Builders FirstSource: From Texas Startup to America's Building Materials Giant

I. Introduction & Episode Context

Picture this: It's 2024, and a single company touches nearly every new home built in America. From the lumber framing your walls to the engineered trusses holding up your roof, from the custom millwork around your windows to the pre-hung doors you walk through—chances are, Builders FirstSource had a hand in it. With over $17 billion in annual revenue, 600 locations sprawling across 43 states, and a market capitalization that's earned it a spot in the S&P 500, this NYSE-listed giant (ticker: BLDR) has become the invisible backbone of American homebuilding.

Yet just 26 years ago, this colossus didn't exist. It was March 1998, and a group of private equity-backed managers in Dallas, Texas, were signing papers to acquire a regional building supply company from Pulte Corporation. They called their new venture BSL Holdings—not exactly a name that rolls off the tongue. Within 18 months, they'd rebrand to Builders FirstSource, but even that ambitious name seemed almost comically aspirational for a company operating in just a handful of states.

The central question driving our story today isn't just how a Texas startup became the nation's largest supplier of structural building products and value-added components. It's how they did it through two of the most brutal economic cycles in modern history—the 2008 financial crisis that obliterated the housing market, and the COVID-19 pandemic that scrambled global supply chains. It's a story of survival, consolidation, and ultimately, domination.

What makes Builders FirstSource particularly fascinating is that it's not a Silicon Valley unicorn or a disruptive tech platform. This is old-economy, pick-up-trucks-and-lumber-yards America. Yet the playbook they've executed—rolling up a fragmented industry through mega-mergers, adding technology and value-added services to commodity products, and building scale advantages that become nearly insurmountable—offers lessons that transcend industries.

Over the next several hours, we'll trace this journey from that 1998 founding through two transformative mega-mergers: the $1.63 billion ProBuild acquisition in 2015 that created a national footprint, and the $11.7 billion BMC merger completed in January 2021 that cemented their dominance. We'll explore how private equity DNA shaped their approach, why they succeeded where dozens of competitors failed, and what their story tells us about building category killers in mature industries.

This isn't just a corporate history—it's a masterclass in strategic patience, operational excellence, and knowing exactly when to strike. Because in the building materials business, as we'll see, timing isn't just important. It's everything.

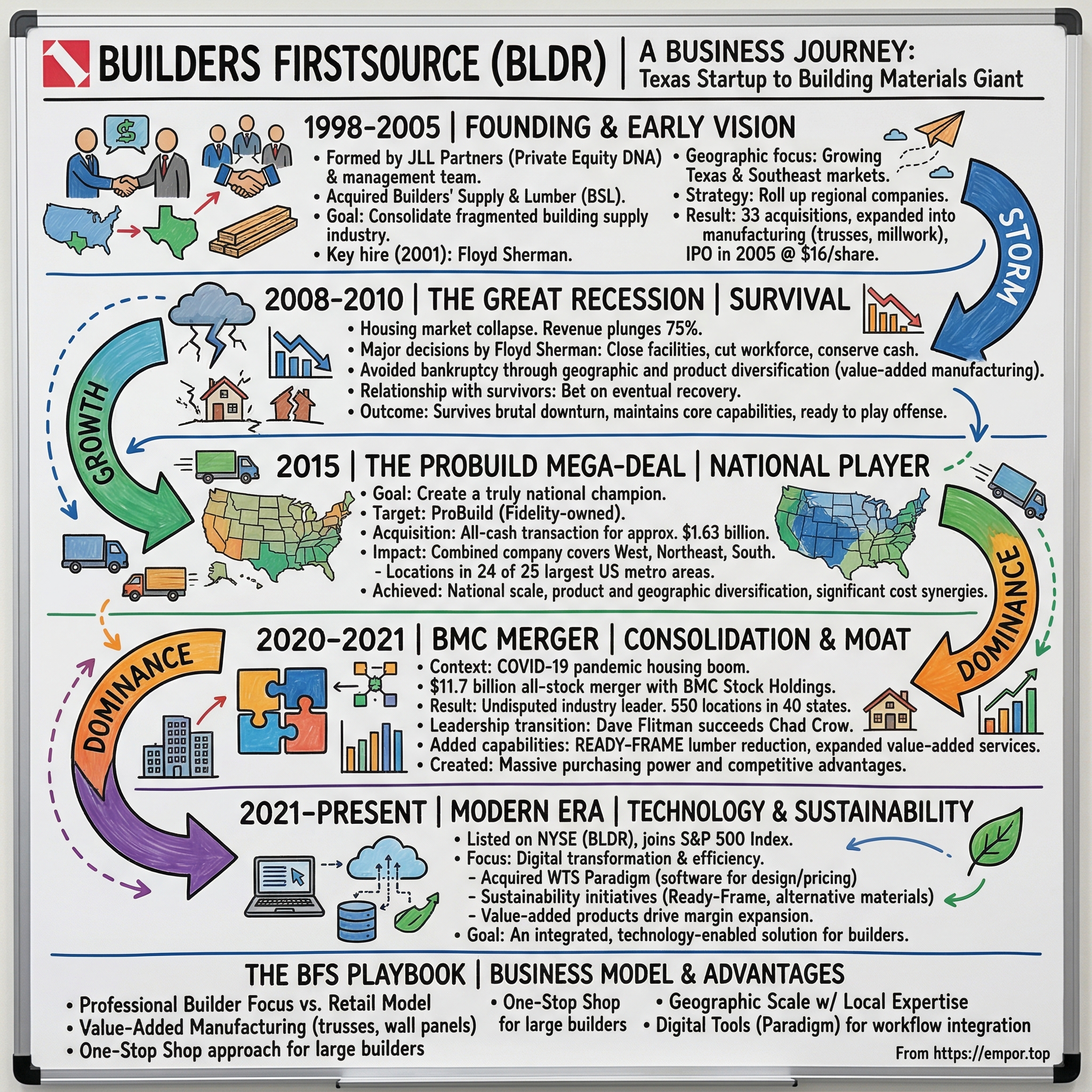

II. The Founding Story & Early Vision (1998-2005)

The conference room at JLL Partners' Manhattan offices hummed with nervous energy in early 1998. Around the table sat a who's who of private equity dealmakers and a handpicked management team, all focused on a single question: Could they build something meaningful in the deeply fragmented, notoriously cyclical world of building materials distribution? The target on the table was Builders' Supply & Lumber Company, a solid but unremarkable regional player that Pulte Corporation, the homebuilding giant, was looking to shed as it refocused on its core business.

For JLL Partners, a middle-market private equity firm founded by former Donaldson, Lufkin & Jenrette executives, this wasn't about finding the next hot tech startup. This was about something more fundamental: recognizing that the American building supply industry, with its thousands of mom-and-pop lumber yards and regional distributors, was ripe for consolidation. The math was compelling—the top 10 players controlled less than 20% of the market. In most mature industries, that number would be closer to 60% or 70%.

The deal closed in March 1998, with the new entity incorporated as BSL Holdings. The name was functional but forgettable—essentially the initials of the acquired company. But names can be changed; what mattered was the vision. The founding team, led by a group of industry veterans who understood both the operational complexities of lumber distribution and the financial engineering possibilities of a roll-up strategy, saw an opportunity that others had missed. By October 1999, the company had shed its functional but forgettable BSL Holdings moniker, rebranding as Builders FirstSource—a name that telegraphed ambition. The company changed its name from BSL Holdings, Inc. to Builders FirstSource, Inc. in October 1999. This wasn't just a cosmetic change; it signaled a shift from being a holding company for acquired assets to being a unified operating entity with a clear identity.

The company was founded in 1998 by Don McAleenan, who would go on to serve as the company's General Counsel and Senior Vice President. McAleenan is a co-founder of BFS and serves as General Counsel. But the real operational leadership came from industry veterans who understood that success in building materials wasn't just about financial engineering—it was about understanding the rhythms of construction sites, the relationships with contractors, and the logistical complexities of getting the right materials to the right place at exactly the right time.

The Texas and Southeastern United States became their proving ground. This wasn't accidental geography. These markets were experiencing explosive growth, driven by population migration, favorable business climates, and a housing boom that seemed like it would never end. Between 1998 and early 2005, the company acquired and integrated thirty-three companies, methodically rolling up small regional players and integrating them into an increasingly sophisticated operation. In 2001, a critical hire would reshape the company's trajectory. Floyd Sherman, former CEO of Triangle Pacific Corp., was named chairman and chief executive officer of Builders FirstSource, joining when the company was at a critical point in its development. Sherman brought 25 years of experience at Triangle Pacific Corp., the last nine of which were as Chairman and Chief Executive Officer, plus three years at Armstrong World Industries. His arrival marked a shift from pure financial engineering to operational excellence. Sherman understood that in the building materials business, relationships were everything—and that the path to greatness wasn't just through acquisitions, but through integrating those acquisitions into a cohesive whole.

The timing of these early years couldn't have been better. The housing market was on fire. Low interest rates, relaxed lending standards, and demographic tailwinds created what seemed like an endless demand for new homes. Builders FirstSource rode this wave, expanding aggressively through both organic growth and acquisitions. Their strategy was clear: become indispensable to professional builders by offering not just products, but solutions. They weren't just selling two-by-fours; they were manufacturing roof trusses, wall panels, and custom millwork—higher-margin, value-added products that saved builders time and labor.

By June 2005, the company was ready for its next act. The Dallas-based company's IPO of about 12.25 million shares priced at $16 a share. Trading under the ticker symbol, "BLDR," the shares opened on the Nasdaq Stock Market at $16.52. The IPO raised capital, but perhaps more importantly, it provided liquidity for the private equity sponsors and positioned the company as a public entity ready to pursue larger acquisitions.

Yet the IPO reception was tepid—shares closed their first day at $15.44, below the offering price. Investors were already beginning to worry about the sustainability of the housing boom. Federal Reserve Chairman Alan Greenspan had started warning about "froth" in local housing markets. But inside Builders FirstSource, the focus remained on execution. They had built a platform. Now they needed to prove it could weather whatever storms lay ahead.

Looking back, those early years from 1998 to 2005 were about laying foundation—both literally and figuratively. The company had grown from a single acquisition to a multi-state operator with manufacturing capabilities and a public listing. But the real test was about to come. Because in the building materials business, as Sherman and his team would soon learn, it's not how you perform in the boom times that defines you. It's how you survive when the music stops.

III. Surviving the Great Recession (2008-2010)

The signs were everywhere if you knew where to look. In late 2006, housing starts began their decline. By 2007, subprime mortgages were imploding. But nothing—absolutely nothing—could have prepared the building materials industry for what happened next. When Lehman Brothers collapsed in September 2008, it wasn't just a financial crisis anymore. It was an existential threat to every company connected to American homebuilding.

For Builders FirstSource, the numbers told a story of unprecedented devastation. Housing starts, which had peaked at over 2 million units annually in 2005, crashed to barely 500,000 by 2009—a 75% decline that ranks among the worst industrial collapses in American history. Revenue evaporated. Customers disappeared overnight. Major homebuilders, once thought invincible, filed for bankruptcy protection. The company that had been built to consolidate a fragmented industry suddenly found itself fighting for survival.

Inside the Dallas headquarters, Floyd Sherman convened his leadership team for what would become a series of gut-wrenching decisions. The playbook for managing through a typical recession was useless—this was something entirely different. The housing market crashes, kickstarting the Great Recession. Making many hard choices, Builders FirstSource successfully avoids bankruptcy and survives the financial crisis.

The decisions came fast and brutal. Facilities that had been acquired just years earlier were shuttered. The workforce, which had grown to serve the boom, was dramatically reduced. Manufacturing plants that had run multiple shifts went dark. But Sherman and his team understood something crucial: they needed to cut deep enough to survive, but not so deep that they couldn't participate in an eventual recovery.

What set Builders FirstSource apart from many competitors who didn't make it through was their diversification—both geographic and operational. While markets like Phoenix and Las Vegas essentially went to zero, other regions held up better. Their value-added manufacturing capabilities, while suffering from reduced volume, maintained better margins than pure distribution. And critically, their private equity DNA had instilled a discipline around cash management and debt levels that proved lifesaving.

The company also made a counterintuitive decision: they continued to invest in their best people and maintained relationships with key customers, even when those customers weren't buying much. Sherman understood that homebuilders who survived would remember who stood by them during the darkest days. This wasn't charity—it was a calculated bet that the housing market would eventually recover, and when it did, relationships would matter more than ever. By 2010, the first green shoots of recovery began to appear. Builders FirstSource starts to see signs of turnaround. For the first time in five years, the company announces revenues exceeding $1 billion. It wasn't much—barely a third of what the company would eventually achieve—but after years of contraction, any growth felt like a victory. In three years' time, it will triple those results.

The survivors of the Great Recession emerged changed. Builders FirstSource had proven it could endure the unthinkable. The company had maintained its core capabilities, preserved key relationships, and kept enough powder dry to eventually go on offense. While dozens of competitors had disappeared—either through bankruptcy, liquidation, or distressed sales—Builders FirstSource was still standing.

But survival alone doesn't create value. Sherman and his team understood that the post-crisis landscape presented a once-in-a-generation opportunity. The industry had been devastated, yes, but that devastation had created massive consolidation opportunities. Distressed assets were available at fraction of pre-crisis valuations. Competitors were weakened or gone entirely. And most importantly, when housing eventually recovered—and demographics suggested it had to—there would be far fewer suppliers to meet that demand.

The stage was set for Builders FirstSource's next act. They had survived the storm. Now it was time to rebuild—not just their own business, but to fundamentally reshape the entire industry. The lessons learned during those dark years from 2008 to 2010 would inform every major decision that followed. Risk management became religion. Cash generation became paramount. And the understanding that housing is cyclical—brutally, unavoidably cyclical—became embedded in the company's DNA.

IV. The ProBuild Mega-Deal: Creating a National Player (2015)

Floyd Sherman stood before the assembled executives in the Builders FirstSource boardroom in early 2015, a map of the United States spread across the conference table. Red pins marked Builders FirstSource locations, clustered heavily in the South and Southeast. Blue pins showed ProBuild's footprint, dominating the West and Northeast. "Gentlemen," Sherman said, his 76-year-old voice still commanding, "this is what a national champion looks like." He swept his hand across the combined territories. "The question is: are we bold enough to make it happen?"

The housing market had finally turned the corner. After years of anemic recovery, single-family housing starts were approaching 700,000 units annually—still far below the pre-crisis peak, but trending decisively upward. More importantly, the supply-demand imbalance was becoming impossible to ignore. Years of underbuilding had created a shortage of homes that would take a decade or more to resolve. For a building materials supplier, this wasn't just opportunity—it was destiny calling. ProBuild's history was itself a cautionary tale of industry consolidation. ProBuild was created in 2006 by Devonshire Investors, the private equity firm affiliated with FMR LLC, the parent company of Fidelity Investments. In 1997, Fidelity Capital, the business development arm of Fidelity Investments, acquired the Strober Organization, a supplier of building materials to professional builders and contractors in the Northeast. In 2008, Fidelity Capital purchased Lanoga Corporation, which was, at the time, the nation's third-largest professional building materials dealer, creating ProBuild through these combined entities.

ProBuild had entered the Great Recession as arguably the nation's largest building materials dealer, with $6 billion in revenue and 17,000 employees. But the housing crash nearly destroyed the company—revenues were cut in half, and Devonshire reportedly pumped hundreds of millions of dollars just to keep it afloat. By 2014, ProBuild had stabilized at roughly $4.5 billion in revenue, but it had never achieved the synergies or market dominance originally envisioned.

For Builders FirstSource, ProBuild represented the deal of a lifetime. The all-cash transaction is valued at approximately $1.63 billion—a price that would have been unthinkable just a few years earlier. The combination creates a diversified national pro dealer with 2014 combined revenues of approximately $6.1 billion. More importantly, it filled critical geographic gaps: ProBuild's strength in the West and Northeast perfectly complemented Builders FirstSource's Southern and Southeastern dominance.

Sherman's vision went beyond mere geography. "This isn't just about getting bigger," he told analysts on the deal announcement call. "It's about building a platform that can serve any professional builder, anywhere in the country, with any product they need." The combined company would operate in 24 of the 25 largest U.S. metropolitan areas, with over 430 locations across 40 states.

The financing structure revealed the confidence behind the deal. Builders FirstSource obtained fully committed financing comprising a rollover of Builders FirstSource's $350 million existing Senior Secured Notes, new debt issuance in the form of $295 million drawn under a new $800 million ABL facility, and a new $550 million Term Loan B. The company also planned to issue $750 million in new Senior Unsecured Notes and $100 million of new equity. It was aggressive leverage—5.6x net debt to adjusted EBITDA on a pro forma basis—but Sherman and his team believed the $100-120 million in expected annual cost synergies would quickly bring that down.

The integration would be Sherman's final major act as CEO. At 76 years old, he had transformed Builders FirstSource from a regional player into a national powerhouse. But executing on the ProBuild integration would require a different kind of leadership—someone who could manage complexity at scale while maintaining the entrepreneurial spirit that had defined the company's first two decades.

The market's initial reaction was mixed. Some investors worried about integration risk and the debt load. Others saw the strategic logic but questioned whether the synergies were achievable. But inside Builders FirstSource, there was a sense of destiny fulfilled. They had survived the Great Recession. They had consolidated when others couldn't. And now, with ProBuild, they had achieved true national scale.

What nobody could have predicted was that this transformative deal was just the opening act. The real consolidation story was still to come.

V. The BMC Merger: Doubling Down on Dominance (2020-2021)

Dave Flitman stared at his computer screen in his home office, the August 2020 heat blazing outside his Dallas window. As CEO of BMC Stock Holdings, he was about to dial into the most important call of his career. On the other end would be Chad Crow, who had succeeded Floyd Sherman as CEO of Builders FirstSource in 2018. The world was six months into a global pandemic. Lumber prices were going haywire. Supply chains were in chaos. And these two industry titans were about to discuss merging their companies in an $11.7 billion all-stock deal that would create an undisputed industry leader. The context for this mega-merger was unlike anything the industry had seen before. COVID-19 had initially frozen construction activity in March 2020, but by summer, something remarkable was happening. Low mortgage rates, combined with a sudden shift to remote work, had triggered an unexpected housing boom. Lumber prices were skyrocketing—they would eventually quadruple from pre-pandemic levels. Supply chains were in chaos, with materials either unavailable or priced at astronomical levels. Yet demand for new homes, particularly in suburbs and smaller cities, was exploding.

Under the terms of the agreement, which has been unanimously approved by the Boards of Directors of both companies, BMC shareholders will receive a fixed exchange ratio of 1.3125 shares of Builders FirstSource common stock for each share of BMC common stock. Upon completion of the merger, existing Builders FirstSource shareholders will own approximately 57% and existing BMC shareholders will own approximately 43% of the combined company on a fully diluted basis.

BMC itself was no stranger to consolidation. The company had been formed through its own series of mergers, most notably combining with Stock Building Supply in 2015. With roughly $5.7 billion in revenue, BMC brought particular strength in millwork, its READY-FRAME lumber reduction system, and a strong presence in growth markets across the West and Southeast. The combined company would operate a network of approximately 550 distribution and manufacturing locations, with a presence in 40 states, including 44 of the top 50 metropolitan statistical areas.

The leadership transition plan was elegant and reflected the merger of equals nature of the deal. After a 90-day transition period following the completion of the merger, Chad Crow, current Chief Executive Officer of Builders FirstSource, will retire as previously announced and will be succeeded as Chief Executive Officer of the combined company by Dave Flitman, current Chief Executive Officer of BMC. Crow, who had joined Builders FirstSource in 1999 and served as CFO during the dark days of the financial crisis, would hand the reins to Flitman, ensuring continuity while bringing fresh perspective.

Flitman's vision for the combined entity was expansive: "This strategic combination of two great organizations is an exciting step forward for both BMC and Builders FirstSource. This transformational merger will enable BMC to further accelerate our profitable growth strategy with a company that also focuses on providing a broad product portfolio and differentiated capabilities deployed through a customer-focused service model."

The expected synergies were substantial—$130 million to $150 million annually by year three. But unlike many merger promises, these weren't just theoretical. Both companies knew each other's operations intimately. They understood where facilities could be consolidated, where procurement could be optimized, and where best practices from each organization could be applied across the combined footprint.

The close of the merger creates the nation's premier supplier of building materials and services, with combined sales of approximately $11.7 billion as of the twelve months ended September 30, 2020. The transaction closed on January 1, 2021—a New Year's Day that marked not just a new beginning for the combined company, but the creation of an industry colossus.

What made this merger particularly remarkable was its timing. Executing a transformational deal during a global pandemic required extraordinary coordination. Due diligence was conducted virtually. Integration planning happened over Zoom calls. Yet both teams managed to maintain momentum, driven by the strategic logic of the combination and the once-in-a-generation market opportunity emerging from the pandemic-driven housing boom.

The market loved it. Shares of both companies surged on the announcement, with BMC jumping 22.4% and Builders FirstSource rising 8.4%. Investors understood what the companies' leadership teams had recognized: in a fragmenting world, scale matters more than ever. The ability to source materials, manage logistics, and serve customers across the entire country would be a decisive competitive advantage in the post-pandemic economy.

VI. Business Model & Competitive Advantages

Walk into a Home Depot on a Saturday morning and you'll see weekend warriors loading their pickup trucks with a few two-by-fours and some plywood. Now drive across town to a Builders FirstSource location at 6 AM on a weekday, and you'll witness something entirely different: a choreographed ballet of forklifts loading flatbed trucks with pre-assembled roof trusses, custom millwork packages sorted by job site, and engineered lumber systems designed specifically for that day's construction projects. This isn't retail—it's the professional building materials business, and understanding the difference is key to understanding why Builders FirstSource has become so dominant.

The professional builder focus versus retail model represents the fundamental strategic choice that defines Builders FirstSource. While Home Depot and Lowe's serve consumers and small contractors who need materials today for projects happening now, Builders FirstSource serves professional builders who need complex, coordinated deliveries of customized products delivered just-in-time to multiple job sites. It's the difference between selling ingredients and delivering a prepared meal—except the meal is a house, and the stakes are measured in millions of dollars.

The value-added manufacturing capabilities are where Builders FirstSource truly differentiates itself. Take roof trusses, for example. A traditional approach would have framers cutting and assembling rafters on-site—a labor-intensive process prone to weather delays and measurement errors. Builders FirstSource manufactures these trusses in climate-controlled facilities using precision equipment, delivering them to the job site ready to install. This saves builders time, reduces labor costs, and improves quality. The company's manufacturing capabilities include trusses (roof and floor), wall panels, custom millwork, aluminum and vinyl windows, and pre-hung door fabrication.

The company serves single-family, multi-family construction, and repair/remodeling. The single-family segment, representing the largest portion of revenue, benefits from the chronic undersupply of homes in America—a deficit that would take years to resolve even if construction accelerated dramatically. Multi-family construction provides diversification and exposure to urban markets where apartments and condominiums dominate. The repair and remodeling segment offers counter-cyclical characteristics—when new construction slows, homeowners often invest in upgrading existing properties.

The geographic strategy reflects decades of careful expansion and strategic acquisition. With approximately 600 distribution and manufacturing locations across 43 states and presence in 92 of the top 100 Metropolitan Statistical Areas, Builders FirstSource has achieved something remarkable: national scale with local expertise. Each location maintains relationships with local builders, understands regional building codes, and can respond to local market conditions while leveraging the purchasing power and operational excellence of a $17+ billion enterprise.

The "one-stop shop" approach creates powerful customer stickiness. A production builder constructing hundreds of homes annually doesn't want to coordinate with dozens of suppliers. They want a single partner who can provide everything from foundation materials to roof shingles, with the logistics expertise to coordinate deliveries across multiple job sites. Once Builders FirstSource becomes embedded in a builder's operations—with dedicated account managers, integrated systems, and established delivery schedules—switching costs become prohibitive.

Digital transformation, accelerated by the WTS Paradigm acquisition in 2021, represents the next frontier. BFS acquires WTS Paradigm, a software solutions and services provider for the building products industry. Paradigm's technology platform allows builders to design homes, generate bills of materials, receive quotes, and manage orders through integrated digital tools. This isn't just about efficiency—it's about becoming so embedded in the builder's workflow that Builders FirstSource becomes indispensable.

The competitive moat continues to widen. Local lumber yards lack the scale to match Builders FirstSource's pricing or product breadth. Regional players can't offer the national footprint that large production builders require. And while Home Depot and Lowe's dominate retail, they're not structured to provide the specialized service, credit terms, and job-site delivery that professional builders demand.

But perhaps the most underappreciated competitive advantage is the company's deep understanding of construction cycles and risk management. Having survived the 2008 financial crisis and thrived through COVID-19, Builders FirstSource has developed a culture of disciplined capital allocation and operational flexibility. They know when to expand aggressively and when to pull back, when to invest in new capabilities and when to focus on optimization.

The numbers tell the story of this model's power. Gross margins have expanded steadily as value-added products grow as a percentage of sales. Customer retention rates among large builders exceed 90%. And the company generates robust free cash flow even during industry downturns, providing the financial flexibility to invest countercyclically.

This isn't a commodity business anymore—it's a value-added manufacturing and logistics enterprise that happens to operate in the building materials space. And that transformation is why Builders FirstSource trades at multiples that would have been unthinkable for a lumber yard just a decade ago.

VII. Modern Era: Technology, Sustainability & Future Bets (2021-Present)

Dave Flitman stood before the opening bell podium at the New York Stock Exchange on July 19, 2021, surrounded by his leadership team. Builders FirstSource completes listing transfer to the New York Stock Exchange. The BFS leadership team rings the opening bell. The symbolic move from NASDAQ to NYSE represented more than just a change of venue—it was a declaration that Builders FirstSource had graduated from growth company to established blue chip. The company that had started as a Texas roll-up was now positioned alongside America's industrial giants.

The post-merger integration with BMC was proceeding better than anyone had dared hope. Despite executing the combination during a pandemic, the company was capturing synergies faster than projected. But Flitman and his team understood that past success meant nothing in a rapidly evolving market. The question wasn't whether they could integrate BMC—that was already proving successful. The question was whether they could transform a traditional building materials company into a technology-enabled solutions provider for the digital age.

The August 2021 acquisition of WTS Paradigm for an undisclosed amount was the opening salvo in this transformation. Paradigm wasn't just software—it was a complete ecosystem for digitizing the homebuilding process. Builders could use Paradigm's tools to design homes, automatically generate optimized bills of materials, receive real-time pricing, and manage orders across multiple job sites. For Builders FirstSource, it meant capturing the customer relationship at the very beginning of the construction process, before a single board was cut.

The sustainability initiatives, particularly the READY-FRAME lumber reduction system inherited from BMC, addressed a critical industry challenge. With lumber prices volatile and environmental concerns mounting, builders needed ways to reduce material usage without compromising structural integrity. READY-FRAME uses advanced engineering to optimize lumber placement, reducing material usage by up to 30% while actually improving strength. It's the kind of innovation that saves builders money while supporting environmental goals—a win-win that creates lasting customer loyalty.

Supply chain resilience became a strategic imperative after COVID-19 exposed the fragility of global logistics networks. Builders FirstSource responded by diversifying supplier relationships, increasing inventory buffers for critical materials, and investing in supply chain visibility tools. When competitors struggled to source materials during the 2021-2022 supply chain crisis, Builders FirstSource's scale and relationships allowed it to maintain better availability—a difference that won long-term customer commitments. The ultimate validation came in December 2023. Builders FirstSource Inc. will join the S&P 500 Index before trading opens Dec. 18, according to S&P Dow Jones Indices. Jabil Inc. and Builders FirstSource Inc. are set to join too. The inclusion in the S&P 500—a significant achievement reflecting the company's growth and position as the industry leader—meant that index funds would become permanent shareholders, providing stability and liquidity that would have been unimaginable during the dark days of 2008.

The competitive landscape continues to evolve with new threats and opportunities. Competition from new entrants leveraging technology, evolving builder needs for more sustainable materials, and the ongoing challenge of housing affordability all require constant innovation. But Builders FirstSource's response has been to lean into these challenges. They're not just distributing materials—they're becoming partners in solving the housing crisis.

The digital transformation extends beyond software. The company is investing in automation at distribution centers, using data analytics to optimize inventory levels, and exploring partnerships with construction technology startups. The goal is ambitious: to make building a home as efficient and predictable as manufacturing a car.

Environmental sustainability has moved from nice-to-have to business imperative. Beyond READY-FRAME, the company is exploring cross-laminated timber, recycled materials, and other sustainable building products. As environmental regulations tighten and consumers demand greener homes, Builders FirstSource is positioning itself as the sustainable choice for professional builders.

The housing affordability crisis presents both challenge and opportunity. With median home prices reaching record levels and mortgage rates elevated, builders are under pressure to reduce costs without sacrificing quality. Builders FirstSource's value-added products—which reduce labor costs and construction time—become even more valuable in this environment. The company's scale allows it to negotiate better prices with manufacturers, savings that can be passed along to builders and ultimately to homebuyers.

Recent strategic moves signal continued ambition. Small tuck-in acquisitions continue to fill geographic gaps and add specialized capabilities. The company maintains a disciplined approach to capital allocation, balancing growth investments with shareholder returns through buybacks and dividends. The balance sheet remains strong, with leverage ratios well within target ranges despite the massive BMC integration.

Looking ahead, the company faces a complex set of opportunities and challenges. The chronic housing shortage suggests years of elevated demand. The aging housing stock requires massive renovation and repair investment. But interest rates, regulatory changes, and economic uncertainty all pose risks. The key to Builders FirstSource's continued success will be maintaining the operational excellence and financial discipline that have defined its journey while continuing to innovate and adapt to changing market conditions.

This modern era represents the culmination of a 26-year journey from regional startup to national champion. But for Dave Flitman and his team, it's just the beginning. The vision now extends beyond being the largest to being the most innovative, the most sustainable, and the most essential partner in solving America's housing challenges.

VIII. Playbook: Lessons in Roll-Up Strategy

There's a moment in every successful roll-up strategy where the acquirer stops buying companies and starts buying capabilities. For Builders FirstSource, that inflection point came somewhere between the ProBuild acquisition and the BMC merger. Understanding this evolution—from financial engineering to operational excellence to strategic transformation—reveals why some roll-ups create lasting value while others collapse under their own weight.

The private equity DNA embedded at founding proved crucial. A management team supported by JLL Partners, a private investment firm, acquires Builders' Supply & Lumber Company from The Pulte Corporation. JLL Partners and later Warburg Pincus didn't just provide capital—they instilled a discipline around value creation that transcended any single deal. Every acquisition had to meet strict return hurdles. Integration plans were developed before deals closed. Synergies were tracked religiously, with accountability down to the facility level.

The art of mega-mergers—ProBuild and BMC integration lessons—deserves its own business school case study. ProBuild taught them that cultural integration matters as much as operational synergies. You can't just slap a new logo on facilities and call it done. The BMC merger, executed during COVID-19, proved that with the right systems and processes, even massive integrations can proceed smoothly. The key was maintaining local relationships while centralizing procurement, standardizing best practices without destroying entrepreneurial spirit, and giving acquired management teams real roles in the combined entity.

Managing through cycles—2008 survival to 2020 opportunism—revealed the importance of financial flexibility. The companies that survived 2008 weren't necessarily the biggest or most profitable going into the crisis. They were the ones with variable cost structures, diverse revenue streams, and management teams willing to make hard decisions quickly. When COVID-19 hit, Builders FirstSource had the balance sheet strength and operational flexibility to not just survive but to execute a transformative merger while competitors struggled to maintain operations.

Scale economics in a fragmented industry create compounding advantages. They've acquired around 50 businesses since their founding. With each acquisition, purchasing power increases. The company can negotiate better terms with manufacturers, invest in technology that smaller competitors can't afford, and spread fixed costs across a larger revenue base. But scale without operational excellence is just bloat. The discipline to continuously optimize operations, eliminate redundancies, and reinvest savings into growth separates winners from losers.

Value-added services as margin expansion represent the evolution from commodity distributor to solutions provider. Every roof truss manufactured, every wall panel assembled, every custom millwork piece produced transforms a low-margin commodity transaction into a higher-margin, stickier customer relationship. Their manufacturing capabilities include trusses (roof and floor), wall panels, custom millwork, aluminum and vinyl windows, and pre-hung door fabrication. The lesson: in commodity businesses, the only sustainable differentiation is adding value that customers can't easily replicate themselves.

Capital allocation—when to buy vs. build vs. return capital—requires constant recalibration. The early years were about buying everything that made strategic sense. The middle years focused on operational improvement and organic growth. The recent past has seen massive transformational deals. And now, with the company generating robust free cash flow and the acquisition pipeline more selective, returning capital through buybacks becomes appropriate. The key is maintaining flexibility to pivot as opportunities arise.

The integration playbook has been refined through repetition:

Week 1-2: Establish communication cadence with acquired employees, meet key customers to assure continuity, and identify quick wins that demonstrate value.

Month 1-3: Integrate purchasing to capture immediate cost savings, standardize safety protocols and training, and map cultural differences and address concerns.

Month 3-6: Implement common systems and processes, optimize facility footprint and inventory, and identify and promote key talent from acquired company.

Month 6-12: Fully integrate sales teams and customer relationships, complete technology systems integration, and measure and report on synergy capture.

The pattern recognition that comes from dozens of acquisitions creates institutional knowledge that becomes its own competitive advantage. The company knows which integration mistakes to avoid, which synergies are real versus illusory, and how to maintain business momentum during transition periods.

But perhaps the most important lesson is knowing when not to acquire. The discipline to walk away from deals that don't meet strategic or financial criteria, even when pressure to grow is intense, separates successful roll-ups from empire builders. Every deal changes the company's DNA slightly. Too many bad deals, and you wake up one day with an unmanageable, unfocused conglomerate.

The playbook continues to evolve. Digital capabilities require different integration approaches than physical facilities. Sustainability initiatives need longer investment horizons than traditional cost-cutting. And as the company grows larger, each acquisition's relative impact decreases, requiring bigger, more transformational deals to move the needle.

What started as a financial engineering play has evolved into something far more sophisticated—a repeatable process for identifying, acquiring, integrating, and optimizing businesses in a way that creates value for all stakeholders. That transformation from financial buyer to strategic operator represents the maturation not just of Builders FirstSource, but of the roll-up strategy itself.

IX. Bear vs. Bull Case Analysis

The investment community remains divided on Builders FirstSource, with compelling arguments on both sides. The bulls see a generational opportunity backed by demographic tailwinds and competitive advantages that only strengthen with scale. The bears worry about cyclical exposure, integration risks, and the possibility that the best days are already behind us. Let's examine both cases with the rigor they deserve.

Bull Case: The Demographic Destiny

The math is inescapable. America is short somewhere between 3 and 7 million homes, depending on which economist you ask. After the Great Recession, the number of home builders declined significantly, and housing production was unable to meet buyer demand. This deficit of housing in the United States continues to exist because of persistent supply-side headwinds for builders. Millennials, the largest generation in U.S. history, are entering prime homebuying years. Gen Z is right behind them. Even if housing starts merely return to historical averages—let alone make up for the deficit—Builders FirstSource wins.

The dominant market position with massive scale advantages can't be replicated. With 600 locations, relationships with every major builder, and manufacturing capabilities that local competitors can't match, Builders FirstSource has achieved escape velocity. The cost to replicate this infrastructure would be prohibitive, and the time required would be measured in decades, not years.

Margin expansion through value-added products tells a powerful story. As builders face labor shortages and time pressures, the willingness to pay for pre-fabricated components only increases. Every truss, panel, and custom millwork piece sold transforms a commodity transaction into a value-added relationship with switching costs that compound over time.

Consolidation opportunities remain abundant despite all the acquisitions to date. The building materials industry remains highly fragmented, with thousands of small, family-owned operations struggling with succession planning, technology investment, and scale disadvantages. Builders FirstSource can continue rolling up these operations at reasonable multiples, immediately capturing synergies through purchasing power and operational improvements.

Digital transformation potential could be the biggest opportunity of all. The construction industry has been one of the slowest to digitize, but that's changing rapidly. Builders FirstSource's investments in technology—from design software to supply chain visibility tools—position it to capture value as the industry modernizes. Imagine a future where builders design homes in Paradigm software, automatically generate optimized bills of materials, and seamlessly order through Builders FirstSource's integrated platform. That's not science fiction—it's happening today, just not at scale yet.

Bear Case: The Cyclical Sword

Cyclical exposure to the housing market remains the fundamental risk. Housing is perhaps the most cyclical industry in America, and Builders FirstSource is leveraged to that cycle. When housing turns down—and it always eventually does—the company's results will suffer. The 2008 experience, while ultimately survivable, showed how brutal these downturns can be.

Interest rate sensitivity compounds the cyclical risk. With mortgage rates elevated and the Federal Reserve committed to controlling inflation, housing affordability has deteriorated significantly. Every percentage point increase in mortgage rates prices out millions of potential buyers, reducing demand for new construction and, consequently, for building materials.

Commodity price volatility adds another layer of complexity. Lumber prices can swing 50% or more in a matter of months, creating margin pressure and inventory risk. While Builders FirstSource tries to pass through price changes, there's always a lag, and rapid deflation can catch the company with high-cost inventory.

Integration execution risks multiply with each acquisition. The BMC merger was the largest in company history, and while integration is proceeding well, the law of large numbers suggests that eventually, something will go wrong. Cultural clashes, systems integration failures, or key customer defections could derail the expected synergies.

Competition from new business models represents an emerging threat. What if Amazon decides to seriously enter building materials distribution? What if venture-backed startups figure out how to digitally disintermediate traditional distribution? What if builders themselves vertically integrate? The company's moat is wide, but it's not infinitely deep.

The Balanced View

The truth, as always, lies somewhere in between. Builders FirstSource has built something remarkable—a scaled, national platform in a fragmented industry with genuine competitive advantages and exposure to favorable long-term trends. But it's not immune to cycles, execution risks, or disruption.

The key variables to watch:

- Housing starts and permits as leading indicators

- Mortgage rate movements and their impact on affordability

- Integration metrics from the BMC merger

- Value-added product mix and margin trends

- Digital adoption rates among builders

- M&A activity and capital allocation decisions

For long-term investors, the question isn't whether Builders FirstSource will face challenges—it will. The question is whether the structural advantages and market position are strong enough to weather those challenges while capturing the upside from America's housing shortage. History suggests they are, but history doesn't always repeat.

X. Epilogue & Strategic Outlook

As Dave Flitman looks out from his office window in Irving, Texas, the view encompasses more than just the Dallas skyline. It represents the geographic heart of American homebuilding—a region where Builders FirstSource has grown from a small regional player to the industry's dominant force. The company that started with a simple premise—consolidating a fragmented industry—has evolved into something far more complex and valuable: an essential infrastructure provider for American housing.

Current market position and financial performance tell a story of successful execution. With over $17 billion in revenue, approximately 28,000 employees, and a market capitalization that has earned S&P 500 inclusion, Builders FirstSource has achieved the scale and stability that seemed impossible during the 2008 crisis. Yet the leadership team maintains the urgency of a startup, understanding that past success guarantees nothing in a rapidly evolving market.

The next chapter—where does BLDR go from here?—will be defined by several strategic imperatives. First, completing the BMC integration while maintaining operational excellence. Second, continuing to shift mix toward higher-margin, value-added products. Third, leveraging technology to become even more embedded in builders' workflows. And fourth, maintaining the financial flexibility to act opportunistically when the next crisis inevitably creates opportunities.

Potential acquisition targets or strategic pivots remain on the table. While the mega-merger phase may be complete, tuck-in acquisitions that add capabilities or fill geographic gaps continue. More intriguingly, the company might expand into adjacent markets—commercial construction, infrastructure, or even direct-to-consumer renovation. The discipline will be maintaining focus while exploring growth opportunities.

The lessons for entrepreneurs and investors in mature industries are profound. Builders FirstSource proves that even in old-economy sectors, massive value creation is possible through operational excellence, strategic consolidation, and customer focus. The company didn't invent building materials or discover some new technology. It simply executed better than competitors, maintained discipline through cycles, and built scale advantages that compound over time.

Final reflections on building a category killer through M&A reveal universal truths about business building. Culture matters as much as strategy. Financial discipline enables strategic flexibility. Customer relationships are the ultimate moat. And perhaps most importantly, success requires both the courage to make bold moves and the wisdom to know when not to act.

The housing affordability crisis that defines our current moment presents both the company's greatest challenge and opportunity. If America is going to build its way out of the housing shortage, it will need Builders FirstSource's products, services, and expertise. The company that survived the housing collapse of 2008 is now positioned to enable the housing expansion of the 2020s and beyond.

But this isn't a victory lap—it's a progress report. The building materials industry will continue evolving. New technologies will emerge. Competitors will adapt. Regulations will change. Economic cycles will turn. The only constant is change itself.

What makes Builders FirstSource compelling isn't that it's immune to these challenges—it's that the company has proven, repeatedly, its ability to adapt and thrive through transformation. From a private equity roll-up to a public company, from regional player to national champion, from survivor to acquirer, from distributor to solutions provider—each evolution has made the company stronger.

The story that began in a Dallas conference room in 1998 with a simple acquisition has become something much larger: a testament to the power of execution, the value of persistence, and the importance of building something that matters. In an era of software unicorns and cryptocurrency speculation, Builders FirstSource reminds us that sometimes the biggest opportunities lie in the most fundamental human needs—in this case, the need for shelter.

As America grapples with how to house its growing population affordably and sustainably, Builders FirstSource stands ready with the products, services, and expertise to help build the solution. The company that was built through consolidation is now building America, one home at a time.

The journey from Texas startup to building materials giant is complete. The journey to solve America's housing challenges has just begun.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube