JSW Steel: India's Industrial Transformation Story

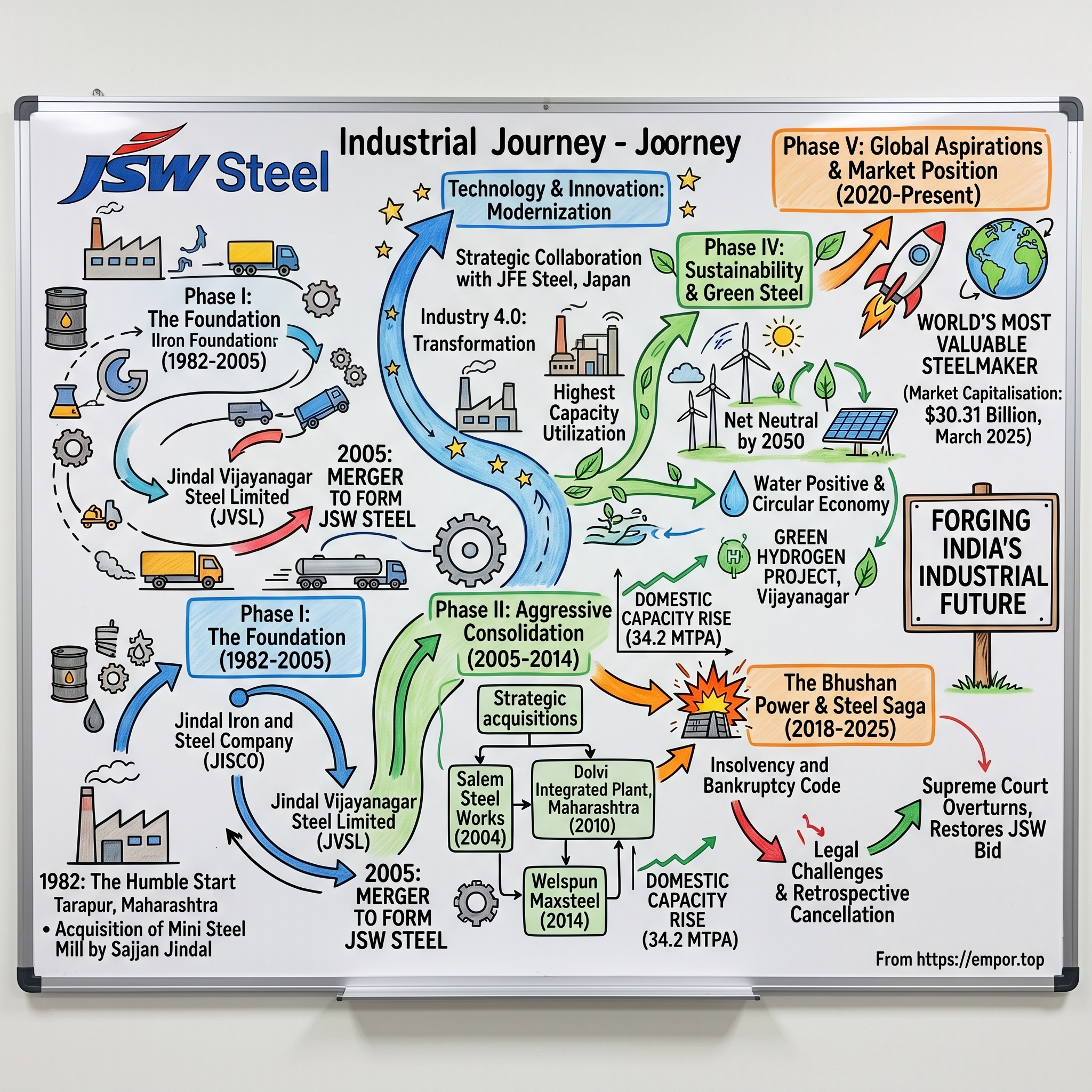

The monsoon winds whipped across the Arabian Sea on a humid March evening in 1982, as trucks rolled into a small re-rolling mill in Tarapur, Maharashtra. Few watching that modest acquisition by a young mechanical engineer named Sajjan Jindal could have imagined they were witnessing the birth of what would become India's largest steelmaker with domestic capacity of 34.2 MTPA. The journey from that single mill to a ₹1,68,824 crore (US$20.0 billion) revenue giant reads like the industrial history of modern India itself—marked by audacious expansions, strategic acquisitions, bitter legal battles, and an unwavering belief that steel forms the backbone of a nation's ambitions.

The story of JSW Steel cannot be told without understanding the convergence of three transformative forces: India's economic liberalization in 1991, the breakup of the Jindal family empire in 2005, and the country's infrastructure-led growth model of the 2020s. Each phase demanded different strategies, different capabilities, and ultimately, different definitions of what it meant to be an Indian steel company competing on a global stage.

I. Introduction & Episode Roadmap

Picture the industrial landscape of India in 1982. The nation's steel production was dominated by public sector behemoths like SAIL, with private players relegated to the margins. Into this tightly controlled market stepped the Jindal Group, acquiring Piramal Steel Limited, which operated a mini steel mill at Tarapur in Maharashtra and renaming it Jindal Iron and Steel Company (JISCO). This wasn't just another business acquisition—it was the first move in what would become one of India's most remarkable industrial transformation stories.

Today, JSW Steel stands as an Indian multinational steel producer based in Mumbai and is a flagship company of the JSW Group. The company's transformation from a single re-rolling mill to becoming the country's largest private steel producer represents more than just corporate growth—it embodies India's own evolution from a controlled economy to an industrial powerhouse. With domestic capacity of 34.2 MTPA, JSW Steel has not merely grown; it has redefined what Indian steel companies can achieve.

The numbers tell only part of the story. For the financial year 2024-25, consolidated revenue stood at ₹1,68,824 crore (US$20.0 billion) and EBITDA at ₹22,904 crore (US$2.7 billion). But beneath these impressive figures lies a narrative of strategic bets, family dynamics, technological leaps, and occasionally, spectacular miscalculations. The company's journey encompasses the visionary leadership of the Jindal family, aggressive consolidation through M&A, international expansion attempts, and most dramatically, the controversial Bhushan Power acquisition that would test the very foundations of India's bankruptcy resolution framework.

What makes JSW Steel particularly fascinating for students of business strategy is how it navigated the unique challenges of building scale in a capital-intensive, cyclical industry within an emerging market context. The company had to master not just the technical complexities of steelmaking, but also the art of managing government relations, securing raw materials in a resource-constrained environment, timing capacity additions to market cycles, and more recently, preparing for a carbon-constrained future.

This deep dive will explore how JSW Steel engineered its rise through multiple phases: the foundational years under patriarch O.P. Jindal, the aggressive expansion under Sajjan Jindal's leadership, the strategic acquisitions that built national scale, the international ambitions that met mixed success, and the recent controversies that have tested the company's resilience. We'll examine the playbook that enabled JSW to expand capacities at a competitive capex per tonne compared to global benchmarks, while also confronting the challenges that continue to constrain Indian manufacturing on the global stage.

The episode structure ahead takes us through distinct eras, each marked by defining strategic choices. We begin with the Jindal dynasty's origins and the unique circumstances that positioned them to capitalize on India's steel opportunity. We trace the evolution from JISCO to JSW Steel, the consolidation plays that built a pan-India footprint, and the global ambitions that saw mixed results. The Bhushan Power saga receives special attention as a cautionary tale about the perils of distressed asset acquisition in India's evolving bankruptcy landscape. We conclude with an analysis of JSW's current market position, future challenges, and the lessons this journey offers for founders and investors navigating industrial businesses in emerging markets.

II. Origins: The Jindal Dynasty & India's Steel Ambitions

The story begins not with Sajjan Jindal, but with his father—O.P. Jindal, a politician and philanthropist from Hisar in Haryana. O.P. Jindal was a farmer's son who began with a small bucket-making unit in Hisar when he was just 22 before he set up Jindal India, a pipe-production unit, in 1964. This transition from agriculture to industry embodied the aspirations of post-independence India, where entrepreneurial energy sought outlets beyond traditional boundaries.

O.P. Jindal understood something fundamental about India's development trajectory: infrastructure would be the binding constraint on growth, and steel would be the binding constraint on infrastructure. While the public sector steel plants focused on large-scale integrated facilities, Jindal saw opportunity in the gaps—smaller, more nimble operations that could serve local markets and adapt quickly to changing demand patterns. His pipe manufacturing business wasn't just about making products; it was about understanding the entire value chain of steel, from procurement to processing to distribution.

The real turning point came in 1982. The JSW Group's foray into steel manufacturing began in 1982, when it set up the Jindal Iron and Steel Company with its first steel plant at Vasind near Mumbai. This wasn't merely geographic expansion—it was a strategic repositioning. Mumbai represented access to ports, proximity to India's commercial capital, and critically, exposure to more sophisticated industrial customers who would push the company to improve quality and capabilities.

What distinguished the Jindal approach from other industrial families of that era was their willingness to embrace technical partnerships and modern management practices while maintaining family control. They understood that competing in steel required more than capital—it demanded operational excellence, technological sophistication, and the ability to manage complex stakeholder relationships. The Vasind plant became a training ground where the next generation would learn not just steelmaking, but the art of building industrial enterprises in India's complex business environment.

The 1991 economic liberalization changed everything. Suddenly, Indian companies could import technology, access foreign capital, and most importantly, expand without seeking endless government permissions. For the Jindals, who had spent a decade building capabilities in a constrained environment, liberalization was like oxygen to a flame. They could now think bigger, move faster, and compete more aggressively.

But the real masterstroke was yet to come. In 1994, Jindal Vijayanagar Steel Limited (JVSL) was established. Situated at Toranagallu in the Bellary–Hospet region of Karnataka, this plant strategically positioned itself in the heart of the high–grade iron ore belt, sprawling across 3,700 acres of land. This wasn't just another plant—it was a statement of intent. The Vijayanagar location offered proximity to iron ore, access to ports on both coasts, and the space to build at a scale that could compete globally.

The vision for Vijayanagar went beyond traditional Indian steel plants. The Jindals wanted to build something that could match the best facilities globally—in scale, in technology, and in efficiency. They brought in international consultants, invested in state-of-the-art equipment, and critically, focused on building a culture of continuous improvement. The plant would eventually become the largest single-location steel manufacturing unit across India.

By the early 2000s, the Jindal steel operations had reached a critical inflection point. They had proven they could build and operate world-class facilities, they had established strong relationships with customers across segments, and they had developed deep expertise in navigating India's complex regulatory environment. But to truly capitalize on India's emerging growth story, they needed scale—and that would require a fundamental restructuring of the family's business empire.

III. Building the Foundation: JISCO to JSW Steel (1982-2005)

The transformation from a modest re-rolling mill to an integrated steel producer required more than just capital investment—it demanded a fundamental reimagination of what an Indian steel company could be. The period from 1982 to 2005 represents JSW's foundational era, where critical capabilities were built, strategic assets were assembled, and the vision for a national champion was crystallized.

The early days at Vasind were about learning the basics of steel processing, but Sajjan Jindal had bigger ambitions. In 1982, he joined the OP Jindal Group as a freshly graduated mechanical engineer from Bengaluru, and within a year he moved to Mumbai to look after the western region operations. In 1983–1984, Jindal's father, Om Prakash Jindal put him to the test by ordering him to turn around operations at two facilities near Mumbai. This trial by fire would shape his management philosophy—hands-on leadership, operational excellence, and the willingness to take calculated risks.

The Vasind plant evolved from basic re-rolling operations to more sophisticated downstream processing. Each expansion was carefully calibrated—adding just enough capacity to meet growing demand while maintaining high utilization rates. This disciplined approach to capital allocation would become a hallmark of JSW's strategy, distinguishing it from competitors who often built ahead of demand and suffered during downturns.

But the real game-changer was Vijayanagar. The decision to build in Karnataka's iron ore belt wasn't obvious—the location was remote, infrastructure was limited, and the state's political environment was complex. Yet Sajjan Jindal saw what others missed: the proximity to high-grade iron ore would provide a sustainable cost advantage, the available land would allow for future expansions, and the state government's development agenda aligned with JSW's growth plans.

The Vijayanagar project stretched JSW's financial and managerial resources to the limit. The company had to build not just a steel plant, but an entire ecosystem—roads, railways, water supply, power generation, and even townships for workers. The company built the world's largest conveyor system with the same objective, which travels ~24 km from the captive mines to the Vijayanagar plant. This conveyor system wasn't just an engineering marvel; it was a strategic moat that would provide cost advantages for decades.

Technology partnerships played a crucial role in this phase. Rather than trying to develop everything in-house, JSW actively sought collaborations with global leaders. It has a strategic collaboration with global leader JFE Steel of Japan, enabling JSW to access new and state-of-the-art technologies to produce & offer high-value special steel products to its customers. These partnerships brought more than just technology—they introduced global best practices in operations, quality control, and safety.

The period also saw JSW developing its unique approach to project execution. Unlike public sector companies that often faced massive delays and cost overruns, JSW developed a reputation for completing projects on time and within budget. This wasn't accidental—it reflected a culture of accountability, detailed planning, and most importantly, the ability to adapt quickly when things went wrong.

Meanwhile, the corporate structure was evolving. He promoted Jindal Iron and Steel Company Limited (JISCO), for manufacturing of Cold Rolled and Galvanized Sheet Products in 1989. He promoted Jindal Vijaynagar Steel Limited (JVSL), JSW Energy Limited (JSWEL), Jindal Praxair Oxygen Limited (JPOCL) and Vijaynagar Minerals Private Limited (VMPL) to ensure complete integration of the manufacturing progress in 1995. Each entity served a specific purpose, but the proliferation of companies was also creating complexity.

The early 2000s brought new challenges and opportunities. China's entry into the WTO in 2001 fundamentally altered global steel dynamics. Suddenly, Indian steel companies faced competition from Chinese imports while also seeing new export opportunities. JSW's response was to focus on product quality and customer relationships rather than competing solely on price. The company invested in developing special grades of steel, building technical service capabilities, and creating long-term partnerships with key customers.

The turning point came with a family tragedy and transformation. Even before the death of OP Jindal in a helicopter accident in 2005, the group's patriarch established a "division of business" framework. First, he gave Prithviraj, Sajjan, Ratan, and Naveen Jindal equal shares of the existing OP Jindal Group he had built up over the years. The patriarch's death could have triggered a destructive succession battle. Instead, the family's prior planning ensured a smooth transition, with each brother taking control of different verticals.

For Sajjan Jindal, this was the moment he had been preparing for his entire career. In 2005, his steel companies, JISCO, and JVSL, were merged to form JSW Steel, and a holding group of the same name. The merger wasn't just about corporate simplification—it was about creating an entity with the scale, resources, and ambition to compete nationally and eventually globally. The new JSW Steel combined JISCO's downstream capabilities with JVSL's upstream steel production, creating an integrated player with the flexibility to serve diverse market segments.

IV. The Consolidation Play: Strategic Acquisitions (2005-2014)

The formation of JSW Steel in 2005 marked the beginning of an aggressive consolidation strategy that would transform the company from a regional player into a national powerhouse. This wasn't consolidation for its own sake—each acquisition was carefully chosen to fill capability gaps, expand geographic reach, or secure strategic assets.

The first major move came even before the formal creation of JSW Steel. In 2004, JSW made a strategic move by acquiring Salem Steel Works, adding to its portfolio. Salem wasn't just another steel plant—it specialized in stainless steel and special alloys, products that commanded premium prices and served sophisticated applications. The acquisition demonstrated JSW's ambition to move up the value chain, competing not just on volume but on technical capability.

The real consolidation opportunity emerged from India's infrastructure boom of the mid-2000s. The economy was growing at 8-9% annually, driving unprecedented demand for steel. But many smaller players lacked the capital or capabilities to expand. For JSW, with its strong balance sheet and operational expertise, this created a buyer's market for strategic assets.

The acquisition of an integrated steel plant at Dolvi, Maharashtra, in 2010 added to their steel production portfolio. The Dolvi acquisition was transformational—it gave JSW a major presence in Western India, closer to key consumption centers and ports. The plant came with modern equipment and established customer relationships, but more importantly, it had expansion potential. JSW would eventually transform Dolvi into one of India's most efficient steel complexes.

The acquisition strategy wasn't limited to buying distressed assets. JSW also pursued brownfield expansions at existing locations, which offered better returns than greenfield projects. The company developed a systematic approach to acquisitions: identify underperforming assets with good bones, negotiate hard on price, invest in modernization, and integrate quickly into the JSW system. This playbook would be refined through multiple transactions.

The acquisition of Welspun Maxsteel in 2014 marked as a diversification in the group's history. Welspun brought plate and coil manufacturing capabilities, expanding JSW's product portfolio into higher-value segments. The timing was crucial—India's infrastructure build-out was driving demand for heavy plates used in construction and industrial applications.

What distinguished JSW's consolidation strategy was the speed and effectiveness of integration. While many Indian conglomerates struggled to absorb acquisitions, JSW developed a systematic integration process. Key managers from successful plants were deployed to new acquisitions, best practices were transferred quickly, and cultural integration was prioritized. The company's young, professional management team—unusual for a family-owned Indian business—proved adept at managing this complexity.

The consolidation wasn't just about acquiring steel plants. JSW also moved to secure raw material sources, recognizing that access to iron ore and coal would become increasingly critical competitive advantages. The company participated in government auctions for mining licenses, formed joint ventures for coal imports, and invested in logistics infrastructure to ensure reliable supply chains.

But the consolidation strategy also had its challenges. Each acquisition brought legacy issues—environmental liabilities, labor disputes, technology gaps. JSW had to navigate India's complex regulatory environment, managing relationships with state governments, environmental agencies, and local communities. The company's ability to manage these stakeholders—what one executive called "the art of getting things done in India"—became a core competitive advantage.

The financial engineering behind these acquisitions was equally sophisticated. JSW pioneered the use of structured transactions in Indian steel, using special purpose vehicles to limit liability, accessing international debt markets for cheaper capital, and timing acquisitions to market cycles. The company's CFO, Seshagiri Rao, became legendary in Indian corporate circles for his ability to structure complex deals and maintain financial discipline even during aggressive expansion phases.

By 2014, JSW Steel had fundamentally transformed India's steel industry landscape. Through a combination of organic growth and strategic acquisitions, the company had built a diversified portfolio of assets across the value chain. It could produce everything from basic long products for construction to sophisticated coated steels for automotive applications. More importantly, it had demonstrated that Indian companies could be successful consolidators, challenging the conventional wisdom that only multinational corporations had this capability.

V. Global Ambitions: International Expansion (2008-2018)

As JSW Steel consolidated its position in India, the company's leadership began looking beyond national borders. The logic was compelling: to compete with global steel giants like ArcelorMittal and Nippon Steel, JSW needed international operations for raw material security, market access, and technological capabilities. The execution, however, would prove far more complex than anticipated.

The first international foray focused on securing raw materials. JSW Group ventured into a rebar joint venture in Georgia in 2008. But more significantly, JSW Steel made a key global acquisition by obtaining mining concessions in Chile in 2008, allowing JSW Steel to secure its raw material sources. Chile offered high-quality iron ore and a stable political environment, providing a hedge against potential supply disruptions in India.

The global financial crisis of 2008-09 temporarily halted international expansion, but it also created opportunities. Distressed assets in developed markets became available at attractive valuations. JSW's leadership saw a chance to acquire technology and market access that would have been impossible during boom times.

The United States became a key focus area. The American steel industry was undergoing consolidation, and JSW identified opportunities to enter through acquisitions rather than greenfield investments. The company acquired steel mills in Texas and Ohio, gaining a foothold in the world's second-largest economy. These weren't trophy assets—they were older facilities that needed investment and modernization. But JSW believed it could apply its low-cost operating model and technical expertise to transform these operations.

The U.S. expansion faced immediate challenges. American steel workers were skeptical of new foreign owners, especially from a country not known for steel exports. Environmental regulations were stricter than in India, requiring significant compliance investments. Most challenging was the market structure—unlike India's relationship-driven market, the U.S. steel market was highly commoditized with volatile pricing.

Europe presented different opportunities and challenges. In 2018, JSW Steel Italy acquired 100% shares of Aferpi S.p.A, Piombino Logistics, and 69.27% of GSI Lucchini S.p.A's share capital from Cevitaly S.r.l for €55 million. The Italian acquisition was strategic—it provided access to European markets and advanced steel-making technology. However, the complexity of Italian labor laws, the high cost structure, and the need for environmental investments made profitability elusive.

The most important international partnership came from Japan. In 2013, the group entered into a collaboration with Japan's JFE Holdings in the electrical steel sector. This wasn't just a commercial arrangement—it was a comprehensive technology transfer agreement that would fundamentally upgrade JSW's capabilities. JFE brought expertise in electrical steels used in power generation and transmission, a high-value segment where Indian capability was limited.

The international expansion strategy revealed both JSW's ambitions and limitations. The company discovered that operational excellence in India didn't automatically translate to success in developed markets. Labor productivity metrics that worked in India were irrelevant in unionized U.S. plants. The low-cost advantage that JSW enjoyed in India disappeared when competing against integrated global players with greater scale.

Raw material security—the original rationale for international expansion—proved more complex than expected. While JSW secured mining assets in Chile, Mozambique, and other countries, developing these resources required massive capital investments and long development timelines. The commodity price collapse of 2014-15 made some of these investments look premature, forcing write-downs and strategic reassessments.

Yet the international expansion wasn't a complete failure. It provided crucial learnings about global best practices, exposed JSW's management to different business models, and created options for future growth. The company developed capabilities in managing multi-currency operations, navigating different regulatory regimes, and serving sophisticated international customers. These capabilities would prove valuable as JSW competed for high-value domestic contracts against international suppliers.

The period also saw JSW beginning to think about sustainability and environmental issues more seriously. International operations, especially in Europe, exposed the company to carbon pricing, stringent environmental regulations, and customer demands for green steel. While these seemed like compliance burdens at the time, they prepared JSW for the sustainability challenges that would become central to the steel industry in the 2020s.

By 2018, JSW's international strategy had evolved from ambitious globalization to selective internationalization. The company pulled back from some overseas ventures, focusing on operations that either secured critical raw materials or provided access to technology and high-value markets. The U.S. operations were restructured to focus on specific product segments where JSW could compete effectively. The European presence was maintained primarily for market access and technology partnerships.

VI. The Bhushan Power Acquisition: Triumph to Tragedy (2018-2025)

No episode in JSW Steel's history better illustrates the opportunities and perils of Indian capitalism than the Bhushan Power and Steel Limited (BPSL) acquisition. What began as a bold move to acquire distressed assets through India's new bankruptcy framework would evolve into a legal nightmare that reached the highest levels of the Indian judiciary and raised fundamental questions about the rule of law in commercial disputes.

The opportunity emerged from India's banking crisis of the mid-2010s. Years of reckless lending had left Indian banks with massive non-performing assets, particularly in infrastructure and metal sectors. BPSL was among the 12 large cases referred to bankruptcy courts by the Reserve Bank of India in 2017. The company owed lenders Rs 48,000 crore. For JSW, this represented a once-in-a-generation opportunity to acquire substantial capacity at a fraction of replacement cost.

The strategic logic was compelling. BPSL's 3.5 million tonne steel plant in Jharsuguda, Odisha, would give JSW a major presence in Eastern India, a region dominated by Tata Steel and SAIL. The plant had modern equipment but had been mismanaged under its previous promoters. JSW believed it could quickly turn around operations through better management, working capital optimization, and integration with its existing operations.

The bidding process was intense. JSW's bid for the 3.5-million tonne steel plant trumped Tata Steel's Rs 16,000-crore offer. JSW Steel was chosen as the winning bidder for BPSL's assets in September 2019, and the resolution plan was approved by the National Company Law Tribunal soon after. The company offered to pay Rs 19,350 crore to the financial creditors, with the lenders taking a nearly 60% haircut.

But then the complications began. The Enforcement Directorate had attached BPSL's assets in connection with money laundering investigations against the former promoters. This created a unique situation—JSW had won the bid through a legal process, but another arm of the government was claiming the assets were proceeds of crime. The case wound its way through various courts, creating uncertainty that would last for years.

Despite the legal challenges, JSW proceeded with the acquisition. JSW Steel on Friday said it has paid Rs 19,350 crore to the financial creditors of Bhushan Power & Steel Ltd towards implementation of the resolution plan for acquiring the company. The payment was made in March 2021, marking the largest acquisition in the history of JSW Steel" said Chairman Sajjan Jindal in a letter to employees.

The initial years seemed to vindicate JSW's strategy. The company invested in upgrading BPSL's operations, improved capacity utilization, and integrated it into its national network. BPSL began contributing positively to JSW's consolidated financials, with analysts estimating it provided approximately 10% of JSW Steel's EBITDA. The acquisition seemed like a textbook case of value creation through operational improvement.

Then came the shock. On 2 May 2025, the Supreme Court of India passed an order for the liquidation of Bhushan Power and Steel Limited under Chapter III of the Insolvency and Bankruptcy Code, 2016, rejecting the resolution plan of JSW Steel, finding it to be non-compliant with the Code. The court's reasoning was technical but devastating—it found procedural violations in the resolution process and held that JSW had not complied with statutory timelines.

The Court also mandated the return of payments made by JSW Steel to creditors and equity contributions within two months. This wasn't just about losing the asset—JSW potentially faced a write-off of not just the Rs 19,350 crore acquisition cost but also the additional capital invested in upgrading the facility. Analysts estimated the total exposure at Rs 25,000-30,000 crore, a potentially crippling blow even for a company of JSW's size.

The Supreme Court's judgment sent shockwaves through India's business community. The CoC also failed to protect the interests of the creditors by taking contradictory stands before the Supreme Court and accepting the payments from JSW without any demurrer and supporting JSW's ill-motivated plan against the interests of the creditors," the court said. If a resolution plan approved by creditors, the NCLT, and implemented over several years could be retrospectively canceled, what did that mean for the sanctity of contracts and the bankruptcy process itself?

JSW's legal team scrambled to respond. A Bench of Justice B V Nagarathna and Justice Satish Sharma ordered the status quo, considering that JSW's "limitation period" for filing a review of the Supreme Court's judgment was not over. The status quo order provided breathing room, but the fundamental issue remained unresolved.

In a dramatic turn, a three-judge Bench led by Chief Justice BR Gavai, marks a decisive course correction in India's insolvency jurisprudence. It reviewed and overturned the earlier judgment of the SC delivered in May 2025 by a Bench led by Justice Bela Trivedi, which had directed liquidation of Bhushan Power and Steel Limited. The September 2025 judgment restored JSW's resolution plan, but the damage to investor confidence had been done.

The financial impact was significant but manageable. BPSL's 4.5-million-tonne-per-annum (mtpa) installed steelmaking facility accounted for 12.6% of JSW Steel's consolidated 35.7-mtpa capacity and ~9.7% of its consolidated FY2025 EBITDA. The potential liquidation of BPSL is therefore expected to impact JSW Steel's near-term earnings.

The Bhushan Power saga revealed fundamental weaknesses in India's commercial dispute resolution system. Even with a new bankruptcy code designed to provide certainty and speed, the process had dragged on for over seven years. The ability of investigating agencies to attach assets after bankruptcy proceedings commenced created uncertainty that deterred bidders. Most fundamentally, the Supreme Court's initial willingness to overturn a completed transaction on procedural grounds raised questions about the stability of property rights in India.

For JSW, the episode was both a learning experience and a test of resilience. The company had to manage not just the financial impact but also the reputational damage from being associated with a controversial acquisition. International investors questioned JSW's risk management processes and the wisdom of pursuing distressed assets in India's uncertain legal environment. Credit rating agencies flagged the Bhushan Power uncertainty as a key risk factor.

Yet the company's fundamental operations remained strong. Even while managing the Bhushan Power crisis, JSW continued to execute its expansion plans, maintain operational excellence, and generate healthy cash flows. The episode demonstrated both the opportunities in India's distressed asset market and the critical importance of understanding and managing legal and regulatory risks.

VII. Technology & Innovation: The Modernization Journey

While financial engineering and M&A grabbed headlines, JSW Steel's sustained competitive advantage came from a less visible but equally important source: its systematic approach to technology adoption and innovation. The company's journey from operating basic re-rolling mills to producing sophisticated automotive-grade steel represents one of the most successful technology transformation stories in Indian manufacturing.

The foundation was laid through strategic partnerships rather than attempting to develop everything internally. JSW Steel has a strategic collaboration with global leader JFE Steel of Japan, enabling JSW to access new and state-of-the-art technologies to produce & offer high-value special steel products to its customers. This partnership went beyond simple technology licensing—it involved deep knowledge transfer, joint product development, and sharing of operational best practices.

The collaboration with JFE was particularly significant in developing capabilities in electrical steel, a highly sophisticated product used in power transformers and electric motors. This is a segment where only a handful of global producers have the necessary technology, and JSW's entry marked a significant milestone for Indian manufacturing capability. The technology transfer included not just equipment and processes but also quality control systems, customer service protocols, and R&D methodologies.

Digital transformation became a strategic priority in the late 2010s. In FY 2024-25, made significant strides by embedding advanced technologies across the entire value chain with more than 2,900 critical assets connected to predictive maintenance platforms. This wasn't digitization for its own sake—each initiative was tied to specific operational improvements. Predictive maintenance reduced unplanned downtime, automated quality control improved product consistency, and digital supply chain management reduced working capital requirements.

The company's approach to Industry 4.0 was pragmatic rather than revolutionary. Instead of attempting wholesale transformation, JSW identified specific pain points where digital solutions could deliver immediate value. For instance, computer vision systems were deployed to detect surface defects in steel products, reducing customer complaints and rework costs. Machine learning algorithms optimized blast furnace operations, improving fuel efficiency and reducing emissions. Digital twins of critical equipment enabled better maintenance planning and capacity utilization.

Innovation extended beyond the factory floor to customer engagement. JSW developed sophisticated technical service capabilities, with teams of metallurgists and application engineers working directly with customers to develop customized solutions. This was particularly important in automotive steel, where each new vehicle platform required specific grade developments and extensive testing. The company established application development centers where customers could test new steel grades in simulated conditions, accelerating product development cycles.

Research and development became increasingly important as JSW moved up the value chain. The company established partnerships with leading technical institutions including IIT Bombay, where it funded research in advanced materials and process technologies. These collaborations produced not just new products but also a pipeline of trained engineers who understood both theoretical concepts and practical applications.

The focus on innovation yielded tangible results. JSW became one of the few Indian companies capable of producing automotive outer body panels that met global quality standards. It developed special grades for India's growing renewable energy sector, including steels for wind turbine towers that could withstand extreme weather conditions. The company even ventured into import substitution, developing grades that were previously sourced entirely from Japan or Europe.

But perhaps the most significant technological achievement was in process efficiency. JSW Steel's inherent strength has been its ability to expand capacities at a competitive capex per tonne compared to global benchmarks. This wasn't just about buying cheaper equipment—it reflected deep process knowledge that enabled JSW to optimize plant designs, reduce construction time, and achieve faster ramp-ups.

The company developed proprietary modifications to standard steel-making processes that improved productivity while reducing costs. For example, JSW's blast furnaces achieved some of the highest productivity rates globally through a combination of raw material preparation techniques, burden distribution systems, and operating practices developed through years of experimentation and optimization.

Quality became a differentiator rather than just a compliance requirement. JSW was among the first Indian steel companies to obtain automotive quality certifications from global OEMs. The company implemented sophisticated statistical process control systems that could detect and correct quality variations in real-time. This capability was crucial in winning contracts from demanding customers like Japanese automotive companies operating in India.

The technology journey also had its challenges. Adopting advanced technologies required significant investment in training and change management. Many workers who had spent decades operating traditional equipment struggled to adapt to digital interfaces and automated systems. JSW invested heavily in skill development, establishing training centers at each plant and partnering with technical institutes to upgrade worker capabilities.

Environmental technology became increasingly important as sustainability concerns grew. JSW invested in waste heat recovery systems, water recycling plants, and air pollution control equipment that went beyond regulatory requirements. These investments were expensive and didn't generate immediate returns, but they positioned the company for a future where environmental performance would be as important as cost competitiveness.

VIII. Sustainability & The Green Steel Revolution

The steel industry's relationship with climate change is paradoxical—steel is essential for building renewable energy infrastructure, yet traditional steel-making is one of the largest industrial sources of CO2 emissions. For JSW Steel, navigating this paradox has become central to its strategy, transforming from a compliance obligation to a competitive differentiator and existential imperative.

JSW's sustainability journey began with recognition on global platforms. World Steel Association's Steel Sustainability Champion (consecutively 2019 to 2021), Leadership Rating (A-) in CDP (2020). These weren't just certificates for the boardroom—they represented systematic changes in how the company approached resource utilization, emissions management, and stakeholder engagement.

The most ambitious initiative is the green hydrogen project at Vijayanagar. JSW Energy will set up a 3,800 tonnes per annum (tpa) green hydrogen plant for supply to JSW Steel. This project, commissioned in late 2025, represents India's largest industrial-scale green hydrogen facility. Under a seven-year offtake agreement, the plant will deliver 3,800 tons of green hydrogen and 30,000 tons of green oxygen annually to JSW Steel.

The green hydrogen project is more than a pilot—it's a blueprint for the future of steel-making. Traditional steel production using blast furnaces requires coking coal, which releases massive amounts of CO2. Green hydrogen can replace coking coal in direct reduced iron (DRI) production, potentially eliminating most emissions from the steel-making process. While the current project is small relative to JSW's total production, it provides crucial learning for eventual scale-up.

The company has set aggressive decarbonization targets. On track to meet emission reduction targets for 2030 and Net Neutral by 2050. Achieving these targets requires fundamental changes in production processes, energy sources, and product mix. JSW is exploring multiple pathways simultaneously—hydrogen-based DRI, carbon capture and storage, and increased use of scrap steel through electric arc furnaces.

Water management has become equally critical, particularly given that many JSW plants are in water-stressed regions. The company implemented zero liquid discharge systems at multiple facilities, treating and recycling every drop of industrial wastewater. Rainwater harvesting systems capture monsoon runoff, reducing dependence on groundwater. These initiatives required substantial capital investment but became essential for maintaining social license to operate in local communities.

Circular economy principles are being embedded across operations. According to the JSW Steel website, the plant reuses more than 95% of its process waste. Blast furnace slag is converted to cement, reducing waste while creating an additional revenue stream. Steel mill scale is recovered and recycled back into the production process. Even seemingly minor waste streams like used refractories are processed to recover valuable metals.

The sustainability push extends beyond JSW's own operations to its entire value chain. The company works with suppliers to reduce their environmental footprint, providing technical assistance and sometimes financing for improvement projects. On the customer side, JSW developed products that enable sustainability—high-strength steels that reduce material usage in construction, electrical steels that improve efficiency in power transmission, and specialized grades for renewable energy applications.

Carbon pricing is becoming a commercial reality rather than a distant threat. The European Union's Carbon Border Adjustment Mechanism (CBAM), which will impose carbon tariffs on steel imports, has forced JSW to accelerate its decarbonization plans. By 2030, the company plans to set up a green steel plant to comply with the European Union's Carbon Border Adjustment Mechanism and gradually reduce it use of blast furnaces throughout its value chain. This isn't just about maintaining access to export markets—it's about preparing for a future where carbon efficiency becomes a primary basis for competition.

The financial implications of sustainability are complex. Green technologies require massive upfront investment with uncertain returns. Hydrogen-based steel production, even when technically feasible, remains significantly more expensive than conventional methods. JSW has to balance the imperative to reduce emissions with the need to remain cost-competitive, particularly when competing against producers in countries with less stringent environmental regulations.

Yet sustainability also creates opportunities. JSW Steel has also been awarded the Sustainability Champion 2025 recognition by the worldsteel Association consecutively for the seventh year. We received Responsible Steel certification for four plants covering 80% of our steel production. ResponsibleSteel certification opens doors to environmentally conscious customers willing to pay premiums for verified sustainable steel. Green financing options provide access to cheaper capital for sustainability projects. Perhaps most importantly, early movement on sustainability builds capabilities that will become essential as regulations tighten globally.

The company is also investing in nature-based solutions. Large-scale afforestation programs around plant sites create carbon sinks while improving local air quality. Biodiversity conservation initiatives protect local ecosystems, building goodwill with communities and environmental groups. These "soft" sustainability initiatives complement the "hard" technology investments, creating a comprehensive approach to environmental stewardship.

Employee engagement has proven crucial for sustainability success. JSW established "green teams" at each plant, empowering workers to identify and implement improvement projects. Energy conservation became part of performance metrics, creating incentives for operational teams to reduce consumption. The company discovered that many of the best sustainability ideas came from shop floor workers who understood processes intimately.

The sustainability transformation faces significant challenges. India's energy grid remains heavily dependent on coal, limiting the impact of electrification initiatives. The domestic market hasn't yet developed willingness to pay premiums for green steel, making it difficult to recover higher production costs. Technology for zero-emission steel production remains immature and expensive. Despite these challenges, JSW's leadership views sustainability not as an option but as an imperative for long-term survival.

IX. The Modern Era: Market Position & Challenges (2020-Present)

The 2020s have brought unprecedented challenges and opportunities for JSW Steel. The COVID-19 pandemic, supply chain disruptions, geopolitical tensions, and accelerating energy transition have created a business environment unlike any in the company's history. Yet this period has also seen JSW achieve remarkable milestones, including becoming the world's most valuable steelmaker, boasting a market capitalisation of nearly $30.31 billion in March 2025.

India's steel demand dynamics have been exceptionally strong. India's crude steel production rose by 6.8% YoY to 40.12MnT in Q4 FY25, and by 5.3% to 152MnT in FY25. Steel consumption grew by 11.2% YoY to 40.27MnT in Q4, while it was up 11.5% to 152MnT for FY25. This was the fourth consecutive year of double-digit steel demand growth in India. This sustained growth, driven by infrastructure spending, urban construction, and manufacturing expansion, has created a favorable environment for domestic producers.

JSW's operational performance has been impressive. we achieved our highest ever production and sales volumes in FY 2024-25. The company's ability to maintain high capacity utilization, optimize product mix, and manage costs has translated into strong financial performance despite global headwinds. The successful commissioning of the 5 MTPA expansion at Vijayanagar has added scale at a time when demand is robust.

The competitive landscape has evolved significantly. While JSW has emerged as India's largest steel producer, competition remains intense. Tata Steel continues to be a formidable rival with its deep pockets and century-long heritage. ArcelorMittal's entry through the acquisition of Essar Steel added a global major to the domestic market. SAIL, despite its public sector constraints, retains significant capacity and government support. New entrants like AMNS (ArcelorMittal Nippon Steel) have brought international best practices and deep pockets.

The import challenge has become increasingly acute. Steel imports increased by 9.2% YoY to 10.5MnT in FY25 while steel exports fell by 26.7% to 6.26MnT. Consequently, India remained a net importer of steel for the second consecutive year. Chinese overcapacity continues to pressure global markets, with subsidized Chinese steel finding its way into India through various routes, including third countries that have free trade agreements with India.

Government policy has been both supportive and challenging. Production-linked incentive schemes for manufacturing have boosted steel demand. Infrastructure spending has remained robust despite fiscal constraints. However, regulatory uncertainty around environmental norms, mining lease extensions, and trade policy has complicated planning. The government's push for domestic manufacturing under "Atmanirbhar Bharat" has created opportunities, but implementation has been uneven.

JSW's response has been multi-pronged. The company continues to pursue capacity expansion, targeting a domestic capacity of 50 MTPA by FY 2030-31. But growth is now more selective, focusing on value-added products and strategic locations. The emphasis has shifted from pure volume growth to improving product mix, customer stickiness, and operational efficiency.

Digital initiatives have accelerated. The pandemic forced rapid adoption of digital tools for everything from customer engagement to remote plant monitoring. JSW developed e-commerce platforms for retail sales, digital supply chain management systems, and virtual customer service capabilities. These initiatives, born of necessity, have become permanent features that improve efficiency and customer experience.

Partnerships have become more important than ever. JSW Steel and South Korea's Posco have signed a pact to explore setting up a 6 million tonnes per annum (MTPA) integrated steel plant in India, with Odisha among the top locations being considered. The HoA outlines the broad framework for the proposed 50:50 joint venture—which was announced in October 2024. As the next step in the proposed venture, JSW and Posco will carry out a detailed feasibility study. Such partnerships bring not just capital but also technology and market access.

The financial strategy has evolved to balance growth with stability. Despite aggressive expansion plans, JSW has maintained reasonable leverage ratios. The company has diversified funding sources, accessing international bond markets, sustainability-linked loans, and domestic capital markets. The focus on cash flow generation has intensified, with working capital optimization and cost reduction programs offsetting margin pressures.

Product innovation continues at pace. JSW has developed specialized steels for India's growing electric vehicle industry, high-strength steels for lightweighting applications, and corrosion-resistant grades for coastal infrastructure. The company is also exploring opportunities in emerging segments like additive manufacturing and steel for hydrogen storage and transportation.

The organizational capabilities have matured significantly. JSW now has deep bench strength in project execution, operational excellence, and stakeholder management. The company has successfully integrated multiple acquisitions, managed complex international operations, and navigated regulatory challenges. This institutional knowledge—hard-won through successes and failures—represents an intangible but valuable asset.

Looking ahead, several challenges loom large. The global economic slowdown could dampen steel demand. Chinese overcapacity remains a structural threat. The energy transition could disrupt traditional steel demand patterns even as it creates new opportunities. Increasing environmental regulations will require massive investments with uncertain returns. Competition for raw materials, particularly high-grade iron ore, will intensify.

Yet JSW's position appears strong. In March 2025, JSW Steel became the most valued steel company in the world, which is a testament to the tremendous value created for shareholders over the years. The journey ahead holds even greater promise, and we step into the future with clarity of purpose and an unshakable belief in India's potential. As India accelerates its journey towards becoming a global economic powerhouse, we are confident that JSW Steel will continue to play a pivotal role in shaping the nation's future.

X. Playbook: Business & Investment Lessons

After four decades of building JSW Steel from a single re-rolling mill to India's largest steel producer, several strategic principles emerge that offer lessons for entrepreneurs, managers, and investors navigating capital-intensive industries in emerging markets.

Brownfield vs. Greenfield: The Capital Efficiency Imperative

JSW's consistent preference for brownfield expansions and acquisitions over greenfield projects reflects deep understanding of capital efficiency in the steel industry. Greenfield projects in steel typically require $1,000-1,500 per tonne of capacity, while brownfield expansions can be done at $500-700 per tonne, and acquisitions of distressed assets even cheaper. This isn't just about lower capital cost—brownfield projects have shorter execution timelines, lower risk, and faster revenue generation.

The company developed a systematic approach to evaluating expansion options. Each potential acquisition was assessed not just on purchase price but on the total cost to bring it to JSW standards. This included modernization capex, working capital requirements, environmental remediation, and integration costs. Many deals that looked attractive on headline valuations were rejected after this comprehensive analysis.

Timing Market Cycles: The Contrarian Advantage

Steel is a deeply cyclical industry, and JSW's ability to time capacity additions and acquisitions to market cycles has been a crucial success factor. The company consistently invested during downturns when assets were cheap and construction costs low, positioning itself to benefit from subsequent upturns. The Dolvi acquisition in 2010, during the post-financial crisis slowdown, exemplified this approach.

This contrarian strategy required strong financial discipline during boom periods. While competitors leveraged up to chase growth when steel prices were high, JSW maintained conservative balance sheets, preserving firepower for downturns. This approach sometimes led to criticism from investors wanting more aggressive growth, but it enabled JSW to survive and thrive through multiple cycles.

M&A Through Distressed Assets: The IBC Opportunity

The introduction of India's Insolvency and Bankruptcy Code created unprecedented opportunities to acquire assets at distressed valuations. JSW became one of the most successful users of the IBC framework, acquiring multiple assets including BPSL, Monnet Ispat, and others. The company developed specialized capabilities in evaluating distressed assets, navigating the IBC process, and quickly turning around acquired operations.

However, the Bhushan Power saga also highlighted the risks. Legal uncertainty, regulatory overreach, and judicial unpredictability can turn attractive acquisitions into nightmares. The lesson is that in emerging markets, legal and regulatory risks often outweigh operational risks. Sophisticated legal structuring, government relations capabilities, and contingency planning are essential for distressed M&A.

Vertical Integration: Controlling Your Destiny

JSW's systematic approach to vertical integration—from iron ore mining to finished steel products—reflects the realities of operating in an emerging market. Unlike developed markets where efficient spot markets exist for inputs, Indian steel companies face chronic uncertainty in raw material availability and pricing. Vertical integration provides supply security and cost predictability.

But vertical integration also brings complexity and capital intensity. JSW learned to be selective, focusing on critical bottlenecks rather than trying to control everything. The company maintained flexibility through a mix of captive and market sources, avoiding the rigidity that full integration can create.

Government Relations: The Hidden Competitive Advantage

In an industry where government permissions are required for everything from land acquisition to capacity expansion to environmental clearances, the ability to navigate the regulatory landscape becomes a critical competitive advantage. JSW developed deep capabilities in stakeholder management, maintaining relationships across political parties and bureaucratic levels.

This wasn't about seeking favors but about understanding the system and working within it effectively. JSW's leadership understood that in India, business and government are necessarily intertwined, and success requires aligning corporate strategy with national priorities. The company's positioning around "Atmanirbhar Bharat" and infrastructure development resonated with policymakers, facilitating approvals and support.

Capital Allocation: Balancing Growth and Returns

For a capital-intensive business like steel, capital allocation decisions determine long-term success or failure. JSW's approach evolved from pure growth focus in early years to a more balanced framework considering returns, risk, and strategic fit. The company learned to walk away from expensive acquisitions, even when they offered strategic benefits, if the financial math didn't work.

The discipline extended to organic investments. Each expansion was evaluated on multiple criteria—IRR, payback period, strategic importance, and risk. Projects were staged to preserve optionality, with commitment to full investment only after initial phases proved successful. This reduced the risk of large-scale failures while maintaining growth momentum.

Family Business Governance: Professionalizing Without Losing Control

JSW successfully navigated the transition from founder-led to professionally managed while maintaining family control. The Jindal family retained strategic decision-making while delegating operational management to professionals. This hybrid model combined the long-term orientation of family ownership with the capabilities and governance standards expected by institutional investors.

Clear separation of family and business interests was crucial. The 2005 family settlement that divided the Jindal empire prevented the destructive conflicts that plague many Indian business families. Within JSW, family members who joined the business were required to prove themselves, starting in operational roles rather than immediately entering the boardroom.

XI. Analysis: Porter's 5 Forces & Hamilton's 7 Powers

Understanding JSW Steel's competitive position requires systematic analysis through established strategic frameworks. Porter's Five Forces reveals the industry structure that shapes profitability, while Hamilton Helmer's 7 Powers identifies the sources of persistent differential returns.

Porter's Five Forces Analysis

Supplier Power: High The steel industry's dependence on bulk raw materials—iron ore and coking coal—gives suppliers significant leverage. India imports 85% of its coking coal requirements, making producers vulnerable to global price fluctuations and supply disruptions. Iron ore, while domestically available, is controlled by a few large miners and subject to government allocation policies. JSW has partially mitigated this through backward integration, securing captive mines that meet 40-45% of requirements, but supplier power remains a structural challenge.

Buyer Power: Moderate The customer landscape is bifurcated. Large industrial customers—automotive OEMs, white goods manufacturers, infrastructure contractors—have significant negotiating leverage, demanding price concessions, extended credit terms, and technical support. However, the retail and small business segment is highly fragmented with limited buyer power. JSW's strategy of developing technical capabilities for specialized grades has reduced buyer power in certain segments, but commodity grade steel remains highly price-competitive.

Threat of Substitutes: Low Steel's unique combination of strength, durability, and recyclability makes substitution difficult in core applications. While aluminum has gained share in automotive to reduce weight, and engineered wood/concrete alternatives exist in construction, steel remains irreplaceable for most structural applications. The threat is more about demand destruction—if infrastructure spending slows or manufacturing shifts elsewhere—rather than material substitution.

Threat of New Entrants: Low The capital requirements for integrated steel production are enormous—a modern 5 MTPA plant requires $5+ billion investment. Beyond capital, entrants need access to raw materials, environmental clearances, land acquisition, and technical expertise. The 7-10 year development timeline for greenfield projects creates additional barriers. However, the IBC has lowered entry barriers by enabling acquisition of distressed assets, as JSW itself demonstrated.

Competitive Rivalry: High Competition among existing players is intense across multiple dimensions. Price competition is fierce in commodity grades, with players undercutting to maintain capacity utilization during downturns. Quality and service competition exists in value-added segments. Companies compete for raw material access through auctions and long-term contracts. The presence of global majors like ArcelorMittal alongside domestic champions like Tata Steel and JSW creates a complex competitive dynamic.

Hamilton's 7 Powers Analysis

Scale Economies: Strong Steel production exhibits classic scale economies. Larger blast furnaces have lower unit costs, overhead spreads across more volume, and procurement leverage increases with size. JSW Steel's ability to expand capacities at a competitive capex per tonne compared to global benchmarks reflects these scale advantages. The company's 34.2 MTPA domestic capacity enables cost advantages that smaller players cannot match. Scale also enables R&D investments, technology partnerships, and market development that create reinforcing advantages.

Network Effects: Limited Traditional steel production has minimal network effects. However, JSW has created modest network benefits through its distribution system, where more retail touchpoints attract more customers and suppliers. The company's technical service network creates some lock-in effects—customers who co-develop specialized grades with JSW face switching costs. Digital initiatives might create stronger network effects over time, but currently, this power source is weak.

Counter-Positioning: Moderate JSW hasn't fundamentally counter-positioned against incumbents but has selectively chosen different approaches. While Tata Steel emphasized premium branding, JSW focused on operational efficiency. While SAIL maintained government relationships, JSW built private sector capabilities. The focus on value-added products versus commodity steel represents mild counter-positioning, but JSW essentially plays the same game with better execution rather than changing the rules.

Switching Costs: Low to Moderate In commodity grades, switching costs are negligible—steel is fungible and customers readily shift suppliers for price advantages. However, in specialized applications, switching costs increase. Automotive grades require extensive testing and certification, creating 2-3 year switching cycles. Technical collaboration on product development creates relationship stickiness. Long-term contracts with volume commitments create commercial switching costs. Overall, JSW has moderately increased switching costs in selected segments.

Branding: Emerging Historically, steel was an unbranded commodity, but JSW has invested in building brand recognition. In retail segments, the JSW brand commands modest premiums for perceived quality and reliability. Corporate branding around sustainability and "Make in India" resonates with certain customers. However, branding remains weak compared to consumer products—most customers still buy based on specifications and price rather than brand preference.

Cornered Resource: Moderate JSW's captive iron ore mines provide some resource advantages, but these are limited by government allocation and pricing policies. The strategic locations of plants, particularly Vijayanagar in the iron ore belt, create logistical advantages that are difficult to replicate. Long-term relationships and technical partnerships represent intangible cornered resources. However, no single resource provides insurmountable advantages—competitors can access similar resources through different means.

Process Power: Strong JSW's operational excellence represents its strongest power source. The company's ability to consistently execute projects on time and budget, achieve superior operational metrics, and integrate acquisitions successfully reflects deep process capabilities developed over decades. The world's largest conveyor system, which travels ~24 km from the captive mines to the Vijayanagar plant, exemplifies infrastructure innovations that create lasting advantages. The tacit knowledge embedded in thousands of employees—from blast furnace operators to project managers—cannot be easily replicated.

XII. Bear vs. Bull Case

The investment case for JSW Steel presents compelling arguments on both sides, reflecting the complex dynamics of operating a capital-intensive business in an emerging market with global ambitions.

Bull Case: The India Infrastructure Supercycle

The most powerful bull argument rests on India's multi-decade infrastructure buildout. The government's strong infrastructure push is set to continue into FY 2025-26 with a planned outlay of ₹11.2 trillion. India's steel consumption per capita remains at 80 kg versus the global average of 230 kg and China's 650 kg, suggesting enormous catch-up potential. As India builds metros, airports, highways, and smart cities, steel demand should compound at high single digits for decades.

This was the fourth consecutive year of double-digit steel demand growth in India, demonstrating sustained momentum that shows no signs of slowing. Unlike China, where steel demand has peaked, India is just entering the steep part of its industrialization S-curve. Demographics support this—India's working-age population is growing, urbanization is accelerating, and rising incomes are driving consumption of steel-intensive goods from cars to appliances.

JSW's competitive position to capture this growth appears strong. As the country's largest steelmaker with domestic capacity of 34.2 MTPA, the company has scale advantages in procurement, distribution, and operations. The planned expansion to 50 MTPA by FY 2030-31 is achievable given the company's track record and available brownfield opportunities.

The value-added product strategy is working. JSW has successfully moved up the value chain, with specialized products now accounting for over 60% of sales. These products command premium pricing, face less import competition, and create customer stickiness. As Indian manufacturing becomes more sophisticated—electric vehicles, renewable energy, defense—demand for specialized steels will accelerate.

Green steel leadership could become a massive differentiator. JSW Steel is set to commission India's largest green hydrogen project for steelmaking at Vijayanagar, positioning the company for a low-carbon future. As carbon border taxes proliferate and customers demand sustainable steel, early movers will capture premium markets. JSW's investments in renewable energy, hydrogen, and process efficiency create options for multiple decarbonization pathways.

Operational excellence provides confidence in execution. The company's ability to expand capacities at a competitive capex per tonne compared to global benchmarks means growth can be funded without excessive leverage. Strong project execution capabilities, proven integration skills, and deep operational knowledge reduce execution risks that plague many industrial expansions.

Bear Case: Structural Challenges and Cyclical Risks

The bear case starts with the Bhushan Power debacle. Despite the Supreme Court's reversal, the episode revealed fundamental risks in India's legal system. If a transaction completed through statutory processes can be unwound years later, what is the value of contracts? The potential exposure of Rs 25,000-30,000 crore represents a material risk to equity value. Even if JSW ultimately prevails, the uncertainty creates an overhang that could persist for years.

China's overcapacity represents an existential threat. China produces over 1 billion tonnes of steel annually—half of global production—and exports 100 million tonnes. He highlighted China's steel exports matching India's production capacity. When China's domestic demand weakens, its exports flood global markets, destroying pricing power. India's free trade agreements with ASEAN countries enable Chinese steel to enter through third countries, circumventing direct import restrictions.

The commodity cycle appears to be turning. After years of strong demand, global growth is slowing. China's property crisis, developed market recession risks, and geopolitical tensions threaten steel demand. JSW's aggressive expansion plans could see new capacity coming online just as markets weaken, crushing utilization and margins. The company's high operating leverage means small changes in utilization have outsized profit impact.

Debt levels remain concerning despite recent improvements. While net debt to EBITDA ratios appear manageable, absolute debt levels are high. Rising interest rates increase financing costs. The massive capex program—Rs 61,863 crore over FY26-28—will require substantial additional borrowing. If cash flows disappoint due to margin compression or demand weakness, leverage could quickly become problematic.

Environmental regulations pose escalating costs with uncertain returns. Carbon taxes, emission standards, and water restrictions require massive investments in pollution control and process changes. Green steel production remains significantly more expensive than conventional methods. While JSW positions these investments as strategic, the reality is they're largely compliance-driven costs that don't generate returns unless green premiums emerge.

Import competition is intensifying. India remained a net importer of steel for the second consecutive year. Despite government rhetoric about self-reliance, policy support remains inconsistent. Trade protection is limited by WTO commitments and diplomatic considerations. Global steel majors with deeper pockets and superior technology can undercut domestic producers when they choose to focus on India.

Key Performance Indicators to Track

For investors monitoring JSW Steel, three KPIs matter most:

EBITDA per Tonne vs. Peers: This metric captures operational efficiency, product mix, and pricing power in a single number. JSW should maintain EBITDA per tonne at least 10% above the domestic industry average to justify its valuation premium. Deterioration relative to peers signals either operational issues or unfavorable mix shift.

Net Debt to EBITDA Ratio: Given the capital intensity and cyclicality, leverage is the key risk metric. The ratio should stay below 3.5x through the cycle, with headroom during expansionary phases. Rising above 4x would signal financial stress, potentially forcing asset sales or equity dilution.

Capacity Utilization Rate: In a high fixed cost business, utilization drives profitability. JSW should maintain utilization above 85% even during downturns, reflecting its operational excellence and market position. Sustained utilization below 80% would indicate either demand problems or operational issues, requiring immediate attention.

XIII. Recent Developments & Future Outlook

The past eighteen months have been transformative for JSW Steel, marked by legal victories and setbacks, strategic partnerships, and bold moves into adjacent businesses that signal the company's evolution beyond pure steel manufacturing.

The most dramatic development was the Supreme Court's flip-flop on Bhushan Power. The May 2025 liquidation order sent shockwaves through India's business community, raising fundamental questions about contract sanctity and judicial consistency. The ruling, delivered on September 26, 2025, by a three-judge Bench led by Chief Justice BR Gavai, marks a decisive course correction in India's insolvency jurisprudence. It reviewed and overturned the earlier judgment of the SC delivered in May 2025 by a Bench led by Justice Bela Trivedi, which had directed liquidation of Bhushan Power and Steel Limited (BPSL), even after the successful implementation of JSW Steel's resolution plan. In its detailed September judgment, Justice Gavai's Bench categorically upheld the JSW resolution plan for BPSL.

While the reversal was welcome, the damage to investor confidence was lasting. The episode highlighted the risks of pursuing distressed assets in India, where legal processes can drag on for years and outcomes remain unpredictable even after implementation. JSW has indicated it may seek a strategic partner for BPSL, suggesting management wants to reduce exposure to this controversial asset.

Beyond steel, JSW Group's diversification is accelerating. As of June 2025, JSW Paints announced that it had signed definitive agreements to acquire up to a 74.76% stake in Akzo Nobel India Limited (ANIL) from Akzo Nobel and its affiliates, for a maximum consideration of ₹8,986 crore (US$1.1 billion), as outlined in the Share Purchase Agreement. This acquisition will make JSW Paints the fourth-largest player in the Indian paint industry. This bold entry into consumer-facing businesses represents a strategic evolution, leveraging the JSW brand and distribution network built through steel retail.

The partnership with POSCO signals renewed international ambitions. Both the steel makers signed non-binding heads of agreement (HoA) in Mumbai. The HoA outlines the broad framework for the proposed 50:50 joint venture. Unlike previous international ventures that struggled, this partnership brings together complementary strengths—JSW's local knowledge and execution capabilities with POSCO's technology and global reach.

The electric vehicle revolution presents both opportunities and challenges. JSW's joint venture with MG Motor positions it to benefit from automotive sector growth, while steel demand from EVs differs from traditional vehicles—less engine components but more battery enclosures and charging infrastructure. The company is developing specialized grades for EV applications, including electrical steels for motors and high-strength steels for battery protection.

India's manufacturing renaissance, accelerated by China+1 strategies and production-linked incentives, creates new steel demand sources. Electronics manufacturing, renewable energy equipment, defense production—each requires specialized steels that JSW is positioned to supply. The company's focus on import substitution aligns perfectly with these trends, replacing expensive imported grades with domestically produced alternatives.

Technological disruption looms on the horizon. Direct reduced iron using hydrogen, molten oxide electrolysis, carbon capture and utilization—multiple pathways to zero-emission steel are being developed globally. JSW's green hydrogen project provides early learning, but massive investments will be required to deploy these technologies at scale. The company that masters green steel production first could dominate future markets, but betting on the wrong technology could prove catastrophic.

The financial outlook remains robust despite challenges. Analysts project steady earnings growth driven by capacity expansion and improving product mix. The successful ramp-up of recent expansions, particularly the 5 MTPA Vijayanagar project, should drive volume growth even if pricing remains volatile. Cost reduction initiatives and operational improvements provide some margin protection against commodity cycles.

However, risks are mounting. Global recession fears, China's economic struggles, and geopolitical tensions create demand uncertainty. Rising protectionism could disrupt global steel trade, potentially helping domestic players but also raising input costs. Climate regulations are tightening faster than expected, potentially stranding assets or requiring accelerated investments.

XIV. Epilogue & Reflections

Standing at JSW Steel's Vijayanagar plant today, watching molten steel flow from blast furnaces while green hydrogen pilots run nearby, one witnesses Indian industry at an inflection point. The journey from that small Tarapur mill to becoming the world's most valuable steel company by market capitalization represents more than corporate success—it embodies India's industrial transformation and the possibilities and perils of building global champions from emerging markets.

What makes JSW Steel special in Indian industrials? It's not just scale, though domestic capacity of 34.2 MTPA is impressive. It's not just financial performance, though revenue of ₹1,68,824 crore demonstrates robust execution. Rather, it's the company's ability to navigate the unique challenges of Indian business while maintaining global ambitions—managing government relations without becoming dependent, pursuing technology partnerships while building indigenous capabilities, expanding aggressively while maintaining financial discipline.

The Bhushan Power saga offers crucial lessons for Indian M&A. The initial acquisition logic was sound—distressed assets at attractive valuations, operational turnaround potential, strategic market entry. The execution was professional—due diligence, financing, integration. Yet the investment nearly became a disaster due to factors outside management control—judicial overreach, regulatory uncertainty, retroactive enforcement. The lesson isn't to avoid distressed assets but to price in regulatory risk and structure transactions to limit downside.

Looking ahead, can JSW become a global steel major? The company has the scale, capabilities, and ambition. But global leadership requires more than domestic dominance. It demands technological leadership, which JSW is pursuing through partnerships and R&D. It requires sustainability credentials, which the green hydrogen project begins to establish. Most critically, it needs ability to compete in global markets, where JSW's track record remains mixed.

The next decade will test whether JSW can transcend its emerging market origins. The company must navigate the energy transition while maintaining competitiveness. It must manage enormous capital requirements while generating adequate returns. It must balance stakeholder demands—from shareholders wanting returns to communities demanding jobs to governments demanding compliance to environmentalists demanding decarbonization.

Key takeaways for founders and investors emerge from JSW's journey:

First, in capital-intensive industries, timing matters more than strategy. JSW's success came from investing during downturns and harvesting during upturns, requiring patience and capital discipline that few possess.

Second, operational excellence trumps financial engineering. While JSW executed complex transactions, its sustainable advantage comes from ability to run plants efficiently, execute projects successfully, and continuously improve operations.

Third, in emerging markets, managing stakeholders is as important as managing operations. JSW's ability to navigate government relations, community expectations, and regulatory requirements enabled growth that pure private sector players couldn't achieve.

Fourth, family businesses can professionalize without losing entrepreneurial edge. The Jindal family's ability to separate ownership from management, recruit professional talent, and maintain long-term orientation provides a model for other family enterprises.

Fifth, sustainability is shifting from cost to opportunity. Early movement on green steel, despite uncertain returns, positions JSW for a carbon-constrained future where clean production becomes a competitive advantage.