Tata Consumer Products: From Tea Gardens to Global FMCG Giant

I. Cold Open & Episode Roadmap

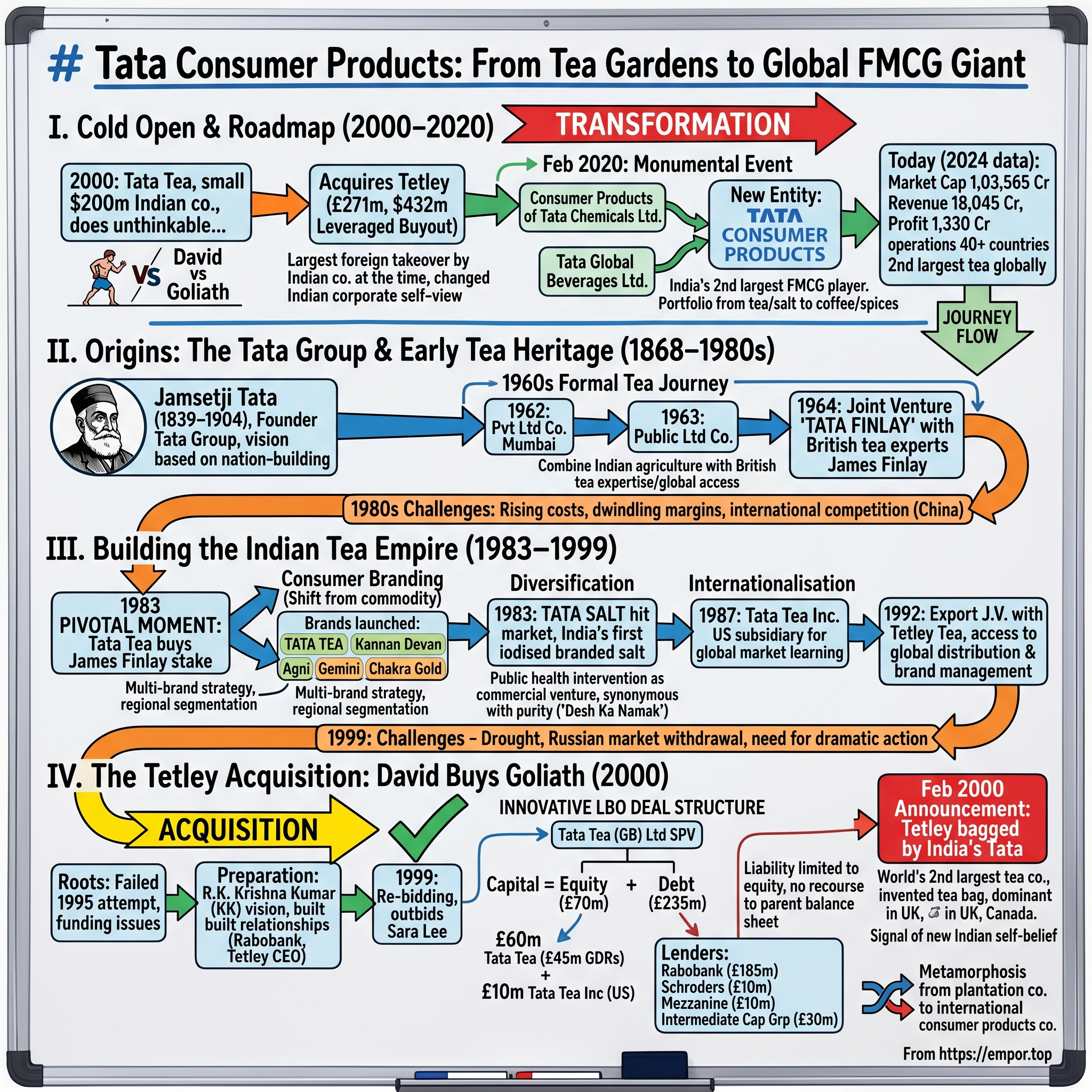

The year was 2000. In the boardrooms of Mumbai, a relatively small Indian tea company with an annual revenue of just $200 million was about to do the unthinkable. Tata Tea, a $200-million company, acquiring Tetley which was nearly four times its net worth - it was the corporate equivalent of David taking on Goliath, except this time, David won.

It was a £271 million ($432 million) leveraged buyout. Tata Tea reportedly outbid the American conglomerate Sara Lee in what was described, at the time, as the largest takeover of a foreign company by an Indian company. This audacious acquisition in February 2000 didn't just transform a tea plantation company into a global beverage powerhouse - it fundamentally changed how Indian corporations viewed themselves on the world stage.

Fast forward to 2020, and another transformative moment unfolds. In February 2020, a monumental event unfolded in the business world. The consumer products business of Tata Chemicals Ltd. joined hands with Tata Global Beverages Ltd., giving rise to a new entity: Tata Consumer Products. This merger represented the culmination of decades of strategic moves, creating India's second-largest FMCG player with a portfolio spanning from the humble tea leaf to premium coffee, from everyday salt to gourmet spices.

Today, Tata Consumer has a market cap of 1,03,565 Crore with revenue of 18,045 Cr and profit of 1,330 Cr. The company that once started as a colonial-era tea venture has evolved into the second largest tea company globally with operations spanning 40+ countries and a brand portfolio that touches hundreds of millions of consumers daily.

This is the story of bold acquisitions and patient capital, of leveraging heritage while embracing innovation, of a company that transformed from commodity trading to brand building. It's about the art of consumer products consolidation in emerging markets and the delicate balance between global ambitions and local roots. We'll explore how a tea company became an FMCG giant, why the Tetley acquisition changed Indian corporate history forever, and what the future holds for this ambitious consumer products powerhouse.

Our journey will take us from the colonial tea gardens of Assam to the boardrooms of London, from the launch of India's first iodized salt to billion-dollar acquisitions in 2024. We'll examine the playbook of international expansion, the challenges of brand portfolio management, and the strategic logic behind creating a unified consumer products entity. This is the Tata Consumer Products story - a masterclass in transformation, timing, and the relentless pursuit of scale in the consumer products industry.

II. Origins: The Tata Group & Early Tea Heritage

To understand Tata Consumer Products, we must first understand the extraordinary vision of one man who changed the trajectory of Indian business forever. Jamsetji Nusserwanji Tata (3 March 1839 – 19 May 1904) was an Indian industrialist and philanthropist who founded the Tata Group, India's largest conglomerate. Born into a family of Zoroastrian priests in Navsari, Gujarat, Jamsetji broke with tradition to become the first businessman in his lineage.

He founded a trading company in 1868 with ₹21,000 capital (worth US$52 million in 2015 prices). This modest beginning would spawn what is today one of the world's most respected business conglomerates. He had four goals in life: setting up an iron and steel company, a world-class learning institution, a unique hotel and a hydroelectric plant. While Jamsetji would only see the Taj Mahal Hotel completed in his lifetime, his vision laid the foundation for institutions that would define modern India.

The Tata Group's philosophy of business was revolutionary for its time. As JRD Tata noted, Jamsetji's entrepreneurial career began "when the passive despair engendered by colonial rule was at its peak". Yet, he believed that business success should enrich the nation, not just the businessman. This ethos of nation-building through enterprise would become the DNA of every Tata venture, including what would eventually become Tata Consumer Products.

The formal journey into tea began much later, in the 1960s. In 1962, it officially kicked off its journey as a private limited company, with its home base in Mumbai, India. In 1963, Tata Consumer Products was converted into a public limited company. But the real foundation was laid in 1964 when Tata teamed up with a big name in Indian tea, James Finlay, forming Tata Finlay. This joint venture with the UK-based James Finlay and Company was strategic - it brought together Indian agricultural prowess with British tea expertise and global market access.

The post-independence context is crucial here. India had inherited vast tea plantations from the colonial era, but most of the value addition and branding happened overseas. Indian tea was exported as a commodity, with British companies capturing most of the premium. The Indian government was keen to change this dynamic, and the Tatas saw an opportunity to create value within India.

For nearly two decades, the joint venture operated successfully, learning the intricacies of tea cultivation, processing, and global trade. But by the early 1980s, the Indian tea industry was facing significant challenges. In the early 1980s, the tea industry in India was experiencing rising input and labour costs and dwindling margins as well as high taxes. India was facing competition in the world market not just from China, but also from other countries entering the business.

The pivotal moment came in 1983. In 1983, Tata Tea bought the stake belonging to the James Finlay group to form the individual entity Tata Tea. This wasn't just a corporate transaction - it was a declaration of independence. In the same year, the company decided to move from the commodities business to consumer branding. The first brand Tata Tea was introduced.

This shift from commodities to consumer branding was revolutionary for its time. Consider the context: in 1983, India was still largely a socialist economy with limited consumer choice. Most Indians bought loose tea from local shops, often adulterated and of inconsistent quality. The concept of packaged, branded tea was alien to most consumers. In spite of being the largest market in the world, the concept of branded tea took time to be accepted.

The early brand portfolio was carefully crafted to appeal to different segments of the Indian market. This was followed by other brands like Kannan Devan, Agni, Gemini and Chakra Gold. Each brand had its own positioning - Kannan Devan leveraged the premium image of its high-altitude estates, Agni targeted the mass market with strong tea, while Chakra Gold went after the premium segment.

But tea wasn't the only frontier. In a move that would prove prescient, In 1983, Tata Salt hit the market, becoming India's first iodised, vacuum-evaporated, branded salt. This was more than just product diversification - it was a public health intervention wrapped in a commercial venture. Iodine deficiency was a major health issue in India, causing developmental problems in children. By creating India's first iodized branded salt, Tata wasn't just building a business; it was addressing a national health challenge.

The introduction of Tata Salt demonstrated the company's ability to identify everyday commodities that could be transformed into trusted brands. Salt, like tea, was sold loose in markets, often contaminated and of variable quality. By applying modern processing techniques and rigorous quality control, Tata Salt quickly became synonymous with purity and health. The tagline "Desh Ka Namak" (The Nation's Salt) resonated deeply with Indian consumers' patriotic sentiments.

As the 1980s progressed, the company began to think beyond Indian borders. In 1987, Tata Tea set up a fully owned subsidiary, Tata Tea Inc., in the United States. This wasn't just about exports - it was about understanding global markets, consumer preferences, and building capabilities for what would become a decades-long internationalization journey.

The late 1980s and early 1990s were transformative years for India. Economic liberalization was on the horizon, global brands were eyeing the Indian market, and Indian companies were beginning to dream of global expansion. It was in this context that one man would emerge as the architect of Tata Tea's global ambitions - R.K. Krishna Kumar, known simply as KK.

KK joined Tata Tea in the 1980s and quickly rose through the ranks with his vision of transforming a plantation company into a global beverages business. In the 1990s, he was Managing Director of Tata Tea, and he had been reflecting on the fall of the Berlin Wall. To KK, this signaled a new world structure, and a new vision for the Company he led.

The fall of the Berlin Wall wasn't just a geopolitical event - it symbolized the emergence of a truly global marketplace. Trade barriers were falling, capital was becoming mobile, and brands were going global. KK realized that for Tata Tea to thrive in this new world, it couldn't remain confined to India. It needed to acquire global brands, access international markets, and build world-class capabilities.

The first concrete step toward this vision came in 1992. It formed an export joint venture with Britain's Tetley Tea in 1992. This wasn't just any partnership - Tetley was one of the world's most recognized tea brands, with dominant positions in the UK and Canadian markets. Through this joint venture, Tata Tea gained invaluable insights into international brand management, global supply chains, and consumer preferences in developed markets.

By the end of the 1990s, Tata Tea had transformed from a plantation company into a formidable player in the Indian branded tea market. By 1999, Tata Tea's brands had a combined market share of 25% in India. The company had 74 tea gardens and was producing 6.2 crore kilograms of tea a year, two-thirds of it packaged and branded.

However, challenges were mounting. Towards the end of the year, the tea business was hit by a drought in much of India. In addition, Russia, once the largest buyer of Indian tea, temporarily withdrew from the market. These external shocks highlighted the vulnerability of being dependent on a single market and commodity. It was clear that dramatic action was needed.

The stage was set for what would become one of the most audacious corporate moves in Indian business history. The partnership with Tetley had given Tata Tea a taste of what was possible. The economic liberalization of India had created the regulatory environment for global acquisitions. And KK had assembled a team ready to take on the world. What came next would not just transform Tata Tea - it would change how Indian corporations saw themselves forever.

III. Building the Indian Tea Empire (1983–1999)

The year 1983 marked a watershed moment in Indian consumer goods history. When Tata Tea bought out James Finlay's stake and embarked on its journey from commodities to brands, it was venturing into uncharted territory. The Indian consumer market of the early 1980s was vastly different from today - purchasing power was limited, retail was fragmented, and brand consciousness was nascent. Yet, this challenging environment would forge the capabilities that would later enable global expansion.

The strategic shift to branding required a complete reimagining of the business model. Commodity trading was straightforward - buy tea from estates, process it, and sell it in bulk to wholesalers. Branding meant understanding consumers, investing in packaging, building distribution networks, and most importantly, creating trust. The launch of the Tata Tea brand in 1983 was accompanied by significant investments in quality control, standardized blending, and moisture-proof packaging - innovations that seem basic today but were revolutionary in the Indian market of the 1980s.

The brilliance of the early brand portfolio strategy lay in its segmentation approach. Kannan Devan, sourced from the high-altitude estates in Munnar, Kerala, commanded premium pricing by emphasizing its origin story and superior flavor. The estates, originally owned by the British, had been transformed into a cooperative owned by workers - a narrative that resonated with post-independence India's socialist ethos. Agni, on the other hand, was positioned as strong, full-bodied tea for the mass market, particularly appealing to consumers in North India who preferred their tea with lots of milk and sugar.

The Gemini brand targeted South India with its specific flavor profile, while Chakra Gold went after the emerging affluent class with its premium positioning. This multi-brand strategy wasn't just about market coverage - it was about learning. Each brand was an experiment in understanding regional preferences, price elasticity, and brand building in a diverse market like India.

Parallel to the tea revolution, the launch of Tata Salt in 1983 demonstrated the company's ability to identify and transform commodity markets. The Indian salt market was dominated by unbranded, often contaminated products sold loose. The government's push for iodization to combat deficiency disorders created an opportunity, but execution was the challenge. Tata Salt's vacuum evaporation technology ensured purity and consistent iodine content, while innovative packaging kept the product free-flowing even in India's humid climate.

The marketing of Tata Salt was masterful in its simplicity. Rather than complex health messages, the brand focused on purity and trust. The white packaging with the simple Tata logo became iconic, standing out in cluttered Indian kitchens. Within a few years, Tata Salt had created and dominated a category that didn't previously exist - branded, packaged salt. By the late 1980s, it had become India's largest selling branded salt, a position it maintains to this day.

Building distribution in 1980s India was perhaps the greatest challenge. India's retail landscape consisted of millions of small kirana stores, each serving a hyperlocal catchment. There were no modern retail chains, no computerized inventory systems, and limited refrigeration. Tata Tea had to build a distribution network from scratch, recruiting and training thousands of distributors and retailers.

The company pioneered several distribution innovations that would become industry standard. It introduced the concept of "freshness dating" on tea packets, assuring consumers of product quality. It invested in branded tea boutiques in major cities, creating an aspirational retail experience. Most importantly, it built direct relationships with retailers through regular sales visits, credit facilities, and merchandising support.

The international expansion that began with Tata Tea Inc. in the United States in 1987 was about more than just exports. The U.S. subsidiary became a learning laboratory for understanding developed market dynamics. American consumers had different tea consumption patterns - they preferred tea bags over loose tea, flavored variants, and increasingly, ready-to-drink formats. The subsidiary also handled instant tea manufacturing, leveraging facilities in Florida and sourcing from the parent company's facilities in Munnar.

The early 1990s brought new opportunities and challenges. India's economic liberalization in 1991 opened doors for foreign investment and competition. Global beverage giants like Unilever's Lipton began eyeing the Indian market seriously. At the same time, liberalization made it easier for Indian companies to access foreign capital and make international acquisitions.

The joint venture with Allied Lyons and Tetley in 1992 was strategically brilliant. Rather than competing with Tetley in export markets, Tata Tea partnered with them, gaining access to their global distribution network while providing them with sourcing advantages from Indian estates. The partnership also exposed Tata Tea's management to global best practices in brand management, marketing, and operational efficiency.

In the 1990s, Tata Tea decided to take its brands into the global markets. This wasn't just about following Indian diaspora markets - it was about competing with global brands on their home turf. The company began participating in international tea auctions, not just as a seller but increasingly as a buyer, sourcing teas from Sri Lanka, Kenya, and other origins to create blends that would appeal to international palates.

The diversification into coffee through the acquisition of Consolidated Coffee Ltd. (later Tata Coffee) demonstrated portfolio thinking. Coffee culture was nascent in India but growing, particularly in South India and urban centers. Moreover, coffee had higher margins than tea and offered exposure to international markets where coffee consumption far exceeded tea.

By the mid-1990s, Tata Tea had emerged as a case study in successful brand building in an emerging market. Management schools studied its transformation from commodity to brand, its multi-brand portfolio strategy, and its distribution innovations. The company was generating healthy cash flows, had built strong brands, and had established international partnerships. Yet, KK and his team knew this wasn't enough.

In the mid-1990s, Tata Tea attempted to buy Tetley. This first attempt in 1995 failed, primarily due to financing challenges. But Tata Tea struggled to put in place the financing required for the acquisition. The failure was a learning experience - it highlighted the limitations of Indian financial markets and the need for innovative financing structures for large international acquisitions.

The late 1990s were marked by consolidation and preparation. The company strengthened its balance sheet, built relationships with international banks, and most importantly, deepened its relationship with Tetley through the joint venture. By 1999, despite challenges from drought and the loss of Russian markets, Tata Tea was ready for its next leap.

The transformation from 1983 to 1999 was remarkable. A plantation company had become a consumer products company. A commodity trader had become a brand builder. A domestic player had developed global ambitions. The company had built the capabilities - in brand management, distribution, and operations - that would be crucial for what came next. The Indian tea empire was built, but the global conquest was about to begin.

IV. The Tetley Acquisition: David Buys Goliath (2000)

The story of how a $200 million Indian company acquired a British icon nearly four times its net worth is one of the most fascinating episodes in global M&A history. It wasn't just about the numbers or the strategic fit - it was about ambition, innovation in deal structuring, and perfect timing that would inspire a generation of Indian entrepreneurs to think globally.

The roots of this acquisition go back to 1995, when Tata Tea first attempted to acquire Tetley. Allied Domecq, Tetley's parent company, was divesting non-core assets, and Tetley was up for sale. A Tata Tea team reached London in early 1995 to pursue the acquisition. I was privileged to be a junior member of this team. We studied mountains of documents, over countless prawn sandwiches and cups of tea. There were also long discussions with the Allied Domecq management, and with bankers who could potentially fund the acquisition. Consensus was achieved on a number of fronts.

But the deal fell through. The financing requirements were simply too large for Indian banks to handle, and international banks were skeptical about an Indian company's ability to manage such a large acquisition. The failure was devastating for KK and his team, but it also provided invaluable lessons. They understood now what it would take - not just in terms of capital, but in terms of preparation, relationships, and structure.

Between 1995 and 1999, KK worked methodically to address each obstacle. In the meanwhile, KK had learnt his lessons from the failed bid of 1995, and was investing his time and effort in tying up the funding required. Eventually, in a long and decisive meeting with Rabobank, he convinced the vice-chairman of the bank at that time, Wouter J. Kolff, to provide the financial backing required. KK recalls that Kolff finally stood up, looked him in the eye for a few seconds, and said – "Done!".

The relationship building wasn't just with banks. On Christmas Eve 1999, Ken Pringle, the CEO of Tetley, unexpectedly dropped by to meet us, and gifted us quaint ceramic figures of the "Tetley Tea Folk" – warm, animated characters. These personal relationships would prove crucial when the bidding process began.

When Tetley came up for sale again in 1999, Tata Tea was ready. But they weren't the only bidder. Tata Tea reportedly outbid the American conglomerate Sara Lee. Sara Lee was a formidable competitor - a multi-billion dollar company with extensive experience in acquisitions. That Tata Tea could outbid them seemed impossible to most observers.

The key was the innovative deal structure. Noshir Soonawala, Finance Director at Tata Sons, helped develop the financial structuring of the transaction. Known to possess a razor-sharp intellect, he put together the required framework for a leveraged buyout, which enabled Tata Tea, a relatively small Company, to undertake this massive acquisition. Such a buyout was unheard of in India, at that time.

The leveraged buyout (LBO) structure was revolutionary for an Indian company. The deal cost Tata $ 450 million (271 million pounds) to acquire Tetley when its net worth stood at a puny $114 million. Here's how the structure worked:

Tata Tea created a special purpose vehicle (SPV) called Tata Tea (Great Britain) Limited. The capital of the SPV included 2 parts, the equity which was 70 million pounds, and the debt which stood at 235 million pounds. The equity was completely financed by Tata Tea out of which, Tata Tea Inc, Tata's company incorporated in the US supplied 10 million pounds, and 60 million pounds was supplied by Tata Tea.

The genius of the structure was in the details. Out of the 60 million, 45 million pounds were raised through GDRs (Global Depository Receipts), allowing Tata Tea to tap international capital markets. The debt was spread over four tranches with a repayment period which ranged from 7 to 9.5 years. The lenders of the debt were Schroders (10 million pounds), Rado Bank (185 million pounds), Mezzanine (10 million pounds), and Intermediate Capital Group (30 million pounds).

The deal was so structured, that although Tata tea retained full control over the venture, the debt portion of the deal did not affect its balance sheet. The liability of acquisition was limited to Tata Tea's equity contribution to the SPV. Also, the lenders had no recourse at all to Tata Tea in India.

The announcement in February 2000 sent shockwaves through the business world. In February 2000, exactly twenty years ago, BBC ran a lead article that made India proud. "Tetley bagged by India's Tata", said the headline. It went on to say – "Tetley Tea, inventor of the tea bag and maker of the traditional English cuppa, is being bought by Tata Tea of India. The deal to buy the world's second largest producer of teabags is worth 271 million UK pounds, and is the biggest acquisition in Indian corporate history".

The reaction in India was electric. Ratan Tata, Chairman, Tata group said, "It is a great signal for global industry by Indian Industry. It is a momentous occasion as an Indian company has been able to acquire a brand and an overseas company". This wasn't just corporate speak - it was a genuine watershed moment for Indian business confidence.

Tetley wasn't just any brand. It was the world's second-largest tea company, invented the tea bag, and held dominant positions in multiple markets. In the UK, it competed neck-and-neck with market leader PG Tips (owned by Unilever). In Canada, it was the undisputed market leader. The brand had history dating back to 1837, global recognition, and sophisticated marketing and distribution capabilities.

For Tata Tea, the acquisition brought immediate scale and global presence. The acquisition of Tetley pitch forked Tata Tea into a position where it could rub shoulders with global behemoths like Unilever and Lawrie. The acquisition of Tetley made Tata Tea the second biggest tea company in the world. (The first being Unilever, owner of Brooke Bond and Lipton). Moreover it also went through a metamorphosis from a plantation company to an international consumer products company.

The integration challenges were immense. Here was an Indian company, used to operating in a developing market with different consumer preferences, cost structures, and business practices, taking over a British company with operations in developed markets. Cultural differences were significant - from decision-making styles to compensation structures to marketing approaches.

This bid was evaluated by the owners, and, in February 2000, it was finally accepted. Tetley had entered the Tata fold! But the real work was just beginning. Integration teams were formed, with members from both companies. The approach was respectful and collaborative - Tata Tea didn't impose its way of doing things but rather learned from Tetley's expertise in developed markets while providing its own insights on cost optimization and emerging market strategies.

The financing structure proved its worth during integration. Because the debt was secured against Tetley's assets and cash flows, not Tata Tea's, the parent company could focus on integration and growth rather than debt servicing. Tetley's strong cash generation capabilities meant the debt was serviced comfortably, with the company even prepaying some tranches ahead of schedule.

The strategic benefits began to materialize quickly. Tata Tea gained access to Tetley's sophisticated blending and flavoring capabilities, its tea bag manufacturing technology, and its deep understanding of developed market consumers. Tetley benefited from Tata Tea's sourcing strengths, its low-cost manufacturing capabilities, and its understanding of emerging markets.

The Tetley acquisition was a path breaking venture in so many ways, and it signaled a new self-belief in India. But here is something I would like to call out. This acquisition took ten long years to fructify, from dream to finish - with many small steps which built trust and confidence, and a deep disappointment becoming an immediate opportunity to learn. Each of us can hope to achieve our own audacious dreams, if we persist, and learn, and persist.

The ripple effects of the Tetley acquisition went far beyond Tata Tea. It inspired a wave of international acquisitions by Indian companies - from Tata Steel's acquisition of Corus to Bharti Airtel's Africa ventures. It showed that Indian companies could compete globally, not just on cost but on strategy and execution. It demonstrated that innovative financing could overcome capital constraints.

The deal also changed perceptions internationally. Global investment banks began to take Indian companies seriously as potential acquirers. International brands became more open to Indian partnerships and acquisitions. The image of Indian business transformed from back-office service providers to global players.

Looking back, the Tetley acquisition was more than just a successful M&A transaction. It was a defining moment in Indian corporate history, a validation of the economic liberalization that had begun a decade earlier, and a preview of India's emergence as a global economic power. For Tata Tea, it was the transformation from an Indian tea company to a global beverages business, setting the stage for two more decades of growth and expansion.

V. International Expansion & Portfolio Building (2000–2019)

The successful integration of Tetley marked the beginning of an ambitious two-decade journey of international expansion and portfolio diversification. What followed wasn't just geographic expansion but a fundamental reimagining of what the company could become - from a tea-focused business to a comprehensive beverages and food company with global ambitions.

The immediate post-Tetley years (2000-2005) were focused on integration and learning. The company discovered that managing a global brand required different capabilities than managing Indian brands. Developed market consumers expected constant innovation - new flavors, formats, and packaging. Marketing in the UK required sophisticated understanding of media fragmentation and digital channels, which were just emerging in India. The company had to build new competencies while maintaining its core strengths.

The transformation wasn't limited to capabilities; it extended to corporate structure and governance. In 2010, recognizing its evolved identity, the company rebranded from Tata Tea to Tata Global Beverages. This wasn't merely cosmetic - it signaled a shift from being an India-centric tea company to a global beverages player. The new structure included regional headquarters, global category management, and integrated supply chain operations spanning continents.

The Eight O'Clock Coffee acquisition in the United States represented another learning curve. Coffee and tea, while both beverages, required different sourcing, processing, and marketing approaches. American coffee culture was sophisticated, with consumers increasingly interested in origin, roasting profiles, and brewing methods. Eight O'Clock, despite being a heritage brand dating back to 1859, needed revitalization to compete with premium players like Starbucks and artisanal roasters.

The company invested heavily in understanding coffee trends, upgrading roasting facilities, and launching premium variants. The 100% Colombian and organic lines were introduced to capture the growing specialty segment. Distribution was expanded beyond traditional grocery into club stores and e-commerce. While Eight O'Clock never achieved the dominance in coffee that Tetley had in tea, it provided valuable experience in managing diverse beverage categories.

The real game-changer came in 2012 with an announcement that surprised many: On 30 January 2012, Tata Consumer Products Limited and Starbucks announced the creation of a 50:50 joint venture called Tata Starbucks Limited, which will own and operate Starbucks outlets branded as Starbucks Coffee "A Tata Alliance" in India. This wasn't just another joint venture - it was a strategic masterstroke that would redefine the company's position in the Indian beverages market.

The Starbucks partnership was years in the making. In January 2011, TATA Coffee and Starbucks corporation announced their plans for opening Starbucks outlets in India. Earlier in 2007, Starbucks had planned to enter the Indian market with a partnership with Kishore Biyani's Future Group but the deal couldn't become successful. Where others had failed, Tata succeeded by offering something unique - not just capital and local knowledge, but a vertically integrated coffee supply chain through Tata Coffee.

On 19 October 2012, Starbucks opened its first store in India, measuring 4,500 sq ft in Elphinstone Building, Horniman Circle, Mumbai. The location was symbolic - in the heart of Mumbai's historic business district, where the Tata Group had its roots. The 50/50 joint venture, named TATA Starbucks Limited, will own and operate Starbucks cafés which will be branded as Starbucks Coffee "A Tata Alliance".

The Starbucks venture was about more than just retail presence. All the espressos sold in Starbucks's Indian outlets are provided by TATA coffee. According to the part of the deal, Starbucks and Tata Coffee Limited will work toward developing and improving the profile of Indian-grown Arabica coffees around the world by elevating the level of Indian coffee. This vertical integration from bean to cup gave the joint venture cost advantages and quality control that pure-play retailers couldn't match.

The localization strategy for Starbucks India demonstrated sophisticated market understanding. Apart from the usual products offered internationally, Starbucks in India has some Indian-style product offerings such as Tandoori Paneer Roll, Chocolate Rossomalai Mousse, Malai Chom Chom Tiramisu, Elaichi Mewa Croissant, Chicken Kathi Roll and Murg Tikka Panini to suit Indian customers. The menu balanced global favorites with local tastes, creating a unique positioning that appealed to aspirational Indian consumers.

By 2019, the thriving 50:50 JV between Tata Consumer Products Ltd and Starbucks Corporation has over 300 stores across 36 cities in India. The venture had achieved something remarkable - making Starbucks accessible to Indian consumers while maintaining its premium positioning, creating a new coffee culture in a traditionally tea-drinking nation.

Meanwhile, in 2015, the company launched Tata Sampann, marking its serious entry into the food business beyond salt. This wasn't just brand extension - it was a strategic bet on the premiumization of Indian food consumption. As Indian consumers became more health-conscious and quality-aware, they were willing to pay premiums for unpolished dals, organic spices, and authentic regional ingredients.

Tata Sampann leveraged the trust in the Tata name but created its own identity focused on nutrition and authenticity. The range expanded rapidly - from basic pulses to ready-to-cook mixes, from cold-pressed oils to superfood supplements. Each product was positioned not just as food but as a health choice, tapping into the growing wellness trend among urban Indians.

The Good Earth acquisition added another dimension - premium and specialty teas. While Tetley served the mainstream market, Good Earth targeted the growing segment interested in herbal teas, organic variants, and wellness blends. This portfolio approach allowed the company to capture value across price points and consumer segments without cannibalizing its core brands.

International expansion continued through both organic growth and acquisitions. The company entered Russia, leveraging Tetley's historical presence. Middle Eastern markets were developed through partnerships with local distributors. In Australia and South Africa, the focus was on the Indian diaspora initially, then expanding to mainstream consumers. Each market required adaptation - from product formulations to packaging sizes to marketing messages.

The decade also saw strategic exits and refocusing. Non-core businesses were divested, and resources were concentrated on categories where the company had competitive advantages. The plantation business, once the core of the company, was gradually de-emphasized in favor of branded consumer products. Manufacturing was consolidated and modernized, with investments in automation and quality systems.

Distribution transformation was another crucial element. In India, the company expanded from 2 million outlets in 2010 to over 3 million by 2019. Modern trade and e-commerce, virtually non-existent in 2000, became significant channels. The company built specialized capabilities for each channel - category management for modern trade, digital marketing for e-commerce, and rural distribution for reaching India's vast hinterland.

Innovation became institutionalized with dedicated R&D centers and innovation teams. The focus wasn't just on new products but on formats and packaging. Ready-to-drink teas and coffees were launched to capture on-the-go consumption. Single-serve sachets made premium products accessible to lower-income consumers. Sustainable packaging initiatives addressed environmental concerns while differentiating the brands.

The period also saw significant investment in brand building. Tata Tea's "Jaago Re" campaign became one of India's most recognized cause-marketing initiatives, linking tea consumption with social awakening. Tetley was repositioned in international markets with updated packaging and contemporary messaging. Digital marketing capabilities were built from scratch, recognizing the shift in media consumption patterns.

By 2019, the company had transformed beyond recognition from its 2000 avatar. Revenue had grown from under $200 million to over $1.8 billion. The portfolio spanned tea, coffee, water, and foods. Operations covered 40 countries. The company had successfully built a multi-category, multi-geography consumer products business. Yet, the leadership recognized that to compete with FMCG giants like Hindustan Unilever and Nestle, another transformation was needed. The stage was set for the creation of Tata Consumer Products.

VI. The Merger & Modern Transformation (2020–Present)

The transformation of Tata Global Beverages into Tata Consumer Products in 2020 represents one of the most ambitious corporate restructurings in Indian FMCG history. This wasn't just a merger or a rebranding - it was the creation of an entirely new entity designed to compete with global FMCG giants on equal terms.

The genesis of this transformation lay in a strategic review initiated by N. Chandrasekaran, Chairman of Tata Sons, who took charge in 2017. Chandrasekaran's vision was to simplify the Tata Group's structure, unlock synergies, and create focused businesses with scale. In the consumer products space, the group had relevant businesses scattered across different companies - beverages in Tata Global Beverages, salt and pulses in Tata Chemicals' consumer division, and various food ventures in other entities.

On 15 May 2019, Tata Chemicals Limited (TCL) announced the de-merger of the Consumer Products Business of TCL and into TGBL through a National Company Law Tribunal ("NCLT") approved scheme of arrangement ("Scheme") to become Tata Consumer. The announcement marked the beginning of a complex corporate restructuring that would take months to execute.

The strategic logic was compelling. The Indian FMCG market was consolidating, with large players gaining share through distribution muscle and brand investments. Standalone businesses in tea or salt, no matter how successful, couldn't achieve the scale needed for efficient distribution, marketing leverage, and innovation investments. By combining businesses, the new entity could offer retailers and distributors a comprehensive portfolio, justify investments in technology and capabilities, and compete more effectively for talent.

TGBL has been renamed Tata Consumer Products Limited. Tata Consumer Products combines the food and beverages brands, which include Tata Salt, Tata Tea, Tata Sampann, Tetley, Soulfull and Himalayan mineral water, under a single umbrella. The unified portfolio immediately made Tata Consumer Products the second-largest FMCG company in India by market capitalization, behind only Hindustan Unilever.

The integration process was meticulously planned. Teams were formed to handle different aspects - sales force integration, supply chain optimization, brand architecture, and technology systems. The goal wasn't just to combine operations but to create something greater than the sum of its parts. Distribution networks were merged, creating one of India's widest FMCG reaches. Procurement was centralized, leveraging scale for better negotiations. Innovation pipelines were consolidated, avoiding duplication and accelerating time-to-market.

The timing of the merger, completed in February 2020, proved both challenging and opportune. Within weeks, India went into COVID-19 lockdown, disrupting operations and supply chains. Yet, the crisis also accelerated certain strategic initiatives. E-commerce adoption exploded, and the company's early investments in digital capabilities paid off. The consolidated entity could respond more nimbly to supply chain disruptions, shifting production and inventory across categories as needed.

The pandemic also accelerated premiumization trends that the company had been betting on. Consumers, concerned about health and safety, were willing to pay more for trusted brands with assured quality. Tata Sampann's positioning around nutrition and purity resonated strongly. Immunity-boosting products were fast-tracked. The company's quick response to changing consumer needs wouldn't have been possible without the integrated structure.

The post-merger phase saw aggressive expansion through acquisitions. In 2021, Tata Consumer Products has acquired Tata SmartFoodz for ₹395 crore. Tata SmartFoodz brought ready-to-eat capabilities and brands like Tata Q, positioning the company in the convenience foods segment.

The acquisition strategy accelerated dramatically in 2024. January 2024 – Capital Foods (75%) by Tata Consumer Products for ₹5,100 crore. Capital Foods, owner of the Ching's Secret and Smith & Jones brands, was a transformative acquisition. Ching's Secret had created and dominated the Indo-Chinese food category in India, with products like noodles, soups, and sauces. The brand had achieved what few Indian food brands had - creating a new category and maintaining leadership despite competition from giants like Nestle and ITC.

The Capital Foods acquisition brought several strategic benefits. It added a high-growth, high-margin category to the portfolio. It provided expertise in foods that complemented the company's beverages strength. Most importantly, it brought a proven innovation and marketing team that had built iconic brands from scratch. Following the recent acquisition of Capital Foods (owner of brands Ching's Secret and Smith & Jones), both front end and back-end integration has been completed on an accelerated timeline, within 60 days of the acquisition. We are leveraging Tata Consumer's GTM to deliver growth across channels while delivering on cost synergies.

The Organic India acquisition for ₹1,900 crore in 2024 represented another strategic direction - premiumization and health. Organic India had built a strong brand in organic teas, supplements, and food products, commanding significant premiums. The acquisition provided entry into the fast-growing organic and nutraceutical segments, capabilities in direct-to-consumer marketing, and international presence in developed markets where organic products had mainstream acceptance.

The transformation wasn't just about acquisitions. Organic growth initiatives were equally important. The company launched new categories and brands, leveraging its distribution muscle and brand equity. Ready-to-drink beverages were expanded beyond basic offerings to include functional drinks, cold coffee, and premium water. The foods portfolio was broadened to include breakfast cereals, snacks, and ready-to-cook products.

Distribution expansion continued aggressively. Sales & Distribution infrastructure was further strengthened, expanding total reach to 4 million outlets as of March '24. The reach was further deepened through the addition of 1300+ distributors in FY24, primarily in Rurban markets. This wasn't just about adding outlets but about creating the right channel mix for different product categories and price points.

Digital transformation became a strategic priority. The company invested in direct-to-consumer platforms, recognizing that digital natives expected to buy directly from brands. Data analytics capabilities were built to understand consumer behavior, optimize trade spending, and personalize marketing. Supply chain digitization improved forecast accuracy and reduced waste. As part of digital transformation agenda, we introduced a new Go-to-market platform. This is a next-gen Distributor Management platform and Sales workforce mobile app. It empowers our distributors and salesforce with real time data, enabling them to make informed decisions, manage tasks effectively and, ultimately, drive business growth. We also launched a best-in-class AI enabled end-to-end commodity procurement platform to optimise the purchase process.

The Starbucks joint venture continued to be a growth driver and learning platform. Through a 50:50 joint-venture between Starbucks Coffee Company and Tata Consumer Products Limited that launched in 2012, Tata Starbucks now operates in over 390 stores across 54 Indian cities, with approximately 4,300 partners (employees) who proudly wear the green apron. The venture provided insights into premium retail, experience marketing, and service excellence that influenced the company's broader strategy.

Innovation became more systematic and consumer-centric. Momentum on innovation continued with innovation-to-sales ratio at 5% + in the India business. We launched one new product nearly every 7 days during the year. This wasn't innovation for its own sake but targeted at specific consumer needs and occasions. Products were designed for portion control, convenience, health benefits, and regional tastes.

International operations were restructured for efficiency and growth. For the quarter, the International business revenue grew 7% (+5% constant currency). The focus shifted from just maintaining presence to driving profitable growth. Unprofitable markets were exited, while investments increased in high-potential geographies. The approach became more nuanced - in developed markets, the focus was on premium and specialty segments, while in emerging markets, the strategy emphasized building scale in mainstream categories.

The organizational transformation was equally important. The company attracted talent from leading FMCG companies, bringing in fresh perspectives and best practices. Performance management systems were overhauled to drive accountability and growth. A culture of innovation and agility was fostered, crucial for competing in fast-changing consumer markets.

By 2024, the transformation was showing results. The company had successfully integrated multiple acquisitions, expanded its portfolio across categories, and built competitive capabilities. In financial year 2024, Tata Consumer Products Limited witnessed its highest revenue, which stood at around 155 billion Indian rupees. More importantly, it had created a platform for sustained growth - with the scale, capabilities, and ambition to compete with any FMCG player globally.

Looking ahead, the company announced ambitious targets for reaching ₹25,000+ crore revenue, driven by continued portfolio expansion, distribution growth, and premiumization. The focus areas were clear - strengthen core categories, accelerate in high-growth segments like ready-to-eat and beverages, expand digital and modern trade presence, and continue strategic acquisitions. The transformation from Tata Tea to Tata Consumer Products was complete, but the journey toward becoming a global FMCG leader had just begun.

VII. The Brand Portfolio & Market Position

Understanding Tata Consumer Products' current market position requires examining not just the breadth of its portfolio but the strategic role each brand plays in the company's ecosystem. With operations spanning 40+ countries and products ranging from everyday essentials to premium offerings, the company has built a portfolio architecture that few Indian FMCG companies can match.

At the heart of the portfolio remains tea, where the company's global leadership is undisputed. The company is world No. 2 branded tea company. This position is built on two pillars - Tata Tea's dominance in India and Tetley's strength in international markets. Tata Tea is the biggest-selling tea brand in India, with sub-brands addressing every price point and regional preference. The master brand strategy allows the company to leverage the Tata Tea equity while targeting specific segments - Premium for urban affluent consumers, Gold for the middle segment, and Agni for price-conscious buyers.

Tetley is the biggest-selling tea brand in Canada and the second-biggest-selling in the United Kingdom and the United States. In Canada, Tetley enjoys over 30% market share, a dominance built over decades. In the UK, despite intense competition from Unilever's PG Tips, Tetley maintains strong number two position through constant innovation in flavors, formats, and packaging. The brand's strength in these developed markets provides both revenue stability and innovation insights that benefit the entire portfolio.

The salt business, anchored by Tata Salt, represents a different strategic value. As India's largest salt brand with over 30% market share, Tata Salt is more than just a product - it's a daily touchpoint with Indian households. The brand's tagline "Desh Ka Namak" (The Nation's Salt) has transcended marketing to become part of Indian cultural lexicon. The trust and distribution reach that Tata Salt provides creates a platform for launching new products and categories.

The evolution of the salt portfolio demonstrates sophisticated portfolio management. Recognizing that commoditization threatens margins, the company has premiumized through variants like Tata Salt Lite (low sodium), Tata Salt Plus (fortified with iron and iodine), and rock salt for health-conscious consumers. Salt revenue grew 9%, driven by strong volume growth. Additionally, in line with our premiumization agenda, the value-added salt portfolio continued its strong momentum and grew 35% during the quarter.

The foods business under Tata Sampann represents the company's future growth engine. Launched in 2015, Sampann has expanded from basic pulses to become a comprehensive food brand. The portfolio now includes unpolished dals, organic spices, ready-to-cook mixes, breakfast cereals, and dry fruits. The brand's positioning around nutrition and authenticity resonates with urban consumers willing to pay premiums for quality and health benefits.

Tata Sampann portfolio continued its strong momentum and grew 37% for the quarter. Our growth businesses (Tata Sampann, RTD, Tata Soulfull, Tata SmartFoodz) continued their strong growth trajectory. This growth isn't just about market expansion but about category creation. Many Sampann products, like unpolished dals and cold-pressed oils, have educated consumers about health benefits, creating new subcategories within traditional food segments.

The recent acquisition of Capital Foods adds a completely new dimension. Ching's Secret isn't just another food brand - it's a category creator that invented Indo-Chinese cuisine for home consumption in India. With products spanning noodles, sauces, soups, and ready-to-eat meals, Ching's provides entry into the fast-growing convenience food segment. The brand's irreverent marketing and strong youth connect complement Tata Consumer's traditional brand portfolio.

The coffee portfolio, while smaller than tea, plays a strategic role. Tata Coffee's plantation heritage provides sourcing advantages and authenticity. The consumer-facing brands - Tata Coffee Grand and Sonnets - target the growing coffee culture in India. The Starbucks joint venture, while technically separate, creates a halo effect and provides learning opportunities. Eight O'Clock Coffee in the US, despite its challenges, maintains the company's presence in the world's largest coffee market.

The water business, led by Himalayan Natural Mineral Water, exemplifies the premiumization strategy. Sourced from the Himalayas and positioned as pure and natural, Himalayan commands significant premiums over regular packaged water. The brand has become the preferred choice for hotels, restaurants, and airlines, providing both margins and brand visibility.

The strategic importance of the Starbucks joint venture extends beyond financial returns. Tata Starbucks now operates in over 390 stores across 54 Indian cities. Each store serves as a brand beacon, reinforcing Tata Consumer's premium credentials. The venture provides insights into retail operations, consumer experience design, and premium positioning that influence the broader portfolio strategy.

Manufacturing and supply chain capabilities underpin the portfolio strength. The company operates multiple tea estates in India, providing quality control from leaf to cup. Seven manufacturing facilities produce over 7 crore kilograms of tea annually. Salt operations include both inland and marine facilities, ensuring supply security. Food processing units have been modernized to meet international quality standards.

The distribution network is perhaps the company's greatest asset. In India, Tata Consumer Products has a reach of over 263 million households, giving it an unparalleled ability to leverage the Tata brand in consumer products. This reach isn't just about coverage but about relationships - with over 2.5 million retail outlets, thousands of distributors, and deep rural penetration that few companies can match.

The international footprint provides both diversification and growth opportunities. The company now operates in the food and beverages industry, with ~56% of their revenue coming from India while the rest is from their international businesses. This geographic diversification reduces dependence on any single market while providing exposure to different consumption trends and economic cycles.

Channel strategy has evolved to match changing retail landscapes. Alternate channels continued to fuel our growth and innovation agenda E-commerce channel grew 35% and Modern Trade recorded 9% growth in FY24. E-commerce isn't just another channel but a platform for launching exclusive products, testing innovations, and building direct consumer relationships. Modern trade provides visibility and premiumization opportunities.

The innovation pipeline reflects portfolio priorities. In beverages, the focus is on ready-to-drink formats, functional benefits, and premium variants. In foods, convenience, health, and authenticity drive development. Packaging innovation addresses sustainability concerns while improving convenience. Digital innovations include D2C platforms, subscription models, and personalized nutrition solutions.

Brand architecture has been carefully crafted to maximize portfolio value. The Tata master brand provides trust and credibility, particularly important in food categories. Individual brands like Tetley and Ching's Secret maintain their distinct identities and equity. The Sampann sub-brand strategy allows expansion into new categories while maintaining positioning consistency.

Market shares across categories demonstrate the portfolio's competitive strength. In tea, the company holds 21% share in India and significant positions internationally. In salt, the 30%+ share in India makes it the undisputed leader. In pulses and spices, while shares are smaller, the premium positioning provides margin advantages. The ready-to-eat segment, strengthened by Capital Foods, provides a platform for growth in convenience foods.

The portfolio's financial contribution varies by category and geography. Tea remains the largest revenue contributor but faces margin pressure from commodity inflation. Salt provides stable revenues and margins. Foods, while currently smaller, shows the highest growth rates and margin potential. International operations provide hard currency revenues and diversification benefits.

Competitive positioning varies by category. In tea and salt, the company enjoys leadership positions with strong brand moats. In foods, it competes with both established FMCG giants and nimble startups. The strategy isn't to dominate every category but to build profitable positions in segments where the company's capabilities provide advantages.

Looking at the portfolio holistically, Tata Consumer Products has successfully transformed from a beverages company to a comprehensive food and beverages player. The portfolio spans the consumption pyramid - from affordable essentials to premium indulgences. It addresses multiple consumption occasions - from morning tea to dinner preparations. Most importantly, it provides a platform for sustained growth through category expansion, premiumization, and geographic diversification.

VIII. Playbook: Business & Strategy Lessons

The transformation of Tata Consumer Products from a regional tea company to a global FMCG player offers rich lessons in strategy, execution, and timing. These insights are particularly valuable for companies in emerging markets aspiring to build global scale while maintaining local relevance.

The Art of the Leveraged Buyout in Emerging Markets

The Tetley acquisition pioneered the use of leveraged buyouts by Indian companies, demonstrating that financial innovation could overcome capital constraints. The key insight wasn't just about using debt but structuring it intelligently. By creating an SPV that ring-fenced the debt from the parent company, Tata Tea protected its balance sheet while gaining full control of a much larger entity. This structure became a template for subsequent Indian cross-border acquisitions.

The lesson extends beyond structure to preparation. The five-year gap between the failed 1995 attempt and successful 2000 acquisition wasn't wasted. The company used this time to build banking relationships, understand regulatory requirements, and deepen operational knowledge of the target. When opportunity knocked again, they were ready with financing, structure, and integration plans.

The psychological impact was equally important. Tata Group Chairman Ratan Tata called it a momentous occasion for the Company. Indeed, it was a defining and historic moment. Tata Tea had created history by acquiring a global brand and business several times its size. It had created history for itself, for the Tata Group and for India. This confidence boost enabled not just Tata but an entire generation of Indian companies to think globally.

Brand Architecture: When to Keep, When to Integrate

The company's approach to brand management demonstrates sophisticated understanding of brand equity and consumer psychology. When Tetley was acquired, there was no attempt to rebrand it as Tata Tea International or to impose Indian identity. The brand's British heritage and global recognition were preserved and leveraged. Similarly, Ching's Secret retained its irreverent, youth-focused identity post-acquisition.

Conversely, the Tata Sampann launch showed when creating a new unified brand makes sense. Rather than marketing individual pulses and spices under separate brands, the company created an umbrella brand that could span categories while maintaining consistent positioning around nutrition and authenticity. This architecture allowed efficient marketing spend while building a scalable platform.

The sub-branding strategy within Tata Tea - Premium, Gold, Agni - demonstrates portfolio management within a master brand. Each targets different segments without diluting the master brand equity. This approach maximizes marketing efficiency while addressing diverse consumer needs. The lesson: brand architecture should follow consumer logic, not corporate structure.

Evolution from Tea/Coffee/Salt Focus to Multi-Category FMCG Player

The journey from single category to multi-category wasn't linear but carefully orchestrated. Each expansion built on existing capabilities while adding new ones. Salt leveraged distribution but required different manufacturing and quality control. Foods leveraged brand trust but needed new sourcing and processing capabilities. The Starbucks venture provided retail experience that influenced the entire portfolio.

The timing of category expansion was crucial. The company didn't diversify when the core was struggling but when it was strong. Tea and salt provided the cash flow and distribution platform for expansion. This patient approach contrasts with companies that diversify prematurely, spreading resources too thin.

The recent acceleration in acquisitions reflects confidence and capability. The ability to acquire and integrate Capital Foods in 60 days shows operational maturity. The company now has the playbook - from due diligence to integration - to execute multiple acquisitions simultaneously. This M&A capability itself becomes a competitive advantage.

Balancing Heritage with Innovation

Tata Consumer Products masterfully balances its 150-year heritage with contemporary relevance. The Tata name provides trust, particularly important in food categories where quality concerns are paramount. But the company avoids being trapped by heritage, constantly innovating in products, packaging, and marketing.

The Jaago Re campaign for Tata Tea exemplifies this balance. While leveraging the brand's heritage, it connected tea consumption with social awakening, making it relevant for younger consumers. Similarly, Tata Salt's evolution from basic iodized salt to fortified variants shows how heritage brands can innovate without losing core equity.

The approach to innovation is pragmatic rather than disruptive. Instead of launching radically new products that might confuse consumers, the company focuses on incremental innovations that address real needs. Ready-to-drink formats for time-pressed consumers, single-serve packs for portion control, organic variants for health-conscious buyers - each innovation solves a specific consumer problem.

The Tata Group Advantage: Patient Capital and Synergies

Being part of the Tata Group provides advantages beyond capital. The patient, long-term approach allows investments in capability building and market development that might not meet quarterly earnings pressures in standalone companies. The Tetley acquisition took years to fully pay off, patience that independent companies might not have had.

Group synergies extend beyond financial. The Taj Hotels relationship provides premium positioning and sampling opportunities for Himalayan water and Tata Tea. Tata Chemicals provides technical expertise for salt and food processing. TCS and other group companies are customers for corporate sales. These synergies, while difficult to quantify, provide competitive advantages.

The Tata brand itself is perhaps the greatest asset. In India, it represents trust, quality, and nationalism - emotional connections that transcend product attributes. This allows the company to enter new categories with instant credibility, a privilege that competitors must earn over years.

Lessons from Failed Ventures

Not every initiative succeeded, and the failures provide valuable lessons. International expansion in some markets didn't achieve expected returns, teaching the importance of market selection and local partnerships. Some product launches failed to resonate, highlighting the need for consumer validation before scaling.

The company's approach to failure is instructive. Rather than dramatic exits, there's usually a quiet withdrawal and reallocation of resources. Failed experiments become learning opportunities, informing future strategies. This fail-fast-learn-faster approach allows continued experimentation without betting the company.

The discipline to exit non-core businesses - like gradual reduction in plantation ownership - shows strategic focus. While plantations provide backward integration, they're capital intensive with volatile returns. The shift from asset ownership to brand building reflects understanding of where value creation happens in modern FMCG.

Distribution as Competitive Advantage in India

In India's fragmented retail landscape, distribution becomes a critical differentiator. The company's reach to 4 million outlets isn't just about coverage but about relationships, credit management, and merchandising. Building this network took decades and represents a moat that new entrants cannot easily replicate.

The approach to distribution evolved with market changes. As modern trade emerged, the company built category management capabilities. As e-commerce exploded, digital marketing and fulfillment capabilities were developed. The key insight: distribution isn't just about reaching outlets but about winning at the point of purchase, regardless of channel.

Rural distribution received special focus, recognizing that rural India represents the next growth frontier. The hub-and-spoke model, using district centers to serve surrounding villages, balances reach with economics. Technology deployment, from handheld devices for sales teams to AI-powered demand forecasting, modernizes traditional distribution.

The strategic playbook that emerges from Tata Consumer Products' journey is clear: start with a strong core, expand adjacently, use M&A to accelerate, balance global and local, invest in capabilities before categories, and maintain strategic patience. These lessons, learned over decades and often through trial and error, provide a roadmap for building scale in consumer products. The playbook continues to evolve, but the fundamental principles - consumer focus, quality obsession, and long-term thinking - remain constant.

IX. Financial Analysis & Market Dynamics

The financial transformation of Tata Consumer Products over the past two decades tells a story of consistent value creation, strategic capital allocation, and the challenges of competing in the intensely competitive FMCG sector. Understanding the numbers behind the narrative provides insights into both achievements and areas for improvement.

Current Financial Metrics and Trajectory

As of 2024, Tata Consumer has a market cap of 1,03,565 Crore, revenue of 18,045 Cr, and profit of 1,330 Cr. These numbers represent a remarkable transformation from the sub-$200 million revenue company that acquired Tetley in 2000. The market capitalization of over ₹1 lakh crore places it among India's most valuable FMCG companies, though still significantly behind Hindustan Unilever's ₹5 lakh crore-plus valuation.

In financial year 2024, Tata Consumer Products Limited witnessed its highest revenue, which stood at around 155 billion Indian rupees. This revenue milestone reflects both organic growth and the impact of recent acquisitions. The growth trajectory has been particularly impressive post-2020 merger, with revenues growing at a CAGR of over 15% despite pandemic-related disruptions.

Profitability metrics reveal both strengths and challenges. In financial year 2024, the net profit of Tata Consumer Products Ltd. amounted to about 9.8 billion Indian rupees. The net margin of approximately 6-7% is respectable but below the 15-20% margins that leaders like Nestle India achieve. This margin differential reflects the company's exposure to commodity categories like tea and salt, where pricing power is limited.

The recent quarterly performance shows momentum with challenges. For the quarter, Revenue from operations grew by 9% (8% in constant currency) as compared to corresponding quarter of the previous year, with strong performance in India business, which grew 10%. Profit before exceptional items and tax at Rs 509 Crores is higher by 12%. Group Net Profit before exceptional items at Rs 427 Crores is up 46% driven by strong operating performance and one-time tax credits during the quarter.

Competition: HUL, Nestle, ITC in India; Unilever Globally

The competitive landscape in Indian FMCG is dominated by a few large players, each with distinct strengths. Hindustan Unilever (HUL), with revenues exceeding ₹50,000 crore, remains the undisputed leader. HUL's portfolio spanning home care, personal care, and foods provides scale advantages in distribution and marketing. Its deep understanding of Indian consumers, built over decades, creates a formidable moat.

Nestle India, while smaller in revenue, enjoys superior margins through focus on high-value categories like infant nutrition, coffee, and chocolates. Its global R&D capabilities and brand strength in categories like Maggi noodles provide pricing power that Tata Consumer is still building. The successful relaunch of Maggi after the 2015 crisis demonstrates resilience that comes from strong brand equity.

ITC represents a different competitive model. Its cigarette business provides cash flows that fund aggressive expansion in FMCG. ITC's strategy of creating focused brands for specific segments - Aashirvaad in atta, Sunfeast in biscuits, Bingo in snacks - shows the power of category focus. With over ₹15,000 crore in FMCG revenues, ITC has emerged as a serious competitor.

Globally, Unilever remains the benchmark in tea with its Lipton and PG Tips brands. Despite Tata Consumer's global presence through Tetley, Unilever's scale provides advantages in procurement, innovation, and marketing. The recent struggles of Unilever's tea business, however, leading to its decision to separate the division, suggest structural challenges in the category that affect all players.

Growth Drivers: Premiumization, Health & Wellness, Convenience

The premiumization trend represents the most significant growth opportunity. Indian consumers, particularly urban millennials, are willing to pay premiums for perceived quality, health benefits, and experience. In FY 24, premium and sub premium segments outperformed the overall business and accounted for over two thirds of India Tea revenue. This shift from commodity to premium is crucial for margin expansion.

Health and wellness trends accelerated by COVID-19 create opportunities across the portfolio. Immunity-boosting teas, organic foods, fortified salt, and nutritious ready-to-eat options address growing health consciousness. The Organic India acquisition positions the company at the forefront of this trend. The challenge is balancing health positioning with taste and affordability, particularly in price-sensitive Indian markets.

Convenience represents another growth vector. Urban lifestyles drive demand for ready-to-eat meals, instant beverages, and portion-controlled packaging. The Capital Foods acquisition with Ching's Secret provides a platform in convenience foods. The ₹5,100 crore investment reflects confidence in this category's potential. Success will depend on innovation speed and distribution efficiency.

International vs Domestic Growth Trajectories

The revenue split between domestic and international operations reveals strategic priorities. ~56% of their revenue coming from India while the rest is from their international businesses. This balance provides diversification while maintaining focus on the high-growth Indian market.

Indian operations benefit from favorable demographics, rising incomes, and increasing brand consciousness. The growth rates in India consistently exceed international markets, justifying continued investment. Categories like ready-to-eat, premium tea, and fortified foods show double-digit growth. Rural penetration remains low, providing runway for expansion.

International operations provide stability and hard currency earnings but face different challenges. Developed markets like the UK and Canada are mature with limited growth. Competition from private labels is intense. The focus has shifted from volume growth to value through premiumization and innovation. Emerging markets offer growth potential but require investment and local adaptation.

Capital Allocation Track Record

The company's capital allocation over the past decade reveals strategic discipline with calculated aggression. The ₹5,100 crore Capital Foods acquisition and ₹1,900 crore Organic India deal represent the largest deployments, signaling confidence in inorganic growth. These acquisitions, totaling nearly ₹7,000 crore, exceed the company's annual profit, showing willingness to leverage for strategic assets.

The integration track record provides confidence. The Tetley acquisition, despite initial challenges, created long-term value. Recent acquisitions like Soulfull and SmartFoodz were successfully integrated. Following the recent acquisition of Capital Foods, both front end and back-end integration has been completed on an accelerated timeline, within 60 days of the acquisition. This execution capability justifies aggressive acquisition strategies.

Organic investments focus on brand building, distribution expansion, and capability development. Marketing spends have increased to 8-10% of revenues, comparable to industry standards. Distribution investments, particularly in rural markets and modern channels, drive reach expansion. Technology investments in digital marketing, e-commerce, and supply chain modernize operations.

Future Growth Vectors: Organic, Ready-to-Eat, Beverages

The organic foods segment represents a significant opportunity. Global organic food markets exceed $100 billion and grow at 10-15% annually. In India, while the market is smaller, growth rates exceed 25%. The Organic India acquisition provides immediate scale and capability. The challenge is making organic accessible beyond niche segments while maintaining authenticity.

Ready-to-eat foods address changing lifestyles and convenience needs. The Indian RTE market, estimated at ₹5,000 crore, grows at 15-20% annually. Nuclear families, working women, and urban migration drive demand. Success requires balancing convenience with taste, nutrition with shelf life, and aspiration with affordability. The Capital Foods platform provides the foundation for expansion.

Beverages remain core with evolution opportunities. Beyond traditional tea and coffee, functional beverages, plant-based drinks, and wellness shots represent growth areas. The Starbucks partnership provides premium positioning while Tata Tea addresses mass markets. Innovation in RTD formats, cold brew coffee, and herbal infusions drives category expansion.

The financial analysis reveals a company in transition. Revenue growth is strong, driven by acquisitions and category expansion. Profitability, while improving, has room for enhancement through premiumization and operational efficiency. The competitive position is solid in core categories with opportunities in emerging segments. Capital allocation shows strategic clarity with execution capability. The trajectory is positive, though achieving global FMCG leader status requires sustained execution over the next decade.

X. Bear vs Bull Case

As we evaluate Tata Consumer Products' investment potential and strategic position, it's crucial to examine both the optimistic and pessimistic scenarios. The tension between these perspectives illuminates the key variables that will determine the company's trajectory over the next decade.

Bull Case: The Optimistic Scenario

India Consumption Story and Rising Per Capita Income

India's demographic dividend is just beginning to pay out. With a median age of 28 years and per capita income still under $3,000, the consumption growth runway extends for decades. As millions enter the middle class annually, their first upgrades include packaged, branded food products replacing loose, unbranded alternatives. Tata Consumer Products, with its trusted brands and extensive distribution, is ideally positioned to capture this transition.

The premiumization trend accelerates as consumers climb the income ladder. A consumer who starts with Tata Salt moves to Tata Salt Lite, then to rock salt or Himalayan pink salt. Similar progression happens in tea, from economy to premium variants. This natural trading up within the portfolio drives revenue growth faster than volume growth, expanding margins. The company's multi-tier portfolio strategy captures value at every step of the consumer journey.

Urban consumption patterns are also evolving favorably. The growth of nuclear families, increasing female workforce participation, and time poverty drive demand for convenience foods. Ready-to-eat meals, instant beverages, and pre-packaged ingredients save time while ensuring quality. The Capital Foods acquisition positions the company perfectly for this convenience revolution.

Strong Brand Portfolio with Pricing Power

The brand portfolio represents decades of consumer trust that competitors cannot quickly replicate. Tata Salt's 40-year heritage, Tata Tea's emotional connection with Indian consumers, and Tetley's global recognition create moats that protect market share and enable pricing power. In an inflationary environment, established brands can pass on cost increases more easily than new entrants.

The Tata brand itself provides an umbrella of trust that enables category expansion. When Tata Sampann enters a new category, it starts with credibility that startups must spend years and millions building. This brand leverage accelerates new product adoption and reduces marketing costs. The recent success of Tata Sampann, growing at 30%+ annually, demonstrates this advantage.

The acquisition strategy adds proven brands with established positions. Ching's Secret didn't just bring products but a brand that created and owns a category. Organic India brings authenticity in organic foods that would take years to build organically. These acquisitions aren't just about revenues but about acquiring brand equities that would be impossible to replicate.

Distribution Reach and Tata Group Backing

The distribution network reaching 4 million outlets represents an infrastructure that took decades to build and would cost billions to replicate. This network provides not just reach but relationships, credit management, and merchandising capabilities. For new products, this distribution highway enables rapid scale that competitors struggle to match.

The Tata Group backing provides advantages beyond capital. Patient investment horizons allow long-term capability building. Group synergies provide cost advantages and market access. The Tata reputation opens doors in international markets and with global partners. The Starbucks partnership, unlikely without the Tata name, exemplifies these advantages.

Financial strength enables strategic flexibility. The ability to make ₹7,000 crore in acquisitions while maintaining investment grade ratings shows balance sheet capacity. Unlike leveraged competitors, the company can pursue opportunities without financial constraints. This flexibility becomes crucial in dynamic markets where speed matters.

International Diversification Hedge

International operations providing 44% of revenues create resilience against India-specific shocks. When Indian consumption slowed during demonetization or COVID lockdowns, international revenues provided stability. This geographic diversification reduces volatility and provides more predictable cash flows.

Currency diversification provides natural hedging. Earnings in pounds, dollars, and euros protect against rupee depreciation. In an inflationary environment with potential currency weakness, international earnings become more valuable when converted to rupees. This currency benefit adds to reported growth beyond operational performance.