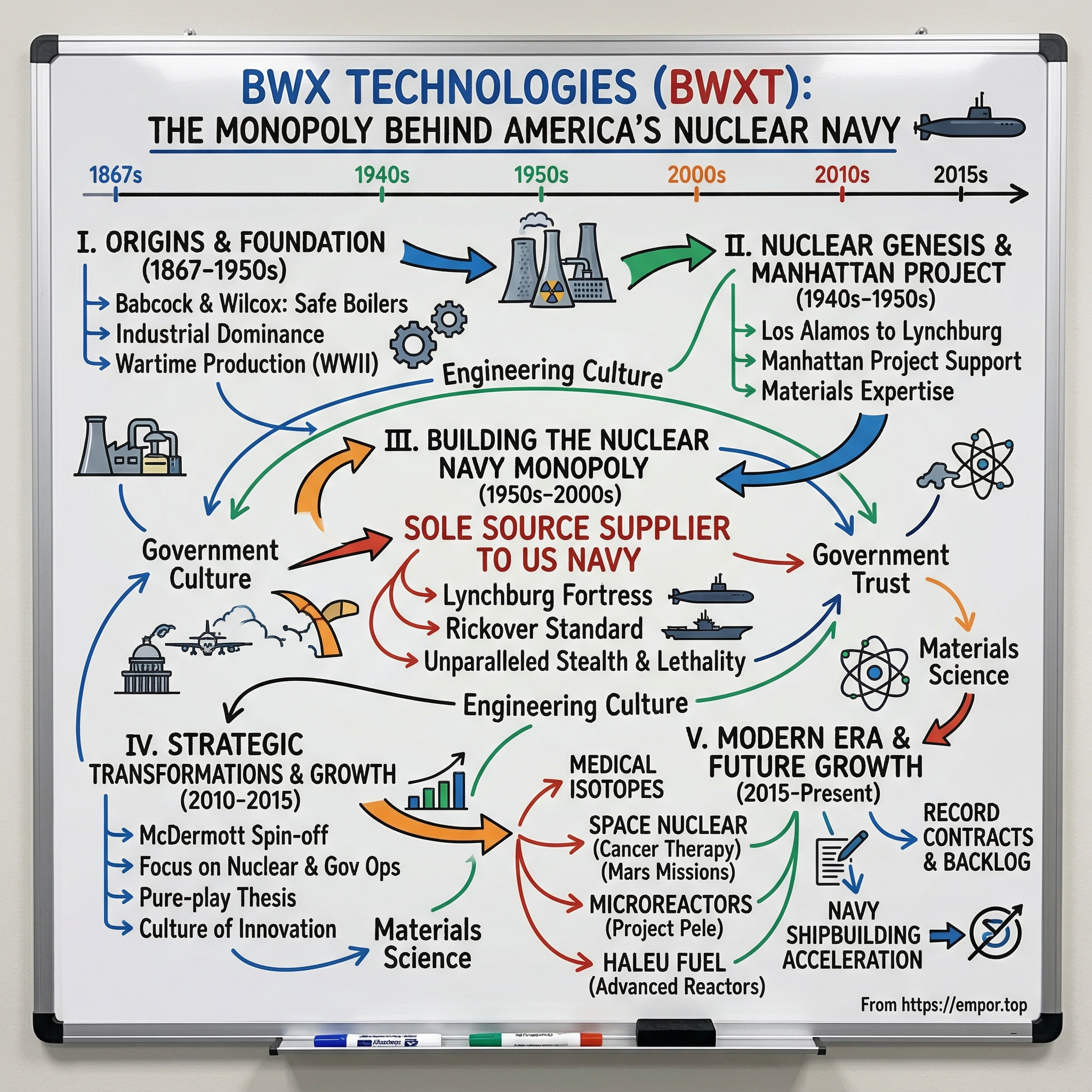

BWX Technologies: The Monopoly Behind America's Nuclear Navy

I. Introduction & Cold Open

Picture this: somewhere beneath the Pacific Ocean, a Virginia-class submarine glides silently through the darkness, its nuclear reactor humming with barely perceptible vibration. Above the waves, a Ford-class aircraft carrier—a floating city of 5,000 souls—cuts through choppy seas, powered by twin reactors that will run for 25 years without refueling. Every single nuclear core powering these vessels, every fuel assembly, every critical component that enables America's naval dominance, comes from one company: BWX Technologies.

It's a monopoly so complete, so entrenched, that the U.S. Navy literally cannot function without it. Yet most investors have never heard of BWXT, this $10.24 billion market cap company tucked away in Lynchburg, Virginia. The impossible question isn't whether BWXT has a moat—it's how a 150-year-old boiler company engineered itself into the most critical supplier for America's nuclear fleet, with no realistic competitor in sight.

This is the story of patient capital deployed over decades, of betting on technologies before markets existed, of navigating the treacherous waters between private enterprise and national security. It's about how mundane steam boilers evolved into nuclear reactors, how government contracts became annuities, and why sometimes the best monopolies hide in plain sight, wrapped in complexity and classification stamps.

We'll trace the arc from Babcock & Wilcox's founding in 1867 through the Manhattan Project, the birth of nuclear propulsion under Admiral Rickover's iron grip, corporate spin-offs and transformations, to today's nuclear renaissance where BWXT stands ready to capitalize on everything from small modular reactors to Mars-bound spacecraft. Along the way, we'll uncover how this company built barriers so high that even the Chinese military can't replicate what they do.

The numbers tell part of the story: $2.7 billion in 2024 revenue, contracts stretching decades into the future, operating margins that would make software companies jealous. But the real story is about engineering culture, institutional knowledge passed down through generations, and the peculiar dynamics of being so essential to national security that your customer can never leave you—and you can never truly compete.

II. Origins: The Babcock & Wilcox Story (1867-1950s)

The Water Tube Revolution

In 1867, while America was still nursing its Civil War wounds, two engineers named George Babcock and Stephen Wilcox were tinkering in a Providence, Rhode Island workshop. They weren't trying to build a defense contractor or a nuclear monopoly—they just wanted to stop boilers from exploding. Industrial America was powered by steam, but boiler explosions killed hundreds annually, turning factories into crime scenes. Babcock and Wilcox's innovation—the water-tube boiler—flipped conventional design on its head, running water through tubes surrounded by hot gases rather than the reverse. It was safer, more efficient, and would become the foundation of an empire.

The early B&W company embodied a peculiar American archetype: the engineering company as educator and evangelist. In 1875, they published "Steam: Its Generation and Use"—not just a manual but a manifesto for the steam age. This wasn't typical corporate literature; it was dense, technical, almost obsessively detailed. The book would be updated and republished continuously for the next 150 years, now in its 42nd edition—the longest continuously published engineering text in the world. This commitment to documentation and knowledge transfer would prove prophetic when B&W entered the nuclear age, where institutional memory meant everything.

Industrial Dominance and Government Ties

By the 1920s, Babcock & Wilcox had become the Intel of the steam age—their boilers powered everything from battleships to power plants. The company developed a reputation for taking on the impossible: boilers that could withstand earthquake zones, installations in the most remote locations, custom solutions for industries that didn't exist five years prior. They weren't just vendors; they were partners in America's industrialization, embedded so deeply in critical infrastructure that extricating them would be unthinkable.

This is where B&W learned its first crucial lesson about government contracts: reliability trumps everything. When your boiler powers a destroyer or a municipal power plant, 99% uptime isn't good enough. The company developed quality control processes that seemed excessive for the era—multiple inspections, redundant testing, documentation that could fill warehouses. Critics called it bureaucratic; B&W called it survival. When you're building for the U.S. Navy, one catastrophic failure doesn't just cost money—it costs lives and contracts that span decades.

The Engineering Culture That Would Build Reactors

What distinguished B&W wasn't just technical competence but an almost fanatical engineering culture. Engineers weren't support staff; they were the company. Promotions went to those who could solve the hardest problems, not those who could sell the most boilers. The company recruited from MIT, Carnegie Tech, and the Naval Academy, creating a pipeline of talent that understood both thermodynamics and discipline. One fascinating detail emerges from the archives: Thomas Edison purchased B&W boiler No. 92 for his Menlo Park laboratory in 1878. Think about that—the wizard of Menlo Park, at the very moment he was inventing the light bulb, trusted B&W to power his workshop. This wasn't just a customer relationship; it was a meeting of American innovation titans, each pushing the boundaries of what technology could achieve.

By the 1930s, B&W had become so integral to American infrastructure that they weren't just suppliers—they were strategic assets. Between 1941 and 1945, B&W designed and delivered 4,100 marine boilers for combat and merchant ships, including 95 percent of the US fleet in Tokyo Bay at Japanese surrender. When Admiral Nimitz accepted Japan's surrender on the USS Missouri, B&W boilers were literally powering history. This wartime production surge wasn't just about volume; it was about proving that B&W could scale quality manufacturing under pressure, a skill that would prove invaluable when nuclear technology arrived.

The transition from the 1940s to the 1950s marks where our story pivots from industrial dominance to nuclear destiny. B&W had spent eight decades perfecting the art of containing extreme heat and pressure, managing complex thermodynamic systems, and most critically, building trust with the U.S. military. They were about to discover that building boilers and building reactors weren't so different after all—both required fanatical attention to safety, deep materials science expertise, and the ability to operate in highly regulated environments where failure wasn't an option.

III. The Manhattan Project & Nuclear Genesis (1940s-1950s)

From Los Alamos to Lynchburg

The telegram arrived at B&W headquarters in 1943, marked with wartime secrecy classifications that few civilians ever saw. The U.S. government needed a company that could work with exotic materials, maintain absolute secrecy, and deliver components with tolerances measured in thousandths of an inch. Previously Babcock & Wilcox Company, BWX Technologies (BWXT) helped provide materials and process development for the Manhattan Project from 1943 – 1945. The executives who read that telegram couldn't have known they were signing up for a relationship that would define their company for the next century.

What B&W brought to the Manhattan Project wasn't nuclear expertise—nobody had that yet. They brought something more valuable: decades of experience working with materials under extreme conditions. When you're building boilers that operate at 2,400°F and 3,500 psi, you learn things about metallurgy that textbooks don't teach. You understand how metals behave under stress, how welds fail, how to inspect for microscopic flaws that could become catastrophic. These weren't sexy capabilities, but they were exactly what the atomic age needed.

The Nautilus Moment: Captain Rickover's Nuclear Submarine Vision

In 1951, a cantankerous naval officer named Hyman Rickover arrived at B&W's door with an impossible request. Congress had authorized the construction of a nuclear-powered submarine for the U.S. Navy, which was planned and personally supervised by Captain Hyman G. Rickover, known as the "Father of the Nuclear Navy." Rickover wasn't looking for vendors; he was looking for partners in an endeavor that had never been attempted—putting a nuclear reactor inside a submarine hull.

The site also designed and fabricated components for the USS Nautilus, the world's first nuclear-powered submarine. This wasn't just another contract; it was B&W's entry into the most exclusive club in defense contracting. Our legacy in naval nuclear propulsion dates back to the 1950s, when we designed and fabricated components for the USS Nautilus, the world's first nuclear-powered submarine. On January 17, 1955, Nautilus SSN-571 with the Mark II reactor installed began its sea trials. Not long after leaving the pier, Commander Wilkinson had a crew member relay this message to the shore: "Underway on Nuclear Power."

What made B&W perfect for Rickover wasn't their nuclear expertise—nobody had that yet. It was their obsession with quality that bordered on paranoia. Rickover famously interviewed every single officer who would serve on nuclear vessels, tens of thousands of interviews over his career. He applied the same scrutiny to contractors. B&W's culture of over-engineering, of testing beyond requirements, of documentation that seemed excessive—these weren't bugs to Rickover; they were features.

The Knowledge Monopoly Begins

In 1958, BWXT began fabricating research and test reactor fuel for laboratories and universities across the nation. This expansion beyond military applications was strategic genius. By becoming the supplier to academic and research institutions, B&W wasn't just building reactors; they were building the entire ecosystem of nuclear expertise. Every PhD student who worked with B&W fuel, every researcher who used their components, became part of an informal network that reinforced B&W's position at the center of American nuclear technology.BWXT is the only North American company to continuously manufacture nuclear steam generators for the commercial nuclear power industry since the 1950s. Let that sink in—while competitors entered and exited, while nuclear optimism turned to Three Mile Island pessimism and back again, B&W never stopped. This consistency created something money can't buy: institutional knowledge passed through generations of engineers, each improving on the last, each adding to a body of knowledge that exists nowhere else.

The partnership between B&W and Rickover's Navy wasn't just business—it was symbiotic evolution. The Navy needed absolute reliability; B&W needed to learn nuclear. Together, they created standards that became industry gospel. When commercial nuclear power arrived in the late 1950s, B&W didn't have to scramble to understand this new technology. They had been living it, breathing it, perfecting it for years. They manufactured components for the first full-scale peacetime nuclear power plant in the US – the Shippingport Atomic Power Station in Pennsylvania, leveraging everything they'd learned from Nautilus.

By the end of the 1950s, B&W had achieved something remarkable: they were simultaneously the most trusted name in naval nuclear propulsion and a pioneer in commercial nuclear power. This wasn't diversification—it was domination across the entire nuclear ecosystem. Every admiral who commanded a nuclear vessel, every engineer who worked on a reactor, every regulator who inspected a plant—they all knew B&W. The company had become synonymous with nuclear excellence, setting the stage for a monopoly that would only strengthen over the coming decades.

IV. Building the Nuclear Navy Monopoly (1960s-2000s)

The Fortress of Lynchburg

By 1965, something profound had happened in Lynchburg, Virginia. What started as a boiler manufacturing town had transformed into America's nuclear arsenal—not of weapons, but of the propulsion systems that would project American power across every ocean. To date, the Navy's submarines and aircraft carriers have safely steamed millions of miles using components manufactured by BWXT. This wasn't luck; it was the result of a deliberate strategy to become so essential that replacement was unthinkable.

The geography itself became part of the moat. BWXT's Lynchburg facility wasn't just a factory; it was a fortress of classified manufacturing techniques, specialized equipment that existed nowhere else, and most critically, people who had spent decades perfecting processes that couldn't be documented in any manual. When a welder at BWXT joined a nuclear-grade component, they weren't following instructions—they were practicing an art passed down through apprenticeships, refined through thousands of repetitions, validated through decades without failure.

The Rickover Standard

Admiral Rickover's influence on BWXT extended far beyond contracts. He created a culture of paranoid excellence that aligned perfectly with B&W's engineering DNA. Rickover would show up unannounced at facilities, quiz workers on procedures, demand explanations for the smallest deviations. One story from the 1970s tells of Rickover finding a microscopic imperfection in a weld x-ray that three inspectors had missed. Rather than just fixing that weld, BWXT re-examined their entire inspection process, ultimately developing new techniques that became industry standard.

This obsession with perfection created an unexpected competitive advantage: regulatory capture through excellence. As the Nuclear Regulatory Commission developed standards for naval reactors, they essentially codified BWXT's processes. Why? Because BWXT's methods had proven themselves through millions of hours of safe operation. Competitors couldn't just meet regulations—they had to meet the "BWXT standard" that sat above and beyond any written requirement.

The Platform Evolution

Our legacy in naval nuclear propulsion dates back to the 1950s, when we designed and fabricated components for the USS Nautilus, the world's first nuclear-powered submarine. Driven by the early objective to minimize fueling interruptions, as seen in today's design of submarine reactors lasting a boat's lifetime and carrier reactors requiring only a single mid-life fueling, the Naval Nuclear Propulsion Program now empowers the U.S. Navy with the ability to maintain unparalleled stealth and lethality across vast oceanic distances.

Today, our reactors power the Navy's Ohio, Virginia, Seawolf and Los Angeles-class submarines. Our reactors also power Nimitz and Ford-class aircraft carriers. Each platform represented not just a new contract but a deepening of the relationship. The Ohio-class submarines, which carry America's sea-based nuclear deterrent, required components so precise that BWXT had to invent new manufacturing techniques. The Virginia-class, designed for the post-Cold War world, needed reactors that could last the entire 33-year life of the submarine without refueling—a requirement that only BWXT could meet.

The Clearance Moat: BWXT's Exclusive Nuclear Facilities

BWXT's Lynchburg facility achieved a distinction that became the ultimate competitive moat, owning the only two Category 1 nuclear facilities licensed by the Nuclear Regulatory Commission to store and process highly enriched uranium. This wasn't just a license—it was a fortress. The security requirements alone would bankrupt most companies: armed guards, blast-resistant buildings, surveillance systems that could track a dust particle. But more than physical security, it required decades of perfect safety records, relationships with intelligence agencies, and a workforce with security clearances that took years to obtain.

NOG-L fabricates fuel-bearing precision components that serve as power units for the nuclear navy. NOG-L is the sole source supplier of these products and services in support of national security, and as such the Facility will remain in operation as long as there is a U.S. nuclear navy. This EPA assessment from a regulatory review captures the reality: BWXT isn't just a contractor; they're infrastructure as essential as the Pentagon itself.

The Economics of Monopoly

The beauty of BWXT's position wasn't just technical—it was economic. Naval nuclear contracts operate on a cost-plus basis, meaning BWXT is guaranteed a profit margin on top of their costs. But here's the genius: the "costs" include maintaining capabilities that no one else has. Every specialized machine, every cleared employee, every safety system—these aren't expenses; they're moat-widening investments that the government pays for.

Consider the replacement cost for a competitor. They would need to: - Build facilities capable of handling highly enriched uranium (minimum $500 million) - Obtain regulatory approvals (5-10 years, if ever) - Recruit and train a workforce with security clearances (another 5-10 years) - Develop the institutional knowledge to meet Navy specifications (priceless) - Survive decades of losses while proving reliability

The total cost? Conservatively $5-10 billion and 15-20 years, with no guarantee of success. And during that time, BWXT would continue improving, moving the target further away. This is why no serious competitor has emerged in 70 years.

Quality Incidents and Trust Recovery

The relationship wasn't without turbulence. In 2009, a saw used to cut fuel components discharged oil containing highly enriched uranium, triggering an alert and NRC response. Rather than hiding or minimizing, BWXT's response became a masterclass in crisis management. They over-communicated, over-corrected, and turned the incident into an opportunity to further strengthen procedures. The Navy's response? They increased orders. Why? Because BWXT had proven that even their mistakes were handled better than anyone else's successes.

This pattern repeated throughout the decades: an incident would occur, BWXT would respond with overwhelming competence, and their position would somehow strengthen. It's counterintuitive but logical—every successfully managed crisis increased the switching costs for the Navy. Better the devil you know, especially when that devil has never had a catastrophic failure.

By 2000, BWXT's monopoly was complete. They weren't just the best supplier of naval nuclear components; they were the only supplier. The knowledge, facilities, clearances, and trust had created barriers so high that the U.S. government had essentially no choice but to continue the relationship. The stage was set for the next phase: corporate transformation that would unlock the value of this irreplaceable asset.

V. The Spin-off & Transformation (2010-2015)

The McDermott Years: Hidden Value

In 2010, BWXT was buried inside McDermott International, a sprawling conglomerate focused on offshore oil and gas construction. To McDermott's management, BWXT was a stable cash generator but a strategic orphan—nuclear submarines had little synergy with laying pipelines in the Gulf of Mexico. This corporate neglect, paradoxically, protected BWXT's culture. While McDermott chased boom-bust energy markets, BWXT quietly strengthened its nuclear fortress, investing in capabilities that would prove prescient when nuclear's renaissance arrived.

It was formed in 2010, named Babcock & Wilcox Nuclear Energy, by the merger of two business units, Nuclear Power Generation Group and Modular Nuclear Energy. This company was later renamed BWXT NE following the July 2015 spin-off of Babcock & Wilcox. This internal reorganization was the first sign that someone understood what they had—not just a government contractor, but a nuclear technology platform with untapped potential.

Enter Rex Geveden: The NASA Engineer Who Transformed BWXT

The transformation accelerated when Geveden arrived in 2015 as COO before advancing to CEO in 2017. His 17-year NASA career, including service as the agency's COO managing a $16 billion portfolio and 10 field centers, brought crucial leadership experience. Geveden saw what others missed: BWXT wasn't just a government contractor; it was a nuclear technology platform waiting to be unleashed.

Geveden brought a NASA engineer's perspective to a company that had been thinking like a defense contractor. At NASA, he'd learned that the impossible just takes longer, that technologies developed for space often find terrestrial applications, and that the future belongs to those who invest before markets exist. He looked at BWXT's capabilities—the only company that could handle highly enriched uranium, decades of reactor expertise, unmatched manufacturing precision—and saw opportunities beyond submarines.

The Strategic Divorce

In 2015, The Babcock & Wilcox Company spun off its power generation business to allow BWXT to focus on government and nuclear operations. This wasn't just corporate restructuring; it was strategic focus at its finest. The power generation business—coal boilers, environmental equipment, conventional energy—was mature, cyclical, and commoditizing. The nuclear business was growing, protected by massive barriers to entry, and positioned for a renaissance.

The spin-off was executed with surgical precision. BWXT kept everything nuclear: the naval contracts, the enriched uranium facilities, the nuclear fuel capabilities, the cleared workforce. Everything else—the legacy coal business that had sustained B&W for a century—was jettisoned into a separate company (Babcock & Wilcox Enterprises) that would struggle and eventually file for bankruptcy in 2019. Meanwhile, BWXT would thrive.

The Pure-Play Thesis

Wall Street initially didn't understand what they were looking at. Here was a company with $1.4 billion in revenue, almost entirely from government contracts, in an industry most investors avoided (nuclear), with capital intensity that would scare off growth investors. The initial market cap of around $3 billion reflected this confusion. But Geveden and his team saw what others didn't: this was a subscription business disguised as a manufacturer.

Think about the economics: multi-decade contracts with the U.S. government, no real competition, pricing that adjusts for inflation, and a customer that literally cannot switch suppliers. The Navy's shipbuilding schedule was public information—every Virginia-class submarine, every Ford-class carrier represented decades of guaranteed revenue for BWXT. This wasn't a cyclical industrial; it was an annuity stream backed by the full faith and credit of the United States government.

Building for the Future

Even as the spin-off was being executed, Geveden was positioning BWXT for opportunities that didn't yet exist. The company had attempted to develop the mPower small modular reactor (SMR) from 2009-2017, ultimately abandoning it after spending hundreds of millions. The mPower reactor – no longer in development as of 2017 – was a scalable, modular reactor with the capacity to provide output in increments of 180 MWe. To many, this looked like failure. To Geveden, it was tuition—expensive learning that would position BWXT perfectly when the nuclear renaissance arrived.

The mPower "failure" taught BWXT crucial lessons: don't go alone (find partners), don't bet on unproven markets (wait for demand signals), but most importantly, keep developing capabilities even without immediate customers. The technologies developed for mPower—manufacturing techniques for small reactors, modular construction methods, advanced fuel handling—would find applications in everything from naval reactors to space propulsion systems.

Cultural Revolution

Perhaps the most important transformation was cultural. BWXT had always been an engineering company, but under Geveden, it became an innovation company that happened to do engineering. The difference was subtle but profound. Engineers solve defined problems; innovators identify problems worth solving. This shift would prove prescient as opportunities emerged in medical isotopes, space nuclear propulsion, and microreactors—markets that didn't exist when the transformation began.

The 2015 spinoff marked BWXT's emergence from the shadows. No longer buried in a conglomerate, no longer weighed down by declining coal markets, the company could finally show investors what a nuclear monopoly looked like when properly managed and strategically positioned. The stage was set for the next act: capitalizing on a nuclear renaissance that was just beginning to stir.

VI. Modern Era: The Nuclear Renaissance Play (2015-Present)

The Two-Headed Monster: Government and Commercial

Post-spinoff, BWXT organized itself into two distinct but synergistic segments. It operates through two segments, Government Operations and Commercial Operations. This wasn't just organizational structure—it was strategic architecture designed to capture value across the entire nuclear ecosystem while maintaining the security requirements of defense work.

Government Operations became the fortress, the unchangeable core that would fund everything else. The numbers tell the story of dominance: BWX Technologies has secured approximately $2.6 billion in contracts from the U.S. Naval Nuclear Propulsion Program to produce naval nuclear reactor components. The work supports ongoing construction of Virginia- and Columbia-class submarines and includes select components for Ford-class aircraft carriers. These aren't just contracts; they're multi-decade commitments that provide the financial foundation for BWXT to take risks elsewhere.

The Columbia-class submarine program alone represents a generational opportunity. These submarines will replace the Ohio-class as America's sea-based nuclear deterrent, with each submarine costing over $8 billion. BWXT's content per submarine isn't disclosed, but industry estimates suggest hundreds of millions per boat, with 12 submarines planned through the 2040s. This is baseload revenue that would make utility companies envious.

The Canadian Acquisition: GE Hitachi Nuclear Energy Canada Purchase

In December 2016, BWXT completed its acquisition of GEH-C, roughly doubling its footprint in Canada. This wasn't just geographic expansion—it was strategic positioning for the CANDU reactor market, which represents 19 operating reactors in Canada plus derivatives in six other countries. The acquisition brought fuel manufacturing, fuel handling systems, and critical expertise in heavy water reactor technology—capabilities that perfectly complemented BWXT's existing portfolio.

The timing was exquisite. Bruce Power had just committed to a CAD 8 billion refurbishment program, and BWXT Canada had already secured contracts worth hundreds of millions for steam generators. The GEH-C acquisition meant BWXT could now offer complete solutions—not just components but entire systems, from fuel to steam generators to tooling. This full-service capability created switching costs so high that customers would think twice before fragmenting their supply chain.

Medical Isotopes: From Weapons to Medicine

In August 2018, BWXT closed on its acquisition of Sotera Health's Nordion medical isotope business, a move that seemed puzzling to outsiders but was brilliant to those who understood nuclear processing. The acquisition accelerates and de-risks BWXT's entry into the medical radioisotope market by adding licensed infrastructure, approximately 150 highly trained and experienced personnel, and two production centers to BWXT.

The synergies weren't obvious but they were profound. Medical isotopes require the same skills BWXT had perfected: handling radioactive materials, precision processing, regulatory compliance, and absolute reliability. But unlike defense work, medical isotopes offered exposure to healthcare markets growing at double-digit rates. Cancer diagnoses were increasing globally, and isotopes like Technetium-99m were essential for millions of procedures annually.

What made this acquisition particularly clever was the infrastructure overlap. The same facilities that process uranium for the Navy could, with modifications, produce medical isotopes. The same quality systems that ensure submarine reactors don't fail could ensure medical isotopes meet pharmaceutical standards. BWXT was leveraging decades of nuclear expertise into a completely new market without starting from scratch.

Space: The Final Frontier

BWXT awarded $18.8 million contract from NASA to initiate conceptual designs for a nuclear thermal propulsion reactor. This wasn't BWXT's first rodeo with space nuclear systems, but it marked a new chapter. Nuclear propulsion could cut Mars transit time in half, and BWXT was the only company with both the nuclear expertise and the security clearances to build these systems.

The space opportunity exemplified BWXT's platform strategy. The same technologies that power submarines could, with modifications, power spacecraft. The same engineers who design naval reactors could design space reactors. The same facilities that manufacture military components could manufacture space components. Every new application leveraged the same core capabilities, creating economies of scope that competitors couldn't match.

Microreactors: The Pentagon's New Toy

BWXT awarded contract from U.S. Department of Defense to build the first advanced nuclear microreactor in the United States. Project Pele, as it's known, represents a paradigm shift in military energy. Instead of vulnerable fuel convoys in combat zones, the military could deploy small, portable nuclear reactors. BWXT wasn't just building a product; they were creating an entirely new market.

The microreactor opportunity showcases BWXT's unique position at the intersection of nuclear technology and national security. No commercial nuclear company has the security clearances to work on military projects. No defense contractor has the nuclear expertise to build reactors. BWXT sits alone in the Venn diagram overlap, a position that becomes more valuable as the military embraces distributed nuclear power.

The Integration Machine

What distinguishes BWXT in the modern era isn't just winning contracts—it's the ability to integrate diverse nuclear applications into a coherent platform. Naval reactors teach lessons applied to medical isotopes. Medical isotope production generates cash flows that fund space reactor development. Space reactor research produces innovations applicable to microreactors. It's a virtuous cycle where each business strengthens the others.

The financial architecture supports this integration. Government contracts provide stable cash flows and fund R&D. Commercial operations offer growth and margin expansion. The combination creates a business model that's both defensive (government backstop) and offensive (commercial growth), a rare combination that explains why BWXT trades at premiums to both pure defense contractors and nuclear utilities.

By 2024, BWXT had transformed from a hidden defense contractor into a nuclear technology platform company. Revenue reached $2.7 billion, margins expanded, and the backlog stretched years into the future. But more importantly, BWXT had positioned itself at the center of every major nuclear trend: the naval buildup, the nuclear medicine boom, the space nuclear renaissance, and the military's embrace of distributed nuclear power. The monopoly wasn't just protected; it was expanding into entirely new domains.

VII. The Numbers & Business Model

The Financial Architecture of a Monopoly

2024 diluted GAAP EPS of $3.07, diluted non-GAAP EPS of $3.33, on revenue of $2.7 billion. These numbers might seem pedestrian to growth investors accustomed to software multiples, but they disguise something remarkable: a business model with the predictability of a utility, the margins of a defense contractor, and the growth of a technology company.

In the last 12 months, BWXT had revenue of $2.78 billion and earned $288.94 million in profits. Earnings per share was $3.14. Break down these numbers and you find something unusual for an industrial company: revenue visibility stretching years into the future, margins that expand despite inflation, and capital allocation optionality that most manufacturers can only dream of.

The Gross Margin Story

Gross margin is 24.15%, with operating and profit margins of 11.66% and 10.39%. For context, Lockheed Martin, one of the most profitable defense contractors, operates with gross margins around 13%. BWXT's superior margins reflect the monopoly premium—when you're the only supplier, you price for value, not competition. But it goes deeper than pricing power.

BWXT's margins embed decades of learning curve effects that competitors can't replicate. Every nuclear component manufactured teaches something about the next one. Every process improvement compounds. When you've manufactured thousands of nuclear components with zero catastrophic failures, your manufacturing process becomes incredibly efficient. Waste approaches zero, rework becomes rare, and first-pass yield approaches 100%. These aren't improvements you can buy; they must be earned through decades of repetition.

The Cost-Plus Paradise

The government operations segment operates largely on cost-plus contracts, a structure that seems archaic in the age of fixed-price everything. But for BWXT, it's genius. Cost-plus means BWXT is guaranteed a profit margin (typically 8-12%) on top of all allowable costs. This includes not just direct manufacturing costs but also overhead, R&D, facility improvements, and talent development. The government essentially funds BWXT's competitive moat.

Here's where it gets interesting: the "costs" in cost-plus include maintaining capabilities that no one else has. That specialized machine that can only manufacture nuclear components? That's a reimbursable cost. Those engineers with decades of experience? Reimbursable. The security infrastructure required for handling enriched uranium? Reimbursable. BWXT is paid to maintain and expand its monopoly.

Cash Flow Dynamics

In the last 12 months, operating cash flow was $426.05 million and capital expenditures -$156.59 million, giving a free cash flow of $269.46 million. The cash conversion is remarkable for a capital-intensive manufacturer. Most industrial companies struggle to convert 50% of net income to free cash flow; BWXT consistently exceeds 90%.

The secret lies in working capital dynamics unique to government contracting. BWXT often receives progress payments before incurring costs, creating negative working capital in growth periods. When the Navy orders reactor components for a new submarine, BWXT gets paid as milestones are reached, not upon final delivery years later. This creates a float similar to insurance companies, where BWXT holds and can invest customer money before delivering products.

The Dividend and Capital Allocation

This stock pays an annual dividend of $1.00, which amounts to a dividend yield of 0.92%. The modest yield might disappoint income investors, but it reflects intelligent capital allocation. BWXT is in growth mode, investing in medical isotopes, space systems, and microreactors. Every dollar retained can be invested at returns far exceeding the cost of capital.

Management has shown discipline in capital allocation, following a clear hierarchy: 1. Organic growth investments (highest returns, strengthens moat) 2. Strategic acquisitions (expand platform, enter adjacent markets) 3. Debt reduction (though leverage is manageable) 4. Dividends (signal confidence, reward patient shareholders) 5. Share buybacks (opportunistic, when stock is clearly undervalued)

The Debt Situation

The company has $55.44 million in cash and $1.20 billion in debt, giving a net cash position of -$1.14 billion. At first glance, this leverage might concern conservative investors. But context matters. BWXT's debt is backed by multi-decade government contracts with virtually zero default risk. The debt-to-EBITDA ratio of approximately 3x is comfortable for a business with BWXT's stability.

More importantly, the debt is strategic. It was largely incurred for acquisitions (GE Hitachi Canada, Nordion) that are already accretive. The interest coverage ratio exceeds 5x, providing ample cushion even in downturns. And with interest rates potentially peaking, BWXT has the option to refinance at lower rates in coming years, providing an easy earnings boost.

Segment Performance Deep Dive

Government Operations generates roughly 70% of revenue but 80% of operating income, reflecting higher margins from sole-source contracts. This segment grows steadily at 3-5% annually, tracking Navy shipbuilding budgets and inflation adjustments. It's the bedrock that funds everything else.

Commercial Operations, the remaining 30% of revenue, is where the growth lives. Medical isotopes are growing at double-digit rates. Nuclear components for power plants benefit from the nuclear renaissance. This segment has lower margins (for now) but higher growth potential. As it scales, margins should expand toward government levels.

Unit Economics That Compound

The unit economics of BWXT's business model create powerful compounding effects. Consider a single reactor component contract: - Initial contract value: $100 million - Gross margin: 24% - But that's just the beginning... - Maintenance and spare parts: $20 million over reactor life - Fuel supply: $30 million over reactor life - Refurbishment/upgrade: $50 million at mid-life - Total lifetime value: $200 million from $100 million initial contract

This recurring revenue stream, hidden in the contract structure, explains why BWXT's return on invested capital consistently exceeds 15%. Every new reactor component sold creates an annuity stream lasting decades.

Comparison to Software Economics

While BWXT isn't a software company, its economics share surprising similarities: - High customer acquisition cost (winning that first Navy contract) - Near-zero marginal cost for additional units (the hard work is in the first component) - Extreme customer stickiness (100% retention rate) - Expansion revenue opportunities (maintenance, upgrades, fuel) - Network effects (more reactors in service = more data = better products)

The difference? BWXT's moat is even deeper than most software companies. You can rebuild Salesforce with enough engineers and time. You cannot rebuild BWXT's capabilities without decades and billions of dollars, if ever.

The numbers tell a story of a business model perfected over decades: predictable revenue, expanding margins, strong cash generation, and returns on capital that compound over time. This isn't just a government contractor or a nuclear manufacturer—it's a tollbooth on America's nuclear infrastructure, collecting fees that grow more valuable as nuclear technology becomes increasingly critical to energy, defense, medicine, and space exploration.

VIII. Competitive Moats & Strategic Position

The Regulatory Moat: Licensed to Print Money

BWXT owns the only two Category 1 nuclear facilities licensed by the Nuclear Regulatory Commission to store and process highly enriched uranium. This isn't just a competitive advantage—it's a legalized monopoly. Obtaining such a license today would require: - 5-10 years of applications and reviews - Hundreds of millions in facility construction - Perfect safety records during probationary periods - Political support at federal and state levels - Community acceptance (good luck building a new enriched uranium facility anywhere)

The license itself becomes self-reinforcing. Every year BWXT operates without incident strengthens their position. Every competitor who might attempt to get licensed faces the question: "Why should we approve you when BWXT has operated safely for 70 years?" The regulatory moat deepens with time, the opposite of most competitive advantages that erode.

The Knowledge Moat: Tacit Understanding That Can't Be Stolen

Nuclear manufacturing isn't like making cars or computers where knowledge can be documented and transferred. Much of BWXT's expertise is tacit—understood but not easily articulated. How do you know when a weld on a nuclear component is perfect? How do you predict how materials will behave under decades of neutron bombardment? These aren't things you learn from textbooks; they're learned through thousands of repetitions under master craftsmen.

BWXT's Lynchburg facility operates like a medieval guild where knowledge passes from master to apprentice over decades. New engineers spend years shadowing veterans before they're allowed to make critical decisions. This apprenticeship model seems anachronistic in the age of YouTube tutorials, but it's the only way to transfer knowledge that exists in fingertips and instincts rather than manuals.

The Trust Moat: 70 Years of Not Screwing Up

In businesses where failure means catastrophe, trust becomes the ultimate moat. BWXT has manufactured components for hundreds of naval reactors. Not one has suffered a catastrophic failure. This isn't just a good track record—it's a perfect one in an arena where perfection is the minimum acceptable standard.

Trust compounds in fascinating ways. When BWXT proposes a new reactor design, the Navy listens because BWXT has earned the right to innovate. When BWXT suggests process improvements, regulators approve them because BWXT has never given them reason to doubt. This trust accelerates everything—approvals come faster, contracts are sole-sourced, and problems are solved collaboratively rather than adversarially.

The Switching Cost Moat: The $10 Billion "Never Mind"

Imagine the Navy wanted to switch suppliers for nuclear components. The switching costs would be staggering: - New supplier qualification: 5-10 years minimum - Facility construction and certification: $1-2 billion - Workforce training and clearances: 5+ years, $500 million - Parallel operations during transition: $1 billion annually - Risk of program delays: Priceless (literally—you can't put a submarine fleet on hold)

But the real switching cost isn't financial—it's existential. The Navy's nuclear program has operated for 70 years without a reactor accident. This perfect record is the foundation of political support for nuclear vessels. One accident with a new supplier could end the nuclear Navy. No admiral would risk their career, and America's naval supremacy, to save money on reactor components.

The Scale Moat: The Denominator Dominance

BWXT manufactures nuclear components at a scale no one else approaches. This creates classic economies of scale, but with a twist. The fixed costs—specialized facilities, cleared personnel, regulatory compliance—are massive. But spread across hundreds of reactor components, the unit costs become manageable. A competitor building five components a year would have astronomical unit costs; BWXT building fifty has competitive costs even on a government cost-plus contract.

Scale also enables specialization. BWXT can afford engineers who spend entire careers perfecting one type of weld or one alloy composition. This specialization drives quality improvements that further separate BWXT from potential competitors. It's a virtuous cycle: scale enables specialization, which improves quality, which wins more contracts, which increases scale.

The Network Moat: The Ecosystem Effect

BWXT isn't just a supplier; they're the hub of America's naval nuclear ecosystem. Every admiral who commanded a nuclear vessel knows BWXT. Every nuclear engineer in the Navy trained on BWXT components. Every shipbuilder designs vessels around BWXT's reactor specifications. This network creates lock-in that goes beyond any single contract.

The network extends to suppliers too. BWXT has cultivated relationships with specialized material suppliers, precision manufacturers, and testing facilities that have evolved to serve BWXT's specific needs. These suppliers have made investments specific to BWXT's requirements. A new competitor would need to rebuild this entire ecosystem, not just their own capabilities.

The Innovation Moat: R&D Funded by Uncle Sam

BWXT's position allows them to conduct R&D with patient capital—the government's. When BWXT develops new manufacturing techniques or materials, the Navy funds it through cost-plus contracts. When BWXT explores space nuclear propulsion, NASA pays. This subsidized R&D creates an innovation advantage that compounds over time.

Commercial companies must justify R&D by near-term returns. BWXT can pursue decade-long research programs because their customer (the government) thinks in decades too. This patient capital has produced breakthrough technologies in nuclear fuel, reactor design, and manufacturing processes that maintain BWXT's technical leadership.

The Cultural Moat: The Rickover DNA

Admiral Rickover's influence on BWXT created a culture that's nearly impossible to replicate. It's a culture of paranoid perfectionism, where good enough never is, where every failure is analyzed to exhaustion, where safety isn't a priority—it's the only priority. This culture, embedded over decades, guides thousands of daily decisions in ways that procedures and manuals never could.

New employees don't just learn processes; they're indoctrinated into a way of thinking about nuclear technology. They learn that cutting corners isn't just wrong—it's unthinkable. This cultural programming creates a workforce that self-polices to standards higher than any regulator requires. You can't hire this culture from competitors because it doesn't exist anywhere else.

The Integration Moat: The Whole Greater Than Parts

BWXT's various moats don't just add to each other—they multiply. Regulatory approval is easier because of the trust moat. The trust moat is stronger because of the knowledge moat. The knowledge moat deepens because of the scale moat. Each reinforces the others in a system that becomes increasingly difficult to assault.

This integration appears in operations too. BWXT's naval nuclear expertise informs their medical isotope business. Their medical isotope production capabilities enhance their space nuclear systems. Their space nuclear research improves their naval reactors. Every business unit strengthens the others, creating synergies that a focused competitor couldn't match.

The strategic position BWXT occupies is perhaps unique in American business: a private company with monopoly control over critical national security infrastructure, protected by moats that strengthen with time, expanding into adjacent markets where the same advantages apply. It's not just a good business—it's an irreplaceable one.

IX. Growth Vectors & Future Opportunities

The SMR Revolution: BWXT's Second Act

The small modular reactor (SMR) revolution is finally happening, a decade after BWXT's expensive mPower failure. But that failure was tuition for what's coming. While BWXT won't build their own SMR, they're positioned to be the essential supplier to everyone who does. Every SMR design needs nuclear-grade components, fuel, and specialized manufacturing—exactly what BWXT provides.

The SMR market could reach $300 billion by 2040, and BWXT doesn't need to win the reactor design competition to win big. They're selling picks and shovels to the gold miners. Whether TerraPower, NuScale, or X-energy wins, they'll need BWXT's components. This supplier strategy is lower risk and higher return than competing in reactor design, where winner-take-all dynamics prevail.

Medical Isotopes: From Bombs to Medicine

The medical isotope market is experiencing unprecedented growth, driven by aging populations and advancing diagnostic techniques. BWXT's acquisition of Nordion positioned them perfectly. But the real opportunity isn't in existing isotopes—it's in new ones. BWXT is developing novel isotopes for targeted cancer therapy, where radioactive particles are attached to antibodies that seek out tumors. It's precision medicine meets nuclear physics.

The economics are compelling. A single dose of Lutetium-177 for prostate cancer can cost $50,000. BWXT can produce it using the same facilities that process uranium for the Navy. The margins are software-like, the market is growing at 15% annually, and BWXT has one of the few facilities capable of handling the radioactive materials. This could be a billion-dollar business by 2030.

Space Nuclear: The Mars Economy

BWXT awarded $18.8 million contract from NASA to initiate conceptual designs for a nuclear thermal propulsion reactor—but this is just the appetizer. NASA's Artemis program aims to establish permanent lunar bases by 2030. Mars missions will follow. All need nuclear power—solar panels don't work well during 14-day lunar nights or Martian dust storms.

BWXT is developing two space nuclear technologies: propulsion and power. Nuclear propulsion could cut Mars travel time from nine months to three, reducing radiation exposure and mission complexity. Nuclear power systems could provide megawatts of electricity for lunar bases or Mars colonies. The market doesn't exist yet, but when it does, BWXT will be the only qualified supplier. SpaceX might get us to Mars, but BWXT will power our stay.

Microreactors: Distributed Nuclear Power

Project Pele, BWXT's microreactor for the Defense Department, is a prototype for something bigger: distributed nuclear power. Imagine nuclear reactors small enough to fit in a shipping container, safe enough to operate without operators, cheap enough to compete with diesel generators. Applications are endless: remote military bases, isolated communities, backup power for data centers, emergency response to natural disasters.

The microreactor market could revolutionize energy access. Alaska villages currently pay $0.50/kWh for diesel-generated electricity. A BWXT microreactor could provide power at $0.10/kWh for 20 years without refueling. The military alone could deploy hundreds. The civilian market could be thousands. At $20 million per unit with 40% gross margins, this could rival BWXT's naval business within a decade.

The HALEU Opportunity: Fuel for the Future

Most advanced reactors need High-Assay Low-Enriched Uranium (HALEU)—uranium enriched to 5-20%, versus 3-5% for current reactors. The U.S. Department of Energy (DOE) estimates the domestic demand for HALEU could reach 50 metric tons per year by 2035. At present only Russia and China have the infrastructure to produce HALEU at scale. This is a national security crisis and a massive opportunity.

BWXT will produce over two metric tons of HALEU over the next five years, with several hundred kilograms expected to be available as early as 2024. They're one of only two U.S. facilities capable of processing highly enriched uranium down to HALEU levels. This isn't just about capturing market share—it's about creating the market. Every advanced reactor demonstration needs HALEU, and BWXT will be one of the only domestic suppliers.

The Climate Change Dividend

Nuclear power is having its iPhone moment. After decades in the wilderness, nuclear is suddenly cool again. Climate change has reframed the debate: it's not nuclear versus renewables, it's zero-carbon versus fossil fuels. Nuclear provides baseload power that renewables can't, without the emissions coal and gas produce. Countries are extending reactor lifespans, restarting shuttered plants, and planning new builds.

For BWXT, this renaissance translates directly to revenue. Every reactor life extension needs replacement parts—steam generators, reactor vessel heads, fuel assemblies. BWXT is one of the few companies capable of manufacturing these components to nuclear specifications. A single steam generator replacement can generate $100+ million in revenue. With hundreds of reactors worldwide approaching life extension decisions, this is a multi-billion dollar opportunity.

The Data Center Dark Horse

Here's an opportunity hiding in plain sight: data centers. AI is driving exponential growth in computing power demand. A single ChatGPT query uses 10x the electricity of a Google search. Data centers already consume 2% of global electricity; this could reach 10% by 2030. Tech companies are making net-zero commitments while their power consumption explodes. The solution? Nuclear.

Microsoft is exploring nuclear-powered data centers. Amazon hired nuclear engineers. Google is funding fusion research. But fusion is decades away. Microreactors are here now, and BWXT is building them. A data center powered by a BWXT microreactor could operate carbon-free, grid-independent, with 20 years between refuelings. For tech companies, it's the ultimate virtue signal with actual virtue. For BWXT, it's a market potentially worth hundreds of reactors.

The Hydrogen Economy Enabler

Green hydrogen requires massive amounts of clean electricity for electrolysis. Nuclear is perfect—constant power output, zero emissions, small footprint. But here's the kicker: high-temperature reactors can produce hydrogen directly through thermochemical processes, no electricity needed. BWXT's advanced reactor designs operate at temperatures perfect for hydrogen production.

The hydrogen economy is still nascent, but when it arrives, nuclear hydrogen will be the only scalable solution. BWXT won't just supply reactors; they'll enable an entire industry. Every steel plant switching from coal to hydrogen, every ammonia facility decarbonizing, every synthetic fuel plant—they'll need nuclear heat. BWXT is positioning to be the picks-and-shovels supplier to the hydrogen gold rush.

International Expansion: The Sleeping Giant

BWXT has historically focused on North America, but international opportunities are emerging. Countries without domestic nuclear industries need partners for their nuclear ambitions. Poland is planning six large reactors. The Philippines is reviving the Bataan nuclear plant. Kenya, Ghana, and Nigeria are exploring nuclear options. These countries need not just reactors but entire ecosystems—fuel supply, maintenance, training.

BWXT could partner with reactor vendors to provide the nuclear infrastructure these countries lack. It's not about competing with Russia or China on reactor sales—it's about being the essential partner for Western reactor deployments. Every AP1000, EPR, or SMR deployed internationally could include BWXT components and services. The international market could eventually dwarf the domestic one.

The growth vectors for BWXT aren't independent—they're synergistic. Medical isotope facilities can produce HALEU. HALEU enables advanced reactors. Advanced reactors produce medical isotopes. Space reactor technology improves terrestrial reactors. Each market BWXT enters strengthens their position in others, creating a compounding effect that accelerates over time. The next decade could see BWXT transform from a $10 billion defense contractor to a $50 billion nuclear technology platform, still with room to grow.

X. Risks, Bear Case & Challenges

The Budget Axe: When Uncle Sam Tightens the Belt

Government Operations generates 70% of revenue, making BWXT acutely vulnerable to federal budget dynamics. The Columbia-class submarine program, BWXT's largest growth driver, carries an estimated $130 billion price tag. In an era of $35 trillion national debt and rising interest payments, even sacred defense programs face scrutiny. A budget sequestration like 2013 could delay submarine construction, immediately impacting BWXT's revenue and forcing painful capacity adjustments.

The risk compounds because naval nuclear programs are "platforms of last resort" for cuts—they get protected until they don't. If fiscal crisis forces choosing between social programs and submarines, political calculus becomes unpredictable. One delayed submarine class could crater BWXT's earnings for years, and the market knows it. This binary risk explains why BWXT trades at discounts to pure commercial industrials despite superior returns on capital.

The Black Swan: Nuclear's Achilles Heel

BWXT has never had a catastrophic nuclear incident, but the industry's history haunts every valuation model. Three Mile Island, Chernobyl, Fukushima—each disaster reshapes public perception for decades. BWXT doesn't operate reactors, but they supply critical components. One failed BWXT component causing a radiation release could destroy not just the stock but the entire business model.

The probability is minuscule—BWXT's safety record is impeccable—but the impact would be existential. Insurance can't cover reputational destruction. The Navy might be forced to diversify suppliers regardless of switching costs. Commercial customers would flee. The medical isotope business would face regulatory purgatory. This tail risk, however remote, caps the multiple investors will pay. It's the shadow that nuclear businesses can never fully escape.

Technology Disruption: When Physics Changes the Game

Fusion energy perpetually sits 20 years away, but what if it doesn't? Commonwealth Fusion Systems raised $1.8 billion. Helion presold electricity to Microsoft. TAE Technologies claims commercialization by 2030. If fusion arrives, fission becomes obsolete overnight. BWXT's naval business might survive—submarines need compact power—but the commercial growth story evaporates.

More near-term, alternative technologies threaten specific markets. Accelerator-based isotope production could obsolete reactor-based medical isotopes. Advances in battery technology could make microreactors unnecessary for remote power. Solar panel efficiency improvements and cost reductions continue to erode nuclear's baseload argument. BWXT invests in R&D, but they're defending multiple technological fronts simultaneously.

The Workforce Crisis: When Knowledge Walks Out the Door

BWXT's true asset isn't facilities or contracts—it's the accumulated knowledge of thousands of nuclear engineers and craftsmen. The expansion of the Advanced Technologies business unit, which currently employs 330 people with plans to grow to 400 by 2025, highlights both opportunity and challenge. But nuclear engineering enrollment has declined 50% since 2010. The average age of nuclear workers approaches 50. Within a decade, institutional knowledge accumulated over generations could retire.

Recruitment faces cultural headwinds. Top engineering graduates flock to Silicon Valley, not Lynchburg. Nuclear carries stigma that stock options can't overcome. BWXT invests heavily in training, but you can't microwave expertise that takes decades to develop. Competitors might not beat BWXT's technology, but demographics could hollow out their capabilities from within.

Execution Risk: The mPower Ghost

The mPower reactor failure haunts BWXT's credibility. The BWXT mPower reactor – no longer in development as of 2017 – was a scalable, modular reactor with the capacity to provide output in increments of 180 MWe. After spending hundreds of millions, BWXT abandoned the project, writing off investments and damaging relationships. Management claims lessons learned, but the failure pattern—over-promise, under-deliver, abandon—is etched in institutional memory.

Current growth initiatives—medical isotopes, microreactors, space nuclear—require flawless execution. Each carries technical risk, regulatory uncertainty, and market development challenges. The Nordion acquisition must be integrated while maintaining quality. The microreactor must work perfectly on first deployment. Space reactors must survive launch and operation. One high-profile failure could trigger investor exodus and strategic retrenchment.

Debt and Capital Allocation: The Leverage Time Bomb

The company has $55.44 million in cash and $1.20 billion in debt, giving a net cash position of -$1.14 billion. While manageable at current interest rates and cash flows, this leverage limits flexibility. Rising rates increase interest expense. Economic downturn could pressure government payments. Acquisition opportunities might pass because balance sheet can't support more debt.

More concerning is capital allocation discipline during growth. The temptation to chase trendy markets—hydrogen, carbon capture, cryptocurrency mining—could dilute focus and destroy value. The board must resist empire building and maintain return hurdles. Every dollar invested in speculative ventures is a dollar not strengthening the core monopoly. WeWork started as an office company; BWXT must remain a nuclear company.

Regulatory Quicksand: When Rules Change Mid-Game

Nuclear regulation remains BWXT's biggest moat, but moats can become prisons. NRC licensing processes take years and millions of dollars. Environmental reviews paralyze projects. State regulations layer additional complexity. One activist judge could halt operations pending reviews. One administration could rewrite rules overnight.

The regulatory environment is becoming more unpredictable. Climate activists demand nuclear expansion while opposing uranium mining. Environmental justice movements target nuclear facilities in minority communities. International agreements could restrict enriched uranium handling. BWXT navigates this maze successfully so far, but regulatory complexity compounds annually. Eventually, compliance costs could exceed value creation.

Competition from State Actors: The China Syndrome

China and Russia aren't just competitors—they're state-backed juggernauts unconstrained by profit requirements. China National Nuclear Corporation has unlimited capital and political mandate to dominate nuclear technology. Rosatom offers reactors with financing, fuel, and take-back services no private company can match. These aren't businesses; they're instruments of state power.

While BWXT's U.S. government business remains protected, international opportunities face subsidized competition. Worse, China could develop naval nuclear capabilities that obsolesce BWXT's technology. Intellectual property theft—through cyber espionage or human intelligence—could transfer decades of BWXT innovation overnight. The moat protects against commercial competitors, not nation-states with different rules.

Market Perception: The Perpetual Discount

Despite strong fundamentals, BWXT trades at discounts to inferior businesses. Nuclear carries stigma. Government dependence signals risk. Capital intensity scares growth investors. Complexity confuses generalists. ESG frameworks struggle to categorize nuclear—is it clean energy or environmental hazard? This perception discount might persist regardless of execution.

The investor base remains narrow: defense funds, utility investors, special situations. Passive flows avoid due to sector classification issues. Growth funds want software margins. Value funds fear technological disruption. This limited demand caps valuation regardless of fundamentals. BWXT could execute perfectly and still trade at 15x earnings while inferior software companies command 50x multiples.

The bear case for BWXT isn't about one risk but the confluence of many. Government budget cuts plus execution failures plus regulatory challenges plus competition could create a vicious cycle. Revenue declines, margins compress, debt becomes burdensome, investment stops, competitive position erodes. The monopoly that seemed impregnable could crumble not from frontal assault but from thousand cuts. Investors must weigh exceptional opportunities against existential risks, knowing that in nuclear, when things go wrong, they go very wrong.

XI. Playbook & Investment Lessons

Building Regulatory Capture the Right Way

BWXT's relationship with regulators offers a masterclass in positive regulatory capture—not through lobbying or corruption, but through competence. They became so good at meeting nuclear standards that they effectively wrote them. When the NRC needs to understand manufacturing feasibility, they call BWXT. When the Navy develops specifications, BWXT provides input. This isn't influence peddling; it's expertise so deep that regulators depend on it.

The lesson for investors: look for companies that shape their regulatory environment through excellence, not lobbying expenditure. These companies don't fight regulations; they help write them. Their compliance costs become competitors' barriers to entry. Their processes become industry standards. Their expertise becomes regulatory requirement. It's a moat that strengthens with each regulatory update.

The Power of Forcing Functions

BWXT's monopoly wasn't planned—it was forced by circumstances. The Navy's zero-tolerance for reactor failures forced absolute quality. The physics of nuclear reactions forced precision manufacturing. The handling of enriched uranium forced security infrastructure. These forcing functions eliminated mediocrity. You either met the standard or didn't exist.

Investors should seek companies with similar forcing functions. Aerospace companies where failure means aircraft fall from the sky. Medical device makers where errors kill patients. Infrastructure providers where downtime costs millions. These forcing functions create cultures and capabilities that competitors can't replicate through willpower alone. The market undervalues these invisible assets.

Patience Capital and Decade Bets

BWXT spent decades investing in capabilities with no immediate payoff. They maintained nuclear expertise through the post-Three Mile Island drought. They developed space nuclear technology before any market existed. They preserved manufacturing capabilities for submarines that wouldn't be built for years. This patient capital, often funded by government contracts, created options with enormous value.

The investment lesson: companies playing decade-long games often trade at discounts to quarterly optimizers. The market struggles to value investments that pay off beyond typical holding periods. But these long-duration bets, when they work, create insurmountable advantages. Amazon's AWS, Tesla's Supercharger network, TSMC's process technology—all required patience capital that seemed irrational until it wasn't.

The Paradox of Boring Businesses

BWXT proves that boring can be beautiful. Nuclear component manufacturing isn't sexy. Government contracting seems sleepy. Industrial processing lacks sizzle. But this perceived boring-ness creates opportunity. Fewer competitors enter boring markets. Fewer investors analyze boring companies. Boring often means predictable, and predictability has value.

Investors should inventory their biases against "boring" and recognize that excitement and returns often inversely correlate. The most exciting companies attract the most competition, capital, and scrutiny. The boring companies quietly compound. Waste Management, Fastenal, Old Dominion Freight Line—boring businesses that crushed the market. BWXT fits this pattern: boring operations, exciting returns.

Capital Intensity as Competitive Advantage

Conventional wisdom says capital-light businesses are superior. BWXT inverts this. Their capital intensity—specialized facilities, expensive equipment, cleared personnel—creates the moat. Competitors can't just raise venture capital and compete. They need billions in physical infrastructure, decades of learning, relationships that can't be bought.

The lesson: capital intensity is bad when it's commoditized (airlines, hotels) but powerful when it's specialized. Look for companies where capital investments create capabilities, not just capacity. Where equipment is customized, not purchased. Where facilities require permits that can't be replicated. Where capital intensity decreases rather than increases competition.

Network Effects in Physical Businesses

BWXT demonstrates that network effects aren't limited to software. Every reactor component they manufacture adds to their data set. Every engineer they train strengthens their talent network. Every supplier relationship deepens ecosystem lock-in. Every successful deployment reinforces customer trust. These physical network effects compound like software networks but with higher switching costs.

Investors underappreciate network effects in physical businesses. John Deere's precision agriculture network. ASML's semiconductor equipment ecosystem. Intuitive Surgical's robotic surgery platform. These companies build networks through physical products that become increasingly valuable as they scale. The dynamics differ from software but the compounding is similar.

The Acquisition Integration Playbook

BWXT's acquisition strategy offers lessons in strategic M&A. They don't buy companies; they buy capabilities. GE Hitachi Canada brought CANDU expertise. Nordion brought isotope infrastructure. Each acquisition plugged a capability gap while leveraging existing strengths. Integration focused on knowledge transfer, not just synergy capture.

The playbook: acquire when you have strategic advantage in integration. BWXT could operate nuclear facilities that others couldn't license. They could achieve security clearances others couldn't obtain. They could cross-sell to customers others couldn't access. These integration advantages meant BWXT could pay fair prices and still create enormous value. It's not about buying cheap but buying what only you can optimize.

The Talent Moat Construction

BWXT's approach to human capital offers lessons beyond typical "people are our greatest asset" platitudes. They don't just hire talent; they create it. Their apprenticeship programs, university partnerships, and career progression paths create workers who literally can't work anywhere else—their skills are too specialized. This isn't employee lock-in through contracts but through capability development.

The investment implication: companies that create rather than acquire talent build deeper moats. Epic Systems trains healthcare IT workers from scratch. Enterprise Rent-A-Car promotes exclusively from within. These companies seem inefficient—why train when you can hire?—but they build cultures and capabilities impossible to replicate through recruitment.

Risk Management Through Redundancy

BWXT's zero-failure record isn't luck—it's engineered through redundancy that seems wasteful but isn't. Multiple inspections of the same weld. Backup systems for backup systems. Documentation that documents documentation. This redundancy is expensive, but in domains where failure is catastrophic, redundancy is the only real risk management.

Investors should value redundancy in critical systems companies. Airlines with multiple maintenance bases. Utilities with generation diversity. Pharmaceuticals with multiple supply chains. This redundancy looks like inefficiency on spreadsheets but provides resilience that prevents zeros. In power law outcomes—where one failure can destroy everything—redundancy is cheap insurance.

The Platform Evolution Strategy

BWXT's evolution from components supplier to nuclear platform demonstrates the power of gradual expansion. They didn't jump from submarines to medical isotopes; they climbed adjacency by adjacency. Each new market leveraged existing capabilities while adding new ones. The platform emerged organically, not through grand strategy but through logical progression.

The lesson for investors: watch for companies climbing adjacency ladders. Adobe from desktop software to creative cloud to experience cloud. Shopify from e-commerce to payments to fulfillment. These aren't pivots but expansions, each building on the last. The best platforms emerge from solving specific problems then generalizing solutions. BWXT solved naval nuclear propulsion, then realized those solutions applied everywhere nuclear technology matters.

The playbook BWXT demonstrates isn't about disruption or innovation or blitzscaling. It's about patient competence, strategic positioning, and compound advantages. It's about building moats through excellence, not financial engineering. It's about creating value through capabilities, not multiple expansion. In a market obsessed with the new, BWXT reminds us that sometimes the best investments are in companies doing difficult things for a very long time.

XII. Bull Case & Valuation

The Misunderstood Compounder

At $10.24 billion market cap, BWXT trades at roughly 33x trailing earnings and 3.7x revenue—multiples that seem full until you understand what you're buying. This isn't a cyclical industrial or a government contractor; it's a monopoly provider to the world's most powerful navy, a picks-and-shovels play on the nuclear renaissance, and an emerging medical technology company rolled into one. The market treats BWXT like Lockheed Martin when it should be viewed like Veeva Systems—a vertical software company that happens to make atoms instead of bits.

The comparison to defense contractors is particularly misleading. Lockheed faces competition on every program. Boeing battles Airbus. Raytheon competes with Northrop. BWXT faces... no one. They're not winning contracts; they're collecting rents on irreplaceable infrastructure. This isn't competition; it's taxation with better margins.

The Hidden SaaS Model

Strip away the industrial facade and BWXT's business model mirrors enterprise software: - Customer acquisition cost: Enormous (decades of capability building) - Customer lifetime value: Infinite (the Navy can never switch) - Net revenue retention: >100% (every submarine needs maintenance) - Gross margins: 24% and expanding - Customer concentration: High but with zero churn risk

The recurring revenue is hidden in the contract structure. That submarine reactor BWXT builds? It needs fuel for 33 years. Those medical isotope facilities? They need feedstock indefinitely. The microreactor deployed to a forward base? It needs maintenance, monitoring, and eventual replacement. Every product sold creates an annuity stream. The "backlog" isn't just contracted revenue; it's a fraction of lifetime value.

The Nuclear Renaissance Multiple

The market hasn't priced in the nuclear renaissance because it doesn't believe it's real. But the evidence is overwhelming. The U.S. Department of Energy estimates domestic demand for HALEU could reach 50 metric tons per year by 2035, and BWXT is one of only two facilities capable of producing it. Every SMR design needs nuclear components. Every life extension needs replacement parts. Every advanced reactor needs specialized fuel.

Apply semiconductor or renewable energy multiples to the nuclear opportunity. First Solar trades at 50x earnings despite commodity solar panel competition. ASML trades at 35x earnings supplying semiconductor equipment. BWXT, supplying irreplaceable nuclear infrastructure with higher barriers to entry than either, trades at a discount. When the market realizes nuclear is having its iPhone moment, multiples will re-rate dramatically.

The Optionality Portfolio

BWXT's growth initiatives represent free options on massive markets: - Medical isotopes: $10 billion market growing 15% annually - Space nuclear: Potentially $5 billion by 2040 - Microreactors: $20 billion addressable market - HALEU production: Monopoly on $2 billion annual market - Hydrogen production: Unquantifiable but massive

Even if half these initiatives fail, the remaining successes could double BWXT's revenue. The market assigns zero value to these options, focusing on near-term government revenue. But optionality in monopoly markets with nuclear-grade barriers to entry is worth far more than standard venture portfolios.

The Geopolitical Put

Every South China Sea confrontation, every Russian submarine patrol, every North Korean missile test increases BWXT's value. The Columbia-class submarine program, initially 12 boats, could expand to 14 or 16 if threats escalate. The Virginia-class production could accelerate from two to three annually. The Navy could decide every carrier needs refueling, not retirement.

This isn't hoping for conflict; it's recognizing that BWXT provides insurance for American naval dominance. That insurance becomes more valuable as threats multiply. The market prices BWXT on current defense budgets, but defense spending is pro-cyclical with threats. A true confrontation with China could double naval nuclear investment overnight.

The ESG Transformation

Nuclear is undergoing an ESG transformation from villain to hero. Microsoft, Google, and Amazon are investing in nuclear to meet climate commitments. The EU classified nuclear as green energy. California extended Diablo Canyon's life. Germany is reconsidering its nuclear exit. This perception shift is early but accelerating.

When nuclear fully transitions from ESG negative to ESG positive, capital flows will reverse. The same funds that divested from nuclear will pile back in. BWXT, as the pure-play nuclear infrastructure provider, will be the primary beneficiary. This isn't reflected in current multiples that still embed an ESG discount.

The Acquisition Multiple Arbitrage

BWXT trades at 33x earnings while acquiring businesses at 10-15x. The Nordion medical isotope business was acquired for less than 2x revenue. Every acquisition immediately re-rates to BWXT's multiple, creating instant value. With $400 million of annual free cash flow and modest leverage capacity, BWXT could acquire $1 billion of revenue at accretive multiples.

The acquisition pipeline is rich. Struggling nuclear services companies need BWXT's balance sheet. International nuclear businesses need U.S. market access. Medical technology companies need nuclear expertise. Each acquisition strengthens the platform while creating financial arbitrage. Roll-up strategies in fragmented markets are common; roll-ups in monopoly markets are extraordinary.

The Dividend Aristocrat Potential

This stock pays an annual dividend of $1.00, which amounts to a dividend yield of 0.92%—seemingly paltry, but consider the trajectory. With 90%+ customer retention, 3-5% organic growth, and expanding margins, BWXT could double earnings by 2030. The payout ratio of 30% leaves room for substantial dividend growth while funding expansion.