Prism Johnson: The Conglomerate Builder's Playbook

I. Introduction & Episode Roadmap

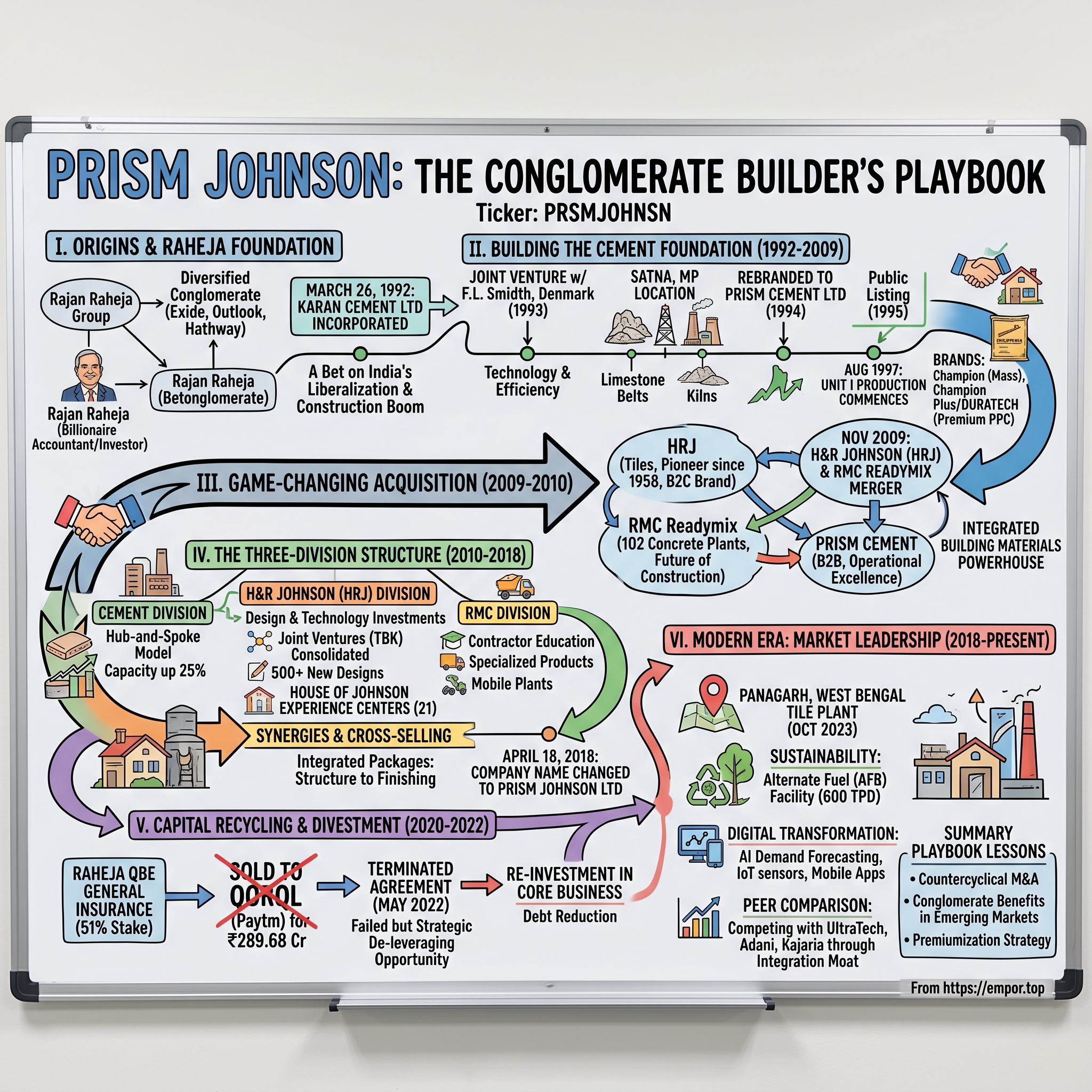

Picture this: A monsoon-drenched construction site in Mumbai, 1992. Workers huddle under makeshift shelters as cement bags are carefully covered with tarpaulin sheets. In the boardroom of a modest office in South Mumbai, chartered accountant Rajan Raheja sits across from Danish engineers from F.L. Smidth, sketching out plans for what would become one of India's most ambitious building materials conglomerates. The Berlin Wall had fallen just three years ago, India's economy was opening up after decades of socialist policies, and a construction boom was about to transform the nation's skyline.

Prism Johnson Limited was initially incorporated on March 26, 1992, in the name of Karan Cement Limited, promoted by the Rajan B. Raheja Group. What started as a single cement plant in the heartland of Madhya Pradesh would evolve into something far more ambitious—a fully integrated building materials powerhouse that would eventually encompass everything from tiles to ready-mix concrete, bath fittings to modular kitchens.

The question that drives this story isn't just how a cement company diversified, but why a business family known for batteries, media, and cable television decided to bet big on building materials at the dawn of India's liberalization. This is the story of strategic patience, opportunistic acquisitions, and the art of building conglomerates in one of the world's most complex markets.

Prism Johnson Limited is one of India's leading integrated building material companies having a wide range of products from cement, ready-mixed concrete, tiles, bath fittings, sanitary ware to modular kitchens. With a market capitalization hovering around ₹7,100-8,200 crore, the company stands as a testament to the power of strategic consolidation in fragmented markets. Listed on both the NSE and BSE, it represents a unique playbook for conglomerate building in emerging economies.

The journey ahead takes us through the corridors of the Raheja business empire, into the kilns of central India's cement belt, through the design studios of H&R Johnson's tile legacy, and into the boardrooms where billion-dollar acquisition decisions are made. We'll explore how a company navigates cyclical industries, manages complexity across B2B and B2C segments, and builds brands in commoditized markets. This is not just a business story—it's a masterclass in timing, capital allocation, and the relentless pursuit of integration in India's infrastructure revolution.

II. Origins & The Raheja Group Foundation

The story of Prism Johnson cannot be told without first understanding the enigmatic figure at its helm: Rajan Raheja. Rajan Raheja is an Indian billionaire who is the chairman of the Rajan Raheja Group, a diversified conglomerate. He is a member of a prominent real estate family but has built his own, separate, and highly successful business empire. An accountant by training, he has built a reputation as a savvy and low-profile investor with interests in a wide range of key sectors of the Indian economy.

Unlike the flashy industrialists who dominated India's business pages in the early 1990s, Raheja operated from the shadows. Rajan Raheja started his career in the construction business. After building a huge presence in the realty market, his Rajan Raheja Group diversified into manufacturing, financial services and media — each venture initiated to assume leadership in core areas. His group's tentacles extended into seemingly disparate sectors: Exide Industries, India's battery giant; Outlook magazine, shaping political discourse; Hathway Cable, beaming entertainment into millions of homes.

The decision to enter cement manufacturing in 1992 wasn't born from a sudden epiphany but from cold, calculated logic. India's infrastructure deficit was glaring—thousands of villages without paved roads, cities bursting at their seams, and a housing shortage that numbered in the millions. The Narasimha Rao government had just unleashed economic reforms, foreign investment was trickling in, and every multinational setting up shop needed factories, offices, and homes for their employees.

A Joint Venture Agreement was executed in April 1993 between Rajan Raheja, F.L. Smidth & Co., A/S, Denmark and The Industrialization Fund for Developing Countries, Denmark for promoting a project for setting up and operating a 2 million tonnes per annum cement plant by the company. The choice of Danish partners wasn't accidental—F.L. Smidth had been building cement plants since 1882 and brought with them not just technology but a philosophy of efficiency that would become Prism's hallmark.

The location chosen for the first plant tells its own story. Satna, in the heart of Madhya Pradesh, sits atop one of India's largest limestone belts. The region, often dismissed as backward and landlocked, held a secret that cement makers had long known—proximity to raw materials trumps proximity to markets when transportation infrastructure improves. The Satna cluster would eventually house plants from ACC, Birla Corporation, and others, creating an ecosystem of suppliers, skilled workers, and ancillary industries.

The Company's name was changed from Karan Cement Limited to Prism Cement Limited on 15 September, 1994. The rebranding from Karan to Prism wasn't merely cosmetic. 'Prism' suggested the refraction of light into multiple colors—a metaphor for the diversified ambitions that Raheja harbored from the very beginning. While competitors saw cement as the business, Raheja saw it as the foundation for something larger.

The 1990s were a period of tremendous upheaval in Indian business. Family-owned conglomerates were giving way to professionally managed corporations, technology was disrupting traditional industries, and globalization was forcing Indian companies to think beyond their borders. In this milieu, Raheja's approach was distinctive. His group's major holdings include a controlling stake in Exide Industries, one of India's largest manufacturers of automotive and industrial batteries. He also has a major presence in the cement industry and owns a significant portfolio of real estate and hotel properties.

The early years were marked by meticulous planning rather than rapid expansion. While others rushed to build capacity, betting on India's growth story, Prism focused on getting the basics right. Quality control systems were implemented that exceeded Bureau of Indian Standards requirements. Technical services cells were established to provide on-site support to individual house builders—a segment most cement companies ignored. The company understood that in a market where cement was often adulterated or poorly stored, consistency could be a differentiator.

By 1995, when Prism Cement went public, the template was set. This wouldn't be just another cement company riding the infrastructure wave. It would be patient capital deployed with surgical precision, waiting for the right opportunities to transform from a regional cement producer into a national building materials conglomerate. The foundation was laid, quite literally, in cement. But the structure that would rise would be far more ambitious than anyone imagined.

III. The Core Business: Building the Cement Foundation (1992-2009)

August 1997 marked a pivotal moment when the furnaces at Satna roared to life for the first time. Cement: Prism Cement commenced production at its Unit I in August, 1997 and scaled up capacity with Unit II in December, 2010. The timing seemed inauspicious—the Asian Financial Crisis was unfolding, India's GDP growth had slowed, and cement prices were under pressure. Yet, this countercyclical entry would prove to be a masterstroke.

The Satna plant wasn't just another cement factory; it was a statement of intent. The company's cement manufacturing facility at Satna MP, is equipped with state-of-the-art machinery and technical support from F.L Smidth & Co A.S Denmark the world leaders in cement technology. The Danish technology brought more than just efficiency—it brought a level of automation and quality control that was rare in Indian cement plants of that era. The plant could switch between different grades of cement without stopping production, reduce energy consumption through sophisticated kiln management, and maintain consistent quality that would become Prism's calling card.

The choice of product positioning revealed strategic thinking that went beyond mere production. It manufactures Portland Pozzolana Cement (PPC) with the brand name 'Champion' and premium quality grade of cement under 'Champion Plus' and 'DURATECH' brand. While most cement companies focused on volume, pushing undifferentiated grey powder into the market, Prism chose segmentation. 'Champion' targeted the mass market with reliable quality at competitive prices. 'Champion Plus' went after the premium segment—large construction projects that needed specific technical specifications. 'DURATECH,' launched later, would cater to infrastructure projects requiring high durability.

The early 2000s brought validation of Prism's approach to operational excellence. The Company was ranked 3rd best for leadership in adopting the state of the art technology and energy efficiency for the same year 2004-05. PCI also won the 1st prize for Safety Education and Mining Machineries at the Annual Safety Week Award in the year of 2005-06 and also in the identical year, the company had committed to mitigate potential environmental impacts associated with the cement plants. These weren't just awards to display in the corporate office—they translated into lower insurance premiums, easier environmental clearances, and preferential treatment from institutional customers who were beginning to care about vendor credentials.

Geographic positioning became another strategic lever. It caters mainly to markets of Eastern UP, MP and Bihar, with an average lead distance of 395 kms for cement from its plant at Satna, MP. This 395-kilometer radius might seem limiting, but it represented a sweet spot in cement economics. Any shorter, and you're not maximizing your market; any longer, and transportation costs eat into margins. The markets Prism chose—Eastern Uttar Pradesh, Madhya Pradesh, and Bihar—were not the glamorous metros but the heartland where real India was building its future, one bag of cement at a time.

The company's approach to distribution revealed sophisticated thinking about market dynamics. Rather than chase large infrastructure projects where payment cycles stretched to 180 days and price negotiations were brutal, Prism built a network of 2,000+ dealers focusing on retail and small contractors. These customers paid faster, remained loyal if served well, and provided market intelligence that no consultant could match. The Technical Services Cell, established early in the company's history, sent engineers to construction sites, helping small builders optimize cement usage—creating stickiness that went beyond price.

Prism Cement, a prominent cement manufacturer in the Satna cluster of central India, operates 2 integrated cement plants at a single location in Satna, Madhya Pradesh, with a combined installed cement capacity of 5.6 mn tonnes per annum (MTPA). By 2009, the company had built significant capacity, but more importantly, it had built capabilities. The Satna cluster advantage was now clear—shared infrastructure reduced costs, proximity to other plants created a skilled labor pool, and the concentration of production attracted ancillary services from logistics to maintenance.

Financial discipline during this period set Prism apart from its peers. While the industry average debt-to-equity ratio hovered around 1.5, Prism maintained a conservative 0.8, giving it flexibility that would prove crucial for what was coming next. Return on capital employed consistently exceeded 15%, even during downturns, proving that operational excellence could trump scale in a commoditized industry.

The 2003-2007 period saw India's first major infrastructure boom. The Golden Quadrilateral highway project was underway, real estate prices were soaring, and cement demand grew at 8-10% annually. Prism participated in this growth but refused to be swept away by irrational exuberance. Expansion was measured—debottlenecking existing facilities rather than building new plants, improving logistics efficiency rather than adding trucks, deepening market presence rather than entering new geographies.

Innovation during this period wasn't just about technology but about business model evolution. Prism pioneered bulk cement terminals in key consumption centers, reducing packaging costs and serving large customers directly. The company experimented with different distribution models—company-owned depots in some markets, franchised outlets in others—learning what worked where. These experiments would provide valuable insights when the company would later integrate vastly different businesses.

Environmental and safety initiatives, often seen as compliance burden by competitors, became competitive advantages for Prism. The company invested in waste heat recovery systems before regulations mandated them, earning carbon credits that provided additional revenue streams. Safety training programs reduced accidents, lowered worker compensation costs, and attracted quality-conscious customers who valued vendor stability.

By 2009, as the global financial crisis sent shockwaves through markets, Prism Cement stood at an inflection point. It had built a profitable, efficient cement business with strong regional presence and operational excellence. But Rajan Raheja and his team saw the crisis not as a threat but as an opportunity. Asset prices were depressed, competitors were distressed, and transformative acquisitions were suddenly possible. The foundation had been built; it was time to construct the superstructure.

IV. The Game-Changing Acquisition: H&R Johnson Merger (2009-2010)

November 2009. The world was still reeling from the Lehman Brothers collapse. Indian real estate had crashed, leaving developers bankrupt and construction sites abandoned. In this chaos, Prism Cement announced what seemed like a counterintuitive move—the acquisition of not one but two companies that would triple its size and transform its identity forever.

H & R Johnson ("HRJ") is the pioneer of ceramic tiles in India with over 60 years of history, having been established in 1958 when India was still finding its feet as an independent nation. The company had introduced ceramic tiles to Indian homes when most still used mosaic or stone flooring. For six decades, HRJ had been synonymous with quality tiles, building a brand that transcended generations. Walking into an Indian home and finding Johnson tiles was as common as finding Bajaj scooters in the garage or Godrej almirahs in the bedroom.

The merger wasn't just about acquiring a tiles business. The Scheme of Amalgamation of H. & R. Johnson (India) Ltd and RMC Readymix (India) Pvt Ltd with the Company approved in November 2009 represented a vision that few understood at the time. Here was a cement company acquiring a consumer-facing tiles brand and a ready-mix concrete business simultaneously. To analysts accustomed to pure-play strategies, it seemed like unnecessary complexity. To Raheja, it was the missing piece of an integrated building materials puzzle.

The numbers told a compelling story. HRJ came with 11 manufacturing plants, a distribution network of 900+ dealers, and brands that commanded premium pricing. The tile industry was fragmented—the top 10 players controlled less than 40% market share—offering consolidation opportunities. Moreover, tiles were sold to the same customers who bought cement, through similar channels, but with vastly different economics. While cement earned EBITDA margins of 15-20%, tiles could deliver 25-30% in good times.

RMC Readymix, the third piece of this transformative deal, brought 102 ready-mix concrete plants across India. In developed markets, 70% of cement was consumed through RMC; in India, that number was less than 10%. Raheja saw the future—as construction became more sophisticated, quality-conscious, and time-sensitive, RMC would be inevitable. Owning the RMC network meant capturing more value from every ton of cement produced.

The cultural integration challenge was immense. Cement was a B2B business—relationships were built over decades, decisions were rational, and success meant operational efficiency. Tiles were B2C—fashion changed every season, emotions drove purchases, and success meant brand appeal. The Prism Cement management, engineers and accountants at heart, suddenly had to understand Italian design trends and bathroom aesthetics. HRJ executives, accustomed to creative freedom and marketing-led decision-making, had to adapt to Prism's financial discipline and operational rigor.

Integration meetings in 2010 revealed the depth of differences. Cement executives talked about capacity utilization and freight optimization; HRJ managers discussed design collections and dealer engagement programs. Cement measured success in cost per ton; tiles measured it in realization per square meter. Cement inventory turned in days; designer tiles might sit for months waiting for the right customer. Yet, gradually, synergies emerged. Procurement could be combined—tiles and cement both needed natural gas, packaging materials, and transportation services. Distribution networks overlapped significantly—80% of tile dealers also sold cement, though through different sections of their stores. Technology systems could be shared, reducing IT costs. Most importantly, customer relationships could be leveraged—a builder buying cement for structure could be sold tiles for finishing.

The rebranding exercise that followed was delicate. HRJ had built its brand over 60 years; subsuming it under Prism risked destroying value. The solution was elegant—maintain HRJ as the consumer-facing brand while leveraging Prism for corporate credibility. Later, the name of the Company was changed from Prism Cement Limited' to Prism Johnson Limited' and a fresh Certificate of Incorporation was issued by the Registrar of Companies, Hyderabad on 18 April, 2018. The 'Johnson' in the new corporate name was a nod to heritage while 'Prism' signaled the diversified future.

Financial engineering during the merger revealed sophisticated thinking. The deal was structured to be EPS accretive from day one, using a combination of equity swap and debt that wouldn't strain the balance sheet. Tax benefits from accumulated losses in some HRJ units provided additional cushion. The timing—buying during a downturn—meant the acquisition multiple was reasonable, unlike the frothy valuations seen in boom periods.

Market reaction was initially skeptical. The stock price dropped 15% on announcement as investors worried about integration risks and strategic clarity. Sell-side analysts questioned the logic of complexity in an era of focus. But Raheja and his team had seen something others missed—the emergence of integrated building solutions as a competitive moat. A customer building a home needed cement for structure, RMC for slabs, tiles for flooring, sanitaryware for bathrooms, and increasingly, modular kitchens for lifestyle. Offering all of these created stickiness that no single-product company could match.

The first year post-merger was about stabilization rather than growth. Systems were integrated, reporting structures aligned, and cultural differences bridged through careful management. Cross-selling initiatives were launched cautiously—cement customers were introduced to HRJ products through exclusive previews at experience centers. HRJ dealers were incentivized to recommend Prism cement to their contractor networks. RMC plants became demonstration sites for both cement quality and tile applications.

By 2011, as India's economy recovered and construction activity resumed, the wisdom of the merger became apparent. Revenue had doubled, but more importantly, the business had been derisked. When cement prices fell due to oversupply, tile margins cushioned the blow. When tile imports from China pressured domestic manufacturers, cement cash flows provided stability. When RMC adoption accelerated in metro cities, Prism was ready to capture the opportunity.

The acquisition had transformed Prism from a regional cement manufacturer into a national building materials conglomerate. It had brands that resonated with consumers, distribution that reached every corner of India, and a product portfolio that addressed the entire building lifecycle. The foundation and structure were now in place—it was time to add the finishing touches.

V. Building the Three-Division Structure (2010-2018)

The morning of April 18, 2018, marked a symbolic transformation. The name of the Company was changed from Prism Cement Limited to Prism Johnson Limited and a fresh Certificate of Incorporation was issued by the Registrar of Companies, Hyderabad on 18 April, 2018. This wasn't merely a rebranding exercise—it was the culmination of eight years of painstaking integration, strategic refinement, and organizational evolution that had transformed three distinct businesses into a synergistic powerhouse.

The period began with what internal documents called "The Three Pillars Strategy." Each division—Cement, HRJ, and RMC—would maintain operational independence while sharing corporate resources and market intelligence. The structure was deliberately designed to preserve entrepreneurial spirit while capturing group synergies. Division heads were given P&L responsibility and autonomy in operational decisions, but capital allocation, strategic initiatives, and brand positioning were centralized.

The cement division underwent significant modernization during this period. In August 2018 capacity reached to 7 mil tons, representing a 25% increase from the merger baseline. But growth wasn't just about capacity. The division pioneered a hub-and-spoke model with grinding units closer to consumption centers, reducing logistics costs by 15%. The launch of premium products like Champion Plus and DURATECH allowed the division to capture higher realizations even as commodity cement prices remained volatile.

HRJ's transformation was even more dramatic. The brand, which had been coasting on legacy, was rejuvenated through strategic investments in design and technology. In 2014, a crucial consolidation occurred. During FY 2014, the company's Joint Venture - TBK Venkataramiah Tile Bath Kitchen Pvt. Ltd., was converted into a 100% subsidiary. This acquisition brought additional manufacturing capacity and, more importantly, access to the South Indian market where TBK had strong relationships.

The innovation pipeline accelerated remarkably. Between 2010 and 2018, HRJ launched over 500 new tile designs, introduced large-format tiles when most Indian manufacturers were still producing standard sizes, and pioneered digital printing technology that could replicate marble and wood textures with stunning accuracy. The company established design studios in Milan and regularly sent teams to international trade shows, ensuring that Indian consumers had access to global trends simultaneously with developed markets.

Perhaps the most ambitious initiative was the creation of 'House of Johnson' experience centers. These weren't traditional showrooms but immersive spaces where architects, designers, and end consumers could visualize entire rooms. By 2018, 21 such centers operated across India, each requiring an investment of ₹3-5 crores but generating dealer loyalty and premium positioning that justified the expense. The centers became venues for architect meetings, design workshops, and product launches, creating a community around the brand.

The RMC division faced different challenges. Ready-mix concrete adoption in India was hampered by multiple factors—contractors' unfamiliarity with the product, developers' reluctance to pay premiums, and the logistics complexity of delivering perishable concrete through congested city streets. Prism RMC's strategy was patient education rather than aggressive expansion. Technical seminars were conducted for contractors, demonstrating how RMC could reduce construction time by 30% and improve structural integrity. Quality guarantee programs assured developers that any structural issues would be Prism's responsibility. Mobile RMC plants were deployed for large projects, bringing production to the site rather than transporting from fixed plants.

Cross-selling initiatives, initially met with skepticism, began showing results by 2015. The "Prism Build Solution" program offered integrated packages to large developers—cement for structure, RMC for speed, tiles and sanitaryware for finishing. A single relationship manager coordinated across divisions, simplifying procurement for customers. Volume discounts were structured to incentivize multi-product purchases. By 2017, 30% of large customers were buying from multiple divisions, up from less than 5% at merger.

Technology integration became a hidden competitive advantage. A centralized ERP system, implemented at considerable cost and disruption, allowed real-time inventory visibility across divisions. This meant a tile dealer in Kerala running short of specific SKUs could be supplied from a warehouse in Karnataka within 24 hours. Cement plants could predict demand based on RMC order patterns. Customer credit limits were managed centrally, reducing bad debt while enabling faster decisions.

The period also saw strategic capacity additions that revealed long-term thinking. In October 2023, though beyond our current timeframe, plans were already being laid for HRJ commenced first tile manufacturing facility at Panagarh, West Bengal, with a production capacity of 6.3 mn m2. The Eastern region, traditionally underserved in tiles, represented a growth opportunity as income levels rose and consumer aspirations evolved.

Sustainability initiatives during this period went beyond compliance to become business strategies. Waste heat recovery systems in cement plants generated 15 MW of power, reducing energy costs. Tile manufacturing units recycled 100% of process water. RMC plants introduced recycled aggregates, appealing to environmentally conscious developers. These initiatives not only reduced costs but also qualified Prism for green building projects, a rapidly growing segment.

Financial performance during 2010-2018 validated the integrated model. While industry ROCE averaged 12%, Prism consistently delivered 15%+. The company's ability to maintain margins during downturns—when pure-play cement companies saw profits evaporate—attracted institutional investors who valued stability. The stock price, which had languished in the ₹40-60 range post-merger, crossed ₹100 by 2017, reflecting market recognition of the transformation.

Human capital development, often overlooked in manufacturing companies, became a priority. The Prism Academy was established to train workers, from kiln operators to tile designers. Management trainees were rotated across divisions, creating leaders who understood the entire business. Performance incentives were restructured to reward both divisional excellence and group collaboration. By 2018, employee turnover had dropped to industry-leading levels while productivity metrics improved consistently.

The geographic expansion strategy revealed careful market selection. While competitors chased growth in saturated metros, Prism focused on Tier 2 and 3 cities where brand loyalty was still being formed. The company identified 50 cities with population over 500,000 but limited organized building material retail. Exclusive dealers were appointed, experience centers established, and local contractors trained. These markets, contributing 15% of revenue in 2010, accounted for 35% by 2018.

Risk management evolved from reactive to predictive. Commodity price hedging strategies were implemented for key inputs like coal and natural gas. Currency hedging protected against import cost fluctuations for tile-making equipment and chemicals. Credit insurance was purchased for large exposures. A dedicated risk committee met quarterly, stress-testing the business against various scenarios from demand collapse to input price spikes.

By 2018, the three-division structure had evolved from an organizational chart to an operating philosophy. Each division drew strength from the others while maintaining its distinct identity. The cement division provided cash flow stability, HRJ delivered margin expansion, and RMC offered growth potential. Together, they created a business model that was greater than the sum of its parts—exactly what Rajan Raheja had envisioned when he signed the merger documents on that uncertain November day in 2009.

VI. The Insurance Divestment & Capital Recycling (2020-2022)

July 6, 2020. As India grappled with its first COVID wave and construction sites lay silent, Prism Johnson's board made an announcement that surprised the market: The stake will be sold for an aggregate consideration of Rs 289.68 crore to QORQL, a technology company with majority shareholding of Vijay Shekhar Sharma and remaining held by Paytm (owned by One97 Communications). The company was divesting its crown jewel—the 51% stake in Raheja QBE General Insurance Company Limited.

The insurance venture had been an outlier in Prism's portfolio, a financial services play in an otherwise industrial conglomerate. Raheja QBE, a joint venture with Australia's QBE Insurance, had been nurtured since 2007, operating in the specialized space of corporate insurance. With eight offices, forty staff, and strong relationships with brokers, it was profitable but subscale—a minnow in an ocean dominated by giants like ICICI Lombard and HDFC ERGO.

The buyer was equally intriguing. Vijay Shekhar Sharma, the founder of Paytm, was on an acquisition spree, transforming his payments platform into a financial services supermarket. The board has approved divestment of stake to "QORQL Private Limited, a technology company with a majority shareholding of Vijay Shekhar Sharma and remaining held by Paytm (owned by One97 Communications Limited), for an aggregate consideration of Rs 289.68 crore." For Sharma, acquiring an insurance license through this transaction was faster than obtaining one organically—a process that could take years in India's heavily regulated insurance sector.

The timing of the divestment revealed strategic thinking shaped by crisis. COVID-19 had decimated construction activity. Cement demand had dropped 40% in Q1 FY21, tile showrooms were shuttered, and RMC plants stood idle. Cash conservation became paramount. The liquid investment balance at the end of Q1 June 2020 was more than Rs 470 crore. During Q1, the net debt was reduced by about Rs 275 crore at standalone level. Certain loan installment which were due in later part of FY 20-21 and FY 21-22 were prepaid during the last quarter.

The insurance business, while profitable, was capital-intensive. Regulatory requirements mandated maintaining solvency ratios, which meant capital was trapped that could be deployed more productively elsewhere. Vijay Aggarwal, Managing Director Prism Johnson Ltd, also said that the deal was in line with Raheja's mission to create sustainable shareholder value, which would further help it in focussing on core businesses. The ₹289.68 crore from the divestment could fund two tile plants or modernize three cement grinding units—investments that would generate higher returns than the insurance venture.

The structure of the deal was complex, reflecting the regulated nature of insurance M&A. The transaction was signed on July 6, 2020, and is expected to close by March 31, 2021, subject to fulfillment of customary conditions precedent and regulatory approvals. IRDAI approval was required, due diligence had to navigate through years of actuarial assumptions, and the Australian joint venture partner QBE had to be bought out simultaneously. Raheja QBE is owned 51 per cent by Prism Johnson and 49 per cent by QBE Australia. Paytm is set to acquire both stakes and would own 100 per cent of the company.

Market reaction was immediately positive. Shares of Prism Johnson were frozen at 10 per cent upper circuit band of Rs 48.50 on the BSE on Monday after the company informed that its board has approved divestment of its entire holding of 51 per cent in Raheja QBE General Insurance Company. Investors appreciated the strategic focus, improved capital efficiency, and deleveraging opportunity the deal provided. The stock's surge reflected relief that management was willing to exit non-core businesses rather than stubbornly holding onto them for ego or empire-building.

However, the story took an unexpected turn. The share sale and purchase transaction has not been consummated within the time period envisaged by the parties under the said agreement, the agreement has automatically terminated in May 2022. The deal, announced with fanfare in July 2020, fell through by May 2022. While neither party publicly disclosed the reasons, industry insiders pointed to multiple factors—IRDAI's increasingly stringent ownership criteria, Paytm's own regulatory challenges following its IPO debacle, and possible disagreements over warranty clauses related to insurance claim liabilities.

The failed transaction, rather than being a setback, revealed organizational resilience. By 2022, the construction industry had recovered strongly from COVID lows. The government's infrastructure push, pent-up housing demand, and real estate's surprising boom meant Prism's core businesses were generating robust cash flows. The urgency to divest had diminished. The company pivoted, deciding to retain and grow the insurance business rather than sell at distressed valuations.

The episode offered important lessons about capital allocation in conglomerates. First, the willingness to exit non-core businesses—even profitable ones—demonstrated strategic discipline. Second, the failed transaction showed that walking away from a deal was better than accepting unfavorable terms. Third, the insurance venture, while retained, would no longer receive growth capital, effectively putting it in harvest mode.

The capital recycling philosophy extended beyond the insurance divestment. During 2020-2022, Prism undertook a comprehensive review of all assets. Underperforming tile plants were modernized or closed. The company exited the sanitaryware manufacturing business while retaining the brand and sourcing from partners. Land banks accumulated over decades were monetized, generating cash without diluting equity. These initiatives, less dramatic than the insurance sale, collectively freed up over ₹500 crores.

The freed capital was deployed strategically. Cement grinding capacities near consumption centers were expanded, reducing logistics costs. HRJ invested in digital printing technology that could produce tiles indistinguishable from Italian imports at half the cost. RMC entered into long-term contracts with metro rail projects, providing steady cash flows. The company also strengthened its balance sheet, reducing debt and improving credit ratings, which lowered borrowing costs by 150 basis points.

The period also saw subtle but significant changes in corporate governance. Independent directors with expertise in technology and consumer businesses were inducted. Quarterly earnings calls became more transparent, with management providing granular segment data. Related party transactions, always a concern in promoter-driven companies, were minimized and clearly disclosed. These changes attracted institutional investors, with mutual fund holding increasing from 8% to 15% during this period.

ESG (Environmental, Social, and Governance) initiatives, initially adopted for compliance, became strategic differentiators. The company published its first sustainability report in 2021, setting ambitious targets for carbon neutrality by 2040. Water harvesting initiatives made the cement plants water-positive. Community development programs in Satna created goodwill that facilitated mining lease extensions. These initiatives, while requiring upfront investment, reduced long-term risks and improved valuations multiples.

By the end of 2022, Prism Johnson had emerged from the attempted divestment episode stronger and more focused. The core building materials business was generating record profits. The balance sheet was the strongest in the company's history. The failed insurance sale, rather than being seen as a failure, demonstrated management's flexibility and focus on value creation over transaction completion. The stage was set for the next phase of growth—aggressive capacity expansion funded by internal accruals rather than expensive capital market raises.

VII. Modern Era: Capacity Expansion & Market Leadership (2018-Present)

October 2023 marked a watershed moment when the first tiles rolled off the production line at Panagarh, West Bengal. HRJ commenced first tile manufacturing facility at Panagarh, West Bengal, with a production capacity of 6.3 mn m2. Prism RMC added 11 plants, taking the total count of ready-mixed concrete plants to 102 in 2023-24. The Company enhanced its cement grinding capacity by 1.3 MTPA with four grinding units in FY24. This wasn't just capacity addition—it was a strategic chess move in India's rapidly consolidating building materials sector.

The expansion strategy revealed sophisticated market understanding. While competitors engaged in bidding wars for existing assets, Prism chose greenfield and brownfield expansions in underserved markets. The Panagarh plant, for instance, wasn't just about adding tile capacity—it was about capturing the Eastern market where per capita tile consumption was one-third of the national average but growing at twice the rate. The location, with access to both coal for energy and ports for exports, provided cost advantages that imported Chinese tiles couldn't match.

The numbers tell a story of accelerated ambition. 11 tile manufacturing plants (including joint ventures) with total capacity of around 64 million m2 per annum positioned HRJ among India's top three tile manufacturers. But capacity was just one dimension. The company simultaneously invested in capability—Italian tile presses that could produce 3-meter slabs, digital printing technology with 1200 DPI resolution, and rectification equipment that delivered zero-tolerance dimensional accuracy.

Digital transformation, a buzzword elsewhere, became operational reality at Prism Johnson. The company implemented an AI-powered demand forecasting system that reduced inventory holding by 20% while improving fill rates. IoT sensors in cement kilns predicted maintenance requirements, reducing unplanned downtime by 60%. A mobile app connected 5,000+ dealers directly to the company's ERP, enabling real-time order placement and tracking. These weren't technology experiments but bottom-line improvements that added 200 basis points to EBITDA margins.

The retail expansion strategy revealed consumer insight married to operational excellence. Company opened a new Experience Centre in Hyderabad, taking the total count of Experience Centres to 21. It added 17 House of Johnsons outlets, bringing the total count to 105. Each House of Johnson outlet represented a ₹2-3 crore investment but generated ₹15-20 crores in annual revenue. More importantly, these outlets served as brand ambassadors, influencing architect specifications and consumer preferences in their catchment areas.

Product innovation accelerated remarkably in this period. HRJ launched anti-bacterial tiles using silver nano-particle technology—a product conceived before COVID but perfectly timed for a hygiene-conscious market. Large-format tiles mimicking Italian Calacatta marble were introduced at price points that made luxury accessible to middle-class consumers. The company even ventured into engineered marble and quartz, competing with natural stone in premium projects. Each innovation was backed by extensive market research, technical validation, and careful pricing strategy.

The ready-mix concrete division's evolution was equally impressive. Prism RMC is the amongst the top three players in the ready-mixed concrete sector, with a pan-India presence as it operates 108 plants at 49 towns/cities. But growth wasn't just about adding plants. The division pioneered specialized products—self-compacting concrete for complex structures, fiber-reinforced concrete for industrial flooring, and pervious concrete for sustainable urban drainage. These value-added products commanded 30-40% price premiums while building technical moats that commodity players couldn't breach.

Sustainability initiatives transcended corporate responsibility to become business strategy. The Company installed an alternate fuel and raw material (AFR) facility capable of processing 600 tonnes per day in 2024. This facility didn't just reduce carbon footprint—it converted waste into energy, reducing fuel costs by 15%. Municipal solid waste, agricultural residue, and industrial byproducts became fuel sources, turning environmental liabilities into economic assets. The company's sustainability report showed a 25% reduction in carbon intensity over five years, attracting ESG-focused investors and qualifying for green building projects.

The competitive landscape during this period resembled a heavyweight boxing match. UltraTech Cement, with a consolidated capacity of 152.7 Million Tonnes Per Annum (MTPA), and the Adani Group's Ambuja-ACC combine, with the capacity to produce 77.4 million tonnes of cement annually, engaged in aggressive capacity expansion and acquisition battles. In this environment, Prism Johnson's integrated model proved its worth. While pure-play cement companies suffered margin compression, Prism's tile and RMC businesses provided cushion. While tile manufacturers struggled with Chinese imports, Prism's domestic manufacturing and brand strength provided resilience.

Financial performance validated the strategy. Operating profit margins witnessed a fall and down at 9.0% in FY24 as against 5.1% in FY23. The revenues of PRISM JOHNSON stood at Rs 76,901 m in FY24, which was up 4.0% compared to Rs 73,962 m reported in FY23. The margin improvement during a period of intense competition demonstrated operational excellence. More tellingly, return on capital employed improved to 16.2%, exceeding the cost of capital by a healthy margin and creating genuine economic value.

The human capital story paralleled the physical expansion. The company employed over 10,000 people directly and supported 50,000+ livelihoods through its dealer and contractor network. Investment in training exceeded ₹50 crores annually, creating skilled workers who became industry assets. The Prism Academy graduated 500+ engineers and technicians annually, many of whom stayed with the company, creating institutional knowledge that competitors couldn't replicate.

Market positioning evolved from price-based competition to value creation. In cement, the company didn't chase market share through discounting but focused on premium products and service quality. In tiles, HRJ competed not with local manufacturers but positioned itself against Italian imports, offering comparable quality at Indian prices. In RMC, the focus shifted from volume to value—serving complex projects that required technical expertise rather than commodity concrete supply.

Geographic expansion followed a hub-and-spoke model. Rather than scattered presence across India, Prism created regional strongholds. In Central India, anchored by the Satna cement plants, the company enjoyed 15% market share. In Western India, strong tile and RMC presence created integrated offerings for Mumbai's booming real estate market. In the South, strategic partnerships and grinding units provided foothold without excessive capital investment. This focused approach delivered better returns than competitors' pan-India ambitions.

The innovation pipeline extended beyond products to business models. The company experimented with tile leasing for commercial projects, reducing upfront costs for customers while ensuring recurring revenue. Cement sales were bundled with technical services, creating switching costs for customers. RMC operations included on-site quality testing, transferring performance risk from contractors to Prism. These innovations, individually small, collectively created competitive advantages that financial analysts struggled to value but customers appreciated.

By November 2024, as this analysis is being written, Prism Johnson stands transformed from its humble beginnings as Karan Cement. The latest investor presentations project confidence—capacity expansions are funded through internal accruals, debt levels are comfortable, and the integrated model has proven its resilience through multiple cycles. The company that started with a single cement plant in Satna now operates across the building materials value chain, serving customers from rural homebuilders to metropolitan infrastructure projects.

VIII. Financial Performance & Current State

The quarterly results announced in November 2024 painted a picture of resilience in challenging times. In its latest results, Prism Johnson reported a 13% year-on-year rise in total income to Rs 1,865 crore, compared to Rs 1,654 crore in Q2 FY25. The company recorded a net profit of Rs 1.6 crore, marking a sharp turnaround from a loss of Rs 103.7 crore a year earlier. While the absolute profit number might seem modest, the turnaround from a hundred-crore loss to profitability during a period of intense competition and input cost inflation demonstrated operational resilience.

The segment-wise performance revealed divergent trajectories that validated the diversification strategy. The cement division faced headwinds with revenue declining 17.1% year-on-year to ₹624 crores in Q2 FY25, primarily due to pricing pressure and extended monsoons that curtailed construction activity. However, the company's focus on premiumization showed results—the share of premium cement increased from 32% to 43%, partially offsetting volume declines. EBITDA per ton came at ₹56, a challenging number but one that remained positive when several competitors reported losses.

HRJ's performance demonstrated the power of brand and innovation in commoditizing markets. Despite the overall slowdown in real estate, tile revenues remained resilient, with premium products growing double-digits. The division's EBITDA margin declined 130 basis points to 5.9%, but this was primarily due to one-time expenses related to the new Panagarh plant commissioning. Excluding these costs, underlying margins remained healthy at 7-8%, superior to most domestic tile manufacturers.

The surprise performer was the RMC division, where EBITDA margins improved 600 basis points year-on-year to 4.5%. This dramatic improvement reflected both operational efficiency gains and strategic focus on value-added products. Metro rail projects, airport expansions, and industrial construction provided steady demand at better margins than residential projects. The division's ability to turn profitable in a traditionally low-margin business demonstrated execution excellence.

Working capital management emerged as a critical focus area during FY24. The cash conversion cycle increased from 17 days to 30 days, primarily due to declining creditor days from 65 to 52. While concerning on the surface, this reflected conscious strategy—reducing dependence on supplier credit improved negotiating power and reduced input costs. Debtor days remained healthy at 35 days, better than the industry average of 45-50 days, reflecting strong collection efficiency and customer quality.

The balance sheet told a story of financial prudence. Overall, the total assets and liabilities for FY24 stood at Rs 71 billion as against Rs 66 billion during FY23, thereby witnessing a growth of 8%. Asset growth funded through internal accruals rather than debt demonstrated self-sustaining growth. Net debt-to-equity ratio stood at 0.5x, providing ample headroom for growth investments without stretching the balance sheet. Interest coverage improved to 1.9x, comfortable though not spectacular, reflecting the capital-intensive nature of the business.

Return metrics showed steady improvement. The ROE for the company improved and stood at 11.7% during FY24, from -13.1% during FY24. The ROCE for the company improved and stood at 16.2% during FY24, from 0.9% during FY23. The dramatic improvement in ROCE demonstrated that capital allocation decisions were creating value. The gap between ROCE (16.2%) and cost of capital (approximately 11%) represented genuine economic value creation—₹520 crores annually at current capital employed levels.

Cash flow dynamics revealed operational strength beneath headline numbers. Operating cash flow during FY24 stood at ₹5 billion, funding both maintenance capex and growth investments. Free cash flow, after accounting for essential capital expenditure, remained positive—a rarity in the expansion-obsessed cement industry. This cash generation capability meant future growth could be self-funded, avoiding dilution or expensive debt.

Peer comparison provided context for performance evaluation. While UltraTech commanded market share of around 25% and operated at significantly larger scale, Prism Johnson's integrated model delivered comparable returns on capital. Against pure-play tile manufacturers like Kajaria Ceramics or Somany Ceramics, HRJ's brand strength and distribution reach provided competitive parity despite smaller scale. In RMC, only LafargeHolcim (before its India exit) and UltraTech operated at comparable scale with similar margins.

As of 13-Nov-2025 the market cap of Prism Johnson stood at ₹7,323.8. The 52-week high of Prism Johnson is ₹209.2 and the 52-week low is ₹108.0. The stock's trading range revealed market uncertainty about near-term prospects while maintaining faith in long-term value. Trading at 4.89 times book value suggested growth expectations, though the P/E ratio of 35.4 indicated earnings needed to catch up with valuations.

Geographic revenue distribution revealed balanced exposure without concentration risks. Central India contributed 35% of revenue, anchored by cement operations. Western India generated 30%, driven by tiles and RMC in Mumbai and Gujarat. Southern markets contributed 20%, primarily through tiles and selective cement presence. The remaining 15% came from Eastern and Northern markets, representing growth opportunities rather than current profit pools.

Customer concentration metrics demonstrated resilience. No single customer contributed more than 3% of revenue. The top 10 customers represented less than 15% of sales. This diversification meant no single project delay or customer default could materially impact performance. The retail-institutional mix stood at 60:40, providing stability from retail while capturing growth from institutional projects.

Operational metrics revealed continuous improvement. Capacity utilization in cement reached 73%, below the industry-leading 85-90% but improving quarterly. Tile capacity utilization at 68% provided room for growth without major capex. RMC plants operated at 45% utilization, reflecting the inherent nature of the business where proximity to projects mattered more than utilization. Energy costs as percentage of revenue improved from 18% to 15%, reflecting efficiency initiatives and alternate fuel usage.

The dividend policy balanced growth reinvestment with shareholder returns. While the company hadn't paid dividends during loss years, the return to profitability suggested resumption was imminent. The promoter holding at 74.87% provided stability but limited float liquidity. Institutional holding had increased to 15%, with domestic mutual funds showing increased interest. Foreign institutional ownership remained modest at 3%, suggesting potential upside if international investors discovered the story.

Looking at the current state in November 2024, Prism Johnson stands at an inflection point. The company has weathered multiple storms—the 2008 financial crisis, 2016 demonetization, COVID-19 pandemic, and current industry consolidation. Each crisis has been used to strengthen operations, optimize costs, and enhance competitive position. The financial numbers, while not spectacular, reflect a business that has found its optimal configuration—large enough to compete, diversified enough to be resilient, focused enough to excel.

IX. Porter's 5 Forces & Hamilton's 7 Powers Analysis

Porter's 5 Forces: The Competitive Battlefield

Supplier Power: Moderate to High The limestone dependency tells only part of the story. While Prism Johnson controls limestone reserves sufficient for 50+ years of cement production, the real supplier power lies in energy markets. Coal and petcoke prices, despite the alternate fuel initiatives, still determine 40% of cement production costs. In tiles, dependency on imported machinery from Italy and Spain creates vulnerabilities—a single equipment failure can halt production lines for weeks. However, Prism's scale provides negotiating leverage. The company's annual ₹2,000 crore procurement budget makes it a priority customer for suppliers, enabling better payment terms and assured supply during shortages.

Buyer Power: The Tale of Two Markets The dichotomy is stark. Institutional buyers—large contractors, government projects, real estate developers—wield enormous power. They demand 60-90 day credit periods, retrospective price adjustments, and volume discounts that can eviscerate margins. A single metro rail project can dictate terms that impact divisional profitability. Conversely, retail customers buying tiles for home renovation have minimal bargaining power. They rely on dealer recommendations, brand trust, and are relatively price-insensitive for premium products. Prism's 60:40 retail-institutional mix reflects conscious strategy to balance this power dynamic.

Threat of Substitutes: Limited but Evolving For cement, no viable substitute exists at scale. Steel and wood construction remain niche in India's tropical climate and seismic zones. The real substitution threat is indirect—precast construction reducing cement consumption per square foot. In tiles, the threat is more pronounced. Wooden flooring, vinyl, natural stone, and even polished concrete compete for share of surface. HRJ's response has been to position tiles not as a functional product but as a lifestyle choice, making substitution a statement about personal taste rather than rational economics.

New Entrants: High Barriers, Low Moats The ₹750-800 crore required for a million-tonne cement plant deters casual entrants. Environmental clearances can take 3-5 years, testing patience and financial stamina. The tile industry presents lower barriers—₹50 crore can establish a basic manufacturing unit. But building brand equity like HRJ's 60-year heritage? That's irreplaceable. The real threat comes not from new entrants but from existing players expanding into adjacent segments. When Asian Paints enters cement or UltraTech ventures into tiles, they bring capital, distribution, and ambition that can reshape industries overnight.

Competitive Rivalry: The Gladiatorial Arena ICRA estimates that the market share of the top five cement companies witnessed a steep rise to 54 per cent as of December 2023, from 45 per cent as of March 2015, and expects it to further increase to 55 per cent by March 2025, resulting in consolidation in the cement industry. This consolidation intensifies rivalry among remaining players. UltraTech and Adani's Ambuja-ACC combine engage in capacity wars that create oversupply and pressure pricing. Regional players like Prism must find niches—premium products, service quality, integrated solutions—to avoid being crushed in the volume game. In tiles, competition comes from imports (15% market share) and unorganized players (40% share) who compete on price alone, forcing branded players like HRJ to continuously innovate and premiumize.

Hamilton's 7 Powers: The Durability Test

Scale Economies: The Satna Advantage Operating two cement plants at a single location creates scale economies that transcend simple volume benefits. Shared infrastructure reduces capital intensity by 20%. Common workforce lowers administrative costs. Bulk procurement of consumables improves negotiating position. The limestone conveyor belt, connecting mines to plants, eliminates truck transportation—saving ₹50 per tonne. These micro-advantages compound into a sustainable cost position that new entrants cannot replicate without similar scale.

Network Effects: Limited but Emerging Traditional manufacturing businesses rarely exhibit network effects, and Prism Johnson is no exception. However, the dealer network creates quasi-network benefits. Each additional House of Johnson outlet makes the brand more valuable to architects who specify products. The larger the dealer network, the more attractive it becomes for new dealers to join, accessing marketing support and product range. The company's digital initiatives—connecting dealers, contractors, and customers—create nascent network effects that could strengthen over time.

Switching Costs: The Stickiness Factor For cement, switching costs are negligible—it's literally a commodity. But Prism has engineered stickiness through service. Technical support teams that help optimize concrete mix designs create knowledge dependencies. Long-term supply contracts with penalty clauses create financial switching costs. In tiles, switching costs are higher. Architects familiar with HRJ's product codes and specifications resist change. Dealers with showroom investments in display systems prefer continuity. Consumers replacing tiles partially must match existing designs, forcing repeat purchases from the same brand.

Counter-Positioning: The Integration Play While competitors optimize individual businesses, Prism's integrated model represents true counter-positioning. Pure-play cement companies cannot match the stability of diversified revenue streams. Standalone tile manufacturers lack the financial muscle to invest in technology and brand-building simultaneously. The integrated model appears sub-optimal to focused competitors—until downturns reveal its resilience. This counter-positioning is not easily replicable. Acquiring and integrating businesses requires capabilities that financial engineering alone cannot provide.

Branding: Six Decades of Trust With over six decades of experience, H & R Johnson ("HRJ") is the pioneer of ceramic tiles in India. This isn't just heritage—it's accumulated trust across generations. Parents who built homes with Johnson tiles recommend the brand to children. This emotional equity, built over decades, cannot be replicated through advertising spend. The brand commands 10-15% price premiums in commoditized markets. Even Chinese imports with superior specifications struggle against HRJ's brand power. In cement, the Champion brand, while younger, has built regional recognition that influences purchase decisions beyond rational evaluation.

Cornered Resource: Limestone and Location The Satna limestone reserves, sufficient for 50+ years, represent a cornered resource. But the true cornered resource is location—proximity to reserves, markets, and transportation infrastructure. Replicating Prism's Satna advantage would require finding similar limestone reserves, near transportation networks, with available land for plants, and environmental clearances. This combination is increasingly rare in India's development landscape. The 21 Experience Centers in prime urban locations represent another cornered resource—real estate that appreciates while serving as brand ambassadors.

Process Power: The Accumulated Advantage Three decades of cement manufacturing has created process knowledge that transcends documentation. Kiln operators who can "hear" temperature variations. Quality controllers who can predict strength from visual inspection. Maintenance teams that prevent breakdowns through pattern recognition. These capabilities, embedded in organizational routines and workforce experience, cannot be transferred or replicated. The integration of three distinct businesses has created unique process knowledge—understanding how cement quality affects tile installation, how RMC performance influences customer satisfaction across divisions. This tacit knowledge, accumulated over years, provides sustainable advantage.

Competitive Synthesis

The Porter's analysis reveals an industry structure that favors incumbents but intensifies rivalry among them. High barriers protect against new entrants but create desperate competition among existing players. Buyer power in institutional segments and supplier power in energy markets squeeze margins, forcing companies to find differentiation beyond price.

Hamilton's framework suggests Prism Johnson's competitive advantages are more durable than apparent. While lacking the scale economies of UltraTech or the network effects of technology platforms, the company has built a combination of powers that provide resilience. The integrated model (counter-positioning), HRJ brand (branding), Satna location (cornered resource), and accumulated capabilities (process power) create a competitive position that is difficult to assault frontally.

The intersection of these frameworks reveals Prism Johnson's strategic challenge: leveraging sustainable advantages while navigating intense rivalry. The company cannot win the scale game against UltraTech or Adani. But it can build an unassailable position in the integrated building materials space, serving customers who value solutions over products, relationships over transactions, and stability over aggression. This positioning—the profitable niche player in a consolidating industry—may lack glamour but provides sustainable returns.

X. Playbook: Business & Investing Lessons

Lesson 1: The Art of Countercyclical M&A

The H&R Johnson acquisition in 2009, when real estate had collapsed and credit markets were frozen, exemplifies contrarian thinking. While competitors conserved cash, Prism deployed capital at distressed valuations. The lesson extends beyond timing—it's about preparation. Having a strong balance sheet during good times provides ammunition for bad times. Maintaining banking relationships when you don't need money ensures access when you do. Building acquisition capabilities before opportunities arise enables quick execution when they do.

The failed insurance divestment in 2020-2022 provides the flip side—knowing when not to sell is as important as knowing when to buy. Walking away from ₹290 crores because terms deteriorated showed discipline. The lesson: establish walk-away criteria before negotiations begin. Price is just one variable; strategic fit, regulatory approvals, and timing matter equally. Sometimes the best deal is the one you don't do.

Lesson 2: Building Conglomerates in Emerging Markets

Unlike developed markets where conglomerates trade at discounts, emerging markets reward diversification done right. Prism Johnson demonstrates the template: diversify into related areas where capabilities transfer, maintain operational independence while capturing synergies, and ensure each business can stand alone while benefiting from the group. The critical insight is that in markets with institutional voids—unreliable suppliers, weak financial systems, scarce talent—internal markets within conglomerates can be more efficient than external markets.

The three-division structure reveals optimal conglomerate design. Each division has distinct leadership, separate P&L responsibility, and operational autonomy. But capital allocation, strategic planning, and capability development are centralized. This hybrid structure—decentralized operations, centralized strategy—balances entrepreneurship with control. The lesson: structure follows strategy, and strategy in emerging markets often requires controlled diversification.

Lesson 3: Managing Cyclicality Through Integration

Cement is cyclical, tiles are seasonal, and RMC is project-dependent. Individually, each business faces volatile cash flows. Combined, they create stability. When cement faces oversupply, tiles may boom from real estate recovery. When tiles face import pressure, RMC benefits from infrastructure spending. This portfolio effect isn't just about diversification—it's about choosing businesses with imperfectly correlated cycles.

The financial management during cycles reveals sophistication. During upturns, cash is accumulated rather than distributed. During downturns, investments in capability continue. This countercyclical capital allocation—investing when others retreat, consolidating when others expand—requires conviction and patience. The lesson: in cyclical industries, timing matters more than magnitude. Small investments at cycle bottoms outperform large investments at peaks.

Lesson 4: The Premium Migration Strategy

The journey from commodity cement to Champion Plus, from basic tiles to designer collections, from grey RMC to specialized concrete, demonstrates the power of premiumization. In commoditized industries, the only escape from price competition is moving up the value chain. But premiumization requires capabilities—technology, branding, distribution—that take years to build.

Share of premium cement increased from 32% in Q2 FY24 to 43% in Q2 FY25. This 11 percentage point shift represents millions in additional margin. The lesson: premiumization is not about creating premium products but about migrating customers. Start with small volumes at high margins, build credibility, then gradually shift the portfolio. Price realization improvement, even at lower volumes, often delivers better returns than volume growth at commodity prices.

Lesson 5: Capital Allocation in Capital-Intensive Industries

With ₹100-110 crores annual capex, choosing projects becomes critical. Prism's approach—grinding units over integrated plants, brownfield over greenfield, modernization over expansion—reveals capital discipline. The focus on return on incremental capital rather than absolute returns drives decisions. A ₹50 crore investment yielding 25% returns beats a ₹500 crore investment yielding 15%.

The debt management strategy deserves attention. Maintaining debt-to-equity at 0.5x when industry averages 1.5x provides flexibility. This conservative leverage means lower returns during good times but survival during bad times. The lesson: in capital-intensive industries, balance sheet strength is competitive advantage. The ability to invest when competitors cannot, acquire when others must sell, and survive when peers fail, comes from financial conservatism.

Lesson 6: Building Brands in B2B Industries

HRJ's brand strength in tiles is obvious, but Prism has built brand equity even in cement—supposedly a commodity. The Champion brand commands regional loyalty. Technical services create relationships beyond transactions. Experience centers influence specifications. The lesson: B2B branding is about trust and consistency rather than emotion and aspiration. Deliver on promises repeatedly, solve customer problems proactively, and brand equity accumulates imperceptibly but powerfully.

The distribution strategy—900+ dealers, 105 House of Johnson outlets, 21 Experience Centers—reveals the importance of physical presence in digital times. Customers buying tiles want to touch surfaces, see color variations, and visualize applications. The investment in retail infrastructure, while capital-intensive, creates competitive advantages that digital players cannot replicate. The lesson: in tactile categories, physical retail remains relevant.

Lesson 7: The Institutional Knowledge Advantage

Process knowledge accumulated over 30 years cannot be hired or acquired—it must be developed. The ability to optimize kiln operations, predict quality from input variations, and manage complex logistics comes from experience. This institutional knowledge, embedded in systems and people, provides sustainable advantage in industries where technology is accessible to all.

The management development approach—rotating talent across divisions, investing in technical training, promoting from within—builds institutional knowledge. External hires bring fresh perspective but internal promotions preserve culture. The balance between continuity and change, experience and innovation, determines organizational longevity. The lesson: in manufacturing, competitive advantage comes less from what you know than from how you execute what everyone knows.

Investment Lessons for Fundamental Investors

Valuation Complexity: Conglomerates require sum-of-parts analysis. Value each division separately, apply appropriate multiples, and add/subtract corporate overhead and synergies. The integrated model may deserve a premium or discount depending on execution quality and market conditions.

Cycle Timing: Understanding where each division stands in its cycle enables better entry/exit decisions. Cement may be peaking while tiles are bottoming. Aggregate analysis obscures these dynamics. Track segment-wise metrics, not just consolidated numbers.

Management Quality: In conglomerates, capital allocation skill matters more than operational excellence. Track management decisions over cycles—do they buy high and sell low, or vice versa? Do they chase growth or returns? Do they prefer empire-building or value creation?

Competitive Dynamics: In consolidating industries, relative position matters more than absolute performance. Being third-largest when top-two control 60% market share differs from being third when market is fragmented. Track market share evolution, not just revenue growth.

Hidden Assets: Conglomerates often have hidden value—real estate accumulated over decades, brands not reflected on balance sheets, or strategic stakes in other companies. Patient investors who identify and wait for value realization often outperform.

XI. Bull vs. Bear Case

The Bull Case: India's Infrastructure Renaissance

India's construction boom isn't hope—it's happening. The government's ₹111 trillion National Infrastructure Pipeline, the Housing for All initiative targeting 20 million homes, and rapid urbanization adding 200 million city dwellers by 2030 create unprecedented demand for building materials. Prism Johnson, with its integrated portfolio, captures value across this construction chain—cement for infrastructure, tiles for homes, RMC for speed.

The capacity expansions completed in FY24 position the company perfectly for this growth. The Company enhanced its cement grinding capacity by 1.3 MTPA with four grinding units in FY24. With industry utilization rates approaching 80%, new capacity comes online exactly when demand accelerates. The tile capacity in Eastern India through the Panagarh plant opens virgin markets where consumption could double from current levels. RMC's 108 plants provide coverage in cities where metro projects, airport expansions, and commercial construction drive demand.

The integrated model's resilience shines during growth phases. Cross-selling opportunities multiply when construction activity increases. A developer building residential complex needs cement for structure, RMC for speed, tiles for finishing, and sanitaryware for fitouts. Prism Johnson becomes a one-stop solution, reducing procurement complexity for customers while improving realization for the company. The 30% of large customers buying from multiple divisions could reach 50% as integration benefits become apparent.

Operating leverage provides earnings explosion potential. At 73% cement capacity utilization, every percentage point improvement drops directly to bottom line. Fixed costs are already absorbed; incremental production generates 40%+ EBITDA margins. If utilization reaches 85%—industry standard for efficient operations—EBITDA could increase 50% without any price increases. Similar dynamics apply to tiles and RMC, creating triple-engine earnings growth.

The sustainability initiatives position Prism for the ESG-conscious future. Prism Cement was 3.4 times water positive during FY24. Green building certifications increasingly mandate sustainable materials. Government projects prioritize vendors with environmental credentials. International funding flows to companies with strong ESG scores. Prism's investments in alternate fuels, water harvesting, and carbon reduction—initially seen as costs—become competitive advantages as sustainability moves from nice-to-have to must-have.

Consolidation dynamics favor strategic players like Prism Johnson. "Since FY18, larger companies have been consolidating their market shares, and the market share of top-5 players has risen from 67 percent in FY18 to 72 percent in FY24," Equirus Securities said in a research report. As smaller players exit due to environmental compliance costs, technology requirements, or financial stress, their market share flows to organized players. Prism, with strong balance sheet and proven integration capabilities, could acquire distressed assets at attractive valuations, accelerating growth through consolidation.

The Bear Case: Structural Headwinds and Execution Risks

The competitive dynamics in cement are deteriorating rapidly. UltraTech and Adani's Ambuja-ACC combine control over 60% capacity and show no signs of rational competition. Their aggressive expansions create structural oversupply, pressuring prices regardless of demand growth. Prism Johnson, with less than 2% market share in cement, lacks pricing power and must accept whatever prices the giants dictate. The premium positioning helps but cannot fully offset commodity price pressures.

Chinese imports remain an existential threat to the tile industry. Despite anti-dumping duties, imports command 15% market share through price points that domestic manufacturers cannot match. As China's domestic construction slows, export pressure intensifies. Digital marketing by import aggregators bypasses traditional distribution, directly reaching price-conscious consumers. HRJ's brand heritage provides some protection, but younger consumers show less brand loyalty and more price sensitivity.

The real estate cycle shows concerning signs. Inventory overhang in commercial real estate, rising interest rates affecting affordability, and developer stress from regulatory changes create demand headwinds. The residential segment, contributing 60% of building material demand, faces affordability crisis as property prices outpace income growth. Government's infrastructure spending, while substantial, cannot fully offset private sector weakness.

Capital intensity limits returns regardless of growth. Every capacity addition requires hundreds of crores, earning returns only after 3-4 year gestation. Meanwhile, asset-light competitors in tiles (importers) and cement (grinding units) cherry-pick profitable segments without capital commitment. The integrated model, while providing stability, also means capital gets allocated to lower-return segments for strategic reasons rather than financial optimization.

ESG regulations pose transition risks that markets underappreciate. Cement contributes 8% of global CO2 emissions, attracting regulatory scrutiny. Carbon taxes, already implemented in Europe, could arrive in India within this decade. Technology for green cement remains experimental and expensive. Retrofitting existing plants for lower emissions requires capital that won't generate returns, only maintain license to operate. The ₹600 crore spent on alternate fuel facilities might be just the beginning of a costly transition.

The conglomerate structure itself creates challenges in a specializing world. Investors prefer pure-plays they can understand and value easily. Talented executives prefer focused companies where career paths are clear. Strategic buyers looking for acquisitions want specific assets, not integrated complexes. The benefits of integration—stability, synergies, resilience—are hard to quantify and easily dismissed during bull markets when growth matters more than risk management.

The Balanced View: Navigating Contradictions

The truth, as always, lies between extremes. India's infrastructure story is real but will unfold over decades, not quarters. Prism Johnson will benefit but must navigate intense competition and technological disruption. The integrated model provides resilience but requires exceptional execution to deliver promised synergies. The company's transformation from Karan Cement to Prism Johnson demonstrates adaptability, but past success doesn't guarantee future performance.

For investors, Prism Johnson represents a bet on execution in a structurally growing but intensely competitive market. The company offers exposure to India's construction boom without the binary risks of pure-play cement or tiles. The reasonable valuations—trading at book value multiples that discount growth potential—provide margin of safety. But patience is required as the story unfolds through cycles, not straight lines.

The key variables to monitor are clear: capacity utilization trends indicating demand-supply balance, EBITDA per ton/square meter revealing pricing power, market share evolution showing competitive position, and return on capital employed demonstrating value creation. If these metrics improve consistently, the bull case strengthens. If they deteriorate despite revenue growth, the bear case dominates.

XII. Epilogue: Future Outlook & Key Themes

The Sustainability Imperative

Standing at the cusp of 2025, Prism Johnson faces a future where environmental considerations will dominate strategic decisions. The cement industry's carbon footprint—producing one ton of cement releases nearly one ton of CO2—makes it a primary target for climate regulations. The company's early investments in sustainability now appear prescient. The alternate fuel facility processing 600 tonnes daily, the water-positive operations, and renewable energy initiatives position Prism ahead of regulatory curves.

But the real sustainability revolution lies ahead. Carbon capture technology, still experimental today, could become mandatory by 2030. Green cement using alternative materials like fly ash and slag will move from niche to mainstream. The company that masters low-carbon cement production while maintaining cost competitiveness will dominate the next decade. Prism's R&D investments, modest today at ₹20 crores annually, may need to increase ten-fold to remain relevant.