Alliant Energy: The Midwest's Quiet Power Evolution

I. Introduction & Episode Roadmap

Picture this: While Tesla captures headlines and tech giants pledge carbon neutrality, a century-old utility company in Cedar Rapids, Iowa, is quietly orchestrating one of America's most ambitious energy transformations. No flashy press conferences, no celebrity CEOs, just methodical execution in cornfields and dairy country. This is the Alliant Energy story—where the real energy transition is happening, one wind turbine and solar panel at a time.

The paradox is striking. Alliant Energy, serving just 1.4 million customers across Iowa and Wisconsin, has become the third-largest utility owner-operator of regulated wind power in America. They're retiring coal plants faster than utilities twice their size, building solar farms where corn once grew, and somehow keeping electricity rates below the national average. In an era when California blackouts make news and Texas grids fail spectacularly, this Midwest utility maintains 99.98% reliability while completely reimagining its generation portfolio.

Why should anyone outside Des Moines or Madison care? Because Alliant's transformation reveals how America's energy transition will actually unfold—not through Silicon Valley disruption or federal mandates, but through pragmatic engineering and regulatory navigation in states that vote purple and prioritize both farmers and factories. This isn't a story about environmental activism; it's about cold economic logic meeting operational excellence in America's heartland.

The journey ahead traverses a century of Midwest industrialization, corporate mergers that reshaped regional power markets, strategic pivots that nearly broke the company, and a renewable revolution that nobody saw coming from a utility founded when coal was king. We'll explore how a company that once powered Iowa's railroads became a renewable energy pioneer, why Wisconsin dairy farmers now host solar panels alongside their cattle, and what Alliant's quiet transformation tells us about the future of American infrastructure.

II. Origins & The Pre-Merger Era (1900s–1997)

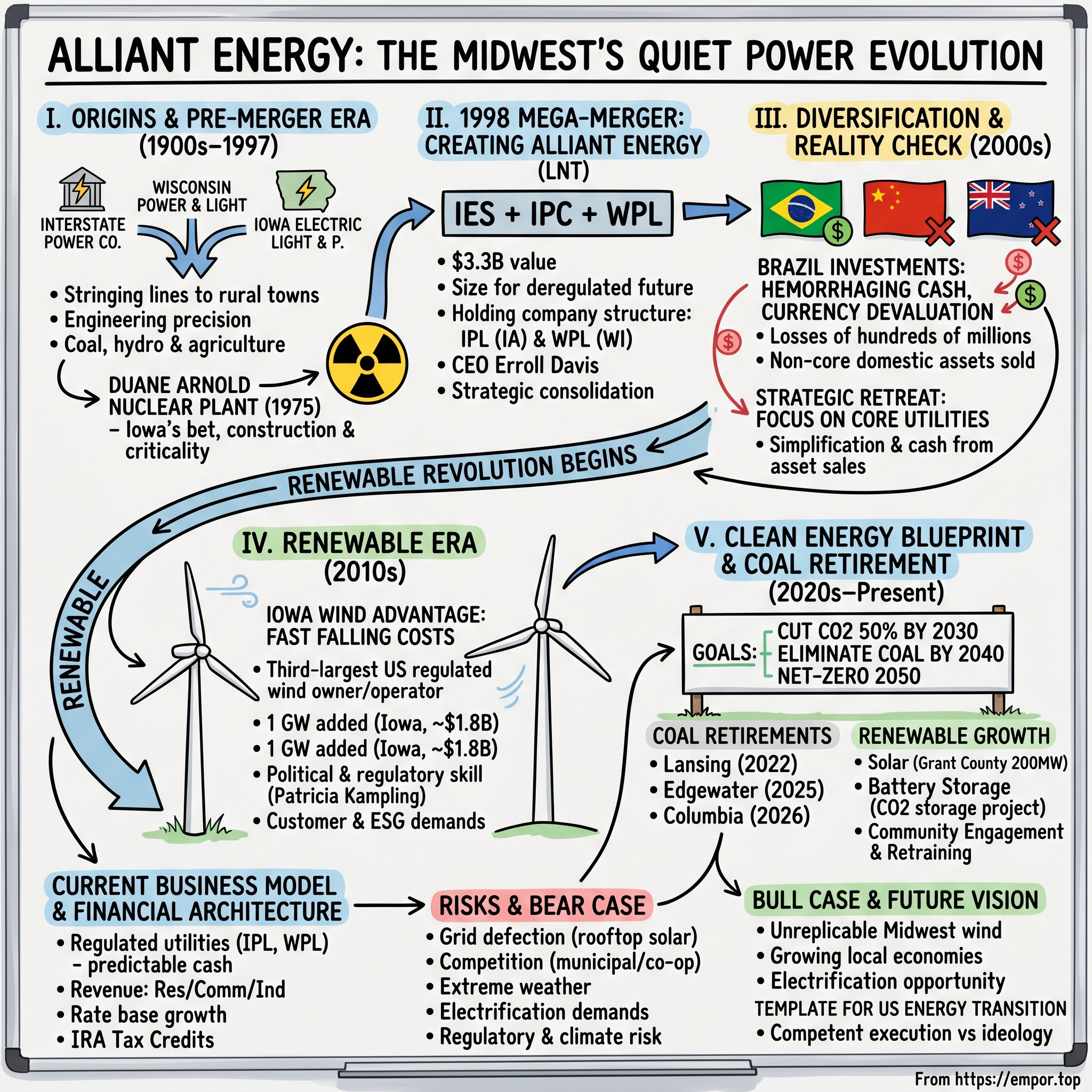

The lights first flickered on in 1917, not in some grand metropolitan ceremony, but across the small towns dotting the Mississippi River between Iowa and Minnesota. Interstate Power Company strung its first transmission lines through cornfields and along railroad tracks, bringing electricity to communities where kerosene lamps still lit most homes. The founders weren't visionaries talking about transforming society—they were engineers and local businessmen who saw opportunity in the mundane miracle of electric power.

By 1924, Wisconsin entered the picture differently. Wisconsin Power and Light emerged from the consolidation of dozens of tiny municipal utilities, each serving a few hundred customers. The company's early leaders, many of them German and Scandinavian immigrants, brought an engineering precision and conservative financial management that would define Wisconsin utilities for generations. They built their systems to withstand brutal winters and serve industries that ran three shifts—paper mills in the Fox Valley, dairy processing in Green County, manufacturers in Madison's growing industrial corridor. Iowa Railway and Light Corporation came next, incorporating in 1925 in Cedar Rapids. IES Utilities incorporated in Iowa in 1925 as the Iowa Railway and Light Corporation, though locals knew it simply as "the electric company." The founders weren't Wall Street financiers but local businessmen who understood that reliable power meant economic development. They built their first hydroelectric plant on the Cedar River, building and operating the first automatic hydroelectric plant in the world in 1917 with a capacity of 20,000 kilowatts—an engineering marvel that ran without human operators, unheard of at the time.

The Great Depression tested everyone. In the 1930s and 1940s, the effects of the Depression and passage of laws to regulate utility operations at the state and federal level had an effect on IPC as well as its neighbors. Small utilities collapsed or merged for survival. Interstate Power somehow expanded, acquiring operations in Iowa, Wisconsin, Minnesota, North and South Dakota, Nebraska, Oklahoma, and Manitoba, Canada in the late 1920s, including the purchase of what became its northern Minnesota territory from the Wilbur Foshay interests. Meanwhile, Iowa Railway and Light changed its name to Iowa Electric Light & Power Company in 1932, signaling its ambitions beyond just Cedar Rapids.

World War II transformed everything. Power demand exploded as Iowa factories converted to military production. The utilities ran their coal plants at maximum capacity, postponing maintenance, pushing equipment past design limits. Engineers worked triple shifts keeping the lights on for defense plants producing everything from ammunition to corn-based ethanol for synthetic rubber. The post-war boom that followed seemed to validate every infrastructure investment—suburban expansion, new factories, the beginning of agricultural mechanization that would transform Iowa farming.

Then came the atomic age. In a decision that would define the company for decades, IES authorized the construction of the Duane Arnold nuclear plant at Palo in 1968. The 615-megawatt facility represented Iowa's bet on nuclear power—clean, modern, seemingly limitless. It was an engineering triumph and a financial gamble that would take decades to fully pay off. Construction began in 1970 and the plant began licensed operations in 1975. Construction was completed and the reactor reached initial criticality on March 23, 1974. The cost was $50 million over budget. Commercial operations began on February 1, 1975. For a utility serving rural Iowa, this represented an enormous gamble on technology and scale.

The parallel tracks continued through the 1980s and early 1990s. Interstate Power expanded and contracted like an accordion—picking up properties adjacent to its system and more easily interconnected: the Eastern Iowa Power system, and the Iowa/Minnesota properties of the Central States Power and Light Corporation. Wisconsin Power and Light pursued steady, conservative growth, serving the state's manufacturing base with remarkable reliability. Neither company was particularly sexy or innovative—they were utilities, after all—but both generated steady dividends and kept the lights on.

By the mid-1990s, the logic of consolidation became undeniable. IES and IPC merged in the mid-1990s to form IPL, creating Interstate Power and Light Company. The name changes tell the story: Iowa Electric Light & Power became IES Utilities Inc. in 1994, signaling modernization. These weren't just rebranding exercises—they reflected fundamental shifts in how utilities saw themselves, from local power providers to regional energy companies preparing for deregulation that everyone assumed was coming.

III. The 1998 Mega-Merger: Creating Alliant Energy

The conference room at the Des Moines Marriott hummed with nervous energy on that April morning in 1998. Executives from IES Industries and WPL Holdings sat across from each other, investment bankers flanking both sides, as they prepared to sign documents creating what would become Alliant Energy Corporation. The merger valued at $3.3 billion wasn't just combining two utilities—it was betting that scale would matter in the deregulated future everyone expected. In 1998, Alliant Energy Corporation was officially formed through the merger of IES Industries, Inc. and WPL Holdings, Inc. The company was actually formed as a three-way merger between IES Industries, Inc., Interstate Power Co., and WPL Holdings, Inc., with Interstate Power being folded into the new structure. The architect of this transformation was Erroll Davis, who became the first President and CEO of Alliant Energy in April 1998, and became Chairman of the Board in April 2000.

The strategic rationale seemed bulletproof at the time. Deregulation was sweeping through utilities—California was opening its markets, Texas was restructuring, and everyone assumed the Midwest would follow. Size meant negotiating power with suppliers, efficiency in operations, and the ability to compete when residential customers could eventually choose their power provider. The combined company would serve nearly a million electric customers and 400,000 gas customers across Iowa and Wisconsin, creating economies of scale that neither predecessor could achieve alone.

This strategic consolidation established Alliant Energy as a regulated utility holding company with two primary subsidiaries: Interstate Power and Light Company (IPL) and Wisconsin Power and Light Company (WPL). The structure was deliberately maintained as two separate operating utilities—a decision that would prove prescient when deregulation stalled and state-level regulation remained paramount.

The name itself—Alliant Energy—signaled ambition beyond traditional utility operations. This wasn't going to be "Iowa-Wisconsin Power Company." The board chose a name suggesting alliances, partnerships, and energy solutions rather than just electricity delivery. Interstate Energy Corporation currently does business under the name Alliant Energy, though technically the legal entity remained Interstate Energy Corporation until a formal name change in May 1999.

Integration proved harder than the bankers' models suggested. Iowa and Wisconsin had different regulatory frameworks, different rate structures, different corporate cultures. The Iowa operations, centered in Cedar Rapids, had a more entrepreneurial bent—they'd built a nuclear plant, after all. Wisconsin Power and Light, based in Madison, operated with Germanic precision and conservative financial management. Merging IT systems took three years. Harmonizing union contracts took longer. Some executives from both sides quietly left, unable to adapt to the new reality.

But the timing, in retrospect, was fortuitous. The merger closed just before the 2000-2001 California energy crisis demonstrated the dangers of poorly designed deregulation. While Enron imploded and merchant generators went bankrupt, Alliant Energy's boring regulated utility model suddenly looked brilliant. The company had scale without speculation, growth without gambling.

IV. The Diversification Years & Reality Check (2000–2010)

The boardroom at Alliant's Madison headquarters buzzed with international ambitions in early 2001. Maps of Brazil covered one wall, feasibility studies for Chinese power plants stacked on the conference table. The company had just acquired interests in power plants in New Zealand and was eyeing opportunities from Mexico to Malaysia. The logic seemed irrefutable: emerging markets needed power, Alliant had expertise, and Wall Street loved growth stories.

The early 2000s presented significant challenges for Alliant Energy, including financial difficulties stemming from an economic downturn and high energy prices. Additionally, the company faced increasing environmental regulations. But these challenges paled compared to what the international ventures would bring. The Brazilian operations hemorrhaged cash as currency devaluations destroyed dollar returns. The Chinese partnerships became mired in local politics and corruption allegations that Alliant's Midwestern executives couldn't navigate. New Zealand's regulatory changes turned profitable assets into liabilities overnight. The numbers tell the brutal story. Alliant Energy's Brazil investments resulted in pre-tax, non-cash asset valuation charges of $334 million (after-tax charges of $202 million, or $1.73 per share) in 2005. Alliant Energy completed the sale of its Brazil investments in January 2006. The company had entered Brazil with great fanfare—"We expect our Brazil investments to be slightly accretive to earnings in 2001 and then to add approximately thirty cents, forty cents and fifty cents per share in the years 2002, 2003 and 2004 respectively," management had promised in 2001. Instead, they lost hundreds of millions.

The 2008 financial crisis arrived just as Alliant was trying to clean up its international mess. Credit markets froze, electricity demand plummeted as factories closed, and suddenly a utility with stable cash flows looked like genius compared to growth-obsessed peers. The board made a crucial decision: retreat to the core. No more adventures in emerging markets, no more complex financial engineering, just focus on Iowa and Wisconsin utilities.

In late 2007, Alliant Energy received final approval to sell their utility services in Illinois to Jo-Carroll Energy. Alliant Energy sold to ITC Holdings their transmission system (34.5 kV, 69 kV, 115 kV, 161 kV and 345 kV) in Iowa and Minnesota in 2007. The transmission sale was particularly strategic—it raised $483 million in cash while removing the capital burden of maintaining aging infrastructure. Some criticized it as short-sighted, but management knew they needed to simplify.

By 2010, the company had essentially completed its strategic retreat. International operations: divested. Non-core domestic assets: sold. Complex financial structures: unwound. What remained was a boring, predictable Midwest utility serving corn farmers and cheese factories. Wall Street yawned. But inside the company, engineers were noticing something interesting: the wind in Iowa was extraordinary, and the cost of turbines was falling fast.

V. The Renewable Revolution Begins (2010–2020)

The wind gauge at the test site near Storm Lake, Iowa, had been spinning for months, recording data that seemed almost too good to be true. Average wind speeds of 8.5 meters per second at hub height, capacity factors approaching 45%—numbers that made Iowa wind resources rival offshore sites. In 2010, while most utilities were still building natural gas plants, Alliant's engineers presented a radical proposal to the board: become the wind capital of America.

The economics were shifting faster than anyone expected. In 2010, wind power cost $70 per megawatt-hour. By 2015, it had fallen to $45. By 2020, new wind projects were coming in under $20—cheaper than running existing coal plants, forget about building new ones. But Alliant's advantage wasn't just economics; it was geography. Iowa sits in the wind corridor that runs from Texas to Canada, with consistent, strong winds and flat terrain perfect for turbine installation. The company boasted that the additions had made it the third-largest utility owner-operator of regulated wind in the U.S. By the end of 2020, Alliant will have added about 1 GW of wind power in Iowa, with an investment totaling about $1.8 billion. The transformation was staggering—from 300 megawatts of wind power in early 2017 to about one gigawatt by 2020.

But this wasn't just about building turbines. Alliant had to navigate complex political terrain. Iowa is a purple state where farmers vote Republican but love wind lease payments. The company's former CEO, Patricia Kampling, worked both sides of the aisle brilliantly. The former CEO of Alliant Energy, Patricia Kampling, wrote a guest editorial in The Gazette where she wrote that Alliant Energy and the American Wind Association presented Republican U.S. Senator Chuck Grassley of Iowa with AWEA's Wind Champion Award. Grassley, a conservative icon, became wind power's biggest advocate because he saw the economic benefits for rural Iowa.

Customer demand evolved dramatically during this period. In 2010, most commercial customers viewed renewable energy as expensive virtue signaling. By 2020, major corporations were demanding 100% renewable power for their facilities. Data centers, in particular, wanted green energy for their ESG commitments. Iowa's combination of wind resources, cool climate for natural cooling, and stable political environment made it attractive for tech companies' expansion.

Alliant expects the actions taken as part of its "Clean Energy Blueprint for Iowa" will save customers $300 million over the next 35 years. The economics had completely flipped—renewable energy was now the financially prudent choice, not the environmental luxury. Combined, the Upland Prairie and the English Farms wind farms can provide clean power for 168,000 homes a year, while also helping lower fuel costs on monthly bills. The fuel needed to produce wind energy is free and does not create emissions.

The company also began preparing for the electrification wave. In 2016, Alliant began offering a $500 rebate for its customers who purchase a home charging station for electric vehicles. This seemed premature in rural Iowa, but management understood that electrification would drive demand growth for decades.

By 2020, Alliant had fundamentally transformed its generation portfolio without fanfare or controversy. While California utilities faced blackouts and Texas's grid would soon fail catastrophically, this Midwest utility was quietly demonstrating that the energy transition could work.

VI. The Clean Energy Blueprint & Coal Retirement Strategy (2020–Present)

The email landed in employees' inboxes on a gray February morning in 2021: "Alliant Energy Announces Path to Eliminate Coal by 2040." For a company that had burned coal for a century, whose heritage plants had powered Iowa's industrialization, this was revolutionary. But inside the C-suite, it was simply the logical conclusion of years of analysis showing coal couldn't compete economically anymore. Alliant Energy has set goals of cutting CO2 emissions in half by 2030, and eliminating all coal from its generation fleet by 2040. The aspiration extends further: achieve net-zero greenhouse gas emissions from our utility operations by 2050. This wasn't greenwashing or corporate virtue signaling—the math was ruthless. Coal plants required expensive environmental retrofits, faced rising maintenance costs as they aged, and couldn't compete with $20 per megawatt-hour wind power.

The systematic retirement schedule reads like a military campaign plan. Alliant Energy plans to retire its coal plant in Lansing by 2022 and transition its Burlington plant from coal to natural gas by 2021. Alliant Energy announces plans to retire the Edgewater Generating Station in Sheboygan by the end of 2022. Closing the coal generation facility and transitioning to renewable energy will help Alliant Energy customers avoid hundreds of millions of dollars in long-term costs. Alliant Energy now intends to retire Edgewater Generating Station in Sheboygan by June 2025; both remaining Columbia Energy Center units in Portage will be retired by June 2026.The replacement strategy is equally ambitious. By the end of 2024, we're planning to have nearly 1,500 MW of solar energy generation. In Wisconsin, we're adding 1,089 MW of solar energy and in Iowa, we're planning for 400 MW of solar. The company completed constructing its Grant County Solar Project, a 200-MW solar array in Potosi, Wisconsin, in 2024, that can generate enough electricity to power over 70,000 homes.

Battery storage represents the next frontier. Planning to add nearly 450 MW of battery storage across both Iowa and Wisconsin, Alliant is solving renewable energy's intermittency challenge. The Columbia Energy Storage Project, featuring Energy Dome's standard-frame 20MW/200MWh CO2 Battery, would be the first of its kind in the United States—using compressed CO2 for long-duration storage rather than lithium-ion batteries.

The grid modernization effort runs parallel to generation transformation. Smart meters, distribution automation, underground lines in critical areas—all the unglamorous infrastructure that makes the energy transition actually work. This isn't Silicon Valley disruption; it's methodical engineering excellence applied to century-old systems.

Community engagement proved crucial. Each coal plant closure meant hundreds of jobs lost, millions in tax revenue vanishing from small towns. Alliant's approach: early notification, retraining programs for workers, and locating renewable projects in the same communities when possible. The Lansing coal plant closure in 2022, for instance, was paired with plans for solar development in the same county.

By 2024, the transformation was undeniable. After these changes, about half of Alliant's energy production in the state will be from renewable resources. The company that once epitomized coal-powered industrialization had become a clean energy leader without fanfare, protests, or political theater—just quiet execution in America's heartland.

VII. Current Business Model & Financial Architecture

Walk into any investment bank's utilities coverage group, and Alliant Energy appears in the "boring but beautiful" category—regulated returns, predictable cash flows, minimal drama. But beneath this sleepy exterior lies sophisticated financial engineering that funds billions in renewable investments while keeping rates competitive. The model is deceptively simple: deploy capital into rate base, earn allowed returns, repeat.

Alliant Energy Corporation (NASDAQ: LNT) provides regulated energy service to approximately 1 million electric and 425,000 natural gas retail customers across Iowa and Wisconsin. The structure remains deliberately bifurcated—Interstate Power and Light Company serves Iowa, Wisconsin Power and Light Company serves Wisconsin. This isn't corporate complexity for its own sake; it's regulatory arbitrage. Each state has different rules, different politics, different renewable mandates. By maintaining separate utilities, Alliant can optimize for each jurisdiction.

The numbers reveal the strategy's effectiveness. In Iowa, Alliant earns a 9.8% return on equity with a 53% equity ratio in its capital structure. Wisconsin allows slightly higher returns but demands more aggressive renewable targets. The company threads this needle expertly, deploying capital where returns are highest while meeting each state's specific requirements.

Revenue composition tells the real story of Middle America's economy. Residential customers generate about 35% of revenues, commercial 30%, and industrial 35%. Unlike coastal utilities dominated by residential demand, Alliant serves factories, farms, and food processors—the productive economy that actually makes things. Major customers include John Deere manufacturing plants, Hormel food processing facilities, and dozens of ethanol plants that turn Iowa corn into fuel.

The capital allocation strategy has shifted dramatically from the diversification era. No more international adventures or merchant generation. Every dollar goes into regulated infrastructure—wind turbines that qualify for production tax credits, solar panels eligible for investment tax credits, grid modernization that increases reliability. The math is beautiful: deploy $1 billion in renewable projects, earn 10% regulated returns, collect federal tax credits worth 30% of investment, pass some savings to customers, keep the rest.

Rate case management has become an art form. Iowa reviews every two years, Wisconsin every year. The company staggers major investments to smooth rate impacts, uses forward test years to capture growth, and negotiates settlements rather than fighting protracted battles. The result: rate increases that track inflation while funding massive infrastructure transformation.

The strategic advantage of being a pure-play regulated utility becomes clear during market volatility. When natural gas prices spike, Alliant passes costs through to customers via fuel adjustment clauses. When renewable costs plummet, they lock in low prices through 20-year power purchase agreements. Heads they win, tails they don't lose—the beauty of regulated monopoly economics.

But the real financial innovation lies in tax credit monetization. The Inflation Reduction Act extended renewable tax credits through 2032, and Alliant has become expert at harvesting them. Production tax credits for wind, investment tax credits for solar, bonus depreciation for all of it—the company generates more tax credits than it can use, selling excess credits to banks and corporations desperate for ESG wins.

The balance sheet reflects this strategy. Debt-to-equity stands at 47%, investment-grade ratings from all agencies, access to capital markets even during turmoil. Two public energy companies that are principally engaged in the generation and distribution of electricity to retail electric customers. Provides electricity to approximately 500,000 retail electric customers in Iowa. Transports natural gas to approximately 230,000 customers in Iowa. The simplicity masks sophistication—this is financial engineering at its most elegant.

VIII. The Energy Transition Playbook

The control room at Prairie Creek Generating Station hummed with quiet tension on a January morning in 2024. Outside, temperatures hit minus-20 Fahrenheit, electricity demand spiked to record levels, and every coal plant still operating ran at maximum capacity. But Prairie Creek would burn its last coal in 18 months, replaced by solar panels that don't work at night and wind turbines that might not spin during polar vortexes. This is the energy transition's central challenge: maintaining reliability while transforming the generation fleet.

Alliant's playbook for managing this transition has become a case study for utilities nationwide. First principle: retire strategically, not ideologically. Each coal plant closure follows a detailed analysis—remaining useful life, required environmental investments, local grid stability, replacement generation availability. The Lansing plant closed when grid reinforcements were complete. Edgewater retires only after nearby solar farms come online. The uncertainty includes global supply chain and economic challenges along with shifting Midcontinent Independent System Operator (MISO) requirements beyond 2022 and regional short-term reliability concerns. MISO's capacity auction for 2025 saw prices jump to $666.50/MW-day from $30/MW-day the year before, reflecting the grid's struggle with retirements outpacing additions. The operator warned of potential capacity shortfalls, with surplus capacity falling from 6.5 GW in 2023 to just 2.6 GW in 2025.

Managing workforce transitions proved equally complex. Alliant Energy's workforce is represented by collective bargaining agreements with the International Brotherhood of Electrical Workers (IBEW). Each coal plant employs hundreds of workers—operators, maintenance technicians, engineers—many with decades of experience. The company's approach: retraining programs for renewable operations, early retirement packages for older workers, and guarantees that no involuntary layoffs would result from the energy transition.

Community stakeholder management during plant closures required delicate navigation. Small towns losing their largest taxpayer and employer faced existential threats. Alliant's playbook: announce closures years in advance, work with economic development agencies to attract new businesses, and when possible, locate renewable projects in the same communities. The Prairie Creek conversion to natural gas, for instance, preserved jobs while reducing emissions.

The financing puzzle reveals sophisticated financial engineering. Federal production tax credits for wind, investment tax credits for solar, accelerated depreciation—Alliant harvests every available subsidy while maintaining regulated returns. The key insight: renewable projects generate more tax benefits than the company can use, creating a secondary revenue stream selling credits to tax-equity investors.

Technology bets have evolved from ideology to economics. Wind dominates in Iowa where capacity factors exceed 40%. Solar makes sense in southern Wisconsin with better solar resources. Battery storage solves intermittency but remains expensive. Natural gas plants provide reliability but face uncertain carbon regulations. The portfolio approach—diversification across technologies—hedges multiple risks.

The execution risk looms large. Alliant plans to deploy billions in capital over the next decade, all while maintaining grid reliability during the transition. Supply chain disruptions, skilled labor shortages, regulatory delays—any could derail carefully orchestrated plans. Yet the company continues its methodical transformation, one turbine and panel at a time.

IX. Competition, Risks & The Bear Case

The threat doesn't come from traditional competitors but from customers themselves. In affluent Madison suburbs, rooftop solar installations proliferate, each one reducing demand for Alliant's electricity during profitable daytime hours while still requiring grid connection for reliability. This "grid defection" risk—customers generating their own power while using the utility as backup—threatens the fundamental utility business model.

Municipal utilities and rural cooperatives present a different challenge. Iowa has over 100 municipal utilities and dozens of cooperatives, many offering lower rates than Alliant. The city of Cedar Falls, for instance, provides electricity 20% cheaper than neighboring Alliant territories. These public power entities don't need profits, have access to tax-exempt financing, and answer directly to local voters rather than Wall Street.

The distributed generation threat accelerates annually. Solar panel costs have fallen 90% since 2010, battery prices drop 10% yearly, and smart home technology enables sophisticated energy management. A manufacturing facility can now install rooftop solar, add battery storage, and reduce grid purchases by 70%. They still need Alliant for reliability, but contribute little to fixed-cost recovery.

Regulatory risk intensifies with each election cycle. Wisconsin's Public Service Commission shifted from skeptical to supportive of renewable energy after gubernatorial changes. Iowa's regulatory environment, traditionally utility-friendly, faces pressure from consumer advocates arguing rates rise too fast. One bad rate case decision—denied cost recovery for stranded coal assets, for instance—could destroy billions in shareholder value.

Climate risk isn't theoretical anymore. The 2020 derecho that damaged Duane Arnold nuclear plant caused $11 billion in agricultural damage across Iowa. Polar vortexes stress the grid when wind doesn't blow and solar doesn't shine. Flooding threatens riverside generation facilities. Droughts reduce hydroelectric output. Each extreme weather event tests infrastructure designed for a more stable climate.

Technology disruption could accelerate beyond current projections. If batteries achieve another 10x improvement in cost and performance—not impossible given lithium-ion's trajectory—distributed storage could make the grid optional for many customers. Hydrogen production from excess renewables, direct air capture of CO2, small modular reactors—any breakthrough could obsolete Alliant's current strategy.

The electrification megatrend creates its own challenges. Electric vehicle adoption, heat pump installations, data center proliferation—all increase electricity demand but in unpredictable spurts. A neighborhood where 50% of residents buy EVs and charge them simultaneously could overload transformers designed for stable loads. Upgrading distribution infrastructure for electrification requires billions in investment with uncertain cost recovery.

Data center demand particularly complicates planning. A single hyperscale data center can consume as much electricity as 50,000 homes, but tech companies demand 100% renewable power, creating impossible equations when wind doesn't blow. Meta and Google want carbon-free energy 24/7, not just on average, forcing utilities to maintain fossil backup while claiming renewable credentials.

Execution risk multiplies with scale. Alliant plans to invest $10 billion through 2028, mostly in renewable generation and grid modernization. But wind turbine delivery delays, solar panel tariffs, transformer shortages, skilled electrician scarcity—any bottleneck cascades through complex project timelines. The company must execute flawlessly while transforming its entire business model.

The stranded asset problem haunts every coal retirement decision. Alliant has billions in undepreciated coal plant investments on its books. Early retirement means writing off these assets, hoping regulators allow recovery through rates. But consumer advocates argue shareholders, not ratepayers, should bear the cost of management's past decisions. Each coal plant closure becomes a regulatory battlefield.

Competition from natural gas remains formidable. Despite renewable cost declines, combined-cycle gas plants provide reliable, dispatchable power at competitive prices. When wind doesn't blow and sun doesn't shine, gas plants ramp up instantly. Until battery storage becomes economically viable at grid scale, natural gas remains essential for reliability, complicating decarbonization narratives.

The bear case ultimately rests on execution complexity. Alliant must simultaneously retire coal plants, build renewables, upgrade the grid, manage workforce transitions, navigate regulatory proceedings, maintain reliability, and keep rates affordable—all while competing technologies and business models emerge. One major stumble—a renewable project failure, extended blackout, or adverse regulatory decision—could unravel investor confidence and strategic momentum.

X. The Bull Case & Future Vision

Stand on a hill in northern Iowa during harvest season and you understand Alliant's competitive advantage immediately. The wind blows constantly—not the gusty, unpredictable wind of mountains or coasts, but steady, powerful, reliable wind perfect for turbines. The land stretches flat to the horizon, ideal for both wind and solar development. This is America's renewable energy Saudi Arabia, and Alliant owns the extraction rights.

The Midwest renewable resource advantage cannot be replicated. Iowa's wind capacity factors approach 45%, among the highest onshore globally. Solar resources, while not Southwest-level, benefit from cooler temperatures that increase panel efficiency. After these changes, about half of Alliant's energy production in the state will be from renewable resources. Land costs remain a fraction of coastal markets, and farmers eagerly lease acreage for steady income that doesn't depend on commodity prices.

Essential infrastructure in growing economies positions Alliant perfectly for the next economic era. Iowa and Wisconsin aren't rust belt casualties but advanced manufacturing hubs. John Deere's precision agriculture equipment, Wisconsin's paper mills, food processing facilities, emerging bioeconomy ventures—all require reliable, affordable, increasingly clean electricity. Unlike utilities serving declining regions, Alliant powers economic growth.

The electrification megatrend transforms from risk to opportunity with proper execution. Electric vehicle adoption, heat pump deployment, industrial process electrification—each increases electricity demand in Alliant's service territory. The company projects 1.5% annual demand growth through 2030, reversing decades of stagnation. More electricity sales across fixed infrastructure means lower unit costs and higher returns.

Constructive regulatory environments in Iowa and Wisconsin enable long-term planning. Both states support utility-scale renewables, approve reasonable returns on invested capital, and understand utilities need financial health to transform infrastructure. Unlike California's adversarial proceedings or Texas's deregulated chaos, Midwest regulation balances stakeholder interests pragmatically.

The company retired a major coal-fired facility in Iowa in 2023 and plans to cease burning coal at its coal-fired facility in Wisconsin before 2030. This disciplined execution builds regulatory credibility—Alliant does what it promises, earning trust that translates into approved rate increases and strategic flexibility.

First-mover advantage in utility-scale renewables creates competitive moats. Alliant has locked up the best wind sites, secured interconnection rights at strategic grid nodes, and developed relationships with landowners across thousands of rural acres. Competitors can't simply replicate this position—the prime sites are taken, interconnection queues stretch for years, and farmer trust takes decades to build.

Strong ESG positioning attracts institutional capital in an era of sustainable investing. Pension funds, sovereign wealth funds, ESG-focused mutual funds—all seek utilities credibly executing energy transitions. Alliant's boring Midwest positioning actually helps; this isn't greenwashing but practical decarbonization in America's industrial heartland.

The financial mathematics of the transition favor incumbent utilities. Renewable projects qualify for federal tax credits worth 30-40% of capital costs. Regulated returns mean Alliant earns 10% on the remaining investment. Customers benefit from lower fuel costs. Everyone wins—except fossil fuel producers. This alignment of incentives creates sustainable competitive advantage.

Grid modernization investments create platform value beyond generation. Smart meters enable time-of-use pricing, demand response, and distributed resource integration. Grid automation reduces outage duration and frequency. Advanced distribution management systems optimize power flows. These digital infrastructure investments create option value for whatever energy future emerges.

The strategic positioning for multiple scenarios demonstrates sophisticated planning. If battery costs plummet, Alliant becomes a storage-enabled renewable utility. If hydrogen emerges, existing wind resources produce green hydrogen. If small modular reactors prove viable, Alliant has sites and grid infrastructure. The company isn't betting on one future but positioning for many.

Customer relationships, often overlooked, provide sustainable advantage. Alliant serves communities where families stay for generations, where trust builds over decades, where reliable service matters more than ideology. These aren't transient urban renters but rooted businesses and households that value stability. This customer base provides patient capital for long-term transformation.

The bull case ultimately envisions Alliant as the template for America's energy transition—practical, economical, and achievable. While coastal utilities struggle with politics and deregulated markets face volatility, this Midwest utility quietly demonstrates that transforming energy systems doesn't require revolution, just competent execution. By 2030, Alliant could operate America's cleanest utility system while maintaining America's most reliable grid, all at rates below the national average.

XI. Epilogue: The Quiet Transformation

The story of Alliant Energy matters precisely because it's not exceptional. This isn't Tesla disrupting transportation or Amazon reimagining commerce. It's a century-old utility in Iowa and Wisconsin, serving farmers and factories, methodically replacing coal plants with wind turbines and solar panels. The transformation happens not through press releases or viral moments but through thousands of incremental decisions executed competently over years.

The lessons for industrial incumbents navigating disruption are profound. First, timing matters more than technology. Alliant didn't pioneer wind power or invent solar panels; they waited until economics favored deployment, then moved decisively. Second, regulatory relationships trump technological advantages. Alliant's constructive engagement with state commissions enabled billions in renewable investments while maintaining financial stability. Third, workforce and community management determine social license. By treating coal plant workers fairly and supporting affected communities, Alliant avoided the opposition that derails energy projects elsewhere.

The Midwest's role in America's energy future emerges as central, not peripheral. While policy debates focus on California's mandates or Texas's market structures, the real energy transition happens in places like Iowa and Wisconsin—states that manufacture things, grow food, and need reliable power year-round. These states demonstrate that clean energy isn't a luxury for wealthy coasts but an economic necessity for industrial competitiveness.

What Alliant's journey tells us about pragmatic climate action challenges dominant narratives. Decarbonization doesn't require environmental activism or government mandates—just proper price signals and competent execution. The company reduces emissions not from ideological commitment but because renewable energy became cheaper than fossil alternatives. This economic logic, not politics, drives sustainable transformation.

The broader implications extend beyond utilities. Every industrial incumbent faces similar challenges—technological disruption, stakeholder pressure, workforce transitions, stranded assets. Alliant's playbook—gradual transformation, stakeholder engagement, financial discipline, strategic opportunism—offers a template for navigating disruption without destruction.

Yet questions remain unanswered. Can Alliant maintain reliability as renewable penetration exceeds 70%? Will distributed generation eventually make utilities obsolete? How will climate change affect Midwest weather patterns and energy demand? Can political consensus on energy policy survive increasing polarization? These uncertainties make Alliant's story ongoing rather than concluded.

The investment implications deserve consideration. Utilities traditionally attracted income-seeking investors wanting stable dividends. But energy transition utilities like Alliant offer something different—growth potential within regulated structures, ESG credentials with economic logic, technology options with downside protection. This isn't your grandfather's utility stock anymore.

For policymakers, Alliant demonstrates that energy transitions can proceed without federal mandates or massive subsidies. State-level regulation, properly structured, incentivizes utilities to decarbonize while maintaining affordability and reliability. The Midwest model—regulated utilities with renewable portfolio standards and constructive commission oversight—may prove more sustainable than deregulated markets or public power alternatives.

The human dimension often gets lost in energy discussions, but Alliant's story is fundamentally about people—the engineers maintaining aging coal plants while training for renewable operations, the farmers earning steady income from wind leases, the factory workers depending on reliable power, the children breathing cleaner air. Energy transformation isn't abstract policy but lived experience in thousands of communities.

Looking forward, Alliant Energy represents both America's energy past and future. The company that once epitomized coal-powered industrialization now pioneers renewable transformation. The utility that served 20th-century manufacturing now powers 21st-century sustainability. This evolution, achieved without fanfare in America's heartland, demonstrates that fundamental change doesn't require revolution—just competent execution of obvious solutions.

The quiet transformation continues. While headlines focus on breakthrough technologies and political battles, Alliant Energy methodically installs another wind turbine in an Iowa cornfield, connects another solar farm in Wisconsin, retires another coal unit ahead of schedule. No press releases, no viral moments, just the systematic transformation of American energy infrastructure, one project at a time.

This is how the energy transition actually happens—not through disruption but evolution, not through mandates but markets, not through ideology but economics. In the end, Alliant Energy's story isn't about one company but about industrial transformation in the 21st century, demonstrating that even the most traditional businesses can reinvent themselves when change becomes inevitable. The lights stay on, the factories keep running, and somehow, imperceptibly, the energy system that powered the last century transforms into one that will power the next.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube