U-Haul Holding Company: America's Orange Empire

Introduction: The $5,000 Startup That Became a Verb

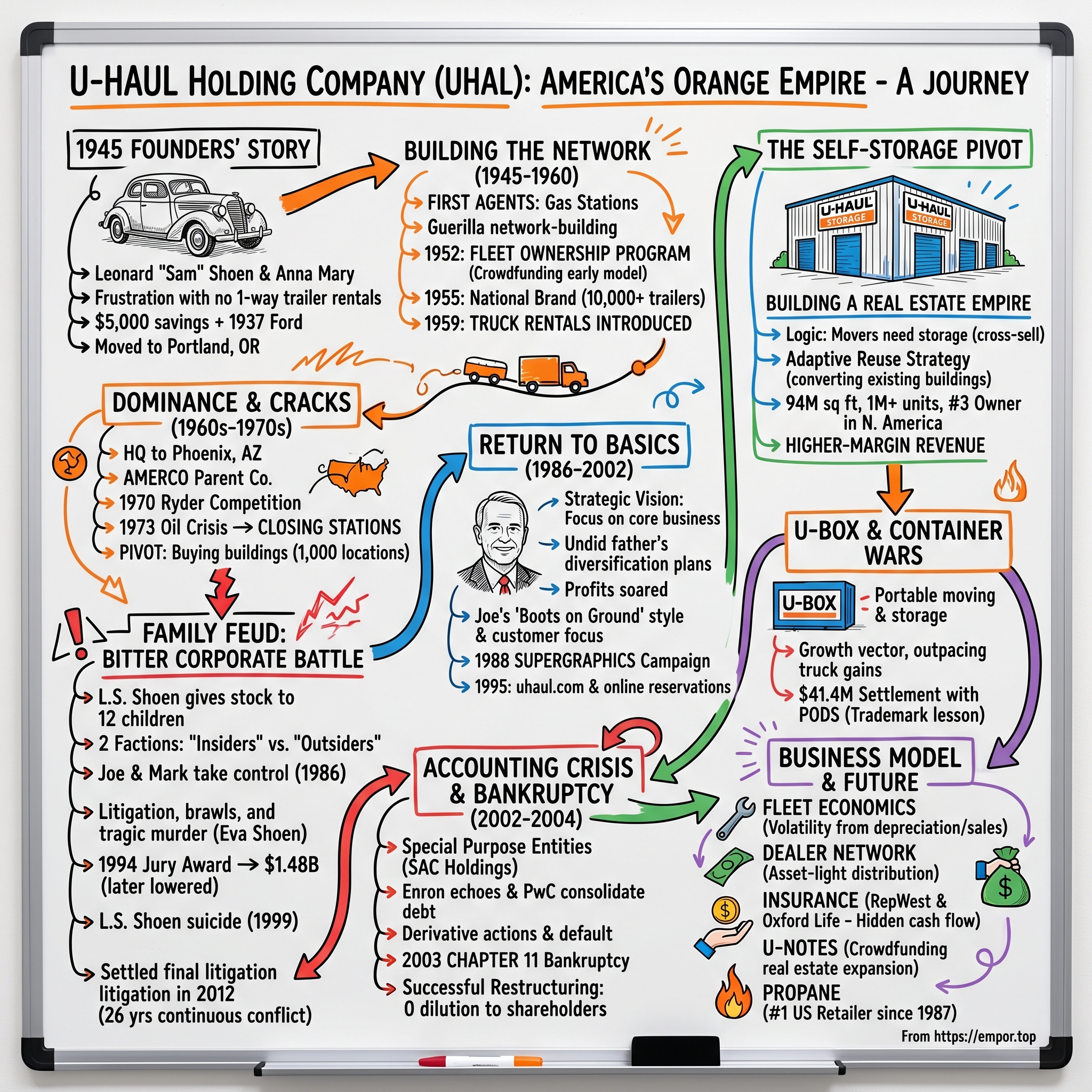

Picture the summer of 1945. World War II has just ended, and across America, millions of young families are on the move—GIs returning home, couples chasing suburban dreams, workers following the postwar industrial boom. On a dusty road between Los Angeles and Portland, Oregon, a 29-year-old Navy veteran named Leonard "Sam" Shoen sits behind the wheel of his 1937 Ford with his wife Anna Mary and their young son, their possessions crammed into whatever would fit. They had tried to rent a trailer for the journey. It couldn't be done.

That frustration—the simple inability to rent a one-way trailer—planted the seed for what would become one of the most recognizable brands in American history. With a 1937 Ford and $5,000 in savings, Sam, Anna Mary and their young son moved from Los Angeles to Portland, Oregon. During the drive, they came up with the name and formulated the outline of what was to become the U-Haul Trailer Rental System.

Eighty years later, U-Haul stands as something extraordinary: a company so ubiquitous that its name has become synonymous with self-moving. The company operates a network of more than 23,000 locations across all 50 states and 10 Canadian provinces, with a fleet of approximately 192,000 trucks, 138,700 trailers and 39,500 towing devices. U-Haul is the third largest self-storage operator in North America, offering 1,024,000 rentable storage units and 88.5 million square feet of self-storage space.

The numbers are staggering for what started as a handful of orange trailers on gas station lots. In 2024, U-Haul Holding Company's revenue was $5.83 billion. The company has a market cap of approximately $10.32 billion as of late November 2025, though that represents a decrease of 26.89% over the past year—a decline driven by the same fleet economics that have defined this business for decades.

But the financial metrics only tell part of the story. U-Haul's journey encompasses one of the most vicious family feuds in American corporate history, a bankruptcy that became a case study in restructuring, and a strategic pivot into real estate that is reshaping the company's future. The question for investors today isn't whether U-Haul is a great business—it clearly is—but whether the company can successfully navigate its transformation from a truck rental operator to a self-storage real estate empire while managing the family dynamics that have defined its existence.

The Founder's Story: From Depression-Era Poverty to American Icon

To understand U-Haul, you must first understand Leonard Samuel Shoen. Leonard Samuel Shoen was an American entrepreneur who founded the U-Haul truck and trailer organization in Ridgefield, Washington. After growing up in the farm belt during the Great Depression, he envisioned the market for rental vehicles for families who wished to avoid the expense of professional transfer and storage companies.

His father moved the family to Oregon in 1923 to farm in the Willamette Valley near Shedd. Shoen worked his way through Oregon State University by running a chain of beauty parlors and barber shops—an early hint of the entrepreneurial hustle that would define his career. The man who would build a billion-dollar empire started out cutting hair to pay tuition.

Shoen served in the U.S. Navy as a Hospital Apprentice First Class in Bayview, Idaho, and Seattle, and was given a medical discharge in 1945 for rheumatic fever. It was during his military service, moving his family from base to base in borrowed trailers, that Shoen first glimpsed the business opportunity hiding in plain sight.

Discharged from the Navy in the summer of 1945, 29-year-old Sam and Anna Mary tried to rent a utility trailer to move their possessions from Los Angeles to Portland, Oregon. It couldn't be done. They had to take only what they could fit in the car. "No one, at that time, seemed ready or willing to serve that need."

What made Shoen different from the millions of other Americans who faced the same frustration was his response. In 1945, at the age of 29, Shoen co-founded U-Haul with his wife, Anna Mary Carty, in Ridgefield, Washington, just north of Vancouver. Anna Mary was the mother of Shoen's first six children. The company was started with an investment of $5,000. In the early years, the Shoens routinely worked 16-hour days and reinvested all their earnings back into the business.

The early trailers were far from polished. The Shoens built them on the Carty Ranch, using whatever materials they could find, often assembling frames on the running gear of scrapped automobiles. The business model was elegantly simple but revolutionary: paint the trailers bright orange so they're instantly recognizable, partner with gas station owners who have unused lot space and need additional revenue streams, and let customers return trailers to any participating location—the one-way rental that professional movers couldn't match.

The first trailers were bought from welding shops or second hand from private owners. Within two weeks of leaving Los Angeles, the first U-Haul trailer was parked on a service station lot and being offered for rent. By the end of 1945, 30 4' x 7' open trailers were on service station lots in Portland, Vancouver and Seattle, Washington. An identity was established. First, the trailers were painted bright orange.

Shoen often gave renters discounts on their trailer rentals if they would find a reputable gas station that would agree to rent U-Haul trailers in the cities to which they moved. This was guerrilla network-building at its finest—customers became salespeople, expanding the network with every move.

Building the Network: The 1945-1960 Foundation Years

The early years tested Shoen's resolve. The purchased trailers—often built on scrapped automobile parts—broke down with painful frequency, sometimes costing more to repair than rental fees could cover. To survive, Sam and Anna Mary moved in with her parents on the Carty Ranch, cutting expenses to the bone while keeping the dream alive.

But Shoen's genius lay in recognizing that network effects could work for physical assets just as powerfully as they would later work for digital platforms. Every new dealer location made every other location more valuable because customers could now complete one-way moves to more destinations. Every returning trailer at a popular destination created inventory exactly where demand existed.

He began building rental trailers at the Carty Ranch in Ridgefield, owned by his parents-in-law, and splitting the fees for their use with gas station owners whom he franchised as agents. The first U-Haul Rental Agent was a Mobil station on Interstate St. in Portland. These early deals were based on little more than a wink and a nod.

By 1952, Shoen had developed another innovation that would fuel expansion: the company established a fleet ownership program that enabled investors (including dealers and eventually employees) to purchase trailers for the U-Haul fleet in return for future dividends. This crowdfunding-before-crowdfunding approach let U-Haul grow its fleet without burdening the balance sheet with debt—a strategy the company would return to decades later with its U-Notes program.

By 1955, there were more than 10,000 U-Haul trailers on the road and the brand was nationally known. A decade after two people and $5,000 started the company, U-Haul had become a household name.

By the end of 1959, the U-Haul trailer fleet consisted of 42,600 trailers. But what made 1959 a true milestone wasn't just fleet growth—it was the introduction of rental trucks. U-Haul trucks were designed specifically for residential moving by do-it-yourself families, opening a market segment that would eventually dwarf the original trailer business.

For investors studying U-Haul's history, the early years reveal a pattern that persists today: the company succeeds by making each individual asset more valuable through network membership. A U-Haul truck in Phoenix isn't just a truck—it's a node in a continental network that makes one-way moves possible. This network effect, built painstakingly over decades, creates a competitive moat that pure-play truck rental competitors struggle to replicate.

Dominance and the First Cracks: 1960s-1970s

By the 1960s, U-Haul had achieved something remarkable: it was the preeminent do-it-yourself moving company in North America. In 1967, at the height of the company's success, Shoen moved his corporate headquarters to Phoenix, Arizona.

In the 1960s, Shoen diversified his holdings by creating AMERCO Inc., from Advanced Management Engineering and Research Company. He pronounced the acronym, "a miracle." AMERCO remains the parent company of U-Haul and related businesses.

But success brought new challenges. The first critical change arose from the founding in 1970 of Ryder System Inc. in Miami. Ryder copied the U-Haul model and became a formidable competitor, eventually growing to near-parity. In 1989 U-Haul and Ryder each controlled nearly 45 percent of the United States market for do-it-yourself rentals of trailers and trucks.

Then came the 1973 oil crisis, which struck at the heart of U-Haul's basic business by curtailing American mobility. The energy crisis also caused fundamental changes in gasoline distribution, resulting in the closing of many independently owned service stations that comprised U-Haul's dealership network. In response, L.S. bought up nearly 1,000 buildings in 1975, many of them cast-off Chrysler dealerships, and began opening company-owned locations.

But it was Shoen's response to the earnings decline that planted the seeds of family conflict. L.S. rose to the challenge with a grand diversification plan that struck many observers—including his own children—as eccentric at best and disastrous at worst. He turned his dealerships into "garden centers," buying bizarre assortments of equipment: furnishings from the Far East, jet skis, lawn mowers, champagne fountains, and folding dance floors. Many dealers had no idea how to market these products.

Meanwhile, Shoen's personal life had grown increasingly complex. While distracted to some extent by growing his business, Shoen also managed multiple marriages after the death of his first wife from a congenital heart defect, and eventually had a total of 12 children, each of whom he made a stockholder. Shoen married Suzanne Gilbaugh in 1958, and they had five more children.

L.S. laid the seeds of his later problems by doling out generous amounts of stock in the company to each of his children. He ended up giving them no less than 94 percent of the company, a move that he would later regret. Referring to the giveaway in a 1988 letter, he wrote: "My ignorance has resulted in much evil."

By distributing stock to twelve children from four different marriages—children who grew up in bunches, with different mothers and different relationships to one another—Shoen created the conditions for one of the most bitter family feuds in American corporate history.

The Family Feud: America's Bitterest Corporate Battle

The story of the Shoen family feud reads like a Greek tragedy—or perhaps more accurately, like something Eugene O'Neill might have written. The story of the Shoen family feud is complex and twisted. There is so much intrafamily violence, it could be the basis of a Eugene O'Neill tragedy. Scattered throughout the family history are totally bizarre acts, threats of violence and a couple of brutal beatings Shoen's sons administered to each other in full view of their father.

Joe Shoen is the third son of U-Haul founder Leonard Shoen. He was raised in Phoenix, Arizona. He attended the College of the Holy Cross, where he graduated with a Bachelor of Arts, and then received a Master of Business Administration from Harvard Business School. He wrote his thesis at Harvard on self-storage businesses. That thesis topic would prove prophetic.

By 1979 Joe and Mark Shoen had resigned from U-Haul because of this dispute over the direction of the company, and a year later Mark's relationship with his father and brother Sam deteriorated still further when they refused to help him out of a financial predicament by buying some of his AMERCO stock. Mark Shoen, who later became president of U-Haul International, noted in an interview with the Los Angeles Times, "[We] were millionaires in name only. We were told we were wealthy, but we didn't have enough money to buy a car."

The fundamental dispute was strategic: The father wanted the company to diversify into the general rentals business while the sons insisted on focusing on its core moving business.

The drama surrounding Phoenix-based U-Haul began in 1986 when the Shoen brothers took control of the company and forced their father, Leonard, into early retirement. The move split the family into warring factions.

By 1986 Joe and Mark Shoen had drummed up enough support among their brothers and sisters to oust L.S. Shoen as chairman of the corporation. The company's finances at that point were precarious: net profits sank to $9.2 million in 1986 and $2.2 million a year later, down from $42 million two years earlier, and debt ballooned to nearly $600 million.

The takeover triggered years of litigation, but the violence extended far beyond courtrooms. In March of 1989 the company's annual meeting allegedly turned into a brawl when L. S. Shoen and his son Mike attempted to set up a tape recorder to record the proceedings.

Then came the murder. In Montrose, Colorado, an ex-con named Frank Marquis admitted that he fatally shot Mrs. Eva Shoen, the wife of Sam Shoen, the oldest son, in Telluride, Colorado, in 1990. But even Marquis' admission from the witness stand that he fired the fatal shot on his own, and that there was no murder-for-hire scheme devised by any of the feuding Shoen brothers, does not bring closure.

The story moved from the business pages to tabloid TV in 1990, when Eva Berg Shoen, the wife of another Shoen son, Sam, was shot to death at the family's cabin in posh Telluride, Colorado. At the time, Leonard Shoen made statements to reporters linking Joe and Mark to the killing, accusations that later became the focus of a libel lawsuit. In November 1994, a New Mexico man was sentenced to 24 years in prison for shooting Eva Shoen in a botched robbery.

The family battle culminated in October 1994 when a Maricopa County Superior Court jury ordered the faction led by Joe and Mark Shoen to pay $1.48 billion to the "outsiders" that include Leonard Shoen and the remaining siblings. A judge later lowered that award to $461 million.

In a sad postscript to the family feud, L.S. Shoen died in October 1999 at the age of 83, apparently having committed suicide by driving his car into a power pole.

U-Haul only recently escaped from the quagmire of family infighting, settling the last of the litigation in 2012. That's 26 years of continuous legal warfare—more than a quarter-century of family dysfunction playing out in courtrooms while employees tried to run a business.

For investors, the family history carries important implications. The Shoen family still controls approximately 40-55% of the company through various holdings. As a family company – Shoen's children Stuart, Sam, and Royal all work for U-Haul – Shoen feels they have more in common with smaller operators than one might think. The third generation is now in leadership positions, raising questions about succession planning that have plagued family businesses throughout history.

The Return to Basics: Joe Shoen's Turnaround (1986-2002)

Whatever one thinks of the family politics, Joe Shoen's strategic vision proved correct. The second generation of Shoens to operate the company moved quickly to undo their father's diversification experiments and return focus to the core moving services that made U-Haul famous.

The brothers moved quickly after assuming control of the company to return it to its basic businesses. They kept U-Haul's rental storage facilities but eliminated many of the company's extraneous rental offerings, focusing on trucks and trailers, boxes, moving pads, and packing materials as featured items at the company's U-Haul Centers.

The results were dramatic. Amerco earned $60 million in the fiscal year ended in April, up from $2.2 million when the brothers took over in 1987. Revenue rose 9.3 percent in the past year to $1.2 billion.

Joe Shoen's management style became legendary within the company. "He's boots on the ground. That's how he knows what's going on. He's always in our field operations, learning, listening, watching, doing," says Bob Wesson, a longtime U-Haul exec. At each location Shoen prints out a P&L statement and asks the manager what Shoen can do to make the business better. He jots down ideas on a pad, then snaps a photo of his notes with his phone to text to his assistant, who then often turns it into a memo to the employees.

The longtime CEO of U-Haul's parent company, Amerco, Shoen has personally responded to customer calls—on average three a day, but sometimes dozens in hours—since he gave out his cellphone number on the TV show Inside Edition in February 2008.

In 1988, U-Haul launched its SuperGraphics campaign, bringing captivating state- and province-themed images to the sides of U-Haul trucks and trailers everywhere—a marketing innovation that cost nothing in media spend but turned every truck into a rolling billboard.

In 1995, U-Haul embraced the digital revolution, launching uhaul.com and making online reservations available. For a company built on physical assets and local dealer relationships, this was a significant cultural shift.

But even as operations improved, the company was building a hidden time bomb on its balance sheet.

The Accounting Crisis & Bankruptcy: 2002-2004

The early 2000s brought U-Haul uncomfortably close to the Enron scandal—not through fraud, but through the same accounting structures that destroyed Enron's credibility.

In 1994 so-called special purpose entities (made infamous by Enron Corporation) collectively known as SAC Holdings had been set up by U-Haul President Mark Shoen to own land where U-Haul storage facilities were based. In February 2002, in the wake of the Enron scandal, AMERCO's auditor, PricewaterhouseCoopers (PwC), told AMERCO that it had to consolidate the results of SAC Holdings with AMERCO and restate the latter's financial results for the previous seven years. During fiscal 2003 the company did so, and the consolidation of SAC Holdings' debt sharply reduced AMERCO's net earnings and net worth.

In September, Paul Shoen, the brother of President Edward Shoen and COO Mark Shoen, filed a derivative action on behalf of AMERCO against SAC Holdings and certain directors and executives of AMERCO alleging breach of fiduciary duty, unjust enrichment, and other causes of action. Over the next few months and into 2003, challenges continued to mount. AMERCO failed to make a $100 million principal payment due to its Series 1997-C BBATs, placing the entire capital structure in default.

Indeed, in October 2002, AMERCO missed a $100 million bond payment and later missed a second payment. Unable to secure new financing, the company filed for Chapter 11 bankruptcy protection in June 2003 to expedite the restructuring of its debt. The filing was unusual in that the company aimed to pay all of its creditors in full and to leave its preferred and common stock intact. In this it was successful.

When AMERCO, the parent company of U-Haul International, emerged from bankruptcy protection in March 2004, it secured an unusual place in history—exiting Chapter 11 with a global capital restructuring that resulted in zero dilution in shareholder value. Alvarez & Marsal, which was retained as the company's financial advisors, executed one of the most successful restructurings on record.

On the effective date of the Company's Plan of Reorganization, AMERCO restructured, on a consensual basis, over $1.2 billion in debt and lease obligations with no dilution to equity holders.

In March 2004 the company emerged from bankruptcy on the back of a $550 million credit facility through a banking syndicate.

The bankruptcy experience revealed both the company's vulnerabilities and its underlying strength. U-Haul's core business remained profitable throughout the crisis—the filing didn't affect actual U-Haul operations. But the episode served as a harsh reminder about the importance of accounting transparency and the dangers of related-party transactions.

The Self-Storage Pivot: Building a Real Estate Empire

If the first eighty years of U-Haul's history were about trucks and trailers, the next era may be defined by something entirely different: real estate.

The strategic logic is elegant. Moving customers need storage. When someone rents a truck to relocate across the country, they often need a place to put their belongings temporarily—whether during a transition, downsizing, or simply because their new home is smaller than their old one. U-Haul already has the customer relationship, the brand recognition, and the physical locations. Adding self-storage creates a natural cross-sell opportunity while generating higher-margin revenue from real estate assets.

U-Haul Holding Company, which entered the storage market in 1993, now owns 94 million square feet of rentable self-storage space. It's the top contributor to new inventory in 2025, adding nearly 3.5M SF—an 11% increase year-over-year.

The 100 largest self storage companies in the US control about 52% of the market—roughly 1 billion square feet of rentable space. Just five companies—Public Storage, Extra Space Storage, U-Haul, National Storage Affiliates, and CubeSmart—control 35.5% of the national inventory.

Although it entered the self storage market in 1993, U-Haul has rapidly expanded its footprint. Today, as a publicly traded company on the New York Stock Exchange, U-Haul boasts 94 million square feet of rentable self storage space, securing its position as the third-largest owner in the U.S.

The growth continues aggressively. Self-storage revenues increased 8.0% as the average monthly number of occupied units increased by 6.2% during fiscal 2025. During fiscal 2025, approximately 6.5 million net rentable square feet (71,000 new rooms) were added.

For fiscal year 2025, same store occupancy decreased 0.5% to 91.9%, revenue per foot increased 3.0%, and the number of locations qualifying for the pool increased by 31. Total portfolio of average occupied rooms increased 39,197, or 6.8%, compared to March 31, 2024.

What makes U-Haul's self-storage strategy distinctive is its adaptive reuse approach—converting existing buildings rather than building from scratch. The company has transformed everything from former Kmart stores to historical industrial buildings into storage facilities, often at costs below ground-up development.

U-Haul is prioritizing the fill-up of newly developed storage units. CFO Jason Berg estimated that as these units reach higher occupancy, roughly 80% of incremental revenue could flow to the bottom line, supporting EBITDA margin recovery.

The competitive landscape in self-storage is both fragmented and intensifying. The self storage market remains a highly fragmented industry, 13,300 owners sharing the national stock. Among them, almost 10,000 are small self storage providers managing less than 100,000 square feet. This diversity, combined with stabilized demand following the pandemic-driven peak and oversupply in some markets, creates a competitive environment that helps keep self storage services largely affordable for consumers. As of March 2025, the average street rate for a storage unit is $134.

U-Haul's primary competitors in self-storage are larger than it—Public Storage leads with 226 million square feet representing 11.3% of national inventory—but U-Haul brings unique advantages: its existing customer relationships, its continental network of locations, and its ability to bundle moving services with storage.

U-Box & The Container Wars: The New Growth Vector

When asked about U-Haul's future, Joe Shoen doesn't hesitate: "Portable storage," Joe answers, without missing a beat. U-Box, U-Haul's moving and storage hybrid, has been growing quickly over the last few years.

U-Box represents U-Haul's entry into the portable moving and storage container market pioneered by PODS. The concept is simple: instead of driving a truck yourself, U-Haul delivers a container to your location. You pack it at your leisure. They pick it up and either store it or deliver it to your new address.

U-Boxes can be kept on someone's property temporarily or stored in U-Haul's secure warehouses until renters are ready to pick them up or have them delivered. It's a natural fit for U-Haul, which people have come to associate with both moving and storage. "That's why we have 5,000 independent self-storage facilities using our trucks," Joe says. "Of course, PODS has been a big player in portables for years, and they're great at what they do, but they're more industrial. Our U-Boxes are designed around household goods, with nice interiors so things won't get banged up. We like to say U-Box is like the Door Dash of moving and storage."

The growth trajectory is impressive. Management described U-Box, the company's portable moving and storage product, as delivering 16% revenue growth and outpacing traditional truck rental gains.

The company sees U-Box as early in its growth cycle, with Vice Chairman Sam Shoen stating that consumer awareness and adoption could allow U-Box to become a pillar comparable in size to the traditional truck rental business.

But the U-Box journey hasn't been without costly missteps. In 2012, PODS sued U-Haul for trademark infringement, claiming that U-Haul improperly used the word "pods" on its website to draw customers to the U-Box service.

In October 2016, Clearwater, FL-based storage company PODS and Phoenix, AZ-based moving company U-Haul entered a settlement which ended a trademark infringement suit first filed in 2012. The $41.4 million settlement ends a legal clash that had previously led to the largest damages award for corrective advertising ever.

The $60.7 million jury verdict handed down in the case during 2014 included a $15.7 million award for disgorged profits. U-Haul had initially claimed that it had made no money on its U-Box container business and had no profits to disgorge, but PODS' counsel was able to argue otherwise.

The PODS settlement was a painful lesson in trademark law, but it hasn't slowed U-Box's expansion. The business continues to grow, and management sees substantial runway ahead.

The Business Model Deep Dive: Fleet, Dealers, Insurance & Innovation

Fleet Economics: The Heart of the Volatility

Understanding U-Haul requires understanding fleet economics—and why they create such earnings volatility.

"We are seeing the high prices we paid for fleet replacements over the last thirty months impact the income statement. Reduced gains on the sale of rental equipment and increased fleet depreciation expense decreased earnings by nearly $260 million for the year compared to fiscal 2024. We have increased depreciation further to recognize this expense in the current period," stated Joe Shoen.

Depreciation expense increased 44.3% (or $294 million), primarily due to the pace of expanding the rental fleet with $1.211 billion spent in capex on its rental equipment fleet during fiscal 2025.

The challenge is that truck purchases occur in bunches based on availability and pricing from manufacturers, but depreciation and resale values flow through the income statement for years afterward. When truck prices were elevated (as they were during supply chain disruptions), U-Haul bought expensive trucks that now generate outsized depreciation expense. When resale values for used trucks decline, gains on sale shrink or turn to losses.

Higher depreciation costs from recent fleet expansion and lower resale values on used cargo vans drove most of the earnings decline. CFO Berg noted that these headwinds are expected to peak this year before moderating as the pace of new truck purchases slows.

The Dealer Network: Asset-Light Distribution

U-Haul's franchising model remains a cornerstone of its growth strategy. The company has outlined plans to expand its independent dealer network in 2025, increasing the availability of rental equipment and enhancing customer convenience. This approach allows U-Haul to scale operations with minimal capital outlay, relying on franchisees to manage localized demand. The robustness of this model is evident in U-Haul's extensive regional footprint, which has historically driven consistent revenue.

The dealer network—those 21,000+ independent locations—represents one of U-Haul's most valuable but underappreciated assets. These dealers pay no franchise fees. Instead, they receive commissions on rentals, creating a mutually beneficial relationship where U-Haul gets ubiquitous distribution without capital investment, and dealers get foot traffic and incremental revenue.

Thanks to a comprehensive plan that Shoen put into place to attract more small businesses, 2,700 new partners have signed on since 2012.

Insurance Subsidiaries: The Hidden Cash Flow Engine

Beyond trucks and storage, U-Haul operates a surprisingly substantial insurance business through RepWest Insurance Company (which provides optional insurance for customers renting U-Haul vehicles and self-storage space) and Oxford Life Insurance Company (which provides annuities, life insurance, and Medicare supplement insurance for senior adults).

The Property and Casualty Insurance segment reported a 30% year-over-year revenue increase to $38.141 million, driven by higher net premiums and favorable claim trends. Life insurance revenue also rose by 8%, supported by investment gains and reduced claims.

These businesses provide stable cash flows and cross-selling opportunities. Every truck rental is an opportunity to sell insurance protection. Every storage customer can be offered coverage against loss. The insurance float generates investment income regardless of equipment rental cycles.

U-Notes: Crowdfunding Before Crowdfunding Was Cool

Perhaps the most innovative aspect of U-Haul's capital strategy is its U-Haul Investors Club—a crowdfunding platform that allows individuals to lend money directly to U-Haul, secured by specific assets.

AMERCO, the parent company of U-Haul International Inc., has used crowdfunding to finance multiple self-storage facilities through an online program called the U-Haul Investors Club. Investments have fixed interest rates and defined payment schedules, with U-Note holders receiving quarterly payments comprised of interest and principal. By the time a U-Note matures, its outstanding principal has been repaid. "U-Haul's concept here is to apply its do-it-yourself mentality, cultivated through its nearly 70 years in the moving and storage business, to the investment arena."

As a "do-it-yourself" company, we have developed an alternative measure to provide investors with the ability to invest directly in U-Notes, issued by U-Haul Holding Company. Our goal is to provide our investors with a fair return on asset backed investments. The idea of the U-Haul Investors Club was inspired by social lending and crowdfunding. Based on this concept, we have brought social lending to the corporate level.

U-Haul leverages financial restructuring and crowdfunding to expand self-storage, securing $121M via U-Notes while repurposing real estate for growth.

Propane: The Unlikely Cash Cow

Since 1987, U-Haul has been the leading U.S. retailer of clean-burning propane, which is available at more than 1,200 Company-owned and -operated stores. U-Haul began selling propane in 1984 and became the largest U.S. retailer by 1987.

How did a truck rental company become America's largest propane retailer? The same logic that drove the dealer network: U-Haul already has the real estate, the customer traffic, and the operational infrastructure. Adding propane sales requires minimal incremental investment and generates meaningful incremental revenue.

Bull Case & Bear Case: Competitive Analysis

The Bull Case

1. Unmatched Network Effects: U-Haul's 23,000+ locations create a one-way rental network that competitors cannot easily replicate. Penske and Budget Truck Rental compete in truck rentals, but neither has the dealer density or one-way flexibility that makes U-Haul the default choice for DIY movers.

2. Self-Storage Upside: The self-storage business generates recurring revenue with 80%+ flow-through margins once facilities are filled. With 71,000 new rooms added in fiscal 2025 alone and a substantial development pipeline, the storage business should provide growing base earnings for years.

3. U-Box Growth Runway: Management plans to continue scaling the U-Box network, with Shoen suggesting the product could eventually match the traditional rental business in size. If U-Box achieves even a fraction of its potential, it represents a substantial growth vector.

4. Depressed Valuation: Despite market headwinds and declining profits, UHAL's valuation is highly attractive both absolutely and relative to peers, presenting significant upside potential. Current earnings are depressed by fleet depreciation headwinds that should moderate.

5. Family Alignment: Joe Shoen's children now work in the business. Unlike the 1980s and 1990s, the current generation appears unified in strategic vision, reducing governance risk.

The Bear Case

1. Fleet Economics Are Brutal: The $260 million earnings hit from depreciation and equipment sales shows how vulnerable profitability is to truck pricing cycles. This isn't a one-time event—it's a structural feature of the business model.

2. Self-Storage Competition Is Intensifying: New self-storage supply in 2025 is expected to reach 55.8 million square feet. Oversupply in certain markets is already pressuring occupancy rates, with U-Haul reporting same-store occupancy declines.

3. Housing Market Sensitivity: U-Haul's core moving business correlates with housing transactions and household formation. In a prolonged housing slump, fewer people move, and those who do move shorter distances (generating less rental revenue).

4. Public Storage Legal Dispute: Joe Shoen, CEO of U-Haul, has had enough. U-Haul filed a complaint in the US District Court of Arizona against Public Storage. The action is designed to protect U-Haul's right to continue its use of the color orange and the word 'orange' when promoting and marketing its storage business. While U-Haul has used orange since 1945, trademark litigation creates uncertainty.

5. Family Control Risks: While the current generation appears aligned, family businesses always carry succession and governance risks that public shareholders cannot control.

Porter's Five Forces Analysis

Threat of New Entrants: Low. Building a national one-way rental network requires decades of investment in dealer relationships, fleet procurement, and brand building. The network effects create substantial barriers.

Bargaining Power of Suppliers: Moderate. U-Haul depends on Ford, GM, and Ram for truck chassis. Concentrated supplier base creates some dependency, though U-Haul's scale provides negotiating leverage.

Bargaining Power of Buyers: Low. Individual customers have limited bargaining power. For one-way moves, U-Haul is often the only practical option.

Threat of Substitutes: Moderate. Full-service movers offer an alternative for those willing to pay premium prices. Portable storage containers (including U-Haul's own U-Box) represent partial substitutes for truck rentals.

Industry Rivalry: Moderate. In truck rentals, U-Haul faces Penske and Budget Truck. In self-storage, competition is fiercer with Public Storage, Extra Space, and thousands of smaller operators.

Hamilton Helmer's 7 Powers Analysis

Network Effects: Yes. The most powerful element of U-Haul's moat. Each location makes every other location more valuable by enabling one-way moves.

Scale Economies: Moderate. Fleet purchasing, shared IT systems, and brand advertising create some scale benefits, though not as pronounced as in purely digital businesses.

Switching Costs: Low. Customers face no meaningful switching costs for individual transactions, though habit and brand recognition create some stickiness.

Counter-Positioning: No. Competitors could theoretically copy U-Haul's model; they simply haven't invested the time and capital.

Process Power: Yes. Decades of operational optimization in fleet management, dealer relationships, and logistics create process advantages difficult for competitors to replicate quickly.

Branding: Yes. U-Haul is effectively a genericized trademark—people say "I need to rent a U-Haul" regardless of which company they actually use.

Cornered Resource: Limited. The dealer network represents something of a cornered resource, though individual dealers can theoretically switch to competitors.

Key Metrics to Track & Investment Considerations

For investors monitoring U-Haul, three KPIs stand out as most critical:

1. Self-Storage Revenue per Square Foot Growth: This metric captures both pricing power and operational efficiency in U-Haul's fastest-growing, highest-margin segment. Fiscal 2025 showed 3.0% growth in revenue per foot despite same-store occupancy declines—evidence of pricing power. Watch for this metric to sustain mid-single-digit growth as facilities mature.

2. U-Box Revenue Growth Rate: Management described U-Box as delivering 16% revenue growth. If management's vision of U-Box eventually matching traditional truck rentals proves correct, this business represents enormous value creation. Track whether growth sustains double digits as the segment scales.

3. Fleet Depreciation Expense as Percentage of Equipment Rental Revenue: This ratio reveals the pressure on core rental profitability. The 44.3% spike in depreciation expense during fiscal 2025 devastated earnings. As this normalizes—with management expecting headwinds to peak—profitability should recover. Track whether depreciation as a percentage of rental revenue returns toward historical averages.

Regulatory & Accounting Considerations

Related-Party Transactions: The 2002-2003 SAC Holdings debacle demonstrated how related-party transactions can create hidden liabilities. While current governance appears improved, investors should monitor any transactions between AMERCO and entities connected to the Shoen family.

Insurance Reserves: The company's insurance subsidiaries require actuarial estimates for claims reserves. Conservative or aggressive reserving choices can significantly impact reported earnings.

Real Estate Valuation: As self-storage becomes a larger portion of the business, the gap between book value (cost minus depreciation) and market value of storage properties may grow. This creates potential hidden value but also accounting complexity.

Conclusion: The Orange Empire's Next Chapter

Eighty years after Leonard and Anna Mary Shoen parked their first orange trailer on a Portland gas station lot, U-Haul stands as one of the great American business stories—a genuine verb company built on a simple insight about what mobile Americans needed.

The company survived family warfare that would have destroyed most businesses. It emerged from bankruptcy with shareholders intact. It transformed itself from a pure truck rental operation into a diversified moving, storage, and insurance enterprise.

Today, U-Haul faces a different challenge: managing the transition from its legacy truck rental business, with its brutal fleet economics and earnings volatility, to a more predictable self-storage real estate model—while growing U-Box into what management believes could be a business as large as traditional truck rentals.

"Moving activity increased over the quarter as demand for our products and services ticked up," stated Joe Shoen. "We are making steady improvements to reduce friction with the customer so that it's easier for the public to choose U-Haul."

For the founder's great-grandchildren now working at the company, the mission remains what it was in 1945: help Americans move themselves, cheaply and reliably. The orange trucks rolling down America's highways are more than moving equipment—they're monuments to entrepreneurial hustle, network economics, and the ability of a family business to survive even its darkest chapters.

The question isn't whether U-Haul will survive. It's whether the company can translate its operational strengths into sustainable earnings growth in a world where moving patterns, real estate markets, and competitive dynamics continue to evolve. For investors willing to look past near-term depreciation headwinds, the orange empire may offer value that the market has yet to fully recognize.

Myth vs. Reality Box:

| Myth | Reality |

|---|---|

| U-Haul is a simple truck rental company | Revenue mix continues evolving: self-storage now contributes ~16% of revenue, with U-Box growing at 16% annually |

| The family feud destroyed the company | U-Haul emerged from the feud with focused strategy, profitable operations, and dominant market position |

| Competitors could easily replicate U-Haul's model | 23,000+ locations built over 80 years create network effects nearly impossible to replicate |

| Earnings declines reflect business deterioration | Current headwinds are primarily accounting (fleet depreciation), not operational; core moving and storage volumes remain healthy |

| Self-storage is a commodity business | U-Haul's integrated moving+storage offering creates differentiation; adaptive reuse strategy reduces development costs |

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube