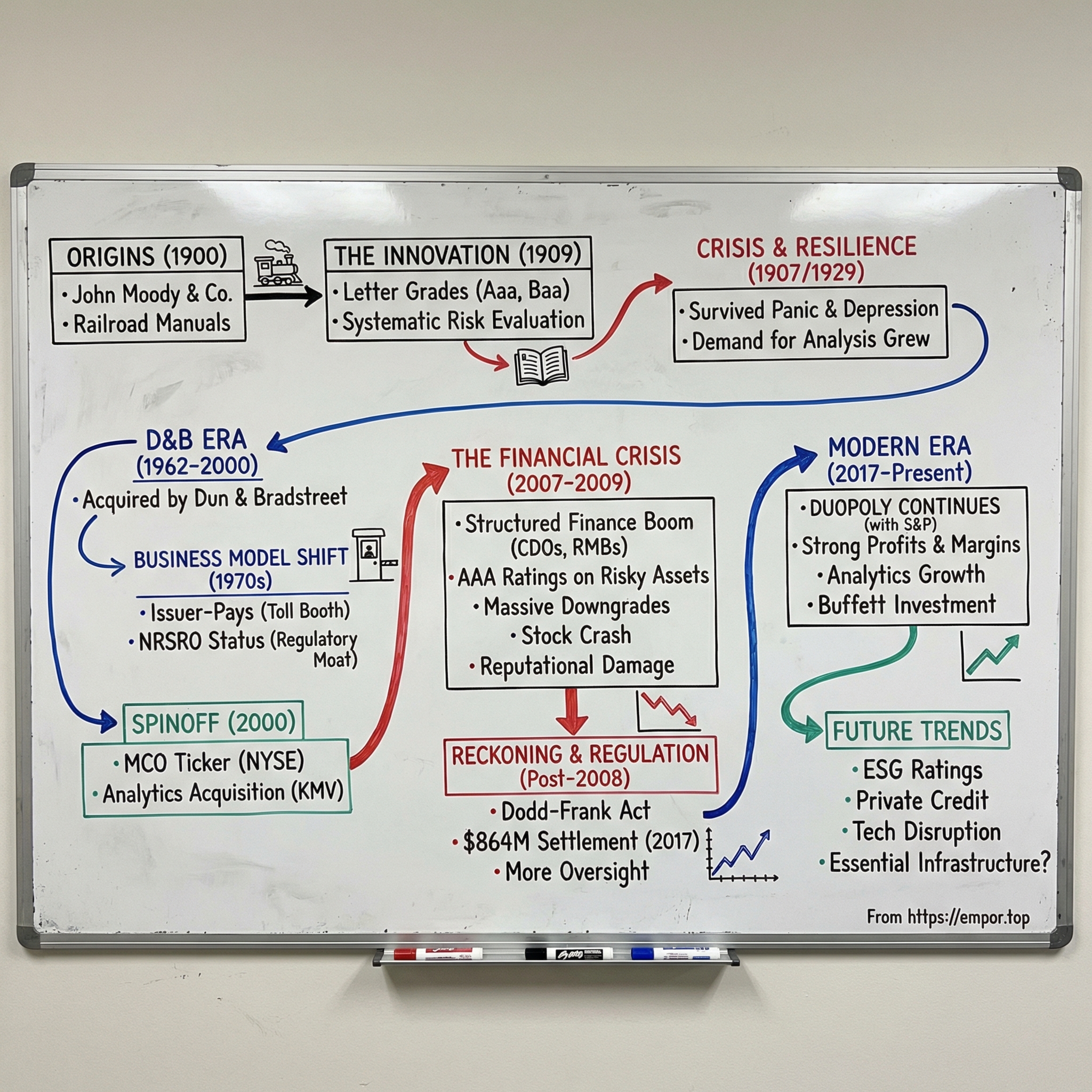

Moody's Corporation: The Power Behind the Rating

I. Introduction & Opening

The year is 2008. Lehman Brothers has just collapsed. AIG teeters on the brink. And in the halls of Congress, a question reverberates: How did mortgage securities stamped with triple-A ratings—the gold standard of safety—turn into toxic waste that nearly destroyed the global financial system? At the center of this storm sits Moody's Corporation, a company whose blessing on complex financial instruments helped fuel the worst financial crisis since the Great Depression.

Here's the paradox that defines modern finance: A business that began in 1900 as a publisher of railroad statistics, printing physical manuals that investors would thumb through in wood-paneled libraries, evolved into one of the most powerful arbiters of global capital. Today, Moody's commands a market capitalization north of $80 billion. Its analysts can move markets with a single rating change—a downgrade can add millions to a country's borrowing costs overnight, while an upgrade can unlock billions in fresh capital.

The story of Moody's is really three stories intertwined. First, it's the tale of John Moody, a financial journalist who invented the credit rating itself—transforming how investors evaluate risk. Second, it's a case study in market structure—how a handful of companies came to dominate the business of judging creditworthiness, creating what critics call a "licensed oligopoly." And third, it's a meditation on trust, reputation, and resilience—how a company can survive having its credibility shattered and rebuild into something even more powerful.

What follows is the journey from those railroad manuals to rating sovereign nations, from charging investors for insights to having borrowers pay for the privilege of being judged, from near-destruction in 2008 to becoming Warren Buffett's third-largest holding. This is how Moody's built, nearly lost, and ultimately reinforced its position as a toll booth on the global capital markets.

II. The John Moody Story & Early Origins (1900-1962)

Picture Jersey City, 1868. John Moody is born—not into wealth or privilege, but into an era when American capitalism was still finding its shape. He was considered an intelligent, primarily self-taught man with a strong sense of right and wrong. This autodidact would go on to invent something so fundamental to modern finance that we can barely imagine capital markets without it: the credit rating.

Moody was an astute businessman who set out to make his mark in the growing investment community of New York. In 1900, at age 32, he spotted a gap in the market that seems obvious in retrospect but was revolutionary at the time. Investors were drowning in data—railroad bonds, industrial securities, mining stocks—but had no systematic way to evaluate them. Moody published his first market assessment, called Moody's Manual of Industrial and Miscellaneous Securities, and established John Moody & Company.

The Manual was filled with data and statistics about the day's trading companies, from financial institutions and government agencies to mining and manufacturing firms. Within a few months of its conception, Moody's Manual had amassed a following and sold out its print run. By 1903 both Moody's Manual and Moody Publishing Company, as the firm was now called, had national reputations.

Success, however, proved fragile. The Panic of 1907—a financial crisis that saw the New York Stock Exchange fall nearly 50% from its peak—devastated Moody along with countless other investors. Financial doom was around the corner; Moody and many of his loyal readers faced ruin after the stock market crash of 1907. Moody was forced to sell his business, including the Manual.

But here's where the story gets interesting. Lesser entrepreneurs might have retreated, licked their wounds, found safer ground. Not John Moody. Within two years, however, Moody was back with a new approach—to provide wary investors with not just information about companies but to go a step further and evaluate their performance and assets. He decided to tackle the burgeoning rail industry and wrote a book entitled Moody's Analyses of Railroad Investments in 1909.

This wasn't just a comeback—it was an innovation that would reshape finance forever. Moody didn't just compile data; he judged it. He assigned letter grades to bonds, creating the now-familiar rating system. Think about the audacity: One man saying "this railroad's bonds are Aaa, but that one's are only Baa." It was subjective, yes, but systematic. And investors, still reeling from 1907, were desperate for exactly this kind of guidance.

His ratings were sought out by investors and Moody responded with a new company, Moody's Investors Service, incorporated in July 1914. The timing was fortuitous—World War I was beginning, capital needs were exploding, and investors needed more guidance than ever. Moody expanded his coverage, rating stocks as well as bonds, and within a decade of his new firm's creation covered the entire U.S. bond market.

The intellectual output matched the business success. Moody also wrote several books for Yale University Press, including The Masters of Capital: A Chronicle of Wall Street and The Railroad Builders: A Chronicle of the Welding of the States, both published in 1919 and reprinted several times. He wasn't just rating bonds; he was documenting the construction of American capitalism itself.

Then came the ultimate test: the 1929 crash and Great Depression. When the stock market crashed in 1929 and ushered in the Great Depression, John Moody did not lose his business like before. He survived and so did his thriving ratings service. Moody continued to write his evaluations and publish his findings despite the collapse of much of the financial community.

This resilience through the Depression cemented Moody's reputation. While banks failed and fortunes evaporated, the need for credit analysis only grew stronger. Investors who had been burned needed Moody's ratings more than ever. The business model had proven itself antifragile—growing stronger under stress.

In February 1958 John Moody died at the age of 89. He had lived to see his innovation become institutionalized, his company become essential infrastructure. Within four years of his death, in 1962, Moody's was bought by credit reporting and information collection giant Dun & Bradstreet Corporation (D&B).

The acquisition marked the end of an era but also the beginning of Moody's transformation from entrepreneurial venture to corporate institution. John Moody had built something that outlived him—not just a company, but a new language for risk that the entire financial world would come to speak.

III. The Dun & Bradstreet Era (1962-2000)

When Dun & Bradstreet acquired Moody's in 1962, it was a match that made strategic sense. D&B, the credit reporting giant, saw natural synergies with Moody's bond rating business. Both companies trafficked in the essential currency of capitalism: trust. But what began as a logical corporate marriage would evolve into something far more complex—a relationship that would fundamentally reshape how credit ratings worked, survive antitrust scrutiny, and ultimately end in divorce.

Life inside the D&B conglomerate brought resources and reach that John Moody could never have imagined. But it also brought a transformation that would prove controversial for decades to come. Moody's expanded its rating services in the 1970s and began charging fees to the companies it covered. The time-consuming, meticulously researched reports done by Moody's proved invaluable to both investors and the covered companies; companies soon realized that a good rating from Moody's was like money in the bank. For many corporate clients, Moody's ratings increased investor confidence and in turn helped add stability to the marketplace.

This shift—from investor-pays to issuer-pays—was seismic. As well, the major agencies began charging the issuers of bonds as well as investors — Moody's began doing this in 1970 — thanks in part to a growing free rider problem related to the increasing availability of inexpensive photocopy machines, and the increased complexity of the financial markets. Think about the elegance and the danger of this pivot. The photocopier, that humble office machine, had created a crisis: investors could simply copy and share rating reports, destroying the subscription model. But the solution created a new problem that critics would hammer for decades—how could Moody's be objective when the companies being rated were writing the checks?

The leading international credit rating agencies (CRAs), namely Moody's, S&P and Fitch (the 'Big Three'), and other CRAs adopted the 'issuer-pay' model in the late 1960s and early 1970s and started to charge issuers for ratings to fund their services. The adoption of the 'issuer-pay' business model enabled CRAs to overcome the problem of the 'freeriding' public goods problem and to assess additional non-public information.

The model proved wildly profitable. Rating agencies also grew in size as the number of issuers grew, both in the United States and abroad, making the credit rating business significantly more profitable. In 2005 Moody's estimated that 90% of credit rating agency revenues came from issuer fees. The business had transformed from a publishing company selling manuals to investors into something more like a tollbooth—you couldn't access the capital markets without paying for a rating.

The regulatory landscape also shifted in Moody's favor. In 1975, the SEC changed its minimum capital requirements for broker-dealers, using bond ratings as a measurement. Moody's and nine other agencies (later five, due to consolidation) were identified by the SEC as "nationally recognized statistical ratings organizations" (NRSROs) This designation was crucial—it essentially gave regulatory force to Moody's opinions. Pension funds, insurance companies, banks—they all needed investment-grade ratings from NRSROs to hold certain securities. The government had effectively mandated demand for Moody's product.

International expansion accelerated through the 1980s and 1990s. The 1980s and beyond saw the global capital market expand; Moody's opened its first overseas offices in Japan in 1985, followed by offices in the United Kingdom in 1986, France in 1988, Germany in 1991, Hong Kong in 1994, India in 1998

But the 1990s also brought turbulence. The last decade of the century was a roller coaster ride for Moody's. In 1994 the company failed to make a profit and in 1995 and 1996 there were rumors of a corporate overhaul. In January 1996 D&B announced its intention to divide into three public companies to better serve its shareholders and market segments. The failure to make a profit in 1994 was shocking for what had become such a dominant franchise. How does a tollbooth lose money?

Then came the legal storm. Soon after news of D&B's upcoming split came the resignation of Moody's president, John Bohn, Jr., in March, followed by rumors of a Department of Justice (DOJ) inquiry concerning possible antitrust violations. The DOJ investigation, which targeted only Moody's ratings service, contacted both its chief rivals—Standard & Poor's Corporation (S&P) and Fitch Investor Services—to provide information. In the midst of the DOJ probe, Moody's reorganized its domestic operations and stepped up plans for international expansion.

The antitrust investigation was serious business. Competitors had complained about Moody's practices, particularly around unsolicited ratings—where Moody's would rate companies that hadn't asked for or paid for ratings, potentially as leverage to get them to become paying clients. The investigation dragged on for years, creating uncertainty about Moody's future.

Meanwhile, Moody's kept expanding globally. In 1998 Moody's bought a 10 percent stake in Korea Investors Service (later increased to more than 50 percent) and began investing in Argentina the following year. The company was building a truly global footprint, recognizing that capital markets were becoming increasingly interconnected.

Finally, in 1999, relief: In 1999 the DOJ investigation into Moody's alleged antitrust violations was closed, and no charges were filed. The company had dodged a bullet that could have fundamentally altered its business model.

But by this point, the relationship with D&B had run its course. Following several years of rumors and pressure from institutional shareholders, in December 1999 Moody's parent Dun & Bradstreet announced it would spin off Moody's Investors Service into a separate publicly traded company. Although Moody's had fewer than 1,500 employees in its division, it represented about 51% of Dun & Bradstreet profits in the year before the announcement.

Think about that statistic: fewer than 1,500 employees generating more than half the profits of a much larger conglomerate. This was a business with extraordinary economics—high margins, recurring revenues, and regulatory moats. No wonder D&B shareholders were clamoring for a spinoff; the market would value this crown jewel far more highly as a standalone company.

IV. The Spinoff & Public Company Era (2000-2007)

September 30, 2000. Independence Day for Moody's Corporation. After 38 years inside the Dun & Bradstreet conglomerate, the rating agency was spinning off as a standalone public company, trading on the New York Stock Exchange under the ticker MCO. For a company that rates everyone else's creditworthiness, there was delicious irony in now being subject to the market's own rating. And the market loved what it saw.

The spin-off was completed on September 30, 2000, and, in the half decade that followed, the value of Moody's shares improved by more than 300%. Think about that trajectory—a tripling of value in five years. What was the market seeing that made it so enthusiastic?

Moody's sales for 1999 had reached $564.2 million, with net income just shy of $156 million. The company finished the year 2000 with $602.3 million and then for its first complete year as a stand-alone company (2001) raked in $797 million in revenues and $212 million in net income. The growth was spectacular—from $602 million to $797 million in a single year, with net margins exceeding 26%.

Moody's commanded a 37 percent share of the corporate bond rating market according to Investor's Business Daily, while rival S&P's had 45 percent and Fitch the remaining 18 percent. Despite S&P's bigger chunk of the market, Moody's maintained the distinction of being named the top credit rating firm for five consecutive years by Institutional Investor.

But the real transformation happening inside Moody's was strategic, not just financial. The company recognized that pure ratings, while lucrative, left it vulnerable to market cycles and regulatory changes. It needed to build a second leg to stand on. Enter the Analytics revolution.

The key acquisition came in February 2002. Moody's purchased KMV (Kealhofer, McQuown and Vasicek), a San Francisco-based quantitative risk management firm, and merged it with MRMS to create Moody's KMV. Credit ratings agency Moody's purchased California-based credit risk management technology firm KMV for $210 million in an all-cash deal.

This wasn't just another tech acquisition. KMV had developed something revolutionary: The company acquired KMV's clients and its software tool for calculating the probability of credit default, here returning the EDF, or "Expected Default Frequency". The EDF model used market data—stock prices, volatility, capital structure—to calculate real-time default probabilities. While Moody's traditional ratings were updated sporadically, EDF scores changed daily with the market.

Moody's KMV integrated financial modeling software from each former company and, in 2003, debuted its credit risk management system, Credit Monitor. Banks loved it. They could now monitor their entire loan portfolio's risk in real-time, using quantitative models rather than just periodic rating updates.

The acquisition spree continued. In 2005, Moody's acquired Economy.com, an economics research and analytics firm based in West Chester, Pennsylvania, adding services related to economic and demographic research, country analysis, and data on industrial, financial, and regional markets. This brought macroeconomic forecasting capabilities into the fold.

Then came a fateful acquisition in 2006. The following year, in December 2006 the firm acquired Wall Street Analytics, a San Francisco-based financial analysis and monitoring software developer founded by Ron Unz, which then became Moody's Wall Street Analytics. The acquisition brought with it software for financial risk management, including CDOnet, a tool for collateralized debt obligation (CDO) valuation.

CDOnet. Remember that name. It was a sophisticated tool for valuing the complex structured products that Wall Street was churning out at breakneck pace. CDOs—collateralized debt obligations—were securities backed by pools of other securities, often mortgage-backed securities themselves. They were complicated, opaque, and incredibly profitable to rate.

And rate them Moody's did. Structured finance went from 28% of Moody's revenue in 1998 to almost 50% in 2007, and "accounted for pretty much all of Moody's growth" during that time. According to the Financial Crisis Inquiry Report, during the years 2005, 2006, and 2007, rating of structured finance products such as mortgage-backed securities made up close to half of Moody's rating revenues.

The numbers were staggering. From 2000 to 2007, revenues from rating structured financial instruments increased more than fourfold. Think about what was happening: Moody's business model had evolved from rating straightforward corporate bonds to evaluating increasingly complex securities that were themselves made up of other securities. It was ratings all the way down.

The market loved these products because Moody's—along with S&P and Fitch—could transform pools of subprime mortgages into AAA-rated securities through the alchemy of structured finance. Take a bunch of BBB-rated mortgage securities, slice them into tranches with different payment priorities, and voilà—the senior tranche gets a AAA rating. It was financial engineering at its most creative.

More than half of the structured finance securities rated by Moody's carried a AAA rating, the highest possible credit rating that is typically reserved for securities deemed to be nearly riskless. Investment banks couldn't create these products fast enough, and they needed Moody's stamp of approval to sell them.

But there were warning signs for those willing to see them. However, there was some question about the models Moody's used to give structured products high ratings. In June 2005, shortly before the subprime mortgage crisis, Moody's updated its approach for estimating default correlation of non-prime/nontraditional mortgages involved in structured financial products like mortgage-backed securities and Collateralized debt obligations. Its new model was based on trends from the previous 20 years, during which time housing prices had been rising, mortgage delinquencies very low

The model assumed that the past would predict the future. That housing prices would keep rising. That mortgage defaults would remain uncorrelated. That the music would never stop.

By 2007, Moody's was printing money. The stock price had soared. Raymond McDaniel, who had become CEO in 2005, was presiding over one of the most profitable businesses in America. The rating agencies had become, in Warren Buffett's famous phrase, "toll bridges" on the capital markets—you couldn't issue debt without paying them.

In August 2007, Moody's Corporation created a new division for its combined non-ratings businesses, Moody's Analytics, to operate separately from Moody's Investors Service. This reorganization would prove prescient—creating a clear separation between the ratings business and everything else just as the ratings business was about to face its greatest crisis.

As 2007 drew to a close, the structured finance machine that had driven Moody's incredible growth was beginning to sputter. Housing prices had peaked. Mortgage defaults were rising. And those AAA-rated structured products? They were about to reveal themselves as anything but riskless.

V. The Financial Crisis & Reckoning (2007-2009)

July 10, 2007. Moody's downgraded 399 subprime mortgage bonds. The market shuddered. But that was just the opening act. What followed over the next eighteen months would expose the rating agencies as either catastrophically wrong or willfully blind—or perhaps both.

The numbers tell a story of staggering failure. Moody's and its close competitors were subject to criticism following large downgrade actions beginning in July 2007. According to the Financial Crisis Inquiry Report, 73% of the mortgage-backed securities Moody's had rated triple-A in 2006 were downgraded to junk by 2010. Think about that transformation: from the safest possible rating to junk in less than four years. It wasn't a mistake; it was a systematic failure.

By autumn 2007, the internal turmoil at Moody's was boiling over. In September, Raymond McDaniel, the CEO, held a town hall meeting with his top managers to discuss what had gone wrong. The feedback he received was devastating. A manager at Moody's in an email sent in September 2007 summed up the situation: "[W]hy didn't we envision that credit would tighten after being loose, and housing prices would fall after rising, after all most economic events are cyclical and bubbles inevitably burst. Combined, these errors make us look either incompetent at credit analysis, or like we sold our soul to the devil for revenue, or a bit of both. Moody's franchise value is based on staying AHEAD OF THE PACK on credit analysis and instead we are in the middle of the pack.

"Incompetent at credit analysis, or like we sold our soul to the devil for revenue." These weren't the words of an outside critic but a senior insider. The phrase would become infamous, quoted in Congressional hearings and newspaper headlines, crystallizing everything that had gone wrong with the rating agencies.

The pressure to deliver favorable ratings had been intense. There was significant pressure put on staff at the credit rating agencies to deliver favourable ratings with the threat that if they didn't then business would be taken elsewhere. When asked by the Financial Crisis Inquiry Commission if the investment banks frequently threatened to withdraw their business if they didn't get their desired rating, a manager at Moody's replied: "Oh God, are you kidding? All the time. I mean, that's routine. I mean, they would threaten you all of the time... It's like, 'Well, next time, we're just going to go with Fitch and S&P.'"

The competition between rating agencies had created a race to the bottom. What happened in 2004 and 2005 with respect to subordinated tranches is that our competition, Fitch and S&P, went nuts. Everything was investment grade... No one cared, because the machine just kept going. The machine—that's what they called it internally. A machine for turning mortgages into AAA-rated securities, regardless of the underlying quality.

Congressional investigators would later uncover even more damning evidence. Other memorable quotes from internal documents included: "It could be structured by cows, and we would rate it" and "Let's hope we are all retired by the time this house of cards falters." These weren't isolated comments from disgruntled employees—they reflected a culture that had lost its way.

The technical failures were equally damning. Starting in 2001, Moody's RMBS group began using an internal tool in rating RMBS that did not calculate the loss given default or expected loss for RMBS below Aaa and did not incorporate Moody's own rating standards. Instead, the tool was designed to "replicate" ratings that had been assigned based on a previous model that calculated expected loss for each tranche and incorporated Moody's rating level standards. They weren't even following their own methodology.

By October 2007, the problems were impossible to ignore. In October 2007, a senior manager in Moody's Asset Finance Group (AFG) noted the following about Moody's RMBS ratings derived from the tool: "I think this is the biggest issue TODAY. [A Moody's AFG Senior Vice President and research manager]'s initial pass shows that our ratings are 4 notches off." Four notches—the difference between investment grade and junk.

The CDO ratings were even worse. Starting in 2004, Moody's did not follow its published idealized expected loss standards in rating certain Aaa CDO securities. Instead, Moody's began using a more lenient standard for rating these Aaa securities but did not issue a publication about this practice to the general market. In 2005, Moody's authorized the expanded use of this practice to all Aaa CDO securities and, in 2006, formally authorized the use of this practice, or of an even more lenient standard, to all Aaa structured finance securities. Throughout this period, although "[m]any arrangers and issuers were aware" that Moody's was using a more lenient Aaa standard, Moody's did not issue publications about these decisions to the general market.

They had secretly lowered their standards while maintaining the appearance of rigor. The insiders knew. The issuers knew. But investors? They were kept in the dark.

As 2008 unfolded, the downgrades accelerated into an avalanche. There were more than 8,000 downgrades in 2007 - an eightfold increase over the previous year. In the first three quarters of 2008, there were 36,880 downgrades, overshadowing the cumulative number of downgrades since 1990. Downgrades were not only more common in 2007 and 2008 but also more severe. The average downgrade was 4.7 notches in 2007 and 5.8 notches in 2008, compared to 2.5 notches in both 2005 and 2006.

The Financial Crisis Inquiry Commission would later deliver a scathing verdict: In its "Conclusions on Chapter 8", the Financial Crisis Inquiry Commission stated: "There was a clear failure of corporate governance at Moody's, which did not ensure the quality of its ratings on tens of thousands of mortgage-backed securities and CDOs."

The reputational damage was catastrophic. Moody's stock price, which had peaked above $70 in early 2007, crashed to below $20 by early 2009. The company that had built its business on trust had lost it spectacularly. Warren Buffett, who owned 13% of the company through Berkshire Hathaway, would later say that the rating agencies had made "a huge mistake" and that their "mania" had contributed to the crisis.

Yet here's the remarkable thing: Moody's survived. More than survived—it would eventually thrive again. How does a company come back from being accused of selling its soul to the devil? How does it rebuild trust after such a spectacular failure?

Part of the answer lay in the structure Moody's had put in place just before the crisis. The creation of Moody's Analytics as a separate division in August 2007 proved prescient. While the ratings business was being pilloried, Analytics could continue to grow, providing software and research services that weren't tainted by the ratings scandal.

But the real answer was more fundamental: the rating agencies were too essential to fail. Despite everything, the capital markets still needed them. The regulatory requirements still mandated their use. And there were still only three major players. The oligopoly structure that had enabled the race to the bottom would also enable the recovery.

As 2009 began, Moody's faced investigations, lawsuits, and calls for fundamental reform. But it also faced opportunity. The credit markets were frozen. When they thawed, someone would need to rate the new bonds. And who else could do it at scale but Moody's, S&P, and Fitch?

VI. Aftermath & Regulatory Response (2009-2017)

The financial crisis had been a near-death experience for the rating agencies. But in the American regulatory system, near-death experiences often lead not to elimination but to intensified oversight. The Dodd-Frank Wall Street Reform and Consumer Protection Act, signed into law on July 21, 2010, would fundamentally reshape the regulatory landscape for credit rating agencies—though not necessarily in the ways reformers had hoped.

The Dodd-Frank Act (2010) found credit ratings to be systemically important to the financial system. Its reforms had four main pillars. The legislation represented Congress's most comprehensive attempt to address the failures exposed by the crisis. But as with many regulatory responses, the cure would prove almost as complex as the disease.

The first pillar aimed at the heart of the problem: the issuer-pays model. First, the Dodd-Frank Act requires the SEC and GAO to study the NRSROs' issuer-pays model and alternatives to it, and required the SEC to recommend a business model for the NRSROs. If no business model were recommended, it required the SEC to create a board that randomly assigns credit rating assignments to the NRSROs—an idea originally embodied in the Franken-Wicker Amendment.

This was potentially revolutionary. Random assignment would break the cozy relationship between issuers and raters. No more rating shopping. No more implicit threats to take business elsewhere. The SEC and GAO conducted their studies of different models, highlighting some of their strengths and weaknesses. Additionally, the SEC held a roundtable to discuss different models' strengths and weaknesses. However, the SEC took no further action since 2013 and has neither endorsed a business model for the NRSROs nor implemented the random assignment model.

The reform that could have fundamentally changed the industry simply... didn't happen. The SEC studied, discussed, deliberated—and then did nothing. The issuer-pays model, the source of so much conflict, remained intact.

The second pillar attempted to reduce regulatory reliance on ratings. Second, the Dodd-Frank Act reduces the official role of NRSROs by requiring regulators to remove and replace the use of credit ratings in regulations that set capital requirements and restrict asset holdings for financial institutions. Regulators responded by replacing credit ratings with three alternative approaches: definitions, regulatory models, and third-party classifications.

This was crucial. By mandating the use of ratings in regulations, the government had essentially created guaranteed demand for the rating agencies' product. Removing these references would, in theory, reduce the rating agencies' power. But implementation proved challenging. How do you replace something so embedded in the financial system's DNA?

The third pillar addressed legal liability—or tried to. The Act attempted to increase the rating agencies' exposure to lawsuits by removing some of their First Amendment protections. But The SEC has not proposed legal liability rules for CRAs. If such a rule were finalized the CRAs would likely challenge it in court on the grounds that their ratings are opinions protected by the First Amendment.

The fourth pillar was classic regulatory response: more oversight. Fourth, the Dodd-Frank Act gives the SEC more power to regulate the NRSROs. Congress required the SEC to create rules for internal controls, conflicts of interest for credit analysts, standards for credit analysts, transparency, internal conflict of interest, and rating performance statistics among other things. The SEC has finalized these rules and is incorporating them in their annual examination of the NRSROs.

The Act also created a new Office of Credit Ratings within the SEC, specifically tasked with overseeing the rating agencies. More examiners, more reports, more compliance requirements. The irony, as critics pointed out, was that Many of these rules were implemented to address the conflicts of interest and behavioral issues of the big three, and ironically those companies are the only ones that can easily afford to comply.

Meanwhile, Moody's was dealing with the immediate aftermath of the crisis through legal settlements. The company faced a barrage of lawsuits from investors who had relied on its ratings. October 2011: Moody's reached a settlement resolving claims by the state of Connecticut that the credit rating company unfairly gave lower ratings to public bonds. July 2012: Moody's said it reached a settlement with stockholders in lawsuits filed over structured finance ratings. April 2013: Moody's reached a settlement avoiding what would have been their first jury trial over crisis-era ratings.

But the big settlement came in 2017. The Department of Justice, 21 states, and the District of Columbia reached a nearly $864 million settlement agreement with Moody's Investors Service Inc., Moody's Analytics Inc., and their parent, Moody's Corporation, the Department announced today. The settlement resolves allegations arising from Moody's role in providing credit ratings for Residential Mortgage-Backed Securities (RMBS) and Collateralized Debt Obligations (CDO), contributing to the worst financial crisis since the Great Depression.

The settlement included damning admissions. Starting in 2004, Moody's did not follow its published idealized expected loss standards in rating certain Aaa CDO securities. Instead, Moody's began using a more lenient standard for rating these Aaa securities but did not issue a publication about this practice to the general market. In 2005, Moody's authorized the expanded use of this practice to all Aaa CDO securities and, in 2006, formally authorized the use of this practice, or of an even more lenient standard, to all Aaa structured finance securities. Throughout this period, although "[m]any arrangers and issuers were aware" that Moody's was using a more lenient Aaa standard, Moody's did not issue publications about these decisions to the general market.

The compliance commitments were extensive. Under the terms of the compliance commitments, Moody's agrees to maintain a host of measures designed to ensure the integrity of its credit ratings. These included separating commercial and rating functions, independent review of methodologies, and compensation changes to reduce conflicts of interest.

Yet through all of this—the regulatory changes, the lawsuits, the settlements, the public opprobrium—Moody's business continued to recover. By 2011, revenues had surpassed pre-crisis levels. The stock price, which had bottomed below $20 in 2009, was climbing steadily back.

How was this possible? The answer lay in a fundamental truth about modern finance: the system still needed rating agencies. In the six years since enactment of Dodd-Frank, regulators have not followed through on many of these reforms... Finally, the SEC has neither endorsed a business model for the NRSROs nor implemented a random assignment procedure.

The most significant reforms simply hadn't happened. The issuer-pays model remained. Regulatory reliance on ratings, while reduced, hadn't been eliminated. And there were still only three major players in the market.

Moreover, Moody's Analytics division was thriving. The separation of the ratings and analytics businesses in 2007 had proved prescient. While Moody's Investors Service dealt with legal challenges and reputational damage, Moody's Analytics was selling risk management software to banks that needed better tools precisely because of the crisis. The division that had started with the KMV acquisition was becoming an increasingly important profit center.

The company was also expanding globally. Emerging markets needed ratings as their capital markets developed. China, India, Brazil—these countries were building financial infrastructure, and Moody's was there to help rate their bonds.

By 2017, when the DOJ settlement was announced, Moody's market cap had not only recovered but exceeded its pre-crisis peak. The company that one manager said had "sold our soul to the devil for revenue" had somehow emerged from purgatory stronger than ever.

The lesson was complex. Yes, the rating agencies had failed catastrophically. Yes, they bore significant responsibility for the crisis. But they were also systemically important—too essential to fail, if not too big. The financial system had been built around them, and rebuilding it without them proved harder than anyone anticipated.

VII. Modern Era: The Duopoly Continues (2017-Present)

Today, Moody's stands as a testament to the power of essential infrastructure in financial markets. With revenues of $7.09 billion in 2024, up 19.81% from the previous year, and net income of $2.058 billion, representing a 28.06% increase from 2023, the company has not just recovered from the financial crisis—it has thrived beyond anyone's expectations.

The numbers tell a story of remarkable resilience. Moody's net income for 2024 was $2.058B, a 28.06% increase from 2023. Moody's net income for 2023 was $1.607B, a 16.96% increase from 2022. The profit margins are extraordinary—approaching 30% in recent years. This is a business that prints money.

The current structure reflects lessons learned from the crisis. The company operates through two distinct segments: Moody's Ratings and Moody's Analytics (now simply called Moody's). This division, formalized just before the 2008 crisis, has proved its worth. While the ratings business remains cyclical and reputation-sensitive, Analytics provides steady, subscription-based revenues from risk management software and data services.

Warren Buffett's continued faith in the company speaks volumes. Warren Buffett looks for top companies that participate in leading the U.S. economy, boring or not, and his holding company, Berkshire Hathaway, owns 13.5% of Moody's stock and is its largest investor. It makes up about 2.5% of the Berkshire Hathaway equity portfolio. Not including dividends, Berkshire's stake in Moody's is up more than 4,600% from its reported cost basis.

What does Buffett see? Moody's has everything that Buffett searches for in an investment: a competitive edge, strong management, a leading position, excellent profitability, strong recurring revenue, and a high free cash flow. The company is, in Buffett's famous phrase, a "toll bridge" on the capital markets—you can't avoid paying if you want to cross.

The oligopoly structure remains firmly intact. Together, they are sometimes referred to as the Big Three credit rating agencies—Moody's, S&P, and Fitch. Despite all the regulatory changes, new entrants, and technological disruption, these three firms continue to dominate global credit ratings. The barriers to entry are formidable: regulatory requirements, decades of performance data, global reach, and most importantly, market acceptance.

The business model has evolved but not fundamentally changed. The issuer-pays model remains, despite its inherent conflicts. Regulatory references to ratings, while reduced, haven't been eliminated. Banks, insurance companies, and pension funds still need investment-grade ratings to hold certain securities. The system that enabled the crisis remains largely in place.

Yet there have been improvements. The compliance infrastructure is more robust. There's greater transparency in methodologies. The separation between commercial and analytical functions is clearer. And perhaps most importantly, there's more skepticism from investors about ratings—they're no longer taken as gospel.

Moody's has also expanded beyond traditional ratings. The Analytics division has become a significant growth driver, offering everything from economic forecasting to climate risk assessment. In 2019, Moody's Corporation purchased the majority share in the California-based climate risk data firm, Four Twenty Seven (427), that "measures the physical risks" of "climate change".

The company has embraced new rating categories. ESG (Environmental, Social, and Governance) ratings have become increasingly important as sustainable investing goes mainstream. Cyber risk ratings are emerging as a new frontier. The rating agency is evolving with the times while maintaining its core franchise.

Internationally, Moody's continues to expand. China, despite developing its own rating agencies, still needs the imprimatur of the global agencies for its companies to access international capital markets. Emerging markets from Indonesia to Nigeria rely on Moody's ratings to attract foreign investment.

The financials reflect this strength. Looking ahead, revenue is forecast to grow 7.9% p.a. on average during the next 3 years, compared to a 6.7% growth forecast for the Capital Markets industry in the US. The company generates enormous free cash flow, has minimal capital requirements, and enjoys pricing power that most businesses can only dream of.

But challenges remain. Private credit markets, which don't require ratings, are growing rapidly. Technology companies are attempting to disrupt the ratings business with AI and alternative data. Regulatory scrutiny, while not as intense as post-2008, remains constant. And the shadow of the financial crisis still lingers—one major ratings failure could reignite calls for fundamental reform.

The duopoly (really a triopoly with Fitch) continues because, fundamentally, the market needs what Moody's provides: an independent (if imperfect) assessment of credit risk that's globally recognized and regulatorily accepted. It's not perfect, but it's the system we have, and changing it has proved harder than anyone anticipated.

VIII. Power Dynamics & Market Structure

Why are there only three major credit rating agencies? After the catastrophic failures of 2008, after Dodd-Frank, after billions in settlements, how does this oligopoly persist? The answer reveals fundamental truths about how modern capitalism works—and why some businesses are almost impossible to disrupt.

Start with the most basic question: What is Moody's actually selling? Not information—that's commoditized. Not even analysis—plenty of firms do that. What Moody's sells is permission. Permission for a pension fund to buy a bond. Permission for a bank to hold a security with minimal capital charges. Permission for a money market fund to invest in commercial paper. The rating is a regulatory key that unlocks access to vast pools of capital.

This creates extraordinary network effects. The more institutions that rely on Moody's ratings, the more issuers need Moody's ratings to access those institutions' capital. The more issuers that get rated, the more data Moody's accumulates, improving its models. The better its models, the more regulators trust its ratings. It's a self-reinforcing cycle that's nearly impossible to break.

Consider the switching costs. An issuer can't simply decide to use a new rating agency. They need one that's recognized by regulators (NRSRO status), accepted by investors, and comparable to existing ratings. Investors have decades of performance data on Moody's ratings—they know what a Moody's Baa1 means in practice. A new entrant's Baa1? Who knows?

The regulatory moat is perhaps the highest barrier. There are currently 10 credit rating agencies that have applied for and been granted registration as an NRSRO. But registration is just the beginning. These agencies must comply with extensive reporting requirements, maintain detailed records, submit to regular examinations, and manage potential conflicts of interest. The compliance costs alone are prohibitive for smaller firms.

But it goes deeper than regulation. Moody's benefits from what economists call a "two-sided market" with strong cross-side network effects. Issuers need Moody's because investors use Moody's ratings. Investors rely on Moody's because issuers get Moody's ratings. Breaking this cycle requires convincing both sides simultaneously—a nearly impossible coordination problem.

The issuer-pays model, despite its conflicts, actually strengthens the oligopoly. A new rating agency faces a chicken-and-egg problem: issuers won't pay for ratings that investors don't use, but investors won't use ratings that issuers haven't paid for. The Big Three already have both sides locked in.

Pricing power flows naturally from this structure. When you're one of only three firms that can provide a regulatory necessity, you can charge accordingly. Moody's doesn't compete on price—it doesn't have to. The cost of a rating is trivial compared to the cost of not having one: being locked out of vast pools of institutional capital.

This pricing power shows up in the margins. Operating margins consistently exceed 40%, sometimes approaching 50%. These are software-like margins for what is essentially a professional services business. Very few companies on Earth can sustain such margins over decades.

The comparison with S&P Global is instructive. S&P and Moody's are near-perfect duopolists, together controlling about 80% of the global ratings market. They don't compete aggressively on price. They maintain similar rating scales. They generally reach similar conclusions on creditworthiness. It's not explicit collusion—it doesn't need to be. The market structure creates natural stability.

This stability extends to market shares. Despite the financial crisis, despite new entrants, despite technological change, market shares have remained remarkably constant. Moody's has about 33%, S&P about 45%, and Fitch about 15%. The remaining 7% is split among smaller players. These percentages have barely budged in two decades.

Why don't new entrants gain traction? Consider what happened to Egan-Jones, one of the few investor-pays rating agencies. Despite avoiding the conflicts of the issuer-pays model, despite NRSRO status, they remain a niche player. The network effects are just too strong.

Even well-funded entrants struggle. Chinese rating agencies, backed by the government, have tried to challenge the Big Three. But outside China, they've gained little traction. Global investors simply don't trust them the way they trust Moody's, S&P, and Fitch.

Technology should be a threat. AI and machine learning can analyze credit risk. Alternative data—satellite imagery, social media sentiment, transaction data—can provide real-time insights. Startups are building algorithmic rating systems. Yet none have made a dent in the oligopoly. Why? Because Moody's ratings aren't really about analytical superiority—they're about market acceptance and regulatory blessing.

The financial crisis should have been an existential threat. If massive failure couldn't break the oligopoly, what could? But the crisis actually reinforced it. The regulatory response focused on reforming the existing players rather than replacing them. New compliance requirements raised barriers to entry. The Big Three adapted and survived.

This isn't to say the oligopoly is permanent. Regulatory changes could alter the landscape—imagine if regulators eliminated rating requirements entirely. Technological disruption could eventually succeed—perhaps blockchain-based decentralized ratings. Private credit markets, which don't require ratings, are growing rapidly.

But for now, the oligopoly endures. It endures because it's woven into the fabric of global finance. It endures because the costs of replacing it exceed the costs of maintaining it. It endures because, despite its flaws, it provides something the market needs: a common language for credit risk that's understood from New York to Tokyo to London.

The power dynamics reveal an uncomfortable truth about modern capitalism: some monopolies and oligopolies exist not because of anti-competitive behavior, but because of the nature of the service itself. Rating agencies are natural oligopolies—markets where a few players will always dominate because of network effects, regulatory requirements, and the need for standardization.

For investors, this creates an interesting paradox. The same factors that make the rating agencies problematic—conflicts of interest, lack of competition, regulatory capture—also make them incredibly profitable investments. It's the ultimate "toll booth" business, extracting rent from the global flow of capital.

IX. Playbook: Business & Investment Lessons

What can we learn from Moody's journey from manual publisher to financial gatekeeper? The lessons go beyond finance, revealing timeless principles about building and investing in enduring businesses.

The Toll Booth Principle

Moody's is the quintessential toll booth business. Every issuer seeking to access public debt markets must pay for ratings—not by law, but by practical necessity. This isn't a competitive market where customers can easily switch or abstain. It's a toll that must be paid to participate in global capital markets.

The lesson for investors: Look for businesses that sit at critical chokepoints in economic activity. These aren't necessarily monopolies by law, but monopolies by circumstance. Payment networks, exchanges, certain software platforms—they all share this toll booth characteristic. Once established, they're extraordinarily difficult to displace and can raise prices faster than inflation for decades.

Information Asymmetry as a Business Model

Moody's doesn't create information—it validates it. The company takes public data, applies judgment, and produces an opinion that carries regulatory and market weight. The genius is that this opinion becomes more valuable than the underlying information itself.

This model—turning information into judgment into permission—appears across the economy. Auditors don't create financial statements; they bless them. Universities don't create knowledge; they certify it. The lesson: In an information-rich world, the scarce resource isn't data but trusted interpretation of data.

Surviving Existential Crises

The 2008 financial crisis should have destroyed Moody's. The company was accused of fundamental failures, paid nearly a billion dollars in settlements, and faced calls for its dissolution. Yet it emerged stronger. How?

First, Moody's was systemically important—too essential to fail, even if not too big. Second, it had diversified (Analytics) before the crisis hit. Third, it had the financial strength to weather the storm. Fourth, and perhaps most importantly, there was no ready alternative. Regulators could punish Moody's, but they couldn't easily replace it.

The investment lesson: Companies that survive existential crises often emerge stronger, with weaker competitors eliminated and reforms that actually entrench their positions. Look at banks post-2008, tech platforms post-antitrust scrutiny, pharma companies post-litigation. Crisis can be opportunity if you have the balance sheet and market position to survive it.

The Analytics Pivot

The creation and growth of Moody's Analytics demonstrates the power of leveraging core competencies into adjacent markets. Analytics uses the same fundamental expertise—credit analysis—but delivers it through software and subscriptions rather than ratings.

This wasn't diversification for its own sake. It was a logical extension that shared customers (financial institutions), expertise (risk assessment), and data (credit information) with the core business. Yet it had different economics—recurring subscriptions versus transactional ratings—and different regulatory exposure.

The lesson: The best diversification leverages existing advantages while changing the business model. Adobe's shift to subscriptions, Microsoft's move to cloud, Netflix's evolution from DVDs to streaming—they all follow this pattern.

Subscription Versus Transaction Economics

Moody's demonstrates both models. Ratings are transactional—paid when bonds are issued. Analytics is subscription-based—paid regularly regardless of activity. The combination provides both growth potential (transactions in boom times) and stability (subscriptions in downturns).

Understanding these dynamics is crucial for investors. Transactional businesses offer more upside but more volatility. Subscription businesses provide predictability but may miss bonanzas. The best businesses, like Moody's, combine both.

Why Buffett Owns It

Warren Buffett's Berkshire Hathaway owns 13.5% of Moody's, and the position has generated returns exceeding 4,600%. What does Buffett see?

First, it's a simple business to understand—companies need ratings to borrow money. Second, it has a durable competitive advantage—the oligopoly structure and regulatory moats. Third, it requires minimal capital investment—no factories, no inventory, just human judgment. Fourth, it has pricing power—the ability to raise prices without losing customers. Fifth, it generates enormous cash flow that can be returned to shareholders.

But perhaps most importantly, Moody's is "anti-fragile." The more complex financial markets become, the more valuable independent credit assessment becomes. Every financial crisis leads to calls for more transparency, more analysis, more ratings—all of which benefit Moody's.

The Regulatory Capture Paradox

Moody's relationship with regulators is complex. Regulations require the use of ratings, creating demand. But regulations also constrain Moody's behavior, limiting its flexibility. The company is simultaneously empowered and imprisoned by regulation.

This creates a fascinating dynamic for investors. Regulatory risk is real—rules could change to eliminate rating requirements. But regulatory moats are also real—new rules typically entrench existing players who can afford compliance costs. The key is distinguishing between regulatory noise (investigations, fines, reforms that don't change the business model) and regulatory threats (fundamental changes to market structure).

Reputation Damage and Recovery

The financial crisis destroyed Moody's reputation. Internal emails about "selling our soul to the devil" became public. The company was blamed for enabling the crisis. Yet here we are, with Moody's more valuable than ever.

The lesson: In businesses with high barriers to entry, reputation damage is often temporary. Customers may hate you but still need you. The key is maintaining operational excellence while reputation recovers. This applies to many industries—airlines recover from crashes, pharma companies from drug recalls, tech companies from privacy breaches. If the underlying business model is strong enough, reputation is renewable.

Building Modern Moats

Could you build a Moody's today? Almost certainly not in the same way. The regulatory permissions, the decades of performance data, the market acceptance—these took a century to accumulate.

But the principles apply to modern businesses. Network effects (social media), regulatory requirements (fintech), switching costs (enterprise software), data advantages (search engines)—these create modern moats. The key is identifying businesses early in their moat-building phase, not after the moat is complete.

The ESG Parallel

Moody's expansion into ESG ratings is instructive. Like credit ratings in 1909, ESG ratings today are subjective, controversial, and lack standardization. But as sustainability becomes mandatory for institutional investors, ESG ratings are becoming essential infrastructure.

This pattern—voluntary adoption becoming market standard becoming regulatory requirement—repeats across industries. Identifying these transitions early can reveal enormous investment opportunities.

The Moody's playbook ultimately teaches that the most powerful businesses don't compete in markets—they create markets where competition is structurally limited. They don't sell products—they sell permissions. They don't provide services—they provide infrastructure. And most importantly, they position themselves so that their success becomes everyone's necessity.

X. Bear vs Bull Case & Valuation

Bull Case: The Indispensable Infrastructure

The bull case for Moody's starts with a simple observation: global debt markets are growing faster than global GDP and will continue to do so for structural reasons. Governments need to finance deficits. Corporations need to fund growth. Infrastructure needs building. Climate transition needs financing. All of this requires debt, and most debt requires ratings.

The numbers are staggering. Global debt markets exceed $130 trillion. Even capturing a few basis points of fees on this mountain of debt creates a massive revenue opportunity. And the mountain keeps growing—global debt has doubled every decade for the past three decades.

Moody's Analytics represents the second leg of growth. This business is transitioning from selling software to selling solutions—cloud-based, subscription-priced, deeply embedded in customer workflows. The margins are expanding as the business scales. Analytics could eventually exceed the ratings business in both size and profitability.

Emerging markets offer decades of growth. As countries develop, their capital markets deepen. Local currency bond markets need ratings. Corporate bond markets need ratings. Structured finance markets need ratings. Moody's is already positioned in these markets, often as the first or second mover.

ESG and climate ratings represent a generational opportunity. Just as credit ratings became mandatory for debt investing, ESG ratings are becoming mandatory for all investing. Moody's is leveraging its credibility and infrastructure to capture this emerging market. The acquisition of Four Twenty Seven for climate risk data shows the company thinking ahead.

The competitive position remains unassailable. Despite everything—the financial crisis, regulatory scrutiny, technological change—the Big Three's market shares haven't materially changed. New entrants have failed. Chinese competitors can't gain global traction. The moat isn't narrowing; if anything, compliance costs and data advantages are widening it.

Operating leverage is enormous. Moody's doesn't need to hire proportionally more analysts as debt markets grow. The same team that rates $1 billion of bonds can rate $10 billion. Technology is making analysts more productive. Margins should continue expanding.

Capital allocation is excellent. The company generates far more cash than it can reinvest, leading to substantial buybacks and dividends. Management has shown discipline in acquisitions, buying complementary businesses at reasonable prices. There's no empire building or wasteful spending.

The Buffett seal of approval matters. Berkshire owning 13.5% provides both validation and stability. Buffett doesn't sell—he holds forever. This patient capital allows management to think long-term.

Valuation, while elevated, is justified by quality. Yes, the stock trades at premium multiples. But premium businesses deserve premium valuations. The consistency of cash flows, the growth trajectory, the margins, the returns on capital—they all justify paying up for quality.

Bear Case: The Fragile Monopoly

The bear case starts with regulatory risk—not tweaks or reforms, but fundamental restructuring. What if regulators finally eliminate rating requirements entirely? What if they implement random assignment of ratings? What if they cap fees? The entire business model depends on regulatory architecture that could change with one law.

Private credit is a existential threat flying under the radar. Direct lending doesn't require ratings. Private credit funds now manage trillions in assets. As this market grows, the addressable market for ratings shrinks. The most sophisticated investors are increasingly bypassing public markets entirely.

Technology disruption is accelerating. AI can now analyze credit risk better than human analysts in many cases. Alternative data provides real-time insights versus Moody's periodic updates. Blockchain could enable decentralized, algorithmic ratings. The technology moat is eroding even if the regulatory moat isn't.

Reputation hasn't fully recovered from 2008. Yes, the business has recovered, but institutional memories are long. The next crisis involving failed ratings could trigger more severe regulatory response. Politicians need scapegoats in crises, and rating agencies are perfect targets.

The issuer-pays conflict remains unresolved. Despite all the compliance measures, the fundamental conflict persists: Moody's is paid by the companies it rates. This creates inevitable pressure for rating inflation. The next bubble will likely involve inflated ratings, restarting the cycle of blame.

Market cyclicality is underappreciated. When debt issuance drops—as it does in every recession—Moody's revenues plummet. The operating leverage works both ways. Fixed costs don't decline when revenues do. The next recession could be particularly severe given current debt levels.

Competition from unexpected angles is emerging. Index providers like MSCI are moving into ESG ratings. Data companies like Bloomberg have rating capabilities. Tech giants could enter if they wanted. The barriers to entry are high but not insurmountable for well-funded players.

Valuation is stretched by any historical measure. The stock trades at over 40x earnings, near historical peaks. The dividend yield is minimal. The growth rate doesn't justify the multiple. Any disappointment—regulatory, competitive, or cyclical—could trigger a major correction.

Key person risk exists. While not dependent on any individual, Moody's depends on maintaining analytical credibility. A major rating failure, a scandal, or a brain drain to competitors could damage the franchise. The company is only as good as its last major call.

China represents both opportunity and threat. If Chinese rating agencies gain international credibility, they could challenge the Western oligopoly. China doesn't play by Western rules. State backing could subsidize a global expansion that undercuts Moody's pricing.

Valuation Perspective

At current prices around $450 per share, Moody's trades at approximately 42x trailing earnings and 38x forward earnings. The EV/EBITDA multiple exceeds 30x. By traditional metrics, the stock is expensive.

But traditional metrics may not apply. Moody's isn't a traditional business—it's a toll booth on global capital markets. The relevant comparisons aren't industrial companies but other financial infrastructure: exchanges, payment networks, data providers. Against these peers, Moody's valuation is reasonable.

The DCF case depends entirely on assumptions about terminal growth and margins. Bulls assume mid-single-digit terminal growth and sustained 40%+ margins. Bears assume growth slows to GDP and margins compress. The stock price implies the bullish scenario.

Risk-reward appears balanced. The company could re-rate higher if Analytics accelerates, ESG takes off, or emerging markets boom. It could re-rate lower if regulation tightens, private credit accelerates, or recession hits. At current valuations, perfection is priced in.

For long-term investors, the key question isn't whether Moody's is cheap—it isn't. The question is whether the business model is sustainable for decades. If you believe credit ratings remain essential infrastructure, the premium valuation may be justified. If you believe the model is vulnerable to disruption, no valuation is safe.

XI. Final Analysis & Lessons

The story of Moody's Corporation is, at its heart, a story about trust in a system that perhaps shouldn't be trusted. Here is a private company, operating for profit, whose opinions carry the force of law. A company that failed catastrophically in 2008, contributing to the worst financial crisis in generations, yet emerged more powerful than before. A business model built on an obvious conflict of interest—being paid by those you judge—that nonetheless persists because the alternatives are worse or non-existent.

This paradox—private companies rating public creditworthiness—reveals something fundamental about modern capitalism. We've outsourced critical public functions to private actors not by design but by evolution. No one planned for three American companies to control global credit assessment. It just happened, step by step, decision by decision, regulation by regulation, until we arrived at a system that no one would design but everyone depends upon.

Could you build a Moody's today? Almost certainly not. The conditions that allowed John Moody to create his rating system—unregulated markets, no established competitors, growing capital needs—no longer exist. But more importantly, you wouldn't need to. The last-mover advantage in rating agencies is enormous. Why compete with Moody's when you can build the next essential infrastructure for tomorrow's markets?

This points to a broader lesson about financial infrastructure. The most powerful businesses don't compete in markets—they become the markets. They position themselves as neutral arbiters while profiting from every transaction. They become so embedded in the system that removing them would cause more damage than tolerating their conflicts.

Yet Moody's also demonstrates the resilience of American capitalism. Despite its flaws, the rating system works well enough most of the time. It allows capital to flow from savers to borrowers, enables price discovery, and provides a common language for risk. Perfect? No. Functional? Yes. And in complex systems, functional beats optimal.

The fine line between essential service and systemic risk remains Moody's central challenge. The company is simultaneously too important to fail and too dangerous to leave unreformed. Each financial cycle tests this balance. So far, the essential service aspect has won—regulators patch rather than replace the system.

For investors, Moody's offers a masterclass in moat analysis. Its competitive advantages—regulatory blessing, network effects, switching costs, data advantages—compound over time. New competitors face not one barrier but multiple interlocking barriers. It's not enough to build a better rating system; you must convince regulators, issuers, and investors simultaneously.

The company also illustrates the power of optionality. When John Moody created his first manual, he couldn't have imagined rating sovereign nations or complex derivatives. When Moody's Corporation went public in 2000, ESG ratings didn't exist. The core competency—assessing creditworthiness—proved extensible in ways no one predicted.

Perhaps most importantly, Moody's shows that in finance, reputation is both everything and nothing. Everything because trust is the ultimate currency. Nothing because when you're essential enough, even shattered trust can be rebuilt. The company's recovery from 2008 proves that institutional necessity trumps institutional memory.

Looking forward, Moody's faces a fascinating test. Can a 20th-century business model survive 21st-century disruption? Can regulatory moats withstand technological torrents? Can the issuer-pays conflict persist in an age of radical transparency?

The answer likely depends on whether we can imagine and implement a better system. Direct lending, algorithmic ratings, decentralized assessment—alternatives exist. But path dependence is powerful. The global financial system has been built around ratings from Moody's, S&P, and Fitch. Changing that architecture would require coordinated action on a scale that seems impossible in our fragmented world.

So Moody's endures, a monument to the power of being first, becoming essential, and surviving long enough to become irreplaceable. It's a business that shouldn't exist in its current form but does because the friction of change exceeds the friction of continuity.

The ultimate lesson may be this: In complex systems, suboptimal solutions that work often persist over optimal solutions that require coordination. Moody's is suboptimal—everyone agrees on that. But it works, mostly. And in the messy reality of global finance, "mostly works" beats "theoretically better" every time.

For students of business, Moody's provides a template for building enduring franchises: Find a critical function. Become the standard. Survive the crises. Extend the franchise. For critics of capitalism, it exemplifies the problems: conflicts of interest, regulatory capture, private profits from public functions. For investors, it represents a paradox: a problematic business model that generates exceptional returns precisely because it's so hard to displace.

The credit rating industry will eventually be disrupted—every industry eventually is. But that disruption is likely still years, perhaps decades, away. Until then, Moody's will continue its role as the imperfect but irreplaceable arbiter of creditworthiness, collecting its toll on the global flow of capital, and demonstrating that in finance, as in life, the most powerful position is to become the judge rather than the judged.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube