McDonald's: The Real Estate Empire Behind the Golden Arches

I. Introduction & Cold Open

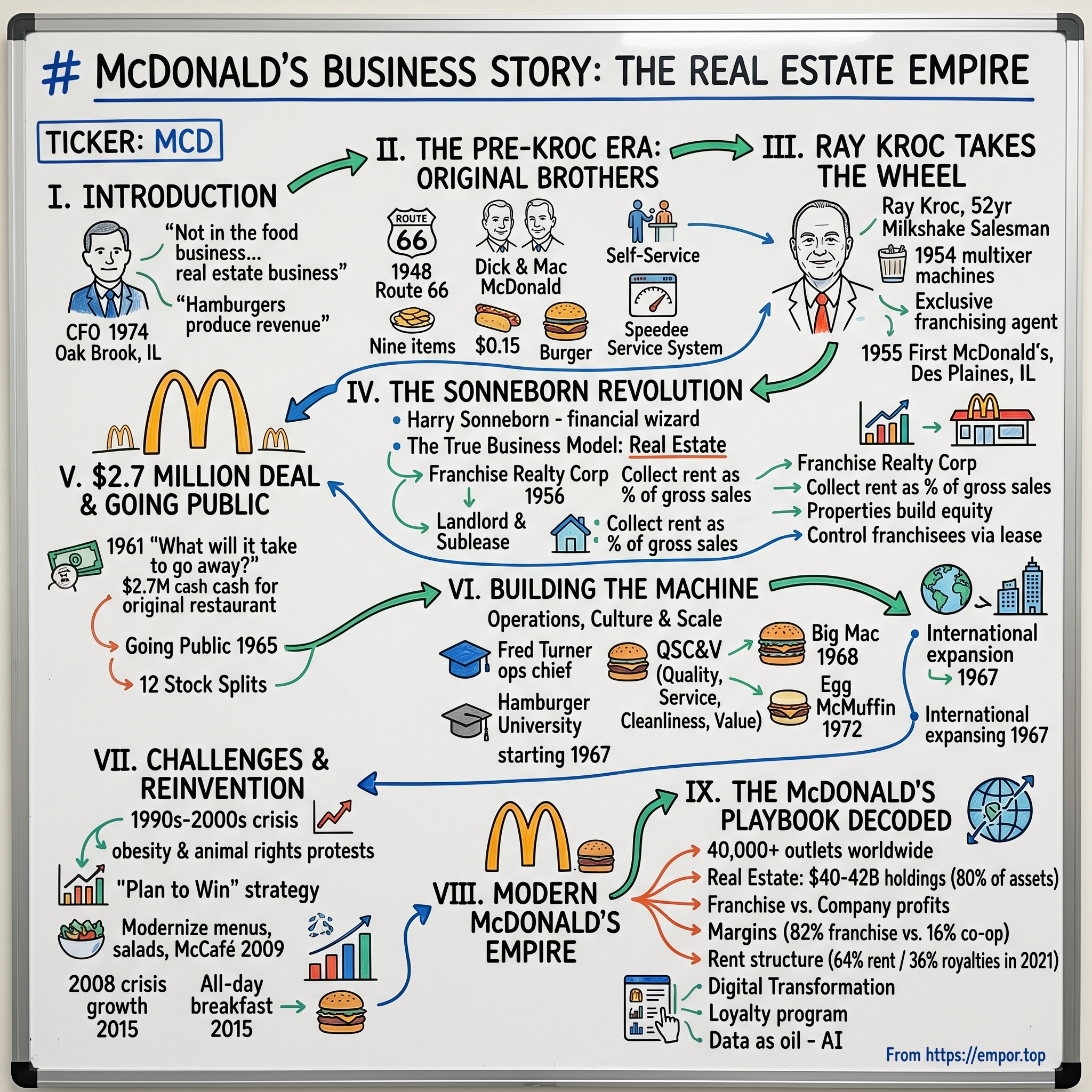

Picture this: It's 1974, and McDonald's executives are huddled in a conference room in Oak Brook, Illinois. The oil crisis has sent inflation soaring, beef prices have doubled, and competitors are slashing prices to survive. Yet McDonald's stock is up 30% that year. How? Because while everyone else was selling burgers, McDonald's was quietly amassing one of the largest real estate portfolios in America. The former CFO Harry J. Sonneborn once stood before a group of Wall Street analysts and delivered what might be the most important line in fast-food history: "We are not technically in the food business. We are in the real estate business. The only reason we sell hamburgers is because they are the greatest producer of revenue from which our tenants can pay us rent."

Today, with McDonald's stock trading at $313.08 and more than 40,000 restaurants worldwide, that paradox has never been more relevant. Is McDonald's really a fast-food company? Or is it one of the world's most sophisticated real estate investment trusts, disguised behind a clown mascot and golden arches?

What we're about to explore is how a 52-year-old milkshake mixer salesman from Illinois built not just a burger empire, but a property portfolio that would make most REITs envious. It's a story of accidental genius, fierce battles over control, and the discovery that the real money wasn't in the fryers—it was in the land beneath them.

II. The Pre-Kroc Era: The Original McDonald Brothers

The California sun beat down on Route 66 as cars lined up at the octagonal drive-in restaurant in San Bernardino. It was 1948, and brothers Richard "Dick" and Maurice "Mac" McDonald were about to fire their entire carhop staff. After years of running a successful but chaotic drive-in, they'd had enough of broken dishes, unreliable teenagers, and the endless complexity of a 25-item menu. What they did next would revolutionize not just their business, but the entire concept of food service.

The McDonald brothers' journey to that pivotal moment began far from California's orange groves. Born in New Hampshire to Irish immigrant parents, Dick and Mac had moved west in the 1920s with dreams of making it in Hollywood. They tried everything—pushing scenery around movie sets, managing a theater, even running a hot dog stand near the Santa Anita racetrack. Each venture taught them something, but none stuck. By 1940, they'd saved enough to open their first real restaurant: a drive-in barbecue joint in San Bernardino, complete with 25 carhops on roller skates serving customers in their cars.

The business was good—annual revenues hit $200,000, substantial for the time—but the brothers saw nothing but problems. The carhops were constantly quitting. Customers complained about wait times. Dishes disappeared faster than they could replace them. Teenagers loitered in the parking lot, turning away families. "We were in a rut," Mac would later recall. "The more we hammered away at the barbecue business, the more dissatisfied we became."

So in December 1948, they shut down for three months and completely reimagined their restaurant. Out went the carhops, the dishes, and most of the menu. In came what they called the "Speedee Service System"—a name that would soon become legendary. They redesigned their kitchen like an assembly line, with each worker responsible for one task. Burgers were pre-assembled. French fries replaced potato chips. The menu shrank to nine items. Most radical of all: hamburgers cost just 15 cents, nearly half what other restaurants charged.

When they reopened, customers were baffled. Where were the carhops? Why did they have to walk to a window? Local newspaper ads had to explain this strange new concept: "No Carhops—No Waitresses—No Dishwashers—No Bus Boys—The McDonald's System is Self-Service!" The first few months were rough. Sales plummeted. But gradually, families discovered something remarkable: they could feed a family of four for less than two dollars, and the food came out in under 30 seconds.

By 1952, the brothers' single location was generating $350,000 annually—nearly double their previous peak. American Restaurant Magazine featured them on the cover with the headline "The McDonald Brothers Present the Speedee Service System." Entrepreneurs started showing up from across the country, notepad in hand, studying every detail. The brothers, flush with success but wary of expansion, began selling franchises for a one-time fee of $950. No royalties, no ongoing fees—just a simple transaction and some basic blueprints for their revolutionary "golden arches" design that architect Stanley Meston had created.

Neil Fox opened the first franchise in Phoenix in 1953, insisting on using the McDonald's name despite the brothers suggesting he use his own. By 1954, the brothers had sold 21 franchises, though only ten were actually operating. They were content—they had their fishing trips, their new Cadillacs, and a business that ran itself. National expansion? That seemed like unnecessary headache.

Then one day in 1954, their milk shake machine supplier called with a curious question. Ray Kroc, a 52-year-old salesman from Prince Castle Sales, wanted to know why a single restaurant in San Bernardino needed eight of his five-spindle Multimixer machines—enough capacity to make 40 milkshakes simultaneously. Most restaurants used one, maybe two. What exactly were the McDonald brothers doing out there in the desert?

Kroc decided he had to see for himself. He flew to Los Angeles, rented a car, and drove the sixty miles east through orange groves and desert scrubland. What he found when he arrived would change his life—and American business—forever. The sight of the lunch rush, with its orchestrated chaos producing perfect burgers every twelve seconds, struck him like a religious vision. Here was efficiency elevated to art. Here was the future.

But the McDonald brothers, comfortable in their success and routine, saw things differently. They'd found their golden goose. Why complicate things with aggressive expansion? They had no idea that the persistent salesman standing in their parking lot, watching customers stream through with bags of burgers, was about to transform their clever little system into the largest restaurant empire the world had ever seen.

III. Ray Kroc Takes the Wheel (1954–1961)

Ray Kroc couldn't sleep that night at the motel in San Bernardino. The image of those silver and red tiles, the ballet of workers at their stations, the endless stream of families walking away with white paper bags—it all swirled in his mind like a fever dream. At 52 years old, after decades of hustling everything from paper cups to real estate in Florida, he'd finally found what he'd been searching for his entire life. He just didn't know it yet.

Kroc's path to that California parking lot had been anything but straight. During World War I, he'd lied about his age to join the Red Cross ambulance corps, training in Connecticut alongside another young dreamer named Walt Disney. While Disney went on to build animation empires, Kroc bounced from job to job through the 1920s and '30s—playing piano in jazz bands, selling paper cups for Lily Tulip Cup Company, hawking real estate in Florida just before the market crashed. He had the salesman's gift of seeing potential everywhere, but nothing quite stuck.

By the early 1940s, he'd found moderate success as the exclusive distributor for the Prince Castle Multimixer, a five-spindle milkshake machine that could make five shakes at once. It was steady work, driving from restaurant to restaurant across the Midwest, demonstrating his machines. But sales were declining. The golden age of the soda fountain was ending. Drive-ins were switching to softer ice cream that didn't need heavy-duty mixers. At 52, Kroc was watching his business slowly die.

Then came that phone call about the McDonald brothers' eight machines. After seeing their operation in 1954, Kroc approached Dick and Mac with trembling enthusiasm. "Why don't you open a McDonald's in Des Plaines?" Mac asked, almost offhandedly. "You could do it." But Kroc had bigger dreams. He wanted to be their exclusive franchising agent, taking their system nationwide while they collected royalties from their California comfort.

The negotiations revealed the fundamental difference between them. The brothers wanted simplicity—maybe a few hundred locations, max. Quality control. No headaches. Kroc envisioned thousands of golden arches from coast to coast. The deal they struck reflected this tension: Kroc would get exclusive rights to franchise the McDonald's system nationwide. The brothers would receive 0.5% of gross sales from all new franchises. Kroc's new company would get 1.9% of gross sales, from which he'd have to cover all expenses of finding franchisees, ensuring quality, and providing support. It was a tough deal—Kroc would later call it "a almost fatal flaw"—but he signed it anyway.

On April 15, 1955, Kroc opened his first McDonald's in Des Plaines, Illinois, a suburb of Chicago. He'd chosen the location carefully—near his home, where he could watch it like a hawk. Opening day was a disaster. The ventilation system couldn't handle the french fry production. The potato storage room was too small. Customers lined up around the building. But Kroc was in his element, sleeves rolled up, working the fry station himself, barking orders, solving problems in real-time.

By year's end, Kroc had opened two more locations, generating combined gross sales of $235,000. But the math was brutal. His 1.9% share meant revenues of just $4,465—before expenses. He was paying managers, covering construction overruns, traveling constantly to check on operators. Meanwhile, he was still trying to sell Multimixers to keep cash flowing. His secretary, June Martino, would later recall him pacing the office, muttering about cash flow, calling franchisees to ensure they'd paid their royalties on time.

The franchisees themselves were a carefully selected bunch. Kroc had strong opinions about who should run a McDonald's. No wealthy investors looking for passive income. No chains or consortiums. He wanted owner-operators—people who would work in their restaurants, sweat the details, treat it like their life's work. "We want the man who will get on his knees and roll up his sleeves," he'd tell prospective franchisees. His ideal operator was often a traveling salesman like himself, someone who understood customer service and had saved enough for the $75,000 total investment required.

But three years in, by 1958, Kroc was nearly broke. The franchise fees barely covered his overhead. He'd mortgaged his house twice. His wife Ethel was threatening divorce over the financial strain. He was 56 years old, working eighteen-hour days, driving from restaurant to restaurant in his Cadillac, personally inspecting french fries with a thermometer. The McDonald brothers, comfortable in California, would occasionally send notes questioning his decisions, his standards, his expansion pace. Every approval had to go through them. Every menu change. Every alteration to the sacred system.

One night in 1956, drowning his frustrations at a country club in Chicago, Kroc poured out his troubles to a fellow member. "You've got a great concept," the man said, "but you're missing the real business here." That man would introduce Kroc to someone who would change everything: Harry J. Sonneborn, a financial wizard from Tastee-Freez with an idea so radical it would transform McDonald's from a struggling franchise operation into one of the world's most valuable companies.

The introduction would come at exactly the right moment. Kroc was desperate, the McDonald brothers were becoming increasingly difficult about approvals, and Sonneborn had been studying the restaurant's books with the eye of someone who saw not just hamburgers and real estate, but an entirely different business model hiding in plain sight.

IV. The Sonneborn Revolution: Discovering the Real Business Model (1956–1967)

Harry Sonneborn didn't eat hamburgers. The lean, precise financial executive from Tastee-Freez viewed food as fuel, nothing more. So when he first met Ray Kroc at that Chicago country club in 1956, he wasn't interested in the quality of McDonald's burgers or the speed of service. While Kroc waxed poetic about french fry perfection, Sonneborn was doing math on a napkin. What he saw in those numbers would revolutionize not just McDonald's, but the entire franchise industry.

"You don't seem to understand," Sonneborn told Kroc after reviewing the books. "You're not in the burger business. You're in the real estate business."

Kroc initially resisted. He was a product man, obsessed with operations, with the perfect fry, the exact pickle placement. Real estate? That was for developers and speculators, not restaurant men. But Sonneborn persisted with a clarity that cut through Kroc's operational fog. The current model—collecting 1.9% of gross sales, with 0.5% going to the McDonald brothers—would never generate enough cash to fund expansion. The math simply didn't work. A restaurant doing $200,000 in annual sales generated just $3,800 for Kroc's company. After paying for field support, accounting, and overhead, there was nothing left.

But what if, Sonneborn proposed, McDonald's became the landlord?

The concept was elegantly simple. Instead of just collecting franchise fees, McDonald's would lease the land and building, then sublease it to the franchisee at a markup. Initially, they'd lease properties themselves from landowners, adding a 20% markup when subleasing to franchisees. But the real opportunity would come when they could buy the land outright, taking out mortgages that the franchisees' rent would pay off. McDonald's would build equity while franchisees built sales.

In 1956, Kroc let Sonneborn establish Franchise Realty Corporation, a separate entity that would handle all real estate transactions. The first deal under the new model was in Hamden, Connecticut. McDonald's leased the property from the landowner, then subleased it to the franchisee at a 20% markup. But Sonneborn had bigger ambitions. By 1957, he'd convinced Kroc to start taking out mortgages to buy properties outright. The company would own both land and building, becoming the franchisee's landlord in the fullest sense.

The genius of Sonneborn's model revealed itself in the details. First, rent was calculated as the greater of a fixed percentage markup (eventually reaching 40%) or 5% of the restaurant's gross sales. This meant that as franchisees succeeded, McDonald's real estate income grew proportionally. Second, McDonald's financed properties using long-term fixed-rate mortgages but passed through variable costs to franchisees. As inflation rose through the 1960s, McDonald's paid off loans with increasingly cheap dollars while collecting increasingly valuable rent.

But perhaps most importantly, property ownership gave McDonald's unprecedented control over its franchisees. Can't maintain standards? Your lease won't be renewed. Want to sell your franchise? McDonald's has approval rights over the buyer. Thinking about adding menu items or changing procedures? Your landlord might have something to say about that.

By 1958, this real estate strategy was generating more income than franchise fees. A restaurant doing $300,000 in sales might pay $15,000 in rent (5% of sales) plus $5,700 in franchise fees—but the rent went straight to paying down mortgages that built McDonald's equity. Within a few years, a property might be paid off entirely, yet still generating that 5% of sales in pure profit.

Sonneborn's disciplined financial approach extended beyond real estate. In 1959, he was appointed McDonald's first president and CEO, with Kroc becoming chairman. Sonneborn instituted rigid financial controls, standardized accounting procedures, and most importantly, a conservative expansion strategy focused on cash flow rather than growth for growth's sake. While Kroc dreamed of golden arches on every corner, Sonneborn insisted each new restaurant had to make financial sense.

The tension between the two men was palpable and, in many ways, productive. Kroc would identify an ideal corner in a growing suburb; Sonneborn would analyze the demographics, traffic patterns, and financing options. Kroc wanted to expand into city centers; Sonneborn's models showed suburban locations generated better returns. Kroc pushed for company-owned stores to showcase best practices; Sonneborn demonstrated that franchised locations with McDonald's as landlord generated superior financial returns.

By 1960, McDonald's owned the real estate for 200 restaurants. The company's balance sheet had been transformed. Instead of just a service fee stream, McDonald's had hard assets—land and buildings in growing suburban markets across America. Banks that had once refused to lend to a "hamburger company" were now eager to finance what they saw as a real estate development firm with excellent tenant quality.

The model created an extraordinary alignment of interests. Franchisees couldn't succeed without strong sales, which meant maintaining McDonald's standards. McDonald's couldn't succeed without successful franchisees paying rent. Everyone had skin in the game. A failed restaurant meant a failed real estate investment. This mutual dependency forced a level of cooperation rare in franchise relationships.

But by 1967, the Kroc-Sonneborn partnership was fracturing. Sonneborn wanted to slow expansion, focusing on maximizing returns from existing properties. Kroc, now freed from the McDonald brothers' control (a story we'll explore next), wanted to accelerate. Sonneborn worried about overextension; Kroc saw competitors like Burger King gaining ground. The arguments became increasingly public and bitter.

The breaking point came at a board meeting where Sonneborn suggested McDonald's had grown enough, that they should focus on operations rather than expansion. Kroc exploded. "The hell with that!" he shouted. "If you can't see the potential, then you don't belong here!" By the end of 1967, Sonneborn was gone, his rigid financial discipline replaced by more aggressive expansion under Kroc's direct control.

Yet Sonneborn's legacy was secure. His real estate model had transformed McDonald's from a struggling franchise company into a property powerhouse. By the time he left, McDonald's owned over $150 million in real estate. The company that couldn't get a bank loan in 1955 was now one of America's largest retail property owners. And the model he created—franchisee as tenant, McDonald's as landlord—would generate billions in value over the coming decades, proving that sometimes the most important innovation isn't in the product you sell, but in how you structure the business itself.

V. The $2.7 Million Deal & Going Public

The letter from Ray Kroc arrived at the McDonald brothers' San Bernardino office on a Tuesday morning in 1961. Dick McDonald opened it first, his hands trembling slightly as he read Kroc's simple question: "What will it take for you to go away?"

For years, the relationship had been deteriorating. Every new idea Kroc had—from adding basement rec rooms to restaurants to selling franchises in new territories—required the brothers' approval. They'd reject proposals seemingly at random, sometimes taking weeks to respond to urgent requests. Kroc would later claim they did it just to torment him, these two men in California who'd created something remarkable but couldn't see its full potential.

The brothers huddled in their small office, the same one where they'd first sketched out the Speedee Service System thirteen years earlier. They were tired—tired of the phone calls, the arguments, the constant push for more, faster, bigger. They wanted to go back to their simple life: their custom Cadillacs, their regular tee times at the country club, their single original restaurant that still bore their name.

"How much?" Mac asked his brother.

Dick pulled out a yellow legal pad and started writing numbers. They wanted enough to net a million dollars each after taxes. That meant roughly $2.7 million total—an astronomical sum for a company that had generated less than $75,000 in profit the previous year.

When Kroc received their response, he nearly choked. $2.7 million? He didn't have $2,700, let alone millions. His house was mortgaged to the hilt. His marriage to Ethel was hanging by a thread, strained by financial pressure and his constant absence. But he knew this was his moment. If he could find the money, he'd finally be free to build McDonald's his way.

Enter Harry Sonneborn's financial network. While Kroc scrambled, Sonneborn calmly worked his contacts. John Bristol, a Princeton graduate who'd made a fortune in manufacturing, was interested. So were several insurance companies looking for alternative investments. But the key player would be Paul Shiefer, an executive at First National Bank of Chicago, who saw past the hamburgers to the real estate empire Sonneborn had been building.

The negotiations were brutal. The brothers wanted cash—no stock, no earn-outs, no payment plans. They also wanted to keep their original San Bernardino restaurant. Fine, Kroc said, but it couldn't be called McDonald's. That name, those golden arches, that would all belong to him. The brothers agreed, planning to rename it "The Big M."

But there was one more issue, whispered about for decades after: the handshake deal. According to Kroc and multiple witnesses, the brothers requested one additional term that their lawyer advised them not to put in writing: 1% of revenues in perpetuity, not just from existing restaurants but from all future McDonald's locations. Kroc agreed, shaking hands on it. The brothers would later claim this royalty was supposed to continue forever, potentially worth hundreds of millions. Kroc would honor it only until the written deal closed.

On December 2, 1961, the papers were signed at the law offices of Chapman and Cutler in Chicago. The McDonald brothers received their $2.7 million—roughly $27 million in today's dollars—and walked away from the empire they'd unknowingly started. They returned to San Bernardino, reopened their restaurant as "The Big M," and watched from afar as their creation exploded across the globe.

But Kroc wasn't done with the brothers yet. In what many saw as a final act of revenge, he opened a new McDonald's just one block from The Big M, eventually driving them out of business. "I ran them out of business," Kroc would later admit with characteristic bluntness. "It was a question of pride."

With the brothers finally gone, Kroc turned to Sonneborn with a new challenge: they needed to go public. The $2.7 million purchase had drained their resources, and expansion required capital—lots of it. Sonneborn, ever the financial architect, began preparing for what would become one of the most successful IPOs of the 1960s.

The roadshow was a study in contrasts. Sonneborn would present the numbers—the real estate portfolio, the cash flows, the franchise agreements. Then Kroc would take over, evangelizing about quality, consistency, and the American dream of business ownership. Investors were initially skeptical. Restaurant stocks were notoriously volatile. But Sonneborn's real estate angle intrigued them. This wasn't just a restaurant company; it was a property company with built-in tenants. On April 21, 1965, McDonald's Corporation went public at $22.50 per share. The stock soared to $30 by the end of the first trading day, making instant millionaires of early investors and validating Sonneborn's financial architecture. A $100 investment at IPO would have bought 4.4 shares—a modest beginning to what would become one of the great wealth-creation stories in American business.

The real magic happened in the decades that followed. McDonald's executed 12 stock splits after going public, expanding share counts by a factor of 729. That initial 4.4-share purchase would have mushroomed into 3,208 shares through splits alone. By 2019, those shares would be worth over $622,000—and that's before accounting for decades of dividend reinvestment.

The public markets gave McDonald's something it had desperately needed: patient capital for aggressive expansion. No longer dependent on franchisee fees to fund growth, the company could now issue bonds backed by its growing real estate portfolio, use stock as currency for acquisitions, and most importantly, signal to potential franchisees that this was a permanent, stable enterprise worth betting their life savings on.

The post-IPO years also marked a subtle but critical shift in how McDonald's presented itself to the world. In meetings with analysts, Sonneborn would emphasize the real estate portfolio, the predictable cash flows, the recession-resistant nature of the business. "We are not technically in the food business," he'd famously tell investors. "We are in the real estate business." It was a message that resonated with Wall Street, transforming McDonald's from a risky restaurant play into a blue-chip property company with unparalleled tenant quality.

VI. Building the Machine: Operations, Culture & Scale (1960s–1980s)

Fred Turner was washing dishes in Ray Kroc's first Des Plaines McDonald's when a potato fell on the floor. Without thinking, he picked it up and threw it back in the fryer. Kroc exploded. "That potato cost me three cents!" he roared. "You throw it away, you've stolen from me, from the customer, from everyone!" Turner, then 23 years old, thought he was about to be fired. Instead, Kroc promoted him. Anyone who needed that lesson once would never forget it.

By 1961, Turner had become Kroc's operations chief, and McDonald's faced a crisis of scale. They had 200 restaurants with 200 different ways of making french fries. Some were crispy, some soggy. Some operators used Idaho russets, others whatever was cheap that week. The Big Mac existed in some locations but not others. Franchisees were adding their own menu items—pizza in one location, fried chicken in another. The system the McDonald brothers had perfected in San Bernardino was fracturing under the weight of expansion.

Turner's solution was radical for the restaurant industry: create a university. Not a training center or a workshop—an actual institution of higher learning dedicated to the science of quick-service restaurants. Hamburger University opened in the basement of a McDonald's in Elk Grove Village, Illinois, in February 1961, with a class of 15 students. Turner himself taught the first course, using a flip chart and a portable grill.

The curriculum was obsessively detailed. There were 19 steps to making perfect french fries, from the specific gravity of the potato (21% solids) to the precise temperature curve for blanching (two minutes at 150°F, cool for 20 minutes, then three minutes at 345°F). Students learned that pickles must be placed in a specific pattern to ensure even distribution. Onions were to be chopped to exactly one-quarter inch. The hamburger patty must be placed on the bun heel first, then dressed in a precise order: mustard, ketchup, onions, pickles. Any deviation was failure.

But Hamburger University taught more than food preparation. Franchisees learned real estate selection, equipment maintenance, crew scheduling, accounting principles. They studied time-motion efficiency, customer psychology, bathroom cleanliness standards. By graduation, they'd earned certificates in "hamburgerology with a minor in french fries"—a joke that masked serious purpose. These weren't just restaurant operators; they were systems engineers, each responsible for maintaining the integrity of the McDonald's machine.

The university became a powerful cultural force. Every franchisee, every manager, eventually every shift supervisor went through the program. They learned not just procedures but philosophy—Kroc's obsession with QSC&V (Quality, Service, Cleanliness, and Value), his hatred of waste, his belief that the customer was king. Stories became legends: Kroc finding a fly in a restaurant and shutting it down on the spot; Turner measuring hold times on burgers with a stopwatch; operations managers checking the temperature of restroom water to ensure comfortable hand-washing.

This operational discipline enabled McDonald's to tackle its next challenge: menu innovation. The Big Mac, introduced systemwide in 1968, wasn't invented by corporate but by Jim Delligatti, a Pittsburgh franchisee. But it took Turner's operations team 19 months to perfect it for mass production—developing the special sauce formula, designing the three-layer bun, creating assembly procedures that maintained speed despite complexity. When it launched nationally, every restaurant could produce an identical Big Mac in under 50 seconds.

The Egg McMuffin, introduced in 1972, represented an even bigger operational challenge. Created by franchisee Herb Peterson in Santa Barbara, it required McDonald's to enter the breakfast business—new equipment, new suppliers, new procedures, new labor schedules. Many franchisees resisted. Breakfast meant opening earlier, training for new products, competing with coffee shops. But Turner's operations machine ground through the obstacles. They developed a new grill for eggs, sourced English muffins that could be toasted quickly, created Canadian bacon specifications. Within five years, breakfast would account for 18% of McDonald's revenues. International expansion became the next frontier. McDonald's continued to grow and expand into international markets beginning in 1967 opening in Canada and Puerto Rico. McDonald's expanded into international markets with the opening in Canada of its restaurant in Richmond, British Columbia in June, 1967. The choice of Canada was deliberate—similar culture, shared language, minimal risk. But it opened the door to thinking globally.

The 1970s saw explosive international growth. In 1971, McDonald's opened its first European restaurant in Zaandam, Netherlands through a joint venture with supermarket chain Albert Heijn called Family Food N.V. The first restaurant in Asia opened in Tokyo, Japan in July 1971, and in December that year, the first German restaurant, which was then in West Germany, opened in Munich–Obergiesing. The first restaurant in Oceania opened in 1971 in Yagoona, Australia. Each market required adaptations—beer in Germany, rice burgers in Taiwan—but the core system remained intact.

Beyond the golden arches themselves, McDonald's pioneered corporate philanthropy in the restaurant industry. The first Ronald McDonald House opened in Philadelphia in 1974, created when Philadelphia Eagles player Fred Hill needed accommodation near the hospital where his daughter was being treated for leukemia. The concept spread worldwide, providing free housing for families with hospitalized children. It was brilliant marketing disguised as charity—or perhaps genuine charity with brilliant marketing benefits.

By 1980, McDonald's had 6,200 restaurants generating $6.2 billion in systemwide sales. The company that couldn't get a bank loan in 1955 was now one of America's most valuable corporations. The operational machine that Turner and his team built could replicate itself anywhere—from Tokyo's Ginza district to the Champs-Élysées. Each restaurant was a perfect copy of the system, yet flexible enough to adapt to local tastes and regulations.

The corporate culture that emerged from this period was unique in American business. McDonald's executives weren't typical corporate suits. They were operations obsessives who could still work a fry station, who spoke in acronyms (QSC&V, ABS—"Always Be Selling"), who viewed their business with almost religious devotion. Store visits by executives became legendary—they'd check the temperature of the dishwater, time the service, taste every product. One executive famously carried a tape measure to ensure that napkin dispensers were exactly 15 inches from the counter edge.

This operational excellence created a virtuous cycle. The better the operations, the stronger the sales. The stronger the sales, the more valuable the real estate. The more valuable the real estate, the more capital for expansion. By the end of the 1980s, what had started as a simple hamburger stand had evolved into something unprecedented: a globally standardized service experience that could be replicated 30,000 times while maintaining remarkable consistency. It was, in its own way, as impressive an achievement as landing on the moon—and considerably more profitable.

VII. Challenges & Reinvention (1990s–2000s)

Jim Cantalupo sat in his office at McDonald's Oak Brook headquarters on a gray morning in January 2002, staring at numbers that seemed impossible. For the first time in its 47-year history, McDonald's had posted a quarterly loss—$343.8 million. The stock had plummeted from $48 to $13, erasing more than half the company's value. Outside, protesters waved signs about obesity and animal rights. Inside, executives whispered about selling off real estate, closing restaurants, maybe even breaking up the company. The empire Ray Kroc built was crumbling.

The roots of the crisis stretched back through the 1990s, a decade when McDonald's had seemed invincible. The company had opened its 20,000th restaurant in 1996, pushing into 100 countries. But growth had become an addiction. New restaurants cannibalized old ones. In suburbs across America, you could stand in one McDonald's parking lot and see another golden arch down the street. The mantra was simple: more stores equals more revenue. Nobody questioned whether customers actually wanted what those stores were selling.

Meanwhile, the world was changing around them. Starbucks taught consumers to pay $4 for coffee. Chipotle—ironically, once owned by McDonald's—showed that people would pay more for "fresh" ingredients and visible preparation. Subway overtook McDonald's in number of locations by emphasizing health with its "Jared" weight-loss campaign. The documentary "Super Size Me" in 2004 would become a cultural phenomenon, with filmmaker Morgan Spurlock documenting his deteriorating health from eating only McDonald's for 30 days.

The menu had become a monster. In the pursuit of growth, McDonald's had added pizza, pasta, fajitas, wings—anything to drive traffic. Kitchen complexity soared. Service times increased. The core promise of fast, consistent food was breaking down. One franchise owner described opening his freezer to find 37 different products, half of which he couldn't identify. "We'd forgotten who we were," he later said.

Cantalupo, brought back from retirement in 2003 to save the company, initiated what he called "Plan to Win"—a radical refocusing on the basics. First, halt new restaurant construction in mature markets. Second, fix the food. Third, modernize the experience. It was a complete reversal of two decades of strategy. Wall Street was skeptical. Activists called for more dramatic change. But Cantalupo had seen McDonald's at its best, and he believed the core model still worked—it just needed evolution, not revolution.

The food transformation began with salads. Not the sad, wilted afterthoughts of the past, but premium salads with grilled chicken, Paul Newman dressing, actual vegetables people wanted to eat. Apple slices appeared in Happy Meals. The disastrous "Super Size" option was eliminated. Trans fats were removed from cooking oils. None of these changes alone would transform McDonald's, but together they began shifting perception. McDonald's wasn't becoming a health food restaurant, but it was acknowledging that customers wanted choices.

The real breakthrough came from an unexpected source: coffee. McDonald's had always served coffee, but it was an afterthought—burnt, bitter, forgotten on warmers for hours. The success of Starbucks stung personally for many executives. How had they let another company own morning coffee when McDonald's had millions of customers starting their day with Egg McMuffins? The McCafé initiative represented the most ambitious menu expansion since breakfast. McCafé coffees including lattes, cappuccinos and mochas were added to the U.S. national menu in 2009, and quickly expanded to include blended ice frappés and smoothies, triple-thick shakes as well as limited-time seasonal offerings. The investment was massive—new equipment, barista training, store renovations. But it worked. Since its nationwide rollout in May 2009, McCafé has helped McDonald's grow its coffee sales from 2 percent of U.S. sales to more than 6 percent, while stealing share from both Starbucks and Dunkin'.

The 2008 financial crisis, paradoxically, helped McDonald's. As consumers traded down from casual dining, McDonald's value proposition suddenly looked attractive again. The Dollar Menu became a lifeline for cash-strapped families. Same-store sales actually increased during the recession, one of the few restaurant chains to achieve that feat. The real estate model proved its genius once again—while competitors who leased their properties faced rent increases or eviction, McDonald's controlled its destiny.

But the most radical change came in 2015: all-day breakfast. For decades, McDonald's had insisted that operational complexity made it impossible to serve Egg McMuffins past 10:30 AM. Franchisees resisted, citing kitchen constraints and equipment limitations. But customer demand was relentless. Twitter campaigns begged for breakfast all day. Competitors like Jack in the Box mocked McDonald's inflexibility.

When McDonald's finally relented in October 2015, it was the biggest menu change in 30 years. The operational challenges were real—grills had to be reconfigured, procedures rewritten, crews retrained. But the impact was immediate. Same-store sales jumped 5.7% in the fourth quarter of 2015, the strongest growth in nearly four years. All-day breakfast had given customers a reason to visit McDonald's at 2 PM, at dinner, whenever they wanted.

By 2009, as the company emerged from its crisis years, it had fundamentally transformed. The real estate portfolio, once seen as dead weight during the dark days of 2002, had appreciated enormously. The menu had evolved while maintaining operational efficiency. Digital ordering and delivery partnerships were beginning to reshape the customer experience. The company that nearly collapsed had engineered one of the great corporate turnarounds in American business history.

VIII. The Modern McDonald's Empire

Walk into a McDonald's in Shanghai at 2 AM and you'll find teenagers studying for exams over McCafé lattes. Visit one in Paris and you might spot macarons in the display case. Pull up to a drive-through in Phoenix and a voice-recognition AI system will take your order. This is the modern McDonald's empire—with more than 40,000 outlets worldwide, it's less a restaurant chain than a global infrastructure project, a real estate colossus that happens to sell hamburgers.

The numbers tell a story that Ray Kroc could never have imagined. Today, McDonald's has over 40,000 restaurant locations worldwide, with around a quarter in the US. But it's the structure beneath those numbers that reveals the true genius of the model that Harry Sonneborn built and subsequent leaders refined. The real estate holdings tell the story. McDonald's owns approximately $40-42 billion worth of land and buildings (before depreciation), with real estate assets accounting for about 80% of total assets on its balance sheet. The company owns about 45% of the land and 70% of the buildings at its 36,000+ locations. This isn't just property ownership—it's strategic control over some of the most valuable commercial corners in the world.

The franchise model has evolved into something approaching perfection. In 2014, McDonald's made $27.4 billion in revenues, of which $9.2 billion came from franchised locations and $18.2 billion from company-operated restaurants. But the real story is in the margins: McDonald's keeps close to 82% of all their franchise-generated revenue versus only 16% of its company-operated restaurant revenue. Of that $18.2 billion generated by company-operated stores, the corporation keeps just $2.9 billion. Of the $9.2 billion coming from franchisees, the corporation keeps $7.6 billion.

Think about that math for a moment. A company-operated restaurant might generate more gross revenue, but after paying for food, labor, utilities, and all the other costs of actually running a restaurant, McDonald's keeps just a sliver. But with franchised locations, the franchisee bears all those operational costs. McDonald's just collects rent and royalties—pure, high-margin income that flows straight to the bottom line.

The rent structure itself is a masterwork of financial engineering. In 2021, McDonald's made $13.1B in revenue from franchisees. Rent was 64% ($8.4B) and Royalties was 36% ($4.6B) of that figure. At the individual level, 8-15% of franchisee sales go to rent. Overall, rent accounts for 35% of McDonald's TOTAL revenue. Franchisees in the U.S. can pay up to 16% of sales in rent, plus a 5% royalty fee and 5% for advertising—meaning McDonald's can capture up to 26% of a restaurant's gross sales before the franchisee pays a single employee or buys a single burger patty.

The 20-year franchise agreements create extraordinary stability. A franchisee invests their life savings—often $1-2 million—into a restaurant. They can't easily walk away. They can't switch brands. They're locked into McDonald's system, dependent on its supply chain, bound by its operational standards. And if they fail to maintain those standards? If franchisees ignored McDonald's guidance, they were breaking the lease and could be evicted. As Sonneborn explained to Wall Street investors: "We are not…in the food business. We are in the real estate business. The only reason we sell $0.15 burgers is because they are the greatest producer of revenue from which our tenants can pay us rent"

The digital transformation represents McDonald's most significant strategic pivot since Sonneborn's real estate revolution. With 150 million 90-day active users and over $20 billion in Systemwide sales to loyalty members, McDonald's loyalty program is one of the largest in the world. Still, the Company plans to increase its active loyalty user base to 250 million 90-day active users and deliver $45 billion in annual Systemwide sales to loyalty members by 2027.

This isn't just about mobile apps and kiosks. Beginning in 2024, the Company will begin to deploy new, universal software that all McDonald's customer and restaurant digital platforms will run on – from the mobile app to loyalty and kiosks in store. The bespoke operating system will enable restaurants to roll out innovation even faster, with less complexity and more stability; and customers will enjoy a more familiar, consistent experience no matter where they go or how they order.

The partnership with Google Cloud announced in December 2023 signals McDonald's understanding that data is the new oil. More shared data means more opportunity to accelerate customized AI solutions. The scale of incoming information from all corners of the globe will allow McDonald's GenAI models to better understand the broadest range of patterns and nuances, resulting in more informed tests and automated solutions to enhance restaurant operations.

IX. Playbook: The McDonald's Business Model Decoded

To understand McDonald's true power, forget everything you think you know about restaurants. This isn't a food company that owns real estate—it's a real estate company that franchises food preparation systems. The distinction matters because it explains why McDonald's can generate returns that make traditional restaurants weep with envy.

Let's break down the three engines that power this machine:

Engine 1: Restaurant Operations Company-operated restaurants are essentially R&D labs disguised as profit centers. They test new products, refine operations, and showcase best practices. But financially, they're the weakest link. After paying for food, labor, and overhead, McDonald's keeps just 16% of revenue from these locations. They exist not for profit but for control—ensuring the system maintains standards that protect the brand value.

Engine 2: Franchise Fees The franchise model is where leverage begins to appear. Franchisees pay a 5% royalty on gross sales plus contribute to national advertising funds. This is pure margin for McDonald's—no food costs, no labor headaches, just a percentage off the top. But even this pales compared to the real money maker.

Engine 3: Real Estate Income Here's where Sonneborn's genius reveals itself. McDonald's charges rent based on the greater of a base amount or a percentage of sales—typically 8-15% in the U.S. This isn't just collecting rent; it's participating in the upside of every Big Mac sold while being protected on the downside by minimum payments. The company uses long-term fixed-rate debt to buy properties but charges variable rent tied to sales. As inflation drives up menu prices, McDonald's rent income grows while its mortgage payments stay flat.

The math is staggering. Of the approximately $9.2 billion in revenue from franchised restaurants, McDonald's keeps about $7.6 billion—an 82% margin. Compare that to the $2.9 billion kept from $18.2 billion in company-operated revenue—just 16%. The franchised restaurants, where McDonald's is the landlord, generate nearly three times the profit on half the revenue.

But the real brilliance lies in how these engines reinforce each other. The real estate control ensures franchise compliance. Franchise fees fund marketing that drives traffic. Increased traffic raises property values. Higher property values support more borrowing for expansion. It's a perpetual motion machine of capital generation.

The franchise selection process itself is a masterclass in risk mitigation. McDonald's doesn't want passive investors; it wants owner-operators who will live and breathe the business. Franchisees must have $500,000 in non-borrowed personal resources. They go through months of training. They can't own other businesses that would distract them. They're not buying a franchise—they're joining a system.

The 20-year franchise agreements lock in this relationship. A franchisee invests $1-2 million, their life savings typically, into a restaurant they don't own on land they don't control. They can't easily pivot to another brand. They can't modify the menu without permission. They're essentially high-stakes employees with skin in the game. And if they fail to maintain standards? McDonald's can terminate the franchise and find another operator for that valuable real estate.

This model creates what Warren Buffett would call a "moat"—a sustainable competitive advantage. Competitors can copy the menu, but they can't replicate 40,000 pieces of strategically located real estate. They can't recreate decades of brand equity. They can't suddenly generate the cash flow to self-finance expansion.

The power of this model shows in downturns. During the 2008 financial crisis, while other restaurants closed, McDonald's same-store sales actually grew. Franchisees, with their life savings at stake, found ways to survive. McDonald's, as landlord, kept collecting rent. The real estate appreciated even as the economy contracted. It's a model built not for good times but for all times.

Today's digital initiatives only strengthen this playbook. Mobile ordering drives frequency. Loyalty programs provide data. Delivery expands the trade area for each restaurant. But none of these would matter without the underlying real estate control that ensures McDonald's captures the value created. Every technological innovation, every menu improvement, every operational efficiency ultimately flows through to higher sales, which means higher rent, which means higher returns on those strategic corners McDonald's has been accumulating for seven decades.

X. Bear Case vs. Bull Case

Bear Case: The Headwinds Gathering Force

The threats facing McDonald's aren't hypothetical—they're already manifesting in the numbers. It's the first time companywide same-store sales have fallen since the fourth quarter of 2020. In the U.S., McDonald's same-store sales decreased 0.7% for the quarter. This isn't just a blip; it's a warning sign that the model that worked for 70 years may be facing structural challenges.

The health consciousness shift isn't a fad—it's a generational change. Millennials and Gen Z consumers increasingly view fast food as a compromise, not a choice. They'll eat McDonald's when convenient, but they're not building the habitual daily patterns that drove previous generations. The average American now eats fast food 159 times per year, down from 180 times a decade ago. When your business model depends on frequency, that trend is existential.

Labor costs are exploding. California's $20 minimum wage for fast-food workers is likely just the beginning. Automation promises relief, but it requires massive capital investment and risks alienating both workers and customers. The social contract that allowed McDonald's to be America's first job for millions of teenagers is fraying.

Market saturation in developed countries means growth must come from emerging markets, but these markets present their own challenges. Lower purchasing power means lower average tickets. Different food cultures resist standardization. Local competitors understand the market better. And geopolitical risks—from the Russia-Ukraine conflict to Middle East tensions—can wipe out years of investment overnight.

The delivery app revolution that initially boosted sales now threatens McDonald's control. Why does McDonald's need prime real estate if customers order through DoorDash? These platforms are inserting themselves between McDonald's and its customers, capturing data, controlling the experience, and taking 15-30% commissions that destroy already thin margins.

Environmental and social governance (ESG) pressures are intensifying. Investors increasingly question the sustainability of a business model built on beef production, single-use packaging, and automobile dependence. The carbon footprint of a Big Mac—from cow to customer—is becoming harder to ignore. Young consumers and employees increasingly want to work for and buy from companies aligned with their values.

Bull Case: The Enduring Strengths

Yet for all these challenges, McDonald's possesses advantages that seem almost insurmountable. The real estate portfolio alone—$40+ billion in strategic locations—would take competitors decades and hundreds of billions to replicate. These aren't just properties; they're forty thousand daily advertisements, physical manifestations of brand presence that no amount of digital marketing can match.

The emerging market opportunity remains massive. While U.S. sales stagnate, markets like China and India are just beginning their fast-food adoption curve. With 150 million 90-day active users and over $20 billion in Systemwide sales to loyalty members, McDonald's loyalty program is one of the largest in the world. As these markets develop, McDonald's established presence and operational expertise provide first-mover advantages that are difficult to overcome.

Digital transformation is still in early innings. To ensure McDonald's restaurant teams are able to deliver the speed, convenience and freshness customers expect when they place a mobile order, the Company will expand its U.S. pilot of Ready On Arrival across its top six markets by 2025. This initiative enables crew members to begin assembling a customer's mobile order prior to their arrival at the restaurant to expedite service and elevate customer satisfaction. The data from digital orders enables personalization and efficiency improvements that weren't possible in the analog era.

The real estate model provides an inflation hedge that's particularly valuable in today's environment. As inflation drives up food costs and menu prices, McDonald's rent income grows proportionally. But their fixed-rate mortgages remain constant. They're essentially shorting the dollar while being long on American consumption—a beautiful hedge in inflationary times.

Brand power remains extraordinary. In a world of infinite choices, the cognitive load of decision-making is exhausting. McDonald's represents certainty—you know exactly what a Big Mac tastes like whether you're in Tokyo, São Paulo, or Cincinnati. That predictability has value that only grows as the world becomes more complex.

The franchise model's resilience has been proven through multiple crises. Franchisees, with their personal wealth at stake, find ways to adapt and survive that corporate management might miss. They're 40,000 entrepreneurs all working to solve the same problems, creating a massive parallel processing system for innovation.

The balance sheet strength gives McDonald's options competitors lack. They can invest in automation, acquire technology companies, or simply wait out weaker competitors. With consistent cash generation from rent and royalties, they have the patience to execute long-term strategies while others scramble for quarterly results.

The Verdict

The bear case is real and pressing. But the bull case rests on structural advantages that seem nearly impossible to replicate. The question isn't whether McDonald's faces challenges—it does. The question is whether any competitor can assemble the combination of real estate, brand power, operational excellence, and financial strength to truly threaten McDonald's dominance. History suggests that betting against McDonald's is like betting against American capitalism itself—possible, but probably not wise.

XI. Reflections & Lessons for Founders

Ray Kroc was 52 when he first saw the McDonald brothers' operation. Harry Sonneborn was already a seasoned executive when he revolutionized the business model. Fred Turner was washing dishes when he learned the lesson that would shape his career. The story of McDonald's isn't about prodigies or first-movers—it's about seeing what others miss, even in plain sight.

Lesson 1: Your Real Business Model Might Be Hidden

For seven years, Kroc thought he was in the hamburger business. He obsessed over pickle placement, fry temperature, and service times. All important, but not the real game. Sonneborn saw what Kroc couldn't: they weren't selling food, they were renting real estate. The food was just the mechanism to generate rent.

How many founders today are fighting the wrong battle? How many software companies think they're selling features when they're really selling workflow transformation? How many content creators think they're in the entertainment business when they're actually in the attention arbitrage business? The discipline to step back and ask "What business are we really in?" can transform a struggling operation into a money-printing machine.

Lesson 2: Systems Enable Scale, But Only with Quality Control

The McDonald brothers invented fast food, but they couldn't scale it. They sold franchises for $950 flat fees and hoped for the best. Kroc understood that systems without control are just suggestions. Hamburger University, with its seemingly absurd curriculum about pickle placement, was actually a brilliant quality control mechanism. Every operator went through the same training, absorbed the same culture, learned the same standards.

Modern founders often face this same tension. You want to scale, but every new employee, every new market, every new product risks diluting what made you special. McDonald's solution—obsessive systematization combined with cultural indoctrination—seems almost militaristic. But it worked. The lesson: scaling isn't about adding locations or features or people. It's about replicating excellence reliably.

Lesson 3: Aligned Incentives Beat Contractual Obligations

McDonald's could have been just another franchisor, collecting fees and fighting with operators about standards. Instead, by becoming the landlord, they created perfect alignment. McDonald's only succeeds if franchisees succeed. Franchisees only succeed if they maintain standards. Everyone rows in the same direction because everyone's economic interests point the same way.

Too many modern businesses create adversarial relationships with their partners. Platforms squeeze suppliers. Employers minimize wages. Customers are seen as extraction opportunities. McDonald's proves that when you align incentives properly, you don't need to manage through conflict—you manage through mutual success.

Lesson 4: Capital Structure Is Strategy

Sonneborn's insight about using fixed-rate debt to buy appreciating assets while collecting variable rent wasn't just financial engineering—it was strategic genius. The capital structure became a competitive advantage. While competitors struggled with working capital, McDonald's was building equity with every burger sold.

Today's founders often treat capital structure as an afterthought, something for the CFO to handle. But how you finance your business determines what strategies you can pursue. McDonald's could afford to be patient because their capital structure provided stability. They could invest in long-term brand building because short-term cash flows were secured by real estate. The lesson: your capital structure should reinforce your strategy, not constrain it.

Lesson 5: The Power of Patient Capital

McDonald's didn't generate meaningful profits for years. The real estate investments took decades to fully mature. If Kroc had been subject to today's quarterly earnings pressures, McDonald's would never have evolved beyond a regional chain. The company's structure—with real estate providing steady cash flows—allowed them to invest in innovations that took years to pay off.

Modern founders, especially in venture-backed companies, rarely have this luxury. But McDonald's history suggests that the biggest opportunities require the longest time horizons. Building real competitive advantages—brand power, network effects, switching costs—takes years or decades, not quarters. The businesses that find ways to access patient capital, whether through structure or strategy, can pursue opportunities others can't afford to wait for.

Lesson 6: Operational Excellence Is a Competitive Advantage

In an era obsessed with disruption and innovation, McDonald's reminds us that operational excellence can be revolutionary. They didn't invent the hamburger. They didn't pioneer restaurants. They just figured out how to make food faster, more consistently, and cheaper than anyone else. Then they did it 40,000 times.

The lesson for founders: you don't always need to invent something new. Sometimes the biggest opportunity is taking something that exists and executing it better than anyone thought possible. Operational excellence compounds. Small improvements, multiplied across thousands of locations and millions of transactions, create insurmountable advantages.

XII. Recent News

The second quarter of 2024 marked an inflection point for McDonald's, revealing both vulnerabilities and resilience in the modern quick-service landscape. The fast-food giant reported second-quarter net income of $2.02 billion, or $2.80 per share, down from $2.31 billion, or $3.15 per share, a year earlier. Its quarterly revenue of $6.49 billion was about flat compared with the year-ago period. McDonald's same-store sales shrank 1%, missing StreetAccount estimates for growth of 0.4%.

These numbers tell a story of transition. The post-pandemic boom has ended. Consumers, squeezed by inflation, are pushing back on fast-food prices that no longer seem "fast" or "cheap." Executives previously warned that the competition for customers had become more fierce as the consumer environment weakened. McDonald's is leaning into discounts to bring back diners. The chain launched a $5 meal deal in late June, five days before the end of the quarter. A week ago, the company told its U.S. system that it plans to extend the value meal past the planned four-week runtime and said that it's bringing back customers.

The technology transformation continues to accelerate, with McDonald's doubling down on its digital future. Mobile ordering is a popular and growing choice for customers, with hundreds of millions of mobile orders recorded during the third quarter of 2023. The partnership with Google Cloud, announced in December 2023, represents more than just a technology upgrade—it's a fundamental reimagining of how McDonald's operates at scale.

Menu innovation remains critical. Core menu items – like the Big Mac, Quarter Pounder, Chicken McNuggets and World-Famous Fries – are truly the core of this business, representing about 65% of Systemwide sales and driving profitable growth. Seventeen classic McDonald's menu items are billion-dollar brands in their own right, beloved by customers around the world.

International performance shows diverging trends. In the U.S., comparable sales results were driven by negative comparable guest counts, partly offset by average check growth due to strategic menu price increases. International Operated Markets segment performance was impacted by negative comparable sales across a number of markets, driven by France. International Developmental Licensed Markets: The continued impact of the war in the Middle East and negative comparable sales in China more than offset growth in other regions.

The labor environment continues to evolve. Automation initiatives are accelerating, with AI-powered drive-through systems being tested in multiple markets. Self-service kiosks are now standard in many locations. But McDonald's is careful to frame these as enhancing rather than replacing human workers, aware of the social and political sensitivities around automation.

Looking ahead, McDonald's has set ambitious targets. The company aims to reach 50,000 restaurants by 2027, representing the fastest growth period in its history. The Company plans to increase its active loyalty user base to 250 million 90-day active users and deliver $45 billion in annual Systemwide sales to loyalty members by 2027. These aren't just growth metrics—they're a bet that the McDonald's model, refined and digitized, still has room to run.

XIII. Links & References

Essential Reading: - "Grinding It Out" by Ray Kroc - The founder's autobiography, equal parts inspiration and score-settling - "McDonald's: Behind The Arches" by John Love - The definitive corporate history - "The Founder" (2016) - Hollywood's take on the Kroc story, surprisingly accurate on business details

Academic & Business Analysis: - Harvard Business School Case: "McDonald's Corporation" (multiple versions from 1980-2020) - Stanford GSB Case: "McDonald's Real Estate Strategy" - Wharton: "The McDonald's Model: How Real Estate Became Fast Food's Secret Sauce"

Financial Resources: - McDonald's Investor Relations (corporate.mcdonalds.com/investors) - SEC EDGAR Database - All 10-K and 10-Q filings - Annual Franchise Disclosure Documents (FDD) - Historical stock performance via Yahoo Finance/Bloomberg

Industry Analysis: - QSR Magazine - Quick service restaurant industry coverage - Nation's Restaurant News - Breaking news and analysis - Technomic - Restaurant industry research and data - IBISWorld - Fast Food Restaurants Industry Report

Real Estate & REIT Comparisons: - National Association of Real Estate Investment Trusts (NAREIT) - Green Street Advisors - Commercial real estate research - CoStar Group - Commercial real estate data

Technology & Innovation: - McDonald's Technology Blog (medium.com/@mcdonaldstechblog) - Restaurant Technology News - Digital transformation case studies from Accenture and Google Cloud

Historical Archives: - McDonald's Corporate Archives (by appointment only) - Ray Kroc Museum at the original Des Plaines location - Newspaper archives: Chicago Tribune, Wall Street Journal, New York Times

Competitor Analysis: - Yum! Brands (KFC, Taco Bell, Pizza Hut) investor materials - Restaurant Brands International (Burger King, Tim Hortons, Popeyes) - Chipotle Mexican Grill - The "anti-McDonald's" model - Starbucks - Parallel real estate strategy in coffee

Conclusion: The Empire's Future

Standing in that San Bernardino parking lot in 1954, Ray Kroc saw the future of American dining. But even his expansive vision couldn't have imagined what McDonald's would become: a real estate empire worth more than Boeing, a technology company processing billions of transactions, a cultural force that defines childhood memories from São Paulo to Seoul.

The genius of McDonald's wasn't in inventing fast food—the McDonald brothers did that. It wasn't even in franchising—plenty of chains had tried that model. The genius was in discovering, almost by accident, that the real business wasn't burgers but the land beneath them. That insight, courtesy of Harry Sonneborn, transformed a struggling restaurant company into one of the most successful business models ever created.

Today, as McDonald's faces new challenges—from health consciousness to digital disruption—the fundamental strength of that model endures. Competitors can copy menus, replicate operations, even poach employees. But they can't recreate 70 years of real estate acquisition, brand building, and system refinement. They can't suddenly own 40,000 strategic corners in prime locations worldwide.

The bear case against McDonald's is real. Changing consumer preferences, labor pressures, and market saturation pose genuine threats. But betting against McDonald's is betting against much more than a restaurant chain. It's betting against American consumption patterns, global urbanization, and the basic human desire for convenient, predictable, affordable food.

More fundamentally, it's betting against a business model that has proven remarkably adaptable. From drive-ins to drive-throughs, from suburbs to cities, from America to the world, from physical to digital—McDonald's has continuously evolved while maintaining its core identity. The golden arches that Ray Kroc franchised, that Harry Sonneborn monetized, that Fred Turner systematized, remain one of the most recognized symbols on Earth.

The next chapter of McDonald's will be written in code as much as in real estate deeds. Artificial intelligence will optimize operations. Digital platforms will personalize experiences. Automation will reshape labor models. But underneath all this technological transformation, the fundamental model endures: control the real estate, maintain the standards, align the incentives, and collect the rent.

For investors, McDonald's represents something increasingly rare: a business with both defensive characteristics (the real estate portfolio, the brand moat) and offensive potential (digital transformation, emerging market growth). It's a 19th-century business model—landlord and tenant—perfected for the 20th century and now being reimagined for the 21st.

For entrepreneurs, McDonald's offers timeless lessons. Your biggest innovation might not be in your product but in your business model. Systems and culture can be more powerful than technology. Aligned incentives beat adversarial relationships. Patient capital enables strategies that impatient capital can't pursue. And sometimes, the most profound insights come not from Silicon Valley whiz kids but from middle-aged salesmen who see opportunity where others see only hamburgers.

The empire that began with 15-cent hamburgers now generates over $20 billion in annual revenue, operates in 100+ countries, and serves 70 million customers daily. It has survived recessions, wars, pandemics, and countless predictions of its demise. The golden arches have outlasted the Soviet Union, dozens of competitors, and several generations of management.

As we look to the future, one thing seems certain: somewhere in the world, at this very moment, a franchisee is unlocking their restaurant before dawn, firing up the grills, and preparing to serve the first customer of the day. They're not thinking about real estate strategies or digital transformation. They're thinking about executing the system, maintaining standards, serving customers. And with every burger sold, every rent payment made, every royalty collected, the empire grows stronger.

That's the ultimate lesson of McDonald's: empires aren't built on grand strategies alone. They're built on millions of small transactions, perfectly executed, repeated endlessly. They're built on the understanding that sometimes the most powerful business model isn't the most innovative—it's the one that aligns everyone's interests toward a common goal. And sometimes, just sometimes, the secret to building a global empire is as simple as realizing you're not in the business you thought you were in.

The golden arches will continue to evolve. But the foundation Sonneborn laid—real estate as the true business, franchisees as aligned partners, systems as competitive advantage—remains as solid as the land McDonald's stands on. In a world of disruption and change, that permanence itself might be McDonald's greatest asset. After all, empires rise and fall, but land endures. And McDonald's, at its core, is in the land business. The hamburgers, as Sonneborn understood, are just the excuse to collect rent.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube