Exelon Corporation: The Evolution of America's Utility Giant

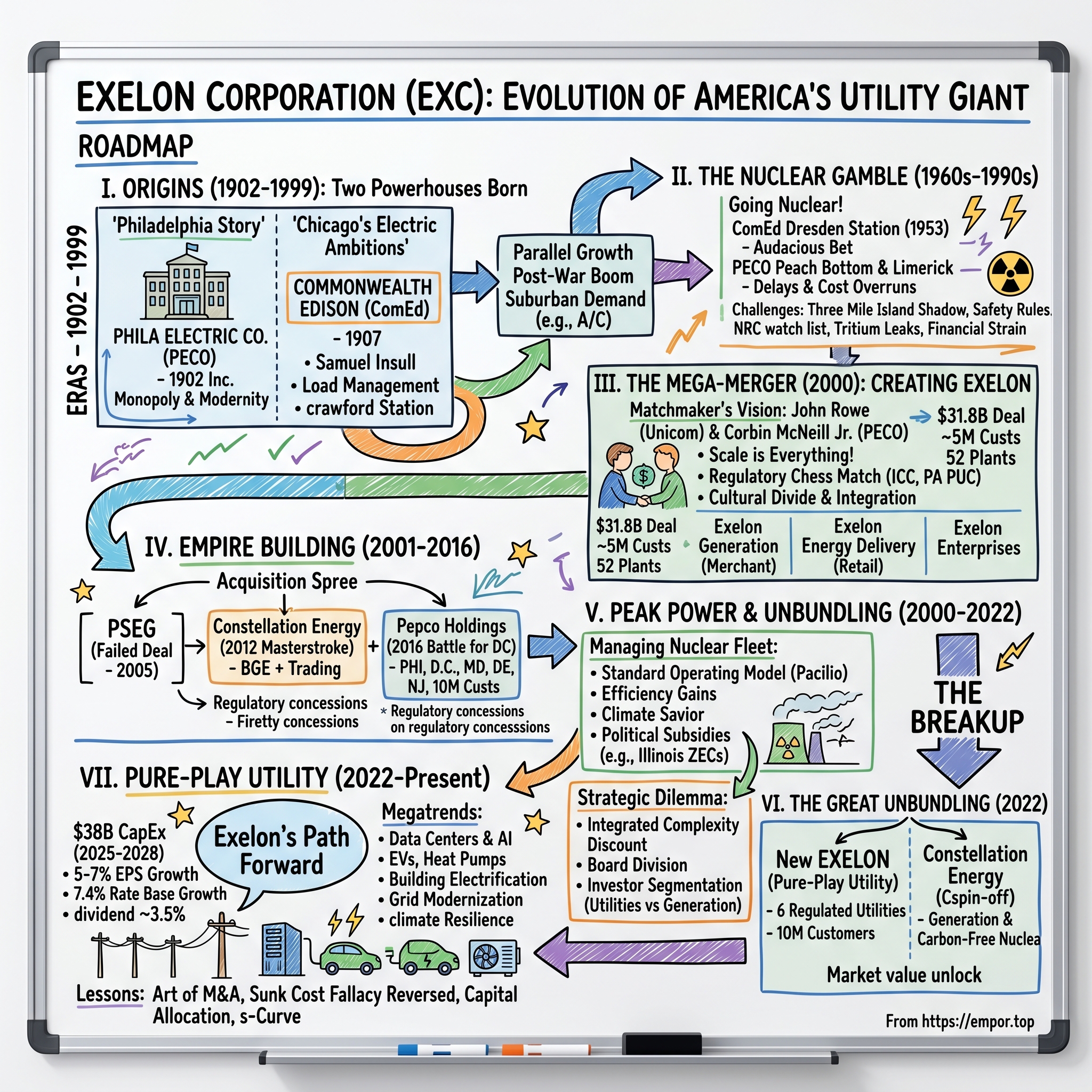

I. Introduction & Episode Roadmap

Picture this: It's a sweltering August day in Chicago, 2003. The mercury hits 103°F. Air conditioners across the city strain the electric grid to its absolute limit. In the control room of Commonwealth Edison, engineers watch nervously as demand spikes toward 23,000 megawatts—dangerously close to maximum capacity. One wrong move, one failed generator, and millions could lose power. This is the razor's edge that electric utilities walk every single day. And on this particular day, the company that would soon become Exelon Corporation was learning a crucial lesson about the future of American energy infrastructure.

Today, Exelon stands as America's largest regulated electric utility, serving approximately 10 million customers across six states through its operating companies. With a market capitalization of $45.94 billion as of August 2025, it ranks 187th on the Fortune 500 and holds the distinction of being the world's 488th most valuable company. But these numbers only tell part of the story.

The real narrative is far more compelling: How did two regional utilities—one born in the steel furnaces of Pennsylvania, the other in the stockyards of Chicago—merge to create the nation's premier electric utility? How did they assemble and then operate the largest nuclear fleet in America, only to spin it off two decades later? And what does their journey tell us about the future of energy in an electrifying world?

This is a story of massive bets on nuclear technology when others ran scared, of regulatory chess matches played across state capitals, of empire building through strategic acquisitions, and ultimately, of recognizing when one company needed to become two. It's about navigating the tension between being a boring, predictable utility that investors love and being an innovative energy company that can meet the demands of the 21st century.

We'll trace Exelon's evolution through several distinct eras: the parallel rise of two regional monopolies in the early 20th century, the audacious nuclear gamble that would define their futures, the mega-merger that created a utility giant, an acquisition spree that expanded their empire, and finally, the strategic unbundling that separated the regulated utility business from the merchant generation fleet. Along the way, we'll extract the business lessons embedded in this century-spanning saga—from capital allocation in capital-intensive industries to the art of regulatory navigation.

The stakes couldn't be higher. As America stands at an energy crossroads—with electric vehicles, data centers, and AI driving unprecedented demand while climate change demands cleaner sources—Exelon's story offers crucial insights into how massive, regulated businesses adapt, transform, and position themselves for the future. This isn't just a utility story; it's a masterclass in strategic transformation, financial engineering, and the delicate balance between public service and shareholder returns.

II. Origins: Two Powerhouses Born (1902–1999)

The Philadelphia Story

The year was 1881, and Philadelphia was about to witness magic. The Brush Electric Light Company of Philadelphia had just installed arc lights along Chestnut Street, turning night into day with the flip of a switch. Crowds gathered to marvel at this electric miracle, unaware they were witnessing the birth of what would become PECO Energy Company. Charles Brush, the inventor behind the technology, had created more than just a lighting system—he had sparked an industrial revolution that would transform American cities.

By 1902, after a series of mergers and consolidations typical of the Gilded Age, the Philadelphia Electric Company officially incorporated. The timing was perfect. Philadelphia was booming—its population had doubled to 1.3 million between 1880 and 1900, factories sprouted along the Delaware River, and the city's appetite for electricity seemed insatiable. The company's early leaders, many of them prominent Philadelphia families with names like Drexel and Biddle, understood they weren't just selling electricity; they were selling modernity itself.

The company's growth strategy was elegantly simple: acquire competitors, expand the grid, and lobby for exclusive franchise rights. By 1920, Philadelphia Electric had absorbed eight rival companies and secured a virtual monopoly over the city's electric service. The regulatory compact was taking shape—in exchange for exclusive service territories and guaranteed returns on investment, the utility would serve all customers at regulated rates. It was a deal that would define the American utility model for the next century.

Chicago's Electric Ambitions

Meanwhile, 800 miles west, a different but parallel story was unfolding. Commonwealth Edison emerged in 1907 under the umbrella of Unicom Corporation, but its roots traced back to Samuel Insull, Thomas Edison's former private secretary who had come to Chicago in 1892 to run Chicago Edison. Insull was a visionary who understood that electricity's true potential lay not in serving wealthy customers with private generators but in creating a vast, interconnected system that could serve everyone.

Insull pioneered the concept of load management—using diverse customer types (factories during the day, streetlights at night, residential in between) to maximize utilization of expensive generating equipment. His Chicago operation became the model for utilities nationwide. By 1907, when Commonwealth Edison was formally created through the merger of Chicago Edison and Commonwealth Electric, it was already one of the largest electric utilities in the nation.

The company's growth through the 1920s was explosive. ComEd built massive coal-fired generating stations along Lake Michigan, using the lake for cooling water and barges for coal delivery. The Crawford Station, opened in 1924, was then the world's largest generating plant. These facilities weren't just engineering marvels; they were monuments to the industrial age, their smokestacks visible for miles, announcing Chicago's emergence as America's second city.

Post-War Expansion and Suburban Dreams

The post-World War II era brought unprecedented challenges and opportunities for both utilities. Returning veterans, suburban expansion, and the consumer revolution drove electricity demand to levels that would have seemed fantastical just a decade earlier. Between 1945 and 1960, residential electricity consumption quadrupled nationwide.

Philadelphia Electric responded by embarking on its most ambitious construction program ever. The company built new generating stations at Eddystone and Schuylkill, each pushing the boundaries of steam turbine technology. The Eddystone station, completed in 1960, featured the world's first supercritical steam unit, operating at pressures and temperatures that seemed to defy physics—3,500 pounds per square inch and 1,200°F.

Commonwealth Edison faced similar demands in Chicago. The post-war boom transformed sleepy farm towns into bustling suburbs almost overnight. Levittown-style developments sprouted across the prairie, each house equipped with electric ranges, water heaters, and that ultimate symbol of American prosperity—air conditioning. ComEd's peak load, which had been 1,400 megawatts in 1945, soared to 4,500 megawatts by 1960.

The Nuclear Dawn

It was in this context of explosive growth that both companies made the decision that would define their futures: going nuclear. Philadelphia Electric first participated in nuclear energy feasibility studies in 1952, joining a consortium studying peacetime uses of atomic energy. The company's engineers traveled to Oak Ridge, Tennessee, and Argonne National Laboratory, absorbing everything they could about this new technology.

The attraction was obvious. A single pound of uranium could produce as much energy as 3 million pounds of coal. No more coal trains, no more ash disposal, no more smokestacks darkening the sky. It seemed like the perfect solution for utilities struggling to keep pace with demand while facing increasing environmental concerns.

Commonwealth Edison moved first, announcing in 1953 that it would build Dresden Nuclear Power Station, one of the first commercial nuclear plants in America. The decision was audacious—the technology was unproven at commercial scale, the costs were uncertain, and public opinion was still shaped by images of mushroom clouds. But ComEd's leadership, particularly CEO Willis Gale, believed nuclear represented the future.

Philadelphia Electric followed suit, though more cautiously. The company began planning what would become the Peach Bottom Atomic Power Station, initially as an experimental high-temperature gas-cooled reactor in partnership with the Atomic Energy Commission. These early nuclear ventures were as much about learning as generating power—they were massive experiments in technology, regulation, and public acceptance.

The Regulatory Dance

Throughout this period, both utilities mastered the intricate dance of utility regulation. The model was deceptively simple: utilities would present their costs to public utility commissions, which would set rates allowing a fair return on invested capital. But in practice, it was a complex game of political influence, technical arguments, and public relations.

Rate cases became elaborate theater. Utilities would hire armies of consultants to justify their investments, while consumer advocates and industrial customers would challenge every assumption. The commissioners, often political appointees, had to balance the utility's need for capital with public pressure to keep rates low. It was a system that rewarded those who could navigate its complexities—and both Philadelphia Electric and Commonwealth Edison proved masters of the game.

By the 1970s, both companies had evolved from local electric companies into sophisticated energy corporations. Philadelphia Electric was serving 1.3 million customers across southeastern Pennsylvania, while Commonwealth Edison dominated northern Illinois with 2.9 million customers. They had survived the Great Depression, powered the Arsenal of Democracy during World War II, and fueled the post-war boom.

Yet challenges loomed. The 1973 oil embargo exposed the vulnerability of fossil fuel dependence. Environmental regulations were tightening, with the Clean Air Act requiring expensive pollution controls. And inflation was driving construction costs sky-high. Both companies doubled down on their nuclear strategies, setting the stage for the dramatic transformations that would follow. The seeds of Exelon were planted, though neither company yet knew they would one day join forces to create something even greater.

III. The Nuclear Gamble: Building America's Atomic Fleet (1960s–1990s)

The Promise and the Peril

The control room at Commonwealth Edison's Dresden Unit 1 hummed with nervous energy on October 15, 1959. Engineers watched as the reactor achieved criticality for the first time—the moment when nuclear fission becomes self-sustaining. Outside, protesters held signs reading "No Atoms for Peace" while inside, executives popped champagne. This scene would replay across America as utilities bet their futures on the atom, but nowhere more dramatically than at Philadelphia Electric and Commonwealth Edison.

The nuclear promise was intoxicating. The Atomic Energy Commission chairman had famously predicted electricity "too cheap to meter." While that proved wildly optimistic, the economics initially seemed compelling. Nuclear plants required massive upfront capital but promised decades of low operating costs. For regulated utilities that could pass construction costs to ratepayers and earn guaranteed returns on their investments, it looked like the perfect bet.

Philadelphia Electric went all-in, viewing nuclear capabilities as essential to maintain service standards while conforming to increasingly strict clean air and water regulations. The company's Limerick Generating Station, announced in 1969, was supposed to be a crown jewel—twin boiling water reactors that would each generate 1,055 megawatts. The initial cost estimate: $700 million. The completion date: 1974 and 1976 for Units 1 and 2 respectively.

Reality proved far messier. Regulatory delays prevented completion of the two nuclear plants at Limerick until the mid and late 1980s—more than a decade behind schedule. The delays weren't just bureaucratic inconveniences; each year added hundreds of millions in interest charges and inflation adjustments. By the time Limerick Unit 1 finally came online in 1986, the project cost had ballooned to $4.5 billion.

Commonwealth Edison's Nuclear Empire

If Philadelphia Electric's nuclear program was ambitious, Commonwealth Edison's was audacious to the point of recklessness. By the early 1970s, ComEd had committed to building 12 nuclear units across six sites in Illinois. No utility in America was making a bigger bet on nuclear power.

The scale was staggering. At its peak, ComEd had over $7 billion in nuclear construction projects underway simultaneously. The company's Dresden, Quad Cities, Zion, LaSalle, Byron, and Braidwood stations would eventually comprise the largest nuclear fleet operated by a single utility. CEO James O'Connor, who led the company from 1964 to 1980, believed nuclear was not just the future but the only viable path forward for meeting Chicago's growing energy needs.

By 1986, ComEd was struggling to finance the $7.1 billion building program for the last three of its 12 nuclear plants. The company's debt had soared to dangerous levels, its credit rating was under pressure, and ratepayers were in revolt over escalating bills. The Illinois Commerce Commission, facing political pressure, began disallowing portions of nuclear construction costs from the rate base—a devastating blow to the utility's economic model.

Three Mile Island's Shadow

Then came March 28, 1979—a date that would forever change the nuclear industry. The partial meltdown at Three Mile Island Unit 2 near Harrisburg, Pennsylvania, though resulting in no deaths or injuries, shattered public confidence in nuclear power. The accident occurred just 12 days after the release of "The China Syndrome," a film depicting a nuclear disaster. The timing couldn't have been worse.

For Philadelphia Electric and Commonwealth Edison, Three Mile Island transformed their nuclear programs from strategic assets into potential liabilities. The Nuclear Regulatory Commission imposed sweeping new safety requirements—control room redesigns, emergency response procedures, backup safety systems. Each mandate added millions to construction costs and months to completion schedules.

Public opposition, previously manageable, became fierce and organized. Anti-nuclear groups staged protests at construction sites, filed lawsuits to delay licensing, and packed public hearings. At ComEd's Byron station, over 500 protesters were arrested in 1981. The company had to hire security forces that rivaled small police departments just to protect their construction sites.

The Operational Nightmare

Even after the plants were built, the challenges were just beginning. By the mid-1990s, only half of ComEd's reactors were typically online at any given time. The company's nuclear capacity factor—the percentage of maximum possible output actually achieved—hovered around 50%, compared to an industry average of 70%. For a fleet that had cost tens of billions to build, this performance was catastrophic.

The problems were systemic. ComEd had built too many plants too quickly, without developing the operational expertise to run them safely and efficiently. The NRC issued fine after fine for various incidents—workers sleeping on duty, failed safety inspections, inadequate maintenance procedures. In 1996, the NRC placed ComEd's entire nuclear fleet on its watch list, threatening to shut down plants if improvements weren't made.

The most embarrassing incident came in 2009 when the NRC fined the company for security guards sleeping at Peach Bottom. Video footage showed guards routinely napping during shifts, sometimes for hours. The imagery—sleeping guards at a nuclear plant—became a public relations nightmare that reinforced every stereotype about utility incompetence.

The Tritium Scandal

Perhaps no incident better illustrated the challenges of nuclear operation than the 2006 disclosure of tritium spills at ComEd's Braidwood Station. The company revealed that radioactive tritium had been leaking from the plant for over a decade, contaminating local groundwater. While the levels posed no immediate health threat, the fact that the leaks had gone unreported for so long sparked outrage.

The Braidwood revelation triggered investigations at all of ComEd's nuclear plants, uncovering similar issues at Dresden and Byron. The company faced hundreds of millions in cleanup costs, regulatory fines, and lawsuits from property owners claiming diminished land values. Trust, already fragile, was shattered.

The Economics Unravel

By 1990, ComEd's nuclear program had resulted in generating capacity exceeding peak demand by 33%, compared to the typical 15% reserve margin maintained by most utilities. This excess capacity, built at enormous cost, sat idle much of the time. The company's rates, driven by the need to recover nuclear construction costs, were among the highest in the Midwest.

Industrial customers began fleeing Illinois for states with cheaper power. Residential customers, trapped by monopoly service territories, seethed at their monthly bills. Politicians, sensing opportunity, began calling for deregulation—a prospect that terrified ComEd executives who knew their nuclear plants couldn't compete with cheap coal and emerging natural gas generation.

The financial strain was evident everywhere. ComEd's stock price languished while other utilities soared. Bond rating agencies threatened downgrades. The dividend, that sacred cow of utility investing, came under pressure. Something had to change.

Learning from Failure

Yet within this operational and financial disaster lay the seeds of redemption. The nuclear plants, for all their problems, were still valuable assets—they just needed better management. The technology itself was sound; it was the execution that had failed.

Some within ComEd began studying best practices from other nuclear operators, particularly those in the Navy's nuclear program. They learned about procedural discipline, continuous training, and the culture of safety that allowed naval reactors to operate flawlessly for decades. Slowly, painfully, they began implementing these lessons.

Philadelphia Electric, having learned from ComEd's mistakes, took a more measured approach to nuclear operations. Their plants, while facing their own challenges, generally performed better. The company developed expertise in nuclear maintenance and refueling that would later prove invaluable.

By the late 1990s, both companies had survived the nuclear gamble, though barely. Their reactors were finally running more reliably, though the financial scars remained. The stage was set for a transformation that would turn these troubled nuclear assets from millstones into goldmines. But first, the companies themselves would need to transform—and that would require joining forces in a merger that would reshape the American utility landscape.

IV. The Mega-Merger: Creating Exelon (2000)

The Matchmaker's Vision

John Rowe sat in his corner office at Unicom's Chicago headquarters in early 1999, staring at a map of the United States marked with colored pins representing every major utility. At 54, Rowe had already earned a reputation as one of the industry's sharpest strategic minds. He'd taken over as CEO of Unicom (Commonwealth Edison's parent company) just a year earlier, inheriting a nuclear fleet in crisis and a company whose stock had been dead money for a decade. But where others saw problems, Rowe saw opportunity.

"Scale," he would tell anyone who'd listen, "scale is everything in the new world." Deregulation was sweeping through state after state, breaking up the old monopoly model. Wholesale power markets were emerging. The industry was about to undergo its biggest transformation since Thomas Edison, and Rowe was determined to be on the winning side.

His eyes kept returning to one pin on the map: Philadelphia. PECO Energy had what Unicom needed—operational excellence, a strong balance sheet, and geographic diversification. Unicom had what PECO wanted—the largest nuclear fleet in America, which despite its problems, would be incredibly valuable if managed properly. Rowe picked up the phone and called Corbin McNeill Jr., PECO's CEO.

The Courtship Dance

The first meeting between Rowe and McNeill took place at a neutral location—the Union Club in New York City—in March 1999. Over aged steaks and expensive wine, the two CEOs sized each other up. McNeill, a Philadelphia blue blood with an engineering background, was everything Rowe wasn't—cautious where Rowe was bold, traditional where Rowe was innovative.

But they shared a crucial insight: the utility industry's old model was dying. States were deregulating generation, forcing utilities to compete. Technology companies were eyeing the electricity market. Natural gas prices were plummeting. Standing still meant slow death.

"Corbin," Rowe said, leaning across the table, "we can build something nobody else can match. Your operational expertise with our nuclear scale. Your Mid-Atlantic presence with our Midwest base. We control nearly 20% of the country's nuclear generation market. In a carbon-constrained world, that's gold."

McNeill was intrigued but worried about cultural fit. PECO was buttoned-up Philadelphia establishment; ComEd was rough-and-tumble Chicago. PECO's nuclear plants ran well; ComEd's were perpetually in regulatory trouble. The integration challenges would be immense.

The $31.8 Billion Handshake

Secret negotiations continued through the summer of 1999. Code names were assigned—Project Eagle for PECO, Project Bear for Unicom. Investment bankers shuttled between Philadelphia and Chicago with models showing potential synergies: $2 billion in cost savings over five years, improved nuclear operations, enhanced trading capabilities.

The dealmaking hit a crucial snag in August over the exchange ratio. PECO shareholders wanted a premium; Unicom argued it was a merger of equals. The negotiations nearly collapsed until Rowe made a strategic concession: PECO shareholders would own 55% of the combined company, and the headquarters would be in Chicago, but significant operations would remain in Philadelphia.

On September 27, 1999, the boards of both companies approved the merger. The next morning, Rowe and McNeill stood together at a press conference in Philadelphia's Union League, announcing the creation of Exelon Corporation—a name chosen because it suggested excellence and energy.

The numbers were staggering: $31.8 billion in combined market value, making it the largest utility merger in U.S. history. The combined company would serve approximately 5 million customers and operate 52 power plants with 52,000 megawatts of capacity. Wall Street's initial reaction was mixed—the stock prices of both companies barely moved.

Regulatory Chess Match

But announcing a merger and completing it were very different things. The deal required approval from the Federal Energy Regulatory Commission, the Nuclear Regulatory Commission, the Department of Justice, the Securities and Exchange Commission, the Pennsylvania Public Utility Commission, and the Illinois Commerce Commission. Each regulator had different concerns and different constituencies.

The Illinois Commerce Commission proved the toughest battleground. Consumer advocates argued the merger would lead to higher rates. Labor unions worried about job losses. Environmental groups opposed the concentration of nuclear power. The hearings dragged on for months, with thousands of pages of testimony.

Rowe personally led the charm offensive, testifying for hours about the merger's benefits. He committed to $1 billion in rate reductions for Illinois customers, no involuntary layoffs for two years, and maintaining both companies' charitable giving. Behind the scenes, lobbyists worked Springfield's corridors, building political support.

The Pennsylvania PUC had its own demands. They wanted guarantees that PECO's Philadelphia headquarters would remain robust, that service quality wouldn't deteriorate, and that Pennsylvania would see its fair share of merger benefits. More concessions, more commitments.

Integration Nightmare

Even as regulators deliberated, integration planning proceeded in secret. Hundreds of employees from both companies were pulled into "clean rooms"—secure facilities where they could plan the merger without violating antitrust laws. The complexity was mind-boggling: two different computer systems, two different nuclear operating procedures, two different corporate cultures.

The cultural divide was real. PECO employees saw themselves as disciplined operators being absorbed by cowboys who couldn't run nuclear plants. ComEd employees viewed PECO as arrogant East Coasters who didn't understand the rough-and-tumble Midwest market. Integration team meetings sometimes devolved into shouting matches.

The nuclear integration was particularly sensitive. PECO's nuclear team, led by Chief Nuclear Officer Mike Pacilio, was tasked with fixing ComEd's troubled fleet. Pacilio, a former Navy nuclear officer, approached the assignment like a military operation. He brought in Navy-trained operators, implemented strict procedural discipline, and created a culture of "verbatim compliance"—do exactly what the procedure says, every time, no exceptions.

October 20, 2000: Birth of a Giant

Finally, after 13 months of regulatory review and integration planning, the merger closed on October 20, 2000. The New York Stock Exchange rang its opening bell as executives from both companies stood on the podium. The ticker symbol EXC appeared for the first time.

The new Exelon was organized into three main divisions: Exelon Generation (combining both companies' nuclear, fossil, and hydro fleets), Exelon Energy Delivery (the retail distribution operations), and Exelon Enterprises (various non-regulated businesses). Rowe became CEO, while McNeill served as Chairman until his retirement in 2003.

The immediate priority was fixing the nuclear fleet. Pacilio's team implemented a standardized operating model across all plants, invested heavily in training and maintenance, and created a culture of continuous improvement. The turnaround was dramatic—within three years, Exelon's nuclear capacity factor rose from 75% to over 93%, adding the equivalent of two new nuclear plants without building anything.

The Synergy Machine

The promised synergies materialized faster than expected. Duplicate corporate functions were eliminated, saving hundreds of millions. The combined company's superior credit rating lowered borrowing costs. Joint purchasing agreements reduced procurement expenses. By 2002, Exelon had exceeded its $2 billion synergy target.

But the real value came from wholesale power trading. Exelon's merchant generation fleet—power plants that sold into competitive markets rather than to regulated utility customers—could now optimize across a much larger geographic footprint. When prices spiked in one region, Exelon could shift generation. When nuclear plants needed refueling, other plants could cover. The trading desk in Baltimore became a profit center, generating hundreds of millions in additional revenue.

Rowe's vision was proving correct. In the newly deregulated world, scale did matter. Exelon's size gave it market power, operational flexibility, and financial strength that smaller competitors couldn't match. The stock price, which had started at $30 at the merger's close, climbed steadily.

Yet success brought new challenges. Regulators grew concerned about Exelon's market power. Competitors complained about unfair advantages. Environmental groups targeted the company as the face of nuclear power. And Rowe, never satisfied, was already planning the next moves in his empire-building strategy. The merger had created a giant, but in Rowe's mind, Exelon was just getting started.

V. Empire Building: The Acquisition Spree (2001–2016)

The Failed PSEG Courtship

The conference room at the Ritz-Carlton in Philadelphia was thick with tension on December 20, 2004. John Rowe faced off against Jim Ferland, CEO of Public Service Enterprise Group (PSEG), New Jersey's largest utility. They'd been negotiating for six months, crafting what would have been a $12 billion merger creating the undisputed king of Northeast utilities. Now it was falling apart.

"Jim, be reasonable," Rowe pressed. "The synergies are obvious. Your New Jersey operations combined with our Pennsylvania and Illinois base—we'd have a corridor from Chicago to the Atlantic."

Ferland shook his head. "John, you know the New Jersey public interest groups will never let this happen. They're already calling it a monopoly. The politicians are running scared."

The PSEG merger had seemed perfect on paper—adding 2.2 million New Jersey customers and more nuclear capacity. But after 18 months of trying, facing fierce opposition from New Jersey public interest groups who feared rate increases and job losses, the companies abandoned the deal in September 2005. Rowe was furious but philosophical: "Sometimes the best deals are the ones you don't make."

The Constellation Energy Masterstroke

By 2008, Rowe had found a new target: Constellation Energy of Baltimore. Constellation was a fascinating hybrid—it owned Baltimore Gas & Electric, a regulated utility serving central Maryland, but also had a massive merchant generation fleet and an energy trading operation that rivaled Wall Street banks.

The financial crisis created the opportunity. Constellation's trading desk had made aggressive bets on power prices that went wrong when markets collapsed. In September 2008, facing margin calls it couldn't meet, Constellation was hours from bankruptcy. Warren Buffett's MidAmerican Energy swooped in with a rescue offer, but it was predatory—$4.7 billion for a company that had been worth $20 billion a year earlier.

Rowe sensed blood in the water. He called Mayo Shattuck, Constellation's CEO, with a different proposal: "Mayo, Buffett's trying to steal your company. Merge with us instead. We'll pay fair value, keep your team intact, and create the premier competitive energy company in America."

The negotiations were complex. French utility EDF owned 9.5% of Constellation and had certain rights. Buffett demanded a $1 billion breakup fee for walking away. Maryland regulators needed convincing. But Rowe navigated each obstacle with surgical precision. On March 12, 2012, the deal closed. Exelon Corporation acquired Constellation Energy Group, Inc., with each share of Constellation Energy receiving 0.93 shares of Exelon common stock. The market capitalization of the combined company reached $34 billion with an enterprise value of $52 billion.

The integration was masterful. The merger created the number one competitive energy provider with one of the industry's cleanest and lowest-cost power generation fleets and one of the largest commercial, industrial and residential customer bases in the United States. Constellation's superior trading platform was merged with Exelon's generation assets, creating unprecedented market reach. Baltimore Gas & Electric added another crown jewel to Exelon's regulated utility portfolio.

Chris Crane, who would succeed Rowe as CEO, later reflected: "The Constellation acquisition wasn't just about size. It was about capabilities. Their trading desk, their customer relationships, their operational excellence—it transformed us from a utility with merchant generation into a true energy company."

The Pepco Holdings Saga: A Battle for Washington

If the Constellation merger was a strategic masterstroke, the Pepco Holdings acquisition was trench warfare. Announced on April 30, 2014, Exelon agreed to acquire Pepco Holdings Inc. (PHI) for $6.8 billion in an all-cash transaction, paying $27.25 per share.

Pepco Holdings brought three prized utilities: Pepco (serving Washington D.C. and Maryland suburbs), Delmarva Power (Delaware and Maryland's Eastern Shore), and Atlantic City Electric (southern New Jersey). For Exelon, it meant adding 2 million customers and extending its footprint into the nation's capital—both literally and symbolically.

But Washington D.C. proved to be hostile territory. Mayor Muriel Bowser came out swinging against the deal, arguing it would lead to higher rates and fewer local jobs. Consumer advocates mobilized, painting Exelon as a Chicago corporation trying to colonize the capital. The D.C. Public Service Commission became ground zero for one of the most contentious utility battles in recent memory.

The first hearing, in June 2015, was a disaster. Protesters packed the room, chanting "No Exelon!" Commissioner Betty Ann Kane grilled Exelon executives about their commitment to renewable energy. "You operate nuclear plants," she said accusingly, as if nuclear power was coal. "How can we trust you to support solar in the District?"

Chris Crane, now CEO after Rowe's 2012 retirement, tried diplomacy: "Commissioner, we're offering $78 million in customer rate credits, $51 million for energy efficiency, and maintaining all local jobs for at least two years." It wasn't enough.

In August 2015, the D.C. PSC rejected the merger in a 2-1 vote. The commission called Exelon's proposals "inadequate" and worried about reduced competition. Wall Street was stunned—utility mergers rarely failed at the regulatory stage. Exelon's stock dropped 3% on the news.

But Crane wasn't giving up. He personally relocated to Washington for weeks, meeting with community groups, ministers, labor unions. Exelon sweetened its offer: $100 million more in customer benefits, a commitment to develop 7 megawatts of solar in D.C., and creation of a $100 million Green Jobs Fund.

The breakthrough came when Exelon agreed to unprecedented concessions: moving Pepco's headquarters back to D.C. from suburban Maryland, appointing D.C. residents to Pepco's board, and committing to source 100% of D.C. government buildings' electricity from wind power by 2019.

Finally, on March 23, 2016, nearly two years after announcement, the merger was approved, making Exelon the largest regulated utility in the US by customer count and total revenue. The final price tag, including all concessions and commitments, approached $8 billion.

Empire Complete

By 2016, John Rowe's vision had been fully realized, even if he was no longer there to see it. Exelon had assembled an empire: six regulated utilities serving 10 million customers from Chicago to Washington, the nation's largest nuclear fleet, and a massive wholesale trading operation.

The numbers were staggering. Annual revenues exceeded $34 billion. The company employed 34,000 people. Its market capitalization topped $30 billion. From two regional utilities at the millennium's start, Exelon had become one of America's largest and most powerful energy companies.

But empires, as history teaches, often contain the seeds of their own transformation. The very diversity that made Exelon powerful—regulated and unregulated, nuclear and renewable, wholesale and retail—was becoming a liability. Investors couldn't figure out how to value such a complex beast. Environmental activists attacked the nuclear operations while free-market advocates criticized the regulated utilities.

Chris Crane, surveying his empire in late 2016, began to wonder if Rowe's creation had grown too complex for its own good. The board started asking uncomfortable questions about strategic focus. Investment bankers, smelling fees, whispered about "unlocking value through separation."

The empire was complete, but already forces were gathering that would split it apart. The age of the conglomerate was ending; the era of the pure-play was about to begin.

VI. Peak Power: Managing the Nuclear Fleet (2000–2021)

The Turnaround Machine

Mike Pacilio stood before Exelon's assembled nuclear operators in March 2001, his Navy submarine commander's bearing unmistakable even in civilian clothes. "Gentlemen," he began, his voice carrying the authority of someone who'd spent years underwater with nuclear reactors, "we're going to run these plants like the Navy runs its reactors. No shortcuts. No excuses. Procedural compliance every single time."

The room was skeptical. These were union operators who'd been running reactors their way for decades. But Pacilio had a mandate from John Rowe: fix the nuclear fleet or watch it get sold for scrap. Exelon operated the largest nuclear fleet in the nation and third largest in the world, with 17 reactors representing approximately 20% of U.S. nuclear industry's power capacity. That fleet was both Exelon's greatest asset and its greatest liability.

The transformation was methodical and relentless. Pacilio brought in dozens of ex-Navy nuclear officers, men and women trained in Admiral Rickover's culture of absolute discipline. They implemented "verbatim compliance"—following procedures word-for-word, no interpretation allowed. They introduced "human performance tools"—practices like three-way communication where every critical instruction was stated, repeated, and confirmed.

The resistance was fierce. At Byron Station, veteran operators threatened to strike when told they had to use written procedures for tasks they'd done from memory for years. At Quad Cities, a senior reactor operator was fired for pencil-whipping a safety check—marking it complete without actually performing it. The message was clear: the old ways were dead.

But the results spoke for themselves. By 2013, Constellation's nuclear energy fleet was running over 94% of the time, 4 percent better than the industry average, with 2020 refueling outage durations of 22 days, 11 days below the industry average. The improvement in capacity factor alone was worth billions—equivalent to building new plants without spending a dime on construction.

The Natural Gas Nightmare

Yet even as operations improved, the economics of nuclear power were collapsing. The shale revolution had arrived with shocking speed. Natural gas prices, which had spiked above $13 per million BTU in 2008, crashed below $2 by 2012. Combined-cycle gas plants could now generate electricity for less than $30 per megawatt-hour. Nuclear plants, with their high fixed costs, needed $35-40 just to break even.

The Quad Cities plant in Illinois became the poster child for nuclear's economic crisis. Despite running at 95% capacity factor, the plant lost $100 million in 2013. The Clinton single-unit plant bled even more red ink. Chris Crane faced an agonizing decision: keep plants running at a loss hoping for market recovery, or start shutting down reactors that had decades of operational life remaining.

"We're not in the charity business," Crane told analysts in 2014. "If these plants can't earn their cost of capital, we'll have to consider retirement." The threat was aimed squarely at state legislators—save these plants or watch them close, taking thousands of jobs and millions in tax revenue with them.

The Subsidy Wars

What followed was one of the most successful lobbying campaigns in corporate history. Exelon deployed an army to Springfield, Illinois, and Albany, New York, armed with economic impact studies and climate change data. The message was simple but powerful: nuclear plants provide carbon-free electricity 24/7, support thousands of high-paying jobs, and anchor local economies. Let them close, and states would miss their climate goals while communities would be devastated.

Illinois blinked first. In December 2016, the state passed the Future Energy Jobs Act, providing $235 million annually in "Zero Emission Credits" to keep Quad Cities and Clinton running. New York followed with similar subsidies for its upstate nuclear plants. Environmental groups were split—some viewed nuclear subsidies as corporate welfare, others recognized nuclear's role in preventing carbon emissions.

The subsidies transformed nuclear economics overnight. Plants that were bleeding cash became profitable. Exelon's stock soared as investors realized the nuclear fleet would survive. But the victory came at a cost—Exelon was now dependent on political favor, its fate tied to the whims of state legislators and governors.

The Safety Scandals

Even as Exelon secured the fleet's economic future, operational incidents continued to plague its reputation. The 2006 tritium revelations at Braidwood hadn't been forgotten. For over a decade, radioactive water had been leaking into the ground, and Exelon hadn't told anyone. When the news broke, property values around the plant plummeted. Lawsuits flew. Trust evaporated.

The company's response was tone-deaf. Executives insisted the tritium levels posed no health risk, which was technically true but missed the point entirely. People didn't want scientific reassurances; they wanted to know why Exelon had hidden the leaks. The incident became a case study in how not to handle a crisis.

Then came the sleeping guards fiasco at Peach Bottom in 2009. A security contractor's video showed guards routinely sleeping during shifts, sometimes for hours. The imagery was devastating—sleeping guards at a nuclear plant, 90 miles from Washington D.C. The NRC's fine was modest, but the reputational damage was immense. Late-night comedians had a field day. "Exelon's new slogan," joked Jon Stewart, "We put the 'unclear' in nuclear."

Each incident reinforced public skepticism about nuclear power, making the political battles for subsidies even harder. Exelon spent millions on public relations, community outreach, and safety improvements, but trust, once broken, proved nearly impossible to rebuild.

Climate Change Salvation

Ironically, it was climate change that ultimately saved Exelon's nuclear fleet. As the scientific consensus on global warming solidified and extreme weather events multiplied, policymakers began recognizing an uncomfortable truth: without nuclear power, carbon reduction goals were impossible.

Nuclear plants provided 20% of America's electricity but over 50% of its carbon-free generation. Closing them would mean burning more natural gas, increasing emissions. The increase in carbon-free electricity from improved nuclear operations was equivalent to taking more than 1.1 million passenger cars off the road each year.

Exelon brilliantly repositioned its narrative. No longer was it a nuclear company; it was "America's largest clean energy company." The plants weren't aging industrial relics; they were "critical climate infrastructure." The subsidies weren't corporate welfare; they were "investments in carbon reduction."

The strategy worked. Democrats who had opposed nuclear for decades began supporting it as a climate necessity. Republicans who had championed fossil fuels recognized nuclear's role in energy independence. For perhaps the first time since the 1960s, nuclear power had bipartisan support.

The Operational Excellence Machine

By 2020, Exelon's nuclear fleet had become an operational marvel. The plants ran like Swiss watches—precise, reliable, profitable. Refueling outages that once took 60 days were completed in 20. Capacity factors exceeded 94% year after year. The fleet generated more electricity with 17 reactors than it had with 19 a decade earlier.

The secret was standardization. Every plant followed identical procedures. Operators trained at exact replicas of control rooms. Best practices spread instantly across the fleet. When Byron developed a new maintenance technique that saved two days on turbine overhauls, every plant implemented it within months.

The financial results were extraordinary. The nuclear fleet generated over $4 billion in annual revenue with EBITDA margins approaching 40%. The plants that John Rowe had bought for pennies on the dollar were now printing money. Wall Street analysts who had once urged Exelon to exit nuclear now praised it as the crown jewel.

The Separation Decision

Yet by 2021, Chris Crane faced a paradox. The nuclear fleet was performing better than ever, but it didn't fit with the rest of Exelon. The regulated utilities wanted to invest in grid modernization and electrification. The nuclear business needed to optimize merchant power markets and carbon credits. Investors complained they couldn't properly value a company that was part regulated utility, part merchant generator.

The board meetings grew increasingly tense. Directors representing utility investors wanted predictable, regulated returns. Those focused on generation saw opportunities in volatile power markets. Environmental, social, and governance (ESG) investors loved the carbon-free nuclear plants but worried about radioactive waste. Growth investors wanted expansion; value investors wanted dividends.

"We're trying to be all things to all people," Crane finally admitted to his senior team in early 2021, "and we're succeeding at none of them."

The solution was radical but obvious: split the company. Let the utilities be utilities. Let the nuclear fleet stand on its own. On February 24, 2021, Exelon announced it would spin off its generation business into a new company: Constellation Energy.

The nuclear fleet that had nearly bankrupted Commonwealth Edison, that had been saved by operational excellence and political subsidies, that had become one of America's most valuable clean energy assets, would finally stand alone. After two decades of integration, Exelon was unbundling itself. The empire was dividing, but perhaps in division, each piece would find its true value.

VII. The Great Unbundling: Constellation Spin-off (2022)

The Boardroom Bombshell

The Exelon board meeting on February 23, 2021, started like any other. Chris Crane presented fourth-quarter earnings (solid), discussed regulatory proceedings (progressing), and reviewed capital allocation (disciplined). Then he clicked to a slide that would reshape American energy: "Strategic Separation Proposal."

The room fell silent. Several directors had been briefed, but others were stunned. Crane was proposing to split Exelon in half—separating the regulated utilities from the competitive generation business, unwinding two decades of empire building.

"Ladies and gentlemen," Crane began, "we've built something remarkable. But we've also created a complexity discount that's destroying shareholder value. Our utility investors want predictable regulated returns. Our generation investors want commodity exposure and carbon upside. By trying to serve both, we're serving neither."

The numbers were compelling. Exelon traded at 11 times earnings while pure-play utilities fetched 15-18 times. The generation business, despite its clean energy credentials, was valued at liquidation prices. Goldman Sachs estimated a separation could unlock $10-15 billion in value.

Director Calvin Butler Jr., who would become CEO of the post-spin Exelon, asked the crucial question: "Chris, are we admitting that John Rowe's vision of an integrated energy company was wrong?"

Crane's response was careful: "John's vision was right for its time. Integration made sense when markets were deregulating and scale mattered. But the world has changed. Investors want focus. Regulators want simplicity. Customers want choice. It's time to evolve."

The Separation Architecture

The complexity of separating a $38 billion company with 34,000 employees across dozens of legal entities was staggering. McKinsey & Company was hired to design the separation, deploying 50 consultants who essentially moved into Exelon's headquarters. Every contract had to be split or assigned. Every employee had to be allocated. Every system had to be divided or duplicated.

The most contentious issue was talent. Both companies needed strong leadership, but there was only one Chris Crane. After weeks of deliberation, the board decided Crane would lead the new Constellation, taking the generation business he'd helped transform. Calvin Butler Jr., who had run Exelon Utilities, would become CEO of the remaining Exelon.

The nuclear fleet would obviously go to Constellation—23 reactors across 14 plants, representing the largest nuclear fleet in America. But what about the renewable assets? The power trading operation? The retail business serving 2 million customers? Each decision required careful analysis of economics, regulations, and strategic fit.

Financial engineering was equally complex. The companies needed separate capital structures, credit ratings, and dividend policies. JPMorgan and Barclays structured a "Reverse Morris Trust" transaction that would be tax-free to shareholders—a crucial consideration given the massive embedded gains in Exelon's stock.

Regulatory Chess Redux

If the business separation was complex, the regulatory approvals were byzantine. The split required consent from the Federal Energy Regulatory Commission, Nuclear Regulatory Commission, and public utility commissions in six states. Each regulator had different concerns and different leverage.

Illinois proved most challenging. Consumer advocates worried the separation would lead to higher rates as Exelon's utilities lost the financial cushion of generation profits. Labor unions feared job losses. Environmental groups questioned whether Commonwealth Edison would still support clean energy without its nuclear sister company.

The Illinois Commerce Commission hearings stretched for months. Exelon committed $700 million in rate credits, promised no layoffs for three years, and agreed to aggressive renewable energy targets. Even then, approval came down to a 3-2 vote, with the chairman casting the deciding ballot.

Maryland regulators extracted their own pound of flesh—commitments to maintain Baltimore employment, accelerated grid investments, and enhanced storm response protocols. The Nuclear Regulatory Commission required elaborate protocols to ensure Constellation could safely operate the nuclear fleet as a standalone company.

Market Reaction and Price Discovery

On February 2, 2022, Exelon completed the corporate spin-off of Constellation Energy, with Exelon shareholders retaining their current shares and receiving one share of Constellation for every three shares of Exelon held at the close of business on January 20, 2022.

The market reaction was explosive—but not immediately in the way Exelon had hoped. In pre-market trading, when Constellation began trading on a "when-issued" basis, the stock opened at $44 but quickly fell to $38. Traders were confused about the company's business model, unsure how to value a merchant nuclear generator in volatile power markets.

But as the day progressed and investors digested the separation's logic, sentiment shifted. Constellation closed its first day at $53.01, up 6% from its opening print. Exelon, now a pure-play utility, closed at $42.86, up 4%. Combined, the two companies were worth $8 billion more than the pre-announcement integrated Exelon.

The credit rating agencies validated the strategy. S&P upgraded Exelon to BBB+, citing its "improved business risk profile as a fully regulated utility." Constellation received a BBB- rating, investment grade but reflecting its merchant generation risks. Both companies could now optimize their capital structures for their specific business models.

Two Companies, Two Strategies

The separated companies immediately pursued divergent strategies that would have been impossible under one roof. Exelon, now purely regulated, announced $38 billion in grid investment over four years—upgrading ancient infrastructure, hardening against climate change, preparing for vehicle electrification. The predictable returns from these investments attracted utility investors seeking stable dividends.

Constellation went in the opposite direction, embracing volatility and opportunity. CEO Joe Dominguez, who had run Exelon's power business, announced aggressive growth plans: extending nuclear licenses to 80 years, developing hydrogen production at nuclear sites, and expanding energy marketing to commercial customers. The company projected 10% annual earnings growth—unheard of for utilities but reasonable for a merchant generator in tight power markets.

The cultural differences were immediately apparent. Exelon's investor calls became staid affairs discussing rate cases and regulatory proceedings. Constellation's calls were dynamic discussions of power prices, capacity auctions, and carbon markets. It was as if one company had split into two different species.

The Constellation Rocket Ship

Constellation's independent life began with remarkable timing. Russia's invasion of Ukraine in February 2022 sent natural gas prices soaring. Power prices followed, especially in regions where Constellation's nuclear plants operated. The Texas freeze of 2021 had already demonstrated the value of reliable baseload generation. Now Europe's energy crisis reinforced nuclear's importance.

The numbers were staggering. Constellation's 2022 revenue hit $24 billion with EBITDA of $3.5 billion. The stock price doubled within six months. The company that had been hidden inside Exelon's complexity was suddenly one of the market's hottest stories.

ESG investors, previously skeptical of nuclear, became believers. Constellation owned America's largest fleet of carbon-free generation at precisely the moment climate concerns peaked. Tech companies seeking clean energy for data centers signed long-term power purchase agreements at premium prices. Microsoft, Amazon, and Google competed for Constellation's carbon-free electrons.

Exelon's Quiet Transformation

While Constellation captured headlines, the new Exelon quietly executed its own transformation. Freed from the volatility of merchant generation, Exelon focused on operational excellence, achieving top quartile performance in customer satisfaction, reduced outage frequency, and faster service restoration, reinforced by substantial infrastructure investments.

The company's six utilities—ComEd, PECO, BGE, Pepco, Delmarva, and Atlantic City Electric—could finally get the investment they needed. Spanning a large, mainly urban service area across Delaware, the District of Columbia, Illinois, Maryland, New Jersey and Pennsylvania, Exelon served the corridors where America's energy transition would happen first.

The strategy was straightforward but powerful: invest aggressively in grid modernization, earn regulated returns, increase the rate base, grow earnings. No commodity exposure, no nuclear risks, just the steady blocking and tackling of utility operations. It was boring, predictable, and exactly what utility investors wanted.

The Validation

By late 2022, the separation's success was undeniable. The combined market value of Exelon and Constellation exceeded $80 billion, nearly double the pre-spin integrated company. Both stocks outperformed their peer groups. Employees who had received equity in both companies saw their wealth multiply.

John Rowe, retired but watching from the sidelines, offered grudging praise: "Chris Crane did what I couldn't—he recognized when integration no longer created value. It takes courage to undo your predecessor's work. But that's what great CEOs do."

The separation became a Harvard Business School case study in strategic transformation. Investment bankers pitched similar splits to other integrated utilities. "The Exelon Model" entered the corporate lexicon—shorthand for recognizing when conglomerate complexity destroys more value than it creates.

Yet questions remained. Had Exelon given up too easily on integration? Would the companies be stronger together in a crisis? What if power markets collapsed and Constellation needed Exelon's regulated cash flows? The separation was irreversible; only time would tell if it was wise. But in that moment, as 2022 ended with both companies thriving independently, the unbundling looked like strategic genius.

VIII. The New Exelon: Pure-Play Utility (2022–Present)

Day One of Independence

Calvin Butler Jr. stood before 300 employees at Exelon's Chicago headquarters on February 3, 2022, the first day after the separation. The atmosphere was subdued—half their colleagues had just left for Constellation, taking the nuclear plants and the generation trading floors that had defined Exelon's identity for two decades.

"I know this feels like a loss," Butler began, his voice carrying across the auditorium. "But we didn't lose anything. We gained focus. We gained clarity. We gained the ability to be the best utility company in America without distractions, without complexity, without apologizing for being what we are—the backbone of American electricity."

The numbers told the real story. The new Exelon operated six regulated utilities across Delaware, the District of Columbia, Illinois, Maryland, New Jersey and Pennsylvania, serving 10 million customers across some of America's most important economic corridors. This wasn't a remnant—it was a powerhouse.

The $38 Billion Bet

Within weeks of separation, Butler announced Exelon's strategic vision: $38 billion in capital expenditures over four years, a 10% increase from previous plans. The scale was breathtaking—more than NASA's entire annual budget, invested in poles, wires, substations, and transformers.

The investment thesis was elegant. Every dollar invested in the rate base earned a regulated return around 9-10%. With $38 billion in new investment, Exelon could grow its rate base by 7.4% annually through 2028. That meant predictable earnings growth of 5-7% per year—not spectacular, but reliable as clockwork.

The timing was perfect. The Inflation Reduction Act had just passed, providing massive incentives for electric vehicles and building electrification. The bipartisan infrastructure law allocated billions for grid modernization. State climate laws mandated aggressive renewable energy targets that required grid upgrades. Everything pointed toward massive electricity demand growth.

"We're not just maintaining the grid," Butler told investors. "We're rebuilding it for the next century. Every Tesla plugged in, every heat pump installed, every data center built—they all need our wires."

The Operational Excellence Revolution

Denis O'Brien, recruited from Australia's Ausgrid to run Exelon Utilities, brought a missionary zeal for operational improvement. His first all-hands meeting was legendary: he showed a slide of Customer Average Interruption Duration Index (CAIDI) scores for every major U.S. utility. Exelon's utilities filled the bottom quartile.

"This is embarrassing," O'Brien said bluntly. "We serve the nation's capital, Chicago, Philadelphia—and our customers lose power more often and for longer than those in Birmingham or Buffalo. That changes now."

O'Brien implemented what he called "Grid GPS"—Granular Performance Standards. Every feeder, every substation, every transformer was monitored in real-time. Machine learning algorithms predicted equipment failures before they happened. Drones inspected transmission lines after storms. Crews were pre-positioned based on weather forecasts.

The results were dramatic: Exelon's utilities achieved top quartile or better performance in customer satisfaction, reduced outage frequency, and faster service restoration. Chicago's summer 2023 heat wave, which would have caused massive blackouts a decade earlier, passed without major incident. Hurricane season 2023 saw power restored 40% faster than historical averages.

The Rate Case Marathon

But operational excellence meant nothing without regulatory approval to recover costs. Exelon faced a brutal reality: it needed rate increases in six jurisdictions, each with different politics, different processes, and different consumer advocates ready to fight.

The Pennsylvania Public Utility Commission hearings for PECO's rate case became a masterclass in regulatory theater. Consumer advocates painted Exelon as a greedy corporation squeezing struggling families. Exelon countered with infrastructure videos showing sparking transformers and sagging power lines. Industrial customers complained about reliability while opposing any rate increases.

The key breakthrough came when Exelon agreed to innovative rate designs. Time-of-use pricing encouraged customers to charge EVs overnight when power was cheap. Energy efficiency programs helped low-income customers reduce bills even as rates rose. Performance-based rates tied Exelon's returns to reliability metrics.

By year-end 2023, Exelon had secured $2.1 billion in annual rate increases across its utilities—not everything requested, but enough to fund the modernization program. The Illinois Commerce Commission chairman called it "a fair balance between infrastructure needs and customer affordability."

Financial Engineering and the Dividend Story

CFO Jeanne Jones, a former Goldman Sachs managing director, transformed Exelon's financial strategy. Gone was the complex hybrid structure trying to balance utility and merchant generation needs. In its place: pure utility finance—predictable, Investment-grade, boring in the best way.

The S&P credit rating upgrade to BBB+ validated the strategy, lowering borrowing costs by 50 basis points and saving hundreds of millions in interest expenses. Jones locked in long-term debt at historically low rates, terming out maturities to match long-lived utility assets.

The dividend strategy was equally disciplined. Exelon announced a 5-7% annual dividend growth target, matching earnings growth. The $1.60 per share annual dividend for 2025 provided a 3.5% yield—attractive for income investors but sustainable given 60% payout ratios.

The Electrification Opportunity

The real excitement came from demand growth projections that seemed almost fantastical. After decades of flat electricity demand, usage was about to explode. Electric vehicles alone could add 20-30% to electricity demand by 2035. Building electrification—replacing gas furnaces with heat pumps—could add another 15%. Data centers and AI computing might double that.

Exelon commissioned a study showing its service territories were ideally positioned for this growth. The Northeast Corridor from D.C. to Philadelphia contained the highest EV adoption rates outside California. Chicago was mandating all-electric new construction. Data centers clustered in Northern Virginia, powered by Dominion but interconnected through Exelon's transmission system.

"We're not hoping for electrification," Butler said at an investor conference. "We're planning for it, investing for it, and we'll be ready when it arrives."

The company launched "Grid of the Future" initiatives in each service territory. Chicago got microgrids that could island neighborhoods during outages. Philadelphia tested vehicle-to-grid technology letting EVs power homes during peaks. Washington D.C. piloted underground networks immune to weather events.

The Climate Resilience Imperative

But climate change threatened everything. The summer of 2024 brought unprecedented challenges: temperatures hit 105°F in Philadelphia, spawning demand records. Derechos with 100-mph winds tore through Illinois. Flash flooding submerged substations in Baltimore. The grid infrastructure built for 20th-century weather was failing in the 21st-century climate.

Exelon's response was massive: $6 billion specifically for climate resilience over five years. Wooden poles were replaced with steel or composite materials. Substations were elevated above flood plains. Underground networks expanded despite tripling installation costs. Vegetation management budgets doubled.

The investments paid off during 2024's Hurricane Marcus, which tracked up the East Coast in September. While other utilities saw millions lose power for weeks, Exelon's hardened infrastructure kept 85% of customers online. The remaining 15% saw power restored in under 48 hours. Regulators took notice, pre-approving climate resilience investments in subsequent rate cases.

Regulatory Challenges and Political Headwinds

Yet success bred scrutiny. Consumer advocates argued Exelon was gold-plating the grid—building unnecessary infrastructure to juice returns. Illinois legislators introduced bills to cap utility returns. Maryland's governor campaigned on reducing utility rates, targeting BGE specifically.

The most serious challenge came from distributed energy resources. Rooftop solar installations in Exelon's territories grew 40% annually. Battery storage became economical for commercial customers. Microgrids let communities disconnect from the utility entirely. The utility death spiral—where departing customers leave remaining ones paying for stranded infrastructure—seemed possible.

Exelon's response was strategic jujitsu: embrace the transformation. The company became the largest installer of utility-scale solar in the Mid-Atlantic. It offered battery storage programs where utilities owned and operated residential batteries. It transformed from opposing net metering to designing programs that fairly compensated solar customers while protecting non-solar ratepayers.

Technology and the Digital Grid

Chief Digital Officer Maria Rodriguez, poached from Google, led Exelon's technological transformation. Her mandate: turn dumb infrastructure into intelligent networks. Smart meters were just the beginning—Exelon deployed sensors everywhere, creating digital twins of its entire grid.

The control rooms looked like something from NASA. Giant screens showed power flows in real-time, colorful animations of electricity moving through the network. AI algorithms predicted equipment failures three days in advance with 94% accuracy. Customer service chatbots resolved 60% of inquiries without human intervention.

But the real revolution was the platform strategy. Exelon opened APIs letting third parties build on its infrastructure. EV charging companies could optimize charging based on grid conditions. HVAC manufacturers could adjust thermostats to reduce peak demand. The utility became not just a power deliverer but a platform for energy innovation.

The Affordability Crisis

Despite Exelon connecting customers to over $450 million in financial energy assistance in 2021, with average rates 16% below those of the largest U.S. metro cities, affordability remained contentious. The massive infrastructure investments required rate increases that hit struggling families hard.

The company's response was comprehensive but controversial. Payment plans extended to 24 months for customers behind on bills. Energy efficiency programs provided free LED bulbs and smart thermostats. A $100 million Exelon Foundation fund supported community organizations helping with utility bills.

Critics argued it wasn't enough. Public power advocates pushed for municipalization in several cities. Chicago aldermen proposed city takeover of ComEd's distribution system. The debate crystallized the fundamental tension: how to modernize aging infrastructure while keeping electricity affordable.

Performance and Outlook

By 2024, the results spoke for themselves. Annual revenue reached $23.0 billion, up 6.0% from 2023. The company reported GAAP earnings of $2.45 per share and adjusted operating earnings of $2.50 per share for 2024, meeting guidance despite significant weather challenges.

Looking forward, the company's strategy was clear and ambitious. Projecting $38 billion of capital expenditures over the next four years, an increase of 10% versus the prior plan, expected rate base growth of 7.4% and operating earnings per share compounded annual growth of 5-7% from 2024 to 2028. The dividend increased to $1.60 per share for 2025, demonstrating confidence in the business model.

The transformation was complete. From a complex conglomerate trying to balance merchant generation and regulated utilities, Exelon had become a focused, pure-play utility positioned for the energy transition. The stock market validated the strategy with steady appreciation, though questions remained about long-term growth potential and regulatory risks. But for now, in this moment of transformation and opportunity, the new Exelon had found its identity: not flashy, not exciting, but essential—the company that keeps the lights on while America reinvents its energy future.

IX. Playbook: Business & Investing Lessons

The Art of Utility M&A: Playing Three-Dimensional Chess

The conference room at Wharton Business School was packed with MBA students eager to hear Chris Crane's guest lecture on "Strategic M&A in Regulated Industries." Crane, now retired, opened with a simple question: "Who can tell me the difference between buying a tech company and buying a utility?"

A student raised her hand: "Utilities have more predictable cash flows?"

"Wrong focus," Crane replied. "When Facebook buys Instagram, they negotiate with shareholders and close in months. When we bought Pepco, we negotiated with shareholders for one day and with regulators for two years. In utility M&A, the sellers aren't really selling—the regulators are."

This was the first lesson: utility mergers are three-dimensional chess. You're negotiating with target management (dimension one), state regulators (dimension two), and political stakeholders (dimension three). Miss any dimension and the deal collapses, as Exelon learned when New Jersey killed the PSEG merger.

The key insight? Start with the regulators, work backward to economics. Exelon's successful deals—Constellation, Pepco—began with understanding what regulators wanted: job protection, rate stability, local investment. The price and terms followed. Failed deals started with financial engineering and tried to retrofit regulatory approval.

"We spent $100 million on the Pepco acquisition," Crane recalled, "and $80 million of that was on regulatory consultants, lobbyists, and community engagement. The bankers got $20 million. That tells you everything about utility M&A priorities."

Nuclear Economics: The Ultimate Operating Leverage Business

The beauty and curse of nuclear power is its cost structure: 80% fixed, 20% variable. A nuclear plant costs roughly the same to run whether it produces one megawatt or one thousand. This creates tremendous operating leverage—small changes in revenue create massive swings in profitability.

Consider Exelon's Quad Cities plant. Fixed costs: $400 million annually (labor, maintenance, property taxes, regulatory compliance). Variable costs: $50 million (uranium fuel). At $40/MWh power prices, the plant loses $100 million annually. At $50/MWh, it makes $200 million. A 25% price increase creates a $300 million profit swing.

This economics lesson explains everything about Exelon's nuclear strategy. When natural gas prices collapsed, nuclear plants hemorrhaged money because fixed costs couldn't adjust. When Exelon improved capacity factors from 75% to 94%, it was like building free power plants—same fixed costs, 25% more output.

The investing implication is profound: nuclear operators are essentially leveraged bets on power prices. When prices are low, they trade like distressed debt. When prices spike, they're money machines. Constellation's 2022-2023 performance—stock price doubling as power prices soared—was operating leverage in action.

The Regulated Utility Model: Banking in Disguise

Here's a secret most investors miss: regulated utilities aren't really power companies—they're banks that happen to own power lines. The business model is identical to banking: borrow money, invest it in assets, earn a spread.

A utility borrows at 4%, invests in power lines, and earns a regulated 9% return. The 5% spread on billions in rate base creates predictable earnings. Like banks, utilities are valued on book value multiples because earnings directly correlate with asset base.

The crucial difference? Banks face credit risk; utilities face regulatory risk. A bank's loan might default; a utility's regulator might disallow cost recovery. But while credit risk is unpredictable, regulatory risk follows patterns. Utilities that maintain good regulatory relationships—through reliability, community investment, and political savvy—consistently earn allowed returns.

Exelon mastered this game post-separation. By focusing solely on regulated utilities, it became predictable as a Treasury bond. The $38 billion capital program wasn't aggressive expansion—it was simply deploying capital at guaranteed spreads, exactly like a bank making loans.

Managing Stranded Assets: The Sunk Cost Fallacy Reversed

Business schools teach the sunk cost fallacy: don't throw good money after bad. But utilities face the reverse problem—regulators force them to throw good money after bad through "stranded asset" recovery.

When environmental regulations made coal plants obsolete, utilities couldn't just write them off. Regulators required continued operation or expensive decommissioning, plus utilities had to recover past investments through customer rates. The political economy was brutal: close a plant, lose jobs, anger politicians, but keep running it and lose money.

Exelon's solution was elegant: transform stranded assets into strategic weapons. Those money-losing nuclear plants? Get states to subsidize them as "clean energy resources." Old coal plants? Convert sites to solar farms or battery storage, maintaining jobs while changing technology. Obsolete city steam systems? Repurpose as district cooling networks for data centers.

The lesson: in regulated industries, there are no stranded assets, only stranded strategies. Every liability can become an asset with the right political framing and regulatory treatment.

Portfolio Theory: The Unbundling Imperative

John Rowe built Exelon on the theory that integrated utilities create value through diversification—stable regulated earnings offset volatile merchant generation. The 2022 separation proved him wrong, but not for reasons he could have foreseen.

The issue wasn't diversification but investor specialization. By 2020, investors had segmented into tribes: utility investors wanted predictability, ESG investors wanted clean energy, growth investors wanted merchant exposure. Trying to serve all three satisfied none.

The math was stark. Integrated Exelon traded at 11x earnings. Post-separation, utility Exelon trades at 16x while Constellation trades at 14x. The parts were worth 40% more than the whole. This wasn't unique to Exelon—across industries, conglomerates trade at discounts to pure plays.

The deeper lesson: portfolio theory works for investors who can easily rebalance but fails for companies where rebalancing requires board approval, regulatory consent, and years of execution. Investors can achieve diversification themselves; they don't need companies to do it for them.

Capital Allocation in Capital-Intensive Industries

Utilities face a unique capital allocation challenge: they must invest continuously just to maintain existing operations. Depreciation isn't an accounting fiction—it represents real infrastructure wearing out. Stop investing and the lights literally go out.

This creates a capital allocation waterfall. First priority: maintenance capex to keep assets running. Second: growth capex to meet new demand. Third: regulatory-mandated investments (storm hardening, smart meters). Only after these commitments can utilities consider dividends or buybacks.

Exelon's genius was recognizing that regulatory-mandated investments, while compulsory, were also the most profitable. When Illinois required smart meters, Exelon earned guaranteed returns on billions in spending. When Maryland mandated storm hardening, BGE got cost recovery plus profit margin. Regulations meant to burden utilities became profit centers.

The framework for utility investors: judge management not on absolute capital allocation but on optimizing within constraints. The best utility CEOs don't fight regulatory mandates—they profit from them.

The Energy Transition Opportunity: Riding the S-Curve

Calvin Butler's favorite slide showed electricity demand from 1950 to 2050. From 1950 to 1980: explosive growth as America electrified. From 1980 to 2020: flat as efficiency offset new uses. From 2020 to 2050: projected explosion as transportation and heating electrify.

"We're at the bottom of the second S-curve," Butler would say. "The first S-curve created modern utilities. The second will be even bigger."

The numbers support his optimism. Exelon projects a $10 billion to $15 billion transmission investment opportunity over the next 5 to 10 years. Every Tesla sold, every heat pump installed, every data center built increases electricity demand. The energy transition isn't just environmental policy—it's a demand supercycle for utilities.

But timing matters. Utilities that invest too early strand capital in underutilized assets. Invest too late and the grid fails, triggering regulatory backlash. The key is matching investment pace to demand growth, maintaining optimal capacity utilization while meeting reliability standards.

The Ultimate Question: Structural Advantage or Regulatory Capture?

The final lesson is philosophical: are utilities great businesses or regulatory captures? Bulls argue utilities have structural advantages—monopoly positions, essential services, guaranteed returns. Bears contend they're political pawns—subject to regulatory whims, forced to subsidize social programs, unable to earn excess returns.

The truth incorporates both views. Utilities are great businesses within regulatory constraints. They can't earn venture capital returns, but they also can't go bankrupt (usually). They're bond proxies with equity upside, boring businesses in an exciting industry.