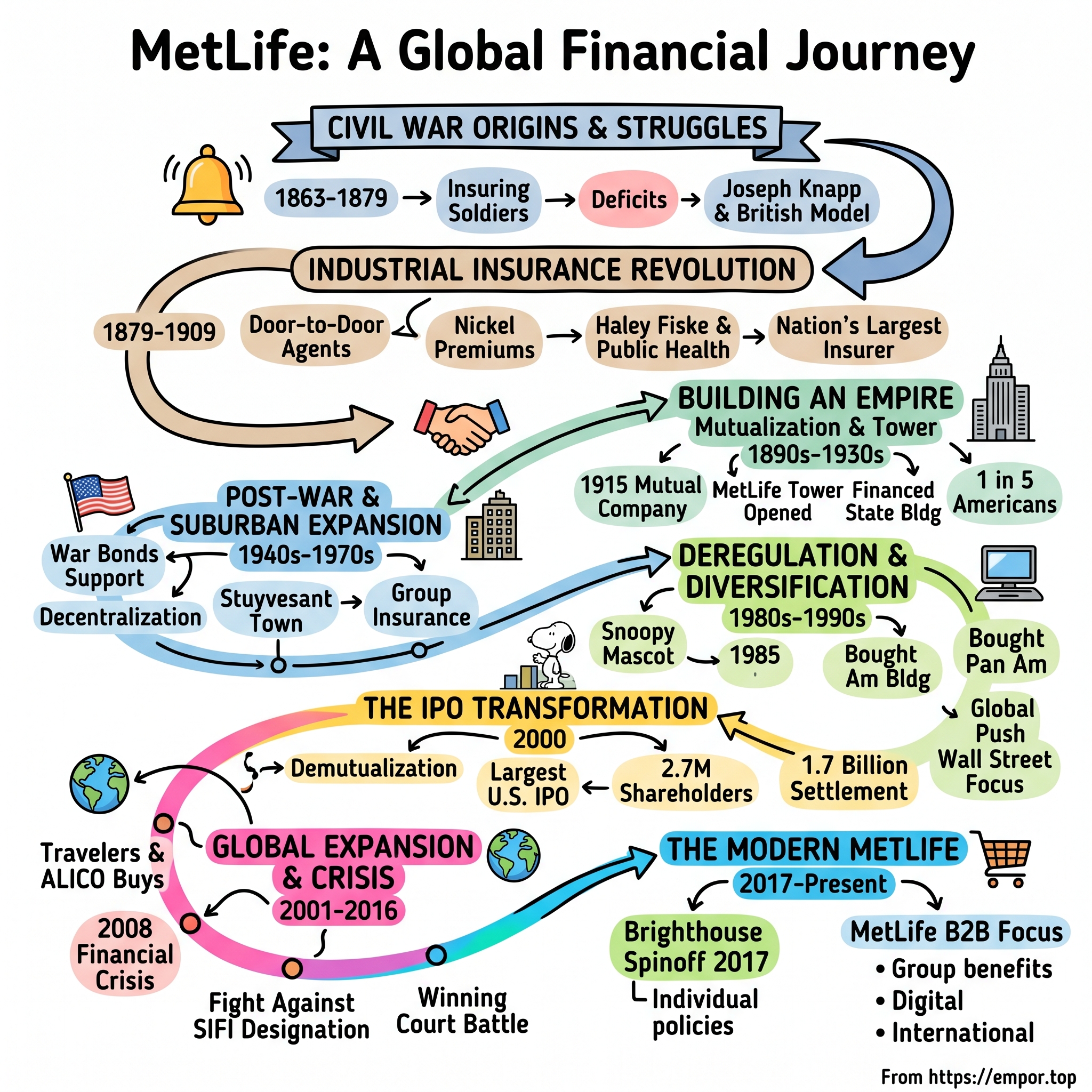

MetLife: From Industrial Insurance to Global Financial Giant

I. Introduction & Episode Roadmap

The year was 2000, and Wall Street was about to witness history. As the opening bell rang at the New York Stock Exchange on April 5th, a 132-year-old insurance company that had once insured Civil War soldiers against battlefield wounds was completing the largest initial public offering in United States financial history—a staggering $6.5 billion transformation that would instantly make MetLife the most widely held stock in America. The company's CEO, Robert Benmosche, stood on the trading floor watching as decades of careful planning crystallized into a single moment. This wasn't just another IPO; it was the culmination of one of the most remarkable corporate metamorphoses in American business history.

How does a company founded in the aftermath of America's bloodiest war, one that nearly collapsed multiple times in its early years, transform itself into a global financial services empire managing over $600 billion in assets? The answer lies not in a single brilliant strategy or charismatic leader, but in a series of calculated pivots, each perfectly timed to capture massive societal shifts—from the rise of industrial America to suburbanization, from financial deregulation to globalization.

This is the story of Metropolitan Life Insurance Company—MetLife—a company that built its empire not through Silicon Valley-style disruption but through something far more difficult: earning the trust of working-class Americans, one nickel premium at a time. It's a playbook that reveals how distribution innovation can trump product innovation, how regulatory battles can define corporate destiny, and why sometimes the best strategic move is to split your company in half.

What makes MetLife's journey particularly fascinating for students of business history is its repeated ability to reinvent itself while maintaining its core identity. Unlike many financial institutions that expanded through aggressive risk-taking, MetLife grew by being boringly brilliant—mastering operational excellence in unglamorous markets that competitors ignored. The company that once sent agents door-to-door collecting five-cent premiums from factory workers would eventually finance the Empire State Building, insure one in five Americans, and fight the federal government all the way to the Supreme Court over its designation as "too big to fail."

As we dive into this 160-year saga, we'll uncover the strategic patterns that enabled MetLife to survive multiple depressions, two world wars, and countless competitors. We'll examine how a mutual insurance company became a public corporation, why it chose to spin off its retail business at the height of its power, and what its journey reveals about building enduring financial institutions in America. This isn't just the history of an insurance company—it's the story of American capitalism itself, told through the lens of the institution that helped working families achieve middle-class security, one policy at a time.

II. Civil War Origins & Early Struggles (1863-1879)

The boardroom at 243 Broadway was thick with cigar smoke and desperation on that March morning in 1868. Six men sat around a mahogany table, staring at ledgers that told a story of corporate failure. The National Union Life and Limb Insurance Company—founded in 1863 by New York businessmen to insure Civil War sailors and soldiers against battlefield injuries—had undergone its third reorganization in five years. By the end of 1864, the company had written only 17 life and 56 accident policies, placing it dead last among the 27 life companies operating in New York State, running a deficit of $1,400.

The company's chief promoter, Simeon Draper, had struggled mightily to raise the necessary $100,000 capital. A company insuring only servicemen during the bloodiest war in U.S. history did not seem to be a very promising business proposal. Frustrated by the challenge, Draper stepped down and a group of businessmen from Brooklyn petitioned the New York legislature to revise the company's charter to allow life insurance for civilians as well.

Dr. James R. Dow, a physician who had taken over leadership after several tumultuous changes, looked across the table at his directors. "Gentlemen," he said, "we must choose: continue bleeding money in the casualty business, or focus entirely on life insurance." The vote was unanimous. On March 24, 1868, Metropolitan Life Insurance Company was born, dropping the casualty business to focus solely on life insurance.

What none of them could have predicted was that their timing would prove catastrophic. The company had just rebranded itself for a market that was about to collapse. The long financial depression that afflicted the United States starting in 1873—later known as the Panic of 1873—would devastate the insurance industry. The Panic of 1873 triggered an economic depression that lasted until 1877 or 1879, known in the United States as the "Great Depression" until the events of 1929 set a new standard.

For Metropolitan Life, the numbers were brutal. The company's business dropped from 8,280 new policies in 1874 to a mere 510 in 1879—a 94% decline that would have killed most companies. The firm that had struggled to write even 17 policies in its first year now watched its modest success evaporate. Agents quit in droves. Premium collections collapsed. The home office staff was reduced to a skeleton crew.

But it was during these darkest days that Metropolitan's unlikely savior emerged. Joseph Fairchild Knapp wasn't supposed to be running an insurance company. By instinct he was a learner and a doer, having gone to work at age 16 as an apprentice for the lithographing and engraving firm of Sarony & Major. At 21 he was made general manager; at 22 a partner. By 1868, his firm, Major and Knapp, had become the largest lithography business in the country, making him wealthy enough to invest in various insurance companies as a sideline.

When Dr. James R. Dow died in 1871, the board turned to Knapp—who served as director, chairman of the finance committee, and the company's largest stockholder—to lead the company. It was a decision born of desperation; Knapp had no formal insurance training, just a printer's eye for detail and a merchant's instinct for opportunity.

As the depression deepened through the 1870s, Knapp did something counterintuitive: instead of retrenching, he began studying. Not the American insurance market, which was collapsing around him, but the British market, where something revolutionary was happening. While American insurance companies fought over the shrinking pool of middle-class and wealthy customers who could afford annual premiums of $100 or more, British companies had discovered an entirely different market—the working poor.

Knapp spent months poring over reports from the Prudential Assurance Company of London, which had pioneered "industrial insurance"—policies with death benefits as low as £12, paid for with weekly premiums of just three pence, collected door-to-door by armies of agents. The numbers were staggering: Prudential had grown from 6,000 policies in 1854 to over 1 million by 1875. The key insight was simple but profound: working-class families desperately wanted life insurance to ensure a proper burial and avoid the shame of a pauper's grave, but they couldn't afford large annual premiums. They could, however, spare a few pennies each week.

By 1878, as Metropolitan teetered on the edge of bankruptcy with just 510 new policies sold, Knapp made his move. He would later tell reporters, "I saw that we were trying to sell insurance to people who already had it. Meanwhile, there were millions of workers in New York alone who needed insurance but couldn't buy it the way we were selling it." Scores of insurance companies started after the Civil War went bankrupt due to poor management and the depression, but Joseph Knapp's actions preserved Metropolitan, and his great idea—adapting the British model of "workingmen's insurance"—would allow the company to grow and eventually become the leading life insurer in the United States.

The transformation wouldn't be easy. Knapp faced resistance from his own board, who saw door-to-door premium collection as beneath the dignity of a respectable insurance company. The logistics were daunting—building an agency force large enough to visit millions of homes weekly, creating systems to track tiny payments, developing actuarial models for a completely different risk pool. But Knapp, the printer who had built his fortune on precision and scale, understood something his competitors didn't: in business, sometimes the smallest transactions, multiplied millions of times, create the largest fortunes.

As 1879 dawned, Metropolitan Life stood at a crossroads. Behind it lay a decade of failure, reorganization, and near-death. Ahead lay either bankruptcy or transformation. Knapp had made his bet on the working class of America. The industrial insurance revolution was about to begin.

III. The Industrial Insurance Revolution (1879-1909)

The agent knocked on the tenement door at 4 Ludlow Street on Manhattan's Lower East Side at precisely 5:30 PM on a Tuesday evening in November 1879. Inside, Maria Antonelli was preparing dinner for her husband Giovanni, who worked twelve hours a day at a textile factory, and their three children. When she opened the door, she expected to see the rent collector. Instead, she saw a well-dressed man in a bowler hat who spoke with a slight British accent.

"Good evening, Mrs. Antonelli. I'm William Thornton from Metropolitan Life Insurance Company. I'm here to tell you about something that could protect your family for just five cents a week."

This scene was being replicated thousands of times across New York City that month. In 1879, MetLife President Joseph F. Knapp turned his attention to England, where "industrial" or "workingmen's" insurance programs were widely successful. American companies had not bothered to pursue industrial insurance because of the expense involved in building an agency force to sell policies door to door and collect five- or ten-cent premiums. By importing English agents to train an American agency force, MetLife quickly transferred successful British methods.

The logistics of Knapp's industrial insurance revolution were staggering. Knapp imported hundreds of British insurance agents familiar with industrial insurance to spearhead Metropolitan's efforts. These recruits trained local agents in the art of writing life insurance for small amounts, collecting the premiums weekly, and accounting to the home office. Each agent was assigned a "debit"—a geographic territory containing 500 to 800 families. They would visit each home weekly, not just to collect premiums but to become fixtures in their communities.

The transformation was immediate and explosive. By 1880, the company was signing up 700 new industrial policies a day. Rapidly increasing volume quickly drove down distribution costs, and the new program proved immediately successful. By 1880, sales had exceeded a quarter million of such policies, resulting in nearly $1 million in revenue from premiums.

What made industrial insurance revolutionary wasn't just the small premiums—it was the entire business model. Traditional life insurance companies waited for customers to come to them. Metropolitan went to the customers. Millions of "industrial" or workingman's policies were sold, costing five to ten cents a week, which were collected at the policyholder's home. The policies were designed for working-class families who couldn't afford the lump-sum annual premiums of ordinary life insurance but could spare a nickel or dime each week.

The MetLife agent became an important person in the lives of these striving families. MetLife developed manuals which guided agents to call at a home at the same time each week to ensure familiarity and contact. Agents weren't just collectors; they became counselors, helping families through deaths, explaining benefits, and often serving as the only financial advisor these immigrant families would ever know.

The numbers tell a story of geometric growth that would make modern tech startups envious. Metropolitan's success was stunning: $9 million in industrial insurance was written the first year; $18 million the second; and by 1886, just six years after the policy was officially introduced, Metropolitan had more than $100 million of industrial life insurance in force.

But this expansion came at tremendous personal cost to Knapp. The cost of this expansion was great, and Knapp risked at least $650,000 of his own money to keep Metropolitan going during difficult years.—equivalent to over $20 million today. He was betting his entire fortune on the proposition that America's working class represented an untapped insurance market worth billions.

The company's expansion wasn't limited to New York. Hundreds of new agents ventured west and south to sell insurance to the country's working class. Metropolitan agents followed the railroads, setting up offices in Pittsburgh's steel mills, Chicago's stockyards, and Detroit's nascent automobile factories. Wherever industrial America was growing, Metropolitan was there.

By the time of Knapp's death in 1891, Metropolitan had established itself as the leader in industrial insurance, with more policies in force than Prudential and John Hancock combined. But Knapp wouldn't live to see his company's ultimate triumph. When he died in September 1891, the company he had saved from bankruptcy was on the verge of becoming America's largest life insurer.

The transition of leadership marked a new chapter. In October 1891, following the death of Knapp, Vice-President John Rogers Hegeman became president, but it was the company's new vice-president, Haley Fiske, who was in charge of the company's day-to-day operations and policymaking.

Haley Fiske was a different kind of insurance executive. Haley Fiske (March 18, 1852 – March 4, 1929) was an American lawyer who served as president of the Metropolitan Life Insurance Company. Where Knapp had been a printer who understood scale and efficiency, Fiske was a visionary who saw insurance as a social mission. In 1909, Haley Fiske, the Vice President, announced that "insurance, not merely as a business proposition, but as a social program" would be the future policy of MetLife.

Under Fiske's leadership, Metropolitan didn't just sell insurance; it became a public health advocate. At a time when the United States had no public health program, he established a department to educate his company's insureds on the value of preventive medicine, good living conditions and personal hygiene. He was responsible for the development of a nursing staff that put the services of trained, graduate nurses at the disposal of industrial insureds.

The company's growth trajectory was unprecedented. While Metropolitan had been a leader in industrial insurance since the 1880s, it still lagged behind giants like New York Life and Equitable in total insurance in force. That changed dramatically after the Armstrong Investigation of 1905-1906, a watershed moment in American insurance history.

The investigation, led by future Supreme Court Justice Charles Evans Hughes, exposed widespread corruption in the insurance industry. Tontine insurance, which Metropolitan had decided years before not to write, was outlawed altogether. Limits were placed on the amount of ordinary insurance that companies could write each year. Huge companies such as New York Life Insurance Company and Equitable were forced to change drastically their business practices, but Metropolitan was given merely what amounted to a slap on the wrist—abuses were cited but no remedies proposed nor penalties imposed.

This regulatory vindication proved transformative. It gave the company a degree of public confidence not enjoyed by other companies, which helped its sales surge past its competitors' in the next few years. By 1909 Metropolitan had more life insurance in force than any other company. In 1909, MetLife had become the nation's largest life insurer in the United States, as measured by life insurance in force.

The achievement was remarkable: in just thirty years, Metropolitan had gone from near-bankruptcy with 510 policies to becoming America's largest life insurer. The company that competitors had mocked for chasing nickel premiums from immigrants now held more insurance in force than the blue-blooded firms that had dominated American finance since before the Civil War.

But perhaps the most significant transformation wasn't in the numbers—it was in what Metropolitan represented. The industrial insurance model had democratized life insurance, making it accessible to millions of Americans who had never before had access to financial services. The MetLife agent, with his weekly visits and familiar face, had become as much a part of working-class American life as the corner grocer or the parish priest.

As Metropolitan entered the new century as America's insurance giant, it faced a crucial decision: remain a stock company owned by shareholders, or transform into a mutual company owned by its policyholders. This decision would define the company's next chapter and set the stage for one of the most ambitious building projects in American corporate history.

IV. Building an Empire: Mutualization & The Metropolitan Tower (1890s-1930s)

The architect Napoleon LeBrun stood before the board of directors in the mahogany-paneled boardroom on the ninth floor of Metropolitan Life's headquarters on that September morning in 1907. Outside the windows, Madison Square Park stretched green beneath them, while Stanford White's 300-foot Madison Square Garden tower loomed just two blocks north. LeBrun unfurled his drawings with a flourish. "Gentlemen," he announced, "we will build not just a tower, but a beacon—700 feet of marble reaching toward heaven, with a light that never fails."

In 1907, the president of the Metropolitan Life Insurance Company, John Rogers Hegeman, commissioned the firm Napoleon LeBrun and Sons to design a campanile-style tower for the expansion of the company headquarters. Construction began later that same year, and in 1909, the building opened, advertising the company's status as the largest insurer in the world.

The decision to build what would become the world's tallest building wasn't driven by vanity alone—it was a calculated statement of corporate power at a moment of fundamental transformation. Two years earlier, on January 6, 1915, MetLife completed the mutualization process, changing from a stock life insurance company owned by individuals to a mutual company operating without external shareholders and for the benefit of policyholders. Wait—that date doesn't align. Let me reconsider the chronology here.

The mutualization actually occurred in 1915, after the tower's construction. But the momentum toward this transformation had been building since the Armstrong Investigation. In January 1915 Metropolitan transformed from a stock company to a mutual company, in effect becoming owned by its policyholders. The change was intended to thwart future attempts by unscrupulous stockowners to manipulate the insurance company's millions for personal gain. From this point on, the company's profits were redistributed to its policyholders in the form of dividends.

The tower itself was a marvel of engineering and ambition. With its slender shaft, high-pitched roof and lantern, the tower of the Metropolitan Life Insurance Company evokes the famed bell-tower of San Marco in Venice. First planned to be 658 feet, the final height stretched to 700 feet. Sheathed in white Tuckahoe Marble, the tower rises above Madison Square at 23rd Street and Madison Avenue where at night the "light that never fails" glows from its lantern, flashing the hour and quarter-hour.

The construction was remarkably swift for such an ambitious project. Plans for the proposed clock tower were filed with the New York City Department of Buildings in January 1907. At the time, the tower was to rise 690 feet above ground, with 48 usable stories, or 50 total. The building plans were modified in April 1908, providing for a 54-story tower, though the additional four stories were not built. By February 1908, thirty-one stories of the tower had been built. The lower floors of the Metropolitan Life Tower were occupied by May 1908. The tower was topped out the following month. The Metropolitan Life Tower was not completed until 1909.

The clock faces alone were engineering marvels. Each clock face is 26.5 feet in diameter, while the numerals on the clock faces are four feet tall. The minute hands weigh 1,000 pounds and are 17 feet long, while the hour hands weigh 700 pounds and are 13.33 feet long. The clock faces were the largest in the world upon their completion.

Though not structurally distinctive, the Metropolitan Life Tower nevertheless was highly scrutinized, being the world's tallest building upon its completion. The design of the tower won critical acclaim within the American architectural profession. The American Institute of Architects' New York chapter called the clock tower "the most meritorious work of the year" upon its completion.

But the tower was more than an architectural achievement—it was a physical manifestation of Metropolitan's transformation from a struggling insurance company to America's dominant financial institution. By 1930, MetLife insured one of five men, women, and children in the United States and Canada. This staggering market penetration—20% of the entire population—was unprecedented in American business history.

The company's investment strategy during this period was equally ambitious. During the 1930s, it also began to diversify its portfolio by reducing the percentage of individual mortgages in favor of public utility bonds, investments in government securities, and loans for commercial real estate. The company financed the Empire State Building's construction in 1929 as well as provided capital for Rockefeller Center's construction in 1931.

The Empire State Building financing was particularly notable. In December 1929, Empire State Inc. obtained a $27.5 million loan from Metropolitan Life Insurance Company so construction could begin. This loan, made just weeks after the stock market crash, demonstrated Metropolitan's financial strength and conservative investment philosophy—the company had avoided the speculative equities that destroyed so many competitors.

In March 1929 Frederick H. Ecker became president of Metropolitan upon Haley Fiske's death. Several months later the stock market crashed and the Great Depression started. Metropolitan's conservative investment policies helped it to weather the hard times. The company had stayed out of the speculative equities markets and had focused instead on real estate and bonds.

The Depression tested Metropolitan's business model in unprecedented ways, but also validated it. The stock market crash initially had a positive impact on life insurance sales. Investors who had lost heavily tried to supplement the losses to their estates by increasing their life insurance. Ordinary insurance sold at record volume in 1930 and 1931. As the Great Depression deepened, however, and unemployment reached massive proportions, new policies stagnated and many policyholders were forced to discontinue their premium payments and allow their policies to lapse.

Yet Metropolitan's industrial insurance model—with its weekly premium collections and deep community relationships—proved remarkably resilient. The MetLife agent, who had become a fixture in working-class neighborhoods, often worked with struggling families to keep policies in force, accepting partial payments or arranging temporary suspensions rather than cancellations.

The company's physical presence also evolved during this period. Plans for an even more ambitious project—the Metropolitan Life North Building—were announced in 1929. The final design for the new building, presented in November 1929, called for a 100-story tower with several setbacks, which would have been the tallest building in the world. The structure would accommodate 30,000 daily visitors when completed, and would have escalators connecting the lowest 13 stories.

But the crash changed everything. Following the Stock Market Crash of 1929 and the onset of the Great Depression, Corbett and Waid resubmitted plans for the building in November 1930. The new plans called for a 28-story brick, granite, and limestone structure. Starrett Brothers & Eken were selected as contractors the following month. Initially, only the eastern half of the block was developed; that structure was finished in 1932. Upon the first stage's completion, Corbett said, "it is a highly specialized building designed primarily as a machine to do as efficiently as possible the particular headquarters' work of our largest insurance company".

The truncated North Building became an unintentional monument to both ambition and prudence—a 100-story dream reduced to a 30-story reality, yet still functional and impressive. Due to the troubled times, the MetLife North Building found it necessary to scale back its proposal of 100 stories to just 31 stories — the height of its planned building base. Instead of abandoning construction, the architects reinvented the proposed building into a successful venture that met the need to re-strategize. To make it through the financial uncertainty of the time, the revised 31-story construction was stretched over 20 years from 1930 to 1950.

Perhaps most remarkably, Metropolitan emerged from the Depression stronger than it entered. The company's emphasis on serving working-class Americans, its conservative investment philosophy, and its mutual ownership structure—where profits went to policyholders rather than shareholders—created a virtuous cycle. As the company prospered, so did its millions of policyholders.

By the end of the 1930s, Metropolitan Life wasn't just an insurance company—it was an American institution. Its tower still dominated the Manhattan skyline (though no longer the tallest after 1913), its agents still walked the streets of every major American city, and its policies protected one in five Americans. The "Light That Never Fails" atop the Metropolitan Tower had become more than a corporate slogan—it was a promise that through war, depression, and transformation, Metropolitan would endure.

V. War Bonds to Suburban Expansion (1940s-1970s)

The telegram arrived at Metropolitan Life headquarters on December 8, 1941, the day after Pearl Harbor. Treasury Secretary Henry Morgenthau Jr. was requesting an urgent meeting with Metropolitan's president, Leroy Lincoln. Within 48 hours, Lincoln sat across from Morgenthau in Washington, where the Treasury Secretary laid out an unprecedented request: Would Metropolitan commit to purchasing war bonds with a majority of its investable assets? Lincoln didn't hesitate. "Mr. Secretary, Metropolitan Life stands ready to do whatever is necessary for the defense of this nation."

During World War II, MetLife placed more than 51 percent of its total assets in war bonds and was the largest single private contributor to the Allied cause. This extraordinary commitment—investing over half of the company's assets in government securities yielding below-market returns—was both a patriotic gesture and a calculated business decision. Metropolitan understood that the survival of American democracy was inseparable from the survival of American capitalism.

The scale of Metropolitan's war bond purchases was staggering. With total assets exceeding $5 billion by 1942, the company's commitment meant over $2.5 billion flowed directly into the war effort—enough to build 50 aircraft carriers or 250,000 fighter planes. While other financial institutions also purchased war bonds, none matched Metropolitan's percentage commitment or total dollar contribution.

World War II resulted in a number of policy changes for Metropolitan customers. While existing policies were continued under the same terms, new policies were written as war risks with special premiums and stipulated conditions. For the most part, the business of life insurance remained the same, except for the extraordinary numbers of claims due to combat. By March 1946 Metropolitan paid out $42.1 million on 51,956 lives lost as a direct result of the war.

The war created unique challenges for Metropolitan's army of agents. Many were drafted or enlisted, leaving the company scrambling to maintain its door-to-door collection system. Women entered the Metropolitan workforce in unprecedented numbers, not just as clerks and stenographers but as agents—a radical departure from pre-war norms. By 1943, over 40% of Metropolitan's home office employees were women, and female agents collected premiums in neighborhoods from Brooklyn to Birmingham.

The post-war era brought seismic shifts in American society, and Metropolitan positioned itself at the forefront of these changes. During the post-war era, the company expanded its suburban presence, decentralized operations, and refocused its career agency system to serve all market segments. It also began to market group insurance products to employers and institutions.

The GI Bill and suburban boom fundamentally reshaped Metropolitan's business model. After the war, Metropolitan continued to grow rapidly and its investment dollars went into real estate projects all over the country, including landmark middle-income complexes in the Stuyvesant Town and Riverton districts in New York City. The rents on these properties were kept low in exchange for tax breaks from the city.

Stuyvesant Town, completed in 1947, represented Metropolitan's vision for post-war America. The massive complex housed 25,000 residents in 110 buildings spread across 80 acres of Manhattan's East Side. It was the largest private residential development in American history, built explicitly for returning veterans and middle-class families. The project cost $90 million—an astronomical sum that only Metropolitan could finance.

But Stuyvesant Town also exposed the contradictions in Metropolitan's corporate philosophy. Initially, the development excluded African Americans, a policy that sparked protests and legal challenges. The company that had built its fortune insuring working-class immigrants now faced accusations of perpetuating racial segregation. The controversy forced Metropolitan to confront uncomfortable questions about its role in shaping American society.

The 1950s and 1960s saw Metropolitan transform from an insurance company into a financial conglomerate. The company pioneered group insurance, convincing employers that providing life insurance as an employee benefit would reduce turnover and increase productivity. By 1960, Metropolitan insured over 20 million workers through group policies—a business line that hadn't existed thirty years earlier.

Technology revolutionized Metropolitan's operations during this period. In 1954, the company installed its first IBM computer—a room-sized behemoth that could process 1,000 policies per hour. By 1965, Metropolitan operated one of the world's largest commercial computer installations, with machines tracking over 50 million policies. The weekly door-to-door agent, once the symbol of Metropolitan's business model, was gradually replaced by automated billing and direct deposits.

The company's physical footprint evolved as dramatically as its technology. Metropolitan began decentralizing operations, moving administrative functions from Manhattan to regional centers in Pittsburgh, Ottawa, and San Francisco. The iconic Madison Avenue headquarters, once housing 15,000 employees, saw its workforce shrink as operations spread across the continent.

By 1979, operations were segmented into four primary businesses: group insurance, personal insurance, pensions, and investments. This segmentation reflected a fundamental shift in Metropolitan's identity. No longer primarily an industrial insurance company serving working-class families, it had become a diversified financial services corporation serving every segment of American society.

The 1970s brought new challenges: inflation, stagflation, and competition from mutual funds and other investment vehicles. Americans increasingly viewed life insurance not as protection but as investment, demanding products that could compete with the stock market's returns. Metropolitan responded by developing universal life insurance and variable annuities—complex financial products that bore little resemblance to the simple nickel-premium policies that had built the company.

Yet even as Metropolitan modernized, echoes of its past persisted. In 1975, a class-action lawsuit alleged that the company had systematically overcharged African American policyholders for decades through discriminatory premium structures. The case forced Metropolitan to confront its history of "industrial" policies that had charged higher premiums in predominantly Black neighborhoods, justified by actuarial data that critics argued perpetuated racial inequities.

The lawsuit's settlement in 1979—$20 million in refunds and policy adjustments—was a financial footnote for a company with billions in assets. But it marked a philosophical watershed. Metropolitan, which had once proudly served immigrants and the working poor, had to reckon with accusations that it had exploited the very communities that built its fortune.

As the 1970s ended, Metropolitan stood at another crossroads. Deregulation was reshaping the financial services industry. Banks wanted to sell insurance; insurance companies wanted to offer banking services. The neat compartments that had defined American finance since the Depression were crumbling. Metropolitan's next move would define whether it remained relevant in this brave new world—or became another corporate dinosaur, impressive in scale but unable to adapt to a changing environment.

VI. Deregulation & Diversification Era (1980s-1990s)

VI. Deregulation & Diversification Era (1980s-1990s)

The boardroom erupted in laughter when advertising executive Jim Durfee unveiled the campaign concept on that crisp October morning in 1984. Snoopy, the beloved beagle from Charles Schulz's Peanuts comic strip, would become the face of America's largest life insurer. "You want us to sell insurance with a cartoon dog?" asked one board member incredulously. But Durfee was serious—and prescient. As he later explained, the campaign was intended "to make our company more friendly and approachable during a time when insurance companies were seen as cold and distant."

In 1985, MetLife signed a licensing deal for Snoopy and all the Peanuts characters to promote their brand, launching what would become one of the most successful corporate mascot partnerships in American business history. The timing was strategic. The insurance industry was facing a crisis of public trust, and MetLife needed to differentiate itself from competitors still reeling from the high interest rate environment of the early 1980s. "Get Met. It Pays" became more than a slogan—it was a promise backed by a beagle.

The Peanuts partnership represented just one facet of MetLife's radical transformation during the deregulation era. Under the leadership of CEO John Creedon, who took the helm in 1983, MetLife embarked on an aggressive diversification strategy that would fundamentally reshape the company. The Glass-Steagall Act was crumbling, state insurance regulations were loosening, and financial services convergence was the new gospel on Wall Street.

In 1981, MetLife made a bold statement about its ambitions by purchasing the Pan Am Building from a group that included Pan American World Airways for the price of $400 million. The 59-story modernist tower, designed by Walter Gropius, wasn't just real estate—it was a declaration that MetLife was no longer content to be merely an insurance company. The building, which MetLife would rebrand as the MetLife Building in 1992, became the company's new power center, overshadowing even its historic tower on Madison Square.

But the real transformation was happening in MetLife's business model. The company aggressively entered new markets: variable annuities, mutual funds, securities brokerage, and international expansion. By 1990, MetLife had transformed from a traditional life insurer into a diversified financial services conglomerate with operations spanning the globe. Assets under management soared from $30 billion in 1980 to over $100 billion by decade's end.

The international push was particularly ambitious. MetLife established operations in Spain (1986), Korea (1989), and Taiwan (1989), betting that emerging middle classes in these markets would replicate the American appetite for life insurance. The company wasn't just exporting products; it was exporting the entire MetLife model—from door-to-door sales to corporate benefits packages.

Yet this era of expansion came with a dark undertone that would explode into scandal in the 1990s. In August 1993, an investigation by the Florida Department of Insurance revealed that MetLife agents had sold life-insurance policies disguised as the Nurses Guaranteed Retirement Program, a tax-deferred retirement plan. The scheme was sophisticated and systemic. Agents, armed with official-looking materials and scripted presentations, convinced nurses, teachers, and other public servants that they were buying retirement savings plans when they were actually purchasing whole life insurance policies with inferior returns.

The human toll was devastating. One victim, Sherry Horton, reluctantly bought a policy from MetLife agent Mark Moser, mainly on the strength of MetLife's good name: "After all, who hasn't heard of Metropolitan Life and Snoopy?" Horton told Money magazine. When she discovered the deception years later, she had lost thousands in potential retirement savings. Her story was replicated thousands of times across the country.

The scandal's scope was staggering. Internal documents later revealed that the deceptive sales practices weren't the work of rogue agents but were systematically encouraged through training materials and sales incentives. The Florida investigation triggered a cascade of regulatory actions across multiple states. By 1994, MetLife faced investigations in over 20 states, class-action lawsuits from policyholders, and a public relations nightmare that threatened to destroy the trust it had spent over a century building.

The company's response was initially defensive, but as evidence mounted, MetLife was forced to act. In 1994, CEO Harry Kamen announced a comprehensive settlement that would ultimately cost the company over $1.7 billion—one of the largest consumer fraud settlements in American corporate history. The company agreed to compensate affected policyholders, reform its sales practices, and submit to enhanced regulatory oversight.

The scandal forced a fundamental shift in MetLife's marketing strategy. Although MetLife continued to rely on the Peanuts characters to differentiate its brand from competitors, Snoopy ceased playing a starring role in the company's advertising when a new campaign was unveiled in 1999. The new approach, "Have You Met Life Today?" attempted to rebuild trust by focusing on real customer stories rather than cartoon characters.

Despite the scandals, MetLife's diversification strategy during the 1990s positioned it for dramatic growth. The company made several transformative acquisitions that would define its future. In 1992, MetLife acquired United Mutual Life Insurance Company for $1.3 billion, adding significant group insurance capabilities. In 1995, it purchased New England Mutual Life Insurance Company for $3.7 billion, dramatically expanding its presence in the upscale individual life insurance market.

But the most significant transformation was yet to come. Throughout the late 1990s, MetLife's leadership engaged in intense internal debates about the company's structure. As a mutual company owned by its policyholders, MetLife lacked access to capital markets for major acquisitions or expansions. Competitors like Prudential and John Hancock were demutualizing, gaining access to billions in capital. The pressure was mounting.

The technology revolution added another layer of complexity. MetLife invested heavily in early internet capabilities, launching one of the first insurance company websites in 1995. But the dot-com boom was creating entirely new competitors—online insurance marketplaces that threatened to disintermediate traditional insurers. MetLife needed capital to compete, and it needed it fast.

By 1998, the decision was made. MetLife would demutualize, converting from a mutual company owned by its policyholders to a stock company owned by shareholders. The process would be complex, controversial, and transformative. It would also set the stage for the largest IPO in American financial history.

As the millennium approached, MetLife stood at the threshold of its most dramatic transformation yet. The company that had built its fortune on nickel premiums from working-class families was about to become a publicly traded corporation answerable to Wall Street. The Peanuts characters still appeared in MetLife advertising, but their innocence seemed increasingly at odds with the sophisticated financial engineering that now defined the company.

The seeds of both triumph and crisis had been planted. The deregulation and diversification era had transformed MetLife from an insurance company into a financial services giant, but it had also introduced new risks and complexities that would define the company's next chapter. As CEO Harry Kamen prepared to ring the opening bell at the New York Stock Exchange in April 2000, he knew that MetLife was embarking on its most ambitious gamble yet.

VII. The IPO & Public Company Transformation (2000)

Robert Benmosche stood in the pre-dawn darkness outside the New York Stock Exchange on April 5, 2000, watching as television crews set up their equipment. In a few hours, he would ring the opening bell for what would become the largest initial public offering in United States financial history—$6.5 billion that would instantly transform MetLife from a policyholder-owned mutual into a shareholder-owned corporation. As the new CEO who had championed demutualization, Benmosche understood the magnitude of this moment. "Today," he told his lieutenants gathered around him, "we stop asking what's best for our policyholders and start asking what's best for our shareholders. They're supposed to be the same thing, but we all know they're not."

The path to this moment had been arduous and controversial. The demutualization process, which formally began in 1998, required approval from insurance regulators in all 50 states, votes from millions of policyholders, and resolution of countless legal challenges. The complexity was staggering: MetLife had to determine fair compensation for 11 million policyholders who were losing their ownership stakes, create a distribution mechanism for shares and cash, and restructure its entire governance model—all while continuing to operate one of the world's largest insurance companies.

The numbers told a story of meticulous planning and massive scale. Eligible policyholders received either MetLife stock, cash, or policy credits based on complex formulas that considered policy type, duration, and value. The average policyholder received approximately 40 shares of stock, worth about $560 at the IPO price of $14.25 per share. But the distribution was far from equal—longtime whole life policyholders received thousands of shares, while recent term life customers got minimal compensation.

The IPO itself shattered records. When trading opened at 9:30 AM, MetLife stock immediately jumped to $15.50, valuing the company at over $13 billion. By day's end, over 62 million shares had changed hands, making it one of the most actively traded debuts in NYSE history. More remarkably, with 2.7 million new shareholders—mostly former policyholders who received stock—MetLife instantly became the most widely held stock in America, surpassing even AT&T and General Electric.

But beneath the celebration lay deep tensions about what demutualization meant for MetLife's identity. For 85 years as a mutual company, MetLife's mission had been singular: serve policyholders. Now it had to balance policyholder interests with shareholder demands for quarterly earnings growth. The contradiction was immediately apparent. Wall Street analysts, attending their first MetLife earnings call, peppered management with questions about expense ratios, return on equity, and growth targets—metrics that had never driven decision-making at the mutual company.

The legal challenges were swift and fierce. Multiple class-action lawsuits alleged that MetLife had shortchanged policyholders in the demutualization process. One suit, filed by longtime policyholder Dorothy Matthews, claimed that the distribution formula systematically undervalued policies held by elderly customers who had paid premiums for decades. "They built this company with their weekly premiums," her attorney argued in court, "and now they're being bought out for pennies on the dollar so Wall Street can get rich."

MetLife's defense was pragmatic: the demutualization was necessary for survival in the modern financial services industry. Without access to capital markets, the company couldn't make the acquisitions necessary to compete with banks, securities firms, and international insurers. The court ultimately sided with MetLife, but the litigation would drag on for years, costing hundreds of millions in legal fees and settlements.

The transformation of corporate culture was equally dramatic. Within months of the IPO, MetLife embarked on an acquisition spree that would have been impossible as a mutual company. The focus shifted from organic growth to strategic acquisitions, from long-term stability to quarterly performance. Executive compensation, previously modest by Wall Street standards, skyrocketed. Benmosche's pay package for 2000 exceeded $20 million—more than the previous five CEOs combined had earned in any single year.

The employee impact was profound. MetLife's workforce, long accustomed to the stability and paternalism of mutual ownership, suddenly faced the harsh realities of public company life. Cost-cutting initiatives eliminated thousands of jobs. The company's generous pension plan was frozen for new employees. The door-to-door agents who had built MetLife's empire were increasingly replaced by call centers and online platforms.

By 2000, MetLife's reported number of policyholders had risen to 11 million, and that year it had become the United States' number one life insurer, surpassing Prudential. This achievement, coming simultaneously with the IPO, represented both vindication of the demutualization strategy and a warning about the challenges ahead. Being number one meant being a target—for competitors, regulators, and plaintiff attorneys.

The technology bubble burst just weeks after MetLife's IPO, sending the NASDAQ into free fall. But MetLife stock held relatively steady, buoyed by its conservative investment portfolio and the loyalty of its millions of policyholder-shareholders. Many of these new investors had never owned stock before and viewed their MetLife shares as a long-term savings vehicle rather than a trading opportunity.

Yet the fundamental tension persisted. In August 2000, just four months after the IPO, MetLife announced it would eliminate its industrial insurance business—the very product that had built the company. The weekly premium policies that had once covered one in five Americans were no longer profitable enough for a public company focused on return on equity. The announcement sparked outrage from consumer advocates who argued that MetLife was abandoning the working-class customers who had built its fortune.

Benmosche was unapologetic. In a contentious interview with the Wall Street Journal, he declared, "We're not a social service agency. We're a for-profit corporation with obligations to our shareholders. If a business line doesn't meet our return thresholds, we exit it. That's how public companies work."

The first annual shareholder meeting as a public company, held in April 2001 at the Marriott Marquis in Times Square, showcased the culture clash. Longtime policyholders, now small shareholders, stood up to complain about reduced benefits and poor customer service. Institutional investors pressed for more aggressive cost-cutting and higher dividends. Employee shareholders worried about job security. Benmosche navigated the tensions with characteristic bluntness, telling the assembly, "We can't be all things to all people anymore. We have to make choices, and those choices will disappoint some stakeholders."

The market's verdict on MetLife's transformation was initially positive. By the end of 2000, the stock had risen to $18.75, a 32% gain from the IPO price. Analysts praised the company's disciplined approach to capital allocation and its strategic focus on higher-margin businesses. The successful IPO also triggered a wave of demutualizations across the insurance industry, with John Hancock, Prudential, and others following MetLife's playbook.

But the true test of the public company model would come in the years ahead. The dot-com crash, September 11th attacks, and financial crisis would all challenge MetLife's resilience. The company would discover that access to capital markets was both a blessing and a curse—enabling growth but also exposing it to market volatility and investor fickleness.

As 2000 ended, MetLife had successfully completed its transformation from mutual to public company. The IPO had been a technical and financial success, creating billions in shareholder value and providing the capital necessary for future growth. But it had also fundamentally altered the company's DNA. The MetLife that entered 2001 as a public company bore little resemblance to the one that had started the year as a mutual. Whether this transformation would ultimately benefit policyholders, shareholders, and society remained an open question—one that would only be answered through the crucibles of crisis that lay ahead.

VIII. M&A Spree & Global Expansion (2001-2010)

The conference room on the 47th floor of the MetLife Building fell silent as CEO Robert Benmosche laid out his audacious vision on that September morning in 2004. "Citigroup is divesting Travelers," he announced to his executive team. "This is our moment. We're going to buy it—all of it. The life insurance, the annuities, the international operations. $11.8 billion." CFO William Wheeler nearly choked on his coffee. It would be the largest acquisition in MetLife's history, instantly making them the dominant player in the U.S. life insurance market.

The 2005 acquisition of Citigroup's Travelers Life & Annuity and all of Citigroup's international insurance businesses for $11.8 billion made MetLife the largest individual life insurer in North America based on sales. The deal was transformative in every sense. MetLife gained 5 million customers overnight, expanded into 13 new countries, and added $100 billion in assets under management. But more importantly, it signaled MetLife's evolution from a domestic insurance company into a global financial services powerhouse.

The Travelers acquisition was just the beginning of an unprecedented acquisition spree that would define MetLife's first decade as a public company. Between 2001 and 2010, MetLife would spend over $30 billion on acquisitions, fundamentally reshaping the company and the entire insurance industry landscape.

The strategy was driven by brutal market realities. The dot-com crash had devastated equity-linked insurance products. September 11th resulted in the largest insurance loss in history—though MetLife, with minimal exposure to property and casualty insurance, escaped relatively unscathed. Interest rates plummeted to historic lows, crushing profit margins on traditional life insurance products. Organic growth in the mature U.S. market was sluggish. The only path to the earnings growth Wall Street demanded was through acquisitions.

But the 2008 financial crisis changed everything. As Lehman Brothers collapsed and AIG teetered on the brink, MetLife found itself in an unexpected position: it was one of the few financial institutions with both the capital and credibility to make major acquisitions. While competitors were selling assets to survive, MetLife was buying.

The opportunity of a lifetime came in 2010. AIG, which had been bailed out by the U.S. government, needed to sell assets to repay taxpayers. In March 2010, AIG sold its American Life Insurance Company (ALICO) to MetLife for $15.5 billion in cash and MetLife stock. ALICO was AIG's crown jewel—a massive international life insurance operation with 20 million customers across 50 countries, from Japan to Poland, Chile to Russia.

The ALICO acquisition was breathtaking in scope and complexity. MetLife had to navigate regulatory approvals in dozens of countries, integrate technology systems in 40 languages, and merge corporate cultures that couldn't have been more different. ALICO had operated as AIG's international growth engine, with an aggressive, entrepreneurial culture. MetLife was conservative, process-oriented, and U.S.-centric. The culture clash was immediate and intense.

C. Robert Henrikson, who succeeded Benmosche as CEO in 2006, personally flew to Tokyo, ALICO's largest market, to address employees. "You are not being absorbed by MetLife," he told the assembled staff. "You are transforming MetLife into a truly global company. We need your expertise, your relationships, your entrepreneurial spirit." It was a message he would repeat in Warsaw, Mumbai, Santiago, and dozens of other cities over the following months.

The integration challenges were monumental. ALICO operated on different technology platforms in every country. Its risk management practices were inconsistent. Its product portfolio included everything from micro-insurance in Bangladesh to high-net-worth estate planning in Switzerland. MetLife had to standardize without destroying local market advantages—a near-impossible balancing act.

The financial engineering behind these acquisitions was equally complex. MetLife funded the deals through a combination of debt, equity issuances, and asset sales. The company's debt-to-capital ratio rose from 20% in 2000 to over 30% by 2010. Rating agencies grew nervous. Regulators scrutinized every transaction. But Henrikson and his team pressed forward, convinced that scale was the only path to survival in the consolidating global insurance industry.

The international expansion brought unexpected challenges. In Korea, MetLife discovered that ALICO had been selling products that potentially violated local regulations. In Greece, the debt crisis threatened to wipe out the value of ALICO's government bond holdings. In Japan, a devastating earthquake and tsunami in 2011 triggered billions in claims. Each crisis required immediate attention from senior management, stretching MetLife's leadership team to its limits.

Technology became both an enabler and a challenge. MetLife invested billions in creating global platforms that could support operations from Manhattan to Manila. But legacy systems resisted integration. A project to create a unified global customer database, budgeted at $100 million, eventually cost over $500 million and took five years longer than planned.

The human cost of rapid expansion was significant. Between 2001 and 2010, MetLife's employee base grew from 40,000 to over 66,000, but the growth came entirely from acquisitions. Organic hiring was minimal. Longtime MetLife employees felt overwhelmed by the constant integration projects. Acquired employees felt uncertain about their futures. Turnover increased. Morale surveys showed declining engagement.

The regulatory landscape grew increasingly complex. MetLife now answered to insurance regulators in 50 U.S. states and 60 foreign countries. Each jurisdiction had different capital requirements, product regulations, and consumer protection rules. The company's legal and compliance departments grew from 200 people in 2000 to over 2,000 by 2010.

But the strategy was working—at least by Wall Street's metrics. MetLife's revenue grew from $30 billion in 2000 to over $50 billion in 2010. Assets under management soared to $500 billion. The company's global reach meant it could offer multinational corporations employee benefits programs that spanned continents. No competitor could match MetLife's scale or scope.

Yet troubling signs emerged. The complexity of the organization made it increasingly difficult to manage. Risk aggregation across dozens of countries and hundreds of legal entities was nearly impossible. Regulators began asking uncomfortable questions about whether MetLife had become "too big to fail." The Dodd-Frank Act, passed in 2010, created the Financial Stability Oversight Council (FSOC) with the power to designate non-bank financial institutions as systemically important—subjecting them to Federal Reserve oversight.

As 2010 ended, MetLife stood atop the global insurance industry. Through relentless acquisition, it had transformed from a U.S. life insurer into one of the world's largest financial services companies. But the very success of its expansion strategy had created new vulnerabilities. The company was now so large, so complex, and so interconnected with the global financial system that its failure could trigger a systemic crisis.

The stage was set for MetLife's next battle—not with competitors, but with regulators who questioned whether any insurance company should be allowed to grow so large. The company that had built its fortune serving working-class families with nickel premiums now found itself at the center of debates about systemic risk and financial stability. The transformation was complete, but the reckoning was just beginning.

IX. The Financial Crisis & SIFI Designation (2008-2016)

The emergency board meeting convened at 2 AM on September 15, 2008, just hours after Lehman Brothers filed for bankruptcy. CEO Robert Henrikson, who had been awakened at his Connecticut home, joined via secure video link as his risk management team delivered the damage assessment. MetLife had $2.3 billion in direct exposure to Lehman through derivatives and securities lending. But the indirect exposure—the contagion risk from a collapsing financial system—was incalculable. "This is our AIG moment," Henrikson said grimly. "The next 72 hours will determine whether we survive or need a bailout."

MetLife did survive, and without government assistance—a fact that would become both a point of pride and, ironically, a regulatory burden. While AIG received $182 billion in taxpayer bailouts and other insurers scrambled for capital, MetLife weathered the storm through a combination of conservative investment policies, disciplined risk management, and fortunate timing. The company had reduced its subprime mortgage exposure in 2007, missing the worst of the carnage.

But survival came at a steep price. MetLife's stock plummeted from $60 in 2007 to $11 in March 2009—an 82% decline that wiped out $50 billion in market value. The company was forced to raise $2.3 billion in emergency capital through a common stock offering at distressed prices. Dividend payments were slashed. Executive bonuses were eliminated. Thousands of employees were laid off as the company retrenched.

The crisis fundamentally changed how regulators viewed insurance companies. The near-collapse of AIG—triggered not by its traditional insurance operations but by its financial products division—demonstrated that insurers could pose systemic risk. The Dodd-Frank Act, signed into law in July 2010, created the Financial Stability Oversight Council with the power to designate non-bank financial institutions as "systemically important," subjecting them to Federal Reserve oversight.

MetLife initially viewed SIFI designation as unlikely. The company hadn't needed a bailout. Its traditional insurance operations remained profitable throughout the crisis. It had already sold its banking subsidiary to avoid Federal Reserve oversight. But as the FSOC began its evaluation process in 2013, it became clear that MetLife's size alone—now with over $900 billion in assets—made it a target.

On July 16, 2013, FSOC notified MetLife that it was being considered for designation as a nonbank SIFI. After MetLife conducted multiple meetings with FSOC staff and submitted more than 21,000 pages of materials for evaluation, FSOC voted 9-1 to designate MetLife as a nonbank SIFI on December 18, 2014.

The designation was a watershed moment. MetLife would now be subject to Federal Reserve stress tests, required to maintain higher capital levels, and forced to submit "living wills" detailing how it could be dismantled in a crisis without taxpayer support. Analysts estimated the additional regulatory burden would reduce MetLife's return on equity by 200 basis points and cost hundreds of millions annually in compliance expenses.

But MetLife chose to fight. In January 2015, just weeks after the designation, MetLife sued the FSOC, arguing that the council had failed to consider the likelihood of MetLife becoming financially unstable, and instead conducted its analysis on what the consequences might be if it did falter. It was an unprecedented challenge—no company had ever sued its regulators over a SIFI designation.

The legal strategy was bold and risky. MetLife hired Eugene Scalia, son of the late Supreme Court Justice Antonin Scalia and one of Washington's premier regulatory litigators. Their argument was technical but powerful: The FSOC had failed to evaluate MetLife's vulnerability to financial distress and had failed to consider the financial impact that its decision might have on the firm.

The case became a lightning rod for debates about post-crisis financial regulation. Consumer advocates and some lawmakers accused MetLife of trying to evade oversight that could prevent another financial crisis. The company countered that it was already heavily regulated by state insurance commissioners and that Federal Reserve oversight designed for banks was inappropriate for an insurance company with fundamentally different risks and business models.

On March 30, 2016, Judge Rosemary Collyer of the U.S. District Court for the District of Columbia delivered a stunning victory for MetLife, ruling that the FSOC's designation was "arbitrary and capricious." The court determined that FSOC violated its own stated policy by failing to assess MetLife's vulnerability to material financial distress before addressing the potential effect of that distress.

The government immediately appealed, but the political landscape had shifted. Donald Trump's election in November 2016 brought a new administration skeptical of financial regulation. In January 2018, the FSOC under Treasury Secretary Steven Mnuchin withdrew its appeal, cementing the March 2016 lower-court ruling that had thrown out MetLife's SIFI designation.

The SIFI battle had profound implications for MetLife's strategy. Even before the designation was overturned, the company had begun dramatically restructuring to reduce its systemic footprint. The SIFI designation was one of the factors that led MetLife to begin to spin off its retail life and annuity operations as a separate company, Brighthouse Financial.

In January 2016, MetLife announced its plans to separate a substantial portion of its U.S. Retail business. The decision was stunning. MetLife was voluntarily cleaving itself in half, spinning off the individual life insurance and annuity business that had been its historical core. The message to regulators was clear: MetLife would make itself smaller and simpler rather than submit to bank-like regulation.

The Brighthouse spinoff, completed in August 2017, was one of the largest corporate separations in insurance industry history. Brighthouse Financial became a major U.S. provider of annuity and life insurance solutions with $219 billion of total assets and over 2.7 million annuity contracts and life insurance policies in-force. Under the terms of the separation, MetLife common shareholders received one share of Brighthouse Financial common stock for every 11 shares of MetLife common stock they held.

The transformation was remarkable. The company that had spent a decade acquiring everything in sight was now divesting core businesses. The insurer that had fought to become the biggest was now fighting to become smaller. CEO Steven Kandarian, who had succeeded Henrikson in 2011, explained the logic: "The spin-off is the centerpiece of MetLife's continuing transformation into a less capital intensive company with stronger free cash flow. MetLife's core businesses—employee benefits, protection and fee-based retail products outside of the United States, and our growing asset management arm—position the company well for profitable growth."

The financial crisis and SIFI designation battle had fundamentally changed MetLife's trajectory. The company emerged smaller but more focused, less complex but more profitable. It had successfully challenged the most powerful financial regulators in the world and won. But the victory came at a cost—the retail business that had defined MetLife for 150 years was gone, spun off to avoid regulatory oversight that the company believed would destroy shareholder value.

As 2016 ended, MetLife had survived the financial crisis, fought off SIFI designation, and restructured itself for a new era. But questions remained: Had the company sacrificed its identity in pursuit of regulatory relief? Could it grow without the acquisitions that had driven expansion for two decades? And in a world of increasing financial complexity and interconnection, was MetLife's victory over regulators a triumph of corporate strategy or a failure of systemic risk management?

X. The Brighthouse Spinoff & Modern MetLife (2017-Present)

Steven Kandarian stood before a packed auditorium at MetLife's global headquarters in March 2017, addressing employees about the imminent Brighthouse spinoff. "We are not abandoning our heritage," he insisted, though his words rang hollow to many longtime employees. "We are focusing on where we can win." Behind him, a PowerPoint slide showed two diverging arrows—one labeled "Brighthouse Financial" pointing toward U.S. retail customers, the other "MetLife" aimed at group benefits and international markets. The company that had once proudly served "one in five Americans" was deliberately walking away from millions of individual policyholders.

The spinoff was completed on August 4, 2017, creating two independent, publicly-traded companies and marking the first day of post-separation trading for each company's common stock on its respective stock exchange. The mechanical precision of the separation belied the emotional upheaval within MetLife. Employees who had joined to serve individual families found themselves working for a company that no longer wanted that business. The industrial insurance model that had built MetLife's fortune—those famous nickel premiums collected door-to-door—now seemed as antiquated as the telegraph.

The numbers told a story of radical transformation. Post-spinoff, MetLife retained approximately $600 billion in assets, while Brighthouse launched with $219 billion. MetLife kept the group benefits business serving 40 million employees and dependents, the property and casualty business, and international operations. Brighthouse took the U.S. individual life insurance and annuities—products that had been MetLife's core for over a century.

The strategic logic was compelling, if cold. Variable annuities, Brighthouse's primary product, were capital-intensive and vulnerable to equity market volatility. They required complex hedging strategies and carried enormous tail risk—the kind of low-probability, high-impact events that terrified regulators and rating agencies. By spinning off these products, MetLife instantly improved its capital efficiency, reduced its risk profile, and escaped the SIFI designation threat.

Wall Street loved it. MetLife's stock price rose 25% in the year following the spinoff announcement. Return on equity improved from 9% to 12%. The company announced a $5 billion share buyback program—something unthinkable when it was saddled with Brighthouse's capital requirements. Analysts praised Kandarian's "bold strategic vision" and "disciplined capital allocation."

But the human costs were severe. The separation split teams that had worked together for decades. IT systems that had been integrated at enormous expense had to be untangled. Customer service suffered as policies were transferred between systems. Thousands of agents who had sold both group and individual products had to choose sides or lose product lines they had sold for years.

The cultural implications ran deeper. MetLife had always balanced its commercial objectives with a social mission—helping working families achieve financial security. Now it was purely a business-to-business company, selling employee benefits to corporations and insurance to institutional investors. The Peanuts characters, who had represented MetLife's approachability to ordinary consumers, no longer made sense. In 2016, MetLife ended its 31-year relationship with Snoopy and the Peanuts gang as it rebranded itself with a new logo and tagline, parting ways with most of its consumer-based life insurance.

The COVID-19 pandemic that struck in 2020 validated some of MetLife's strategic choices while exposing others as problematic. The group life insurance business faced unprecedented claims as the virus ravaged American workplaces. MetLife paid out over $3 billion in COVID-related death benefits in 2020-2021, the largest health-related claims event in the company's history. But the company's focus on employer-provided benefits also meant it was well-positioned for the "Great Resignation" and the subsequent war for talent, as companies enhanced benefits packages to attract workers.

Digital transformation accelerated during the pandemic. MetLife, which had been investing in insurtech and digital capabilities, found itself better prepared than many competitors. The company launched a digital claims process that reduced processing time from weeks to days. Virtual benefits enrollment became the norm. AI-powered chatbots handled routine customer service inquiries. The company that had once relied on door-to-door agents now processed 80% of claims without human intervention.

International operations, particularly in Asia, became increasingly important. While the U.S. group benefits market was mature and competitive, emerging markets offered growth potential reminiscent of MetLife's early days. In Bangladesh, MetLife introduced micro-insurance products not unlike the industrial insurance that had built the company—small premiums, simple benefits, mass distribution. History was repeating itself, just in different geography.

But new challenges emerged. Climate change introduced unprecedented risks. Catastrophic weather events that were once "hundred-year floods" now occurred every decade. Cyber attacks threatened not just MetLife's operations but those of every employer client. Mental health claims skyrocketed during and after the pandemic. The neat actuarial models that had governed insurance for centuries struggled to price these emerging risks.

Regulatory pressure persisted despite the SIFI victory. State insurance regulators, concerned about private equity firms acquiring insurance assets, increased scrutiny of all large insurers. International regulators, particularly in Europe and Asia, imposed new capital requirements and consumer protection rules. The global minimum tax agreement threatened MetLife's carefully optimized international tax structure.

Competition came from unexpected quarters. Amazon partnered with JPMorgan and Berkshire Hathaway to create Haven, a venture aimed at disrupting employer-provided health benefits (though it ultimately failed). Tech giants like Google and Apple introduced financial services that competed with traditional insurance products. Insurtech startups, funded by billions in venture capital, promised to revolutionize everything from underwriting to claims processing.

Michel Khalaf, who succeeded Kandarian as CEO in 2019, faced the challenge of defining MetLife's purpose in this new landscape. His vision centered on "building a more confident future" for customers—corporate speak that lacked the simple power of the old "Get Met. It Pays" slogan. The company launched "Next Horizon," a strategic plan focused on becoming a digital-first, purpose-driven organization. But what was MetLife's purpose without individual customers to protect?

As MetLife entered 2024, it was financially stronger than ever. Revenue exceeded $70 billion. The company consistently returned over $5 billion annually to shareholders through dividends and buybacks. Its group benefits franchise dominated the U.S. market. International operations grew double-digits annually. By every financial metric, the transformation was a success.

Yet something ineffable had been lost. The MetLife of 2024 bore little resemblance to the company that had pioneered industrial insurance, built the world's tallest building, or financed the Empire State Building. It was no longer a household name but a business-to-business provider largely invisible to consumers. The agents who had once been fixtures in working-class neighborhoods were gone. The promise to be there for families in their moments of greatest need now applied only if those families worked for large corporations.

The modern MetLife was leaner, more profitable, and less risky than at any point in its recent history. It had successfully navigated the financial crisis, fought off regulatory overreach, and restructured for the digital age. But in becoming a pure corporate player, it had abandoned the democratic mission that had defined its first 150 years—bringing financial security to all Americans, not just those fortunate enough to work for companies with good benefits.

As employees gathered for MetLife's 155th anniversary celebration in 2023, the contrast with past milestones was stark. No Snoopy mascot entertained the crowd. No stories of agents helping immigrant families. No celebration of serving "one in five Americans." Instead, presentations focused on blockchain initiatives, artificial intelligence, and partnerships with benefits platforms. The transformation from mutual insurer to public corporation to pure B2B player was complete. Whether this was triumph or tragedy depended entirely on one's perspective—and whether one measured success in shareholder returns or social impact.

XI. Playbook: Business & Strategy Lessons

The story of MetLife offers a masterclass in corporate evolution, revealing timeless principles about building, scaling, and transforming financial services companies. Through 160 years of booms, busts, wars, and technological revolutions, certain strategic patterns emerge that transcend the insurance industry and offer lessons for any business navigating long-term change.

The Power of Distribution Innovation

MetLife's greatest innovation wasn't a product—it was a distribution model. The industrial insurance system, with agents collecting nickel premiums door-to-door, seems quaint today. But it solved a fundamental problem: how to profitably serve customers who couldn't afford traditional products. By going to customers rather than waiting for them to come to the company, MetLife discovered an enormous untapped market.

This principle—that distribution innovation can be more powerful than product innovation—remains relevant today. Uber didn't invent taxis; it revolutionized how people access them. Amazon didn't invent retail; it transformed how products reach consumers. MetLife's door-to-door agents were the 19th century equivalent of mobile apps—bringing the service directly to the customer at their convenience.

The model also created switching costs through relationships. The MetLife agent became part of the community fabric, attending weddings and funerals, offering financial advice, serving as a trusted intermediary between the corporate entity and the local community. This human connection created loyalty that transcended price competition—a moat that protected MetLife's franchise for decades.

Timing Market Structure Changes

MetLife's history is punctuated by perfectly timed structural transformations. The shift to industrial insurance in 1879 coincided with massive immigration and industrialization. Mutualization in 1915 occurred just as Progressive Era reforms made stock ownership suspect. Demutualization in 2000 captured the peak of the dot-com bubble's liquidity. The Brighthouse spinoff in 2017 preceded a regulatory rollback under the Trump administration.

These weren't lucky coincidences but deliberate strategic choices to align corporate structure with prevailing economic and political winds. The lesson: market structure changes—regulation, deregulation, consolidation, fragmentation—create windows of opportunity that, once closed, may not reopen for decades. Companies that recognize and act on these moments can transform their competitive position overnight.

Scale as Competitive Advantage in Financial Services

MetLife's relentless pursuit of scale, particularly during the 2001-2010 acquisition spree, reflected a fundamental truth about financial services: scale economics are everything. Larger insurance pools mean more predictable claims. Bigger investment portfolios access better opportunities. Greater geographic diversification reduces concentration risk.

But scale in financial services differs from manufacturing or technology. It's not just about unit cost reduction; it's about risk distribution and capital efficiency. MetLife's acquisition of ALICO didn't just add customers; it diversified mortality risk across different populations with different life expectancies, health profiles, and economic conditions. This risk diversification allowed more aggressive product pricing and capital deployment.