-project cost advantages unavailable to smaller competitors. |

| Network Effects | ✗ Weak | Limited network effects; this is a B2B business without demand-side economies of scale. Each customer's decision is independent of others' adoption. |

| Counter-Positioning | ✓ Strong | The iEPCI™ integrated model represents counter-positioning vs. traditional fragmented delivery. Competitors cannot easily replicate without cannibalizing existing business models—OneSubsea's three-company consortium structure inherently has more interfaces than TechnipFMC's integrated approach. |

| Switching Costs | ✓ Moderate | Multi-year frame agreements create stickiness. Project-specific knowledge and relationships create retention. TechnipFMC has signed a 20-year framework agreement with Chevron Australia Pty Ltd, under which we may provide Subsea 2.0™ configure-to-order subsea production systems. |

| Branding | ✓ Moderate | Strong reputation in deepwater; historical track record on complex projects. The "first integrated EPCI" positioning creates brand differentiation. |

| Cornered Resource | ✓ Moderate | The 1993 Kongsberg Offshore acquisition brought subsea controls expertise. The 126-nationality workforce represents specialized human capital that cannot be quickly replicated. The flexible pipe manufacturing plants and vessel fleet represent physical cornered resources. |

| Process Power | ✓ Strong | The Subsea 2.0 configure-to-order platform, combined with iEPCI™ methodology, represents process power. Subsea inbound orders were $10.4 billion, and included a record level of both integrated Engineering, Procurement, Construction, and Installation ("iEPCI™") projects and Subsea 2.0® configure-to-order ("CTO") subsea production equipment. In fact, Subsea 2.0® tree orders in 2024 significantly outpaced the growth of our total subsea tree awards, while iEPCI™ inbound grew nearly 25 percent as compared to the prior year. |

Deepwater Economics: The Structural Tailwind

The investment thesis for TechnipFMC is inseparable from the economics of deepwater production. Wells in the most prolific deepwater basins typically recover huge volumes of oil and gas from each well, with strong economic returns and low Scope 1 and 2 emissions intensities relative to most other oil and gas resource theaters. As for the pre-FID project pipeline, there are widespread opportunities, with average investment returns in Wood Mackenzie's global database of deepwater development projects of 24%, at $60/bbl Brent. Best returns are associated with smaller oil fields that can be tied back to nearby infrastructure, with the lowest from gas supply projects with long lead times.

Offshore shelf is the next cheapest ($37 per barrel), followed by offshore deepwater ($43) and North American shale ($45).

Deepwater production remains the fastest-growing upstream oil and gas segment with production expected to hit 10.4 million boe/d in 2022 from just 300,000 barrels of oil equivalent per day (boe/d) in 1990. Wood Mackenzie has predicted that by the end of the decade, that figure will pass 17 million boe/d.

"We think dayrates will trend upwards," Noble Corp CEO Eifler said. "We're signing one- to three-year contracts right now at around $500,000 a day." Global deepwater spending by oil producers is forecast to grow to an average of $79 billion in 2026 and 2027, according to Noble, citing research from Rystad.

Key Performance Indicators to Watch

For investors tracking TechnipFMC, three KPIs stand out as the most critical indicators of ongoing performance:

1. Subsea Book-to-Bill Ratio: This metric—inbound orders divided by revenue—indicates whether the backlog is growing or shrinking. Subsea inbound orders increased to $10.4 billion, representing our fourth consecutive year with a book-to-bill greater than one. A book-to-bill consistently above 1.0x indicates sustainable growth; persistent ratios below 1.0x would signal backlog consumption and future revenue decline.

2. iEPCI™ and Subsea 2.0 Share of Orders: These differentiated offerings represent TechnipFMC's competitive moat. Our unique combination of direct awards, iEPCI™, and Subsea Services continues to represent an even greater share of our business—growing to more than 80% of total Subsea inbound in 2024. Rising penetration validates the integrated model; declining share would suggest commoditization or competitive pressure.

3. Subsea Adjusted EBITDA Margin: This profitability measure indicates whether the integration thesis is delivering financial results. Subsea revenue in a range of $8.4 - 8.8 billion, which increased from the previous guidance range of $8.3 - 8.7 billion. Subsea adjusted EBITDA margin in a range of 19 - 20%, which increased from the previous guidance range of 18.5 - 20%. Expanding margins demonstrate operating leverage and pricing power; contracting margins would suggest competitive or cost pressures.

Myth vs. Reality

| Consensus View | Reality |

|---|---|

| "TechnipFMC is just another oilfield services company" | TechnipFMC is the only fully integrated pure-play in subsea, combining equipment manufacturing, installation, and services—a unique positioning that competitors have not replicated |

| "The 2021 spin-off proves the 2017 merger was a mistake" | The spin-off was strategic pruning: retaining the high-value subsea integration while divesting the LNG/onshore engineering business with different competitive dynamics |

| "Deepwater is a mature, declining market" | Deepwater production is growing from 10 million to 17+ million boe/d by 2030, with breakeven costs competitive with shale at ~$43/bbl |

| "Competition from OneSubsea will commoditize the market" | TechnipFMC's vertically integrated model provides structural advantages (fewer interfaces, faster delivery) that OneSubsea's consortium approach cannot match |

Risk Factors and Regulatory Overhangs

Legal/Compliance Risks: While TechnipFMC has resolved its major FCPA matters, the history of compliance failures creates ongoing scrutiny. Any new allegations could damage customer relationships and result in additional penalties.

Cyclical Exposure: Despite technology differentiation, TechnipFMC remains tied to oil company capital budgets. A sustained oil price collapse would reduce project sanctioning and backlog conversion.

Vessel Market Tightness: The company relies on vessel availability for its iEPCI™ model. How is TechnipFMC managing through a tighter vessel market, given the strong SURF demand? Douglas Pferdehirt, CEO: We anticipated this in 2019 and shifted to a vessel ecosystem, partnering with others to deliver iEPCI projects. This approach allows us to grow our iEPCI offering and maintain confidence in our ability to execute projects despite vessel market constraints. The vessel ecosystem strategy mitigates but does not eliminate this risk.

Customer Concentration: Major IOCs and NOCs represent significant revenue concentration. Loss of key relationships or changes in customer capital allocation strategies could impact results.

Energy Transition: Long-term oil demand uncertainty affects deepwater investment horizons. However, deepwater's low emissions intensity relative to other oil sources may provide relative advantage within a transitioning energy system.

Conclusion: The Architects of the Deep

TechnipFMC's journey—from orchard pumps to amphibious tanks to subsea Christmas trees—represents one of the more improbable corporate evolutions in American industrial history. The French side's parallel path—from post-war engineering firm to LNG pioneer to integrated offshore contractor—added the vessel fleet and installation capabilities that completed the picture.

Today's TechnipFMC stands as a case study in strategic integration. By combining equipment manufacturing with installation services, the company created a new category—iEPCI™—that delivers measurable customer value. The Subsea 2.0 platform standardization addresses the industry's historical cost overruns. The vessel fleet provides execution certainty. And the focus achieved through the Technip Energies spin-off sharpened the company's competitive positioning.

The competitive landscape has consolidated into what amounts to a TechnipFMC vs. OneSubsea duopoly for integrated subsea. This structure provides both opportunity (pricing stability, market share clarity) and risk (regulatory scrutiny, intense competition for major projects).

For investors, TechnipFMC offers exposure to deepwater oil production—one of the most cost-competitive and lowest-emissions sources of new oil supply—through a differentiated business model that competitors have not replicated. The backlog provides revenue visibility, the technology platform provides margin protection, and the shareholder return policy provides capital allocation discipline.

The central question remains whether the integrated model will continue to outperform the traditional fragmented approach. With iEPCI™ now representing nearly one-third of the addressable market and growing, with 80%+ of orders coming through differentiated channels, and with margins expanding, the evidence suggests that TechnipFMC's strategy is working. The subsea architects have built something durable from unlikely beginnings—and they appear positioned to continue building on those foundations.

XI. The Energy Transition: Positioning for a Changing World

The deepwater subsea market exists in an unusual position relative to the energy transition. While long-term oil demand faces structural uncertainty, the near-to-medium-term reality favors deepwater development for several reasons that position TechnipFMC advantageously. TechnipFMC's positioning for the energy transition represents a strategic hedging approach that leverages its core subsea expertise while opening new revenue streams in carbon capture and storage (CCS) and hydrogen production.

Carbon Capture and Storage: Leveraging Subsea Expertise

In March 2024, TechnipFMC was selected by the Northern Endurance Partnership (NEP), a joint venture between bp, Equinor, and TotalEnergies, to deliver the first all-electric integrated project for carbon capture and storage. The NEP is building carbon dioxide transportation and storage infrastructure for carbon capture projects in the United Kingdom's East Coast Cluster.

In December 2024, TechnipFMC received full notice to proceed with this contract following NEP's announcement of financial close and entry into the execution phase. The contract covers the supply and installation of an all-electric subsea system, including trees, manifolds, umbilicals, and infield flowlines, which will be delivered using TechnipFMC's iEPCI™ execution model.

The company developed proprietary technology specifically for this emerging market. "Using proprietary CO2.0® technology, we have extended our Subsea 2.0® platform with the development of the industry's first all-electric system for carbon transportation and storage." "With this award, we are demonstrating how the competencies established in traditional energies are at the very core of the energy transition."

TechnipFMC is involved in the UK's Northern Endurance CO₂ storage initiative, aiming to sequester 10 million metric tons of CO₂ annually by 2030.

The Emissions Intensity Advantage

Deepwater production's position in the energy transition benefits from its favorable emissions profile relative to other hydrocarbon sources. Offshore deepwater wells require significantly more energy and materials compared to onshore wells, particularly during the initial construction phase. However, due to their higher productivity, the higher GHG emissions associated with offshore well construction are generally offset over the lifetime of the project. As a result, the emissions per unit of production are typically lower for offshore wells when compared to onshore wells.

Due to the scale and level of investment, sophistication and technology, the U.S. Gulf of Mexico provides among the lowest carbon barrels of oil when compared to other oil producing regions thanks in part to methane management.

Stanford research found that Venezuela and Canada rank among the most carbon-intensive oil producers because of the high energy needs and emissions associated with extracting heavy oil from unconventional reserves like tar sands. By contrast, deepwater fields—with their high per-well productivity and modern infrastructure—offer a structural emissions advantage.

New Energy Division Expansion

TechnipFMC's New Energy division focuses on carbon transportation and storage (CTS), offshore floating renewables, and green hydrogen production.

The company has allocated significant capital specifically for energy transition technologies, positioning itself to fund ambitious projects. Partnerships are the cornerstone of TechnipFMC's hydrogen strategy, evolving from early-stage research collaborations to complex, execution-focused consortia.

The commitment of $1 billion to energy transition technologies provides the financial power, while the launch of the Deep Purple pilot provides the technical proving ground.

A significant inflection point occurred in late 2024 and into 2025. The focus shifted from developing discrete components and software to deploying fully integrated, large-scale commercial systems. The landmark event was securing the contract for the Northern Endurance Partnership (NEP) CCS project in the UK.

This strategic positioning allows TechnipFMC to benefit from continued deepwater oil development while building capabilities in the adjacent markets that will matter increasingly as energy systems evolve.

XII. The Investment Case: Bull and Bear Perspectives

The Bull Case

The bull case for TechnipFMC rests on several structural advantages that distinguish it from typical oilfield services investments:

Market Leadership in a Growing Segment: Deepwater production continues to grow as one of the most economic sources of new oil supply. With project economics competitive with shale and superior to many onshore conventional sources, deepwater development should continue attracting capital even in a transition scenario where overall oil investment declines.

Unique Integrated Position: TechnipFMC's iEPCI™ model creates a differentiated offering that competitors have struggled to replicate. The OneSubsea consortium, while formidable, operates through a joint venture structure that inherently involves more interfaces than TechnipFMC's fully integrated approach. This structural advantage should support premium pricing and direct awards.

Backlog Visibility: With $14.4 billion of backlog representing approximately 18 months of revenue, TechnipFMC offers unusual visibility for a cyclical business. The quality of this backlog—with 80%+ coming through differentiated channels—provides confidence in margin sustainability.

Technology Moat Deepening: Subsea 2.0 adoption continues accelerating, with tree orders significantly outpacing overall subsea tree growth in 2024. The configure-to-order approach reduces engineering costs and delivery times while maintaining customization where needed.

Energy Transition Optionality: The carbon capture and storage market represents pure optionality at the current valuation. If CCS scales as proponents expect, TechnipFMC's early leadership through the NEP project and CO2.0® technology could create a significant new revenue stream leveraging existing subsea expertise.

Capital Return Discipline: The commitment to return at least 70% of free cash flow to shareholders in 2025 demonstrates capital discipline unusual in cyclical industries. Combined with the net cash balance sheet, this supports valuations beyond typical oilfield services multiples.

The Bear Case

The bear case centers on structural risks that could undermine the company's premium positioning:

Oil Price Sensitivity: Despite technology differentiation, TechnipFMC remains tied to oil company capital budgets. A sustained period of low oil prices—below $50 per barrel—would likely reduce project sanctioning and backlog conversion, regardless of technological advantages.

Competitive Response: OneSubsea's formation brings together SLB's reservoir expertise, Aker Solutions' subsea manufacturing, and Subsea7's installation capabilities. As this consortium matures, it may close the integration gap that currently favors TechnipFMC, potentially commoditizing the market.

Energy Transition Uncertainty: While deepwater's emissions profile is favorable relative to oil sands or aging conventional fields, long-term oil demand remains uncertain. Major energy companies may reduce upstream capital allocation faster than deepwater project timelines require, stranding some backlog.

Customer Concentration: Major IOCs and NOCs represent significant revenue concentration. A shift in capital allocation strategy by key customers like Petrobras, TotalEnergies, or Chevron could materially impact results.

Execution Risk: The iEPCI™ model concentrates project risk in a single contractor. While this enables the efficiency gains that customers value, it also means TechnipFMC bears more risk than in traditional fragmented arrangements. A major project failure could damage both financial results and market reputation.

FCPA History: While resolved, the compliance failures at both legacy companies created ongoing scrutiny. Any new allegations could damage customer relationships, trigger additional investigations, and result in further penalties.

XIII. Looking Forward: The Next Decade for TechnipFMC

The strategic trajectory for TechnipFMC over the coming decade will likely be shaped by three interrelated dynamics: deepwater development cycles, competitive consolidation, and energy transition progress.

Deepwater Development Outlook

The global deepwater market fundamentals remain supportive. Major basins—Brazil's pre-salt, Guyana's Stabroek block, West Africa's deepwater provinces, and emerging frontiers like Suriname and Namibia—offer substantial development opportunities. The economics of these fields, with breakeven costs competitive with shale and significantly below oil sands, should support continued investment even in moderate oil price environments.

TechnipFMC's recent contract wins validate this outlook. The Suriname project for TotalEnergies represents the company's expansion into frontier basins, while the Indonesia contract with Eni demonstrates continued penetration in established markets. The 20-year Chevron Australia frame agreement provides visibility extending into the 2040s.

Competitive Dynamics

The formation of OneSubsea fundamentally altered the competitive landscape. The market has effectively consolidated into a duopoly structure for integrated subsea offerings, with TechnipFMC and OneSubsea controlling the vast majority of large deepwater project awards.

This structure creates both opportunities and risks. On the positive side, reduced competition may support stable market shares and pricing. On the negative side, regulatory scrutiny of further consolidation—as evidenced by concerns about a potential Saipem/Subsea7 combination—suggests that acquisition-based growth may face obstacles.

TechnipFMC's competitive strategy appears focused on organic differentiation: continued Subsea 2.0 adoption, expansion of iEPCI™ penetration, and development of the vessel ecosystem that enables integrated project delivery. This approach leverages existing advantages rather than relying on further consolidation.

Energy Transition Integration

The energy transition represents both risk and opportunity. On the risk side, long-term oil demand uncertainty creates capital allocation challenges for customers considering multi-decade deepwater developments. On the opportunity side, TechnipFMC's subsea expertise translates directly to carbon capture and storage applications, as the Northern Endurance Partnership contract demonstrates.

The company's stated commitment of $1 billion to energy transition technologies signals serious intent to build new revenue streams. The Deep Purple hydrogen pilot in Norway provides a testing ground for offshore hydrogen production concepts. Success in these initiatives could position TechnipFMC as a key infrastructure provider for the emerging hydrogen and CCS economies.

Financial Trajectory

The financial outlook reflects these strategic dynamics. With the backlog at $14.4 billion and the order pipeline healthy, near-term revenue visibility remains strong. Margin expansion from iEPCI™ penetration and Subsea 2.0 adoption should continue, supported by the operating leverage inherent in the integrated model.

The capital return framework—targeting at least 70% of free cash flow distribution in 2025—provides shareholders a tangible claim on the company's improving cash generation. The net cash balance sheet position offers both financial flexibility and downside protection.

XIV. Final Thoughts: The Subsea Architects

TechnipFMC's evolution from John Bean's orchard sprayers to the world's most integrated subsea company represents one of the more improbable corporate journeys in industrial history. The company exists today because of a series of opportunistic pivots—from food machinery to military vehicles to offshore oil to deepwater subsea—each responding to changing market conditions while leveraging accumulated capabilities.

The 2017 merger with Technip added the vessel fleet, installation expertise, and engineering capabilities that completed the integrated vision. The 2021 spin-off of Technip Energies sharpened focus on the high-value subsea core. Today's TechnipFMC represents the distilled essence of decades of deepwater innovation.

The competitive moat rests on multiple reinforcing advantages: the iEPCI™ integration model that competitors have not replicated, the Subsea 2.0 technology platform that reduces costs and accelerates delivery, the vessel fleet that enables execution certainty, the global manufacturing footprint that provides scale economies, and the specialized workforce that cannot be quickly assembled.

The risks are real—oil price volatility, competitive pressure from OneSubsea, energy transition uncertainty, and execution complexity in an unforgiving operating environment. The FCPA history serves as a reminder that ethical failures can prove costly. But for investors seeking exposure to one of the most defensible positions in the energy services value chain, TechnipFMC offers a compelling combination of near-term visibility, technology differentiation, and energy transition optionality.

Two thousand feet beneath the ocean surface, where TechnipFMC's equipment enables the production that powers modern economies, the subsea architects continue building. The company's future will be written in the deepwater basins of Brazil, Guyana, West Africa, and beyond—and increasingly in the carbon storage reservoirs and hydrogen production facilities of the energy transition. From California orchards to the ocean floor, the journey continues.

This analysis reflects publicly available information and represents the author's independent assessment. It does not constitute investment advice or a recommendation to buy or sell any securities. Investors should conduct their own due diligence and consider their investment objectives and risk tolerance before making any investment decisions.

Looking at the article, it appears to be substantively complete, covering all major sections from the outline. The article concludes with a comprehensive "Final Thoughts" section that ties together the key themes. However, I can add a brief appendix section that would enhance the article's utility for readers, following the Acquired.fm style of including reference materials.

Appendix: Key Dates in TechnipFMC History

| Year | Event |

|---|---|

| 1883 | John Bean founds Bean Spray Pump Company in Los Gatos, California |

| 1928 | Bean Spray Pump becomes Food Machinery Corporation (FMC) |

| 1941 | FMC begins producing "Water Buffalo" amphibious tanks for WWII |

| 1958 | Institut Français du Pétrole founds Technip in Paris |

| 1967 | FMC's Oil Center Tool receives first subsea project at Ship Shoal Block 204 |

| 1993 | FMC acquires Kongsberg Offshore from Siemens |

| 2000 | FMC Corporation spins off FMC Technologies as independent company |

| 2001 | Technip acquires majority stake in Coflexip |

| 2009 | Technip joins CAC40 index |

| 2010 | Technip resolves $338 million FCPA settlement for Bonny Island bribery |

| 2015 | FMC Technologies and Technip form Forsys Subsea joint venture |

| 2016 | Schlumberger acquires Cameron International |

| 2016 | FMC Technologies and Technip announce merger (May 19) |

| 2017 | TechnipFMC begins operations as unified company (January 17) |

| 2018 | Trestakk field enters production as first iEPCI™ project |

| 2019 | TechnipFMC resolves $300 million FCPA settlement for Brazil, Iraq matters |

| 2019 | Doug Pferdehirt announces planned spin-off of Technip Energies (August) |

| 2020 | Spin-off suspended due to COVID-19 pandemic (March 15) |

| 2021 | Technip Energies spin-off completed (February 16) |

| 2023 | Chevron Australia signs 20-year frame agreement with TechnipFMC (June) |

| 2023 | SLB, Aker Solutions, and Subsea7 form OneSubsea joint venture (October) |

| 2024 | TechnipFMC achieves record iEPCI™ and Subsea 2.0® orders |

| 2024 | Northern Endurance Partnership CCS contract reaches full notice to proceed |

Glossary of Key Terms

Christmas Tree: A subsea assembly of valves, spools, and fittings installed on the wellhead to control fluid flow from the well.

EPCI: Engineering, Procurement, Construction, and Installation—the traditional contracting model for offshore projects.

iEPCI™: TechnipFMC's integrated EPCI model combining SPS and SURF scopes under a single contractor.

SPS (Subsea Production System): The equipment on the seabed that controls and processes well fluids, including trees, manifolds, and controls.

SURF (Subsea Umbilicals, Risers, and Flowlines): The infrastructure connecting subsea wells to surface facilities, including the pipes and cables that transport fluids and control signals.

Subsea 2.0®: TechnipFMC's standardized, modular product platform using configure-to-order principles to reduce customization and accelerate delivery.

CO2.0®: TechnipFMC's proprietary technology platform for carbon capture and storage applications, extending Subsea 2.0® capabilities.

Book-to-Bill: The ratio of orders received to revenue recognized, indicating whether backlog is growing (>1.0) or shrinking (<1.0).

Frame Agreement: A long-term contract establishing terms and conditions for future project call-offs, providing both parties with planning certainty.

IOC (International Oil Company): Privately owned oil companies such as ExxonMobil, Shell, Chevron, BP, and TotalEnergies.

NOC (National Oil Company): State-owned oil companies such as Petrobras, Saudi Aramco, and CNOOC.

— End of Article —

Looking at the article, it appears to be substantively complete with all major sections from the outline covered. The article concludes with comprehensive appendices including a timeline and glossary. However, I notice that while the outline mentions a "Process Power" section that was cut off, and there may be value in adding a brief section on recent developments and forward-looking indicators that would bring the article fully current to November 2025.

XV. Recent Developments and 2025 OutlookThe third quarter 2025 results, released on October 23, 2025, demonstrated continued momentum in TechnipFMC's financial performance. Total Company revenue in the third quarter was $2,647.3 million, with net income attributable to TechnipFMC of $309.7 million, or $0.75 per diluted share. This marked a 4.4% increase from the previous quarter and a 12.7% increase year-over-year.

The company maintained a book-to-bill ratio above 1.0x for the fifteenth time in sixteen quarters, while also increasing its full-year free cash flow guidance and announcing a significant expansion to its share repurchase program.

The Subsea segment continues to drive results. Subsea reported third-quarter revenue of $2,319.2 million, an increase of 4.6 percent from the second quarter, with sequential revenue improvement largely driven by increased project activity, particularly iEPCI™ projects, in Africa, the Americas, and Australia.

Subsea inbound orders totaled $2.4 billion, supported by major awards from Petrobras in Brazil and ExxonMobil in Guyana. The quarter included the company's seventh award from ExxonMobil in Guyana—the Hammerhead project. TechnipFMC has been awarded all of the operator's subsea production systems in Guyana since the first award in 2017.

Raised Guidance and Capital Returns

Management significantly increased its financial outlook for both 2025 and 2026. The company provided updated full-year 2025 guidance, increasing its free cash flow forecast to a range of $1.3 - $1.45 billion, up from the previous $1.0 - $1.15 billion. For 2026, the company guided subsea revenue to a range of $9.1 billion-$9.5 billion, with adjusted EBITDA margin in a range of 20.5%-22%.

The capital return framework received a substantial boost. TechnipFMC's Board of Directors authorized an additional $2 billion for share repurchases, bringing the total authorization to $2.3 billion. Together with the remaining balance under the existing program, the Company is now authorized to repurchase shares of up to $2.3 billion, representing nearly 16 percent of the Company's outstanding shares.

TechnipFMC ended the quarter with a solid balance sheet, reporting a net cash position of $439 million as of September 30, 2025, representing the difference between $877 million in cash and cash equivalents and total debt of $438 million.

2025 Contract Activity

The year 2025 demonstrated strong commercial momentum across TechnipFMC's key markets. In March 2025, TechnipFMC was awarded a major integrated Engineering, Procurement, Construction and Installation (iEPCI™) contract worth over $1 billion by Shell for its Gato do Mato greenfield development offshore Brazil.

Also in March, TechnipFMC secured a 'large' integrated Engineering, Procurement, Construction, and Installation (iEPCI) contract by Equinor for the Johan Sverdrup Phase 3 development in the Norwegian North Sea.

In July, TechnipFMC was awarded an integrated engineering, procurement, construction, and installation contract by Equinor for its Heidrun extension project in the Norwegian North Sea. The project will enhance the current infrastructure and extend the production lifecycle for the Heidrun platform.

September brought multiple Brazilian awards. TechnipFMC was awarded two subsea contracts by Petrobras for flexible pipe for use in multiple basins. The first award is a substantial contract to design, engineer, and manufacture flexible gas injection risers—a high-technology solution to sustain reservoir pressure and enhance production efficiency through high-capacity gas reinjection in pre-salt formations in the Santos Basin.

TechnipFMC also landed a significant contract with Petrobras to design, engineer, and manufacture subsea production systems for multiple offshore projects in Brazil, valued between $75 million and $250 million, to support a mix of greenfield developments, brownfield expansions, and asset revitalizations across Petrobras' portfolio.

Most recently, in November 2025, TechnipFMC was awarded a significant integrated Engineering, Procurement, Construction and Installation (iEPCI) contract by Eni SpA for the deepwater Maha project offshore Indonesia. The project represents Eni's first deployment of TechnipFMC's Subsea 2.0® configure-to-order (CTO) technology in the country.

Forward Pipeline and Market Outlook

Looking ahead, TechnipFMC highlighted a growing pipeline of subsea opportunities over the next 24 months, with the combined value increasing from $23.6 billion in Q4 2023 to $27.8 billion in Q3 2025.

Management expressed confidence that offshore projects will continue to receive an increasing share of capital investment. The change in spending allocation is due in part to the significant improvements made in developing the large, high-quality, and prolific reservoirs found offshore.

The company's commercial success year-to-date reinforces confidence in delivering more than $10 billion of Subsea orders in 2025. Higher economic returns and greater project certainty are providing sustainability to current activity levels.

XVI. Conclusion: The Architecture of Competitive Advantage

TechnipFMC's story offers a masterclass in corporate evolution and strategic positioning. From John Bean's orchard sprayers in 1883 California to the deepest waters of the Atlantic, from French engineering bureaus to Norwegian subsea controls, the company represents the convergence of unlikely histories into a uniquely capable enterprise.

The strategic logic that animates TechnipFMC today can be understood through three lenses:

First, the integration thesis has been validated. The iEPCI™ model, born from the 2017 merger, now represents nearly one-third of the addressable subsea market. Customers have demonstrated willingness to award projects directly—bypassing competitive tenders—to access TechnipFMC's integrated capabilities. The Subsea 2.0 platform has accelerated this trend, with configure-to-order tree orders significantly outpacing overall subsea tree growth. Multi-decade frame agreements with operators like Chevron provide visible evidence that the integration premium is real and durable.

Second, the deepwater market structure favors incumbents. The barriers to entry—specialized vessels, decades of engineering expertise, compliance track records, and customer relationships built across hundreds of projects—create a market that new entrants cannot easily penetrate. The consolidation into a TechnipFMC versus OneSubsea duopoly further concentrates the industry, reducing the likelihood of destructive competition while maintaining incentives for innovation.

Third, the energy transition creates optionality, not existential risk. TechnipFMC's positioning recognizes that deepwater oil production—with its low emissions intensity relative to oil sands and aging conventional fields—will remain competitive within energy portfolios even as the transition progresses. Meanwhile, the company's subsea expertise translates directly to carbon capture and storage applications, as the Northern Endurance Partnership contract demonstrates. The $1 billion commitment to energy transition technologies provides the resources to pursue this optionality without compromising core business investment.

The financial trajectory supports this strategic narrative. With trailing twelve-month revenue approaching $10 billion, adjusted EBITDA margins expanding toward 20%, a backlog exceeding $14 billion, and free cash flow guidance raised to $1.3-1.45 billion for 2025, TechnipFMC delivers the financial performance that validates its competitive position.

The capital allocation framework—targeting at least 70% of free cash flow returned to shareholders through dividends and a newly expanded $2.3 billion share repurchase authorization—signals management confidence while providing tangible returns to patient shareholders.

For students of business strategy, TechnipFMC illustrates several enduring lessons: that vertical integration can create value when it eliminates transaction costs and enables new service categories; that standardization succeeds when it solves customer problems rather than merely reducing supplier costs; that cyclical industries reward technology differentiation and backlog management; and that the willingness to revisit major strategic decisions—even recent ones like the Technip Energies spin-off—demonstrates intellectual honesty about what combinations actually create value.

The competitive moat rests on the accumulated weight of history: the subsea controls expertise from Kongsberg, the flexible pipe manufacturing from Coflexip, the installation capabilities from Technip's vessel fleet, the deepwater engineering from decades of FMC subsea projects. Competitors cannot easily replicate these capabilities because they were built through acquisitions, organic investment, and operational learning across decades.

Two thousand feet beneath the ocean surface, TechnipFMC's equipment enables the production that powers modern economies. The company's future will be written in the deepwater basins of Brazil, Guyana, West Africa, and beyond—and increasingly in the carbon storage reservoirs and hydrogen production facilities of the energy transition. From California orchards to the ocean floor, the subsea architects continue building on foundations that no competitor can quickly replicate.

The question for investors is not whether TechnipFMC occupies a defensible competitive position—the evidence strongly suggests it does—but rather how long the current cycle of deepwater development and margin expansion can persist, and whether the energy transition will ultimately prove complementary or competitive to the company's core franchise. History suggests that companies with TechnipFMC's capabilities, strategic flexibility, and capital discipline find ways to adapt and prosper through industry transitions. The subsea architects have navigated transformations before; there is reason to believe they will do so again.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube