Mastercard: The Interbank Alliance That Conquered Global Payments

I. Introduction & Episode Roadmap

Picture this: May 25, 2006. The trading floor at the New York Stock Exchange buzzes with unusual energy. Mastercard, the payment network that processes billions of transactions annually, is about to go public at $39 per share. The bankers who built this company over four decades—many of whom fought tooth and nail to prevent this very moment—watch as their cooperative transforms into a Delaware corporation. What they couldn't know then was that this $4.6 billion market cap company would balloon into a $525 billion behemoth by 2024, delivering an eye-watering 11,334% return to those brave enough to buy on day one.

But here's what makes this story truly remarkable: Mastercard shouldn't exist. It was born from rejection, built through cooperation among fierce competitors, and succeeded despite having no first-mover advantage in a market where network effects typically create winner-take-all dynamics. How did seventeen bankers meeting in a Buffalo hotel room create one half of the most powerful duopoly in global finance?

The answer lies in a forty-year journey of strategic pivots, technological leaps, and most importantly, the accidental creation of what might be capitalism's most perfect competitive structure—two networks that compete fiercely while collectively dominating global payments. Today, Mastercard sits as the world's 19th most valuable company, processing over 100 billion transactions annually, yet 85% of global transactions still happen in cash. The growth runway ahead might be even more spectacular than the journey behind.

This is the story of how a consortium of regional banks challenged Bank of America's payment card monopoly and inadvertently built one of the greatest toll-booth businesses ever created. It's a tale of network effects, regulatory battles, and the transformation from a sleepy cooperative to a technology powerhouse. Most surprisingly, it's the story of how cooperation among competitors created more value than any single company could have achieved alone.

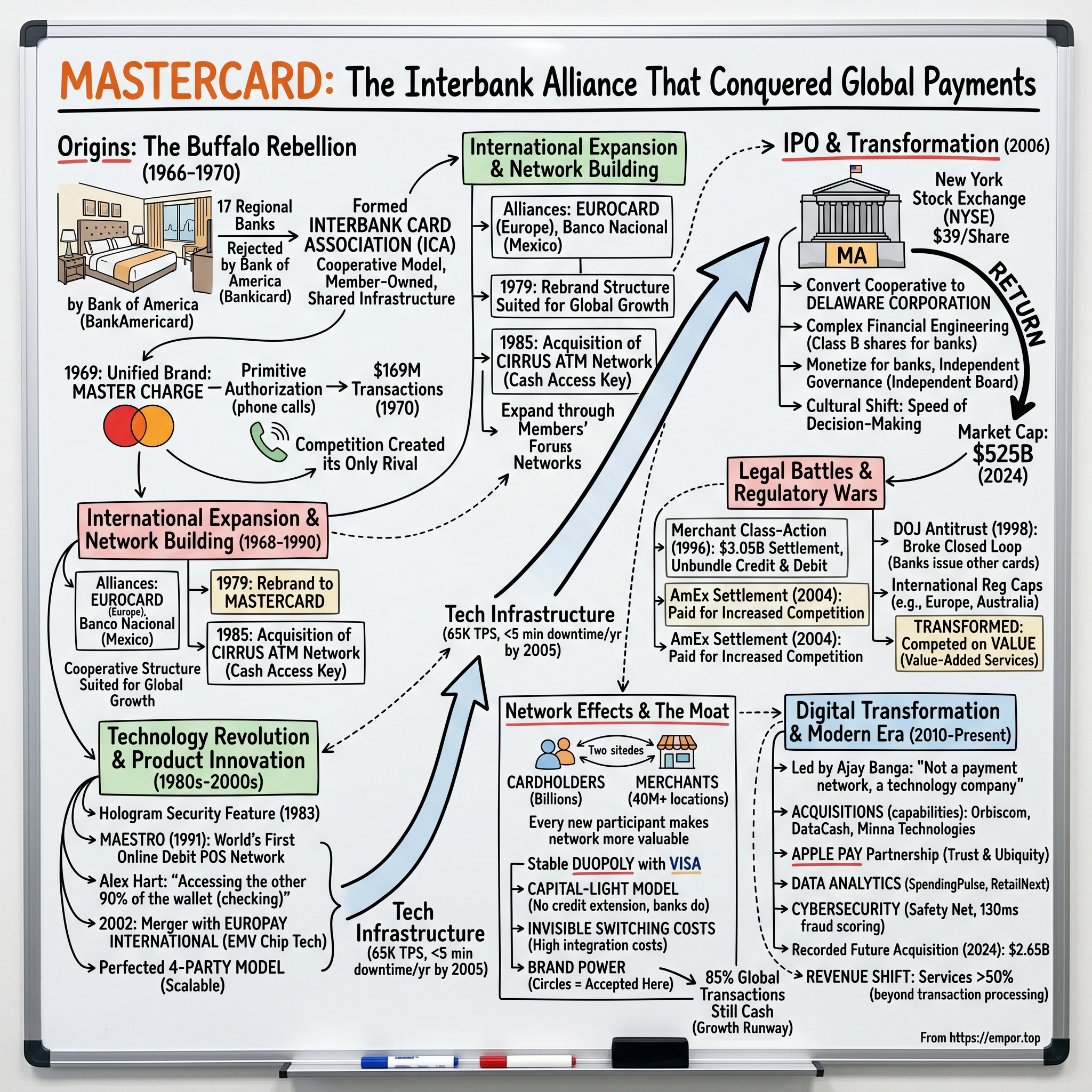

II. Origins: The Buffalo Rebellion (1966-1970)

The Snowy Buffalo hotel conference room in 1966 felt more like a war council than a business meeting. Karl H. Hinke, a vice president at Marine Midland Bank, had just returned from California with bad news. Bank of America had rejected his request for a BankAmericard license—the dominant payment card of the era. Around the table sat representatives from sixteen other banks, all nursing the same rejection, all feeling the squeeze of being locked out of the emerging credit card revolution.

"Gentlemen," Hinke began, his German accent still detectable despite decades in America, "if they won't let us join their network, we'll build our own."

What happened next would reshape global commerce. These seventeen banks, none particularly large or powerful on their own, decided to form the Interbank Card Association (ICA). Unlike BankAmericard, which Bank of America controlled with an iron fist, ICA would operate as a true cooperative. No single bank would dominate. Committees of members would make decisions. It was radical, messy, and according to most experts at the time, doomed to fail.

The founding principle was deceptively simple yet revolutionary: create a payment network where banks could compete for customers while cooperating on infrastructure. Think of it as building a shared highway system where everyone agrees on the rules of the road but races their own cars. This structure would prove to be ICA's secret weapon—and nearly its undoing.

By the end of 1967, Hinke's rebellion had attracted 150 member banks. The growth was explosive but chaotic. Each bank issued cards with different designs, different names, different terms. Merchants couldn't tell if they were accepting the same network's cards. The solution came in 1969 with a unified brand: Master Charge: The Interbank Card, featuring two overlapping circles—one orange, one yellow—that would eventually become one of the world's most recognizable logos.

The early authorization system was comically primitive by today's standards. When a merchant accepted a Master Charge card, they literally picked up a phone and called a centralized authorization center. An operator would flip through printed lists of card numbers, checking credit limits and stolen card reports. A $50 purchase could take five minutes to approve. Yet this creaky infrastructure processed $169 million in transactions by 1970—proof that even imperfect networks create tremendous value when they connect enough participants.

What made ICA different from BankAmericard wasn't just its cooperative structure—it was its mindset. While Bank of America treated its card as a product to control, ICA's members saw Master Charge as a platform to build upon. This philosophical difference would define the next five decades of competition. Where BankAmericard (soon to become Visa) led with control and standardization, Master Charge innovated through member initiatives and regional experimentation.

The irony wasn't lost on industry observers: Bank of America's rejection of those seventeen banks didn't protect its monopoly—it created its only real competitor. By trying to lock others out, they inadvertently sparked the creation of a rival network that would eventually process nearly half of all payment card transactions globally. Sometimes the best strategic moves come from your competitors' mistakes.

III. International Expansion & Network Building (1968-1990)

While American banks were still figuring out how to make phone authorizations work reliably, ICA's leadership made a counterintuitive decision that would define Mastercard's trajectory: go global before going national. In 1968, just two years after formation and while still struggling with brand recognition in the United States, ICA struck strategic alliances with Eurocard in Europe and Banco Nacional in Mexico.

The Eurocard deal was particularly audacious. Here was ICA, barely known in Buffalo, negotiating with a consortium that included every major European bank. The Europeans saw something American observers missed: ICA's cooperative structure was perfectly suited for international expansion. No European bank wanted to accept American dominance—but they were happy to join a member-owned network where they'd have a voice.

Russell Hogg, who would later become Mastercard's president, recalled the first international authorization test in 1972: "We processed a transaction from a British Access card in a shop in Tokyo. It took 45 minutes, three phone calls across time zones, and probably cost us $50 in long-distance charges for a $12 purchase. Everyone celebrated like we'd landed on the moon."

That anecdote captures both the absurdity and ambition of early international expansion. The economics were terrible, the technology was inadequate, but ICA understood something fundamental: payment networks are only as valuable as their reach. Every new country added exponential value to every existing member. A card useful in London and New York was worth far more than one limited to either city alone.

The 1979 rebrand from Master Charge to MasterCard wasn't just cosmetic—it signaled a shift from American credit product to global payment network. The name change cost $30 million in 1979 dollars, causing revolt among member banks who thought the money could be better spent on technology. But management understood that brand recognition was infrastructure too. You can't build a global network if merchants don't recognize your mark.

The 1985 acquisition of Cirrus ATM network marked another strategic inflection point. ATMs were still novel—many consumers didn't trust machines with their money—but MasterCard's leadership saw them as the first wave of payment digitization. More importantly, Cirrus gave MasterCard something Visa didn't have: a massive installed base of cash access points. Suddenly, a MasterCard wasn't just for purchases—it was your key to cash anywhere in the world.

But the real competitive advantage during this period wasn't any single innovation—it was the cooperative structure everyone thought would be ICA's weakness. When MasterCard wanted to enter Japan, six member banks already had relationships there. When they needed to navigate German banking regulations, Deutsche Bank members led the charge. When China began opening in 1987, HSBC provided the connections. The network expanded through its members' networks, creating a web of relationships no single company could have built.

The 1988 launch of the first payment card in the Soviet Union exemplified this approach. While American Express struggled to get meetings with Soviet officials, MasterCard's European members had existing trade finance relationships. The card itself was almost symbolic—few Soviet citizens could qualify, fewer merchants could accept it—but it established presence before the fall of the Berlin Wall. When Eastern Europe opened, MasterCard was already there.

By 1990, MasterCard operated in 50 countries with 22,000 member financial institutions. The scrappy Buffalo rebellion had become a global federation. The cooperative structure that experts predicted would cause paralysis had instead created the most internationally diverse payment network in history. The lesson was clear: sometimes the best way to compete globally is to let local players lead locally while providing the connective tissue that binds them together.

IV. Technology Revolution & Product Innovation (1980s-2000s)

The 1983 introduction of hologram security features on MasterCard plastics seems quaint now, but it represented a fundamental shift in how the company thought about innovation. While Visa focused on scale and standardization, MasterCard positioned itself as the technology pioneer. The hologram wasn't just about preventing fraud—though it cut counterfeit losses by 38% in the first year—it was about signaling to banks and consumers that MasterCard meant cutting-edge.

The real revolution came in 1991 with Maestro, the world's first online point-of-sale debit network. To understand how radical this was, consider that most debit transactions in 1991 were still processed like checks—batched at end of day, settled over several days, with no real-time authorization. Maestro processed everything instantly. The transaction hit your bank account immediately. Merchants got guaranteed payment. It was checking account access with credit card convenience.

The technical challenge was staggering. MasterCard had to convince thousands of banks to upgrade their core systems, connect them in real-time, and maintain 99.99% uptime—all while processing millions of transactions daily. The Maestro project cost over $500 million and took four years to fully deploy. Many board members thought it was insane to spend that much on debit when credit cards had higher interchange fees.

But CEO Alex "Pete" Hart saw what others missed: debit would eventually dwarf credit. His famous 1990 board presentation included a simple chart showing that checking accounts held 10 times more money than credit lines. "We're fighting over 10% of the wallet," he said. "Debit lets us access the other 90%." By 2000, Maestro processed more transactions than MasterCard credit—validation of Hart's expensive bet.

The 2002 merger with Europay International was sold to the press as geographic expansion, but insiders knew it was really about technology consolidation. Europay had developed EMV chip technology—those smart chips that are now ubiquitous—while MasterCard had superior network infrastructure. The merger wasn't just adding European volume; it was acquiring the technology standard that would define payment security for the next two decades.

The four-party model that MasterCard perfected during this period deserves special attention because it's the architecture that enabled everything else. In American Express's three-party model, AmEx issues the card, acquires the merchant, and processes the transaction—controlling everything but limiting scale. MasterCard's four-party model separated these roles: issuing banks competed for consumers, acquiring banks competed for merchants, and MasterCard simply connected them. It was messier but infinitely more scalable.

This model created unexpected innovation vectors. When First USA wanted to offer cash-back rewards in 1994, they didn't need MasterCard's permission—they just did it. When Commerce Bank wanted to offer no-fee checking with debit cards in 1996, they could. The network enabled innovation at the edges while maintaining stability at the core. It's the same principle that made the internet successful: simple protocols that enable complex applications.

The technology investments of this era—roughly $3 billion between 1990 and 2005—transformed MasterCard from a payment processor to a technology company that happened to process payments. The authorization network could handle 65,000 transactions per second. The fraud detection systems used early artificial intelligence to spot patterns humans couldn't see. The data warehouse knew more about global spending patterns than most governments.

By 2005, on the eve of its IPO, MasterCard's technology infrastructure was processing 23 billion transactions annually with 99.999% uptime—that's less than 5 minutes of downtime per year. The Buffalo cooperative had become one of the world's most reliable technology platforms, all while maintaining the member-governance structure everyone said would prevent serious innovation. Sometimes the best technology comes from necessity, not strategy.

V. Legal Battles & Regulatory Wars

The courtroom in Brooklyn, 1996, was packed beyond capacity. Four million merchants had joined forces in the largest class-action antitrust lawsuit in American history, and their target sat at the defendant's table: MasterCard and Visa executives, looking uncomfortable in the unfamiliar arena of public scrutiny. The charge? Forcing merchants who accepted credit cards to also accept more expensive debit cards—a practice the merchants claimed cost them billions in unnecessary fees.

The lawsuit exposed the uncomfortable reality of MasterCard's business model: the network's value came partially from market power that bordered on coercion. Merchants couldn't refuse MasterCard debit if they wanted MasterCard credit, and they certainly couldn't survive without accepting MasterCard credit. It was the classic antitrust pattern—tying one product to another—but MasterCard argued it was necessary for network integrity.

The 2003 settlement—$3.05 billion, the largest antitrust award in history at that time—fundamentally changed MasterCard's strategy. Beyond the eye-watering payout, MasterCard had to unbundle credit and debit acceptance. Merchants could now choose one without the other. Wall Street predicted disaster; surely merchants would drop expensive debit products. Instead, something unexpected happened: freed from coercion, MasterCard had to compete on value, and they discovered they were actually good at it. Debit volume grew 40% in the two years after settlement.

The 1998 Department of Justice lawsuit hit even closer to home. The DOJ alleged that MasterCard and Visa's rules prohibiting member banks from issuing American Express or Discover cards violated antitrust law. The government's argument was elegant: the two networks controlled 75% of the market and used that control to lock out competitors. MasterCard's defense was equally simple: banks created these networks and should control who participates.

When Judge Barbara Jones ruled against MasterCard and Visa in 2001, she didn't just find antitrust violation—she essentially declared the entire cooperative structure anticompetitive. Member banks could now issue any company's cards. Within six months, Citibank was issuing American Express cards, and Bank of America was exploring Discover partnerships. The closed loop was broken.

The $1.8 billion settlement with American Express in 2004 added insult to injury. AmEx had sued claiming the exclusionary rules cost them billions in lost business. The settlement amount was painful, but the strategic implications were worse: MasterCard had to allow its greatest competitor into its own members' portfolios. CEO Bob Selander called it "paying for the privilege of increased competition."

But here's where the story gets interesting: these legal defeats transformed MasterCard into a stronger company. Forced to compete without coercion, MasterCard invested heavily in value-added services. They built fraud protection systems that actually worked. They created loyalty programs merchants wanted. They developed data analytics that helped retailers understand their customers. The company that had relied on market power learned to compete on merit.

The international regulatory battles told a different story. In Europe, the Commission capped interchange fees at 0.3% for credit and 0.2% for debit—roughly one-third of U.S. levels. In Australia, the Reserve Bank went even further, forcing radical transparency in fee structures. Each jurisdiction brought new rules, new caps, new requirements. MasterCard needed armies of lawyers and lobbyists just to maintain existing business.

Yet somehow, margins kept expanding. How? Because MasterCard discovered that interchange fees, while important, weren't the only revenue stream. Data analytics, fraud protection, consulting services, cross-border processing—these value-added services carried even higher margins than traditional transaction processing. Regulatory pressure on one revenue stream forced innovation in others. By 2005, non-interchange revenue exceeded 35% of total revenue, up from 10% in 1995.

The legal battles also accelerated a crucial strategic shift: the decision to go public. As a cooperative, every lawsuit implicated member banks. As a public company, MasterCard could fight its own battles without dragging members into court. The IPO wasn't just about capital or governance—it was about legal independence. Sometimes the best defense against regulation is structural change that makes the regulation less relevant.

VI. The IPO & Transformation (2006)

The boardroom at MasterCard's Purchase, New York headquarters on a cold January morning in 2006 was tense. CEO Bob Selander stood before a divided board of directors—half representing global banks that had built MasterCard over forty years, half independent directors brought in to prepare for the public offering. The question on the table wasn't whether to go public anymore—that decision had been made. The question was how to price forty years of cooperative ownership into a single number.

"Gentlemen," Selander began, "we're not just taking a company public. We're transforming an entire governance model while the plane is flying." The numbers were staggering: 25,000 member financial institutions would have to approve the transformation, regulatory approvals were needed in 210 countries, and somehow they had to maintain business operations processing 40 million transactions daily during the transition.

The preparation took three years and cost $450 million—before a single share was sold. MasterCard had to legally separate from its member banks, create independent governance structures, and most challengingly, convince competing banks to give up control of their collectively-owned asset. Why would Bank of America and JPMorgan Chase surrender ownership of something they'd spent decades building?

The answer lay in a brilliant piece of financial engineering. Member banks received Class B shares that carried no economic rights but maintained voting control during a transition period. They could monetize their ownership through the IPO while keeping enough control to ensure MasterCard wouldn't turn against them. It was having your cake and eating it too—a structure so complex the SEC took six months just to understand it.

May 25, 2006, arrived with unusual fanfare for an IPO. MasterCard priced 95.5 million shares at $39 each—the upper end of the range—raising $2.4 billion. Within minutes of trading, shares shot up to $46. By day's end, MasterCard was worth $5.4 billion, making it the largest IPO of the year. The member banks that had collectively owned MasterCard suddenly held liquid shares worth billions. Citigroup alone netted $1.1 billion from selling its stake.

But the real transformation wasn't financial—it was cultural. As a cooperative, MasterCard moved at the speed of committee consensus. Every major decision required member approval. Innovation happened in working groups that met quarterly. As a public company, Selander could make strategic decisions in days, not months. The first test came immediately: within six weeks of IPO, MasterCard announced a $1.5 billion technology investment that would have taken two years to approve under the old structure.

The governance transformation was equally dramatic. The old board of 18 bank representatives was replaced with 12 directors, only three from financial institutions. The new chairman, Rick Haythornthwaite, came from British retailing—deliberately chosen because he'd never worked in banking. "We needed directors who would ask why things were done certain ways," Selander explained, "not people who already knew the answer."

Wall Street initially struggled to value MasterCard. Analysts compared it to payment processors like First Data (trading at 12x earnings) or financial services companies like State Street (18x earnings). But prescient investors recognized MasterCard was neither—it was a network effect business like eBay or Google. Those who understood this dynamic and bought at $39 watched shares reach $120 within 18 months—a 207% return while the S&P 500 gained just 11%.

The IPO also unleashed competitive dynamics that had been suppressed for decades. As a cooperative, MasterCard couldn't really compete against its own members. If Bank of America wanted to push American Express cards, MasterCard had to smile and accept it. As a public company, MasterCard could fight back. They launched issuer incentive programs that rewarded exclusive relationships. They acquired processing companies that competed with bank-owned processors. The servant had become a competitor.

The numbers tell the transformation story: In 2005, MasterCard's last full year as a cooperative, revenue was $2.9 billion with net income of $267 million. By 2010, revenue had nearly doubled to $5.5 billion with net income of $1.8 billion—a seven-fold increase in profitability. The same network, processing similar transaction volumes, had become dramatically more profitable simply by changing its governance structure.

VII. Network Effects & The Moat

Picture a merchant in rural Idaho in 2010. She runs a small coffee shop, processes maybe 100 transactions daily. One morning, a customer presents a MasterCard. If she doesn't accept it, the customer walks across the street to Starbucks. But here's the beautiful catch: once she starts accepting MasterCard, she can't stop. Her customers expect it. New customers come because of it. She's locked into a network she can neither escape nor replicate.

This is the elegant tyranny of two-sided network effects, and MasterCard has perfected it into one of business history's most powerful moats. Every new cardholder makes MasterCard more valuable to merchants. Every new merchant makes it more valuable to cardholders. It's a perpetual motion machine of value creation, and once it reaches critical mass—which MasterCard achieved decades ago—it becomes nearly impossible to disrupt.

The numbers are staggering. As of 2015, despite sixty years of electronic payment innovation, 85% of global transactions still happened in cash or check. MasterCard and Visa collectively processed about 8% of global payment volume. The total addressable market wasn't just large—it was almost incomprehensibly vast. $100 trillion in cash transactions waiting to be digitized. At a 0.2% net revenue yield, that's $200 billion in potential annual revenue. MasterCard was a $10 billion revenue company fishing in a $200 billion pond.

The duopoly structure with Visa created something even more powerful than monopoly: stable competition. Together, they control 82% of global card transactions (excluding China where UnionPay dominates). American Express holds 7.3%, Discover barely registers outside the U.S. This isn't market failure—it's network effects working exactly as theory predicts. Two networks can coexist when switching costs are high. Three is unstable. Four is impossible.

The capital efficiency of this model defies conventional business logic. MasterCard's five-year average return on equity from 2010-2015 was 43%. Not 4.3%—forty-three percent. The free cash flow margin averaged 34%. These aren't software margins—they're better. Software companies have to constantly innovate or risk disruption. MasterCard's innovation budget is largely optional. The network is the product, and networks get stronger with age, not weaker.

The switching costs are invisible but overwhelming. A bank spent an average of $50 million to integrate with MasterCard's systems. Merchants invested thousands in point-of-sale terminals. Consumers carry the cards in their wallets, have the numbers memorized, use them for recurring payments. To switch from MasterCard, all three parties—bank, merchant, consumer—would have to move simultaneously. It's a three-body problem with no solution.

But the real moat isn't technology or even network effects—it's regulatory capture through standardization. MasterCard and Visa don't just process payments; they define how payments work. Their rules become industry standards. Their security protocols become regulatory requirements. Their networks become too essential to fail. When the European Central Bank wanted to create instant payments, they didn't compete with MasterCard—they hired them as consultants.

The toll-booth analogy is almost perfect. MasterCard owns no stores, holds no inventory, extends no credit. They simply stand between buyers and sellers, collecting 0.13% of every transaction that crosses their network. It's like owning the only bridge between two cities—you don't care what's in the trucks, you just collect your toll. The difference is that physical bridges can be rebuilt elsewhere. Network bridges exist in economic space where geography doesn't apply.

The brand power amplifies everything else. Those two interlocking circles—now simplified to just red and yellow—appear 2.8 billion times on cards worldwide. The logo appears at 40 million merchant locations. It's seen by billions of people thousands of times per year. MasterCard spent $4 billion on marketing between 2010-2020, not to acquire customers—banks do that—but to maintain mental availability. When you think payment, you think MasterCard or Visa. There's no third option in most minds.

The 2019 decision to drop "mastercard" from the logo—leaving just the circles—demonstrated supreme confidence. Like Nike's swoosh or Apple's apple, the symbol had transcended language. It meant the same thing in Tokyo, London, and São Paulo: accepted here. The brand had become infrastructure—as essential and invisible as plumbing, until it's not there.

VIII. Digital Transformation & Modern Era (2010-Present)

Ajay Banga walked into his first all-hands meeting as CEO in July 2010 with a simple message that shocked MasterCard's 5,500 employees: "We're not a payment network anymore. We're a technology company. If you don't believe that, you're at the wrong company." Coming from a consumer goods background at Citigroup, Banga saw what insiders had missed—MasterCard's future wasn't in processing more credit card transactions but in reimagining what a payment network could be.

The acquisition spree that followed was unprecedented in MasterCard's conservative history. Between 2009 and 2012, they bought Orbiscom (prepaid card technology), DataCash (payment gateway), Travelex's prepaid business, and Truaxis (mobile commerce). Total spend: $2.3 billion. Wall Street was confused—why was a company with 40% margins buying lower-margin businesses? Banga's response was characteristically blunt: "We're not buying revenues, we're buying capabilities we'll need in five years."

Orbiscom became MasterCard Labs, the company's innovation arm. Within 18 months, Labs had filed 127 patents and launched pilot programs in 15 countries. The Singapore office experimented with biometric payments. The Dublin team worked on blockchain applications. The Silicon Valley outpost embedded engineers at Apple and Google. For a company that had taken three years to approve the hologram in the 1980s, the pace was dizzying.

The 2014 Apple Pay partnership marked the inflection point. When Tim Cook announced that iPhones would become payment devices, he needed a network partner. American Express begged for exclusivity. PayPal offered better economics. But Apple chose MasterCard and Visa as primary partners. Why? Because they understood that payment networks aren't about technology—they're about trust and ubiquity. Apple had the devices; MasterCard had 40 million acceptance points.

The integration took just four months—lightning speed for financial services. MasterCard's role was invisible to consumers: when you tap your iPhone, you think Apple Pay, not MasterCard. But every transaction runs through MasterCard's rails, generates MasterCard's fees, and reinforces MasterCard's network effects. It was strategic jiu-jitsu—using Apple's strength to extend MasterCard's reach.

The data analytics transformation was equally profound but less visible. MasterCard processes 75 billion transactions annually—each one containing merchant, amount, location, time, and category data. This dataset, properly anonymized and analyzed, was worth more than the transaction fees themselves. RetailNext, launched in 2015, gave merchants insights that transformed their businesses: foot traffic patterns, customer loyalty metrics, competitive intelligence.

SpendingPulse, MasterCard's macro-economic tracking service, became so accurate that the Federal Reserve and European Central Bank subscribed. They could track economic activity in real-time while governments waited for monthly reports. During COVID-19, MasterCard knew about spending shifts weeks before official statistics. This wasn't payment processing—it was economic intelligence.

The cybersecurity investments were staggering but necessary. MasterCard's Safety Net system uses artificial intelligence to analyze every transaction across 210 countries in real-time, scoring fraud probability in 130 milliseconds. The system prevented $20 billion in fraud in 2020 alone. But the real innovation was making security invisible—consumers never knew their transactions were being protected by algorithms that would make the NSA jealous.

The expansion into B2B payments represented the largest opportunity. While consumer payments grabbed headlines, business payments were five times larger and still 90% paper-based. MasterCard Track, launched in 2018, wasn't just digitizing B2B payments—it was reimagining them. Real-time tracking, automatic reconciliation, integrated supply chain finance. It turned payments from a back-office function into a strategic capability.

The blockchain experiments deserve special mention, not because they succeeded but because they showed MasterCard's strategic evolution. While Bitcoin maximalists proclaimed the death of traditional payments, MasterCard quietly filed 35 blockchain patents and ran pilots with central banks. They weren't trying to preserve the status quo—they were ensuring that whatever came next, MasterCard would process it.

By 2020, Banga's transformation was complete. MasterCard's revenue had grown from $5.5 billion to $15.3 billion. But more importantly, the revenue mix had shifted: traditional transaction processing was now less than 60% of revenue. The rest came from services that didn't exist a decade earlier. The company that had spent forty years as a utility had become a technology platform that happened to move money.

IX. Playbook: Business & Investment Lessons

The MasterCard story reads like a masterclass in network effects, but the real lessons run deeper than simple connectivity. When seventeen banks met in Buffalo, they weren't trying to build a network effects business—that term wouldn't be coined for decades. They were solving a practical problem: how to compete with Bank of America without Bank of America's resources. Their solution—cooperative competition—accidentally created one of history's most powerful business models.

The first lesson is counterintuitive: sometimes the best monopolies come from competition. MasterCard and Visa competed fiercely for forty years, yet this competition strengthened both networks rather than weakening them. They pushed each other to innovate, expand internationally, and improve technology. A single monopolist might have extracted more short-term profit but would never have achieved the global ubiquity that two competing networks created. Competition created more value than monopoly would have.

The capital-light model that emerged wasn't designed—it was discovered. MasterCard doesn't extend credit (issuing banks do), doesn't recruit merchants (acquiring banks do), and doesn't manufacture cards (vendors do). They simply maintain the rails and rules. This radical outsourcing of everything except the core network created leverage ratios that make software companies jealous. When revenue grows 10%, profits grow 20%. When others take the credit risk, you just collect the toll.

The governance transformation from cooperative to public company offers a crucial insight: ownership structure determines strategic capability. As a cooperative, MasterCard couldn't make bold bets or move quickly. As a public company, they could acquire aggressively and invest billions in technology. The same assets under different ownership generated radically different returns. Sometimes the best investment isn't in new assets but in restructuring existing ones.

The regulatory battles teach perhaps the most valuable lesson: regulation can be a competitive advantage if you're already inside the walls. Every new rule, requirement, and compliance burden makes it harder for new entrants. MasterCard spends $500 million annually on compliance—a cost they can easily afford but which would crush a startup. The regulations meant to constrain them became the moat that protects them.

The brand strategy—building awareness for something consumers never directly choose—seems wasteful until you understand its true purpose. MasterCard doesn't advertise to acquire customers; they advertise to prevent defection. Every "Priceless" campaign reminds banks why MasterCard cards are worth issuing and merchants why the logo is worth displaying. It's defensive marketing disguised as offensive marketing.

The 30-40% operating margins that continue widening violate basic economic theory. In competitive markets, margins should compress over time. But MasterCard's margins expand because the network effects compound. Every new user makes the network more valuable to existing users. Every new use case increases switching costs. The business gets better with age, like wine or whisky, not worse like cars or computers.

The acquisition strategy post-IPO reveals sophisticated capital allocation. They didn't buy competitors (antitrust issues) or adjacent networks (integration challenges). They bought capabilities: data analytics, cybersecurity, mobile technology. Each acquisition was small enough to integrate but strategic enough to matter. They were building new revenue streams on top of existing network effects—leverage on top of leverage.

The international expansion strategy—going wide before going deep—contradicts conventional wisdom but makes perfect sense for networks. A payment network useful in 100 countries at 10% penetration is more valuable than one with 90% penetration in 10 countries. Ubiquity matters more than density for payment networks. You can always increase penetration, but you can't easily expand geography once competitors entrench.

For investors, MasterCard demonstrates that the best businesses are often hiding in plain sight. Everyone knew MasterCard processed payments. Few understood they were investing in one of the last great toll-booth businesses. The company trades at 45x earnings not because investors are irrational but because they're rational—the earnings stream is that predictable, the moat is that wide, and the growth runway is that long.

X. Bear vs. Bull Analysis

The Bull Case: A Forty-Year Runway at 40% Margins

The bulls see MasterCard as barely scratching the surface of a generational shift. Start with the basic math: $100 trillion in annual cash transactions globally, MasterCard processing about $6 trillion. Even capturing an additional 5% of cash transactions would double their business. At current take rates and margins, that's $50 billion in additional market cap for every percentage point of cash digitization.

The secular tailwinds are undeniable. E-commerce grows 15% annually while retail grows 3%. Cross-border payments grow 7% annually as globalization continues despite political rhetoric. Contactless payments, accelerated by COVID-19, are making cash psychologically obsolete—who wants to touch dirty paper when you can tap your phone? In Sweden, cash transactions fell from 39% to 9% in just a decade. That's MasterCard's future playing out in real-time.

The B2B opportunity alone could double MasterCard's addressable market. $120 trillion in annual B2B payments, still 88% check and wire transfer. MasterCard Track and blockchain initiatives are early innings of digitizing this massive pool. The margins are even better than consumer payments because businesses value data and integration more than consumers value rewards.

New revenue streams keep materializing. Open banking regulations force banks to share data—MasterCard monetizes it. Governments want to digitize benefits distribution—MasterCard processes it. Cryptocurrencies need on-ramps to traditional finance—MasterCard provides them. Every financial innovation seems to create new toll booths for MasterCard to operate.

The competitive position appears unassailable. Starting a new payment network is like starting a new internet—theoretically possible, practically impossible. The Chinese firewall that protects UnionPay also traps it. American Express and Discover lack global reach. Fintech disruptors like Square and PayPal still process through MasterCard rails. Even central bank digital currencies would likely use existing networks for distribution.

The Bear Case: The Slow-Motion Disruption Nobody Sees Coming

The bears point to regulatory storm clouds gathering globally. The European Union's 0.3% interchange cap was just the beginning. American politicians from both parties regularly threaten similar action. Each basis point of interchange reduction directly hits net income. If U.S. interchange fees fell to European levels, MasterCard would lose 30% of revenue overnight.

Central bank digital currencies represent existential risk that bulls underestimate. When China launches digital yuan internationally, it won't need MasterCard rails. When the Federal Reserve launches FedNow for instant payments, banks can bypass card networks entirely. CBDCs aren't science fiction—they're being piloted in 100 countries. MasterCard's response—"we'll process CBDCs too"—sounds like Blockbuster saying they'll stream movies.

Big Tech ambitions are more serious than investors realize. Apple Pay looks cooperative today, but Apple has 1.5 billion active devices and $200 billion in cash. They could buy Square, integrate deeply, and slowly disintermediate MasterCard. Google's payment ambitions failed before, but they're patient. Amazon processes $500 billion in gross merchandise value—why would they forever pay MasterCard fees when they could build their own network?

The China problem isn't just UnionPay's dominance—it's the model it represents. Government-directed payment networks with zero merchant fees. As other emerging markets develop, will they follow the MasterCard model of private networks and high fees, or the China model of public networks and low fees? India's UPI already processes more transactions than MasterCard globally, at near-zero cost.

The generational shift in consumer behavior cuts both ways. Gen Z doesn't care about credit cards—they use Buy Now Pay Later services that bypass traditional networks. Venmo and Cash App train young consumers that P2P payments should be free. Cryptocurrency native generations might never enter the traditional financial system. MasterCard's attempting to stay relevant, but they're essentially taxing new payment methods rather than enabling them.

The ESG backlash is intensifying. MasterCard enables $6 trillion in consumption annually, much of it debt-funded. As inequality concerns grow, payment networks that facilitate consumer debt look increasingly problematic. The "war on cash" narrative positions MasterCard as anti-privacy, anti-poor, and anti-freedom. These concerns seem fringe today but social license to operate can evaporate quickly.

The Synthesis: Gradual Decline from an Enormous Peak

The realistic scenario probably lies between extremes. MasterCard will continue growing and generating enormous profits for years, possibly decades. But the growth rate will slow, margins will compress, and multiples will contract. They'll evolve from a growth story to a value stock—still profitable but no longer magical. The transition from 45x to 25x earnings would cut the stock price 44% even if earnings continued growing.

XI. Epilogue & Final Reflections

Standing in MasterCard's headquarters in Purchase, New York today, you'd never guess this company started in a Buffalo hotel room. The walls display artifacts from fifty years of payments history—the original Master Charge cards, early POS terminals, the first chip cards. But what's most striking isn't what's displayed but what's missing: any sense that this company's best days are behind it.

The unlikely success of the bank consortium model violated every principle of strategy. Competitors shouldn't cooperate successfully. Committees shouldn't innovate quickly. Cooperatives shouldn't generate superior returns. Yet MasterCard did all three, creating $500 billion in market value from an initial investment measured in thousands. Sometimes the best strategies are the ones that shouldn't work.

The accidental creation of perfect competition with Visa might be capitalism's greatest unintended consequence. Neither company planned to create a duopoly. They were simply trying to survive and grow. But their fierce competition created more value than either could have achieved alone. They pushed each other internationally, forced each other to innovate, and prevented each other from becoming lazy monopolists. Competition created more value than monopoly would have.

The biggest surprise from researching MasterCard's history is how many times they nearly failed. The early authorization systems barely worked. The international expansion lost money for a decade. The legal battles could have destroyed the company. The IPO almost didn't happen. Success seems inevitable in hindsight but was anything but certain in real-time. Persistence mattered more than perfection.

What would success look like in ten years? MasterCard processing $20 trillion annually, with China somehow opened, CBDCs integrated rather than competitive, and new revenue streams we can't imagine today. The bear case—MasterCard marginalized by government networks and Big Tech—seems possible but improbable. Networks this powerful don't disappear; they evolve or get absorbed but rarely vanish.

The key lesson for founders building network effect businesses is counterintuitive: focus on the network, not the effects. MasterCard spent forty years building infrastructure before fully monetizing it. They prioritized ubiquity over profitability. They let members capture most of the value while they captured just enough. Only after achieving global scale did they optimize for margins. Build the network first; monetize it second.

The transformation from cooperative to public company offers another crucial insight: governance evolution can be as important as business evolution. The same assets under different ownership structures generate radically different returns. Sometimes the best pivot isn't changing your product but changing your structure.

XII. Recent News

Q3 2024 Financial Performance

Mastercard's Q3 2024 earnings report highlights a strong financial performance, with net revenue increasing by 13% year-over-year to $7,369 million, compared to $6,533 million in Q3 2023. On a currency-neutral basis, net revenue grew by 14%. The results exceeded analyst expectations and demonstrated the company's ability to deliver growth across all business segments.

The payment network segment contributed $4,629 million, reflecting a 10% increase year-over-year, primarily due to growth in domestic and cross-border dollar volumes and an increase in switched transactions. Value-added services and solutions revenue grew by 18% to $2,740 million, driven by consulting, marketing services, and fraud and security solutions.

Key operational metrics showed robust growth: - Gross dollar volume grew 10% to $2.5 trillion, cross-border volume rose 17%, and switched transactions increased 11% - Contactless now represents approximately 70% of all in-person switched purchase transactions - As of September 30, 2024, customers had issued 3.4 billion Mastercard and Maestro-branded cards

CEO Michael Miebach commented on the results, stating: "Our strong performance this quarter, with net revenue growth of 13%, or 14% on a currency-neutral basis, highlights how we are delivering across all aspects of our business."

Strategic Acquisitions: Building the Future

Recorded Future Acquisition

Mastercard expanded its cybersecurity services with an agreement to acquire global threat intelligence company Recorded Future from Insight Partners for $2.65 billion. The acquisition was completed in December 2024.

Recorded Future is the world's largest threat intelligence company, with more than 1,900 clients across 75 countries, including the governments of 45 countries and over 50% of the Fortune 100. The strategic rationale centers on enhancing Mastercard's cybersecurity capabilities at a time when cybercrime is projected to cost $9.2 trillion globally in 2024 alone.

Johan Gerber, EVP of Security Solutions at Mastercard, explained the strategic fit: "As the world becomes more digitized, there's an increased focus on securing every interaction and transaction against evolving cyber threats. Adding Recorded Future's AI-driven threat intelligence capabilities to our cybersecurity services, identity solutions and real-time fraud scoring will enable us to better support our customers in these efforts."

Minna Technologies Acquisition

Mastercard agreed to acquire subscription management service Minna Technologies. The deal aims to ease the frustration consumers feel when dealing with subscription services. Founded in 2016 and headquartered in Gothenburg, Minna creates technology that assists consumers in managing their subscriptions directly within banking applications and websites.

The acquisition addresses a growing pain point in the digital economy, where the number of subscriptions globally has climbed to 6.8 billion, with analysts at Juniper Research expecting that number to climb to 9.3 billion by 2028. The Sweden-based company has connected with more than 22,000 subscription businesses, served more than 120 million retail bank and fintech users, and saved customers more than $1 billion in spending on unwanted subscriptions.

Capital Allocation and Shareholder Returns

Mastercard continues to demonstrate strong capital management: - During the third quarter, Mastercard repurchased 6.3 million shares at a cost of $2.9 billion and paid $611 million in dividends - By October 28, Mastercard spent nearly $983 million on further share buybacks, leaving $5.6 billion available under its current repurchase programs

Forward Outlook

Management provided guidance suggesting continued strength: - Year-over-year net revenue growth is expected to be at the low-teens range on a currency-neutral basis excluding acquisitions for Q4 2024. Acquisitions are forecasted to have a minimal impact on this growth rate, while foreign exchange is expected to create a zero to one percentage point headwind for the quarter.

The company's strategic focus remains on capitalizing on the secular shift from cash to digital payments, expanding value-added services, and leveraging recent acquisitions to enhance its competitive position in cybersecurity and subscription management—areas that represent significant growth opportunities beyond traditional payment processing.

XIII. Links & Resources

Investor Relations - Mastercard Investor Relations: investor.mastercard.com - Annual Reports & SEC Filings: investor.mastercard.com/financials-and-sec-filings - Quarterly Earnings: investor.mastercard.com/financials-and-sec-filings/quarterly-results

Industry Analysis - Nilson Report (Payment Industry Intelligence) - Federal Reserve Payments Study - European Central Bank Payment Statistics - Bank for International Settlements - Committee on Payments

Historical Resources - "Electronic Value Exchange" by David Stearns (History of Payment Networks) - "Paying with Plastic" by David Evans & Richard Schmalensee - Harvard Business School Case Studies on Mastercard IPO

Regulatory & Legal - U.S. Department of Justice Antitrust Division - European Commission Competition Policy - Consumer Financial Protection Bureau - Federal Trade Commission

Technology & Innovation - Mastercard Labs: labs.mastercard.com - Mastercard Developers: developer.mastercard.com - EMV Standards: emvco.com

Recent Acquisitions - Recorded Future: recordedfuture.com - Minna Technologies: minnatechnologies.com

Competitive Intelligence - Visa Investor Relations: investor.visa.com - American Express Investor Relations: ir.americanexpress.com - UnionPay International: unionpayintl.com

This analysis represents an independent examination of Mastercard's business evolution and market position. It synthesizes publicly available information through 2024 and should not be considered investment advice. The transformation from a bank cooperative to one of the world's most valuable companies offers profound lessons about network effects, strategic patience, and the power of platforms in the digital age.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube