Mid-America Apartment Communities: The Sunbelt REIT Empire

I. Introduction & Episode Roadmap

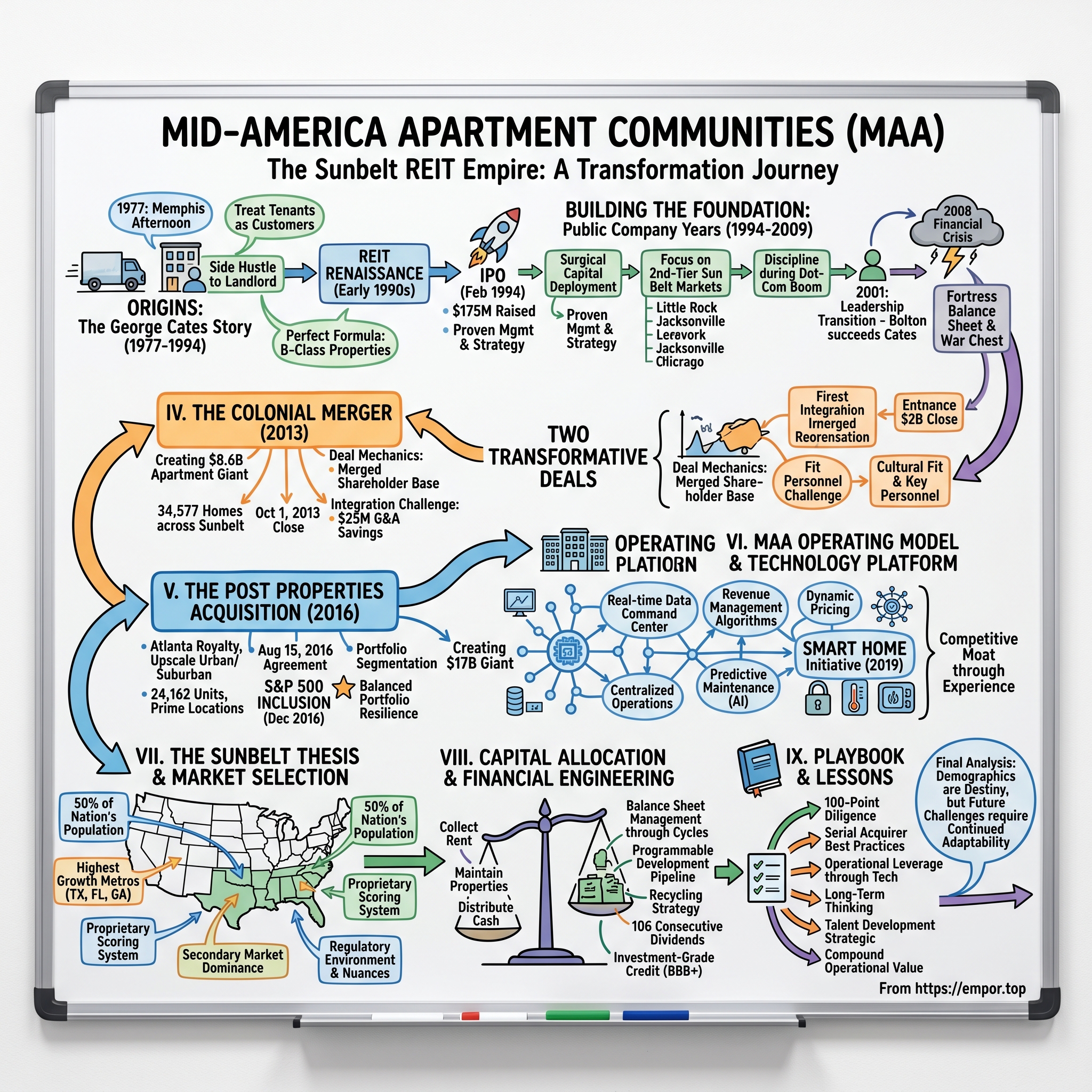

Picture this: It's a sweltering Memphis afternoon in 1977, and George Cates, a successful truck dealer with a side interest in real estate, is walking through one of his apartment properties. The tenants wave hello—they know him by name because he personally handles their maintenance requests when his property manager is overwhelmed. Fast forward to today, and that modest operation has morphed into Mid-America Apartment Communities, a $20 billion real estate empire that houses over 300,000 Americans across the Sunbelt. As of December 31, 2020, MAA owned 300 apartment communities containing 100,490 apartment units, making it the largest owner of apartments in the United States.

The transformation from truck dealer's side hustle to America's apartment landlord is not just a story of growth—it's a masterclass in timing markets, serial acquisitions, and operational excellence. This is the tale of how Southern hospitality met Wall Street sophistication, how a Memphis company bet on the Sunbelt before everyone else, and how patient capital allocation in the most boring corner of real estate—multifamily housing—created extraordinary wealth.

We'll explore three transformative deals that reshaped the company, unpack the Sunbelt thesis that drove its geographic strategy, and examine the operational playbook that turned commodity apartments into a differentiated business. Along the way, we'll discover how MAA pioneered revenue management systems, centralized operations across hundreds of properties, and built a technology platform that manages over 100,000 homes with stunning efficiency.

The questions we'll answer: How does a REIT execute multiple multi-billion dollar mergers without destroying value? What makes apartment ownership in Dallas different from Denver? And perhaps most importantly—in an industry where the product is essentially identical four walls and a roof, how do you build a sustainable competitive advantage?

II. Origins: The George Cates Story (1977-1994)

George E. Cates didn't set out to revolutionize American apartment ownership. In 1977, he was running a successful truck dealership in Memphis when he started buying small apartment complexes on the side. Memphis in the late '70s was experiencing a quiet transformation—FedEx had just moved its headquarters there in 1973, bringing with it a new class of young professionals who needed housing. Cates noticed something others missed: these workers wanted quality apartments, not just cheap ones.

The Memphis connection runs deeper than geography. Tennessee had no state income tax, making it attractive for businesses and workers alike. The city sat at the crossroads of major interstate highways, positioned perfectly between the established Northeast and the emerging Southwest. But most importantly, Memphis real estate was cheap—you could buy a 100-unit complex for what a 20-unit building cost in California. Cates understood that in real estate, you make your money when you buy, not when you sell.

For sixteen years, Cates operated in the shadows, methodically acquiring and improving properties throughout Tennessee and the broader Southeast. His philosophy was simple but revolutionary for the time: treat apartment living as a consumer service business, not just a real estate investment. While other landlords saw tenants as necessary evils, Cates saw customers. He invested in property amenities, insisted on responsive maintenance, and—unusually for the era—actually tracked resident satisfaction.

The private years from 1977 to 1993 were about perfecting the formula. Cates discovered that B-class properties—not luxury, not low-income, but solid middle-market apartments—generated the most consistent returns. These properties served teachers, nurses, young professionals, and empty nesters who valued location and quality but couldn't afford luxury high-rises. It was a massive, underserved market hiding in plain sight. In 1993, everything changed. The company was organized as a real estate investment trust, positioning itself to capitalize on the REIT renaissance of the early 1990s. The timing was perfect—real estate prices had crashed following the savings and loan crisis, creating once-in-a-generation buying opportunities. REITs, which had languished since their creation by Congress in 1960, suddenly became the vehicle of choice for recapitalizing distressed real estate. REITs were required by law to pay out at least 95 percent of their taxable income to shareholders each year, and with real estate of all stripes available at distressed prices in the early 1990s REITs finally became an attractive mainstream investment option.

The IPO decision came quickly. In February 1994, the company acquired The Cates Company from George E. Cates and became a public company via an initial public offering. He took the company public under the name Mid-America Apartment Communities, raising $175 million from shareholders. The offering was a watershed moment—not just for MAA but for the entire apartment REIT sector. Here was a company with a 17-year track record, proven management, and a focused strategy going public at precisely the moment when institutional capital was desperate for quality real estate exposure.

What made MAA different from the dozens of other REITs going public in 1993-1994? First, Cates had already built the infrastructure—property management systems, regional offices, maintenance protocols—that others would spend years developing. Second, the portfolio was already geographically diversified across multiple Southeast markets, reducing concentration risk. But most importantly, MAA had something intangible: a culture of operational excellence that treated apartment management as a hospitality business, not just a rent collection operation.

By the end of 1993 he employed 175 people to manage 22 properties in four states, in all containing some 5,600 apartments. These numbers might seem quaint compared to today's 100,000+ unit portfolio, but they represented something profound: proof that the model worked. Each property generated consistent cash flow, maintained high occupancy, and required minimal capital expenditure because they were well-maintained from day one. This operational discipline would become MAA's calling card as it entered the public markets, setting the stage for three decades of methodical expansion.

III. Building the Foundation: The Public Company Years (1994-2009)

The morning after MAA's IPO in February 1994, George Cates walked into the Memphis headquarters to find his phone ringing off the hook. Investment bankers, brokers, and property owners all wanted to know one thing: what was MAA buying next? The $175 million IPO proceeds were burning a hole in everyone's imagination—except Cates's. His first move as CEO of a public company was to do nothing. For six months, MAA didn't acquire a single property, focusing instead on integrating systems, training staff, and proving to Wall Street that it could deliver consistent quarterly results.

When MAA finally started deploying capital in late 1994, the strategy was surgical. Mid-America wasted little time in expanding its portfolio, concentrating on acquisitions in second-tier Sun Belt markets, such as Little Rock, Arkansas; Louisville, Kentucky; Jacksonville, Florida; Columbus, South Carolina; and Jackson, Mississippi. These weren't the glamorous markets that attracted headlines, but they had something more valuable: stable employment bases, limited new supply, and acquisition prices 30-50% below replacement cost.

The dot-com boom of the late 1990s tested MAA's discipline. While coastal REITs chased tech workers in San Francisco and Seattle, paying astronomical prices for properties, MAA stayed true to its knitting. The company continued buying in places like Chattanooga and Greenville—markets that barely registered on most investors' radars. When the tech bubble burst in 2000, MAA's "boring" portfolio suddenly looked brilliant. Occupancy remained above 94% even as coastal markets saw massive resident turnover and rent declines. But the real innovation during these years wasn't in acquisitions—it was in operations. MAA pioneered what would become industry standard practices: centralized purchasing, revenue management systems borrowed from the hotel industry, and standardized maintenance protocols. They were among the first apartment companies to invest heavily in technology, implementing online rent payments in 1999 when most property managers still collected paper checks.

The leadership transition that would define MAA's next chapter began taking shape in the late 1990s. E. Eric Bolton, Jr., a graduate of the University of Memphis with degrees in accounting and an MBA, had cut his teeth in Dallas with Trammell Crow Company, ultimately becoming CFO for Trammell Crow Asset Management. After several years in commercial banking, Bolton joined Mid-America soon after the REIT's IPO in 1994, and three years later was named the company's president and chief operating officer.

In 2001, 45-year-old Bolton succeeded George Cates as chief executive officer as part of a formal succession plan approved by the board of directors in 1997. The transition was seamless—Cates had been grooming Bolton for years, and the strategy remained consistent: focus on the Sunbelt, maintain operational excellence, and grow methodically. In September 2002 Bolton would also succeed Cates as Mid-America's chairman. Cates, who turned 65, retired, although he stayed on as a member of the board of directors.

The 2008 financial crisis would test Bolton's leadership and MAA's conservative approach. While other REITs struggled with over-leverage and development pipelines they couldn't finance, MAA entered the crisis with a fortress balance sheet and minimal development exposure. They didn't just survive—they prepared to thrive. As competitors retreated, MAA quietly assembled a war chest, knowing that the next few years would bring acquisition opportunities not seen since the early 1990s.In March 2009, founder George E. Cates retired, marking the end of an era but cementing his legacy as a visionary who saw the potential in Sunbelt apartments decades before it became conventional wisdom. The foundation he built—conservative leverage, operational excellence, and geographic focus—would prove its worth in the transformative deals that lay ahead.

IV. The Colonial Merger: Doubling Down on Sunbelt (2013)

The board meeting on June 3, 2013, lasted until midnight. Eric Bolton had just presented the most ambitious proposal in MAA's history: a merger with Colonial Properties Trust that would create an $8.6 billion apartment giant. Board members peppered him with questions about integration risk, cultural fit, and whether MAA was biting off more than it could chew. Colonial owned 34,577 apartment homes across the same Sunbelt markets MAA targeted—it was almost too perfect. That perfection made some directors nervous.

The post-financial crisis landscape had created a unique window. Capital was returning to real estate, but many REITs remained wounded from the 2008-2009 meltdown. Colonial Properties Trust, despite strong properties and recovering fundamentals, traded at a discount to replacement cost. Their first quarter 2013 results showed multifamily same-property net operating income up 6.8% and occupancy at 96.1%—impressive numbers that paradoxically made them more attractive as an acquisition target, not less. Strong operators with good portfolios but sub-scale platforms were exactly what MAA was hunting for.

MAA (NYSE: MAA) and Colonial Properties Trust (NYSE: CLP) announced that they had entered into a definitive merger agreement under which MAA and Colonial Properties Trust would merge, creating a Sunbelt-focused, publicly traded, multifamily REIT. The combined company was expected to have a pro forma equity market capitalization of approximately $5.1 billion and a total market capitalization of $8.6 billion.

The deal mechanics were elegant in their simplicity. As a result of the merger, each former Colonial Properties Trust common share was converted into 0.36 of a newly issued MAA common share. Former Colonial Properties Trust shareholders held approximately 44 percent of the combined company's equity, with continuing MAA shareholders holding approximately 56 percent. This wasn't a takeover—it was a true merger, with Colonial shareholders becoming significant owners in the combined entity.

On October 1, 2013, the deal closed. MAA and Colonial Properties Trust announced the completion of the merger of the two companies, forming a combined company with equity market capitalization of approximately $4.9 billion and a total market capitalization of approximately $8.3 billion. The final numbers were slightly lower than initial projections due to market movements, but the strategic logic remained compelling.

The integration challenge was immense. As of October 1, 2013, after giving effect to the merger, MAA owned or had ownership interest in approximately 85,000 apartment units. Overnight, MAA had nearly doubled in size. But Bolton's team had spent months preparing. They created integration teams for every function—property management, accounting, IT, human resources. The goal wasn't just to combine two companies but to capture synergies while preserving what made each organization successful.

Annual gross G&A savings were estimated to be approximately $25 million. These weren't just paper synergies. By eliminating duplicate corporate functions, consolidating vendor contracts, and implementing MAA's revenue management systems across Colonial's properties, the company could reduce costs while improving operations. Within 18 months, they exceeded the synergy targets.

The cultural integration proved smoother than many expected. Both companies shared Sunbelt DNA, understood the same resident demographics, and had similar operational philosophies. MAA retained key Colonial personnel, particularly those with deep local market knowledge. Edward T. Wright, former Executive Vice President of Multifamily Development for Colonial Properties Trust, served as Executive Vice President of Development and Capital Projects for the combined company. This wasn't conquest—it was combination.

What made the Colonial merger transformative wasn't just size but strategic positioning. The combined portfolio created density in key markets that neither company could achieve alone. In Atlanta, Dallas, and Charlotte, MAA now had sufficient scale to justify regional maintenance facilities, centralized leasing centers, and dedicated market research teams. Scale became a competitive weapon.

The market response validated the strategy. MAA's stock price rose steadily post-merger as investors recognized that the company had executed a complex integration while maintaining operational performance. Occupancy remained above 95% throughout the integration period, and same-store revenue growth accelerated as MAA's more sophisticated pricing algorithms were applied to Colonial's properties.

V. The Post Properties Acquisition: Creating a Giant (2016)

Three years after digesting Colonial, Eric Bolton stood before MAA's board in August 2016 with an even bolder proposition. Post Properties wasn't just another apartment REIT—it was Atlanta royalty, founded in 1970 by John A. Williams and Douglas Bates, with a portfolio of upscale urban and suburban communities that commanded premium rents. As of December 31, 2015, Post owned interests in 24,162 apartment units in 61 communities. These weren't MAA's traditional B-class properties; Post specialized in A-class assets in prime locations. The strategic question was whether MAA could integrate a fundamentally different product type without losing its operational focus.

The answer lay in market evolution. The Sunbelt wasn't just growing—it was maturing. Cities like Atlanta, Dallas, and Charlotte now had urban cores that rivaled coastal markets in sophistication and rental rates. Young professionals who once fled to New York or San Francisco were staying put, demanding the same quality apartments they would find in gateway cities. Post Properties had spent decades perfecting this urban/suburban luxury product. MAA needed that expertise to capture the high end of the market.

On August 15, 2016, MAA and Post Properties announced they had entered into a definitive merger agreement. The merger brings together two highly complementary multifamily portfolios with a combined asset base consisting of approximately 105,000 multifamily units in 317 properties. The combined company was expected to have a pro forma equity market capitalization of approximately $12 billion and a total market capitalization of approximately $17 billion.

Under the terms of the agreement, each share of Post common stock will be converted into 0.71 shares of newly issued MAA common stock. On a pro forma basis, following the merger, former MAA equity holders will hold approximately 67.7 percent of the combined company's equity, and former Post equity holders will hold approximately 32.3 percent.

The shareholder votes in November 2016 were overwhelming endorsements. Approximately 87% of the outstanding shares of MAA common stock voted at the MAA special meeting, with approximately 99% of the votes cast in favor of the merger. Post Properties shareholders showed similar enthusiasm, with approximately 88% of outstanding shares voting and 99% approving the deal.

On December 1, 2016, the merger closed. MAA and Post Properties announced the completion of the merger of the two companies, forming a combined company with equity market capitalization of approximately $11 billion and a total market capitalization of approximately $15 billion. The market capitalization came in slightly below initial projections, but the strategic value was immense.

Annual gross overhead synergies are estimated to be approximately $20 million. The combined company is expected to benefit from the elimination of duplicative costs associated with supporting a public company platform. But the real value wasn't in cost cuts—it was in revenue enhancement. Post's sophisticated amenity packages, concierge services, and premium positioning could be selectively applied across MAA's portfolio, driving rent growth without massive capital investment.

The integration challenge this time was cultural as much as operational. Post Properties had cultivated an upscale brand identity—their properties featured resort-style pools, high-end fitness centers, and concierge services. MAA's properties, while well-maintained, were more utilitarian. The solution was portfolio segmentation: maintain Post's luxury positioning in urban cores while applying MAA's operational efficiency to Post's suburban assets.

David P. Stockert, former President and CEO of Post Properties, joined MAA's board, bringing institutional knowledge and relationships. This wasn't a hostile takeover but a negotiated combination that preserved the best of both companies. The integration teams learned from the Colonial experience, moving faster on systems integration while being more deliberate about brand positioning.

The Post merger had an unexpected benefit: S&P 500 inclusion. In December 2016, the company acquired Post Properties and was added to the S&P 500 Index. This wasn't just a symbolic achievement. S&P 500 inclusion meant automatic buying from index funds, lower cost of capital, and validation as a blue-chip REIT. The company that started as a Memphis truck dealer's side project was now in the same index as Apple and Microsoft.

What made the Post acquisition transformative was portfolio balance. MAA now owned everything from workforce housing in secondary markets to luxury high-rises in Atlanta. This diversification provided resilience—when luxury markets softened, B-class properties picked up the slack. When secondary markets struggled with new supply, urban properties outperformed. The combined company's ten largest markets by unit count became Atlanta, Dallas, Austin, Charlotte, Raleigh, Orlando, Tampa, Fort Worth, Houston and Washington, DC—a who's who of Sunbelt growth markets.

VI. The MAA Operating Model & Technology Platform

Walk into MAA's command center in Memphis on any given morning, and you'll find a scene that looks more like a tech company than a traditional property manager. Dozens of screens display real-time data from over 100,000 apartments: occupancy rates, maintenance requests, prospect traffic, even weather patterns that might affect leasing activity. This is the nerve center of what MAA calls its "Full-Cycle" investment philosophy—a comprehensive approach to creating value at every stage of an asset's life.

The revenue management revolution at MAA began in earnest in 2010, when the company hired data scientists from the airline industry. The insight was simple but powerful: apartments, like airline seats, are perishable inventory. Every day a unit sits vacant is revenue lost forever. MAA built dynamic pricing algorithms that adjusted rents daily based on supply, demand, seasonality, and competitive positioning. A one-bedroom apartment in Atlanta might be priced at $1,400 on Monday and $1,425 by Friday if web traffic and tour schedules indicated strengthening demand.

But technology without human insight is just expensive software. MAA's innovation was combining algorithmic pricing with local market knowledge. The system might recommend a rent increase, but regional managers could override it based on factors the algorithm couldn't see: a new employer moving to town, a competitor's property under renovation, or subtle shifts in resident preferences. This hybrid approach consistently generated 50-100 basis points of additional revenue growth compared to pure algorithmic or pure human decision-making.

The centralized operations model, refined over two decades, is a masterclass in efficiency. Instead of each property having its own accounting, marketing, and IT support, MAA centralized these functions in Memphis and regional hubs. A maintenance request submitted via the MAA app at 10 PM in Orlando gets routed to the 24-hour command center, prioritized by urgency, assigned to the appropriate technician, and scheduled for the next morning—all without anyone at the local property being involved.

This centralization extends to procurement. MAA's scale—over 100,000 units—gives it enormous purchasing power. The company negotiates national contracts for everything from appliances to insurance, achieving cost savings of 15-20% compared to property-by-property purchasing. But they learned not to over-centralize. Paint colors, landscaping choices, and amenity offerings remain locally determined because resident preferences vary significantly between markets.

The technology platform MAA built isn't just about efficiency—it's about resident experience. The MAA resident app, launched in 2018 and continuously updated, handles everything from lease signing to maintenance requests to package notifications. Residents can pay rent, reserve amenities, communicate with neighbors, and even order services like dog walking or dry cleaning. The app has become so integral that properties with higher app adoption rates show 2-3% better retention.

Predictive maintenance represents the next frontier. MAA's systems now track the age and usage patterns of every major appliance and system across the portfolio. The AI predicts when an HVAC unit will likely fail, scheduling preventive maintenance before residents experience problems. This proactive approach reduced emergency maintenance calls by 30% and improved resident satisfaction scores significantly.

The "Smart Home" initiative, rolled out beginning in 2019, equipped units with smart thermostats, locks, and leak detectors. Beyond the resident benefits, these devices provide MAA with unprecedented operational intelligence. Smart thermostats reduce energy costs and prevent HVAC damage from extreme settings. Smart locks eliminate the cost and security risk of physical keys. Leak detectors prevent water damage that can cost tens of thousands to remediate.

Cost discipline permeates the organization but not at the expense of quality. MAA discovered that spending slightly more on quality materials—better carpet, more durable appliances, premium paint—actually reduced total cost over time through longer replacement cycles and fewer maintenance calls. They call it "value engineering": optimizing the total cost of ownership rather than minimizing initial expense.

The human element remains crucial despite all the technology. MAA invests heavily in training, with new property managers spending two weeks in Memphis learning not just systems but philosophy. The company promotes from within whenever possible, creating career paths from leasing agent to regional manager. This investment in people shows in the numbers: MAA's employee turnover is 40% below industry average, and properties with longer-tenured staff consistently outperform on every operational metric.

Perhaps most impressively, MAA has made this complex operation appear simple to residents. The average resident never sees the sophisticated systems running behind the scenes. They just experience an apartment community that works: maintenance issues resolved quickly, rent payments processed seamlessly, and staff who seem to genuinely care about their satisfaction. This operational excellence, scaled across 100,000+ units, creates a competitive moat that's nearly impossible for smaller operators to replicate.

VII. The Sunbelt Thesis & Market Selection

In 1977, when George Cates started buying apartments in Memphis, the term "Sunbelt" had only recently entered the American lexicon. Political analyst Kevin Phillips coined it in his 1969 book "The Emerging Republican Majority," predicting a massive demographic shift from the Rust Belt to the southern third of the nation. Cates didn't need academic analysis to see what was happening—he could watch the FedEx planes landing in Memphis, bringing jobs and young workers who needed housing. That early observation would become the foundation of MAA's geographic strategy for the next five decades.

The Sunbelt thesis rests on demographics so powerful they seem almost gravitational. According to a 2019 Legg Mason report, the region has approximately 50% of the nation's population and is poised to grow to 55% by 2030. Houston had the largest population jump of approximately 19%, followed by over 18% in Dallas, both more than triple the national population growth rate of roughly 6% during that time period, according to Census data. These aren't marginal shifts—they're tectonic movements of American population and economic activity.

MAA's market selection criteria evolved from simple intuition to sophisticated analysis. The company developed a proprietary scoring system that evaluates markets on multiple dimensions: job growth diversity (not just total growth but sector balance), in-migration patterns, housing affordability relative to incomes, supply constraints, and regulatory environment. A market like Austin might score high on job growth but face challenges from oversupply. Charlotte might have more moderate growth but better supply-demand balance. The art is in portfolio construction that balances these trade-offs.

The secondary market strategy deserves special attention. While competitors fought over Dallas and Atlanta, MAA quietly built dominant positions in markets like Charleston, Greenville, and Chattanooga. These cities, with populations between 200,000 and 800,000, offered several advantages: less institutional competition, more stable resident bases, and surprisingly strong demographics. A Google engineer in Mountain View might pay $3,500 for a one-bedroom; their counterpart working remotely from Greenville might pay $1,400 for a two-bedroom with amenities.

The top 10 destinations for absolute population growth over the last year are all Sun Belt metros. Four are in Texas: Dallas-Fort Worth (#1), Houston (#2), Austin (#6), and San Antonio (#9). Three are in Florida: Orlando (#5), Tampa (#7), and Jacksonville (#10). Third-ranked Atlanta, Georgia; fourth-ranked Phoenix, Arizona; and eighth-ranked Charlotte, North Carolina, round out the list. This concentration creates network effects—as more people move to these metros, they become more attractive to employers, which attracts more people, creating a virtuous cycle.

The urban versus suburban balance became increasingly important post-2020. America's movement from core to suburban cities continued as well. Within the 50 largest metros, the total population living in core urban counties rose only very slightly last year after falling sharply from 2020 to 2021. Suburban counties in the top 50 metros, meantime, grew almost as fast as they did the prior year. MAA's portfolio, with its mix of urban and suburban properties acquired through the Colonial and Post mergers, was perfectly positioned for this shift.

Weather matters more than northerners want to admit. The Sun Belt has seen substantial population growth post-World War II from an influx of people seeking a warm and sunny climate, a surge in retiring baby boomers, and growing economic opportunities. The advent of air conditioning created more comfortable summer conditions and allowed more manufacturing and industry to locate in the Sun Belt. But it's not just about temperature—it's about lifestyle. The ability to be outdoors year-round, lower heating costs, and reduced weather-related maintenance all contribute to both resident satisfaction and operational efficiency.

The economic drivers go beyond population growth. The oil industry helped propel states such as Texas and Louisiana forward, and tourism grew in Florida, and Southern California. More recently, high tech and new economy industries have been major drivers of growth in California, Florida, Texas, and other parts of the Sun Belt. This economic diversification is crucial—MAA learned from Houston's 1980s oil bust that single-industry dependence is dangerous, no matter how strong that industry appears.

Competition in Sunbelt markets has intensified, but MAA's early entry provides advantages. In many secondary markets, MAA owns the best-located properties, acquired when land was cheap. New competitors must build on inferior sites or pay premium prices for land. MAA's local market knowledge, accumulated over decades, helps identify micro-markets where supply-demand dynamics differ from the broader metro area.

The regulatory environment in Sunbelt states generally favors development and property rights, but MAA has learned to navigate the variations. Texas has no state income tax but higher property taxes. Florida has homestead exemptions that can affect resident mobility. Georgia has landlord-friendly eviction laws but Atlanta has considered rent control. Understanding these nuances and their impact on operations is crucial for maintaining margins.

Looking ahead, the Sunbelt thesis faces challenges. In top Sunbelt cities like Austin, rents dropped by more than 5% in 2024. Other Sunbelt cities haven't fared as poorly, but the supply of multifamily units has yet to be absorbed by the market. Climate change poses long-term questions about the sustainability of growth in water-stressed areas. Political polarization might affect migration patterns. But the fundamental drivers—job growth, affordability, lifestyle preferences—remain intact. MAA's geographic concentration, once seen as a risk, now looks like prescient positioning for where America is moving.

VIII. Capital Allocation & Financial Engineering

The REIT structure is both a blessing and a curse. By law, REITs must distribute at least 90% of taxable income to shareholders as dividends (the requirement was 95% when MAA went public). This creates a reliable income stream for investors but severely limits internal capital generation. Every major acquisition, every development project, every significant renovation requires accessing external capital markets. For MAA's management, this constraint became a discipline that would define their approach to capital allocation.

Eric Bolton often describes MAA's capital allocation philosophy as "boring on purpose." While tech companies chase moonshots and retailers reinvent themselves every few years, MAA does essentially the same thing every quarter: collect rent, maintain properties, and distribute cash to shareholders. The magic is in the optimization of this seemingly simple model. Every basis point of improved occupancy, every dollar of expense saved, every slight improvement in resident retention flows directly to the bottom line and into shareholders' pockets.

The balance sheet management through cycles reveals MAA's financial sophistication. Heading into the 2008 financial crisis, MAA had one of the lowest leverage ratios in the REIT sector—debt to total capitalization below 40%. This wasn't luck or excessive conservatism; it was deliberate preparation. Management had studied previous real estate cycles and understood that access to capital, not asset quality, determines survival in downturns. When credit markets froze, MAA could still function. When competitors needed to sell assets at distressed prices, MAA was buying.

The development versus acquisition trade-off is perpetually debated in MAA's boardroom. Development offers higher returns—building a 300-unit complex might generate 150-200 basis points of additional yield versus buying a similar property. But development carries execution risk, market timing risk, and massive capital commitment. MAA's solution is programmatic: maintain a modest development pipeline of 2-3% of total assets, focusing on markets they know intimately, and only build when construction costs make sense relative to acquisition prices.

The recycling strategy—selling assets to fund growth—is where MAA's discipline shines. Every year, the company evaluates its bottom quartile of properties. These might be older assets requiring significant capital investment, properties in markets losing momentum, or simply assets where MAA has maximized value. By selling 1-2% of the portfolio annually at premium valuations and redeploying proceeds into higher-growth opportunities, MAA maintains portfolio quality while self-funding growth. The dividend story is remarkable for its consistency. MAA has paid 106 consecutive quarterly common dividends and delivered a long-term return to shareholders that has consistently ranked in the top-tier of performances within the overall REIT sector. MAA currently pays investors $6.06 per share annually, or approximately 4.00% yield. The company increased its dividend 7 times in the past 5 years, and its payout has grown 10.7% over the same time period. This isn't just returning capital—it's compound growth that rivals many growth stocks while providing current income.

Cost of capital advantages at scale manifest in multiple ways. MAA's investment-grade credit rating (BBB+ from S&P) means it can borrow at rates 100-150 basis points below non-investment grade REITs. When acquiring a $200 million property portfolio, that difference translates to $2-3 million in annual interest savings—pure profit that drops to the bottom line. The company maintains a well-laddered debt maturity schedule, never having more than 15% of debt maturing in any single year, which prevents refinancing crunches.

The equity capital markets strategy is equally sophisticated. MAA uses its at-the-market (ATM) equity program to raise capital opportunistically. When the stock trades above net asset value (NAV), management can issue shares accretively, using proceeds to fund acquisitions or development. When shares trade below NAV, they pause equity issuance and rely more on asset sales and debt financing. This dynamic approach prevents dilution while maintaining growth momentum.

Financial engineering at MAA isn't about complex derivatives or aggressive accounting—it's about optimization within the REIT framework. The company structures joint ventures for development projects, limiting capital exposure while maintaining operational control. They use tax-deferred 1031 exchanges when recycling assets, preserving capital for reinvestment. Even something as mundane as property insurance is financially engineered, with MAA self-insuring for smaller claims to reduce premiums while maintaining catastrophic coverage.

The FFO (Funds From Operations) and AFFO (Adjusted Funds From Operations) metrics that REITs report deserve attention. FFO adds back depreciation to net income, recognizing that real estate often appreciates rather than depreciates. AFFO goes further, subtracting recurring capital expenditures to show true cash generation. MAA's AFFO per share has grown at a 7-8% compound rate over the past decade—remarkable consistency for a real estate company through multiple cycles.

What distinguishes MAA's capital allocation is the long-term perspective. While quarterly earnings calls focus on occupancy rates and same-store revenue growth, management thinks in decades. The Post Properties acquisition in 2016 diluted near-term FFO but positioned MAA for the urban-to-suburban shift that accelerated during COVID. Development projects with 5-7 year horizons get approved based on demographic trends, not current market conditions.

The balance between growth and income defines the REIT investor base, and MAA has carefully cultivated both constituencies. Growth investors appreciate the 7-8% annual FFO growth and expansion opportunities. Income investors value the 4% dividend yield and consistent payout growth. This dual appeal creates a more stable shareholder base, reducing stock volatility and lowering the cost of equity capital.

Risk management permeates every capital decision. MAA maintains significant liquidity through an undrawn credit facility, typically $500 million or more. They hedge interest rate exposure on floating-rate debt. Geographic and property-type diversification reduces concentration risk. Even the dividend policy—targeting 70% of AFFO—leaves cushion for downturns while returning substantial cash to shareholders.

IX. Playbook: Lessons in REIT Excellence

The conference room in MAA's Memphis headquarters has witnessed dozens of acquisition negotiations over the decades. The playbook that emerged from these deals—refined through trial, error, and eventual mastery—offers lessons that extend far beyond real estate. When MAA evaluates an acquisition target, they follow a 100-point diligence checklist developed over 30 years, covering everything from environmental assessments to employee benefit plan liabilities. But the real insight is knowing which 10 points actually matter.

Serial acquirer best practices start with cultural assessment. Before MAA even looks at financial statements, they evaluate cultural fit. Will the target's property managers embrace MAA's customer service philosophy? Can their maintenance teams adapt to MAA's preventive maintenance protocols? The Colonial and Post mergers succeeded partly because both companies shared similar values around resident service and operational excellence. When culture aligns, integration friction decreases dramatically.

The integration playbook reads like a military operation. Day 1: Announce retention bonuses for key personnel, implement MAA's accounting systems, and begin property inspections. Week 1: Conduct all-hands meetings at every property, explaining what changes and what doesn't. Month 1: Implement revenue management systems, renegotiate vendor contracts, and standardize operating procedures. Month 3: Fully integrated into MAA's platform, generating targeted synergies. This systematic approach reduces uncertainty and accelerates value creation.

Operational leverage through technology isn't about replacing people—it's about amplifying their effectiveness. A MAA property manager oversees 20% more units than the industry average, not because they work harder but because technology handles routine tasks. Automated rent collection, AI-powered maintenance scheduling, and centralized accounting free property staff to focus on resident relationships and property improvement. Technology becomes a force multiplier, not a replacement.

Building a moat in a commoditized industry requires thinking differently about competition. Apartments are fundamentally similar—four walls, appliances, parking. MAA's moat isn't the physical product but the entire resident experience. Their renewal rate consistently exceeds 55%, well above the 50% industry average. Each renewal saves $2,000-3,000 in turnover costs and vacancy loss. Multiply that by 50,000+ renewals annually, and resident retention becomes a $100+ million annual competitive advantage.

Long-term thinking in a quarterly earnings world creates opportunities others miss. When COVID hit in March 2020, many REITs slashed spending and froze hiring. MAA accelerated technology investments and selectively acquired distressed properties. They understood that the pandemic would eventually end, but the operational improvements and strategic acquisitions would provide benefits for decades. This countercyclical thinking—investing when others retreat—has defined MAA's most successful moves.

The power of geographic focus becomes evident in market downturns. When Austin's tech market cooled in 2023, MAA could shift leasing staff from Austin to still-hot markets like Orlando and Raleigh. Properties in oversupplied submarkets could offer concessions while those in tight markets pushed rents. This portfolio balance—impossible for single-market operators—smooths performance across cycles. Geographic diversity within the Sunbelt provides resilience without sacrificing the demographic tailwinds.

Creating value through operations, not financial engineering, represents a philosophical choice. While some REITs chase yield through aggressive leverage or complex structures, MAA focuses on blocking and tackling: improving occupancy by 50 basis points, reducing turnover by 2%, cutting maintenance costs by 3%. These incremental improvements, compounded across 100,000+ units over years, create enormous value. It's boring, it's methodical, and it works.

The technology adoption curve in real estate typically lags other industries by 5-10 years. MAA flips this disadvantage into opportunity by being an early adopter in a late-adopting industry. They were among the first to implement revenue management, centralized operations, and smart home technology. Being first provides learning advantages—by the time competitors adopt similar systems, MAA has already optimized them and moved on to the next innovation.

Talent development might seem incongruous with apartments, but MAA treats it as strategic. They hire MBAs for property management roles, knowing that smart, ambitious people will find ways to improve operations. Their management training program is legendary in the industry—a two-year rotation through every department. Alumni of this program now run properties, regions, and competing REITs. This investment in human capital creates institutional knowledge that can't be replicated through acquisition.

The vendor ecosystem MAA has cultivated deserves recognition. Rather than squeezing suppliers for every penny, MAA partners with key vendors on multi-year contracts with performance incentives. The maintenance contractor who reduces service calls gets a bonus. The landscaping company that improves property ratings shares in the upside. This alignment creates a network effect where everyone—residents, employees, vendors, and shareholders—benefits from operational improvement.

Perhaps the most important lesson is patience. MAA didn't become America's largest apartment owner through grand gestures but through thousands of small, correct decisions compounded over decades. They bought the right properties in the right markets at the right prices. They maintained them meticulously. They treated residents fairly. They returned cash to shareholders consistently. In an era of disruption and transformation, MAA proves that sometimes the best strategy is simply doing the obvious things extraordinarily well.

X. Analysis: Bull vs. Bear Case

The bull case for MAA begins with demographics so powerful they border on destiny. The Sunbelt's population growth isn't slowing—if anything, it's accelerating as remote work untethers knowledge workers from expensive coastal cities. Millennials, the largest generation in American history, are entering prime household formation years. Gen Z follows close behind. Meanwhile, housing affordability has pushed homeownership out of reach for millions, creating permanent renters who might have bought homes in previous generations. MAA sits at the intersection of all these trends.

Scale advantages compound in ways that aren't immediately obvious. MAA's 100,000+ units provide negotiating leverage with national vendors—insurance companies, appliance manufacturers, maintenance providers. But scale also enables technology investments that smaller operators can't justify. The $50 million MAA spends on proprietary revenue management systems would bankrupt a 5,000-unit operator. Spread across 100,000 units, it's $500 per unit—recovered through 0.5% better pricing. These scale economics create a widening moat.

Operational excellence isn't a buzzword at MAA—it's measurable. Same-store operating margins consistently rank in the top quartile among public apartment REITs. Maintenance costs per unit are 10-15% below peer average. Employee turnover is 40% lower than industry benchmarks. These aren't accidents or temporary advantages—they're the result of decades of process refinement, technology investment, and cultural development. Operational excellence becomes self-reinforcing as best practices spread across the portfolio.

The technology platform MAA has built represents tens of millions in investment and decades of refinement. A competitor starting today would need to spend similar amounts just to reach parity, with no guarantee of success. Meanwhile, MAA continues investing, pulling further ahead. The platform handles everything from prospect management to predictive maintenance to financial reporting. It's not one system but dozens, all integrated, all optimized, all improving. Technology creates competitive advantage that compounds over time.

But the bear case has merit, starting with interest rate sensitivity. REITs are bond proxies for many investors—when treasury yields rise, REIT valuations typically fall. MAA's 4% dividend yield looks less attractive when risk-free treasuries yield 5%. Rising rates also increase borrowing costs, reducing development returns and acquisition NOI yields. While MAA has managed through multiple rate cycles, the current environment of structurally higher rates could pressure valuations for years.

New supply concerns are real and mounting. In top Sunbelt cities like Austin, rents dropped by more than 5% in 2024. Other Sunbelt cities haven't fared as poorly, but the supply of multifamily units has yet to be absorbed by the market. The development pipeline, while moderating, remains elevated by historical standards. Supply and demand imbalances can persist for years, pressuring rents and occupancy even in growing markets.

The affordability crisis presents both opportunity and threat. Rents have grown faster than incomes for a decade, pushing affordability to breaking points in many markets. Resident rent-to-income ratios above 30% historically predict higher turnover and payment delinquencies. Political pressure for rent control grows with each election cycle. While MAA has avoided rent-controlled markets, the political winds could shift, especially in purple states like Georgia and Arizona.

Single-family rental competition has emerged as a serious threat. Institutional investors like Invitation Homes and American Homes 4 Rent have assembled portfolios of hundreds of thousands of single-family rentals. These homes offer more space, privacy, and often better school districts than apartments. For families—a key MAA demographic—single-family rentals provide a compelling alternative. Build-to-rent communities blur the line further between multifamily and single-family living.

Regulatory risks multiply across MAA's footprint. Eviction moratoriums during COVID showed how quickly property rights can be suspended. Source-of-income discrimination laws force acceptance of Section 8 vouchers. Fair housing regulations grow more complex annually. Environmental regulations around energy efficiency and water usage add costs. While these affect all landlords, institutional owners like MAA face greater scrutiny and enforcement.

Technology disruption could come from unexpected directions. Airbnb and short-term rentals compete for residents in some markets. Co-living startups target young professionals with flexible, furnished options. PropTech companies that promise to revolutionize property management receive billions in venture funding. While MAA has proven adaptable, the next disruption might move faster than a traditional REIT can respond.

Competitive threats from other REITs continue intensifying. Camden Property Trust, AvalonBay Communities, and Equity Residential all target similar markets and demographics. Private equity firms raise massive funds to buy apartments, competing for acquisitions and accepting lower returns. International capital sees U.S. apartments as safe havens, driving up prices. The easy acquisitions are gone—every deal now faces multiple bidders.

The balanced view acknowledges both narratives have validity. MAA's strengths—scale, operational excellence, geographic positioning—are real and durable. But the challenges—supply, affordability, competition—are equally real. The question isn't whether MAA will face headwinds but whether their advantages outweigh the challenges. History suggests betting against MAA has been a losing proposition, but past performance doesn't guarantee future results.

XI. Looking Forward: The Next Chapter

Standing in MAA's newest development site in Charleston, South Carolina, in June 2025, you can feel the company's confidence in the future. MAA closed on the acquisition of a land parcel located in Charleston, South Carolina through our pre-purchase development program and began construction on a 336-unit multifamily apartment community. This isn't just another apartment complex—it's a bet on the continued migration to quality-of-life markets, the permanence of remote work, and the enduring appeal of the Sunbelt lifestyle.

The current portfolio tells a story of methodical expansion and strategic focus. As of June 30, 2025, MAA had ownership interest in 104,347 apartment units, including communities currently in development, across 16 states and the District of Columbia. The slight variation from the March 31, 2025 count of 104,011 units reflects both new development coming online and strategic dispositions—a constant rebalancing to maintain portfolio quality.

The strengthening demand/supply dynamic coupled with our growing development pipeline, which is nearing $1 billion, should support robust revenue and earnings performance and enhance long-term value creation. This billion-dollar development commitment represents a significant acceleration from historical levels, reflecting management's confidence in long-term fundamentals despite near-term supply challenges. The company is positioning for the supply trough expected in 2026-2027, when today's development starts will deliver into a market with minimal new competition.

ESG initiatives have evolved from compliance checkbox to competitive advantage. 62% of its portfolio is updated to all LED lighting, and the company has 31 green-certified communities. These aren't just feel-good initiatives—LED lighting reduces operating costs by $200-300 per unit annually while improving resident satisfaction. Water conservation systems, installed across the portfolio, have reduced consumption by 15% even as occupancy increased. Solar panels on select properties provide both green credentials and electricity cost hedging.

The sustainability push extends beyond environmental concerns. MAA's social initiatives include workforce housing preservation—maintaining affordability in B-class properties even as markets gentrify. The company's Open Arms Foundation, MAA's corporate charity, provides emergency assistance to residents facing temporary financial hardship. These programs build community loyalty that translates into higher retention and lower turnover costs.

The housing affordability challenge looms as both threat and opportunity. Median home prices in MAA's markets have increased 40-60% since 2020, while mortgage rates have more than doubled. This mathematical impossibility of homeownership for many creates a generation of permanent renters. MAA's response has been segmentation: luxury properties for those who choose to rent, workforce housing for those who must rent, and everything in between.

The new development pipeline reveals strategic priorities. Charleston, Charlotte, and Raleigh dominate the development map—secondary markets with primary market demographics. These aren't speculative bets but calculated investments in markets with diverse employment, limited supply constraints, and favorable regulatory environments. Each development undergoes rigorous underwriting assuming higher interest rates, construction cost inflation, and conservative rent growth.

Technology roadmap ambitions extend far beyond current capabilities. MAA is piloting AI-powered leasing agents that can tour properties virtually, answer questions, and even negotiate lease terms within parameters. Predictive analytics identify residents likely to move out three months before they give notice, enabling proactive retention efforts. Automated underwriting approves qualified applicants in minutes, not days. These aren't far-off dreams but active pilots with planned portfolio-wide rollouts.

It has installed Smart Home technology (unit entry locks, mobile control of lights and thermostat, and leak monitoring) in 93,000 units across its portfolio. The next phase includes AI-powered energy optimization that learns resident patterns and adjusts systems automatically, potentially saving 20-30% on utility costs. Package management systems using automated lockers and drone delivery compatibility are being tested. The apartment of 2030 will be fundamentally different from today's, and MAA intends to define that difference.

Management transition represents both risk and opportunity. While Eric Bolton transitioned to Executive Chairman in April 2025 with Brad Hill becoming CEO, the strategic direction remains consistent. Hill, who joined MAA in 2010 and previously served as President and Chief Investment Officer, represents continuity with fresh perspective. His background in transactions and development positions MAA well for the next phase of growth.

Potential M&A opportunities exist despite the massive consolidation already achieved. Smaller REITs struggling with technology investment requirements and operational complexity become attractive targets. Private portfolios facing refinancing challenges in a higher-rate environment might seek MAA's balance sheet strength. The company has the scale and expertise to absorb 10,000-20,000 unit portfolios without integration strain.

As of June 30, 2025, resident turnover in the Same Store Portfolio remained historically low at 41.0% with a record low level of move-outs associated with buying single family-homes of 11.0%. This data point reveals a fundamental shift: residents aren't moving out to buy homes because they can't afford to. The American Dream of homeownership, at least temporarily, has become the American Reality of renting. For MAA, this societal shift provides a tailwind that could last a generation.

Looking ahead, MAA faces a paradox: never have the long-term fundamentals been stronger, yet never have the near-term challenges been more complex. Supply overhangs will pressure rents through 2025. Political pressure for affordability measures will intensify. Technology disruption will accelerate. But MAA has navigated every previous challenge through a combination of operational excellence, strategic positioning, and patient capital allocation. The truck dealer's side project has become America's apartment empire, and the next chapter is just beginning to be written.

XII. Links & Resources

For those seeking to delve deeper into MAA's story, the company maintains comprehensive investor relations materials at ir.maac.com. Quarterly earnings presentations provide management's unfiltered view of market conditions, while SEC filings offer the granular detail that serious analysts require. The annual 10-K filing, typically exceeding 200 pages, contains everything from property-by-property listings to detailed risk disclosures that reveal management's deepest concerns.

Industry research from Green Street Advisors and CBRE provides essential context for understanding apartment market dynamics. The National Multifamily Housing Council's quarterly surveys track industry sentiment, while academic papers from MIT's Center for Real Estate and the Urban Land Institute explore longer-term trends affecting multifamily housing. The Journal of Real Estate Finance and Economics regularly publishes peer-reviewed research on REIT performance and valuation methodologies.

Books like Sam Zell's "Am I Being Too Subtle?" offer insights into the real estate mogul mindset that shaped the modern REIT industry. "The Perfect Investment" by Paul Moore provides a compelling case for multifamily investing that explains why institutional capital continues flowing into the sector. For those interested in the mechanics of REIT investing, Ralph Block's "Investing in REITs" remains the definitive primer despite being published years ago.

Podcast appearances by MAA executives on platforms like The Walker Webcast and NAREIT's REIT Report provide more conversational insights than formal earnings calls. Brad Hill's discussions about operational excellence and Eric Bolton's perspectives on capital allocation reveal the thinking behind MAA's strategic decisions. Industry conferences like REITWorld and the ULI Fall Meeting often feature MAA executives discussing broader market trends.

Historical coverage of MAA's transformative deals in publications like The Wall Street Journal and Commercial Property Executive captures the market sentiment at crucial moments. The skepticism around the Colonial merger in 2013 and enthusiasm for the Post acquisition in 2016 provide lessons in how market perception can differ from ultimate outcomes.

XIII. Recent News & Developments

The latest developments paint a picture of resilience amid challenging conditions. MAA reported Q2 Core FFO of $2.15 per share, surpassing forecasts, with President and CEO Brad Hill noting that "Second quarter Core FFO results exceeded our expectations" and highlighting "record demand for rental housing that persists in our markets, leading to second quarter blended lease performance 40 bps higher than last year" delivered through "record resident retention and robust renewal pricing, resulting in strong occupancy and a 100 bps sequential improvement in Same Store blended pricing."

Resident turnover in the Same Store Portfolio hit a record low of 41.0%, with move-outs tied to home purchases at 11.0%—a sign of sustained rental demand despite broader affordability challenges. This data reinforces the thesis that homeownership affordability has created a generation of renters by necessity, not choice.

The development pipeline continues expanding aggressively. MAA has 8 communities under development with total expected costs of $942.5 million, plus 6 lease-up communities with costs to date of $573.9 million. In June 2025, MAA closed on the acquisition of a land parcel in Charleston, SC, through its pre-purchase development program and started construction on a 336-unit multifamily apartment community.

Management transitions have proceeded smoothly. MAA announced the appointment of A. Bradley Hill (48) as its President and Chief Executive Officer effective April 1, 2025, succeeding H. Eric Bolton, who transitioned to Executive Chairman. The continuity of leadership—Hill had been with MAA since 2010—ensures strategic consistency while bringing fresh energy to the CEO role.

Financial engineering continues with MAA's operating partnership, Mid-America Apartments, L.P. ("MAALP"), pricing a $350,000,000 offering of MAALP's 4.950% senior unsecured notes due March 1, 2035, priced at 99.170% of the principal amount, with closing expected on December 18, 2024. This demonstrates continued access to capital markets despite rate volatility.

Looking ahead, guidance reflects both confidence and caution. This residential REIT revised its projections and now expects 2025 core FFO per share in the range of $8.65-$8.89 compared with $8.61-$8.93 guided earlier, with the midpoint remaining unchanged at $8.77. The tightened range suggests improved visibility even as challenges persist.

Market headwinds remain real. Austin, Phoenix, and Nashville markets are facing significant pricing pressure due to record supply. Sunbelt states face rent drops and oversupply issues, while Midwest markets show stronger rent growth due to limited new construction. This geographic dispersion within MAA's portfolio provides natural hedging.

Analyst sentiment has evolved cautiously. MAA price target lowered to $170 from $180 at Scotiabank in August 2025, while MAA was upgraded to Outperform from Neutral at Mizuho. According to 20 analysts, the average rating for MAA stock is "Buy." The 12-month stock price target is $164.05, which is an increase of 14.70% from the latest price.

XIV. Final Analysis & Conclusion

Standing at the crossroads of 2025, MAA embodies both the promise and peril of American apartment ownership. The company that George Cates built from a Memphis truck dealership has become a $20 billion testament to the power of patient capital allocation, operational excellence, and geographic focus. Yet the very factors that drove its success—Sunbelt growth, demographic tailwinds, housing unaffordability—now face unprecedented tests.

The bull case remains compelling. Demographics are destiny, and America continues producing more households than homes. The math is brutally simple: with median home prices in MAA's markets up 40-60% since 2020 and mortgage rates doubled, millions of would-be buyers remain trapped in rentals. MAA's 41% turnover rate—the lowest in company history—proves this isn't theory but reality. Each percentage point of reduced turnover saves millions in marketing and renovation costs while providing pricing power that flows directly to the bottom line.

Operational excellence at scale creates competitive advantages that compound over time. MAA's technology platform, built over decades and costing tens of millions, can't be replicated by smaller operators. The ability to dynamically price 100,000+ units, centralize operations across 16 states, and maintain 95%+ occupancy through market cycles represents institutional knowledge that money alone can't buy. When competitors struggle with basic property management, MAA is implementing AI-powered leasing and predictive maintenance.

But the bear case has teeth. Supply overhangs in Austin, Phoenix, and Nashville aren't abstract concerns—they're crushing rents today. The development pipeline that looked brilliant in 2021 now must lease into softening markets. Political pressure for rent control grows with each election cycle, and while MAA has avoided regulated markets, the political winds could shift dramatically. The American Dream of homeownership might be deferred, but it hasn't died, and eventually, supply and demand must reconcile.

The interest rate environment poses particular challenges. While MAA's investment-grade balance sheet provides flexibility, the entire REIT sector trades as a bond proxy. When treasuries yield 5%, a 4% dividend yield loses luster, regardless of growth prospects. The cost of capital has fundamentally shifted, making acquisitions less accretive and development returns more marginal. The easy money era that fueled MAA's growth has definitively ended.

What makes MAA fascinating isn't its victories but its adaptability. The company that specialized in B-class suburban properties successfully integrated Post's urban luxury portfolio. The REIT that grew through acquisitions pivoted to development when buying became too expensive. The operator that once collected paper checks now runs one of the industry's most sophisticated technology platforms. This evolutionary capacity—rare in real estate—suggests MAA can navigate whatever comes next.

The path forward requires threading multiple needles simultaneously. MAA must absorb new supply while maintaining occupancy, push rents without triggering political backlash, develop new properties without oversupplying markets, and generate growth while paying out 90% of taxable income. It's a high-wire act that would challenge any management team, made more difficult by macroeconomic uncertainty and evolving resident expectations.

Yet MAA's history suggests betting against them is dangerous. Every previous crisis—the dot-com bust, 2008 financial crisis, COVID pandemic—became an opportunity for MAA to emerge stronger. The company's conservative leverage, operational discipline, and patient capital allocation create resilience that becomes visible only in downturns. While others retreated, MAA advanced. While competitors struggled, MAA thrived.

The investment case ultimately depends on time horizon and risk tolerance. For those seeking immediate gratification, MAA offers little excitement—same-store NOI declining, new supply pressuring rents, and political risks mounting. But for patient investors who think in decades, not quarters, MAA represents a bet on American demographic destiny, executed by proven operators with irreplaceable assets in irreplaceable locations.

The truck dealer from Memphis who started buying apartments in 1977 probably never imagined his company would house 300,000 Americans and trade on the S&P 500. But George Cates understood something fundamental: people always need homes, and providing quality housing at fair prices in growing markets is a recipe for enduring success. That simple insight, scaled and systematized over five decades, created one of American real estate's great success stories.

As we look toward 2030 and beyond, MAA faces its next evolution. The Sunbelt will continue growing—that seems certain. Technology will reshape property management—that's already happening. The housing affordability crisis will persist—mathematics ensures it. Within these mega-trends, MAA must continue adapting, innovating, and executing. The company that mastered the art of boring excellence in apartment operations must now navigate a world where the only constant is change.

The story of Mid-America Apartment Communities is far from over. In fact, as America grapples with housing its growing population, as technology transforms every industry, and as the Sunbelt continues its inexorable rise, MAA's most important chapters may lie ahead. The foundation Cates built, the scale Bolton achieved, and the platform Hill now commands position MAA to define American apartment living for the next generation.

For investors, residents, and observers, MAA represents something larger than a REIT—it's a proxy for American demographic transformation, a case study in operational excellence, and a testament to the power of patient capital allocation. Whether MAA continues its ascent or stumbles under new challenges will reveal much about the future of American housing, the viability of the REIT model, and the endurance of the Sunbelt thesis.

The apartment empire that began in Memphis has become American infrastructure, as essential as highways or utilities. In a nation where homeownership increasingly feels like fantasy, MAA provides reality—100,000+ homes for teachers, nurses, engineers, and families who make America work. That's not just a business model; it's a responsibility. How MAA shoulders that responsibility while generating returns for shareholders will determine whether the next 50 years prove as successful as the first.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube