McCormick & Company: The Spice Empire's Journey from Baltimore Cellar to Global Flavor Giant

I. Introduction & Cold Open

The boardroom at McCormick's Hunt Valley headquarters erupted in tension. It was July 2017, and CEO Lawrence Kurzius faced the biggest decision in the company's 128-year history. On the table: a $4.2 billion acquisition of Reckitt Benckiser's food division—home to Frank's RedHot and French's Mustard. Unilever had already bid. So had Hormel. The price tag was astronomical—seven times revenue, more than double what McCormick itself traded at. Board members shifted nervously. This single decision would either cement McCormick's dominance in the condiment aisle or saddle it with crippling debt. Kurzius leaned forward: "We pay up to win."

That moment crystallized everything McCormick had become—a company willing to bet billions on America's evolving taste buds, from a Baltimore cellar operation selling root beer door-to-door to the world's undisputed spice emperor controlling what flavors reach your table.

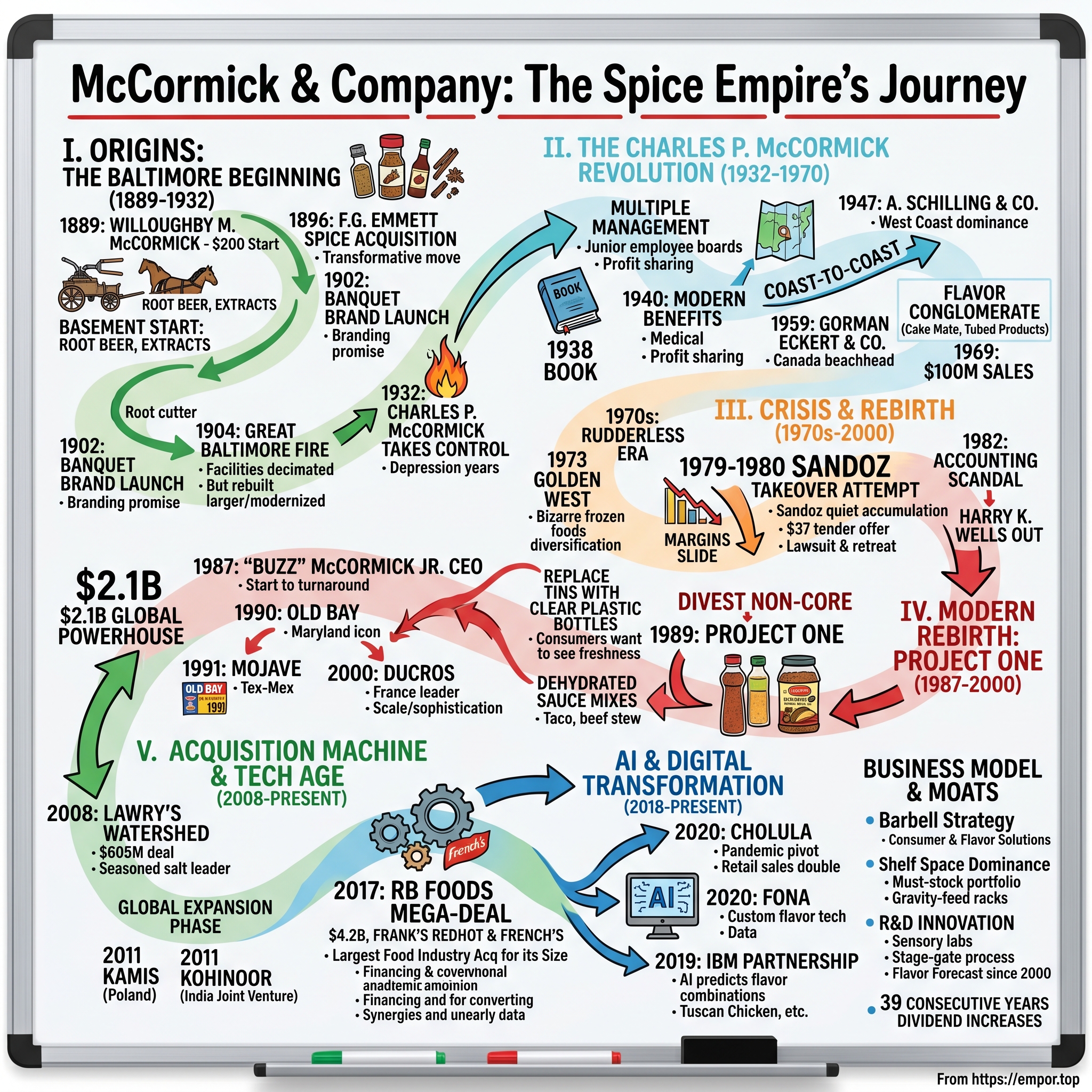

Picture this: In 1889, a 25-year-old Willoughby M. McCormick borrowed $200—roughly $7,000 in today's money—to buy a second-hand root cutter, a horse, and a wagon. He started selling flavoring extracts from a single room and cellar in Baltimore, knocking on doors, one household at a time. Fast forward to today: McCormick commands $6.7 billion in annual sales across 150 countries, owns virtually every major spice brand you recognize, and holds roughly 20% of the global packaged spice market. The company has increased its dividend for 39 consecutive years, employs 14,000 people worldwide, and its products sit in 95% of American kitchens.

The central question isn't just how a door-to-door salesman built a spice monopoly—it's how a company selling the world's oldest commodity, something humans have traded for millennia, continues to generate 15% operating margins and command an $18 billion market capitalization. The answer lies in a story of patient capital, strategic brilliance, and an uncanny ability to predict what flavors Americans will crave next.

II. Origins: The Baltimore Beginning (1889-1932)

The Founder's Story

Baltimore in 1889 was America's sixth-largest city—a bustling port where German immigrants ran breweries, Italian families opened restaurants, and the smell of Old Bay (though not yet invented) seemed destined to permeate the air. Into this milieu stepped Willoughby M. McCormick, whose ambition far exceeded his means. At 25, he possessed the kind of restless energy that would either build an empire or end in bankruptcy.

His business model was primitive but effective: manufacture flavoring extracts, fruit syrups, and root beer in a basement, load them onto a wagon, and sell them door-to-door. Think of it as the 19th-century equivalent of a direct-to-consumer startup, except instead of Facebook ads, you had a horse that needed feeding and Baltimore's notorious humidity making your products spoil if you didn't move them fast enough.

The genius wasn't in what Willoughby sold—dozens of competitors peddled similar wares. It was his motto that set him apart: "Make the Best—Someone Will Buy It." In an era of rampant food adulteration (pepper cut with charcoal dust, cinnamon bark mixed with sawdust), McCormick's commitment to quality was revolutionary. He personally tested every batch, refused to cut corners even when competitors undercut his prices, and slowly built a reputation that traveled faster than his horse-drawn wagon.

Critical Early Moves

The pivotal moment came in 1896. Willoughby had been grinding away for seven years, building modest success but nothing transformative. Then F.G. Emmett Spice Company came up for sale. Emmett was established, respected, and crucially, had relationships with Baltimore's growing food processing industry. Willoughby scraped together the funds—mortgaging everything, borrowing from skeptical relatives—and acquired it. Overnight, McCormick & Company transformed from a flavoring extract operation to a legitimate spice business.

By 1902, Willoughby launched the Banquet Brand for spices and mustards—a prescient move toward brand differentiation when most spices were sold as undifferentiated commodities in bulk. The branding wasn't just aesthetic; it was a promise. When you bought Banquet, you weren't just buying cinnamon—you were buying McCormick's reputation.

Then came near-disaster. The Great Baltimore Fire of 1904 started on a frigid February morning and burned for 31 hours, destroying 1,500 buildings across 70 city blocks. McCormick's facilities were decimated—machinery melted into abstract sculptures, inventory turned to ash, decades of records vanished. Insurance covered only a fraction of losses. Most businesses would have folded. Willoughby did something extraordinary: he borrowed more money, rebuilt larger than before, and used the catastrophe as an opportunity to modernize equipment. Within a year, sales exceeded pre-fire levels.

By 1921, McCormick had erected a nine-story headquarters in downtown Baltimore—complete with its own printing plant, testing laboratory, and employee cafeteria (radical for the era). The building wasn't just functional; it was a statement. McCormick had arrived. Sales hit $5 million by 1928—roughly $85 million in today's dollars.

The Black Pepper Scandal

Not everything was smooth sailing. In 1916, the U.S. Bureau of Chemistry (predecessor to the FDA) launched an investigation into McCormick's black pepper. Government chemists found "adulteration"—not with harmful substances, but with pepper dust and stems that naturally occurred during processing but technically violated pure food laws. The company was fined and forced to change its labeling.

Willoughby could have fought it, claimed industry standard practice (which it was), or quietly paid the fine and continued. Instead, he instituted even stricter quality controls, began advertising the incident as proof of McCormick's transparency, and turned a potential scandal into a marketing coup. "Even the government tests our spices," became an unofficial slogan. Sales of black pepper actually increased.

Succession Planning

The most important hire Willoughby ever made walked through the door in 1912: his nephew, Charles P. McCormick. At 16, Charles started in the factory, learning every operation from grinding spices to maintaining machinery. Willoughby was building more than a business—he was crafting a dynasty.

Charles possessed something Willoughby lacked: formal business education and modern management ideas. While Willoughby ruled through force of personality, Charles studied organizational psychology, employee motivation, and systematic expansion. By 1925, Charles was elected to the board. When Willoughby died suddenly of a heart attack in 1932—at the depths of the Great Depression with banks failing daily—36-year-old Charles inherited a company generating $3.5 million in annual sales but facing the worst economic crisis in American history.

The transition could have destroyed McCormick. Instead, it marked the beginning of its most transformative era.

III. The Charles P. McCormick Revolution (1932-1970)

Management Innovation During Depression

Charles P. McCormick took control of a profitable company in the worst possible year. In 1932, unemployment hit 24%, thousands of banks had failed, and Americans were more concerned with finding bread than seasoning it. Most CEOs would have cut costs, fired workers, and hunkered down. Charles did the opposite.

His first act as president was radical: he called an all-hands meeting and announced that while salaries might need temporary cuts, no one would be fired. Instead, he introduced something he called "Multiple Management"—a system where junior employees formed boards that paralleled senior management, proposing ideas and sharing in profits when their suggestions succeeded. Think of it as Google's "20% time" policy, except invented during the Depression by a spice company.

The psychology was brilliant. While competitors' employees feared for their jobs, McCormick's workforce was energized, proposing cost-saving measures and process improvements. One junior board suggested eliminating fancy packaging for industrial customers—saving $50,000 annually. Another proposed selling spice racks to grocery stores, creating permanent McCormick real estate in American kitchens.

Within one year—while the Depression deepened—McCormick returned to profitability. Charles didn't keep the secret. He published a book about Multiple Management in 1938, gave speeches across the country, and helped implement the system at companies throughout the US, Canada, and Britain. His philosophy, captured in company archives: "I valued opinions of others, wasn't threatened by contrary ideas."

By 1940, McCormick offered benefits that wouldn't become standard for decades: medical insurance, profit sharing, and what they called "psychological wages"—recognition, advancement opportunities, and genuine input into company decisions. During World War II, when workers could easily jump to defense contractors, McCormick retained 94% of its workforce.

Geographic Expansion

Charles understood something fundamental: spice preferences are regional, but spice companies could be national. Post-WWII America was mobile, prosperous, and experimenting with food. McCormick needed to be everywhere.

The masterstroke came in 1947 with the acquisition of A. Schilling & Company. Schilling wasn't just any competitor—it was San Francisco's oldest spice company, founded in 1881, with dominant market share west of the Rockies. The price was steep, but Charles saw what others missed: complementary distribution networks. McCormick owned the East Coast; Schilling owned the West. Together, they had true coast-to-coast coverage.

Rather than force the McCormick brand onto Western customers loyal to Schilling, Charles did something counterintuitive: he kept both brands. For the next 45 years, identical products were sold as McCormick east of the Mississippi and Schilling to the west. This dual-branding strategy—now standard in consumer goods—was revolutionary for its time.

The expansion accelerated: - 1953: Ben-Hur Products in California, adding manufacturing capacity - 1959: Gorman Eckert & Co., Canada's largest spice firm, providing international beachhead - 1961: Acquisition of Baltimore's Gilroy Foods, entering the industrial seasoning market

Each acquisition followed a pattern: identify the regional leader, pay a premium for quality, maintain local management and brand equity, then slowly integrate back-office operations. It was a playbook that would define McCormick's M&A strategy for decades.

Building the Conglomerate

The 1960s saw Charles transform McCormick from a spice company into a flavor conglomerate. The acquisitions came fast:

- Baker Extract Company (1962): Premium vanilla and extracts

- Cake Mate (1965): Decorating products for home bakers

- Childers Foods (1967): Portion-control condiments for restaurants

- Tubed Products (1968): Innovative packaging for food service

But the real innovation wasn't what McCormick bought—it was how they integrated acquisitions. Charles personally visited each acquired company, spent weeks on the factory floor, and implemented Multiple Management systems. Employee satisfaction scores at acquired companies typically increased within six months. When competitors conducted hostile takeovers, McCormick conducted cultural transformations.

By 1969, when Charles announced his retirement, McCormick generated $100 million in annual sales—a 30-fold increase from when he took over. The company operated plants in California, Canada, and the UK, employed thousands, and had transformed from a regional Baltimore business into a multinational corporation.

Charles P. McCormick died of a heart attack on July 1, 1970, just months after retiring. His legacy wasn't just financial—he had proven that treating employees as partners rather than costs could drive extraordinary returns. The question was whether McCormick could maintain that culture as it entered a new decade of challenges.

IV. Crisis & The Sandoz Takeover Attempt (1970s-1982)

The Golden West Era

The 1970s started with McCormick rudderless. Charles's successor, Harry K. Wells, lacked his predecessor's vision and charisma. While America was discovering ethnic cuisines—Chinese takeout proliferating, Mexican restaurants expanding beyond the Southwest—McCormick chased a bizarre diversification strategy: frozen foods.

The 1973 acquisition of Golden West Foods seemed logical enough. Frozen onion rings and mushrooms weren't that different from dehydrated vegetables, right? Wrong. Frozen foods required different distribution, different customers, different everything. But Wells doubled down: TV Time Foods (frozen snacks), Astro Foods (frozen desserts), Han-Dee Pak (frozen portion-control foods). By 1978, McCormick operated massive freezer warehouses, a fleet of refrigerated trucks, and competed against giants like Ore-Ida and Birds Eye.

The financials told the story: while spice margins held steady at 15-20%, frozen foods barely broke even. Working capital requirements exploded. Return on invested capital plummeted. McCormick stock, which had traded at 20 times earnings in 1972, fell to just 8 times by 1979.

The Sandoz Drama (1979-1980)

Enter Sandoz Ltd., the Swiss pharmaceutical giant better known today as Novartis. In early 1979, with McCormick stock languishing at $19, Sandoz quietly accumulated 5% of shares. Then came the bombshell: a $37-per-share tender offer for the remainder—a 95% premium.

The McCormick board panicked. This wasn't just about money; it was about identity. McCormick had been independent for 90 years, a Baltimore institution, a family-controlled enterprise even after going public. Being swallowed by a Swiss drug company felt like corporate death.

The defense was chaotic but effective. First, McCormick bought back Sandoz's stake at $28—a 47% premium but below Sandoz's offer price. Wild rumors swept Wall Street: Was McCormick negotiating? Were other bidders circling? The stock became a speculative football, swinging 10% daily.

In October 1979, Sandoz formally announced its takeover intention. McCormick's response was unprecedented: they sued in May 1980, claiming Sandoz violated securities laws, manipulated the market, and acted in bad faith. The legal arguments were weak, but the delay tactics worked. Sandoz, facing regulatory scrutiny and realizing McCormick would scorch the earth rather than surrender, retreated in September 1980.

Victory came at a price. McCormick had spent millions on legal fees, buybacks, and golden parachutes. Debt levels were uncomfortably high. The company had survived, but barely.

The Accounting Scandal

Just when stability seemed possible, internal auditors discovered something horrifying in 1982: for five years, from 1977 to 1980, McCormick had systematically delayed expense recognition to meet profit targets. Nothing illegal—just aggressive accounting that pushed the boundaries of GAAP. But in the post-Watergate era of corporate accountability, it was devastating.

The board's response was swift and severe. Wells was forced out. For the first time in company history, outside directors were brought in—not just independent board members, but true outsiders with no Baltimore connections, no spice industry experience, no loyalty to the old ways.

The new CEO, Harry K. Wells's hastily appointed successor, inherited a mess: frozen food divisions hemorrhaging cash, accounting credibility shattered, employee morale at historic lows, and domestic spice consumption falling 20% as Americans embraced convenience foods over home cooking.

McCormick needed more than new management. It needed resurrection. The stage was set for perhaps the most important hire in company history—one that would transform McCormick from a troubled conglomerate back to its spice roots, and then beyond anyone's imagination.

V. The Modern Rebirth: Project One (1987-2000)

New Leadership

Charles P. McCormick Jr.—call him "Buzz" to differentiate from his famous great-uncle—wasn't supposed to be CEO. In 1987, he was running McCormick's European operations from London, content to stay an ocean away from Baltimore's boardroom drama. But when the board called, family duty prevailed. At 39, Buzz became the youngest CEO in company history, inheriting a company that had lost its way.

His first hundred days were brutal. Buzz discovered frozen foods were losing $20 million annually—worse than anyone realized. The spice business, while profitable, was stagnant. McCormick's iconic red-and-white tins looked dated next to competitors' modern packaging. Market share was eroding to private labels. Something radical was needed.

The boardroom presentation that changed everything came in March 1988. Buzz proposed divesting all non-core businesses—every frozen food operation, regardless of sunk costs—and reinvesting $200 million into modernizing the spice business. Board members gasped. That was more than McCormick's entire annual profit. "We're going to revolutionize how America buys spices," Buzz declared. "Or we're going to fail spectacularly trying."

Project One Revolution

Project One launched in 1989—McCormick's centennial year, which felt symbolic. The initiative's centerpiece was audacious: replace every single red-and-white tin in America with clear plastic bottles. Not just new products—every existing package in every store, restaurant, and warehouse.

The logistics were nightmarish. McCormick needed to:

- Retool 14 production facilities for plastic bottles

- Educate retailers about new shelf configurations

- Convince consumers that plastic was better than metal

- Execute the transition without losing shelf space to competitors

The clear bottles weren't just aesthetic. Consumer research showed people wanted to see spices before buying—checking color, freshness, texture. The new bottles had wider openings (easier to measure), clearer labels (recipes on back), and most importantly, looked premium despite costing less to produce than tins.

The gamble worked. Within 18 months, McCormick had converted 90% of retail distribution. Sales jumped 15% in year one alone. Competitors scrambled to copy the format, but McCormick had already locked up the best shelf positions. The psychological impact was profound: McCormick went from looking tired to looking innovative overnight.

But Buzz wasn't done. Alongside packaging, he launched dehydrated sauce mixes—products like taco seasoning, spaghetti sauce mix, and beef stew seasoning that aligned with busy households wanting home-cooked meals without extensive prep. These mixes generated 40% gross margins, double that of pure spices.

Strategic Acquisitions & Portfolio Building

With the core business revitalized, Buzz turned to acquisitions—but with discipline his predecessors lacked. Each target had to meet specific criteria: strong brand equity, defensible market position, and synergies with existing operations.

The 1990 Old Bay acquisition exemplified this strategy. Old Bay wasn't just a seasoning—it was Maryland's cultural icon, created in 1939 by a German-Jewish refugee and synonymous with Chesapeake Bay seafood. McCormick paid a premium but gained something priceless: authentic regional heritage that couldn't be replicated.

The deals accelerated, each adding a piece to McCormick's flavor mosaic: - 1991: Mojave Foods—Southwest seasonings riding the Tex-Mex wave - 1993: Golden Dipt—seafood breading products for the growing casual dining sector

International expansion followed a different playbook. Rather than export American brands, McCormick acquired local champions:

- Grupo Pesa (Mexico): Leading Mexican spice brand when NAFTA was creating cross-border opportunities

- Tuko Oy (Finland): Nordic flavors for increasingly sophisticated European consumers

- Butto (Switzerland): Premium positioning in wealthy Alpine markets

The crown jewel came in 2000 with Ducros, France's leading spice brand. The French were notoriously resistant to foreign foods, but Ducros was untouchably French. McCormick paid €335 million—expensive, but it provided European scale and sophistication. Ducros was later renamed McCormick France, but the products remained decidedly French.

By 2000, Buzz had transformed McCormick from a troubled $400 million company to a $2.1 billion global powerhouse. The company that almost fell to Swiss pharmaceuticals now operated on six continents. But the biggest transformations were yet to come.

VI. The Acquisition Machine Era (2008-2017)

The Lawry's Watershed

Alan Wilson took the CEO reins in 2008, just as Lehman Brothers collapsed and the global economy cratered. Most CEOs would have battened down the hatches. Wilson went shopping.

His target was Lawry's—the seasoned salt empire built from a single Beverly Hills restaurant in 1938. Unilever owned it but considered spices non-core. Wilson smelled opportunity. The negotiation dragged through the financial crisis, with Unilever's asking price dropping weekly as credit markets froze. McCormick struck in late 2008, paying $605 million—the largest acquisition in company history.

The FTC almost killed it. Regulators worried about McCormick controlling too much of the seasoned salt market. In a creative solution, McCormick agreed to sell its Season-All brand to Morton Salt, preserving competition while keeping Lawry's crown jewel products. The deal closed in July 2008, just as the recession hit bottom.

Lawry's delivered immediately. The brand had 70% market share in seasoned salts, exclusive partnerships with major steakhouse chains, and margins that made McCormick's accountants weep with joy. Within two years, the acquisition had paid for itself.

Global Expansion Phase

Wilson's successor, Lawrence Kurzius, accelerated the acquisition pace starting in 2011. Where previous CEOs bought opportunistically, Kurzius operated with private equity precision. Each deal fit a specific strategic gap:Kitchen Basics in 2011 for $38 million—liquid stocks capturing the home-cooking renaissance. Kamis S.A. (Poland) for $291 million the same year—Eastern European entry when those markets were booming

The Eastern European foothold through Kamis wasn't just strategic positioning—it was prescient. Kamis was a brand leader in spices, seasonings, mustards and other flavor products in Poland. Annual sales of the business were approximately 300 million Polish zloty (approximately $105 million in U.S. dollars). McCormick agreed to acquire the company for approximately 830 million Polish zloty (approximately $291 million in U.S. dollars). Kamis was a leading consumer brand in Poland with approximately a 45% share of the spice and seasoning category and 30% share of the mustard category. Founded in 1991, the business had expanded beyond Poland with distribution subsidiaries in Russia, Romania and Ukraine, and exports into a number of other Central and Eastern Europe countries.

But India represented the real prize. McCormick signed an agreement in 2011 to form a joint venture with Kohinoor Foods Ltd (KFL) to market and sell its basmati rice and food products in India. Annual net sales of Kohinoor Speciality Foods India were projected to be approximately $85 million. McCormick invested a total of $115 million for this transaction which included McCormick holding an 85% interest in the new joint venture. McCormick invested a total of 5.2 billion Indian rupees ($113 million U.S. dollars) for this transaction. Since 1976, the 'Kohinoor' brand had been one of the top national brands in the basmati rice category in India, with a category share above 15% among more than 100 other brands. In addition, Kohinoor had expanded its business beyond rice with the introduction of ready-to-eat products, cook-in sauces, cooking pastes, spices, seasonings and frozen foods. The venture would eventually hit turbulence—a dispute over rice supplies in 2015, followed by McCormick acquiring the remaining 15% in 2017, then ultimately divesting the brand to Adani Wilmar in 2022—but it provided crucial lessons about emerging market complexities.

The domestic acquisitions revealed Kurzius's understanding of American palates evolving. The purchase price for Stubb's was approximately $100 million subject to certain closing adjustments. McCormick acquired the Stubb's business for a cash payment of approximately $100 million subject to certain closing adjustments. After opening his first Stubb's Legendary Bar-B-Q restaurant in 1968, C.B. Stubblefield began selling his popular sauces to retail grocers in 1992. These products featured bold flavors made of high quality ingredients from a man that knew BBQ. With newly expanded distribution and product offerings, annual sales growth exceeded 20% in both 2013 and 2014. Annual sales of the business were projected to reach $30 million in 2015. At first glance, paying three times revenue for a $30 million BBQ sauce business seemed excessive. But Kurzius saw what spreadsheets missed: authenticity couldn't be manufactured.

The Italian acquisition of Enrico Giotti in 2016 added another dimension. The purchase price for Giotti was approximately 120 million Euro (127 million U.S. dollars) subject to certain closing adjustments and the transaction multiple was expected to be approximately 12 times EBITDA (earnings before interest, tax, depreciation and amortization). Financed with cash and short-term borrowings, McCormick expected to record an acquisition price of 120 million Euros (127 million U.S. dollars), subject to certain closing adjustments. The purchase price for Giotti was 120 million Euro (127 million U.S. dollars) subject to certain closing adjustments. The transaction multiple was approximately 12 times EBITDA. Giotti was well known in the industry for its innovative beverage, sweet, savory and dairy flavor applications. Annual sales were approximately 53 million Euro (56 million U.S. dollars). The acquisition of Giotti expanded the breadth of value-added products for McCormick's industrial segment including additional expertise in flavoring health and nutrition products. This wasn't about retail shelves—it was about becoming indispensable to food manufacturers navigating health-conscious consumers.

The RB Foods Mega-Deal (2017)

The phone call came on a Friday afternoon in March 2017. Reckitt Benckiser, the British consumer goods conglomerate, had decided to divest its food division. The portfolio included Frank's RedHot—America's #1 hot sauce—and French's Mustard, the yellow standard bearer since 1904. RB wanted a quick, clean sale. No auctions. Select bidders only.

Kurzius assembled his team that weekend. The math was daunting: RB Foods generated $600 million in annual revenue with EBITDA margins north of 30%—double McCormick's average. The asking price would likely exceed $4 billion. McCormick's entire market cap was $12 billion.

The competition was formidable. Unilever had the scale and distribution muscle. Hormel Foods, riding high from its Skippy peanut butter acquisition, wanted to expand its condiment portfolio. Private equity firms circled, sensing a breakup opportunity.

But Kurzius had advantages others lacked. McCormick already manufactured private label hot sauce for major retailers—they understood the category's economics intimately. Their Flavor Solutions division supplied ingredients to many of the same quick-service restaurants where Frank's and French's dominated. Most importantly, McCormick had proven it could integrate large acquisitions without destroying brand equity.

The first bid went in at $3.8 billion. RB balked. Unilever bid $4 billion. Hormel matched. The investment committee at McCormick faced a choice: walk away from a transformational deal or pay a price that would terrify Wall Street.

"What's Frank's RedHot worth to the company that already owns Lawry's, Old Bay, and Cholula?" Kurzius asked the board. "What's French's Mustard worth when bundled with our foodservice business?" The answer wasn't in the spreadsheets—it was in the strategic logic of category dominance.

The winning bid: $4.2 billion. Seven times revenue. Twenty times EBITDA. The largest acquisition in food industry history for a company McCormick's size. Analysts called it reckless. Short sellers piled in, betting the debt burden would cripple operations.

They were wrong. Within eighteen months, McCormick had refinanced the acquisition debt at favorable rates, achieved $50 million in cost synergies, and accelerated Frank's RedHot growth through innovative flavors and expanded distribution. The hot sauce category was exploding—growing 8% annually as millennials doused everything in spicy condiments. Frank's wasn't just a brand; it was a platform for flavor innovation across McCormick's entire portfolio.

The integration revealed Kurzius's operational genius. Rather than impose McCormick's culture on RB Foods, he cherry-picked best practices from both organizations. RB's lean manufacturing techniques improved McCormick's plant efficiency. McCormick's Multiple Management philosophy energized RB's workforce. French's Mustard, which had been neglected under RB's pharmaceutical focus, suddenly had resources for innovation. New flavors launched. Food service partnerships expanded. Market share, declining for years, stabilized then grew.

By 2019, RB Foods was contributing $650 million in annual revenue with margins intact. The acquisition that was supposed to sink McCormick had instead catapulted it into a new tier of food companies—too large for easy acquisition, too valuable to ignore.

VII. The AI & Digital Transformation (2018-Present)

Recent Strategic Moves

The Cholula acquisition in 2020 should have been impossible. COVID-19 had shuttered restaurants—hot sauce's primary channel. Capital markets were frozen. McCormick's stock had plummeted 30% in March. Yet Kurzius paid $800 million to L Catterton for the Mexican hot sauce brand, seeing opportunity where others saw catastrophe.

His logic was counterintuitive but brilliant: pandemic lockdowns had turned millions of Americans into home chefs, experimenting with flavors they'd previously encountered only in restaurants. Hot sauce consumption at retail was surging even as foodservice collapsed. Cholula, with its distinctive wooden cap and authentic Mexican heritage, was perfectly positioned for this shift. Within six months, retail sales had doubled, validating the pandemic pivot.

The FONA acquisition the same year flew under the radar but was equally strategic. The Geneva, Illinois-based flavor manufacturer specialized in creating custom flavors for the food industry—everything from vanilla profiles for ice cream manufacturers to savory notes for soup companies. FONA brought proprietary flavor technology and deep customer relationships that would take decades to build organically. More importantly, it brought data—millions of flavor combinations and their performance metrics across categories.

The 2018 headquarters move from Sparks to Hunt Valley, Maryland, represented more than real estate optimization. The new facility featured state-of-the-art innovation labs, test kitchens visible from the lobby, and collaborative spaces designed to break down silos between consumer and industrial divisions. Employees from different brands and functions suddenly found themselves sharing elevators, sparking conversations that led to unexpected innovations.

Technology Innovation

The partnership with IBM announced in 2019 marked McCormick's boldest technological leap. The collaboration wasn't about automation or efficiency—it was about creativity itself. Could artificial intelligence predict the next sriracha? Could machine learning identify flavor combinations humans would never consider?

IBM's Watson analyzed millions of data points: recipe databases, social media flavor trends, restaurant menus, even food science papers on taste perception. McCormick fed it their proprietary data: successful and failed product launches, regional taste preferences, seasonal consumption patterns. The AI didn't replace McCormick's food scientists—it amplified their capabilities.

The first AI-developed products launched under the "ONE" platform in late 2019: Tuscan Chicken seasoning, Bourbon Pork Tenderloin, and New Orleans Sausage. Skeptics dismissed them as gimmicks. Then sales data arrived. The AI-developed seasonings outperformed traditionally developed products by 14% in test markets. More impressively, they achieved 20% higher repeat purchase rates.

But the real breakthrough came in the Flavor Solutions division. Food manufacturers struggling with sodium reduction, sugar replacement, or plant-based formulations could now access AI-powered flavor systems that maintained taste while meeting health objectives. A major soup manufacturer reduced sodium by 30% using McCormick's AI-developed flavor system without sacrificing consumer acceptance. A plant-based meat company achieved "bleeding" visual effects and umami depth through McCormick's computational flavor matching.

The digital transformation extended beyond R&D. E-commerce, an afterthought pre-pandemic, became central to strategy. McCormick launched direct-to-consumer platforms for personalized spice blends, subscription boxes for international cuisines, and QR-coded packaging linking to recipe videos. By 2023, digital sales exceeded $500 million annually.

Current Performance

The numbers tell only part of the story. 2024 revenue of $6.724 billion reflects modest 0.92% growth—hardly spectacular. But beneath the headline, transformation churns. The Consumer segment, despite flat volumes, maintains pricing power in an inflationary environment. The Flavor Solutions segment, growing 14% with expanding margins, validates the shift toward value-added industrial products.

Market capitalization hovering around $18.7 billion suggests investor ambivalence—neither excessive enthusiasm nor deep skepticism. The price-to-earnings ratio of 25 reflects premium valuation but not bubble territory. For a company founded when Benjamin Harrison was president, such steady appreciation seems almost quaint in an era of meme stocks and crypto speculation.

Yet the 39th consecutive year of dividend increases reveals something profound: McCormick has mastered the art of consistent wealth creation across multiple economic cycles. Through stagflation, dot-com bubbles, financial crises, and pandemics, those quarterly checks keep arriving. For investors seeking excitement, look elsewhere. For those seeking compound returns over decades, McCormick delivers.

The workforce of 14,000 globally represents another transformation. Once concentrated in Baltimore, McCormick now operates technical centers in Shanghai, Singapore, and Mumbai. Food scientists in Poland collaborate with AI engineers in Maryland. Supply chain managers in Mexico coordinate with procurement teams in France. The company that started with one man and a horse-drawn wagon has become a complex global organism, sensing flavor trends across continents and responding with precision.

VIII. Business Model & Competitive Moats

Two-Segment Strategy

McCormick's business architecture resembles a barbell—two massive weights connected by shared capabilities. The Consumer segment ($4.1 billion in 2024 revenue) faces shoppers directly: the iconic red-cap bottles in grocery aisles, Old Bay at seafood counters, Frank's RedHot in condiment sections. The Flavor Solutions segment ($2.6 billion) operates invisibly, supplying the seasoning in McDonald's burgers, the coating on KFC chicken, the flavor in Campbell's soups.

This dual structure creates resilience. When restaurants shuttered during COVID, retail sales surged. When inflation squeezed consumer budgets, quick-service restaurants—and their need for consistent flavoring—thrived. Geographic diversity compounds this stability: Asian markets accelerate while European ones mature, emerging economies discover packaged spices as developed ones premiumize.

The segments share more than risk mitigation—they create competitive advantages neither could achieve alone. Consumer insights from retail sales inform industrial innovation. A hot sauce trend spotted in grocery stores becomes a flavor system sold to restaurant chains. Industrial relationships provide scale economies in procurement that benefit consumer products. The Vietnamese cinnamon McCormick sources for Cinnabon can be packaged for holiday bakers.

The Power of Distribution

Walk into any American supermarket and witness McCormick's true moat: shelf space. The spice aisle isn't just dominated by McCormick—it's essentially designed by them. The company pioneered the gravity-feed spice rack system in the 1960s, providing the fixtures free to retailers in exchange for premier positioning. Today's versions include LED lighting, digital price tags, and inventory management systems that create switching costs retailers won't pay.

The breadth of McCormick's portfolio enables unique leverage. Retailers need Old Bay for Maryland customers, Zatarain's for Louisiana markets, and basic black pepper for everyone. Competitors offering single products or limited lines can't match this must-stock portfolio. McCormick's sales representatives don't just take orders—they manage entire categories, analyzing movement data, optimizing assortments, and essentially becoming outsourced category managers for overwhelmed retailers.

In foodservice, distribution takes different forms but remains equally powerful. McCormick maintains dedicated culinary teams that work with chain restaurants on menu development. When Chipotle wanted a signature honey vinaigrette, McCormick created it. When Subway needed a garlic aioli that wouldn't separate, McCormick formulated it. These relationships, built over decades, create dependencies that transcend simple supplier relationships.

Brand Portfolio Strategy

McCormick's brand strategy reflects sophisticated market segmentation. The flagship McCormick brand anchors the mainstream: reliable, affordable, ubiquitous. But around this core orbits a constellation of specialized brands, each owning specific usage occasions or regional preferences.

Lawry's dominates steakhouse seasonings—a $400 million category McCormick essentially created. Old Bay owns seafood seasoning so completely that competing products position themselves as "Old Bay alternatives." Zatarain's provides authentic New Orleans flavors that McCormick couldn't credibly deliver. Thai Kitchen and Simply Asia capture the growing Asian cuisine segment without diluting McCormick's mainstream positioning.

The hot sauce portfolio exemplifies this precision. Frank's RedHot owns Buffalo sauce applications—wings, dips, pizza. Cholula targets Mexican cuisine and breakfast applications. The core McCormick brand offers basic hot sauce for price-conscious consumers. Each brand maintains distinct flavor profiles, heat levels, and usage occasions, allowing McCormick to capture maximum shelf space without cannibalization.

Recent acquisitions follow this logic. Kitchen Basics wasn't about entering the broth category—it was about owning the premium, culinary-inspired segment. Stubb's BBQ wasn't about another sauce—it was about authentic, craft positioning in barbecue. Each acquisition fills a specific gap in McCormick's flavor map, creating a portfolio that addresses every conceivable consumer need.

Innovation & R&D

McCormick's research extends far beyond mixing spices. The company operates 24 technical innovation centers globally, employing over 500 scientists, engineers, and culinary professionals. These aren't just test kitchens—they're sophisticated laboratories equipped with gas chromatographs for analyzing volatile compounds, texture analyzers for measuring mouthfeel, and sensory evaluation facilities for quantifying consumer perception.

The innovation process begins with trend identification. McCormick's proprietary Flavor Forecast, published annually since 2000, has predicted the rise of sriracha, the emergence of Everything Bagel seasoning, and the current Nashville Hot phenomenon with uncanny accuracy. This isn't guesswork—it's systematic analysis of restaurant menus, social media mentions, ethnic demographic shifts, and travel patterns.

Product development follows a stage-gate process refined over decades. Concepts undergo sensory optimization using response surface methodology—a statistical technique that identifies ideal flavor balances. Shelf stability testing subjects products to accelerated aging, ensuring that oregano in Phoenix maintains potency as long as oregano in Seattle. Manufacturing trials verify that products can be produced consistently across multiple facilities.

But innovation increasingly means solving customer problems, not just creating flavors. When food manufacturers face sodium reduction mandates, McCormick develops flavor systems that maintain taste perception despite lower salt content. When plant-based meat alternatives struggle with authentic flavors, McCormick creates complex seasoning blends that trigger carnivorous satisfaction. When restaurants need globally inspired limited-time offers, McCormick provides turnkey flavor solutions with guaranteed supply chains.

The AI partnership with IBM represents innovation's next frontier. Machine learning models predict flavor combinations humans wouldn't conceive—like the ONE platform's Tuscan Chicken seasoning that paired sun-dried tomato with unexpected cardamom notes. Natural language processing analyzes food blogs, identifying emerging flavor vocabularies before they reach mainstream consciousness. Computer vision systems evaluate color consistency in paprika shipments more accurately than human inspectors.

IX. Financial Analysis & Investment Case

Growth Drivers

The millennial palate revolution drives McCormick's most powerful secular trend. This generation, raised on sriracha and travel, views bold flavors not as exotic but essential. They don't just tolerate heat—they chase it, turning hot sauce into a $2 billion category growing 8% annually. McCormick owns the two largest brands (Frank's and Cholula) and supplies private label to most others.

International expansion offers decades of growth runway. In China, where McCormick entered in 1989, compound annual growth exceeds 15% as urbanization creates demand for convenient flavor solutions. India's spice market, traditionally dominated by local mills and wet markets, slowly shifts toward packaged products as food safety concerns mount. McCormick's joint ventures and acquisitions position it to capture this transition.

The premiumization trend transcends geography. Consumers who once bought generic black pepper now select Tellicherry or Lampong varieties. Basic chili powder gives way to specific chile blends—ancho, guajillo, chipotle. McCormick's clear bottles and product education enable this trading up, expanding revenue per customer even when volume remains flat.

The food-away-from-home recovery provides near-term catalysts. Restaurant traffic hasn't fully recovered to 2019 levels, suggesting pent-up demand. As dining normalizes, McCormick's Flavor Solutions segment benefits disproportionately—restaurants require consistent flavor profiles that only industrial suppliers can guarantee.

Margin Story

McCormick's margin expansion story unfolds across multiple vectors. The Consumer segment's $740 million operating income (18% margin) has room for improvement as price realization catches up with input cost inflation. Private label competition limits pricing power in basic spices, but premium products and brand extensions face less resistance.

The Flavor Solutions segment tells a more compelling story: $330 million operating income growing 14% annually with expanding margins. Industrial customers value consistency and innovation over lowest cost. A flavor system that enables 30% sodium reduction or successful plant-based formulation commands premium pricing. As the segment shifts toward more value-added products, margins should approach 15% over time.

The Comprehensive Continuous Improvement (CCI) program, launched in 2016, targets $450 million in cost savings by 2025. Unlike slash-and-burn restructuring, CCI focuses on sustainable efficiency: automating packaging lines, optimizing transportation networks, consolidating procurement. Early results exceeded targets, funding growth investments while protecting margins.

The RB Foods acquisition, initially margin-dilutive, now contributes accretively. Frank's and French's operate with 30%+ EBITDA margins, pulling up McCormick's consolidated performance. Synergy realization exceeded guidance: procurement savings from combined scale, distribution efficiency from fuller trucks, innovation leverage from shared R&D. The deal that analysts called overpriced now looks prescient.

Capital Allocation

McCormick's capital allocation reflects remarkable discipline for a company with acquisition appetite. The dividend, increased for 39 consecutive years, consumes roughly $350 million annually—a 2% yield that won't excite income investors but demonstrates commitment to shareholder returns. The board targets a 50% payout ratio, balancing return of capital with growth investment.

M&A remains the primary growth vehicle, but with selectivity. Management targets 4-8% annual sales growth, half from organic expansion and half from acquisitions. The hurdle rate for deals: mid-teens return on invested capital within three years. This discipline means walking away from auctions, accepting slower growth rather than overpaying.

Share repurchases occur opportunistically rather than systematically. McCormick bought back $600 million in shares during the 2020 market dislocation, retiring 4% of shares outstanding at attractive prices. But repurchases pause when acquisition opportunities emerge or valuations extend. This flexibility preserves dry powder for strategic moves.

The balance sheet remains conservative despite acquisition activity. Net debt of $4.5 billion equals 2.5x EBITDA—comfortable for a stable consumer products company. McCormick maintains investment-grade ratings (BBB+ from S&P), ensuring access to capital markets. The dual-class share structure, with the McCormick family controlling 70% of voting rights, enables long-term thinking without activist interference.

Risks & Challenges

Private label competition intensifies across categories. Retailers, squeezed by e-commerce and seeking margin improvement, aggressively promote store brands. McCormick's response—innovation, premiumization, brand building—works but requires constant investment. In commoditized categories like black pepper, market share slowly erodes.

Input cost inflation presents ongoing challenges. Vanilla prices can triple based on Madagascar weather. Pepper availability depends on Vietnamese politics. Transportation costs spiked 40% post-pandemic. While McCormick eventually passes costs to customers, timing lags pressure margins. The company's size provides some insulation—smaller competitors lack scale to hedge effectively—but volatility remains.

Integration complexity multiplies with each acquisition. McCormick now operates dozens of manufacturing facilities across six continents, each with distinct regulatory requirements, labor dynamics, and infrastructure challenges. The company has integrated successfully so far, but each deal adds operational complexity that could eventually overwhelm management capacity.

Consumer packaged goods face structural headwinds. E-commerce disintermediates traditional retail relationships. Direct-to-consumer brands cherry-pick profitable niches. Meal kit services bundle their own seasonings. Young consumers show less brand loyalty than previous generations. McCormick must constantly evolve to remain relevant.

X. Lessons & Legacy

The Power of Patient Capital

McCormick's 135-year journey from Baltimore cellar to global giant illustrates compound returns' extraordinary power. A hypothetical $1,000 investment when McCormick went public in 1955 would be worth over $3 million today—assuming dividend reinvestment. That's 15% annual returns across seven decades, through multiple recessions, wars, and pandemics.

This performance didn't require genius stock-picking or perfect timing. It required patience—holding through the 1970s stagflation when spice consumption plummeted, the 1982 accounting scandal that nearly destroyed credibility, the 2008 financial crisis when credit markets froze. Investors who sold during any crisis missed the subsequent recovery that lifted McCormick to new heights.

The dual-class structure that gives the McCormick family control despite owning only 20% of economic interest draws governance criticism. But it also enables genuinely long-term thinking. While competitors optimize quarterly earnings, McCormick invests in 10-year brand-building campaigns. While activists demand immediate margin expansion, McCormick accepts dilution from transformational acquisitions.

M&A Excellence

From F.G. Emmett in 1896 to RB Foods in 2017, McCormick has completed over 50 acquisitions. The company's M&A playbook, refined over a century, offers lessons:

First, buy brands, not just assets. Every major McCormick acquisition brought established brand equity: Schilling's West Coast heritage, Old Bay's Baltimore authenticity, Frank's RedHot's Buffalo legacy. Building brands from scratch takes decades; buying them accelerates growth immediately.

Second, maintain local identity while leveraging global scale. Ducros remains French in France, Kamis stays Polish in Poland, but both benefit from McCormick's procurement power and innovation capabilities. This balance—local face, global muscle—enables premium pricing and cost efficiency simultaneously.

Third, pay for strategic value, not just financial metrics. The RB Foods price (7x revenue) looked insane on spreadsheets but made strategic sense. Controlling Frank's RedHot and French's Mustard created category dominance that competitors couldn't replicate regardless of spending.

Innovation Paradox

McCormick sells humanity's oldest traded commodities—spices that Marco Polo would recognize. Yet the company embraces cutting-edge technology: AI-developed flavors, blockchain supply chain tracking, robotic manufacturing. This paradox—ancient products, modern methods—defines McCormick's competitive advantage.

Innovation at McCormick doesn't mean disruption. The company has never created a category-killing product that obsoleted existing offerings. Instead, innovation means constant incremental improvement: clearer bottles that display spices better, flip-top caps that preserve freshness longer, grinder attachments that release volatile oils immediately before use.

The AI partnership exemplifies this philosophy. McCormick doesn't use artificial intelligence to replace human creativity but to augment it. Food scientists still develop flavors; AI helps them identify combinations they wouldn't otherwise consider. Culinary experts still create recipes; machine learning helps predict which ones consumers will embrace.

Corporate Culture

The Multiple Management system Charles P. McCormick introduced in 1932 still influences company culture. Modern versions include innovation tournaments where employee ideas compete for funding, reverse mentoring programs where younger staff teach digital skills to executives, and "flavor councils" where workers from different functions collaborate on new products.

This participatory culture creates unusual employee loyalty. McCormick's turnover rate runs half the industry average. Many employees build entire careers within the company, accumulating deep expertise that can't be easily replaced. The headquarters café still serves employee recipes, maintaining connection between workers and products they produce.

"Bring the Joy of Flavor to Life"—McCormick's mission statement—sounds like corporate pablum. But employees genuinely embrace it. Product developers describe their work as "democratizing flavor," making restaurant-quality tastes accessible to home cooks. Supply chain managers talk about "protecting flavor integrity" from farm to table. This shared purpose, cultivated over generations, creates organizational cohesion that transcends individual roles.

XI. Recent News & Future Outlook

The spice industry stands at an inflection point. Climate change threatens traditional growing regions—Vietnamese pepper farms face unprecedented droughts, Madagascar vanilla suffers from cyclone intensity, Indian turmeric yields decline. McCormick's response involves both adaptation and innovation: partnering with farmers on sustainable practices, developing heat-resistant varietals, and exploring alternative sources like cellular agriculture for vanilla.

Recent quarterly earnings reflect these transitions. Volume declines in developed markets mask mix improvement toward premium products. The Flavor Solutions segment's double-digit growth validates the industrial strategy. China recovery post-Zero-COVID provides tailwinds. But margin pressure from transportation and labor costs persists, requiring careful price management.

The competitive landscape intensifies. Unilever's acquisition of The Vegetarian Butcher signals major players entering McCormick's flavor solutions space. Private equity consolidation of regional spice companies creates new competitors with financial backing. Amazon's private label expansion includes spices and seasonings, threatening traditional retail relationships.

Yet McCormick's response demonstrates confidence. The company increased R&D spending 20% in 2024, focusing on plant-based flavor systems and health-conscious formulations. New distribution partnerships with meal kit services and ghost kitchens expand reach beyond traditional channels. The board authorized $2 billion for acquisitions over the next three years, suggesting major moves ahead.

Final Analysis: The Flavor of Patient Prosperity

McCormick & Company presents a paradox for modern investors. In an era obsessed with disruption, it represents continuity. While markets chase the next breakthrough, McCormick profits from selling the same black pepper and cinnamon humans have traded for millennia. The company that began with Willoughby McCormick's horse-drawn wagon now uses artificial intelligence, but the core mission—making food taste better—remains unchanged.

The investment case rests not on explosive growth but on competitive position. McCormick doesn't need to grow rapidly when it already controls 20% of the global spice market and owns most major brands consumers recognize. The company doesn't need dramatic margin expansion when it already generates 15% operating margins selling commodities. It doesn't need to transform when its transformation—from regional spice merchant to global flavor solutions provider—already succeeded.

For investors seeking excitement, McCormick disappoints. The stock rarely moves dramatically. Headlines seldom feature the company except during acquisitions. Analysts maintain neutral ratings, neither wildly bullish nor deeply bearish. The business plods along, raising prices slightly faster than inflation, acquiring complementary brands, returning cash to shareholders.

But this perceived tedium masks extraordinary wealth creation. McCormick has delivered positive returns in 34 of the last 40 years. The dividend, increased for 39 consecutive years, compounds wealth independent of stock appreciation. The company survived two world wars, the Great Depression, dozens of recessions, and a global pandemic not just intact but stronger. Few businesses can make such claims.

The future promises challenges—climate change, input inflation, changing consumer preferences, technological disruption. But McCormick has adapted for 135 years. The company that once sold root beer door-to-door now develops AI-powered flavor systems for plant-based meat. The business that started in a Baltimore cellar now operates innovation centers globally. The brand that began with "Make the Best—Someone Will Buy It" now owns virtually every spice brand someone might buy.

In the end, McCormick's story isn't about spices—it's about resilience. It's about building competitive advantages so durable they survive generational transitions. It's about creating shareholder value not through financial engineering but through operational excellence. It's about the radical idea that selling quality products at fair prices, treating employees as partners, and thinking in decades rather than quarters can build enduring prosperity.

The spice trade created and destroyed empires, launched voyages of discovery, and shaped global commerce for millennia. McCormick didn't invent this trade—it simply perfected it for the modern age. And in that perfection lies a lesson for investors: sometimes the best opportunities aren't in disrupting industries but in dominating them, not in creating new categories but in consolidating existing ones, not in explosive growth but in patient compound returns.

As Willoughby McCormick understood in 1889, and as the company still proves today: Make the best, and someone will buy it. For 135 years, someone has. For decades to come, someone will.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube