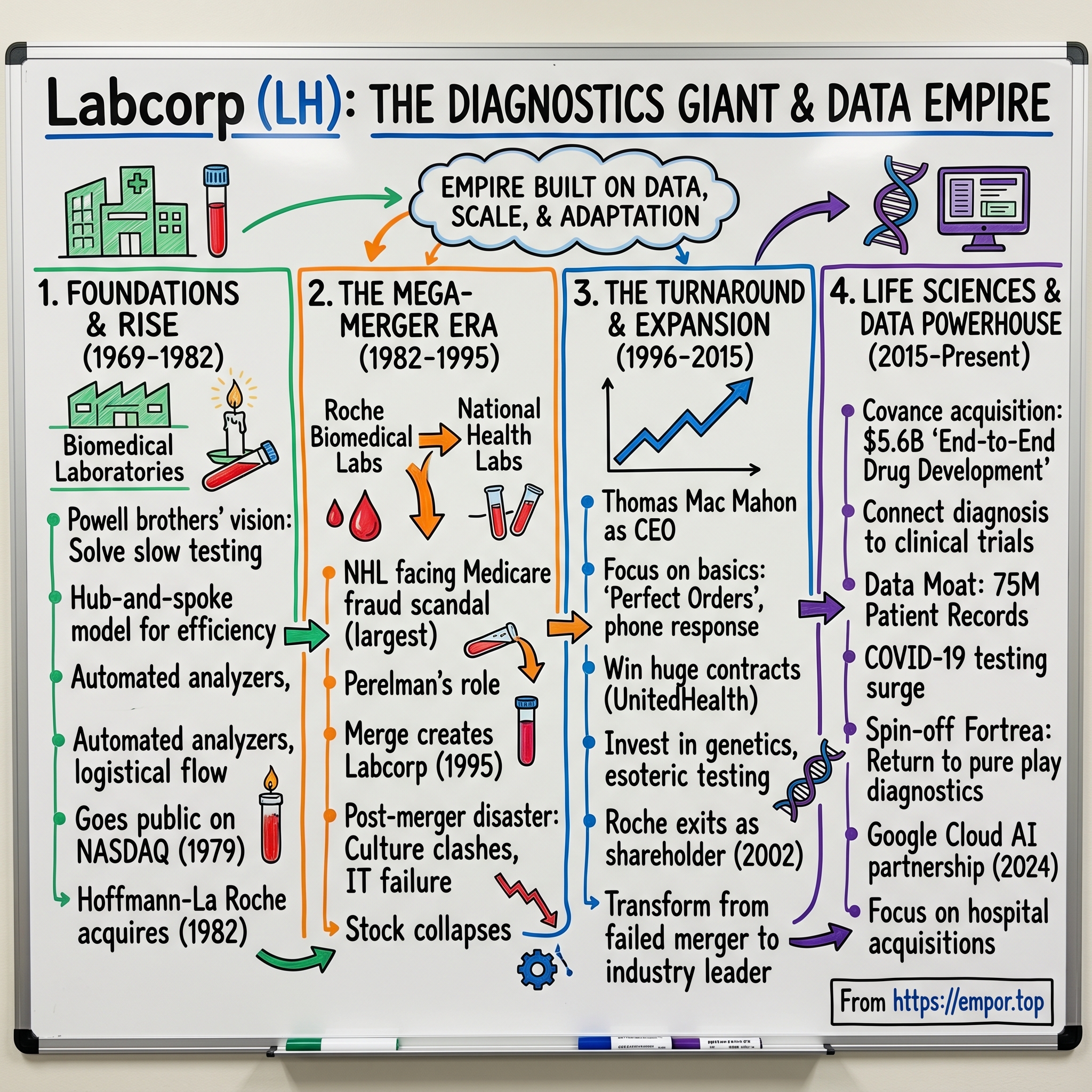

LabCorp: The Diagnostics Giant That Built Healthcare's Data Empire

I. Introduction & Episode Roadmap

The year is 1969. In the basement of an abandoned hospital in Burlington, North Carolina, three brothers are drawing blood samples by candlelight during a power outage. They've mortgaged their futures, borrowed from their biology professor father, and convinced local banks to bet on an audacious idea: that American healthcare is about to undergo a revolution in diagnostics, and whoever builds the infrastructure first will own the future.

Jim Powell, the medical student among them, had experienced the problem firsthand at Duke. A critically ill patient needed a specialized test. The sample was shipped to California. Two weeks later, the results arrived—three days after the patient had died. "Never again," he told his brothers. "We're going to fix this."

Today, that basement operation processes over 500 million tests annually as Laboratory Corporation of America—LabCorp—a $25 billion colossus that touches one in two Americans each year. With 2,000 patient service centers and 6,000 in-office phlebotomists across the United States, LabCorp has become the invisible infrastructure of American healthcare. Your annual physical, your COVID test, your genetic screening—there's a good chance LabCorp processed it, analyzed it, and added it to a database of 75 million patient records that represents one of healthcare's most valuable data moats.

But here's what makes this story remarkable: LabCorp isn't just a lab company that got big. It's a company that surfed every wave of healthcare transformation—from Medicare's creation to managed care's rise, from the genomics revolution to COVID-19's testing surge—and emerged stronger each time. It survived fraud scandals, hostile takeovers, and a disastrous merger that nearly killed it. It expanded from simple blood tests to drug development, from local labs to global operations, from analog processes to AI-powered diagnostics.

This is the story of how a regional laboratory became healthcare's data empire, why every attempt to disrupt it has failed, and what its journey reveals about building enduring value in healthcare. We'll explore the Powell brothers' original vision, the dark chapter of Medicare fraud that nearly destroyed the industry, the merger that created modern LabCorp, and the strategic masterstroke of acquiring Covance that transformed it from a diagnostics company into a life sciences powerhouse.

Along the way, we'll uncover the competitive dynamics that make this business far more defensible than it appears, the network effects that grow stronger with scale, and why, despite all the technological disruption in healthcare, the company processing blood samples in Burlington, North Carolina remains as essential today as it was in that hospital basement 55 years ago.

II. Origin Story: The Powell Brothers & Biomedical Laboratories (1969-1982)

Jim Powell was running late for rounds at Duke University Hospital in 1963 when the attending physician pulled him aside. "Powell, remember that lymphoma patient from three weeks ago? The one we sent the specialized panel to California for?" Jim nodded—the patient, a 42-year-old father of three, had been deteriorating rapidly. "Results just came in. Highly treatable variant. Would have responded beautifully to therapy." The attending paused. "He died last Tuesday."

That moment crystallized everything wrong with American laboratory medicine in the 1960s. Routine tests were done in hospital basements by technicians working banker's hours. Specialized tests—the ones that actually changed treatment decisions—required shipping samples across the country to one of a handful of reference laboratories. By the time results returned, patients had either recovered, deteriorated beyond help, or died. Medicine was becoming more sophisticated, but the infrastructure to support it was stuck in the 1940s.

Jim Powell saw an opportunity that went beyond fixing a broken system. He envisioned a hub-and-spoke model that would revolutionize diagnostic testing: centralized laboratories using cutting-edge automation to process massive volumes at low cost, connected to a network of collection sites that made testing convenient for patients and profitable for doctors. It was FedEx for blood samples, Walmart for lab tests, and it would require three things: capital, operational excellence, and perfect timing.

For capital, Jim turned to his brothers Thomas and Edward, both successful businessmen in Burlington. But the real bankroll came from their father, Thomas Edward Powell, whose story deserves its own telling. A biology professor at tiny Elon College, the elder Powell had built Carolina Biological Supply from nothing into the dominant provider of specimens and equipment to high school science classes across America. He understood scale, distribution, and most importantly, he understood that infrastructure businesses—unsexy, capital-intensive, operationally complex—were the ones that lasted.

In 1969, with $165,000 cobbled together from family funds and local bank loans, the Powell brothers purchased the abandoned Alamance General Hospital building in Burlington. The basement became their first laboratory. The upper floors, still containing abandoned patient beds and surgical equipment, served as overflow storage. Their first employee was a single technician who could run 20 tests per day. Their first client was a local family physician who sent three samples as a favor to the Powell family.

But the Powells weren't thinking small. From day one, they built for scale. They invested in the first generation of automated analyzers—machines that could run hundreds of tests simultaneously with minimal human intervention. They developed proprietary logistics systems to move samples from collection to testing to reporting faster than anyone else. Most critically, they understood that in diagnostics, volume wasn't just about revenue—it was about data, accuracy, and negotiating power.

The strategy was elegant in its simplicity: target the Research Triangle's booming medical community, offer faster turnaround than hospital labs, better service than national competitors, and prices that reflected their growing economies of scale. When a doctor's office called with a question, they reached a person who knew their name. When a hospital needed emergency testing at 2 AM, Biomedical's couriers were there in 30 minutes. When Medicare reimbursement rates changed, Biomedical adjusted their billing systems overnight while competitors took months.

By 1972, just three years after founding, Biomedical Laboratories had expanded beyond North Carolina into Virginia and South Carolina. Revenue hit $1 million. The Powells reinvested every penny into new equipment, new locations, and most importantly, new capabilities. They were among the first to offer comprehensive drug testing for employers, helping create an entirely new market. They pioneered direct-to-physician marketing, sending sales representatives with medical backgrounds to explain complex test panels. They turned laboratory medicine from a necessary evil into a profit center for physician practices.

The real breakthrough came in 1975 when Biomedical won the contract to provide laboratory services for North Carolina's Medicaid program. It was a massive validation—the state government was essentially saying this six-year-old company was more reliable than established hospital laboratories. Revenue jumped to $8 million. The company added "Reference" to its name, becoming Biomedical Reference Laboratories, signaling its evolution from local lab to regional powerhouse.

By 1979, the Powells faced a crossroads. They had built something remarkable—a profitable, growing company with 400 employees and $30 million in revenue. But the diagnostics industry was consolidating rapidly. National players were acquiring regional labs, using public market capital to fund expansion. The Powells could remain a large regional player, constantly defending their turf, or they could join the national stage.

They chose to go public, listing on NASDAQ in September 1979 at $11 per share. The offering raised $15 million, valuing the company at $55 million. Jim Powell, now CEO, told investors they would use the proceeds to expand into Florida and Texas, upgrade their technology infrastructure, and potentially acquire smaller laboratories. What he didn't say—what he perhaps didn't know—was that Biomedical Reference Laboratories had already attracted the attention of one of the world's largest pharmaceutical companies.

Hoffmann-La Roche, the Swiss pharmaceutical giant, was watching the American diagnostics market with growing interest. They saw diagnostic testing not just as a service business but as the future of pharmaceutical development. Who better to develop companion diagnostics—tests that determined which patients would respond to specific drugs—than a company that understood both medicines and testing? And who better to acquire than the fastest-growing, best-managed regional laboratory in America?

The courtship was swift. In 1982, just three years after going public, Roche acquired Biomedical Reference Laboratories for $163.5 million—nearly triple its IPO valuation. The Powell brothers had turned a $165,000 investment into a nine-figure exit in just 13 years. Jim Powell agreed to stay on as president, helping Roche build what would become Roche Biomedical Laboratories, soon to be one of the four largest laboratory companies in America.

But this was just the first act. Roche's deep pockets would fund massive expansion, sophisticated new testing capabilities, and eventually, a merger that would create modern LabCorp. The Powell brothers had built the foundation, but the empire was yet to come.

III. The National Health Laboratories Parallel Story (1971-1995)

While the Powell brothers were building their testing empire in North Carolina's Research Triangle, 400 miles south in Fort Lauderdale, a very different laboratory story was unfolding—one that would showcase both the incredible profit potential of diagnostic testing and the dark temptations that came with processing millions of Medicare claims.

National Health Laboratories started life in 1968 as DCL BioMedical, a small clinical testing operation in South Florida. The timing was perfect: Medicare had launched just three years earlier, creating a guaranteed payment stream for medical services. Florida's exploding retiree population meant endless demand for blood tests, urinalysis, and basic panels. All you needed was a CLIA-certified lab, some phlebotomists, and a billing department that understood Medicare's arcane reimbursement codes.

In 1971, Revlon—yes, the cosmetics company—acquired DCL BioMedical as part of its bizarre 1970s strategy to become a healthcare conglomerate. Under Revlon's ownership, the company was renamed National Health Laboratories Incorporated in 1974 and began an aggressive expansion across the Sun Belt. The business model was ruthlessly efficient: target high-Medicare markets, offer doctors lucrative contracts for their testing business, and bill the government for every test possible.

By 1980, National Health had become a cash machine, generating 40% EBITDA margins on work that required minimal capital investment. The laboratory business, executives discovered, had an almost narcotic quality—once you had the infrastructure, every additional test was nearly pure profit. Medicare paid promptly, rarely questioned bills, and the aging American population guaranteed volume growth of 10-15% annually.

Enter Ronald Perelman, the corporate raider who would become one of the 1980s' most controversial figures. In 1985, Perelman acquired Revlon in a hostile takeover, inheriting National Health Laboratories as part of the package. While the cosmetics business got the headlines, Perelman quickly recognized that the laboratory subsidiary was the real jewel. He spun it off as an independent company, took it public, and retained majority control.

Under Perelman's ownership, National Health Laboratories transformed from an aggressive competitor into something more troubling. The company pioneered what it called "pull-through" strategies—paying doctors above-market rates for routine tests to capture their lucrative specialized testing. It developed sophisticated software to automatically add related tests to doctor orders, a practice called "reflex testing" that tripled average bill sizes. Most controversially, it began offering doctors "consulting agreements" and "lease payments" that looked suspiciously like kickbacks for testing referrals.

The money was staggering. By 1991, National Health Laboratories generated $635 million in revenue with net margins approaching 15%. Perelman's stake was worth over $500 million. The company's stock price had increased ten-fold since its IPO. Wall Street analysts praised its "innovative marketing strategies" and "deep physician relationships." What they didn't know was that federal investigators had been building a case against the company for three years.

The hammer fell on March 3, 1992. FBI agents raided National Health Laboratories' headquarters, carting away boxes of billing records, internal memos, and physician contracts. The charges were damning: systematic Medicare fraud, including billing for tests never performed, billing for unnecessary tests, and paying illegal kickbacks to doctors. The investigation, code-named "Operation Labscam," would become the largest healthcare fraud case in American history.

The details that emerged were shocking. Prosecutors alleged that National Health had created elaborate schemes to defraud Medicare, including:

- "Unbundling" comprehensive test panels into individual components to maximize reimbursement

- Running tests on samples that were too old or contaminated to produce accurate results

- Creating fictitious "standing orders" that automatically triggered expensive test cascades

- Paying doctors $100,000+ annual "consulting fees" for minimal or no actual work

- Providing free equipment, staff, and supplies to physician offices in exchange for testing referrals

The whistleblower testimony was particularly damaging. Former employees described a culture where managers received bonuses based on Medicare billing volumes, where sales representatives were taught to coach doctors on maximizing reimbursements, and where internal compliance warnings were routinely ignored. One former executive testified that the company viewed Medicare fraud fines as "a cost of doing business," budgeting millions annually for settlements.

In December 1992, National Health Laboratories agreed to pay $111 million to settle the charges—at the time, the largest Medicare fraud settlement in history. The company admitted no wrongdoing but agreed to enter a "corporate integrity agreement" that subjected it to intense federal oversight. The reputational damage was severe. Major hospital systems canceled contracts. Physicians, fearing their own liability, moved their testing elsewhere. The stock price collapsed from $28 to $7.

But Perelman, ever the financial engineer, saw opportunity in crisis. The laboratory industry was consolidating, and National Health—despite its tainted reputation—still had valuable assets: advanced testing capabilities, a national network of collection sites, and ironically, some of the industry's most sophisticated billing systems. What it needed was a merger partner with clean hands and deep pockets.

That partner emerged in an unexpected form: Roche Biomedical Laboratories, the company built on the foundation of the Powell brothers' original Biomedical Reference Laboratories. Roche had spent the decade since acquiring Biomedical building one of the nation's most advanced testing operations. It had avoided the Medicare fraud scandals through conservative billing practices and Swiss-style compliance culture. But it lacked National Health's market penetration and operational efficiency.

The merger negotiations, which began in secret in early 1994, were complex. Roche wanted National Health's assets but not its liabilities. Perelman wanted to exit with maximum value while avoiding further legal exposure. The solution was elegant: Roche would contribute its laboratory operations plus $186.7 million in cash to National Health Laboratories Holdings in exchange for 49.9% of the combined company. Perelman would receive approximately $100 million in cash and retain a minority stake. The new entity would be called Laboratory Corporation of America Holdings—LabCorp.

On paper, it was a merger of equals—the third and fourth largest laboratory companies in America joining forces to challenge industry leader SmithKline Beecham Clinical Laboratories. Combined revenue would approach $1.7 billion. The company would have 39 major laboratories, 15,000 employees, and the most comprehensive test menu in the industry. Analysts predicted significant synergies from eliminating duplicate facilities, standardizing operations, and leveraging combined purchasing power.

The reality would prove far messier. The two companies had radically different cultures—Roche's conservative, process-oriented approach versus National Health's aggressive, sales-driven mentality. Their information systems were incompatible. Their billing practices were at opposite extremes. Most critically, the Medicare fraud settlement's corporate integrity agreement would hang over the combined company like a sword of Damocles, limiting its ability to implement aggressive growth strategies.

As 1995 dawned, the merger was set to close. James Powell, the medical student who had started Biomedical Reference Laboratories in a hospital basement 26 years earlier, would return as CEO of the combined company. His task: merge two incompatible cultures, satisfy federal oversight requirements, compete against larger rivals, and somehow create value from what many observers considered a deeply flawed transaction. The smart money was betting against him.

IV. The Mega-Merger: Creating LabCorp (1995)

The conference room at the Waldorf-Astoria fell silent as James Powell stood to address the assembled bankers, lawyers, and executives. It was December 12, 1994, and after six months of secret negotiations, they were about to announce the creation of Laboratory Corporation of America. Powell, now 58 with silver hair and the careful manner of someone who had built and sold companies, looked at the faces around the table—Roche executives skeptical of partnering with a tainted company, National Health managers defensive about their past, investment bankers calculating their fees.

"Gentlemen," Powell began, "we're not here to create the biggest laboratory company in America. We're here to create the best one. And that's going to require everyone in this room to forget everything they think they know about how this industry works."

The deal structure itself was a masterpiece of financial engineering that satisfied all parties while creating massive complexity. Here's how it worked: Hoffmann-La Roche would contribute its Roche Biomedical Laboratories subsidiary—valued at approximately $800 million—plus $186.7 million in cash to National Health Laboratories Holdings. In exchange, Roche would receive 49.9% of the combined company's equity, keeping them just below the 50% threshold that would require full consolidation on their financial statements.

Ronald Perelman, who owned 47% of National Health Laboratories, would see his stake diluted to approximately 23.5% but would receive $100 million in cash—effectively allowing him to take money off the table while maintaining significant upside. Public shareholders would own the remaining 26.6%. The new company would assume $590 million in existing debt from both entities, plus an additional $288 million in new borrowing to finance the cash payments, bringing total debt to nearly $960 million.

The projected synergies were tantalizing. Investment bankers from Morgan Stanley presented slides showing $150 million in annual cost savings from consolidating overlapping laboratories, eliminating redundant sales forces, and leveraging combined purchasing power. The companies had complementary geographic footprints—Roche strong in the Northeast and Midwest, National Health dominant in the South and Southwest. Together, they would have the scale to compete for national managed care contracts that neither could win alone.

But from day one, the cultural integration was a disaster. The first combined management meeting, held at LabCorp's new Burlington headquarters in January 1995, devolved into barely concealed hostility. Roche executives, speaking in precise Swiss-accented English, presented 200-page process documents for laboratory standardization. National Health managers, many of whom had survived the fraud investigation, responded with eye rolls and whispered comments about "European bureaucracy."

The IT integration was even worse. Roche Biomedical ran on a customized IBM mainframe system that had been developed over 15 years. National Health used a patchwork of acquired systems held together by proprietary middleware. The consultants from Accenture estimated it would take three years and $200 million to create a unified platform. They had budgeted six months and $30 million.

Then there were the physicians. Many doctors' offices had relationships with both companies, often playing them against each other for better pricing. When the merger was announced, instead of celebrating reduced complexity, physicians panicked about losing negotiating leverage. Major hospital systems in Texas and California immediately put their contracts out for bid, inviting Quest Diagnostics and SmithKline Beecham to compete for business LabCorp had considered secure.

The operational integration exposed deeper problems. When teams began consolidating laboratories, they discovered that Roche and National Health used different testing methodologies for many assays. A cholesterol test run in a former Roche lab might produce a result 5-10% different from the same sample tested in a former National Health facility. For physicians accustomed to tracking patient trends over time, this was unacceptable. LabCorp had to maintain parallel testing operations far longer than planned, destroying the projected cost savings.

The sales force integration was particularly contentious. Roche's sales representatives were technical specialists, often with advanced degrees, who sold based on scientific credibility. National Health's reps were relationship builders who knew every physician's birthday, golf handicap, and kids' names. When Powell tried to combine them into unified territories, the result was chaos. Former Roche reps alienated doctors with their academic approach. Former National Health reps couldn't answer technical questions about new genetic tests.

By May 1995, just five months after the merger announcement, the wheels were coming off. First-quarter results showed revenue down 3% year-over-year as clients defected. Operating margins collapsed from a projected 15% to barely 8%. The stock price, which had briefly touched $20 on merger announcement, fell below $12. The debt load, manageable at projected cash flows, suddenly looked crushing.

The Wall Street Journal ran a devastating piece titled "Laboratory Experiment Gone Wrong," featuring interviews with disgruntled employees and confused physicians. One anonymous executive was quoted saying, "It's like watching two dysfunctional families trying to plan a wedding while the house is on fire." Moody's put LabCorp's debt on negative watch. Three board members representing public shareholders threatened to resign.

Powell, who had built Biomedical Reference Laboratories through sheer determination, refused to give up. In June 1995, he made a dramatic decision: instead of trying to blend the cultures, he would preserve what worked from each. Roche's rigorous quality standards would govern all testing operations. National Health's aggressive sales culture would drive growth. The company would maintain dual headquarters—Burlington for operations, Fort Lauderdale for sales and marketing—until natural attrition allowed consolidation.

The financial engineering to buy time was equally creative. Powell negotiated a new $1.2 billion credit facility with a syndicate led by Chase Manhattan, using future cash flows as collateral. He sold non-core assets, including a small diagnostics manufacturing division, to raise $80 million. Most controversially, he implemented "Project Titan," a massive cost-cutting program that eliminated 2,000 jobs—nearly 15% of the workforce.

The Medicare corporate integrity agreement, inherited from National Health's fraud settlement, added another layer of complexity. Federal monitors had the right to review all billing practices, physician contracts, and marketing materials. Every new sales initiative required approval from compliance officers. The company spent $15 million annually on external auditors. While competitors offered physicians lucrative partnerships, LabCorp could barely buy them lunch without triggering scrutiny.

By December 1995, a year after the merger announcement, LabCorp was technically profitable but strategically adrift. Revenue for the year came in at $1.63 billion, below the $1.7 billion projected. The company posted a net loss of $38 million after restructuring charges. The stock price ended the year at $8.75, down 56% from its merger-announcement peak. Forbes magazine included LabCorp in its annual "Worst Mergers" list, calling it "a case study in how not to combine companies."

Yet Powell saw something others didn't. Despite the chaos, LabCorp had successfully integrated its basic testing operations. The company was processing 250,000 specimens daily with 99.7% accuracy. Customer defections had stabilized. The combined company's test menu—over 4,000 different assays—was unmatched in the industry. Most importantly, the fundamental thesis remained sound: healthcare was becoming more complex, diagnostic testing was essential, and scale would ultimately win.

In his 1995 annual letter to shareholders, Powell wrote: "This has been a year of extraordinary challenge and transformation. We have taken two proud companies with different histories, cultures, and approaches, and begun forging them into something new. The process has been more difficult than anticipated, the costs higher than projected. But we are building the foundation for a company that will define diagnostic medicine for the next generation."

The skeptics far outnumbered the believers. Short interest in LabCorp stock reached 30% of float. The company's largest institutional investor, Fidelity, reduced its position by half. Ronald Perelman, who had remained uncharacteristically quiet during the turmoil, was rumored to be exploring a sale of his stake to private equity.

As 1996 began, LabCorp faced a stark choice: continue the slow integration and risk being picked apart by competitors, or make bold moves that could either save or destroy the company. Powell, the medical student who had started this journey after watching a patient die waiting for test results, chose bold. The turnaround that followed would become a Harvard Business School case study, but first, things would get even worse.

V. The Turnaround Years (1996-2006)

Thomas Mac Mahon stepped off the elevator at LabCorp's Burlington headquarters on a humid June morning in 1997, carrying a single cardboard box and wearing the same rumpled suit he'd worn to his interview. The 52-year-old former hospital administrator had just been named CEO, replacing James Powell who agreed to step aside after the board's ultimatum: find new leadership or face a hostile takeover. Mac Mahon's first act wasn't to call an all-hands meeting or issue a strategy memo. He walked straight to the laboratory floor, put on a lab coat, and spent his first day watching technicians process samples.

"I wanted to understand what actually worked," Mac Mahon would later tell Fortune magazine. "Everyone was focused on what was broken—the IT systems, the culture clash, the debt. But 15,000 people were coming to work every day and successfully processing half a million tests. That operational excellence was our foundation. Everything else could be fixed."

Mac Mahon was an unusual choice to lead a diagnostics company. He had no laboratory experience, no medical degree, and had never run a public company. What he had was a reputation as healthcare's best operational mind. At Franciscan Health System, he'd consolidated seven struggling hospitals into the Southwest's most profitable Catholic health network. At HCA, he'd turned around 12 underperforming facilities in 18 months. His philosophy was simple: focus relentlessly on what customers value, eliminate everything else, and execute with precision.

His first 100 days at LabCorp became legendary in turnaround circles. He visited 47 laboratories, met with over 500 physicians, and personally reviewed 10,000 customer complaints. He discovered that LabCorp's problems weren't primarily about integration—they were about basic blocking and tackling. Test results were delivered late. Phone calls went unanswered. Billing errors frustrated physicians. The merger chaos had distracted management from operational fundamentals.

The transformation started with something seemingly trivial: answer the phone. Mac Mahon discovered that the average hold time for physicians calling with questions was 12 minutes. He implemented a new standard: every call answered within 60 seconds. It required hiring 200 additional customer service representatives and completely reorganizing the call center operations, but within six months, physician satisfaction scores increased by 40%.

Next came reliability. Mac Mahon introduced what he called "Perfect Orders"—test results delivered accurately, completely, and on time. In 1997, only 76% of orders met this standard. He set a target of 95% within two years. Achieving it required standardizing processes across all laboratories, investing $50 million in new automation equipment, and implementing rigorous quality controls. By 1999, LabCorp hit 94.7% Perfect Orders, industry-leading performance that became a key competitive advantage.

But Mac Mahon's masterstroke was recognizing that LabCorp's competition wasn't just other laboratories—it was the entire inefficiency of healthcare administration. He pioneered electronic ordering and resulting systems that eliminated paper requisitions and fax machines. He created integrated billing platforms that simplified physician office operations. He turned LabCorp from a vendor into a partner that made doctors' lives easier.

The financials reflected the operational improvements. Revenue grew from $1.6 billion in 1996 to $2.2 billion in 2000. More importantly, EBITDA margins expanded from 8% to 18% as operational efficiency improved. The stock price, which had bottomed at $6 in late 1996, reached $42 by early 2000. The debt that had nearly crushed the company was refinanced at lower rates and systematically paid down.

During this period, LabCorp also began building capabilities that would define its future. In 1999, the company acquired National Genetics Institute for $80 million, gaining HIV genotyping and viral load testing capabilities just as these tests were becoming standard of care. The acquisition seemed expensive for a company with only $20 million in revenue, but Mac Mahon saw what others missed: genetic testing would transform medicine, and LabCorp needed to be at the forefront.

The genomics bet paid off faster than anyone expected. In 2001, LabCorp launched one of the industry's first pharmacogenetic tests, determining which patients would respond to certain cancer drugs based on their genetic profiles. By 2003, the company's esoteric testing division—specialized tests beyond routine blood work—generated $400 million in revenue with 40% margins. Wall Street analysts who had dismissed LabCorp as a commodity business suddenly recognized it as a technology company.

The competitive dynamics with Quest Diagnostics during this period deserve special attention. Quest, formed through the 1990s consolidation of Corning's MetPath, SmithKline Beecham Clinical Laboratories, and dozens of smaller labs, had emerged as the industry leader with 30% market share versus LabCorp's 25%. The rivalry was intense and often personal. Both companies would bid aggressively for the same contracts, sometimes operating at a loss to deny business to their rival.

The battle for exclusive managed care contracts became the primary battlefield. In 2002, LabCorp won the exclusive laboratory contract for UnitedHealth Group, covering 18 million lives. It was a massive victory that guaranteed volume and shut Quest out of a significant market segment. Quest responded by winning Aetna's business. The industry was bifurcating into LabCorp and Quest territories, with smaller players increasingly squeezed out.

Mac Mahon's acquisition strategy during this period was disciplined and strategic. Unlike the failed mega-merger that created LabCorp, he focused on bolt-on acquisitions that added specific capabilities or geographic density. The 2001 acquisition of Dynacare's U.S. operations for $385 million brought strong presence in the Pacific Northwest. The 2003 purchase of Dianon Systems for $595 million added pathology expertise and hospital relationships. Each acquisition was integrated methodically, with clear synergy targets and cultural integration plans.

The most transformative acquisition of this era was Esoterix in 2002. For $155 million, LabCorp acquired not just a specialty laboratory but a different business model. Esoterix focused exclusively on complex, high-margin tests for specialty physicians—oncologists, endocrinologists, rheumatologists. Its average revenue per test was $400 versus $25 for routine testing. Mac Mahon kept Esoterix as a separate brand, recognizing that specialty physicians valued its focused expertise.

By 2004, LabCorp had completed its transformation from troubled merger to industry leader. Revenue reached $3.1 billion. The company was processing 300 million tests annually. The stock price hit $55, giving LabCorp a market capitalization of $8 billion. The Medicare corporate integrity agreement, that albatross from the National Health fraud settlement, finally expired. Mac Mahon had delivered one of healthcare's great turnarounds.

But the industry was changing again. Hospitals were consolidating and bringing testing in-house. Managed care organizations were demanding ever-lower prices. New technologies—from point-of-care testing to direct-to-consumer genetics—threatened to disrupt the traditional laboratory model. Most significantly, pharmaceutical companies were struggling with drug development productivity and looking for partners who could help them bring drugs to market faster and more efficiently.

In March 2002, a critical milestone occurred that would shape LabCorp's future: Roche sold its remaining 49.9% stake in the company through a secondary offering at $36 per share, raising $2.8 billion. LabCorp was finally free from its founding shareholder, able to chart its own strategic course. The company used the opportunity to implement a poison pill defense against hostile takeovers and authorize a $500 million share buyback program.

As Mac Mahon prepared to retire in 2006, handing leadership to his hand-picked successor David King, he reflected on the journey in his final shareholder letter: "Nine years ago, LabCorp was a failed merger, overwhelmed by debt, losing customers, and lacking strategic direction. Today, we are the partner of choice for physicians, health plans, and hospitals across America. We've proven that operational excellence, customer focus, and strategic discipline can transform even the most challenged situations."

The numbers backed up his claims. From 1997 to 2006, LabCorp's revenue grew at 12% annually. EBITDA increased from $130 million to $620 million. The stock delivered a 22% annual return, dramatically outperforming the S&P 500. The company that Forbes had called one of the worst mergers of the 1990s was now featured in Good to Great as an example of successful transformation.

But Mac Mahon's greatest achievement might have been cultural. He had taken two incompatible organizations—Roche's process-oriented culture and National Health's aggressive sales mentality—and forged them into something new: a company that combined operational excellence with commercial innovation. Employee turnover fell from 35% to 12%. LabCorp regularly appeared on Fortune's "Best Companies to Work For" lists.

As David King took the CEO reins in November 2006, he inherited a strong company facing new challenges. The core diagnostic testing business was mature, growing at GDP rates. Price pressure from managed care was intensifying. Most intriguingly, pharmaceutical companies were approaching LabCorp with a radical proposition: why just test patients when you could help develop the drugs they need? The answer to that question would lead to LabCorp's boldest move yet.

VI. The Covance Acquisition: Becoming a Life Sciences Giant (2015)

David King stood before a packed auditorium at J.P. Morgan's 2014 Healthcare Conference in San Francisco, preparing to field what he knew would be a skeptical question. An analyst from Bernstein had just asked the question everyone was thinking: "David, LabCorp is a diagnostics company. You test patients. Covance develops drugs. They test mice. Why on earth would you pay $5.6 billion—your entire market cap just five years ago—to enter a completely different business?"

King smiled, having anticipated this moment for the two years he'd been secretly negotiating the largest acquisition in laboratory services history. "Let me tell you about a patient I met last month," he began. "Susan, 42 years old, diagnosed with late-stage lung cancer. Her oncologist ordered our comprehensive genomic panel, which identified a rare mutation. There was a drug in Phase III trials that targeted exactly that mutation. But Susan couldn't get it—the trial was fully enrolled. She died three months later."

The auditorium fell silent. King continued: "Now imagine if the company that diagnosed Susan's cancer was also the company running that clinical trial. Imagine if we could seamlessly connect diagnosis to treatment, if we could use our diagnostic data to design better trials, recruit patients faster, and bring life-saving drugs to market years earlier. That's not entering a different business. That's creating an entirely new one."

The vision King articulated—end-to-end drug development from discovery through commercialization—had been percolating since his first days as CEO in 2006. But it took the convergence of multiple trends to make it possible: the genomics revolution making personalized medicine real, pharmaceutical companies desperate to improve R&D productivity, and Covance itself struggling as an independent company in an consolidating industry.

Covance's journey to this moment was its own remarkable story. Founded in 1997 through the merger of Corning Pharmaceutical Services and Hazleton Laboratories, Covance had built one of the world's largest contract research organizations (CROs). The company managed clinical trials for pharmaceutical companies, conducted preclinical safety testing, and operated central laboratories for trial sample analysis. By 2014, Covance generated $2.4 billion in revenue but faced intense pressure from larger competitors like Quintiles and PPD.

The courtship between LabCorp and Covance began informally at a 2013 industry conference in Vienna. King and Covance CEO Joe Herring found themselves seated together at a dinner, commiserating about common challenges: pricing pressure, regulatory complexity, the need for global scale. After several drinks, Herring posed a hypothetical: "What if we combined forces? Your diagnostic data informing our trial design. Our drug development expertise creating companion diagnostics for your testing menu."

What started as idle speculation became serious exploration. King assembled a small team, code-named "Project Saturn," to analyze the strategic rationale. The findings were compelling: LabCorp's diagnostic database could identify patients for clinical trials 50% faster than traditional recruitment methods. Covance's drug development expertise could help LabCorp create proprietary tests for new therapies. Together, they could offer pharmaceutical companies something no one else could—a partner that could take a drug from concept to market and develop the diagnostic tests to identify which patients would benefit.

The financial engineering of the deal was complex but elegant. LabCorp would pay $75.76 in cash and 0.2686 LabCorp shares for each Covance share, valuing the company at $105 per share—a 32% premium to Covance's closing price before acquisition rumors emerged. To finance the $4.4 billion cash portion, LabCorp arranged a bridge loan from Bank of America Merrill Lynch, planning to refinance with long-term debt and potentially selling non-core assets.

The integration plan was dramatically different from the disastrous 1995 merger that created LabCorp. Instead of forcing immediate consolidation, King planned to run Covance as a separate division for at least three years. Covance would keep its brand, management team, and operational independence. Integration would focus on specific areas where collaboration created clear value: using LabCorp's patient data for trial recruitment, developing companion diagnostics, and combining laboratory operations where it made sense.

When the deal was announced on November 3, 2014, the market reaction was swift and brutal. LabCorp's stock fell 7% in a single day. Analysts questioned the strategic logic, the integration risk, and especially the price. Covance was trading at 18 times EBITDA, rich even for a growing CRO. LabCorp would add $5.5 billion in debt to its balance sheet, pushing leverage ratios to uncomfortable levels. Moody's immediately put LabCorp's credit rating on negative watch.

The skepticism was understandable. The laboratory services and CRO industries had fundamentally different business models. Diagnostic testing was a volume business with thin margins, rapid turnaround, and local market dynamics. Drug development was a project business with long cycles, global operations, and complex regulatory requirements. LabCorp's sales force called on physicians' offices; Covance's business developers negotiated with pharmaceutical executives. The IT systems, operational processes, and even corporate cultures were entirely different.

But King had done his homework. He identified $150 million in annual cost synergies, primarily from combining central laboratory operations, eliminating duplicate facilities, and leveraging purchasing power. More importantly, he projected $500 million in revenue synergies within five years from new service offerings that neither company could create alone. The math worked if—and only if—the execution was flawless.

The integration began even before the deal closed in February 2015. Joint teams identified 50 "Quick Win" initiatives that could demonstrate value within the first 100 days. The most visible was Project Beacon, which used LabCorp's diagnostic database to accelerate patient recruitment for a Covance-managed oncology trial. What typically took six months was accomplished in ten weeks, saving the pharmaceutical sponsor $15 million and potentially bringing a life-saving drug to market months earlier.

The cultural integration proved surprisingly smooth, perhaps because both companies had learned from past mistakes. Instead of forcing uniformity, King celebrated differences. LabCorp's operational efficiency complemented Covance's scientific creativity. Covance's global reach enhanced LabCorp's domestic strength. Town halls featured employees from both companies sharing success stories. Integration wasn't about one company absorbing another but about creating something new.

By the end of 2015, the early results validated King's vision. The combined company generated $8.5 billion in revenue with EBITDA margins expanding to 19%. The identified cost synergies were achieved six months ahead of schedule. More importantly, LabCorp won three major integrated drug development contracts where the combination of diagnostic and CRO capabilities was the differentiator. The stock price, which had bottomed at $95 after the acquisition announcement, climbed back above $120.

The real breakthrough came in 2016 with the launch of LabCorp's Integrated Drug Development platform. Pharmaceutical companies could now partner with a single organization that would design their clinical trials, recruit patients using diagnostic data, manage trial operations globally, analyze samples in central laboratories, and develop companion diagnostics for commercial launch. It was a value proposition no competitor could match.

One early success story illustrated the power of the model. A mid-sized biotech was developing a targeted therapy for a rare genetic form of diabetes. Traditional patient recruitment would have taken two years and cost $50 million. LabCorp identified potential patients through its diagnostic database, confirmed eligibility through genetic testing, and enrolled the full trial in eight months for $20 million. The drug received FDA approval 18 months faster than projected, generating an additional $500 million in sales for the sponsor.

The financial markets gradually recognized the transformation. By 2017, LabCorp was no longer valued as a diagnostic company trading at 12 times earnings. It was now viewed as a life sciences company deserving of an 18 times multiple. The stock price reached $155, validating the Covance acquisition price that had seemed so rich three years earlier. The company's market capitalization exceeded $15 billion for the first time.

But the Covance acquisition's greatest impact might have been strategic rather than financial. It positioned LabCorp at the intersection of two massive trends reshaping healthcare: personalized medicine and value-based care. As drugs became more targeted, diagnostic tests to identify the right patients became essential. As healthcare payment shifted from volume to outcomes, proving which treatments worked for which patients became critical. LabCorp now had capabilities across this entire value chain.

The acquisition also changed LabCorp's competitive position. Quest Diagnostics, still focused primarily on diagnostic testing, could no longer match LabCorp's breadth of offerings. CROs like IQVIA (the merged Quintiles-IMS Health) lacked LabCorp's diagnostic foundation. Pharmaceutical companies increasingly viewed LabCorp not as a vendor but as a strategic partner essential to their success.

By 2019, four years post-acquisition, the numbers told the story. The drug development segment generated $4.2 billion in revenue, growing at 8% annually. The promised $500 million in revenue synergies had been exceeded by 40%. The company's enterprise value had increased by $12 billion since the acquisition, more than double what LabCorp paid for Covance. Even the harshest critics admitted King had pulled off one of healthcare's most successful transformations.

In his 2019 shareholder letter, King reflected on the journey: "When we acquired Covance, many questioned why a diagnostic company would enter drug development. Today, that question seems quaint. The future of healthcare isn't about diagnostics or drug development—it's about using data and science to improve patient outcomes. LabCorp is uniquely positioned to lead this transformation."

But even as King celebrated the Covance success, new challenges emerged. The drug development business was cyclical, dependent on pharmaceutical R&D spending. The integration, while successful, had added complexity and diverted management attention from the core diagnostic business. Some investors argued LabCorp had become too complex, that the sum of parts was worth more than the whole. These tensions would eventually lead to another dramatic transformation, but first, LabCorp would face its greatest test yet: COVID-19.

VII. Modern Era: Data, Technology & COVID-19 (2016-Present)

Dr. Brian Caveney, LabCorp's Chief Medical Officer, was reviewing routine flu surveillance data in his Durham office on January 18, 2020, when an unusual email arrived from the company's Seattle laboratory. "Brian—seeing strange pneumonia cases that don't match any known pathogens. Similar to reports from Wuhan. Should we be worried?" Within 72 hours, LabCorp had assembled a crisis response team. Within two weeks, they were developing one of America's first COVID-19 tests. Within two months, they would be processing 200,000 tests daily, transforming from a behind-the-scenes service provider into a frontline defender of public health.

The COVID-19 pandemic revealed something fundamental about LabCorp that even industry insiders hadn't fully appreciated: the company wasn't just processing tests—it was operating one of America's most critical data infrastructure platforms. Every test result, every patient sample, every geographic cluster of infections flowed through LabCorp's systems, creating a real-time map of the pandemic's spread that proved invaluable to public health officials.

But let's rewind to understand how LabCorp had positioned itself for this moment. Since 2016, under David King's leadership, the company had quietly built capabilities that would prove essential during the pandemic. The diagnostic data platform, initially created to identify patients for clinical trials, had evolved into something far more powerful—a longitudinal health record spanning 75 million Americans, updated daily with new test results, trackable across years of medical history.

The technology transformation began with Project Phoenix in 2017, a $500 million investment to modernize LabCorp's entire IT infrastructure. The legacy systems—some dating back to the 1990s mergers—were replaced with cloud-based platforms capable of processing millions of transactions simultaneously. Artificial intelligence algorithms were deployed to identify testing patterns, flag potential errors, and predict disease outbreaks. What had been a collection of regional databases became a unified national platform.

The business model innovation was equally significant. LabCorp launched consumer-initiated testing in 2018, allowing patients to order their own blood work through an app. The Pixel by LabCorp home collection kit for genetic testing competed directly with 23andMe but with the credibility of medical-grade testing. The company partnered with Walgreens to place collection sites in 600 stores, making testing as convenient as picking up prescriptions. These initiatives seemed incremental at the time but would prove transformative when COVID hit.

When the pandemic arrived in early 2020, LabCorp's response was swift and coordinated. By March 5, just two weeks after the first U.S. COVID death, LabCorp had received Emergency Use Authorization for its COVID-19 RT-PCR test. The company immediately began processing 20,000 tests daily, quickly ramping to 50,000 by April and 200,000 by July. At peak capacity, LabCorp was processing more COVID tests than any other commercial laboratory in America.

The operational challenge was staggering. LabCorp had to source millions of nasopharyngeal swabs when global supplies were depleted. They had to train thousands of healthcare workers in proper collection techniques. They had to modify laboratories designed for routine blood work to handle infectious respiratory samples. They had to build IT systems capable of reporting results to patients, physicians, employers, and public health departments simultaneously.

The financial impact was extraordinary. COVID testing generated $4.2 billion in revenue in 2020 alone—nearly equivalent to the entire drug development division. Operating margins expanded to 24% as the fixed-cost laboratory infrastructure absorbed massive volume increases. The stock price surged from $160 in March 2020 to $280 by February 2021. LabCorp generated more free cash flow in 2020 than the previous three years combined.

But King and his team recognized COVID as more than a financial windfall—it was an opportunity to fundamentally reshape the company. The pandemic had accelerated every trend they'd been investing in: consumer-initiated testing, home collection, digital health integration, real-time data analytics. LabCorp used its COVID profits to double down on these capabilities, acquiring smaller digital health companies and building new technology platforms.

The data moat that emerged from COVID testing was perhaps the most valuable asset. LabCorp could track infection rates by zip code, identify emerging variants through genetic sequencing, and correlate COVID outcomes with pre-existing conditions documented in historical test results. This information proved invaluable not just for public health but for pharmaceutical companies developing vaccines and treatments. Pfizer, Moderna, and Johnson & Johnson all partnered with LabCorp for their vaccine trials, leveraging both the Covance clinical trial capabilities and the diagnostic testing infrastructure.

The competitive dynamics during COVID were fascinating. Quest Diagnostics, LabCorp's traditional rival, was equally aggressive in COVID testing, processing similar volumes. But smaller laboratories were overwhelmed, lacking the scale and infrastructure to handle the surge. Many regional labs, unable to compete, sold themselves to LabCorp or Quest. The pandemic accelerated industry consolidation by at least five years.

The direct-to-consumer transformation accelerated dramatically. Pre-COVID, less than 2% of LabCorp's testing was consumer-initiated. By 2021, it was 15% and growing. The company launched at-home collection kits for everything from cholesterol panels to STD testing. The LabCorp app, downloaded by 10 million Americans for COVID results, became a platform for ongoing health monitoring. Consumers who had never thought about laboratory testing now had direct relationships with LabCorp.

Technology investments went far beyond consumer interfaces. LabCorp deployed artificial intelligence to predict test demand, optimize laboratory workflows, and identify potential diagnostic errors before they occurred. Machine learning algorithms reviewed every test result, comparing them to historical patterns and flagging anomalies for human review. The company claimed these systems improved accuracy by 15% while reducing turnaround time by 20%.

The precision medicine initiatives that had seemed futuristic just years earlier became mainstream. LabCorp's oncology division grew 30% annually as genetic testing became standard of care for cancer treatment. The company's 500-gene panel could identify targeted therapy options for 85% of cancer patients. Pharmaceutical companies increasingly required LabCorp's companion diagnostics to identify patients for their specialized drugs.

But success brought new challenges. In late 2021, as COVID testing volumes declined from their peak, investors questioned LabCorp's growth trajectory. The stock price fell from $280 to $220 as the market worried about tough comparisons. Activist investor Jana Partners took a 5% stake and pushed for strategic changes, arguing the company's complexity was destroying value.

The pressure led to a dramatic decision. In July 2022, LabCorp announced it would spin off its drug development business—essentially unwinding the Covance acquisition—into a separate public company called Fortrea. The rationale was compelling: the diagnostic and drug development businesses had different growth profiles, capital requirements, and investor bases. Separating them would allow each to pursue focused strategies and achieve appropriate valuations.

The Fortrea spinoff, completed in July 2023, was financially elegant. LabCorp shareholders received one share of Fortrea for every share of LabCorp owned. The drug development business, generating $3.3 billion in revenue, was valued at $3.5 billion at spinoff—less than LabCorp paid for Covance but still creating value given the synergies captured during ownership. LabCorp retained a 20% stake in Fortrea, maintaining strategic flexibility.

Post-spinoff, LabCorp emerged as a pure-play diagnostics company but fundamentally transformed from its pre-Covance state. The company now had unmatched specialty testing capabilities, direct consumer relationships, and a data platform that competitors couldn't replicate. Revenue exceeded $12 billion with 20% EBITDA margins. The company was processing 600 million tests annually—more than twice its pre-COVID volume.

The technology transformation continued to accelerate. In 2024, LabCorp announced a partnership with Google Cloud to use generative AI for test interpretation and patient communication. The company launched a longitudinal health platform that gave patients access to all their historical test results with AI-powered insights about trends and risks. They introduced same-day resulting for routine tests in major metropolitan areas, using automated laboratories and drone delivery in pilot markets.

Competition evolved beyond traditional rivals. Amazon's acquisition of One Medical included laboratory services. CVS Health expanded its HealthHUB locations to include comprehensive testing. Digital health startups like Everlywell and LetsGetChecked offered convenient home testing, though they typically used LabCorp or Quest for actual laboratory processing. The competitive moat wasn't just about laboratories anymore—it was about data, relationships, and integration into the broader healthcare ecosystem.

As 2024 progressed, LabCorp faced a fundamental strategic question: what kind of company did it want to be? The pure diagnostics focus post-Fortrea spinoff provided clarity but also limitations. Growth in routine testing remained modest. Price pressure from payers continued. New technologies threatened to move testing from centralized laboratories to point-of-care settings.

Adam Schechter, who became CEO in 2019 after David King's retirement, articulated a vision of LabCorp as a "health insights company." The future wasn't just about processing tests but about using diagnostic data to predict disease, monitor treatment effectiveness, and improve population health. It was an ambitious vision that would require continued investment in technology, new partnerships with health systems and payers, and careful navigation of privacy and regulatory concerns.

The modern LabCorp—post-COVID, post-Fortrea, mid-digital transformation—was both stronger and more vulnerable than ever. The company had unprecedented scale, unmatched data assets, and deep customer relationships. But it also faced technological disruption, evolving competition, and questions about whether centralized laboratory testing would remain relevant in an increasingly distributed healthcare system. The next chapter of the LabCorp story was being written in real-time, and the outcome was far from certain.

VIII. Business Model & Competitive Advantages

Picture the LabCorp machine at 3 AM on a Tuesday. In Burlington, North Carolina, a FedEx plane touches down carrying 50,000 blood samples collected Monday afternoon from physician offices across the Southeast. Automated sorting systems route each sample to one of 40 specialized testing areas. By 6 AM, results are flowing back to physicians' electronic health records. By the time doctors arrive at their offices, Monday's tests are complete, accurately reported, and billed to insurance. This happens every single day, 365 days a year, with 99.7% accuracy. Understanding how this machine works—and why it's nearly impossible to replicate—reveals why LabCorp's business model has endured for half a century.

The network effects in diagnostic testing are more powerful than most investors appreciate. Every additional test LabCorp processes makes the next test more valuable. Here's why: diagnostic accuracy depends on reference ranges—understanding what's "normal" for specific populations. A cholesterol level that's concerning for a 25-year-old athlete might be typical for a 65-year-old diabetic. LabCorp's database of 75 million patients, with longitudinal records spanning decades, provides reference ranges of unprecedented precision. A startup might match LabCorp's testing technology, but they can't replicate fifty years of accumulated data.

The geographic density economics are equally compelling. In Raleigh-Durham, LabCorp operates 47 patient service centers within a 30-mile radius. A courier can collect samples from multiple locations in a single route, delivering them to the central laboratory within the two-hour window required for accurate testing. The company processes 50,000 samples daily from this region at a marginal cost of $3 per sample. A competitor entering this market would need to process at least 10,000 samples daily to approach break-even. But to get 10,000 samples, they'd need contracts with hundreds of physician offices, who won't switch from LabCorp unless the new entrant can match their turnaround time, which requires geographic density, which requires volume—a classic chicken-and-egg problem.

The payor relationships represent another powerful moat. LabCorp has negotiated contracts with every major insurance company in America, a process that took decades and required demonstrating consistent quality, accurate billing, and competitive pricing. These contracts aren't just agreements—they're complex integrations involving electronic billing systems, prior authorization protocols, and compliance frameworks. When UnitedHealth Group, covering 50 million lives, makes LabCorp a preferred provider, they're not just choosing a vendor—they're integrating LabCorp into their entire care delivery model.

Consider the billing complexity that LabCorp has mastered. A comprehensive metabolic panel might be reimbursed at $45 by Medicare, $62 by Blue Cross Blue Shield, $38 by Medicaid, and $147 if paid out-of-pocket. The same test, four different prices, each with different documentation requirements, prior authorization rules, and payment timelines. LabCorp processes 600 million such transactions annually with a 94% first-pass payment rate. They've turned administrative complexity into competitive advantage—smaller laboratories simply can't afford the infrastructure to navigate this maze.

The specialty versus routine testing mix showcases LabCorp's strategic positioning. Routine tests—complete blood counts, basic metabolic panels, lipid profiles—generate 60% of volume but only 35% of revenue. These commoditized tests face constant price pressure but provide the volume foundation that justifies infrastructure investments. Specialty tests—genetic panels, tumor markers, esoteric immunoassays—represent 40% of volume but 65% of revenue with margins exceeding 40%. Competitors can cherry-pick specialty testing, but without routine volume, they can't achieve the scale economies that make the business model work.

The capital intensity creates formidable barriers to entry. A single state-of-the-art automated chemistry analyzer costs $2 million and processes 9,000 tests per hour. But you need redundancy, so that's two analyzers. Plus specialized equipment for hematology ($500,000), immunoassay ($1.5 million), molecular diagnostics ($3 million), and mass spectrometry ($2 million). A competitive laboratory requires $50 million in equipment alone, before considering real estate, IT systems, or working capital. And that equipment becomes obsolete every 5-7 years, requiring constant reinvestment.

The regulatory barriers are equally daunting. Every LabCorp laboratory maintains CLIA (Clinical Laboratory Improvement Amendments) certification, requiring rigorous quality systems, proficiency testing, and regular inspections. Developing a new test requires analytical validation (does it measure what it claims?), clinical validation (does it provide useful medical information?), and often FDA approval. LabCorp spends $200 million annually on regulatory compliance. A startup might have superior technology, but without regulatory approvals, they can't generate a single dollar of revenue.

The data moat deserves special attention. LabCorp's database isn't just big—it's longitudinal, linked, and continuously updated. They can track a patient's cholesterol levels over 20 years, correlate them with medication history, and predict cardiovascular risk with unprecedented accuracy. This data enables personalized reference ranges (your results compared to similar patients), predictive analytics (identifying disease before symptoms appear), and population health insights (tracking disease trends across demographics). Competitors might replicate LabCorp's testing capabilities, but they can't recreate decades of accumulated data.

The logistics infrastructure represents hidden competitive advantage. LabCorp operates a fleet of 5,000 vehicles running optimized routes to 100,000 collection points daily. Their proprietary routing software, developed over decades, minimizes transport time while maintaining sample integrity. They've negotiated priority handling agreements with FedEx and UPS for overnight delivery from remote locations. The company maintains redundant transportation networks—if weather grounds flights, ground couriers ensure samples still reach laboratories. This logistics capability isn't visible to customers, but it's essential to the value proposition.

The vertical integration strategy provides both cost advantages and quality control. LabCorp manufactures many of its own reagents, maintaining quality while reducing costs by 30% versus external suppliers. The company develops proprietary laboratory information systems tailored to its workflows. They train their own phlebotomists through LabCorp University, ensuring consistent collection techniques. This integration seems inefficient in isolation—why make your own reagents when you could buy them?—but it provides control and cost advantages that compound over time.

The switching costs for physicians are higher than apparent. When a doctor's office switches laboratories, they must retrain staff on new requisition systems, learn new test codes, adapt to different reference ranges, and explain to patients why they need to go to different locations. Electronic health record integrations must be reconfigured. Historical test results might not transfer seamlessly. The disruption typically lasts months. Unless a competitor offers dramatically better service or significantly lower prices, inertia favors the incumbent.

The business model evolution reveals strategic sophistication. LabCorp began as a fee-for-service business—process test, send bill, collect payment. They've gradually shifted toward value-based contracts where they share risk with payers. Under these arrangements, LabCorp might guarantee certain quality metrics, utilization rates, or even patient outcomes. This evolution from vendor to partner makes LabCorp embedded in the healthcare system rather than adjacent to it.

The competitive dynamics with Quest Diagnostics have created an effective duopoly. Together, LabCorp and Quest control 45% of the $85 billion U.S. clinical laboratory market. They compete fiercely for contracts but maintain rational pricing discipline. When regional laboratories struggle, LabCorp and Quest typically acquire them at reasonable multiples. New entrants face the prospect of competing against two scaled players with deep pockets and decades of experience. It's not impossible—just very, very difficult.

The platform extensibility enables new revenue streams without proportional investment. LabCorp's infrastructure—laboratories, logistics, billing systems—can support adjacent services with minimal modification. Adding a new genetic test leverages existing collection networks and customer relationships. Launching home collection kits utilizes the same laboratory infrastructure. Expanding into employer wellness programs requires only incremental sales and marketing investment. The marginal cost of growth is far lower than the average cost of operations.

Why is this business model so hard to disrupt? It's not any single advantage but the interconnection of multiple reinforcing advantages. Scale enables data accumulation which improves quality which attracts volume which increases scale. Geographic density reduces costs which enables competitive pricing which wins contracts which increases density. Regulatory compliance creates barriers which limits competition which supports pricing which funds compliance. It's a virtuous cycle that strengthens over time.

The financial characteristics reflect these competitive advantages. LabCorp generates 20% EBITDA margins in what many consider a commodity business. Return on invested capital exceeds 12%, impressive for a capital-intensive industry. Free cash flow conversion approaches 70% of EBITDA. The business requires no working capital—patients and insurers pay after services are delivered. These aren't the metrics of a vulnerable commodity business but of a company with substantial and sustainable competitive advantages.

Understanding LabCorp's business model reveals why every attempt to disrupt the clinical laboratory industry has struggled. Theranos promised to revolutionize blood testing with proprietary technology but couldn't match LabCorp's operational excellence. Direct-to-consumer testing companies like Everlywell offer convenience but rely on LabCorp for actual laboratory processing. Digital health startups can improve the frontend experience but can't replicate the backend infrastructure. Technology might transform how tests are ordered and reported, but someone still needs to process 600 million samples annually with 99.7% accuracy. Until that changes, LabCorp's business model remains remarkably resilient.

IX. Playbook: Lessons for Builders & Investors

The conference room at Bessemer Venture Partners was silent as the young founder finished his pitch. "We're going to be the Uber of laboratory testing," he declared confidently. "No physical laboratories, just software connecting patients to testing services." The senior partner, who had served on LabCorp's board during the Covance acquisition, leaned forward. "Let me tell you why every venture-backed lab services startup in the last decade has either failed or ended up partnering with LabCorp," he began. "It's not about technology. It's about understanding how complex systems actually change."

The LabCorp story offers a masterclass in building enduring value in healthcare, but the lessons often contradict Silicon Valley wisdom. Where tech evangelists preach disruption, LabCorp succeeded through patient consolidation. Where consultants recommend focus, LabCorp thrived by expanding scope at precisely the right moments. Where financial engineers pursue maximum leverage, LabCorp learned that resilience matters more than optimization.

Lesson 1: The Power of Consolidation in Fragmented Markets

When the Powell brothers started acquiring small laboratories in the 1970s, the U.S. diagnostic testing market consisted of thousands of independent labs, each serving local physicians. The conventional wisdom was that laboratory testing was inherently local—doctors wanted to work with labs they knew, patients preferred nearby locations. The Powells recognized something others missed: while service delivery was local, the underlying economics were national.

The consolidation playbook LabCorp perfected has three components. First, acquire subscale players at reasonable multiples (typically 6-8x EBITDA for regional labs). Second, maintain local brand and relationships while centralizing backend operations. Third, reinvest scale economies into capabilities that subscale players can't match—specialized testing, IT systems, regulatory compliance. The genius is that each acquisition makes the next one more valuable through network effects and operational leverage.

Consider LabCorp's 2002 acquisition of Dynacare's U.S. operations for $385 million. Dynacare was losing money, processing 40,000 samples daily across inefficient regional laboratories. LabCorp maintained Dynacare's customer relationships but routed testing to its efficient mega-laboratories. Within 18 months, the acquisition was generating $50 million in EBITDA—a 13% return on investment before considering revenue synergies. The lesson: in fragmented industries with scale economies, patient consolidation creates more value than dramatic transformation.

Lesson 2: Riding Technology Waves While Maintaining the Core

LabCorp has survived multiple technological transitions that were supposed to obsolete centralized laboratory testing. In the 1990s, point-of-care testing would eliminate the need for reference labs. In the 2000s, pharmacogenomics would shift testing to specialized biotech companies. In the 2010s, digital health startups would own the customer relationship. Each time, LabCorp absorbed the innovation rather than being displaced by it.

The key insight: incumbent advantages in healthcare are stronger than most industries because of regulatory requirements, quality demands, and integration complexity. When new technology emerges, LabCorp can adopt it faster than startups can build infrastructure. The company spent $500 million developing genetic testing capabilities, but that investment was funded by cash flow from routine testing. Startups had to raise venture capital at dilutive valuations to develop similar capabilities without the benefit of a profitable core business.

The COVID-19 response exemplified this principle. Digital health companies had better apps and consumer interfaces, but when America needed 200,000 daily COVID tests, only LabCorp and Quest had the laboratory infrastructure to deliver. The company partnered with digital health startups for customer acquisition while maintaining control of the value-creating laboratory operations. The lesson: in healthcare, technology enables new business models but rarely replaces core infrastructure.

Lesson 3: Managing Through Regulatory and Reimbursement Changes

LabCorp has survived every major healthcare regulatory shift of the past fifty years: Medicare's creation, DRG implementation, managed care's rise, the Affordable Care Act, value-based payment models. Each change threatened the business model. Each time, LabCorp emerged stronger. The pattern reveals a crucial capability: anticipating regulatory changes and positioning ahead of them rather than reacting after the fact.

When Medicare introduced competitive bidding for laboratory services in 2018, cutting reimbursement rates by 30% for routine tests, many laboratories faced bankruptcy. LabCorp had anticipated this for years, shifting its mix toward specialty testing, reducing cost structure through automation, and negotiating value-based contracts with private payers. The reimbursement cuts that destroyed smaller competitors actually accelerated market share gains for LabCorp.

The playbook for regulatory resilience has four elements: maintain regulatory expertise at the board and executive level, invest in compliance infrastructure before it's required, shape policy through industry associations and lobbying, and structure the business to thrive under multiple regulatory scenarios. LabCorp spends $20 million annually on government relations—not to prevent change but to understand and influence it.

Lesson 4: The Acquisition Integration Playbook

LabCorp has completed over 30 acquisitions, from small regional laboratories to the $5.6 billion Covance transaction. The failures (notably the original 1995 merger) and successes reveal clear patterns about what works in healthcare consolidation.

Successful acquisitions share three characteristics. First, clear strategic rationale beyond cost synergies—new capabilities, geographic expansion, or customer relationships. Second, cultural compatibility assessment before deal announcement, not after. Third, integration pacing that prioritizes value capture over speed. The Covance acquisition succeeded because LabCorp ran it as a separate division for years, only integrating where clear value existed.

Failed acquisitions typically involve forced integration of incompatible operations, unrealistic synergy targets that require destroying what made the target valuable, and underestimating the complexity of harmonizing different IT systems, billing practices, and quality standards. The original NHL-Roche merger failed because it tried to fully integrate two incompatible companies within 18 months.

Lesson 5: Building Trust in Healthcare—Quality as Non-Negotiable

Healthcare isn't like consumer software where you can launch a minimum viable product and iterate based on user feedback. A single high-profile quality failure can destroy decades of reputation. LabCorp processes 600 million tests annually with 99.7% accuracy—impressive, but it means 1.8 million errors per year. The company invests enormously to push that error rate ever lower because trust, once lost in healthcare, rarely returns.

The quality playbook involves redundancy at every level (backup equipment, secondary review processes, parallel testing capabilities), transparency when errors occur (immediate notification, root cause analysis, preventive measures), and continuous investment in quality systems even when they don't generate immediate ROI. LabCorp spends $300 million annually on quality assurance—3% of revenue that directly reduces profitability but ensures long-term sustainability.

Lesson 6: When to Expand Scope vs. Focus

LabCorp's history includes both successful scope expansion (adding specialty testing, entering drug development) and strategic retreats (spinning off Fortrea, exiting international markets). The pattern suggests a framework for scope decisions in complex businesses.

Expand scope when: adjacent capabilities leverage existing infrastructure, new services strengthen core competitive advantages, and customers explicitly request integrated solutions. The Covance acquisition made sense because pharmaceutical companies wanted integrated diagnostic and drug development services.