MCX: India's Commodity Trading Revolution

I. Introduction & Episode Roadmap

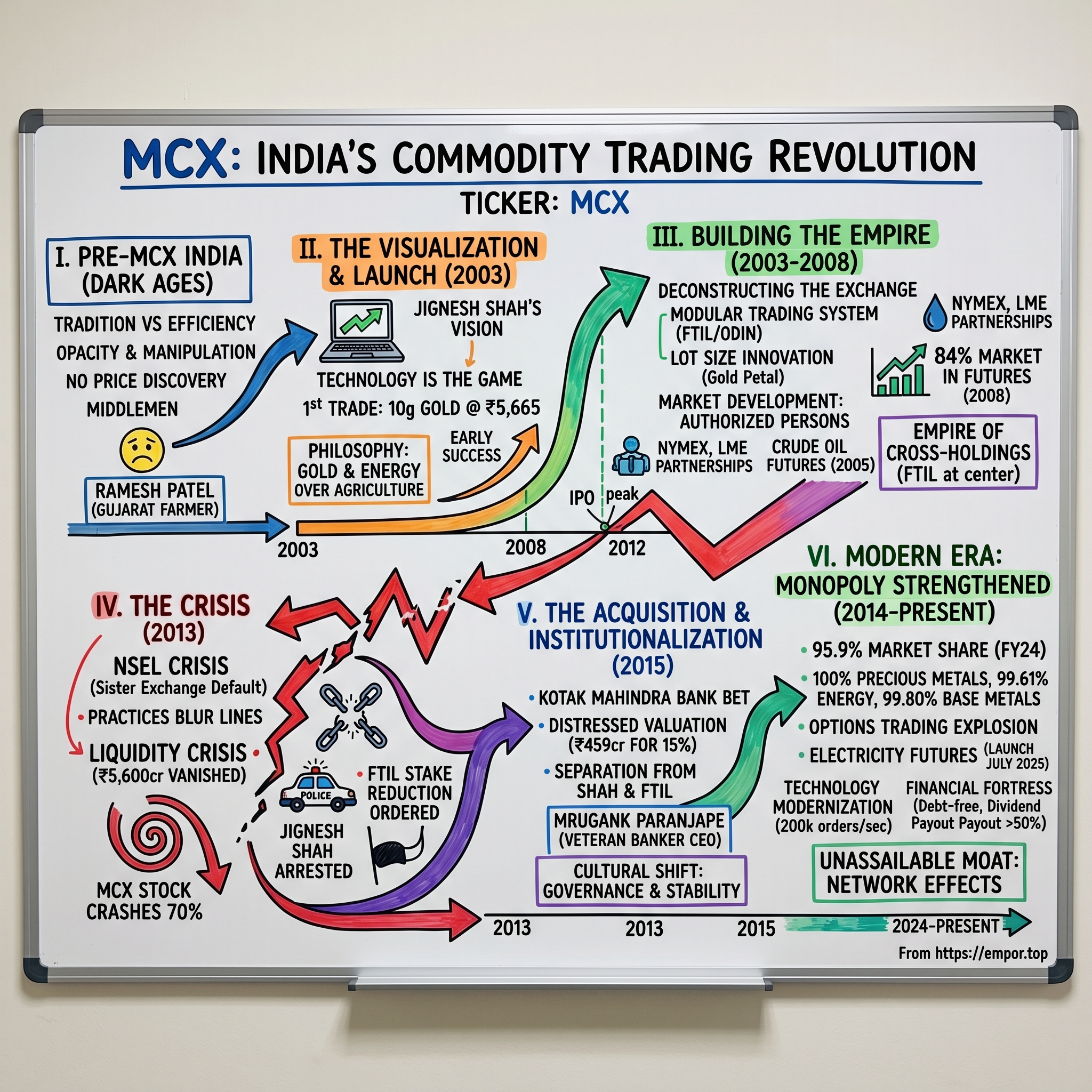

Picture this: November 2003, Mumbai's financial district. A software engineer turned entrepreneur named Jignesh Shah stands before a small gathering of bankers and commodity traders. He's about to launch something audacious—India's first fully electronic, national-level commodity exchange. The skeptics in the room outnumber the believers. India's commodity markets have operated the same way for centuries: regional, paper-based, opaque. Who is this 36-year-old technocrat to think he can revolutionize an entire industry?

Fast forward to 2008. Shah is on the Forbes India rich list, his creation—the Multi Commodity Exchange of India—commands over 80% market share in commodity futures trading. By 2012, MCX goes public at a valuation that makes investment bankers dizzy: 30 times earnings, oversubscribed 54 times. Shah's personal net worth crosses $1 billion. He's built what appears to be an unassailable monopoly in one of the world's fastest-growing commodity markets.

Then, in July 2013, everything collapses. A sister exchange under Shah's control defaults on ₹5,600 crore in payments. Within months, Shah is arrested, banned from capital markets, forced to sell his stake at a massive discount. The empire he built over a decade crumbles in weeks.

Yet here's the twist that makes this story extraordinary: MCX didn't just survive—it thrived. Today, under new ownership by the Kotak Mahindra group, MCX controls an even more dominant position than at its peak under Shah. The numbers tell a remarkable story: MCX commands a 95.9% share in the commodity futures market, with 100% control of precious metals & stones trading, 99.61% in energy, and 99.80% in base metals. Some sources report market share as high as 97.84% in commodity futures trading. This is a monopoly so complete it would make even the robber barons of the Gilded Age envious.

How does a company survive the spectacular implosion of its founder, endure regulatory upheaval, face down competition from India's largest stock exchanges, and emerge with an even stronger monopoly than before? How did the very regulatory system that destroyed Jignesh Shah end up protecting and strengthening the fortress he built?

This is a story about more than just a commodity exchange. It's about the architecture of modern capitalism in emerging markets—how technology, regulation, and network effects combine to create unassailable competitive positions. It's about the paradox of Indian business: a market that simultaneously celebrates entrepreneurial ambition and punishes those who fly too close to the sun. And it's about an asset so valuable that even after its creator's disgrace, India's most conservative financial institution—Kotak Mahindra Bank—was willing to bet nearly half a billion rupees on it.

Over the next several hours, we'll unpack every layer of this extraordinary business. We'll explore the medieval chaos of India's pre-digital commodity markets, trace Shah's meteoric rise from BSE techie to billionaire, dissect the NSEL crisis that brought him down, and analyze how MCX not only survived but thrived under new ownership. We'll examine the economics of exchange monopolies, decode the regulatory moat that protects MCX, and evaluate whether this fortress can withstand the twin threats of technology disruption and regulatory intervention.

By the end, you'll understand why MCX represents one of the most fascinating case studies in modern financial infrastructure—a business that proves sometimes the best assets are those that survive their creators. Let's begin where all great Indian business stories must: in the chaos that preceded order.

II. Pre-MCX India: The Dark Ages of Commodity Trading

Mumbai, 1999. Step into the Mulji Jetha Market in Zaveri Bazaar, and you enter a world that hasn't changed in centuries. Gold traders huddle in cramped shops, scribbling prices on chits of paper, settling deals with handshakes and honor. A farmer from Gujarat wanting to hedge his cotton crop must physically travel to the regional exchange in Rajkot. An aluminum manufacturer in Chennai seeking to lock in copper prices deals through a maze of brokers, each taking their cut, none offering transparency.

This was India's commodity market at the turn of the millennium—a $100 billion economy operating like a medieval bazaar. Over 20 regional commodity exchanges dotted the landscape, each with its own rules, its own settlement mechanisms, its own opacity. The Cotton Association in Mumbai, the Rajkot Seeds Oil & Bullion Merchants Association, the Delhi Oilseeds Exchange—names that evoked tradition but masked inefficiency.

The problems were systemic and devastating. Price discovery? Non-existent. A gold trader in Delhi might quote prices 2-3% different from Mumbai, creating massive arbitrage opportunities for the connected few. Risk management? Primitive. Farmers couldn't hedge crop prices effectively, leading to countless tragedies during price crashes. Market manipulation? Rampant. The infamous "Guar Seed Crisis" of 2000 saw prices manipulated by cartels, destroying thousands of small traders.

Consider the plight of Ramesh Patel, a fictional but representative cotton farmer from Ahmedabad. In 2001, he harvested his crop in October, when prices were ₹2,100 per quintal. By the time he transported his cotton to the local mandi and found buyers through multiple intermediaries, prices had crashed to ₹1,750. Had a transparent, electronic futures market existed, he could have locked in October prices months in advance. Instead, like millions of Indian farmers, he was at the mercy of spot market volatility and middlemen.

The regulatory framework was equally archaic. The Forward Markets Commission (FMC), established in 1953 under the Forward Contracts (Regulation) Act of 1952, operated more like a colonial-era oversight body than a modern regulator. It lacked autonomy, reported to the Department of Consumer Affairs (not the Finance Ministry), and had limited punitive powers. The FMC could suspend futures trading in commodities at will—and frequently did, creating massive uncertainty for market participants.

Then came the watershed moment. In 2002, the government appointed the Kabra Committee to review commodity futures trading. Their report was damning: India's commodity markets were failing farmers, failing industry, and failing the economy. The committee recommended revolutionary changes: establish national-level electronic exchanges, allow futures trading in all commodities, strengthen the regulatory framework.

The timing was perfect. India's GDP was growing at 4-5% annually, accelerating toward the 8-9% boom years. The global commodity supercycle was beginning—oil prices would triple between 2002 and 2008, gold would quadruple, agricultural commodities would see unprecedented volatility. India, with its massive agricultural base and growing industrial appetite, needed modern commodity markets more than ever.

In April 2003, the government acted. It invited applications for setting up national-level multi-commodity exchanges. The requirements were stringent: minimum net worth of ₹100 crore, nationwide access through technology, robust risk management systems. Only three entities had the vision and capability to apply.

The first was National Multi-Commodity Exchange (NMCE), promoted by Central Warehousing Corporation and Gujarat State Agricultural Marketing Board—a government-backed initiative that launched with great fanfare but little innovation. The second was National Commodity & Derivatives Exchange (NCDEX), backed by heavyweight institutions including NSE, ICICI Bank, and Life Insurance Corporation—the establishment's answer to commodity trading.

The third applicant was different. It came from a technology company called Financial Technologies India Limited (FTIL), led by a soft-spoken engineer named Jignesh Shah. While NMCE had government backing and NCDEX had institutional muscle, FTIL had something else: a vision to completely reimagine how commodity markets could work.

The old guard scoffed. How could a technology company with no commodity trading experience compete with established players? They didn't understand that in the transition from physical to electronic markets, technology wasn't just an enabler—it was the entire game. And Jignesh Shah, the unlikely disruptor from Mumbai's suburbs, was about to prove that in the digital age, software could indeed eat the commodities world.

III. The Founder's Journey: Jignesh Shah's Rise

The year is 1987. A 20-year-old Jignesh Shah, fresh out of Mumbai University with an engineering degree, walks into the Bombay Stock Exchange for his first day of work. The BSE is still operating on an open outcry system—traders shouting, papers flying, organized chaos that somehow produces India's stock prices. Shah is assigned to the IT department, tasked with the unglamorous job of maintaining the exchange's rudimentary computer systems.

But where others saw mundane technical work, Shah saw revolution waiting to happen. He spent his nights not in Mumbai's clubs but hunched over programming manuals, teaching himself the intricacies of trading systems architecture. His colleagues remember him as obsessed, constantly sketching diagrams of how electronic trading could transform markets. "Jignesh would carry these notebooks everywhere," recalls a former BSE colleague who requested anonymity. "Even during lunch, he'd be drawing flowcharts of order matching algorithms."

By 1988, Shah had seen enough. With ₹50,000—his entire life savings plus loans from family—he founded Financial Technologies India Limited. The company's first office was a 250-square-foot room in Mumbai's Andheri suburb, so small that Shah's desk doubled as the conference table. The business plan was audacious for its time: build trading technology that could rival systems from Reuters and Bloomberg, but tailored for emerging markets.

The early years were brutal. FTIL's first product, a DOS-based trading terminal for brokers, sold exactly seven units in its first year. Shah survived by taking consulting projects, building custom software for small brokerages. But he never deviated from his core vision: India would eventually need world-class financial technology, and he would be ready when it did.

The breakthrough came in 1994 when the National Stock Exchange was establishing India's first fully electronic exchange. FTIL won a contract to provide broker terminals—not the main exchange system, but enough to establish credibility. Shah used every rupee of profit to hire engineers, not from India's business schools but from regional engineering colleges, young programmers who shared his obsession with building from first principles.

FTIL's 1995 IPO raised ₹15 crore, modest by today's standards but transformational for Shah. He immediately deployed the capital into R&D, creating what he called the "ODIN architecture"—a modular trading system that could handle multiple asset classes, multiple exchanges, with microsecond latency. While Indian financial firms were still importing technology, Shah was building intellectual property.

By 2002, FTIL had quietly become India's largest provider of trading terminals, with over 100,000 installations. But Shah saw terminals as merely the gateway drug. The real opportunity was exchanges themselves. When the government announced the commodity exchange licenses in 2003, Shah had been preparing for five years.

The MCX launch on November 10, 2003, was quintessentially Shah—low-key but precisely orchestrated. While NCDEX held glitzy events with Bollywood celebrities, MCX's inauguration was a technical demonstration. Shah personally conducted the first trade, buying 10 grams of gold at ₹5,665, then immediately showed how the system could handle 10,000 simultaneous orders without latency.

What distinguished MCX wasn't just technology but philosophy. NCDEX focused on agricultural commodities, believing that was India's need. Shah bet on gold and energy, understanding that India's middle class cared more about gold prices than guar seed. "Everyone said I was crazy focusing on gold," Shah later told an interviewer. "But every Indian family understands gold. It was our gateway to mass participation."

The strategy was brilliant. MCX's gold contracts became the most traded commodity futures in India within six months. By 2005, daily volumes exceeded ₹1,000 crore. The exchange's success attracted heavyweight investors: In February 2012, MCX held its IPO, raising $134 million and becoming India's only publicly listed exchange.

Shah's management style was distinctive—part tech visionary, part micromanager. Employees describe 2 AM emails with detailed product specifications, surprise visits to the technology center where he'd review code line by line. He maintained a mysterious persona, rarely giving interviews, preferring to let MCX's numbers speak. And speak they did: by 2008, MCX was the world's sixth-largest commodity exchange by volume.

The international expansion showcased Shah's ambition. MCX took strategic stakes in Dubai Gold & Commodities Exchange, formed partnerships with Chicago Mercantile Exchange, created a network of exchanges across emerging markets. Shah's vision wasn't just an Indian exchange but a parallel financial infrastructure for the developing world.

By 2008, Forbes pegged Shah's net worth at $1.2 billion. He had built not just MCX but an exchange conglomerate—Indian Energy Exchange for power trading, Singapore Mercantile Exchange for global commodities, Dubai Gold & Commodities Exchange for Middle East markets. The financial press dubbed him "India's Exchange King."

Yet there were warning signs. Shah's empire was built on intricate cross-holdings, with FTIL at the center of a complex web. He controlled exchanges while also selling them technology, creating potential conflicts of interest. Regulatory relationships, initially cordial, grew tense as Shah's power expanded. The Forward Markets Commission expressed concerns about FTIL's influence over MCX operations.

The tipping point came with the National Spot Exchange Limited (NSEL), launched in 2008. While MCX dealt in futures, NSEL was meant for spot trading—immediate delivery of commodities. But under Shah's aggressive growth push, NSEL began offering products that blurred the line between spot and futures, attracting investors with promises of guaranteed returns.

In 2012, at MCX's IPO, Shah stood at his zenith. The offering was oversubscribed 54 times, valuations touched ₹7,000 crore, and Shah's paper wealth exceeded $2 billion. He had proven that an Indian technology entrepreneur could build world-class financial infrastructure.

But empires built on aggressive innovation often carry the seeds of their own destruction. The very creativity that allowed Shah to reimagine commodity trading would soon lead him into regulatory grey zones that would destroy everything he had built. The king of exchanges was about to learn that in India's financial markets, flying too high invariably leads to a fall.

IV. Building the Exchange Empire (2003-2008)

The first trade on MCX happened at 10:00 AM on November 10, 2003—10 grams of gold at ₹5,665. Within four hours, the exchange had processed 1,000 trades. Within four weeks, daily volumes crossed ₹100 crore. Within four months, MCX had overtaken both NMCE and NCDEX in trading volumes. The velocity of conquest was breathtaking.

How did a latecomer with no commodity expertise demolish established competitors so quickly? The answer lay in Shah's systematic deconstruction of what an exchange actually does. While competitors thought of themselves as commodity market, Shah understood exchanges as technology businesses with commodity licensing. This philosophical difference drove every strategic decision.

Take the choice of initial products. NCDEX, backed by agricultural institutions, launched with 21 agricultural commodities—mustard seed, guar, jeera, turmeric. Noble intentions, addressing India's farming needs. But agricultural futures are complex: multiple grades, seasonal patterns, delivery challenges, fragmented user base. MCX launched with just four contracts: gold, silver, copper, and crude oil. Simple, standardized, globally benchmarked, appealing to both institutions and retail traders.

The gold contract was masterful product design. The standard lot size was 1 kilogram—large enough to attract serious traders, small enough for affluent retail participation. But MCX also introduced "Gold Guinea" (8 grams) and "Gold Petal" (1 gram) contracts. Suddenly, a middle-class investor could trade gold futures with just ₹5,000 capital. No other exchange had democratized commodity trading this way.

The technology infrastructure was revolutionary for 2003 India. MCX's trading engine, built on FTIL's ODIN platform, could process 15,000 orders per second—fifty times the capacity of regional exchanges. Latency was under 10 milliseconds, comparable to international standards. But the real innovation was resilience: the system had six levels of redundancy, automatic failover capabilities, and had 99.98% uptime in its first year.

Shah's approach to market development was equally systematic. Rather than wait for traders to come to MCX, he went to them. The exchange established 700 membership terminals in the first year, but more importantly, created an army of 10,000 "Authorized Persons"—local agents who could aggregate orders from smaller traders. A jeweler in Coimbatore, a oil dealer in Guwahati, could now access the same markets as institutional traders in Mumbai.

The alliance strategy reflected Shah's global ambitions. In 2005, MCX signed memorandums with New York Mercantile Exchange (NYMEX) for energy products, London Metal Exchange (LME) for base metals, and Tokyo Commodity Exchange (TOCOM) for precious metals. These weren't mere paper agreements. MCX contracts began tracking global benchmarks, with Indian prices discovering their natural premium or discount to international markets.

But the masterstroke was the July 2005 launch of crude oil futures. India imported 70% of its oil, yet had no domestic price discovery mechanism. MCX's crude contract, settled against international benchmarks but traded in rupees, became an instant hit. Daily volumes crossed ₹500 crore within months. For the first time, Indian companies could hedge oil price risk without accessing international markets.

The growth numbers were staggering. From ₹40,000 crore turnover in FY2004, MCX reached ₹15 lakh crore in FY2006, then ₹32 lakh crore in FY2008. Market share in commodity futures grew from 15% at launch to 62% by 2006, to 84% by 2008. In bullion, MCX's dominance was absolute—98% market share in gold futures, 99% in silver.

The human story behind these numbers was equally remarkable. Shah had assembled a team of mavericks. The head of products was poached from Chicago Board of Trade. The technology chief came from NASDAQ. The business development head was a former commodity trader who'd blown up his own portfolio but understood market psychology. This eclectic mix, united by Shah's vision, created a culture of relentless innovation.

New products launched monthly. Mentha oil futures for Uttar Pradesh farmers. Natural gas contracts for fertilizer companies. Even exotic products like cardamom and steel found their way onto MCX screens. Not all succeeded—the infamous potato futures contract saw zero trades in six months—but the willingness to experiment set MCX apart.

The exchange's physical infrastructure grew equally fast. From one disaster recovery site in 2003, MCX expanded to four data centers by 2008. Warehouses for commodity delivery sprouted across India—750 delivery centers by 2008, each with electronic surveillance, scientific storage, and quality testing facilities. MCX wasn't just enabling paper trading; it was rebuilding India's commodity supply chain.

International expansion accelerated after 2006. MCX took a 5% stake in Dubai Gold & Commodities Exchange, helping design its entire trading architecture. The Singapore Mercantile Exchange, majority-owned by FTIL, launched as Asia's first international multi-commodity exchange. Shah spoke of creating an "alternative trading axis" for emerging markets, independent of Chicago-London-New York dominance.

By 2008, institutional validation was complete. State Bank of India, HDFC Bank, Union Bank, and other majors held stakes in MCX. International investors like Fidelity, Merrill Lynch, and Goldman Sachs were shareholders. The exchange's board read like a who's who of Indian finance. MCX had transformed from Shah's personal venture to a national institution.

The financials were extraordinary. EBITDA margins exceeded 60%—the beauty of exchange economics where marginal costs approach zero. Return on equity topped 35%. The balance sheet was fortress-like: zero debt, ₹500 crore in cash, no significant capital requirements for growth. MCX was literally printing money.

Yet beneath the success lay structural tensions. FTIL still owned 26% of MCX while being its primary technology vendor—a clear conflict of interest. The Forward Markets Commission grew increasingly uncomfortable with Shah's influence. Competitors complained about MCX's aggressive business practices, alleging everything from predatory pricing to exclusive dealing arrangements.

The launch of NSEL in 2008 marked a pivotal moment. While MCX was Shah's crown jewel, NSEL was his attempt to extend dominance into spot markets. The exchange promised to revolutionize agricultural trading by providing spot price discovery and financing against warehouse receipts. Noble goals, but the execution would prove catastrophic.

As 2008 ended, MCX stood as one of India's great entrepreneurial success stories. A single individual with no commodity background had built the world's sixth-largest commodity exchange in five years. Daily trading volumes exceeded ₹25,000 crore. Market capitalization implied a valuation over $2 billion. Jignesh Shah was mentioned alongside Narayana Murthy and Azim Premji as icons of Indian enterprise.

But success in Indian business attracts scrutiny, and scrutiny reveals flaws. The same aggressive innovation that built MCX was about to destroy its creator. The empire had been built; its unraveling was about to begin.

V. The IPO and Peak Valuation (2012)

February 22, 2012, 9:15 AM. The MCX IPO opened for subscription at the Bombay Stock Exchange. Within 30 minutes, the retail portion was fully subscribed. By noon, institutional demand exceeded supply five times. When the book closed on February 24, the numbers were staggering: 54.13 times oversubscription overall, with the Qualified Institutional Buyers portion subscribed 91.5 times. For context, this was higher than the subscription rates for Infosys, TCS, or any major Indian technology IPO of the decade.

The pricing itself told a story of extraordinary confidence. MCX raised $134 million through the offering of 6.5 million shares, pricing at ₹1,032 per share—the upper end of the ₹860-1,032 price band. This valued MCX at ₹5,291 crore, approximately 30 times its FY2011 earnings. In an era when established banks traded at 15x earnings and technology companies at 20x, MCX commanded valuations typically reserved for hyper-growth internet companies.

What drove this frenzy? The investment thesis was seductively simple. India's commodity markets were growing at 40% annually. MCX controlled 85% market share with seemingly insurmountable network effects. The business model was a cash machine—68% EBITDA margins, zero debt, minimal capital requirements. Regulation created a protective moat. It was, in banker parlance, "the perfect monopoly."

The IPO prospectus, a 524-page tome, revealed fascinating details about the business. Revenue for FY2011 stood at ₹324 crore, with ₹175 crore in profit. But the quality of earnings was exceptional—92% came from transaction fees, highly predictable and recurring. Customer concentration was minimal; the top 10 members contributed only 18% of revenues. Operating leverage was tremendous; a 10% increase in volumes translated to 18% increase in profits.

The allocation drama was intense. Mutual funds battled for shares—HDFC, ICICI Prudential, and Reliance funds each received less than half their requested allocation. Foreign institutions were equally aggressive; Government of Singapore Investment Corporation, Fidelity, T. Rowe Price all participated. Retail investors, allocated 35% of the issue, saw it as a once-in-a-decade opportunity to own India's commodity market infrastructure.

March 9, 2012—listing day. MCX opened at ₹1,170, a 13% premium to issue price. Within minutes, it touched ₹1,241, valuing the company at over ₹6,300 crore. Trading volumes exceeded ₹500 crore in the first hour. By day's end, MCX had created roughly ₹4,000 crore in market value—paper wealth that made early investors delirious with success.

The stakeholder dynamics post-IPO were intriguing. FTIL's stake diluted from 31.2% to 26%, though still maintaining effective control. Public shareholders now owned 43%, creating genuine free float. Financial institutions collectively held 24%, providing credibility but also demanding governance improvements. The government, through various entities, retained about 7%, ensuring public interest representation.

Jignesh Shah's personal windfall was substantial but complex. While he didn't sell shares directly in the IPO, his stake in FTIL meant indirect ownership worth approximately ₹800 crore in MCX alone. Combined with holdings in other exchanges, his paper wealth exceeded ₹3,000 crore. Forbes India estimated his net worth at $1.5 billion, ranking him among India's 50 richest individuals.

The market's reception validated Shah's decade-long vision. Analysts published euphoric reports. Morgan Stanley set a target price of ₹1,400, citing "unassailable competitive position." Goldman Sachs highlighted "regulatory barriers creating permanent moat." CLSA's report was titled simply: "License to Print Money."

But euphoria masked underlying concerns. The Forward Markets Commission had been expressing discomfort about FTIL's dual role as shareholder and technology provider. MCX paid FTIL approximately ₹50 crore annually for technology services—not huge in absolute terms, but the exclusivity raised eyebrows. Competitors alleged MCX used its market power to squeeze them out, offering negative trading fees to large clients.

The corporate governance structure drew scrutiny. While MCX had independent directors, FTIL's 26% stake gave Shah effective veto power over major decisions. The board included respected names—former SEBI officials, retired bankers—but critics questioned their real independence. The audit committee had flagged several related-party transactions requiring closer examination.

More troubling were whispers about NSEL, MCX's sister exchange. Market participants spoke of unusual trading patterns, contracts that seemed to violate spot market regulations, promises of guaranteed returns that sounded too good to be true. The financial press, caught up in IPO euphoria, largely ignored these concerns. Who wanted to question India's great commodity exchange success story?

The months following IPO saw frenzied activity. MCX announced new products weekly—electricity futures, carbon credits, even weather derivatives. International expansion accelerated with plans for exchanges in Africa and Latin America. Technology spending doubled to ₹100 crore annually. The company spoke of becoming "the NYSE of commodities."

By December 2012, MCX stock touched ₹1,371, a 33% gain from IPO price. Market capitalization exceeded ₹7,000 crore. Daily trading volumes on the exchange crossed ₹40,000 crore. Every metric pointed upward. Shah gave a rare interview declaring MCX would achieve $10 billion valuation within three years.

The institutional framework was evolving too. In September 2012, the government announced plans to merge Forward Markets Commission with SEBI, bringing commodity markets under unified regulation. This was seen as positive for MCX—SEBI's deeper pockets and stronger governance would legitimize commodity trading, attracting more institutional participation.

Yet danger signs accumulated. A forensic reading of MCX's first post-IPO annual report revealed increasing Days Sales Outstanding, suggesting collection challenges. Employee turnover in senior positions had spiked. Three independent directors resigned citing "personal reasons"—market code for boardroom disagreements. The technology contract with FTIL, due for renewal, became a contentious board issue.

The IPO had achieved its financial objectives spectacularly. MCX was now a public company with blue-chip shareholders, substantial capital, and market validation. But it had also brought scrutiny, governance demands, and regulatory attention that a closely-held company could avoid. The very success that made MCX public would soon make its flaws public too.

As 2012 ended, MCX seemed positioned for perpetual dominance. The stock market valued it at 35 times earnings. Daily volumes were setting records. International expansion plans were ambitious. Jignesh Shah spoke of MCX becoming a global powerhouse, the emerging market alternative to CME and ICE.

Within six months, this entire edifice would crumble. The IPO that marked MCX's coronation as India's commodity exchange monopoly also marked the beginning of the end for its creator. The crisis that would unfold would test whether MCX was truly an institution or merely an extension of one man's ambition. The answer would reshape India's commodity markets forever.

VI. The NSEL Crisis: Fall from Grace (2013)

July 31, 2013, 4:30 PM. A terse circular from National Spot Exchange Limited landed in the inboxes of 13,000 investors: "Due to serious liquidity crisis, the exchange is unable to meet its settlement obligations. All trading suspended immediately." With those words, ₹5,600 crore vanished into thin air, and Jignesh Shah's carefully constructed empire began its catastrophic collapse.

The NSEL crisis didn't emerge from nowhere—it had been building for years behind a facade of innovation. NSEL, launched in 2008, was supposed to be MCX's complement: while MCX handled futures, NSEL would revolutionize spot trading. The pitch was compelling. Farmers could sell commodities directly to buyers, eliminating middlemen. Investors could finance this trade, earning 13-15% returns by providing working capital. Everyone would win in this new, efficient marketplace.

But the reality was different. NSEL had created products called "paired contracts"—simultaneously buying in the spot market and selling in the forward market, typically with a 25-35 day gap. Investors were told their money was financing genuine commodity trades, backed by physical stocks in warehouses. The returns seemed reasonable for trade financing, the counterparties appeared credible, and FTIL's reputation provided comfort.

The unraveling began with a routine government inspection in July 2013. Officials visiting NSEL warehouses found them nearly empty. Where 175,000 tonnes of commodities should have existed, there was nothing but dust and forged receipts. The paired contracts weren't financing real trade but were simply financing schemes, with the same collateral pledged multiple times to different lenders.

The numbers were staggering. Twenty-four borrowers owed ₹5,600 crore to 13,000 investors, primarily high-net-worth individuals and small trading firms who'd been chasing "safe" returns. The largest defaulter, Mohan India, owed ₹965 crore. Others included companies with minimal net worth that had borrowed hundreds of crores. The due diligence had been non-existent, the risk management a facade.

The mechanics of the fraud were breathtakingly simple. A company would "sell" commodities to NSEL investors, promising to buy them back after 25 days at a higher price—effectively a loan disguised as a trade. NSEL would guarantee settlement, comfort that convinced investors to participate. But the commodities often didn't exist, the companies had no ability to repay, and NSEL had no capital to honor its guarantee.

August 6, 2013. The Forward Markets Commission issued its first order: FTIL declared "not fit and proper" to run exchanges. The reasoning was damning. NSEL had violated its license by offering forward contracts beyond 11 days, effectively operating as an illegal futures exchange. FTIL, as NSEL's owner, had either orchestrated the violations or been grossly negligent in oversight.

The contagion spread immediately to MCX. On August 7, MCX stock crashed 20%, wiping out ₹1,400 crore in market value. By month-end, it had fallen 65% from its peak. The logic was brutal but clear: if FTIL had allowed such massive fraud at NSEL, what was happening at MCX? Could Shah be trusted with India's largest commodity exchange?

Shah's initial response was denial mixed with deflection. In a rare press conference on August 14, he claimed NSEL was a victim of borrower defaults, not perpetrator of fraud. He promised to recover money from defaulters, hired lawyers to chase assets, even offered his personal guarantee for partial recovery. But the damage was irreversible. The man who'd avoided media for years was now its primary target.

The regulatory hammering intensified. September 2013: SEBI banned Shah from capital markets for non-cooperation in investigations. October 2013: Economic Offences Wing filed criminal charges for fraud, criminal breach of trust, and cheating. November 2013: Enforcement Directorate initiated money laundering investigations. December 2013: Ministry of Corporate Affairs ordered inspection of all FTIL-related entities.

The human tragedy was enormous. Among NSEL's victims were retired government servants who'd invested life savings, small traders who'd borrowed to invest, even Shah's own employees who'd put bonuses into NSEL products. Support groups formed, protests erupted outside FTIL offices, suicide threats emerged. The media covered each development breathlessly, with Shah's face splashed across newspapers as the villain who'd destroyed middle-class savings.

March 2014 brought the decisive blow. SEBI declared FTIL "not fit and proper" to own exchange stakes, ordering it to reduce holdings in MCX from 26% to 2% within six months. The regulator's order was scathing, detailing how FTIL had violated basic principles of exchange governance, mixed client and proprietary funds, and failed to maintain arms-length relationships with group entities.

Shah's arrest on May 7, 2014, marked the nadir. Mumbai Police took him from his Breach Candy residence at 6 AM, parading him before media cameras—a deliberate humiliation for someone who'd cultivated mystique. Though granted bail after 45 days, the images of Shah in custody, haggard and diminished, symbolized the complete destruction of his reputation.

The legal battles multiplied exponentially. By end-2014, Shah faced 15 criminal cases, 23 civil suits, and regulatory proceedings from FMC, SEBI, RBI, and Income Tax. His passport was impounded, assets frozen, banned from holding directorships. The man who'd built a billion-dollar empire couldn't access his own bank accounts.

The systemic implications were profound. NSEL's collapse triggered debates about regulatory oversight, exchange governance, and investor protection. The Forward Markets Commission, already scheduled for merger with SEBI, was essentially discredited for missing the fraud. The government fast-tracked regulatory reforms, tightening rules on spot exchanges, related-party transactions, and settlement guarantees.

For MCX, the immediate challenge was survival. Trading volumes plummeted 40% as participants lost confidence. Several large members withdrew, citing reputational risk. International partners distanced themselves—CME terminated its memorandum of understanding, LME suspended cooperation. The exchange that had seemed invincible a year earlier was fighting for relevance.

The investigation revelations were damaging. Forensic audits revealed NSEL had been losing money since inception, with losses hidden through accounting jugglery. The "innovative" products were designed primarily to circumvent regulations. Several FTIL employees had received kickbacks from defaulting borrowers. The rot went deeper than anyone had imagined.

October 2013 marked Shah's formal capitulation. Under intense regulatory pressure, he announced FTIL would exit the exchange business entirely. The statement was brief, bitter: "Despite our pioneering contribution to India's financial markets, circumstances force us to withdraw from exchange ownership." The empire built over a decade would be dismantled in months.

The search for buyers began immediately. MCX, despite the crisis, remained an attractive asset—dominant market position, strong technology, clean balance sheet (unlike NSEL). But potential acquirers wanted complete separation from Shah and FTIL. The technology contracts would need renegotiation, the governance structure overhaul, the regulatory clearances numerous.

As 2013 ended, the transformation was complete. Jignesh Shah had gone from billionaire visionary to disgraced financial pariah in five months. MCX's stock had crashed 70%, though the underlying business remained profitable. NSEL investors recovered barely 15% of their money despite years of legal battles. The Indian commodity market had lost its most innovative entrepreneur but perhaps gained necessary sobriety.

The NSEL crisis became a watershed in Indian financial history, mentioned alongside Harshad Mehta and Ketan Parekh scams. But unlike those cases of pure market manipulation, NSEL represented something more complex—innovation pushed too far, ambition unchecked by governance, regulation failing to keep pace with financial engineering.

The question now was whether MCX could survive without its creator. Could an exchange built on one man's vision transform into a sustainable institution? The answer would come from an unlikely source—one of India's most conservative financial institutions was about to make a contrarian bet that would reshape commodity markets again.

VII. The Kotak Acquisition: Institutionalization

March 30, 2015, Kotak Mahindra Bank headquarters, Mumbai. Uday Kotak, India's richest banker, faced a decision that his board considered borderline reckless. On the table was a proposal to acquire 15% of MCX for ₹459 crore—a huge bet on an exchange tainted by scandal, facing regulatory uncertainty, with trading volumes down 40% from peak. His investment committee was split. The risk managers saw disaster. But Kotak saw something else: India's commodity market infrastructure available at a distressed valuation.

The backstory to this moment was complex. Following SEBI's order to reduce stake, FTIL had been desperately seeking buyers for its 26% MCX holding. The process had been humiliating. Initial feelers to strategic investors—NYSE, Singapore Exchange, London Stock Exchange—received polite rejections. Nobody wanted association with the NSEL scandal. Domestic institutions were equally wary; the reputational risk seemed to outweigh any potential returns.

The auction process launched in December 2014 reflected this pessimism. FTIL set a floor price of ₹500 per share, a 40% discount to the prevailing market price of ₹830. Even at this distressed valuation, initial interest was lukewarm. The Bombay Stock Exchange expressed interest but withdrew citing regulatory complications. Bajaj Finserv evaluated but passed. The National Stock Exchange couldn't bid due to competitive restrictions.

Enter Kotak Mahindra, an institution that had built its reputation on conservative banking and measured risks. The interest seemed incongruous—what was India's most careful bank doing bidding for an exchange associated with India's messiest financial scandal? But Kotak's analysis went deeper than headlines.

The due diligence team, led by senior executive Dipak Gupta, spent three months inside MCX. They examined every contract, interviewed key employees, analyzed technology architecture, stress-tested financials. Their conclusion was counterintuitive: MCX's core business was completely insulated from NSEL. The technology was robust, market position dominant, regulatory moat intact. The scandal had destroyed price, not value.

The valuation math was compelling. At ₹600 per share (the eventual purchase price), Kotak was paying less than 20 times FY2014 earnings—compared to 35 times at IPO. The replacement cost of MCX's technology and infrastructure exceeded ₹1,000 crore. The customer relationships and regulatory licenses were essentially priceless. Even assuming zero growth, the investment would yield 15% returns through dividends alone.

But Kotak's interest went beyond financial returns. The bank saw MCX as strategic entry into capital markets infrastructure. Commodity financing was growing at 25% annually. Corporate clients needed hedging solutions. Owning India's dominant commodity exchange would position Kotak at the center of this ecosystem. It was a 10-year bet on India's financialization.

The negotiation was brutal. FTIL, desperate for regulatory approval to exit, had little leverage. Kotak demanded warranties on technology ownership, indemnities against NSEL liabilities, and board seats proportionate to shareholding. The final price of ₹459 crore for 15% stake valued MCX at just ₹3,060 crore—42% below its IPO valuation three years earlier.

The regulatory approval process was extensive. SEBI scrutinized Kotak's fitness as exchange owner, examining everything from capital adequacy to management competence. FMC evaluated potential conflicts of interest. Competition Commission analyzed market concentration impacts. The approval, granted in August 2015, came with conditions: strict arm's-length operations, Chinese walls between banking and exchange, and independent board oversight.

Kotak's entry catalyzed broader institutionalization. State Bank of India increased its stake to 7%. HDFC Bank acquired 5%. Collectively, India's largest financial institutions now owned over 40% of MCX. The shareholder register that once featured mysterious trading firms and Shah's associates now read like a who's who of Indian finance.

The management transformation was equally dramatic. Kotak brought in Mrugank Paranjape, a veteran banker with no commodity experience but deep governance expertise, as CEO. The board was reconstituted with independent directors from RBI, SEBI, and industry. The technology contract with FTIL, source of endless controversy, was terminated and operations insourced.

The cultural shift was palpable. MCX's office in Mumbai's Bandra-Kurla Complex, once known for Shah's 2 AM emails and mercurial management, became a model of corporate governance. Quarterly earnings calls replaced sporadic disclosures. Risk management, previously focused on trading, expanded to operational and regulatory risks. Employee stock options, suspended during crisis, were reinstated to retain talent.

The operational improvements were systematic. Technology spending increased to ₹150 crore annually, focused on latency reduction and cybersecurity. New products launched after extensive consultation rather than Shah's unilateral decisions. International partnerships, severed during scandal, were slowly rebuilt—though now as commercial relationships rather than strategic alliances.

The financial recovery was swift. FY2016 revenues grew 18% to ₹380 crore as confidence returned. EBITDA margins improved to 61% through cost optimization. The stock price, which had bottomed at ₹475 in August 2014, crossed ₹1,000 by December 2015. Kotak's investment had nearly doubled in eight months. But the most significant change was strategic repositioning. Under Shah, MCX had pursued growth at any cost—new products, international ventures, aggressive pricing. Under Kotak, the focus shifted to sustainable profitability. Unprofitable contracts were discontinued. International ambitions were shelved. The emphasis moved from market share (already dominant) to margin expansion.

The technology transformation deserves special mention. In 2014, Kotak Mahindra Bank acquired a 15% stake in Multi Commodity Exchange (MCX) from Financial Technologies Group for ₹459 crore, but the real work began after acquisition. MCX spent ₹200 crore over two years completely rebuilding its technology stack, migrating from FTIL's systems to a combination of in-house development and third-party solutions. The new architecture improved latency by 40%, reduced operational costs by 25%, and eliminated any technological dependence on Shah's companies.

The regulatory relationship transformation was equally important. Under Shah, MCX had an adversarial relationship with regulators—pushing boundaries, exploiting loopholes. Kotak brought a collaborative approach. Monthly meetings with SEBI replaced annual confrontations. Compliance staff doubled. Every new product underwent extensive regulatory consultation. The exchange that had been seen as rogue became the model corporate citizen.

Market participants noticed the change immediately. "MCX under Shah was innovative but unpredictable," noted a senior commodities trader. "Under Kotak, it became boring but reliable. For an exchange, boring is good." Trading volumes, which had plummeted during the crisis, began steady recovery. New members joined, reassured by institutional ownership.

The competitive dynamics also shifted. NSE and BSE, India's largest stock exchanges, had long wanted to enter commodity trading but were blocked by regulations. Post-crisis, regulators were more amenable to competition. But MCX's institutional backing made it a formidable incumbent. When NSE finally launched commodity trading in 2018, MCX retained over 90% market share—the moat had held.

For Kotak, the investment proved extraordinarily successful. Beyond financial returns, MCX provided strategic benefits: deep understanding of commodity markets, relationships with corporate hedgers, data on trading patterns. The bank launched new products—commodity financing, structured derivatives—leveraging MCX insights. The ecosystem play Shah had envisioned was being realized, just under different ownership.

The broader lesson was profound. MCX's successful transition from founder-led to institution-owned proved that Indian financial infrastructure could mature beyond individual dependence. The exchange that had been Jignesh Shah's personal creation became a true market institution, owned by India's leading banks, governed by independent boards, regulated by strengthened oversight.

By 2016, the transformation was complete. MCX's market share exceeded 90%, revenues crossed ₹400 crore, and the stock price recovered to IPO levels. Kotak's stake, acquired for ₹459 crore, was worth over ₹800 crore. But the real victory wasn't financial—it was proving that even the most spectacular corporate collapse could be reversed through patient, systematic institution-building.

The Kotak acquisition marked the end of MCX's adolescence and the beginning of its maturity. The exchange would never again see the explosive innovation of the Shah era, but it would also never again face existential crisis. In choosing stability over dynamism, MCX had chosen survival. And in India's commodity markets, survival itself was success.

VIII. Modern Era: Monopoly Strengthened (2014-Present)

The numbers tell a story of complete market domination. MCX has a 95.9% share in the commodity futures market in FY24. It controls a 100% share of precious metals & stones, 99.61% in energy & 99.80% in base metals. If anything, MCX's monopoly has strengthened since the crisis that nearly destroyed it. How did an exchange that lost its founder, faced regulatory censure, and saw volumes collapse emerge with even greater market power?

The answer begins with an unlikely ally: the Indian government's 2016 demonetization drive. When Prime Minister Modi withdrew 86% of currency notes overnight, Indian savers rushed to gold—but physical gold markets were in chaos. MCX's electronic gold contracts became the only reliable price discovery mechanism. Daily volumes in gold futures jumped 300% in November 2016. The exchange that had been tainted by scandal was suddenly indispensable national infrastructure.

The integration with SEBI in September 2015 marked another turning point. The Forward Markets Commission, which had overseen commodities since 1953, was merged into SEBI, bringing commodity and securities markets under unified regulation. For MCX, this meant access to SEBI's deeper resources, clearer regulations, and most importantly, institutional legitimacy. The same regulator overseeing BSE and NSE now oversaw MCX—a powerful signal to market participants.

Product innovation accelerated post-2017, but with a distinctly different flavor from the Shah era. Where Shah had launched products weekly with minimal consultation, the new MCX spent months developing each contract. The 2018 launch of brass futures involved 18 months of industry consultation, pilot trading programs, and warehousing infrastructure development. Slow, methodical, but successful—the contract achieved ₹100 crore daily volumes within six months.

The competitive threat from NSE's commodity segment launch in October 2018 proved anticlimactic. Despite NSE's massive resources and existing relationships with brokers, their commodity volumes remained negligible. MCX's network effects were simply too strong—every hedger, every speculator, every arbitrageur was already on MCX. Why trade on NSE's thin markets when MCX offered deep liquidity? Three years after launch, NSE's commodity market share remained below 2%.

Technology modernization continued relentlessly. In 2019, MCX completed migration to a new trading platform capable of processing 200,000 orders per second—10x the previous capacity. Latency dropped to microseconds. Co-location services allowed high-frequency traders direct access to exchange servers. The exchange that had pioneered electronic commodity trading in India was ensuring it remained at the technological frontier.

The introduction of options trading marked a strategic inflection. Launched in October 2017 with gold options, the product category exploded. By 2020, MCX was trading crude oil options, copper options, silver options. MCX is the 7th largest by the number of commodity futures traded and the 6th largest by the number of commodity options. Options provided hedgers more flexibility and speculators more leverage, driving volumes to record levels.

But the true test came with COVID-19. On April 20, 2020, WTI crude oil futures went negative for the first time in history. MCX's crude contracts, which tracked WTI, faced an unprecedented situation. The exchange's risk management systems, upgraded post-NSEL crisis, handled the volatility flawlessly. While some international brokers faced massive losses, MCX cleared all trades without defaults. The crisis that could have destroyed confidence instead enhanced it.

The commodity transaction tax (CTT) introduction in July 2020 was supposed to level the playing field between exchanges. The government imposed 0.01% tax on commodity derivatives, similar to securities. Industry worried this would kill volumes—agricultural futures trading had collapsed when CTT was introduced in 2013. But MCX's volumes barely budged. When you control 96% of the market, traders have nowhere else to go. Recent product launches showcase the mature MCX's strategic focus. The Multi Commodity Exchange of India (MCX) officially launched electricity futures trading on Thursday, July 10, 2025, following regulatory approval from the Securities and Exchange Board of India (SEBI) in June 2025. This wasn't Shah-style innovation for innovation's sake, but careful expansion into adjacent markets where MCX's infrastructure provided natural advantages. The introduction of electricity futures marks a landmark development, enabling businesses, power companies, and investors to manage risks associated with electricity price fluctuations and unpredictable demand patterns. The financial performance reflects this monopolistic positioning. Q1 FY2026 results were extraordinary: revenue of ₹373.21 crore, up 59% year-over-year. Profit after tax of ₹203.19 crore, up 83% from the previous year. Average daily turnover reached ₹3,10,775 crore, driven by renewed participant interest. This wasn't just recovery from crisis—it was acceleration beyond previous peaks.

The institutional participation story deserves special attention. Mutual funds, initially banned from commodity derivatives, received permission in 2019. Alternative Investment Funds followed in 2020. Foreign Portfolio Investors gained access in 2021. Each new category of participant deepened liquidity, reduced volatility, and legitimized commodity trading as an asset class. MCX, as the monopoly platform, captured all this flow.

International recognition followed domestic dominance. MCX ranks among the world's top commodity exchanges—7th largest by futures volume, 6th by options. The exchange trades more gold futures than any exchange outside China. Its crude oil contract is Asia's most liquid energy derivative. These aren't just vanity metrics—they attract global participants who need exposure to Indian commodity prices.

The regulatory moat has only strengthened. SEBI's 2019 guidelines on exchange ownership make new entry virtually impossible. Minimum net worth requirements exceed ₹300 crore. Technology specifications demand microsecond latency. Product approval processes take 12-18 months. Even if a competitor cleared these hurdles, they'd face MCX's 96% market share—an insurmountable network effect.

Recent strategic initiatives showcase sophisticated thinking. The index derivatives launched in 2022—MCX iCOMDEX Bullion, Base Metal indices—allow portfolio-level hedging. The warehouse financing platform connects physical and derivatives markets. The data analytics services monetize MCX's unique dataset of Indian commodity flows. Each initiative leverages the core monopoly while expanding the moat.

The balance sheet remains a fortress. Cash and investments exceed ₹1,400 crore. The company is debt-free. Capital expenditure runs at ₹100-150 crore annually, easily funded from operations. Dividend payout ratios exceed 50%, returning cash to shareholders while retaining sufficient capital for growth. This is the financial profile of a mature monopoly.

Looking ahead, growth drivers remain robust. India's commodity market penetration is minimal—less than 1% of physical market participants use derivatives. Financialization is accelerating as corporations professionalize risk management. New products like carbon credits and weather derivatives could open entirely new markets. The monopoly position ensures MCX captures the vast majority of this growth.

The transformation from Shah's MCX to today's institutionalized monopoly is complete. The exchange that nearly collapsed in scandal has emerged stronger than ever. Daily volumes exceed ₹300,000 crore. Market share approaches 100% in key segments. Profitability margins exceed 50%. The stock trades at all-time highs, valued at over ₹40,000 crore.

Yet questions remain. Can any business maintain 96% market share indefinitely? Will regulators eventually force competition? Could technology disruption—blockchain, decentralized exchanges—threaten the monopoly? These are the uncertainties that prevent MCX from trading at truly astronomical valuations despite its dominant position.

For now, MCX stands as perhaps India's most successful financial infrastructure monopoly. It survived its founder's disgrace, regulatory upheaval, competitive threats, and emerged with strengthened dominance. The modern MCX may lack the swashbuckling innovation of the Shah era, but it has something more valuable: institutional permanence. In India's commodity markets, MCX isn't just dominant—it's indispensable.

IX. Business Model Deep Dive

To understand MCX's economics, imagine owning the only toll bridge across a major river. Every vehicle must cross, you set the price, and your only costs are minimal maintenance. Now multiply that by India's entire commodity market—₹100 trillion in annual physical trade requiring price discovery and risk management. That's MCX's business model: a toll collector on the entire commodity economy with near-zero marginal costs.

The revenue architecture is elegantly simple yet devastatingly effective. Transaction fees account for 85% of revenues—MCX charges both buyers and sellers on every trade. The rates are minuscule, typically 0.0001% to 0.001% of contract value, but volumes are massive. A single day's turnover of ₹300,000 crore generates ₹3-4 crore in transaction fees. With 250 trading days annually, that's ₹750-1,000 crore from transaction fees alone.

But here's the genius: MCX's fee structure creates a virtuous cycle. Lower fees attract more volume, which creates deeper liquidity, which attracts more participants, who generate more volume. Competitors can't simply undercut prices because without liquidity, lower fees are meaningless. It's like trying to compete with Google by building a cheaper search engine—price isn't the product, network effects are.

The operational leverage is staggering. Whether MCX processes 1,000 trades or 1 million, the technology infrastructure cost remains largely fixed. Staff costs are stable—you need the same surveillance team regardless of volumes. Regulatory compliance doesn't scale with activity. This means every incremental rupee of revenue flows almost directly to the bottom line. EBITDA margins consistently exceed 60%, among the highest of any listed Indian company.

Technology licensing, though reduced post-FTIL exit, remains a meaningful revenue stream. MCX licenses its trading platform to smaller regional exchanges, its data feeds to brokers, its risk management systems to clearinghouses. These generate ₹50-75 crore annually—high-margin revenues that require minimal incremental investment. It's selling the same product multiple times to different customers.

The data monetization opportunity is vastly underexploited. MCX possesses India's most comprehensive dataset on commodity flows, price patterns, and trader behavior. Every transaction, every order, every cancellation generates valuable information. Currently, MCX sells basic data feeds for ₹30-40 crore annually. But sophisticated analytics—predictive models, sentiment indicators, flow analysis—could multiply this revenue stream.

Membership fees provide a stable base. MCX has approximately 350 trading members, 50,000 authorized persons, and 2,000 clearing members. Annual membership fees range from ₹50,000 to ₹50 lakh depending on category. This generates ₹75-100 crore in highly predictable revenue. More importantly, membership fees create switching costs—members have invested in connectivity, training, and compliance specific to MCX.

The clearing and settlement revenues are growing rapidly. While MCX doesn't directly clear trades (that's done by its subsidiary, Multi Commodity Exchange Clearing Corporation), it earns fees for settlement services, collateral management, and margin administration. As options volumes grow—requiring daily mark-to-market and complex margin calculations—these revenues are expanding at 30% annually.

Working capital dynamics are extraordinary. MCX collects fees instantly on execution but pays expenses monthly. This negative working capital cycle means growth actually generates cash rather than consuming it. The faster MCX grows, the more cash it accumulates. In most businesses, growth requires capital. At MCX, growth provides capital.

The balance sheet tells a story of financial fortress. Company is almost debt free. Cash and investments exceed ₹1,400 crore, generating ₹80-100 crore in investment income annually. This isn't idle cash—it's regulatory capital, providing comfort to participants and regulators. But it also means MCX earns substantial income simply from existing, before processing a single trade.

Capital allocation has been disciplined post-institutionalization. Annual capex of ₹100-150 crore maintains technological edge—new matching engines, enhanced surveillance systems, cybersecurity upgrades. R&D spending of ₹50 crore annually develops new products. The rest flows to shareholders—dividend payout ratios exceed 50%, with special dividends during exceptional years.

The unit economics are remarkable. Customer acquisition cost is essentially zero—traders come to MCX because that's where liquidity exists. Customer lifetime value is enormous—institutional traders generate millions in fees over decades. The ratio of LTV to CAC approaches infinity, a mathematical impossibility in normal businesses but reality for monopoly infrastructure.

Competitive dynamics reinforce economics. When NSE launched commodity trading, they offered negative fees—paying traders to provide liquidity. Yet they captured less than 2% market share. Why? Because in exchange economics, liquidity is the product, not price. Traders will pay higher fees for better execution. MCX's monopoly liquidity allows it to charge premium prices while maintaining dominant share.

The regulatory framework provides additional economic protection. SEBI mandates minimum net worth for exchanges, specific technology requirements, elaborate compliance procedures. These regulations, while ensuring market integrity, also create massive barriers to entry. A new exchange would need ₹500+ crore just to meet regulatory requirements before generating a single rupee of revenue.

International comparisons highlight MCX's advantageous position. CME Group, the world's largest derivatives exchange, operates in competitive markets with 30-40% share in key products. Their EBITDA margins are 45-50%. MCX, with 96% market share and similar cost structures, achieves 60-65% margins. Monopoly power translates directly to superior economics.

The risk-reward profile is asymmetric. Downside is limited—even losing 20% market share would leave MCX dominant with 75%+ share. Upside is substantial—India's commodity derivatives penetration is less than 1% of physical markets versus 20-30% in developed economies. A 10x growth opportunity exists even assuming no market share gains.

Future economics could improve further. Blockchain technology could reduce settlement costs. Artificial intelligence could automate surveillance. Cloud computing could lower infrastructure expenses. Each technological advance improves margins while strengthening competitive moats. MCX is a rare business where technology is purely margin-accretive rather than disruptive.

The sustainability question is critical. Can 60%+ margins persist indefinitely? History suggests yes—exchange monopolies globally have maintained high margins for decades. The Chicago Board of Trade dominated grain futures for 150 years. The London Metal Exchange controlled base metals for a century. Once established, exchange monopolies are nearly impossible to dislodge.

Yet regulatory risk looms. SEBI could mandate fee reductions, force market share caps, or promote competition. But regulators face a dilemma: weakening MCX could fragment liquidity, increase systemic risk, and harm market integrity. The cure could be worse than the disease. This regulatory catch-22 protects MCX's economics.

The true moat isn't technology or regulation—it's liquidity network effects. Every trader wants to trade where every other trader trades. This self-reinforcing dynamic means MCX's competitive advantage strengthens with scale. The bigger MCX gets, the harder it becomes to compete. It's a business model that would make Warren Buffett weep with joy—simple, profitable, and nearly impossible to disrupt.

In essence, MCX has achieved the holy grail of business models: a legal monopoly in a growing market with network effects, high margins, negative working capital, and minimal capital requirements. It's a toll road on India's commodity economy that gets wider and more profitable with every passing year. The only question isn't whether MCX will remain profitable, but just how profitable it can become.

X. Playbook: Lessons & Analysis

The MCX story offers a masterclass in building, destroying, and rebuilding financial infrastructure monopolies. Each phase—Shah's creation, the NSEL crisis, Kotak's rescue—provides distinct lessons that transcend commodity markets. This is ultimately a story about power: how to acquire it, how to lose it, and how institutions outlast individuals.

Lesson 1: First-Mover Advantage in Regulated Markets Is Everything

Shah understood something his competitors missed: in exchange businesses, being first isn't an advantage—it's the only thing that matters. By launching MCX just weeks before NCDEX, he captured the crucial early liquidity. Traders went where traders were, creating a self-reinforcing cycle. NCDEX never recovered from starting second, despite superior institutional backing.

The playbook is clear: in winner-take-all markets, speed trumps perfection. Shah launched with four products while competitors planned twenty. He focused on simple, global commodities while others chased complex agricultural contracts. Better to capture the market with a minimally viable product than lose it with a perfect one.

Lesson 2: Technology Is Table Stakes, Not Differentiator

MCX's technology was superior—microsecond latency, six-sigma reliability, elegant architecture. But technology alone didn't win. NCDEX had decent technology. NSE had better technology. Yet MCX dominated because Shah understood technology's proper role: it must be good enough to not lose, not good enough to win.

The real differentiator was distribution. MCX's 10,000 authorized persons reaching small traders mattered more than nanosecond latency improvements. The lesson for technology businesses is sobering: in financial infrastructure, distribution beats product every time.

Lesson 3: Regulatory Relationships Are The Ultimate Moat

MCX's relationship with regulators followed a three-act tragedy. Act 1: Cooperative innovation, with regulators supportive of market development. Act 2: Aggressive boundary-pushing, exploiting regulatory gaps. Act 3: Spectacular collapse when regulators turned hostile.

The Kotak era demonstrates the opposite playbook: boring, compliant, predictable. Monthly regulatory meetings. Preemptive consultation on new products. Conservative interpretation of rules. The result? Regulators became MCX's protectors, maintaining barriers that preserve its monopoly. The lesson: in regulated industries, being loved by regulators beats being smart.

Lesson 4: Founder Control Is Double-Edged Sword

Shah's absolute control enabled MCX's early success. Quick decisions, bold bets, relentless execution—impossible in committee-run organizations. But the same control enabled NSEL's disaster. No checks on Shah's ambition, no questioning of aggressive accounting, no pushback on regulatory violations.

The institutionalization under Kotak shows the alternative: slower decision-making but sustainable growth, less innovation but more stability, lower peaks but no valleys. For investors, the lesson is clear: founder-led businesses offer higher returns and higher risks. The key is knowing when founders become liabilities rather than assets.

Lesson 5: Corporate Governance Is Not Optional

The NSEL crisis was fundamentally a governance failure. Related-party transactions, conflicted board members, aggressive accounting—all classic governance red flags. Shah believed MCX's success exempted it from governance norms. The market's brutal punishment proved otherwise.

Post-crisis MCX demonstrates governance as competitive advantage. Independent directors with real power. Arms-length related-party transactions. Conservative accounting. Boring? Yes. But boring governance enables exciting returns. The playbook: treat governance as revenue-generating investment, not compliance cost.

Lesson 6: Network Effects Create Winner-Take-All Dynamics

MCX's 96% market share seems impossible in competitive markets. But exchange economics are different. Liquidity attracts liquidity. The value to each participant increases with total participants. Once critical mass is achieved, the network becomes self-sustaining and essentially unassailable.

This has profound implications for strategy. In network businesses, market share matters more than profitability initially. Shah understood this, offering negative fees to build liquidity. Competitors who focused on profitability never achieved the scale to compete. The playbook: in network businesses, lose money to gain share, then monetize the monopoly.

Lesson 7: Trust Is The Ultimate Currency

The NSEL crisis destroyed trust instantly. Years of reputation-building evaporated in days. Trading volumes collapsed not because MCX's technology failed but because participants lost faith. The recovery under Kotak was essentially trust reconstruction—new owners, new governance, new culture.

Financial infrastructure is ultimately trust infrastructure. Participants must trust the exchange won't fail, won't cheat, won't disappear. This trust, once lost, requires generational change to rebuild. The playbook: protect trust more zealously than profits. It takes decades to build, moments to destroy, and lifetimes to rebuild.

Lesson 8: Simplicity Scales, Complexity Fails

MCX succeeded with simple products—gold, silver, crude oil. NCDEX failed with complex agricultural contracts. The pattern holds globally: successful exchanges start simple and add complexity gradually. Failed exchanges start complex and never achieve scale.

The broader lesson transcends exchanges. In any platform business, simple and liquid beats complex and customized. Start with the largest, most standardized market. Achieve dominance. Then gradually add complexity. The playbook: capture the mainstream before serving niches.

Lesson 9: Crisis Creates Opportunity for Contrarians

Kotak's acquisition of MCX at distressed valuations demonstrates crisis investing at its finest. When sentiment is uniformly negative, prices detach from fundamental value. Kotak saw past the headlines to the underlying monopoly. Their 100% return in two years validates contrarian thinking.

But successful crisis investing requires more than courage. Kotak spent months on due diligence, understanding exactly what they were buying. They had the balance sheet to wait for recovery. They brought operational expertise to fix problems. The playbook: in crisis, buy quality assets with temporary problems, not poor assets with permanent problems.

Lesson 10: Institutions Outlast Individuals

The ultimate lesson is about permanence. Jignesh Shah built MCX but couldn't sustain it. His personal ambitions, conflicts, and failures nearly destroyed the institution. Under institutional ownership, MCX has flourished beyond Shah's imagination.

This pattern repeats across industries. Founder-led companies achieve breakthrough success but often face existential crises during succession. Those that successfully institutionalize—developing systems, processes, and governance independent of individuals—survive and thrive. Those that remain personality-dependent disappear with their founders.

The Meta-Lesson: Power Dynamics in Emerging Markets

MCX's story illuminates how power operates in emerging markets. Initial success requires navigating regulatory ambiguity, exploiting first-mover advantages, and building networks before rules solidify. But sustainable success requires different skills: regulatory compliance, institutional governance, and strategic patience.

Shah mastered the first game but failed the second. Kotak understood both games, acquiring Shah's creation at distressed prices and transforming it into institutional asset. This pattern—entrepreneurs creating, failing, and institutions capturing value—repeats across emerging markets.

For investors, the playbook is clear: back entrepreneurs early, but prepare for institutional transition. For entrepreneurs, the lesson is harder: building great companies requires knowing when to step aside. For regulators, the challenge is balance: enabling innovation while preventing excess.

The MCX story continues evolving, but its lessons are timeless. In financial markets, trust matters more than technology. In regulated industries, compliance beats innovation. In network businesses, liquidity is everything. And in all businesses, institutions outlast individuals.

These aren't just lessons about commodity exchanges. They're insights into how modern capitalism operates, how financial infrastructure develops, and how power shifts between entrepreneurs, institutions, and regulators. MCX's journey from startup to monopoly to crisis to resurrection encapsulates the entire lifecycle of financial innovation.

The playbook, ultimately, is about understanding these dynamics and positioning accordingly. Whether you're an entrepreneur, investor, or regulator, the MCX story offers a template for navigating the complex intersection of technology, regulation, and finance in emerging markets.

XI. Bull vs. Bear Case

The investment case for MCX presents a fascinating study in extremes. Bulls see an unassailable monopoly in a rapidly growing market. Bears see regulatory overreach and technological disruption. Both sides marshal compelling evidence. The truth, as always, lies in the nuanced evaluation of probabilities.

The Bull Case: Monopoly Mathematics

The arithmetic of MCX's dominance is staggering. Start with market share: Co. has a 95.9% share in the Commodity future market in FY24. It controls a 100% share of Precious metals & stones, 99.61% in Energy & 99.80% in base metals. In business, 60% market share is dominance. 80% is monopoly. 96% is essentially a utility. MCX has achieved a position so dominant that competition isn't just difficult—it's economically irrational.

The growth trajectory remains exponential. India's commodity derivatives penetration is less than 1% of physical market value, compared to 20-30% in developed markets. Even assuming India reaches just 10% penetration over the next decade, MCX's volumes would grow 10x. At current take rates, that implies revenues of ₹10,000+ crore annually. The monopoly ensures MCX captures virtually all this growth.

Operational leverage amplifies returns. MCX's marginal cost of processing an additional trade approaches zero. Fixed costs—technology, staff, compliance—are already covered. This means revenue growth flows directly to profits. If revenues grow 10x, profits might grow 15-20x. Few businesses offer such explosive earnings potential.

The balance sheet provides unshakeable foundation. Company is almost debt free. With ₹1,400+ crore in cash, MCX could survive years of zero revenue. This financial fortress makes MCX essentially bankruptcy-proof, removing downside risk that haunts leveraged businesses. In finance, survival is success—and MCX's survival is guaranteed.

New product launches expand the addressable market. The Multi Commodity Exchange of India (MCX) officially launched electricity futures trading on Thursday, July 10, 2025. This move follows regulatory approval from the Securities and Exchange Board of India (SEBI) in June 2025. The introduction of electricity futures marks a landmark development, enabling businesses, power companies, and investors to manage risks associated with electricity price fluctuations and unpredictable demand patterns. Each new product category—carbon credits next, weather derivatives after—adds billions to TAM without cannibalization.

Institutional ownership provides governance stability. Kotak Mahindra Bank, State Bank of India, HDFC Bank—India's most conservative institutions own MCX. These aren't momentum traders but permanent capital. Their presence ensures professional management, conservative practices, and long-term thinking. The cowboy capitalism of the Shah era is permanently banished.

International expansion opportunities remain untapped. MCX's technology and expertise could power exchanges across emerging markets. Africa, Southeast Asia, Latin America—all need commodity trading infrastructure. Licensing deals or joint ventures could generate hundreds of crores without capital investment. The playbook that built MCX could be replicated globally.

The regulatory moat strengthens annually. Each new SEBI rule—higher net worth requirements, stricter technology standards, longer approval processes—makes new entry harder. Ironically, the regulations meant to control MCX now protect it. It's like environmental regulations that bankrupt small players while entrenching large incumbents.

Margin expansion seems inevitable. As volumes grow, MCX gains pricing power. Transaction fees could increase 20-30% without losing share—where else would traders go? Data monetization, barely started, could add ₹200-300 crore in pure margin revenue. Clearing services, technology licensing, index products—each adds high-margin revenue streams.

The bull case culminates in simple math: a monopoly business growing at 20-30% annually, with 60% margins, minimal capital requirements, and essentially no bankruptcy risk should trade at 40-50x earnings. MCX trades at roughly 25x. The valuation gap suggests 60-100% upside even assuming no multiple expansion.

The Bear Case: Regulatory Sword of Damocles

The bear thesis begins with regulatory reality. SEBI could destroy MCX's economics with a single circular. Mandate fee caps—profits evaporate. Force market share limits—monopoly disappears. Promote competition—margins collapse. MCX exists at regulatory pleasure, and pleasure can become displeasure instantly.

Historical precedent is sobering. India has repeatedly destroyed profitable monopolies through regulatory intervention. Telecom companies saw spectrum prices skyrocket. Power utilities faced tariff caps. Drug companies encountered price controls. Why should MCX escape the fate of every other "excessive" profit pool in India?

Political risk looms large. MCX's 60% margins during farmer distress and inflation create terrible optics. A populist government could easily paint MCX as a parasite on productive economy, extracting rents from farmers and businesses. The narrative writes itself: "Why should paper traders profit while real producers suffer?"