FDC Limited: The ORS Pioneer and India's Healthcare Champion

I. Introduction & Cold Open

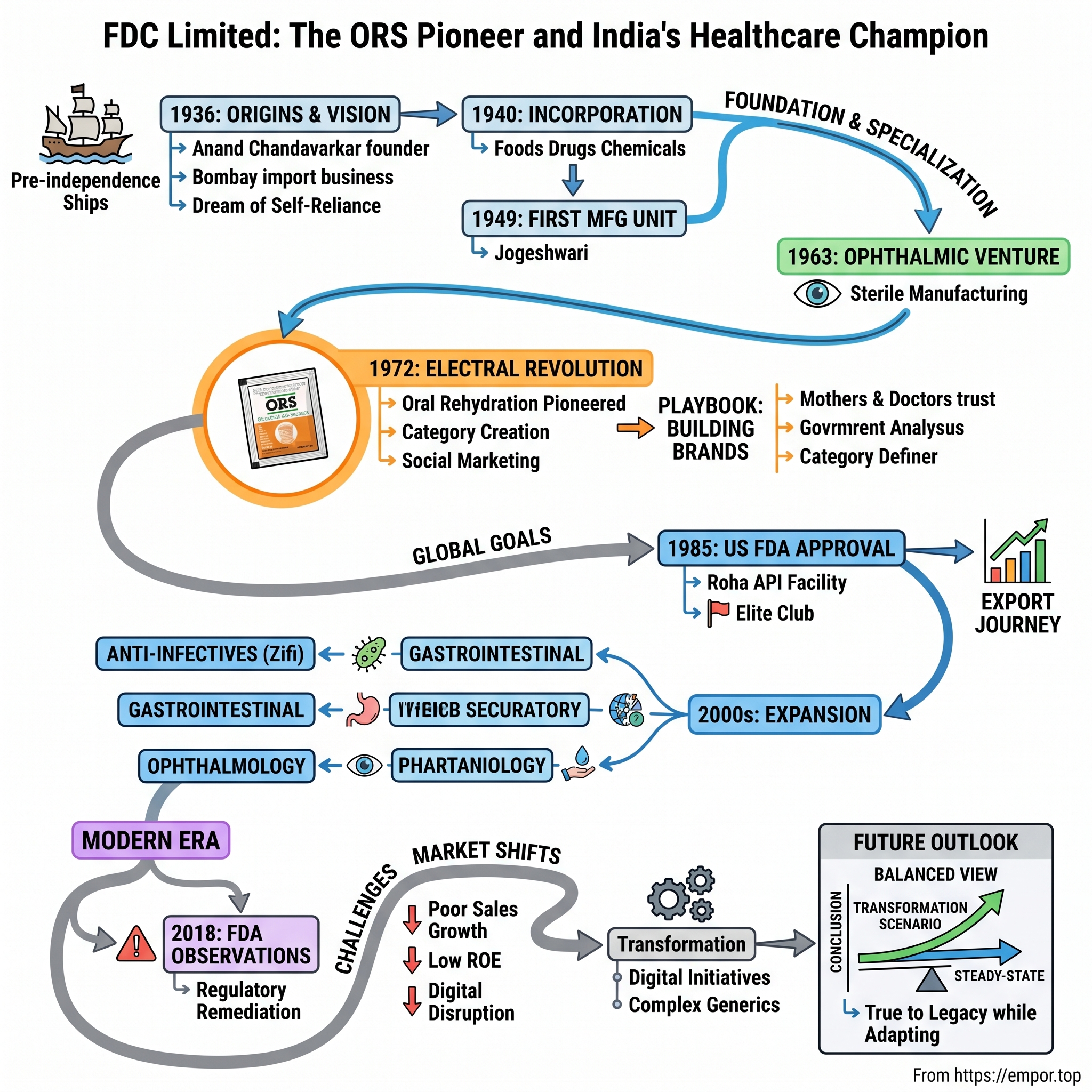

The year is 1972. In a modest laboratory in Mumbai's Jogeshwari suburb, a team of Indian scientists huddles over a simple formula that would save millions of lives. They're not developing a complex cancer drug or a breakthrough vaccine. They're perfecting something far more basic yet revolutionary: a precise mixture of salts and glucose that, when dissolved in water, could prevent children from dying of diarrhea—then India's silent killer claiming over 600,000 young lives annually.

This was FDC Limited, and their product would become Electral—a brand so synonymous with oral rehydration that three generations of Indian mothers would reach for it instinctively whenever their children fell ill. But how did a company that started as an import business in colonial India, founded by a visionary named Anand Chandavarkar in 1936, transform into a global leader in ORS manufacturing and one of the first Indian pharmaceutical companies to receive FDA approval?

The story of FDC is not just about pharmaceuticals—it's about nation-building through healthcare, about creating categories where none existed, and about the audacious belief that an Indian company could meet global quality standards when most of the world saw India as merely a market for Western drugs. Today, FDC stands as a ₹2,100 crore enterprise, manufacturing everything from anti-infectives to nutraceuticals, with facilities approved by regulators from Washington to Tokyo.

Yet this is also a story of missed opportunities and strategic pivots. While contemporaries like Dr. Reddy's and Sun Pharma built global empires worth tens of billions of dollars, FDC chose a different path—one focused on therapeutic specialization rather than blockbuster generics, on building unshakeable brand moats in commoditized categories rather than chasing patent cliffs. Was this prudence or a lack of ambition? The answer, as we'll discover, reveals fundamental truths about strategy, timing, and the choices that define corporate destiny.

This episode traces FDC's 88-year journey from a pre-independence trading firm to a publicly-listed pharmaceutical manufacturer, from pioneering ORS in India to navigating the complexities of FDA regulations and price controls. We'll explore how a family-controlled business maintained its identity through three generations while adapting to seismic shifts in Indian healthcare policy, global pharmaceutical standards, and market dynamics.

Along the way, we'll unpack the playbook of building brands in commoditized markets, the art of backward integration in pharmaceuticals, and the delicate balance between innovation and affordability in a price-sensitive market like India. We'll examine why some strategic decisions that seemed conservative at the time may have been exactly right, while others that appeared bold might have constrained future growth.

So buckle up as we dive deep into the story of FDC Limited—a company that chose depth over breadth, specialization over diversification, and in doing so, carved out a unique position in India's pharmaceutical landscape. This is not just a business story; it's a chronicle of how healthcare access was democratized in India, one sachet of Electral at a time.

II. Pre-Independence Origins & The Chandavarkar Vision (1936-1949)

Picture Bombay in 1936. The Gateway of India, barely a decade old, watches over a bustling port where steamships unload cargo from Liverpool, Hamburg, and New York. The city thrums with the energy of global commerce, yet beneath the colonial grandeur lies a stark reality: India imports nearly everything of medical value. From aspirin to surgical gauze, from baby food to bandages, the subcontinent depends entirely on foreign suppliers for its healthcare needs.

Into this world steps Anand Chandavarkar, a young entrepreneur whose vision extends far beyond the immediate profits of import trading. While his contemporaries see opportunity in simply distributing Western goods to Indian consumers, Chandavarkar sees something different—he sees dependence as a form of bondage more insidious than political subjugation. His dream? To build a company that would one day manufacture what India then could only import.

The timing of Chandavarkar's venture was no accident. The 1930s marked a unique inflection point in Indian commercial history. The Swadeshi movement had awakened a generation to the power of economic self-reliance. Indian industrialists like the Tatas and Birlas were proving that natives could build world-class enterprises. The Government of India Act of 1935 had just granted provincial autonomy, creating the first stirrings of self-governance. In this charged atmosphere, starting an import business wasn't just commerce—it was preparation for independence.

Chandavarkar began modestly, importing infant foods, drugs, and surgical appliances. But unlike typical traders who focused on maximizing margins, he obsessed over understanding these products. Why were certain formulations more effective? How were surgical instruments manufactured to such precision? What made Western baby food more nutritious than traditional alternatives? Each import shipment became a lesson in pharmaceutical science and manufacturing excellence.

The business grew steadily through the late 1930s, but Chandavarkar knew that true success meant evolution beyond trading. On September 23, 1940—while Europe was engulfed in war and India's independence movement gathered steam—he formally incorporated FDC Limited. The acronym itself was deliberately ambiguous, allowing the company flexibility to define its future. Some said it stood for "Foods Drugs Chemicals," others claimed "Fairdeal Corporation." Chandavarkar preferred the mystery; it gave him room to maneuver.

World War II transformed everything. Suddenly, import routes were disrupted. Ships that once brought medicines now carried military supplies. The Bengal Famine of 1943 killed millions, partly due to lack of access to basic medical supplies. These catastrophes reinforced Chandavarkar's conviction: India needed its own pharmaceutical manufacturing capability. It wasn't just good business—it was a matter of national survival.

As independence approached in 1947, Chandavarkar made his boldest move yet. While others worried about partition's chaos and capital flight, he saw opportunity in uncertainty. Properties were available at distressed prices. Skilled chemists and technicians, previously employed by British firms, were seeking new opportunities. Most importantly, the soon-to-be independent government would surely prioritize domestic manufacturing over imports.

In 1949, just two years after independence, FDC established its first formulation unit at Jogeshwari, then a suburb on Bombay's outskirts. The location was strategic—close enough to the commercial center for business dealings, far enough for affordable land, and perfectly positioned near the Western Railway line for distribution. The facility was modest: a few tablet presses, basic mixing equipment, and a small quality control laboratory. But it represented something profound—the transformation from trader to manufacturer, from dependent to self-reliant.

The early products were simple: vitamin tablets, cough syrups, basic antibiotics. Nothing revolutionary in formulation, but revolutionary in implication. Each tablet pressed at Jogeshwari was a small declaration of independence. The quality wasn't yet world-class—how could it be, with limited equipment and nascent expertise? But it was Indian-made, and in the euphoria of newly-won freedom, that mattered immensely.

Chandavarkar understood that post-independence India would be shaped by two forces: socialist planning and import substitution. Nehru's government would control licenses, regulate prices, and allocate resources. Success would require not just manufacturing capability but political navigation. FDC positioned itself perfectly—small enough to avoid threatening established players, sophisticated enough to be taken seriously by regulators, and patriotic enough to align with national objectives.

By 1949's end, as India's Constitution was being drafted and the nation's industrial policy taking shape, FDC had completed its first transformation. No longer just an import house, it was now a manufacturer. The revenues were tiny, the products basic, but the foundation was laid. Chandavarkar's vision—born in colonial subjugation, nurtured through world war, and realized in independence—had taken its first concrete form.

What Chandavarkar perhaps didn't fully appreciate was how prescient his timing had been. The 1950s would bring the Industrial Policy Resolution, making pharmaceuticals a priority sector. The 1960s would see patent law changes favoring process innovation over product patents. The 1970s would witness the rise of public sector pharmaceutical companies and stringent import restrictions. Each policy shift would benefit companies that had already established manufacturing capabilities. By moving early, FDC had positioned itself to ride every wave of India's pharmaceutical evolution.

III. Building the Foundation: Specialization Era (1950s-1970s)

The Jogeshwari facility in 1963 hummed with an unusual energy. While most Indian pharmaceutical companies were content manufacturing generic tablets and syrups, FDC's research team was attempting something audacious: creating specialized ophthalmic formulations. The challenge was immense—eye drops required sterility levels that most Indian facilities couldn't achieve, preservative systems that wouldn't irritate sensitive corneal tissue, and packaging that could maintain product integrity in India's harsh climate. When FDC succeeded, it became the first company in Southeast Asia to master this specialized manufacturing. It was a defining moment that would shape the company's philosophy for decades: don't just manufacture, specialize.

This strategic pivot toward specialization wasn't obvious. The 1950s and early 1960s were the golden age of broad-based manufacturing in India. The Industrial Policy Resolution of 1956 had reserved basic drugs for the public sector, pushing private companies toward formulations. Most players responded by producing everything—antibiotics, vitamins, analgesics, whatever the market demanded. Volume was king, margins were thin, and differentiation was minimal.

But FDC's leadership, now expanded beyond Chandavarkar to include a cadre of scientifically-trained managers, saw opportunity in complexity. Ophthalmic products required specialized equipment, trained personnel, and rigorous quality control. The barriers to entry were high, competition was limited, and margins were superior. More importantly, doctors valued quality in ophthalmic products far more than in general medicines—a substandard antibiotic might be ineffective, but a contaminated eye drop could cause blindness.

The ophthalmic venture's success validated FDC's specialization strategy, but the real revolution came in 1972 with a product that seemed almost mundanely simple: oral rehydration salts. The backstory is worth dwelling on. The World Health Organization had just endorsed ORS as a treatment for diarrheal dehydration, calling it "potentially the most important medical advance of the century." The formula was basic—sodium chloride, potassium chloride, sodium bicarbonate, and glucose in precise proportions. No patents, no proprietary technology, seemingly no competitive advantage.

Yet FDC recognized what others missed: in India, the challenge wasn't formulation but implementation. How do you convince millions of mothers, many illiterate, to use a medical powder instead of traditional remedies? How do you ensure quality when the product must be stable in 45-degree heat and monsoon humidity? How do you create a brand in a category that doesn't yet exist?

The answer came in the form of Electral, a name that would become synonymous with ORS in India. The branding was brilliant—scientific enough to convey medical credibility, simple enough to be remembered by rural consumers. The packaging was revolutionary for its time: single-dose sachets that eliminated measurement errors, multilingual instructions with pictographs for illiterate users, and a distinctive orange color that stood out on pharmacy shelves.

But FDC's masterstroke was recognizing that Electral wasn't just a pharmaceutical product—it was a public health intervention. The company worked with government health programs, trained thousands of rural health workers, and conducted awareness campaigns that taught mothers to recognize dehydration symptoms. This wasn't traditional pharmaceutical marketing; it was category creation at its finest.

The impact was staggering. Within a decade, Electral had helped reduce childhood diarrheal deaths in India by over 50%. The brand became so dominant that many Indians still use "Electral" as a generic term for any ORS, much like "Xerox" for photocopying. The product generated modest revenues initially, but it created something far more valuable: trust, distribution reach, and a reputation for quality that would underpin FDC's growth for decades.

The 1974 recognition from the Government of India for R&D excellence wasn't just a certificate to hang on the wall—it was validation of FDC's strategic direction. While other companies were reverse-engineering Western drugs, FDC was adapting formulations for Indian conditions. Their research focused on stability in tropical climates, taste-masking for pediatric formulations, and cost-effective manufacturing processes. This wasn't cutting-edge molecular research, but it was practical innovation that solved real problems.

The decade also saw FDC's crucial decision to backward integrate into active pharmaceutical ingredients (APIs). The Roha facility, established in the mid-1970s, represented a massive capital commitment for a company of FDC's size. The conventional wisdom suggested focusing on formulations where margins were better and capital requirements lower. But FDC's leadership understood that API manufacturing provided three critical advantages: supply security in an era of import restrictions, cost advantages through vertical integration, and most importantly, quality control from raw material to finished product.

The Roha plant specialized in fermentation-based APIs, particularly antibiotics. The technology was complex—maintaining sterile conditions, controlling fermentation parameters, and achieving consistent yields required expertise that few Indian companies possessed. FDC recruited talent from public sector enterprises, sent engineers to Eastern Europe for training (Western countries being largely closed to Indian companies then), and invested heavily in quality control laboratories.

By the late 1970s, FDC had evolved far from its trading origins. It manufactured specialized formulations that required technical expertise. It had created a category-defining brand in Electral. It controlled its API supply chain. It had government recognition for R&D. Most importantly, it had developed a culture of specialization—the belief that depth trumped breadth, that expertise created sustainable advantages, and that solving specific problems generated more value than chasing every opportunity.

This foundation would prove crucial for the next phase of FDC's evolution. The 1980s would bring economic liberalization, global competition, and regulatory scrutiny. Companies that had spread themselves thin would struggle. But FDC, with its specialized capabilities and vertical integration, was positioned to not just survive but to attempt something even more audacious: earning approval from the world's toughest pharmaceutical regulator, the US FDA.

IV. The Electral Revolution: Creating a Category (1972-1990s)

The numbers were devastating. In 1970s India, diarrhea killed more children than malaria, measles, and malnutrition combined. Every year, over 600,000 children under five died from what was essentially dehydration—a condition that could be treated with a solution simpler than lemonade. In villages across Bihar, Uttar Pradesh, and Rajasthan, mothers watched helplessly as their children succumbed to what locals called "loose motions," unaware that the cure cost less than a cup of tea.

Dr. Dilip Mahalanabis had just returned from treating cholera victims in Bangladesh refugee camps during the 1971 war. He had witnessed something remarkable: oral rehydration therapy saving lives when intravenous fluids were unavailable. The science was elegant—glucose enhanced sodium absorption in the intestine, pulling water along with it. The WHO had endorsed the therapy, but implementation in India faced a fundamental problem: how do you deliver a medical intervention to millions of households where the nearest doctor might be fifty kilometers away?

FDC's leadership recognized that Electral needed to be more than a pharmaceutical product—it needed to be a consumer revolution disguised as medicine. The first challenge was formulation. The WHO formula was effective but tasted terrible—imagine drinking seawater mixed with sugar. FDC's formulators spent months perfecting a version that maintained medical efficacy while being palatable enough for children to accept. They added flavoring agents that wouldn't interfere with absorption, adjusted the osmolality to reduce nausea, and created a formula that remained stable in India's extreme temperatures.

The packaging innovation was equally critical. Glass bottles were impractical for rural distribution. Bulk powder required precise measurement—impossible without proper tools. FDC's solution was ingenious: pre-measured sachets containing exactly enough powder for 200ml of water, the optimal volume for pediatric administration. The sachets were made from specialized laminate that prevented moisture ingress during monsoons and maintained product integrity in desert heat. Each design decision solved a specific Indian problem.

But the real genius lay in the go-to-market strategy. FDC recognized that Electral faced three distinct audiences: doctors who needed scientific convincing, pharmacists who controlled point-of-sale recommendations, and mothers who made the actual purchase decision. Each required a different approach.

For doctors, FDC conducted continuing medical education programs, distributed WHO literature, and sponsored research on diarrheal diseases in Indian conditions. The message was clinical: Electral could prevent 90% of diarrheal deaths if administered early. The company recruited medical representatives who could explain osmolality and electrolyte balance, not just push product.

For pharmacists, the approach was commercial but nuanced. Electral offered better margins than competing products, but FDC also provided education on recognizing dehydration symptoms. Pharmacists became quasi-health advisors, able to recommend Electral when mothers described their children's conditions. This elevated their status in communities while driving sales.

The masterstroke was the mother-focused campaign. FDC created visual communication tools that transcended literacy barriers. The iconic image of a wilted plant being revived by water became synonymous with rehydration. Radio jingles in regional languages taught mothers to recognize sunken eyes and dry lips as danger signs. The message was simple: "Jab pet kharab, Electral jawaab" (When stomach's upset, Electral's the answer).

Distribution presented another massive challenge. India's pharmaceutical distribution in the 1970s was concentrated in urban areas. Rural regions, where diarrheal deaths were highest, had minimal pharmacy presence. FDC pioneered what would later be called "social marketing"—partnering with government primary health centers, training ASHA workers, and even working with traditional healers who commanded community trust.

The company made a crucial decision: in government programs and rural health camps, Electral would be provided at cost or even free. This wasn't charity—it was market development. Every child saved created a family that would trust Electral for life. Every successful treatment generated word-of-mouth marketing more powerful than any advertisement.

By 1980, Electral had achieved something remarkable: 40% market share in a category it had essentially created. Competitors had entered—both multinationals like Glaxo and domestic players like Jagsonpal—but Electral's first-mover advantage proved insurmountable. The brand had become genericized in the best possible way. Mothers didn't ask for ORS; they asked for Electral.

The financial performance was equally impressive. While Electral's unit price was low—intentionally kept affordable—volumes were staggering. By 1985, FDC was producing over 100 million sachets annually. The gross margins were healthy because of vertical integration and economies of scale. More importantly, Electral created a distribution network and brand equity that FDC could leverage for other products.

The product evolution continued through the 1980s and 1990s. FDC introduced flavored variants for better pediatric compliance. They developed Electral RTD (ready-to-drink) for situations where clean water wasn't available. They created Enerzal, a energy drink variant for athletes and laborers, expanding beyond medical to wellness positioning. Each innovation strengthened the franchise while maintaining the core equity.

The public health impact was transformational. By 1990, diarrheal deaths in India had declined by over 60%. While multiple factors contributed—improved sanitation, better healthcare access, rising incomes—Electral's role was undeniable. The Lancet published a study crediting ORS adoption, led by brands like Electral, as saving more lives than any other medical intervention in the 1980s.

What FDC had achieved with Electral went beyond commercial success. They had demonstrated that an Indian company could create a global-standard product, build a brand in a commoditized category, and generate both profit and social impact. They had proven that specialization and deep market understanding could triumph over scale and resources.

The Electral story also revealed FDC's strategic DNA: the ability to identify underserved therapeutic needs, create products that solved specific Indian problems, and build brands through education rather than pure advertising. This playbook would be replicated across other categories, but never quite with the same transformative impact.

As the 1990s approached, bringing economic liberalization and global competition, FDC's position seemed secure. Electral generated steady cash flows, the brand moat appeared impregnable, and the company's reputation for quality was unmatched. But FDC's leadership understood that domestic success, however impressive, was insufficient. The next frontier lay beyond India's borders, in the regulated markets of the United States and Europe, where quality standards were unforgiving and competition was global.

V. Going Global: The FDA Approval & Export Journey (1985-2000s)

The letter arrived at FDC's Mumbai headquarters on a humid August morning in 1985. The US Food and Drug Administration had completed its inspection of the Roha API facility. The verdict: approved. In that moment, FDC became one of the first Indian pharmaceutical companies to receive FDA certification, joining an elite club that included only Ranbaxy and a handful of others. But unlike the celebration that might be expected, the mood at FDC was one of quiet validation. They had spent five years preparing for this inspection, transforming not just their manufacturing processes but their entire organizational culture.

The journey to FDA approval began in 1980 with a sobering realization. FDC's leadership, touring pharmaceutical facilities in Switzerland and Germany, understood the chasm between Indian and global standards. It wasn't about capability—Indian scientists were as talented as any. It was about systems, documentation, and a mindset where quality wasn't just important but sacrosanct. The decision to pursue FDA approval was contentious. The investment required was massive, perhaps 30% of FDC's annual revenue. The probability of success was uncertain. Many board members questioned why FDC needed FDA approval when the domestic market offered plenty of growth.

The answer came from Chandavarkar's successor generation, now led by his son who had trained in pharmaceutical sciences in the United States. They saw FDA approval not as an end but as a means—a forcing function that would elevate FDC's capabilities across the board. Products made for the US market would set quality benchmarks for domestic production. The discipline required for FDA compliance would improve operational efficiency. Most importantly, FDA certification would open doors to partnerships and opportunities that would otherwise remain closed.

The transformation of the Roha facility was comprehensive. Every piece of equipment was evaluated against FDA standards. Those that didn't meet specifications were replaced, regardless of remaining useful life. The quality control laboratory was expanded to include sophisticated analytical instruments—HPLC systems, mass spectrometers, dissolution apparatus—that cost more than some companies' entire annual R&D budgets. But the hardest changes were cultural. FDA compliance required documentation of everything—every batch record, every deviation, every investigation. For an organization accustomed to informal communication and flexible processes, this was revolutionary.

FDC hired consultants who had worked with the FDA, recruited quality assurance professionals from multinational companies, and sent teams to the United States to understand regulatory expectations. They created Standard Operating Procedures (SOPs) for every process, from raw material receipt to finished product release. They implemented a "right first time" philosophy where preventing errors was prioritized over correcting them.

The FDA inspection itself was grueling—five days of intense scrutiny where inspectors examined everything from air handling systems to training records. The success wasn't just in receiving approval but in doing so without major observations. The inspector's report noted FDC's "commitment to quality" and "robust systems"—high praise from an agency known for its exacting standards.

With FDA approval in hand, FDC faced a new challenge: actually penetrating the US market. The approval opened doors, but walking through them required different capabilities. The US generic market was intensely competitive, dominated by companies like Teva and Mylan with deep pockets and established relationships. FDC's strategy was clever: rather than competing head-on in high-volume generics, they focused on complex APIs where their fermentation expertise provided an edge.

The first major success came with Cephalosporin intermediates, where FDC's fermentation capabilities and cost structure allowed them to offer competitive prices while maintaining FDA-compliant quality. By 1990, FDC was supplying APIs to several US generic manufacturers, generating valuable foreign exchange and establishing credibility in regulated markets.

The European expansion followed a different trajectory. While the US market was about meeting uniform FDA standards, Europe required navigating multiple regulatory regimes. FDC pursued a country-by-country strategy, starting with the UK (where colonial connections facilitated entry) and gradually expanding to Germany, France, and Italy. Each market required specific regulatory dossiers, local partnerships, and understanding of reimbursement systems.

The 1996 IPO marked a watershed moment in FDC's globalization journey. The capital raised—approximately ₹50 crores—was specifically earmarked for expanding manufacturing capacity and upgrading facilities to meet international standards. The IPO prospectus positioned FDC not as another domestic pharmaceutical company but as an emerging global player with FDA-approved facilities and growing export revenues.

The investor response was enthusiastic. The issue was oversubscribed 12 times, with strong interest from institutional investors who recognized the value of FDA approval. The listing provided not just capital but credibility. International partners who had been hesitant to work with a private Indian company were reassured by the transparency and governance standards required of public companies.

The late 1990s saw FDC aggressively expanding its manufacturing footprint. The Goa facility, strategically located near Mormugao port for export convenience, was designed from the ground up to meet international standards. The Baddi plant in Himachal Pradesh took advantage of tax incentives while maintaining FDA-compliant standards. Each facility specialized in different products—Roha for APIs, Goa for oral solid dosages, Baddi for specialized formulations—creating centers of excellence rather than redundant capacities.

The international partnership strategy was equally sophisticated. Rather than simply being a contract manufacturer, FDC sought strategic relationships where both parties brought unique value. With a Japanese company, FDC provided cost-effective manufacturing while gaining access to advanced fermentation technology. With a UK distributor, FDC offered regulatory support for European filings while leveraging their marketing network.

By 2000, FDC's transformation was complete. Export revenues had grown from virtually nothing in 1985 to over 30% of total sales. The Roha facility had been successfully inspected by the FDA nine times, a record that few global companies could match. FDC was supplying APIs to over 40 countries, from regulated markets like Canada and Japan to emerging economies in Southeast Asia and Latin America.

But perhaps the most important achievement was the organizational capability FDC had built. The company now had over 200 professionals trained in international regulatory affairs. Its quality systems were benchmarked against global best practices. Its R&D could develop products specifically for international markets, understanding the nuances of different regulatory requirements.

The international success also had profound implications for the domestic business. The discipline required for FDA compliance improved quality across all products, even those sold only in India. The premium pricing achieved in export markets improved overall margins. The technological capabilities developed for international products could be leveraged for domestic innovation.

As the new millennium dawned, FDC stood at an interesting juncture. It had successfully transformed from a domestic player to a global participant. It had proven that an Indian company could meet the world's toughest quality standards. But the competitive landscape was evolving rapidly. Chinese manufacturers were emerging as formidable competitors in APIs. Indian peers like Dr. Reddy's and Sun Pharma were growing through aggressive acquisitions. The question was: having built these capabilities, how should FDC deploy them for the next phase of growth?

VI. Product Portfolio Expansion & Therapeutic Leadership (2000s-2010s)

The conference room at FDC's Mumbai headquarters in 2003 witnessed a heated debate. On one side were executives arguing for a "blockbuster" strategy—develop or acquire a few high-value products that could generate billions in revenue. They pointed to Ranbaxy's success with Simvastatin and Dr. Reddy's with Omeprazole. On the other side were traditionalists who believed FDC's strength lay in its portfolio approach—multiple products across therapeutic categories, each contributing steady revenues without concentration risk. The decision made that day would define FDC's trajectory for the next decade.

FDC chose portfolio breadth over blockbuster depth, but with a twist: they would build therapeutic franchises where they could claim leadership positions. The strategy was to identify therapeutic areas with specific Indian disease burdens, develop comprehensive product lines, and create prescription habits among doctors. It was a middle path between scattered opportunism and concentrated bets.

The anti-infective franchise became the cornerstone of this strategy. By 2005, infectious diseases still accounted for over 30% of India's disease burden. FDC's antibiotic portfolio was carefully constructed: Zifi (Cefixime) for respiratory infections, Zathrin (Azithromycin) for atypical pathogens, Zipod (Cefpodoxime) for resistant strains. Each product was positioned for specific indications, creating a "ladder" that doctors could climb based on infection severity.

The brilliance lay not just in product selection but in execution. FDC's medical representatives were trained not as salespeople but as therapeutic specialists. They could discuss antibiotic resistance patterns, recommend combination therapies, and provide clinical evidence for treatment protocols. This consultative approach resonated with doctors increasingly concerned about antibiotic resistance and treatment failures.

The gastrointestinal portfolio followed a similar philosophy but with different dynamics. While Electral remained the flagship, FDC recognized that gastrointestinal health extended beyond rehydration. They developed products for the entire digestive spectrum: antacids for hyperacidity, proton pump inhibitors for ulcers, probiotics for gut health, enzymes for digestion. The strategy was to become the "GI specialist" in doctors' minds—when they thought digestive health, they thought FDC.

The vitamin and mineral segment presented unique challenges. This category straddled the line between prescription pharmaceuticals and consumer health products. FDC's approach was distinctive: they focused on medically-relevant nutritional deficiencies rather than lifestyle supplements. Vitcofol, their vitamin C and folic acid combination, was positioned for pregnancy and post-illness recovery. Pyrimon, an iron supplement, targeted India's massive anemia burden. These weren't "wellness" products but medical interventions for documented deficiencies.

The ophthalmology franchise, FDC's oldest specialty, underwent significant evolution. As India's diabetes epidemic drove increasing rates of diabetic retinopathy and glaucoma, FDC developed specialized formulations for these conditions. They introduced combination eye drops that improved patient compliance, preservative-free formulations for sensitive eyes, and sustained-release preparations that reduced dosing frequency. The technical complexity of these products created barriers to entry that protected margins.

But the most interesting development was FDC's entry into nutraceuticals with Enerzal. This represented a strategic departure—moving from treatment to prevention, from prescription to consumer marketing. Enerzal was positioned uniquely: not as a sports drink competing with Gatorade, but as a "health drink" for India's working class. Construction workers, farmers, and factory employees who lost electrolytes through sweat became the target market. The product leveraged Electral's credibility while accessing new consumption occasions.

The R&D strategy during this period deserves special attention. FDC allocated 2-2.5% of revenues to R&D—modest by global standards but significant for an Indian company focused on generics. The research wasn't aimed at new molecular entities but at what FDC called "value-added generics"—improved formulations of existing drugs. They developed taste-masked pediatric formulations, extended-release versions for better compliance, and fixed-dose combinations that simplified treatment regimens.

The fixed-dose combination (FDC) strategy was particularly important in the Indian context. Indian patients often struggled with treatment compliance when prescribed multiple medications. FDC (the company) developed FDCs (the products) that combined complementary drugs in single tablets. Their antibiotic-plus-probiotic combinations reduced gastrointestinal side effects. Their vitamin-mineral complexes addressed multiple deficiencies simultaneously. While these combinations faced regulatory scrutiny in developed markets, they solved real problems in India's resource-constrained healthcare system.

Price control regulations under the National List of Essential Medicines (NLEM) created both challenges and opportunities. When key products like certain antibiotics came under price control, margins compressed dramatically. FDC responded by reformulating products to escape price controls while maintaining therapeutic efficacy. They also shifted focus to non-NLEM products where pricing freedom remained. This regulatory arbitrage required constant vigilance and product portfolio adjustment.

The distribution strategy evolved to match portfolio expansion. FDC built one of India's most extensive pharmaceutical distribution networks—reaching over 60,000 pharmacies directly and another 200,000 through distributors. But coverage alone wasn't enough. FDC pioneered "prescription tracking" systems that monitored which doctors prescribed which products, allowing targeted medical representative visits and customized promotional strategies.

The marketing approach balanced medical credibility with brand building. Continuing medical education programs positioned FDC as a knowledge partner for doctors. Patient education initiatives, particularly around antibiotic resistance and nutritional deficiencies, created disease awareness that drove prescription demand. Trade marketing programs ensured pharmacist recommendations when prescription brands weren't specified.

By 2010, the portfolio strategy's results were evident. Anti-infectives contributed 42% of revenues, providing stable cash flows from a therapeutic area with consistent demand. Gastrointestinal products, anchored by Electral, contributed 24%, combining legacy strength with new innovations. The diversification reduced dependence on any single product while maintaining focus on core therapeutic areas.

The financial performance validated the strategy. Revenues grew at 12% CAGR through the decade, reaching ₹1,500 crores by 2010. EBITDA margins remained healthy at 18-20%, superior to pure generic players but below innovator companies. The return on capital employed exceeded 20%, indicating efficient asset utilization despite extensive manufacturing infrastructure.

Yet challenges were emerging. The portfolio breadth that provided stability also diluted focus. Marketing 200+ products required extensive field force and promotional spending. Some therapeutic areas, despite years of investment, failed to achieve leadership positions. The question arose: was FDC spreading itself too thin in pursuit of diversification?

The competitive landscape was also intensifying. Multinational companies, previously focused on patented products, were entering the branded generics space. Indian companies were consolidating, creating larger entities with greater resources. The traditional relationship-based medical marketing was giving way to data-driven approaches that required technological investments.

As the 2010s began, FDC faced strategic choices. Should it continue the portfolio approach or focus on fewer, larger brands? Should it pursue acquisitions to gain scale or remain focused on organic growth? Should it increase R&D investment to develop differentiated products or optimize the existing portfolio for profitability? These decisions would determine whether FDC could maintain its distinctive position in an increasingly competitive market.

VII. Modern Era: Challenges & Transformation (2010s-Present)

The morning of March 15, 2018, began like any other at FDC's Mumbai headquarters. The stock market had opened steady, orders were flowing normally, and the executive team was reviewing quarterly targets. Then the email arrived. The US FDA had issued observations following their inspection of FDC's Roha facility—the same plant that had been approved nine times consecutively since 1985. The observations weren't catastrophic, but they signaled something deeper: the world's pharmaceutical quality standards had evolved faster than FDC had adapted.

FDC reports Q4FY25 revenue Rs.492cr (+6.5%), FY25 Rs.2108cr (+8.5%), US export down due to regulatory issues. This single line in a recent earnings report encapsulates the challenge that has defined FDC's modern era. After decades of steady growth, the company found itself at an inflection point where past strengths—stable products, established relationships, proven quality—were no longer sufficient for future success.

The regulatory challenges emerged gradually. FDA inspection standards had become increasingly stringent post-2015, following high-profile quality failures at other Indian pharmaceutical companies. Details of FDC's U.S. FDA Inspections show a pattern of "Voluntary Action Indicated" outcomes—not outright failures, but clear signals that improvements were needed. The issues weren't about product quality per se but about documentation, data integrity, and quality systems that hadn't kept pace with evolving expectations.

The financial impact was immediate and material. US exports, which had grown steadily for three decades, began declining. International customers, wary of supply disruptions, diversified their vendor base. The Roha facility, once FDC's crown jewel of regulatory compliance, became a liability requiring significant remediation investment. Management estimated that addressing FDA observations and upgrading quality systems would require over ₹100 crores—a massive commitment for a company generating ₹2,100 crores in annual revenue.

But regulatory challenges were just one dimension of FDC's modern struggles. The domestic market, long FDC's fortress, was undergoing fundamental transformation. The company has delivered a poor sales growth of 9.46% over past five years. Company has a low return on equity of 12.0% over last 3 years. These metrics revealed a deeper malaise: FDC's traditional playbook was losing effectiveness.

The competitive landscape had shifted dramatically. Multinational pharmaceutical companies, previously focused on patented drugs, aggressively entered the branded generics space following patent cliffs. Companies like Abbott and Pfizer leveraged global R&D capabilities to introduce differentiated formulations that commanded premium pricing. Meanwhile, domestic peers like Mankind Pharma and Alkem grew rapidly through aggressive field force expansion and doctor engagement programs that FDC couldn't match without diluting margins.

Digital disruption added another layer of complexity. E-pharmacies like PharmEasy and 1mg began disintermediating traditional distribution channels. Doctors increasingly relied on digital tools for prescribing decisions, diminishing the effectiveness of traditional medical representative visits. Patients became more informed, often requesting specific brands based on online research rather than accepting pharmacist recommendations where FDC's relationships had historically driven sales.

The COVID-19 pandemic initially appeared beneficial. Demand for vitamins, immunity boosters, and respiratory products surged. FDC's Zifi and other anti-infectives saw increased prescription as prophylactic treatments. But the pandemic also accelerated structural changes that challenged FDC's model. Telemedicine adoption reduced in-person doctor visits where medical representatives traditionally influenced prescribing. Supply chain disruptions highlighted the vulnerability of FDC's concentrated manufacturing footprint. Most critically, the pandemic-driven focus on innovation and speed exposed FDC's relatively modest R&D capabilities.

Operating income during the year rose 14.6% on a year-on-year (YoY) basis. The company's operating profit decreased by 23.6% YoY during the fiscal. Operating profit margins witnessed a fall and stood at 16.6% in FY22 as against 24.9% in FY21. Net profit for the year declined by 28.2% YoY. Net profit margins during the year declined from 22.6% in FY21 to 14.1% in FY22. These FY2022 numbers told a stark story: revenue growth couldn't compensate for margin compression. Raw material costs surged due to supply chain disruptions and China's environmental crackdowns on API manufacturing. Price controls under NLEM expanded, covering more of FDC's portfolio. Marketing costs escalated as competition intensified.

The family ownership structure, long a source of stability, became a constraint in this environment. Promoter Holding: 69.7% indicated continued family control, but also limited FDC's strategic flexibility. Professional managers advocated for bold moves—acquisitions to gain scale, partnerships for innovation, aggressive R&D investments. But the promoter family, cognizant of preserving legacy and maintaining control, preferred organic growth and financial prudence. This conservatism, while protecting downside, also limited upside potential.

Management attempted various strategic initiatives. They launched differentiated products in niche segments—pediatric formulations, geriatric supplements, combination therapies for lifestyle diseases. They invested in field force productivity tools, deploying tablets and CRM systems to improve medical representative effectiveness. They explored international markets beyond the US, targeting Africa and Southeast Asia where regulatory requirements were less stringent.

Yet these initiatives felt incremental rather than transformational. While peers like Cipla ventured into biosimilars and complex generics, FDC remained focused on conventional formulations. While Sun Pharma built global scale through acquisitions, FDC grew organically. While Dr. Reddy's invested 8-10% of revenues in R&D, FDC prioritizes research and development, allocating 2-2.5% of its revenue to R&D expenses—respectable but insufficient for breakthrough innovation.

The financial metrics reflected this strategic stasis. Over the past 5 years, the revenue of FDC has grown at a CAGR of 9.4%. Over the past 5 years, FDC net profit has grown at a CAGR of 5.6%. In an industry where leaders grew at 15-20% annually, FDC's single-digit growth meant steady market share loss. The company wasn't failing—it was slowly becoming irrelevant.

The board recognized the need for transformation but struggled with execution. A new CEO was appointed in 2019, bringing experience from multinational pharmaceutical companies. Digital transformation initiatives were launched, including e-detailing platforms and data analytics capabilities. The R&D focus shifted toward complex generics and specialty products with higher entry barriers. Manufacturing excellence programs aimed to address regulatory concerns while improving efficiency.

However, cultural change proved challenging. The organization, accustomed to relationship-based business and gradual evolution, struggled with the pace of change required. Senior managers, many with decades of tenure, resisted new approaches that challenged traditional methods. The field force, comfortable with established doctor relationships, was slow to adopt digital tools. The R&D team, historically focused on incremental formulation improvements, lacked capabilities for complex product development.

By 2023, FDC found itself at a crossroads. The domestic market remained stable but growth was decelerating. US export down due to regulatory issues continued to impact international revenues. New product launches generated modest incremental sales but no blockbusters emerged. The stock price reflected investor skepticism, trading at valuations below industry averages despite the company's strong brand portfolio and manufacturing capabilities.

The path forward required difficult choices. Should FDC double down on its core therapeutic areas or diversify into new segments? Should it pursue acquisitions to gain scale or remain focused on organic growth? Should it increase R&D spending to develop differentiated products or optimize the existing portfolio for profitability? Should it consider strategic partnerships that might dilute family control but accelerate transformation?

As 2024 progressed, some green shoots emerged. Regulatory remediation efforts showed progress, with recent FDA inspections yielding better outcomes. Digital initiatives began showing results, with e-detailing improving field force productivity. Cost optimization programs helped protect margins despite pricing pressures. The domestic business, while growing slowly, maintained its market position in key therapeutic areas.

Yet fundamental questions remained unanswered. In an industry increasingly dominated by scale players and innovation leaders, what was FDC's sustainable differentiator? How could a company with proud heritage but modest resources compete against global giants and aggressive domestic rivals? Could incremental evolution suffice, or was revolutionary transformation necessary?

The modern era had taught FDC harsh lessons. Quality standards that were acceptable yesterday became inadequate today. Business models that generated decades of success became obstacles to future growth. Capabilities that differentiated in the past became table stakes for participation. The company that had successfully navigated independence, built manufacturing excellence, created category-defining brands, and achieved global regulatory approvals now faced its greatest challenge: remaining relevant in a rapidly evolving pharmaceutical landscape.

VIII. Business Model & Competitive Analysis

The conference room walls at FDC's strategy session in 2019 were covered with charts, matrices, and competitive landscapes. One particular slide commanded attention: it showed FDC's position in what consultants call the "strategic sweet spot"—not large enough to compete on scale, not innovative enough to command premium pricing, but somehow still profitable and resilient. The executive team stared at this paradox, trying to decode why FDC's seemingly disadvantaged position had endured for decades while theoretically stronger companies had faltered.

FDC's business model defies conventional pharmaceutical industry wisdom. Anti-infective medicines contribute 42% of revenues, followed by gastro intestinal 24%, vitamins/ minerals 7%, ophthalmology 6%, cardiac 7%, dermatology 4% and others 11%. This portfolio composition reveals a deliberate strategy: focus on acute therapies with predictable demand rather than chronic segments with higher patient lifetime value but intense competition. It's a choice that prioritizes stability over growth, cash generation over market expansion.

The integrated manufacturing model—APIs plus formulations—provides FDC with strategic flexibility that pure-play formulators lack. When API prices spike due to Chinese supply disruptions or regulatory crackdowns, FDC's backward integration provides a buffer. When formulation markets become oversupplied, API exports to other manufacturers provide alternative revenue streams. This vertical integration isn't just about cost control; it's about risk mitigation in an industry where supply chain disruptions can destroy profitability overnight.

Consider the competitive dynamics in anti-infectives, FDC's largest segment. The market is fragmented, with over 300 brands competing across various molecules. Theoretically, this should destroy profitability. Yet FDC maintains healthy margins through micro-segmentation. Zifi isn't just another Cefixime brand; it's positioned specifically for respiratory infections in pediatric populations. Zathrin targets atypical pneumonia in adults. Zipod addresses resistant urinary tract infections. Each product occupies a specific niche, creating multiple small moats rather than one large fortress.

The geographic strategy is equally nuanced. While peers chase the US generics market with its binary outcomes—either you win big on first-to-file opportunities or lose money on commoditized products—FDC focuses on semi-regulated markets. 90% of the apis, manufactured at the Roha facility, are being exported to the USA, Canada, Japan, Malaysia, Europe and the Middle East countries for APIs, but formulation exports target different geographies where brand equity matters more than pure price competition.

This approach reflects a deeper understanding of pharmaceutical market structure. In the US, generics are pure commodities where lowest cost wins. In India, brands matter because doctors prescribe by brand name, not molecule. In emerging markets like Africa and Southeast Asia, reliability and availability trump innovation. FDC has chosen to compete where its strengths—brand building, relationship management, supply reliability—matter most.

The R&D allocation strategy further illuminates FDC's model. While spending only 2-2.5% of revenues on R&D appears inadequate compared to innovator companies spending 15-20%, FDC's R&D productivity metrics tell a different story. The company doesn't pursue new molecular entities with 10% success probability and billion-dollar development costs. Instead, it focuses on reformulations, taste-masking, stability improvements—incremental innovations with 80% success probability and modest investment requirements. The return on R&D investment, measured as new product revenue divided by R&D spend, actually exceeds many companies with higher absolute R&D budgets.

The distribution strategy leverages India's unique pharmaceutical market structure. Unlike developed markets where pharmacy chains dominate, India has over 800,000 independent pharmacies. FDC's field force of 2,000 medical representatives doesn't just detail doctors; they manage relationships across this fragmented ecosystem. Each representative covers 200-250 doctors and 50-60 pharmacies, creating dense relationship networks that new entrants struggle to replicate.

The competitive positioning becomes clearer when compared to specific rivals. Against multinationals like GSK or Pfizer, FDC can't match R&D capabilities or global scale. But FDC's lower cost structure and local market knowledge allow it to profitably serve segments that multinationals find unattractive. Against domestic giants like Sun Pharma or Cipla, FDC lacks scale and acquisition firepower. But FDC's focused portfolio and specialized capabilities in specific therapeutic areas create defensive positions that are expensive to attack.

The most instructive comparison is with companies that chose different paths from similar starting points. Wockhardt, once a peer, pursued aggressive international expansion through acquisitions, eventually facing financial distress. Panacea Biotec ventured into vaccines and biotechnology, struggling with development costs and regulatory challenges. Ind-Swift Laboratories diversified across multiple businesses, losing focus and eventually facing bankruptcy. FDC's conservative approach, while limiting growth, avoided these existential risks.

The financial architecture supporting this model is revealing. Company is almost debt free, providing flexibility to weather downturns without financial distress. Working capital management is conservative, with higher inventory levels ensuring supply continuity even during disruptions. Capital allocation prioritizes maintenance over growth, with steady dividends rewarding patient shareholders rather than aggressive reinvestment pursuing uncertain returns.

The pricing strategy navigates India's complex regulatory environment skillfully. When products come under price control, FDC introduces modified versions—new combinations, improved delivery systems, pediatric formulations—that escape controls while serving genuine medical needs. This isn't regulatory arbitrage; it's adaptive innovation that balances affordability with sustainability.

The organizational capabilities that support this model are often overlooked. FDC has developed deep expertise in specific areas: fermentation technology for antibiotics, taste-masking for pediatric formulations, stability in tropical conditions for export markets. These capabilities aren't revolutionary, but they're difficult to replicate without years of experience and trial-and-error learning.

The customer relationship model differs markedly from transaction-oriented competitors. FDC's medical representatives often cover the same territories for years, building trust with doctors through consistent presence rather than aggressive promotion. The company sponsors continuing medical education programs that provide genuine educational value rather than disguised marketing. This relationship depth creates switching costs that price competition alone cannot overcome.

Yet this model faces structural challenges. The acute therapy focus means FDC misses the recurring revenue streams from chronic disease management—diabetes, hypertension, mental health—that drive growth for industry leaders. The domestic market concentration exposes FDC to Indian regulatory changes and economic cycles. The limited R&D investment constrains ability to develop truly differentiated products that command premium pricing.

The competitive threats are evolving. Digital health platforms are creating direct-to-consumer channels that bypass traditional doctor-pharmacy relationships. Artificial intelligence is enabling personalized medicine that commoditizes standard treatments. Global pharmaceutical companies are building India-specific strategies that combine international R&D with local market knowledge. Chinese and Bangladeshi manufacturers are entering India with cost structures that even FDC cannot match.

The strategic options facing FDC reflect these realities. The company could pursue "string of pearls" acquisitions—buying small, specialized companies that fit its therapeutic focus. It could build digital capabilities to engage directly with patients, reducing dependence on traditional channels. It could partner with international companies, providing local market access in exchange for product portfolios. Or it could double down on its current model, accepting slower growth but maintaining profitability and independence.

The business model analysis reveals an uncomfortable truth: FDC's strategy is perfectly optimized for a market structure that is rapidly disappearing. The fragmented, relationship-driven, brand-conscious Indian pharmaceutical market that FDC mastered is evolving toward consolidation, digitization, and commoditization. The company's integrated manufacturing model, therapeutic specialization, and conservative financial approach generated decades of success but may constrain future opportunities.

What emerges is a portrait of a company caught between eras. FDC is too successful to require radical transformation but not dynamic enough to capture emerging opportunities. Its business model generates sufficient returns to satisfy current shareholders but insufficient growth to attract new investors. Its competitive position is defensible against current threats but vulnerable to discontinuous change.

The fundamental question isn't whether FDC's business model is good or bad—it's whether it's fit for purpose in the evolving pharmaceutical landscape. The answer, frustratingly, is both yes and no. Yes, because the model continues generating profits, serving patients, and creating value. No, because the model's inherent constraints prevent FDC from capturing the exponential opportunities that industry transformation presents. This ambiguity—profitable but not growing, stable but not exciting, successful but not thriving—defines FDC's strategic challenge and competitive reality.

IX. Playbook: Lessons from FDC's Journey

Building Brands in Commoditized Categories: The Electral Masterclass

Every MBA program teaches that commoditized products can't sustain brand premiums. Electral proves them wrong. The product is literally just salts and glucose—a formula published by the WHO, manufactured by dozens of companies, with zero patent protection. Yet Electral commands 40% market share and premium pricing in a category where the cheapest product should theoretically win. How did FDC achieve this?

The answer lies in understanding that brands aren't built on products but on problems solved. FDC recognized that mothers buying ORS weren't purchasing a medical product; they were seeking reassurance that their child would recover. The brand promise wasn't about sodium-glucose cotransport or osmolality—it was about trust in a moment of crisis. Every element of Electral's strategy reinforced this trust: the consistent orange packaging that stood out on pharmacy shelves, the single-dose sachets that eliminated measurement anxiety, the simple instructions that worked across literacy levels.

The distribution strategy was equally crucial. FDC didn't just sell Electral; they embedded it in India's healthcare infrastructure. By working with government programs, training rural health workers, and educating traditional healers, FDC made Electral part of the standard treatment protocol before formal protocols even existed. When a mother in rural Bihar asks for diarrhea medicine, the pharmacy doesn't stock multiple ORS brands—they stock Electral, because that's what the local health worker recommends, what the government supplies, and what neighbors have used successfully.

The lesson extends beyond pharmaceuticals: in commoditized categories, win by defining the category itself. Don't compete on product features; compete on problem definition. Make your brand synonymous with the solution, not just a solution.

First-Mover Advantages in Regulated Manufacturing

FDC's 1985 FDA approval, among the first for an Indian company, created advantages that persisted for decades. But the real lesson isn't about being first—it's about what you do with that position. FDC used its early FDA approval not just to access US markets but to transform its entire organization. The quality systems required for FDA compliance became the standard for all manufacturing. The documentation discipline spread from production to R&D to commercial operations. The regulatory expertise developed for US filings was leveraged for European, Japanese, and other regulated markets.

This created a virtuous cycle. Early FDA approval attracted international partners who needed reliable Indian manufacturers. These partnerships brought technology transfer and knowledge exchange that further enhanced capabilities. Enhanced capabilities enabled more complex products that commanded better margins. Better margins funded continued investment in quality and compliance. By the time competitors achieved FDA approval, FDC had moved beyond mere compliance to excellence.

The playbook applies broadly: in regulated industries, early compliance isn't just about market access—it's about organizational transformation. The discipline required for regulatory approval, if properly leveraged, creates capabilities that compound over time. The key is viewing regulation not as a cost but as a forcing function for excellence.

Managing Multi-Generational Family Businesses

FDC's journey through three generations of family control offers lessons in longevity. The company avoided both extremes that destroy family businesses: neither did patriarchs cling to control beyond their effectiveness, nor did successors revolutionize away from core strengths. Each generation adapted to its era while preserving essential DNA. The founder built the foundation through import and early manufacturing. The second generation achieved global standards and public listing. The third generation navigates digital transformation and market evolution.

The governance structure balanced family control with professional management. Independent directors brought external perspectives without threatening family ownership. Professional CEOs executed strategy while family members focused on long-term vision. The 69.7% promoter holding provided stability while public shareholding ensured accountability. This structure avoided both the stagnation of complete family control and the short-termism of dispersed ownership.

The succession planning was deliberate, not accidental. Next-generation family members gained international education and external experience before joining FDC. They started in operational roles, proving competence before assuming leadership. The transition periods were long, allowing knowledge transfer and relationship continuity. This patient approach contrasted with dramatic succession battles that destroyed many Indian family businesses.

Balancing Innovation with Price-Controlled Markets

Operating in India's price-controlled pharmaceutical market requires a different innovation paradigm. FDC couldn't pursue the standard model of high R&D investment recouped through premium pricing. Instead, they developed what might be called "appropriate innovation"—improvements that mattered to Indian patients and were economically viable under price controls.

The innovation portfolio focused on practical problems: making medicines palatable for children, ensuring stability without refrigeration, creating combinations that improved compliance. These weren't breakthrough innovations that won scientific awards, but they solved real problems for millions of patients. The R&D investment of 2-2.5% of revenues seems modest, but the return on this investment—measured by successful product launches and market acceptance—exceeded companies spending much more.

The regulatory arbitrage was sophisticated. When products came under price control, FDC introduced modified versions that escaped controls while providing genuine medical benefits. A simple antibiotic became a taste-masked pediatric formulation. A basic vitamin became a sustained-release preparation. These weren't cynical workarounds but legitimate innovations that balanced affordability with sustainability.

The Importance of Backward Integration in Pharma

FDC's decision to backward integrate into APIs in the 1970s, when most Indian companies focused on formulations, created enduring advantages. The benefits extended beyond cost control. API manufacturing provided supply security when international sources were unreliable. It enabled quality control from raw material to finished product. It created regulatory assets—FDA-approved API facilities—that opened international markets. It generated technical capabilities in fermentation and chemical synthesis that differentiated FDC's formulations.

The integration strategy was selective, not comprehensive. FDC didn't attempt to manufacture all APIs but focused on strategic molecules where they could achieve competitive advantage. They specialized in fermentation-based antibiotics where their expertise created barriers to entry. They avoided commodity APIs where Chinese manufacturers had insurmountable cost advantages. This selective integration balanced control with capital efficiency.

The lesson transcends pharmaceuticals: backward integration makes sense when it provides strategic control, not just cost reduction. The key is identifying critical dependencies where supply uncertainty or quality variability can destroy value, then building capabilities that create sustainable advantage rather than just replacing external suppliers.

Long-term Thinking in Cyclical Industries

Pharmaceutical markets exhibit multiple overlapping cycles: regulatory changes, patent expirations, disease patterns, economic conditions. FDC's steady performance through these cycles reflects a long-term orientation that many competitors lack. The company didn't chase every opportunity during boom periods nor panic during downturns. This patience allowed FDC to avoid both the overexpansion that destroyed aggressive competitors and the underinvestment that marginalized conservative ones.

The capital allocation reflected this long-term thinking. During the 2000s boom, when easy credit fueled acquisition sprees, FDC remained disciplined. While competitors leveraged balance sheets to buy growth, FDC maintained financial flexibility. When the financial crisis hit and overleveraged companies faced distress, FDC could operate normally and even opportunistically expand. The debt-free balance sheet wasn't just financial conservatism—it was strategic optionality.

The product portfolio strategy showed similar patience. FDC didn't abandon therapeutic areas during temporary downturns or rush into hot segments during bubbles. They maintained presence in anti-infectives even as industry attention shifted to lifestyle diseases. They continued investing in ORS despite low margins. This consistency created cumulative advantages—brand equity, distribution relationships, technical expertise—that competitors couldn't quickly replicate.

The Meta-Lesson: Strategic Coherence

The overarching lesson from FDC's playbook is strategic coherence—the alignment of multiple decisions over time toward a consistent positioning. FDC didn't excel at any single dimension—they weren't the most innovative, largest, or fastest-growing. But every decision reinforced a consistent strategy: serving India's mass market health needs through specialized capabilities and trusted brands.

This coherence created what strategists call "complementarities"—where each element reinforces others. The therapeutic focus on acute care aligned with the brand-building capability in OTC-like categories. The backward integration supported the quality reputation required for regulated market exports. The conservative financial approach enabled the patient brand-building that created sustainable differentiation. The family ownership provided the long-term orientation that justified capability investments.

The result is a strategy that's difficult to attack piecemeal. Competitors can match individual elements—anyone can manufacture ORS or get FDA approval or build field force. But replicating the entire system—the interconnected capabilities, relationships, and reputation built over decades—requires commitments that few companies can sustain.

This strategic coherence also explains FDC's limitations. The same consistency that created defensibility also constrained adaptability. The capabilities optimized for serving India's mass market made it difficult to compete in innovation-driven segments. The conservative financial approach that ensured survival prevented transformational growth. The therapeutic focus that created depth sacrificed breadth. FDC's strategy is coherent but also constraining—a trade-off that every company must navigate.

X. Bear vs. Bull Case & Future Outlook

The Bear Case: Structural Headwinds Intensifying

The bear thesis on FDC starts with a simple observation: Company has a low return on equity of 12.0% over last 3 years—in an industry where leaders generate 20-25% ROE, this signals fundamental competitive disadvantage. The mathematics are unforgiving. With ROE barely exceeding India's risk-free rate, FDC essentially destroys value for equity holders after adjusting for risk. This isn't a temporary problem but a structural reality reflecting FDC's subscale position in an increasingly winner-take-all industry.

The regulatory overhang looms large. US export down due to regulatory issues isn't just about current revenue loss—it's about credibility destruction. FDA issues, once resolved, leave lasting scars. Customers who found alternative suppliers rarely return completely. The investments required to upgrade facilities to current standards generate minimal returns. More troublingly, the regulatory challenges suggest organizational capabilities haven't kept pace with global standards, raising questions about future competitiveness even in domestic markets.

The domestic market dynamics are equally concerning. Price controls under NLEM cover an expanding portion of FDC's portfolio, with government policies increasingly favoring affordability over innovation. The Jan Aushadhi program, offering generic medicines at 50-90% discounts, directly threatens branded generics like FDC's. As insurance coverage expands and reimbursement shifts toward lowest-cost alternatives, FDC's brand premiums become unsustainable.

The acute therapy focus—42% revenues from anti-infectives—faces structural decline. As India's disease burden shifts from infectious to chronic diseases, FDC's portfolio becomes increasingly misaligned with market growth. Anti-infective consumption is declining with improved sanitation and healthcare access. Meanwhile, diabetes, cardiovascular, and oncology segments where FDC has minimal presence are exploding. Repositioning would require massive R&D investments that FDC's conservative approach precludes.

Competition is intensifying from every direction. Global giants like Abbott and Pfizer are building India-specific strategies that combine international innovation with local execution. Chinese manufacturers offer APIs and formulations at prices FDC cannot match. Digital-native companies are disrupting distribution channels and patient engagement models. Even traditional Indian competitors are consolidating, creating scale advantages in procurement, marketing, and R&D that FDC cannot overcome.

The innovation deficit is perhaps most damaging. With R&D spending at 2-2.5% of revenues versus 8-10% for leaders, FDC cannot develop differentiated products that escape commoditization. The pipeline consists primarily of line extensions and combinations that provide temporary relief from price pressure but no sustainable advantage. Without breakthrough innovation, FDC is condemned to competing on execution in markets where execution is increasingly table stakes.

The family ownership structure, while providing stability, limits strategic flexibility. The 69.7% promoter holding prevents transformational M&A that requires equity dilution. Professional managers capable of driving change are reluctant to join companies where family members occupy key positions. The conservative culture that served well in stable times becomes a liability when disruption requires bold moves.

Digital disruption threatens FDC's traditional strengths. E-pharmacies bypass the retail relationships FDC cultivated over decades. Telemedicine reduces the importance of medical representative detailing. AI-driven diagnosis and treatment protocols commoditize prescription decisions. Digital therapeutic alternatives reduce demand for traditional pharmaceuticals. FDC's minimal digital capabilities leave it vulnerable to obsolescence.

The financial trajectory is concerning. The company has delivered a poor sales growth of 9.46% over past five years while industry leaders grew at 15-20%. This isn't cyclical underperformance but steady market share loss. With limited pricing power, modest volume growth, and no breakthrough products, where does future growth come from? The answer, bearishly, is nowhere—FDC faces inevitable decline into irrelevance.

The Bull Case: Hidden Strengths and Transformation Potential

The bull thesis begins with valuation. At current levels, FDC trades at significant discount to peers despite superior balance sheet strength and brand portfolio value. Company is almost debt free provides flexibility that leveraged competitors lack. The market is pricing FDC for terminal decline, creating asymmetric upside if execution merely stabilizes.

The brand portfolio is undervalued by conventional metrics. Electral alone, with 40% market share in ORS, could be worth ₹2,000-3,000 crores to a strategic acquirer—nearly 40% of FDC's current market capitalization. Zifi, Enerzal, and other established brands have sustained pricing power despite generic competition. These aren't just products but medical habits embedded in prescription behavior over generations.

The regulatory issues, while painful, are addressable. FDA remediation is progressing, with recent inspections showing improvement. Once resolved, FDC can resume US exports with enhanced quality systems that differentiate from competitors. The investments in compliance, while dilutive short-term, create long-term competitive advantages as regulatory standards continue rising globally.

The domestic market opportunity remains massive. India's pharmaceutical market will grow from $50 billion to $130 billion by 2030, driven by expanding healthcare access, insurance coverage, and rising incomes. Even maintaining market share in this expanding pie generates substantial absolute growth. FDC's distribution reach—60,000 pharmacies directly—provides infrastructure that new entrants cannot easily replicate.

The acute therapy focus, while unfashionable, offers defensive characteristics. Infectious diseases won't disappear—climate change, urbanization, and antimicrobial resistance ensure continued demand for anti-infectives. The COVID-19 pandemic reminded everyone that infectious disease preparedness remains critical. FDC's expertise in antibiotics and antivirals positions it well for future pandemics or biodefense requirements.

The transformation potential is real if management embraces change. The debt-free balance sheet enables transformational acquisitions without financial distress. The established brand equity provides a platform for adjacent category expansion. The manufacturing infrastructure, once upgraded, can support contract manufacturing for global partners. The regulatory expertise, properly leveraged, can enable complex generic development.

Emerging market expansion offers underappreciated opportunity. Africa's pharmaceutical market is growing at 20% annually, with demand for quality affordable medicines exceeding supply. Southeast Asian markets offer similar dynamics. FDC's products—designed for tropical stability and affordability—are perfectly suited for these markets. The regulatory requirements are less stringent than developed markets, playing to FDC's capabilities.

The ESG tailwinds are strengthening. FDC's focus on essential medicines, affordable pricing, and domestic manufacturing aligns with stakeholder capitalism trends. Government policies increasingly favor local manufacturers for supply security. The "China plus one" strategy of global pharmaceutical companies creates partnership opportunities. FDC's established infrastructure and compliance history position it as a reliable partner.

Healthcare infrastructure expansion in India creates new opportunities. The government's push for health and wellness centers, expansion of Ayushman Bharat insurance coverage, and focus on preventive care all expand pharmaceutical consumption. FDC's portfolio of essential medicines and preventive products like vitamins and ORS are well-positioned to benefit from these initiatives.