Swiggy: The Quick Commerce Revolution

I. Introduction & Cold Open

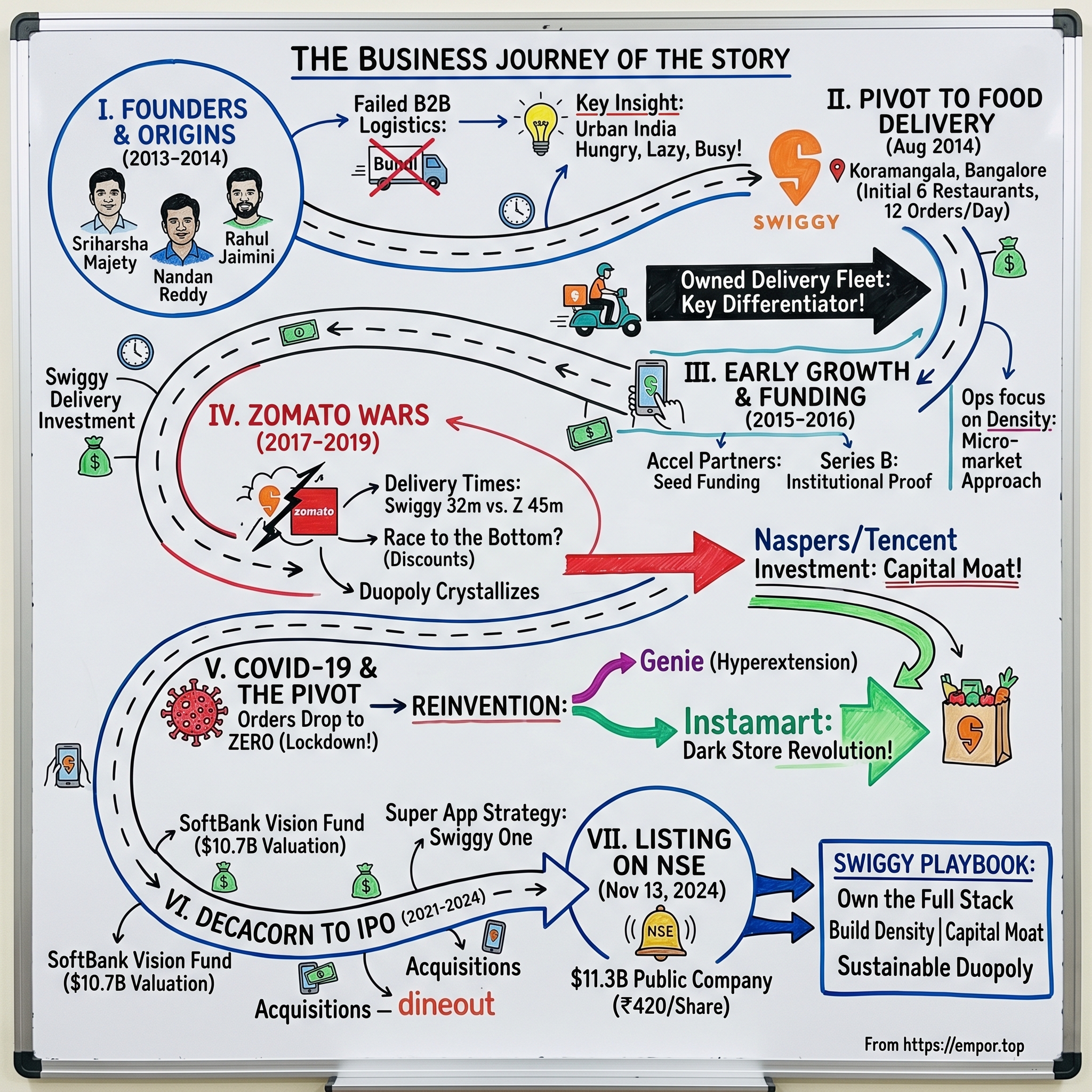

The monsoon rain hammered against the windows of a cramped Koramangala apartment in Bangalore, August 2014. Inside, three engineers hunched over laptops, their screens glowing with spreadsheets tracking exactly six restaurant partners and twelve delivery orders from the previous day. One of them, Sriharsha Majety, pushed back from his desk and looked at his co-founders with the kind of exhausted determination that only comes from having already failed once before. Just two months earlier, he had shut down Bundl, a logistics startup that had burned through savings and patience in equal measure. Now, with Swiggy, he was betting everything on a deceptively simple insight: people in urban India were hungry, lazy, and increasingly willing to pay someone else to brave the traffic and bring them dinner.

Ten years later, that bet would be worth $11.3 billion.

When Swiggy's shares began trading on the National Stock Exchange on November 13, 2024, at ₹420 per share—a 7.69% premium over its IPO price of ₹390—it marked more than just another tech listing. This was the culmination of India's most audacious experiment in redefining convenience itself. From those six restaurants in Koramangala, Swiggy had expanded to over 580 cities, employed hundreds of thousands of delivery partners, and fundamentally altered how 112 million Indians think about everything from dinner to groceries to forgotten phone chargers that absolutely must arrive within ten minutes.

But here's the provocative question that every investor, entrepreneur, and competitor should be asking: How did a failed logistics company pivot to create not just a food delivery giant, but a quick-commerce platform that's rewriting the rules of urban consumption in the world's most populous nation? The answer isn't just about technology or capital—though Swiggy has raised and burned through spectacular amounts of both. It's about timing, tenacity, and the willingness to own every messy, operational detail of the delivery experience when everyone else was building marketplaces.

This is the story of how Swiggy went from Bundl's ashes to IPO glory, fought the Zomato wars to a profitable stalemate, survived COVID by reinventing itself as a dark store operator, and positioned itself at the center of India's next consumer revolution: the promise that anything you want can appear at your doorstep faster than you can make coffee. It's a story of three friends who understood something fundamental about human nature—that convenience, once experienced, becomes indispensable—and built a business model that makes that convenience feel magical, even when it's powered by thousands of riders navigating chaotic streets with insulated bags strapped to their bikes.

What follows is an examination of not just a company, but a phenomenon. We'll dissect the operational innovations that gave Swiggy its edge, the strategic decisions that nearly killed it, and the brutal economics of a business where success is measured in minutes saved and percentage points of take rate. We'll explore how a food delivery company became a super app, why owning the fleet mattered more than anyone predicted, and what the future holds for a business model that promises to compress the time between desire and fulfillment to almost nothing.

The rain has stopped in Bangalore, but Swiggy's riders are still out there, weaving through traffic, racing against time, carrying not just food but the entire promise of modern urban life: that technology can solve the ancient problem of hunger, one delivery at a time. Let's begin where all great pivots start—with failure.

II. Origins: The Bundl Story & Pre-History

The cafeteria at BITS Pilani's Rajasthan campus stays open until 2 AM, a concession to the nocturnal habits of engineering students who treat sleep as an optional feature rather than a core requirement. It was here, sometime in 2009, that Sriharsha Majety first met Nandan Reddy at a photography club meeting. Majety, two years senior, was explaining the technical specifications of a new DSLR camera with the kind of intensity usually reserved for thermodynamics equations. Reddy, quieter but equally obsessive, was mentally calculating aperture settings. Neither knew that this late-night conversation about F-stops and shutter speeds would eventually lead to a company that would reshape how India eats.

Majety came from entrepreneurial stock—his father owned a restaurant in Vijayawada, Andhra Pradesh, where young Sriharsha spent summers watching the controlled chaos of a kitchen during the dinner rush. The restaurant business was in his blood, but not in the way his father expected. While the elder Majety focused on perfecting biryanis and managing temperamental chefs, Sriharsha was fascinated by the logistics: How do you predict demand? How do you optimize inventory when your product has a shelf life measured in hours? These weren't questions a teenager typically asks, but Majety wasn't typical. At BITS, while his classmates dreamed of packages from Infosys or Microsoft, he was reading case studies about FedEx and wondering why India's logistics infrastructure was still stuck in the 1990s.

After graduation, Majety did what ambitious BITS graduates do: he joined Nomura as an analyst. The investment banking years in London were formative, not for the financial modeling skills—though those would prove useful later—but for the exposure to how efficiently things worked in developed markets. He could order anything online and have it delivered the next day. Restaurant food arrived hot, on time, with real-time tracking. The contrast with India was stark. Back home for Diwali in 2012, he tried to order dinner in Bangalore and spent forty minutes on the phone explaining his address to a restaurant that was literally three kilometers away. The food arrived cold, late, and wrong. That night, he called Nandan Reddy, who was working at NetApp and equally frustrated with India's broken delivery ecosystem.

"What if we fixed logistics first?" Majety proposed during a Skype call that stretched until dawn. Not food delivery, not e-commerce, but the underlying infrastructure that made everything else possible. Reddy was intrigued enough to book a flight to London, where the two spent a week backpacking through Europe, not to see the Eiffel Tower or drink beer in Munich, but to study how logistics companies operated. They stood outside DHL distribution centers at 5 AM, watched how Deliveroo riders navigated London's narrow streets, and filled notebooks with observations about route optimization and hub-and-spoke models.

By August 2013, they were back in India, ready to build Bundl—a B2B logistics service that would help e-commerce companies handle last-mile delivery. The thesis was compelling: India's e-commerce market was exploding, but delivery remained a bottleneck. Small sellers couldn't afford their own fleet; large marketplaces struggled with reliability. Bundl would be the layer that connected them, the FedEx for India's digital economy. They raised a small angel round, hired a team, and set up operations in Bangalore.

For ten months, they fought reality. The unit economics were brutal—customer acquisition costs were high, order volumes from small businesses were unpredictable, and competing with established players like Blue Dart on price was suicide. But the real problem was timing. In 2013, India's e-commerce ecosystem wasn't mature enough to support a specialized logistics layer. Flipkart and Amazon were building their own delivery networks. Small sellers couldn't afford premium logistics services. Bundl was a solution in search of a problem, or rather, a solution that arrived five years too early.

By June 2014, with bank accounts depleted and morale shattered, Majety made the call to shut down Bundl. The team dispersed, investors wrote off their checks, and what seemed like a promising startup became another statistic in Bangalore's startup graveyard. Majety spent the next few weeks in his apartment, ordering food from various restaurants, partly because he couldn't bring himself to cook, partly because he was studying something. Every delivery was a data point: Which restaurants had their own delivery? How long did orders take? What was the error rate?

The bachelor life he and Reddy were living became their inadvertent market research lab. They ordered from the same restaurants repeatedly, experiencing firsthand the inconsistency, the cold food, the missing items, the drivers who couldn't find addresses. The pain point wasn't abstract—it was personal, daily, visceral. One evening, after receiving the wrong order for the third time that week, Majety called Reddy with a different proposition: "What if we didn't fix logistics for everyone? What if we just fixed it for food?"

The insight was subtle but profound. Food delivery wasn't just another logistics problem—it was a unique challenge with specific constraints. Food has a thirty-minute half-life for quality. Restaurants operate on thin margins and can't afford delivery infrastructure. Consumers order impulsively and expect instant gratification. The market wasn't looking for a logistics platform; it needed a delivery partner that understood the restaurant business. Majety's childhood in his father's restaurant suddenly became relevant. This wasn't about moving packages; it was about preserving the dining experience in transit.

But they needed someone who could build the technology to make it work. Enter Rahul Jaimini, a senior software engineer at Myntra who had built systems handling millions of fashion orders. A mutual friend introduced them, and Jaimini was immediately intrigued—not by the business plan, which was still forming, but by the technical challenge. Could you build a system that dynamically assigned orders to drivers, optimized routes in real-time, and predicted preparation times accurately enough to ensure food arrived hot? It was the kind of problem that made engineers lose sleep in the best way.

In August 2014, just two months after Bundl's funeral, the three co-founders incorporated Swiggy. The name—derived from "swiggy," suggesting something swift and smooth—was chosen in a fifteen-minute brainstorming session. They had no money, no restaurants, no drivers, and no customers. What they had was a thesis born from failure: that owning the entire delivery experience, rather than just connecting restaurants to customers, was the key to cracking food delivery in India. While competitors built marketplaces, Swiggy would build infrastructure. While others focused on metros, they would perfect the model in Bangalore first. While everyone else tried to be asset-light, they would embrace the operational complexity that others avoided.

The transformation from Bundl to Swiggy wasn't just a pivot—it was a complete philosophical reversal. Where Bundl tried to be a platform, Swiggy would be a service. Where Bundl avoided operational complexity, Swiggy would embrace it. The lessons from failure had crystallized into a strategy, and that strategy was about to collide with a market that didn't yet know it was hungry for change.

III. The Pivot: Finding Product-Market Fit

The first Swiggy office was a two-bedroom apartment in Koramangala where the living room served as both conference room and delivery dispatch center. Rahul Jaimini had quit his job at Myntra—a decision his parents called "career suicide"—to join two founders who had just failed at their previous startup. The entire technology infrastructure was three laptops and a whiteboard where they manually tracked orders with different colored markers: red for pending, yellow for preparing, green for delivered. It was August 2014, and they had convinced exactly six restaurants to participate in their experiment.

The personal pain point that drove the pivot was almost comically specific. Nandan and Harsha had been living the bachelor life in Bangalore, subsisting on a diet of restaurant food that arrived with the consistency of Bangalore traffic—which is to say, unpredictably and usually disappointing. They once ordered Chinese food that arrived two hours late with the soup having leaked into the fried rice, creating an unintentional fusion dish that nobody wanted. Another time, they spent forty-five minutes explaining their address to a delivery person who ultimately gave up and returned the food to the restaurant. These weren't edge cases; they were the norm. The market wasn't broken—it simply didn't exist in any meaningful way.

Jaimini's addition to the founding team was catalytic, not just for his technical skills but for his systematic approach to problem-solving. While Majety and Reddy had identified the problem, Jaimini could architect the solution. He spent his first week not writing code but shadowing delivery drivers from local restaurants, timing every aspect of their workflow with a stopwatch. How long did it take to find parking? How many orders could one person realistically handle? What was the optimal radius for delivery? The data was revealing: most restaurants limited delivery to a two-kilometer radius not because of food quality concerns but because their single delivery boy couldn't handle longer distances without the entire system breaking down.

The key insight that would define Swiggy's entire strategy emerged from a simple observation: restaurants were terrible at logistics because logistics wasn't their business. A good biryani chef shouldn't have to think about route optimization. A Chinese restaurant owner shouldn't need to manage a fleet of drivers. The existing model forced restaurants to be in two businesses simultaneously—food preparation and delivery operations—and they were predictably bad at the second one. The marketplace models that were emerging, like Foodpanda, simply connected customers to restaurants but left the actual delivery problem unsolved. It was like building a beautiful frontend for a broken backend.

"What if we owned the entire delivery fleet?" Majety proposed during one of their late-night strategy sessions. The reaction from everyone they pitched—investors, advisors, even friends—was uniformly negative. Owning assets was considered primitive in 2014. The entire startup ecosystem was obsessed with asset-light models, platforms, and marketplaces. Uber didn't own cars. Airbnb didn't own houses. Why would Swiggy own delivery drivers? But the founders had learned from Bundl that sometimes the theoretical best model and the practical best model diverge dramatically. In India's chaotic, fragmented market, control mattered more than capital efficiency.

They started with six restaurants in Koramangala, Bangalore's startup neighborhood where experimental business models were as common as craft coffee shops. The pitch to restaurants was simple: Swiggy would handle all delivery operations for a commission on each order. Restaurants wouldn't need to hire drivers, manage logistics, or handle customer complaints about delivery. They could focus on what they did best—cooking food. The first restaurant to sign up was Brahmin's Coffee Bar, a local South Indian joint known for its idlis. The owner, skeptical but curious, agreed to a trial period.

The first order came on August 15, 2014—Independence Day, which felt symbolically appropriate. It was for two masala dosas and a filter coffee, ordered by a software engineer who lived three blocks away. Majety himself did the delivery, racing through Koramangala's narrow streets on a borrowed scooter, the food packed in a cardboard box they had bought from a local packaging store. The entire order value was ₹130. Swiggy's commission was ₹26. It took forty-five minutes from order placement to delivery, and they lost money on the transaction when accounting for the petrol. But the food arrived hot, the customer was surprised by the professional packaging, and they had proved the model could work.

The early operations were almost comically manual. Jaimini had built a basic ordering system, but route optimization meant Reddy looking at Google Maps and calling drivers to tell them where to go next. Customer support was Majety's personal phone number. Marketing was walking into restaurants and convincing skeptical owners to try their service. They hired their first delivery executive—they insisted on calling them "delivery partners" from day one—a week after launch. By the end of the first month, they had ten drivers, twenty-five restaurant partners, and were processing about fifty orders per day.

What set Swiggy apart wasn't just owning the fleet but the obsessive focus on the delivery experience. Every driver was trained not just on navigation but on customer interaction. They standardized packaging, providing restaurants with Swiggy-branded bags that kept food warm. They implemented a simple but effective quality check: drivers would verify the order against the receipt before leaving the restaurant. These seem obvious in retrospect, but in 2014's Wild West of food delivery, they were revolutionary.

The product-market fit revealed itself not in explosive growth but in retention metrics. Customers who ordered once ordered again within a week at rates that surprised even the founders. Restaurants that initially signed up for trial periods extended indefinitely. The NPS scores—when they finally started measuring them—were in the 70s, unheard of for a logistics service. They had found something that worked, but it worked precisely because it was operationally intensive, capital-hungry, and difficult to scale. Every conventional startup wisdom said this was a bad business. The founders decided conventional wisdom was wrong.

By December 2014, Swiggy was processing 200 orders per day across Koramangala and had expanded to 100 restaurant partners. The unit economics were still negative—they were losing about ₹50 per order when factoring in all costs—but the trajectory was clear. Order volumes were growing 30% month-over-month. Customer acquisition costs were dropping as word-of-mouth kicked in. Restaurant partners were actively recommending Swiggy to other restaurant owners. They had found product-market fit not by building a platform but by solving an operational problem that everyone else had deemed too messy to touch.

The pivot from Bundl to Swiggy was complete, but it had fundamentally changed the founders' understanding of what business they were building. This wasn't a technology company that happened to do delivery; it was an operations company that used technology as leverage. The distinction would prove crucial as they entered the next phase: convincing investors that a business model everyone said couldn't scale was actually the future of food delivery in India.

IV. Early Growth & Finding Investors

The Accel Partners office in Bangalore's Koramangala neighborhood has a conference room nicknamed "The Colosseum" where brutal partnership meetings determine which startups receive funding and which get polite rejections. In January 2015, Sriharsha Majety sat in that room, laptop open to a spreadsheet showing Swiggy's metrics: 500 orders per day, 150 restaurant partners, and burn rate that would deplete their remaining cash in six weeks. Across the table, Accel partner Shekhar Kirani was doing mental math that didn't add up. The unit economics were negative, the operational complexity was massive, and the model went against everything the venture capital playbook prescribed. Yet something about the retention cohorts made him pause.

"Show me the month-two retention again," Kirani said, leaning forward. The number was 65%—customers who ordered in their first month were still ordering in their second month at rates that defied industry standards. In the food delivery graveyard of 2015, where startups were dying weekly, Swiggy had somehow created addiction. The meeting that was scheduled for thirty minutes stretched to three hours.

The venture capital ecosystem in 2015 was simultaneously bullish on India's consumer internet opportunity and bearish on food delivery specifically. The sector was in complete turmoil. Foodpanda, despite raising significant capital, was bleeding money and would soon be acquired by Ola Cabs in a fire sale. TinyOwl, once valued at over $100 million, was imploding spectacularly—their employees would literally hold the founders hostage over unpaid salaries. Ola Cafe, Uber's food delivery experiment, and a dozen other startups were all competing for the same customers with unsustainable discounts. The conventional wisdom was that food delivery in India was a race to the bottom where everyone would lose.

But Kirani saw something different in Swiggy's approach. While competitors were spending heavily on customer acquisition—offering 50% discounts, free delivery, cash backs—Swiggy was spending on infrastructure. They had forty-five delivery partners on payroll, a small but critical difference from the contractor model others used. They had invested in insulated delivery bags that actually kept food warm. They had built a simple but effective driver allocation algorithm that reduced delivery times by 20%. These weren't sexy investments that made headlines, but they created a moat that discounts couldn't breach.

The due diligence process was unconventional. Instead of focusing solely on financial models, Kirani's team ordered food through Swiggy every day for two weeks, timing deliveries, checking food temperature, calling customer service with fake complaints. They also ordered from competitors, creating a detailed comparison matrix. The difference was stark: Swiggy's food arrived faster, warmer, and with fewer errors. The customer service actually solved problems instead of offering empty apologies. It was execution excellence in a market where execution was everything.

In March 2015, Accel led a $2 million seed round, with SAIF Partners (now Elevation Capital) joining as co-investor. The term sheet negotiations revealed the founders' priorities: they pushed for a larger ESOP pool for early employees and operational flexibility over valuation optimization. They knew they were building an execution-heavy business where talent retention would matter more than paper valuations. The round valued Swiggy at roughly $10 million, a modest number that reflected both the market skepticism and the early stage of the business.

With fresh capital, Swiggy faced a critical strategic decision: expand geographically or deepen penetration in Bangalore? The temptation to plant flags in Mumbai and Delhi was strong—competitors were already claiming "national presence" in their PR releases. But Majety, influenced by his study of successful logistics companies, chose density over breadth. They divided Bangalore into micro-markets, launching neighborhood by neighborhood, ensuring each area had sufficient restaurant density and delivery capacity before moving to the next. It was the same playbook DoorDash would later use in the US, though neither company knew about the other at the time.

By June 2015, Swiggy had expanded from just Koramangala to cover most of Bangalore, processing 2,000 orders per day. But the real validation came from an unexpected source: restaurants started approaching them. The initial skepticism from restaurant owners had transformed into active demand. Word spread through the restaurant community that Swiggy actually delivered on its promises—orders arrived on time, customer complaints were handled professionally, and most importantly, payment settlements happened weekly without delays. In India's trust-deficit market, reliability was revolutionary.

The expansion to other cities began in September 2015, but it wasn't the haphazard land grab that characterized competitor strategies. Each city launch followed a playbook refined in Bangalore: start with one high-density neighborhood, usually where young professionals lived. Partner with recognized local restaurants first to build credibility. Hire delivery partners from the local community who knew the area's geography. Build density before expanding the coverage area. By December 2015, Swiggy was operational in eight cities—Bangalore, Mumbai, Delhi, Chennai, Hyderabad, Pune, Kolkata, and Gurgaon—but within each city, they operated in select neighborhoods rather than claiming citywide coverage.

The Series B fundraise in 2016 happened against a dramatically different backdrop. The food delivery bloodbath had claimed multiple casualties. TinyOwl was effectively dead. Foodpanda had been absorbed by Ola. Zomato, primarily a restaurant discovery platform, was tentatively entering delivery. The market had consolidated from over twenty players to fewer than five. Swiggy hadn't just survived; it had grown 10x while maintaining relatively healthy unit economics in its mature Bangalore market.

Norwest Venture Partners led the $15 million Series B, with Accel and SAIF participating. But the round also brought in two strategic investors that would prove crucial: Bessemer Venture Partners, known for their operational expertise, and Harmony Partners, which had deep connections in the restaurant industry. The capital was important, but the expertise and networks these investors brought were invaluable. Bessemer's portfolio services team helped Swiggy implement driver training programs adapted from their US portfolio companies. Harmony facilitated partnerships with restaurant chains that had previously been skeptical of third-party delivery.

The inflection point was visible in the data by late 2016. Swiggy crossed 100,000 orders per day. Month-on-month growth stabilized at 20-25%. More importantly, contribution margins in Bangalore turned positive—the first proof that the model could work economically. They had 5,000 delivery partners across eight cities and partnerships with over 10,000 restaurants. The scrappy startup that had manually tracked orders on a whiteboard was becoming a real company.

But success attracted attention. Zomato, with its massive restaurant database and recent $200 million fundraise, was coming for the delivery market. Uber was expanding UberEATS globally and eyeing India. Amazon was rumored to be exploring food delivery. The small player advantage—being ignored while perfecting the model—was ending. The next phase wouldn't be about proving the model worked; it would be about defending market share in what was about to become one of India's most brutal startup wars.

V. The Zomato Wars & Market Dynamics

The December 2016 Swiggy leadership meeting at the Sheraton Hotel in Bangalore had the atmosphere of a war council. On the projection screen was a map of India with red dots representing Zomato's delivery presence and blue dots showing Swiggy's coverage. The red was spreading faster. Deepinder Goyal, Zomato's CEO, had just announced a $200 million war chest specifically for food delivery, backed by a public declaration that Zomato would become India's food delivery leader within eighteen months. For the first time since pivoting from Bundl, Swiggy faced an existential threat from a competitor with deeper pockets, better brand recognition, and a database of every restaurant in India.

"They have everything except one thing," Majety told his leadership team, pointing to a slide showing delivery times. "They don't have our obsession with operations." It sounded like bravado, but the data supported it. Zomato's average delivery time was 45 minutes; Swiggy's was 32. Zomato's order accuracy was 87%; Swiggy's was 94%. These weren't just metrics—they were the difference between a customer ordering again tomorrow or deleting the app in frustration.

The market dynamics in 2017 created a perfect storm for competitive intensity. India's smartphone penetration had crossed 300 million users. Jio's revolutionary data pricing made mobile internet essentially free. Digital payments were finally gaining traction post-demonetization. The food delivery TAM (Total Addressable Market) had expanded from $1 billion to a projected $8 billion by 2020. This wasn't a winner-take-all market anymore; it was winner-take-most, and both companies knew it.

Zomato's entry strategy was a masterclass in leveraging existing assets. They had spent eight years building a restaurant discovery platform with menus, photos, and reviews for over 1.5 million restaurants. They had 120 million monthly active users who already opened the app to decide where to eat. Adding a "deliver" button seemed like a natural extension. They could onboard restaurants at unprecedented speed—sometimes adding 1,000 new delivery partners in a single day. Their brand was synonymous with food; Swiggy was still explaining to customers that they weren't a restaurant.

But Swiggy had built something Zomato couldn't quickly replicate: operational density. In Bangalore, Swiggy had 1,200 delivery partners for roughly 3,000 restaurants, a ratio that enabled sub-30-minute delivery times. Zomato, trying to scale rapidly, had 800 delivery partners for 5,000 restaurants in the same city. The math was brutal—longer wait times, longer delivery times, unhappier customers. Zomato was playing for breadth; Swiggy was playing for depth.

The commission rate war began in March 2017. Restaurants typically paid 20-25% commission on delivery orders. Zomato, leveraging its restaurant relationships, offered 15% rates to exclusive partners. Swiggy responded not by cutting rates but by introducing "Swiggy Access," a program where they invested in kitchen infrastructure for restaurants wanting to expand to new areas without capital investment. It was a counter-intuitive move—spending more money when a competitor was starting a price war—but it locked in relationships with key restaurant partners who valued growth over marginally lower commissions.

The customer acquisition battle was more visible and more vicious. Zomato launched "Zomato Gold," a subscription program offering complimentary dishes at restaurants, extended to delivery with significant discounts. Swiggy responded with "Swiggy Super," later renamed "Swiggy One," providing free delivery and exclusive discounts for a monthly fee. Both companies were essentially paying customers to create habits, betting that lifetime value would eventually exceed acquisition costs. The monthly cash burn for both companies exceeded $20 million by mid-2017.

Geographic expansion became a chess match. When Zomato announced entry into Tier 2 cities like Jaipur and Lucknow, Swiggy would launch there within weeks, sometimes before they were operationally ready. When Swiggy entered Ahmadabad, Zomato followed within ten days. Both companies were planting flags, knowing that the first mover in smaller cities could lock in both restaurant partnerships and customer habits before competition arrived. By end of 2017, the coverage maps looked like a Jackson Pollock painting—overlapping territories with no clear winner.

The differentiation strategies that emerged revealed each company's DNA. Zomato leveraged its content and discovery strengths, launching "Zomato Kitchen" for cloud kitchens and "Hyperpure" for restaurant supplies. They were building a full-stack restaurant services company with delivery as one component. Swiggy doubled down on delivery excellence, launching "Swiggy Scheduled" for advance orders and "Swiggy Daily" for homemade meal subscriptions. Where Zomato built horizontally across restaurant services, Swiggy built vertically into different delivery use cases.

A pivotal moment came in September 2017 when Naspers, the South African technology investor, needed to choose between backing Swiggy or Zomato for the Indian food delivery market. Both companies pitched aggressively. Zomato emphasized its brand strength and restaurant relationships. Swiggy presented cohort retention data showing that customers acquired in 2015 were still ordering at 60% of their peak frequency two years later. Naspers chose Swiggy, leading an $80 million round that valued the company at $700 million. The signal to the market was clear: smart money was betting on execution over brand.

The competitive dynamics created unexpected innovation. The pressure to differentiate led Swiggy to launch "Swiggy POP," single-serve meals under ₹100 targeting individual diners rather than families. Zomato responded with "Zomato Originals," partnering with celebrity chefs to create exclusive dishes. Both companies started investing heavily in cloud kitchens—delivery-only restaurants that could serve multiple brands from a single location. The war was forcing both companies to reimagine not just food delivery but food itself.

By early 2018, market share data showed a deadlock: Swiggy held 46% of the market, Zomato controlled 54%. But the definition of "market" was becoming fuzzy. In metros, Swiggy dominated with 48% share. In Tier 2 cities, Zomato's early entry gave them 55% share. Among high-frequency users (ordering more than eight times per month), Swiggy had 52%. Among casual users, Zomato led with 51%. Both companies could claim victory depending on how they sliced the data.

The human cost of the war was significant. Both companies were burning through delivery partners with monthly churn rates exceeding 30%. The pressure to deliver faster led to accidents, with delivery partners racing through traffic to meet aggressive targets. Customer service teams were overwhelmed, handling thousands of complaints daily about late deliveries, wrong orders, and missing items. The growth-at-all-costs mentality was creating operational debt that would take years to repay.

February 2018 brought a new dimension to the competition when Meituan-Dianping, the Chinese food delivery giant, co-led a $100 million round in Swiggy alongside Naspers. The investment came with technology transfer agreements, giving Swiggy access to algorithms and operational playbooks refined in China's even more competitive market. Zomato responded by deepening its relationship with Ant Financial, Alibaba's financial services arm. The India food delivery war was becoming a proxy battle for Chinese technology giants.

The war reached its crescendo in late 2018 with both companies raising massive rounds within weeks of each other. Swiggy raised $1 billion led by Naspers and Tencent, achieving a $3.3 billion valuation. Zomato raised $200 million from Ant Financial at a $2 billion valuation. The capital arms race meant both companies could sustain losses for years. The market had spoken: India was big enough for two players, but probably not three. The duopoly that exists today was crystallizing.

As 2019 began, fatigue was setting in on both sides. The unsustainable discounts were training customers to be promiscuous, switching between apps based on which offered better deals. Restaurant partners were frustrated with high commissions and the commoditization of their brands. Investors were asking uncomfortable questions about paths to profitability. The war had established market positions but at a pyrrhic cost. Neither company had won decisively, but both had learned that competition in India's food delivery market would be a marathon, not a sprint. The next phase would require a different strategy—one focused on sustainability over growth, innovation over imitation, and perhaps most importantly, preparing for a black swan event that nobody saw coming.

VI. COVID & The Dark Store Revolution

March 24, 2020, 8 PM. Prime Minister Modi announced a nationwide lockdown with four hours' notice. In Swiggy's Bangalore headquarters, now empty except for a skeleton crisis management team, the real-time order tracker showed something unprecedented: order volumes dropping to zero. Not declining, not slowing—zero. Across India, 45,000 delivery partners were being turned away at apartment complexes and neighborhood checkpoints. Restaurants were shuttering, unsure if food delivery counted as "essential services." Three years of growth evaporated in three hours. Sriharsha Majety, watching the monitors go dark, turned to his leadership team on a Zoom call: "We either die here, or we reinvent everything."

The first forty-eight hours were about survival, not strategy. The operations team worked with local police commissioners to get movement passes for delivery partners. The legal team lobbied government officials to clarify that food delivery was indeed essential. The finance team ran scenarios—at zero revenue, Swiggy had eight weeks of runway. But the real crisis was human. Thousands of delivery partners, mostly migrants, were stranded without income. Restaurants, already operating on thin margins, faced bankruptcy. The entire ecosystem Swiggy had spent six years building was collapsing.

The immediate response was triage. Swiggy launched a relief fund, providing direct cash transfers to delivery partners. They offered free marketing credits to restaurant partners and waived commissions for the first month. But charity couldn't sustain a business. By April, with lockdowns extending indefinitely, a different strategy emerged. If people couldn't go to stores, stores had to go to people—not just restaurants, but everything. The infrastructure for hyperlocal delivery existed; the use case just needed to expand.

"Swiggy Genie" had actually launched in September 2019 as a pickup-and-drop service, mostly used for forgotten documents or sending keys to friends. During lockdown, it exploded into something else entirely. Customers used it to get medicines from pharmacies, vegetables from local vendors, even electronics from shops that had never considered delivery. Order volumes grew 50x in three weeks. But Genie was a band-aid, not a solution. The real opportunity was in structured instant grocery delivery, a space where Swiggy had been experimenting since 2019 with "Swiggy Stores."

The decision to shut down Swiggy Stores and launch Instamart in August 2020 was made during a virtual board meeting where directors were spread across eight time zones. The grocery delivery space was already crowded—BigBasket, Grofers (now Blinkit), and Amazon were established players. But they were all operating on a marketplace or warehouse model with delivery times measured in hours or days. Swiggy's insight, borrowed from Chinese players like MissFresh and reinforced by Meituan's playbook, was that grocery delivery needed to be as fast as food delivery. That meant dark stores.

A dark store is a contradiction—a retail space that customers never enter, optimized entirely for picking and packing rather than shopping experience. Swiggy's first dark store opened in a former clothing outlet in Bangalore's Bellandur neighborhood. Two thousand square feet, 1,800 SKUs, eight staff members, and a promise: groceries delivered in under 45 minutes. The unit economics were terrifying. The store cost ₹15 lakhs to set up, ₹3 lakhs monthly to operate, and was processing 100 orders per day at an average order value of ₹400. They were losing ₹200 per order. But the retention metrics were extraordinary—customers who ordered once ordered again within a week at 80% rates.

The dark store model required rethinking everything. Traditional grocery stores optimize for browsing; dark stores optimize for picking speed. SKUs were arranged not by category but by popularity—milk and bread near the entrance, exotic vegetables in the back. Inventory management became algorithmic, predicting neighborhood-level demand for specific products. The technology stack, originally built for restaurant orders, had to handle fundamentally different complexity. A restaurant order might have ten items from one location; a grocery order could have fifty items that needed to be picked, packed, and quality-checked in under ten minutes.

By November 2020, Instamart had ten dark stores across Bangalore and Gurgaon. The competition was intensifying. Grofers was pivoting to instant delivery. A new startup called Zepto, founded by two Stanford dropouts, promised ten-minute delivery. Dunzo, backed by Reliance, was expanding aggressively. The quick commerce wars were beginning, fought not with restaurants but with real estate and inventory. The game was about density—who could build the most dark stores in the most neighborhoods fastest.

The human impact of COVID on Swiggy was devastating but revealing. In May 2020, the company laid off 1,100 employees, primarily in sales and operations roles made redundant by lockdowns. Cloud kitchens, once seen as the future, were particularly hit—Swiggy shut down three-fourths of its cloud kitchen operations as demand for restaurant food cratered. But the crisis also revealed resilience. Delivery partners who stayed saw earnings increase as demand concentrated among fewer workers. Restaurant partners who adapted—creating "lockdown menus" with comfort foods and family packs—saw orders surge.

The strategic pivot during COVID went beyond just adding groceries. Swiggy recognized that the pandemic had accelerated a fundamental shift in consumer behavior. The convenience economy wasn't just about laziness anymore; it was about safety, time optimization, and urban lifestyle adaptation. People working from home didn't want to spend lunch breaks shopping. Families juggling remote work and online schooling needed predictable delivery windows. The TAM for instant delivery had expanded from young professionals ordering dinner to essentially everyone needing everything.

Instamart's growth trajectory through 2021 was hockey-stick vertical. From 10 dark stores in November 2020, they expanded to 150 by December 2021. Order volumes grew from 1,000 per day to 100,000. The SKU count expanded from 1,800 to 6,000, then 10,000, eventually reaching 19,000 by 2024. But the real innovation was in the operating model. Unlike food delivery where Swiggy was an intermediary, in quick commerce they controlled the entire stack—procurement, inventory, storage, and delivery. It was the Bundl vision finally realized, just in a completely different context.

The challenges were immense. Each dark store was essentially a small business requiring local permits, inventory financing, and wastage management. The working capital requirements were massive—Swiggy had to buy inventory upfront and hold it, unlike food delivery where restaurants bore that cost. The technology complexity multiplied. Route optimization for groceries was different from food—you could batch multiple grocery orders but not restaurant orders. Quality control became critical as Swiggy was now responsible for the actual products, not just their delivery.

Competition in quick commerce was even more brutal than food delivery. Zepto raised $200 million promising to define the ten-minute delivery category. Blinkit (formerly Grofers) had Zomato's backing and deeper grocery expertise. Dunzo had Reliance's deep pockets. Amazon and Flipkart were testing their own instant delivery services. The market was seeing $100 million funding rounds every quarter, all chasing the same thesis: that instant gratification would become the default expectation for urban commerce.

By early 2022, Instamart had established itself as a serious player with 500+ dark stores across 30 cities. The unit economics were improving but still negative. The average order value had increased to ₹500, delivery costs had dropped to ₹40 per order through batching, and contribution margins were approaching breakeven in mature stores. But the capital requirements were staggering. Each dark store needed ₹20-30 lakhs in inventory, the real estate costs were significant, and the technology infrastructure investment was continuous.

The COVID period transformed Swiggy from a food delivery company to a quick commerce platform. The crisis that almost killed the company had forced an evolution that might have taken years otherwise. By the time lockdowns ended and restaurants fully reopened, consumer habits had permanently shifted. The expectation of instant delivery had expanded from food to groceries to essentially everything. Swiggy had survived COVID, but more importantly, it had used the crisis to position itself at the center of India's next consumer revolution. The question now wasn't whether quick commerce would work—that had been proven. The question was who would win the land grab, and at what cost.

VII. Unicorn to Decacorn: The Funding Journey

The Softbank Vision Fund office in Tokyo operates on what founder Masayoshi Son calls "300-year thinking"—planning for centuries, not quarters. But in July 2021, when Swiggy's leadership team presented via video conference from Bangalore, the conversation was about the next 300 days. India's startup ecosystem was experiencing a funding tsunami. Zomato had just gone public at a $9 billion valuation. Every growth-stage startup was raising rounds at valuations that would have seemed delusional twelve months earlier. For Swiggy, it was the moment to load the war chest for what everyone knew would be the final phase of the quick commerce battle.

The presentation deck was 150 slides of controlled chaos. Food delivery GMV growing 40% year-over-year. Instamart expanding to two new cities weekly. Genie processing everything from birthday cakes to mobile phones. The numbers were massive—50 million monthly active users, 200,000 restaurant partners, 300,000 delivery partners—but the burn rate was equally staggering. Swiggy was losing $40 million monthly, and that was considered efficient by Indian startup standards. The ask was bold: $1.25 billion at a $5.5 billion pre-money valuation, the largest private round in Indian startup history.

Masayoshi Son's team had one primary question: "How do you become worth $50 billion?" Not $10 billion, not $20 billion, but $50 billion. In Softbank's calculus, anything less wasn't worth their time. Majety's answer revealed how much Swiggy's ambition had expanded from those six restaurants in Koramangala. This wasn't about food delivery or even quick commerce. This was about owning the transaction layer for urban India—every meal, every grocery run, every convenience need, flowing through Swiggy's platform. The vision was audacious enough to get Softbank's attention.

The July 2021 round was a masterclass in momentum fundraising. Softbank led with $450 million, but the real story was the cap table transformation. Prosus (formerly Naspers) maintained its position with $300 million. New investors included Accel, Qatar Investment Authority, and Singapore's GIC. The round was oversubscribed 3x, with investors literally competing to get allocation. The valuation jump from $3.6 billion in April 2020 to $5.5 billion in July 2021 seemed conservative given that Zomato was trading at 20x forward revenue multiples in public markets.

But the capital wasn't just about vanity metrics or paper valuations. Swiggy was fighting multiple wars simultaneously. Against Zomato in food delivery. Against Zepto, Blinkit, and Dunzo in quick commerce. Against Amazon and Flipkart in broader e-commerce. Each battlefield required different weapons. Food delivery needed restaurant partnerships and delivery density. Quick commerce needed real estate and inventory. The broader platform play needed technology infrastructure and talent. The $1.25 billion was strategic ammunition, allocated with military precision.

The acquisition strategy that followed was revealing. Swiggy didn't buy competitors—that would have triggered regulatory scrutiny. Instead, they bought capabilities. In early 2022, they acquired Dineout from Times Internet for $120 million, gaining not just a restaurant reservation platform but also relationships with 50,000 premium restaurants and, crucially, their data on dining patterns. The deal was structured entirely in stock, preserving cash for operations while aligning Dineout's team with Swiggy's long-term success.

The Dineout acquisition was about more than just reservations. It was Swiggy's entry into the $40 billion dine-out market, which dwarfed food delivery. The strategic logic was compelling: use delivery to build daily habits, use dining to build premium relationships. A customer might order from Swiggy twice a week but dine out for special occasions. Owning both touchpoints meant owning the entire food journey. The integration was seamless—Dineout became another tab in the Swiggy app, but the backend systems were completely rebuilt to leverage Swiggy's technology infrastructure.

By January 2022, the funding environment had shifted dramatically. The public markets were punishing growth stocks. Zomato's stock had crashed 60% from its IPO highs. Suddenly, profitability mattered more than growth. But Swiggy had one more card to play. Invesco, the US asset manager with $1.5 trillion under management, was looking for private market exposure to Indian consumer technology. They led a $700 million round at a $10.7 billion valuation, making Swiggy India's third decacorn after Paytm and Byju's.

The Invesco round was different from previous raises. The terms included specific profitability milestones, governance improvements, and a clear path to IPO. This wasn't growth capital anymore; it was pre-IPO positioning. Invesco's involvement brought institutional discipline. They demanded monthly board meetings, detailed unit economics reporting, and a three-year path to EBITDA positivity. The era of "growth at all costs" was officially over.

The capital allocation strategy post-Invesco revealed Swiggy's maturation. Instead of burning money on customer acquisition, they invested in infrastructure. $200 million went to Instamart expansion, but focused on store-level profitability rather than blind expansion. $150 million funded technology development, particularly in AI-driven demand prediction and route optimization. $100 million created a driver welfare fund, providing insurance, education support, and emergency assistance. It was patient capital deployment, optimizing for sustainable advantages rather than temporary market share gains.

The super app strategy crystallized during this period. Swiggy wasn't just adding services; they were building an ecosystem. Swiggy One, the membership program, unified benefits across food delivery, Instamart, and Dineout. Swiggy Money, a digital wallet, kept transactions within the ecosystem. Swiggy Daily, the homemade meal subscription service, targeted a completely different use case from restaurant delivery. Each service reinforced others, creating multiple touchpoints with consumers and increasing lifetime value.

The SteppinOut acquisition in late 2022 seemed puzzling initially. Why would a food delivery company buy an events and experiences platform? But it fit the broader vision of owning urban lifestyle transactions. A user might order lunch from Swiggy, buy groceries from Instamart, book dinner through Dineout, and purchase concert tickets through SteppinOut. The same delivery fleet could deliver food or event tickets. The same customer support could handle restaurant complaints or booking issues. The platform economics were compelling—near-zero marginal cost for additional services on existing infrastructure.

The funding journey from unicorn to decacorn wasn't just about raising capital; it was about transformation. Each round brought not just money but strategic value. Naspers brought global marketplace expertise. Softbank brought aggressive growth capital. Invesco brought public market discipline. The cap table read like a who's who of global technology investors, but more importantly, each investor pushed Swiggy to evolve. The scrappy startup that manually tracked orders had become a sophisticated technology platform processing millions of transactions daily.

The financial metrics by late 2022 were staggering. Annual GMV exceeded $4 billion. Revenue run rate approached $1.5 billion. The company employed 5,000 full-time employees and engaged 300,000 delivery partners. Instamart alone was processing 500,000 orders daily. But the most important metric was improving unit economics. Contribution margins in the food delivery business had turned positive. Mature Instamart stores were approaching breakeven. The path to profitability, while still long, was finally visible.

The decision to prepare for an IPO, made in late 2022, was driven by multiple factors. The private markets had effectively closed for large rounds. Existing investors wanted liquidity options. Employees holding ESOPs needed an exit path. But most importantly, Swiggy needed permanent capital access to fight the next phase of the quick commerce war. The public markets, despite their volatility, offered something private markets couldn't: the ability to raise capital based on performance, not promises.

As 2023 began, Swiggy's valuation journey from $10 million seed to $10.7 billion decacorn seemed inevitable in hindsight but was anything but predetermined. Each funding round was a bet on a different thesis. The seed round bet on fixing food delivery logistics. Series A bet on building delivery infrastructure. Growth rounds bet on market domination. Late-stage rounds bet on platform expansion. The IPO would bet on something else entirely: that Swiggy could transition from growth to profitability while maintaining its market position. It was the ultimate test for a company that had always defied conventional wisdom.

VIII. The IPO & Public Markets Transition

The conference room on the 47th floor of the Bombay Stock Exchange building has witnessed countless corporate dreams either crystallize or crumble. On November 13, 2024, at 9:15 AM, Sriharsha Majety stood there in a navy blue suit—a departure from his usual hoodie and jeans—preparing to ring the opening bell. The screens showed SWIGGY in bold letters, preceded by ₹420, a 7.69% premium to the IPO price of ₹390. In that moment, the food delivery startup born in a Koramangala apartment officially became an $11.3 billion public company. But the journey to this moment had been anything but smooth.

The preparation for going public began with brutal cost-cutting in January 2024. Swiggy laid off 400 employees, 6% of its corporate workforce, primarily in roles that had become redundant through automation or consolidation. The optics were terrible—laying off employees months before a massive liquidity event—but the math was unavoidable. Public markets would scrutinize every expense line, and Swiggy needed to demonstrate fiscal discipline. The severance packages were generous, including accelerated ESOP vesting and placement support, but the message was clear: the era of startup excess was over.

The conversion to a public limited company in April 2024 triggered a cascade of structural changes. The confidential filing with SEBI revealed complexities that private investors had overlooked. Swiggy had no identifiable promoter—unusual for Indian companies where founder control is typically sacrosanct. The ownership was distributed across 75 investors with no single entity owning more than 10%. This structure, while ensuring no single point of control, raised governance questions. Who would drive long-term strategy when the largest shareholders were financial investors with different time horizons?

The red herring prospectus, filed in September 2024, was 600 pages of dense financial and operational disclosure. For the first time, the public could see inside Swiggy's black box. Revenue from operations had grown from ₹5,704.90 crore in FY22 to ₹11,247.39 crore in FY24, a 97% increase. But losses, while declining, remained substantial—₹2,350 crore in FY24. The unit economics were improving but still negative in growth segments like Instamart. The prospectus revealed that food delivery was actually profitable on a contribution margin basis, but quick commerce was burning cash at unprecedented rates.

The ₹11,327 crore offering structure was complex, balancing multiple objectives. ₹4,499 crore was primary capital for Swiggy's growth plans. ₹6,828 crore was an offer for sale (OFS) by existing investors seeking exits. The pricing band of ₹371-390 per share valued Swiggy between $10.8-11.3 billion, a premium to the last private round but below the $12-15 billion that bankers had initially suggested. The conservative pricing reflected market realities—global tech stocks were volatile, Indian IPOs had been underperforming, and Zomato's stock was trading at just 8x revenue compared to 20x at its peak.

The roadshow in October 2024 was exhausting. Majety and CFO Rahul Bothra presented to over 200 institutional investors across Mumbai, Singapore, London, and New York. The same questions emerged repeatedly: When would Swiggy become profitable? How sustainable was the quick commerce model? Could they compete with Zomato's improving margins? The answers required delicate balance—optimistic enough to excite investors but realistic enough to maintain credibility. The pitch evolved from "growth at all costs" to "disciplined expansion with a clear path to profitability by FY27."

The anchor investor book, which closed on November 5, showed tepid interest. International funds allocated $600 million, less than the $1 billion hoped for. Domestic institutions were more enthusiastic but price-sensitive. The retail portion was the wild card—Indian retail investors had been burned by recent tech IPOs but remained fascinated by consumer technology stories. The subscription opened on November 6 with cautious optimism. By November 8, when bidding closed, the issue was subscribed 3.59 times, respectable but not spectacular.

The allocation process revealed market dynamics. Qualified Institutional Buyers (QIBs) received 75% of shares, high-net-worth individuals got 15%, and retail investors received 10%. But within these categories, the distribution was telling. Long-only funds dominated QIB allocation, suggesting confidence in Swiggy's long-term story. Retail subscription was highest in metros where Swiggy operated, indicating brand loyalty translating to investment interest. The employee portion was oversubscribed 5x, reflecting internal confidence despite recent layoffs.

Listing day, November 13, 2024, began with nervous energy. The grey market premium had been volatile, swinging between ₹5-30 per share. When trading opened at ₹420, a 7.69% premium, there was visible relief in Swiggy's makeshift war room at the BSE. But the real test came in the first hour of trading. Volume was heavy—50 million shares changed hands. The price held steady, closing the first day at ₹424, a modest but meaningful victory. Swiggy was now worth more than Jubilant FoodWorks (Domino's India) and Westlife Development (McDonald's India) combined.

The use of proceeds, detailed in the prospectus, revealed strategic priorities. ₹1,179 crore was earmarked for dark store expansion, specifically 500 new Instamart locations. ₹730 crore would fund technology infrastructure, particularly AI and automation. ₹647 crore was allocated for brand marketing, acknowledging that public companies needed broader awareness. ₹503 crore would remain as working capital for the quick commerce business. Notably absent was any mention of acquisitions, suggesting organic growth was the primary strategy.

The governance structure post-IPO was deliberately independent. The board included heavy-hitters like Sahil Barua (Delhivery founder) and Revathy Ashok (veteran director). The founders retained board seats but not control—Majety owned just 6.5% post-IPO. This structure was designed to appeal to institutional investors wary of founder-dominated companies. The quarterly earnings call commitment, audit committee independence, and detailed disclosure standards all signaled maturation from startup to corporation.

The immediate post-IPO period tested Swiggy's public market readiness. The first earnings announcement in February 2025 would be scrutinized minutely. The company pre-emptively set expectations, warning that Q3 was traditionally weak due to the festival season impact on restaurant operations. They also announced that Instamart expansion would accelerate, potentially impacting short-term margins. The market's reaction would determine whether Swiggy could access public markets for future capital needs or would remain dependent on operational cash flow.

The employee wealth creation from the IPO was substantial but unevenly distributed. Early employees who had persevered through the Bundl failure became paper millionaires. Delivery partners, classified as gig workers, received no equity participation—a sore point that highlighted the gig economy's structural inequalities. The ESOP pool expansion to 7% of equity was generous by Indian standards but raised questions about talent retention as employees could now liquidate holdings.

The competitive implications of the IPO were significant. With permanent capital access, Swiggy could match Zomato's moves without returning to private markets. The disclosure requirements meant both companies could see each other's detailed metrics quarterly, potentially reducing irrational competition. The public market discipline would force both to prioritize profitability over market share. The duopoly structure, now crystallized with both companies public, suggested a shift from warfare to wary coexistence.

The international investor perspective on Swiggy's IPO was revealing. Comparisons weren't to Zomato but to DoorDash, Delivery Hero, and Meituan. By these standards, Swiggy was trading at attractive valuations—3x forward revenue versus 5x for global peers. But the India discount reflected real concerns: regulatory uncertainty, competitive intensity, and unclear path to profitability. The inclusion in MSCI indices, expected by mid-2025, would bring passive flows but also greater scrutiny.

As the first trading week ended, Swiggy's stock had settled at ₹418, maintaining most of its listing gains. The verdict was clear but not emphatic: public markets would give Swiggy a chance but demanded proof of sustainable economics. The transformation from private to public company was complete in legal terms but just beginning operationally. Every decision would now be viewed through the lens of quarterly earnings. Every strategic move would be debated on business channels. Every competitor action would impact stock price. The freedom of private capital was gone, replaced by the discipline and scrutiny of public markets. For a company that had always defied conventional wisdom, it was perhaps the ultimate test: Could Swiggy satisfy public market expectations while maintaining the innovation and aggression that had brought it this far?

IX. Business Model & Unit Economics Deep Dive

The spreadsheet on the screen looked like a small city's municipal budget. Revenue streams flowing from fifteen different sources. Cost centers spreading across twenty categories. At the center, a single cell showing the number that mattered: contribution margin, finally positive at 2.3% for Q3 FY24. But that aggregate number masked a complex reality. Food delivery was generating 8% margins. Instamart was burning cash at -12% margins. Platform innovations like Genie were somewhere in between. Understanding Swiggy's business model required decomposing this complexity into its constituent parts, each with its own economics, growth trajectory, and strategic rationale. The five distinct business verticals revealed fundamentally different economics and strategic purposes. Revenue from operations increased from ₹5,704.90 crore in FY22 to ₹8,264.60 crore in FY23 to ₹11,247.39 crore in FY24, representing a 36% year-over-year growth in the most recent fiscal year. But beneath these aggregate numbers lay five distinct businesses, each with its own trajectory.

Food delivery, the original business, generated ₹6,100 crore in FY24, growing 17% year-over-year. The economics here had matured significantly. Take rates—Swiggy's percentage of each order—had stabilized at 23-25%, comprising restaurant commissions (18-20%), delivery charges (₹30-40 per order), and platform fees (₹5-7 per order introduced in 2023). The controversial platform fee, initially met with customer backlash, had become normalized. Every order now contributed positively to gross margins, though the definition of "positive" required careful parsing.

The delivery economics breakdown revealed why owning the fleet mattered. Average order value (AOV) in food delivery was ₹385. Delivery cost per order was ₹42, comprising driver payment (₹35), fuel reimbursement (₹5), and insurance/equipment (₹2). But this was where density created magic. In high-density areas like Koramangala, drivers could complete three orders per hour. In low-density areas, it dropped to 1.5 orders. The same driver cost yielded different unit economics based purely on operational density. This explained Swiggy's micro-market approach—saturate neighborhoods before expanding.

Quick commerce through Instamart was the growth engine, generating ₹1,100 crore gross revenue in FY24, nearly doubling from the previous year. But the economics were brutal. Each dark store required ₹30 lakhs in inventory investment, ₹15 lakhs in setup costs, and ₹3 lakhs monthly operating expenses. Average order values were lower than food delivery at ₹450, but order frequency was higher—power users ordered 12-15 times monthly versus 8-10 for food delivery. The path to profitability required each store to process 500+ orders daily. By June 2024, only 30% of stores had achieved this threshold.

The Out-of-Home consumption business, comprising Dineout and SteppinOut acquisitions, operated on entirely different economics. This was a high-margin, asset-light business generating revenue through restaurant commissions on reservations (₹50-200 per cover) and event ticketing fees (5-10% of ticket value). The strategic value exceeded financial contribution—it provided data on dining patterns, relationships with premium restaurants, and a hedge against the commoditization of food delivery.

Platform Innovation, the catch-all category including Swiggy Genie and private labels, was essentially Swiggy's R&D department with revenue. Genie, the pickup-and-drop service, had negative unit economics but served as a customer acquisition tool and driver utilization optimizer. During lean hours, food delivery drivers could fulfill Genie orders, improving overall fleet economics. Private labels—Swiggy-branded products in Instamart—had 40% gross margins versus 15% for third-party products, but required inventory risk and quality control infrastructure.

The B2B Supply Chain vertical, serving restaurants with ingredients and supplies, was the least visible but potentially most strategic. By aggregating demand from thousands of restaurants, Swiggy could negotiate better prices from suppliers, passing some savings to restaurants while keeping a margin. This created stickiness—restaurants integrated into Swiggy's supply chain were less likely to switch to competitors. The unit economics were positive from day one, but growth was deliberately controlled to avoid channel conflict with restaurant partners.

The path to profitability was visible in the numbers: losses had reduced by 44% from ₹4,179 crore in FY23 to ₹2,350 crore in FY24. EBITDA margins for food delivery had improved to -1.9% in the first nine months of FY24, compared to -17.5% in FY23. The improvement came from multiple levers: platform fees adding 2% to margins, delivery charge optimization adding 1.5%, and reduced discounting adding 3%. Marketing efficiency had improved dramatically—customer acquisition cost had dropped from ₹450 in 2019 to ₹180 in 2024, while lifetime value had increased from ₹2,000 to ₹3,500.

The cash flow transformation was remarkable—Swiggy generated positive operating cash flow of ₹1,312 crore in FY24, compared to negative cash flow in previous years. This wasn't just accounting manipulation but genuine operational improvement. Working capital had turned negative in the food delivery business—Swiggy collected from customers immediately but paid restaurants weekly, creating a float that funded operations.

The membership model, Swiggy One, had become a critical economic driver. At ₹99 per month for unlimited free deliveries plus discounts, it seemed like a loss leader. But the math worked differently at scale. Swiggy One members ordered 3x more frequently than non-members. The increased order volume more than compensated for free delivery, while the subscription revenue provided predictable cash flow. By 2024, Swiggy One had 5 million subscribers generating ₹600 crore in annual subscription revenue with 90% retention rates.

The technology investments, often invisible in financial statements, drove operational leverage. The routing algorithm alone saved ₹15 per delivery through optimization. Demand prediction reduced food wastage in Instamart by 30%. Dynamic pricing during peak hours added 2% to margins without explicit surge pricing. Automated customer service handled 70% of queries, reducing support costs by ₹200 crore annually. These weren't one-time gains but compounding advantages that widened the moat against new entrants.

During the first nine months of FY24, Swiggy's gross order value stood at ₹24,230 crore, with food delivery comprising 76.2%. The GOV-to-revenue conversion rate of approximately 23% seemed low compared to global peers, but reflected India's price sensitivity. Unlike DoorDash or Uber Eats, which could charge 30%+ take rates, Swiggy operated in a market where ₹10 differences in delivery charges influenced customer choice. The business model had adapted to this reality through volume economics rather than margin optimization.

The capital allocation revealed strategic priorities. Of the ₹11,247 crore revenue in FY24, approximately ₹2,000 crore was reinvested in Instamart expansion, ₹800 crore in technology development, ₹600 crore in driver incentives and welfare, and ₹400 crore in new initiatives. This reinvestment rate of nearly 35% of revenue was high by mature company standards but necessary for market leadership. The question wasn't whether Swiggy could be profitable—food delivery had already proven that—but whether it could become profitable while continuing to grow at 30%+ rates.

The competitive benchmarking was inevitable and revealing. Zomato's food delivery business had achieved operational profitability, but Swiggy argued their investments in new verticals would yield higher long-term returns. The market would ultimately judge whether Swiggy's platform approach or Zomato's focused execution would prevail. But the unit economics suggested both could coexist profitably—the Indian market was large enough, and the duopoly structure enabled rational pricing.

By 2024, Swiggy had 112.73 million users who had transacted on its platform, each representing a relationship, a set of preferences, a lifetime value calculation. The business model had evolved from simple food delivery to a complex platform optimizing across multiple variables: customer acquisition cost versus lifetime value, order density versus geographic coverage, service quality versus operational cost, growth versus profitability. The spreadsheet that started this section, with its thousands of cells and complex formulas, was really a mathematical representation of urban India's convenience economy. And at ₹390 per share, public market investors were betting that Swiggy had solved the equation.

X. Playbook: Strategic Lessons

The whiteboard in Swiggy's strategy room has a simple diagram that encapsulates ten years of learning: three interlocking circles labeled "Demand," "Supply," and "Fulfillment," with "Swiggy" at the intersection. Every strategic decision, every pivot, every investment could be traced back to strengthening one of these circles or the connections between them. This wasn't unique insight—every marketplace understood this trinity. But Swiggy's playbook was different because they chose to own all three circles rather than just facilitate connections between them. That decision, made in a Koramangala apartment in 2014, cascaded into everything that followed.

The power of owning the full stack versus the marketplace model wasn't immediately obvious. In 2014, asset-light was gospel. Uber owned no cars. Airbnb owned no houses. Facebook created no content. The conventional wisdom said platforms should be pipes, not producers. But Majety and his co-founders had learned from Bundl's failure that in India's chaotic, fragmented market, control mattered more than capital efficiency. When you own the delivery fleet, you control quality. When you control quality, you build trust. When you build trust, you create habits. When you create habits, you own the customer relationship. It was a longer, more expensive path, but it created defensibility that pure marketplaces couldn't match.

Swiggy's dedicated delivery fleet, real-time tracking, and no minimum order requirements revolutionized food delivery in India. The "no minimum order" policy was particularly revealing. Competitors required ₹200-300 minimum orders to ensure viable economics. Swiggy accepted ₹50 orders for a single samosa, losing money on each transaction but building habituation. A customer who ordered a ₹50 samosa today would order a ₹500 family meal tomorrow. The lifetime value math justified the short-term loss, but only if you owned the fulfillment and could control the experience.

Network effects in three-sided marketplaces operate differently than in two-sided ones. In a traditional marketplace, more buyers attract more sellers and vice versa—a virtuous cycle. But in three-sided marketplaces with restaurants, customers, and delivery partners, the dynamics are more complex. More customers increase order volume, which attracts more delivery partners, which reduces delivery times, which attracts more restaurants, which increases variety, which attracts more customers. But the cycle can also work in reverse—too many delivery partners without sufficient orders leads to poor driver economics, causing churn, increasing delivery times, reducing customer satisfaction, leading restaurants to disable delivery. Swiggy learned to manage this delicate balance through dynamic incentives, surge pricing during peak hours, and guaranteed minimum earnings for drivers during off-peak times.

The importance of timing explained why Bundl failed but Swiggy succeeded. Bundl arrived in 2013 when smartphone penetration was under 10%, digital payments were virtually non-existent, and e-commerce was nascent. By 2014, just one year later, smartphones were reaching 15% penetration, growing rapidly. The ecosystem had reached a tipping point where convenience services could achieve critical mass. But timing wasn't just about market readiness—it was about competitive dynamics. Swiggy entered when food delivery was broken but not yet competitive. By the time Zomato and others arrived, Swiggy had established operational density that created genuine advantages. The lesson: being too early is the same as being wrong, but being first when the market is ready creates compounding advantages.

Capital as a moat in operationally intensive businesses was counterintuitive but real. In software businesses, capital provides limited advantage—a small team can build products that compete with giants. But in operations-heavy businesses like food delivery and quick commerce, capital creates genuine moats. Each dark store costs ₹50 lakhs to establish. Achieving city-wide coverage requires hundreds of stores. Driver acquisition and training costs thousands per person. Technology infrastructure requires continuous investment. A new entrant needs not just a better product but billions in capital to achieve competitive density. Swiggy's $3 billion in cumulative funding wasn't just growth capital—it was moat construction.

The platform expansion strategy revealed sophisticated thinking about when to add new verticals. The sequence mattered: food delivery first to build logistics infrastructure and customer relationships. Grocery delivery next to leverage the same infrastructure for adjacent use cases. Dineout to own the complete food journey. Genie to maximize fleet utilization. Each addition built on previous capabilities while adding new ones. The failed experiments—Swiggy Daily, Swiggy Stores—were valuable for what they revealed: subscription models for home food didn't work because variety mattered more than consistency. The successes—Instamart, Dineout—worked because they leveraged existing strengths while addressing genuine pain points.

The hyperlocal commerce thesis that Swiggy pioneered went beyond just delivery. Swiggy, known for pioneering hyperlocal commerce in India, operates through five main segments via its unified app. It was about creating a transaction layer for urban India where the digital and physical worlds merged. A restaurant wasn't just a kitchen but a node in a logistics network. A dark store wasn't just a warehouse but a forward deployment of inventory. A delivery partner wasn't just labor but a mobile sensor providing real-time data about demand patterns, traffic conditions, and consumer behavior. This systems thinking transformed operational challenges into data advantages.

The economics of density became Swiggy's core strategic insight. In low-density markets, unit economics never worked—delivery costs were too high, preparation times too variable, customer acquisition too expensive. But in high-density micro-markets, everything inverted. Delivery costs dropped through batching. Restaurants optimized operations for delivery. Word-of-mouth reduced marketing costs. Swiggy learned to identify and saturate these micro-markets—typically 2-3 square kilometer areas with high smartphone penetration, young demographics, and sufficient restaurant density. Only after achieving dominance in one micro-market would they expand to adjacent areas. This patient, systematic expansion took longer but created sustainable advantages.

The innovation framework that emerged from ten years of experimentation was surprisingly disciplined. Every new initiative had to pass three tests: Does it leverage existing capabilities? Does it expand the addressable market? Does it increase customer frequency or basket size? Instamart passed all three—it leveraged delivery infrastructure, expanded from restaurant food to groceries, and increased order frequency from 8 to 15 times monthly. Swiggy Daily failed all three—it required new capabilities (subscription management), addressed the same market (food consumers), and actually reduced order variety. This framework prevented the random diversification that killed many startups.