Mondelez International: The Empire of Snacking

I. Cold Open & Episode Setup

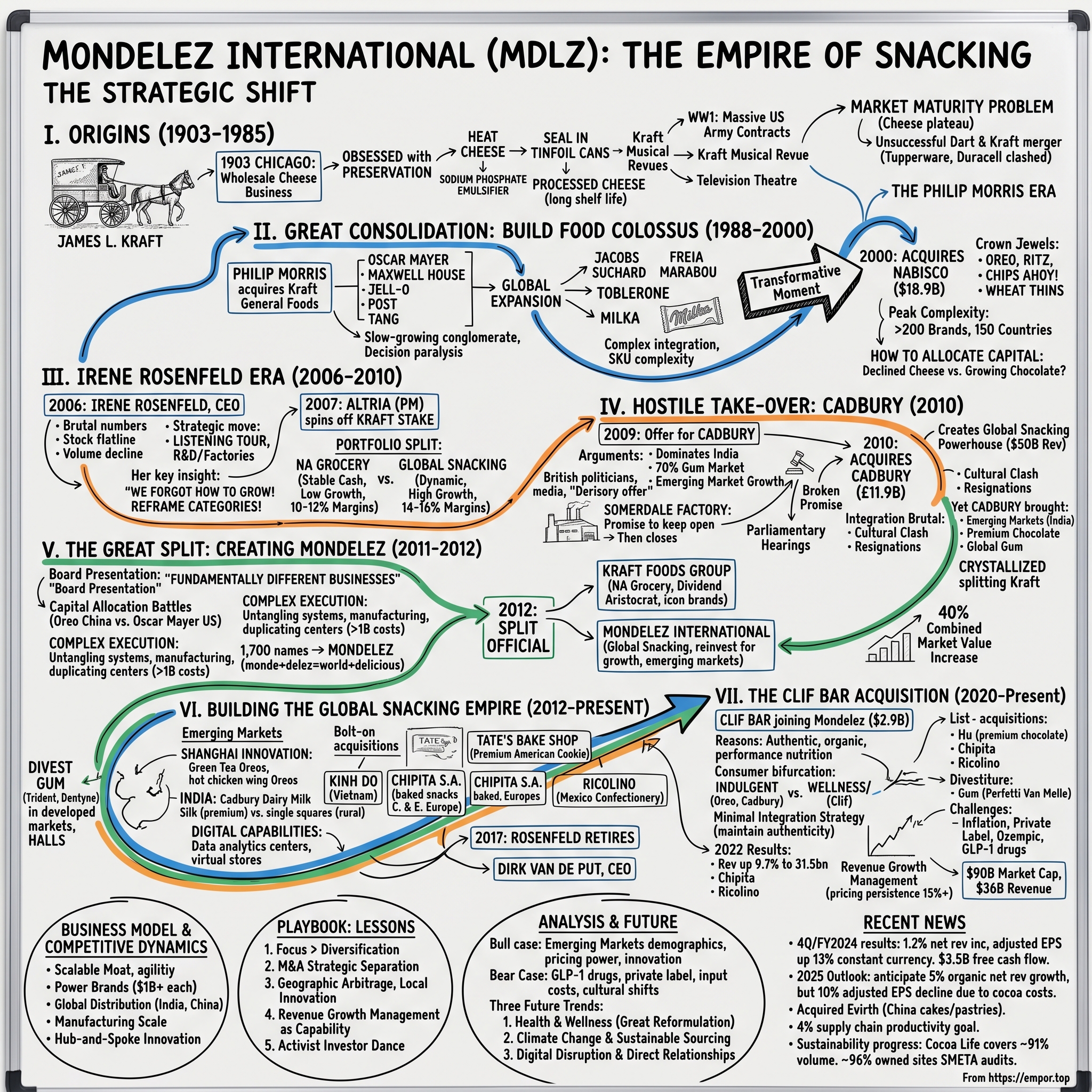

Picture this: It's 2011, and Irene Rosenfeld is standing before Kraft Foods' board in Northfield, Illinois, about to propose something radical. The company she leads generates $54 billion in annual revenue, employs 127,000 people, and sells everything from Oscar Mayer hot dogs to Oreo cookies. But Rosenfeld sees what others don't—these businesses have nothing in common anymore. The meeting that day would set in motion one of the most consequential corporate splits in food industry history, creating what would become Mondelez International.

Here's the provocative question that should keep every investor up at night: How does a century-old cheese company transform itself into the world's premier snacking powerhouse, commanding premium valuations while its grocery peers languish? The answer involves hostile takeovers, British parliamentary hearings, activist investors, and a fundamental reimagining of what a food company can be.

Today, Mondelez International stands as a $90 billion market cap colossus, generating $36 billion in revenue across more than 150 countries. Its brands—Oreo, Cadbury, Toblerone, Trident—aren't just products; they're cultural institutions worth billions each. The company controls approximately 14% of the global chocolate market and holds the #1 position in biscuits worldwide. In emerging markets, where the real growth lies, Mondelez commands even more impressive positions.

But this isn't just a story about scale. It's about focus—the deliberate, sometimes painful narrowing from a sprawling conglomerate to a pure-play snacking company. It's about recognizing that selling cheese in Wisconsin and selling chocolate in India require fundamentally different business models, growth trajectories, and investor bases.

The central tension that drives this entire narrative: In mature consumer markets, can you actually have both growth and margins? Mondelez's answer has been to abandon the slow-growth grocery aisles entirely, betting everything on the higher-margin, faster-growing world of snacking. Whether that bet pays off in an era of Ozempic, health consciousness, and private label pressure—well, that's what makes this story so compelling.

We'll trace this journey from James L. Kraft's horse-drawn cheese wagon in 1903 Chicago through the Philip Morris years, the hostile Cadbury takeover that shook Britain, and the strategic split that created today's snacking empire. Along the way, we'll unpack the playbook for value creation in consumer goods: when to buy, when to sell, when to split, and most importantly, when to completely reimagine your business.

II. Origins: The Kraft Cheese Dynasty (1903-1985)

The summer of 1903 was brutally hot in Chicago, and James Lewis Kraft was failing. The 29-year-old Canadian immigrant had invested his life savings—$65—into a wholesale cheese business, buying wheels of cheddar from Wisconsin farms and delivering them to Chicago grocers via horse-drawn wagon. Within months, he was nearly bankrupt. His horse, Paddy, was worth more than his remaining inventory.

But Kraft noticed something crucial: cheese spoiled quickly in those pre-refrigeration days, and grocers hated the waste. While competitors focused on volume, Kraft became obsessed with preservation. By 1915, he'd developed a revolutionary process—heating cheese to 175 degrees Fahrenheit, adding sodium phosphate as an emulsifier, then sealing it in tinfoil-lined cans. The result: processed cheese that could last months without refrigeration.

World War I transformed Kraft from clever inventor to industrial titan. The U.S. Army needed shelf-stable protein for troops in European trenches. Kraft supplied 6 million pounds of processed cheese to the military, establishing both massive production capacity and a generation of Americans who'd grown accustomed to the taste. By 1920, Kraft was selling 15 million pounds annually.

The company went public in 1924, and J.L. Kraft proved as innovative in marketing as in food science. He sponsored the "Kraft Musical Revue" radio program in 1933—one of network radio's first branded shows. The Kraft Television Theatre followed in 1947, becoming appointment viewing for millions. These weren't just advertisements; Kraft was creating shared cultural moments around its brand. The product portfolio by 1980 was staggering: Kraft Singles (launched 1947), Cheez Whiz (1953), Cracker Barrel (1954), and dozens of other brands. But the company faced a classic mature-market problem—cheese consumption in America was plateauing. Growth required either international expansion or diversification, and Kraft had attempted both with mixed results.

In 1980, Kraft merged with Dart Industries (makers of Tupperware and Duracell batteries) to form Dart & Kraft. The logic seemed compelling—combine stable food cash flows with higher-growth consumer products. But the cultures clashed terribly. Tupperware's direct-sales model had nothing in common with grocery distribution. By 1986, the experiment ended with a demerger, and Kraft emerged independent but weakened.

Then came 1985 and the beginning of the Philip Morris era. Philip Morris Companies Inc. acquired General Foods for $5.6 billion, followed by Kraft itself in 1988 for $12.9 billion—at the time, the largest non-oil merger in U.S. history.

Why would a tobacco company want to own food brands? The answer reveals the strategic paranoia of 1980s Philip Morris. By 1985, cigarette consumption in the U.S. was declining, health concerns were mounting, and litigation threats loomed. CEO Hamish Maxwell saw food as the perfect hedge—recession-resistant, litigation-light, and offering similar brand management skills. Plus, Philip Morris generated so much cash from Marlboro that it needed productive deployment opportunities.

The 1988 Kraft acquisition wasn't friendly. Philip Morris launched a hostile bid, eventually paying $106 per share after Kraft's board initially rejected a $90 offer. John Richman, Kraft's CEO, fought the takeover for weeks before capitulating. The integration that followed would reshape American food.

III. The Great Consolidation: Building a Food Colossus (1988-2000)

The conference room at Philip Morris headquarters in New York, January 1989. Hamish Maxwell sits across from Michael Miles, the executive he's chosen to run the newly combined Kraft General Foods. The mandate is simple but audacious: create the world's largest food company by merging two proud, century-old organizations with completely different cultures.

The 1989 merger combined Kraft with Philip Morris's General Foods unit—makers of Oscar Mayer meats, Maxwell House coffee, Jell-O gelatin, Post Cereals, and Tang. On paper, the combination was brilliant. General Foods brought coffee and breakfast; Kraft dominated cheese and lunch. Together, they could own entire supermarket aisles.

But the reality proved messier. General Foods executives, based in White Plains, viewed themselves as sophisticated brand marketers—the people who'd invented Tang for NASA. Kraft managers in Glenview, Illinois, saw themselves as innovation-driven entrepreneurs. The cultures mixed like oil and water.

The merged entity became slow in addressing product line issues due to its size and company politics. Decision-making that once took weeks now required months of committee meetings. Innovation stalled. While smaller competitors launched new products, Kraft General Foods struggled to get approval for label changes.

Yet Philip Morris pushed forward with international expansion. In 1990, they acquired Jacobs Suchard, the European coffee and confectionery giant, along with Freia Marabou, a Scandinavian confectionery maker. These deals brought iconic brands like Toblerone, Milka, and Suchard into the portfolio. Suddenly, Kraft General Foods wasn't just American—it was global.

The Jacobs Suchard acquisition deserves special attention. Founded in 1825 in Switzerland, Jacobs Suchard had built a European empire around coffee and chocolate. The company owned Carte Noire coffee in France, Jacobs coffee in Germany, and chocolate brands across the continent. The $3.8 billion price tag was steep, but it gave Philip Morris instant European distribution and manufacturing.

Integration proved challenging. European operations ran differently—smaller production runs, more SKUs, complex labor regulations. The Toblerone factory in Bern had been making the same triangular chocolate for 80 years; now American executives wanted to "optimize" production. Cultural sensitivity wasn't Philip Morris's strong suit.

By 1995, Philip Morris reorganized again, creating Kraft Foods Inc. as the umbrella organization. The company now generated over $30 billion in annual revenue but growth was slowing. Mature markets, private label competition, and retail consolidation all pressured margins. CEO Bob Morrison, who'd replaced Michael Miles, focused on cost-cutting rather than growth. Wall Street yawned.

Then came the transformative moment: In 2000, Philip Morris acquired Nabisco Holdings for $18.9 billion and merged it with Kraft Foods. This wasn't just another acquisition—it was a bet-the-company move that would define the next decade.

Nabisco brought crown jewels: Oreo, Ritz, Chips Ahoy!, Wheat Thins, Triscuit, and dozens of other billion-dollar brands. The company traced its origins to 1898 when Adolphus Green merged several northeastern bakeries to form the National Biscuit Company. Through the 20th century, Nabisco had become synonymous with American snacking.

But Nabisco came with baggage. RJR Nabisco, its previous owner, had loaded the company with debt from the infamous 1989 leveraged buyout—the one immortalized in "Barbarians at the Gate." Cost-cutting had hollowed out R&D. Brands were under-invested. Manufacturing needed modernization.

In 2001, Philip Morris took Kraft Foods public, selling 280 million shares in what became the third-largest IPO of all time, raising $8.7 billion while retaining an 88.1% stake. The IPO valued Kraft at nearly $60 billion, making it instantly one of the world's most valuable food companies.

The portfolio at peak complexity was mind-boggling: over 200 brands across 150 countries. From Oscar Mayer hot dogs to Oreo cookies, Maxwell House coffee to Milka chocolate, Philadelphia cream cheese to Ritz crackers. The company operated 166 manufacturing facilities and employed 114,000 people. Annual revenue exceeded $33 billion.

But size brought problems. How do you manage brands with such different consumer bases, distribution channels, and growth profiles? How do you allocate capital between declining categories like processed cheese and growing ones like premium chocolate? How do you innovate when any new product might cannibalize five existing ones?

These questions would soon find an unlikely answer in a returning executive who'd left Kraft years earlier, frustrated by the bureaucracy. Her name was Irene Rosenfeld.

IV. The Irene Rosenfeld Era Begins (2006-2010)

June 26, 2006. Irene Rosenfeld walks into Kraft's Northfield headquarters as CEO for the first time in nearly three years. She'd left in 2003, exhausted by the Philip Morris bureaucracy, to run PepsiCo's Frito-Lay division. Now she was back, recruited by the board to revive a company that had lost its way.

The numbers were brutal. Kraft's stock had flatlined for five years. Volume was declining in 15 of 20 major categories. Market share was eroding to private label and nimbler competitors. Employee morale surveys showed record dissatisfaction. One executive later told me: "It felt like working in a food museum—great history, no future."

Rosenfeld's first move surprised everyone: she went on a listening tour. Not to Wall Street or major customers, but to Kraft's factories and R&D centers. She spent days in the Oreo plant in New Jersey, the Oscar Mayer facility in Wisconsin, the coffee operations in Europe. She ate lunch with line workers, sat in on brand meetings, even worked a packaging shift.

What she heard was devastating. Innovation had been replaced by endless cost-cutting. Brand managers spent more time on PowerPoints than products. The Philadelphia cream cheese team hadn't launched a significant innovation in five years. Oreo, despite being the world's favorite cookie, had no presence in China or India.

"We'd forgotten how to grow," Rosenfeld later reflected. "We were so focused on delivering quarterly earnings that we'd stopped investing in our brands' futures."

Her strategic authority expanded in March 2007 when Altria (Philip Morris's new name) spun off its remaining Kraft stake, distributing all shares to Altria shareholders. Finally, Kraft was independent—no longer a cash cow for a tobacco company but a standalone food enterprise.

Rosenfeld articulated a new vision: "Reframe the categories." Instead of accepting decline in mature markets, reimagine the products. Make Oreo a global power brand. Transform Tang from powdered nostalgia to emerging market phenomenon. Turn Cadbury—well, first she had to acquire Cadbury.

The operational turnaround was methodical. She restructured the company into five global units, eliminated layers of management, and pushed decision-making closer to markets. The "One Kraft" initiative broke down silos between U.S. and international operations. She increased advertising spending by 20% while simultaneously improving margins through supply chain optimization.

But the real insight was recognizing the fundamental split in Kraft's portfolio. On one side: North American grocery—Oscar Mayer, Kraft Macaroni & Cheese, Maxwell House. Stable, cash-generative, but growing at GDP or less. On the other: global snacking—Oreo, Trident, the European chocolate brands. Higher growth, better margins, enormous international potential.

In a 2008 investor presentation, Rosenfeld showed two charts that would prove prophetic. The first mapped revenue growth potential—snacking categories growing at 5-7% annually versus grocery at 1-2%. The second showed margin profiles—snacking delivering 14-16% operating margins versus grocery's 10-12%. The conclusion was obvious even if the solution wasn't: these businesses didn't belong together.

Wall Street initially loved the turnaround. Kraft's stock rose 40% in Rosenfeld's first two years. But she knew incremental improvement wasn't enough. The company needed a transformative acquisition to achieve global scale in snacking. Her target: Cadbury, the 180-year-old British confectionery icon.

The approach would trigger one of the most controversial takeover battles in corporate history.

V. The Cadbury Acquisition: A Hostile Takeover Story (2010)

August 2009. Rosenfeld sits in her Northfield office, staring at a map of global chocolate consumption. The opportunity is obvious: while Americans consume 11 pounds of chocolate annually, the global average is just 2 pounds. In China and India, it's measured in ounces. Whoever owns emerging market chocolate distribution will dominate the category for decades.

Cadbury controls that distribution. Founded by John Cadbury in Birmingham in 1824 as a social enterprise (the Cadbury family were Quakers who built model villages for workers), the company had become Britain's most beloved corporation. It dominated India through Cadbury Dairy Milk, owned 70% of the gum market through Trident and Dentyne, and generated £5.4 billion in revenue across 60 countries.

On September 7, 2009, Kraft made an unsolicited £10.2 billion ($16.7 billion) offer for Cadbury. The reaction was volcanic. Cadbury's chairman Roger Carr called it "derisory." British politicians denounced American corporate imperialism. The media painted Rosenfeld as a villain intent on destroying British heritage.

Cadbury CEO Todd Stitzer launched a fierce defense. In presentations titled "Transform Cadbury," he promised standalone growth that would exceed any merger benefits. He portrayed Kraft as a lumbering, debt-laden American conglomerate that would destroy Cadbury's unique culture. The rhetoric got personal—Stitzer called Kraft's products "cheap plastic cheese."

But Rosenfeld had done her homework. She knew Cadbury's vulnerabilities: slowing growth in developed markets, underinvestment in manufacturing, pressure from activists. She also knew Cadbury's shareholders—largely institutional investors who cared more about returns than heritage.

The Somerdale Factory became the battle's defining controversy. During negotiations, Rosenfeld promised to keep open Cadbury's historic Somerdale facility near Bristol, reversing Cadbury's own closure plans. It was a key concession to win political support. Within weeks of the deal closing, Kraft announced Somerdale would close anyway, citing "incomplete information" during due diligence.

The betrayal sparked parliamentary hearings. Rosenfeld was summoned to Westminster to explain herself. The Business Secretary called it "a straight broken promise." The incident would haunt Kraft's reputation in Britain for years, making future acquisitions politically toxic. By January 2010, facing competition from a potential Hershey-Ferrero counterbid and pressure from her own board, Rosenfeld raised the offer to £11.9 billion ($19.5 billion) or 840 pence per share plus a 10 pence special dividend—approximately £11.5 billion in total value. The final offer valued Cadbury at £11.9 billion (US$19.7 billion).

On 2 February 2010, Kraft secured over 71% of Cadbury's shares thus finalising the deal. The acquisition created a global snacking powerhouse with annual revenues of approximately $50 billion and sales in approximately 160 countries.

But integration proved brutal. Cultural differences ran deep—Cadbury's paternalistic Quaker heritage versus Kraft's quarterly earnings obsession. The promised investment in innovation often meant cost-cutting disguised as "efficiency." British managers fled in droves. On 3 February, the Chairman Roger Carr, chief executive Todd Stitzer and chief financial officer Andrew Bonfield all announced their resignations. Stitzer had worked at the company for 27 years.

Yet strategically, the deal was transformative. Cadbury brought exactly what Rosenfeld needed: emerging market presence, especially in India where Cadbury Dairy Milk held iconic status; global gum brands that complemented Kraft's portfolio; and premium chocolate to balance mass-market biscuits.

More importantly, Cadbury crystallized Rosenfeld's vision for splitting Kraft. The integration meetings revealed the fundamental incompatibility—Cadbury executives couldn't understand why they were discussing Velveeta cheese strategies. Oscar Mayer managers saw chocolate as a distraction from their core grocery business. The businesses literally spoke different languages.

By late 2010, with Cadbury integration underway but cultures clashing, Rosenfeld began planning something even bolder than the acquisition: completely splitting Kraft Foods into two separate companies.

VI. The Great Split: Creating Mondelez (2011-2012)

The boardroom at Kraft Foods headquarters, August 4, 2011. Irene Rosenfeld stands before a presentation that will reshape the entire company. The slide reads: "Strategic Rationale for Separation." What follows is a masterclass in corporate clarity.

"We have two fundamentally different businesses hiding inside one company," Rosenfeld began. "Our North American grocery business—stable, cash-generative, but growing slowly. Our global snacks business—dynamic, expanding internationally, with attractive margins. They require different strategies, different investment levels, different types of management. There are simply not enough common threads to justify keeping them together."

The board had seen this coming. Since the Cadbury acquisition, the tension between the businesses had become untenable. Capital allocation meetings devolved into zero-sum battles. Should they invest in expanding Oreo production in China or upgrading Oscar Mayer facilities in Wisconsin? Should management incentives prioritize growth or cash generation? Every decision became a compromise that satisfied no one.

The numbers made the case compelling. The snacking business—chocolate, biscuits, gum, candy—generated operating margins of 14-16% with organic revenue growth of 5-7% annually. The grocery business—cheese, meats, coffee, meals—delivered 10-12% margins with 1-2% growth. Different multiples, different investor bases, different futures.

But execution would be complex. Splitting a $50 billion company with operations in 170 countries required untangling everything from IT systems to pension obligations. Manufacturing facilities that produced both snacks and grocery products needed separation. Shared service centers supporting both businesses required duplication. The one-time costs would exceed $1 billion.

The naming process itself became a cultural flashpoint. The snacking company needed a new identity—global, modern, free from American grocery store associations. After considering 1,700 names and spending millions on consultants, they landed on Mondelez (pronounced "mon-dah-LEEZ"). The name combined "monde" (world in Latin) with "delez," a made-up word suggesting delicious. Critics mocked it as corporate gibberish. Employees struggled to pronounce it. But it was globally trademarkable and Google-unique.

Wall Street's initial reaction was skeptical. Why destroy synergies? Why duplicate costs? Why fix something that wasn't obviously broken? Activist investor Nelson Peltz, who'd taken a position in Kraft, publicly questioned the split's logic, arguing for selling higher-growth businesses instead.

But Rosenfeld had conviction born from operational reality. In investor meetings, she painted two futures: Kraft Foods North America would become a dividend aristocrat, returning cash to shareholders while maintaining iconic American brands. Mondelez International would reinvest for growth, expand in emerging markets, and build global snacking platforms.

October 1, 2012. The split becomes official. Kraft Foods Group begins trading on NASDAQ, focused entirely on North American grocery. Mondelez International debuts on NASDAQ the same day, inheriting the entire snacks portfolio plus international grocery operations. The market capitalization split roughly 35% to Kraft, 65% to Mondelez, reflecting their relative growth prospects.

The operational separation was remarkably clean. Within months, both companies were functioning independently with minimal disruption. Kraft Foods Group, led by Tony Vernon, immediately announced cost reductions and dividend increases. Mondelez, with Rosenfeld as CEO, unveiled aggressive emerging market expansion plans.

The contrast in trajectories proved immediate. In its first quarter as an independent company, Mondelez reported organic revenue growth of 4.1%, driven by emerging markets growing at 10%. Kraft Foods Group reported flat revenues but expanding margins through cost management.

By any financial measure, the split was a triumph. Within two years, the combined market value of both companies exceeded the pre-split valuation by over 40%. Each business could finally optimize for its natural investor base—growth seekers for Mondelez, income investors for Kraft.

Yet the human cost was substantial. Thousands of employees faced relocation or redundancy. Communities with factories producing both snacks and grocery products watched facilities close or dramatically downsize. The efficiency came at the price of disruption that rippled through hundreds of towns.

The split also marked a philosophical divide in food industry strategy. Would scale and diversification matter more, as companies like Nestlé and Unilever believed? Or would focus and specialization win, as Mondelez and Kraft were betting? The next decade would provide the answer.

VII. Building the Global Snacking Empire (2012-2020)

Shanghai, 2013. Inside a gleaming new Mondelez innovation center, food scientists work on something that would have seemed sacrilegious to American Oreo purists: green tea-flavored cream. Down the hall, another team develops hot chicken wing Oreos. In Beijing, researchers test Oreo wafer rolls, abandoning the iconic sandwich cookie format entirely.

This wasn't brand dilution—it was Rosenfeld's emerging markets masterplan in action. While U.S. consumers wanted their Oreos unchanged since 1912, Chinese consumers saw the original as too sweet, too big, too American. So Mondelez rebuilt Oreo for China: smaller packages, local flavors, lower price points. By 2014, Oreo became the #1 biscuit brand in China, a market where it barely existed five years earlier.

The emerging markets strategy was deceptively simple: take global brands, add local innovation, and invest aggressively in distribution. But execution required cultural sensitivity that old Kraft never possessed. In India, Mondelez launched Cadbury Dairy Milk Silk at premium price points while simultaneously selling single-square portions of regular Dairy Milk for a few rupees in rural villages. In Brazil, they created Lacta chocolate with higher melting points to survive tropical distribution. In Russia, they bought local champion Alpen Gold and gradually premiumized it.

As Rosenfeld proclaimed, "Together we have impressive global reach and an unrivalled portfolio of iconic brands, with tremendous growth potential. With annual revenues of approximately $50 billion, the combined company is the world's second largest food company".

The results were extraordinary. From 2012 to 2017, Rosenfeld delivered 20 of 21 quarters of organic revenue growth, a streak virtually unheard of in mature food companies. Emerging markets grew from 35% of revenue to 42%. Operating margins expanded 320 basis points despite heavy growth investments.

But Mondelez wasn't just growing organically. The company executed a series of surgical acquisitions that strengthened specific capabilities and geographic positions. In March 2004, Kraft acquired juice maker Veryfine, though this predated the Mondelez split. More relevant was the strategic portfolio reshaping in the Mondelez era. The acquisition portfolio was carefully curated. Kinh Do (2014): A leading snack company in Vietnam, which allowed Mondelēz to expand into the Southeast Asian market. In May 2018, Mondelēz announced an agreement to acquire Tate's Bake Shop for approximately $500 million. Tate's Bake Shop (2018): A premium American cookie brand, which allowed Mondelēz to bolster its domestic "premium" cookie and baked dessert portfolio.

The Tate's acquisition epitomized Mondelez's "bolt-on" strategy. In the four years since the close, Tate's has more than doubled revenues. By keeping it as a standalone business with its original management, Mondelez preserved the brand's authenticity while leveraging its distribution muscle.

But the real transformation came through digital capabilities. Mondelez built data analytics centers that tracked real-time consumption patterns across markets. They launched e-commerce platforms in China that went from zero to $500 million in sales within three years. They created "virtual stores" in subway stations where consumers could scan QR codes to order snacks for home delivery.

The operational discipline was remarkable. Despite investing heavily in growth, Mondelez improved gross margins from 37% to 40% through supply chain optimization. They reduced SKU complexity by 25% while increasing innovation output. They standardized manufacturing processes across regions while maintaining local product variations.

November 2017 marked a transition. After 11 years as CEO and having delivered exceptional shareholder returns, Rosenfeld announced her retirement. She handed leadership to Dirk Van de Put, a Belgian executive who'd previously run McCain Foods. Van de Put inherited a transformed company—focused, growing, and generating consistent returns.

Under Van de Put, the acquisition pace accelerated. On May 26, 2021, Mondelez announced an agreement to acquire Greek snack company Chipita S.A., a high-growth key player in the Central and Eastern European croissants and baked snacks category. On January 3, 2022, Mondelez announced that the acquisition was complete. In May 2022, it was announced Mondelez had acquired Grupo Bimbo's confectionery business, Ricolino, for approximately US$1.3 billion.

The portfolio reshaping continued with strategic divestitures. On May 10, 2022, Mondelez announced that it would sell its gum business, including Trident and Dentyne, in developed markets including North America and parts of Europe, as well as the entire Halls cough drop business. On December 19, 2022, Mondelez announced that it was selling its gum business, including the Trident, Dentyne, Chiclets and Bubblicious brands, to Perfetti Van Melle, the makers of Mentos.

By 2020, Mondelez had become exactly what Rosenfeld envisioned: a pure-play global snacking company with leading positions in chocolate, biscuits, and baked snacks. The transformation from American food conglomerate to international snacking powerhouse was complete.

VIII. The Clif Bar Acquisition & Portfolio Evolution (2020-Present)

June 2022, Emeryville, California. Sally Grimes, CEO of Clif Bar, stands before her employees with bittersweet news. After 30 years of fierce independence, turning down multiple acquisition offers, Clif Bar is joining Mondelez International for $2.9 billion. The room is silent—this company built its identity on remaining private, on doing business differently.

Mondelēz International announced an agreement to acquire Clif Bar & Company, leading U.S. maker of nutritious energy bars with organic ingredients, for $2.9 billion with additional contingent earnout consideration. The acquisition of leading on-trend brands CLIF®, LUNA® and CLIF Kid® expands Mondelēz International's global snack bar business to more than $1 billion.

The Clif Bar story represented both Mondelez's evolution and the broader transformation of food industry M&A. This wasn't about scale or cost synergies—Clif Bar would remain operationally independent. It was about buying into a consumer trend that Mondelez couldn't build internally: authentic, organic, performance nutrition.

Clif Bar's journey began in 1990 when Gary Erickson, a baker and cyclist, created an energy bar that actually tasted good. The company became famous for walking away from a $120 million acquisition offer in 2000, choosing to remain private and values-driven. They gave employees equity, sourced organic ingredients, and became a B Corporation. This was the antithesis of big food.

Yet by 2022, the founders were ready to exit, and Mondelez offered something unique: operational autonomy with global resources. As Sally Grimes stated, "Mondelēz International is the right partner at the right time to support Clif in our next chapter of growth."

The acquisition came at a crucial moment in Mondelez's portfolio evolution. Consumer behavior was bifurcating—on one side, indulgent treats for emotional comfort; on the other, functional snacks for performance and health. Mondelez dominated indulgence with Oreo and Cadbury. Clif Bar gave them credibility in wellness.

In its 2022 annual earnings report, Mondelez posted a 9.7% revenue increase for the year, to $31.5bn, primarily driven by incremental net revenues of $351m from its acquisitions of Clif Bar, along with Chipita and Ricolino.

The integration strategy was deliberately minimal. Clif Bar kept its Emeryville headquarters, its management team, and its culture. Mondelez provided distribution expansion—getting Clif into convenience stores, international markets, and new channels. Within months, Clif products appeared in 20,000 additional U.S. outlets.

But this acquisition also highlighted the challenges facing large food companies. At $2.9 billion for a business generating roughly $800 million in revenue, Mondelez paid a premium valuation of roughly 3.6x sales—expensive even for a high-growth brand. The deal included earnout provisions tied to future performance, suggesting even Mondelez wasn't certain about growth trajectories.

The broader portfolio strategy under Van de Put became clear: reshape toward higher growth, higher margin categories while maintaining scale advantages. So far in 2022, Mondelēz International has announced an agreement to acquire Ricolino, Mexico's leading confectionary company, from Grupo Bimbo and closed on its acquisition of Chipita S.A., a leader in the Central and Eastern European snack-size cakes and pastries category.

Each acquisition targeted specific capabilities or geographies. Chipita brought European bakery expertise and Central European distribution. Ricolino provided Mexican market leadership and Hispanic consumer insights applicable across the Americas. Perfect Snacks added refrigerated distribution capabilities. Hu Master Holdings, acquired for over $250 million, brought premium chocolate credibility.

The divestiture side was equally strategic. The gum business, while generating $1+ billion in revenue, faced structural headwinds—declining usage among younger consumers, competition from mints, and high marketing costs. Selling to Perfetti Van Melle, a focused confectionery player, made strategic sense even if it reduced scale.

By 2023, Mondelez's portfolio looked radically different from the Kraft Foods behemoth of 2010. Gone were grocery staples, beverages, and meals. In their place: a focused collection of global snacking brands generating 90%+ of revenue from chocolate, biscuits, and baked snacks.

The financial results validated the strategy. Organic revenue growth averaged 3-4% annually, well above food industry averages. Operating margins expanded to 15-17%, among the highest in packaged food. Return on invested capital exceeded 12%, suggesting efficient capital deployment despite premium acquisition prices.

Yet challenges emerged. Input cost inflation—cocoa, wheat, sugar—pressured margins. Private label gained share in developed markets as consumers traded down. Ozempic and other GLP-1 drugs threatened snacking occasions. ESG pressures around palm oil, cocoa sourcing, and packaging intensified.

The company's response revealed its operational sophistication. Revenue growth management—the art of strategic pricing—became a core capability. Mondelez raised prices 15%+ cumulatively from 2021-2023 while maintaining volumes, a feat few consumer companies achieved. They reformulated products to reduce sugar and portion sizes while maintaining taste. They invested in sustainable sourcing programs that, while costly, protected long-term supply access.

As of 2024, Mondelez stands as a $90+ billion market cap company, generating $36 billion in annual revenue across 150 countries. The transformation from diversified food conglomerate to focused snacking pure-play is complete. Whether this focused strategy can navigate the health-conscious, digitally-native future remains the critical question.

IX. Business Model & Competitive Dynamics

The Mondelez conference room in Chicago, 2024. Chief Financial Officer Luca Zaramella projects a simple slide: two pyramids. The first shows Mondelez's brand portfolio—70% of revenue from brands holding #1 or #2 market positions. The second shows geographic exposure—40% emerging markets, 60% developed. "This is our moat," he says. "Scale where it matters, agility where it counts."

Understanding Mondelez's business model requires appreciating the economics of global snacking. Unlike beverages (dominated by Coca-Cola and PepsiCo) or meals (fragmented among thousands of players), snacking occupies a sweet spot—consolidated enough for scale advantages, diverse enough for innovation, resilient enough for economic downturns.

The revenue foundation rests on what Mondelez calls "power brands"—10 franchises each generating over $1 billion annually. Oreo leads at nearly $4 billion in global sales. Cadbury Dairy Milk follows at $3 billion. These aren't just products; they're cultural institutions with pricing power that defies economic logic. During the 2022-2023 inflation surge, Mondelez raised Oreo prices 20%+ cumulatively while losing minimal volume.

Distribution provides the second competitive advantage. Mondelez operates through multiple channels: modern trade (supermarkets), traditional trade (small stores), e-commerce, and convenience. In India, they reach 2 million retail outlets directly. In China, they're in 300,000 stores. This infrastructure, built over decades, would cost tens of billions to replicate.

Manufacturing scale offers the third edge. Mondelez operates 130+ factories globally, with regional hubs specializing in specific products. The Bahrain plant supplies Middle Eastern markets with locally-adapted products. The Mexico facilities serve as the base for Latin American expansion. This network enables global efficiency with local customization—a difficult balance competitors struggle to achieve.

The innovation model has evolved from Kraft's centralized approach to Mondelez's "hub and spoke" system. Global R&D centers in New Jersey, Reading (UK), and Singapore develop platform technologies. Regional teams adapt these for local tastes. The result: 15% of revenue from products launched in the past three years, yet 70% of these "new" products are variations of existing brands.

Marketing spend—roughly $1.5 billion annually—focuses overwhelmingly on power brands. Mondelez spends more promoting Oreo than most companies' entire marketing budgets. This concentration creates a virtuous cycle: high awareness drives trial, trial drives repeat purchase, repeat purchase justifies marketing spend.

The competitive landscape reveals why focus matters. Nestlé, with 2000+ brands across dozens of categories, struggles with complexity. PepsiCo splits attention between beverages and snacks. Mars remains private, limiting acquisition currency and transparency. Only Ferrero matches Mondelez's snacking focus, but with less geographic diversity.

Private label represents the most insidious threat. In European biscuits, private label commands 30%+ share in some markets. Mondelez's response: premiumization (Oreo Thins), innovation (Oreo frozen desserts), and cost reduction to maintain price gaps. The strategy works—private label gains have slowed—but requires constant vigilance.

Emerging market dynamics differ entirely. In India, local players like Britannia and Parle compete on price and distribution. Mondelez counters with aspirational positioning—Cadbury Silk as a premium gift, Oreo as Western sophistication. The approach trades volume for value, accepting smaller market share at higher margins.

Digital disruption creates both opportunity and threat. E-commerce enables direct-to-consumer models, personalized products, and data-driven innovation. But it also empowers insurgent brands to bypass traditional distribution. Mondelez has responded by acquiring digital-native brands (Hu), creating online-exclusive products, and building data analytics capabilities.

The capital allocation framework reveals strategic discipline. Mondelez targets 90%+ free cash flow conversion, generating $3+ billion annually. Priorities are clear: dividends (yielding 2-3%), share buybacks ($2+ billion annually), bolt-on acquisitions (3-5% of revenue), and minimal debt (2x EBITDA target).

Environmental, Social, and Governance (ESG) pressures increasingly shape strategy. Cocoa sourcing faces scrutiny over child labor and deforestation. Palm oil usage draws environmental criticism. Plastic packaging creates waste concerns. Sugar content attracts health advocates. Mondelez invests hundreds of millions annually in sustainable sourcing, reformulation, and packaging innovation—necessary costs of operating at scale.

The margin structure tells the efficiency story. Gross margins of 38-40% lag some competitors but reflect emerging market exposure and premium ingredients. Operating margins of 15-17% match best-in-class peers through SG&A leverage. The key: revenue growth management that expands margins despite input cost pressure.

Currency exposure adds complexity. With 75%+ of revenue outside the U.S. but reporting in dollars, foreign exchange creates volatility. A strong dollar hurts reported results even when local currency performance excels. Mondelez hedges transaction exposure but accepts translation risk—a conscious choice prioritizing operational focus over financial engineering.

The ultimate competitive advantage may be intangible: management quality. The company has successfully navigated CEO transitions (Rosenfeld to Van de Put), activist investors (Peltz, Ackman), and portfolio transformation. The executive team averages 20+ years of industry experience. The board includes former CEOs and industry experts. This human capital, while hard to quantify, drives strategic decisions that compound over time.

X. Playbook: Lessons from the Mondelez Journey

Let's step back and examine the strategic patterns that emerge from Mondelez's two-decade transformation. These aren't just historical curiosities—they're blueprints for value creation in consumer goods, tested through multiple economic cycles and market disruptions.

Lesson 1: Portfolio Focus Beats Diversification

The conventional wisdom in the 1990s held that diversification reduced risk. Kraft Foods embodied this philosophy—cheese, coffee, cookies, hot dogs, beverages—something for every meal occasion. The theory: when one category declined, others would compensate.

Mondelez proved the opposite. By focusing exclusively on snacking, they achieved operational excellence impossible in a diversified portfolio. Marketing teams became snacking experts. Supply chains optimized for similar products. Innovation accelerated without competing priorities. The result: higher growth, better margins, superior returns.

The key insight: in mature consumer markets, depth beats breadth. It's better to dominate a few categories than participate in many. Focus enables the accumulation of competitive advantages that diversification dilutes.

Lesson 2: The M&A Integration Paradox

Traditional M&A playbooks emphasize integration—combine operations, eliminate redundancies, capture synergies. Mondelez's recent acquisitions suggest a different approach: strategic separation.

Tate's Bake Shop, Clif Bar, and Hu operate largely independently. They keep their founders, facilities, and cultures. Mondelez provides distribution, capital, and expertise but doesn't homogenize operations. This "federation" model preserves entrepreneurial energy while leveraging corporate scale.

The lesson: in consumer brands, authenticity has value that integration destroys. Sometimes the best synergy is no synergy—letting acquired brands maintain their uniqueness while providing selective support.

Lesson 3: Geographic Arbitrage Through Local Innovation

Most multinationals pursue geographic expansion through standardization—sell the same products everywhere. Mondelez does the opposite: they take global brands and localize them radically.

Oreo in China tastes different than Oreo in America. Cadbury in India has different formats than Cadbury in the UK. This localization seems inefficient—more SKUs, more complexity, higher costs. But it drives market share and pricing power that standardization never could.

The insight: in food, culture beats efficiency. Consumers will pay premiums for products that respect local tastes. The operational complexity is an investment that competitors struggle to match.

Lesson 4: Revenue Growth Management as a Core Capability

During 2021-2023, Mondelez raised prices over 20% cumulatively while maintaining market share. This wasn't luck—it was sophisticated revenue growth management combining:

- Pack size optimization (smaller sizes at higher per-unit prices)

- Mix management (pushing premium variants)

- Promotional discipline (fewer deep discounts)

- Channel strategy (emphasizing higher-margin outlets)

- Competitive intelligence (matching but not leading price increases)

The playbook: treat pricing as a capability, not a decision. Build systems, analytics, and expertise that enable surgical price realization without volume destruction.

Lesson 5: The Activist Investor Dance

Mondelez has attracted multiple activist investors—Nelson Peltz (Trian), Bill Ackman (Pershing Square), and others. Rather than resist, management selectively embraced activist ideas while maintaining strategic control.

When Peltz pushed for margin improvement, Mondelez delivered through efficiency rather than his suggested cuts. When Ackman advocated for leverage, Mondelez modestly increased debt while maintaining flexibility. This "constructive engagement" captured value while avoiding disruption.

The lesson: activists often identify real issues but propose suboptimal solutions. Smart management teams address the underlying problems their own way.

Lesson 6: Capital Allocation in Slow-Growth Industries

With organic growth limited to 3-4% annually, capital allocation becomes crucial. Mondelez's framework:

- Organic investment threshold: Only invest in projects with 15%+ IRR

- Acquisition discipline: Pay premiums only for strategic assets that can't be built

- Dividend consistency: Steady, growing payouts that attract income investors

- Opportunistic buybacks: Accelerate when valuations compress

- Debt optimization: Maintain investment-grade ratings while utilizing cheap capital

This framework generates 10%+ annual shareholder returns despite modest growth—proof that capital allocation can create value even in mature industries.

Lesson 7: Managing Complexity Through Simplification

Despite operating in 150+ countries with dozens of brands, Mondelez maintains operational simplicity through radical standardization in non-customer-facing areas:

- Common ERP systems globally

- Standardized manufacturing processes

- Unified procurement strategies

- Centralized treasury and tax functions

- Shared business services for transactional activities

This "complexity where it matters, simplicity where it doesn't" approach enables global scale with local responsiveness.

Lesson 8: The Innovation Portfolio Balance

Mondelez manages innovation across three horizons:

- Core renovation (70% of effort): Improving existing products—new Oreo flavors, better Cadbury recipes

- Adjacent expansion (20%): Extending into related categories—Oreo ice cream, Cadbury biscuits

- Transformational bets (10%): Entirely new platforms—protein snacks, functional foods

This 70-20-10 allocation ensures steady improvement while exploring future growth. Most companies either over-invest in moonshots or under-invest in innovation entirely.

Lesson 9: Stakeholder Management in Controversial Industries

Snacking faces criticism—obesity, diabetes, environmental impact. Mondelez's response framework:

- Acknowledge legitimate concerns: Don't deny health or environmental issues

- Invest in solutions: Reformulation, sustainable sourcing, portion control

- Communicate progress: Regular ESG reporting with measurable targets

- Maintain perspective: Snacking in moderation is compatible with healthy lifestyles

This balanced approach maintains social license while protecting business model—neither capitulating to critics nor ignoring legitimate issues.

Lesson 10: Building Institutional Capabilities

The most important lesson may be the least tangible: Mondelez has built institutional capabilities that transcend individual leaders. The company successfully navigated CEO transitions, strategy shifts, and market disruptions because knowledge and processes are embedded in the organization, not dependent on heroes.

This institutional strength—reflected in consistent execution, strategic discipline, and operational excellence—may be Mondelez's greatest competitive advantage and hardest to replicate.

XI. Analysis & Investment Case

The Bull Case: A Defensive Growth Compounder

The optimistic view on Mondelez rests on five pillars that collectively suggest the company can deliver high-single-digit total returns with below-market volatility—an attractive proposition in uncertain times.

First, emerging market demographics remain compelling. While developed markets obsess over Ozempic and sugar reduction, 2 billion consumers in Asia, Africa, and Latin America are entering the middle class. Their per-capita chocolate consumption is 1/10th of developed markets. As incomes rise, snacking follows—a pattern repeated across every developing economy. Mondelez's 40% emerging market exposure provides decades of growth runway.

Second, pricing power persists despite inflation concerns. The 2021-2023 period provided a real-world stress test: Mondelez raised prices 20%+ while maintaining volumes. This pricing resilience reflects brand strength, category dynamics (small-ticket impulse purchases), and competitive rationality. Even if inflation moderates, the ability to take 3-4% annual pricing provides a growth floor.

Third, the innovation pipeline addresses health concerns. Portion-controlled formats, reduced sugar recipes, protein-enhanced variants, and functional ingredients show Mondelez isn't ignoring health trends. The Clif Bar acquisition brings credibility. The company can simultaneously serve indulgence and wellness occasions—a portfolio advantage pure-play healthy brands lack.

Fourth, operational leverage remains untapped. Despite margin expansion, Mondelez hasn't maximized efficiency. Digital transformation, automation, and AI-driven demand planning could expand margins 200-300 basis points over five years. The company's scale makes even small improvements material—10 basis points equals $35 million in operating profit.

Fifth, capital allocation flexibility provides optionality. With $3+ billion in annual free cash flow and modest leverage, Mondelez can pursue transformative M&A, accelerate buybacks, or increase dividends as opportunities arise. This flexibility is valuable when markets are volatile—management can pivot capital allocation to maximize returns.

The Bear Case: Structural Headwinds Intensifying

The pessimistic view sees multiple threats converging to pressure Mondelez's business model, potentially leading to value trap dynamics where the stock appears cheap but fundamentals deteriorate.

First, GLP-1 drugs represent an existential threat. Ozempic, Wegovy, and similar medications reduce appetite and specifically curb cravings for sweet, high-calorie snacks—Mondelez's core portfolio. With 50+ million Americans potentially on these drugs by 2030, snacking occasions could decline 10-20%. No amount of innovation can offset this behavioral shift.

Second, private label momentum accelerates. European retailers like Aldi and Lidl are expanding globally with private label-centric models. Their cookies and chocolate match branded quality at 30-50% lower prices. As consumers face economic pressure, trading down accelerates. Mondelez's premium pricing becomes a liability, not an asset.

Third, input cost volatility destroys predictability. Cocoa prices have tripled since 2020. Climate change makes agricultural commodities increasingly volatile. While Mondelez can pass through costs short-term, sustained inflation causes demand destruction. The margin stability investors value disappears.

Fourth, regulatory pressure mounts globally. Sugar taxes, marketing restrictions, front-of-pack warning labels, and plastic packaging bans proliferate. Each regulation incrementally pressures volumes, raises costs, or requires reformulation. Death by a thousand regulatory cuts.

Fifth, cultural shifts disadvantage legacy brands. Younger consumers prefer authentic, sustainable, local brands over global corporations. Mondelez's scale—once an advantage—becomes a liability. Acquiring trendy brands helps temporarily but integration challenges and founder departures destroy what made them special.

The Valuation Debate

At 20x forward P/E, Mondelez trades at a premium to packaged food peers (16-18x) but a discount to pure-play snacking companies like Hershey (23x). Bulls argue this valuation is justified by superior growth, margins, and capital allocation. Bears see multiple compression ahead as growth slows.

The EV/EBITDA multiple of 14x similarly splits the difference between staples (10-12x) and growth food companies (16-20x). This "goldilocks" valuation leaves room for re-rating in either direction based on execution.

Discounted cash flow analysis suggests fair value ranges from $65-85 per share depending on terminal growth assumptions (2-4%) and WACC (6-8%). The wide range reflects genuine uncertainty about long-term industry dynamics.

Scenario Analysis

Best Case (20% probability): Emerging markets accelerate, health concerns prove overblown, M&A creates value. Stock reaches $100+ as multiples expand.

Base Case (60% probability): Steady 3-4% organic growth, gradual margin expansion, consistent capital returns. Stock compounds at 7-9% annually.

Worst Case (20% probability): GLP-1 drugs devastate demand, private label takes share, margins compress. Stock declines to $50 as multiples contract.

Comparisons to Peers

Versus Nestlé: Mondelez offers more focus but less diversification. Higher margins but smaller scale. Better recent execution but less geographic balance.

Versus PepsiCo: Mondelez is pure-play snacking versus PepsiCo's beverage/snack mix. Higher growth potential but less defensive characteristics.

Versus Hershey: Mondelez has global reach versus Hershey's U.S. concentration. More diverse portfolio but less pricing power in chocolate.

Versus Unilever: Mondelez demonstrates strategic clarity Unilever lacks. Better organic growth but higher valuation.

The Investment Decision

Mondelez represents a quintessential "quality at a reasonable price" opportunity. The company won't shoot the lights out—3-4% organic growth is the ceiling. But execution excellence, capital allocation discipline, and defensive characteristics provide downside protection.

For growth investors, Mondelez disappoints—better opportunities exist in technology or healthcare. For value investors, the valuation lacks a margin of safety. But for investors seeking steady compounding with managed risk, Mondelez fits perfectly.

The key insight: Mondelez is a bet on execution over excitement. In a world of disruption, sometimes boring is beautiful.

XII. The Future of Snacking & Final Thoughts

The year is 2030. A Mondelez executive stands before investors, presenting results that would seem impossible today. The company generates 40% of revenue from products that don't yet exist. Artificial intelligence designs new flavors based on social media sentiment analysis. Precision fermentation creates chocolate without cocoa beans. Personalized nutrition tailors snacks to individual microbiomes.

This isn't science fiction—it's the future Mondelez must navigate. The question isn't whether snacking survives but how it evolves. Three mega-trends will reshape the industry, and Mondelez's response will determine whether it remains a market leader or becomes a cautionary tale.

Health and Wellness: The Great Reformulation

The tension between indulgence and health isn't new, but resolution approaches. Consumers increasingly demand both—products that deliver pleasure without guilt. This isn't about eliminating sugar or reducing portions; it's about fundamental reinvention.

Consider protein-enriched chocolate that aids muscle recovery. Or cookies with prebiotics that improve gut health. Or snacks that enhance cognitive function through nootropic ingredients. These aren't niche products—they're the future mainstream.

Mondelez's approach reveals strategic thinking. Rather than abandon indulgence, they're expanding the definition of snacking. The Clif Bar acquisition brings functional nutrition expertise. Internal R&D explores alternative sweeteners, novel proteins, and bioactive compounds. The goal: make snacking part of the wellness solution, not the problem.

But execution challenges loom. Reformulation that maintains taste is technically difficult and expensive. Consumer education takes time. Regulatory frameworks for functional foods remain uncertain. Success requires patience and investment that quarterly earnings pressure discourages.

Climate Change and Sustainable Sourcing

By 2050, climate change will fundamentally alter agricultural production. Cocoa cultivation zones will shift. Wheat yields will fluctuate wildly. Water scarcity will pressure manufacturing. These aren't distant risks—they're current realities requiring immediate action.

Mondelez's response spans the value chain. They're investing in drought-resistant cocoa varieties, supporting farmers with climate adaptation training, and exploring alternative ingredients like cellular agriculture. The Cocoa Life program, reaching 200,000 farmers, isn't corporate charity—it's supply chain survival.

Packaging presents another challenge. Consumers demand plastic reduction, but alternatives often compromise product quality or shelf life. Mondelez experiments with compostable films, reusable containers, and concentrated formats. The winner hasn't emerged, but experimentation is essential.

The investment required is staggering—hundreds of millions annually with uncertain returns. But the alternative—supply disruption and reputational damage—is worse. Climate adaptation isn't optional; it's existential.

Digital Disruption and Direct Relationships

The traditional model—manufacture, ship to retailers, hope consumers buy—is dying. Digital commerce enables direct relationships, personalized experiences, and data-driven innovation. But it also disintermediates traditional advantages.

Mondelez's digital transformation extends beyond e-commerce. They're building platforms that connect directly with consumers—apps that gamify snacking, subscription services for favorite products, virtual experiences that build brand affinity. The goal: own the consumer relationship, not just the product.

But Silicon Valley isn't standing still. Amazon's private label snacks leverage purchase data advantages. Instagram food brands build communities before products. Netflix might enter snacking to enhance viewing experiences. Competition comes from unexpected angles.

The response requires capabilities Mondelez historically lacked—software development, data science, user experience design. Building these internally takes time; acquiring them is expensive and culturally challenging. The digital transformation is as much about mindset as technology.

Geographic Expansion: The Final Frontiers

While developed markets stagnate and China slows, Africa and South Asia represent the final frontier for growth. Nigeria's 200 million people consume minimal chocolate. Bangladesh's rising middle class discovers packaged snacks. These markets offer decades of expansion potential.

But entry isn't simple. Infrastructure limitations, regulatory complexity, and entrenched local competitors create barriers. Mondelez must build distribution from scratch, adapt products for local tastes, and compete against companies with home-field advantages.

The playbook from China and India provides lessons. Start with cities, build brand awareness, expand distribution gradually. Accept lower margins initially to establish presence. Partner with local companies for market knowledge. Patience and persistence matter more than speed.

M&A Possibilities: The Next Transformation

Speculation about Mondelez's future inevitably includes M&A scenarios—as acquirer or target. The company's clean portfolio, strong cash generation, and focused strategy make it attractive for various possibilities.

As an acquirer, Mondelez could pursue transformative deals. Buying Kellogg's snacks business would add scale in crackers and wholesome snacks. Acquiring Ferrero seems impossible given family ownership, but stranger things have happened. Rolling up premium chocolate brands could strengthen positioning.

As a target, Mondelez attracts interest from multiple angles. Private equity could leverage the stable cash flows. PepsiCo might reunite snacking and beverages. Nestlé could eliminate a competitor while gaining focus. Even Amazon or a technology company might view Mondelez as entry into physical products.

But the most likely scenario may be independence. Mondelez has achieved the scale, focus, and profitability that make standalone success viable. The activist investors have been satisfied. Management executes consistently. Sometimes the best deal is no deal.

Key Takeaways for Operators and Investors

For operators in consumer goods, Mondelez offers clear lessons:

- Focus beats diversification in mature markets

- Local adaptation drives global success

- Portfolio management requires courage to cut and discipline to hold

- Cultural authenticity in acquisitions preserves value

- Institutional capabilities matter more than individual brilliance

For investors, the takeaways differ:

- Steady execution compounds over time

- Premium valuations for focused companies persist

- Management quality manifests in capital allocation

- ESG issues are business issues—ignore at your peril

- Sometimes boring businesses make the best investments

The Ultimate Question

As we conclude this journey from Kraft's cheese wagon to Mondelez's global empire, one question remains: Is this a story of triumph or a prelude to disruption?

The optimist sees a company that successfully transformed from declining conglomerate to focused growth company. The pessimist sees structural challenges that no amount of execution can overcome. The realist sees both—a well-managed company navigating genuine threats with skill but no guarantees.

Perhaps that's the lesson. In business, as in snacking, success isn't about perfection—it's about adaptation. Mondelez has proven remarkably adaptable over decades. Whether that adaptability continues will determine if the next century is as successful as the last.

The empire of snacking stands strong today. Tomorrow remains unwritten. And that uncertainty—the gap between what is and what might be—is where investment opportunity lives.

XIII. Recent News### **

Latest Earnings and Financial Performance**

Mondelez International reported its fourth quarter and full year 2024 results on February 4, 2025. "Fiscal 2024 was another strong year of performance for our company. We delivered balanced top-line growth, strong earnings, and robust free cash flow generation, while returning significant capital back to shareholders," said Dirk Van de Put, Chair and Chief Executive Officer. "As we transition into 2025, we remain focused on executing against our long-term growth strategy and delivering on our chocolate business playbook to navigate unprecedented cocoa cost inflation. Our teams are well-equipped to stay agile and take the necessary actions to navigate this challenging operating environment. We believe we are solidly positioned for attractive long-term top- and bottom-line growth."

For fiscal year 2024, the company achieved several notable milestones: - Net revenues increased 1.2 percent as Organic Net Revenue growth of 4.3 percent and incremental net revenue from our acquisition of Evirth was partially offset by unfavorable currency-related items - Diluted EPS declined by 5.5% to $3.42, mainly due to previous gains not being repeated. The company managed to generate a free cash flow of $3.5 billion and returned $4.7 billion to shareholders. Adjusted EPS, however, saw a 13% increase on a constant currency basis, thanks to operational gains and lower taxes - With 2024 net revenues of approximately $36 billion, MDLZ is leading the future of snacking with iconic global and local brands

2025 Outlook and Challenges

Looking ahead to 2025, Mondelēz International anticipates organic net revenue growth of around 5%, despite expecting a 10% decline in adjusted EPS due to cocoa cost challenges. The company faces several headwinds:

- Mondelez International Inc (NASDAQ:MDLZ) faces unprecedented cocoa cost inflation, impacting profitability and requiring strategic adjustments. The company expects an adjusted EPS decline of approximately 10% in 2025 due to high cocoa costs

- North America's biscuit category is experiencing softness, with limited pricing possibilities and increased elasticities. The company anticipates potential headwinds from new executive orders imposing tariffs on US imports from Mexico and Canada

Strategic Acquisitions and Portfolio Optimization

On November 1, 2024, the company acquired Evirth (Shanghai) Industrial Co., Ltd. ("Evirth"), a leading manufacturer of cakes and pastries in China. The acquisition will continue to expand the company's growth in the cakes and pastries categories. The acquisition added incremental net revenues of $72 million (constant currency basis) during the three months and twelve months ended December 31, 2024 and operating income of $10 million during the three months and twelve months ended December 31, 2024

Operational Excellence and Productivity

Dirk Van De Put, CEO, stated that Mondelez aims for a 4% gross productivity improvement in its supply chain, marking one of the highest productivity programs in the company's history. This target reflects efforts to manage costs and improve efficiency amid challenging market conditions

Sustainability Progress

Mondelēz International, Inc. (Nasdaq: MDLZ) today released its 2024 Snacking Made Right Report, highlighting the Company's progress against its Sustainability goals. This year's report underscores Mondelēz International's ongoing dedication to making snacking more sustainable and reiterates its commitment to prioritizing Sustainability as the fourth pillar in its long-term Strategy – alongside Growth, Execution and Culture. Highlights of the company's 2024 progress include: Advancing responsible sourcing through Cocoa Life, the company's signature cocoa sustainability program, helping to empower farming communities and regenerate landscapes, now covering nearly 91% of cocoa volume

~96% of owned manufacturing sites and ~98% of prioritized suppliers have completed third-party SMETA audits in the past 3 years. HRDD coverage has been expanded to increase coverage of suppliers' manufacturing and logistic sites handling the company's finished products. Since launching its dedicated Human Rights Policy in 2021, the company has trained more than ~50,000 colleagues on human rights issues, including ~7,000 in manufacturing and logistics, and ~3,000 in key stewardship roles

Leadership and Market Position

The company continues under the leadership of CEO Dirk Van de Put and CFO Luca Zaramella, maintaining its position as one of the world's largest snacking companies. Despite near-term challenges from cocoa inflation and changing consumer behaviors, management remains confident in the company's long-term positioning and ability to navigate current headwinds through pricing actions, productivity improvements, and strategic portfolio management.

XIV. Links & Resources

Official Company Resources

- Investor Relations: ir.mondelezinternational.com

- Corporate Website: www.mondelezinternational.com

- SEC Filings: Available through EDGAR database

- Annual Reports: 2024 10-K and proxy statements

- Sustainability Reports: 2024 Snacking Made Right Report

Key Industry Reports

- Euromonitor International: Global Snacking Industry Analysis

- IRI/Circana: U.S. Snacking Category Performance Data

- Nielsen: Global Chocolate and Confectionery Market Reports

- McKinsey: Future of Food in America Series

Academic and Historical Resources

- Harvard Business School Cases on Kraft-Cadbury Acquisition

- Wharton School Analysis of Mondelez Split Strategy

- "The Cadbury Story" by John Bradley

- "Barbarians at the Gate" (for RJR Nabisco background)

Financial Analysis Platforms

- Bloomberg Terminal: MDLZ US Equity

- S&P Capital IQ Company Reports

- Morningstar Direct Coverage

- FactSet Company Analytics

Trade Publications

- Food Business News

- Confectionery News

- Just Food Global

- The Grocer (UK)

- Candy Industry Magazine

Regulatory and ESG Resources

- Cocoa Life Program Reports

- Fair Trade Certification Database

- CDP Climate Change Disclosures

- SASB Food & Beverage Standards

Executive Interviews and Presentations

- CAGNY Conference Presentations (Annual)

- Deutsche Bank Global Consumer Conference Materials

- Barclays Global Consumer Staples Conference

- CEO Dirk Van de Put Media Appearances

- Former CEO Irene Rosenfeld Interviews Archive

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube