LyondellBasell: The Chemical Giant That Died and Was Reborn

I. Introduction & Opening Hook

Picture this: December 20, 2007. In a gleaming conference room overlooking Manhattan, executives from Access Industries pop champagne bottles. They've just closed the deal of the decade—a $19 billion acquisition of Houston-based Lyondell Chemical Company by Basell Polyolefins, creating the third-largest chemical company on Earth. The timing seemed perfect. Oil prices were soaring, chemical margins were healthy, and the combined entity would dominate global polyolefins markets from Houston to Rotterdam to Hong Kong.

Thirteen months later, those same executives would be filing for Chapter 11 bankruptcy protection, crushed under $24 billion in debt as the worst financial crisis since the Great Depression vaporized demand for plastics. The company that was supposed to rule the chemical world had become the largest bankruptcy in the sector's history—a cautionary tale about leverage, timing, and hubris that cost investors billions.

Yet here's where the story takes an extraordinary turn. Today, LyondellBasell stands as one of the most profitable chemical companies in the world, generating over $40 billion in annual revenue with industry-leading margins. The company that died in 2009 was reborn stronger, leaner, and perfectly positioned to ride the American shale revolution to unprecedented profits. How did a company go from the worst-timed merger in chemical history to becoming a cash-generating machine that's returned over $30 billion to shareholders since 2010?

This is the story of three remarkable leaders—Len Blavatnik, the Soviet-born billionaire who orchestrated both the deal and the resurrection; Jim Gallogly, the turnaround specialist who guided the company through bankruptcy; and Bob Patel, the operations guru who transformed it into a sustainability-focused powerhouse. It's a story about the brutal cyclicality of commodity chemicals, the transformative power of shale gas, and the art of corporate resurrection.

But most of all, it's a story about timing. In business, as in chemistry, the same elements combined at different temperatures and pressures yield entirely different results. For LyondellBasell, the difference between catastrophe and triumph was measured not in decades or years, but in months. The company that filed for bankruptcy when oil was $40 per barrel would emerge just as the shale boom was about to flood America with cheap natural gas liquids, creating the greatest feedstock advantage in chemical industry history.

The journey from Nobel Prize-winning discoveries to bankruptcy court to becoming one of the S&P 500's best performers is unlike any other corporate saga. It involves Ukrainian oligarchs, Texas wildcatters, Dutch engineers, and Wall Street restructuring specialists. It spans from post-war Europe's reconstruction to China's industrial rise to the circular economy revolution. And at its heart lies a simple but profound question: Can a company built on fossil fuels reinvent itself for a sustainable future?

II. The Deep History: Nobel Prizes and Chemical Foundations (1950s-1990s)

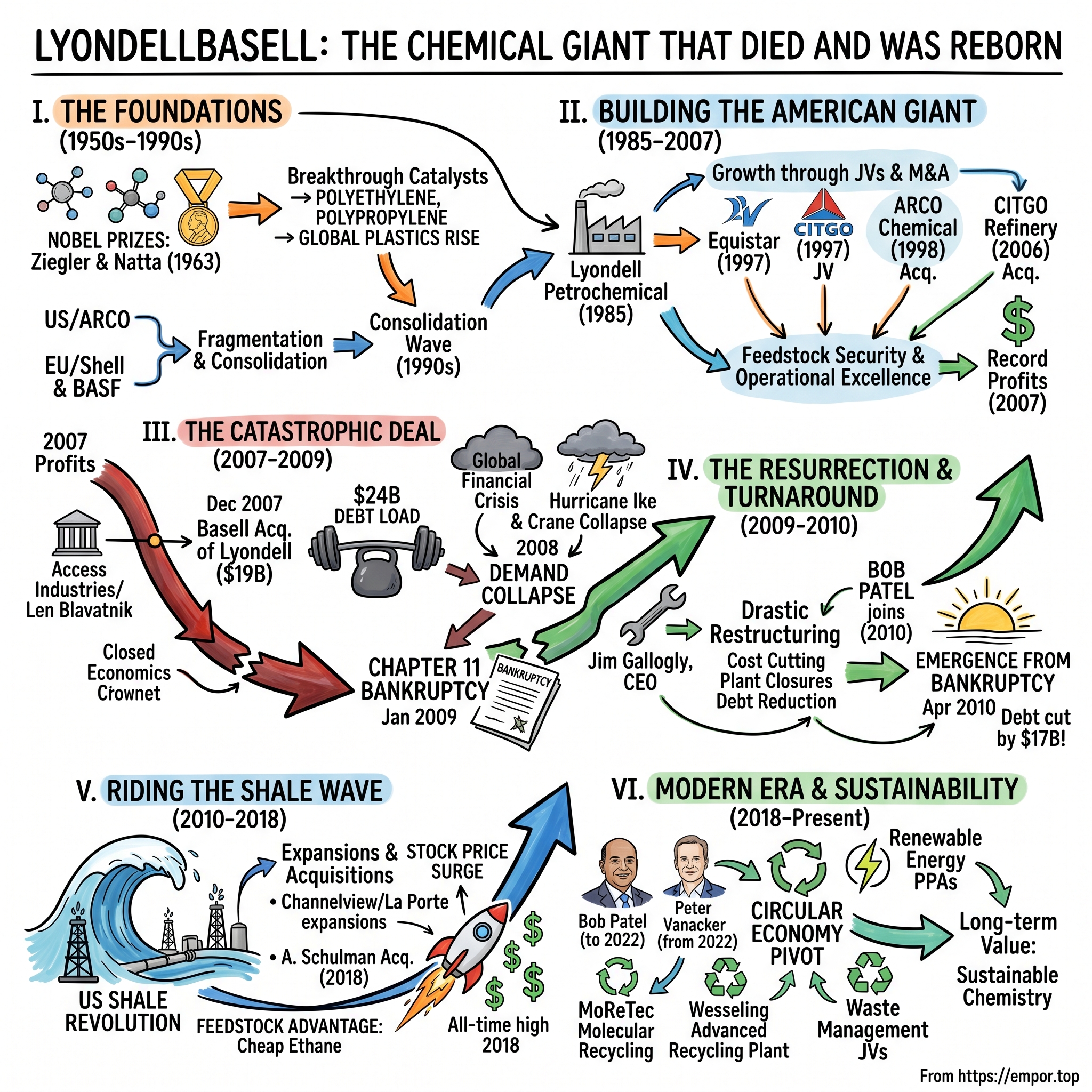

The morning of December 10, 1963, in Stockholm's Concert Hall was crisp and ceremonial. Karl Ziegler, a methodical German chemist, and Giulio Natta, an elegant Italian professor, stood before Sweden's King Gustaf VI Adolf to receive the Nobel Prize in Chemistry. Their discovery—catalysts that could polymerize ethylene and propylene at low pressures and temperatures—seemed arcane to the audience. Yet within two decades, their work would transform civilization itself, creating the plastics that would define modern life.

Ziegler had stumbled upon his breakthrough almost by accident in 1953 at the Max Planck Institute in Mülheim. While investigating aluminum compounds, his team discovered that adding titanium created a catalyst that could link ethylene molecules into long chains—polyethylene—at room temperature and atmospheric pressure. Previously, making polyethylene required pressures of 1,000 atmospheres and temperatures exceeding 200°C. Ziegler's catalyst was like finding a key that unlocked a door engineers had been trying to break down with sledgehammers.

Natta, working at the Polytechnic Institute of Milan, took Ziegler's discovery further. Using similar catalysts on propylene, he created polypropylene—a plastic that was stronger, more heat-resistant, and more versatile than polyethylene. But Natta's real genius was recognizing that these catalysts didn't just make polymers; they made stereoregular polymers, with molecular structures as ordered as crystal lattices. This ordering gave the plastics unprecedented strength and clarity. "We are not just making materials," Natta told his students, "we are architecting molecules."

By the 1960s, chemical giants across Europe and America were licensing Ziegler-Natta technology, racing to build polyolefin plants. In the Netherlands, Royal Dutch Shell partnered with BASF to create massive complexes. In Italy, Montedison—formed from the merger of Montecatini (Natta's patron) and Edison—became a polyolefins powerhouse. In Germany, Hoechst invested billions of Deutsche Marks in propylene capacity. These companies weren't just making plastics; they were building the material foundation for the consumer economy.

The American story unfolded differently, driven more by oil than by chemistry. Atlantic Richfield Company—ARCO—had grown rich pumping crude from Alaska's North Slope. But ARCO's executives saw that the real money wasn't in selling oil; it was in transforming oil into higher-value products. In 1966, ARCO acquired Sinclair Oil, gaining refineries and chemical plants across the Gulf Coast. By 1985, ARCO had spun off its chemical operations into ARCO Chemical Company, based in Newton Square, Pennsylvania, but with its heart in the sprawling complexes along the Houston Ship Channel.

The Houston facilities were marvels of industrial engineering. The Channelview complex alone covered 3,900 acres—larger than many cities—with miles of pipes carrying ethylene, propylene, and dozens of other chemicals between crackers, reactors, and storage tanks. Workers described it as a city of steel, where the air shimmered with heat and the night sky glowed orange from flare stacks. These weren't factories in any traditional sense; they were continuous-flow chemical machines that ran 24/7, turning natural gas liquids into the building blocks of modern life.

Dan Smith arrived at ARCO Chemical in 1976 as a young engineer fresh from Georgia Tech. Over two decades, he rose through the ranks, developing a reputation as someone who understood both the chemistry and the business. "Dan could walk through a plant and spot inefficiencies like a conductor hearing a wrong note," recalled a former colleague. By the mid-1990s, Smith had become president of ARCO Chemical, overseeing one of America's largest petrochemical operations.

But the chemical industry of the 1990s was fragmenting and consolidating simultaneously. In Europe, the old national champions were breaking apart—Hoechst spinning off chemicals to focus on pharmaceuticals, Montedison restructuring after near-bankruptcy. In America, oil companies were questioning whether chemicals fit their portfolios. The industry was trapped in a brutal cycle: when times were good, everyone added capacity; when times were bad, nobody could afford to shut down plants because the fixed costs were too high.

The solution, industry consultants argued, was consolidation. Bigger companies could optimize production across multiple plants, negotiate better feedstock contracts, and weather downturns. This logic drove a wave of joint ventures and acquisitions. In 1997, Lyondell (which had been formed from ARCO Chemical's IPO in 1985) partnered with Millennium Chemicals and Occidental Chemical to create Equistar Chemicals, combining their ethylene and polyethylene operations. The venture instantly became one of North America's largest petrochemical companies, but the structure was unwieldy—three parents with different strategies trying to manage one child.

Meanwhile, across the Atlantic, a different consolidation story was unfolding. Shell and BASF, frustrated by poor returns from their polyolefins businesses, decided to combine them into a joint venture called Basell in 2000. The logic was compelling: Shell brought feedstock advantages and global presence; BASF contributed world-class technology and operational excellence. The new entity would have revenues exceeding €6 billion and plants from Wesseling to Bayport.

Yet even as these megadeals were signed, the fundamental challenge remained: polyolefins were becoming commoditized. The Ziegler-Natta catalysts that had once been revolutionary were now standard. Chinese companies were building massive plants using licensed technology. Margins were compressed between volatile oil prices (which determined costs) and competitive markets (which limited pricing power). The winners, everyone understood, would be those with either the lowest costs or the most differentiated products.

By the early 2000s, the stage was set for even bolder consolidation. The fragments of the post-war chemical industry—the Nobel Prize technologies, the oil company spin-offs, the European national champions—were about to be assembled into something unprecedented. But first, an unlikely player would enter the scene: a Soviet-born entrepreneur who had made his fortune in Russian aluminum and was now looking to build a global industrial empire from his base in New York.

The chemical industry's deep history—from Nobel Prizes to industrial giants to fragmentation—had created the pieces of a puzzle. Soon, Len Blavatnik would attempt to assemble them into a masterpiece. The question was whether he was building a monument to industrial ambition or a tower destined to collapse under its own weight.

III. The Lyondell Story: Building an American Chemical Giant (1985-2007)

The incorporation documents for Lyondell Petrochemical Company, filed in Delaware on March 27, 1985, ran just twelve pages. But those dozen sheets of legal boilerplate represented one of the most ambitious spin-offs in American corporate history. ARCO, flush with Alaskan oil profits but frustrated by chemical industry volatility, was setting its chemical division free. The new company would start life with $1.3 billion in revenues, 2,300 employees, and some of the most sophisticated petrochemical assets on the Gulf Coast.

Bob Gower, Lyondell's first CEO, was a chemical engineer who'd spent his entire career at ARCO. Standing before employees at the Channelview complex on the company's first day as an independent entity, he made a promise: "We're not going to be just another chemical company. We're going to be the most efficient, most innovative, most profitable polyolefins producer in North America." It was Texas-sized ambition, but Gower had reason for confidence. Lyondell's plants were newer and more efficient than most competitors', and the company had inherited ARCO's culture of operational excellence.

The early years validated Gower's optimism. Lyondell went public in January 1989 at $15 per share, raising $1.25 billion in what was then the largest IPO in chemical industry history. Wall Street loved the story: a pure-play petrochemical company with modern assets, skilled workforce, and exposure to the growing plastics market. By 1990, the stock had doubled. "Lyondell was the anti-conglomerate," explained a former Morgan Stanley chemicals analyst. "While everyone else was diversifying, they were focusing."

But focus meant vulnerability to cycles, and the 1991 recession hit hard. Polyethylene prices plummeted from 42 cents per pound to 28 cents. Lyondell's earnings evaporated, and the stock crashed below its IPO price. Gower, under pressure from the board, made a fateful decision: instead of retrenching, Lyondell would grow its way out of trouble through strategic acquisitions and joint ventures.

The Equistar joint venture, announced in December 1997, was Gower's masterpiece of financial engineering. Lyondell contributed its ethylene and polyethylene assets; Millennium Chemicals added its Quantum Chemical operations; Occidental Chemical threw in its petrochemical plants. The combined entity would have $6 billion in revenues and become North America's largest ethylene producer. But the structure was byzantine—Lyondell owned 41%, Millennium 29%, and Occidental 30%—creating governance nightmares that would haunt the company for years.

Dan Smith took over as CEO in 1999, inheriting both Gower's ambitions and his complicated legacy. Smith was a different breed of executive—less engineer, more dealmaker. His first major move was audacious: acquiring ARCO Chemical, Lyondell's former parent company, for $5.6 billion in June 1998. The irony wasn't lost on anyone. "The child swallowing the parent," the Houston Chronicle headline read. But Smith saw logic where others saw symbolism. ARCO Chemical brought propylene oxide and styrene operations that complemented Lyondell's olefins business, creating an integrated powerhouse.

The integration was brutal. Smith cut 1,000 jobs, closed redundant offices, and consolidated operations. But he also invested heavily in technology, particularly in propylene oxide production. Lyondell had developed a proprietary process that produced propylene oxide without creating byproducts—a breakthrough that gave them a significant cost advantage. "Most companies made propylene oxide and got stuck with chlorine or styrene they had to sell," explained a former technology director. "We made just propylene oxide, pure and simple."

By 2004, Smith was ready for his next big move: acquiring Millennium Chemicals for $2.3 billion. This wasn't just about adding capacity; it was about consolidating the Equistar joint venture under Lyondell's full control. The deal negotiations were tortuous, with Occidental demanding top dollar for its stake and Millennium shareholders skeptical about selling. Smith spent months shuttling between Houston, Dallas, and New York, crafting a deal that satisfied all parties. When it closed in November 2004, Lyondell had revenues exceeding $18 billion and had become America's third-largest chemical company.

But Smith's masterstroke came in 2006 with the $2.1 billion acquisition of Citgo's 41.25% interest in the Houston Refining LP. The refinery, located adjacent to Lyondell's Channelview complex, processed 270,000 barrels of crude oil daily. This wasn't just vertical integration; it was about feedstock security. The refinery could provide Lyondell's chemical plants with naphtha and other raw materials, insulating them from supply disruptions and price volatility. "We went from being at the mercy of oil companies to controlling our own destiny," Smith told investors.

The Houston Refining acquisition transformed Lyondell's economics. In 2006, the company earned $1.4 billion in EBITDA. By early 2007, analysts were projecting $2 billion for the year. The stock hit an all-time high of $43 in May 2007. Smith, now 64 and contemplating retirement, had built the American chemical champion he'd envisioned. Lyondell employed 10,000 people, operated plants across the Gulf Coast, and had technology licenses generating royalties from China to Saudi Arabia.

The company culture Smith had fostered was distinctly Texan—informal but intense, collaborative but competitive. At the Houston headquarters, executives wore boots and jeans as often as suits. Decisions were made quickly, often in hallway conversations rather than formal meetings. Safety was paramount—every meeting started with a "safety moment"—but risk-taking was encouraged. "We hired chemical cowboys," recalled a former HR director. "People who could handle the pressure of running billion-dollar assets where one wrong decision could cause an explosion."

The international expansion was accelerating too. Lyondell had joint ventures in Mexico, technology partnerships in Asia, and was exploring opportunities in the Middle East. The company's POSM (propylene oxide/styrene monomer) technology was considered best-in-class, with plants using Lyondell licenses producing millions of tons annually worldwide. Smith had even started discussions about building a massive complex in Saudi Arabia, partnering with Saudi Aramco to convert cheap natural gas into high-value chemicals.

But success bred attention, and not all of it was welcome. Private equity firms, flush with cheap credit from the booming leveraged finance markets, saw Lyondell as an ideal LBO candidate: strong cash flows, hard assets, and a management team nearing retirement. Throughout 2007, rumors swirled about potential bidders. Apollo Management, Blackstone, and KKR all reportedly ran the numbers. But the most serious interest came from an unexpected source: Basell Polyolefins, the European joint venture that had recently been acquired by a Russian-American billionaire named Leonard Blavatnik.

Smith initially rebuffed Basell's overtures. Lyondell was performing well, and he saw no need to sell. But Blavatnik was persistent, and his offers kept climbing. By November 2007, with Basell offering $48 per share—a 45% premium to where the stock had been trading—Smith and the board faced a dilemma. The price was extraordinary, but the timing felt wrong. Credit markets were already showing signs of stress. Several major LBOs had failed to close. The subprime mortgage crisis was spreading.

The board meeting on November 16, 2007, lasted twelve hours. Outside advisors from Merrill Lynch and Wachtell Lipton presented fairness opinions. Some directors worried about the debt levels Basell would need to finance the deal. Others argued they had a fiduciary duty to accept such a generous offer. Smith, exhausted and perhaps ready to pass the torch, ultimately supported the deal. "Forty-eight dollars is a price we may never see again," he told the board.

The merger agreement, signed on December 17, 2007, valued Lyondell at $19 billion enterprise value, including $2.8 billion in existing debt. It was the largest acquisition in chemical industry history. Smith would receive $45 million in change-of-control payments. Employees would share $300 million in accelerated vesting of stock options. Everyone, it seemed, was getting rich.

Three weeks later, as champagne corks popped in Houston and New York to celebrate the closing, oil prices hit $100 per barrel for the first time in history. It felt like validation—high oil prices meant strong demand for chemicals. Nobody at those celebrations could have imagined that within a year, oil would crash to $32, demand for plastics would evaporate, and the combined company would be fighting for survival in bankruptcy court. Dan Smith's American chemical champion was about to enter the darkest chapter in its history, merged with a European rival and controlled by a Russian-American oligarch just as the global economy was about to collapse.

IV. Enter Len Blavatnik: The Basell Acquisition (2005-2007)

Leonard Valentinovich Blavatnik's path from Moscow to Manhattan reads like a post-Soviet thriller. Born in 1957 in Odessa to a Jewish family, he emigrated to the United States in 1978 with his parents and $75 in his pocket. By 2007, he was worth $10 billion and orchestrating the largest chemical industry acquisition in history from his offices high above Fifth Avenue. The journey between those points involved Harvard Business School, Russian aluminum wars, and a friendship with Viktor Vekselberg that would reshape global industry.

Blavatnik's accent carried only the faintest trace of Russian when he addressed Basell's management team in Amsterdam in August 2005. Access Industries, his privately held industrial group, had just won the auction for Basell Polyolefins with a $5.7 billion bid, beating out Apollo, Blackstone, and a consortium of chemical companies. "We are not financial engineers," Blavatnik told the assembled executives. "We are builders. We buy assets and we improve them. We hold them. We grow them." His words were carefully chosen to reassure managers worried about private equity's slash-and-burn reputation.

The Basell acquisition was Blavatnik's boldest move yet outside the former Soviet Union. He'd made his first fortune in the 1990s Russian privatizations, partnering with Vekselberg to acquire oil and aluminum assets at fire-sale prices. Their crown jewel was TNK, an oil company they'd built through acquisitions and later sold to BP for $7 billion. But Blavatnik understood that remaining purely in Russian assets was dangerous. He needed geographic diversification and assets in stable, law-abiding jurisdictions. Chemicals, with their hard assets and predictable cash flows, were perfect.

Volker Trautz, Basell's CEO, initially viewed Blavatnik with suspicion. Trautz was a BASF lifer, a German chemical engineer who'd run plants from Ludwigshafen to Tarragona. The idea of working for a Russian-American financier seemed incongruous. But their first meeting, in Blavatnik's London mansion overlooking Hyde Park, changed his mind. "Len understood chemicals," Trautz later recalled. "He asked about catalyst technology, propylene yields, the Chinese capacity additions. He'd done his homework."

Blavatnik's vision for Basell was ambitious but logical: combine the company's European technology leadership with American scale to create the first truly global polyolefins champion. Basell had brilliant technology—its Spheripol and Spherilene processes were industry standards—but lacked feedstock advantages. American producers like Lyondell had access to cheap natural gas liquids but needed technology to differentiate their products. The combination would be formidable.

The first two years under Access Industries ownership exceeded expectations. Blavatnik invested €300 million upgrading Basell's plants, improving efficiency by 15%. He hired McKinsey to streamline operations, cutting $200 million in annual costs without closing a single facility. Most importantly, he gave Trautz autonomy. "Len would call with ideas, suggestions, but never orders," said a former Basell executive. "He understood that chemicals aren't like trading aluminum—you need deep technical knowledge."

By early 2007, Basell was generating over $1 billion in annual EBITDA. The company's Hostalen process for making polyethylene was winning new licenses globally. Its polypropylene catalyst technology was a generation ahead of competitors. Blavatnik could have IPO'd the company for a massive profit. Investment bankers from Goldman Sachs and JPMorgan pitched valuations exceeding $10 billion. But Blavatnik had a different idea: instead of selling Basell, why not use it as a platform for something bigger?

The pursuit of Lyondell began quietly in March 2007. Blavatnik hired Lazard Frères, the boutique investment bank known for complex cross-border deals. Eugene Davis, Lazard's vice chairman and a restructuring specialist, led the approach. The initial overture to Dan Smith was rebuffed politely but firmly. Lyondell wasn't for sale. But Blavatnik, who'd learned patience during the chaotic Russian privatizations, simply waited and watched.

By July 2007, with credit markets still flush and chemical prices strong, Blavatnik decided to move aggressively. He instructed Davis to offer $40 per share, a 20% premium to Lyondell's stock price. Smith and Lyondell's board rejected it as inadequate. Blavatnik raised to $44. Still no. The negotiations took on a theatrical quality, with offers and counteroffers delivered via formal letters heavy with legal language. Behind the scenes, though, the real discussions were more nuanced.

The turning point came in October 2007 when Blavatnik flew to Houston for a secret meeting with Smith at the Houstonian Hotel. Over dinner, the two men found unexpected common ground. Both were operators, not financiers. Both believed in the long-term potential of chemicals despite the cyclicality. And both saw the logic of combining their companies. "Dan was tired," a person familiar with the meeting later said. "He'd built something great, but he was ready to hand it off. Len represented continuity, not disruption."

The financing for the deal was a monument to pre-crisis excess. Access Industries would contribute $3 billion in equity. Apollo Management and Ares Management, two private equity firms Blavatnik had cultivated relationships with, would add another $1.5 billion. The remaining $14.5 billion would come from debt: $8 billion in bank loans led by Goldman Sachs, UBS, and Citigroup; $4 billion in bridge loans; and $2.5 billion in high-yield bonds. The pro forma leverage ratio would be 7.5x EBITDA—aggressive even by 2007 standards.

The lawyers worked around the clock to close the deal before year-end. Wachtell Lipton represented Lyondell; Kirkland & Ellis advised Access Industries. The merger agreement ran 245 pages, with elaborate provisions for everything from environmental liabilities to pension obligations. But the most important clause was also the simplest: Access Industries would pay $48 per share in cash, no financing condition. If the banks backed out, Blavatnik was still on the hook.

The announcement on November 19, 2007, sent shockwaves through the chemical industry. "Len Blavatnik's $19 Billion Bet on Plastics," the Wall Street Journal headline screamed. Competitors were stunned. Dow Chemical's CEO called it "financially aggressive." BASF's chairman termed it "strategically bold but risky." Saudi Basic Industries Corporation (SABIC) immediately began reconsidering its own expansion plans, worried about competing with the combined entity.

Blavatnik held a town hall for Lyondell employees in Houston on December 4, 2007. Standing before 500 workers in the auditorium, he tried to calm fears about layoffs and plant closures. "This is not about cost-cutting," he insisted. "This is about growth. Together, Basell and Lyondell will have the scale to compete globally, the technology to differentiate our products, and the financial strength to invest through cycles." He announced $100 million in retention bonuses for key employees and promised to maintain Houston as the headquarters.

The integration planning was already underway, led by teams from both companies and McKinsey consultants. They identified $300 million in annual synergies from procurement savings, logistics optimization, and best-practice sharing. The combined company would have revenues exceeding $50 billion, 60 production sites across 19 countries, and technology licenses generating $400 million in annual royalties. On paper, it looked unstoppable.

But even as the deal closed on December 20, 2007, warning signs were flashing. Bear Stearns had collapsed. The subprime crisis was spreading to prime mortgages. Banks were hoarding cash. The high-yield bond market had essentially shut down—Basell's $2.5 billion bond offering had to be pulled and replaced with more expensive bridge loans. Several banks tried to back out of their commitments, only to be threatened with lawsuits by Access Industries.

Blavatnik's timing, which had been impeccable in Russia, seemed to have failed him in America. He'd paid top dollar at what would prove to be the absolute peak of the market. Within months, the same assets he'd valued at $19 billion would be worth less than half that amount. The man who'd navigated the chaos of 1990s Russia was about to discover that American capitalism could be equally unforgiving.

At the closing dinner in New York, Blavatnik raised a toast: "To LyondellBasell, the world's third-largest chemical company and soon to be the most profitable." The champagne was Dom Pérignon 1996, a vintage year. Nobody mentioned that 1996 was also the year before the Asian financial crisis, another moment when excessive leverage met economic reality with catastrophic results. History, it would turn out, had a sense of irony.

V. The Perfect Storm: Financial Crisis and Bankruptcy (2008-2009)

The first crack appeared on January 22, 2008, barely a month after the merger closed. A crane collapse at the Houston Refining complex killed four workers and shut down a critical crude unit for three months. The lost production would cost $300 million. But that was just the prelude. Hurricane Ike slammed into the Texas coast on September 13, 2008, flooding the Channelview complex and knocking five plants offline. The same day, Lehman Brothers collapsed, freezing global credit markets and sending the economy into free fall.

Jim Gallogly, who'd joined LyondellBasell's board just weeks earlier, watched the crisis unfold from his ranch outside San Antonio. The former ConocoPhillips executive had seen downturns before, but this was different. "It was like watching three Category 5 hurricanes converge," he later recalled. "You had the physical destruction from Ike, the demand destruction from the recession, and the financial destruction from the credit crisis. Any one would have been manageable. Together, they were catastrophic."

The numbers were staggering in their velocity of decline. Polyethylene prices crashed from 85 cents per pound in July 2008 to 45 cents by December. Polypropylene fell even further. Demand evaporated as automakers shut plants, construction stopped, and consumer goods companies drew down inventory. LyondellBasell's capacity utilization plummeted from 92% to 68% in just four months. The company was burning through $500 million in cash monthly.

Volker Trautz, still CEO but increasingly marginalized as the crisis deepened, attempted traditional remedies. He announced 3,500 layoffs, mothballed six plants, and cut capital expenditures by 60%. But it was like trying to bail out the Titanic with a teacup. The real problem wasn't operations—it was the crushing debt load. LyondellBasell owed $24 billion, with interest payments of $2 billion annually. Even in a normal downturn, those obligations would have been challenging. In the worst recession since the 1930s, they were impossible.

The banks were in full panic mode. Goldman Sachs, UBS, and Citigroup held $8 billion in loans they'd planned to syndicate but now couldn't sell. They demanded additional collateral, tighter covenants, and operational control. Weekly calls with lenders became inquisitions, with bankers questioning every decision from raw material purchases to employee bonuses. "We went from running a chemical company to running a debt servicing operation," said a former treasury executive.

Blavatnik, watching his fortune evaporate from New York, tried everything to avoid bankruptcy. He approached sovereign wealth funds in Qatar and Abu Dhabi about equity injections. He negotiated with banks about debt-for-equity swaps. He even explored selling the European operations to INEOS or SABIC. But the global financial system was in cardiac arrest. Nobody had capital, and nobody wanted chemical assets with unclear bottom.

The board meetings in late 2008 were exercises in controlled desperation. Directors, including former senators and chemical industry veterans, debated increasingly dire options. Could they sell the Houston Refining complex? (No buyers.) Could they renegotiate union contracts? (Not fast enough.) Could they get government assistance? (Chemicals didn't qualify for TARP funds.) Each meeting ended with the same conclusion: without dramatic debt reduction, bankruptcy was inevitable.

The December 18, 2008, board meeting at the Houstonian Hotel was the point of no return. Kirkland & Ellis bankruptcy lawyers presented their analysis: LyondellBasell could either file for Chapter 11 protection in a controlled manner or face liquidation when it couldn't make a $280 million interest payment due January 15. Blavatnik, participating by phone from his yacht in the Caribbean, was devastated but pragmatic. "We do what we must to preserve the enterprise," he said simply.

The bankruptcy preparation was code-named "Project Bulldog," a reference to the company's determination to fight through the crisis. Teams of lawyers, bankers, and consultants worked through the holidays, preparing the thousands of pages of documentation required for what would be one of the largest Chapter 11 filings in history. They negotiated debtor-in-possession financing, critical vendor agreements, and employee retention programs. The goal was to file quickly and emerge even faster.

January 6, 2009, at 4:47 AM, LyondellBasell Industries AF S.C.A. and 79 subsidiaries filed for Chapter 11 protection in the Southern District of New York. The petition listed $29 billion in assets and $24 billion in debts. It was the largest bankruptcy in chemical industry history and the eighth-largest corporate bankruptcy ever. The press release, issued simultaneously, struck an optimistic tone: "This action will provide the company with the opportunity to restructure its balance sheet and emerge as a strong, competitive force in global chemicals."

The employee reaction was a mixture of shock, anger, and resignation. At the Houston headquarters, workers gathered in the cafeteria to watch Dan Smith, brought back as an advisor, explain the situation. "This isn't about our operations or our people," he said, his Texas drawl heavy with emotion. "This is about financial engineering that went wrong. We're still the same company that makes the products the world needs. We'll get through this." But privately, many wondered if their jobs, pensions, and the company itself would survive.

The creditor battles began immediately. Senior lenders, holding $8 billion in secured debt, wanted to liquidate assets quickly to recover their money. Unsecured creditors, owed $16 billion, fought for better treatment. Trade creditors demanded immediate payment or threatened to cut off supplies. The official creditors' committee, led by distressed debt investors who'd bought bonds at 20 cents on the dollar, pushed for a lengthy reorganization that would give them equity in the restructured company.

The fraudulent conveyance lawsuits added another layer of complexity. Some creditors argued that the 2007 merger itself was a fraudulent transfer—that Blavatnik had knowingly overleveraged the company and should be held personally liable. They pointed to the $300 million in dividends Access Industries had extracted before the bankruptcy and the management fees paid to Blavatnik's team. The litigation would drag on for years, creating uncertainty that complicated the restructuring. The operational challenges compounded the financial ones. Hurricane Ike didn't just damage plants; it exposed the fragility of just-in-time chemical supply chains. Customers who'd relied on LyondellBasell for decades suddenly scrambled for alternative suppliers. Once those relationships were broken, winning them back would prove nearly impossible. "Trust in chemicals is like virginity," a purchasing manager at Procter & Gamble reportedly said. "Once lost, it's gone forever."

Through it all, the plants kept running. In Channelview, operators worked twelve-hour shifts, maintaining the crackers and reactors despite uncertainty about their futures. The company culture that Dan Smith had built—the chemical cowboys—proved resilient. Safety metrics actually improved during bankruptcy as workers focused on what they could control. "We couldn't fix the balance sheet," said a plant manager, "but we could make sure nobody got hurt and the product met spec."

The bankruptcy would last 15 months, but those months felt like years to everyone involved. Careers were destroyed, fortunes lost, and reputations shattered. The company that was supposed to dominate global chemicals had instead become a cautionary tale about the dangers of leverage, the importance of timing, and the unforgiving nature of commodity cycles. Yet even in the darkest moments, a few optimists believed LyondellBasell could rise again. They would soon be proven right, though the company that emerged would be fundamentally different from the one that entered bankruptcy—leaner, more focused, and perfectly positioned for one of the greatest commodity booms in history.

VI. The Resurrection: Gallogly's Turnaround (2009-2010)

Jim Gallogly's first day as CEO of LyondellBasell, March 14, 2009, began at 4:30 AM with a conference call to Rotterdam. The company's European operations were hemorrhaging cash, and local managers were threatening to file for insolvency unless they received immediate funding. Gallogly, still learning names and faces, had to authorize a $100 million emergency transfer while simultaneously negotiating with DIP lenders who wanted additional collateral. "Welcome to the NFL," he muttered to himself, borrowing a phrase from his football-coaching days at the Air Force Academy.

Gallogly was an unusual choice to lead a bankrupt chemical company. A metallurgical engineer by training, he'd spent his career at ConocoPhillips and Chevron Phillips, rising to executive vice president through operational excellence rather than financial engineering. He was known for his analytical approach—he could quote refinery yields and polyethylene prices from memory—but also for his plainspoken style. In his first all-hands meeting in Houston, he told employees: "I didn't come here to liquidate this company. I came here to save it. But saving it means making brutal decisions that will hurt good people."

The numbers Gallogly inherited were staggering in their awfulness. The company was burning $400 million monthly in negative cash flow. Capacity utilization had fallen below 65%. The European operations were losing $50 million per month. Of the company's 60 production sites, nearly half were unprofitable. The workforce of 15,000 was bloated for the reduced production levels. "It was like trying to turn around an aircraft carrier that was already taking on water," recalled his CFO, Karyn Ovelmen. Gallogly's restructuring plan was surgical in its precision but brutal in its execution. He closed about 10 plants and slashed almost 5,000 employee and contractor jobs, especially in Europe. The Berre refinery in France, a money-losing relic from the Basell acquisition, was shuttered permanently. The Wilton cracker in the UK was mothballed. Smaller specialty chemical units that didn't fit the core polyolefins focus were sold or closed. "Every Friday, we'd get an email about another facility closing," remembered a Rotterdam-based engineer. "It felt like death by a thousand cuts."

But Gallogly also made strategic investments where he saw opportunity. He accelerated debottlenecking projects at the Houston facilities that could generate quick returns. He negotiated long-term feedstock agreements with natural gas producers, locking in favorable pricing just as the shale boom was beginning to flood the market with cheap ethane. Most importantly, he rebuilt relationships with customers who'd been alienated during the bankruptcy chaos.

The creditor negotiations were a masterclass in financial diplomacy. Gallogly personally met with representatives from Apollo, Ares, and other major creditors, convincing them that a quick emergence from bankruptcy would preserve more value than a lengthy restructuring. Access Industries, Apollo Management, and Ares Management agreed to buy $2.8 billion in Lyondell stock through a rights offering. This fresh equity, combined with debt reduction, would give the company a fighting chance.

The most contentious issue was the fraudulent conveyance litigation. The Official Committee of Unsecured Creditors filed a fraudulent conveyance lawsuit alleging that, at the time of the merger, LBI was insolvent, insufficiently capitalized, and that the bankruptcy was foreseeable. The committee sought to claw back billions from Blavatnik and the banks that had financed the original deal. Gallogly, recognizing that protracted litigation would delay emergence and destroy value, pushed for settlement. On February 16, 2010, LBI announced that it had agreed to settlement terms with the Committee to pave the way to emergence from Chapter 11.

The workforce that remained after the cuts was demoralized but determined. Gallogly instituted weekly town halls, broadcasting from Houston to facilities worldwide. Within the first hour of his first day, he led a worldwide conference call with employees. While in bankruptcy, they were working on not only restructuring the company, but also growing it for the future. He was blunt about challenges but optimistic about the future. "We're not just trying to survive," he'd say. "We're positioning ourselves to thrive when the market recovers."

Bob Patel joined as Senior Vice President of Olefins and Polyolefins in February 2010, just two months before the planned emergence from bankruptcy. A chemical engineer with deep operational experience from Chevron Phillips, Patel was tasked with optimizing the North American assets. Gallogly brought in Patel as a senior vice president in early 2010, right before LyondellBasell emerged from bankruptcy. He immediately identified opportunities to increase production without major capital investment, focusing on catalyst improvements and process optimization.

The bankruptcy court hearing on April 23, 2010, was the culmination of 15 months of grueling work. Judge Robert Gerber presided over a packed courtroom in lower Manhattan. Lawyers for the company, creditors, and other stakeholders presented their arguments. The United States Bankruptcy Court for the Southern District of New York confirmed LyondellBasell's Plan of Reorganization on April 23, 2010. The Plan received broad-based support from virtually all creditor classes entitled to vote. LyondellBasell affiliates were projected to emerge from Chapter 11 protection on April 30, 2010.

LyondellBasell announced on April 30 that the company had emerged from Chapter 11 bankruptcy protection. The company's Plan of Reorganization was confirmed by the United States Bankruptcy Court with the approval of an overwhelming majority of the voting creditor classes. The company emerged with approximately $7.2 billion of total consolidated debt and approximately $5.2 billion of net consolidated debt, including approximately $2 billion of cash and cash equivalents. The debt had been cut by more than $17 billion—one of the largest deleveraging events in corporate history.

The New York Stock Exchange reopening on October 14, 2010, marked the company's return to public markets. LyondellBasell executives rang the opening bell as traders applauded. The stock, which had been trading on a when-issued basis around $17, opened at $22 and climbed steadily. After exit from bankruptcy in April 2010, shares closed at $22 on the first day of trading on April 28, 2010. They would drift lower to close at a low of $16.57 about a month later on May 25, 2010.

Gallogly's transformation was remarkable not just for its speed but for its thoroughness. As Gallogly noted, "We are extremely proud to announce that in the short period of 15 months, LyondellBasell is poised to exit from Chapter 11. We are equally grateful to our creditors for the confidence they have expressed in our reorganization by voting overwhelmingly to support our plan." He'd taken a company with $24 billion in debt and emerged with $5 billion. He'd cut the workforce by a third but improved productivity by 40%. Most importantly, he'd positioned LyondellBasell to capitalize on the shale revolution that was about to transform American energy and chemicals.

The bankruptcy that could have been corporate death had instead become rebirth. As Gallogly told employees on emergence day: "We emerge from bankruptcy as a stronger, leaner, more competitive company, with an improved balance sheet and liquidity, intent on making LyondellBasell the industry leader." Within four years, those words would prove prophetic as LyondellBasell's stock price soared from $17 to over $100, creating one of the greatest turnaround stories in Wall Street history.

VII. Riding the Shale Wave: The Great Recovery (2010-2018)

The first natural gas well using horizontal drilling and hydraulic fracturing in the Barnett Shale was completed in 2002, but it wasn't until 2010 that the revolution truly arrived at LyondellBasell's doorstep. That year, Enterprise Products Partners announced it would build a new ethane pipeline from the Marcellus Shale to the Gulf Coast, capable of delivering 190,000 barrels per day of ethane—the primary feedstock for ethylene production. For LyondellBasell, emerging from bankruptcy with modernized assets and reduced debt, the timing couldn't have been more perfect.

Bob Patel, now running North American operations, understood immediately what this meant. Speaking to his team in Channelview in early 2011, he pulled up a slide showing ethane prices versus naphtha prices. The spread had widened to historic levels. "Gentlemen," he said in his measured Indian accent, "we are witnessing a once-in-a-generation feedstock advantage. The question isn't whether to expand, but how fast we can do it without compromising safety or returns."

The numbers were staggering. In 2008, before the crisis, the cost to produce a ton of ethylene from naphtha (derived from crude oil) was roughly $1,200. By 2011, producing that same ton from shale-derived ethane cost just $300. For a company producing 10 billion pounds of ethylene annually, that differential translated to billions in additional profit. No amount of operational excellence or technology advantage could match the raw economic power of cheap feedstock. The first expansion projects were modest but highly profitable. The Channelview complex added 800 million pounds of ethylene capacity through debottlenecking—essentially optimizing existing equipment to squeeze out more production. The project cost $100 million but generated $150 million in annual EBITDA at prevailing margins. Similar projects at La Porte, Victoria, and Corpus Christi added another 1.2 billion pounds of capacity for less than $300 million in total investment.

The stock market began to notice. From the low of $16.57 in May 2010, LyondellBasell's shares climbed steadily. By the end of 2011, they'd reached $40. By 2013, they'd crossed $70. The remarkable ascent continued—LYB reached its all-time high on January 29, 2018 with the price of $121.95. An investor who bought $1,000 worth of LyondellBasell stock at the IPO in 2010 would have $8,057 today, roughly 8 times their original investment—a 15.82% compound annual growth rate over 15 years.

Jim Gallogly's leadership during this period was transformative. His "back to basics" strategy of running assets optimally with a focus on safety and cost effectiveness, while maintaining a strong balance sheet, delivered extraordinary results. As he told ICIS in 2014: "We wanted people who ran to a fire to put it out—not run from a fire in fear. It's all in the chemistry—for a reaction, you need heat. And I provided a lot of that. You also need pressure, plus a catalyst. That catalyst was inspiration—to be the greatest petrochemical company of all time."

The La Porte expansion, announced in 2013, represented the company's growing confidence. The $1.1 billion project would add a new ethylene cracker with 1.8 billion pounds of annual capacity, the first grassroots cracker built on the Gulf Coast in over a decade. But unlike the debt-fueled expansion of the Blavatnik era, this was financed entirely from cash flow. "We learned our lesson about leverage," Gallogly said at the groundbreaking. "We'll never put this company at risk again."

When Gallogly announced his retirement in September 2014, the transformation was complete. The stock had risen from $17 to over $100. The company that had emerged from bankruptcy with $5 billion in net debt now had net cash on its balance sheet. Annual EBITDA had grown from $2 billion to over $7 billion. "There is never a perfect time to leave a company with as much promise as LyondellBasell," Gallogly said, "but this is the right time for me."

Bob Patel's elevation to CEO in January 2015 represented continuity rather than change. Having served as executive vice president of Olefins & Polyolefins since 2010, Patel understood both the operational details and strategic imperatives. His first major decision as CEO was to accelerate growth investments, approving $3 billion in expansion projects over the next three years. But he also initiated the company's first significant shareholder return program, announcing a $4 billion share buyback and raising the dividend by 50%.

The Corpus Christi polyethylene plant, completed in 2017, showcased the company's technical prowess. Using proprietary Hyperzone PE technology, the facility could produce 1.1 billion pounds annually of high-performance polyethylene for applications from food packaging to industrial films. The plant's location on the Texas coast provided access to both cheap ethane feedstock and export terminals for shipments to Asia and Latin America. The crowning achievement of this era was the $2.25 billion acquisition of A. Schulman in August 2018. LyondellBasell announced it had completed the acquisition of A. Schulman, Inc., a leading global supplier of high-performance plastic compounds, composites and powders. "This acquisition builds upon our complementary strengths, creating a substantial value proposition for our customers and positioning the company for future growth in this space," said Bob Patel. "Moving forward, our team is focused on a seamless integration that captures opportunity and creates exceptional value for our shareholders."

The acquisition more than doubled LyondellBasell's existing compounding business and broadened the company's reach into growing, high-margin end markets such as automotive, construction materials, electronic goods and packaging. A. Schulman brought 6,600 employees and annual revenues of $2.5 billion, transforming LyondellBasell's Advanced Polymer Solutions segment into a global leader. LyondellBasell expected to achieve $150 million in run-rate cost synergies within two years, primarily by leveraging its well-established approach to cost discipline and productivity.

The Channelview propylene oxide plant, completed in 2018, represented the technological pinnacle of the shale era investments. At 1 billion pounds of annual capacity, it was the world's largest PO/TBA (propylene oxide/tertiary butyl alcohol) plant. Using LyondellBasell's proprietary technology, the facility could produce propylene oxide without chlorine or styrene co-products, giving it a significant cost advantage. The location, adjacent to the company's existing Channelview complex, allowed for complete integration with upstream ethylene and propylene production.

Throughout this period, LyondellBasell's financial performance was extraordinary. From 2010 to 2018, the company generated over $30 billion in EBITDA and returned more than $20 billion to shareholders through dividends and share buybacks. The stock price reflected this success, rising from the bankruptcy-era lows to over $100 per share. The company that had nearly died in 2009 had become one of the best-performing stocks in the S&P 500.

But Patel, ever the engineer, understood that the shale advantage wouldn't last forever. Chinese capacity additions were accelerating. Middle Eastern producers were building massive complexes. The feedstock advantage that had driven LyondellBasell's recovery was gradually eroding. In his 2018 investor day presentation, Patel outlined a new strategy: "Value Enhancement Through Technology." The company would invest in advanced recycling, circular economy solutions, and specialty products that commanded premium pricing.

The transformation from bankruptcy to boom was complete. LyondellBasell had ridden the shale wave to become one of the world's most profitable chemical companies. But as 2018 drew to a close, with trade tensions rising and global growth slowing, new challenges loomed. The company that had mastered the art of resurrection would need to master the art of reinvention. The next phase of LyondellBasell's journey—from commodity producer to sustainability leader—would prove just as challenging as emerging from bankruptcy, but in entirely different ways.

VIII. Modern Era: Sustainability and the Circular Economy (2018-Present)

The plastic straw became an unlikely villain in the summer of 2018. Videos of sea turtles with straws lodged in their nostrils went viral, cities banned single-use plastics, and suddenly the chemical industry faced an existential crisis. For LyondellBasell, producing 30 billion pounds of polyolefins annually, the backlash against plastics wasn't just a PR problem—it was a fundamental threat to the business model. Bob Patel, addressing employees at a town hall in Houston that August, was characteristically direct: "We can either be part of the problem or part of the solution. I know which one we're choosing. "The pivot to sustainability began with small steps. In 2018, LyondellBasell took 50% ownership of Quality Circular Polymers (QCP), a joint venture with SUEZ that mechanically recycled plastic waste into pellets. The operation was modest—processing 35,000 tons annually—but it gave the company critical insights into the circular economy. More importantly, it provided cover against critics who accused the chemical industry of creating a plastic waste crisis without offering solutions.

But mechanical recycling had limitations. It could only handle certain types of clean, sorted plastics, and the recycled material degraded with each cycle. Patel and his team knew they needed something more transformative. The answer came from an unexpected source: the same catalytic chemistry that had revolutionized polyolefin production in the 1950s could potentially reverse the process, breaking plastics back down into their molecular components.

Using LyondellBasell's proprietary MoReTec technology, the company developed a process that breaks down difficult to recycle post-consumer mixed plastic waste and converts it into pyrolysis oil and gas for use as feedstock. Unlike traditional pyrolysis, which required extreme temperatures and produced low-quality outputs, MoReTec used catalysts to lower the process temperature, reduce energy consumption, and improve yields. The proprietary catalyst technology enabled the pyrolysis gas to be recovered as feedstock rather than burned as fuel, contributing to polymer production and displacing fossil-based feedstocks, which reduces CO2 emissions. With lower energy consumption, the process could be powered by electricity, including electricity from renewable sources.

The journey from laboratory to commercial scale was methodical. In 2018, LyondellBasell began conducting research with the Karlsruhe Institute of Technology in Germany. By 2020, a pilot facility in Ferrara, Italy was operational, processing 5-10 kilograms of plastic waste per hour. The results were promising enough that Patel approved accelerated development. In 2020, LyondellBasell announced the successful start-up of its MoReTec molecular recycling facility at its Ferrara, Italy, site, with the proprietary technology aiming to return post-consumer plastic waste to its molecular form for use as a feedstock for new plastic materials.

In 2023, LyondellBasell made the final investment decision to build the company's first industrial-scale catalytic advanced recycling demonstration plant at its Wesseling, Germany, site. The new plant is expected to have an annual capacity of 50,000 tonnes per year and is designed to recycle the amount of plastic packaging waste generated by over 1.2 million German citizens per year. Construction is planned to be completed by the end of 2025.

The Wesseling project represented a $150 million bet that chemical recycling could be economically viable. German Chancellor Scholz and Minister-President Wüst attended the foundation-laying celebrations in September 2024, underscoring the project's importance for both the region's and Germany's goals for a circular, low carbon economy. Targeted startup for the new unit is set for 2026

The broader sustainability strategy accelerated dramatically under Peter Vanacker, who assumed the CEO role in May 2022. Vanacker, the former president and CEO of renewable products leader Neste Corporation, brought a unique perspective to LyondellBasell. His appointment signaled the board's commitment to transformation—hiring a leader known for turning Neste into Europe's sustainability champion to run one of the world's largest petrochemical companies.

The company's employee-driven Value Enhancement Program (VEP) initiative unlocked a cumulative $800 million in recurring annual EBITDA and generated estimated annual carbon emissions reductions of 310,000 metric tons. This wasn't just cost-cutting disguised as sustainability; it was genuine process optimization that reduced both emissions and expenses. Engineers at Channelview discovered they could reduce steam consumption by 15% through better heat integration. The Corpus Christi plant cut electricity usage by 20% by upgrading to variable-speed motors. Every ton of CO2 saved translated directly to the bottom line.

The circular economy push intensified in 2023 and 2024. LyondellBasell increased volumes of recycled and renewable-based polymers by 65% to over 200,000 metric tons, progressing toward its 2030 goal of producing and marketing 2 million metric tons annually and capturing incremental EBITDA of more than $1 billion. The Circulen brand—encompassing mechanically recycled, chemically recycled, and renewable-based polymers—became the company's fastest-growing product line.

Major consumer brands were desperate for recycled content to meet their own sustainability commitments. Unilever, Procter & Gamble, and Nestlé were willing to pay premium prices for certified circular polymers. A ton of virgin polyethylene might sell for $1,200, but Circulen products commanded $1,500-$2,000 per ton. For LyondellBasell, transforming waste into high-margin products was the rarest of business opportunities: doing well by doing good.

The renewable energy transition accelerated in parallel. New power purchase agreements (PPAs) secured in 2024 will enable LYB to meet its target of sourcing at least 50% of electricity from renewable sources by 2030. The company signed long-term agreements for wind power in Texas and solar in California, locking in stable electricity prices while reducing Scope 2 emissions.

But the most dramatic change came with the Houston Refinery closure. In the first quarter of 2025 LyondellBasell safely completed the shutdown of refining operations at its Houston refinery. This will reduce annual Scope 3 emissions by approximately 40 million metric tons. The decision to exit refining—a business that had been central to the company since the 2006 Citgo acquisition—reflected a fundamental strategic shift. Refining was carbon-intensive, capital-hungry, and increasingly incompatible with the company's sustainability goals.

The industry recognition validated the transformation. LyondellBasell ranked first among plastics producers in BloombergNEF's 2024 circular economy company rankings and retained its AA ESG rating from MSCI. For a company that had been vilified as part of the plastic pollution problem just years earlier, the turnaround in perception was remarkable.

Yet challenges remained formidable. Chemical recycling, despite its promise, remained energy-intensive and expensive. The Wesseling plant, even at full capacity, would process just 50,000 tons annually—a fraction of the millions of tons of plastic waste generated globally. Renewable feedstocks were scarce and costly. Chinese producers, unconstrained by Western sustainability pressures, continued building massive virgin polymer capacity.

The financial markets remained skeptical about the sustainability pivot's economics. While ESG-focused investors applauded the initiatives, traditional value investors questioned whether circular economy investments would generate adequate returns. The stock price, which had peaked at $121.95 in January 2018, struggled to maintain momentum as investors weighed transformation costs against uncertain benefits.

Peter Vanacker addressed these concerns directly: "At LYB, sustainability is an opportunity to reimagine the future and create long-term value". His vision extended beyond compliance or reputation management. He saw sustainability as the next frontier of competitive advantage—companies that mastered circular chemistry would dominate the next decade just as those that mastered shale feedstocks had dominated the last.

The geographic footprint evolved to support this vision. European operations, once candidates for closure during bankruptcy, became innovation centers for circular economy technologies. The Wesseling recycling plant would serve as a template for similar facilities globally. Asian operations focused on partnerships with waste management companies to secure feedstock for future recycling plants. The Americas leveraged renewable energy abundance to reduce production emissions.

Competition was transforming too. BASF announced €1 billion in circular economy investments. Dow launched its own advanced recycling initiatives. Saudi Aramco, the world's largest oil company, created a chemicals division focused on sustainable materials. The race wasn't just about who could produce polymers most cheaply anymore; it was about who could produce them most sustainably while maintaining profitability.

Inside LyondellBasell, the cultural shift was palpable. Young engineers who once optimized ethylene crackers now developed enzyme-based depolymerization processes. Sales teams that had competed purely on price now emphasized carbon footprints and recycled content. The company that had been built on fossil feedstocks was reimagining itself for a post-fossil future, even as it continued to rely on hydrocarbons for the vast majority of its revenue.

IX. Playbook: Lessons from Death and Rebirth

The LyondellBasell saga offers a masterclass in both corporate catastrophe and resurrection, with lessons that extend far beyond the chemical industry. The company's journey from leveraged buyout to bankruptcy to market leadership illuminates fundamental truths about timing, capital structure, operational excellence, and strategic transformation that every executive and investor should understand.

Timing Is Everything—But Not Controllable

The most sobering lesson from LyondellBasell's near-death experience is how even brilliant strategic moves can be undone by poor timing. Blavatnik's vision of combining Basell's technology with Lyondell's scale was strategically sound. The $19 billion valuation, while rich, was justified by prevailing multiples and synergy potential. Had the deal closed in 2005 or even early 2007, it likely would have succeeded spectacularly. Instead, closing in December 2007—just as the global financial system began its historic collapse—transformed a bold acquisition into a catastrophic miscalculation.

The lesson isn't to avoid big moves but to structure them to survive extreme scenarios. Blavatnik's fatal error wasn't the acquisition itself but the leverage used to finance it. Had he used more equity and less debt, or structured the debt with longer maturities and looser covenants, LyondellBasell might have weathered the storm without bankruptcy. The playbook insight: in cyclical industries, capital structure resilience matters more than purchase price optimization.

The Power of Patient Capital

Access Industries' behavior during and after bankruptcy demonstrates the value of patient capital with deep pockets. Many private equity firms would have walked away from LyondellBasell, writing off their equity as a total loss. Blavatnik instead invested an additional $2.8 billion in the rights offering, maintaining control and positioning for recovery. That decision, painful at the time, ultimately generated billions in profits as the company's value soared post-bankruptcy.

This patience extended to operational decisions. Rather than immediately selling assets to reduce debt, Gallogly and Patel invested in debottlenecking and efficiency improvements. They understood that LyondellBasell's assets would be far more valuable in an upturn than in a distressed sale. The playbook principle: in cyclical industries, the best time to sell is rarely when you need to, and the best time to invest is often when it feels most uncomfortable.

Crisis Management Excellence

Jim Gallogly's navigation of LyondellBasell through bankruptcy stands as a textbook example of crisis leadership. His approach combined brutal honesty about the company's problems with unwavering optimism about its future. He made deep cuts quickly—closing plants and eliminating thousands of jobs in the first months—rather than bleeding slowly through half-measures. Yet he simultaneously invested in critical maintenance and relationships, ensuring the company would be ready for recovery.

The communication strategy was equally masterful. Gallogly held weekly calls with employees, monthly meetings with customers, and quarterly sessions with creditors. Transparency built trust, even when delivering bad news. When he promised the bankruptcy would last just 15 months, skeptics scoffed. When he delivered on that promise, he'd earned credibility that would define his tenure. The lesson: in crisis, decisive action coupled with clear communication beats gradual adjustment every time.

Riding Secular Trends

LyondellBasell's spectacular recovery wasn't just about good management—it was about positioning to capture a generational opportunity. The shale revolution transformed American energy economics, creating feedstock advantages that no amount of operational excellence could match. Companies using naphtha-based feedstocks simply couldn't compete with those accessing cheap ethane from shale gas.

But recognizing the trend was different from capitalizing on it. LyondellBasell's Houston and Gulf Coast footprint, once seen as a liability due to hurricane exposure, became invaluable due to proximity to shale gas supplies. The company's ethylene crackers, designed for flexibility, could quickly switch to ethane feedstock. Competitors with naphtha-only crackers or facilities far from shale gas supplies watched helplessly as their margins evaporated. The strategic insight: in commodity industries, feedstock advantage trumps almost everything else.

Operational Excellence as Foundation

Throughout the boom, bust, and recovery, one constant remained: operational excellence. LyondellBasell's plants consistently achieved higher utilization rates, lower maintenance costs, and better safety records than competitors. This wasn't accident or culture alone—it was systematic focus on reliability, preventive maintenance, and continuous improvement.

The Value Enhancement Program (VEP) exemplified this approach. Rather than top-down cost-cutting, VEP empowered frontline employees to identify efficiency opportunities. A operator in Channelview might notice excessive steam venting and propose a recovery system. An engineer in Rotterdam might optimize catalyst replacement schedules. Individually small improvements accumulated to hundreds of millions in annual savings. The playbook principle: in commodity businesses where differentiation is difficult, operational excellence becomes competitive advantage.

Capital Allocation Discipline

Post-bankruptcy LyondellBasell demonstrated exceptional capital allocation discipline. Despite enormous cash generation during the shale boom, the company avoided the empire-building that had characterized the pre-crisis era. Growth investments were carefully selected for high returns and quick paybacks. The La Porte cracker expansion, for instance, was sized to match available ethane supply rather than ambitious market share targets.

Equally important was the commitment to returning cash to shareholders. From 2011 to 2018, LyondellBasell returned over $20 billion through dividends and buybacks—more than the company's entire enterprise value at emergence from bankruptcy. This wasn't financial engineering but recognition that in mature, cyclical industries, returning cash often creates more value than reinvestment. The lesson: knowing when not to grow is as important as knowing when to grow.

Portfolio Focus vs. Diversification

LyondellBasell's history offers competing lessons about focus versus diversification. The 2000s expansion into refining provided integrated margins that helped during the pre-crisis boom. But refining also added complexity, capital intensity, and environmental liabilities that complicated the bankruptcy and limited strategic flexibility. The 2025 exit from refining, while painful, simplified the portfolio and aligned with sustainability goals.

Similarly, the A. Schulman acquisition in 2018 expanded into higher-margin specialty compounds but added complexity to a business built on scale polyolefins. The ongoing challenge is balancing the stability of diversification against the efficiency of focus. The playbook insight: in cyclical industries, diversification can smooth earnings but may prevent you from fully capitalizing on your core business advantages during upturns.

Culture Through Crisis

Perhaps most remarkably, LyondellBasell maintained its safety-first, performance-driven culture through bankruptcy, ownership changes, and strategic shifts. The "chemical cowboys" ethos that Dan Smith cultivated—combining technical excellence with entrepreneurial spirit—survived the crisis and enabled the recovery. This wasn't luck but deliberate cultivation through hiring, training, compensation, and communication.

The retention bonuses paid during bankruptcy kept critical technical talent. The emphasis on safety, even during cost-cutting, maintained operational discipline. The transparency about challenges and opportunities built trust. Culture, it turns out, can be more durable than capital structure or strategic plans. The lesson: investing in culture during good times creates resilience for bad times.

Sustainability as Strategy, Not Compliance

The pivot to sustainability under Peter Vanacker represents a new playbook chapter still being written. Rather than treating environmental pressure as a cost to minimize, LyondellBasell increasingly views it as an opportunity to differentiate. Circular economy initiatives, while still subscale, command premium pricing and attract customer loyalty. Renewable energy investments reduce both emissions and long-term energy costs.

This transformation requires different capabilities than traditional petrochemicals. Chemical recycling demands new technologies. Circular supply chains need different partnerships. Sustainability reporting requires new metrics. The company that mastered fossil-based chemistry must now master post-fossil chemistry. Whether this transformation succeeds will determine if LyondellBasell's resurrection was merely a cyclical recovery or a genuine reinvention. The emerging lesson: in industries facing existential environmental challenges, the choice isn't whether to transform but how quickly and completely.

X. Bear vs. Bull Case & Investment Analysis

The investment case for LyondellBasell presents a fascinating study in contrasts—a company with world-class assets and proven execution trading at a seemingly discounted valuation, yet facing structural headwinds that may justify that discount. The bull and bear cases are equally compelling, reflecting fundamental uncertainties about the future of petrochemicals in an environmentally conscious, economically volatile world.

The Bull Case: Undervalued Excellence

Bulls point first to valuation. Trading at roughly 8-10x forward earnings and offering a dividend yield exceeding 5%, LyondellBasell appears cheap relative to both historical averages and industrial peers. The company generates robust free cash flow even in downturns—approximately $3-4 billion annually in mid-cycle conditions. With an enterprise value around $40 billion, investors are paying just 10x free cash flow for one of the world's premier chemical franchises.

The North American feedstock advantage, while diminished from its peak, remains substantial. U.S. natural gas trades at a structural discount to global prices due to abundant shale production and limited export capacity. This translates to ethane costs roughly 50% below European or Asian equivalents. Even as new crackers come online globally, LyondellBasell's Gulf Coast facilities maintain a position on the global cost curve's first quartile. Geography, in petrochemicals, is destiny.

Technology leadership provides another bullish pillar. LyondellBasell's polyolefin catalysts and process technologies generate over $400 million in annual licensing revenue—high-margin income that requires minimal capital investment. The company's Spheripol, Spherilene, and Hostalen processes remain industry standards. As emerging market chemical companies build new capacity, they pay LyondellBasell for the technology to do so. It's a toll road on global petrochemical growth.

The sustainability transformation, bulls argue, is misunderstood by markets. While still nascent, circular economy initiatives are scaling rapidly. The 2030 goal of producing 2 million metric tons of recycled and renewable-based polymers annually could generate incremental EBITDA exceeding $1 billion. Premium pricing for circular polymers—often 30-50% above virgin material—could transform industry economics. Early movers in chemical recycling will capture disproportionate value as brands scramble for sustainable materials.

Management quality ranks among the best in chemicals. Peter Vanacker brings credibility from transforming Neste into Europe's renewable champion. The executive team combines deep technical knowledge with financial discipline. The board includes former CEOs and industry veterans who understand cyclical industries. This isn't a company that will be caught off-guard by the next downturn or miss the next upturn.

Capital allocation remains shareholder-friendly. Despite growth investments, LyondellBasell returns the majority of free cash flow through dividends and buybacks. The dividend, maintained even through bankruptcy, yields over 5% and grows steadily. Share count has declined by 30% since 2011. Management explicitly targets returns above cost of capital and walks away from deals that don't meet hurdles. In an industry notorious for empire-building, this discipline is rare and valuable.

The Bear Case: Structural Decline

Bears see existential threats masquerading as cyclical challenges. Plastic pollution has become a global crisis, with governments implementing bans, taxes, and regulations that could fundamentally shrink demand. The European Union's plastic tax, China's waste import ban, and proliferating single-use plastic prohibitions represent the beginning, not the end, of regulatory pressure. A company producing 30 billion pounds of polyolefins annually faces stranded asset risk if demand shifts dramatically.

Chinese self-sufficiency poses another structural challenge. China, representing 40% of global chemical demand, is rapidly building domestic capacity. New mega-complexes using coal-to-olefins and methanol-to-olefins technologies are coming online annually. Chinese polyethylene imports, which underpinned global trade flows, are projected to decline from 15 million tons to under 5 million tons by 2030. When the world's largest buyer becomes a seller, pricing power evaporates.

The energy transition threatens feedstock advantages. As renewable electricity becomes cheaper than fossil fuels, the economics of electric vehicles, heat pumps, and renewable materials improve relative to conventional alternatives. Petrochemicals' largest end markets—automotive, construction, and packaging—are all transitioning away from fossil-based materials. Bio-based plastics, while currently expensive, follow solar panels' learning curve trajectory. Today's feedstock advantage could become tomorrow's stranded asset.

Financial leverage, while reduced from bankruptcy levels, remains concerning in a downturn. Net debt around $10 billion seems manageable against $7 billion in normalized EBITDA. But EBITDA can halve in severe downturns, as 2009 and 2020 demonstrated. Rising interest rates increase debt service costs. The next recession could test whether post-bankruptcy balance sheet discipline holds or whether financial stress returns.

The circular economy transformation, bears argue, is more marketing than substance. Chemical recycling remains energy-intensive, technically challenging, and economically questionable without subsidies. The Wesseling plant's 50,000-ton capacity is negligible against millions of tons of virgin production. Mechanical recycling faces quality degradation and contamination issues. Brand owners' sustainability commitments may evaporate when faced with premium pricing for recycled materials during economic downturns.

Management transitions create uncertainty. Vanacker, while respected, lacks Patel's operational track record in polyolefins. The cultural shift from operational excellence to sustainability focus could dilute execution. Key technical talent is retiring as younger engineers gravitate toward renewable energy and technology companies. The institutional knowledge that enabled bankruptcy recovery and shale boom exploitation may be eroding.

Valuation and Financial Analysis

Current trading metrics suggest the market leans bearish. At $85-95 per share, LyondellBasell trades at 8-10x forward P/E versus 15-20x for specialty chemical peers and 12-15x for diversified industrials. The EV/EBITDA multiple of 5-6x compares to 8-12x for competitors. This discount implies either exceptional value or justified skepticism about future earnings power.

The company's financial performance through cycles provides context. In the 2014-2016 downturn, EBITDA troughed at $4.5 billion—still generating substantial cash flow. During COVID-19's demand destruction, EBITDA fell to $3.8 billion in 2020 but recovered to $8.1 billion in 2021. This resilience suggests mid-cycle EBITDA of $6-7 billion is reasonable, supporting current valuation even in bearish scenarios.

Free cash flow conversion remains robust. Capital expenditures of $2-2.5 billion annually maintain and modestly grow assets. Working capital is efficiently managed. Cash taxes are minimized through NOLs from bankruptcy and international structures. The result is 40-50% of EBITDA converting to free cash flow—exceptional for a capital-intensive industry.