Visa: The Network That Ate the World

I. Introduction & Episode Roadmap

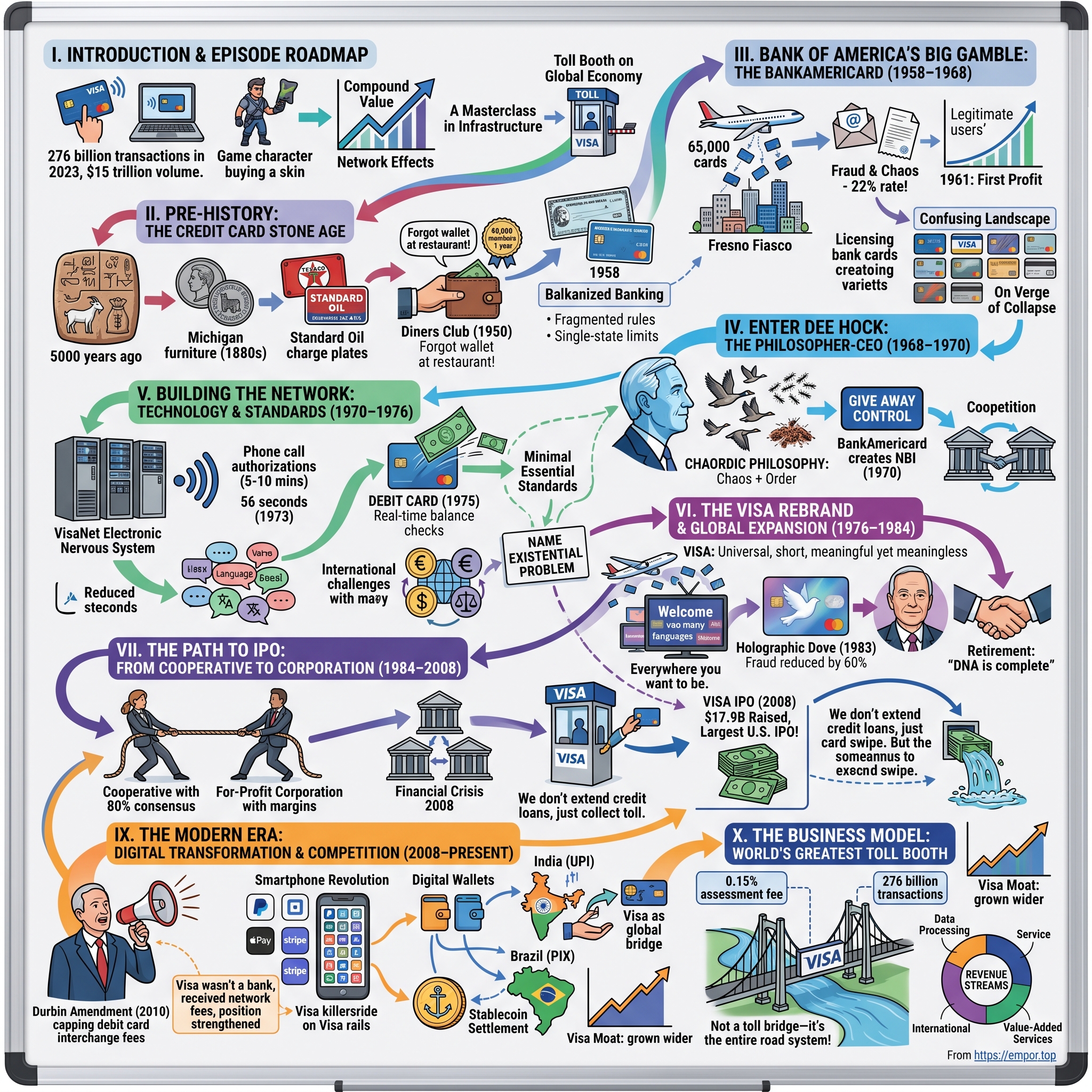

Picture this: Every second of every day, somewhere in the world, 8,750 Visa transactions are being processed. A grandmother in Tokyo taps her card at a convenience store. A startup founder in Lagos pays for cloud services. A teenager in São Paulo buys a skin in Fortnite. By the time you finish reading this sentence, another 43,750 transactions will have flowed through Visa's network. In 2023 alone, Visa processed 276 billion transactions worth $15 trillion—more than the GDP of China.

But here's the thing that should blow your mind: This global financial nervous system, this infrastructure that underpins modern commerce, started as an internal credit card experiment at a single California bank. Not a technology company. Not a government initiative. Not even a consortium of financial giants. Just Bank of America, trying to figure out how to make more money from consumer lending in the 1950s.

The central paradox of Visa's story is this: How did a bank's internal credit card program—one that nearly bankrupted its division in the early years—evolve into the world's largest payment network, a company worth $664 billion that takes a tiny cut of nearly half the world's electronic transactions?

This is a story about network effects at their purest—how connecting buyers and sellers creates value that compounds exponentially. It's about "coopetition," that strange dance where fierce competitors must cooperate to create the very playing field they compete on. It's about standards—boring, technical standards—as a source of immense power. And perhaps most fascinatingly, it's about how giving up control can be the ultimate path to dominance.

You'll meet Dee Hock, the philosopher-CEO who looked more like a Utah utility worker than a financial revolutionary, yet who designed an organizational structure so radical that he had to invent a new word—"chaordic"—to describe it. You'll see how Visa survived the 2008 financial crisis while the banks that owned it collapsed. You'll understand why, despite the rise of PayPal, Square, Apple Pay, and a thousand fintech startups, Visa's moat has only grown wider.

What you're about to learn isn't just the history of a payment network. It's a masterclass in building infrastructure that becomes so essential, so embedded in the fabric of commerce, that it essentially becomes a toll booth on the global economy. This is how chaos became order, how competition became cooperation, and how a piece of plastic became the foundation of digital commerce.

II. Pre-History: The Credit Card Stone Age

The Sumerian merchants of ancient Mesopotamia would have understood Visa's business model immediately. Five thousand years ago, they were already carving credit transactions into clay tablets—"2 goats now, 3 bushels of barley at harvest." The human desire to buy now and pay later is as old as commerce itself.

Fast forward to 1880s America. A furniture store owner in Grand Rapids, Michigan, starts handing out metal coins to his best customers. Present the coin, charge your purchase, settle up at month's end. By the 1920s, these "charge plates"—metal cards embossed with customer information—were spreading through department stores across America. Western Union had issued 250,000 metal "shopper's plates" by 1914. Oil companies like Texaco and Standard Oil began issuing their own cards in the 1920s, creating the first taste of network effects: the more stations accepted your card, the more valuable it became.

But the real revolution began over lunch at Major's Cabin Grill in Manhattan in 1949. Frank McNamara, a businessman, reached for his wallet to pay and realized he'd forgotten it. Embarrassed, he had to call his wife to bring money. That moment of humiliation sparked an idea: What if there was a card that restaurants would accept as payment, and the card company would handle collection later?

By February 1950, McNamara and his partner Ralph Schneider had launched Diners Club with 27 participating restaurants and 200 members. Within a year, they had 20,000 cardholders. Diners Club wasn't technically a credit card—it was a charge card, requiring full payment each month—but it proved the model could work. The company took 7% from merchants and charged members $5 annually. Simple, elegant, profitable.

American Express watched Diners Club's success with interest. AmEx had dominated travel money for a century with their traveler's checks—in 1957, they had $2.5 billion worth in circulation, earning float income that would make Warren Buffett weep with joy. When AmEx launched their charge card in 1958, they had an immediate advantage: 8,500 existing travel offices worldwide and relationships with hotels and restaurants. Within five years, AmEx cards were everywhere that mattered.

But here's what's fascinating: banks, the institutions you'd expect to dominate consumer credit, wanted nothing to do with credit cards initially. Why? Three reasons. First, banking was absurdly fragmented—the U.S. had 13,500 banks in 1958, most operating in single states due to Depression-era regulations. Second, banks made their money from commercial lending to businesses, not fiddling with small consumer transactions. Third, and most importantly, credit cards looked like a operational nightmare. You had to sign up merchants, issue cards, handle authorizations, process transactions, deal with fraud, manage collections—all for maybe 1-2% of transaction volume.

The state of American banking in the 1950s was almost quaint by today's standards. The McFadden Act of 1927 and Banking Act of 1933 had essentially frozen banks within state lines. Bank of America, the nation's largest bank, could only operate in California. Chase could only operate in New York. This Balkanization meant that any bank wanting to create a credit card network faced an impossible choice: stay local and irrelevant, or somehow convince competing banks to cooperate.

Most banks looked at this landscape and decided to stick with what they knew: taking deposits and making loans. But at Bank of America's headquarters in San Francisco, a group of executives were about to make a bet that would transform not just their bank, but the entire concept of money itself.

III. Bank of America's Big Gamble: The BankAmericard (1958–1968)

Joseph P. Williams had a problem. As Senior Vice President of Bank of America in 1958, he watched consumer lending grow at rivals while his bank sat on the sidelines. Bank of America was already a giant—$9 billion in assets, 700 branches across California—but Williams knew that consumer credit was the future. The average American family was buying cars, appliances, and televisions on installment plans. Why shouldn't Bank of America get a piece of every purchase?

The solution came from an unlikely source: a small experiment in Fresno. Why Fresno? It was isolated enough to contain a disaster if things went wrong, large enough at 250,000 people to provide meaningful data, and diverse enough economically to represent broader America. Plus, Bank of America already had 45% market share there. If they were going to test a credit card, Fresno was their laboratory.

On September 18, 1958, Bank of America did something that would be illegal today and seemed insane even then: they mailed 65,000 unsolicited BankAmericards to every Bank of America customer in Fresno. No application. No credit check. Just a piece of paper that said "BankAmericard" with a $300 credit limit (about $3,000 in today's money). The accompanying letter was almost apologetic: "You may use your BankAmericard to buy anything you want at any of the 300 merchants listed."

The cards weren't even plastic—they were paper, with raised numbers that could be imprinted on carbon paper slips. The bank had spent months secretly signing up those 300 merchants, promising them something revolutionary: customers could buy now, Bank of America would pay the merchant immediately (minus 6%), and the bank would collect from the customer later.

Within days, the experiment turned into chaos.

Criminals quickly realized that stealing mail could yield hundreds of active credit cards. Fraudsters opened post office boxes under false names just to receive cards. Merchants began running the same charge slip multiple times. Customers who had never asked for credit suddenly had $300 in purchasing power—many went on shopping sprees with no intention of paying. One Bank of America executive later called it "total chaos."

By Christmas 1958, the Fresno experiment was hemorrhaging money. The fraud rate hit 22%—for every $100 in legitimate purchases, $22 was stolen. The bank had projected losses of $450,000 in the first year; actual losses exceeded $2 million. Inside Bank of America, executives were in panic mode. Board members wanted to kill the program. The press, when they found out, had a field day: "Bank of America's Fresno Fiasco."

But Williams and his team saw something in the data that kept them going: legitimate customers loved the cards. Despite the fraud, despite the chaos, honest customers were using their BankAmericards for everything from groceries to gas. Merchants, once they figured out the system, loved getting paid immediately instead of managing their own credit accounts. There was a real business here, buried under the operational disasters.

The next three years were a grinding battle to make the system work. Bank of America created one of the first computerized authorization systems, where merchants could call a center to verify large purchases. They developed fraud detection patterns—unusual spending sequences that suggested stolen cards. They hired former FBI agents to investigate fraud rings. They even created a new position that had never existed before: the credit card security specialist.

By May 1961—32 months after the Fresno drop—BankAmericard finally turned its first monthly profit. The bank kept this secret, telling no one outside senior management. Why? Because they had realized something profound: they were building a network, and networks are winner-take-all. Every day they could operate without competition was a day they could sign more merchants and issue more cards, strengthening the network effects.

But by 1966, the secret was out. Other banks had launched their own cards. A Chicago consortium had created Master Charge (later MasterCard). The landscape was turning into chaos—merchants had to accept dozens of different cards, each with different systems, different carbon slips, different payment schedules. A restaurant in Los Angeles might need to deal with BankAmericard, Master Charge, Uni-Card, Everything Card, and a half-dozen others.

Bank of America made a crucial decision: instead of trying to crush competitors, they would license the BankAmericard system to other banks. By 1968, they had licensed to banks in 15 states and 5 countries. But this created new problems. Each licensee modified the system slightly. Cards from one bank wouldn't work smoothly with another bank's merchants. Customer service was a nightmare. Returns and chargebacks could take months to resolve.

The licensing banks were increasingly frustrated. They were paying fees to Bank of America while competing against them. They had no say in how the system evolved. At a particularly tense meeting in 1968, one banker stood up and declared: "We're building Bank of America's network with our money and our customers. This has to change."

That banker was right. The entire BankAmericard system was on the verge of collapse. Banks were threatening to abandon it entirely. Merchants were in revolt over the confusion. Into this chaos walked an unlikely savior: a 39-year-old banker from Seattle named Dee Hock, who had ideas about organization that seemed to come from another planet entirely.

IV. Enter Dee Hock: The Philosopher-CEO (1968–1970)

Dee Ward Hock didn't look like a revolutionary. In 1968, at 39 years old, he was a middle manager at National Bank of Commerce in Seattle, running their struggling BankAmericard operation. The son of a utility lineman from Utah, Hock had never graduated from college. He'd worked as everything from a brick factory laborer to a finance company collector. By any reasonable measure, he was nobody special—just another Mormon kid from the mountain West trying to make it in banking.

But Hock saw the world differently. While his fellow bankers focused on interest rates and credit losses, Hock spent his evenings reading books on cybernetics, chaos theory, and evolutionary biology. He was obsessed with a question that seemed to have nothing to do with credit cards: How does order emerge from chaos in nature? How do flocks of birds coordinate without a leader? How do ant colonies build complex structures without central planning?

When Hock arrived at the Columbus, Ohio meeting in October 1968—a gathering of 243 banks all licensees of BankAmericard, all furious at the chaos—he was supposed to be just another angry participant. The meeting was a disaster from the start. Banks were screaming at each other. East Coast banks wanted one solution, West Coast banks another. International licensees felt ignored. Everyone blamed Bank of America for the mess, while Bank of America insisted they were doing their best.

On the second day, as the meeting devolved into shouting matches, Hock did something unexpected. He walked to the microphone during a break and said: "I'd like to form a committee to study these problems. Who wants to join?" It was such a mundane proposal—form a committee!—that people agreed just to move things along. Hock was elected to lead it almost by accident; nobody else wanted the job of herding these angry cats.

But Hock had a radical vision that he shared with no one at first. He believed the entire structure of BankAmericard was wrong. It wasn't that Bank of America was doing a bad job managing the network. It was that no single entity should manage it at all. The network should manage itself, like a flock of birds or a colony of ants.

Over the next eighteen months, Hock engaged in what can only be described as organizational jiujitsu. He convinced the committee that incremental fixes wouldn't work. He flew to San Francisco and met with Bank of America's leadership, including Kenneth Larkin, the senior executive overseeing BankAmericard. Instead of demanding concessions, Hock asked a simple question: "What if you could have all the benefits of the network without any of the headaches of managing it?"

Hock's proposal was unprecedented in corporate history: Bank of America should give up ownership of BankAmericard entirely. Not sell it—give it away. The network would be owned by all the banks that participated in it, governed by rules that required near-unanimous consent to change, operated as a for-profit company that would never retain earnings. Every dollar of profit would flow back to the member banks.

Larkin thought Hock was insane. "You want us to give away a system we spent $100 million building?" But Hock kept pushing his argument: Bank of America would still be the largest issuer of cards. They'd still make money on every transaction. But they'd no longer be responsible for managing hundreds of angry licensees. And—this was the key insight—a network owned by all its members would grow far faster than one controlled by a single bank.

The governance structure Hock proposed was unlike anything in corporate America. Major decisions would require 80% approval from member banks. No single bank could own more than 10% of the votes, regardless of their size. The organization would have a board elected by regions, ensuring geographic diversity. It would be incorporated as a for-profit company to ensure efficiency, but it would never retain earnings—all profits would be distributed to members or reinvested in the network.

Bank of America's board initially rejected the proposal. Why give up control of something so valuable? But by late 1969, the reality was undeniable: the current system was failing. Licensees were defecting. Master Charge was gaining ground by offering banks more autonomy. On March 8, 1970, Bank of America shocked the financial world by announcing they would transfer ownership of BankAmericard to a new entity: National BankAmericard Inc. (NBI).

Hock was elected as the first CEO of NBI, beating out several more conventional candidates. His first all-hands meeting with the staff was characteristic. Instead of talking about profit margins or market share, he talked about creating "an organization that could transcend the old ways of thinking about corporations." He spoke about "distributed intelligence" and "self-organizing systems." Half the audience thought he was a genius. The other half thought he was completely nuts.

One early employee recalled: "Dee would walk into a meeting about transaction processing and start talking about how geese fly in formation. We'd be discussing interchange fees and he'd bring up ant colonies. It was bizarre. But somehow, it worked."

What Hock understood, and what his contemporaries missed, was that a payment network is fundamentally different from a traditional business. It's not about manufacturing products or delivering services. It's about creating a standard—a common language that allows economic actors to communicate. And standards, paradoxically, become more powerful when no one controls them. The internet protocol TCP/IP is powerful precisely because no company owns it. Hock was applying this insight to payments decades before it became conventional wisdom in technology.

By the end of 1970, NBI had 243 member banks with 29 million cardholders. The chaos was beginning to transform into order. But the real work—building the technological and operational infrastructure that would scale to billions of transactions—was just beginning.

V. Building the Network: Technology & Standards (1970–1976)

The computer room at NBI's data center in San Mateo, California, was hot enough to fry an egg. In 1973, the air conditioning had failed again, and technicians were frantically fanning IBM System/370 mainframes with pieces of cardboard. These machines, each the size of a refrigerator and costing $2 million, were processing authorization requests from across the country. Every minute of downtime meant thousands of declined transactions and furious customers standing at checkout counters.

This was the reality of building VisaNet, the electronic nervous system that would eventually handle 65,000 transactions per second. But in 1973, NBI was processing just 30 transactions per minute, and even that was pushing the limits of existing technology.

The challenge wasn't just technical—it was organizational. Each member bank had its own systems, its own procedures, its own forms. A transaction from a Security Pacific card used at a Chase merchant involved four different computer systems that had never been designed to talk to each other. Getting them to communicate reliably was like trying to get four people who spoke different languages to collaborate on writing a novel.

Hock's solution was characteristically unconventional. Instead of mandating a single system that all banks must adopt—which would have caused a revolt—he created what he called "minimal essential standards." Banks could use any technology they wanted, any procedures they preferred, as long as they could send and receive messages in a standard format. It was the payment equivalent of saying: "I don't care what language you think in, but when you talk to the network, you speak this specific dialect."

The first breakthrough came in 1973 with the launch of the electronic authorization system. Previously, authorizations required phone calls—a merchant would literally call the card-issuing bank to verify a purchase over $50. This could take 5-10 minutes per transaction. The new system reduced this to 56 seconds. By today's standards that seems glacial, but in 1973 it was revolutionary.

The system worked through a elegant relay race. A merchant's point-of-sale terminal would dial into their bank's computer. That bank would route the request through NBI's central switch to the card-issuing bank. The issuing bank would check the account and send back an approval or decline. The entire round trip: 56 seconds. Merchants loved it. Fraud plummeted. Customers didn't have to wait in embarrassment while someone called their bank.

But the real innovation wasn't the speed—it was the standardization. Every message followed the same format: 16-digit card number, 4-digit merchant code, transaction amount, date, time. This seems obvious now, but in 1973, getting hundreds of banks to agree on something as simple as date format (MM/DD/YY or DD/MM/YY?) required months of negotiation.

Then came an unexpected innovation from an unlikely source. In 1975, First National Bank of Seattle wanted to offer something radical: a card that would immediately deduct money from a checking account instead of creating a credit balance. They called it a "debit card." NBI's executives were skeptical. Why would customers want to pay immediately when they could pay later? But Hock saw the potential: this could expand the network beyond credit into all electronic payments.

The technical challenge was immense. Debit transactions required real-time balance checking, something credit cards didn't need. The authorization system had to be upgraded to handle a new message type. Banks had to modify their core banking systems to handle instant debits. It took two years to fully implement, but by 1977, debit cards were processing through VisaNet.

The international expansion brought even greater challenges. In 1974, Hock created IBANCO (International Bank Card Company) to manage operations outside the U.S. But "international" meant dealing with different currencies, different regulations, different cultural attitudes toward credit. In Japan, credit cards were seen as shameful—a sign you couldn't manage money. In Germany, strict data protection laws meant transaction data couldn't leave the country. In Brazil, hyperinflation meant transaction amounts could change between authorization and settlement.

The solution was elegant: create regional processing centers that could handle local requirements while still connecting to the global network. Like the internet would later do with packet routing, VisaNet created a system where transactions could find multiple paths to their destination. If the direct link from London to New York was down, the transaction could route through Toronto or San Francisco.

But the biggest challenge was the simplest: the name. "BankAmericard" was toxic internationally. Foreign banks refused to promote a card with "America" in the name. In France, Carte Bleue members wouldn't even put the BankAmericard logo on their cards. In the UK, Barclaycard was considering leaving the network entirely rather than co-brand with what seemed like American imperialism.

The name problem had become existential. Without a unified global brand, the network would fragment. Merchants wouldn't know which cards to accept. Customers wouldn't know which ATMs would work. The network effects that made the system valuable would collapse. Hock knew they needed a new name—something universal, pronounceable in any language, meaningful yet meaningless.

The search for that name would become one of the most expensive branding exercises in corporate history. And the solution, when it came, would be so simple that everyone would wonder why they hadn't thought of it before.

VI. The Visa Rebrand & Global Expansion (1976–1984)

The conference room at NBI's San Francisco headquarters looked like a linguistic war zone. It was March 1976, and scattered across the table were hundreds of potential names written on index cards. "Summa." "Bancor." "Ameri-card." "Worldpay." For six months, NBI had paid naming consultants, linguists, and branding experts over $2 million (roughly $10 million today) to find a replacement for "BankAmericard."

Dee Hock picked up one card that simply read "Visa." It had been suggested by someone who noted that the word meant the same thing in almost every language—a document that grants permission to enter. It was short, symmetrical, and ended with an open vowel sound that psychologists said conveyed positivity. Most importantly, it belonged to no country, no bank, no existing meaning in commerce.

"This is it," Hock announced. The room was skeptical. Visa? It sounded like a government form. But Hock saw genius in its simplicity. The word worked in French (vee-zah), Japanese (bi-za), Spanish (vee-sah), Arabic, Mandarin. You could paint it on a sign in Lagos or Stockholm and everyone would pronounce it nearly the same way.

The rebrand would cost $10 million to execute—replacing millions of cards, updating thousands of merchant decals, advertising the change globally. Bank of America's executives were furious. They had built the BankAmericard brand over 18 years. Now they had to tell customers their BankAmericard was becoming a "Visa card." Kenneth Larkin reportedly threw the proposal across his desk, shouting, "We're giving up millions in brand value for what? A passport joke?"

But Hock had the votes. The member banks, especially international ones, overwhelmingly supported the change. On July 1, 1976, in a coordinated global campaign, BankAmericard became Visa simultaneously in 87 countries. In Japan, Sumitomo Card became Visa. In France, Carte Bleue added the Visa logo. In Canada, Chargex transformed overnight.

The launch campaign was brilliant in its simplicity: "Think of it as money." Not credit, not a card, but money itself. Television ads showed the card being accepted from Anchorage to Zimbabwe. One ad featured a montage of "Welcome" in dozens of languages, ending with "Welcome to Visa—everywhere you want to be."

The immediate impact was stunning. Within six months, merchant acceptance increased 40%. Cross-border transactions—previously a nightmare of confusion—jumped 200%. The unified brand created what marketers now call a "network effect multiplier": each new user and merchant made the network exponentially more valuable.

But the real innovation came in 1983 with a small holographic dove. Counterfeiting had become a massive problem—criminals were creating fake cards using nothing more than embossing machines and stolen account numbers. The hologram, which would become Visa's signature security feature, was almost impossible to replicate with 1980s technology. It showed a dove that appeared to fly when you tilted the card, created using a laser etching process that only three facilities in the world could produce.

The hologram reduced fraud by 60% within a year. But more importantly, it became a trust symbol. Customers learned to look for the dove. Merchants knew a card with the hologram was legitimate. It was physical proof of the network's promise: this payment will be honored.

Meanwhile, VisaNet was evolving into something unprecedented. By 1980, the network was processing 100 million transactions annually through four redundant data centers. The system had achieved what engineers called "five nines" reliability—99.999% uptime, meaning less than 5 minutes of downtime per year. Each data center could handle the full network load, synchronized in real-time through dedicated satellite links and fiber optic cables.

The technical specifications were mind-boggling for the era. The network could route a transaction from Tokyo to Buenos Aires to London to New York in under 2 seconds. It could handle authorization requests in 47 different currencies, automatically calculating exchange rates updated every 15 minutes. It could detect potential fraud by analyzing spending patterns across millions of accounts simultaneously—if someone used a card in Miami and then "again" in Moscow an hour later, the system would flag it instantly.

But Hock was already looking beyond. In 1984, at age 55, he shocked everyone by announcing his retirement. At the farewell dinner, he gave a speech that seemed more like a philosophy lecture than a corporate goodbye: "We've built more than a payment network. We've created a new form of organization—one that's neither purely competitive nor purely cooperative. It's something else, something that doesn't yet have a name."

When pressed why he was leaving at the peak of success, Hock gave a typically cryptic answer: "The foundation is complete. The network is self-sustaining. My job was to create the DNA, not to manage the organism." Many thought he was burned out. Others suspected he was frustrated with the increasingly corporate culture as traditional banking executives replaced his original team of mavericks.

The truth was simpler and more complex: Hock believed the organization had evolved beyond his vision. It was becoming more traditional, more hierarchical, more like the corporations he had tried to transcend. The board wanted five-year strategic plans. Member banks wanted predictable returns. The chaos was becoming order, but perhaps too much order.

By the time Hock left in May 1984, Visa had 236 million cards in circulation, accepted at 3.4 million merchants across 150 countries. The network was processing 2.5 billion transactions annually worth $175 billion. From the chaos of competing bank cards, a global standard had emerged.

But Hock's most lasting contribution wasn't the network or the brand. It was an idea that would take decades to fully appreciate—an organizational philosophy he called "chaordic," blending chaos and order in a way that seemed to mirror nature itself.

VII. The Chaordic Philosophy: Order from Chaos

In retirement, sitting on his 200-acre ranch in Pescadero, California, Dee Hock spent years trying to articulate what he had created at Visa. The traditional language of business—profit margins, market share, competitive advantage—seemed inadequate. What he had built didn't fit the normal categories. It wasn't purely competitive like a typical corporation. It wasn't purely cooperative like a nonprofit. It was something else entirely.

Hock coined the term "chaordic" from the words "chaos" and "order" to describe this new organizational form. The concept wasn't just wordplay. It represented a fundamental insight about how complex systems actually work in nature. A flock of starlings wheeling through the sky appears chaotic, yet follows simple rules that create stunning order. An ant colony seems anarchic, yet builds structures of remarkable complexity. The human brain has no CEO neuron, yet produces consciousness.

In a chaordic organization, members "simultaneously engaged in the most intense cooperation and fierce competition"—a paradox that traditional management theory said was impossible. At Visa, banks cooperated to create standards and infrastructure while competing ferociously for customers. They shared technology while guarding their customer lists. They built a common brand while maintaining separate identities.

Hock laid out six principles that defined a chaordic organization. First, purpose must be clear and shared by all participants—not imposed from above but emerging from collective agreement. Second, governance must be distributed—no single entity can control the whole. Third, ownership must be equitable—those who create value must share in it. Fourth, the organization must be infinitely malleable—able to evolve without revolution. Fifth, it must embrace both competition and cooperation simultaneously. Sixth, it must be self-organizing and self-governing, with minimal central authority.

Consider how radically this differed from conventional corporate wisdom. At General Motors or IBM in the 1970s, strategy flowed from the C-suite down through layers of management. At Visa, strategy emerged from thousands of member banks experimenting simultaneously. GM could dictate that all divisions use the same accounting system. Visa could only suggest standards and hope members adopted them voluntarily.

As Hock noted, this structure mirrors modern phenomena: "Ethereum, for instance, is a kind of 2.0 version of the chaordic spirit—where cooperation and competition are balanced in a way that mirrors the natural order". Today's decentralized autonomous organizations (DAOs) and blockchain networks follow principles Hock articulated decades earlier. Bitcoin has no CEO, no headquarters, no employees—yet processes billions in transactions. Wikipedia has no editorial board, yet produces the world's largest encyclopedia. These are chaordic organizations, whether they use the term or not.

The practical implications were profound. Traditional organizations respond to problems by adding rules, procedures, controls. Chaordic organizations respond by clarifying principles and letting members self-organize solutions. When fraud became a problem, Visa didn't create a massive anti-fraud department. It established standards for fraud detection and let each bank implement their own systems, sharing what worked.

This approach enabled incredible innovation. When First National Bank of Seattle wanted to create debit cards, they didn't need permission from Visa headquarters. They just needed to ensure their innovation worked within the network's standards. When Japanese banks wanted to add features for their market, they could—as long as the cards still functioned globally. The network evolved through distributed experimentation, not central planning.

But the chaordic model had critics. Traditional executives found it maddening. How do you manage without control? How do you plan without authority? How do you compete when you're also cooperating? One Chase executive complained: "Every Visa meeting feels like herding cats. We spend hours debating things that a normal company would just decide."

Hock himself recognized the challenge, commenting in 2015: "We live in the 21st century but are still using command and control organizational structures from the 16th century. Bitcoin is one of the best examples of how a decentralized, peer-to-peer organization can solve problems that these dated organizations cannot... it presents incredible opportunities for new levels of efficiency and transparency in financial transactions".

The irony was that Visa itself began moving away from chaordic principles after Hock's departure. The IPO process required traditional corporate governance. Public markets demanded predictable earnings. Regulators wanted clear accountability. By 2008, Visa looked much more like a conventional corporation than the radical experiment Hock had created.

Yet the chaordic idea lives on, not in Visa's current structure but in the broader digital economy. Every open-source software project is essentially chaordic—developers cooperate on code while competing on implementations. Every social network is chaordic—users create content cooperatively while competing for attention. Every cryptocurrency network is chaordic—miners cooperate to maintain the blockchain while competing for rewards.

In his 1991 Business Hall of Fame acceptance speech, Hock revealed his personal philosophy: "Through the years, I have greatly feared and sought to keep at bay the four beasts that inevitably devour their keeper—Ego, Envy, Avarice, and Ambition". This wasn't just personal modesty. It was recognition that centralized power corrupts, that hierarchy breeds dysfunction, that command-and-control ultimately fails in complex systems.

The ultimate validation of Hock's philosophy came not from business school case studies but from Visa's survival through every economic crisis since 1970. During the 2008 financial meltdown, hierarchical banks collapsed while the chaordic network they had created continued processing transactions without interruption. Order had indeed emerged from chaos, just as Hock had predicted.

VIII. The Path to IPO: From Cooperative to Corporation (1984–2008)

Charles Phillips arrived at Visa headquarters in Foster City, California, in January 1995 with a mandate that would have terrified most executives: transform a cooperative owned by competing banks into a for-profit corporation that could go public. Phillips, a former Morgan Stanley investment banker, understood something fundamental—the cooperative structure that had enabled Visa's growth was now constraining it.

The world had changed dramatically since Dee Hock's retirement in 1984. The internet was emerging. Electronic commerce was no longer science fiction. New competitors like PayPal were being born in Silicon Valley garages. Meanwhile, Visa remained structured as a series of regional cooperatives with Byzantine governance requiring 80% approval for major decisions. Getting 21,000 member banks to agree on anything was like herding cats through quicksand.

Phillips and his successor, Carl Pascarella (who took over in 2001), began the slow process of corporatization. They streamlined operations, cutting costs by $300 million. They unified technology platforms that had fragmented across regions. They began thinking like a public company—focused on margins, efficiency, growth metrics—rather than a cooperative focused on member consensus.

The catalyst for change came from an unexpected source: MasterCard. In 2006, Visa's closest competitor went public, and its stock more than quintupled in less than two years. Suddenly, Visa's member banks realized they were sitting on a goldmine. The same network they'd built cooperatively could be worth tens of billions as a public company.

On October 11, 2006, Visa announced that some of its businesses would be merged and become a publicly traded company, Visa Inc. Under the IPO restructuring, Visa Canada, Visa International, and Visa USA were merged into the new public company. The announcement triggered eighteen months of frantic preparation. Investment bankers from JPMorgan and Goldman Sachs essentially moved into Visa's offices. Lawyers worked around the clock to untangle decades of cooperative agreements.

The timing could not have been worse—or better, depending on your perspective. By late 2007, the subprime mortgage crisis was metastasizing into a full-blown financial crisis. Bear Stearns was hemorrhaging money. Lehman Brothers was marking down billions in assets. The very banks that owned Visa were on the verge of collapse.

On March 18, 2008, Visa priced its initial public offering at $44 a share, raising $17.9 billion and becoming the largest IPO in U.S. history, surpassing the $11 billion record held by AT&T wireless. This came amid a Wall Street comeback that included a Federal Reserve rate cut, surprisingly strong earnings from Goldman Sachs and Lehman Brothers, and a 420-point spike in the Dow.

The IPO was remarkable in context—this was March 2008, just five days after JPMorgan offered to buy the remnants of the battered investment bank Bear Stearns for just $2 per share. The financial world was melting down, yet here was Visa raising more money than any company in American history.

On March 19, 2008, the first day shares traded on the New York Stock Exchange, the stock closed at $56.50 per share—a 28% first-day pop that added $5 billion in market value. The IPO created instant windfalls for Visa's bank owners: JPMorgan Chase received about $1.25 billion (five times more than it paid for Bear Stearns), Bank of America got roughly $625 million, National City about $435 million, Citigroup about $300 million, and U.S. Bancorp and Wells Fargo both got more than $270 million.

But here's what made Visa different from every other financial company in 2008: Visa doesn't make credit card loans, and it certainly wasn't issuing mortgages. Visa is simply a payment network—a toll road—and it collects a fee on every swipe of a Visa card. While banks were collapsing under bad loans, Visa kept collecting its toll.

Unlike lenders, Visa doesn't carry any consumer debt on its books. The company makes money from processing fees, which had been steadily rising for years, including through the past two U.S. recessions in 1991 and 2001. Since 2001, Visa had enticed consumers to use cards more frequently for staples like groceries, gas, and utility bills—about 42% of transactions were "nondiscretionary" by 2008, up from 27% in 2000.

Joseph Saunders, who became CEO in 2007, understood this dynamic perfectly. A former card executive at Washington Mutual and Fleet Financial, Saunders positioned Visa as the anti-bank: "We don't lend money. We don't take deposits. We don't have credit risk. We're a technology company that happens to operate in financial services."

The contrast with traditional banks became stark as 2008 progressed. While Citigroup needed $45 billion in government bailouts, while Bank of America absorbed the toxic Merrill Lynch, while Washington Mutual collapsed entirely, Visa kept printing money. In fiscal 2008, despite "increasing economic turbulence worldwide, Visa posted strong revenue and earnings gains," according to CEO Saunders, who noted the company's "network business model" and "the continuing secular shift to electronic payments".

The IPO also came with protections that would prove crucial. Visa deposited $3 billion in an escrow account to insulate shareholders from lawsuits. This "retrospective responsibility plan" meant that any legal liabilities from the pre-IPO era would be borne by the former member banks, not public shareholders. It was like buying a house where the seller agrees to pay for any foundation problems discovered later.

The transformation from cooperative to corporation fundamentally changed Visa's DNA. The chaordic principles Dee Hock had embedded—distributed decision-making, cooperative competition, minimal hierarchy—gave way to traditional corporate governance. The company now had quarterly earnings calls, activist investors, stock-based compensation. It optimized for shareholder value rather than member consensus.

Some saw this as inevitable evolution. Others saw it as betrayal of Hock's vision. The man himself, watching from his ranch in Pescadero, reportedly told friends: "They've taken a living organism and turned it into a machine. It will make money, lots of money. But it will never again innovate the way it once did."

Yet the numbers were undeniable. Visa's stock initially rallied after the March 2008 IPO, more than doubling in value over two months, reaching an all-time high of $89.83 in May 2008, though it later tumbled to a low of $41.78 in January 2009 as investors feared credit risk. But even at its low, Visa was worth more than many of the banks that had owned it.

The IPO marked the end of Visa as a radical organizational experiment and the beginning of Visa as a conventional public company. But it also validated Hock's original insight: a payment network, once established, becomes almost impossible to dislodge. The cooperative had built the network. The corporation would harvest its value.

The timing, in retrospect, was perfect. Visa went public at the last possible moment before the window slammed shut, raising capital that would fuel expansion through the recession. While the banks that created it struggled to survive, their creation thrived. The student had not just surpassed the teachers—it had rendered them almost irrelevant.

IX. The Modern Era: Digital Transformation & Competition (2008–Present)

Dick Durbin, the Democratic Senator from Illinois, had no idea he was about to transform the payments industry when he stood up on the Senate floor on May 13, 2010. The financial crisis was still raw. Public anger at banks was at fever pitch. Into this environment, Durbin introduced a last-minute amendment to the Dodd-Frank financial reform bill that would cap debit card interchange fees. It was passed as part of the Dodd–Frank financial reform legislation in 2010, as a last-minute addition by Dick Durbin.

"Wall Street reform is really about two things: holding the big banks accountable for how they operate and empowering consumers to make good financial choices. Passage of this amendment is a win for the public on both fronts. Passage of this measure gives small businesses and their customers a real chance in the fight against the outrageously high 'swipe fees' charged by Visa and MasterCard. It will prevent the giant credit card companies from using anti-competitive practices, allow merchants to offer discounts to their customers and restore common sense and fairness to this broken system."

Prior to the Durbin amendment, card swipe fees were previously unregulated and averaged about 44 cents per transaction. The Durbin amendment also gave the Federal Reserve the power to regulate debit card interchange fees, and on December 16, 2010, the Fed proposed a maximum interchange fee of 12 cents per debit card transaction, which CardHub.com estimated would cost large banks $14 billion annually.

Visa's stock plummeted. In a single day, billions in market value evaporated. Investors panicked—if the government could regulate debit fees, what was stopping them from regulating credit? International transactions? The entire toll booth model seemed under threat.

The rule that the Federal Reserve issued went into effect on October 1, 2011 and capped the interchange rate paid to non-exempt card issuers at 0.05 percent plus twenty-one cents. The rule also allowed these non-exempt card issuers to earn an additional one-cent fraud prevention adjustment for implementation of fraud prevention policies.

The impact was immediate and brutal for banks with over $10 billion in assets. Debit interchange fee income fell for treated banks, leading to a fall in noninterest income. Banks only partially offset this loss with deposit fees. But here's what investors missed: Visa wasn't a bank. It didn't receive interchange fees—it received network fees. The Durbin Amendment capped what banks could charge merchants, but it didn't cap what Visa could charge banks for processing transactions.

In fact, Durbin may have inadvertently strengthened Visa's position. The law applies to banks with over $10 billion in assets, and these banks would have to charge debit card interchange fees that are "reasonable and proportional to the actual cost" of processing the transaction. Small banks and credit unions were exempt, creating a two-tier system that made Visa's network even more essential for routing transactions efficiently.

Meanwhile, the shift from credit to debit accelerated. For the first time ever, in 2006, U.S. consumers made more debit purchases than credit charges. That's partly why transaction volume has remained strong even as spending declines; for the first time ever, in 2006, U.S. consumers made more debit purchases than credit charges. By 2015, debit cards accounted for more transactions than credit cards on Visa's network—a complete reversal from two decades earlier.

But the real story of Visa's modern era isn't about regulation. It's about the smartphone revolution that nobody saw coming in 2008. When Steve Jobs unveiled the iPhone in 2007, payments weren't even on the roadmap. Yet within a decade, mobile payments would transform how billions of people interact with money.

The first wave came through apps. PayPal, which had gone public in 2002, suddenly found new life as a mobile payment platform. Square, founded in 2009 by Twitter co-founder Jack Dorsey, turned every smartphone into a credit card terminal. Venmo made splitting dinner bills social. Stripe made accepting payments online as simple as copying and pasting seven lines of code.

Each of these companies was supposedly going to kill Visa. Tech blogs breathlessly proclaimed the death of credit cards. Yet something curious happened: almost all these "Visa killers" ended up riding on Visa's rails. PayPal needed to fund accounts from somewhere—Visa cards. Square needed to accept payments—Visa cards. Even Venmo, when users wanted to cash out instantly, charged them a fee and used—you guessed it—Visa's network.

The mobile wallet wars intensified when Apple Pay launched in 2014. Apple had everything—the devices, the customer relationships, the brand power. Surely this would finally disintermediate Visa. But Tim Cook's negotiators quickly discovered what everyone else had learned: fighting Visa's network effects was like fighting gravity. Instead of replacing Visa, Apple Pay became Visa's newest distribution channel. Every Apple Pay transaction still ran through Visa's network, still generated fees for Visa, still strengthened Visa's moat.

Google Pay, Samsung Pay, and dozens of other digital wallets followed the same pattern. They competed fiercely for consumers' attention while all quietly paying tribute to Visa's network. It was as if every road to Rome not only led through Rome but had to pay a toll to enter.

The numbers tell the story. In 2008, when Visa went public, it processed 62 billion transactions. By 2023, that number had exploded to 276 billion. Visa sold 406 million shares at US$44 per share ($2 above the high end of the expected $37–42 pricing range), raising US$17.9 billion in what was then the largest initial public offering in U.S. history. The company that was worth $36 billion at IPO is now worth $664 billion—an increase of 18x in less than 17 years.

The international expansion has been even more dramatic. Visa's U.S. revenue grew a healthy 23% in fiscal year 2007, but its international revenue soared 57% over 2006. And as formerly cash-based economies in South Korea, China and India embrace the new electronic forms of payments—mobile phone–based transactions are garnering the most buzz—Visa's money-making opportunities are enormous.

Consider India's Unified Payments Interface (UPI), launched in 2016. It processes billions of transactions monthly, enabling instant bank-to-bank transfers through QR codes. Many predicted it would make card networks obsolete in India. Yet Visa adapted, partnering with Indian banks, investing in local fintech startups, and positioning itself as the bridge between India's domestic payment revolution and global commerce. When Indian consumers want to buy from Amazon or book international travel, they still need Visa.

The same pattern plays out globally. China has Alipay and WeChat Pay, which dominate domestic payments. But when Chinese tourists travel abroad or Chinese businesses need to accept international payments, they turn to Visa. Brazil has PIX, its instant payment system. Yet Brazilian e-commerce sites still prominently display Visa logos because consumers trust the brand and merchants need access to international customers.

In January 2020 Visa announced it would acquire Plaid for $5.3 billion. In November 2020, the United States Department of Justice (DOJ) sued to block Visa's acquisition of fintech startup Plaid, claiming that the merger would violate antitrust laws. The DOJ's argument was revealing: they claimed Visa was trying to eliminate a potential future competitor, comparing Plaid to "a volcano" that could threaten Visa's monopoly. Visa eventually abandoned the deal, but the message was clear—the government saw Visa's moat as nearly impregnable.

The rise of cryptocurrency presented another supposed existential threat. Bitcoin was explicitly designed to eliminate intermediaries like Visa. Ethereum enabled smart contracts that could handle payments without traditional networks. Stablecoins promised the benefits of crypto without the volatility. Yet by 2021, Visa announced the acceptance of stablecoin USDC to settle transactions on its network. Rather than fighting crypto, Visa was co-opting it, becoming the bridge between traditional finance and the blockchain future.

Even the COVID-19 pandemic, which devastated most financial services companies, only accelerated Visa's growth. As physical retail shut down, e-commerce exploded. Contactless payments, which had struggled for adoption for years, suddenly became mandatory. Cash, already in decline, became almost taboo—who wanted to handle physical money during a pandemic? Every trend favored Visa.

The threats keep coming. Central bank digital currencies. Real-time payment systems. Buy-now-pay-later services. Neo-banks. Yet Visa keeps growing, keeps adapting, keeps collecting its toll. It's added new revenue streams—data analytics, fraud prevention, consulting services—while never losing focus on its core network.

Today, Visa processes 65,000 transactions per second through data centers that can handle 100 billion computations per second. The network that started with paper cards and carbon-copy slips now uses artificial intelligence to detect fraud in milliseconds, blockchain to settle cross-border transactions, and APIs to embed payments into any digital experience.

The transformation from Dee Hock's chaordic cooperative to today's corporate giant is complete. The radical organizational experiment has become a conventional corporation. The industry disruptor has become the incumbent. The chaos has become order—perhaps too much order.

Yet the fundamental insight remains unchanged: in payments, the network is everything. And Visa's network, built over 65 years, funded by thousands of banks, trusted by billions of consumers, accepted by tens of millions of merchants, has proven remarkably difficult to displace. Every new payment innovation, rather than replacing Visa, seems to make it stronger. The network that ate the world keeps eating.

X. The Business Model: World's Greatest Toll Booth

Warren Buffett once called the credit card business "a toll bridge over a river with no other bridges for miles." He was wrong. Visa isn't a toll bridge—it's something far more powerful. It's the entire road system, and every other form of transportation must somehow connect to it.

To understand Visa's business model, forget everything you think you know about credit cards. Visa uses interchange reimbursement fees as transfer fees between acquiring banks and issuing banks for each Visa card transaction. Visa uses these fees to balance and grow the payment system for the benefit of all participants. But here's the critical distinction: Interchange is not revenue to Visa in Canada. Interchange is a value transfer between financial institutions for accepting payments.

This is the genius of Visa's model and why so many investors misunderstand it. Anytime a card gets swiped, the merchant bears a cost, the biggest portion of which is known as an interchange. Some might think that this interchange fee, usually ranging from 1.5% to 3.5% depending on the card used and other factors, all goes to Visa and Mastercard. That's not true. The interchange fee goes to the issuing bank.

So how does Visa actually make money? Visa and Mastercard, which operate the underlying payment networks that connect all the different stakeholders, collect what's called an assessment fee, roughly 0.15% of a card transaction. This is a tiny part of what a merchant pays. Given that in the last three months of 2023, Visa handled $3.9 trillion of volume and Mastercard handled $2.4 trillion of volume, the assessment fees can add up to tens of billions of dollars in annual revenue.

Think about that math for a second. Visa takes just 0.14-0.15% of each transaction. On a $100 purchase, that's 15 cents. The issuing bank might get $2.50. The merchant's bank gets maybe 50 cents. Yet Visa, taking its tiny slice billions of times over, generated $32.7 billion in revenue in 2023.

The revenue breaks down into four main streams:

Data Processing Revenue ($16.0B in 2023): Visa earns revenue by processing transaction data and offering analytical services to partners. This is the core toll—every transaction that moves through VisaNet generates a processing fee.

Service Revenue ($14.8B in 2023): This includes income from Visa's payment processing services and technological solutions like transaction processing, clearing, settlement, risk management, and security services.

International Transaction Revenue ($11.6B in 2023): Generated from cross-border transaction processing and currency conversion activities. Cross-border transactions are Visa's highest-margin business—the complexity justifies higher fees.

The fourth stream, not detailed in recent reports but growing rapidly, includes value-added services: fraud prevention, data analytics, consulting, and loyalty programs. These services deepen Visa's relationships with banks and merchants while generating recurring revenue beyond transaction fees.

The brilliance of this model becomes clear when you examine the unit economics. Processing a transaction costs Visa essentially nothing on the margin. The network is already built. The data centers are running. The satellites are transmitting. Whether Visa processes 100 billion or 300 billion transactions, the incremental cost is negligible. This is why Visa's operating margins exceed 65%—among the highest of any large company on Earth.

The network itself is a marvel of engineering that most people never think about. VisaNet operates through four primary data centers with full redundancy—if three centers were destroyed simultaneously, the fourth could handle the entire global load. The system processes 65,000 transactions per second at peak, with the capacity for 100 billion computations per second. Response time from swipe to authorization averages 1.5 seconds globally, whether you're buying coffee in Manhattan or carpets in Marrakech.

But the technical infrastructure is just table stakes. The real moat is the multi-sided network effect. Every new cardholder makes Visa more valuable to merchants. Every new merchant makes Visa more valuable to cardholders. Every bank that joins makes the network more valuable to other banks. It's a virtuous cycle that's nearly impossible to break.

Consider what it would take to compete with Visa. You'd need to convince millions of merchants to accept your card—but merchants won't accept cards without cardholders. You'd need millions of cardholders—but consumers won't carry cards that aren't widely accepted. You'd need thousands of banks to issue cards and process transactions—but banks won't invest in a network without merchants and cardholders. It's a three-sided chicken-and-egg problem, and Visa solved it 50 years ago.

The regulatory moat is equally formidable. Visa operates in over 200 countries, each with different financial regulations, data protection laws, and technical standards. The company has spent decades building relationships with regulators, understanding local requirements, and ensuring compliance. A new entrant would need to navigate this maze from scratch—assuming regulators even allow new networks to operate.

The switching costs create another layer of protection. Banks have spent billions integrating with Visa's systems. Merchants have invested in point-of-sale terminals specifically configured for Visa. Consumers have memorized their card numbers, set up auto-pay, and accumulated rewards. Even if a superior network emerged tomorrow, the friction of switching would be enormous.

Nominal payment volume serves as a hedge against inflation, making it a primary revenue driver. If commodity costs rise, Visa's revenue automatically increases. This is crucial: Visa is one of the few businesses that actually benefits from inflation. As prices rise, transaction values rise, and Visa's percentage-based fees rise automatically. No pricing negotiations needed.

The capital efficiency is perhaps the most underappreciated aspect. Visa generates over $15 billion in free cash flow annually while spending just $2 billion on capital expenditures. Compare that to a telecom company like AT&T, which must spend $20 billion annually just to maintain its network. Or to a manufacturer like General Motors, which needs massive factories and inventory. Visa's capital-light model means almost all profit flows straight to shareholders.

Risk management is built into the model's DNA. Visa doesn't extend credit, so it has no credit risk. It doesn't hold deposits, so it has no liquidity risk. It doesn't own inventory, so it has no inventory risk. It doesn't manufacture products, so it has no product liability. The company is essentially a utility that clips a coupon on global commerce.

The pricing power is extraordinary. Effective 4/15/2023, the maximum allowable surcharge for Visa transitions in the US and US territories is decreasing to 3% per transaction. Yet even with regulatory pressure and merchant complaints, Visa has consistently raised prices faster than inflation. Why? Because the value provided—instant, secure, global payments—far exceeds the cost. Would Amazon really stop accepting Visa to save 0.15%? Would consumers switch banks if their Visa card was discontinued?

The durability of this model is proven by its consistency. Through the dot-com crash, the 2008 financial crisis, the COVID pandemic, Visa kept processing transactions, kept generating fees, kept growing. Wars, recessions, pandemics—nothing stops commerce, and nothing stops Visa from taking its toll.

This isn't just a good business model. It's one of the greatest business models ever created. No inventory, no credit risk, no manufacturing, no obsolescence—just a tiny tax on the river of global commerce that grows wider every year. As one hedge fund manager put it: "Visa is the closest thing to a perfect business that exists in public markets."

XI. Playbook: Lessons for Builders & Investors

After studying Visa's 65-year journey from a bank's credit card experiment to a $664 billion global infrastructure company, several timeless lessons emerge for builders and investors. These aren't just historical curiosities—they're principles that apply to any network business, platform, or marketplace being built today.

The Power of Giving Up Control to Gain Influence

Bank of America's decision to give up ownership of BankAmericard in 1970 seemed insane at the time. They had spent $100 million building the network. They owned the brand. They controlled the technology. Yet by relinquishing control to create National BankAmericard Inc. (later Visa), they gained something far more valuable: a network that would grow exponentially because every participant had skin in the game.

This principle appears repeatedly in successful platforms. The internet grew because no one controlled it. Linux succeeded because Linus Torvalds gave up control to the community. Ethereum thrives because no single entity owns it. The lesson: sometimes the path to dominance is surrendering dominion. When you try to control a network, you limit it to your own capabilities. When you release control but maintain influence through standards and governance, the network can grow beyond any single entity's constraints.

Standards as a Business Model

Visa doesn't sell products. It doesn't even really sell services. It sells standards—a common language that allows economic actors to communicate. The 16-digit card number. The magnetic stripe specification. The EMV chip protocol. The authorization message format. These boring, technical standards are Visa's true product.

Building a standards-based business requires different thinking. You're not competing on features or price. You're competing on adoption and trust. The standard itself has no value—its value comes from how many others adopt it. This is why Visa spent decades giving away technology, subsidizing adoption, and even helping competitors implement their standards. They understood that owning the standard was more valuable than owning the technology.

Coopetition: When Competitors Must Cooperate

Visa pioneered a model where fierce competitors (banks) cooperated to create infrastructure they all needed but none could build alone. Chase and Bank of America compete viciously for customers, yet they cooperate seamlessly on Visa standards. This "coopetition" model has become the template for modern platforms.

The key insight: identify what competitors need but can't efficiently build separately. Create a neutral ground where they can cooperate on infrastructure while competing on service. Amazon Web Services follows this model—competitors like Netflix and Disney+ both use AWS while battling for viewers. Apple's App Store enables competing apps while taking its cut. The lesson: find the common need, build the shared infrastructure, then let competition flourish on top.

Network Effects: Building vs. Buying

Visa's network effects weren't bought—they were built over decades through millions of small decisions. Each merchant added. Each card issued. Each bank recruited. Network effects can't be acquired through M&A; they must be cultivated through patient growth.

This is why Visa's attempts to buy into new networks (like the failed Plaid acquisition) often struggle. You can buy technology, talent, even customers—but you can't buy the trust and habits that create true network effects. PayPal learned this when it tried to force users to adopt new products. Google learned it with Google+. The lesson: network effects are earned, not purchased.

The Importance of Governance Structure

Dee Hock's governance innovation—creating an organization owned by its members with high thresholds for change—seems arcane. But it solved a fundamental problem: how do you get competitors to invest in shared infrastructure? The answer: create governance that protects everyone from everyone else.

The 80% voting requirement meant no single bank could hijack the network. Regional representation ensured geographic balance. The for-profit structure ensured efficiency. The no-retained-earnings rule meant value flowed to participants, not management. This governance structure was as important as the technology in Visa's success.

Modern platforms often fail because they get governance wrong. They're either too centralized (killing innovation) or too decentralized (creating chaos). The lesson: design governance that balances stability with evolution, cooperation with competition, efficiency with fairness.

When to Choose Growth Over Profits

For its first three years, BankAmericard lost enormous sums. The Fresno drop was a disaster. Fraud was rampant. Operations were chaos. Yet Bank of America kept investing because they understood: in network businesses, scale is everything. You must reach critical mass before the model works.

This principle drives modern platform strategy. Amazon lost money for years while building scale. Uber still loses money in many markets while establishing network density. The lesson: in network businesses, premature profit optimization can kill growth. You need courage (and capital) to push through the valley of death to reach network effects on the other side.

The Toll Booth Business Model

Visa's model is elegantly simple: build essential infrastructure, then take a tiny cut of every transaction. Don't try to capture too much value (that attracts competition and regulation). Don't provide the service itself (that creates operational complexity). Just facilitate and tax.

This toll booth model appears everywhere now. Apple's App Store takes 30% of digital transactions. Google takes a cut of ad revenues. Amazon takes a percentage of third-party sales. The lesson: position yourself as infrastructure, not application. Be the platform, not the product. Own the rails, not the trains.

Timing and Patience in Network Businesses

Visa took 16 years from founding (1958) to reaching profitability at scale (1974). It took another 34 years to go public (2008). This patient capital approach is almost impossible in today's venture environment, yet it's often necessary for true infrastructure plays.

The lesson: network businesses have different time horizons than traditional businesses. They require patient capital, long-term thinking, and the courage to persist through years of losses. The payoff, as Visa demonstrates, can be extraordinary—but only for those with the patience to wait.

The Power of Boring

Visa is boring. Payment processing is boring. Standards are boring. But boring is beautiful in business. Boring means predictable. Boring means essential. Boring means defensible. While everyone chases the hot new thing, boring businesses quietly compound value for decades.

The Infrastructure Paradox

The best infrastructure becomes invisible. Nobody thinks about Visa when they buy coffee. Nobody considers the electrical grid when they flip a switch. The paradox: the more essential you become, the less people notice you. This invisibility is actually a moat—it means you've become part of the assumed environment, too fundamental to question or replace.

For builders, the lesson is to aim for invisibility through ubiquity. For investors, it's to look for businesses so boring and essential that they've become invisible. These are often the best long-term compounders—hidden in plain sight, collecting their toll on human activity, as essential and unnoticed as the roads we drive on.

XII. Bear vs. Bull Case

Bull Case: The Secular Shift Has Just Begun

The bulls see Visa as still being in the early innings of a multi-decade transformation. Start with the staggering statistic: 80% of the world's transactions are still cash. In the United States, supposedly the most advanced payment market, cash still accounts for 20% of transactions. In Europe, it's 50%. In emerging markets like India, Indonesia, and Nigeria, cash dominance exceeds 90%. Every percentage point shift from cash to electronic payments represents billions in additional payment volume for Visa.

The international expansion opportunity is particularly compelling. In 2023, Visa boasts 4.3 billion users, collaborates with 14,000 financial institutions, and records a payment volume of $12.3 trillion. Yet this barely scratches the surface of global commerce. The middle class in Asia and Africa is expected to add 2 billion people by 2030. These new consumers will leapfrog cash entirely, moving straight to digital payments via smartphones. Visa is positioning itself as the bridge between local payment methods and global commerce.

New payment types offer another growth vector. Business-to-business (B2B) payments, still dominated by checks and wire transfers, represent a $120 trillion annual opportunity. Visa is only now beginning to penetrate this market with virtual cards and straight-through processing. Cross-border payments, growing at 15% annually driven by global e-commerce and remote work, carry Visa's highest margins. New verticals like healthcare payments, government disbursements, and even cryptocurrency settlement are just beginning to digitize.

The network effects only strengthen with scale. Every new user, merchant, and use case makes the network more valuable to all participants. This creates a compounding effect where Visa's competitive advantage actually widens over time rather than eroding. The company that was worth $36 billion at IPO is now worth $664 billion—and bulls argue this is still early.

The regulatory moat paradoxically strengthens Visa's position. While regulations like the Durbin Amendment grab headlines, they actually create barriers to entry. New competitors must navigate an increasingly complex regulatory landscape that Visa has already mastered. The company's compliance infrastructure, built over decades, would cost tens of billions to replicate.

Switching costs continue to rise as Visa embeds deeper into the financial system. Banks are integrating Visa's fraud prevention, data analytics, and loyalty platforms. Merchants are adopting Visa's APIs for everything from recurring billing to installment payments. Consumers are storing credentials in digital wallets, setting up autopay, and accumulating rewards. Each integration makes switching more painful and less likely.

The inflation hedge aspect is particularly relevant in today's environment. Nominal payment volume serves as a hedge against inflation, making it a primary revenue driver. If commodity costs rise, Visa's revenue automatically increases. While most companies struggle with inflation, Visa benefits automatically as transaction values rise with prices.

Bulls also point to Visa's incredible capital efficiency. With 65% operating margins and minimal capital requirements, the company can return massive amounts of cash to shareholders while still investing in growth. The dividend has grown every year since the IPO, and the company has bought back over $50 billion in stock, reducing share count by 25%.

Bear Case: The Threats Are Real and Multiplying

The bears see storm clouds gathering on multiple fronts. Start with regulation. The Durbin Amendment was just the beginning. Senator Durbin's Credit Card Competition Act, if passed, would extend similar price controls to credit cards. The European Union continues to ratchet down interchange fees. Governments worldwide are waking up to the "tax" that card networks impose on their economies.

Central bank digital currencies (CBDCs) represent an existential threat that bulls underestimate. China's digital yuan already has 260 million users and processes billions in transactions. The European Central Bank is developing a digital euro. The Federal Reserve is exploring a digital dollar. These government-backed digital currencies could bypass card networks entirely, especially for domestic transactions. Why would governments allow private companies to tax their digital currencies?

Alternative payment methods are fragmenting the market. In China, Alipay and WeChat Pay have essentially eliminated card usage. In India, UPI processes 10 billion transactions monthly with zero merchant fees. Brazil's PIX grew from zero to 15% of payments in just two years. These aren't just regional alternatives—they're proof that countries can build payment infrastructure without Visa.

Big Tech competition is intensifying. Apple Pay isn't just a wallet—it's building its own payment infrastructure with Apple Pay Later and Apple Cash. Google, Amazon, and Meta are all developing payment capabilities that could eventually bypass traditional networks. These companies have the scale, technology, and customer relationships to build alternative networks. More importantly, they can subsidize payments with profits from other businesses.

Market saturation in developed countries limits growth potential. In the U.S., card penetration is already over 80%. Europe is similar. These markets drive the majority of Visa's profits, but growth is slowing to GDP-plus rates. The high-growth emerging markets have lower transaction values and face more competition from local alternatives.

The rise of real-time payment systems undermines Visa's value proposition. FedNow in the U.S., the Single Euro Payments Area (SEPA) in Europe, and similar systems worldwide enable instant bank-to-bank transfers without card networks. As these systems mature and add features like request-to-pay and recurring transfers, they could displace cards for many use cases.

Cryptocurrency and blockchain technology, while currently complementary, could eventually disintermediate traditional networks. Stablecoins like USDC enable instant, global transfers without traditional infrastructure. Smart contracts could handle complex payment logic without intermediaries. While adoption is still early, the technology is improving rapidly.

The bears also worry about concentration risk. Visa's largest customers—JPMorgan Chase, Bank of America, Wells Fargo—are massive and growing through consolidation. These mega-banks have increasing negotiating power and could demand lower fees or even build alternative networks. Amazon famously banned Visa cards in the UK over fees (though later reversed), showing that even Visa isn't immune to customer pushback.

Valuation is another concern. At 30x earnings, Visa trades at a significant premium to the market. This valuation assumes continued high growth and margin expansion. Any disappointment—whether from regulation, competition, or macro weakness—could trigger multiple compression. The stock has been a massive winner, but trees don't grow to the sky.

The Verdict: Asymmetric Risk/Reward

The bull-bear debate ultimately comes down to timeframes and probabilities. Over the next 5-10 years, the bulls have history on their side. The shift from cash to electronic payments has been consistent for 50 years across every country, through every economic cycle. Visa has survived and thrived through multiple technological transitions—from paper to magnetic stripe to chip to contactless to mobile. The company's track record of adaptation is unmatched.

But the bears raise valid concerns about the 10-20 year horizon. The convergence of CBDCs, real-time payments, and blockchain technology could fundamentally reshape the payments landscape. Visa's moat, while formidable, isn't impregnable. The question is whether Visa can evolve fast enough to remain relevant in a potentially post-card world.

For investors, the key is weighing the certainty of near-term cash flows against the uncertainty of long-term disruption. Visa will likely remain highly profitable for the next decade. Whether it maintains its dominance for the next two decades is less clear. This asymmetry—near-term visibility versus long-term uncertainty—defines the investment debate.

The truth likely lies somewhere in between. Visa will probably lose some market share to alternatives but remain profitable and essential. The company might not grow at 15% forever, but it doesn't need to at current valuations. Even modest growth with continued margin expansion and capital returns could generate attractive returns.

The biggest risk might be the one nobody's discussing: that success breeds complacency. Visa has been so successful for so long that it might miss the next platform shift. The company that disrupted banking might itself be disrupted—not by a frontal assault, but by a thousand cuts from technologies and business models that don't yet exist.

XIII. Epilogue: The Network That Ate the World

Stand in any checkout line, anywhere in the world, and watch. The ritual is so common it's invisible: card presented, machine beeps, receipt prints. In that mundane moment, a packet of data has traveled potentially thousands of miles, passed through multiple data centers, been verified against billions of previous transactions, checked for fraud patterns, authorized by a distant bank, and settled between financial institutions—all in less than two seconds. From 65,000 cards mailed in Fresno to 4 billion cards globally, from paper slips and carbon copies to artificial intelligence and blockchain, Visa's journey mirrors the transformation of money itself.