Meituan: China's "Super App" for Everything Local

I. Introduction & Episode Roadmap

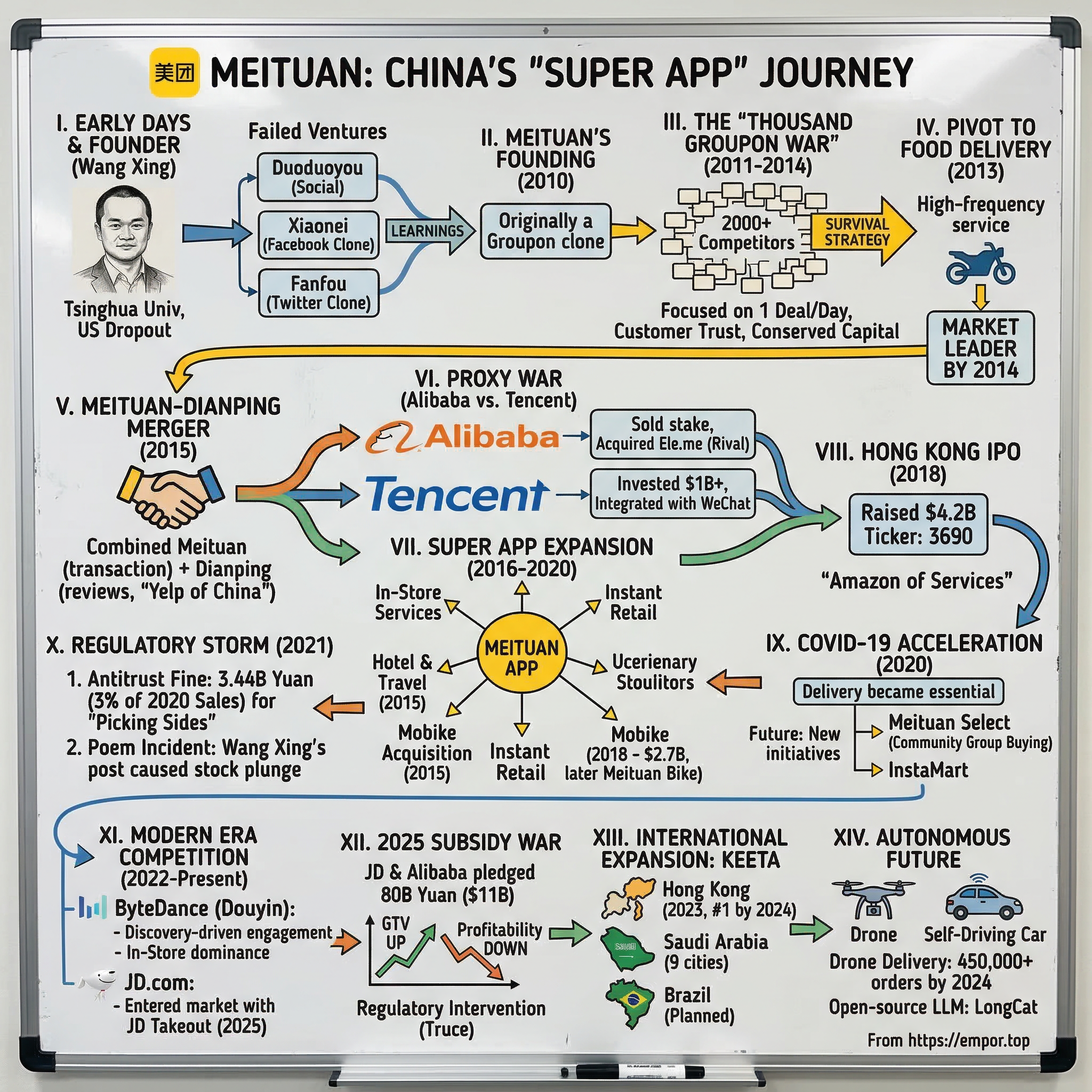

Picture a city of 22 million people, each waking up to a simple question that technology has fundamentally transformed: What should I eat? In Beijing, Shanghai, Shenzhen, and hundreds of other Chinese cities, the answer increasingly flows through a single yellow-branded ecosystem—a company that started as a humble Groupon clone and evolved into what its founder calls "the Amazon of services."

Meituan is a Chinese technology company that operates a platform for local services including on‑demand food delivery, in‑store services and consumer reviews under the Dazhong Dianping brand, hotel and travel bookings, and instant retail. By the end of 2024, Meituan had over 770 million annual transacting users and over 14.5 million annual active merchants on its platform. To put that in perspective, that's more users than the entire population of Europe.

The central question that animates this story: How did a Groupon clone survive the "Thousand Groupon War"—when over 2,000 daily deals companies battled for supremacy—merge with its fiercest rival, navigate a proxy war between Alibaba and Tencent, weather a brutal regulatory crackdown, and emerge as China's undisputed local services champion?

The answer lies in understanding one man's relentless pursuit of what he calls the "infinite game"—and his uncanny ability to learn from failure, copy intelligently, and execute ruthlessly when others stumbled.

Analysts say Meituan now holds about 64–67% of the market, delivering over 50 million orders each day. Meituan has not only dominated, but also skillfully fended off challenges from Douyin (China's TikTok) in the local services and F&B space. Today, the company faces its most significant competitive challenge in years, as JD.com and Alibaba pour billions into subsidies to challenge its dominance. But to understand where Meituan is going, we must first understand where it came from—and the serial entrepreneur who built it.

II. The Serial Entrepreneur: Wang Xing's Journey

Background & Education

In the winter landscape of Longyan, a modest city in Fujian Province, a family's trajectory was being shaped by forces both tragic and transformative. Wang Xing's family suffered greatly after the PRC took power. His grandfather was driven to suicide during the Cultural Revolution, and his father spent years forced to work in the countryside and unable to attend college on account of his family background. After China's reform and opening-up, however, his dad made a fortune in construction.

Wang Xing was born in 1979 in Longyan, Fujian, China. Born in Fujian Province, Wang was the son of a wealthy businessman and factory owner. As a child, Wang was an avid reader and excelled at school, graduating from Beijing's Tsinghua University in 2001. Tsinghua, often called China's MIT, produces the country's technical elite—the engineers and scientists who would later power China's technological rise.

Wang received a bachelor's degree in electronic engineering in 2001. He enrolled in a PhD program in computer engineering at the University of Delaware from 2001 to 2004, but dropped out with a master's degree in computer engineering. After leaving the University of Delaware, Wang returned to China to launch his business career.

The timing of his return proved prescient. By 2004, China's internet sector was on the cusp of explosive growth, and Wang sensed an opportunity that no PhD dissertation could match. But three years later, 25-year-old Wang took the brave step of dropping out of his PhD course at Delaware in the U.S., and moved back to Beijing to enter the world of business.

The Failed Ventures That Built a Founder

What followed was a decade of relentless experimentation—and repeated failure. Serial entrepreneur Wang Xing had over a dozen failed projects under his belt before striking it rich by founding Meituan, one of China's most successful mega-apps.

In his first technology startup, Wang along with a couple of friends, tried to create a Chinese version of the then-social networking site Friendster. His first such site was called Duoduoyou (兜兜友; lit. 'Pocket–Pocket Friends'), targeting students in various Chinese universities. The venture fizzled.

Undeterred, Wang pivoted to what was then the hottest trend in American social networking. According to 163.com, Wang was undaunted by his failure and began a careful study of American social networks. He decided to target a segment of the market and in 2005 he set up a Chinese version of Facebook, a network mainly for college students called Xiaonei.

Xiaonei—meaning "within campus"—caught fire among Chinese university students. Before starting meituan.com in March 2010, he served as founder and CEO of fanfou.com, the first Chinese micro-blogging service. Prior to that, he was the founder of renren.com (formerly known as xiaonei.com), one of the largest social networks in China.

But Wang's inexperience in fundraising proved costly. When he made a social network, the product was solid, but he couldn't find an investor and was forced to sell. The company was acquired by China InterActive Corp in October 2006 and later renamed Renren Inc., eventually going public on the NYSE in 2011—without Wang at the helm.

The pattern repeated with Fanfou, China's first Twitter clone, which Wang launched in 2007. He previously served as chief executive officer of Fanfou from 2007 to 2010. Fanfou gained traction but ran afoul of government censors during politically sensitive events. The platform was shuttered temporarily, and though it returned, it never achieved the scale Wang envisioned.

The Intellectual Framework

What distinguishes Wang from other serial entrepreneurs is his intellectual approach to business. He is also known for picking fights with half of China's internet companies.

Wang became known as "the copycat" because of his habit for creating Chinese versions of successful Western businesses. But this characterization misses something crucial: Wang wasn't merely copying—he was learning. Each failed venture taught him something about Chinese internet users, about fundraising, about timing, and about the brutal competitive dynamics of China's tech sector.

He has low EQ, he often offends, and he doesn't have any partner to make up for this deficiency. Yet this same directness made him a formidable strategist. In public, Wang Xing has called out Jack Ma at least three times. First he said that Alibaba would stoop to any low, that Jack was a liar, and that Taobao started out by selling fake and shoddy products.

But behind the money and success, Wang remains a "poet entrepreneur," a nickname earned from his frequent blog posts on Fanfou (a platform he created in 2007). His posts blend business observations with literary references, classical Chinese poetry, and Western philosophy—a window into the mind of someone who sees entrepreneurship as something more than wealth creation.

Wang's intellectual framework would prove essential when, in 2010, he spotted an opportunity that would finally deliver the success that had eluded him. This time, he would be ready.

III. Meituan's Founding & The "Thousand Groupon War" (2010-2014)

The Groupon Moment

The story of Meituan begins on March 4, 2010, in a Beijing office where Wang Xing had just watched Groupon's meteoric rise in America. The daily deals model was elegant in its simplicity: aggregate consumer demand, negotiate deep discounts with local merchants, and take a commission on each sale. For a market as vast as China's, the opportunity was enormous.

In 2010, Wang established the Chinese group-buying site Meituan, which was based on the business model of Groupon. The company's name, "Meituan," means "beautiful group," reflecting its group-buying origins—though Wang would later redefine what that grouping could mean.

Wang founded Meituan in 2010 with the funding of 12 million USD from Sequoia Capitals. Sequoia's bet on Wang, despite his track record of failed exits, reflected the firm's conviction that the founder had finally found the right model at the right time.

But Wang wasn't alone. The Groupon frenzy had gripped Chinese entrepreneurs like a gold rush. His Meituan was one of about five thousand Groupon clones that launched around 2011. Industry estimates suggested that over 2,000 voucher-selling companies emerged in the space within months—a chaotic scramble that would later be called the "Thousand Groupon War."

The Brutal Consolidation

The war was bloody and fast. According to a report by Tech In Asia in 2012, the average discount offered by the top players in the daily deals space was 60%, which meant that most startups were kicked out of the game early due to unsustainable losses.

Most competitors focused on volume—launching multiple deals per day, spending heavily on advertising, and burning through venture capital in a race to the bottom. Wang chose a different path.

For starters, he decided to only launch one product a day, ensuring that the merchants really felt the benefits of his partnership. Also, Meituan was the first to guarantee automatic refunds for customers whose purchases expired. While his competitors were burning cash to gain market share, Wang preserved funds, reckoning that other firms' ad spend at the time would help educate the customer but not necessarily breed loyalty. Through his frugal management he won the trust of major investors and was able to raise a huge round.

The strategy was counterintuitive but brilliant. By focusing on fewer, higher-quality deals, Meituan built a reputation for reliability. By guaranteeing refunds, it earned consumer trust. And by conserving capital while others burned through theirs, Wang positioned Meituan to outlast the competition.

Strategic Differentiation

The real insight, however, went deeper than operational efficiency. Wang recognized something that his competitors missed entirely.

As Wang later explained his philosophy: competitors "thought the business was group buying. We thought the business was e-commerce for services." This subtle but profound distinction would guide Meituan's evolution for the next decade.

Meituan's food delivery option, established in 2013, has become central to its revenue stream with the pandemic accelerating demand for food delivery adoption. Widely used, the service has emerged as a key driver of user engagement on the platform, pushing traffic to other offerings such as hotel and travel bookings.

By 2013, with rivals continuing to fade away, Wang shifted from volume discounts at restaurants to direct food delivery—a pivot that would define the company's future. Food delivery wasn't just another service; it was a high-frequency activity that could drive daily user engagement and serve as a gateway to countless other services.

Early Funding & Survival

The consolidation was swift. Meituan has survived thousands of Chinese group-buying sites to emerge on top, fighting of a spate of entrants that began in 2010.

Dianping then raised $850 million at a $4.05 billion valuation confirmed in April 2015. According to the Wall Street Journal, Dianping boasted more than 190 million monthly active users at the time, while Meituan generated $7.4 billion in transaction volume that year.

By 2014, Meituan had emerged as the clear leader, but the fight was far from over. A new competitor loomed—one backed by the resources of China's most powerful internet giant. To survive, Wang would need to make the most consequential deal of his career.

IV. The Meituan-Dianping Mega-Merger (2015)

The Strategic Context

Meituan was set up in 2010 as a group purchasing platform. In the following years, Meituan expanded the business and grew into one of the biggest online to offline platforms providing lifestyle services in China. Dianping, a consumer review website, was set up in 2003 and its services include viewing the information of various restaurants and stores, giving scores and making comments.

Dianping was, in essence, China's Yelp—a comprehensive database of user-generated reviews covering millions of local merchants. Founded by Zhang Tao in Shanghai in 2003, it had the consumer trust and review data that Meituan lacked. Meituan, in turn, had the transactional infrastructure and operational execution that Dianping envied.

With competition and pressure from Baidu and Alibaba, both Meituan and Dianping struggled to gain a dominant position due to significant flaws in their operating models. In order to safeguard themselves, they chose to merge.

The pressure was intensifying. Baidu spokesman Kaiser Kuo described the merger as "an extreme measure that shows just how seriously Meituan and Dianping view the threat from Baidu Nuomi". "Between March and September, Baidu Nuomi gained about two percentage points a month of market share by gross merchandise volume."

The Deal Structure

On October 8, 2015, Meituan and Dianping, a Chinese group buying site, became one company.

Two Chinese startups separately backed by Alibaba Group Holding Ltd. and Tencent Holdings Ltd. have agreed to a merger that will create a $15 billion provider of local services including restaurant reviews and movie bookings, people with knowledge of the matter said. The combination of Meituan.com, part-owned by Alibaba, with Tencent-backed Dianping.com may be announced as soon as Thursday, the people said. Meituan's shareholders will own about 60 percent of the combined company.

The structure reflected Meituan's stronger operational position. Wang Xing would lead the combined entity as CEO, with Dianping's Zhang Tao becoming chairman—a configuration that soon saw Wang consolidating control.

In 2015, Dianping merged with Meituan, a major player in the Chinese group-buying market, to form Meituan-Dianping. This merger created a formidable force in the online-to-offline (O2O) space, combining Dianping's review platform with Meituan's e-commerce capabilities.

Post-Merger Fundraising

On January 19, 2016, Meituan Dianping announced that it has raised more than $3.3 billion.

From that point forward, Meituan-Dianping became the decidedly dominant player in the daily deals space. The conglomerate went on to raise more than $7.3 billion in capital, raising its valuation from $18 to $30 billion in less than two years.

The merger followed a template that was becoming familiar in China's tech sector—the 2015 combination of ride-hailing rivals Didi Dache and Kuaidi Dache, and the merger of classifieds giants 58.com and Ganji.com. Chinese internet companies had discovered that in winner-take-all markets, it was often better to merge with your fiercest rival than to burn capital fighting them.

The merger between Dianping and Meituan will not only help consolidate their market share, but stem the massive spend both companies invest in subsidizing their services.

But this merger came with a complication that would soon tear apart the company's investor coalition: Alibaba had backed Meituan, while Tencent had backed Dianping. After the merger, both tech giants held stakes in the combined entity. The uneasy truce would not last.

V. The Alibaba-Tencent Proxy War & Food Delivery Dominance (2016-2018)

Breaking from Alibaba, Embracing Tencent

The Meituan-Dianping merger created one of China's most powerful consumer technology companies. But it also planted the seeds of conflict. Alibaba had been an early investor in Meituan, and Jack Ma expected loyalty—or at least deference.

Wang Xing provided neither.

Because he accepted Tencent's investment, he and Jack Ma had a falling out.

On the heels of the merger that produced China's ridesharing giant Didi Chuxing, Dianping and Meituan announced its deal to merge in October 2015. (After the merger, Alibaba sold its minority stake in the company.)

The divorce from Alibaba was acrimonious. Wang had chosen Tencent as his patron, and in China's zero-sum tech ecosystem, that meant making an enemy of Alibaba. The e-commerce giant would soon launch its own assault on Meituan's core business.

Meituan brokered a deal with Alibaba's longtime archrival, Tencent Holdings Ltd. Tencent agreed to lead Meituan's fundraising by pledging $1 billion, merge Tencent's own delivery service with Meituan, and let the combined company operate independently. The deal gave Meituan access to Tencent's WeChat ecosystem—the most valuable real estate in Chinese mobile internet.

Food Delivery as Core Business

By 2018, food delivery had become central to Meituan's identity and economics. Though the company operated across hundreds of categories—from hotel bookings to movie tickets—delivery drove daily engagement and defined the brand in consumers' minds.

The economics were brutal but scalable. Meituan had built a network of millions of delivery riders, sophisticated logistics algorithms, and deep relationships with restaurants. The network effects were powerful: more riders meant faster deliveries, which attracted more consumers, which attracted more restaurants, which required more riders.

Earlier this week, Alibaba said it would assume full control of Chinese food delivery platform Ele.me, a rival to Meituan. In April 2018, Alibaba acquired Ele.me at a whopping price-point of $9.5 billion—signaling that the e-commerce giant was not conceding the food delivery market without a fight.

The proxy war had begun in earnest. Meituan and Ele.me would spend billions on subsidies, rider incentives, and merchant acquisition over the following years.

The Mobike Acquisition

In this competitive crucible, Wang made one of his boldest moves: acquiring Mobike, one of the world's largest bike-sharing companies.

Meituan Dianping is buying bike-sharing firm Mobike for $2.7 billion excluding debt.

Tencent is an investor in Meituan Dianping and Mobike, and unifying the two could help Meituan Dianping battle Ele.me, the $9.6 billion delivery service that Alibaba just bought in full last week. Indeed, Caixin reports that Tencent CEO Pony Ma himself brokered the deal.

The strategic logic was compelling: bike-sharing represented the "last mile" of urban transportation, complementing Meituan's delivery network and providing another high-frequency touchpoint with consumers. Data analytics from Meituan's 320 million active customers revealed that a majority of users seek out transportation services to get to and from restaurants and other local lifestyle points-of-interest.

But the acquisition proved costly. China's once-booming bike-sharing market took a hit in 2018 as firms fought to dominate key cities. Tencent-backed Meituan incurred a net loss of 28.8 billion yuan ($4.4 billion) in the first half of that year, mainly due to Mobike's acquisition costs.

Chinese web company Meituan-Dianping acquired Mobike for US$2.7 billion in April 2018. Parent company Meituan-Dianping announced name change from Mobike to Meituan Bike on January 23, 2019 as part of an ongoing integration.

The Mobike deal significantly weighed on the company's financial performance for all of 2018. Meituan reported a net loss of 8.5 billion yuan ($1.26 billion) that year, triple the 2.85 billion yuan loss in 2017. But Wang was playing a longer game—building the super-app infrastructure that would eventually drive profits at scale.

VI. The Hong Kong IPO & Public Company Era (2018)

Going Public

Despite the losses and the competitive intensity, Wang pressed forward with plans to take Meituan public. The timing was delicate: markets were volatile, and Chinese tech IPOs had recently disappointed.

On September 20, 2018, Meituan Dianping debuted on the Hong Kong stock exchange at an IPO price of HK$69 per share.

The company raised $4.2 billion from its IPO, pricing its shares near the top of its target range. This made it the world's biggest internet-focused float since Alibaba's $25 billion New York listing in 2014.

The company's market cap reached about HK$400 billion (US$51 billion), exceeding that of many top Hong Kong companies on the benchmark index. The Beijing-based company, which raised US$4.2 billion in the city's second-biggest technology initial public offering this year, opened higher and briefly touched HK$74 per share.

Shares in Meituan, whose app is used by more than 300 million people, jumped as much as 7% in morning trading in Hong Kong. The stock ended the day up 5%, giving it a market value of about $50 billion.

The strong debut validated both Wang's strategic vision and investors' appetite for exposure to China's rapidly digitalizing consumer economy.

IPO Financials & Scale

The IPO prospectus revealed the scale of what Meituan had built. Surpassing China's second-largest e-commerce company JD.com, Meituan Dianping became the fourth-largest tech giant after BAT (Baidu, Alibaba, Tencent) in China.

"In the past eight years we have built the largest food delivery platform in China, and now every day we have 20 million people order food from us. We deliver in under 30 minutes. I think it is a huge market, because everyone needs to eat and most people eat three times a day, so now I think we are going to build a even bigger platform. Meituan Dianping is going to become one of the most important technology companies in people's lives in China," Wang told Bloomberg TV.

Meituan, which likes to call itself the "Amazon of services," is benefiting from Chinese consumers' enthusiasm for doing as much as possible through their phones.

Meituan is also - after Xiaomi - the latest company with a dual-class share structure to file for a Hong Kong listing, under the city's new rules designed to attract tech companies. The dual-class structure allowed Wang to maintain control of the company even as he sold shares to public investors—ensuring that strategic decisions would remain in the hands of the founder who had navigated Meituan through so many competitive battles.

VII. Super App Expansion & COVID-19 Acceleration (2019-2020)

Business Diversification

By 2019, Meituan had evolved far beyond its group-buying origins. He is known for building the lifestyle empire Meituan-Dianping, with businesses encompassing food delivery, internet group purchases, taxi-hailing, bike sharing, travel and a variety of leisure services.

Meituan entered the hotel and travel services space in 2015. Since then, it has expanded partnerships with over 900 hotel chains.

The analogy often used is apt: Meituan represents an amalgamation of DoorDash, Yelp, MakeMyTrip, Uber, and Mobike—all bundled into a single ecosystem where consumers can order dinner, book a hotel, hail a ride, and rent a bike without ever leaving the app.

The key insight driving this expansion was frequency. Food delivery is a daily activity; hotels are booked occasionally. But by bundling high-frequency and low-frequency services together, Meituan could acquire customers cheaply through food delivery and monetize them across higher-margin services like hotels and travel.

Community Group Buying & COVID Response

When COVID-19 hit China in early 2020, Meituan's delivery infrastructure proved essential. Lockdowns transformed food delivery from a convenience into a necessity, and the company's logistics network became critical infrastructure.

Meituan Select, launched in 2020 during the pandemic, targeted a different segment entirely: lower-tier markets and non-immediate demand products. The platform uses a bulk purchasing model, grouping orders and enabling cost savings for customers. By early 2021, Meituan Select covered more than 20 provinces, representing the company's push into rural China.

The company has successfully expanded its Meituan InstaMart and Xiaoxiang operations, particularly in lower-tier cities, meeting growing consumer demand.

The pandemic period also accelerated Meituan's investment in autonomous technologies. In April 2021, Meituan raised $9.98 billion in additional financing via the sale of $3 billion in convertible bonds and $7 billion in equities. The funds will be used to expand into China's groceries space as well as to develop autonomous technologies in the drone and delivery space.

VIII. Regulatory Storm & The Tech Crackdown (2021)

The Antitrust Investigation

The year 2021 brought a reckoning for China's technology giants. Beijing, increasingly concerned about the power of private tech companies, launched a sweeping regulatory crackdown that would reshape the entire sector.

Meituan has seen around $38.96 billion wiped off its value in the past two weeks as Beijing turns its regulatory scrutiny on the Chinese food delivery giant. On April 26, China's State Administration for Market Regulation (SAMR) opened an investigation into "suspected monopolistic practices" of Meituan.

SAMR in April began investigating Meituan over abuses of its dominance in China's online food delivery market, including practices known as "picking sides," in which a platform forces merchants to work exclusively with it and shun competitors. The regulator found that since 2018, Meituan has abused its dominant market position to implement different rates on merchants, force them to enter exclusivity agreements.

The practice of "picking sides"—forcing merchants to choose between Meituan and competitors like Ele.me—had been widespread across China's internet platforms. But with regulators newly aggressive, Meituan faced its most serious crisis since the Thousand Groupon War.

The Record Fine

China's market regulator levied a 3.44 billion yuan ($533 million) fine on Meituan for anti-competitive practices, ending a months-long probe on the food-delivery giant.

Meituan's 3% penalty was less both in value and percentage than a record 18 billion yuan fine handed to Alibaba in April, also for anti-competitive behavior. The fine was calculated as 3% of the company's domestic sales for 2020, a relatively lenient penalty. Meituan will also have to return 1.29 billion yuan of merchant deposits which were taken as part of exclusivity agreements that the regulator ruled unlawful.

The penalty, while substantial, was manageable for a company of Meituan's scale. More significantly, it marked the end of regulatory uncertainty—allowing the company to move forward with a clear understanding of the new rules.

The Poem Incident

In the midst of the regulatory storm, Wang Xing made an uncharacteristic misstep. On 3 May 2021, Wang posted a Tang Dynasty (618–907 AD) poem about book burning on Fanfou, a social media platform owned by himself. The action was reported by Quartz News as a veiled swipe against the general secretaryship of Xi Jinping's clampdown on civil society, intellectual and academic freedom since ascension to office. The poem, entitled "Book Burning Pit," speaks about the late emperor Qin Shi Huang's practice of beheading scholars and burning books, only to be overthrown by illiterate rebels later during his reign. As a result of the post, Meituan's shares plunged 7.1% on the same day, wiping $36.98 billion from the company's market cap over the subsequent weeks.

Wang deleted the post and issued a clarification on May 9. He noted the emperor was overthrown by two people who didn't have much of an education and used it to express a business lesson. "This reminds me that the most dangerous rivals are usually not those you expect."

The incident highlighted the delicate position that China's tech entrepreneurs occupy—successful enough to attract regulatory attention, yet ultimately subordinate to political authority. Wang's clarification recast the poem as a business observation rather than political commentary, but the episode served as a reminder of the constraints within which Chinese tech companies operate.

IX. Modern Era: Competition & International Expansion (2022-Present)

Intensifying Competition

Emerging from the regulatory storm, Meituan faced new competitive challenges. ByteDance's Douyin poses a significant threat to Meituan, with the widely-used short video platform reporting a 256% growth in gross merchandise volume (GMV) for local life services last year. Zhang characterized Douyin as an influential and rational opponent, describing the ongoing battle as a "brutal and tormented warfare" without an immediate winner.

China's food delivery industry has been relatively quiet since the dust of the war between Meituan and Douyin settled. As our previous reports on Douyin's ventures into the local services market described, Douyin captured a substantial part of the in-store group buying market. Still, it failed to challenge Meituan significantly in the delivery market.

Meituan and Ctrip dominate food delivery and travel bookings, but ByteDance uses Douyin to embed these services into daily content consumption. A user can watch a restaurant video, click a voucher, and book instantly without leaving the app. While ByteDance lacks Meituan's logistics depth, its advantage lies in discovery-driven engagement that introduces new merchants to consumers organically.

The competitive landscape shifted dramatically in early 2025. On February 11, 2025, JD.com officially launched JD Takeout, with delivery mainly being handled by Dada Express.

JD.com's entry into the food-delivery market has shaken up a sector dominated by Meituan and Alibaba-owned Ele.me. In February, JD unveiled JD Takeaway, promising zero commissions for merchants who joined early.

The 2025 Subsidy War

The competition escalated into what observers called an "irrational" subsidy-driven price war. In less than 100 days, China's food delivery landscape has been reshaped by an intense subsidy war, with JD.com and Alibaba together pledging a staggering RMB 80 billion (around $11 billion) to challenge Meituan's dominance.

In China's fiercely competitive market, the latest price war is playing out in the growing "instant commerce" sector, where companies are launching massive subsidies and other incentives to get consumers to spend. The 'instant commerce' sector is backed by massive networks of scooter drivers that quickly transport everything from food and drink to fast fashion and gadgets. The space is mostly occupied by three main players, including the established e-commerce heavyweights JD.com and Alibaba, as well as delivery platform Meituan.

Transactions on these platforms surged from 100 million daily orders at the start of the year to 250 million by mid-July, according to the South China Morning Post.

When asked about the recent surge in orders driven by Alibaba's aggressive coupon and discount campaigns, Wang remarked, "Orders are just numbers," and highlighted that order count and valuable gross transaction value (GTV) are two different things. Speaking on the rapid rise of China's instant retail market, from 100 million daily orders earlier this year to 250 million on July 12, Wang bluntly labeled "most of it a bubble."

Operating profit plummeted from 15.2 billion yuan in the second quarter of 2024 to 3.7 billion yuan in the same period of 2025, with the operating profit margin decreasing from 25.1% to 5.7% year-on-year.

The profitability collapse was dramatic but, in Meituan's view, necessary to defend market position. By August 2025, regulators intervened. Meituan, Alibaba Group Holding Ltd., and JD.com Inc. vowed Friday to curb "disorderly competition" and cease the price-based rivalry that's threatened to erode margins and prompted warnings from government agencies. Hong Kong-listed shares in all three companies rose after they issued statements within minutes of each other pledging to promote a fair business environment. The three companies have sought to out-do each other with a series of discounts and subsidies aimed at carving out a greater share of the $80 billion-plus food delivery market.

International Expansion: KeeTa Goes Global

While defending the domestic market, Meituan simultaneously pushed into international markets—its first significant move beyond mainland China.

In May 2023 Meituan launched its first food delivery service - named Keeta. It was the first time Meituan offered its products outside of mainland China. Keeta began operating in the districts of Mong Kok and Tai Kok Tsui, with plans to expand to the rest of Hong Kong by the end of 2023.

Keeta's path to gain market share quickly appears to follow a playbook that it tested out in Hong Kong. A year after its entry in Hong Kong, Keeta had toppled the original duopoly of Foodpanda and Deliveroo by leading in order volume by May 2024, according to a report from Measurable AI, a consumer data company.

The Hong Kong success provided a template for broader expansion. As of now, Keeta has entered 9 cities across Saudi Arabia, essentially covering all cities with populations over one million. Our performance in Saudi Arabia has also been quite encouraging.

In September 2024 Meituan launched its platform Keeta in Riyadh, Saudi Arabia offering free deliveries and discounts during its initial launch phase for customers. Meituan announced plans to capture up to 80% of the Saudi Arabian food delivery market by 2025. Keeta's expansion plans align with Saudi Arabia's vision for 2030, with an investment of SR1 billion ($266.6 million) to improve operations, create jobs, and enhance services.

Our future expansion into Brazil has drawn more attention recently, particularly after President Lula visited China last month and signed an investment memorandum with us, in which we plan to invest USD 1 billion over the next five years to develop Meituan's business in Brazil. Brazil is arguably the farthest country from us — it's on the other side of the world. A flight from Beijing to São Paulo takes at least 25 hours. But we're not deterred by the distance. We believe Brazil is a promising market.

Wang Xing, Meituan's founder and CEO, stated, "Internationalization is one of Meituan's long-term development strategies, and we will continue to push forward in expanding overseas markets. In the Asia-Pacific and Middle Eastern regions, our valuable experience and advanced technology in the delivery industry will benefit users, and this excites us."

Autonomous Technology & AI Investment

While fighting competitive wars, Meituan has been quietly building the infrastructure for the next generation of delivery—drones and autonomous vehicles that could fundamentally reshape unit economics.

Chinese food delivery firm Meituan announced that its self-developed fourth-generation drone has passed a regulatory review by the Civil Aviation Administration of China, earning the country's first operating certificate for nationwide low-altitude logistics coverage. The license would allow Meituan to launch regular commercial drone delivery services across China, marking a significant milestone in the company's push to scale up its autonomous logistics network. Since the establishment of Meituan's drone unit in 2017, the company has opened 53 delivery routes in major cities including Shenzhen, Beijing, Shanghai, Guangzhou, and Nanjing. By the end of 2024, Meituan drones had completed over 450,000 orders.

On 20 March 2025, Meituan, China's market leader in food delivery and quick commerce, officially launched drone delivery service in Hong Kong. At the launch ceremony, Hong Kong Chief Executive John Lee gave the takeoff command in person. Moments later, Meituan's "Keeta" drone completed the city's inaugural low-altitude logistics drop, landing a meal at the Hong Kong University of Science and Technology.

Meituan's core delivery network is already highly optimized. Further gains from traditional couriers will likely be incremental. But autonomous drones could break through that ceiling.

In late August 2025, Meituan officially released and open-sourced its large language model LongCat, also known as LongCat-Flash or LongCat-Flash-Chat. The announcement was made via Meituan's official social media account on August 31, 2025, X (formerly Twitter).

X. Investment Analysis: The Bull and Bear Case

Financial Performance & Metrics

In the third quarter of 2024, Meituan Dianping reported significant financial growth, with revenues reaching RMB 93.6 billion, marking a 22.4% increase from the previous year.

Meituan (MPNGF) reported a 22.4% year-over-year increase in total revenue, reaching RMB93.6 billion. Adjusted net profit surged by 124% to RMB12.2 billion, showcasing significant profitability improvements.

On May 26, China retail technology company Meituan (stock code: 3690.HK) released its Q1 2025 financial report. The report shows Meituan's revenue for the first quarter reached CNY 86.6 billion, an 18% year-on-year increase, and the net profit was CNY 10.06 billion, an 87.3% year-on-year increase.

However, the subsidy war has significantly impacted recent quarters. Due to the intensified competition in food delivery sector, the operating profit of our Core local commerce segment significantly declined to RMB3.7 billion for the second quarter of 2025 on a year-over-year basis. Meanwhile, the operating loss for our New initiatives segment expanded to RMB1.9 billion due to overseas expansion on a year-over-year basis. As a result, our adjusted EBITDA and adjusted net profit for this period declined to RMB2.8 billion and RMB1.5 billion, respectively.

Competitive Dynamics: Porter's Five Forces Analysis

Threat of New Entrants: Medium-High While Meituan has established formidable network effects and logistics infrastructure, the 2025 entry of JD.com demonstrates that well-resourced competitors can mount serious challenges. The key barriers are delivery rider networks and merchant relationships—both of which can be breached with sufficient capital.

Bargaining Power of Suppliers (Restaurants): Medium Merchants depend on Meituan for customer traffic, but the duopoly structure with Ele.me (and now JD) gives them some negotiating leverage. The antitrust fine and subsequent regulatory scrutiny has increased merchant power by limiting exclusivity practices.

Bargaining Power of Buyers: High Consumers face low switching costs between delivery platforms and have demonstrated willingness to follow subsidies. User loyalty remains questionable when competitors offer aggressive promotions.

Threat of Substitutes: Medium Physical dining remains the primary alternative, and its share has been relatively stable post-pandemic. However, changes in consumer behavior—such as cooking at home during economic uncertainty—represent latent competitive pressure.

Competitive Rivalry: Very High Meituan still holds a commanding share of over 70% in the food delivery market, and that lead won't be easy to shake. But growth now hinges more on supply-side tweaks.

The intensity of competition has reached extraordinary levels. JD's push into food delivery may have generated a loss of more than 10 billion yuan in the second quarter, according to Nomura's analysis published Thursday.

Hamilton Helmer's 7 Powers Analysis

Scale Economies: Strong Meituan's logistics network benefits from density economics—more orders in an area allow more efficient routing, reducing per-order costs. In the domestic market, Meituan has focused on deepening its food delivery business and successfully built a real-time delivery network that supports over 60 million orders daily. In addition, Meituan has developed a leading global order allocation system and algorithms, strong logistics capabilities, and rich offline operational experience.

Network Effects: Strong The denser the distribution of merchant outlets, the more riders there are, which in turn increases customer traffic, effectively reducing the overall cost rate. This is undoubtedly a solid moat for Meituan.

Counter-Positioning: Moderate Meituan's super-app model combines multiple services in ways that would require significant restructuring for competitors to replicate. Alibaba and JD are both attempting to build similar ecosystems, but from different starting points.

Switching Costs: Low Individual users can easily switch between Meituan, Ele.me, and JD Takeaway. Merchant switching costs are somewhat higher due to integration work, but the platform's attempt to enforce exclusivity was deemed anti-competitive.

Branding: Moderate The yellow Meituan brand is ubiquitous in Chinese cities, but food delivery has proven to be a commodity-like service where price trumps brand loyalty.

Cornered Resource: Moderate Meituan's historical data on Chinese consumer preferences and restaurant performance represents a valuable resource, though not truly irreplaceable.

Process Power: Strong Years of optimization have produced sophisticated logistics algorithms that competitors must work to replicate. He described food delivery as "a delicate and low-margin business," claiming that no one understands the industry's mechanics better than Meituan.

Bull Case

-

Dominant Market Position: Despite intense competition, Meituan maintains 65%+ market share in food delivery—the highest-frequency local services category.

-

Super-App Ecosystem: Cross-selling opportunities across food, hotels, travel, and services provide revenue diversification and customer retention.

-

International Expansion: Keeta's early success in Hong Kong and Saudi Arabia suggests the model can travel, opening a significant new growth vector.

-

Autonomous Technology: If drones and self-driving vehicles can meaningfully reduce delivery costs, Meituan's investments could deliver significant margin expansion.

-

Regulatory Clarity: The 2021 fine resolved major regulatory uncertainty; intervention in the 2025 subsidy war may actually benefit Meituan by limiting competitors' ability to buy market share.

Bear Case

-

Subsidy War Destruction: The current competitive intensity has obliterated margins, and there's no guarantee that profitability will recover to previous levels.

-

JD.com Commitment: Experts say one aim of JD's attack is to distract and pressure Meituan from its incursion into e-commerce, ultimately protecting JD's core business. If JD views food delivery as strategically necessary regardless of profitability, the competitive pressure could persist for years.

-

Consumer Behavior Shift: In an economically uncertain environment, Chinese consumers have become more price-sensitive. This favors whoever offers the deepest subsidies, not necessarily the best service.

-

Regulatory Risk: China's tech sector remains subject to political considerations that are difficult to predict. Wang Xing's 2021 poem incident demonstrated the reputational risks.

-

International Execution: Expanding to Brazil and the Middle East involves navigating vastly different regulatory environments, consumer preferences, and competitive dynamics. Success is not guaranteed.

XI. Key Performance Indicators to Watch

For investors tracking Meituan's ongoing performance, three metrics deserve particular attention:

1. Core Local Commerce Operating Margin This metric captures the profitability of Meituan's dominant food delivery and in-store businesses. The collapse from 25.1% to 5.7% in Q2 2025 reflects subsidy war intensity. Recovery toward historical levels (15-25%) would signal competitive normalization.

2. Gross Transaction Value (GTV) per Transacting User With 770+ million transacting users, growth must increasingly come from wallet share rather than user acquisition. Rising GTV per user indicates successful cross-selling and ecosystem deepening; declining GTV suggests subsidy-driven volume without real engagement.

3. International Operating Losses as Percentage of Revenue As Keeta expands globally, the investment required will weigh on profitability. Investors should monitor whether international losses are declining as a percentage of revenue—indicating a path to sustainability—or expanding, which could suggest execution challenges.

XII. Conclusion: The Infinite Game Continues

Wang Xing's intellectual framework—drawn from James Carse's concept of finite versus infinite games—provides the appropriate lens for understanding Meituan. Where competitors see discrete battles to be won or lost, Wang sees an endless process of adaptation and expansion.

This orientation explains both Meituan's successes and its current challenges. The company's willingness to sacrifice short-term profitability for long-term position—visible in the Mobike acquisition, the community group buying push, and the international expansion—reflects infinite game thinking. So does its patience in developing autonomous delivery technology over eight years before achieving meaningful scale.

Yet the infinite game framework also explains why Meituan finds itself in an expensive war of attrition. If Wang truly believes that "orders are just numbers," then ceding market share to heavily-subsidized competitors becomes intolerable regardless of the immediate financial impact.

Wang Puzhong, CEO of Meituan's Core Local Commerce once predicted the subsidy war could be ended in three ways: one side being completely defeated or acquired; a stalemate leading to mutual retreat; or intervention from a higher authority to force a truce. Judging by the current developments, the third scenario may be playing out.

The regulatory intervention of 2025 may provide the off-ramp that no competitor could admit to wanting. If the subsidy war truly ends, Meituan's operational advantages—its logistics efficiency, its merchant relationships, its data moat—should reassert themselves.

But the competitive landscape has permanently changed. JD.com has established a delivery capability that won't simply disappear. Alibaba's Ele.me remains well-funded and determined. And Douyin continues to explore local services from its position as China's attention gatekeeper.

What hasn't changed is Wang Xing himself—still posting philosophical observations on Fanfou, still thinking in decades rather than quarters, still playing the infinite game he first discovered in a Delaware graduate library more than twenty years ago. For investors betting on Meituan, they're ultimately betting on Wang's ability to keep playing—and winning—a game that never ends.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube