Emerson Electric: The Automation Pioneer's Next Act

I. Introduction & Episode Roadmap

Picture this: It's 2022, and in a gleaming St. Louis boardroom, Lal Karsanbhai—barely a year into his CEO role at Emerson Electric—is making the biggest bet of his career. He's about to sell off 55% of the company's climate technologies business for $14 billion to Blackstone, essentially cutting away a third of Emerson's revenue in one stroke. For a 132-year-old company that had never met a business it didn't want to keep, this was heresy. Yet Karsanbhai saw what others didn't: the future of industrial automation wasn't in being everything to everyone—it was in being indispensable to the factories, refineries, and critical infrastructure that power the global economy.

How did a company that started making electric fans in 1890 become a $78 billion automation powerhouse? How did it survive two world wars, countless recessions, and the digital revolution while maintaining 68 consecutive years of dividend increases—a feat matched by only a handful of companies globally? And why, after more than a century of patient accumulation, did it suddenly decide to radically transform itself?

This is the story of Emerson Electric—a company that built its empire on the unglamorous but essential task of making things run. From electric motors to process control systems, from airplane armament to artificial intelligence-powered industrial software, Emerson has repeatedly reinvented itself while maintaining an almost religious devotion to operational excellence. It's a playbook that combines Germanic precision with American ambition, conservative financial management with bold strategic pivots.

We'll explore how two Scottish immigrants and a Civil War veteran created an industrial giant, how a series of legendary CEOs built one of the most disciplined corporate cultures in America, and how today's leadership is betting everything on becoming the dominant force in industrial automation. Along the way, we'll unpack the lessons: when to diversify versus focus, how to execute transformative M&A, and what it really takes to sustain excellence across centuries.

The stakes couldn't be higher. As the world reshores manufacturing, digitizes infrastructure, and races toward net-zero emissions, the companies that control industrial automation will essentially control the means of production for the 21st century. This is Emerson's story—and it's far from over.

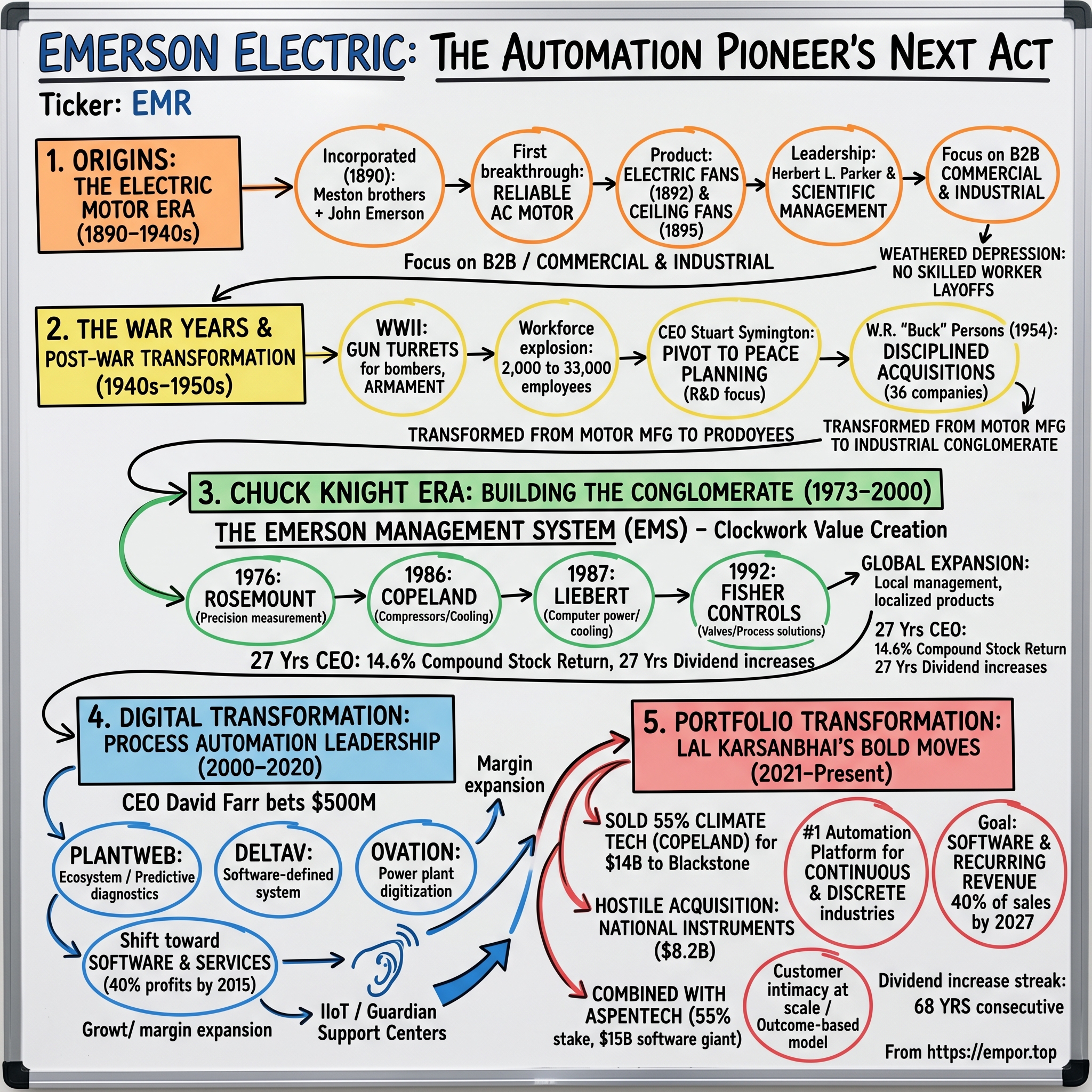

II. Origins & The Electric Motor Era (1890–1940s)

The August heat in St. Louis was suffocating in 1890. Inside a modest workshop, two Scottish-born brothers, Charles and Alexander Meston, were tinkering with what would become their obsession: a reliable alternating current motor. The brothers had immigrated to America with engineering skills and entrepreneurial hunger, but what they lacked was capital. Enter John Wesley Emerson—a fascinating character who embodied the American dream. A former Union Army officer who'd fought at Shiloh, turned judge, turned lawyer, Emerson saw opportunity where others saw only spinning copper and magnets.

On September 24, 1890, The Emerson Electric Manufacturing Company was officially incorporated with $50,000 in capital—roughly $1.7 million in today's dollars. Emerson himself became the financial backer and president, lending his name to the enterprise, though he'd never touched a wrench in his life. The Meston brothers brought the technical expertise. This division of labor—financial acumen paired with engineering excellence—would become an Emerson hallmark for the next century.

Their first breakthrough wasn't glamorous but it was genius: electric fans. As American cities grew vertically in the 1890s, skyscrapers created a new problem—how to make upper floors bearable in summer heat. Emerson's electric fans weren't the first on the market, but they were the most reliable. While competitors' motors burned out or ran erratically on the unstable electrical grids of the era, Emerson's ran steady. By 1892, they were selling fans across North America, establishing a reputation that would outlive the founders.

The real innovation came in 1895 when Emerson introduced the first electric ceiling fan. Think about the audacity of this: mounting a heavy electric motor to a ceiling in an era when most people still feared electricity might burn their houses down. Yet it worked brilliantly, making high-rise buildings suddenly livable year-round. Within a decade, Emerson ceiling fans were spinning in hotels from New York to San Francisco, in Southern plantation homes, and in the new department stores reshaping American commerce.

By 1920, under the leadership of Herbert L. Parker—a detail-obsessed engineer who reportedly tested every hundredth motor personally—Emerson had become synonymous with quality. Parker instituted what he called "scientific management," borrowing from Frederick Taylor but adding his own twist: every worker was trained not just to build motors, but to understand why each component mattered. This wasn't just assembly; it was craftsmanship at industrial scale.

The numbers tell the story: from $50,000 in initial capital to $2.8 million in annual sales by 1920. But the real asset wasn't on the balance sheet—it was the reputation. When General Electric or Westinghouse wanted to outsource specialized motor production, they came to Emerson. The company had positioned itself as the Intel Inside of the electric motor age—not always the brand on the outside, but the technology that made everything run.

Parker also pioneered something radical for the time: profit-sharing with employees. Starting in 1924, workers received bonuses based on company performance—creating a culture of ownership that would persist through generations. As one veteran employee recalled decades later: "We didn't work for Emerson; we were Emerson."

The 1920s brought both opportunity and challenge. Consumer electricity adoption exploded—by 1929, 70% of American homes had power, up from just 8% in 1907. Emerson rode this wave, expanding into water pumps, industrial motors, and even early refrigeration systems. But they also made a crucial strategic decision: while competitors chased consumer markets, Emerson doubled down on commercial and industrial applications. Why? Higher margins, longer relationships, and less susceptibility to consumer whims.

This focus on B2B would prove prescient. When the Great Depression hit in 1929, consumer spending collapsed, but factories still needed motors, buildings still needed ventilation, and infrastructure still needed maintenance. Emerson's revenue dropped 40% from 1929 to 1933—painful, but far better than the 70-80% collapses seen by consumer-focused competitors. More importantly, they didn't lay off their skilled workers, choosing instead to cut hours and executive pay. This decision would pay dividends when recovery came.

By 1940, Emerson Electric had weathered five decades of booms, busts, and technological upheaval. They'd built a culture of engineering excellence, financial discipline, and employee loyalty that would serve them well in the trials ahead. Little did they know that world events would soon transform them from a successful regional manufacturer into a critical player in the American war machine—and set the stage for their evolution into an industrial conglomerate.

III. The War Years & Post-War Transformation (1940s–1950s)

December 8, 1941. As President Roosevelt addressed Congress about "a date which will live in infamy," Stuart Symington was already on a train to St. Louis. The 40-year-old executive had just been recruited to run Emerson Electric, and Pearl Harbor had transformed his mandate overnight. Symington wasn't an engineer—he was a dealmaker who'd built his reputation turning around struggling companies. But what Emerson needed now wasn't a turnaround artist; it needed a wartime production czar.

Symington's first day at Emerson was theatrical. He gathered all 2,000 employees in the main factory floor and delivered a speech that workers would still quote decades later: "Gentlemen—and ladies—we are no longer in the business of making motors and fans. We are in the business of winning a war. Every rivet you place, every wire you solder, might save an American life." Within 72 hours, he had War Department officials touring the facility, calculating how to convert fan assembly lines into weapons production.

The transformation was staggering. By March 1942, Emerson's factories were churning out gun turrets for B-17 Flying Fortresses and B-24 Liberators. The company developed and manufactured the first airborne radar systems, the computing gunsights that gave American bombers their lethal accuracy, and specialized electric motors for everything from submarine periscopes to tank turrets. The precision that once went into making ceiling fans spin silently now went into ensuring a gun turret could track a Messerschmitt at 300 miles per hour.

The numbers beggar belief: Emerson's workforce exploded from 2,000 to 33,000 employees. They operated 24 hours a day, seven days a week. Women comprised 40% of the workforce—"Rosie the Riveters" who could calibrate a gun sight to thousandths of an inch. The company built entire new factories, including a massive underground facility in case of air raids (which, thankfully, never came to Missouri). By 1944, Emerson had become the world's largest manufacturer of airplane armament.

Here's what's remarkable: Emerson ranked 52nd among all U.S. corporations in the value of World War II military production contracts—ahead of household names like Coca-Cola, Procter & Gamble, and Union Pacific. They produced over $500 million worth of armaments (roughly $8 billion in today's dollars), including 75% of all gun turrets used by the U.S. Air Force. The company that had started making fans to cool people down was now making weapons that would help bring down the Axis powers.

But Symington understood something crucial: this windfall was temporary. Even as production peaked in 1944, he was planning for peace. He created what he called "shadow teams"—groups of engineers working on civilian applications for military technology. Radar became industrial sensing. Precision manufacturing techniques developed for gun sights were applied to instrumentation. The organizational capabilities built to manage 33,000 workers would be redirected toward peacetime expansion.

V-J Day in August 1945 brought celebration and crisis in equal measure. Within six months, military contracts worth $400 million annually vanished. Employment crashed from 33,000 to 8,000. Lesser companies might have collapsed, but Symington executed a masterful pivot. He used the company's sterling wartime reputation to acquire distressed competitors, picking up valuable patents and customer relationships for pennies on the dollar. He convinced the board to maintain R&D spending even as revenues plummeted, betting that American industry would boom once soldiers returned home.

The bet paid off spectacularly. By 1950, Emerson's civilian sales had not only recovered but exceeded wartime peaks. They were making motors for the washing machines in new suburban homes, fans for the office buildings rising in every American city, and components for the nascent television industry. The company had also learned something vital: diversification was survival. Never again would they depend on a single market or technology.

Enter W.R. "Buck" Persons in 1954—a name that sounds like a character from a Western but who was actually a Harvard-trained lawyer with an accountant's heart. Where Symington had been charismatic and bold, Persons was methodical and acquisitive. He looked at Emerson's strong balance sheet and solid cash generation and saw a platform for empire building.

Persons pioneered what would become the Emerson playbook: disciplined acquisition. Between 1954 and 1973, he acquired 36 companies—not random purchases, but carefully selected firms that either expanded Emerson's technological capabilities or gave them entry into new markets. Ridge Tool Company brought them into professional tools. U.S. Electrical Motors expanded their industrial presence. In-Sink-Erator gave them a consumer brand with pricing power.

Each acquisition followed the same pattern: identify a well-run company in a fragmented industry, pay a fair price (never overpay), integrate operations while maintaining local management, apply Emerson's operational disciplines, and watch margins expand. It was private equity before private equity existed, except Persons never sold—he accumulated.

The results were extraordinary. When Persons retired in 1973, Emerson had 82 plants, 31,000 employees, and $800 million in sales—a 20-fold increase from when he started. More importantly, he had transformed Emerson from a motor manufacturer into a diversified industrial conglomerate with leadership positions in multiple markets. The company now had the scale and scope to weather any single industry downturn.

But perhaps Persons' greatest contribution was cultural. He instituted what he called "planning discipline"—every division had to present detailed five-year plans, updated annually, with specific metrics and accountability. Managers who hit their numbers were rewarded lavishly; those who didn't were replaced quickly but respectfully. This wasn't cruel; it was clarity. Everyone knew the rules of the game.

As Persons prepared to hand over the reins in 1973, he had one last task: choosing his successor. He needed someone who could take his system and supercharge it, someone who understood both operations and strategy, someone who could think globally while executing locally. He found that person in Charles F. Knight—Chuck to everyone who knew him—a 37-year-old executive who would transform Emerson from a successful American conglomerate into a global industrial powerhouse. The stage was set for the next act in the Emerson story.

IV. The Chuck Knight Era: Building an Industrial Conglomerate (1973–2000)

Chuck Knight's first board meeting as CEO in October 1973 was a disaster—and he'd planned it that way. The 37-year-old had just taken the helm of Emerson Electric, and instead of presenting a rosy vision, he delivered what one director later called "the most brutally honest assessment I'd ever heard from a chief executive." Knight's message was simple: Emerson was good, but good was the enemy of great. Margins were acceptable but not exceptional. International presence was minimal. R&D spending was scattered. Most damningly, there was no systematic way to drive continuous improvement across the company's sprawling operations.

"We're playing checkers while our global competitors are playing chess," Knight told the stunned board. Then he unveiled his solution: the Emerson Management System, or EMS—a framework that would become legendary in corporate America and be studied at Harvard Business School for decades.

The EMS wasn't revolutionary in its components but in its synthesis and execution. It combined elements of strategic planning, operational excellence, and financial discipline into what Knight called "a clockwork mechanism for creating value." Every division would follow the same planning cycle: five-year strategic plans updated annually, detailed competitive analyses, technology roadmaps, and—critically—specific financial targets with no excuses accepted for missing them.

But here's what made Knight different from the slash-and-burn CEOs of his era: he coupled accountability with investment. Miss your targets? You were gone. But hit them? Knight would shower you with resources to grow faster. He created what he called "profit pools"—maps of where money was actually made in each industry—and directed investment toward the deepest pools with surgical precision.

The first major test of Knight's strategy came in 1976 with the acquisition of Rosemount Inc., a Minnesota-based maker of precision measurement instruments. The company was struggling, but Knight saw something others missed: Rosemount's sensors were critical for process control in refineries, chemical plants, and pharmaceutical facilities—industries where downtime cost millions per hour. These customers would pay premium prices for reliability. Under Emerson's operational discipline, Rosemount's margins expanded from 8% to over 20% within three years.

Knight's acquisition philosophy was distinctly different from the conglomerate builders of the 1960s. While ITT and Litton Industries bought anything that moved, Knight focused exclusively on industrial technologies with competitive moats. His criteria were rigid: the target had to be number one or two in its market, have sustainable differentiation, offer cross-selling opportunities with existing Emerson businesses, and be run by management willing to embrace the EMS (or willing to be replaced).

The Copeland Corporation acquisition in 1986 exemplified this approach. Copeland made compressors for air conditioning and refrigeration—not sexy, but absolutely critical. Every supermarket, every data center, every hospital needed reliable cooling. Knight paid $750 million—a fortune at the time—but he understood something fundamental: as the world got hotter and more digital, cooling would only become more critical. By 2000, Copeland was generating over $2 billion in revenue with operating margins above 15%.

But Knight's masterpiece was the 1992 acquisition of Fisher Controls for $1.28 billion. Fisher made the valves and regulators that controlled flow in everything from oil refineries to pharmaceutical plants. Combined with Rosemount's sensors and Emerson's other process control businesses, Knight had assembled something unprecedented: an end-to-end automation platform for continuous process industries. Competitors sold components; Emerson could now sell complete solutions.

The international expansion under Knight was equally methodical. Rather than the typical American approach of sending expats to run foreign operations, Knight insisted on local management who understood local markets. But—and this was crucial—they all had to adopt the EMS. The planning calendars were synchronized globally. Best practices were shared religiously. A plant manager in Shanghai could learn from a breakthrough in St. Louis within weeks.

By 1990, international sales had grown from virtually nothing to 40% of revenue. Emerson wasn't just exporting from America; they were manufacturing in 20 countries, designing products for local markets, and competing head-to-head with Siemens in Germany, Schneider in France, and Mitsubishi in Japan.

The financial discipline Knight imposed was almost military in its precision. He instituted a practice called "President's Operating Report"—every month, every division president had to submit a detailed analysis of performance versus plan. Miss your numbers once? You explained why. Twice? You explained your correction plan. Three times? You explained to your replacement. This sounds harsh, but Knight coupled it with unprecedented transparency. Every manager could see every other division's performance. Success was celebrated publicly; failure was addressed privately but swiftly.

The results spoke for themselves. During Knight's 27-year tenure, Emerson's stock delivered a compound annual return of 14.6%, outperforming the S&P 500 by nearly 4 percentage points annually. Revenue grew from $1.3 billion to $15.5 billion. Operating margins expanded from 9% to 19%. Most remarkably, Emerson increased its dividend for 27 consecutive years under Knight—a record that would continue long after his retirement.

But perhaps Knight's most important innovation was cultural. He created what he called "the Emerson leader"—executives who thought like owners, operated with discipline, and continuously improved their businesses. These weren't just managers; they were entrepreneurs within a corporate framework. The company became known as a CEO factory—David Farr (who would succeed Knight), George Tamke, Charlie Peters, and dozens of others who went on to run major corporations all learned the Emerson way under Knight.

Knight also understood something that many of his peers missed: operational excellence without innovation is a recipe for slow decline. So while he squeezed inefficiencies out of existing operations, he also poured money into R&D, but with a twist. Instead of centralized research labs working on blue-sky projects, Emerson's R&D was embedded in the business units, focused on solving specific customer problems. This produced less Nobel Prize-winning science but far more profitable products.

The 1987 acquisition of Liebert Corporation illustrated this perfectly. Liebert made cooling and power systems for computer rooms—a niche market in 1987. But Knight's team had noticed something: as businesses became more dependent on computers, even brief outages were catastrophic. Liebert's uninterruptible power supplies and precision cooling systems were becoming mission-critical infrastructure. Under Emerson, Liebert expanded from computer rooms to telecommunications, then to data centers. By 2000, what had been a $200 million acquisition was generating over $1 billion in revenue.

As Knight prepared to step down in 2000, he had one more transformation to execute: choosing his successor. He selected David Farr, a career Emerson executive who had run multiple divisions and understood both the discipline of the EMS and the need for evolution. Knight's parting advice to Farr was prescient: "The industrial world is going digital. Emerson has to lead that transformation or become irrelevant."

Knight left behind more than a successful company—he left a system, a culture, and a philosophy that had turned a Midwestern manufacturer into one of the world's premier industrial companies. The Emerson Management System he created would be studied, copied, and adapted by hundreds of companies worldwide. But as Farr would soon discover, maintaining excellence while transforming for the digital age would require rethinking some of Knight's most sacred principles. The clockwork mechanism would need new gears.

V. Digital Transformation & Process Automation Leadership (2000–2020)

David Farr's first major decision as CEO in October 2000 seemed like corporate suicide. Standing before 300 of Emerson's top executives, he announced that the company would bet $500 million—nearly 10% of its market cap—on something called PlantWeb. The room was silent. Here was Emerson, the paragon of operational discipline, about to gamble on software and sensors when the dot-com bubble was literally bursting around them. NASDAQ had peaked just six months earlier. Cisco, the poster child of the digital revolution, had lost 70% of its value. And Farr wanted to turn an industrial conglomerate into a technology company?

"Gentlemen," Farr said, breaking the silence, "our customers don't want valves and sensors. They want to know their plants won't explode, their products will meet specifications, and their operations will run profitably. We're going to give them that—not through better hardware, but through intelligence."

PlantWeb wasn't just a product; it was a philosophy. Instead of selling individual components, Emerson would create an ecosystem where every valve, every sensor, every control system could communicate, creating what Farr called "the self-aware plant." Predictive diagnostics would identify failing equipment before it broke. Advanced analytics would optimize processes in real-time. Remote monitoring would let a engineer in Houston troubleshoot a platform in the North Sea.

The timing seemed terrible but was actually perfect. While Silicon Valley was imploding, industrial companies were desperately trying to squeeze more efficiency from aging infrastructure. A refinery shutdown cost $5 million per day. A pharmaceutical batch failure meant millions in lost product. PlantWeb promised to prevent both—and customers were willing to pay premium prices for that insurance.

The DeltaV digital automation system, launched in 2001, was even more ambitious. Traditional control systems were hardware-centric, requiring massive upfront engineering and physical rewiring for any changes. DeltaV was software-defined—configurations could be changed with clicks, not cables. It was virtualization before VMware made it cool, cloud architecture before AWS existed. A chemical plant could reconfigure production lines in hours instead of weeks.

But Farr understood something his predecessors might have missed: technology without domain expertise is worthless in industrial markets. So while Emerson hired software engineers by the thousand, they embedded them with process engineers who had spent decades in refineries, chemical plants, and pharmaceutical facilities. The result was software that actually solved real problems rather than creating new ones.

The 2008 financial crisis tested this digital transformation like nothing else could. Industrial production plummeted. Capital spending froze. Competitors slashed R&D and laid off engineers. Farr made a contrarian bet: he maintained R&D spending at 6% of sales and actually accelerated digital initiatives. Why? He'd noticed something curious in the data: while customers weren't buying new plants, they were desperate to make existing assets more efficient. Digital retrofit became Emerson's growth engine during the recession.

The Ovation platform for power generation showcased this perfectly. Power plants built in the 1970s were running on control systems that literally used paper charts. Ovation could digitize these dinosaurs, improving efficiency by 3-5%—which doesn't sound like much until you realize a 1,000-megawatt plant saves $10 million annually from a 3% improvement. By 2010, Ovation was controlling 20% of U.S. power generation capacity.

Farr also recognized that Industrial Internet of Things (IIoT) wasn't just about connecting devices—it was about making sense of the data tsunami. Emerson's Plantweb Insight applications used machine learning before it was trendy, analyzing patterns from millions of sensors to predict equipment failures weeks in advance. One customer, a Gulf Coast refinery, avoided a catastrophic compressor failure that would have cost $50 million in downtime and repairs—the warning came from algorithms that noticed a 0.02% vibration anomaly that human operators had missed.

The cultural transformation required for this digital pivot was massive. Emerson had to evolve from a hardware company that happened to have software to a solutions company where hardware and software were inseparable. This meant recruiting talent from Microsoft, Google, and Oracle—people who had never set foot in a refinery—and convincing them to move to St. Louis. It meant retraining thousands of sales engineers to sell outcomes instead of products. It meant cannibalizing profitable hardware sales with software subscriptions.

The financial model transformation was equally dramatic. Traditional industrial companies lived on capital expenditure cycles—boom when customers built new facilities, bust when they didn't. Software and services created recurring revenue streams that smoothed these cycles. By 2015, software and services represented 30% of Emerson's automation revenue but over 40% of profits, with gross margins above 60% compared to 35% for hardware.

Farr's leadership during the COVID-19 pandemic's early days (he retired in February 2021) proved the value of this transformation. While competitors struggled with supply chain disruptions and travel restrictions, Emerson could monitor and optimize customer operations remotely. Their Guardian support centers—essentially industrial mission control rooms—kept critical infrastructure running when engineers couldn't physically access sites.

The numbers validate Farr's digital bet. Despite facing the 2008 financial crisis, the oil price collapse of 2014-2016, and the early pandemic, Emerson's stock delivered a 565% total return during his tenure, significantly outperforming both the S&P 500 and industrial peers. Automation solutions grew from 35% of company revenue in 2000 to over 65% by 2020. Operating margins in the automation business expanded to 20.5%, rivaling pure software companies.

But Farr's greatest achievement might be preparing Emerson for its next transformation. As he handed the reins to Lal Karsanbhai in February 2021, he left behind not just a profitable company but one with the technological foundation to compete in an increasingly software-defined industrial world. The question was: would Karsanbhai continue the digital evolution, or would he revolution the entire portfolio? As we'd soon learn, he chose revolution.

VI. The Portfolio Transformation: Lal Karsanbhai's Bold Moves (2021–Present)

Lal Karsanbhai's first investor call as CEO in February 2021 was notably subdued. The soft-spoken engineer, who had spent 25 years at Emerson working his way up through the automation business, seemed like the quintessential insider pick—safe, steady, predictable. Wall Street analysts typed notes about "continuity" and "incremental improvement." They had no idea they were listening to a revolutionary in sheep's clothing.

Eighteen months later, those same analysts were scrambling to revise their models as Karsanbhai announced the unthinkable: Emerson would sell a 55% controlling stake in its climate technologies business to Blackstone for $14 billion. This wasn't trimming around the edges—this was sawing off a third of the company. Climate technologies had been part of Emerson since the Copeland acquisition in 1986. It generated $5 billion in annual revenue. It was profitable, growing, and benefiting from secular tailwinds around energy efficiency and electrification.

"Why would you sell a good business?" one analyst asked during the call. Karsanbhai's response revealed his strategic clarity: "Because good businesses trading at good multiples give us capital to buy great businesses that will define our future. We're not managing a portfolio; we're building the dominant automation platform for the next century."

The Blackstone deal was structured brilliantly. Emerson retained a 45% stake, ensuring participation in future upside while removing the business from consolidated financials. The $14 billion proceeds gave Karsanbhai a war chest that would make any activist investor salivate—except he had no intention of returning it to shareholders. He was going shopping.

The target was already in his sights: National Instruments. NI wasn't just another acquisition target; it was the missing piece in Emerson's automation puzzle. While Emerson dominated process industries—oil, chemicals, pharmaceuticals—NI owned test and measurement for discrete manufacturing: semiconductors, electronics, automotive. Combining them would create something unprecedented: an automation giant spanning both continuous and discrete industries.

But NI's board wasn't interested in selling. So Karsanbhai did something Chuck Knight would never have done: he went hostile. On January 17, 2023, Emerson publicly announced an unsolicited offer of $53 per share, valuing NI at $7.6 billion. The press release was a masterpiece of polite aggression, praising NI's technology while questioning its strategic direction and governance.

The eight-month battle that followed was corporate theater at its finest. NI's board rejected the initial offer as "inadequate." Emerson raised to $56. NI adopted a poison pill. Emerson launched a proxy fight. Activist investors circled like vultures. The financial media covered every thrust and parry. Behind the scenes, Karsanbhai was playing three-dimensional chess—negotiating with NI, managing his own board's patience, and keeping other potential bidders at bay.

The breakthrough came in May 2023 when Emerson agreed to pay $60 per share—$8.2 billion in total—but with conditions that showed Karsanbhai's discipline. The deal included specific revenue and cost synergy targets, intellectual property protections, and—critically—retention packages for key NI engineers. This wasn't a financial engineering play; it was a strategic transformation.

The integration has been masterful. Rather than the typical corporate integration (slash costs, eliminate duplicates, declare victory), Karsanbhai took a different approach. He appointed Ritu Favre—a 30-year technology veteran from the semiconductor industry—to lead the combined test and measurement business. Her mandate wasn't integration but innovation: combine NI's software prowess with Emerson's domain expertise to create new solutions neither company could have built alone.

The early results vindicate the strategy. In the first year post-acquisition, Emerson realized $100 million in cost synergies—exactly as promised—but more importantly, won $300 million in new contracts from customers who wanted integrated automation and test solutions. A leading electric vehicle manufacturer, for instance, used Emerson's combined platform to reduce battery testing time by 40% while improving quality control. These aren't just sales wins; they're proof points of a new competitive advantage.

But Karsanbhai wasn't done transforming the portfolio. The AspenTech transaction, completed in 2022, was perhaps even more strategically important than NI. Emerson contributed its industrial software businesses and $6 billion in cash for a 55% stake in the combined entity, creating a $15 billion industrial software powerhouse. This wasn't just adding software capabilities; it was positioning Emerson at the intersection of operational technology (OT) and information technology (IT)—where the real value creation in industrial automation will happen.

The strategic logic is compelling. AspenTech's optimization software helps refineries and chemical plants maximize yield and minimize energy consumption—often improving profitability by tens of millions annually. Combined with Emerson's control systems and instrumentation, customers get a closed-loop solution: AspenTech software determines optimal operating parameters, Emerson systems execute them, sensors verify results, and machine learning continuously improves performance.

Karsanbhai has also been ruthlessly pruning non-core assets. The InSinkErator disposal business—profitable but completely disconnected from automation—was sold for $3 billion. The Therm-O-Disc sensing business went for $1.8 billion. These weren't distressed sales; they were strategic divestitures of good businesses that didn't fit the automation-centric vision.

The cultural transformation under Karsanbhai has been equally dramatic. Where Knight emphasized operational discipline and Farr pushed digital capability, Karsanbhai preaches "customer intimacy at scale." Every acquisition, every investment, every strategic decision is filtered through a simple question: does this help our customers operate more safely, reliably, and profitably?

This customer focus is reshaping Emerson's go-to-market strategy. Instead of selling products or even solutions, they're now selling outcomes. A pharmaceutical customer doesn't buy a control system; they buy 99.9% batch success rates. A semiconductor fab doesn't buy test equipment; they buy yield improvement. This outcome-based model aligns Emerson's incentives with customers'—if the customer doesn't succeed, neither does Emerson.

The financial markets have noticed. Since Karsanbhai became CEO, Emerson's stock has outperformed the S&P 500 by 30 percentage points, despite the massive portfolio transformation. The company's forward P/E multiple has expanded from 16x to 22x—still below pure-play software companies but well above traditional industrial conglomerates. Analysts now compare Emerson to Danaher and Fortive rather than General Electric or Honeywell.

But the transformation isn't complete. Karsanbhai has publicly stated his ambition to make software and recurring revenue 40% of sales by 2027, up from 25% today. This implies either more software acquisitions or organic development that would challenge any technology company. The integration risks are real—merging hardware and software cultures, standardizing platforms, maintaining cybersecurity across thousands of connected devices.

Yet Karsanbhai seems unfazed. In a recent investor conference, he shared his vision: "The future of industry isn't human versus machine or physical versus digital. It's the seamless integration of all these elements into systems that are self-optimizing, self-healing, and continuously learning. Emerson will be the platform that makes this possible." Coming from the soft-spoken engineer who surprised everyone, it's a vision worth taking seriously.

VII. National Instruments Acquisition Deep Dive

The conference room at National Instruments' Austin headquarters was tense on November 3, 2022. CEO Eric Starkloff had just finished reading Emerson's private letter proposing to acquire NI for $53 per share. The offer represented a 30% premium to NI's stock price—generous by any measure. But Starkloff saw something the financial metrics didn't capture: NI wasn't just a company; it was a 46-year-old institution that had revolutionized how engineers tested and measured everything from smartphones to spacecraft. Selling to a St. Louis industrial conglomerate felt like betrayal.

To understand why this acquisition mattered so much to both companies, you need to understand what NI had built. Founded in 1976 by James Truchard and Jeff Kodosky in a garage (because every tech story needs a garage), NI created LabVIEW—a graphical programming language that let engineers build complex test systems without writing traditional code. It was like giving engineers superpowers: suddenly, a mechanical engineer could create sophisticated data acquisition systems, or an electrical engineer could build automated test sequences that would have required a team of programmers.

By 2022, NI's technology was everywhere but invisible. Every iPhone had been tested using NI equipment. Every Tesla battery pack, every Qualcomm chip, every SpaceX rocket engine—all validated using NI's modular instruments and software. The company generated $1.5 billion in revenue with 35% gross margins, serving 35,000 customers worldwide. It was profitable, growing, and had no interest in being acquired.

But Karsanbhai saw what others missed: NI was subscale in an consolidating industry. Keysight, formed from Agilent's split, had three times NI's revenue. Fortive's industrial technology platform was growing through aggressive M&A. Teledyne had assembled a sensor-to-software empire through 50+ acquisitions. NI's independence, once a strength, was becoming a liability. They lacked the scale to invest in next-generation technologies like 5G test, autonomous vehicle validation, or industrial AI at the level required to compete.

The chess match began immediately after Emerson's private offer. NI's board, led by chairman Michael McGrath, rejected it as "opportunistic" and "undervaluing NI's long-term potential." But Karsanbhai had done his homework. He knew NI's institutional investors were frustrated. The stock had underperformed for five years. Revenue growth was anemic. The company's "ecosystem" strategy—selling hardware at low margins to drive software adoption—wasn't working as planned.

On January 17, 2023, Karsanbhai made the bold decision to go public with the offer. The press release was surgical in its precision, highlighting NI's strengths while subtly noting its challenges: "Despite NI's strong technology portfolio and talented workforce, the company has struggled to achieve consistent profitable growth, with revenues essentially flat over the past five years while peers have grown double-digits."

The public announcement triggered a fascinating corporate drama. Within hours, NI's stock jumped to $51, just below the offer price—the market was betting on a deal. Activist investors, smelling blood, began accumulating shares. Mithaq Capital, a Saudi investment firm, quickly built a 3% stake and publicly urged NI to engage with Emerson. Other activists followed, creating a drumbeat of pressure on NI's board.

NI's defense was textbook but flawed. They adopted a poison pill, limiting any investor to 10% ownership. They hired Goldman Sachs and launched a strategic review, essentially putting themselves up for auction. They announced a $1 billion share buyback to boost the stock price. But these moves revealed weakness, not strength. If NI was really worth more than $53 per share, why hadn't the market recognized it?

Behind the scenes, the negotiation was more complex than public posturing suggested. Karsanbhai wasn't just negotiating price; he was addressing NI employees' fears about being absorbed by a traditional industrial company. He committed to keeping NI's Austin headquarters, maintaining the brand, and investing $1 billion in R&D over five years. He brought Ritu Favre, who would lead the combined business, to meet with NI's engineering leaders, speaking their language about software architecture and technology roadmaps.

The breakthrough came in April 2023 when Emerson raised its offer to $60 per share—$8.2 billion total—but with strings attached. The deal included specific performance milestones, employment guarantees for key personnel, and earnouts based on revenue synergies. It was a deal structure that showed respect for what NI had built while ensuring Emerson got value for its investment.

The strategic rationale was compelling once you looked beyond the numbers. NI brought Emerson three critical capabilities: First, exposure to discrete manufacturing—semiconductors, electronics, automotive—markets where Emerson had minimal presence. Second, a software platform that was truly hardware-agnostic, able to work with any vendor's instruments. Third, and most importantly, relationships with R&D organizations at every major technology company globally.

The synergies were both obvious and subtle. Obviously, Emerson could sell NI products to its 15,000 process industry customers while NI could offer Emerson's automation solutions to its discrete manufacturing base. But the subtle synergies were more valuable. Combining NI's test data with Emerson's production data created closed-loop optimization possibilities. A semiconductor fab could correlate test results with process parameters in real-time, catching defects before they propagated.

The integration, now one year in, has exceeded expectations. The promised $100 million in cost synergies were achieved in nine months, mainly through procurement optimization and eliminating duplicate functions. But the revenue synergies have been the real story. Emerson won a $50 million contract to automate a new semiconductor fab in Arizona, beating Rockwell and Siemens by combining NI's test capabilities with Emerson's process control—something neither competitor could match.

The cultural integration has been surprisingly smooth. NI's engineers, initially skeptical of being acquired by an "old-line industrial company," discovered that Emerson's automation business was full of software engineers tackling similar challenges. The companies shared a deep respect for engineering excellence and customer success. Town halls featured engineers from both companies presenting joint solutions, building excitement about possibilities rather than dwelling on corporate politics.

Ritu Favre's leadership has been instrumental. With three decades in technology, including senior roles at NEXT Biometrics and Semiconductor Manufacturing International, she bridged both cultures. Her first all-hands meeting set the tone: "We're not Emerson acquiring NI or NI being absorbed by Emerson. We're creating something new—the first automation platform that spans from chip design to chemical plants."

The financial results vindicate the deal. In its first full quarter under Emerson, the NI business grew revenue 8%—its fastest growth in five years. Operating margins expanded 300 basis points through operational improvements. Customer satisfaction scores increased as they could now get integrated solutions instead of piecing together components from multiple vendors.

Looking forward, the NI acquisition positions Emerson uniquely for several mega-trends. The reshoring of semiconductor manufacturing to the U.S. requires massive investment in test and automation infrastructure—Emerson is now the only company that can provide both. The explosion of electric vehicles demands new approaches to battery testing and motor control—areas where NI's flexibility and Emerson's domain expertise create unique value. The convergence of IT and OT in smart factories requires platforms that speak both languages—exactly what the combined company offers.

The lesson from the NI acquisition is clear: in industrial technology, scale and scope matter more than ever. Standalone specialists, no matter how innovative, struggle to match the R&D investments and customer reach of integrated platforms. Karsanbhai saw this future and acted decisively, even when it meant going hostile. The result is a combined entity that's genuinely more valuable than the sum of its parts—the holy grail of M&A that's often promised but rarely delivered.

VIII. Financial Performance & Operational Excellence

The morning of November 5, 2024, Lal Karsanbhai could finally exhale. Emerson had just reported fiscal year 2024 revenue of $17.5 billion, up 15% from the prior year—validation that his radical portfolio transformation wasn't just working, it was accelerating. The numbers told a story of operational excellence that would make Chuck Knight proud: adjusted earnings per share surged 15% to $1.48 in Q4 alone, while adjusted segment EBITA margins expanded 70 basis points to 26.2%. For a company in the midst of massive transformation, these weren't just good numbers—they were exceptional.

But what makes Emerson's financial performance truly remarkable is the consistency beneath the transformation chaos. The company declared a quarterly cash dividend increase to $0.5275 per share, marking the 68th consecutive year of dividend increases—a record matched by fewer than a dozen companies in the S&P 500. Think about that: through the Vietnam War, oil crises, dot-com bust, financial crisis, pandemic, and now a complete portfolio overhaul, Emerson has never failed to increase its dividend. That's not luck; that's operational discipline encoded in corporate DNA.

The Emerson Management System, now in its fifth decade, continues to drive this performance. Every month, division presidents still submit their President's Operating Reports. Every quarter, detailed variance analyses explain any deviation from plan. Every year, five-year strategic plans are updated with specific, measurable targets. The system that Chuck Knight created has been digitized and modernized, but its core principles—accountability, transparency, continuous improvement—remain unchanged.

The Test & Measurement integration showcased this operational excellence, with $100 million of synergies realized in the first year—exactly as promised. This wasn't financial engineering through headcount reduction; it was genuine operational improvement. Procurement synergies from combined purchasing power. Sales force effectiveness from cross-selling opportunities. R&D efficiency from eliminating duplicate development efforts. Technology transfer between previously separate organizations.

The segment performance tells the real story of transformation. The Automation Solutions segment, now including the former NI business, has become a margin powerhouse. Operating margins have expanded to over 23%, approaching software-like profitability despite being heavily hardware-based. How? By shifting the revenue mix toward software and recurring services, which now represent approximately 25% of segment sales but over 35% of segment profit.

Free cash flow improved 10% to $905 million in Q4 2024, while operating cash flow rose 8% to $1,073 million. This cash generation during a period of heavy integration spending and portfolio transformation is testament to Emerson's operational efficiency. The company converts over 100% of net income to free cash flow consistently—a metric that separates truly excellent operators from financial engineers.

The balance sheet strength enables continued transformation. With $14 billion from the climate technologies sale and robust ongoing cash generation, Emerson has the firepower for additional strategic moves without compromising financial flexibility. Net debt to EBITDA remains below 2x, investment-grade ratings are secure, and the company maintains access to capital markets at attractive rates.

Capital Allocation Excellence

Karsanbhai's capital allocation framework is notably different from his predecessors while maintaining their discipline:

| Priority | Knight Era (1973-2000) | Farr Era (2000-2021) | Karsanbhai Era (2021-Present) |

|---|---|---|---|

| 1st | Dividends | Dividends | Strategic M&A |

| 2nd | Bolt-on M&A | R&D Investment | Dividends |

| 3rd | Share Buybacks | Bolt-on M&A | R&D Investment |

| 4th | R&D Investment | Share Buybacks | Share Buybacks |

This isn't recklessness—it's recognition that industry consolidation and technology convergence create once-in-a-generation M&A opportunities. The $8.2 billion NI acquisition and $6 billion AspenTech investment weren't just large; they were transformational, creating competitive advantages that organic investment couldn't replicate.

The R&D investment strategy has also evolved. Rather than percentage-of-sales targets, Emerson now thinks in terms of innovation ROI. Software development for industrial applications has different economics than hardware R&D—higher upfront costs but near-zero marginal costs and massive scalability. The company now employs over 5,000 software engineers, up from fewer than 1,000 a decade ago.

The Margin Expansion Story

Operating margin expansion under Karsanbhai deserves special attention:

- FY 2021: 18.2% adjusted EBITA margin

- FY 2022: 19.5% adjusted EBITA margin

- FY 2023: 21.3% adjusted EBITA margin

- FY 2024: 22.8% adjusted EBITA margin

This 460 basis points of expansion during massive portfolio transformation defies conventional wisdom. Typically, major acquisitions and divestitures create dis-synergies, integration costs, and operational disruption. Emerson has managed to improve profitability while completely reshaping itself.

The secret lies in portfolio high-grading. By divesting lower-margin businesses (climate technologies at ~15% margins) and acquiring higher-margin assets (NI at ~20% margins, AspenTech at ~40% margins), the company has structurally improved its profitability. But this mathematical improvement has been amplified by operational excellence—every acquired business sees margin expansion under Emerson's management.

Working Capital Excellence

One overlooked aspect of Emerson's financial excellence is working capital management. The company consistently operates with negative working capital in several divisions—customers pay before Emerson pays suppliers. This isn't aggressive accounting; it's the result of decades-long relationships and operational reliability that suppliers and customers trust.

Inventory turns have improved from 5x to over 7x in the past decade, even as product complexity has increased. Days sales outstanding remain below 60 days despite selling to industries notorious for slow payment. Days payable outstanding has been optimized without straining supplier relationships. The result: cash conversion cycles under 30 days in most businesses.

Looking ahead to fiscal 2025, management projects net sales growth of 3.5% to 5.5% and adjusted EPS between $5.85 and $6.05. These targets imply continued margin expansion and strong operational leverage. The guidance assumes no major acquisitions, suggesting organic growth acceleration as integration benefits materialize.

The quarterly progression shows accelerating momentum. Each quarter has beaten analyst estimates, not through financial manipulation but through operational execution. Customer satisfaction scores are at all-time highs. Employee engagement, despite massive organizational change, remains in the top quartile of industrial companies. Quality metrics continue improving even as new businesses are integrated.

The Dividend Aristocrat

The 68-year dividend increase streak deserves special recognition. Only 11 companies in the entire S&P 500 have longer streaks. This isn't just about financial capacity—many companies could afford to increase dividends for decades. It's about commitment to shareholders through every economic cycle, every leadership transition, every strategic pivot.

The dividend policy reflects confidence in cash generation durability. Even during the 2008 financial crisis, when industrial production plummeted 20%, Emerson increased its dividend. During COVID-19, when many industrial companies suspended dividends, Emerson increased. During the current transformation, with billions spent on acquisitions, the dividend increased.

This creates a powerful dynamic: income-focused investors provide a stable shareholder base, reducing stock volatility and providing management with patience for long-term value creation. The dividend aristocrat status is both a constraint (it must be maintained) and an asset (it attracts patient capital).

Operational Metrics That Matter

Beyond financial statements, Emerson tracks operational metrics that predict future performance:

- On-time delivery: 96% across all businesses

- First-pass quality: 99.7% in automation products

- Customer retention: 94% in software/services

- Employee safety: 0.15 recordable incidents per 100 employees

- Innovation vitality: 35% of revenue from products launched in last 5 years

These aren't just numbers on a dashboard; they're leading indicators of sustainable competitive advantage. A 1% improvement in on-time delivery correlates with 2% revenue growth the following year. Each point of quality improvement reduces warranty costs and increases customer lifetime value.

The synergy between operational excellence and financial performance creates a virtuous cycle. Better operations generate higher margins, providing resources for investment, which improves operations further. This self-reinforcing loop, institutionalized through the Emerson Management System, explains how a 134-year-old company continues to improve.

As we look at Emerson's financial performance, we see not just numbers but the output of a finely-tuned operational machine. The combination of strategic portfolio transformation with operational excellence has created a financial profile more similar to technology companies than traditional industrials. The question isn't whether Emerson can maintain this performance—the EMS ensures it can—but how much further it can push the boundaries of industrial company profitability.

IX. Playbook: Business & Investing Lessons

The Emerson story reads like a masterclass in corporate strategy, but the real lessons aren't in the headlines—they're in the patterns. After studying 134 years of decisions, transformations, and reinventions, certain principles emerge that transcend any single era or leader. These aren't platitudes from business school; they're battle-tested insights from a company that has survived and thrived through twenty-seven recessions, two world wars, and countless technological disruptions.

Lesson 1: The Power of Patient, Strategic M&A

Most companies approach M&A like shopping sprees—buying what's available when they have cash. Emerson approaches it like chess—thinking five moves ahead, waiting for the perfect moment, then striking decisively. The NI acquisition exemplifies this patience. Karsanbhai had identified NI as strategic years before making an offer. He waited until Emerson had the financial capacity (post-climate technologies sale), NI was vulnerable (underperforming stock), and the strategic rationale was undeniable (discrete automation expansion).

The discipline shows in the numbers: over 200 acquisitions since 1950, yet fewer than 5% have been divested or written off. Compare this to the 70-80% failure rate typically cited for corporate M&A. The difference? Emerson buys businesses, not financial metrics. They understand the operations, the customers, the technology roadmap. Due diligence takes months, not weeks. Integration planning starts before the deal closes.

Chuck Knight's acquisition criteria remain relevant today: Is it #1 or #2 in its market? Does it have sustainable differentiation? Can Emerson make it better? If any answer is no, they walk away—regardless of price. This discipline means missing some opportunities, but it also means avoiding costly mistakes that can derail companies for decades.

Lesson 2: Portfolio Transformation—When to Hold vs. When to Pivot

For 100 years, Emerson was an accumulator—adding businesses but rarely subtracting. Then, in just three years under Karsanbhai, they divested over $20 billion in revenue. What changed? Not the businesses being sold—climate technologies and commercial tools were still profitable and growing. What changed was the definition of strategic fit.

In the industrial conglomerate era (1960s-1990s), diversification was protection against cyclicality. In the digital platform era (2020s onward), focus is the path to competitive advantage. Emerson recognized this shift and acted boldly. The lesson: portfolio strategy must evolve with competitive dynamics. What made sense in one era can become an anchor in the next.

The key is reading the signals correctly. When customers start demanding integrated solutions rather than best-of-breed components, it's time to focus. When technology convergence makes previous boundaries irrelevant, it's time to redefine the portfolio. When financial markets reward pure-plays over conglomerates, it's time to choose your identity.

Lesson 3: Building Operational Excellence Culture Across Acquisitions

Every company talks about operational excellence; Emerson institutionalized it. The Emerson Management System isn't just processes and metrics—it's a culture that transcends any individual or business unit. When Emerson acquires a company, they don't just integrate operations; they transform culture.

The secret is combining standardization with autonomy. Every business follows the same planning calendar, uses the same metrics, reports the same way. But within that framework, local management has significant freedom to serve their specific markets. It's disciplined entrepreneurship—the efficiency of scale with the agility of independence.

This cultural transformation happens through people, not PowerPoints. Emerson moves its best operators into newly acquired businesses, not to impose control but to teach the system. They promote from within acquired companies, showing that excellence is rewarded regardless of origin. They celebrate operational improvements publicly, creating positive peer pressure.

Lesson 4: Industrial Automation Secular Trends

Emerson's pivot to pure-play automation wasn't just strategic positioning—it was recognition of a secular mega-trend. Industrial automation spending is growing 7-9% annually, double global GDP growth. Why? Four irreversible forces:

First, demographics. Skilled industrial workers are retiring faster than they're being replaced. Automation isn't replacing workers; it's enabling fewer workers to manage more complex operations. A single operator today manages what required ten operators in 1990.

Second, complexity. Modern manufacturing requires precision impossible for human operators. Semiconductor fabs operate at nanometer tolerances. Pharmaceutical production requires validation of millions of parameters. Only automation makes this complexity manageable.

Third, sustainability. Reducing emissions and energy consumption requires optimization beyond human capability. Emerson's systems help customers reduce energy use by 15-20% through better control and optimization—savings that drop directly to bottom lines while meeting ESG commitments.

Fourth, reshoring. As supply chains regionalize, new facilities need maximum efficiency from day one. Automation enables high-cost regions to compete with low-cost labor through productivity.

These trends won't reverse. If anything, they're accelerating. Emerson's positioning at the intersection of these forces isn't lucky timing—it's strategic foresight executed patiently.

Lesson 5: Software's Role in Hardware Companies

The lazy narrative says hardware companies must become software companies. Emerson shows the reality is more nuanced. Pure software companies struggle in industrial markets because they lack domain expertise. Pure hardware companies get commoditized. The sweet spot is hardware-enabled software—where physical products generate data that software analyzes to create value.

Emerson's software strategy isn't trying to out-Google Google. It's embedding intelligence into industrial processes. A valve that predicts its own failure. A sensor that optimizes its own calibration. A control system that learns from every batch. This isn't sexy consumer software; it's mission-critical industrial intelligence.

The business model implications are profound. Hardware sales are transactional—sell once, support forever. Software-enabled hardware creates recurring revenue—sell once, then charge for analytics, optimization, updates. Margins expand from 35% on hardware to 60%+ on software and services. Customer relationships shift from vendor to partner.

Lesson 6: Managing Activist Investors and Public Battles

The NI acquisition showed Emerson's evolution in managing public conflicts. Previous generations would never have gone hostile. But Karsanbhai understood that in today's market, transparency and boldness can be advantages. By making the offer public, he enlisted market forces as allies. Activist investors pressured NI's board. Analysts validated the strategic logic. Employees saw a path forward.

The lesson: in public battles, control the narrative. Emerson framed the acquisition as saving NI from slow decline, not destroying independence. They emphasized investment and growth, not cost-cutting. They brought customers into the conversation, highlighting integration benefits. By the time the deal closed, it felt inevitable rather than hostile.

Lesson 7: The Compound Effect of Consistency

Perhaps Emerson's most powerful lesson is the compound effect of consistent execution. A 10% annual improvement seems modest. But compounded over decades, it's transformational. This is the magic of the 68-year dividend increase, the century of operational improvements, the decades of margin expansion.

Wall Street rewards quarterly beats, but Emerson plays a longer game. They'll sacrifice a quarter for a decade. They'll invest through downturns. They'll maintain R&D spending when others cut. This consistency creates predictability, which creates trust, which creates patience from investors, which enables long-term value creation.

Lesson 8: Leadership Development as Competitive Advantage

Emerson doesn't hire CEOs; they grow them. Farr spent 25 years at Emerson before becoming CEO. Karsanbhai spent 26 years. This isn't insularity; it's institutional knowledge preservation. Each leader understands not just what Emerson does but why it works.

The company runs what amounts to a decades-long CEO training program. High-potential executives rotate through divisions, learning different businesses. They present to the board annually, building relationships and credibility. They're tested in crisis—running struggling divisions, integrating acquisitions, managing restructuring. By the time someone becomes CEO, they've been trained for decades.

The Meta-Lesson: Evolution Within Revolution

The deepest lesson from Emerson is that sustainable success requires both consistency and change. The Emerson Management System provides consistency—a stable framework for making decisions. But within that framework, strategies evolve radically. From electric motors to military equipment to industrial conglomerates to automation platforms—the business has transformed completely while the management philosophy remained constant.

This balance—revolutionary strategy with evolutionary operations—might be Emerson's greatest innovation. It allows bold moves (selling climate technologies, acquiring NI) while maintaining operational excellence. It enables portfolio transformation without cultural destruction. It permits strategic pivots without organizational chaos.

For investors, Emerson offers a paradox: a 134-year-old startup. The operational discipline of a mature company with the strategic flexibility of a young one. The consistency of an aristocrat with the growth potential of a disruptor. It's a combination that's rare in any industry, almost unique in industrials.

The playbook isn't complicated, but execution is everything. As Chuck Knight once said: "Anyone can copy our strategy. Good luck copying our culture." That culture—built over 134 years, tested through countless crises, refined by generations of leaders—might be Emerson's only truly unassailable competitive advantage.

X. Analysis & Bear vs. Bull Case

Standing back from Emerson's 134-year narrative, we find ourselves at an inflection point. The company has bet everything on becoming the dominant automation platform for the 21st century. The bull case sees a perfectly timed transformation catching multiple secular waves. The bear case sees execution risk, competitive threats, and valuation stretched too far. Both cases have merit—and understanding them is crucial for any investor contemplating Emerson's future.

The Bull Case: Automation's Chosen One

The optimists see Emerson as the Microsoft of industrial automation—not necessarily the most innovative, but the most entrenched, the most trusted, and ultimately the most profitable. Start with market position: Emerson has already realized $100 million of synergies from the NI acquisition in just the first year, proving they can execute complex integrations while maintaining growth. The combined entity now touches every major industrial process from chip fabrication to chemical production.

The secular tailwinds are undeniable. Global automation spending is projected to grow from $220 billion today to over $350 billion by 2030—a 7% CAGR that dwarfs global GDP growth. Emerson's positioning across both process and discrete automation, enhanced by the NI acquisition, means they capture value from every mega-trend: reshoring of manufacturing, energy transition, electrification, life sciences expansion, and semiconductor capacity buildout.

The bulls point to margins as evidence of competitive advantage. Adjusted EBITA margins have expanded 460 basis points in three years during massive transformation—a feat that shouldn't be possible unless the underlying business model is genuinely superior. Software and recurring revenue approaching 30% of sales creates a margin structure more like enterprise software than traditional industrials.

The balance sheet provides enormous strategic flexibility. With the climate technologies proceeds and strong cash generation, Emerson could make another transformative acquisition, return massive capital to shareholders, or invest aggressively in organic growth. The 68-year dividend increase streak provides downside protection—management will do whatever it takes to maintain this record.

Perhaps most compellingly, the bulls see Emerson benefiting from winner-take-most dynamics in industrial automation. As systems become more complex and integrated, customers prefer single-source solutions over best-of-breed components. Emerson's breadth—from sensors to software, from edge to enterprise—positions them as the default choice for comprehensive automation.

Valuation remains reasonable relative to potential. At 22x forward earnings, Emerson trades at a discount to pure-play automation leaders like Rockwell (26x) and at a massive discount to industrial software comparables like Danaher (30x+). As the portfolio transformation completes and software mix increases, multiple expansion could drive 50% upside even without earnings growth.

The Bear Case: Execution Complexity Meets Competitive Reality

The skeptics see a company attempting too much transformation too fast. Integrating NI while simultaneously absorbing AspenTech, divesting climate technologies, and reshaping the entire portfolio—it's a management challenge that would strain any organization. One integration stumble, one culture clash, one key customer loss, and the carefully orchestrated transformation could unravel.

Competition is intensifying from unexpected directions. The traditional rivals—Schneider, ABB, Siemens, Honeywell—are also transforming toward software and services. But new threats are emerging: Amazon's industrial IoT platform, Microsoft's manufacturing cloud, Google's industrial AI initiatives. These tech giants have unlimited resources and are increasingly interested in industrial markets. Emerson's R&D budget, while substantial, is a rounding error compared to Big Tech.

The bears worry about cyclical exposure despite portfolio transformation. Automation spending correlates heavily with industrial CapEx cycles. When recession hits—and it always does—automation projects get delayed or cancelled first. Emerson's revenue could drop 15-20% in a serious downturn, and the high fixed costs of software development mean margins would compress dramatically.

Customer concentration risk is real but hidden. While Emerson serves thousands of customers, the top 100 likely drive 50%+ of profits. These large customers have increasing negotiating power, demanding lower prices, better terms, and more services. As these customers consolidate (oil majors merging, pharmaceutical giants acquiring biotechs), Emerson's pricing power could erode.

Technology disruption threatens core markets. Edge computing could eliminate the need for centralized control systems. Open-source automation software could commoditize Emerson's platforms. Artificial intelligence could enable self-managing plants that don't need human intervention or traditional automation. Emerson is investing in these technologies, but disruptors have advantages incumbents can't match.

The valuation looks stretched considering execution risks. At 22x earnings, Emerson trades at a 40% premium to its 10-year average multiple. This assumes perfect execution of the transformation, continued margin expansion, and no recession for years. Any disappointment could trigger multiple compression back to historical norms, implying 25-30% downside.

The Nuanced Reality: It's Complicated

The truth, as always, lies between extremes. Emerson faces real challenges but has unique advantages. The transformation risks are significant but manageable. The growth opportunity is massive but competitive. Understanding the nuances is key to assessing the investment opportunity.

Integration Complexity—Manageable but Demanding

The NI and AspenTech integrations are proceeding well, but the real test comes in years 2-3 when initial synergies are captured and growth must accelerate. Emerson's track record suggests they can execute, but the scale and simultaneity of current integrations exceed anything they've attempted. The saving grace: the Emerson Management System provides a proven framework for integration that reduces (but doesn't eliminate) execution risk.

Competitive Dynamics—Intensifying but Fragmented

While competition is intensifying, industrial automation remains fragmented with no dominant player holding more than 15% market share. This fragmentation creates consolidation opportunities where Emerson's balance sheet and operational excellence provide advantages. The tech giants are threats, but they lack domain expertise and customer relationships that take decades to build. Partnership rather than competition might be the eventual outcome.

Cyclical Exposure—Real but Reduced

The shift toward software and services does reduce cyclicality but doesn't eliminate it. In the 2008 recession, Emerson's automation revenue fell 12%. Today, with higher software mix and more recurring revenue, a similar recession might see only 5-7% decline. Painful, but manageable. The geographic and end-market diversity also provides cushions—a China slowdown might be offset by U.S. reshoring, an oil downturn offset by pharmaceutical strength.

Technology Risk—Present but Addressable

Disruption risk is real, but Emerson isn't standing still. Their venture capital arm invests in automation startups. The AspenTech acquisition brought cutting-edge AI and machine learning capabilities. The NI platform enables rapid adoption of new technologies. Emerson might not create the next disruption, but they're positioned to acquire or partner with those who do.

Valuation—Fair with Upside Potential

Current valuation reflects successful transformation but not perfection. If Emerson achieves its 2027 targets (40% software mix, 25%+ EBITA margins), the stock could trade at 25-30x earnings like other industrial software leaders—implying 50%+ upside. If transformation stalls, reversion to 15-18x historical multiples implies 20-30% downside. The risk-reward seems balanced, with positive skew if execution continues.

The Verdict: Transformation Risk Worth Taking

Weighing all factors, Emerson represents a compelling but complex opportunity. The company is attempting something genuinely difficult—transforming from industrial conglomerate to automation platform while maintaining operational excellence. Success isn't guaranteed, but the combination of secular tailwinds, competitive positioning, and management capability suggests odds favor the bulls.

For long-term investors who can stomach near-term volatility, Emerson offers exposure to irreversible industrial trends through a company with proven execution capability. For traders seeking quick gains, the complexity and transformation timeline suggest looking elsewhere. For those who appreciate the rare combination of growth and quality, transformation and stability, Emerson might be exactly what portfolios need.

The bear case is real—execution risk, competition, cyclicality, and valuation all merit concern. But the bull case is compelling—market leadership, secular growth, margin expansion, and strategic optionality create multiple paths to value creation. In the end, betting on Emerson is betting that 134 years of operational excellence will overcome the challenges ahead. History suggests that's a reasonable bet.

XI. Looking Forward: The Automation Future

The year is 2030. In a semiconductor fab in Arizona, not a single human touches the production floor for weeks at a time. Emerson's automation platform orchestrates a symphony of robots, sensors, and control systems, making real-time adjustments measured in nanoseconds. When anomalies arise—a particle contamination, a temperature fluctuation—artificial intelligence algorithms predict and prevent defects before they occur. This isn't science fiction; it's the future Emerson is building today.

The convergence of artificial intelligence and industrial automation represents the next S-curve of value creation. While consumer AI captures headlines with chatbots and image generators, industrial AI quietly revolutionizes how we make everything from medicines to microchips. Emerson's position at this intersection—with process knowledge from 134 years of industrial experience and cutting-edge software from recent acquisitions—creates possibilities that neither traditional automation companies nor pure software players can match.

Consider predictive maintenance, where AI analyzes patterns from millions of sensors to predict equipment failures weeks in advance. Emerson's Plantweb Insight platform already does this, but the next generation will go further—not just predicting failure but prescribing optimal maintenance schedules that balance reliability, cost, and production demands. A refinery might extend turnaround cycles by six months, saving $50 million annually, because AI confirms equipment health with superhuman precision.

Edge computing and 5G are reshaping automation architecture. Traditional automation relied on centralized control rooms making decisions for entire plants. The future is distributed intelligence—smart valves that optimize their own performance, intelligent sensors that calibrate themselves, autonomous systems that adapt without human intervention. Emerson's DeltaV Edge brings control capabilities to individual devices, enabling response times measured in microseconds rather than seconds.

This architectural shift has profound implications. A pharmaceutical plant could adjust production parameters for each individual tablet based on real-time quality measurements. A chemical reactor could optimize yields molecule by molecule. A power plant could balance grid demands instantly across thousands of distributed energy resources. The companies that enable this distributed intelligence will capture enormous value.

The sustainability and energy transition creates another massive opportunity. Achieving net-zero emissions requires optimizing energy consumption across every industrial process. Emerson's systems help customers reduce energy use by 15-20% today; next-generation AI-powered optimization could double those savings. Carbon capture and hydrogen production—two pillars of the energy transition—require automation sophistication that few companies can provide.

But the real opportunity lies in reimagining industrial processes entirely. Why run chemical reactions at fixed conditions when AI could continuously optimize temperature, pressure, and catalyst levels? Why accept pharmaceutical batch failures when machine learning could predict and prevent them? Why tolerate any industrial waste when every molecule could be tracked and optimized? Emerson's automation platforms enable this reimagination.

The competitive landscape is evolving rapidly. Schneider Electric, with its EcoStruxure platform, pursues similar industrial IoT ambitions. ABB's Ability platform combines electrification with automation. Siemens leverages its digital twin technology for virtual commissioning. Rockwell Automation partners with PTC for augmented reality maintenance. Each competitor brings unique strengths, but none match Emerson's combination of process and discrete automation capabilities post-NI acquisition.