STERIS: The Invisible Infrastructure of Modern Healthcare

I. Introduction: The Company That Keeps Hospitals Safe

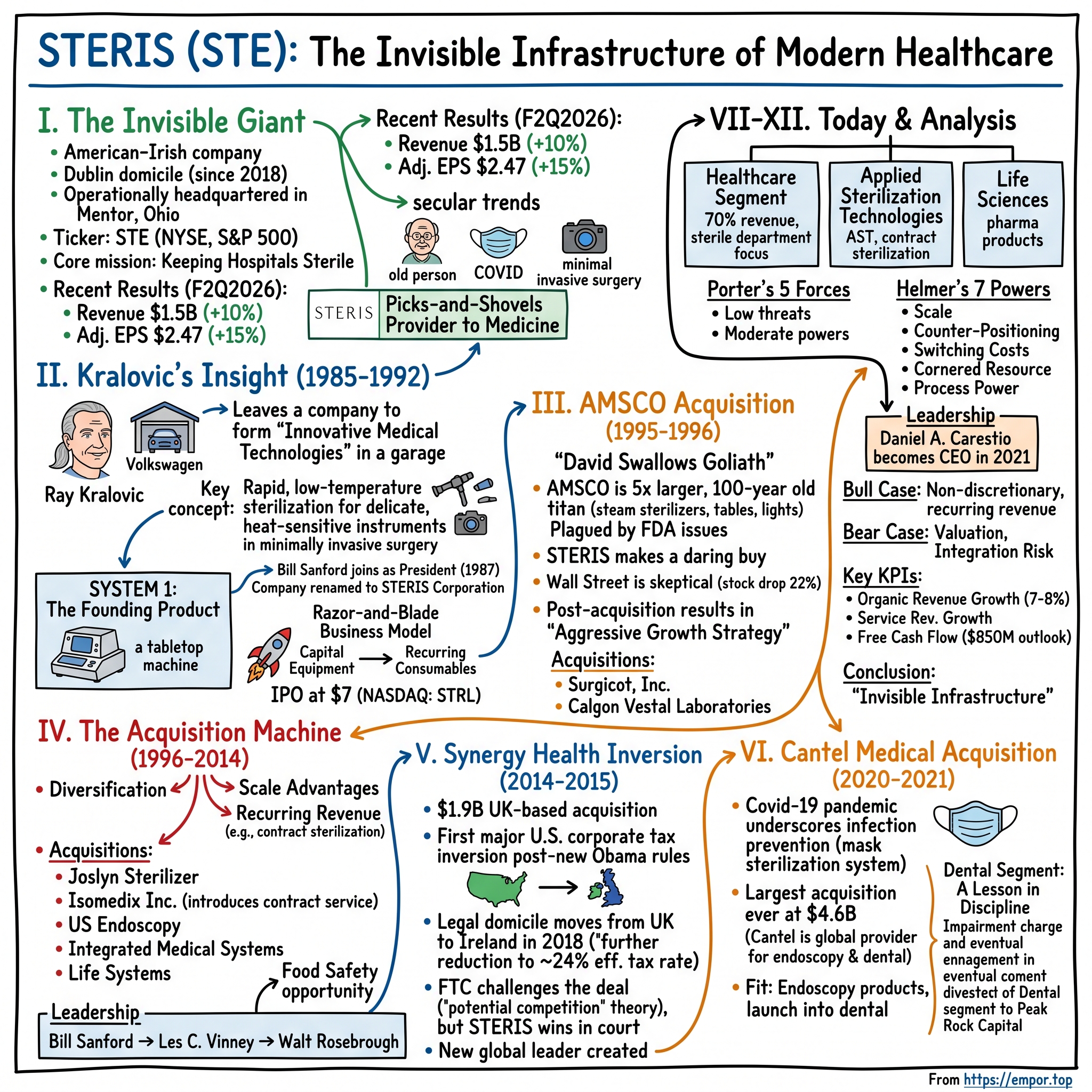

Picture yourself waking up in a hospital recovery room. The surgery went well, the doctors are confident, and you're on your way to healing. What you probably didn't think about—what virtually no one thinks about—is the invisible army of sterilization systems, chemical solutions, and procedural equipment that made your safe operation possible. Somewhere in that hospital, a tabletop machine the size of a small refrigerator quietly hummed through its cycle, killing every microorganism on the delicate endoscope that had just examined your internal organs. That machine, and thousands of others like it, likely came from a company headquartered in Mentor, Ohio—though legally domiciled in Dublin, Ireland—that has built a $25 billion empire on the simple but profound mission of keeping hospitals sterile.

STERIS plc is an American-Irish-based medical equipment company specializing in sterilization and surgical products for the US healthcare system. STERIS is operationally headquartered in Mentor, Ohio, but has been legally registered since 2018 in Dublin, Ireland for tax purposes; it was previously registered in the United Kingdom from 2014 to 2018. STERIS is quoted on the NYSE, and is a constituent of the S&P 500 Index.

The company's most recent results paint a picture of robust health. STERIS reported a 10% revenue increase, reaching $1.5 billion in total revenue from continuing operations for the second quarter of fiscal 2026, with constant currency organic revenue growth of 9%. Adjusted earnings per diluted share from continuing operations rose by 15% to $2.47.

But the numbers only tell part of the story. What makes STERIS fascinating from an investor's perspective is its strategic position at the nexus of several powerful secular trends: the aging global population driving more surgical procedures, the increasing focus on infection prevention post-COVID, and the explosive growth of minimally invasive surgery that requires specialized sterilization equipment. STERIS has built itself into the picks-and-shovels provider to modern medicine—a company that doesn't make headlines but makes headlines possible.

This is a story of acquisition-driven compounding over four decades, of tax optimization executed with almost artistic precision, and of the rare business strategy that turns "boring" into a competitive advantage. It's the story of how a microbiologist's garage experiment became the invisible infrastructure of global healthcare.

II. The Founding Innovation: Dr. Kralovic's Insight (1985-1992)

In 1985, medicine was undergoing a revolution that would change how surgeons operated—literally. Minimally invasive surgery, using tiny cameras and tools inserted through small incisions, was transforming from experimental curiosity to mainstream practice. Arthroscopy for joint problems, laparoscopy for abdominal procedures, and endoscopy for diagnostic work all required delicate, heat-sensitive instruments that the medical establishment had no good way to sterilize.

Ray Kralovic left his employer, the Pittsburgh-based American Sterilizer Co., to develop his own technique for sterilizing surgical instruments used in minimally invasive surgeries such as endoscopy and arthroscopy. Traditionally, surgical equipment had been sterilized in a lengthy process that involved high temperatures and strong disinfectants. However, the delicate heat-sensitive instruments used in minimally invasive procedures could not withstand the intensive sterilization process used on the more durable instruments. Kralovic's idea was to develop a rapid, low-temperature sterilization system that could be safely used on heat-sensitive equipment.

Dr. Raymond Kralovic was an unlikely entrepreneur. From looking at Ray Kralovic, you might not guess that he invented the technology behind a billion-dollar company. After all, the late co-founder of Steris Corp. had a long, gray ponytail, drove a Volkswagen and never dressed like a bigwig. And he always had time to help someone with a big idea. Born in Weirton, West Virginia in 1940, the son of a steelworker, Kralovic put himself through college and earned a doctorate in microbiology. He had worked at American Sterilizer Company—ironically, the very company that STERIS would later acquire—when he developed his revolutionary concept.

In the mid-1980s, Kralovic was employed as a microbiologist at another company when he conceived a low-temperature, liquid sterilization process. When he presented his theory to management he was told to take his idea and leave—which is exactly what he did.

The rejection became a founding myth. Kralovic relocated to northeast Ohio and set about making his vision reality. Microbiologist Raymond Kralovic, Ph.D., conceived a low-temperature, liquid sterilization process to meet the growing need for sterilization of these devices. In 1985, Ray founded Innovative Medical Technologies, the forerunner of STERIS, in Mentor, Ohio. In 1987, businessperson Bill Sanford joined the company as president, and the company changed its name to STERIS Corporation.

Bill Sanford: The Businessman Who Built the Platform

If Kralovic was the scientific visionary, Bill Sanford was the entrepreneurial engine that transformed a laboratory concept into a commercial powerhouse. If Bill Sanford had continued on his intended path, he might still be tossing the pigskin rather than hitting the links in his retirement. The self-proclaimed sports fanatic initially wanted to be a college football coach, but while home in Kansas on spring break of his senior year at Kansas State University in 1965, the zoology major saw an ad for a management training program at American Hospital Supply Co. Though he was offered a job as a coach at a division III college paying $350 a month, Mr. Sanford entered the management training program in Kansas City because it paid $525 a month. That early move set the stage for him to later help launch, oversee and grow Steris Corp., the Mentor-based sterilization and medical device company, into a global enterprise.

Kralovic first approached Primus Venture Partners, a Cleveland venture capital firm. Primus was unwilling to take on the concept, but suggested that Kralovic contact Bill Sanford, a health care consultant with a reputation for buying and selling medical technology. Kralovic was able to convince Sanford of the new sterilization system's potential for success, and STERIS was formed with a venture capital investment of $1.2 million. Sanford became the new company's CEO.

What happened next demonstrated both Kralovic's scientific resilience and Sanford's operational acumen. Four months after Steris received venture capital, the company learned that the original liquid compound that the System 1 was supposed to use didn't work as expected. Kralovic was told to find a compound that would work. And he did. "The most important thing he did was find an alternative to what was thought would work but didn't work instead of quitting," Sanford said.

This early crisis revealed a pattern that would define STERIS: technical problems were solvable challenges, not existential threats. The company pushed forward.

SYSTEM 1: The Founding Product

In 1988, the Steris Corporation launched its flagship product: the SYSTEM 1 liquid chemical sterilant processing system. The System 1 was a complete low-temperature sterilization system that could be used at or near the site of the surgical procedure. The system included a tabletop computer-controlled central unit, a single-use sterilizing solution, and various sizes of containers and trays. The patented sterilizing solution contained a chemical biocide that killed microorganisms, along with an anti-corrosion formula that protected the instruments.

The business model embedded in SYSTEM 1 was elegant and durable. Meanwhile, the System 1 was rapidly growing in popularity. Between the company's fiscal 1993 and 1994 years, sales climbed 70 percent to $45.8 million, and stock prices doubled. Because every one-time sale of a System 1 ensured continued sales of STERIS 20, the patented sterilizing solution, STERIS had a built-in stream of recurring revenue. By 1995, the company's revenues were almost evenly split between capital equipment sales and recurring sales of consumables, such as chemicals and other accessories.

This razor-and-blade model—capital equipment that locked in years of consumable purchases—became the template for STERIS's entire business strategy. Every sterilizer sold was an annuity of chemical solutions, every surgical table an ongoing service contract.

As Executive Founder and Chairman, he led STERIS in only ten years from a start-up with five employees and a $3 million valuation to a NYSE-listed public company with 5,000 employees and a market value of $2 billion.

STERIS made an initial public offering of shares of common stock at $7 a share, and the Company was registered on the NASDAQ exchange as STRL.

The IPO marked the end of STERIS's startup phase, but Sanford and his team were already planning something far more audacious—an acquisition that would transform the company from a successful niche player into an industry leader.

III. The AMSCO Acquisition: David Swallows Goliath (1995-1996)

In December 1995, STERIS made an announcement that seemed to defy corporate gravity. This decade-old startup, still finding its footing as a public company, planned to acquire Amsco International—a century-old industry titan that was five times its size.

What made this acquisition so unusual was that, with more than 2,000 employees and $400 million in sales, Amsco was at least five times the size of STERIS. The 100-year-old Amsco was the nation's leading manufacturer of steam and gas sterilizers, surgical tables and lights, and related infection prevention products. Despite its strong market position, however, the company was plagued with FDA regulatory problems, diminishing sales numbers, and a too-rapid turnover in management. Amsco needed a boost—and STERIS needed to diversify its product line.

The history of Amsco made this acquisition particularly poetic. The company traced its origins to 1894, when the American Sterilizer Company pioneered the concept of sterile operating rooms—the very foundation of modern hospital practice. Amsco had literally invented the industry that STERIS was now disrupting.

The Market's Verdict: Skepticism

Wall Street's reaction was swift and brutal. The Amsco buy also had negative short-term effects on the company's stock. Analysts and investors predicted that Amsco's bulk and baggage would drag down STERIS' pace of growth. When the acquisition was announced in December 1995, the company's stock dropped 22 percent in a single day. The worries continued in the months both before and after the deal closed. STERIS stock fluctuated throughout 1996, slowly gaining momentum only to drop sharply again in January 1997, when the company posted earnings below analysts' expectations.

The skeptics weren't unreasonable. A small company acquiring a much larger troubled competitor had all the hallmarks of hubris. Amsco's regulatory problems with the FDA were serious; its management instability was concerning; and integrating such a large operation into STERIS's still-developing infrastructure seemed like a recipe for disaster.

But Bill Sanford saw something different. "When we began STERIS 10 years ago, we knew we would always have to have a broader and deeper product line," said STERIS CEO Bill Sanford. "Amsco was a leader in some of the more traditional technologies, and the product lines were very complementary, with no overlap," he explained.

Execution and Integration

The acquisition, which was completed in May 1996, added some 300 items to STERIS' product line. It also positioned the company as an industry leader in both the large-scale, heat-based sterilization systems traditionally used in hospitals and the smaller, low-temperature systems it pioneered, which were often used in outpatient and clinic settings.

The strategic logic was elegant: STERIS's innovative low-temperature systems served the emerging outpatient and minimally invasive surgery market, while Amsco's traditional steam sterilizers served the established hospital infrastructure. Together, the combined company could offer customers a complete sterilization solution across every clinical setting.

Despite wobbly stock prices and Wall Street naysayers, STERIS proceeded undaunted to pursue an aggressive growth strategy. In September 1996, the company acquired Surgicot, Inc., a developer of sterility assurance technologies and products. Three months later, the company bought Calgon Vestal Laboratories, the infection and contamination control division of Bristol-Myers Squibb.

The Amsco acquisition taught STERIS's leadership team several crucial lessons that would shape the next three decades of strategy. First, market skepticism about transformational deals can create buying opportunities for companies with conviction. Second, troubled assets in good industries can be rehabilitated with strong management. Third, scale in healthcare infrastructure creates compounding advantages in customer relationships, service capabilities, and negotiating leverage.

What investors initially feared as overreach proved to be the foundation of an acquisition machine.

IV. Building the Platform: The Acquisition Machine (1996-2014)

The post-Amsco era marked STERIS's transformation from a single-product company into a diversified healthcare infrastructure platform. The strategy was consistent: identify adjacent markets, acquire leading positions, integrate efficiently, and repeat.

Rapid Consolidation (1996-1997)

After a six-month lull, STERIS re-entered the acquisitions game in mid-1997. In July, the company purchased Joslyn Sterilizer Corporation, a Rochester, New York, manufacturer of steam and low-temperature gas sterilizers. Two months later, it purchased the New Jersey-based Isomedix Inc. for $130 million. With facilities in the United States, Canada, and Puerto Rico, Isomedix provided contract sterilization services to manufacturers of prepackaged medical equipment and consumer products. Its sterilization methods included irradiation, fumigation, and electron beam sterilization.

The Isomedix acquisition deserves particular attention because it introduced STERIS to an entirely new business model: contract sterilization services. Rather than selling equipment to customers who sterilize their own products, Isomedix provided the sterilization service itself—a recurring revenue stream that would become increasingly important to STERIS's overall business.

The Food Safety Opportunity

Shortly after acquiring Isomedix, STERIS caught an unexpected break. Shortly after it was acquired, STERIS' new Isomedix division made news. On December 3, 1997, the U.S. Food and Drug Administration approved the company's use of irradiation on red meat to reduce bacterial contamination and help protect consumers from food-borne illnesses. FDA approval of the petition, which Isomedix had prepared and submitted in 1994, opened up new business opportunities for STERIS.

This regulatory approval expanded STERIS's addressable market beyond healthcare into food safety—a diversification that would prove valuable during periods of healthcare spending volatility.

Financial Results: The Fruits of Integration

The integration of these acquisitions produced dramatic financial results. The company organized a Food Safety Initiative business unit to direct growth in the newly opened arena. STERIS ended its fiscal year on March 31, 1998 with net revenues of $720 million, a 22 percent increase from the previous year. The total revenues were evenly divided between sales of capital equipment and sales of recurring consumables, accessories, and services. The company posted net income of $65.5 million for the year, a vast improvement over the previous year's $30.6 million loss.

STERIS entered 1999 with more than 4,500 employees; more than 20 sales offices in 17 countries; and 20 production and manufacturing facilities in Canada, Finland, Germany, Sweden, and the United States. In the 11 years since the introduction of the System 1, the company had gone from offering one product plus accessories to more than 2,500 products in 24 major categories.

2000s-2014: Steady Expansion

The acquisition pace continued throughout the 2000s, though with more measured frequency. Key transactions included:

- Hausted (2004): A surgical table manufacturer that complemented STERIS's surgical lighting and equipment portfolio

- Hamo Holding AG (2008): Expanded the washer-disinfector product line

- Reliance Medical Products (2009): Added surgical lighting capabilities

- In 2012, Steris acquired US Endoscopy for $270 million.

- On April 1, 2014, Steris announced its acquisition of Integrated Medical Systems International Inc. for ~$175 million. Shortly after, Steris also acquired Chesterfield, Missouri-based Life Systems.

Through this period, STERIS cycled through three CEOs. STERIS CFO Les C. Vinney was named second president and CEO. Walt Rosebrough becomes the third president and CEO.

Walter M Rosebrough, Jr., serves as Director and President and Chief Executive Officer since October 2007. From February 2005 to September 2007, Rosebrough served as President and Chief Executive Officer of Coastal Hydraulics, Inc. Previously, Rosebrough spent nearly 20 years in the healthcare industry in various roles as a senior executive with Hill-Rom Holdings, Inc., a worldwide provider of medical equipment and related services, including President and Chief Executive Officer of Support Systems International and President and Chief Executive Officer of Hill-Rom.

Rosebrough brought deep healthcare industry experience and a commitment to operational excellence. Under his leadership, STERIS would execute its most ambitious transactions yet.

V. The Synergy Health Inversion: A New Corporate Structure (2014-2015)

In October 2014, STERIS announced a deal that would fundamentally reshape its corporate structure while dramatically expanding its global footprint. The $1.9 billion acquisition of UK-based Synergy Health was notable not just for its size, but for what it represented: the first major U.S. corporate tax inversion after the Obama administration announced new rules designed to prevent exactly such transactions.

The Deal Structure

In October 2014, Steris executed a tax inversion from the United States to the United Kingdom, via an offer made to acquire UK-based Synergy Health for $1.9 billion. The tax inversion was notable as it was the first US inversion post the new rules introduced by the Obama administration in 2014 to curb US corporations moving their "legal domicile" to reduce their exposure to US corporate taxation.

Steris, a Mentor, Ohio-based provider of medical equipment and workflow-management software, will technically become a British company after it acquires Synergy Health—the biggest purchase Steris has ever made. But the company being formed to house the combined business, which is being called New Steris, will be based in the United Kingdom, a move intended to lower Steris' corporate tax rate. Steris, which has about 8,000 employees, is buying a company with 6,000 employees. Steris expects to generate $1.9 billion in sales during the fiscal year that ends on March 31, while Synergy generated $605 million during its most recent fiscal year.

Strategic Rationale: Beyond Taxes

While the tax benefits were significant, STERIS's management insisted the deal made strategic sense independent of tax considerations. Synergy provides outsourced sterilization services for medical device manufacturers, hospitals, and other industries. "Together, we create a balanced portfolio of products and services that can be tailored to best serve the evolving needs of our global customers," Steris CEO Walt Rosebrough said. The merger is expected to close by March 31, 2015.

The transaction is expected to result in a total annual pre-tax cost saving of USD30m or more from the fiscal year 2017. In addition, the effective tax rate of New STERIS will fall from 31.3 percent last year to about 25 percent.

Analysts were cautiously supportive. "There's a lot of political noise around tax inversions, but this is primarily a U.S. company acquiring a company in the same space with a very good international presence," Charles Weston, an analyst at Numis Securities in London, told Bloomberg. "The deal makes sense even in the absence of tax advantages." Those new tax restrictions have caused some companies to reconsider inversions.

The FTC Challenge

However, the deal faced an unexpected obstacle. The Federal Trade Commission today issued an administrative complaint charging that Steris Corporation's proposed $1.9 billion acquisition of Synergy Health plc would violate the antitrust laws by significantly reducing future competition in regional markets for sterilization of products using radiation, particularly gamma or x-ray radiation. The Commission also authorized agency staff to seek a temporary restraining order and preliminary injunction in federal court to maintain the status quo pending an administrative trial on the merits. According to the FTC's complaint, Steris, headquartered in Mentor, Ohio, and United Kingdom-based Synergy both provide contract sterilization services for companies that need to ensure their products are free of unwanted microorganisms before they reach customers. Implanted medical devices and human tissue products, for example, must meet stringent requirements for sterilization.

The FTC's theory was unusual—a "potential competition" case based on the argument that Synergy was planning to enter the U.S. market with x-ray sterilization technology and that the merger would eliminate this future competition. On September 24, 2015, the U.S. District Court for the Northern District of Ohio denied the Federal Trade Commission's ("FTC") motion for a preliminary injunction to prevent the merger. Merger cases are rarely litigated, and the decision marks the first trial defeat in recent years for either of the U.S. antitrust agencies.

Under the FTC's theory, Synergy's abandonment of its plans deprived the U.S. contract sterilization market of "actual potential competition." At trial, STERIS and Synergy disputed the FTC's contentions, demonstrating that Synergy abandoned plans to enter the U.S. with X-ray sterilization due to a multitude of business factors, including a lack of customer commitment, uncertain technology, and increasing costs. The case was heard in August 2015 before U.S. District Judge Dan A. Polster. In an opinion issued on September 24, 2015, the court concluded that the "evidence unequivocally show[ed]" Synergy was justified in terminating its X-ray project when it did, and the FTC failed to carry its burden.

Completion and Ireland Redomiciliation

STERIS plc announced today that it has completed the previously announced combination of STERIS Corporation and Synergy Health plc. As a result of the transaction, STERIS Corporation and Synergy are now combined under STERIS. The ordinary shares of STERIS will begin trading on the New York Stock Exchange under STERIS Corporation's historical ticker symbol, "STE" beginning November 3, 2015. "This combination marks a significant milestone for STERIS, creating a stronger global leader in infection prevention and sterilization."

But the corporate structure story didn't end there. In November 2018, STERIS made another move that demonstrated its sophisticated approach to tax optimization. In November 2018, Steris announced that it would further re-domicile its legal headquarters from the United Kingdom to Ireland. Steris is operationally headquartered in Mentor, Ohio, but has been legally registered since 2018 in Dublin, Ireland for tax purposes. Steris had reduced its corporate tax rate from 31.3 percent to 20 percent as a result of its 2014 tax inversion to the United Kingdom, however, it believed a further reduction could be achieved by moving to Ireland.

Surgical appliances manufacturer Steris says it will move its corporate base to Ireland as a result of Brexit. The move, which is subject to shareholder approval, comes just three years after it become the first US company to agree a corporate inversion deal after President Barack Obama's administration announced measures to clamp down on the practice. Steris's $1.9 billion cash-and-share takeover of Synergy Healthcare in November 2015 saw it relocate to Britain just seven months before the UK voted to leave the European Union. Chief executive Walt Rosebrough said re-domiciling to Ireland was its "best path forward".

The cumulative effect of these tax maneuvers reduced STERIS's effective tax rate from over 31% to approximately 24%—a permanent, structural advantage that flows directly to shareholders.

VI. The Cantel Medical Acquisition: Doubling Down (2020-2021)

The COVID-19 pandemic created unprecedented challenges for healthcare companies, but it also created unprecedented opportunities. For STERIS, the pandemic underscored the critical importance of infection prevention—and set the stage for its largest acquisition ever.

Pandemic Context

In April 2020, Steris received emergency use authorization from the FDA for a N95 mask sterilization system to help address the shortage of personal protective equipment during the 2019-20 coronavirus pandemic. In November 2020, Steris acquired Key Surgical, a leading global provider of sterile processing, operating room, and endoscopy products.

The company also recently expanded its market presence with the $850 million purchase of Key Surgical in October 2020.

Then, in January 2021, STERIS announced the crown jewel of its acquisition strategy.

The Cantel Deal

STERIS plc and Cantel Medical Corp today announced that STERIS has signed a definitive agreement to acquire Cantel, through a U.S. subsidiary. Cantel is a global provider of infection prevention products and services primarily to endoscopy and dental Customers. Under the terms of the agreement, STERIS will acquire Cantel in a cash and stock transaction valued at $84.66 per Cantel common share, based on STERIS's closing share price of $200.46 on January 11, 2021. This represents a total equity value of approximately $3.6 billion and a total enterprise value of approximately $4.6 billion, including Cantel's net debt and convertible notes.

Cantel's products include specialized medical device reprocessing systems for endoscopy and renal dialysis, advanced water purification equipment, sterilants, disinfectants and cleaners, sterility assurance monitoring products for hospitals and dental clinics, disposable infection control products primarily for dental and GI endoscopy markets, instruments and instrument reprocessing workflow systems serving the dental industry. Additionally, Cantel provides technical service for its products.

Strategic Fit

Cantel Medical adds to Steris' infection control business with a collection of endoscopy products and launches the company into the dental market. Wall Street analysts were positive on the deal, saying Steris was the most logical buyer and Cantel Medical has room to grow. "We believe that the COVID-19 pandemic has resulted in an increased focus on infection prevention, which we expect to serve as a tailwind for [Cantel Medical's] business over the longer-term," Needham analysts wrote.

STERIS plc today announced that it has completed the previously announced acquisition of Cantel Medical, a global provider of infection prevention products and services to endoscopy, dental, dialysis and life sciences Customers. "We are pleased to announce the closing of the Cantel Medical acquisition, which will complement and extend STERIS's product and service offerings, global reach and Customers," said Walt Rosebrough, President and Chief Executive Officer of STERIS. "We welcome Cantel people to the STERIS team, and look forward to working together to create more value for our Customers, our people, and our shareholders."

The Dental Segment: A Lesson in Discipline

Not all acquisitions work perfectly, and STERIS demonstrated admirable discipline in addressing a clear failure. During the quarter, the Company recorded a $490.6 million pre-tax, non-cash impairment charge related to the goodwill associated with its Dental segment acquired in the June 2021 acquisition of Cantel. The charge is primarily driven by deteriorating macro-economic conditions, including rising interest rates and increased supply chain and inflationary costs, as well as uncertainty regarding the impact such economic strains may have on patient and Customer behavior in the short-term.

Rather than persist with an underperforming asset, management moved decisively. STERIS plc today announced that the Company has entered into a definitive agreement to divest its Dental segment to Peak Rock Capital, a leading middle-market private investment firm, for $787.5 million. The Transaction is structured as an equity sale. The Transaction terms also include the opportunity for STERIS to receive an additional earnout of up to $12.5 million. The Dental segment reported revenue of $407 million and contributed segment operating income of $86 million in the trailing twelve-month period ended December 31, 2023.

"We are pleased with the strong finish to the fiscal year, as our Healthcare segment continued their trend of outperformance, driven primarily by strength in the United States," said Dan Carestio, President and CEO of STERIS. "We have made several strategic decisions in fiscal 2024 that will position STERIS for future growth, including today's targeted restructuring announcement and the announcement to divest the Dental segment. Heading into fiscal 2025, I am confident in our ability to deliver on our long-term commitments of mid-to-high single digit revenue growth and double-digit earnings growth."

VII. STERIS Today: Business Model Deep Dive

Understanding STERIS's current business requires examining its three primary operating segments and the strategic logic that binds them together.

Healthcare Segment

The Healthcare segment is STERIS's largest and most profitable business, accounting for roughly 70% of total revenues. The Healthcare segment offers cleaning chemistries and sterility assurance products; automated endoscope reprocessing system and tracking products; endoscopy accessories, washers, sterilizers, and other pieces of capital equipment for the operation of a sterile processing department; and equipment used directly in procedure rooms, including surgical tables, lights, and connectivity solutions, as well as equipment management services. It also provides capital equipment installation, maintenance, upgradation, repair, and troubleshooting services; preventive maintenance programs and repair services; instrument, devices, and endoscope repair and maintenance services; and custom process improvement consulting and outsourced instrument sterile processing services. The AST segment provides contract sterilization and testing services for medical device and pharmaceutical manufacturers through a network of contract sterilization and laboratory facilities, as well as integrated sterilization equipment.

The business model is elegant in its simplicity. Hospitals need sterilization equipment—they have no choice in the matter. Once installed, this equipment requires ongoing supplies of consumables and regular maintenance services. Customer switching costs are high due to staff training, regulatory compliance requirements, and workflow integration.

Recent performance has been strong. Healthcare revenue as reported grew 9% in the second quarter to $1,033.8 million compared with $944.2 million in the second quarter of fiscal 2025. This performance reflected 13% improvement in service revenue, 10% growth in consumable revenue and 4% growth in capital equipment revenue. Constant currency organic revenue growth was 9% compared to last year's second quarter. Healthcare operating income was $259.5 million compared with $228.0 million in last year's second quarter. The increase in operating income was primarily due to improved volume, price, productivity and the benefit of prior restructuring efforts, which were partially offset by tariff costs and inflation.

Applied Sterilization Technologies (AST) Segment

The AST segment provides contract sterilization services—STERIS sterilizes products for other companies rather than selling them equipment to do it themselves. Fiscal 2026 second quarter revenue for Applied Sterilization Technologies (AST) increased 10% as reported to $281.5 million compared with $256.7 million in the same period last year. This performance reflected 13% growth in service revenue and a 76% decline in capital equipment revenue. Constant currency organic revenue growth was 7% compared to last year's second quarter. Segment operating income was $127.6 million in the second quarter of fiscal 2026, compared with operating income of $109.9 million in the same period last year. The operating income increase compared with the prior year primarily reflects improved price, volume and favorable mix.

Q: How is the reshoring trend in Life Sciences impacting STERIS? A: Daniel Carestio mentioned that any expansion or relocation of manufacturing by large pharma customers generally benefits STERIS' capital equipment business. While there is more discussion than actual movement, some benefits are being realized, particularly in the GMP and pharma capital equipment sectors.

Life Sciences Segment

The Life Sciences segment designs, manufactures, and sells consumable products, such as pharmaceutical detergents, cleanroom disinfectants and sterilants, pharmaceutical grade and research sterilizers and washers, sterility assurance and maintenance products, vaporized hydrogen peroxide room decontamination systems and sterilizers, and high purity water and pure steam generators. This segment also offers equipment installation, maintenance, upgradation, repair, and troubleshooting services; and preventive maintenance programs and repair services. It serves its products and services to hospitals, other healthcare providers, and pharmaceutical manufacturers.

Life Sciences second quarter revenue as reported increased 13% to $145.0 million compared with $127.9 million in the second quarter of fiscal 2025. This performance reflected 39% growth in capital equipment revenue, 9% growth in service revenue and 7% growth in consumable revenue.

Recent Financial Performance

STERIS plc recently reported strong second quarter results, with sales rising to US$1.46 billion and net income reaching US$191.9 million, both up significantly from the prior year, and confirmed its fiscal 2026 revenue growth guidance of 8-9%.

Constant currency organic revenue from continuing operations is now anticipated to grow 7-8% compared with prior expectations of 6-7%. Adjusted earnings per diluted share from continuing operations are also increasing and are now expected to be in the range of $10.15 to $10.30 compared with prior expectations of $9.90 to $10.15. Included in this outlook is the negative impact of tariffs, estimated to reduce pre-tax profit by approximately $45 million, unchanged from prior outlook. The fiscal 2026 outlook assumes an effective tax rate of approximately 24%. Capital expenditures are anticipated to be approximately $375 million. Free cash flow is now expected to be approximately $850 million, an increase from prior expectations of $820 million.

VIII. Competitive Analysis: Porter's Five Forces and Helmer's Seven Powers

Understanding STERIS's competitive position requires examining both the industry structure and the company's specific sources of durable advantage.

Porter's Five Forces Analysis

Threat of New Entrants: LOW

The sterilization industry presents formidable barriers to entry. The complaint also states that most companies needing such sterilization services cannot do it in-house, and instead contract with facilities within 500 miles. Sterilization of large volumes of dense and heterogeneously packaged products is only feasible with gamma radiation generated by Cobalt 60. In the U.S., only Steris and one other company currently provide contract gamma sterilization services.

Capital requirements are substantial. A single gamma irradiation facility requires tens of millions in investment, specialized equipment (including radioactive materials subject to Nuclear Regulatory Commission oversight), and years of regulatory approvals. The institutional knowledge required to operate reliably is accumulated over decades.

Bargaining Power of Suppliers: MODERATE

STERIS sources specialized components for sterilizers, chemicals for consumables, and radioactive materials for contract sterilization. While some inputs are commoditized, others (particularly Cobalt-60 for gamma sterilization) have limited suppliers. However, STERIS's scale provides negotiating leverage, and vertical integration in chemicals manufacturing reduces dependence.

Bargaining Power of Buyers: MODERATE

Hospital systems and large medical device manufacturers have significant purchasing power. However, sterilization equipment represents critical infrastructure—there are no acceptable substitutes—and switching costs are high due to staff training, regulatory compliance, and workflow integration. Price sensitivity exists but is tempered by the relatively small share of healthcare budgets devoted to sterilization.

Threat of Substitutes: LOW

There is no substitute for sterile medical equipment. Infection prevention is non-negotiable. Within sterilization methods, different technologies compete (steam, ethylene oxide, gamma radiation, electron beam), but STERIS offers all major modalities, reducing substitution risk at the company level.

Competitive Rivalry: MODERATE

The market for sterilization equipment is competitive, and it has a presence of large international companies along with many smaller companies. Companies such as STERIS, Getinge, Sotera Health, 3M Company, and Fortive contribute to approximately 70% of the market share.

Steris' competitors include 3M, Getinge Group, and Belimed (Metall Zug).

Competition is concentrated among a few major players, suggesting rational competitive dynamics. Steris Corporation account for the largest share of sterilization equipment market in 2023. STERIS possesses a promising array of sterilization products and services within its portfolio.

Hamilton Helmer's Seven Powers Analysis

Scale Economies: PRESENT

STERIS's global manufacturing and service network creates unit cost advantages that smaller competitors cannot replicate. The company operates contract sterilization facilities across multiple continents, shares R&D costs across product lines, and spreads regulatory compliance overhead across substantial revenue.

Network Effects: LIMITED

Unlike software platforms, sterilization equipment doesn't exhibit strong network effects. One hospital's use of STERIS equipment doesn't directly increase value for other hospitals.

Counter-Positioning: PRESENT HISTORICALLY

STERIS's original innovation—low-temperature liquid sterilization—represented a classic counter-positioning move. Incumbent players like AMSCO were committed to steam and gas technologies; adopting Kralovic's innovation would have cannibalized their existing business. This allowed STERIS to establish a beachhead before eventually acquiring AMSCO itself.

Switching Costs: STRONG

Once sterilization equipment is installed, switching costs are substantial: staff retraining, workflow redesign, regulatory revalidation, and service contract disruption all discourage customers from changing vendors.

Branding: MODERATE

The STERIS and AMSCO brands carry significant credibility in healthcare settings. However, purchasing decisions in healthcare are typically made by supply chain professionals and infection control specialists rather than consumers, limiting the premium that branding alone can command.

Cornered Resource: PRESENT

STERIS has accumulated decades of institutional knowledge about sterilization science, regulatory requirements across global markets, and customer workflow optimization. This knowledge base is difficult to replicate and represents a genuine cornered resource.

Process Power: STRONG

The company's lean manufacturing initiatives, acquisition integration capabilities, and global service network represent accumulated process advantages. Dan has been with STERIS over twenty years with progressively increasing responsibilities in marketing, sales, and general management. He drove our improvements in Life Sciences and Applied Sterilization Technologies (AST) segments the past decade. He led the successful integration of the Synergy Health AST business, took on the additional leadership of our Healthcare IPT business when that leader retired, and finally became responsible for all our operations as COO in 2018. The success of all three of our business segments since he became COO is a testament to Dan and the STERIS leadership team.

IX. Leadership and Governance

The CEO Transition

Daniel A. Carestio became President and CEO of STERIS July 29, 2021 and sits on its board of directors. Prior to being appointed President and CEO, Mr. Carestio served as COO and was responsible for all STERIS operating businesses. He began his career at STERIS in 1997 as an Associate Product Manager for Life Sciences Sterility Assurance Products. Mr. Carestio sits on the board of directors of the Advanced Medical Technology Association (AdvaMed) and University Hospitals and is a member of the Center for Corporate Innovation.

The leadership transition from Walt Rosebrough to Dan Carestio represented a well-planned succession from an external hire (Rosebrough) to a homegrown leader who had risen through the ranks over more than two decades. "This announcement follows a well-planned and thoughtful succession process, which prioritizes developing leaders from within the Company," said Dr. Mohsen Sohi, Chairman of the Board. "Dan has a long history of demonstrating his ability to lead and drive results, and the Board has full confidence in him as the next CEO for STERIS. We are fortunate to have had Walt's leadership for well over a decade, through some of the most challenging times in STERIS's history. During Walt's tenure, we have grown revenue three-fold, completed close to fifty acquisitions, added more than 8,000 people to our workforce and grown shareholder value nearly 10 times, adding over $14 billion of market capitalization."

Carestio's background in operations—particularly his role integrating the Synergy Health acquisition—positioned him well for a period of consolidation following the Cantel deal.

X. Bull Case vs. Bear Case

The Bull Case

Non-Discretionary Demand: Hospitals cannot choose to stop sterilizing surgical instruments. Unlike elective procedures that may be deferred during economic downturns, infection prevention is a regulatory and ethical requirement. This creates extraordinary revenue stability.

Recurring Revenue Model: Capital equipment sales generate years of consumable purchases and service contracts. The installed base of STERIS equipment represents a substantial annuity stream.

Demographic Tailwinds: The global population is aging, driving increased surgical procedure volumes. Minimally invasive surgery continues to gain share, requiring the specialized low-temperature sterilization that STERIS pioneered.

Acquisition Track Record: Management has demonstrated the ability to identify, acquire, and integrate complementary businesses over four decades. The Dental segment divestiture shows discipline in exiting underperforming assets.

Tax-Advantaged Structure: The Ireland domiciliation provides ongoing tax benefits relative to U.S.-domiciled competitors.

The Bear Case

Valuation: STERIS trades at a premium multiple, reflecting market recognition of its quality. At current prices, much good news appears priced in.

Interest Rate Sensitivity: Hospital capital expenditure budgets are influenced by healthcare system finances, which in turn are affected by government reimbursement rates and broader economic conditions. Rising interest rates could pressure customer spending.

Integration Risk: The Cantel acquisition significantly increased STERIS's debt load and complexity. While the Dental divestiture helped, integration of the remaining businesses continues.

Regulatory Risk: Environmental concerns about ethylene oxide sterilization could lead to stricter regulations. While STERIS offers alternative technologies, any disruption to EO operations would require adjustment.

Single-Use Devices: The rise of single-use endoscopes and other medical devices could reduce demand for sterilization services over the long term. Q: What is the current state of single-use scopes, and how does it affect STERIS? A: Daniel Carestio stated that single-use scopes have a place, especially for small diameter scopes like hysteroscopy and bronchoscopes. However, large diameter scopes used for procedures like colonoscopies remain robust and cost-effective, making them less likely to be replaced by single-use options. The focus of disposable scope manufacturers is primarily on small diameter scopes.

XI. Key Performance Indicators for Investors

For long-term fundamental investors tracking STERIS, three metrics deserve particular attention:

1. Constant Currency Organic Revenue Growth

This metric strips out acquisition effects and currency fluctuations to reveal underlying business momentum. STERIS's target range of 6-8% constant currency organic growth reflects management's confidence in secular demand drivers. Sustained performance below 5% would signal market share loss or demand softness; consistent performance above 8% would suggest the market underestimates growth potential.

2. Service Revenue Growth Rate

Within the Healthcare segment, service revenue (equipment maintenance, instrument repair, outsourced reprocessing) is higher-margin and more recurring than capital equipment sales. Faster service revenue growth indicates deepening customer relationships and expanded wallet share. This performance reflected 13% improvement in service revenue, 10% growth in consumable revenue and 4% growth in capital equipment revenue. The recent 13% service growth significantly outpacing capital equipment growth is a positive indicator.

3. Free Cash Flow Conversion

Fiscal 2026 Free Cash Flow Outlook: Increased to $850 million. STERIS's capital-light model (after initial equipment installation) should generate strong cash conversion. Free cash flow funds debt repayment, acquisitions, dividends, and share repurchases. Monitoring the ratio of free cash flow to adjusted net income reveals earnings quality and capital efficiency.

XII. Conclusion: The Invisible Infrastructure

Raymond Kralovic died on New Year's Eve 2013, at the age of 73. "Ray was a pioneer in sterile processing technologies and a respected scientist whose vision was instrumental in the creation of STERIS," said Stephen Norton. The ponytailed microbiologist who conceived of low-temperature liquid sterilization in a garage left behind a company that now touches virtually every surgical procedure performed in the developed world.

STERIS's journey from a startup with five employees to an S&P 500 constituent with $5+ billion in annual revenues illustrates several timeless business principles. First, solving real problems in essential industries creates durable franchises. Second, capital allocation discipline—knowing when to acquire and when to divest—compounds value over time. Third, corporate structure matters; STERIS's tax optimization has created permanent shareholder advantages. Fourth, leadership transitions executed thoughtfully preserve institutional knowledge while bringing fresh perspectives.

The company that Bill Sanford almost chose football coaching over, that Wall Street wrote off when it acquired AMSCO, that the FTC tried to block from buying Synergy Health, has emerged as the dominant global franchise in infection prevention.

In an era obsessed with artificial intelligence and software disruption, STERIS offers a reminder that unglamorous businesses serving essential needs can generate extraordinary shareholder returns. The next time you wake up in a hospital recovery room, you'll know who to thank for the invisible infrastructure that kept you safe.

Disclosure: This article is for informational purposes only and does not constitute investment advice. Investors should conduct their own due diligence before making investment decisions.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube