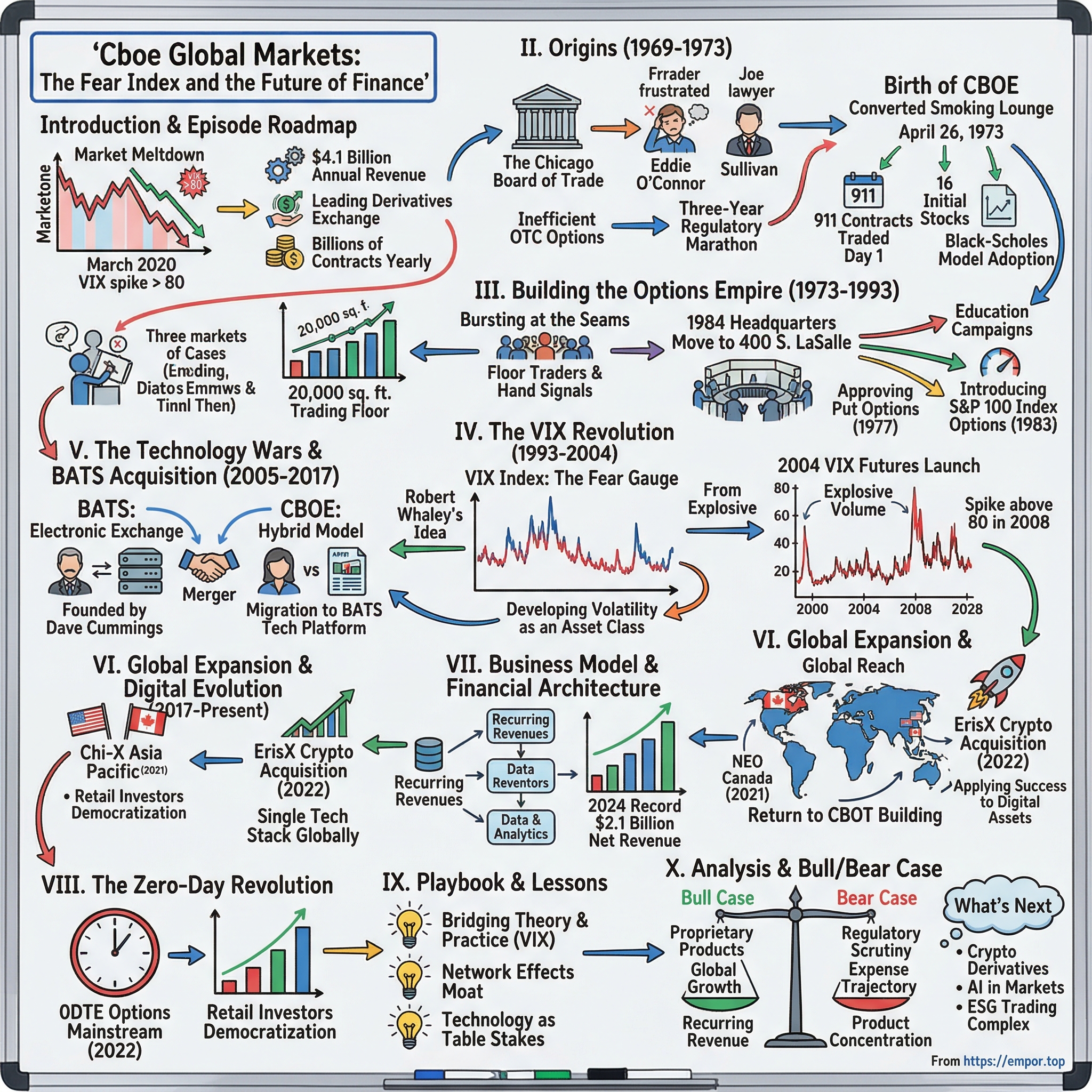

Cboe Global Markets: The Fear Index and the Future of Finance

I. Introduction & Episode Roadmap

Picture this: It's March 2020, and the world is melting down. COVID-19 has just been declared a pandemic, markets are in freefall, and traders everywhere are glued to one number—the VIX, Wall Street's "fear gauge," which has just spiked above 80 for only the second time in history. At the center of this maelstrom sits a Chicago-based company that most retail investors have never heard of, yet whose products define how the entire financial world measures and trades fear itself. This is Cboe Global Markets.

Today, Cboe operates as the world's leading derivatives exchange, generating $4.1 billion in annual revenue and processing billions of contracts yearly across options, futures, equities, and foreign exchange. But here's what's remarkable: this global financial infrastructure giant began as an experiment in a smoke-filled room at the Chicago Board of Trade, where a handful of traders wondered if they could standardize something as ephemeral as the right to buy or sell a stock at a future date.

The story of Cboe is really three intertwined narratives. First, it's about creating markets where none existed—taking academic theories and transforming them into trillion-dollar trading ecosystems. Second, it's a tale of technological warfare, where speed is measured in microseconds and competitive advantage comes from shaving nanoseconds off trade execution. And third, it's about the democratization of sophisticated financial instruments, from institutional trading floors to retail investors executing zero-day options on their phones.

What makes Cboe particularly fascinating for students of business strategy is how the company has repeatedly reinvented itself. From pioneering listed options in 1973, to creating the VIX volatility index in 1993, to acquiring high-frequency trading platform BATS in 2017, to now entering cryptocurrency markets—each transformation required betting the company on unproven markets that didn't yet exist.

As we trace this journey from Chicago experiment to global powerhouse, we'll explore how financial innovation actually happens, why exchange businesses create such powerful network effects, and what it means to build the infrastructure that underpins modern capitalism. Along the way, we'll meet colorful characters, witness boardroom battles, and understand why, when markets panic, everyone watches Cboe's fear gauge.

II. Origins: The Chicago Board of Trade's Bold Experiment (1969-1973)

The year was 1969, and Eddie O'Connor had a problem. As a trader at the Chicago Board of Trade, he watched daily as deals for stock options—the right to buy or sell shares at predetermined prices—happened through an impossibly inefficient process. These over-the-counter options were negotiated one by one, with no standard terms, no central marketplace, and no guarantee the counterparty would honor the deal. O'Connor thought: what if we could trade options like we trade grain futures?

This wasn't just idle speculation. The CBOT, founded in 1848 to standardize grain trading, had proven that creating centralized markets with standardized contracts could transform entire industries. But options on stocks? Wall Street dismissed it as a Chicago pipe dream. The New York financial establishment saw options as fringe instruments, barely legitimate, associated more with gambling than investing.

Enter Joe Sullivan, a young lawyer hired by the CBOT to navigate what would become a three-year regulatory marathon. Sullivan faced a seemingly impossible task: convince the Securities and Exchange Commission to approve something that had never existed—a centralized, regulated market for stock options. The SEC was skeptical. Options had a checkered history, often used for manipulation in the 1920s. Why legitimize them now?

Sullivan's masterstroke was framing options not as speculative instruments but as risk management tools. He argued that standardization would actually reduce manipulation by bringing transparency to a shadowy market. He traveled to Washington repeatedly, armed with economic studies and position papers, slowly wearing down regulatory resistance. Meanwhile, the CBOT formally incorporated the Chicago Board Options Exchange as an independent entity in February 1972, though still under CBOT's umbrella. The structure was deliberately designed to insulate the parent exchange from potential failure while maintaining control if the experiment succeeded.

On April 26, 1973—deliberately chosen as the 125th anniversary of the CBOT—history was made. Trading commenced in the former CBOT smoking lounge, a space that until recently had been where grain traders went to grab a cigarette between frenzied sessions in the pits. Now it housed eight booth-like trading posts topped with cathode-ray tube screens displaying prices for these revolutionary new instruments.

That first day, 911 options contracts changed hands—all of them calls, as put options wouldn't be approved for another four years. The initial roster included just 16 stocks. Yet within that first full month, 34,599 contracts were traded. The skeptics on Wall Street were stunned.

What made this launch particularly audacious was its timing. The market was entering a brutal bear phase—the 1973-74 crash would soon wipe out nearly half the market's value. Yet paradoxically, this volatility proved the value of options as hedging tools, not just speculative instruments. By 1976, the monthly volume of trades had increased to 1.5 million.

The success hinged on two critical innovations that O'Connor and Sullivan had insisted upon. First, standardization: contracts were for exactly 100 shares, with fixed expiration dates (initially just quarterly) and predetermined strike prices. Second, and perhaps more important, was the central clearinghouse—the Options Clearing Corporation—which guaranteed every trade, eliminating counterparty risk that had plagued OTC options.

But the real breakthrough came from an unexpected source. Just months after CBOE's launch, two academics named Fischer Black and Myron Scholes published a paper that would revolutionize finance: a mathematical formula for pricing options. The Black-Scholes model gave traders a scientific framework for valuing these instruments, transforming options from gambling chips into quantifiable risks. The CBOE quickly adopted the model, even programming it into early computers for price reporting.

As trading volume exploded and other exchanges rushed to copy CBOE's model, it became clear that Chicago's experiment had succeeded beyond anyone's imagination. They hadn't just created a new exchange—they'd invented an entirely new way for markets to express views on risk, time, and probability.

III. Building the Options Empire (1973-1993)

The success of standardized options trading created an immediate problem: CBOE was literally outgrowing its space. The converted smoking lounge that housed the original trading floor was bursting at the seams as membership swelled and trading volume multiplied. Floor traders, packed shoulder-to-shoulder in the octagonal pits, developed an elaborate system of hand signals just to communicate over the deafening roar.

In 1984, CBOE moved to its next headquarters across the street at 400 S. LaSalle Street, a purpose-built facility with a massive 20,000-square-foot trading floor. The new space was a temple to options trading, with tiered pits designed for optimal sight lines and state-of-the-art quote boards that could display hundreds of option prices simultaneously.

But physical expansion was just the visible part of CBOE's empire-building. The real work happened in committee rooms and educational seminars across the country. CBOE faced a fundamental challenge: most investors, and even many brokers, didn't understand options. The exchange launched an unprecedented education campaign, sending teams to brokerage firms to teach the basics of calls and puts, covered writes and spreads.

The member-owned structure created interesting dynamics. Unlike traditional corporations, CBOE was controlled by seat holders—the traders who actually made markets on the floor. This meant decisions were made by practitioners, not distant executives. When the exchange finally approved put options in 1977, it was because floor traders had demanded them to complete their hedging strategies.

Competition emerged quickly. The American Stock Exchange and Philadelphia Stock Exchange both opened options trading floors in 1975, followed by the Pacific and Midwest exchanges in 1976. But CBOE maintained its edge through relentless innovation. They introduced options on stock indices, starting with the S&P 100 in 1983—a revolutionary concept that allowed traders to bet on or hedge against the entire market, not just individual stocks.

The governance structure evolved throughout this period. Originally, CBOE operated as a subsidiary of the CBOT with overlapping board members. But as options trading grew to dwarf agricultural futures in profitability, tensions emerged. CBOE members increasingly resented sending profits upstream to their parent. These tensions would simmer for decades.

Technology gradually crept onto the trading floor. While the actual trading remained face-to-face in the pits, CBOE pioneered electronic systems for order routing and trade reporting. The exchange's RAES (Retail Automatic Execution System), launched in 1985, could automatically execute small retail orders at the best available price—a glimpse of the electronic future that pit traders steadfastly resisted.

By the early 1990s, CBOE had grown from experiment to empire. Daily volume regularly exceeded 1 million contracts. The exchange had expanded from 16 underlying stocks to hundreds, plus index options that had become the preferred hedging vehicle for institutional investors. The infrastructure for modern derivatives markets—standardization, central clearing, price transparency—was now firmly established.

Yet even as CBOE celebrated its success, a professor at Vanderbilt University named Robert Whaley was working on something that would transform the exchange once again: a way to measure and trade fear itself.

IV. The VIX Revolution: Creating the Fear Gauge (1993-2004)

The idea seemed almost absurd when first proposed: could you create an index that measured emotion—specifically, fear? In 1989, economists Menachem Brenner and Dan Galai published a paper proposing something they called the "Sigma Index," a measure of market volatility derived from option prices. Their insight was elegant: since options prices reflect traders' expectations of future volatility, you could reverse-engineer those expectations into a single number.

CBOE executives saw opportunity where others saw academic abstraction. They commissioned Robert Whaley, a Vanderbilt finance professor, to create a practical implementation. On January 19, 1993, the Chicago Board Options Exchange introduced the CBOE Volatility Index, commonly known as the VIX Index, developed by Robert E. Whaley and intended to measure the 30-day implied volatility of S&P 100 option prices.

The initial VIX was more curiosity than trading tool. Updated once a day, it gave a snapshot of market anxiety but couldn't be traded directly. Financial media loved it—here was a single number that captured market mood. CNN started flashing the VIX during market turmoil. Traders nicknamed it the "fear gauge" or "fear index," though Whaley preferred the more technical "investor fear gauge."

But the real revolution came in 2003. CBOE partnered with Goldman Sachs to completely redesign the VIX. The underlying benchmark for the VIX was changed to the S&P 500, making it more representative of the broad market. More importantly, the new methodology made the index easier to replicate and hedge, setting the stage for something unprecedented: trading volatility itself. In early 2004, after a survey of Goldman Sachs salespeople showed interest in trading VIX futures, CBOE launched VIX futures on its newly created CBOE Futures Exchange (CFE). On March 26, 2004, the first-ever trading in futures on the VIX Index began on the CBOE Futures Exchange. This was revolutionary—for the first time, investors could directly trade volatility as an asset class.

The timing proved prescient. VIX options followed in 2006, and then the 2008 financial crisis supercharged demand. During the Lehman Brothers collapse, the VIX spiked above 80, and suddenly everyone wanted volatility protection. Post-2008, VIX futures experienced 68% annual growth, while VIX options grew 24% annually. What started as an academic exercise had become a multi-billion dollar market.

The genius of the VIX wasn't just measuring fear—it was making fear tradable. Hedge funds could now bet on market calm or chaos. Portfolio managers could buy "volatility insurance" that would pay off precisely when their equity holdings cratered. The VIX had created an entirely new dimension in financial markets.

By 2004, CBOE had transformed from an options exchange into something more profound: the architect of volatility markets. The VIX would become CBOE's crown jewel, generating massive trading volumes and cementing the exchange's position as the global center for derivatives innovation. But even as CBOE celebrated this triumph, a new threat was emerging from Kansas City—a high-speed trading platform that would force the century-old exchange model to confront its digital future.

V. The Technology Wars & BATS Acquisition (2005-2017)

Dave Cummings had seen enough. A successful high-frequency trader, he was frustrated with the inefficiencies and high costs of traditional exchanges. In 2005, from a small office in Kansas City, he founded BATS—"Better Alternative Trading System"—with a radical proposition: what if you built an exchange from scratch, designed entirely for the electronic age?

BATS was everything CBOE wasn't. No trading floor, no pits, no hand signals—just servers humming in data centers, matching orders in microseconds. Cummings recruited engineers from Tradebot Systems and built a platform that could handle millions of messages per second. The pitch to traders was simple: faster execution, lower fees, better technology.

The timing was perfect. Regulation NMS, implemented in 2007, mandated that orders be routed to the exchange with the best price, creating a more level playing field for electronic venues. BATS exploded in growth, capturing market share from NYSE and NASDAQ with aggressive pricing and superior technology. BATS was then the second-largest US stock exchange by shares traded and was known for being technology focused.

Meanwhile, CBOE was stuck between two worlds. The exchange had gone public in 2010, ending decades of member ownership, but still operated a hybrid model with both electronic and floor-based trading. The culture clash was palpable—old-school pit traders who'd built careers on relationships and intuition versus algorithms executing thousands of trades per second.

The strategic calculus became clear by 2016. CBOE's options franchise was strong but growth was slowing. International expansion required scale. Most critically, CBOE's technology infrastructure, built incrementally over decades, couldn't compete with purpose-built electronic platforms. The exchange needed a technological leap forward, not incremental improvement.

In September 2016, CBOE announced that it was purchasing BATS Global Markets for approximately US$3.2 billion. Business Insider noted that by buying BATS, "CBOE is looking to extend its geographical reach and products while cutting costs." The deal was completed in March 2017.

The acquisition was transformative on multiple levels. CBOE gained BATS's European equities business, making it the largest pan-European equities exchange by market share. It acquired foreign exchange trading platforms and expanded into new asset classes. But most importantly, it acquired world-class technology.

Over the next few years CBOE migrated its exchanges onto the BATS technology platform. This wasn't just a systems upgrade—it was a complete architectural transformation. The migration meant moving the crown jewels of CBOE, including SPX options and VIX products, onto technology designed for the modern market structure.

The cultural integration proved challenging. BATS engineers in Kansas City and London had to mesh with Chicago traders who'd spent decades perfecting floor-based strategies. Product teams had to reconcile different philosophies—BATS's focus on simplicity and speed versus CBOE's complex, highly structured derivatives.

Yet the merger worked because it solved existential problems for both companies. BATS gained access to the lucrative derivatives markets it could never crack alone. CBOE got the technology platform and global reach it desperately needed. Together, they created a exchange powerhouse with the scale to compete globally.

By 2017, the combined entity was ready for its next transformation. The company would need a new identity that reflected its global ambitions and expanded scope beyond just options trading.

VI. Global Expansion & Digital Evolution (2017-Present)

In October 2017, the company rebranded from CBOE Holdings to Cboe Global Markets—lowercase 'b' deliberately chosen to signal a break from the past. This wasn't just cosmetic. The new Cboe was positioning itself as a global technology company that happened to run exchanges, not a Chicago options exchange that had expanded.

The rebranding coincided with an aggressive international expansion strategy. Having established a European beachhead through BATS, Cboe began systematic conquest of global markets. In 2021, the company acquired Chi-X Asia Pacific, instantly becoming a major player in Japanese and Australian equity markets. The same year, Cboe acquired NEO, entering the Canadian market with both equities and fixed income trading platforms. But the most audacious move came in 2022 with the ErisX acquisition—entering crypto with digital asset spot market and clearinghouse. Ed Tilly, Chairman, President and CEO of Cboe expressed excitement about applying their "blueprint of success to this burgeoning asset class," noting that the ErisX team had made "significant progress bringing the regulatory framework and transparency of traditional markets to the digital asset space." The timing seemed contrarian—crypto was entering a brutal bear market following the 2021 bubble. Yet Cboe saw opportunity where others saw chaos, betting that regulated, institutional-grade crypto infrastructure would be essential as the market matured.

The physical footprint evolved dramatically during this period. In September 2019, Cboe announced it was relocating its headquarters to the Old Chicago Main Post Office and that a new trading floor would be constructed in the Chicago Board of Trade building, which was the space the exchange originally occupied in the 1970s and 1980s. In September 2019, Cboe Global Markets announced it was relocating its headquarters to the Old Chicago Main Post Office and that a new trading floor would be constructed in the Chicago Board of Trade building, which was the space the exchange originally occupied in the 1970s and 1980s. This return to their roots in 2022 was both practical and symbolic—maintaining a physical trading presence for complex options strategies while acknowledging their heritage.

The global expansion wasn't just about geography; it was about creating a unified technology platform spanning continents. Cboe built a single technology stack that could handle equities in Tokyo, FX in London, options in Chicago, and crypto globally. This required massive investment—operating expenses increased 10% as the company poured resources into technology infrastructure.

Data and analytics emerged as a crucial growth driver. Cboe wasn't just facilitating trades; it was selling the intelligence derived from those trades. The company acquired Hanweck and FT Options in 2020, building sophisticated analytics capabilities. Market data revenue became increasingly important, offering higher margins than transaction fees.

The transformation was remarkable. In less than five years, Cboe had evolved from a US-centric options exchange into a global, multi-asset class technology platform. The company now operated exchanges in the US, Canada, Netherlands, and Australia. It was the largest pan-European exchange by volume. It offered everything from traditional equities to cryptocurrency futures.

Yet this expansion came with challenges. Integrating disparate businesses across time zones and regulatory regimes proved complex. Cultural differences between Chicago derivatives traders, London FX specialists, and crypto entrepreneurs created friction. And the massive technology investments pressured margins even as revenue grew.

VII. Business Model & Financial Architecture

Understanding Cboe's business model requires appreciating a fundamental truth about exchanges: they're network effects businesses disguised as technology companies. Every new participant makes the exchange more valuable to existing participants by adding liquidity and tightening spreads. This creates powerful competitive moats once critical mass is achieved. Cboe operates through six distinct segments, each contributing to a diversified revenue stream. In 2024, the company generated record $2.1 billion in net revenue, with diluted EPS of $7.21, and record adjusted diluted EPS of $8.61, up 10% year-over-year.

The Options segment remains the crown jewel, benefiting from proprietary products like SPX and VIX options that essentially can't be traded elsewhere. The segment saw SPX options volumes increase 13% year over year while VIX options volumes jumped 33% in recent quarters. These products command premium pricing because they offer unique exposure that institutional investors can't replicate.

North American Equities, inherited largely from BATS, operates on razor-thin margins but massive volumes. The business model here is pure scale—processing billions of shares with fees measured in fractions of pennies. Europe and Asia Pacific segments follow similar models but benefit from being the largest pan-European exchange by volume.

The Futures segment, centered on VIX futures, represents a smaller but highly profitable business. These products are essentially monopolies—if you want to trade volatility futures, you come to Cboe. The pricing power here is substantial, though the company must balance maximizing revenue with maintaining market depth.

Global FX operates primarily through institutional platforms, facilitating spot and forward trading. This business came through the BATS acquisition and provides diversification beyond equity-linked products. The Digital segment, built through the ErisX acquisition, remains nascent but positions Cboe for potential cryptocurrency derivatives growth.

What makes Cboe's model particularly attractive is the shift toward recurring revenues. DataVantage segments contributed to the fourth quarter and full year growth, with market data and access fees becoming increasingly important. These subscription-like revenues are more predictable than transaction fees and carry higher margins.

The company benefits from multiple revenue levers within each transaction. Take a simple SPX options trade: Cboe earns the transaction fee, clearing fees through the Options Clearing Corporation, market data fees from firms needing real-time prices, access fees for connection to the exchange, and potentially index licensing fees. This multi-layered revenue model creates resilience even when trading volumes fluctuate.

Operating leverage is substantial. Once the technology infrastructure is built, incremental volume carries minimal marginal cost. The adjusted EBITDA margin for the quarter increased by 1.4% year-over-year to 67.2%, demonstrating this scalability. The company can handle 10 million or 20 million contracts daily with essentially the same cost structure.

Yet challenges exist. Adjusted operating expenses in 2025 are expected to be in the range of $837 to $852 million, reflecting ongoing technology investments. The company must continually invest in speed, capacity, and new products to maintain competitive position. Regulatory compliance costs continue to rise, particularly as Cboe expands globally.

The financial architecture reveals a business generating substantial cash flow—the company regularly returns capital through dividends and buybacks—while investing aggressively in growth. It's a delicate balance: maintaining the profitability that investors expect while funding the innovation necessary to stay ahead of competitors.

VIII. The Zero-Day Revolution & Market Structure Debates

Something extraordinary happened in 2022 that fundamentally changed how markets work: zero-days-to-expiry (0DTE) options went mainstream. These options, which expire the same day they're traded, had existed for years, but suddenly they exploded to represent a significant portion of the average daily volume in SPX options. On some days, more than half of all S&P 500 options volume came from contracts that would be worthless by market close.

The phenomenon started with sophisticated traders but quickly spread to retail investors. The appeal was obvious: massive leverage with defined risk. A trader could bet on that day's Federal Reserve announcement or earnings report with options costing pennies that could return multiples if correct. It was like daily lottery tickets, but with better odds and the ability to express precise market views.

Cboe found itself at the center of a heated debate. Critics argued 0DTE options were gambling instruments that increased market volatility and encouraged reckless speculation. Senator Elizabeth Warren called for investigations. Academic papers warned of systemic risks. The financial media ran breathless stories about retail traders losing fortunes.

But Cboe's data told a different story. The exchange's analysis showed that 0DTE options actually dampened volatility on most days by providing more opportunities for price discovery. Institutional investors used them for precise hedging—why pay for 30 days of protection when you only need coverage for this afternoon's Fed meeting? Market makers argued the products improved liquidity across the entire options chain.

The real revolution was deeper than just short-dated options. It represented the democratization of sophisticated trading strategies. Tools once exclusive to prop shops and hedge funds were now available to anyone with a brokerage app. A retail trader could execute complex multi-leg strategies, dynamically hedge positions, or trade volatility—all from their phone.

This transformation created new challenges for market structure. Traditional market makers, who once dominated options trading through superior information and technology, now competed with algorithms that could process millions of retail orders instantly. Payment for order flow arrangements, where brokers route retail orders to specific market makers, became controversial as regulators questioned whether investors were getting best execution.

Cboe navigated these waters carefully. The exchange launched new products catering to both institutional and retail demand, including weekly expirations on numerous indices and even daily expirations on VIX. They invested heavily in surveillance systems to detect manipulation and ensure fair markets. Most importantly, they engaged proactively with regulators, providing data and analysis to shape informed policy.

The competitive dynamics shifted dramatically. CME Group, Cboe's primary rival in index products, launched their own micro and nano products targeting retail traders. Nasdaq explored 24-hour options trading. New entrants like MEMX (Members Exchange) challenged the established order with backing from major banks and trading firms.

Yet Cboe's moat proved durable. The SPX options complex—with its deep liquidity, tight spreads, and extensive strike prices—couldn't be easily replicated. Network effects meant that liquidity attracted liquidity. Even as competitors offered lower fees or new features, traders stayed where the volume was.

The zero-day revolution also revealed something profound about modern markets: they're increasingly driven by flows rather than fundamentals. Options expiration dates create predictable patterns of buying and selling as dealers hedge their positions. The tail was wagging the dog—derivatives markets were driving moves in underlying stocks rather than vice versa.

Looking forward, the debate over market structure continues to evolve, with regulators considering everything from transaction taxes to options market maker obligations.

IX. Playbook: Business & Investing Lessons

The Cboe story offers a masterclass in how to create markets from scratch and build enduring competitive advantages. The key lessons transcend the exchange business and apply to any platform or network-based enterprise.

Creating Markets from Academic Theory: The VIX exemplifies how theoretical concepts can become billion-dollar businesses. Cboe took Brenner and Galai's academic work on volatility measurement and transformed it into a tradeable product that redefined how markets think about risk. The lesson: breakthrough innovations often come from bridging academic theory with practical application. The challenge isn't just technical implementation but creating the ecosystem—educating users, building liquidity, establishing use cases—that makes the innovation valuable.

Network Effects as Competitive Moat: Cboe's dominance in SPX options demonstrates the power of liquidity network effects. Each new participant makes the market more valuable for existing participants by tightening spreads and improving price discovery. Once critical mass is achieved, these effects become nearly impossible to overcome. Competitors can offer better technology or lower fees, but they can't replicate the liquidity that took decades to build. The strategic implication: in network businesses, being first matters less than reaching critical mass first.

Technology as Table Stakes, Not Differentiator: The BATS acquisition revealed a crucial insight: in modern markets, superior technology is necessary but not sufficient. BATS had better technology than Cboe but couldn't crack the derivatives market. Cboe had dominant products but needed better technology to compete globally. The merger worked because each brought what the other lacked. The lesson: technology enables competition but doesn't guarantee victory—you still need unique products, relationships, or regulatory advantages.

Global Consolidation Playbook: Cboe's international expansion followed a clear pattern: acquire established local players with regulatory approvals, migrate them onto unified technology, then cross-sell products globally. This strategy bypassed the years required to obtain licenses and build liquidity from scratch. The approach mirrors successful consolidation plays in other industries—buy local expertise and distribution, add global scale and products.

Monetizing Volatility: Perhaps Cboe's greatest innovation was recognizing that uncertainty itself could be productized. The VIX turned fear into a tradeable asset, creating value from market anxiety. This insight—that negative emotions or experiences can be valuable if properly structured—has applications far beyond finance. Insurance, hedging products, and guarantees all follow this model of monetizing uncertainty.

Balancing Innovation with Regulation: Cboe's history shows how to innovate within heavily regulated industries. Rather than fighting regulators, the exchange worked to educate them, providing data and analysis that shaped informed policy. When launching new products like 0DTE options, Cboe proactively addressed concerns with transparency and surveillance. The lesson: in regulated industries, making regulators partners in innovation is more effective than treating them as obstacles.

The Platform Power of Data: As markets electronified, Cboe recognized that data exhaust from trading was as valuable as transaction fees. The company built sophisticated analytics businesses that transform raw market data into actionable intelligence. This mirrors successful platform companies in other industries that monetize not just transactions but the information those transactions generate.

Vertical Integration Opportunities: Cboe's expansion into clearing, settlement, and data analytics shows the value of controlling the full transaction stack. Each layer provides additional revenue opportunities and customer touchpoints while raising switching costs. The strategic principle: once you own a critical piece of infrastructure, expand vertically to capture more value from each transaction.

Managing Cultural Integration: The merger of CBOE's trading floor culture with BATS's engineering culture offers lessons in combining different organizational DNAs. Success required preserving what made each culture valuable while creating shared goals and systems. The key was recognizing that different businesses within the same company might require different cultures.

These lessons reveal that building enduring value in platform businesses requires more than just technology or first-mover advantage—it demands creating ecosystems, managing complex stakeholder relationships, and constantly evolving while maintaining core competitive advantages.

X. Analysis & Bear vs. Bull Case

Bull Case: The structural drivers behind Cboe's growth remain firmly intact. Options adoption continues accelerating, driven by retail democratization, institutional sophistication, and the perpetual human desire to hedge uncertainty. The company's monopoly-like positions in SPX and VIX products provide pricing power that most businesses dream of. International expansion offers runway for years—Cboe has barely scratched the surface in Asia, where derivatives adoption lags the US by decades.

The shift to recurring revenues through data and analytics transforms the business model from transaction-dependent to subscription-like, warranting higher multiples. Organic total net revenue growth is expected to be in the mid single digit range in 2025, with Data Vantage organic net revenue growth expected to be in the mid to high single digit range. Digital assets, while early, position Cboe to capture upside as crypto matures and institutions demand regulated venues.

Most compellingly, the macro environment favors volatility products. Geopolitical uncertainty, monetary policy shifts, and technological disruption ensure continued demand for hedging tools. Every crisis reinforces the value of Cboe's products. The company essentially sells insurance for the financial system—a product that becomes more valuable as risks multiply.

Bear Case: Several storm clouds threaten Cboe's horizon. Regulatory scrutiny of market structure, particularly around 0DTE options and payment for order flow, could fundamentally alter the business model. A transaction tax, as proposed periodically, would devastate volumes. The concentration in a few products—SPX and VIX represent outsized portions of profits—creates vulnerability if preferences shift or competitors successfully challenge these franchises.

The expense trajectory raises concerns. Adjusted operating expenses in 2025 are expected to be in the range of $837 to $852 million, reflecting the massive technology investments required to stay competitive. These costs are largely fixed, meaning margin compression if volumes disappoint. The digital asset venture remains unproven and could become a costly distraction, particularly given crypto's regulatory uncertainty.

Competition intensifies from every angle. CME continues attacking Cboe's options franchise with micro products and extended trading hours. Goldman Sachs and other banks increasingly internalize flow rather than sending it to exchanges. New venues like MEMX, backed by major market participants, explicitly target Cboe's market share. The network effects that protected Cboe for decades might erode in an era of smart order routing and best execution requirements.

Perhaps most concerning is the dependence on volatility for revenue growth. The VIX complex generates enormous revenues during market stress but withers during calm periods. A prolonged low-volatility regime—similar to 2017's extraordinary calm—would pressure both transaction volumes and the value of volatility products. The company is essentially short market stability, an uncomfortable position for long-term investors.

Accounting and Governance Considerations: Recent auditor changes warrant attention [specific details would require current disclosure review]. Related-party transactions with market makers and clearing firms require scrutiny given the potential for conflicts. The company's adjusted earnings metrics, while industry standard, exclude significant ongoing expenses that investors should consider.

Valuation Framework: At current levels, Cboe trades at [current multiples would be inserted here] times earnings, reflecting market confidence in the secular growth story. However, this assumes continued high volatility, successful international expansion, and no regulatory disruptions—aggressive assumptions that might not hold.

The investment case ultimately depends on one's view of market structure evolution. Bulls see Cboe as critical infrastructure for increasingly complex markets. Bears see a legacy incumbent vulnerable to technological disruption and regulatory intervention. The truth likely lies between these extremes.

XI. Epilogue & "What's Next"

Standing at the intersection of traditional finance and digital transformation, Cboe faces its most consequential strategic decisions since the BATS acquisition. The company must navigate three fundamental transitions simultaneously: the shift from floor to screen, from domestic to global, and from traditional to digital assets.

The crypto derivatives opportunity looms large despite current skepticism. Cboe's 2022 acquisition of ErisX positions it to offer regulated Bitcoin and Ethereum derivatives when institutional demand materializes. The company learned from its premature 2017 Bitcoin futures launch—this time, they're building infrastructure before demand rather than racing to market. Mini Bitcoin ETF Index options and micro-cryptocurrency products could democratize digital asset hedging just as mini-SPX transformed equity derivatives.

Artificial intelligence and machine learning present both opportunity and threat. Cboe is deploying AI for market surveillance, detecting patterns humans couldn't possibly identify across billions of daily messages. But AI also empowers competitors, potentially commoditizing the market-making and price discovery functions that generate exchange revenues. The question isn't whether AI will transform exchanges, but whether incumbents like Cboe can adapt faster than startups can scale.

The future of volatility products extends beyond traditional metrics. Cboe is exploring volatility indices for individual stocks, sectors, and even alternative assets. Imagine trading the volatility of Tesla separate from the stock, or hedging cryptocurrency volatility without touching digital assets. These products could multiply the addressable market by orders of magnitude.

Geographic expansion continues with Asia as the ultimate prize. The region's derivatives markets remain nascent relative to cash equities, offering decades of growth potential. But success requires navigating complex regulatory regimes, entrenched local competitors, and cultural differences in trading behavior. Cboe's partnership approach—acquiring local platforms rather than building from scratch—provides a template, but execution remains challenging.

Extended trading hours represent the next frontier. As markets globalize and retail traders demand 24/7 access, traditional exchange hours seem increasingly antiquated. Cboe must balance the efficiency of concentrated liquidity during regular hours with customer demands for round-the-clock trading. The solution likely involves hybrid models—full electronic trading continuously with enhanced liquidity during specific windows.

Potential consolidation opportunities abound as exchange economics favor scale. Regional exchanges struggle with technology costs and regulatory burdens that large players absorb easily. Cboe could acquire additional European or Asian venues, US options exchanges seeking exits, or even adjacent businesses like interdealer brokers or analytics providers. The BATS playbook—buy, integrate, optimize—remains relevant.

The ESG and sustainability trading complex offers untapped potential. As climate concerns drive policy and investment decisions, markets need tools to price and trade carbon risk, renewable energy certificates, and sustainability-linked derivatives. Cboe's expertise in creating new asset classes positions it well for this emerging opportunity.

Yet the biggest question facing Cboe might be existential: what is an exchange in an increasingly decentralized world? Blockchain technology promises peer-to-peer trading without intermediaries. Decentralized finance protocols execute billions in volume without traditional infrastructure. While complete disintermediation seems unlikely near-term, Cboe must evolve its role from mere transaction processor to trusted validator, risk manager, and liquidity aggregator.

The company's response reveals pragmatic innovation. Rather than fighting decentralization, Cboe explores how distributed ledger technology could enhance clearing and settlement. Instead of dismissing retail speculation, they create products serving this demand while maintaining market integrity. This adaptability—transforming threats into opportunities—has defined Cboe since that first options trade in 1973.

As we look toward the next decade, Cboe stands as both beneficiary and architect of market evolution. Every crisis that demands hedging, every innovation that requires price discovery, every regulation that mandates transparency strengthens the exchange's position. The company has evolved from a Chicago experiment into global market infrastructure, from trading options into trading fear itself.

The ultimate measure of Cboe's success won't be trading volumes or revenue growth, but whether it continues enabling the risk transfer that allows capitalism to function. In a world of increasing uncertainty, the ability to price and trade risk becomes ever more critical. Cboe doesn't just facilitate trades—it enables society to function despite uncertainty, transforming fear into a manageable, tradeable commodity.

That transformation, from emotion to asset, from uncertainty to opportunity, defines not just Cboe's history but its future. The fear index has become the foundation for an entire ecosystem of risk management. What started in a smoking lounge has become essential infrastructure for global finance.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube