Kellanova: The Global Snacking Powerhouse Story

I. Introduction & Episode Roadmap

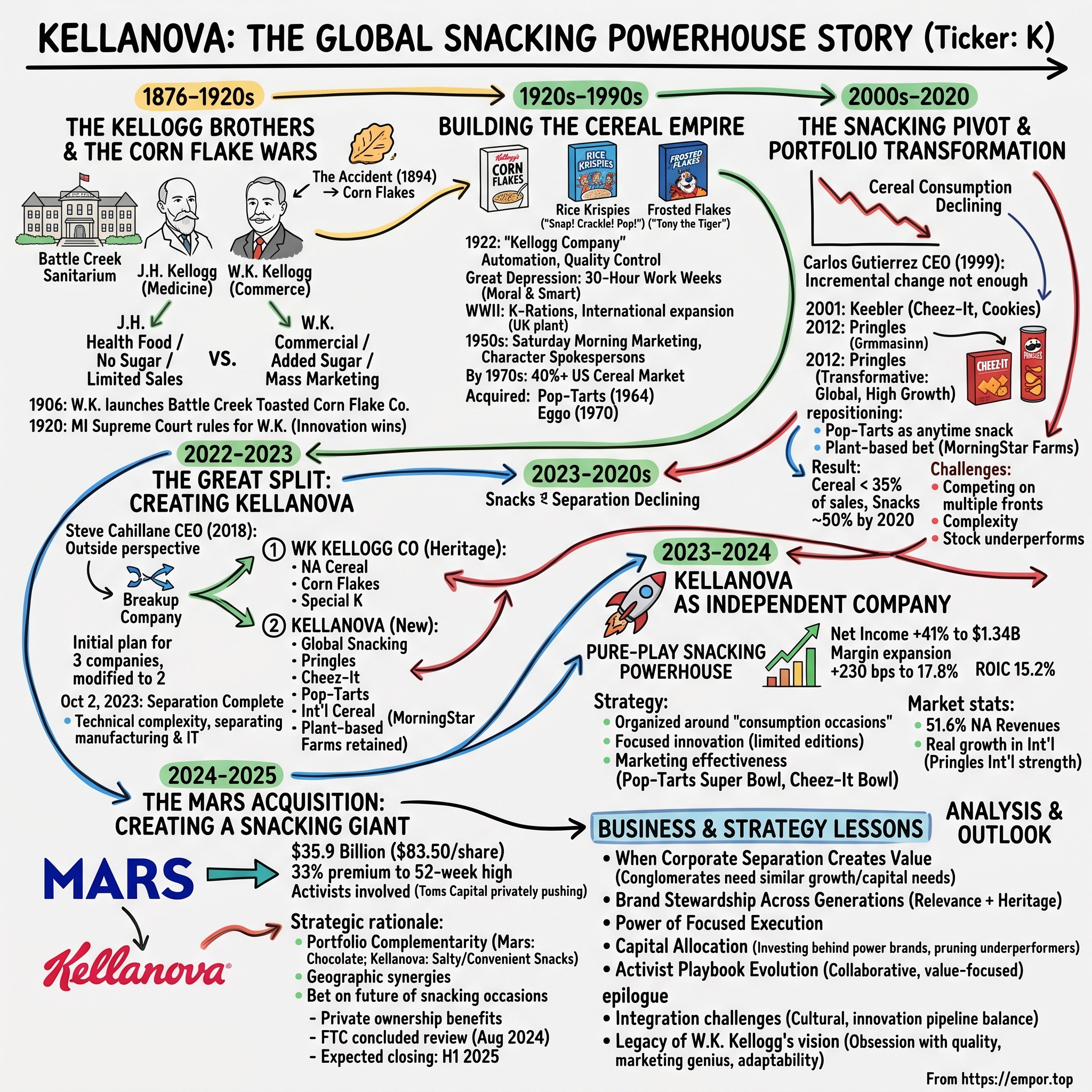

Picture this: August 14, 2024, 6:30 AM Eastern. The wire services light up with news that would reshape the global snacking landscape—Mars, the secretive candy giant behind M&M's and Snickers, announces it will acquire Kellanova for $35.9 billion, or $83.50 per share. The price represents a 33% premium to the previous day's close. Wall Street analysts scramble to update their models. Food industry executives reach for their phones. And somewhere in Battle Creek, Michigan—the city that built America's breakfast—the ghosts of the Kellogg brothers witness the final chapter of their 118-year legacy.

But here's what makes this story remarkable: Kellanova wasn't even two years old when Mars came calling. It was born from one of the most audacious corporate splits in consumer goods history, a surgical separation that transformed a struggling cereal conglomerate into a focused snacking powerhouse generating $13.5 billion in annual revenue. The company that Mars pursued wasn't the Kellogg's your grandparents knew—it was something entirely new, yet built on foundations dating back to 1906.

The fundamental question we're exploring today cuts to the heart of modern corporate strategy: How did a company founded on corn flakes and health food zealotry evolve into a global snacking empire spanning Pringles, Cheez-It, and Pop-Tarts? And why did this transformation require literally splitting the company in half?

This is a story of family feuds that shaped an industry, of portfolio transformations that defied conventional wisdom, and of a management team that bet everything on a simple insight: the future of food isn't about three square meals—it's about snacking all day long. We'll trace the journey from the Battle Creek Sanitarium's experimental kitchen to Mars's boardroom, examining how religious fervor gave way to marketing genius, how breakfast dominance evolved into snacking supremacy, and how a 117-year-old company reinvented itself for the next century.

The themes we'll explore resonate far beyond food: the tension between mission and profit, the challenge of managing complexity at global scale, the art of knowing when to split rather than fix, and the ultimate test of any consumer business—staying relevant across generations while your customers' habits fundamentally change.

II. The Kellogg Brothers & The Corn Flake Wars (1876–1920s)

The story begins not in a boardroom or factory, but in a sanitarium kitchen in Battle Creek, Michigan, where religious conviction and medical experimentation would accidentally create an industry worth hundreds of billions today.

In 1876, a 24-year-old physician named John Harvey Kellogg became medical superintendent of the Western Health Reform Institute, soon renamed the Battle Creek Sanitarium. John Harvey wasn't just any doctor—he was a Seventh-day Adventist zealot who believed that diet could cure not just physical ailments but moral ones too. His sanitarium became a mecca for America's elite seeking treatment through what he called "biologic living": vegetarianism, exercise, frequent enemas, and complete abstinence from alcohol, tobacco, and what he considered the great evil—masturbation.

Into this peculiar world came William Keith Kellogg in 1880, not as a patient but as his older brother's bookkeeper and general assistant. Where John Harvey was bombastic and evangelical, Will Keith (as he preferred to be called) was quiet, methodical, and harbored deep resentments. For 25 years, he toiled in his brother's shadow, managing the sanitarium's books, handling correspondence, and even giving John Harvey his daily shaves—all while earning a fraction of what his talents deserved.

The accident that would spawn an empire occurred in 1894. The brothers were experimenting with wheat dough, trying to create a digestible bread substitute for sanitarium patients. They left some cooked wheat sitting out overnight, and when they returned, the wheat had gone stale. Rather than throw it away—Will Keith was nothing if not frugal—they ran it through rollers. Instead of sheets, they got flakes. Toasted, these wheat flakes proved surprisingly palatable. By 1895, they'd replicated the process with corn, creating what would become the foundation of a global industry.

But here's where the story turns from invention to conflict. John Harvey saw these flakes as medicine, part of his holy mission to reform American eating habits. Will Keith saw dollar signs and an escape from his brother's shadow. John Harvey allowed patients to mail-order the cereals through the Sanitas Food Company, but refused to add sugar or actively market them—that would compromise their healthful purity. Will Keith watched in frustration as dozens of imitators, including a former patient named C.W. Post, launched competing products with aggressive marketing and added sweeteners, building fortunes on the Kelloggs' invention.

The breaking point came in 1906. Will Keith, now 46 years old, had spent his entire adult life in servitude to his brother's vision. With backing from a St. Louis insurance executive, he launched the Battle Creek Toasted Corn Flake Company on February 19, 1906, directly competing with his brother's Sanitas operation. His first innovation? Adding sugar to the flakes, making them actually taste good. His second? Marketing genius that would define consumer goods for the next century.

Will Keith understood something his brother never did: selling food wasn't about nutrition or moral improvement—it was about desire, convenience, and emotional connection. He gave away free samples by the trainload. He placed ads in women's magazines when that was considered unseemly. He created one of the first signature logos—his own signature—which still appears on Kellogg's products today. Most brilliantly, he printed "Beware of imitations. None genuine without this signature" on every box, turning his brother's refusal to sign the products into a competitive advantage.

The legal battle between the brothers was vicious and public. John Harvey sued to stop Will Keith from using the Kellogg name. Will Keith countersued. The case dragged through Michigan courts for years, with each brother presenting evidence of betrayal and bad faith. John Harvey testified that his brother had stolen his recipes and violated sacred trust. Will Keith argued that he had developed the commercial corn flake formula independently and had every right to his own family name.

The Michigan Supreme Court's 1920 ruling in Will Keith's favor wasn't just a legal victory—it was a philosophical one. The court essentially decided that commercial innovation trumped medical pioneering, that the person who brought a product to market successfully had greater claim than the inventor who kept it locked in therapeutic use. John Harvey would continue running his sanitarium until his death in 1943, increasingly bitter and irrelevant. Will Keith would build one of the great American corporations.

By 1909, just three years after founding, Will Keith's company was producing 120,000 cases of Corn Flakes daily. He pioneered concepts we take for granted today: the importance of shelf space, the power of children as marketing targets, the value of nutritional claims (even dubious ones). He created the modern breakfast itself—quick, convenient, branded. Before Kellogg's, most Americans ate leftovers or porridge for breakfast. After Kellogg's, they ate from boxes decorated with cartoon characters.

The deeper irony of the Kellogg story is that both brothers were right, just for different eras. John Harvey's obsession with nutrition and whole foods seems prescient today, when consumers scrutinize ingredients and sugar content. Will Keith's genius for mass production and marketing created the packaged food industry but also its eventual crisis of trust. The tension between health and commerce that split the brothers would, a century later, split their company.

III. Building the Cereal Empire (1920s–1990s)

With the legal battles settled and full control of the commercial enterprise, Will Keith Kellogg set about building something unprecedented: a food company based not on local distribution or commodity processing, but on brand power and national reach. The company officially became "Kellogg Company" in 1922, dropping the geographic identifier that limited its ambitions.

The 1920s roared for Kellogg's as they did for America. Will Keith proved to be not just a marketing genius but a pioneering industrialist. He invested heavily in automation and quality control, innovations that allowed Kellogg's to maintain consistency across millions of boxes. He built massive factories designed specifically for cereal production, with custom equipment that could toast flakes to precise specifications. By 1925, Kellogg's was spending $1 million annually on advertising—an astronomical sum that dwarfed competitors and established the template for consumer goods marketing.

Then came 1929 and the Great Depression. While other companies retrenched, Will Keith made a counterintuitive decision that would define Kellogg's culture for generations: he shifted his factories to 30-hour work weeks, not to cut costs but to employ more workers. The six-hour shifts allowed Kellogg's to hire hundreds of additional employees when jobs were desperately scarce. Will Keith believed this wasn't just moral but smart business—employed people buy cereal. The experiment continued until World War II and earned Kellogg's extraordinary loyalty in Battle Creek, where the company became synonymous with responsible capitalism.

The Depression also accelerated Kellogg's product innovation. Rice Krispies launched in 1928 with the ingenious "Snap! Crackle! Pop!" campaign—anthropomorphizing the sound of milk hitting puffed rice. The characters wouldn't appear until 1933, but the auditory branding was revolutionary. Kellogg's understood that breakfast was a multisensory experience, and they could own specific sounds, textures, and rituals.

World War II transformed Kellogg's from an American company into a global force. The company supplied K-rations to troops, introducing millions of soldiers to packaged breakfast foods. More importantly, Will Keith anticipated the post-war boom and began planning international expansion even as bombs fell on London. In 1938, Kellogg's had opened a plant in Manchester, England. Despite the war, Will Keith insisted on maintaining and even expanding UK operations, believing that American-style marketing and breakfast habits would spread globally.

He was spectacularly right. The Trafford Park facility in Manchester would become Kellogg's largest factory in the world by the 1960s, producing not just for Britain but for all of Europe. Kellogg's didn't just export American products—they adapted to local tastes while maintaining brand consistency. Corn Flakes might be sweetened differently in Japan than Germany, but Tony the Tiger looked the same everywhere.

Speaking of Tony, the 1950s brought Kellogg's greatest marketing innovation: the character spokesperson. Tony the Tiger debuted in 1952 for Frosted Flakes (originally called Sugar Frosted Flakes, before sugar became a dirty word). His "They're Gr-r-reat!" became one of advertising's most enduring taglines. Toucan Sam followed in 1963 for Froot Loops, Dig 'Em Frog for Sugar Smacks, and dozens of others. These weren't just mascots—they were Saturday morning companions for millions of children, building emotional connections that lasted lifetimes.

The economics of the cereal business in its golden age were extraordinary. The basic ingredients—corn, wheat, rice, sugar—cost pennies. The manufacturing process, once scaled, was highly automated. The real value was in the brand, the shelf space, and the marketing muscle to defend both. Gross margins could exceed 60%. Return on invested capital routinely topped 20%. It was one of the best businesses in the world.

By the 1970s, Kellogg's commanded over 40% of the U.S. ready-to-eat cereal market. The company had expanded beyond breakfast into adjacent categories through acquisition and development. Pop-Tarts launched in 1964, creating the toaster pastry category. Eggo waffles were acquired in 1970, extending Kellogg's breakfast dominance into the freezer aisle. The company seemed unstoppable.

But success bred complacency. Through the 1980s, Kellogg's focused on defending its cereal fortress rather than anticipating how American eating habits were changing. The company's R&D focused on line extensions—new flavors of existing brands—rather than breakthrough innovation. Marketing spend remained enormous but increasingly ineffective as media fragmented and Saturday morning cartoons lost their cultural centrality.

The first warning signs appeared in the late 1980s. Private label cereals, once dismissed as inferior knockoffs, began taking share by offering similar quality at half the price. Health-conscious consumers started questioning the sugar content in children's cereals. Most ominously, breakfast itself began declining as a meal occasion. Americans increasingly skipped breakfast or grabbed something portable. The bowl-and-spoon ritual that Kellogg's had spent 80 years perfecting was becoming obsolete.

By 1999, when Carlos Gutierrez became CEO, Kellogg's faced an existential crisis. Market share had dropped below 32%. Sales growth had stagnated. The stock price languished. The company that Will Keith built on innovation and marketing genius had become a bloated, slow-moving giant dependent on a declining category. Gutierrez, a Cuban immigrant who had started as a Kellogg's sales representative in Mexico City, understood that incremental change wouldn't suffice. Kellogg's needed transformation.

IV. The Snacking Pivot & Portfolio Transformation (2000s–2020)

The millennium opened with Kellogg's facing a stark reality: Americans were falling out of love with cereal. Not gradually, but dramatically. Per capita cereal consumption, which had grown steadily since Will Keith's day, began declining in the late 1990s and accelerated through the 2000s. Younger consumers saw cereal as processed, sugary, and inconvenient compared to grab-and-go options. The got-milk campaigns and prize-inside promotions felt increasingly desperate.

Carlos Gutierrez didn't try to reverse these trends—he accepted them and began positioning Kellogg's for a different future. His insight was simple but profound: Kellogg's wasn't really in the cereal business; it was in the business of convenient, branded food moments. If those moments were shifting from the breakfast table to the car, office, and couch, Kellogg's needed to follow.

The transformation began with a series of acquisitions that puzzled Wall Street but would prove prescient. In 2001, Kellogg's bought Keebler for $3.9 billion, adding cookies, crackers, and most importantly, Cheez-It to the portfolio. Critics called it expensive and distracting. Gutierrez saw it as essential portfolio evolution—these were products people ate all day long, with higher growth rates and better margins than cereal.

The real masterstroke came in 2012 under CEO John Bryant, when Kellogg's acquired Pringles from Procter & Gamble for $2.7 billion. P&G was exiting food to focus on household and personal care, viewing Pringles as a distraction despite its $1.5 billion in annual sales. For Kellogg's, Pringles represented everything the company needed: a global brand growing at 6% annually, consumed primarily as a snack rather than meal accompaniment, and with expansion potential in emerging markets where cereal faced cultural barriers.

The Pringles deal was transformative beyond its financials. It gave Kellogg's instant credibility in snacking and critical mass in international markets. Pringles was already sold in over 140 countries, with particular strength in Asia and Latin America where Kellogg's cereal business struggled. The brand's unique packaging—the iconic tube—provided a competitive moat that bags couldn't match. And unlike cereal, which required educating consumers about an entirely new meal occasion, potato crisps were universally understood.

But Kellogg's didn't just buy its way into snacking—it innovated within its existing portfolio. Pop-Tarts, long viewed as a breakfast item, was repositioned as an anytime snack. New flavors targeted adult tastes. Packaging shifted from family-size boxes to portable pouches. Marketing moved from morning TV to social media, where Pop-Tarts developed a cult following through irreverent Twitter content that would have horrified Will Keith but delighted millennials.

The company also made a bold bet on plant-based foods, acquiring Worthington Foods and its MorningStar Farms brand in 1999. This seemed bizarre at the time—what did veggie burgers have to do with corn flakes? But Kellogg's management saw the trend toward flexitarian eating before it had a name. By 2019, MorningStar Farms had grown to nearly $400 million in annual sales, commanding 27% of the U.S. meat alternatives market.

The portfolio transformation was remarkable in its scope. In 2000, roughly 70% of Kellogg's revenues came from cereal. By 2020, cereal represented less than 35% of sales, with snacks accounting for nearly half. The company had successfully diversified away from its declining core business while maintaining overall growth—a feat few century-old companies achieve.

Yet this transformation created its own challenges. Kellogg's was now competing on multiple fronts against different competitors with different capabilities. In cereal, it battled General Mills and Post. In cookies and crackers, it faced Mondelēz and Campbell's. In snacks, it competed with PepsiCo's Frito-Lay juggernaut. In frozen foods, it challenged Nestlé and Conagra. The complexity was overwhelming.

International expansion added another layer of difficulty. While Pringles and snacks traveled well across borders, cereal remained stubbornly cultural. In Asia, where rice porridge and savory breakfasts dominated, Kellogg's struggled to gain traction despite decades of effort. In Latin America, economic volatility whipsawed results. Europe delivered steady but slow growth. The company was trying to be everything to everyone everywhere—a recipe for mediocrity.

By 2018, when Steve Cahillane took over as CEO, Kellogg's faced a new crisis. Despite the successful pivot to snacking, the company's stock had underperformed peers for five straight years. Activist investors circled, demanding either dramatic cost cuts or a breakup. The consensus view was that Kellogg's conglomerate structure destroyed value—high-growth snacks subsidized declining cereal, international markets diluted North American returns, and management couldn't optimize such a diverse portfolio.

Cahillane, who had previously run Nature's Bounty and worked at Coca-Cola, brought an outsider's perspective. He saw what insiders couldn't: Kellogg's wasn't one company awkwardly stitched together—it was three distinct businesses trapped in a single corporate structure. The solution wasn't to optimize the portfolio but to liberate it.

V. The Great Split: Creating Kellanova (2022–2023)

June 21, 2022, marked a watershed moment in Kellogg's history. At 6:45 AM, before markets opened, CEO Steve Cahillane announced what many considered unthinkable: Kellogg Company would split into three independent, publicly traded companies. The cereal business would return to its roots as a focused North American operator. The plant-based division would pursue its own growth trajectory. And the global snacking business—representing nearly 80% of revenues—would emerge as a pure-play snacking powerhouse.

The announcement shocked even seasoned industry observers. Food companies had been consolidating for decades, pursuing scale and synergies. Here was Kellogg's doing the opposite, voluntarily breaking apart a 116-year-old institution. Cahillane framed it as liberation, not destruction: "These businesses have different growth profiles, different capital needs, different competitive dynamics. Forcing them to share a single structure and strategy constrains all of them."

The initial plan was elegantly simple in concept but fiendishly complex in execution. The North American cereal business would keep the iconic Kellogg's name and Battle Creek headquarters, along with brands like Corn Flakes, Frosted Flakes, and Special K. The plant-based business, anchored by MorningStar Farms, would pursue the explosive growth in meat alternatives. The global snacking and international cereal business would take everything else—Pringles, Cheez-It, Pop-Tarts, Eggo, and cereal operations outside North America.

Wall Street's reaction was swift and positive. Kellogg's stock jumped 8% on the announcement, adding $2 billion in market value in a single day. Analysts who had criticized the company's muddled portfolio suddenly praised its strategic clarity. The sum of the parts, they calculated, was worth 30-40% more than the conglomerate whole.

But eight months later, in a dramatic reversal that demonstrated both strategic flexibility and the complexity of the task, Kellogg's announced it was modifying the plan. The plant-based spinoff was cancelled. Instead of three companies, there would be two. MorningStar Farms and the other meat alternative brands would remain with the global snacking business.

The reversal was embarrassing but arguably correct. The plant-based market had cooled considerably since the initial announcement. Beyond Meat's stock had collapsed 95% from its peaks. Impossible Foods was struggling to raise capital. What looked like a hypergrowth category in June 2022 appeared more like a niche segment by February 2023. A standalone plant-based company might struggle to access capital markets or achieve necessary scale.

More importantly, the reversal revealed how thoroughly Cahillane's team had stress-tested their assumptions. They modeled different scenarios, consulted with bankers and potential investors, and ultimately concluded that two strong companies were better than two strong companies and one weak one. The plant-based business would benefit from the snacking company's scale and distribution network. Shareholders would capture more value. It was a painful but correct decision. On March 15, 2023, the names were finally revealed: the global snacking business would become Kellanova, while the North American cereal company would be called WK Kellogg Co, honoring the founder. The naming choices were telling. Kellanova—a portmanteau of Kellogg and the Latin word "nova" meaning new—signaled transformation and global ambition. WK Kellogg Co represented heritage and tradition, returning to the founder's initials that hadn't been used corporately in over a century.

The technical complexity of the separation was staggering. The separation was achieved through the distribution of all of the shares of WK Kellogg Co to holders of Kellanova common stock at 12:01 a.m. EDT on October 2, 2023, with Kellanova shareowners receiving one share of WK Kellogg Co common stock for every four shares of Kellanova common stock held on the record date. This wasn't just a financial transaction—it required separating shared services, IT systems, supply chains, and thousands of employees who had worked together for decades.

Consider the operational nightmare: Kellogg's operated integrated manufacturing facilities where cereal and snacks shared equipment, warehouses, and logistics networks. Customer relationships spanned both portfolios—Walmart didn't want separate sales teams for Corn Flakes and Pringles. International operations were particularly complex, with many markets selling both cereal and snacks through unified organizations. Every contract, every system, every process had to be evaluated and potentially split.

The human dimension was equally challenging. Employees who had built careers at Kellogg's suddenly faced a choice: join the growth-oriented Kellanova or stick with the heritage WK Kellogg Co. Battle Creek, the company's spiritual home, would remain headquarters for WK Kellogg Co, while Kellanova would establish its base in Chicago, symbolically moving from small-town manufacturing heritage to global commercial hub.

It is projected to generate net sales of approximately $13.4-$13.6 billion and adjusted-basis EBITDA of approximately $2.25-$2.3 billion in 2024. The financial engineering was precise: Kellanova would carry most of the debt but also most of the growth assets. WK Kellogg Co would be nearly debt-free but face the challenge of reviving a declining category. "After more than a year of comprehensive planning and execution, we are more confident than ever that the separation will produce two stronger companies and create substantial value for shareowners," stated Steve Cahillane.

The market mechanics of the separation were carefully orchestrated to ensure orderly trading. When-issued trading began on September 27, allowing price discovery before the official split. The use of due-bills ensured that buyers in the final days before separation understood they were purchasing rights to both companies. It was a masterclass in corporate finance execution.

Today, Kellanova, formerly known as Kellogg Company, (NYSE: K), announced the completion of the previously announced separation of its North American cereal business, WK Kellogg Co, resulting in two independent, public companies, each better positioned to unlock its full standalone potential. When October 2, 2023, arrived, the transformation was complete. The 117-year-old Kellogg Company ceased to exist, replaced by two focused entities with distinct strategies, cultures, and destinies.

VI. Kellanova as Independent Company (2023–2024)

Kellanova's first earnings call as an independent company in November 2023 set the tone for its new identity. CEO Steve Cahillane opened not with nostalgia for Kellogg's heritage but with a forward-looking vision: "We are now a pure-play global snacking powerhouse, unencumbered by declining categories and free to invest aggressively behind our highest-return opportunities."

The numbers backed up the rhetoric. In its first full year as an independent entity, Kellanova delivered results that exceeded even bull-case projections. Net income surged 41% to $1.34 billion, while adjusted earnings per share hit $3.86, beating guidance by nearly 10%. But the headline numbers obscured an even more impressive operational transformation happening beneath the surface.

The portfolio that Kellanova inherited was already strong but unfocused. Pringles generated over $3 billion in annual sales across 140 countries. Cheez-It dominated the U.S. cheese cracker category with a 50% market share. Pop-Tarts owned toaster pastries with 80% share. RXBAR had emerged from nowhere to become a $300 million protein bar powerhouse. Eggo controlled 65% of frozen waffles. Each brand was a category leader, but they'd never been managed as a coherent portfolio.

Cahillane's first strategic move was to reorganize the company around consumption occasions rather than product categories. Instead of managing cookies, crackers, and chips separately, Kellanova created teams focused on "savory snacking," "sweet snacking," "convenient nutrition," and "frozen occasions." This seemingly simple reorganization had profound implications. Suddenly, Pringles and Cheez-It could coordinate promotions. Pop-Tarts and Nutri-Grain could share consumer insights. The sum became greater than its parts.

The geographic footprint told another story of untapped potential. While North America generated 51.6% of revenues, the real growth was coming from international markets. Europe contributed 19.6% of sales but was growing at 8% annually as Pringles gained distribution. Asia, Middle East, and Africa represented 18.92% of revenues with double-digit growth rates. Latin America, despite economic volatility, delivered 9.89% of sales and showed improving momentum.

Innovation, freed from the bureaucracy of the old Kellogg structure, accelerated dramatically. Pringles launched limited-edition flavors monthly, some becoming permanent additions to the lineup. Cheez-It introduced Snap'd, a thin crispy version that competed directly with premium crackers. Pop-Tarts collaborated with everything from Dunkin' Donuts to Jolly Rancher, creating buzz-worthy limited editions that drove social media engagement and trial.

But the most impressive transformation was in marketing effectiveness. Kellanova didn't just spend more—it spent smarter. The company's 2024 Super Bowl ad for Pop-Tarts, featuring a edible mascot sacrifice, generated over 4 billion media impressions for a $7 million investment. A college football partnership made Cheez-It synonymous with bowl season, culminating in the Cheez-It Citrus Bowl that turned the brand into a cultural phenomenon.

Digital engagement became a core competency. Pop-Tarts' Twitter account, with its surreal humor and willingness to engage in brand wars, accumulated 500,000 followers and routinely went viral. Pringles partnered with gaming platforms and esports tournaments, reaching younger consumers where they spent time. Even traditional TV spending was optimized through programmatic buying and advanced analytics.

Supply chain transformation, less visible but equally important, drove margin expansion. Kellanova invested $500 million in automation and efficiency improvements in its first year alone. Smart factories using AI-driven demand forecasting reduced waste by 15%. Direct-to-consumer capabilities, while still small, grew 300% as the company experimented with subscription models and personalized variety packs.

The results spoke for themselves. Operating margins expanded 230 basis points to 17.8%. Return on invested capital jumped to 15.2%. Free cash flow exceeded $1.5 billion, providing flexibility for both growth investment and shareholder returns. The stock price appreciated 28% in Kellanova's first year, dramatically outperforming both the S&P 500 and food sector peers.

Yet challenges remained. Input cost inflation, particularly in cocoa and packaging materials, pressured margins. Private label competition intensified as retailers improved their offerings. Most significantly, volume growth remained elusive—Kellanova's revenue growth came primarily from pricing and mix improvement rather than selling more units.

The company also faced criticism for its ESG initiatives, or lack thereof. While Kellanova committed to sustainable packaging and responsible sourcing, activists argued these efforts were insufficient given the environmental impact of snack food production. Labor relations were strained after a 2023 strike at several facilities. And nutritional concerns about ultra-processed foods gained mainstream attention, potentially threatening long-term demand.

But as 2024 progressed, Kellanova's strategic position strengthened. Q2 results showed accelerating organic growth. International expansion exceeded targets. New product success rates improved to industry-leading levels. The company that had been freed from the declining cereal business was proving that focus and execution could drive exceptional value creation.

Then came the call that would change everything.

VII. The Mars Acquisition: Creating a Snacking Giant (2024–2025)

The news broke at dawn on August 14, 2024: Mars, Incorporated, a family-owned, global leader in pet care, snacking and food, and Kellanova have entered into a definitive agreement under which Mars has agreed to acquire Kellanova for $83.50 per share in cash, for a total consideration of $35.9 billion, including assumed net leverage. The transaction price represented a premium of approximately 44% to Kellanova's unaffected 30-trading day volume weighted average price and a premium of approximately 33% to Kellanova's unaffected 52-week high as of August 2, 2024.

The premium was eye-popping, even in an era of inflated M&A valuations. Mars was paying 16.4 times Kellanova's last twelve months adjusted EBITDA—a multiple typically reserved for high-growth tech companies, not mature food businesses. The financial press immediately questioned whether Mars had overpaid. Kellanova's stock jumped 8% to near the offer price, suggesting the market expected the deal to close without competing bids. Behind the scenes, a crucial catalyst had been at work. The acquisition comes after months of engagement with Toms Capital Investment Management, an activist fund run by Benjamin Pass which had amassed a sizeable stake in Kellanova. Toms Capital had been privately pushing Cahillane and Kellanova management to pursue strategic and organizational changes. The activist investor, which had taken an undisclosed "significant" stake in Kellanova in May 2024, had been quietly building pressure for strategic alternatives.

Toms Capital wasn't a typical activist making public demands and proxy threats. Benjamin Pass preferred to work behind the scenes, as he had done previously at Colgate-Palmolive in collaboration with Dan Loeb's Third Point. His message to Kellanova's board was simple: the company was undervalued, the snacking portfolio was world-class, and strategic buyers would pay a significant premium for these assets. Either management needed to accelerate value creation or explore a sale.

The timing was perfect for Mars. The privately held candy giant, with over $50 billion in annual revenue, had been searching for a transformative acquisition to achieve its stated goal of doubling its snacking business to $36 billion within a decade. Under CEO Poul Weihrauch, Mars had pursued a dual strategy of small bolt-on acquisitions like Kind bars and Kevin's Natural Foods while hunting for a mega-deal that could reshape its portfolio overnight.

"We buy businesses to grow businesses, and we look to grow for generations," Mars CEO Poul Weihrauch said on CNBC's "Money Movers." This wasn't corporate speak—it was Mars's DNA. As a private company controlled by the Mars family, they could think in decades rather than quarters. They'd held Wrigley for 16 years since acquiring it for $23 billion. They'd owned Uncle Ben's rice for over 40 years. When Mars bought something, they rarely sold.

The strategic logic was compelling. Mars dominated confectionery but had limited presence in salty snacks, the fastest-growing segment of the snacking market. Kellanova brought immediate scale in precisely the categories Mars lacked. Pringles would complement Mars's sweet snacks. Cheez-It would provide entry into the massive cheese snack category. Pop-Tarts could leverage Mars's convenience store relationships. The international footprint was particularly attractive—Kellanova was strong in markets where Mars was weak and vice versa.

But the price remained contentious. At 16.4 times EBITDA, Mars was paying a premium typically reserved for high-growth technology companies or scarce pharmaceutical assets. Food company acquisitions typically traded at 10-12 times EBITDA. Even accounting for synergies, the math was challenging. Mars would need to dramatically accelerate Kellanova's growth or achieve unprecedented cost savings to justify the valuation.

The regulatory path added another layer of complexity. While The W.K. Kellogg Foundation Trust and the Gund Family have entered into agreements pursuant to which they have committed to vote shares representing 20.7% of Kellanova's common stock, as of August 9, 2024, in favor of the transaction, ensuring shareholder support, antitrust approval was far from certain. The combined entity would control significant market share in several snacking categories. Consumer advocacy groups immediately raised concerns about reduced competition and higher prices. In a special meeting on Nov. 1, more than 99.5% of the 266,772,146 shareholder votes cast gave the go-ahead to the merger agreement, demonstrating overwhelming investor support despite the premium valuation. Shareholders participating in the vote represented approximately 77.5% of Kellanova's outstanding shares of common stock, well above the threshold needed for approval. Interestingly, 58% of voting shareholders rejected the merger's proposed executive compensation package, suggesting some concern about management windfalls from the deal.

The strategic rationale Mars presented was compelling on multiple dimensions. First, portfolio complementarity: Mars dominated chocolate and candy while Kellanova ruled salty snacks and convenience foods. There was minimal overlap, reducing antitrust concerns. Second, geographic synergies: Mars's strength in Asia paired perfectly with Kellanova's Latin American presence. Third, channel diversification: Kellanova's grocery dominance complemented Mars's convenience store strength.

But perhaps most importantly, the acquisition represented a fundamental bet on the future of food consumption. Mars believed that traditional meal occasions were permanently disrupted, that snacking would continue to grow as a share of stomach, and that winning in snacks meant owning a portfolio spanning sweet, salty, healthy, and indulgent. The combined entity would have unmatched breadth, from M&M's to Pringles, from Kind bars to Pop-Tarts.

The cultural fit was equally important. Both companies shared Midwestern roots, family-influenced governance (Mars directly, Kellanova through the Kellogg Foundation's shareholding), and long-term orientation. Both had resisted the quarterly earnings treadmill that plagued public food companies. Both invested heavily in brands rather than chasing promotional volume.

The U.S. Federal Trade Commission (FTC) has concluded its antitrust review of Mars' pending acquisition of Kellanova without the imposition of any condition or requiring any remedy. The transaction has now received all but one of the 28 required regulatory clearances, with only the review by the European Commission outstanding. This regulatory momentum suggested the deal would close on schedule in the first half of 2025.

For Kellanova employees, the acquisition brought both opportunity and uncertainty. After the closing of the transaction, Battle Creek, MI, will remain a core location for the combined organization. Mars Snacking remains headquartered in Chicago. But beyond these commitments, integration plans remained vague. Would Mars maintain Kellanova's innovation centers? How would sales forces be combined? Which executives would lead the merged entity?

The financial markets rendered their verdict swiftly. Kellanova's stock traded just below the $83.50 offer price, suggesting high confidence in deal completion. Mars's bonds, when they came to market to finance the acquisition, were oversubscribed despite the massive size. Food company stocks broadly rallied on speculation about further consolidation. If Mars would pay 16 times EBITDA for Kellanova, what might Mondelēz or Nestlé command?

VIII. Playbook: Business & Strategy Lessons

The Kellanova story offers a masterclass in portfolio management, demonstrating when corporate separation creates more value than integration. The key insight: conglomerates work when businesses share similar growth rates, capital needs, and competitive dynamics. When these diverge significantly, forced cohabitation destroys value for all parties.

Consider Kellogg's predicament in 2021. The cereal business needed defensive investment to slow share losses. The snacking business needed growth investment to capture share. International markets needed patient capital to build distribution. Plant-based needed venture-style risk-taking. No single strategy could optimize all four. No management team could execute four different playbooks simultaneously. The conglomerate structure had become a straightjacket.

The lesson extends beyond food. General Electric's breakup into three companies followed similar logic. Johnson & Johnson's split of consumer from pharmaceutical recognized different risk profiles and valuations. Even tech giants like Alphabet and Meta create internal structures that allow different businesses to operate independently. The era of the omnibus conglomerate has ended; focus and fit drive value creation.

The second lesson involves the art of timing separations. Kellogg's didn't split at the first sign of trouble—they tried integration, cost-cutting, acquisitions, and restructuring first. Only when these failed to unlock value did separation become inevitable. But they also didn't wait too long. The cereal business still had value as an independent entity. The snacking portfolio was strong enough to attract premium buyers. Timing the split required balancing patience with urgency.

Brand stewardship across generations emerges as another critical theme. Kellogg's spent a century building brands like Frosted Flakes and Pop-Tarts into cultural icons. These weren't just products but shared experiences across generations. The challenge was maintaining relevance without abandoning heritage. Pop-Tarts succeeded by embracing ironic nostalgia. Pringles stayed fresh through constant flavor innovation. Cheez-It leveraged its authenticity in an era of artisanal everything.

The company's approach to brand lifecycle management was particularly instructive. Rather than abandon declining brands, Kellogg's/Kellanova found new contexts for old products. Cereal became a snack. Pop-Tarts became a social media phenomenon. Eggo transcended frozen waffles to become a cultural reference point. The lesson: great brands can transcend their original categories if managed creatively.

The power of focused execution post-spinoff cannot be overstated. Kellanova's first-year performance—41% net income growth, 230 basis points of margin expansion—wasn't due to new strategies or capabilities. It was the result of alignment, clarity, and urgency that comes from independence. Decisions that would have taken months in the conglomerate structure happened in weeks. Investments that would have been diluted across four businesses were concentrated on the highest returns.

Capital allocation in consumer goods presents unique challenges that Kellanova navigated skillfully. Unlike tech companies that can pour capital into R&D, food companies face diminishing returns on innovation spending. Unlike retailers that can expand locations, manufacturers are constrained by consumption growth. Kellanova's solution was portfolio optimization—investing behind power brands while pruning underperformers, expanding in high-growth geographies while maintaining developed market positions.

The activist investor playbook, as demonstrated by Toms Capital, shows evolution in shareholder activism. Rather than public campaigns and proxy fights, Toms worked behind the scenes to build consensus for value creation. They didn't prescribe specific strategies but pushed for strategic alternatives to be explored. This collaborative activism, focused on long-term value rather than short-term financial engineering, represents the maturation of the activist model.

Managing complexity at global scale remains one of the most underappreciated challenges in consumer goods. Kellanova operated in 180 countries, each with different regulations, consumer preferences, and competitive dynamics. They manufactured in dozens of facilities with different capabilities and costs. They sold through thousands of customers with conflicting demands. The ability to manage this complexity while maintaining efficiency and innovation is what separates great operators from mediocre ones.

The Mars acquisition illustrates the power of patient capital in driving industry consolidation. As a private company, Mars could pay prices that public companies couldn't justify to quarterly-focused shareholders. They could accept lower returns in early years knowing they'd hold the asset for decades. They could invest in integration without worrying about earnings dilution. This structural advantage of private ownership becomes more powerful as public markets become more short-term oriented.

Finally, the story demonstrates how creating value through corporate separations requires more than financial engineering. It demands operational excellence, strategic clarity, cultural transformation, and flawless execution. The companies that succeed—like Kellanova—are those that use separation as a catalyst for fundamental improvement, not just a one-time value unlock.

IX. Analysis & Investment Perspective

Kellanova's final quarters as an independent company demonstrated the power of focused execution. Kellanova delivered fourth-quarter 2024 results, wherein the top and bottom lines beat the Zacks Consensus Estimate, and earnings grew year over year. This marked another strong quarterly performance, driven by a growth-focused portfolio and effective execution across the organization. With a robust presence in emerging markets, Kellanova achieved better-than-expected sales growth despite tough industry conditions while improving profit margins at a faster pace than expected.

The numbers tell a compelling story of operational excellence. On a currency-neutral basis, adjusted earnings per share (EPS) rose 19.2% to 93 cents. The bottom line surpassed the Zacks Consensus Estimate of 82 cents. The company recorded net sales of $3,124 million, which surpassed the Zacks Consensus Estimate of $3,093 million. However, the top line fell 1.6% year over year. Organic net sales (excluding currency impacts) grew 7%, driven by improved volumes and price/mix.

What's particularly impressive is the margin expansion story. Kellanova's adjusted operating profit increased 14.4% to $448 million while rising 19.9% to $470 million on a currency-neutral basis. This wasn't just pricing power—it was the result of systematic productivity improvements, supply chain optimization, and portfolio focus. The company was extracting more profit from every dollar of sales, a key metric for consumer goods companies facing input cost pressures.

From a competitive positioning perspective, Kellanova had carved out a unique niche. Unlike Mondelēz, which competed across multiple categories with varying success, Kellanova dominated specific segments. Pringles held nearly 10% global share of potato crisps. Cheez-It owned 50% of the U.S. cheese cracker market. Pop-Tarts had 80% of toaster pastries. This concentration created defensive moats that would be difficult for competitors to breach.

The comparison with PepsiCo's Frito-Lay division is instructive. Frito-Lay generated roughly $23 billion in annual sales versus Kellanova's $13 billion, but Frito-Lay's growth had slowed to low single digits while Kellanova was delivering 7% organic growth. Frito-Lay's operating margins were superior at around 25% versus Kellanova's 17%, but the gap was closing. Most importantly, Kellanova's international exposure provided more growth runway than Frito-Lay's North America concentration.

The snacking megatrend underpinning Kellanova's strategy shows no signs of abating. Consumer eating patterns have fundamentally shifted from three structured meals to multiple snacking occasions throughout the day. This isn't just an American phenomenon—it's global, driven by urbanization, longer working hours, and changing household structures. The global snacks market is projected to grow at 5-6% annually through 2030, significantly faster than traditional food categories.

Geographic opportunities remain substantial despite Kellanova's global presence. Sales in the North America segment amounted to $1,561 million, down 1.7% year over year due to the adverse price/mix and currency headwinds, partly made up by volume growth. However, emerging markets continued to show strength, particularly in Asia and Latin America where snacking penetration remains low relative to developed markets.

Myth vs Reality: The Premium Paid by Mars

Consensus View: Mars dramatically overpaid at 16.4x EBITDA for a mature food company.

Reality: The multiple reflects several factors the market underappreciated: - Kellanova's EBITDA was temporarily depressed by separation costs and would normalize higher - The synergy potential exceeded $500 million annually within three years - Private ownership allows for investment cycles public markets wouldn't tolerate - The strategic value of achieving scale in snacking justified premium pricing

ESG considerations, while not driving the deal, added complexity. Kellanova had committed to sustainable packaging and responsible sourcing, but critics argued these efforts were insufficient. The company faced pressure on multiple fronts: environmental groups criticized single-serve packaging waste, health advocates challenged ultra-processed food promotion, and labor unions pushed for better wages and working conditions. Mars's private ownership might actually accelerate ESG investments that public markets would punish in the short term.

The investment perspective ultimately depends on time horizon and risk tolerance. For Kellanova shareholders, the Mars acquisition delivered immediate value realization at an attractive premium. The 33% premium to the 52-week high represented exceptional value capture, particularly given the uncertain macroeconomic environment. Shareholders who bought at the spinoff received nearly 50% returns in just over a year.

For Mars, the acquisition is a decade-long bet on snacking's continued growth and their ability to extract synergies from scale. If they achieve their stated goal of doubling the snacking business to $36 billion by 2034, the purchase price will look prescient. If snacking growth slows or integration proves challenging, they've overpaid for a mature business.

The broader implications for the food industry are profound. The Mars-Kellanova combination signals that scale still matters in consumer goods, despite the rise of niche brands and direct-to-consumer models. It suggests that private capital will continue to play a major role in industry consolidation. And it demonstrates that focused portfolios command premium valuations over conglomerates.

X. Epilogue & Future Outlook

As we look toward the anticipated closing in the first half of 2025, the integration challenges facing Mars and Kellanova are both mundane and monumental. The mundane involves thousands of decisions about systems, processes, and personnel. Which ERP platform will survive? How will sales territories be reorganized? Who will lead the combined snacking division? These tactical choices, while unglamorous, will determine whether the promised synergies materialize.

The monumental challenges involve cultural integration and strategic direction. Kellanova emerged from its spinoff with entrepreneurial energy and urgency. Mars operates with the patience and deliberation of multi-generational family ownership. Kellanova's employees thrived on public market pressure and quarterly earnings calls. Mars associates (never employees) work in an environment where five-year plans actually mean something. Bridging these cultures without losing what makes each special will test leadership at all levels.

After the closing of the transaction, Battle Creek, MI, will remain a core location for the combined organization. Mars Snacking remains headquartered in Chicago. But beyond these commitments, the future footprint remains uncertain. Will Mars maintain Kellanova's innovation centers? How will international operations be consolidated? These decisions will ripple through communities that have depended on these facilities for generations.

The innovation pipeline represents perhaps the greatest opportunity and challenge. Kellanova had accelerated new product development post-spinoff, launching dozens of line extensions and limited editions. Mars traditionally takes a longer view, preferring to perfect products before launch. The combined entity must balance Mars's quality obsession with Kellanova's speed to market. Success means leveraging Mars's global R&D capabilities to accelerate Kellanova's innovation while maintaining the playful experimentation that made Pop-Tarts a social media phenomenon.

The future of food M&A will be shaped by this transaction's success or failure. If Mars successfully integrates Kellanova and achieves promised synergies, expect more mega-deals as companies pursue scale. If integration proves challenging or synergies disappoint, the industry might pivot toward smaller, strategic acquisitions. Private equity and family offices are watching closely, ready to deploy capital if opportunities emerge.

The competitive response is already taking shape. Mondelēz accelerated its snacking investments, acquiring Clif Bar and expanding Oreo into new formats. PepsiCo doubled down on Frito-Lay's innovation pipeline, launching more products in 2024 than the previous three years combined. General Mills and others are evaluating their portfolios, considering whether focus or scale offers the better path forward.

Emerging categories present both opportunity and disruption risk. Alternative proteins, despite Kellanova's retreat from a standalone plant-based spinoff, remain a long-term growth vector. Functional snacks—products that deliver specific health benefits beyond basic nutrition—are growing at double-digit rates. Personalized nutrition, enabled by AI and biomarkers, could fundamentally reshape how consumers choose foods. The Mars-Kellanova combination must navigate these trends while defending core categories.

The international growth opportunity cannot be overstated. Asia's middle class will add 2 billion consumers over the next decade. Africa's young population is adopting Western consumption patterns. Latin America's economic development is creating new snacking occasions. The combined entity's global footprint positions it to capture these opportunities, but execution will require local adaptation and patient investment.

Technology and digital transformation will reshape every aspect of the business. Direct-to-consumer channels, while still small, are growing rapidly. AI-powered demand forecasting can reduce waste and improve service levels. Automation can offset labor inflation. Digital marketing can create deeper consumer connections at lower cost. The companies that win will be those that successfully blend physical and digital capabilities.

The Legacy of W.K. Kellogg's Vision

As we conclude this epic journey from Battle Creek sanitarium to global snacking powerhouse, it's worth reflecting on what W.K. Kellogg would make of his company's evolution. The man who spent 25 years in his brother's shadow before founding a cereal empire at age 46 would likely appreciate the irony—his company found its greatest success by moving beyond the category he created.

Yet the fundamental principles W.K. established remain intact. The obsession with quality—he once ordered an entire production run destroyed because the flakes weren't properly toasted—lives on in Kellanova's manufacturing excellence. The marketing genius that turned breakfast from leftovers to branded experience continues in Pop-Tarts' social media mastery. The commitment to community, expressed through his 30-hour work week during the Depression, echoes in modern ESG initiatives.

The transformation from Kellogg Company to Kellanova to Mars Snacking represents not betrayal of the founder's vision but its evolution. W.K. didn't set out to make cereal—he wanted to build a business that improved people's lives through convenient, quality food. That mission remains unchanged, even as its expression shifts from breakfast bowls to snacking occasions.

The split that created Kellanova vindicated both Kellogg brothers in unexpected ways. John Harvey's vision of food as medicine finds expression in functional snacks and better-for-you options. W.K.'s commercial genius scales globally through brands that transcend their categories. The bitter feud that split the brothers ultimately created more value than their collaboration ever could.

For founders and investors, the Kellanova story offers timeless lessons. Focus beats diversification when businesses diverge. Cultural alignment matters more than strategic fit in acquisitions. Patient capital can pay prices impatient capital cannot justify. Great brands transcend their original categories. And sometimes, the best way to honor a legacy is to transform it completely.

The announcement that marked the end of Kellanova as an independent company also marked a beginning. Not just for Mars's expanded snacking ambitions, but for an industry grappling with fundamental change. As consumer habits evolve, as technology reshapes commerce, as sustainability becomes imperative rather than optional, the companies that thrive will be those that embrace transformation rather than resist it.

Standing in the Battle Creek headquarters that W.K. Kellogg built, looking at production lines that now ship products to 180 countries, one can't help but marvel at the journey. From accidental invention to intentional innovation. From family feud to global empire. From morning ritual to all-day occasion. From Kellogg Company to Kellanova to whatever comes next.

The corn flakes may have started it all, but they were never the end goal. They were simply the beginning of a conversation between a company and its consumers about what food could be—convenient, enjoyable, accessible, and perhaps even magical. That conversation continues today in every bag of Cheez-Its opened, every tube of Pringles popped, every Pop-Tart toasted. And it will continue tomorrow in ways W.K. Kellogg could never have imagined but would certainly have appreciated.

The story of Kellanova reminds us that in business, as in life, the only constant is change. The companies that survive aren't necessarily the strongest or the smartest, but the most adaptable. Kellanova adapted from cereal to snacking, from conglomerate to focused portfolio, from public to private ownership. Each transformation was painful, risky, and ultimately necessary.

As the Mars acquisition closes and Kellanova ceases to exist as a legal entity, its spirit lives on—in the brands consumers love, the innovation pipeline that keeps them relevant, and the fundamental belief that food is more than sustenance. It's comfort, joy, connection, and culture. That's the legacy of 118 years of evolution, from sanitarium kitchen to global snacking powerhouse. And that's the foundation on which the next chapter will be built.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube