Marathon Petroleum Corporation: From Ohio Oil to America's Refining Giant

I. Introduction & Episode Overview

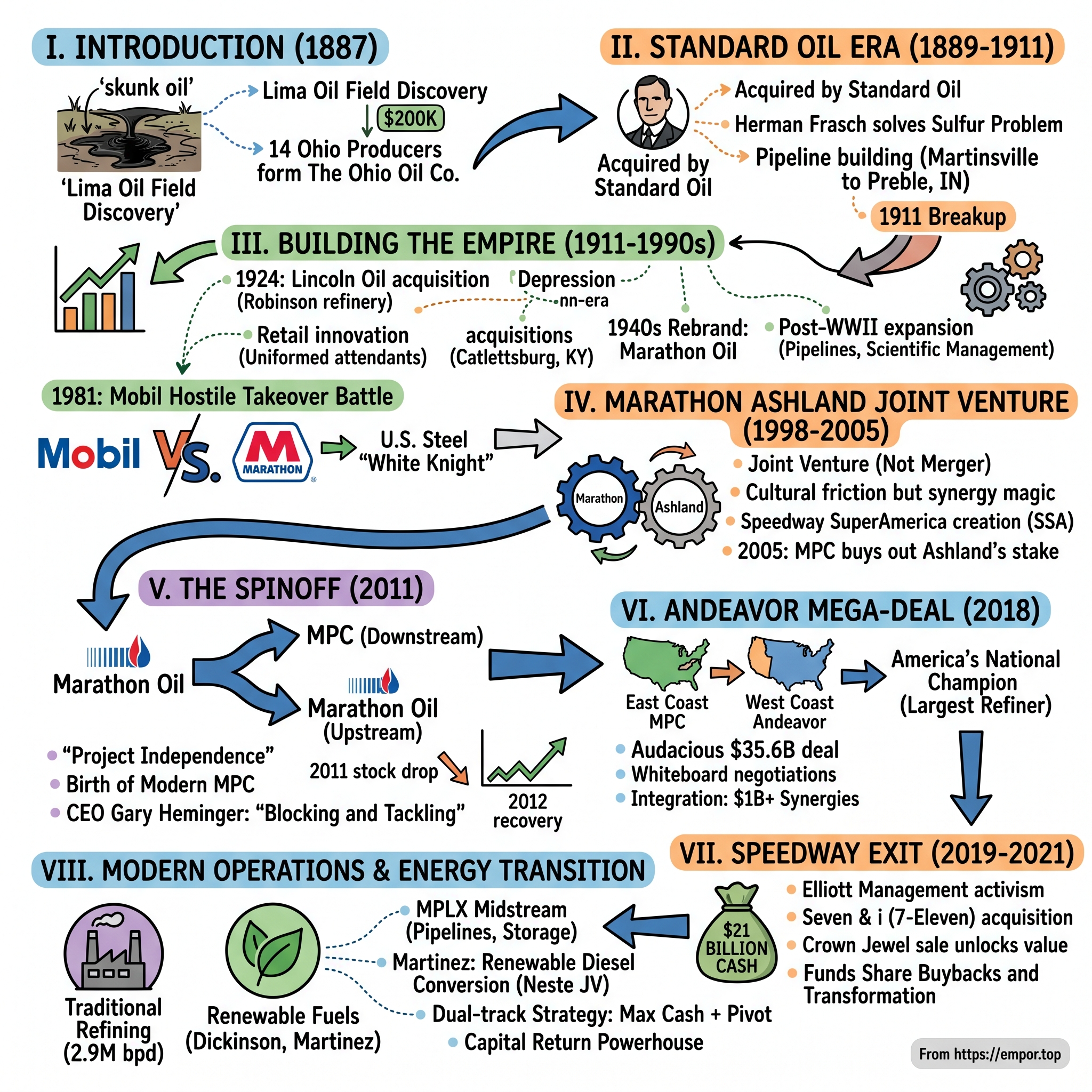

Picture this: It's 1887 in northwestern Ohio, and the ground literally bubbles with opportunity. Black gold seeps through limestone formations near Lima, creating what locals call "skunk oil" for its sulfuric stench. While Standard Oil's empire stretches across America, a group of Ohio wildcatters sees something others miss—this foul-smelling crude might just be the foundation of an energy giant. They band together to form The Ohio Oil Company, setting in motion a 137-year journey that would create Marathon Petroleum Corporation, today's largest refining system in the United States.

The story of Marathon Petroleum reads like a masterclass in strategic patience and operational excellence. From its origins as a scrappy Ohio producer, through absorption into Rockefeller's Standard Oil empire, to its resurrection as an independent company, and ultimately its transformation into America's refining champion—this is a tale of knowing exactly when to zig while competitors zag.

At its core, MPC represents something uniquely American: the ability to reinvent yourself completely while never forgetting where you came from. The company that once pumped sulfurous Ohio crude now processes 2.9 million barrels per day across the most sophisticated refining network on the continent. It's survived antitrust breakups, hostile takeover attempts, commodity super-cycles, and now faces its greatest challenge yet—the energy transition.

The central question we're exploring isn't just how a regional oil company became a national powerhouse. It's how Marathon consistently made contrarian bets that paid off spectacularly. When others integrated upstream, Marathon doubled down on refining. When peers chased international expansion, Marathon consolidated domestically. When activists demanded breakups, Marathon actually listened—and created billions in value.

This deep dive traces Marathon's DNA from those sulfurous Ohio oil fields through the boardroom battles that shaped modern American energy. We'll examine the three transformative deals that defined MPC: the Ashland joint venture that taught them partnership dynamics, the Andeavor acquisition that created a coast-to-coast empire, and the Speedway divestiture that proved sometimes the best deal is knowing what to sell.

Today's Marathon Petroleum stands at a fascinating inflection point. It's simultaneously the ultimate beneficiary of America's fossil fuel infrastructure advantage and a company actively preparing for a lower-carbon future. The playbook they're writing—maximize cash from traditional assets while strategically pivoting to renewables—might just be the template for how legacy energy companies navigate the next decade.

What makes Marathon's story particularly compelling for investors is its consistent ability to create value through cycles. This isn't a growth-at-any-cost narrative or a turnaround story. It's something rarer: a company that understood its competitive advantages, exploited them ruthlessly, and knew exactly when to evolve. As we'll discover, the secret sauce isn't just operational excellence—it's the discipline to say no until the perfect yes appears.

II. Founding Era & Standard Oil Dynasty (1887–1911)

The Lima oil field discovery of 1885 changed everything. Unlike the sweet Pennsylvania crude that built Rockefeller's fortune, Lima crude was cursed—so laden with sulfur that kerosene refined from it would blacken lamp chimneys and fill rooms with noxious fumes. Standard Oil initially dismissed it as worthless. That dismissal created an opening that fourteen small Ohio producers would exploit, banding together in 1887 to form The Ohio Oil Company with a mere $200,000 in capital.

The founding wasn't glamorous. These weren't visionary industrialists but practical men who understood that survival meant cooperation. Their first headquarters was a cramped office above a hardware store in Lima, where company secretary W.H. Shatzer kept meticulous records in leather-bound ledgers that still exist today. By pooling resources, they could afford drilling equipment, storage tanks, and most critically, experimentation with refining techniques that might crack the sulfur problem.

Within two years, Ohio Oil had become the state's largest producer, pumping 12,000 barrels daily from over 80 wells. But success attracted attention from the one entity no independent oil company could resist: Standard Oil. John D. Rockefeller had initially scoffed at Lima crude, reportedly saying it was "good for nothing but road tar." But when chemist Herman Frasch developed a process to remove sulfur using copper oxide, Rockefeller moved with characteristic speed and ruthlessness.

The 1889 acquisition negotiations revealed Rockefeller's genius for both intimidation and seduction. Ohio Oil's board initially demanded $1 million—five times their founding capital. Standard's negotiators laughed, then systematically demonstrated how they could destroy Ohio Oil through price wars and transportation monopolies. The final deal: $340,000 in Standard Oil certificates, making Ohio Oil's shareholders suddenly wealthy but entirely dependent on Rockefeller's empire. Company lore holds that one director wept at the signing, saying "We've sold our birthright," while another replied, "Yes, but for a fortune, not pottage."

Under Standard's ownership, Ohio Oil transformed from scrappy wildcatter to industrial powerhouse. The 1895 headquarters move to Findlay—a larger city with better rail connections—symbolized this evolution. Standard poured capital into Ohio Oil, funding massive infrastructure projects that independent companies could never afford. The crown jewel was the 1906 pipeline from Martinsville, Illinois to Preble, Indiana—a 280-mile engineering marvel that required 74 pumping stations and crossed 14 rivers.

The pipeline's construction manager, J.C. Donnell, would later become Ohio Oil's first post-Standard president, and his approach—meticulous planning, over-engineering for safety, obsessive focus on operational efficiency—became encoded in the company's DNA. Workers joked that Donnell inspected every weld personally, but the pipeline operated for 47 years without a major incident, a safety record that established Ohio Oil's reputation for operational excellence.

But even as Ohio Oil prospered within Standard's empire, storm clouds gathered in Washington. Theodore Roosevelt's trust-busting crusade had Standard Oil squarely in its sights. Company executives in Findlay followed the antitrust proceedings with mixed emotions—fear of independence competing with excitement about self-determination. Internal memos from 1910 show frantic preparation for potential separation, with departments creating shadow organizational structures "just in case."

The Supreme Court's 1911 decision to break up Standard Oil under the Sherman Antitrust Act liberated 33 companies, including Ohio Oil. The company received its independence with 3,900 producing wells, storage capacity for 12 million barrels, 450 miles of pipeline, and most importantly, a culture forged in both entrepreneurial scrambling and corporate discipline. The Findlay headquarters erupted in celebration—and trepidation. After 22 years inside Standard's protective embrace, Ohio Oil would have to prove it could survive alone.

The transition revealed character. While some Standard spinoffs immediately sought new partners or buyers, Ohio Oil's board declared independence definitively. Their first act: approving a massive drilling program in Illinois, betting the company's entire cash position on new fields. It was either inspired confidence or dangerous hubris. As we'd learn repeatedly over the next century, when Marathon (as Ohio Oil would become) made big bets, they had an uncanny ability to be right.

III. Building the Refining Empire (1911–1990s)

Independence from Standard Oil felt like being pushed from a comfortable nest at 30,000 feet—exhilarating and terrifying in equal measure. Ohio Oil's first board meeting as an independent company in July 1911 lasted fourteen hours, with directors chain-smoking cigars and arguing about everything from capital allocation to company letterhead. The immediate challenge wasn't finding oil—they had plenty of that. It was building an integrated business that could compete with the now-fragmented but still formidable Standard Oil successors.

The company's first major strategic move came in 1924 with the acquisition of Lincoln Oil Refining Company, a deal that would establish a pattern Marathon would follow for the next century: buy distressed assets, apply operational excellence, and extract value others couldn't see. Lincoln Oil brought the Robinson, Illinois refinery—a 12,000 barrel-per-day facility that local newspapers called "a rusted monument to failed ambition." Ohio Oil's engineers descended on Robinson like an occupying army, rebuilding furnaces, replacing miles of piping, and implementing safety protocols that were revolutionary for the era. Within eighteen months, Robinson was processing 25,000 barrels daily with industry-leading yields.

The Lincoln acquisition also brought seventeen Linco brand service stations scattered across Illinois and Indiana. These weren't the gleaming white-box stations we know today but converted barns and shacks with hand-painted signs and manual pumps. Yet Ohio Oil treated them like laboratories for retail innovation. They introduced uniformed attendants (revolutionary in 1925), standardized service protocols, and most importantly, guaranteed gasoline quality—a promise that meant something when competitors routinely diluted their products.

The 1920s roared for Ohio Oil, with annual revenues jumping from $3 million to $47 million. But success bred vulnerability. The company's heavy Illinois crude production and limited refining capacity created a dangerous imbalance. CEO Thomas Donnell (son of the pipeline builder) recognized this structural weakness and launched what insiders called "The Grand Strategy"—a decade-long transformation from crude producer to integrated oil company.

The transformation accelerated through the 1930s despite the Depression. While competitors retrenched, Ohio Oil methodically acquired struggling refineries, pipeline systems, and retail networks at fire-sale prices. The crown jewel came in 1936: the Catlettsburg, Kentucky refinery, purchased from Ashland Oil (ironically, a company they'd partner with sixty years later). Catlettsburg processed heavy Appalachian crude that others considered worthless, but Ohio Oil's chemists had developed proprietary techniques for extracting premium products from challenging feedstocks—a competitive advantage that persists today.

The company's 1940s rebrand to Marathon Oil reflected both ambition and strategic positioning. The Marathon name—inspired by the legendary Greek battle—replaced the provincial "Ohio Oil" identity just as the company expanded nationally. Marketing executives tested seventeen different names in focus groups across twelve cities before selecting Marathon, with one executive noting it "suggested both endurance and victory—exactly our corporate ethos."

Post-World War II America ran on oil, and Marathon ran hard to keep up. The company's 1950s expansion was breathtaking in scope: new refineries in Texas City and Detroit, a 1,000-mile pipeline from West Texas to Illinois, and a retail network that grew from 300 to 2,400 stations. But the most important development was cultural. Marathon pioneered what it called "scientific management"—using data analytics, operations research, and early computer modeling to optimize every aspect of the business. While competitors relied on intuition and experience, Marathon measured everything.

The 1960s brought international adventures—drilling in Libya, exploring in the North Sea, building refineries in Germany. But unlike peers who went "empire building," Marathon's international forays were surgical and strategic. They entered markets where they had specific technical advantages and exited quickly when those advantages eroded. The discipline to walk away from seemingly attractive opportunities became a Marathon hallmark.

Then came 1981, the year that nearly ended everything. Mobil Oil, cash-rich from Middle Eastern operations, launched a hostile takeover bid for Marathon at $85 per share—a 50% premium that had Wall Street salivating. Marathon's board, led by the pugnacious Harold Hoopman, fought with everything they had. They sued in seven states, lobbied Congress for intervention, and launched a media campaign portraying Mobil as a job-destroying monopolist.

The battle's climax came in a smoke-filled conference room at New York's Waldorf-Astoria hotel. With Mobil's victory seeming inevitable, Marathon played its last card: a white knight in the form of U.S. Steel Corporation. The steel giant offered $125 per share—outbidding Mobil dramatically but promising to keep Marathon's management and operations intact. The deal closed in March 1982, making Marathon a U.S. Steel subsidiary but preserving its operational independence.

Under U.S. Steel's ownership (later USX Corporation), Marathon enjoyed benign neglect in the best possible way. USX needed Marathon's cash generation to fund steel operations and debt service, but otherwise left the oil company alone. This autonomy allowed Marathon to perfect what internal documents called the "Marathon Way"—a relentless focus on operational efficiency, safety, and incremental improvement rather than transformational gambles.

By the 1990s, Marathon had evolved into something unique in American oil: not the biggest, not the most international, not the most integrated, but arguably the best-run pure refining and marketing operation in the country. The company processed 950,000 barrels daily across six refineries, each operating in the top quartile for utilization and yield. The retail network had grown to 3,900 stations, with the Speedway brand becoming synonymous with clean restrooms and consistent service—details that seemed trivial but drove customer loyalty.

The stage was set for Marathon's next evolution. The reliable cash generator within USX was about to break free again, armed with decades of operational excellence and a clear vision of value creation through focus rather than sprawl. As the new millennium approached, Marathon's leadership sensed opportunity in an industry ripe for consolidation.

IV. The Marathon Ashland Joint Venture (1998–2005)

The late 1990s oil industry resembled a high-stakes poker game where everyone kept raising but nobody wanted to show their cards first. Crude prices had collapsed to $10 per barrel in 1998, refining margins were tissue-thin, and environmental regulations threatened billions in upgrade costs. In this environment, Marathon's CEO Mike Stice and Ashland Inc.'s CEO Paul Chellgren met for what was supposed to be a courtesy dinner at Louisville's exclusive Pendennis Club. Four bourbon pours later, they'd sketched on a cocktail napkin what would become Marathon Ashland Petroleum LLC.

The logic was compelling to the point of obviousness—once someone had the courage to propose it. Marathon brought six refineries and 2,100 Speedway stations east of the Mississippi. Ashland contributed three refineries and 3,100 SuperAmerica convenience stores in the Midwest. Combined, they'd create the nation's sixth-largest refiner with enough scale to survive the coming consolidation. But the real genius was in the structure: a joint venture rather than a merger, preserving both companies' flexibility while capturing immediate synergies.

The negotiations revealed fascinating cultural dynamics. Marathon's team, led by deal architect Janet Groeber, approached everything with engineer's precision—spreadsheets modeling synergies down to the penny, integration plans mapped to the hour. Ashland's negotiators, steeped in Kentucky's genteel business culture, preferred handshake agreements and trust. The tension created magic: Marathon's rigor with Ashland's relationship focus produced an unusually thoughtful deal structure that anticipated problems rather than just papering them over.

The joint venture officially launched January 1, 1998, with a combined enterprise value of $8.2 billion. But the real story was what happened in the trenches. At the Canton, Ohio refinery, Marathon and Ashland engineers who'd competed for decades suddenly found themselves collaborating. Initial suspicion gave way to respect as best practices emerged. Ashland's innovative maintenance scheduling reduced downtime by 15%. Marathon's yield optimization protocols increased gasoline production by 3%. These might sound like marginal improvements, but at refining scale, they translated to hundreds of millions in annual value.

The retail integration proved even more fascinating. Speedway and SuperAmerica occupied different niches—Speedway focused on fuel and efficiency, SuperAmerica on food and convenience. Rather than force homogenization, leadership made a brilliant decision: let them compete internally. Stores in overlapping markets tested different concepts, with winning formats rolled out system-wide. The "co-opetition" model drove innovation that neither brand would have achieved alone.

The venture's masterstroke came in 2001 with the creation of Speedway SuperAmerica LLC (SSA), consolidating all retail operations under unified management while maintaining distinct brands. The timing was perfect—just as hypermarket gas stations were crushing independent operators, SSA had the scale to negotiate with suppliers, invest in technology, and most importantly, gather customer data that informed everything from fuel pricing to coffee selection.

Behind the operational success, however, tensions simmered. Marathon executives, accustomed to USX's hands-off approach, chafed at Ashland's more involved board oversight. Ashland's team, meanwhile, grew frustrated with Marathon's methodical decision-making. The CEOs held monthly "alignment dinners," which insiders describe as "diplomatic summits where grievances were aired over expensive wine." These sessions prevented minor frictions from becoming major fractures.

The relationship's inflection point came in 2003 when Ashland announced its strategic shift away from energy toward specialty chemicals. CEO Jim O'Brien (who'd replaced Chellgren) told analysts that Ashland's future lay in high-margin industrial products, not commodity refining. For Marathon, still controlled by USX but sensing independence on the horizon, this was the opening they'd been waiting for.

The 2004 negotiations for Marathon to buy out Ashland's stake revealed how much both companies had learned from their partnership. There was no acrimony, no competing bids, no investment banker drama. Both sides knew the asset's value precisely because they'd operated it together for six years. The final price—$3.7 billion for Ashland's 38% stake—was reached in three meetings, with most time spent on transition logistics rather than valuation disputes.

The September 2005 closing marked more than just a transaction completion. For Marathon, it meant controlling a refining and marketing platform that could stand independently. For Ashland, it provided capital to complete their specialty chemical transformation. Both companies got exactly what they needed, when they needed it—the rarest of outcomes in corporate divorces.

The venture's seven-year run generated profound lessons that would guide Marathon's future moves. First, cultural integration matters more than synergy spreadsheets. Second, maintaining operational autonomy within financial partnership preserves entrepreneurial energy. Third, and most importantly, the best partnerships have built-in exit strategies that allow graceful separation when strategies diverge. These weren't just theoretical insights—they were battle-tested principles that would prove invaluable when Marathon approached its next transformative deal.

V. The Spinoff: Birth of Modern MPC (2011)

The conversation that would reshape American refining started with an unlikely question at a 2009 USX board meeting: "Why exactly do we own an oil company?" The director asking wasn't being facetious. USX Corporation, the renamed U.S. Steel, had transformed into a hodgepodge of industrial assets with no clear strategic thread. Marathon Oil generated most of the profits but received a conglomerate discount from Wall Street. Something had to give.

The internal codename was "Project Independence," though Marathon executives privately called it "The Great Escape." CEO Clarence Cazalot Jr., a Louisiana native with a chemist's precision and a poker player's instincts, had been quietly preparing for separation since 2008. His team built shadow organizational structures, negotiated separate credit facilities, and most crucially, convinced USX's board that two pure-play companies would be worth more than one confused conglomerate.

The spinoff's complexity rivaled the Manhattan Project. Marathon Oil needed to be split into two entities: upstream exploration and production would keep the Marathon Oil name, while downstream refining, marketing, and transportation would become Marathon Petroleum Corporation. The division of assets alone took eighteen months and 400 lawyers. Who got which pipeline? How were joint facilities allocated? What about 40,000 employees' pension obligations? Every decision rippled through tax implications, regulatory requirements, and competitive positioning.

Gary Heminger's appointment as MPC's first CEO sent a crucial signal. A Marathon lifer who'd started as a refinery engineer in 1975, Heminger embodied operational excellence over financial engineering. His first all-hands address in Findlay's auditorium was quintessential Heminger: no soaring rhetoric, just a methodical explanation of how MPC would win through "blocking and tackling better than anyone else." Employees describe leaving that meeting with unusual clarity about their mission.

The financial architecture deserved its own MBA case study. MPC would start life with $2.4 billion in debt—manageable but not negligible—and a market cap around $20 billion. The refining portfolio included seven facilities processing 1.2 million barrels daily, the fourth-largest capacity in America. The crown jewel was Speedway, now 1,350 stores generating $1.5 billion in annual EBITDA. The MPLX pipeline assets, though not yet separately public, provided steady midstream cash flows.

Wall Street's initial reaction was tepid bordering on hostile. July 1, 2011—MPC's first trading day—saw the stock open at $31 and promptly drop 5%. Analysts questioned everything: Why hadn't MPC kept more integrated production? Could pure-play refiners survive volatile crack spreads? Wasn't Speedway better owned by a dedicated retailer? One particularly harsh research note called MPC "a collection of decent assets with no compelling equity story."

Heminger and CFO Tim Griffith responded with what they called the "Show Me Strategy"—forget grand visions, just deliver consistent quarterly results. The first earnings call was a masterclass in expectation management. Griffith walked through maintenance schedules, seasonal patterns, and regional dynamics with numbing detail. The message: we're operators, not promoters. Judge us by our numbers, not our narratives.

The early challenges were real and immediate. Three months after independence, refining margins collapsed as European debt crisis fears crushed demand. MPC's stock touched $25, down 20% from the spinoff price. Internal emails (later disclosed in litigation) show genuine panic among some directors about whether independence had been a terrible mistake. Heminger's response was to accelerate operational improvements rather than cut growth capital—a contrarian bet on margins eventually recovering.

The Garyville, Louisiana refinery expansion became MPC's first major independent decision and nearly its last. The project to add 180,000 barrels of daily capacity would cost $2.2 billion—massive for a company with a $15 billion market cap. The board debated for three contentious sessions, with directors split between growth advocates and balance sheet conservatives. Heminger broke the tie with a simple argument: "If we don't believe in our own operations enough to invest, why should shareholders?"

By year-end 2011, green shoots appeared. Refining margins recovered as driving demand surprised to the upside. Speedway's same-store sales grew 4%, beating all competitors. Most importantly, MPC's refineries ran at 94% utilization—industry-leading performance that validated Heminger's operational focus. The stock closed 2011 at $33, modest appreciation but critical psychological validation.

The first full year of independence—2012—transformed skeptics into believers. MPC generated $3.4 billion in EBITDA, crushed earnings estimates for four straight quarters, and raised the dividend twice. The stock doubled to $66. Suddenly, the same analysts who'd questioned the spinoff's logic were praising MPC's "pure-play focus" and "best-in-class operations." The vindication was sweet but Heminger, ever pragmatic, warned employees against complacency: "We're one refinery explosion away from being yesterday's story."

The spinoff's success transcended financial metrics. MPC had proven that in modern energy, focus beats integration. While oil majors struggled with competing capital allocation priorities between upstream and downstream, MPC could optimize entirely for refining and marketing. Every dollar of capex, every management hour, every strategic decision aimed at a single goal: be America's best refiner. That clarity, more than any specific asset or capability, became MPC's sustainable competitive advantage.

VI. The Andeavor Mega-Deal: Creating a National Champion (2018)

The text message that changed American refining came at 2:47 AM on a Sunday in December 2017. Gary Heminger, suffering from insomnia in a Denver hotel, messaged Andeavor CEO Greg Goff: "Coffee when you're back from Europe? Have an idea." Goff, landing at Heathrow, responded immediately: "Tuesday. Your idea better be good to justify flying to Findlay."

The idea was audacious to the point of absurdity: combine MPC and Andeavor to create America's first truly national refiner. The deal would require $35.6 billion in enterprise value, regulatory approval across multiple jurisdictions, and integration of 29,000 employees. It would also catapult the combined company past Valero as America's largest refiner, with 3.1 million barrels of daily capacity stretching from California to Ohio.

The strategic logic was elegant in its simplicity. MPC dominated east of the Mississippi River with sophisticated refineries processing heavy Canadian crude. Andeavor (formerly Tesoro) controlled the West Coast and Rocky Mountains, with efficient facilities optimized for light tight oil. Combined, they'd have geographic diversification no competitor could match, capture massive synergies from logistics optimization, and most importantly, gain unprecedented market power in refined product pricing.

That first coffee meeting in Heminger's spartan Findlay office lasted six hours. Both CEOs, chemical engineers by training, sketched refinery configurations on whiteboards like professors solving equations. They identified $1 billion in annual synergies within the first hour—just from eliminating duplicate crude purchases and optimizing product flows between regions. By hour three, they'd mapped out an integration plan. By hour six, they'd agreed on social issues: Heminger would be CEO, Goff would be executive chairman, and both management teams would be blended based on merit rather than company origin.

The negotiation's most fascinating element was what didn't happen: no bidding war. Heminger and Goff agreed early that investment bankers would destroy value through auction dynamics. Instead, they personally negotiated the exchange ratio (1.87 MPC shares per Andeavor share) based on detailed operational models rather than stock price premiums. When bankers later complained about lost fees, Goff reportedly said, "That's exactly the point."

The April 30, 2018 announcement sent shockwaves through the energy sector. The $23.3 billion equity value represented a 24% premium—generous but not excessive. More interesting was the market's reaction: both stocks rose, adding $4 billion in combined market cap on announcement day. Wall Street, typically skeptical of mega-mergers, recognized this was different. As one analyst noted, "This isn't empire building—it's the logical conclusion of U.S. refining consolidation."

The integration planning revealed both companies' operational DNA. MPC appointed 24 integration teams, each with co-leaders from both companies. The teams had extraordinary autonomy but clear metrics: identify synergies, minimize disruption, and decide quickly. The "Clean Sheet Reviews" became legendary—every process from crude purchasing to bathroom cleaning was evaluated without regard to legacy ownership. The best practice won, period.

The regulatory approval process tested everyone's patience. The Federal Trade Commission demanded divestitures in California and North Dakota where combined market share exceeded 50%. Rather than fight, MPC immediately agreed to sell terminals and pipeline stakes to Love's Travel Stops for $1.5 billion. The quick capitulation surprised regulators accustomed to prolonged negotiations, accelerating approval by months.

The human integration proved more challenging than asset combination. Andeavor's entrepreneurial, West Coast culture clashed with MPC's methodical, Midwest approach. Early integration meetings featured what participants called "polite hostility"—surface cooperation masking deep skepticism. The breakthrough came during a joint safety workshop where an Andeavor engineer's innovation reduced refinery incidents by 30%. MPC engineers' enthusiastic adoption of the practice broke cultural ice more effectively than any team-building exercise.

October 1, 2018—the closing date—marked the beginning rather than end of value creation. The first integrated executive meeting lasted 72 straight hours as leaders worked through immediate decisions: Which crude contracts to cancel? How to schedule refinery maintenance? Where to prioritize growth capital? The exhaustion was intentional—Heminger believed making tough decisions while tired revealed true judgment.

The synergy realization exceeded even optimistic projections. Within six months, the combined company achieved $600 million in annual run-rate savings. The real magic came from revenue synergies nobody had modeled. MPC's Gulf Coast refineries could now supply Andeavor's Western retail network during California refinery maintenance, capturing premium pricing. Andeavor's Rockies crude could flow to MPC's Midwest refineries when Canadian supplies tightened. These opportunities, invisible to separate companies, generated an additional $400 million annually.

The creation of a coast-to-coast refining network also transformed competitive dynamics. When Philadelphia Energy Solutions declared bankruptcy in 2019, MPC could immediately redirect product flows to capture East Coast market share. When California implemented new fuel specifications, MPC's geographic diversity meant compliance costs were spread across a broader base. Competitors, locked into regional footprints, couldn't match this flexibility.

By 2019's end, the Andeavor acquisition was hailed as the decade's best energy deal. MPC's stock had risen 45% post-merger while peers struggled. The company generated $4.8 billion in free cash flow, funding both growth investments and massive shareholder returns. But Heminger, ever paranoid about success breeding complacency, was already planning the next transformation. The Andeavor deal had created America's refining champion. Now came the harder question: what to do with that championship platform in a rapidly changing energy landscape?

VII. The Speedway Exit: Strategic Pivot (2019–2021)

The phone call that would unlock $21 billion in value came from an unexpected source: Elliott Management's Paul Singer, calling Gary Heminger directly on his cell at 6 AM on a September 2019 Saturday. "Gary, we need to talk about Speedway. You're sitting on a goldmine that the market refuses to recognize. We can help—whether you want it or not."

Elliott had quietly accumulated a $2.5 billion stake in MPC, making them the largest active investor in energy. Their 38-page presentation, leaked to media before MPC's board had fully digested it, was surgical in its critique. Speedway, generating $2.2 billion in EBITDA, was being valued by the market at maybe 6x multiple within MPC's consolidated structure. As a standalone company, convenience store peers traded at 12-14x multiples. The math was elementary: separation could create $15-20 billion in value overnight.

The boardroom dynamics were explosive. Directors who'd overseen Speedway's growth from regional chain to national powerhouse felt personally attacked. CFO Tim Griffith reportedly slammed the table, saying "We built this business—now Wall Street wants us to give it away?" But lead director John Surma, a former U.S. Steel CEO who understood conglomerate discounts intimately, argued for pragmatism: "Our job isn't to own assets—it's to maximize value. If the market pays more for separation, we separate."

The strategic review launched in October 2019 was unprecedented in scope. MPC hired three investment banks, two consulting firms, and a dedicated team of 50 employees to evaluate every option: IPO, spin-off, strategic sale, or status quo. They modeled 47 different scenarios, from selling individual regions to complex tax-free structures. The analysis filled 10,000 pages, which Heminger insisted on reading personally, annotating margins with mechanical pencil in his precise engineer's handwriting.

The pandemic initially seemed to kill any deal possibility. March 2020 saw Speedway's fuel volumes crater 70% as lockdowns emptied highways. Same-store merchandise sales collapsed. The business that generated $750 million in quarterly EBITDA suddenly barely broke even. Elliott went silent, their activism seemingly overtaken by survival concerns. Inside MPC, relief mixed with frustration—the strategic review had consumed enormous resources for apparently nothing.

But Seven & i Holdings, the Japanese owner of 7-Eleven, saw opportunity where others saw catastrophe. CEO Ryuichi Isaka had been studying Speedway for years, recognizing that combining it with 7-Eleven's 9,800 U.S. stores would create an unassailable convenience retail platform. While competitors retreated, Isaka flew to Ohio in May 2020—one of the first international executives to travel post-pandemic—for secret negotiations with Heminger.

The initial offer was insulting: $18 billion, barely 8x Speedway's normalized EBITDA. Heminger's response was classic: he pulled out a thick binder of Speedway's operating metrics, showing store-by-store performance, customer loyalty scores, and real estate values. "This isn't distressed merchandise," he told Isaka. "This is the premier convenience retail platform in America, temporarily impacted by a black swan event. The price is $22 billion, or we walk."

The negotiation stretched through the summer of 2020, conducted through video calls that started at midnight Ohio time to accommodate Tokyo schedules. The sticking points were fascinating: not price, which settled at $21 billion, but operational details. Who would supply Speedway stores during the transition? How would loyalty programs integrate? What about Speedway's proprietary food brands that had cult followings in the Midwest? Each issue required careful choreography to preserve value while enabling separation.

The August 2020 announcement stunned the market for multiple reasons. First, the price—$21 billion was the largest acquisition in Seven & i's history and the biggest convenience store deal ever. Second, the timing—executing a mega-deal during a pandemic seemed either brilliant or insane. Third, the structure—an all-cash transaction that would deliver $16.5 billion after-tax to MPC, enabling massive capital returns while maintaining investment flexibility.

The regulatory review became a case study in careful stakeholder management. The FTC raised concerns about regional concentration, particularly in California where 7-Eleven and Speedway overlapped significantly. Rather than fight, Seven & i preemptively agreed to divest 293 stores to satisfy regulators. State attorneys general, unions, and community groups all needed reassurance that jobs and services would be preserved. MPC and Seven & i held 47 town halls, promising no store closures or job cuts for at least two years.

The integration planning revealed how sophisticated both companies had become. Speedway would maintain its brand and operating autonomy for 24 months while Seven & i learned the business. Japanese executives spent months in Speedway stores, studying everything from coffee preparation to employee scheduling. They were particularly fascinated by Speedway's made-to-order food program, which generated higher margins than anything in 7-Eleven's portfolio.

The May 2021 closing was bittersweet for MPC employees. Speedway had been part of Marathon's identity for decades—many executives started their careers managing stores. The farewell ceremony in Enon, Ohio featured emotional speeches from employees who'd spent entire careers building Speedway into America's third-largest convenience chain. But there was also recognition that Speedway needed resources and focus that MPC, increasingly concentrated on energy transition, couldn't provide.

The capital allocation following the sale validated the strategic logic. MPC announced a $10 billion share buyback, reducing share count by 35%. Debt dropped to investment-grade metrics. Most importantly, the company had $5 billion in dry powder for renewable diesel investments and other energy transition initiatives. The same Elliott Management that had agitated for change declared victory, with Singer personally calling Heminger to say, "You did the right thing, the right way."

The Speedway sale's impact transcended financial metrics. It demonstrated that MPC's leadership could make hard strategic choices, even when they contradicted decades of empire-building instinct. In selling their crown jewel at peak value to fund transformation, MPC showed rare corporate discipline. As one board member reflected, "The hardest thing in business isn't buying assets—it's knowing when to sell them."

VIII. Modern Operations & Energy Transition

Inside Marathon Petroleum's massive Garyville, Louisiana refinery, a transformation is underway that captures the essence of modern energy economics. In one section, traditional crude distillation towers process 600,000 barrels daily of Canadian heavy and Bakken light crudes—the backbone of American transportation fuel. A quarter-mile away, gleaming new hydrotreaters convert soybean oil and animal fats into renewable diesel, identical in molecular structure to petroleum diesel but with 60% lower lifecycle emissions. This physical juxtaposition—fossil and renewable infrastructure literally sharing fence lines—embodies MPC's strategic balancing act.

The current refining footprint reads like a geography lesson in American energy. MPC operates the Dickinson, North Dakota renewables facility with capacity to produce 184 million gallons per year of renewable diesel, while the Martinez Renewable Fuels joint venture with Neste Corporation can produce 730 million gallons annually. The traditional refining system remains massive: thirteen refineries processing approximately 2.9 million barrels per calendar day from Texas City to Detroit, Canton to Los Angeles. Each facility optimized for specific crude slates, product demands, and regional dynamics that only locals truly understand.

The MPLX master limited partnership represents MPC's midstream crown jewel, though "crown jewel" understates its strategic importance. With 2024 generating $6.4 billion in adjusted EBITDA, MPLX provides the steady cash flows that enable MPC's aggressive capital returns and energy transition investments. The partnership owns 11,000 miles of pipelines, 63 million barrels of storage capacity, and gathering systems across every major U.S. shale basin. But MPLX's real value lies in its connectivity—the ability to move molecules efficiently from wellhead to refinery to market, capturing margins at every step.

The Martinez facility transformation from petroleum refinery to renewable diesel production exemplifies MPC's transition strategy. The former refinery has been repurposed using Topsoe's HydroFlex technology to convert bio-feedstocks into renewable diesel, currently operating at 260 million gallons per year with expansion to 730 million gallons expected. The conversion wasn't just about installing new equipment—it required reimagining an entire industrial ecosystem, from feedstock sourcing to product distribution.

The renewable diesel economics reveal both opportunity and challenge. The Martinez facility is currently not profitable, with challenges expected until full nameplate capacity is achieved. Yet management remains confident that at full capacity, Martinez will become "one of the more profitable renewable diesel facilities" in the country. The key lies in feedstock flexibility—the ability to process everything from used cooking oil to soybean oil to tallow, switching based on availability and pricing.

MPC estimates its conversion of the Martinez facility will reduce manufacturing greenhouse gas emissions by 60%, total criteria air pollutants by 70%, and water use by 1 billion gallons annually. These aren't just environmental wins—they're economic advantages in California's carbon-constrained market where Low Carbon Fuel Standard credits can generate hundreds of millions in additional revenue.

The operational excellence that defined Marathon's fossil fuel success now drives its renewable evolution. At Dickinson, North Dakota, what was once the nation's second-largest renewable diesel facility operates with the same relentless efficiency metrics as traditional refineries: 95%+ utilization, industry-leading yields, minimal unplanned downtime. The facility processes local soybean oil and corn oil, creating a circular agricultural economy that resonates with Midwest farmers who've become unexpected allies in the energy transition.

The integration of renewable and traditional operations creates unexpected synergies. Hydrogen produced for renewable diesel processing can also desulfurize petroleum products. Heat integration between units reduces overall energy consumption. Most importantly, the operational expertise developed over decades in petroleum refining—catalyst management, process optimization, safety protocols—transfers directly to renewable operations.

In Q4 2024, MPC established a separate Renewable Diesel segment to enhance comparability with peers, recognizing renewable diesel as a distinct business requiring dedicated management focus and capital allocation. This organizational change signals more than accounting clarity—it represents a fundamental recognition that renewable fuels aren't a side project but a core business demanding equal attention to traditional refining.

The market dynamics facing MPC's traditional refining business remain surprisingly robust despite energy transition narratives. U.S. refining capacity has actually declined by 1 million barrels per day since 2019 as smaller, less efficient refineries close. Meanwhile, global oil demand continues growing, albeit at a decelerating pace. This supply-demand imbalance, combined with MPC's scale advantages, positions the company to generate substantial cash flows even as it pivots toward renewables.

The capital allocation framework emerging from this dual-track strategy is elegantly simple: maximize cash from traditional assets, invest selectively in renewables, return excess capital to shareholders. In 2024, MPC generated approximately $7.5 billion in free cash flow while investing $1.2 billion in growth projects, primarily renewable diesel and midstream expansion. The remaining cash funded $10.2 billion in share repurchases and dividends, among the industry's most aggressive return programs.

Environmental regulations increasingly shape operational decisions. California's Advanced Clean Cars II rule mandating 100% zero-emission vehicle sales by 2035 might seem threatening, but MPC's West Coast refineries are already pivoting to jet fuel and marine fuel production where electrification faces greater challenges. The Inflation Reduction Act's renewable fuel tax credits, while complex and evolving, provide crucial support for renewable diesel economics during the technology learning curve.

The technology portfolio extends beyond renewable diesel. MPC is exploring renewable naphtha for petrochemical feedstock, sustainable aviation fuel for airline customers desperate to meet emissions targets, and even "blue" hydrogen from natural gas with carbon capture. Each technology is evaluated through the same rigorous lens: can it generate returns above the cost of capital while reducing emissions? The discipline to say no to scientifically interesting but economically marginal projects preserves capital for truly transformative investments.

Labor relations in this transition prove surprisingly collaborative. The United Steelworkers union, representing thousands of refinery workers, initially viewed renewable fuels with suspicion—would green jobs replace traditional roles? MPC's approach of converting existing refineries rather than building greenfield facilities meant job preservation with reskilling. A petroleum process operator can become a renewable diesel operator with modest training. This labor continuity maintains institutional knowledge while reducing transition friction.

The supply chain transformation required for renewable feedstocks rivals the complexity of crude oil logistics. MPC now manages relationships with rendering plants, soybean processors, and restaurant grease collectors—a far cry from traditional crude oil suppliers. The company has invested in feedstock pretreatment facilities to ensure consistent quality and built strategic inventory to buffer against agricultural seasonality. This vertical integration into feedstock processing provides competitive advantages similar to those refiners historically enjoyed through crude oil production ownership.

Looking ahead, MPC's operational strategy appears increasingly prescient. By maintaining world-class traditional refining while building renewable fuel capabilities, the company preserves optionality in an uncertain energy future. If petroleum demand declines faster than expected, renewable capacity provides a growth avenue. If the energy transition proceeds more slowly, traditional assets generate cash to fund patient transformation. Either way, MPC's operational excellence—the blocking and tackling Heminger emphasized—remains the constant that drives value creation regardless of feedstock or product slate.

IX. Playbook: Business & Investment Lessons

M&A Excellence: The Art of Strategic Patience

Marathon's acquisition track record reveals a consistent pattern: wait for distress, move decisively, integrate methodically. The Ashland joint venture taught them that the best deals preserve optionality—structure agreements with clear exit paths rather than permanent commitments. The Andeavor acquisition demonstrated that mega-deals succeed through operational logic, not financial engineering. When Heminger and Goff negotiated directly rather than through bankers, they saved hundreds of millions in fees while creating superior alignment. The Speedway divestiture proved the ultimate M&A discipline: knowing when to sell the crown jewel.

The company's M&A philosophy centers on operational synergies rather than multiple expansion. Every deal must answer three questions: Does it enhance our competitive position? Can we integrate it without disrupting base operations? Will it generate returns above our cost of capital through cycles? This framework killed dozens of potential transactions that looked attractive on paper but failed operational scrutiny. The discipline to walk away from bad deals proves as valuable as the courage to pursue good ones.

Timing the Cycle: Converting Volatility into Value

MPC's cycle management resembles a masterclass in commodity market navigation. The company maintains what executives call a "cycle clock"—a proprietary model tracking dozens of indicators from crack spreads to inventory builds to shipping rates. But the real insight isn't predicting cycles—it's positioning to profit regardless of timing. High operational leverage means small margin improvements generate massive cash flow increases. Low financial leverage means the balance sheet survives margin compression without distress.

The capital allocation through cycles follows a contrarian pattern. When margins peak and competitors chase growth, MPC returns cash to shareholders. When margins trough and others retrench, MPC invests in capacity and capability. This countercyclical approach requires institutional patience that public markets rarely reward in real-time but consistently appreciate retrospectively. The Garyville expansion during 2011's margin collapse exemplified this philosophy—a $2.2 billion bet that margins would recover, which generated billions in cumulative value.

Capital Allocation Mastery: The Power of Simplicity

MPC's capital allocation framework strips away complexity to focus on fundamental value creation. Growth capital must generate 15%+ unlevered returns. Maintenance capital preserves but doesn't expand earning power. Everything else goes to shareholders through dividends and buybacks. This simplicity enables rapid decision-making and clear accountability. Project sponsors know their hurdle rates. The board knows its priorities. Investors know what to expect.

The share repurchase program represents perhaps the most aggressive in American energy. Since 2011, MPC has retired over 40% of shares outstanding, creating tremendous per-share value accretion. But this isn't mindless buying—the company accelerates repurchases when the stock trades below intrinsic value and moderates when valuations extend. The ability to time both operations and capital allocation creates a powerful value-creation flywheel.

Operational Leverage: Scale as Competitive Moat

MPC's scale advantages compound in ways that smaller competitors can't replicate. The company's crude purchasing power enables 10-15 cent per barrel discounts. Its logistics network provides flexibility to redirect products to highest-value markets within hours. Its technical expertise allows rapid deployment of best practices across facilities. These advantages might seem modest individually but aggregate to hundreds of millions in annual value creation.

The operational leverage extends to regulatory compliance and technology development. When California mandates new fuel specifications, MPC spreads compliance costs across 3 million barrels of daily production. When renewable diesel technology advances, lessons from Martinez immediately transfer to Dickinson. This ability to amortize both costs and knowledge across a massive base business provides sustainable competitive advantages that pure-play renewable companies can't match.

Portfolio Management: Strategic Coherence Through Simplification

The evolution from integrated oil company to pure-play refiner to renewable fuel pioneer demonstrates portfolio management discipline rare in corporate America. Each transformation involved shedding successful businesses to focus on core competencies. The Marathon Oil spinoff separated upstream from downstream. The Speedway sale removed retail from refining. Now, renewable fuels emerge as a distinct segment requiring dedicated resources.

This progressive simplification might seem like retreat, but it actually represents strategic advance. By focusing on what MPC does best—converting feedstocks into transportation fuels—the company maximizes return on invested capital while minimizing complexity. The clarity of purpose enables better capital allocation, clearer communication, and faster decision-making. In industries where conglomerates traditionally dominated, MPC proves that focus beats breadth.

Stakeholder Balance: The Quadruple Bottom Line

MPC's stakeholder management transcends typical corporate rhetoric about balance. The company explicitly manages four constituencies: shareholders (who provide capital), employees (who provide expertise), communities (who provide social license), and regulators (who provide operating permission). Each major decision evaluates impact across all four dimensions. The Speedway sale, for instance, maximized shareholder value while preserving jobs, maintaining community presence, and satisfying regulatory concerns.

This stakeholder balance proves particularly crucial in refining, where a single explosion can destroy billions in value and community opposition can block expansions regardless of economics. MPC's safety record—consistently top-quartile performance across all facilities—isn't just ethical imperative but economic necessity. The $500 million annually invested in environmental compliance and safety might seem like dead weight to financial engineers, but it's actually the foundation enabling everything else.

The most sophisticated aspect of MPC's playbook is recognizing that these elements interconnect and reinforce. M&A excellence enables scale advantages. Scale advantages generate cash for capital allocation. Capital allocation funds operational improvements. Operational improvements attract M&A opportunities. This virtuous cycle, built over decades and protected zealously, represents MPC's true competitive moat—one that no competitor can quickly replicate regardless of capital availability.

X. Bear vs. Bull Analysis

Bear Case: The Structural Decline Scenario

The bear thesis begins with an uncomfortable truth: petroleum demand destruction isn't a question of if but when. Electric vehicle adoption, despite current growing pains, follows an exponential curve that will eventually devastate gasoline demand. California's 2035 internal combustion engine ban represents the first domino; other states and countries will follow. MPC's 2.9 million barrels of daily refining capacity could become stranded assets within two decades, worthless monuments to a fossil fuel era.

The energy transition threatens MPC asymmetrically compared to integrated oil majors. While ExxonMobil and Chevron can pivot to natural gas, chemicals, and even lithium production, MPC remains wedded to transportation fuels. Renewable diesel provides no real escape—it's a bridge fuel that will itself become obsolete as electrification advances. The company is essentially rearranging deck chairs on the Titanic, generating cash today from assets that won't exist tomorrow.

Regulatory risks multiply beyond simple demand destruction. Carbon pricing mechanisms, whether explicit taxes or cap-and-trade systems, will systematically disadvantage fossil fuel refining. Environmental justice movements increasingly target refineries as symbols of corporate pollution, creating permitting nightmares for expansions and modernizations. The EPA's recent particulate matter standards alone could require billions in additional compliance costs. Each new regulation chips away at refining economics, death by a thousand regulatory cuts.

The commodity cycle exposure that historically created opportunity now represents existential threat. Refining margins have compressed structurally as global capacity exceeds demand. The "golden age" of 2022-2023 when crack spreads exploded won't repeat because it reflected temporary supply-demand imbalances from Russian sanctions and COVID recovery. Future margins will revert to historical means or worse, squeezing cash generation precisely when MPC needs capital for energy transition investments.

Competition intensifies from unexpected directions. International refiners, particularly in Asia and the Middle East, enjoy lower costs and fewer environmental constraints. Technology companies are entering energy with unlimited capital and no legacy infrastructure burdens. Even within renewable diesel, pure-play competitors like Diamond Green Diesel operate without the distraction and complexity of traditional refining. MPC fights a multi-front war with one hand tied behind its back.

The capital allocation strategy, while shareholder-friendly today, might prove short-sighted tomorrow. The $10+ billion returned annually to shareholders could instead fund massive renewable energy investments or technology acquisitions. By prioritizing near-term returns over long-term transformation, MPC risks becoming the energy sector's version of Blockbuster—highly profitable until suddenly irrelevant.

Bull Case: The Energy Realism Thesis

The bull thesis rests on energy pragmatism: the world needs liquid transportation fuels for decades, and MPC owns the best assets to provide them. MPC expects demand growth to exceed the net impact of capacity additions and rationalizations through the end of the decade, supporting an enhanced mid-cycle environment for refining. Even aggressive EV adoption scenarios show global oil demand growing through 2030 and plateauing rather than collapsing thereafter. Aviation, shipping, petrochemicals, and heavy transport have no viable alternatives to liquid fuels for the foreseeable future.

MPC's competitive position actually strengthens as the industry contracts. Smaller, less efficient refineries close first, reducing supply. Environmental regulations create barriers to new construction. The result: a oligopolistic industry structure where survivors like MPC enjoy pricing power unimaginable during the capacity overbuild era. The company's scale, efficiency, and geographic diversity position it as the last refiner standing in many markets.

The renewable diesel pivot represents genuine option value, not greenwashing. With the Dickinson facility producing 184 million gallons annually, the Martinez joint venture targeting 730 million gallons, and additional feedstock aggregation assets, MPC has built one of America's largest renewable diesel platforms. As traditional biodiesel producers struggle with feedstock costs and technology challenges, MPC's operational excellence provides sustainable competitive advantages. The renewable business might not save the world, but it will generate attractive returns.

Geographic and product diversification provides resilience that bears underestimate. When California refining margins compress, Gulf Coast operations compensate. When gasoline demand weakens, jet fuel and petrochemical feedstocks provide support. This portfolio effect smooths earnings through cycles while providing multiple levers for value creation. The MPLX midstream partnership alone generates enough stable cash flow to support the dividend through any conceivable downturn.

The capital return program creates a compelling near-term value proposition regardless of long-term concerns. At current buyback rates, MPC will retire 10% of shares annually while maintaining a secure and growing dividend. For investors with 3-5 year time horizons, the combination of capital returns and modest multiple expansion could generate 15-20% annual returns even if the bear thesis eventually proves correct.

As of December 31, 2024, MPC maintained $3.2 billion in cash and $5 billion available on its revolving credit facility, while returning $1.6 billion to shareholders in Q4 through $1.3 billion in share repurchases and $292 million in dividends, with $7.8 billion remaining under share repurchase authorizations. This financial fortress provides flexibility to navigate any transition scenario while rewarding patient shareholders.

The technology and operational capabilities developed over 137 years won't suddenly become worthless. Process engineering expertise transfers across feedstocks. Supply chain management skills apply regardless of products. Safety and environmental excellence remain valuable whatever the energy source. MPC's human and intellectual capital provides option value that financial statements don't capture but strategic acquirers would pay premiums to obtain.

The Synthesis: Gradual Transition, Not Sudden Collapse

Reality likely lies between extremes. Petroleum demand will decline but gradually, providing decades of cash generation for disciplined operators. Renewable fuels will grow but remain niche, generating attractive returns without replacing traditional refining. Regulations will tighten but pragmatically, recognizing that economic disruption serves no one's interests. MPC will neither disappear nor dominate but will successfully navigate a middle path that rewards shareholders while adapting to energy transition realities.

The key insight for investors: MPC's value derives less from predicting the energy future than from operational excellence in the energy present. Whether processing crude oil or soybean oil, the company's ability to run assets efficiently, allocate capital wisely, and adapt strategically remains constant. In a world of energy uncertainty, betting on operational competence rather than commodity forecasts provides the margin of safety that intelligent investing requires.

XI. Grading & Final Thoughts

Overall Execution Grade: A-

Marathon Petroleum earns an A- for transforming from a regional Ohio producer into America's refining champion through disciplined capital allocation, operational excellence, and strategic patience. The grade reflects exceptional execution with minor deductions for renewable diesel growing pains and occasional stakeholder communication missteps.

Strategic Decisions Scorecard:

The 2011 spinoff from Marathon Oil: A+

Perfect timing, clean execution, immediate value creation. The independence unlocked focus and flexibility that enabled everything following.

The Ashland joint venture (1998-2005): B+

Smart structure, good synergies, but perhaps held too long. Earlier exit might have accelerated standalone value creation.

The Andeavor acquisition (2018): A

Transformational deal executed flawlessly. The only question: could they have paid less if they'd waited six months?

The Speedway divestiture (2021): A

Selling the crown jewel at peak valuation to fund transformation showed rare corporate courage. The price exceeded all expectations.

Renewable diesel investments: B

Strategically sound but operationally challenged. Martinez struggles remind us that operational excellence doesn't automatically transfer across technologies.

Capital allocation framework: A+

The combination of aggressive buybacks, growing dividends, and disciplined growth investment creates a value-creation machine that few companies match.

Comparison to Peers:

Versus Valero Energy: MPC operates more efficiently but Valero acted earlier on renewable diesel, gaining first-mover advantages. Valero's international exposure provides diversification MPC lacks. Edge: MPC domestically, Valero globally.

Versus Phillips 66: Both emerged from integrated oil companies around the same time. Phillips 66's chemicals and midstream exposure provides more stability. MPC's pure refining focus enables higher returns through cycles. Edge: Depends on risk tolerance.

Versus integrated majors: MPC can't match the resource depth of ExxonMobil or Chevron, but its focused strategy generates superior returns on capital employed. For pure refining exposure, MPC provides cleaner investment thesis. Edge: MPC for refining, majors for energy diversification.

Biggest Surprises from the Research:

First, the consistency of operational excellence across 137 years and multiple ownership structures. Whether independent, part of Standard Oil, owned by U.S. Steel, or standalone public company, Marathon maintained engineering discipline and safety focus that transcended corporate structure.

Second, the willingness to sell crown jewel assets at the right price. Most companies become emotionally attached to successful businesses. MPC's sale of Speedway—a business they built from nothing into a $21 billion asset—showed remarkable strategic discipline.

Third, the importance of geography in refining economics. MPC's concentration in the U.S. initially seemed like weakness versus globally diversified competitors. Instead, it became strength as U.S. energy independence and infrastructure advantages created structural competitive advantages.

Fourth, how little the energy transition has actually impacted current operations. Despite endless headlines about peak oil and stranded assets, MPC's traditional refining business generates record cash flows. The disconnect between narrative and numbers remains striking.

What Other Companies Can Learn:

Focus beats diversification when you possess genuine operational advantages. MPC's decision to concentrate on refining rather than maintain integration up and down the energy chain enabled excellence that generalists couldn't match.

Patient capital allocation creates more value than aggressive growth. MPC's willingness to return capital when opportunities don't meet hurdle rates, then invest aggressively when they do, generated superior long-term returns versus peers who always stayed fully invested.

Cultural consistency matters more than strategic brilliance. MPC's engineering culture—focused on safety, efficiency, and continuous improvement—survived multiple owners and strategies. This cultural bedrock enabled successful execution regardless of strategic direction.

Stakeholder management isn't separate from value creation—it enables it. MPC's emphasis on safety, environmental compliance, and community relations might seem like overhead, but it actually provides the social license that permits profitable operations.

The best partnerships have built-in exits. From the Ashland joint venture to the Speedway sale agreement, MPC structures deals with clear separation mechanisms. This optionality enables value-maximizing outcomes as circumstances change.

Final Assessment:

Marathon Petroleum represents American industrial capitalism at its most effective: identifying comparative advantages, exploiting them relentlessly, and adapting pragmatically as conditions change. The company isn't perfect—renewable diesel struggles and occasional regulatory conflicts reveal limitations. But the combination of operational excellence, capital discipline, and strategic flexibility creates a value-creation platform that should reward shareholders through energy transition uncertainties.

For long-term investors, MPC offers a compelling proposition: own the best traditional refining assets generating massive cash flows today, with free options on renewable fuels and energy transition opportunities tomorrow. The bear case of stranded assets deserves consideration but seems premature given petroleum demand resilience and MPC's adaptation capabilities.

The ultimate test comes in the next decade as energy transition accelerates and traditional refining potentially peaks. Can MPC successfully pivot to renewable fuels and alternative energy while maintaining operational excellence? History suggests yes—this company has reinvented itself repeatedly over 137 years. Betting against that track record seems unwise, even as the energy landscape transforms around it.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube