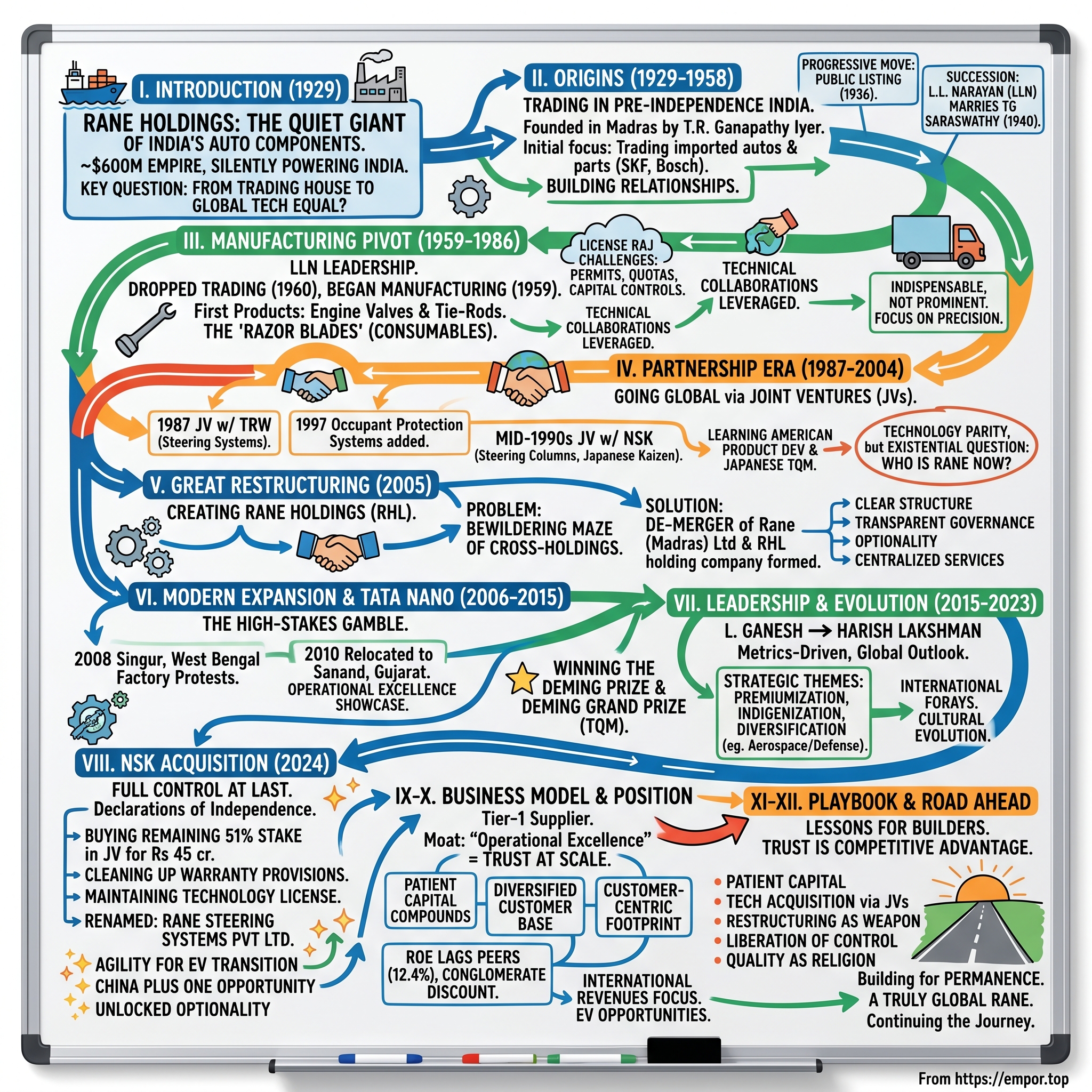

Rane Holdings: The Quiet Giant of India's Auto Component Revolution

I. Introduction & Setting the Stage

The morning mist clings to Marina Beach in Chennai as the first shift workers stream through the gates of a nondescript factory compound on Velachery Road. Most passersby wouldn't give it a second glance—just another industrial facility in India's Detroit. Yet behind these weathered walls beats the heart of a $600 million empire that has quietly powered India's automotive revolution for nearly a century.

Rane Holdings commands sales of ₹52.36 billion (US$620 million), making it one of India's largest auto component conglomerates. According to The Automotive Horizon, the company has "dominat[ed] the domestic [Indian] auto component space" for "decades". But mention Rane to the average investor—even sophisticated ones—and you'll likely get blank stares.

This anonymity is deliberate, almost philosophical. While flashier rivals court headlines, Rane has methodically built an empire spanning ten different companies, manufacturing everything from steering systems that guide millions of vehicles daily to the friction materials that bring them safely to a stop. Their components hide in plain sight—in the Tata Nano that promised to motorize middle India, in the Ashok Leyland trucks that form the backbone of Indian logistics, in the Mahindra tractors that feed a nation.

The central question of our story isn't just how a company founded in 1929 in Madras by T.R. Ganapathy Iyer became India's steering systems powerhouse—it's how a trading house born in colonial India transformed itself into a technological equal of global giants, and why, after 27 years of successful partnership, it's now taking full control of its destiny.

This is a story of three transformations: from trader to manufacturer, from imitator to innovator, from junior partner to sovereign. It's about navigating the treacherous waters of the License Raj, surviving liberalization's creative destruction, and thriving in the age of globalization. Above all, it's about the peculiar genius required to build an industrial champion in a developing economy—patient capital, technological pragmatism, and an almost zen-like acceptance of playing the long game.

II. Origins: Trading in Pre-Independence India (1929-1958)

Picture Madras in 1929: George V's portrait hangs in government offices, the Bengal famine is still a year away, and Gandhi's salt march hasn't yet captured the world's imagination. The city's Mount Road thrums with imported Morris Oxfords and Austin Sevens—symbols of colonial prosperity accessible only to the British and a thin slice of Indian elite. Into this world steps T.R. Ganapathy Iyer, a man whose vision would outlive the Raj itself.

In 1928, the firm decided to expand its operations to Madras city. Ganapathy Iyer was the man chosen for the job. He wasn't starting from scratch—he'd already proven himself in Bombay's competitive auto trade. But Madras represented something different: a chance to build his own empire in South India's commercial capital.

The timing seemed almost perverse. The world was reeling under the impact of the Great Depression. The Government of India had a largely unhelpful policy when it came to business. But Ganapathy Iyer went ahead. This wasn't optimism—it was calculated defiance. While others retreated, he saw opportunity in crisis.

The first meeting of Rane, Madras (Ltd) took place on 21st March 1930 and among those present were Ganapathy Iyer and his wife Meenakshi. He and his wife had the first and second allotment of shares in their name, followed by the third lot in the name of their daughter, TG Saraswathy. This family shareholding pattern—seemingly mundane—would prove crucial decades later when succession questions arose.

By 1936, the company underwent restructuring and public listing, a remarkably progressive move for an Indian business of that era. The board composition reflected Iyer's strategic thinking—mixing family with professionals, locals with cosmopolitans. The directors included Jamnadas Mehta (a businessman and Congress activist who was designated Chairman) and Dr TM Kajiji (a well-known figure and a close associate of Jamnadas Mehta).

What Rane actually did in these early years was deceptively simple yet strategically profound. Initially, the company, then known as Rane (Madras) Ltd., focused on trading automobiles and automotive parts. But this wasn't mere arbitrage. Iyer was building something far more valuable: relationships. Every imported SKF bearing, every Bosch magneto, every Lucas headlamp that passed through Rane's books created a connection—with suppliers who would later become technology partners, with customers who would become India's first generation of automotive manufacturers, with mechanics who formed the backbone of India's emerging automotive service industry.

The entrepreneurial side of Iyer emerged in unexpected ways. In 1939, Iyer suggested that Rane enter into the life insurance business, a sector that was then booming in India despite the threat of war. The auditors to the company objected... Undaunted, Iyer went ahead on his own and collaborated with HD Raja in founding Vanguard, a Madras-based insurance company. He became a director on the Board of the firm and its allied companies... He was also one of the promoters of the Madras Finance Corporation Ltd which was into leasing and financing of the purchase of vehicles. He was also the founder of Chandra Ltd... and Nalin Publicity Bureau which probably handled the advertisements released by Rane.

This diversification revealed Iyer's understanding of ecosystem building. Financing vehicles, insuring them, advertising them—he wasn't just selling auto parts; he was nurturing an entire automotive economy in South India.

But it was Iyer's succession planning that proved most visionary. LL NARAYAN, THE MAN whose shoulders were to bear the burden of managing the companies and the family of TR Ganapathy Iyer had joined the Group in 1940 or so... A Botany graduate, he was the son of a Medical Officer in Cochin State. Having joined the company, LLN sufficiently impressed Ganapathy Iyer for the latter to consider him son-in-law material. LLN married TG Saraswathy, Ganapathy Iyer's eldest daughter.

This wasn't nepotism—it was strategic succession. After his death, the business was taken over by his son-in-law Lakshmana Iyer Lakshminarayan, popularly known as LLN, among friends and business circles. Under the leadership of LLN, the company was shaped into an auto-component business house. LLN remained as the founder chairman of the group for over three decades.

The transformation from Iyer to LLN marked more than leadership change—it signaled a fundamental strategic pivot that would define Rane's next chapter.

III. The Manufacturing Pivot: From Trading to Building (1959-1986)

The year 1959 doesn't appear in most Indian business history books. While Nehru's temples of modern India—steel plants and dams—captured headlines, a quieter revolution was brewing in a modest facility in Alandur, Chennai. Manufacturing operations commenced at Alandur with engine valves and tie-rods. For Rane, this wasn't just adding a factory—it was crossing the Rubicon from merchant to maker.

LLN understood what many Indian businessmen of his generation didn't: trading had a ceiling, but manufacturing had none. During the early periods Rane Madras Ltd was engaged in trading only. Later in the year 1960, they completely dropped trading and started manufacturing and it all started with the manufacture of Tie Rod ends at their plant in Velachery, Chennai. The decision to abandon trading entirely—not hedge, not diversify, but completely pivot—required extraordinary conviction.

The product choice was telling. Engine valves and tie-rod ends weren't glamorous, but they were essential. Every internal combustion engine needed valves—dozens of them. Every vehicle with wheels needed steering linkages. These were consumables, wearing out predictably, demanding replacement regularly. LLN had found Rane's razor blades.

But making these components in 1960s India was like performing surgery with kitchen knives. The License Raj—that suffocating web of permits, quotas, and bureaucratic controls—made importing even basic machine tools an odyssey. Want a German lathe? Get in line for an import license. Need specialty steel? Apply for a raw material quota. Planning to expand capacity? Seek government permission, wait years.

This is where Rane's relationships, cultivated over three decades of trading, paid dividends. When the government restricted imports to conserve foreign exchange, Rane could leverage its supplier relationships to access technology through other means. Technical collaboration agreements became the loophole—bring in the knowledge, not the machines.

Rane Group history began its manufacturing journey in 1959, initially producing engine valves and tie-rods. By early 1961, the company had established a robust distribution network across India. This distribution network—inherited from the trading days—gave Rane an enormous advantage. While competitors struggled to reach customers, Rane's components flowed through channels built over 30 years.

The manufacturing expansion followed a pattern that would become Rane's signature: start with one product, master it, then expand adjacently. As the automobile industry flourished, the business spread to the manufacturing of other suspension and steering systems. Steering linkages led to steering gears. Engine valves led to valve guides and tappets. Each new product leveraged existing capabilities while adding new ones.

By the mid-1970s, Rane had become something unique in Indian manufacturing: a company that could claim genuine technical competence in precision engineering. The numbers tell part of the story, but the real achievement was institutional. Rane had created a culture of quality in an ecosystem that often rewarded mere adequacy.

The ecosystem itself was evolving. Maruti's entry in the early 1980s would revolutionize Indian automotive manufacturing, but before Maruti, there was the commercial vehicle boom. Ashok Leyland, TELCO (later Tata Motors), Mahindra—these companies were mechanizing Indian agriculture and logistics. Each needed reliable, locally-made components. Rane was perfectly positioned.

Yet the most important development of this era wasn't a product or a customer—it was a mindset. Rane had discovered its core philosophy: be indispensable, not prominent. Let others chase glory; Rane would chase precision. This philosophy would guide every decision in the decades ahead, from choosing joint venture partners to structuring complex corporate reorganizations.

IV. The Partnership Era: Going Global Through JVs (1987-2004)

The Berlin Wall still stood when Rane made a decision that would define its next three decades. In 1987, while India remained largely closed to the world, the JV was founded by Rane and TRW to produce steering systems for commercial vehicles. This wasn't just a business deal—it was a bet on India's eventual integration with the global economy, placed four years before liberalization.

The TRW partnership represented a new model for Indian manufacturing. Unlike the technical collaboration agreements of the License Raj era—essentially technology rental schemes—this was genuine partnership. TRW brought technology; Rane brought market access. TRW brought global standards; Rane brought local manufacturing expertise. Both brought capital, both shared risk, both expected returns.

The timing proved prescient. When P.V. Narasimha Rao and Manmohan Singh unleashed liberalization in 1991, Rane was already positioned for the new India. While competitors scrambled to find foreign partners, Rane was adding occupant protection systems for passenger cars in 1997 to its TRW joint venture. Airbags and seatbelts—products that seemed almost absurdly premature for an Indian market where basic safety was still optional—but Rane saw where India was heading.

The NSK partnership, formed in the mid-1990s, followed a similar logic but different dynamics. The company formed significant joint ventures, such as the one with NSK, Japan, and Torrington Company, U.S., in 1996-97. NSK brought steering column technology—the crucial link between steering wheel and steering gear. But more importantly, NSK brought Japanese manufacturing philosophy: kaizen, just-in-time, total quality management.

These weren't passive partnerships. Each joint venture became a university where Rane engineers learned not just how to make products, but how to think about manufacturing. The TRW venture taught American-style product development—rapid prototyping, concurrent engineering, design for manufacturing. The NSK venture taught Japanese-style production—eliminating waste, continuous improvement, respect for workers.

But partnerships extract a price beyond the equity dilution. Every joint venture is also a joint limitation. Product strategies need consensus. Technology roadmaps require agreement. Market expansions demand approval. For a company used to LLN's autocratic decisiveness, this democracy of decision-making chafed.

The deeper challenge was existential. Who was Rane becoming in these partnerships? With TRW, they were the junior partner learning from the master. With NSK, they were the local partner providing market access. But what happened when the student matched the master? When the local partner understood the local market better than any global principal ever could?

These questions gained urgency as India's automotive market exploded in the late 1990s. The Maruti-Suzuki phenomenon had democratized car ownership, but the real boom was in commercial vehicles. India's GDP was growing at 6-8% annually; goods needed to move. Every truck, every bus, every tractor needed steering systems. The market was large enough to sustain multiple players, but Rane's joint ventures meant it couldn't freely pursue every opportunity.

These partnerships were crucial for technological advancement and market expansion, contributing to the evolution of Rane business segments. By 2004, Rane had become a technology company that happened to manufacture auto components, rather than a manufacturing company trying to acquire technology. The transformation was complete, but the structure was becoming unwieldy.

The joint venture era had given Rane technology, credibility, and capabilities. But as the new millennium dawned, it became clear that Rane's corporate structure—a bewildering maze of cross-holdings, joint ventures, and subsidiary relationships—was becoming a constraint. Something had to give.

V. The Great Restructuring: Creating Rane Holdings (2005)

Corporate restructurings rarely make for compelling narratives. They're the business equivalent of refactoring code—necessary, complex, largely invisible to end users. But Rane's 2005 restructuring was different. This was architectural surgery on a living organism, performed while the patient continued running factories, serving customers, and generating cash flow.

The problem was elegant in its complexity. Over 75 years, Rane had grown organically, opportunistically, sometimes haphazardly. A major restructuring in 2005 led to the de-merger of Rane (Madras) Ltd. and the formation of Rane Holdings Ltd. (RHL) as the group holding company. But this bland description obscures the Gordian knot that needed untangling.

Imagine a corporate structure where the parent company owned shares in subsidiaries, which owned shares in other group companies, which sometimes owned shares in the parent. Where manufacturing operations were mixed with investments. Where strategic holdings were confused with treasury investments. The structure had evolved to minimize taxes and preserve family control, but it had become impossible for investors to value or understand.

In terms of the Scheme the manufacturing undertaking of the Company was demerged / transferred to RMML with effect from July 01 2004. Further the name of RMML was changed to Rane Madras Limited and the Company was renamed as Rane Holdings Limited. This wasn't just renaming—it was rebirth. The old Rane (Madras) Ltd, the original 1929 entity, shed its manufacturing operations and became a pure holding company.

The elegance lay in the execution. The conclusion of the restructuring exercise within the Group has achieved complete elimination of cross-holdings among group companies, as envisaged. Every subsidiary became clearly defined. Every holding became transparent. Every conflict of interest was eliminated.

But why do this? Why put the company through this expensive, time-consuming, risky exercise?

The answer lay in Rane's ambitions. To compete globally, Rane needed access to capital markets. To access capital markets efficiently, it needed a structure investors could understand. The old structure, with its circular holdings and mixed operations, traded at a massive conglomerate discount. Investors couldn't value what they couldn't understand.

The restructuring also solved a governance problem. Rane Holdings later made additional investments, making Rane (Madras) Ltd. a wholly-owned subsidiary. Clean structures enabled clean governance. Independent directors could be truly independent. Minority shareholders' interests could be properly protected. Related party transactions could be clearly identified and fairly priced.

RHL is a listed company with investments exclusively in the group companies. This focus was crucial. Rane Holdings became a pure play on the Rane Group's success—no distractions, no unrelated diversifications, no treasure hunts for hidden value.

The restructuring also created optionality. Each operating company could now raise capital independently. Each could form joint ventures without affecting others. Each could be valued on its own merits. If Rane ever needed to sell a business, it could do so cleanly. If it wanted to list a subsidiary, the path was clear.

The market's initial reaction was muted—restructurings always are. But over time, the benefits became apparent. The holding company structure allowed Rane to provide shared services efficiently. RHL owns the trademark in Rane and provides a range of services to group companies. These include employee training and development, investor services, business development and Information systems support.

This centralization of services created economies of scale while maintaining entrepreneurial autonomy in operating companies. Each subsidiary could focus on manufacturing while the holding company handled corporate functions. It was the best of both worlds—entrepreneurial energy with corporate sophistication.

The restructuring also facilitated leadership transition. With clean structures, professional managers could be hired for specific businesses. Family members could focus on strategic oversight rather than operational minutiae. The foundation was laid for Rane's next transformation—from a family business to a professionally managed corporation with family oversight.

VI. Modern Expansion & The Tata Nano Chapter (2006-2015)

The Tata Nano factory in Sanand, Gujarat, stands as a monument to both ambition and adaptation. But for Rane, it represents something more: the high-stakes gamble of betting on someone else's dream. Tata motors remains its major customer and is the primary parts manufacturer for Tata's Nano. When Ratan Tata envisioned the People's Car, Rane didn't just supply components—it restructured its entire growth strategy around a project that would either revolutionize Indian mobility or become history's most publicized failure.

The Nano commitment wasn't incremental. The company has also set up a dedicated plant for Tata Nano in Sanand, Gujarat. This meant capital expenditure in the hundreds of crores, dedicated production lines, specialized tooling, and trained workers—all for a car that existed more in imagination than reality when investments began.

But the real drama unfolded in Singur, West Bengal, in 2008. The Nano plant, nearly complete, became the flashpoint for one of India's most violent industrial disputes. Farmers protested land acquisition. Political parties mobilized opposition. Violence erupted. And then, in a stunning reversal, Tata pulled out. The company was forced to change its manufacturing facility from West Bengal to Gujarat after Tata moved out.

For Rane, this was catastrophe in slow motion. Millions invested in West Bengal—potentially worthless. Supply chains designed for Singur—now useless. Workers trained, equipment installed, production schedules planned—all in limbo. The board faced a stark choice: write off the investments and retreat, or double down and follow Tata to Gujarat.

They chose to follow. Not out of loyalty—sentiment has no place in auto components—but from calculated assessment. If the Nano succeeded, early suppliers would capture enormous value. If it failed, Rane would survive—it had before, it would again. But missing the opportunity if Nano succeeded? That was the unacceptable risk.

The Gujarat relocation revealed Rane's operational excellence. While media focused on Tata's miraculous factory construction in Sanand, Rane quietly rebuilt its entire supply infrastructure in record time. New plant, new workers, new logistics—all operational when the first Nano rolled off the line in 2010.

Yet even as Rane bet big on the Nano, it was hedging through geographic expansion. In 2020 the group had manufacturing facilities in Chennai, Puducherry, Hyderabad, Mysore, Tumkur, Pantnagar, Bawal, Trichy, Sanand. Each location was chosen strategically—close to customers, with good logistics, available skilled labor, and state government incentives.

This wasn't empire building—it was risk mitigation through diversification. If one customer faltered, others would compensate. If one region faced disruption, others continued operating. The 2008 financial crisis had taught Indian manufacturers that concentration was vulnerability.

The period also saw Rane's most ambitious technological upgrades. The company wasn't just expanding capacity; it was enhancing capability. Aluminum die-casting facilities for weight reduction. Computer-controlled machining centers for precision. Testing facilities that exceeded customer requirements. Rane was preparing for a future where "good enough" would no longer be good enough.

Quality became religion, not rhetoric. The Rane Group embarked on the TQM journey in the year 2000 under the leadership of Mr. L. Lakshman who was then the Chairman. Commencing from 2003, five of our Rane Companies won the Deming Prize and three of our Group companies went on to win Deming Grand Prize. The Deming Prize—Japan's most prestigious quality award—wasn't just recognition. It was validation that an Indian company could match global quality standards.

Meanwhile, the Nano was struggling. The People's Car had become a symbol of cheap, not affordable. Sales disappointed. Tata's one-lakh rupee dream became a marketing nightmare. By 2015, it was clear the Nano would never achieve its revolutionary ambitions.

For Rane, the Nano's failure was painful but not fatal. The dedicated facility pivoted to other products. The capabilities developed for high-volume, low-cost manufacturing found other applications. The relationships strengthened during crisis proved valuable in other ventures. Failure, handled correctly, became education.

The larger lesson was about customer concentration. Automobile companies that use its products include Ashok Leyland, Volvo, M&M, Tafe, Tata among many others. Tata motors remains its major customer. The Nano experience taught Rane that customer diversity wasn't just about revenue—it was about survival.

VII. Leadership Transition & Strategic Evolution (2015-2023)

The conference room at Rane Holdings' Chennai headquarters has witnessed many transitions, but few as consequential as the one unfolding in the mid-2010s. The patriarch L. Lakshman, who had guided Rane through liberalization and globalization, was preparing to hand over leadership to a new generation. But this wasn't your typical Indian family succession drama—it was a masterclass in institutional evolution.

Mr L Ganesh (LG) is the Chairman and Managing Director of Rane Holdings Limited. LG is a Chartered Accountant and holds an MBA from the Pennsylvania State University, USA. He has over 48 years of Industry experience and has played a key role in establishing strong footprint in global markets and winning the coveted Deming award.

L. Ganesh wasn't just another family member warming a chair. His credentials read like a private equity powerhouse resume: He was the Global partner of The Carlyle Group and the India Head of Asia Buyout Fund from 2005 to 2011. He has also served as the M & A Head and former Board member of DSP Merrill Lynch Ltd. This was someone who had evaluated hundreds of companies, structured complex deals, and understood global capital markets intimately.

The impact was immediate. Under Ganesh's leadership, Rane became more institutional, more metrics-driven, more globally oriented. But the crowning achievement came in November 2022. Recognised for his outstanding contribution in dissemination and promotion (Overseas) of Total Quality Management (TQM), L. Ganesh, Chairman of Rane Group, was conferred the prestigious Deming Award. He became the third Indian and fifth globally to be bestowed with this prestigious award.

But even as Ganesh provided strategic oversight, operational leadership was transitioning to the next generation. Mr Harish Lakshman holds Bachelor's degree in Mechanical Engineering from BITS, Pilani, and Master's degree in Business from Krannert School of Management at Purdue University, USA. With over 29 years of Industry experience, he has successfully been leading portfolios like marketing, operations, export business development. He is driving the Rane Group's mission to achieve accelerated profitable growth.

Harish Lakshman represented a different archetype—the engineer-MBA who understood both product and profit. His tenure as President of Automotive Component Manufacturers Association of India (ACMA) for the period 2013-14 gave him industry-wide perspective and relationships that would prove invaluable.

The dual leadership structure—L. Ganesh as Chairman, Harish Lakshman as Vice Chairman—created productive tension. Ganesh brought financial sophistication and global perspective. Harish brought operational excellence and customer intimacy. Together, they navigated Rane through one of the most turbulent periods in automotive history.

The strategic evolution during this period was marked by three themes: premiumization, indigenization, and diversification.

Premiumization meant moving up the value chain. No longer content with simple mechanical components, Rane invested in electronic power steering, advanced safety systems, and lightweight materials. The market was bifurcating—ultra-low-cost at one end, high-technology at the other. Rane chose technology.

Indigenization was both opportunity and necessity. The Make in India campaign created policy tailwinds. Global supply chain disruptions made local manufacturing attractive. Chinese component dominance triggered strategic concerns. Rane's response was aggressive localization—not just assembly, but genuine manufacturing capability.

Diversification took an unexpected turn. The Company acquired 26% stake in SasMos HET Technologies Limited in FY 2012. This wasn't auto components—it was defense and aerospace, sectors with completely different dynamics but similar precision engineering requirements. The logic was capability leverage—skills developed for automotive could serve aviation.

The period also saw Rane's most ambitious international forays. He has played a key role in establishing strong footprint in global markets. But unlike Indian companies that acquired distressed Western assets, Rane focused on organic expansion and technical partnerships. The approach was patient, methodical, very Rane.

Leadership transition also meant cultural evolution. The paternalistic management style of the LLN era gave way to professional meritocracy. Performance management systems replaced loyalty-based promotions. Stock options supplemented salaries. Rane was becoming a modern corporation while retaining family values.

Yet challenges mounted. Company has a low return on equity of 12.4% over last 3 years. Earnings include an other income of Rs.277 Cr. The conglomerate structure, despite the 2005 restructuring, still traded at a discount. Return on equity lagged peers. The market questioned whether Rane's diversified approach made sense in an era of focused plays.

The response came in March 2024, when L Ganesh retired and handed over the baton to Harish Lakshman. Winner of the prestigious Deming Award, L Ganesh will be a non-executive director and continue as chairman and managing director of Rane Holdings. This wasn't retirement—it was evolution. Ganesh remained engaged while Harish took operational control, ensuring continuity with change.

VIII. The NSK Acquisition: Full Control at Last (2024)

July 1, 2024, began like any other Monday at the Bombay Stock Exchange. Then, at 9:15 AM, a notice flashed across terminals: Rane Holdings Ltd announced that it will buy the remaining 51% stake in its joint venture, Rane NSK Steering Systems Pvt Ltd, from Japan's NSK Ltd for Rs 45 crore. Within minutes, Rane Holdings' share price surged 20% on the National Stock Exchange, reaching a 52-week high of Rs 1,605 per share.

The market's euphoria seemed disproportionate to the deal size—Rs 45 crore was pocket change for a group with revenues exceeding Rs 4,800 crore. But sophisticated investors understood: this wasn't just an acquisition. It was a declaration of independence.

The NSK joint venture had been established in 1997, manufacturing steering columns—the mechanical link between steering wheel and steering mechanism. For 27 years, it had been a successful partnership. It earned Rs 1,718.7 crore in the financial year 2024, up 14% from the previous year. By any measure, the JV was thriving. So why buy out a successful partner?

The answer lay in Rane's evolving strategic calculus. Joint ventures, once essential for technology access, had become constraints in the age of electric vehicles and autonomous driving. Every strategic decision required consensus. Every investment needed approval. Every new customer engagement triggered complex discussions about territory and technology rights.

Harish Lakshman, Chairman of Rane Group, said, 'We deeply value our relationship with NSK over the past two and a half decades, which has helped us establish a strong position in the Indian automotive steering market. This acquisition further expands our group's expertise in steering systems.' The diplomatic language obscured a profound shift—Rane no longer needed foreign partners to validate its technology credentials.

The structure of the deal revealed sophisticated thinking. A cash consideration of INR 450 million will be paid by Rane Holdings Limited. All cash, no complex earn-outs or contingencies. Clean, simple, decisive. The purchase price—approximately Rs 49 per share on a base of Rs 10—suggested a fair valuation, neither stealing from NSK nor overpaying for control.

Critically, RSSL will maintain its existing technology license and supply agreements with NSK Steering & Control, Inc. This wasn't a hostile divorce but an amicable evolution. NSK retained technology partner status without equity exposure. Rane gained operational freedom while maintaining technical support. Both parties won.

The timing was no accident. The Indian automotive market was at an inflection point. Electric vehicles were transitioning from experiment to mainstream. Steering systems for EVs differed fundamentally from traditional vehicles—no engine vibration to dampen, different weight distributions to manage, new packaging constraints to navigate. Rane needed agility to respond, not committee meetings to deliberate.

There was also the China factor. Global supply chains were regionalizing. "China Plus One" strategies meant opportunity for Indian suppliers. But global customers wanted suppliers who could make decisions quickly, invest aggressively, and take risks independently. Joint ventures, with their inherent decision-making complexity, were disadvantages in this new world.

The financial engineering was elegant. The company had to set aside approximately Rs 5 billion for warranty provisions, of which Rs 4.72 billion has already been disbursed, leaving about Rs 280 million remaining. The warranty issue—a persistent overhang on the JV's financials—was nearly resolved. Rane was buying a cleaned-up business, not inheriting massive contingent liabilities.

But the real masterstroke was what happened next. This will make Rane NSK Steering Systems a fully owned subsidiary of Rane Holdings and it will be renamed Rane Steering Systems Pvt Ltd. The renaming wasn't cosmetic—it was strategic. For the first time in decades, a major Rane manufacturing entity would carry only the Rane name. No TRW, no NSK, no foreign validation required.

The acquisition also simplified Rane's corporate structure. Instead of a web of joint ventures with different partners, varying shareholdings, and complex governance, Rane was moving toward a cleaner model: wholly-owned subsidiaries where possible, strategic partnerships where necessary, but always with clear control and decision rights.

Market reaction validated the strategy. The 20% single-day surge wasn't just about this deal—it was about what this deal signified. Rane was signaling confidence in its own capabilities. It was preparing for a future where speed mattered more than credentials, where agility trumped pedigree.

The NSK acquisition marked the end of an era—the joint venture era that had defined Rane's growth for three decades—and the beginning of another. Rane was no longer the junior partner learning from global masters. It was a master in its own right, confident enough to chart its own course.

IX. Business Model & Competitive Position

Step into any of Rane's factories and you'll notice something unusual for Indian manufacturing: the absence of chaos. No frantic shouting, no last-minute scrambles, no heroic firefighting. Instead, there's an almost zen-like rhythm—parts flowing in predetermined patterns, workers moving with practiced precision, machines humming in calibrated harmony. This operational excellence isn't accidental. It's the physical manifestation of a business model refined over nine decades.

At its core, Rane operates as a Tier-1 supplier—selling directly to original equipment manufacturers (OEMs) rather than through intermediaries. Rane Holdings Limited manages strategic investments across Rane Group subsidiaries and joint ventures, licensing the Rane trademark and providing management, IT, business development, and investor services within the group. But this clinical description misses the nuance. Rane isn't just a supplier; it's an extension of its customers' engineering departments.

Consider the product portfolio breadth. Manufactures steering and suspension systems, friction materials, valve train components, occupant safety systems and die-casting products for passenger vehicles, commercial vehicles, farm tractors, two-wheelers, and three-wheeler. This isn't random diversification—it's strategic adjacency. Each product category leverages similar manufacturing capabilities: precision machining, metallurgy expertise, quality control systems.

The competitive moat isn't technology alone—Chinese competitors can reverse-engineer products, and global giants have deeper R&D budgets. Rane's edge lies in what consultants call "operational excellence" but what really means trust at scale. When Ashok Leyland designs a new truck, they don't bid out steering systems to the lowest bidder. They call Rane, knowing that Rane will deliver on time, every time, with quality that won't embarrass them in the field.

This trust translates into pricing power, but not the kind you might expect. Rane doesn't extract monopoly rents—Indian OEMs are too cost-conscious for that. Instead, Rane gets what matters more: long-term contracts, early involvement in new platforms, and most crucially, payment terms that don't destroy working capital. In an industry where 120-day payment cycles are common, these soft benefits matter enormously.

The customer concentration risk is real but manageable. Automobile companies that use its products include Ashok Leyland, Volvo, M&M, Tafe, Tata among many others. Tata motors remains its major customer. No single customer represents more than 25% of revenues—concentrated enough for economies of scale, diversified enough to survive any single customer's troubles.

The manufacturing footprint reflects this customer-centric approach. Plants aren't located for cheap labor or tax benefits—they're positioned near customers. The Pantnagar facility serves Tata Motors. The Chennai cluster serves the southern automotive hub. Each location minimizes logistics costs and response times while maximizing customer intimacy.

But the real competitive advantage might be cultural. Rane embodies what economists call "patient capital"—the ability to invest for decades-long returns rather than quarterly earnings. This shows in everything from employee tenure (average factory experience exceeds 15 years) to technology investments (implementing systems that won't pay back for five years) to market development (entering segments that won't be profitable until volumes build).

The holding company structure amplifies these advantages. RHL owns the trademark in Rane and provides a range of services to group companies. These include employee training and development, investor services, business development and Information systems support. Centralized services create scale economies. Shared learning accelerates capability building. Group reputation helps individual companies win business.

Yet challenges persist. The return on equity question won't disappear. Company has a low return on equity of 12.4% over last 3 years. Earnings include an other income of Rs.277 Cr. In a market that rewards asset-light software companies with 40% returns, Rane's capital-intensive manufacturing looks antiquated. The conglomerate discount remains sticky—investors struggle to value diversity, preferring pure plays they can easily model.

Competition intensifies from multiple directions. Global giants like Bosch and Continental bring superior technology and deep pockets. Chinese entrants offer "good enough" quality at disruptive prices. New-age startups target electric vehicle opportunities without legacy overhead. And customers themselves backward-integrate, questioning why they need suppliers for components they could make themselves.

Rane's response has been measured, almost philosophical. Rather than chase every opportunity or match every competitive move, it doubles down on core strengths. Quality that exceeds requirements. Delivery reliability that customers plan around. Engineering support that solves problems before they become crises. Relationships that transcend commercial transactions.

X. Financial Analysis & Investment Thesis

The numbers tell a story, but not the one you might expect. Mkt Cap: 2,322 Crore, Revenue: 4,872 Cr, Profit: 259 Cr. At first glance, Rane Holdings looks like a pedestrian performer—single-digit revenue growth, margins that would embarrass a software company, returns that barely exceed the cost of capital. But this surface reading misses the chess game being played.

Start with the obvious bear case. Company has a low return on equity of 12.4% over last 3 years. Earnings include an other income of Rs.277 Cr. A 12.4% ROE in an era of 15% risk-free rates (adjusted for India risk) means Rane destroys value, right? Not quite. The Rs 277 crore of other income—primarily dividends from joint ventures and treasury operations—obscures operational performance. Strip this out, and the core business ROE drops further. The bears growl louder.

The capital allocation puzzle deepens when you examine the cash flow statement. Rane generates consistent operating cash flow—the factories are cash machines. But this cash immediately disappears into capital expenditure. New machines, expanded facilities, technology upgrades—a never-ending treadmill of investment just to maintain competitive position. It's the Red Queen's race: running faster and faster just to stay in place.

The holding company discount compounds these issues. Investors value Rane Holdings based on its stake in operating companies, then apply a 20-30% haircut for the holding structure. Why? Because minority investors in the holdco have no direct claim on subsidiary cash flows. You own Rane Holdings, not Rane Madras or Rane Brake Lining. The subsidiaries could generate billions; unless they dividend it up, holdco shareholders see nothing.

But here's where the investment thesis gets interesting. The bear case assumes the status quo persists—that Rane remains a sprawling conglomerate, that returns stay suppressed, that the holding discount is permanent. The NSK acquisition suggests management disagrees.

Consider the strategic optionality. Rane Holdings sits on valuable stakes in operating companies that could be monetized. The crown jewel—the steering systems business—now fully owned after the NSK buyout, could be listed separately. Based on peer valuations, this business alone could be worth Rs 3,000-4,000 crore. The brake lining business, the engine valve business—each could unlock value through separate listings or strategic sales.

The technology transition creates additional optionality. Electric vehicles need different components—but they still need steering systems, still need brake components (arguably more given regenerative braking complexity), still need precision-manufactured parts. Rane's capabilities translate; the products evolve. Every disruption creates opportunity for prepared operators.

The international expansion story remains underappreciated. He has played a key role in establishing strong footprint in global markets. Indian auto component exports are growing at 15-20% annually as global OEMs discover India's manufacturing competitiveness. Rane, with its quality credentials and established relationships, is perfectly positioned to capture this growth.

The management quality factor deserves premium valuation but receives none. He is the third Indian and fifth globally to be bestowed with this prestigious award for his contributions. L. Ganesh's Deming Award isn't just a trophy—it's validation of world-class management systems. In industries where operational excellence determines survival, this matters enormously.

The balance sheet provides comfort even to skeptics. Debt remains manageable—mostly working capital financing rather than leveraged expansion. The subsidiaries are self-funding. The holding company has investment flexibility. This isn't a leveraged bet on automotive growth; it's a conservative play on Indian manufacturing excellence.

Valuation requires nuance. On trailing P/E, Rane looks expensive relative to its ROE. But on replacement cost of assets, it's trading at a significant discount. Building Rane's manufacturing footprint from scratch would cost multiples of current market capitalization. The factories, the relationships, the technical capabilities—these can't be replicated quickly or cheaply.

The real question isn't whether Rane is cheap or expensive today—it's whether Indian automotive manufacturing has a future. If India becomes the world's factory for small cars and two-wheelers (as China was for electronics), Rane wins big. If electric vehicles democratize transportation in emerging markets, Rane supplies critical components. If global supply chains permanently regionalize, Rane benefits from both import substitution and export growth.

The investment case ultimately reduces to a bet on execution. Can management improve returns through operational excellence? Can they unlock value through strategic actions? Can they navigate technology transitions while maintaining profitability? The track record suggests yes, but the market demands proof.

XI. Playbook: Lessons for Builders

Every business story teaches lessons, but most are situation-specific—what worked for software won't work for steel. Rane's playbook is different. These aren't tactics but principles, applicable whether you're building auto components or aerospace systems, whether in India or Indonesia.

Lesson 1: Patient Capital Compounds

Rane's nine-decade journey demonstrates the power of thinking in decades, not quarters. The 1959 decision to abandon trading for manufacturing took 20 years to fully pay off. The joint ventures of the 1990s created capabilities that generated returns in the 2010s. The quality investments of the 2000s built reputation that wins business today. In manufacturing, there are no overnight successes—only overnight failures.

Lesson 2: Technology Acquisition Through Partnership

The joint venture model Rane perfected offers a template for capability building in emerging markets. Don't just license technology—create partnerships where both parties have skin in the game. The JV was founded in 1987 by Rane and TRW to produce steering systems for commercial vehicles. In 1997, the company added occupant protection systems for passenger cars. With the acquisition of TRW in 2015, ZF Group became a co-owner. Start with products for local markets, evolve to global standards, eventually achieve technology parity, then seek independence.

Lesson 3: Restructuring as Strategic Weapon

The 2005 restructuring shows how corporate structure can constrain or enable strategy. The conclusion of the restructuring exercise within the Group has achieved complete elimination of cross-holdings among group companies. Complex structures might optimize taxes short-term but destroy value long-term. Clean structures attract investors, enable governance, and create strategic flexibility. The pain of restructuring is temporary; the benefits are permanent.

Lesson 4: Trust as Competitive Advantage

In industries where product failure can kill people—automotive, aerospace, medical devices—trust matters more than price. Rane built trust through decades of consistent delivery, quality that exceeded specifications, and standing behind products when things went wrong. Trust can't be bought through marketing or acquired through M&A. It must be earned through repetition and protected zealously.

Lesson 5: The Liberation of Taking Control

The NSK acquisition reveals a profound truth: junior partners eventually outgrow their seniors. Rane Group Chairman Harish Lakshman said the acquisition will strengthen the group's expertise in steering systems. Don't cling to partnerships past their expiration date. When you no longer need validation, seek independence. The price of control might seem high, but the cost of constraint is higher.

Lesson 6: Geographic Dispersion as Risk Mitigation

In 2020 the group had manufacturing facilities in Chennai, Puducherry, Hyderabad, Mysore, Tumkur, Pantnagar, Bawal, Trichy, Sanand. Rane's distributed manufacturing model teaches resilience through redundancy. Single points of failure—one factory, one customer, one geography—are vulnerabilities. Dispersion increases costs but ensures survival. In manufacturing, survival precedes success.

Lesson 7: Family Business Succession Without Drama

Indian family businesses often implode during succession. Rane's transition from L. Lakshman to L. Ganesh to Harish Lakshman shows another way. Professionalize early, separate ownership from operation, bring in external talent for operational roles, keep family for strategic oversight. Merit matters more than blood, but blood provides continuity that merit alone cannot.

Lesson 8: Quality as Religion, Not Department

Commencing from 2003, five of our Rane Companies won the Deming Prize and three of our Group companies went on to win Deming Grand Prize. The Deming journey wasn't about winning awards but embedding quality thinking in organizational DNA. Quality isn't inspection at the end; it's discipline at every step. In precision manufacturing, good enough never is.

Lesson 9: The Courage to Say No

What Rane didn't do is as instructive as what it did. No flashy acquisitions of distressed Western assets. No unrelated diversification into real estate or retail. No financial engineering to juice short-term returns. Staying focused requires saying no to seemingly attractive opportunities that don't fit core capabilities.

Lesson 10: Building for Permanence

In an era of unicorns and exits, Rane represents something unfashionable: building for permanence. No founder has cashed out. No private equity has stripped assets. No strategic buyer has absorbed operations. This isn't about lifestyle businesses or family pride—it's about recognizing that some capabilities take generations to build and moments to destroy.

XII. Epilogue: The Road Ahead

The automotive world of 2024 would seem like science fiction to T.R. Ganapathy Iyer. Electric vehicles glide silently through streets. Software updates change vehicle performance overnight. Artificial intelligence predicts component failures before they occur. The internal combustion engine—the technology that built Rane—faces existential threat. Yet Rane not only survives but thrives. How?

The answer lies in understanding what Rane really sells. Not steering columns or brake pads or engine valves, but trust in critical components. Whether a vehicle is powered by petrol, batteries, or hydrogen, it needs to steer precisely. Whether it's driven by humans or algorithms, it needs to stop reliably. The products evolve; the need for precision manufacturing endures.

The electric transition presents both threat and opportunity. Threat because EVs have fewer components—no engine valves needed when there's no engine. Opportunity because EVs demand different components—more sophisticated steering systems for heavier vehicles, advanced thermal management solutions, lightweight materials for range optimization. Rane's response has been measured: invest in EV-relevant technologies while maximizing returns from ICE components while they last.

The international expansion ambition articulated by leadership deserves attention. Rane Holdings is focused on strengthening its domestic leadership and increasing international revenues. The company is expanding its focus on the aftermarket segment, which is a growing area. But this isn't about planting flags or acquisition headlines. It's about following customers as they globalize, leveraging India's cost advantages for export markets, and building redundancy against domestic market volatility.

The leadership transition to Harish Lakshman marks more than generational change—it signals strategic evolution. He has successfully been leading portfolios like marketing, operations, export business development. He is driving the Rane Group's mission to achieve accelerated profitable growth. "Accelerated profitable growth"—note the emphasis on both speed and returns. The patient capital era isn't ending, but the metabolism is increasing.

The competitive landscape will only intensify. Chinese component manufacturers, having dominated their domestic market, are expanding globally with prices that seem to defy physics. Global giants are consolidating, creating suppliers with revenues exceeding many OEMs. Technology companies are entering automotive, bringing software capabilities but needing hardware partners. In this environment, Rane's positioning as a trusted, flexible, mid-sized supplier might be exactly right.

The financial markets remain skeptical—the conglomerate discount persists, ROE questions linger, growth concerns multiply. But Rane has survived skepticism before. It survived colonial extraction, socialist stagnation, liberalization disruption, and global competition. Each challenge strengthened capabilities, deepened relationships, and reinforced culture.

Can Rane become India's Bosch or Continental? The scale gap seems insurmountable—Continental's revenue exceeds Rane's by 50x. But scale isn't destiny. Specialized excellence can triumph over generalized adequacy. Rane doesn't need to become Continental; it needs to become the best version of Rane.

The most profound question facing Rane isn't about technology or competition or financial returns. It's about purpose. For 95 years, Rane has enabled mobility—helping India progress from bullock carts to Ambassadors to Innovas. As India becomes the world's most populous nation, as hundreds of millions seek better lives through movement, that purpose remains vital.

The road ahead will test every capability Rane has built—technological adaptability, operational excellence, financial prudence, relationship depth. But roads are what Rane knows. Every steering system it manufactures helps someone navigate their journey. Every brake component ensures they arrive safely. Every valve enables motion.

T.R. Ganapathy Iyer started by importing automobiles to colonial Madras. His successors now export components worldwide. The trader became manufacturer, the imitator became innovator, the junior partner became sovereign. The transformation isn't complete—transformation never is—but the trajectory is clear.

Rane's story offers no guarantee of future success. Disruption could still destroy value. Competition could erode margins. Technology could obsolete products. But betting against a company that has survived everything from world wars to global pandemics, that has transformed itself from trader to manufacturer to technology company, that has built trust over generations—that seems like the riskier proposition.

The quiet giant of Indian auto components remains quiet by choice, giant by persistence. In a world of hype and headlines, Rane continues doing what it has always done: making components that work, building relationships that last, creating value that endures. The road ahead is uncertain, but Rane has always been about the journey, not just the destination.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube