Lowe's Companies: Building America's Home Improvement Dreams

I. Introduction & Episode Roadmap

Picture a Saturday morning in suburban Charlotte, 1989. A contractor pulls into a massive new warehouse store, its orange sign blazing in the morning sun. Home Depot has just claimed the crown as America's largest home improvement retailer. Twenty miles away, in a smaller, more traditional store, Lowe's executives huddle around a conference table, grappling with an existential question: How do you compete when you've just become number two?

This is the story of Lowe's Companies—a century-old institution that transformed from a small-town North Carolina hardware store into America's second-largest home improvement retailer, operating over 2,100 stores and generating more than $86 billion in annual revenue. It's a tale of family feuds, strategic pivots, and the relentless pursuit of a rival that always seems one step ahead. The fundamental challenge for any #2 company is clear: Do you imitate the leader, differentiate, or find an entirely new game? For Lowe's, this question has defined its existence since that fateful 1989 moment when Home Depot claimed the crown. Yet the company that stands today—with over 1,700 stores and approximately 300,000 associates, generating more than $83 billion in fiscal year 2024 sales—represents one of retail's most fascinating transformations.

What makes Lowe's particularly compelling isn't just its David-versus-Goliath narrative against Home Depot. It's how a family hardware store from North Carolina systematically built competitive advantages, stumbled through strategic missteps, and ultimately found its footing under unlikely leadership. This is a story about the power of operational excellence, the perils of international expansion, and the surprising advantages that sometimes come from being second.

The themes we'll explore resonate far beyond home improvement retail. How does a century-old company reinvent itself multiple times? What happens when professional management replaces family control? And perhaps most intriguingly: In an industry where scale typically wins, how does the smaller player carve out sustainable competitive advantages?

II. Origins: The Lowe Family Hardware Store (1921–1952)

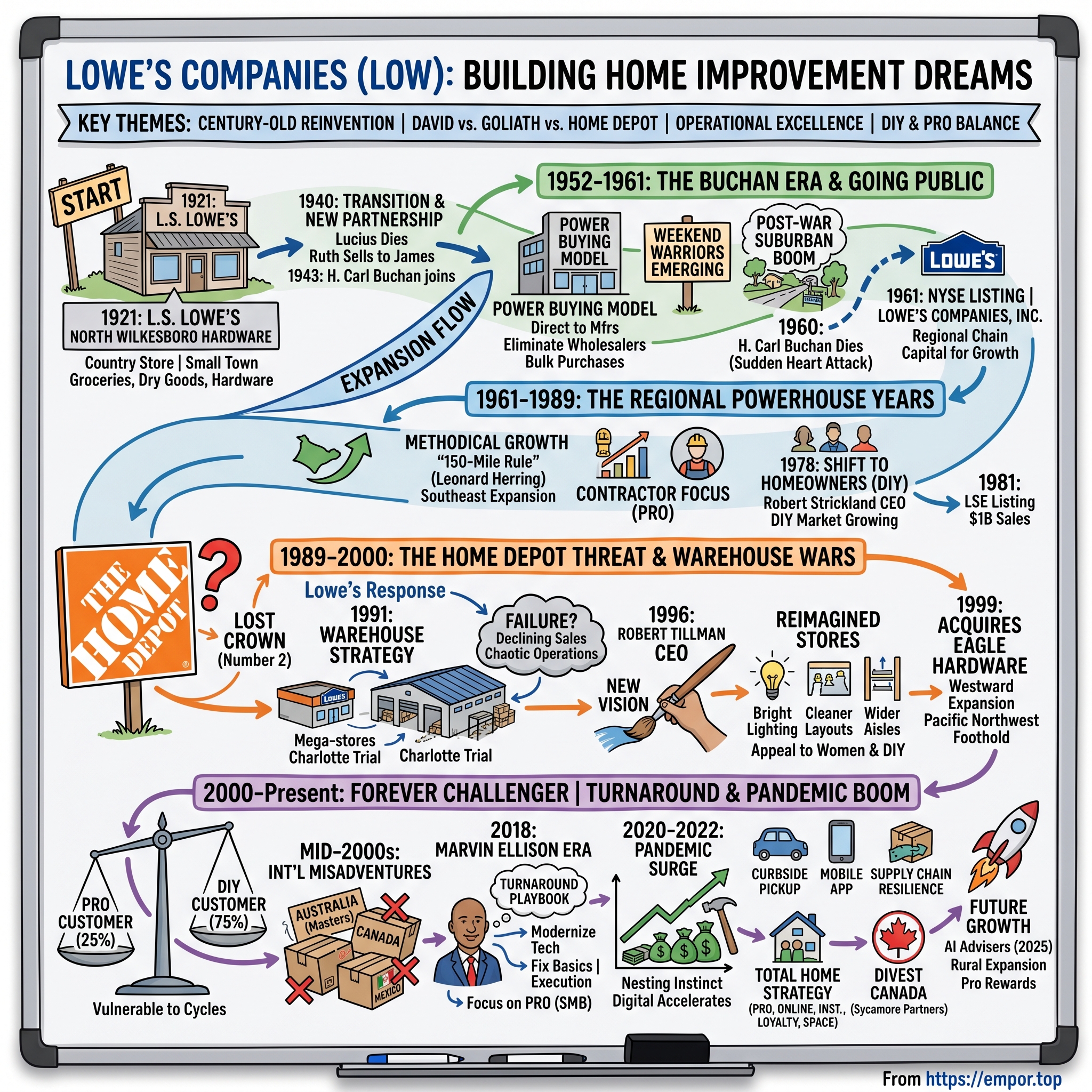

The year was 1921, and Calvin Coolidge had just become Vice President. In the small town of North Wilkesboro, North Carolina—population barely 2,000—Lucius Smith Lowe opened a modest hardware store. He couldn't have imagined that his humble shop, tucked between the Blue Ridge Mountains and the Yadkin River, would spawn one of America's retail giants.

L.S. Lowe's North Wilkesboro Hardware was quintessentially small-town America. The shelves carried everything from horse tack to snuff, from dry goods to fresh produce. Hardware was almost an afterthought—just another category among the groceries and notions that kept the community supplied. This was retail as community service, where credit was extended on a handshake and everybody knew your name.

Then came 1940. Lucius Lowe died suddenly, leaving behind a thriving but modest business. His daughter Ruth Buchan inherited the store, but she had no interest in running it. In a transaction that would reshape American retail, she sold the business to her brother James for $4,200—roughly $90,000 in today's dollars. It was a family deal, done quietly, with no fanfare.

James Lowe was competent but conventional. He might have run the store for decades as his father had, serving the local community with the same mix of merchandise. But in 1943, he made a decision that would change everything: he brought in his brother-in-law, H. Carl Buchan, as a partner.

Carl Buchan was different. Where others saw a hardware store, he saw a supply chain revolution waiting to happen. A World War II veteran with an eye for opportunity, Buchan recognized something profound happening in post-war America. The GIs were coming home. They were getting married, having babies, and building houses at a rate the country had never seen. The suburban boom was beginning, and Buchan wanted Lowe's positioned to supply it.

His masterstroke was deceptively simple: eliminate the middleman. While other hardware stores bought from wholesalers—accepting their markups and limited selection—Buchan went straight to manufacturers. He'd drive his truck to factories, negotiate bulk purchases, and pass the savings to customers. This wasn't just about price; it was about fundamentally reimagining how a hardware store operated.

By 1949, this model had proven successful enough to open a second location in Sparta, North Carolina. The product mix had completely transformed—gone were the groceries and dry goods, replaced by lumber, tools, and building supplies. Buchan wasn't running a general store anymore; he was building a construction supply company disguised as a retail operation.

When James Lowe exited the business in 1952, selling his stake to Buchan, the company bore little resemblance to the store Lucius had founded. Under Buchan's sole ownership, expansion accelerated dramatically. By 1955, stores had opened in Durham, Asheville, and Charlotte—North Carolina's major cities. The company had grown from one store to six, from serving a town to serving a state.

What Buchan understood, perhaps better than his contemporaries, was that post-war America represented a fundamental shift in how people lived. The suburban single-family home wasn't just a housing trend; it was a cultural revolution. And every one of those homes would need lumber for additions, paint for walls, tools for repairs. He was building the infrastructure for the American Dream, one store at a time. The transformation from L.S. Lowe's country store to Buchan's building supply chain was complete.

III. The Buchan Era & Going Public (1952–1961)

Carl Buchan was only 36 when he became sole owner of Lowe's in 1952, but he operated with the strategic vision of someone twice his age. His office in North Wilkesboro became a laboratory for retail innovation, where he'd spread out maps of the Southeast, marking potential store locations with the precision of a military campaign. By 1960, he had expanded the chain to 15 stores, each one positioned to capture the post-war construction boom.

Buchan's genius lay not just in expansion but in reimagining the entire hardware retail model. While competitors maintained traditional wholesale relationships, he pioneered what would later be called "power buying"—leveraging volume to negotiate directly with manufacturers. A typical hardware store might stock 20 different types of hammers from various wholesalers; Buchan would buy 10,000 hammers directly from Estwing or Stanley, securing prices that undercut everyone else by 30-40%.

He also understood psychology. Buchan insisted that stores display prices prominently—unusual for the era when many retailers preferred negotiable pricing. His philosophy was simple: "Let the customer know they're getting wholesale prices. Make them feel like insiders." He'd often be found on store floors, watching how customers moved through the aisles, adjusting displays based on traffic patterns.

By early 1960, Lowe's was generating nearly $30 million in annual revenue. Carl Buchan, at 44, was at the peak of his powers, planning an aggressive expansion that would take the company throughout the Southeast. He had just finalized plans for five new stores and was negotiating directly with lumber mills in Georgia and Alabama.

Then, on November 13, 1960, everything changed. Buchan suffered a fatal heart attack, dying instantly at his desk. He left behind a wife, three children, and a company suddenly without its visionary leader. The stores were closed for his funeral—the only time in company history all locations would simultaneously shut their doors.

The board of directors faced a crisis. Buchan had been Lowe's—its strategist, its negotiator, its cultural cornerstone. There was no succession plan, no obvious heir apparent. For three weeks, the company drifted while board members debated whether to sell to a larger chain or attempt to continue independently.

The solution came from an unlikely source: a five-man executive committee consisting of middle managers who had worked closely with Buchan. Robert Strickland, who had run the Asheville store; Leonard Herring, the company's first professional accountant; Pete Kulynych, who managed supplier relationships; John Belk, who handled real estate; and Bill McElwee, who oversaw warehousing. None had Buchan's charisma or vision, but together they understood his system.

This committee made a radical decision: take the company public. It was a move Buchan himself had considered but never executed. The reasoning was both practical and strategic. Going public would provide capital for expansion without requiring debt, create liquidity for Buchan's widow and other shareholders, and most importantly, institutionalize the company beyond any single leader.

On October 10, 1961, Lowe's Companies, Inc. began trading on the over-the-counter market. The initial public offering of 400,000 shares at $12.25 raised nearly $5 million—modest by today's standards but transformational for a regional hardware chain. The first day saw moderate trading, with the stock closing at $12.75, a good but not spectacular debut.

But the real victory came two months later. On December 19, 1961, Lowe's achieved what only 1,200 companies had accomplished: listing on the New York Stock Exchange. For a company that had been a single small-town store just 40 years earlier, it was a stunning achievement. The NYSE listing provided credibility with suppliers, access to capital markets, and a currency—stock options—to attract professional management.

The transition from family business to public company fundamentally altered Lowe's DNA. Where Buchan had made decisions intuitively, the new leadership required data and consensus. Where he had maintained relationships through handshakes and personal visits, the company now needed systems and processes. It was the end of Lowe's as a regional family business. What emerged would become something far larger, though perhaps less personal—a transformation that would define the company's next chapter as it raced to build scale before competitors could catch up.

IV. Building Scale: The Regional Powerhouse Years (1961–1989)

The morning after Lowe's NYSE debut, Robert Strickland stood in the parking lot of the North Wilkesboro store, watching contractors load their trucks. These professionals—builders, plumbers, electricians—had been Lowe's bread and butter since Buchan's day. They'd arrive at 6 AM, buy in bulk, and pay on account. But Strickland noticed something else: the weekend warriors, showing up in station wagons, buying single sheets of plywood, asking endless questions. The contractors called them "civilians" with barely concealed disdain. But Strickland saw opportunity.

By 1962, one year after going public, Lowe's had grown to 21 stores across North Carolina, generating $32 million in annual revenue. The executive committee's conservative approach—measured expansion, careful cost control—was working. But the retail landscape was shifting. The interstate highway system was connecting previously isolated markets. Shopping centers were sprouting in suburbs. And a new generation of homeowners, raised on Popular Mechanics and This Old House, wanted to do their own repairs.

Leonard Herring, the analytical accountant of the five-man team, became the unlikely architect of Lowe's expansion strategy. He developed what he called the "150-mile rule"—no new store more than 150 miles from an existing location, ensuring efficient distribution and management oversight. Using demographic data that was revolutionary for the time, he identified markets with specific characteristics: growing populations, rising incomes, and crucially, high rates of home ownership.

The expansion was methodical but relentless. By 1970, Lowe's had crossed state lines into South Carolina, Tennessee, and Virginia. By 1975, the company operated 59 stores across seven states. Revenue exceeded $150 million. But success brought scrutiny. The Federal Trade Commission investigated Lowe's buying practices, concerned about its growing market power. The investigation ultimately cleared the company but signaled that Lowe's had become too big to operate under the radar.

Then came 1978, and with it, a changing of the guard. Robert Strickland, who had gradually emerged as first among equals in the executive committee, was formally named CEO. At 56, Strickland was a different breed from Buchan—less visionary, perhaps, but with a systematic mind for process and scale. His first major decision would transform the company.

"We're going after the homeowner," Strickland announced at the 1979 annual meeting. The strategy was heretical. Contractors were reliable, bought in volume, and required minimal service. Homeowners were unpredictable, needed hand-holding, and bought smaller quantities. But Strickland had done the math. The DIY market was growing at 15% annually, versus 5% for professional construction. More importantly, DIY customers paid retail prices, not contractor discounts.

The shift required reimagining everything. Stores added weekend hours. They hired staff who could explain, not just sell. They created how-to clinics—"Building a Deck," "Installing a Toilet," "Basic Electrical Repairs." They even published a newsletter with project plans. Old-timers grumbled that Lowe's was becoming "too soft," but the numbers didn't lie. By 1985, more than half of sales came from non-professional customers.

January 26, 1981, marked another milestone: Lowe's was listed on the London Stock Exchange, one of the first American retailers to do so. That same year, the company crossed $1 billion in sales, earning a record $25 million profit. The kid from North Wilkesboro had grown up.

But success attracted competition. Throughout the 1980s, regional chains like Builders Square, Hechinger, and Rickel expanded aggressively. And there was another competitor, growing even faster, with a radical new format. Home Depot, founded in 1978 by Bernie Marcus and Arthur Blank, was revolutionizing hardware retail with massive warehouse stores, rock-bottom prices, and an orange-aproned army of helpful associates.

The collision was inevitable. In 1989, industry data confirmed what everyone suspected: Home Depot had surpassed Lowe's as America's largest home improvement retailer. After 68 years, 38 of them as the industry leader, Lowe's was now number two.

At the company's 1989 Christmas party, Strickland addressed employees with characteristic directness: "Being second means we have to be better. Better service, better locations, better for our communities." But privately, he knew that incremental improvements wouldn't be enough. Lowe's needed a revolution of its own. The era of steady, careful expansion was over. The warehouse wars were about to begin.

V. The Home Depot Threat & Warehouse Transformation (1989–2000)

Bernie Marcus stood in the first Home Depot, surveying his 60,000-square-foot warehouse in Atlanta, where forklifts operated alongside customers and merchandise was stacked to the rafters. "We're not retailers," he told his co-founder Arthur Blank in 1978. "We're theater." By 1989, when Home Depot claimed the industry crown from Lowe's, that theater was playing to packed houses across America.

The news hit Lowe's headquarters like a thunderbolt. For decades, the company had competed against regional chains playing by similar rules—traditional stores, professional focus, steady expansion. Home Depot had changed the game entirely. Their stores were three times larger than typical Lowe's locations. They stayed open nights and weekends. Most devastatingly, their prices were 20-30% lower on comparable items.

Robert Strickland, now 67 and nearing retirement, faced the hardest decision of his career. Lowe's operated 300 stores averaging 20,000 square feet—profitable, efficient, but suddenly obsolete. Converting to warehouse formats would cost billions, cannibalize existing stores, and require capabilities Lowe's didn't possess. The board was divided. Some pushed for acquisition targets to quickly gain scale. Others advocated staying the course, focusing on smaller markets Home Depot ignored.

The debate raged through 1990. Then Strickland made a characteristic move: he commissioned a study. Consultants spent six months analyzing every aspect of both companies' operations. Their conclusion was stark: without warehouse stores, Lowe's would be relegated to secondary markets within five years. The only question was how fast to transform.

In early 1991, Lowe's officially announced its warehouse strategy. The first mega-store—85,000 square feet—would open in Charlotte, directly challenging a Home Depot two miles away. It was a declaration of war, and everyone knew it.

The Charlotte store opened in October 1991 to mixed results. Sales were strong, but operations were chaotic. Lowe's had built a big box but hadn't transformed its DNA. Inventory systems designed for 20,000-square-foot stores broke down at scale. Associates trained in contractor sales struggled with DIY customers asking about paint colors and garden fertilizers. Most embarrassingly, Home Depot's prices were still lower on 60% of comparable items. By 1994, the transformation was clearly failing. Lowe's had opened 25 warehouse stores, but same-store sales were declining. The stock had underperformed the S&P 500 for three consecutive years. Leonard Herring, the last of the original five-man committee, was struggling as CEO. The board knew dramatic action was needed.

Enter Robert L. Tillman. A Lowe's lifer who had started as an entry-level office manager trainee in 1962, Tillman had worked his way through virtually every department—store management, merchandising, operations. Named to the board in 1994 and becoming president and CEO in 1996, Tillman brought something Lowe's desperately needed: a clear vision of what a modern home improvement retailer should be.

Tillman's insight was counterintuitive. While everyone obsessed over competing with Home Depot on price and selection, he noticed something else in the research: women initiated 80 percent of home improvement projects. Yet both Lowe's and Home Depot were essentially masculine environments—concrete floors, harsh lighting, minimal service. "We're missing half our market," Tillman told the board.

The transformation Tillman orchestrated was comprehensive. Stores were brightened with better lighting, cleaner layouts, and wider aisles. Product mix shifted to include more appliances, high-end bathroom fixtures, and designer paint lines like Laura Ashley. Customer service became paramount—not just knowledgeable staff, but approachable ones. It was retail theater of a different kind than Home Depot's warehouse aesthetic.

1995 marked another crucial development: the launch of Lowes.com. While primitive by today's standards—essentially an online catalog—it signaled that Lowe's understood retail's digital future earlier than most. Home Depot wouldn't launch its website until 1999.

The strategy started working. By 1998, same-store sales were growing at 5% annually. In 1997, Tillman committed $1.5 billion to create 100 new stores in the West, targeting prime markets in Arizona, California, and Nevada including Phoenix, Tucson, Los Angeles, San Diego, and Las Vegas. The westward expansion was crucial—these markets were growing faster than Lowe's traditional Southeast base.

But the real coup came in November 1999. Lowe's announced the acquisition of Eagle Hardware & Garden, a chain of 32 warehouse-scale stores based in Renton, Washington. For $1.3 billion, Lowe's gained instant critical mass in the Pacific Northwest and California. More importantly, Eagle's stores were already second-generation big boxes—bright, organized, customer-friendly. They validated Tillman's vision.

By 2000, Lowe's operated over 650 stores in 40 states, with revenues approaching $19 billion. The company had successfully transformed from regional hardware chain to national big-box retailer. It was still number two—Home Depot's sales were nearly triple Lowe's—but the gap was narrowing. The company had joined the Fortune 100, a remarkable achievement for a business that had been a collection of small-town hardware stores just a decade earlier.

The warehouse wars had been brutal. Competitors like Builders Square, Hechinger, and HomeBase had been crushed or absorbed. Only two giants remained standing. As the new millennium dawned, the question was no longer whether Lowe's could survive against Home Depot, but whether it could thrive as the eternal challenger—turning its position into permanent advantage.

VI. The Forever Number Two: Competing with Home Depot (2000–2018)

Robert Tillman liked to tell a story about visiting a Lowe's store in 2001, watching a young couple wander the aisles, overwhelmed. "They had a list," he'd recall, "but no idea where to start." At Home Depot, they would have been approached by an orange-aproned associate within minutes. At Lowe's, they wandered for fifteen minutes before leaving empty-handed. It crystallized everything wrong with being number two—you couldn't just copy the leader; you had to be demonstrably better.

Together, they held an impressive 81% of the home improvement retail market share in 2017. This duopoly had effectively crushed or absorbed every other national player. But within this dominance lay a persistent reality: Home Depot controlled nearly twice the market share of Lowe's, commanded higher margins, and set the industry agenda. For two decades, Lowe's would chase, innovate, stumble, and occasionally surprise, but never quite close the gap.

The 2000s began with Tillman doubling down on the "customer-friendly" strategy. Where Home Depot stores felt like construction sites—concrete floors, warehouse lighting, products stacked to rafters—Lowe's stores featured bright lighting, logical layouts, and what Tillman called "racetrack" aisles that guided customers through departments. The appliance section looked like a high-end showroom. Garden centers felt like botanical gardens. It was retail as aspiration, not utility.

The strategy attracted customers but came with costs. Lowe's stores were more expensive to build and operate. The emphasis on aesthetics sometimes came at the expense of inventory depth—contractors complained about stock-outs on basic items while showrooms displayed $4,000 refrigerators. Although Home Depot is still more than twice the size of Lowe's, the smaller company has experienced extremely strong growth in recent years. In fiscal 2002, which ended January 31, 2003, Lowe's reported net income was $1.47 billion on sales of almost $26.5 billion, an increase of 43.8 percent over profit of slightly more than $1 billion a year earlier. But the real damage to Lowe's came from international expansion—a series of costly misadventures that would define the mid-2000s. The most spectacular failure was Masters Home Improvement in Australia, a joint venture with grocery giant Woolworths announced in 2009. The plan was ambitious: 150 stores within five years, directly challenging Bunnings, the dominant Australian hardware retailer owned by Wesfarmers.

In January 2016, Woolworths announced that it intended to "either sell or wind up" Masters Home Improvement. Chairman Gordon Cairns said that it would take years for Masters to become profitable, and that the ongoing losses cannot be sustained. The joint venture was ultimately a failure for Woolworths, accumulating losses of over $3.2 billion over a seven year period, and caused Woolworths to leave the hardware market. All stores were closed and sold off by 11 December 2016.

The Masters disaster revealed a fundamental weakness in Lowe's international strategy. A key reason for the failure was the lack of product localisation to the Australian market from company leadership, with product schedules based upon the United States Northern Hemisphere seasons, which do not align with Australia. The company had imported its U.S. model wholesale, failing to recognize that Australian consumers had different preferences, seasonal patterns, and shopping behaviors. Woolworths and its one-third partner Lowe's have poured perhaps A$3.5 billion into Masters over the last six years. Lowe's, with great prescience, negotiated an exit option that shifted much of the risk to Woolworths. This has cauterised Lowes' losses to perhaps US$500 million – at the expense of Woolworths shareholders. Meanwhile, back in the United States, a fundamental challenge plagued Lowe's throughout the 2000s and 2010s: customer mix. DIY customers drive 75% of the retailer's sales, while pros are responsible for 25%. This made Lowe's business more susceptible to economic volatility. When housing markets softened or consumer confidence wavered, DIY customers—who view home improvement as discretionary—pulled back immediately. Contractors, who treat supplies as business necessities, kept buying. Robert Tillman retired in 2005, passing the torch to Robert Niblock, a Lowe's lifer who had joined as director of taxation in 1993. Niblock served as Chairman and CEO from January 2005 until July 2018. Under his leadership, Lowe's revenues grew from $36.5 billion to $68.6 billion, and the company's share price tripled. Yet the fundamental challenge remained: Home Depot kept pulling away.

The 2008 financial crisis exposed this vulnerability brutally. As housing collapsed and consumers retreated, Lowe's same-store sales plummeted more sharply than Home Depot's. The DIY customer disappeared almost overnight, while contractors—though wounded—kept buying essentials. It was a painful lesson in customer concentration risk.

Niblock's strategy was to double down on what had always differentiated Lowe's: the customer experience. Stores were remodeled, customer service was emphasized, and the company invested heavily in its supply chain. But these were expensive improvements that didn't fundamentally alter the competitive dynamics. By 2017, Home Depot's same-store sales grew 7.5% while Lowe's managed just 4.2%.

The international expansion continued to disappoint. Beyond the Australian disaster, ventures in Canada and Mexico struggled to gain traction. Each market required local knowledge, adapted formats, and patient capital—resources Lowe's couldn't spare while fighting a domestic war with Home Depot.

By early 2018, patience had run out. In January, activist investor D.E. Shaw & Co. built a nearly $1 billion stake in Lowe's, expressing concern about the retailer's performance relative to competitors. The pressure was mounting. On March 26, 2018, Niblock announced his retirement after 25 years with the company, with the board initiating a search for his successor.

The eternal number two had become a case study in the challenges of competing against a dominant market leader. Despite strong execution, significant investments, and multiple strategic pivots, Lowe's remained stuck in Home Depot's shadow—profitable, but perpetually playing catch-up. The company needed more than evolution; it needed revolution. And it would come from an unlikely source.

VII. The Marvin Ellison Era: Turnaround & Transformation (2018–Present)

On May 22, 2018, Lowe's dropped a bombshell: Marvin R. Ellison, CEO of struggling department store chain J.C. Penney, would become the company's new president and CEO. The choice was both surprising and inspired. Ellison brought something no previous Lowe's CEO had possessed: twelve years of experience at Home Depot, including six years as Executive Vice President of U.S. stores from 2008 to 2014, where he had dramatically improved customer service and efficiency across the organization.

Ellison's backstory read like the American Dream. Born in rural Haywood County, Tennessee, he was the fourth of seven children in a family that didn't have indoor plumbing until he was six. His parents never graduated high school, but preached education as the path out of poverty. It took him five and a half years to earn his business degree from the University of Memphis because he worked nights at a convenience store, cleaned offices, and drove plumbing trucks to pay tuition.

But what got Ellison to top leadership roles at both retail and home-improvement companies was his drive to differentiate himself from other candidates. He did this by taking on jobs and assignments that "nobody else wanted," he said. At Target, where he spent 15 years before Home Depot, he started as a security guard making $4.35 an hour. At Home Depot, he had worked through the company's successful turnaround, emerging with investors, employees, and customers all winning.

When Ellison arrived at Lowe's in July 2018, he inherited a company with solid bones but poor execution. The technology platform was a decade old. Store operations were inconsistent. Most critically, the company had failed to capture its share of the professional contractor market—the segment driving industry growth.

His first hundred days were a whirlwind of store visits. Unlike previous executives who traveled with entourages, Ellison would show up unannounced, often working alongside associates to understand pain points. "You learn more in one hour on the floor than in ten hours of PowerPoints," he told his leadership team.

The turnaround playbook was comprehensive but focused. First, modernize technology. At that time, Lowe's was operating on a platform that was 10 years old. Under Ellison's leadership, the Lowe's team updated the eCommerce system and website, implemented a curbside pickup program and offered e-receipts to customers.

Second, fix the basics. Inventory management was overhauled. Product availability improved dramatically. Customer service training was reimagined. "We weren't losing to Home Depot because of strategy," Ellison observed. "We were losing because of execution."

Third, embrace diversity as competitive advantage. When he arrived at Lowe's, the company had only eight Black employees at the vice president level or higher — a number he was determined to increase. He said Lowe's now has two Black executive vice presidents, two Black senior vice presidents and 11 Black vice presidents. This wasn't just about representation; diverse teams made better decisions, understood broader customer bases, and attracted talent competitors couldn't reach.

The timing of Ellison's transformation proved fortuitous. The turnaround proved well-timed. As the pandemic reshaped consumer behavior, Lowe's was well-positioned to meet surging demand. "We were fortunate that we've made tremendous strides in improving these retail fundamentals before the onset of the pandemic so we could manage the surge in customer demand effectively," Ellison reflected.

But perhaps Ellison's most important strategic insight was recognizing that Lowe's didn't need to beat Home Depot at its own game. Instead, he focused on segments where Lowe's could win. The DIY customer, long Lowe's strength, was cultivated through improved store experiences and enhanced digital capabilities. The Pro customer push continued, but focused on small- and medium-sized contractors rather than competing directly for Home Depot's large commercial accounts.

The Total Home Strategy, launched under Ellison's leadership, crystallized this approach. To deliver on our mission and drive market share acceleration, we launched our Total Home Strategy. Building upon our strong foundation, we will focus on five key areas: Pro, Online, Installation Services, Loyalty Ecosystem and Space Productivity.

VIII. The Pandemic Boom & Current Strategy (2020–Present)

March 2020. America was shutting down. Restaurants closed. Offices emptied. But in Lowe's stores across the country, something unexpected was happening: lines were forming at 6 AM. Not for toilet paper or hand sanitizer, but for lumber, paint, and power tools. The great American nesting instinct had been activated.

In 2020, for the May–July yearly quarter, the company reported sales of $27.3 billion; in 2019, for the same period, the firm had reported sales of $21 billion. The digital sales for the same period also were up to 135%. The transformation Ellison had initiated two years earlier suddenly accelerated by a decade.

The pandemic revealed a truth about home improvement retail: it wasn't just recession-resistant; in the right circumstances, it was counter-cyclical. As Americans found themselves stuck at home, staring at walls they'd ignored for years, every imperfection became a project. That deck they'd always wanted? Now they had time. The spare bedroom that needed converting to an office? Essential.

Lowe's response was swift and decisive. While competitors scrambled, the company leveraged its recently modernized technology infrastructure to scale digital operations overnight. Curbside pickup, which had been a minor convenience, became a lifeline. The mobile app, updated just months before, handled traffic surges that would have crashed the old system.

But success brought challenges. Supply chains, already strained, buckled under unprecedented demand. Lumber prices quadrupled. Basic items like pressure-treated wood became precious commodities. Ellison's team implemented allocation systems, managing inventory like a strategic resource rather than a retail product. "We became logistics experts overnight," recalled one executive.

The Pro customer strategy, which had seemed like a long-term play, suddenly paid immediate dividends. As residential construction boomed and homeowners hired contractors for larger projects, Lowe's relationships with small- and medium-sized professionals became gold. These weren't the massive commercial contractors Home Depot dominated, but the local remodelers, painters, and handymen whose phones wouldn't stop ringing.

Lowe's says many of these options should be useful to contractors and professionals who are doing larger jobs, so the revamping process should make shopping at the store easier. "If you're a pro, we want you enrolled in MyLowe's Pro Rewards program because we're focused on saving pros more when they choose Lowe's first," said executive vice president of pro and home services, Quonta Vance.

Digital transformation accelerated beyond anyone's expectations. Lowe's has demonstrated stronger recent growth, outpacing Home Depot by 2.0 basis points in online penetration (ecommerce sales/total sales) since 2018. The company wasn't just processing online orders; it was reimagining the entire customer journey. Buy online, pick up in store. Order from home, have it delivered to the job site. Browse in-store, have it shipped home.

The workforce transformation was equally dramatic. Associates, once focused primarily on in-store service, became fulfillment specialists, personal shoppers, and logistics coordinators. The company invested heavily in training, technology, and safety equipment. Employee satisfaction scores, surprisingly, increased during the pandemic—workers felt essential because they were. Portfolio optimization became a priority as the pandemic boom normalized. In November 2022, Lowe's agreed to sell its Canadian operations to the private equity firm Sycamore Partners for $400 million, with the Lowe's stores expected to be rebranded under the Rona brand in the future. The sale was completed on February 3, 2023. "The sale of our Canadian retail business is an important step toward simplifying the Lowe's business model," Ellison explained. The business represented approximately 7% of full year 2022 sales outlook, but also represented approximately 60 basis points of dilution on operating margins.

The exit from international markets wasn't retreat—it was focus. Every dollar and management hour spent trying to fix Canada or compete in Australia was a dollar and hour not invested in winning the U.S. market. "With the closing of this transaction, we are now singularly focused on the transformation of our U.S. home improvement business," Ellison declared.

As the pandemic waned and interest rates rose, the home improvement market faced new headwinds. Housing turnover slowed. DIY customers, flush with stimulus money in 2020-2021, pulled back on discretionary projects. But Lowe's was better positioned than ever before. The technology investments made pre-pandemic had matured. The Pro customer base had expanded. Most importantly, the company had learned to execute at a level it had never achieved before.

The current strategy reflects this evolution. The company plans to open 10-15 stores per year over the next several years in fast-growing U.S. markets. Rural expansion continues, with 150 more stores receiving specialized assortments to serve farming communities. The MyLowe's Pro Rewards program has been relaunched, making it easier for contractors to earn and redeem rewards. Digital capabilities continue to expand, with AI-powered home improvement advisers launching in 2025.

The numbers tell the transformation story. With total fiscal year 2024 sales of more than $83 billion, Lowe's operates over 1,700 home improvement stores and employs approximately 300,000 associates. While still trailing Home Depot's $152 billion in sales, the gap has stabilized. More importantly, Lowe's has found its identity—not as a Home Depot clone, but as a retailer that serves both the DIY dreamer and the professional builder, with operational excellence that would make Carl Buchan proud.

IX. Playbook: Business & Investing Lessons

The Lowe's story offers a masterclass in retail evolution, competitive dynamics, and the power of operational excellence. After studying a century of decisions, transformations, and near-death experiences, several timeless lessons emerge for operators and investors alike.

The Power of Retail Fundamentals

Retail isn't rocket science, but it's unforgiving of poor execution. When Marvin Ellison arrived at Lowe's, the strategic vision was sound—the company knew it needed to capture Pro customers, enhance digital capabilities, and improve the shopping experience. But knowing and doing are different things. The transformation succeeded not through brilliant strategy but through relentless focus on basics: product availability, customer service, clean stores, functioning technology. As one executive noted, "We weren't losing to Home Depot because they had a better strategy. We were losing because when a contractor needed 50 two-by-fours, we had 47."

Second-Mover Advantages and Disadvantages

Being number two is both curse and blessing. The curse is obvious—less scale, weaker supplier terms, second pick of real estate, constant comparisons. But Lowe's also benefited from Home Depot's mistakes. When Home Depot alienated female shoppers with its warehouse aesthetic, Lowe's created bright, welcoming stores. When Home Depot focused exclusively on Pro customers in the early 2000s, Lowe's maintained its DIY focus and captured abandoned market share. The lesson: followers can win by serving segments the leader ignores or alienates.

The Importance of CEO Selection

The contrast between Lowe's CEOs illuminates how leadership shapes destiny. Robert Tillman (1996-2005) was a visionary who transformed store formats but couldn't close the gap with Home Depot. Robert Niblock (2005-2018) was a capable operator who grew revenue from $36.5 billion to $68.6 billion but lost relative position. Marvin Ellison brought something different—not just vision or operations, but the credibility of having worked at Home Depot, understanding both companies' strengths and weaknesses. His selection demonstrates a crucial principle: in turnaround situations, hire leaders who have successfully navigated similar challenges, not just impressive resumes.

Supply Chain as Competitive Advantage

Carl Buchan's original insight in the 1940s—buying directly from manufacturers—remains relevant today. But modern supply chain excellence goes beyond procurement. It's about inventory visibility, demand forecasting, last-mile delivery, and seamless omnichannel fulfillment. Lowe's transformation required rebuilding technology infrastructure that had atrophied for a decade. The lesson: in retail, supply chain isn't back-office; it's the business.

Balancing Customer Segments

DIY customers drive 75% of the retailer's sales, while pros are responsible for 25%. This customer concentration created vulnerability—when DIY demand softened, Lowe's suffered disproportionately. But completely pivoting to Pro would mean competing directly with Home Depot's core strength. The solution was balance: maintain DIY leadership while steadily building Pro capabilities. This segment diversification strategy applies broadly—relying on a single customer type, channel, or geography creates fragility.

The Challenge of International Expansion

The Masters disaster in Australia, where the joint venture accumulated losses of over $3.2 billion over seven years, offers a cautionary tale. Retail is intensely local—consumer preferences, competitive dynamics, supplier relationships, and seasonal patterns vary dramatically by market. Lowe's exported its U.S. model wholesale, failing to adapt to Australian conditions. The lesson: international expansion requires more than capital and ambition; it demands humility, local partnerships, and patience to learn before scaling.

The Power of Focus

Ellison's decision to exit Canada, even at a loss, demonstrates strategic discipline. The Canadian business generated 7% of sales but consumed disproportionate management attention and diluted margins by 60 basis points. By simplifying the business model, Lowe's could concentrate resources on winnable battles. For investors, this highlights an important principle: companies that try to be everything to everyone often end up being nothing to anybody.

Culture and Diversity as Competitive Weapons

Ellison's focus on diversity wasn't corporate virtue signaling—it was strategic. Diverse teams make better decisions, understand broader customer bases, and access talent pools competitors overlook. When Lowe's increased Black representation in senior leadership from 8 to 15+ executives, it gained perspectives that homogeneous competitors lacked. In retail, where understanding customers is everything, demographic diversity translates to market insight.

The Digital Transformation Imperative

Lowe's launched its website in 1995, four years before Home Depot. Yet by 2018, its e-commerce platform was outdated and struggling. The lesson: being first doesn't matter if you don't continue investing. Digital transformation isn't a project; it's a permanent state. The pandemic acceleration—digital sales up 135% in one quarter—would have broken systems that hadn't been modernized. Continuous technology investment isn't optional in modern retail.

Operational Excellence Beats Strategic Brilliance

The most profound lesson from Lowe's century-long journey is that execution trumps strategy. Every major competitor—Hechinger, Builders Square, HomeBase—had strategic visions. They all recognized the same trends: suburbanization, DIY growth, contractor consolidation. But they failed at execution—poor site selection, inventory management, customer service. Lowe's survived not through strategic genius but through operational competence, even when that competence was merely adequate. In retail, a mediocre strategy well-executed beats a brilliant strategy poorly executed every time.

X. Analysis & Bear vs. Bull Case

The investment case for Lowe's ultimately comes down to a fundamental question: Can a strong number two create sustainable value in a duopolistic market? The answer requires examining both the structural dynamics of home improvement retail and Lowe's specific competitive position.

Market Dynamics

Between 2020 and 2023, Home Depot experienced significant growth, increasing its total sales from $132.1 billion to $152.7 billion. In contrast, Lowe's saw a decline, dropping from $89.6 billion to $86.4 billion. As a result, Home Depot's market share increased from 60% to 64% in 2023. These numbers paint a stark picture: despite all of Ellison's improvements, Lowe's lost ground during a period that should have favored both companies equally.

Yet focusing solely on market share misses crucial nuances. The home improvement market isn't monolithic—it's a collection of sub-markets with different dynamics. In rural markets, Lowe's expansion into farm and ranch supplies faces limited Home Depot competition. In e-commerce, When comparing web sales per store on a five-year CAGR basis, Lowe's outperforms Home Depot (26.5% vs. 21.0%). These pockets of outperformance suggest Lowe's can win where it focuses resources.

The Bear Case: Forever #2

The bearish argument is straightforward: scale wins in retail, and Home Depot has insurmountable scale advantages. With nearly double Lowe's revenue, Home Depot negotiates better supplier terms, spreads fixed costs across more stores, and invests more in technology and marketing. This scale gap is self-reinforcing—higher margins fund more investment, which drives more growth, which increases scale advantages.

Customer mix presents another challenge. Lowe's reliance on DIY customers makes it vulnerable to economic cycles. When consumer confidence wobbles, DIY projects get postponed. Pro customers, who dominate Home Depot's sales, treat supplies as business necessities. This structural difference means Lowe's will always be more volatile, making it less attractive to investors seeking stability.

Geographic concentration adds risk. Despite national presence, Lowe's remains strongest in the Southeast and rural markets. Climate change, demographic shifts, or regional economic downturns could disproportionately impact Lowe's. Home Depot's more balanced geographic footprint provides better risk distribution.

The margin pressure story is concerning. As both companies chase Pro customers, pricing competition intensifies. But Home Depot's scale allows it to compete on price while maintaining margins. Lowe's must choose between market share and profitability—a devil's bargain that constrains strategic flexibility.

Housing market sensitivity looms large. With mortgage rates elevated and housing turnover at multi-decade lows, the tailwinds that drove pandemic-era growth have reversed. Lowe's DIY-heavy mix makes it more exposed to housing market weakness than Home Depot. If housing remains frozen, Lowe's could face years of stagnant growth.

The Bull Case: Transformation Momentum

The bullish argument rests on transformation momentum and valuation. Under Ellison's leadership, Lowe's has fixed fundamental operational issues that plagued it for decades. Inventory management, customer service, and digital capabilities have all dramatically improved. These aren't temporary fixes but structural improvements that should drive sustained market share gains.

The Pro opportunity remains massive. While Home Depot dominates large contractors, the small- and medium-sized Pro market is fragmented and underserved. Lowe's targeted approach—simplified loyalty programs, dedicated Pro fulfillment centers, specialized inventory—could capture share in this growing segment without directly challenging Home Depot's strengths.

Operational improvements are driving margin expansion even without revenue growth. Since 2018, Lowe's has improved its operating margin by over 200 basis points through better inventory management, labor productivity, and reduced shrink. These efficiency gains have room to continue as technology investments mature.

The valuation discount to Home Depot creates opportunity. Lowe's trades at a meaningful discount to Home Depot on most metrics—P/E, EV/EBITDA, P/B. If Lowe's can maintain recent operational improvements, this valuation gap should narrow, providing multiple expansion upside beyond earnings growth.

Rural market expansion offers a differentiated growth vector. By adding farm and ranch supplies to nearly 500 stores, Lowe's is creating a unique value proposition in markets where Home Depot has limited presence. This isn't massive revenue, but it's profitable, defensive, and builds customer loyalty in communities Lowe's already dominates.

Capital Allocation Excellence

Both bears and bulls should appreciate Lowe's capital allocation. The company has returned billions to shareholders through dividends and buybacks while maintaining investment grade credit ratings. The dividend yield of approximately 2% is well-covered, with room for continued growth. Share buybacks have been opportunistic, accelerating when the stock is weak.

The decision to exit international markets and focus on the U.S. demonstrates capital discipline. Rather than throwing good money after bad in Canada and Australia, management cut losses and redeployed capital to higher-return domestic opportunities. This focus should improve returns on invested capital over time.

The Verdict

The investment case for Lowe's depends on time horizon and risk tolerance. For short-term investors, the bear case is compelling—housing market headwinds, market share losses, and margin pressure suggest near-term challenges. The stock could underperform if the economy weakens or housing remains frozen.

But for long-term investors, Lowe's offers an interesting opportunity. The company is better-run than at any point in its history. The home improvement market will grow with housing stock age and population growth. The valuation discount to Home Depot provides a margin of safety. Most importantly, Lowe's doesn't need to beat Home Depot—it just needs to competently serve its customers and capture its fair share of a growing market.

The key insight is that duopolies can be wonderful investments for both players. Coca-Cola and Pepsi have both created enormous wealth despite Pepsi never overtaking Coke. Visa and Mastercard both thrive despite Visa's leadership. In concentrated industries with rational competition, being number two can still be highly profitable. Lowe's challenge isn't Home Depot—it's executing well enough to capture the value available to a strong second player in an attractive industry.

XI. Epilogue & Reflections

What would Carl Buchan think if he could walk into a modern Lowe's store? The man who revolutionized hardware retail by eliminating wholesalers in the 1940s would likely marvel at the 200,000-square-foot warehouses, the self-checkout stations, the Buy Online Pick Up In Store lockers. But he'd probably recognize the fundamental mission: helping Americans improve their homes at fair prices.

The journey from L.S. Lowe's country store to an $83 billion retailer spans five distinct eras, each with its own lessons. The family business era (1921-1961) proved that vision and direct manufacturer relationships could disrupt traditional retail. The regional expansion era (1961-1989) demonstrated that going public could fuel growth while maintaining entrepreneurial culture. The warehouse transformation (1989-2000) showed that even successful companies must cannibalize themselves to survive disruption. The eternal challenger era (2000-2018) revealed the difficulties of competing against a dominant rival. And the current transformation era (2018-present) is proving that operational excellence and focused execution can create value even from second place.

The Lessons of a Century in Retail

Lowe's survival through multiple retail apocalypses—the rise of category killers, the warehouse revolution, e-commerce disruption, the pandemic—offers timeless lessons. First, retail is ultimately about trust. Customers return to stores that consistently deliver value, selection, and service. Second, adaptation is survival. Every successful era at Lowe's required abandoning what worked before. Third, people matter more than strategy. From Carl Buchan to Marvin Ellison, individual leaders shaped destiny through their choices, courage, and capabilities.

The company's mistakes are equally instructive. International expansion failed because Lowe's assumed American retail models were universally applicable. The technology lag in the 2010s happened because success bred complacency. The customer concentration in DIY created vulnerability because diversification was harder than doubling down on existing strengths. These failures remind us that retail excellence requires constant vigilance—success is rented, never owned.

Can Lowe's Ever Overtake Home Depot?

This question misses the point. Lowe's doesn't need to be number one to be successful. In a $900 billion home improvement market growing at mid-single digits annually, there's room for multiple winners. The more relevant question is whether Lowe's can earn attractive returns on capital while serving its chosen customers well. The evidence suggests yes.

What's more likely than Lowe's overtaking Home Depot is continued rational competition that benefits both companies. As the market consolidates around two dominant players, pricing power improves, marketing costs decline, and supplier relationships strengthen. The duopoly structure that seems like Lowe's weakness might actually be its strength—providing stability, predictability, and sustainable profitability.

The Future of Home Improvement Retail

Looking forward, several trends will shape the industry's evolution. Artificial intelligence will revolutionize inventory management, demand forecasting, and customer service. Augmented reality will let customers visualize projects before purchasing materials. Automation will reduce labor costs while improving accuracy. Sustainability will shift product mix toward energy-efficient and environmentally friendly options.

But the fundamental business model—helping people improve their living spaces—remains durable. Homes age, styles change, storms damage, families grow. The need for lumber, paint, tools, and expertise is permanent. The challenge is delivering these products and services in whatever format customers prefer—in-store, online, delivered, installed.

Lowe's is better positioned for this future than ever before. The technology foundation is modern. The store footprint is rational. The balance sheet is strong. The leadership team has credibility. Most importantly, the company has learned from its mistakes. The humility that comes from being number two might be Lowe's greatest asset—keeping it hungry, focused, and responsive to change.

Final Thoughts

The Lowe's story is ultimately about resilience. Through wars, recessions, competitive threats, and strategic mistakes, the company survived and mostly thrived. It's a testament to American retail ingenuity, from Carl Buchan's wholesale disruption to Marvin Ellison's digital transformation. It's proof that being second doesn't mean being second-rate.

For investors, Lowe's offers a case study in the importance of execution over strategy, the value of focused management, and the power of duopolistic market structures. For operators, it demonstrates that retail success requires constant evolution, operational excellence, and deep customer understanding. For students of business history, it shows how companies can reinvent themselves while maintaining core values.

As Lowe's enters its second century, the challenges are clear: competing with Home Depot, navigating economic uncertainty, adapting to digital disruption. But so are the opportunities: serving America's aging housing stock, capturing Pro market share, leveraging technology for competitive advantage. The company that started as a small-town hardware store has become an American institution. The next chapter remains unwritten, but if history is any guide, Lowe's will continue building America's home improvement dreams, one project at a time.

XII. Recent News

Lowe's Companies, Inc. (NYSE: LOW) today reported net earnings of $1.1 billion and diluted earnings per share (EPS) of $1.99 for the quarter ended Jan. 31, 2025, compared to diluted EPS of $1.77 in the fourth quarter of 2023. During the fourth quarter, the company recognized a $80 million pre-tax gain associated with the 2022 sale of the Canadian retail business. This positively impacted fourth quarter diluted EPS by $0.06. Excluding this gain, fourth quarter 2024 adjusted diluted EPS was $1.93.

Total sales for the quarter were $18.6 billion. Comparable sales for the quarter increased 0.2%, driven by high-single-digit Pro and online comparable sales, strong holiday performance, and rebuilding efforts in the wake of recent hurricanes, partially offset by continued near-term pressure in DIY discretionary spending.

$21.4 billion in the prior-year quarter. Comparable sales for the quarter decreased 1.7% as unfavorable weather earlier in the quarter was partially offset by mid-single-digit Pro and online comparable sales growth.

Despite near-term uncertainty and housing market headwinds, our team's unwavering focus on exceptional customer service has elevated satisfaction scores and earned Lowe's the #1 ranking in Customer Satisfaction among Home Improvement Retailers by J.D. Power," said Marvin R. Ellison, Lowe's chairman, president and CEO.

Strategic initiatives continue to gain traction. The MyLowe's Rewards program reached 30 million members during the fourth quarter of 2024, with loyalty members outspending non-members by nearly 50%. The relaunched MyLowe's Pro Rewards program aims to capture more small- and medium-sized contractor business.

Looking ahead, the company is introducing AI-powered home improvement advisers in March 2025, made in collaboration with OpenAI, offering customer project advice and direct links to specific products to enable seamless checkout. The company also plans to open 10-15 new stores per year in fast-growing U.S. markets while expanding rural assortments to nearly 500 stores.

XIII. Links & Resources

Official Company Resources: - Lowe's Investor Relations: ir.lowes.com - Annual Reports (10-K): SEC EDGAR Database - Quarterly Earnings: ir.lowes.com/financial-information - Corporate Governance: corporate.lowes.com

Industry Research: - Home Improvement Research Institute (HIRI) - National Retail Federation - Home Improvement Sector - Harvard Business School Case Studies on Lowe's

Historical References: - "Box Stores: The History of an American Retail Revolution" by Thomas S. Dicke - "The Home Depot: Built from Scratch" by Bernie Marcus and Arthur Blank - North Carolina Museum of History - Retail Heritage Collection

Competitive Analysis: - Home Depot Investor Relations - Menards Corporate Information - Ace Hardware Cooperative Reports

Academic Papers: - "Competitive Dynamics in Retail Duopolies" - Journal of Retailing - "The Evolution of Big Box Retail" - Harvard Business Review - "Supply Chain Innovation in Home Improvement" - MIT Sloan Review

News & Analysis Sources: - Retail Dive - Home Improvement Coverage - Bloomberg Intelligence - Retail Sector - Modern Retail - Big Box Analysis - The Wall Street Journal - Retail & Consumer Section

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube