Interactive Brokers: The Algorithm That Ate Wall Street

I. Introduction & Episode Teaser

Picture this: It's 1985, and the Chicago Board Options Exchange trading floor is in uproar. A Hungarian immigrant named Thomas Peterffy has just wheeled in a contraption that looks like it belongs in a science fiction movie—a computer terminal jerry-rigged with cables running directly to the exchange's data feed. The floor traders are screaming, the exchange officials are threatening lawsuits, and Peterffy? He's calmly explaining that he's simply following the rules. No one said the "keyboard" had to be operated by human fingers.

This moment—equal parts audacious and inevitable—captures the essence of Interactive Brokers' story. Today, IBKR processes an average of 2.6 million trades per trading day, making it the largest electronic trading platform in the United States by daily average revenue trades. The company that started with one man's $100,000 investment is now worth over $30 billion, serving 3.3 million customers across 36 countries.

But here's the paradox that makes this story fascinating: Interactive Brokers succeeded not by catering to Wall Street's establishment, but by systematically dismantling it. Every innovation, every product launch, every strategic decision has been guided by a simple principle—eliminate the middleman, automate everything, and pass the savings to customers. It's a philosophy that has made Thomas Peterffy one of the richest people in America while keeping him virtually unknown outside financial circles.

What we're about to explore isn't just a business success story. It's a masterclass in compound innovation—how small technological advantages, relentlessly pursued over decades, can topple entire industries. From handheld computers on trading floors to algorithms that execute millions of trades per second, Interactive Brokers didn't just adapt to the digital revolution in finance. They wrote its playbook.

The roadmap ahead takes us from communist Hungary to the pinnacle of American capitalism, from analog trading pits to quantum computing, from a one-man operation to a global financial infrastructure company. Along the way, we'll discover how an outsider with an engineering mindset built the operating system that powers modern markets—and why, after 45 years, the disruption is just beginning.

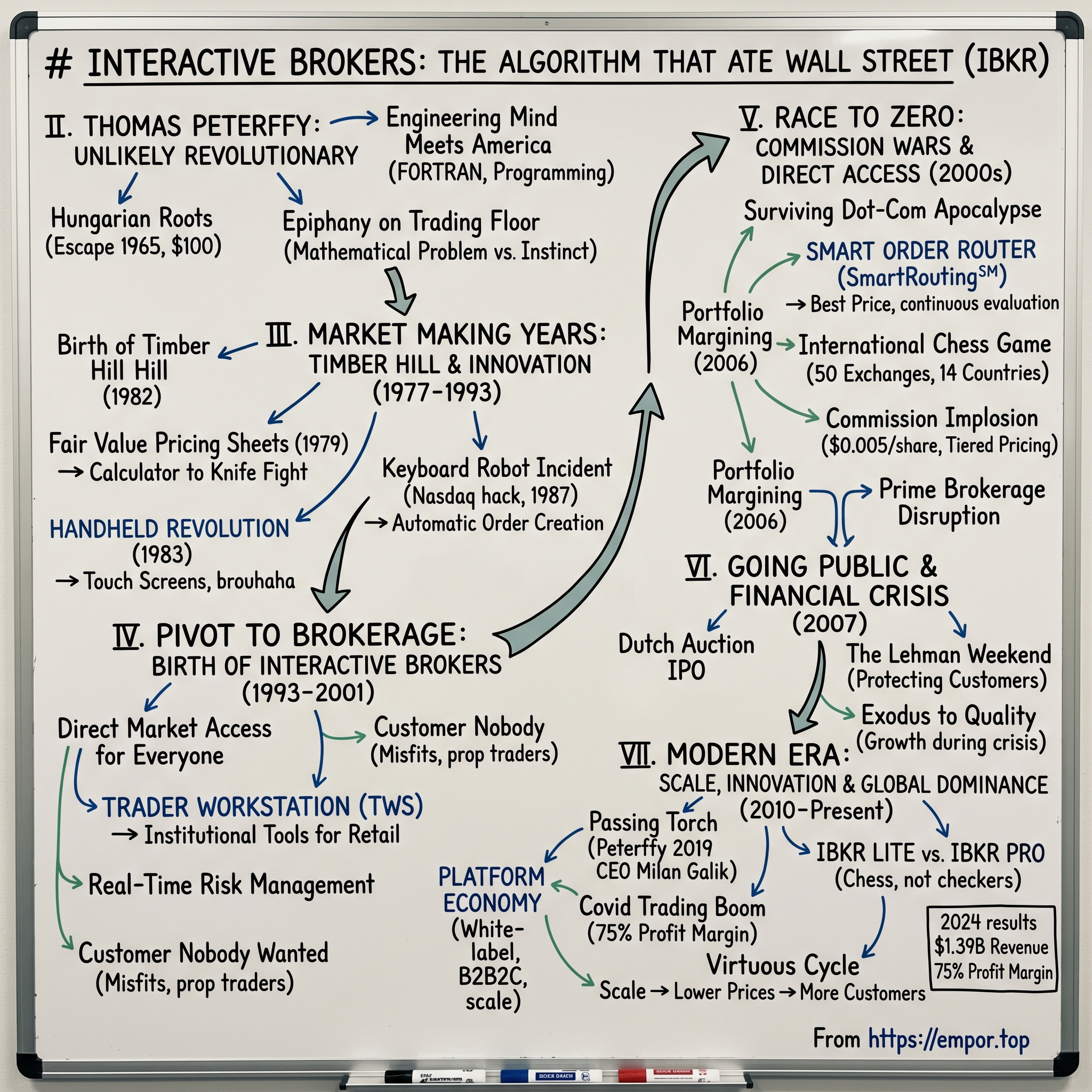

II. Thomas Peterffy: The Unlikely Revolutionary

The Hungarian Roots

Thomas Peterffy's journey to becoming Wall Street's greatest disruptor began in the basement of a Budapest hospital in 1944, where his pregnant mother took shelter from Allied bombing raids. Born into a Hungary ravaged by war and soon to be suffocated by Soviet communism, Peterffy's early life was marked by scarcity and surveillance. His parents divorced when he was young, and at age 12, his father—an entrepreneur whose business had been nationalized by the communist regime—made a decision that would change everything: he would escape to the West, and somehow, he would bring his children.

The escape came in 1965. Peterffy, then 21, received permission to visit his father in West Germany—a rare privilege in communist Hungary. He packed a single suitcase, knowing he would never return. "I left with the equivalent of maybe $100 sewn into my coat," Peterffy would later recall. "And absolutely no idea what America would be like except what I'd seen in contraband movies."

The Engineering Mind Meets America

Arriving in New York in December 1965, speaking no English, Peterffy found work as a draftsman at an engineering firm. But this was the 1960s, and computers were beginning to transform engineering. Peterffy taught himself programming at night, studying FORTRAN manuals with a Hungarian-English dictionary beside him. Within two years, he'd moved from draftsman to computer programmer, quintupling his salary. By 1970, he worked as a programmer on Wall Street, developing trading software. The transition was serendipitous—a consulting firm needed someone who understood both engineering and the emerging world of mainframe computers. Peterffy's ability to see patterns in code would soon translate into seeing patterns in markets.

The Epiphany on the Trading Floor

Peterffy left his career designing financial modeling software and bought a seat on the American Stock Exchange to trade equity options in 1977. The price? $36,000—nearly his entire savings. His first day on the floor was a disaster. He didn't understand the hand signals, couldn't keep up with the shouting, and lost money on nearly every trade. "I went home that night thinking I'd made the biggest mistake of my life," he later admitted.

But Peterffy had noticed something the veteran traders hadn't: the pricing of options was fundamentally a mathematical problem. While others relied on gut instinct and experience, he saw Black-Scholes formulas and probability distributions. He wrote code in his head during the trading day and then applied his ideas to computerized trading models after hours.

The Cultural Clash

The contrast between Peterffy and the typical American floor trader couldn't have been starker. They were loud, gregarious, often from multi-generational trading families. He was quiet, methodical, and spoke with a thick Hungarian accent that marked him as an outsider. They traded on relationships and reputation; he traded on mathematics and efficiency.

"I think the way a CEO runs his company is a reflection of his background. Business is a collection of processes, and my job is to automate those processes so that they can be done with the greatest amount of efficiency", Peterffy would later explain. This wasn't just a business philosophy—it was a worldview shaped by seeing human systems fail catastrophically in communist Hungary.

The floor traders called him "the robot" behind his back. They mocked his handheld calculators and printed pricing sheets. But while they were laughing, Peterffy was calculating. He realized that if he could price options faster and more accurately than human intuition allowed, he could find arbitrage opportunities invisible to the naked eye.

The Vision Takes Shape

What drove Peterffy wasn't just profit—it was an almost aesthetic revulsion at inefficiency. Watching traders scream prices across a crowded floor, seeing orders transcribed by hand multiple times, witnessing the constant errors and delays—it all offended his engineering sensibilities. "Markets should be like physics," he once said. "Predictable, measurable, precise."

By 1978, Peterffy had formed T.P. & Co., his first company. The name was deliberately bland—he didn't want attention. What he wanted was to build a machine that could trade better than any human. Not just faster, but fundamentally better—making thousands of micro-decisions based on real-time probability calculations that no human brain could process.

His apartment became a workshop. Soldering irons next to option pricing models. Computer parts scattered among hand-drawn market diagrams. He was simultaneously learning the intricate social dynamics of the trading floor while plotting its obsolescence. The Hungarian refugee who arrived with $100 was about to declare war on Wall Street's entire way of doing business.

III. The Market Making Years: Timber Hill & Early Innovation (1977-1993)

The Birth of Timber Hill

In 1982, T.P. & Co. underwent a transformation that would define its future—it became Timber Hill Inc. The name came from Peterffy's property in Connecticut, but it also reflected something deeper: a desire to build something solid, enduring, rooted. Where Wall Street firms chose names evoking prestige and tradition, Peterffy chose one that suggested patient growth.

The company's first innovation had actually come three years earlier. In 1979, it became the first to use fair value pricing sheets on a stock exchange trading floor. Picture the scene: traders clutching crumpled papers with yesterday's prices, making split-second decisions based on memory and instinct. Then Peterffy appears with freshly printed sheets, updated that morning using his computer models. "It was like bringing a calculator to a knife fight," one former AMEX trader recalled.

The Handheld Revolution: Timber Hill's Trading Computers in 1983

In 1983, Timber Hill created the first handheld computers used for trading. The devices were revolutionary—battery-powered units with touch screens where traders could input a stock price and instantly get recommended option prices. As Peterffy explained in a 2016 interview, the battery-powered units had touch screens for the user to input a stock price and it would produce the recommended option prices, and it also tracked positions and continually repriced options on stocks.

But innovation bred resistance. When he first brought a 12-inch-long by 9-inch-wide device to the exchange floor, a committee in the exchange told him it was too big. When he made the device smaller, the committee stated that no analytic devices were allowed to be used on the exchange floor. The CBOE's opposition was particularly fierce. "It caused a brouhaha," recalls a former CBOE trader. "People got kind of hysterical at the idea of changing the rules."

The Keyboard Robot Incident

In 1987, Peterffy also created the first fully automated algorithmic trading system, to automatically create and submit orders to a market. But the story of how this came to be is perhaps the most emblematic of Peterffy's entire approach to innovation.

It happens at Nasdaq, the world's first electronic stock exchange, meaning there is no trading floor. You buy and sell by typing orders into a computer, a Nasdaq terminal. Peterffy, of course, doesn't want to have to type in orders, so he and his engineers hack into the terminal. They wire it up to their computer, which starts trading up a storm.

Then came the confrontation. So many trades that a high-up official with Nasdaq comes by to see what's going on and the guy sees just this one terminal attached to a computer. PETERFFY: He looks and looks and looks and he says, well, tell me how you're doing this? And so I explain to him what's happening here and then he says I don't think you can do this, but let me go back to my office and I'll let you know.

The man calls back and says I'm sorry. The Nasdaq rulebook says you can't go cutting wires. All orders have to be entered through the keyboard. You have one week to fix it.

Peterffy's solution was audacious in its literal interpretation of the rules. Peterffy and his engineers come up with a solution. Trades have to be entered on the keyboard - fine. They build a machine to do that. PETERFFY: So it was basically - they were rubber fingers that are typing.

KESTENBAUM: What did that thing sound like when it was running? PETERFFY: Like a machine (imitating machine sound) because it was typing so fast. The robot became legendary on Wall Street—a physical manifestation of the absurdity of resisting technological progress.

The S&P 500 Gambit

By 1987, Timber Hill faced a critical juncture. In 1987, the CBOE was about to close down its S&P 500 options market due to the options not attracting sufficient trader interest. Because of this, Peterffy pledged that Timber Hill would make tight markets in the product for a year if the exchange would allow the traders to use handheld computers on the trading floor. The exchange agreed, and more traders were attracted by the change in pricing; today S&P 500 options are the most actively traded stock market index options in the U.S.

This wasn't just a business deal—it was a Trojan horse. Peterffy knew that once the CBOE allowed computers for one product, the precedent would be set. Within months, his handheld devices were spreading across the floor like a contagion. Traditional traders watched in horror as their edge evaporated, replaced by silicon and code.

Global Expansion

In 1990, Timber Hill Deutschland GmbH was incorporated in Germany, and shortly thereafter began trading equity derivatives at the Deutsche Terminbörse (DTB), marking the first time that Timber Hill used one of its trading systems on a fully automated exchange. In 1992, Timber Hill began trading at the Swiss Options and Financial Futures Exchange, which merged with DTB in 1998 to become Eurex. At that time, Timber Hill had 142 employees.

The international expansion wasn't just about geography—it was about finding markets where electronic trading was welcomed, not fought. European exchanges, unburdened by decades of floor trading tradition, proved more receptive to Peterffy's vision. Each new market was a laboratory for refining the algorithms that would eventually conquer Wall Street.

By 1993, Timber Hill had become a global force, but Peterffy saw a bigger opportunity. The same technology that gave him an edge in market making could revolutionize how all investors accessed markets. The stage was set for the next chapter: transforming from a trading firm into a broker that would democratize the tools of Wall Street.

IV. The Pivot to Brokerage: Birth of Interactive Brokers (1993-2001)

The Strategic Inflection Point

The year 1993 marked a fundamental shift in Peterffy's vision. Between 1993 and 1994, the corporate group Interactive Brokers Group was created, and the subsidiary Interactive Brokers LLC was created to control its electronic brokerage, and to keep it separate from Timber Hill, which conducts market making. This wasn't just a business expansion—it was a philosophical evolution. Peterffy realized that the real revolution wasn't in being the best trader, but in giving everyone else the tools to trade like he did.

The decision came from a simple observation: retail investors were being fleeced. They paid $100 or more per trade to full-service brokers who often knew less about markets than a computer algorithm. Meanwhile, Peterffy's systems were executing trades for pennies. The spread between what was possible and what was available to regular investors was obscene.

"Why should only institutions have access to these tools?" Peterffy asked his team. "If we can trade electronically, so should everyone else." It was a radical proposition in 1993. Charles Schwab was still primarily a phone-based discount broker. E*TRADE existed but was tiny. The internet was barely commercial. Yet Peterffy saw the future clearly: direct market access for everyone.

Building the Trader Workstation

The crown jewel of Interactive Brokers would be its Trader Workstation (TWS)—a platform that put institutional-grade tools in the hands of individual traders. But building it required solving problems that didn't yet have solutions.

First challenge: How do you display real-time data from dozens of exchanges around the world on a 1990s computer with dial-up internet? Peterffy's team invented compression algorithms that could squeeze market data into packets small enough to transmit over 56k modems. They built predictive caching systems that anticipated what data users would need next.

Second challenge: How do you let retail customers trade complex instruments safely? The team created the first real-time risk management system for retail trading. Every order was checked against the customer's buying power, margin requirements, and risk parameters before execution. It prevented the catastrophic losses that plagued other early online brokers.

Third challenge: How do you route orders to get the best price across fragmented markets? This led to the development of SmartRouting, an algorithm that would scan every exchange and ECN to find the best price, then route the order there in milliseconds. It was technology that major Wall Street firms were just beginning to build, now available to anyone with $10,000 to open an account.

The Customer Nobody Wanted

Interactive Brokers' first customers weren't day traders or retirees—they were the misfits of the financial world. Proprietary traders who'd been kicked out of firms for being too aggressive. Hedge fund managers working from their apartments. Foreign investors who couldn't access U.S. markets through traditional brokers.

One early customer was a physics PhD who'd quit academia to trade options from his basement. He'd calculated that with Interactive Brokers' commission structure, strategies that were unprofitable elsewhere could generate consistent returns. Within a year, he was managing $10 million.

Another was a group of Russian mathematicians who'd developed statistical arbitrage models but couldn't find a broker who'd let them execute hundreds of trades per day without crushing fees. Interactive Brokers not only welcomed them but built API connections so they could plug their models directly into the markets.

These weren't the customers Merrill Lynch wanted. But they were exactly who Peterffy was building for—sophisticated, demanding, and willing to pay for quality execution over hand-holding.

The Dot-Com Laboratory

The late 1990s internet bubble provided the perfect testing ground for Interactive Brokers' technology. As day trading exploded and online brokers proliferated, most firms struggled with capacity. E*TRADE crashed during high-volume days. Ameritrade's systems froze during volatility.

Interactive Brokers, built on the same infrastructure that handled Timber Hill's massive trading volumes, never went down. While competitors celebrated adding features like streaming quotes (revolutionary at the time), Interactive Brokers was already offering portfolio margining, options analytics, and direct access to foreign markets.

The difference was philosophical. Other online brokers were trying to replicate the traditional brokerage experience online—research reports, investment advice, user-friendly interfaces. Interactive Brokers assumed its users knew what they were doing and just wanted the most powerful tools possible.

The Corporate Restructuring

In 2001, the corporate name of the Timber Hill Group LLC was changed to Interactive Brokers Group LLC, which at the time handled 200,000 trades per day. This wasn't just a rebranding—it reflected a fundamental shift in the company's identity. The brokerage business was no longer a side project; it was the future.

The restructuring also solved a potential conflict of interest. By clearly separating the market-making and brokerage operations, Peterffy could assure customers that their orders weren't being front-run by the firm's proprietary trading. It was a level of transparency unusual on Wall Street, where firms routinely traded against their own clients.

By 2001, Interactive Brokers had 50,000 accounts and was processing more trades per account than any other retail broker. But this was just the beginning. The real test would come with the dot-com crash and its aftermath—a period that would destroy many online brokers but cement Interactive Brokers' position as the platform for serious traders.

V. The Race to Zero: Commission Wars & Direct Access (2000s)

Surviving the Dot-Com Apocalypse

March 2000. The NASDAQ peaks at 5,048 before beginning its sickening descent. Within two years, it would lose 78% of its value. Online brokers, who'd grown fat on day-trading commissions, watched their customer bases evaporate. DLJdirect was sold for scrap. Dozens of smaller firms simply vanished.

Interactive Brokers not only survived—it thrived. Why? Because while others had built their businesses on retail speculation, Peterffy had built infrastructure for professional trading. When the amateurs fled, the professionals remained. And in volatile markets, professionals trade more, not less.

The firm's conservative approach to margin lending also proved prescient. While competitors had loosened requirements to attract day traders, Interactive Brokers maintained strict risk controls. When the market crashed, they had minimal bad debt while others wrote off billions.

"We're not in the business of enabling gambling," Peterffy told his staff. "We're in the business of providing tools for disciplined trading." This distinction would define everything that followed.

The Smart Order Router Revolution

In 2002, Interactive Brokers unveiled what would become its most important innovation: SmartRouting. The concept was simple but the execution was staggeringly complex. Instead of sending orders to a single exchange, the system would scan every venue—NYSE, NASDAQ, ECNs, regional exchanges—and route to wherever offered the best price.

But "best price" was more nuanced than it appeared. The algorithm considered not just the quoted price but the likelihood of execution, the speed of the venue, hidden liquidity, and even the probability of price improvement. It made decisions in microseconds that would take human traders minutes to analyze.IB SmartRoutingSM delivers support for best price execution, searching for the best stock, option, combination prices at the time of your order. Unlike smart routers from other online brokers, IB SmartRoutingSM never routes and forgets about your order. It continuously evaluates fast changing market conditions and dynamically re-routes all or parts of your order seeking to achieve optimal execution and maximize your rebate.

The impact was immediate and devastating to competitors. A study by the firm showed that customers using SmartRouting saved an average of $1.50 per 100 shares traded compared to routing to a single exchange. For active traders executing hundreds of trades per month, this meant thousands of dollars in savings.

The International Chess Game

While U.S. brokers fought over domestic market share, Peterffy played a different game entirely. By 2005, Interactive Brokers offered direct access to 50 exchanges in 14 countries. A trader in Texas could buy Japanese stocks in Tokyo, German bonds in Frankfurt, and Canadian options in Montreal—all from the same account, with the same platform.

The complexity of this was staggering. Different time zones, currencies, regulations, settlement procedures. Each market had its own quirks and requirements. Interactive Brokers built adapters for each, creating a universal translator for global finance.

But the real innovation was in currency handling. Instead of forcing customers to manually convert currencies for each trade, Interactive Brokers created a real-time currency market within its platform. Customers could hold multiple currencies, automatically convert at interbank rates, and even earn interest on positive balances. It turned what had been a major friction point in international investing into a profit center.

The Commission Implosion

By 2005, Interactive Brokers was charging $0.005 per share for stock trades—half a penny. At ETRADE, the same trade cost $12.99. The math was brutal: an Interactive Brokers customer trading 1,000 shares paid $5; an ETRADE customer paid $12.99 regardless of share count. For anyone trading more than a few hundred shares, the choice was obvious.

But Peterffy wasn't satisfied. In 2006, he introduced tiered pricing that went as low as $0.0035 per share for high-volume traders. Then came unbundled pricing, where sophisticated traders could choose to add liquidity to exchanges and actually receive rebates on their trades. Some customers were literally being paid to trade.

The industry response was predictable: "It's unsustainable," "They're buying market share," "The model will collapse." But they misunderstood the economics. Interactive Brokers' cost per trade was measured in fractions of pennies. Their technology infrastructure, built over decades, could handle millions of trades with minimal human intervention. What looked like predatory pricing was actually a sustainable business model—just one that made everyone else's model obsolete.

The Prime Brokerage Disruption

In 2004, Interactive Brokers launched its Universal Account, a single account that could trade stocks, options, futures, forex, and bonds globally. But the real revolution came with the introduction of portfolio margining in 2006—a risk-based margin system previously available only to institutional traders.

Traditional brokers used crude rules: 50% margin for stocks, 20% for options. Portfolio margining looked at the actual risk of the entire portfolio, often resulting in margin requirements 70% lower. A hedged portfolio that would require $100,000 in margin at Schwab might need only $30,000 at Interactive Brokers.

This attracted a new category of customer: small hedge funds and professional traders who previously needed prime brokers. Why pay Goldman Sachs millions in fees when Interactive Brokers offered better execution, lower financing rates, and superior technology for a fraction of the cost?

By 2007, Interactive Brokers was clearing 15% of all U.S. options volume despite having less than 1% of brokerage accounts. They'd become the infrastructure for a shadow financial system—thousands of small professional traders operating with institutional-grade tools.

VI. Going Public: The 2007 IPO & Financial Crisis

The Dutch Auction Rebellion

On May 3, 2007, the company went public via an initial public offering (IPO) on the Nasdaq, selling 40 million shares, or 10% of the company, at $30.01 per share via a Dutch auction. The choice of a Dutch auction was vintage Peterffy—a deliberate rejection of Wall Street's traditional IPO process where investment banks allocate shares to favored clients who then flip them for quick profits.

"Why should investment bankers decide who gets shares and at what price?" Peterffy asked his board. "Let the market decide." The Dutch auction allowed any investor to bid, with shares allocated based on actual demand rather than banker relationships. It was the same principle that drove everything at Interactive Brokers: eliminate the middleman, let technology determine fair value.

The IPO raised $1.2 billion, valuing the company at approximately $12 billion. But the real significance wasn't the money raised—it was what Peterffy didn't do. He didn't sell a single share. Neither did any other insider. This wasn't a cash-out event; it was a strategic move to create currency for acquisitions and provide transparency for customers who wanted to know their broker was financially sound.

Wall Street's reaction was predictable skepticism. Interactive Brokers had generated $578 million in pre-tax income in the first nine months of 2006 on revenue of $969 million—a profit margin that seemed impossible. How could a broker charging pennies per trade be more profitable than firms charging hundreds of times more?

The Lehman Weekend

September 14, 2008. Lehman Brothers, with $600 billion in assets, was hours from bankruptcy. The global financial system teetered on the edge of collapse. Interactive Brokers had $11.5 billion in customer assets at Lehman's London subsidiary, frozen in the bankruptcy.

Peterffy didn't panic. He called an emergency meeting at 3 AM. "We have two problems," he told his team. "First, protecting our customers. Second, surviving what's coming." While other brokers scrambled to understand their exposure, Interactive Brokers knew exactly where every dollar was—their real-time risk systems had been tracking it for years.

The solution was audacious. Interactive Brokers would advance its own capital to make customers whole while fighting to recover assets from Lehman's estate. It would cost hundreds of millions, but Peterffy saw it as an investment in trust. "If customers think their assets aren't safe with us, we have no business."

Trading in the Chaos

As markets collapsed in October 2008, most brokers raised margin requirements, restricted short selling, and limited trading. Interactive Brokers did the opposite. They kept markets open, maintained normal margin for qualified accounts, and even reduced commissions for high-volume traders.

The risk management systems Peterffy had built over 30 years proved their worth. While other brokers suffered massive losses from customer defaults, Interactive Brokers' automated liquidation systems prevented catastrophic losses. The system would begin closing positions when accounts fell below maintenance margin, executing trades in milliseconds before losses could cascade.

During the worst week of the crisis, when the VIX spiked above 80 and daily market moves exceeded 10%, Interactive Brokers processed record volumes without a single system failure. More remarkably, they made money every single day of the crisis. Not through proprietary trading—market making had been clearly separated from the brokerage—but through the simple mechanics of their business model: more volume meant more commissions and wider interest rate spreads.

The Exodus to Quality

Between 2007 and 2013, Interactive's brokerage arm revenue and pretax profits grew from $391 to $814 million, however, the marketmaker's profits dropped drastically from $331 million to $72 million. This wasn't a failure—it was a deliberate strategic shift. As markets became more electronic and competitive, Peterffy recognized that the real value wasn't in market making but in providing infrastructure.

The financial crisis triggered a flight to quality that benefited Interactive Brokers enormously. Customers fled from firms like E*TRADE and TD Ameritrade, which had seemed solid but proved vulnerable. Interactive Brokers, with its conservative balance sheet and transparent operations, became the safe haven for serious traders.

One customer, a hedge fund manager who moved $100 million to Interactive Brokers in 2009, explained the decision: "During the crisis, I could log into my account and see exactly where my assets were held, down to the specific securities and custodian banks. Try getting that transparency anywhere else."

The Regulatory Dividend

The post-crisis regulatory environment, which crushed many financial firms, actually benefited Interactive Brokers. Dodd-Frank, Basel III, MiFID II—regulations that cost major banks billions in compliance became competitive advantages for a firm that had been operating with institutional-grade risk controls since the 1980s.

When regulators mandated real-time risk reporting, Interactive Brokers already had it. When they required segregation of customer assets, Interactive Brokers had been doing it for decades. When they demanded algorithmic trading controls, Interactive Brokers' systems exceeded every requirement.

Peterffy testified before Congress in 2010, warning about the dangers of high-frequency trading even as his firm benefited from electronic markets. His message was consistent: "Automation is inevitable and beneficial, but it must be properly controlled. We need circuit breakers, position limits, and real-time risk monitoring." It was the same philosophy he'd followed since the 1970s—embrace technology but respect its power.

By 2010, Interactive Brokers had emerged from the financial crisis stronger than ever. Customer accounts had grown 40% during the crisis years. Equity capital exceeded $4 billion. The firm that Wall Street had dismissed as a niche player for options nerds was now one of the most profitable brokers in America. The foundation was set for the next phase: becoming the default platform for global electronic trading.

VII. The Modern Era: Scale, Innovation & Global Dominance (2010-Present)

The Passing of the Torch

In 2019, at age 75, Thomas Peterffy made a decision that surprised no one and everyone simultaneously: The company's founder Thomas Peterffy stepped down from CEO position in 2019, when he turned 75. He retained the position of Chairman, while President Milan Galik was appointed CEO.

Milan Galik wasn't a Wall Street veteran or a technology visionary. He was an operations specialist who'd joined Interactive Brokers in 1990 as employee number 95, working his way up through the unglamorous trenches of clearing and settlement. His appointment sent a clear message: the era of revolutionary innovation was giving way to relentless execution.

"Thomas built the machine," Galik said in his first all-hands meeting as CEO. "My job is to make it run faster, cheaper, and everywhere."

The Robinhood Response: Creating IBKR Lite

In September 2019, the company launched commission-free trades via "IBKR Lite". This wasn't capitulation to Robinhood—it was chess, not checkers. Interactive Brokers created a two-tier system: IBKR Lite for casual investors who wanted free trades, and IBKR Pro for serious traders who understood that execution quality mattered more than commission costs.

"Interactive Brokers has always been known as the low-cost broker for sophisticated investors and institutions. We are able to provide superior pricing due to our focus on automation," said Thomas Peterffy. "With Interactive Brokers, clients can choose to pay no commissions and have their orders routed to market makers like many other retail brokers do or pay Interactive Brokers' ultra-low commissions and receive professional executions through our IB SmartRouting system."

The genius was in the segmentation. IBKR Lite orders were routed to market makers who paid for order flow—the same model Robinhood used. But IBKR Pro continued using SmartRouting, often achieving price improvement that exceeded the commission cost. Professional traders stayed on Pro; retail investors got their free trades. Everyone won, and Interactive Brokers captured both markets.

The COVID Trading Boom

March 2020. Markets in freefall. The VIX above 80. Trading volumes exploding as the world went into lockdown. For most brokers, it was chaos. Systems crashed, margin calls cascaded, customer service collapsed under the volume.

At Interactive Brokers, it was Tuesday.

The infrastructure built to handle Timber Hill's massive market-making operations barely noticed the surge in retail volume. While Robinhood restricted trading and E*TRADE's systems buckled, Interactive Brokers processed record volumes without a hiccup. Customer accounts increased 30% year-on-year to 3.34 million. Customer equity increased 33% from the year-ago quarter to $568.2 billion. The profit margin stood at 75 per cent.

The pandemic didn't just bring new customers—it brought the right customers. Professional traders fleeing established firms. International investors seeking access to U.S. markets. Cryptocurrency traders wanting a regulated platform. Each segment found exactly what they needed at Interactive Brokers.

The Technology Arms Race Continues

The modern Interactive Brokers is a technology company that happens to be a broker. The firm employs more software engineers than traders. Its annual technology spend exceeds the total revenue of many competitors. And the innovation never stops.

Recent launches read like a Silicon Valley product roadmap: cryptocurrency trading (11 coins with 24/7 access), fractional shares, forecast contracts on elections, API improvements that allow millisecond-latency trading. Each addition carefully calibrated to attract new customer segments without compromising the core platform.

The international expansion has been particularly impressive. The firm has operations in 36 countries and 28 currencies. More than half of the company's customers reside outside the United States, in approximately 200 countries. This isn't just geographic diversification—it's a bet that electronic trading will eventually dominate every market globally.

The Platform Economy

Interactive Brokers has become something more fundamental than a broker—it's become infrastructure. Thousands of smaller brokers, advisors, and fintech companies white-label Interactive Brokers' technology. They handle customer acquisition and service; Interactive Brokers handles execution, clearing, and custody.

This B2B2C model is brilliantly scalable. Interactive Brokers doesn't need to spend on marketing or customer service for these accounts. They just provide the pipes, collecting a few basis points on every trade. It's the AWS model applied to finance—why compete with your customers when you can power them?

The numbers tell the story. Interactive Brokers closed the fourth quarter of 2024 with reported revenue of approximately $1.39 billion, a year-over-year increase of 21.7 per cent. The company's reported pre-tax income also grew by 27.4 per cent to $1.04 billion. The profit margin stood at 75 per cent—a number that would make even software companies envious.

VIII. The Power Law Business Model

The Beautiful Economics of Scale

To understand Interactive Brokers' business model, imagine a highway. Building the highway costs billions—land acquisition, construction, maintenance. But once built, the marginal cost of each additional car is nearly zero. The highway can handle one car or ten thousand; the infrastructure cost is the same.

Interactive Brokers spent 40 years building its highway—the servers, the software, the connections to 150 exchanges worldwide. Now, every additional customer is nearly pure profit. The same systems that handle one trade can handle millions. The same risk management algorithms work for $10,000 accounts and $10 billion accounts.

The Three Revenue Streams

Interactive Brokers makes money three ways, and each scales differently:

Commissions (30% of revenue): The headline numbers are shocking—$0.005 per share for stocks, $0.65 per option contract. But with 3.12 million DARTs (Daily Average Revenue Trades), those pennies add up to $477 million quarterly. More importantly, higher volumes actually reduce per-trade costs through exchange rebates and operational efficiency.

Net Interest Income (62% of revenue): This is the hidden goldmine. Customers hold $120 billion in cash balances. Interactive Brokers pays them interest, but at rates below what it earns investing that cash. With $64 billion in margin loans at rates starting at 6.83%, the spread is enormous. Every Fed rate hike is pure profit—a 25 basis point increase adds $64 million to annual income.

Market Making (8% of revenue): Though diminished from its peak, Timber Hill still operates, providing liquidity in less efficient markets. This isn't the core business anymore, but it's a nice hedge—when volatility spikes and retail traders flee, market-making profits often increase.

Operating Leverage at Its Finest

The company's cost structure is almost entirely fixed. Engineers, servers, exchange connections—these costs barely change whether they process one million or ten million trades daily. This creates staggering operating leverage.

Consider the math: If revenues increase 20%, costs might increase 5%. That 15% difference flows straight to the bottom line. This is why Interactive Brokers' profit margins keep expanding even as they cut prices—volume growth more than compensates for lower unit economics.

General and administrative expenses are just $59 million quarterly on $1.4 billion in revenue—an overhead ratio of 4%. For comparison, traditional brokers run at 40-60%. This isn't efficiency; it's a different species of business.

The Network Effects Nobody Sees

The obvious network effect is liquidity—more traders mean better prices, attracting more traders. But Interactive Brokers has built subtler network effects:

Data Network Effects: Every trade generates data that improves routing algorithms. The SmartRouter gets smarter with scale, creating better execution that attracts more volume.

API Ecosystem: Thousands of developers build on Interactive Brokers' APIs. Each integration makes the platform more valuable, creating switching costs for sophisticated users.

Global Liquidity Network: A trader in Singapore can provide liquidity to someone in Sweden trading U.S. options. This global pooling of liquidity is nearly impossible to replicate.

Regulatory Network Effects: Interactive Brokers is registered in dozens of countries. Each new geography requires years of regulatory work. But once established, they become the default platform for cross-border trading.

Capital Efficiency Maximized

The profit margin stood at 75 per cent. This isn't a typo. Three-quarters of every revenue dollar becomes profit. This efficiency comes from radical automation and a refusal to provide services that don't scale.

No branches. Minimal customer service. No research analysts. No relationship managers. No free dinners or golf outings. Just pure, efficient, electronic execution.

This laser focus means Interactive Brokers can profitably serve customers that would bankrupt traditional brokers. A $10,000 account executing five trades per month generates maybe $10 in monthly revenue. At Morgan Stanley, that customer loses money. At Interactive Brokers, with near-zero marginal costs, it's profitable.

The Virtuous Cycle

Scale enables lower prices, which attracts more customers, which increases scale. But unlike typical price wars that destroy industry profitability, Interactive Brokers' scale advantages are structural. Competitors can match prices, but they can't match the unit economics.

This creates a virtuous cycle: 1. More customers → higher volumes 2. Higher volumes → better exchange pricing 3. Better exchange pricing → lower costs 4. Lower costs → lower prices for customers 5. Lower prices → more customers

Each turn of the cycle widens the moat. A competitor starting today would need to process millions of trades daily just to achieve the same unit economics Interactive Brokers had in 2010. It's not just about catching up—the target keeps moving.

IX. Ownership, Control & Corporate Structure

The Peterffy Dynasty

Thomas Peterffy holds approximately 91% of IBG Holdings LLC, making him the company's controlling shareholder. Approximately 74.2% of the voting power is held by IBG Holdings LLC. This structure is both elegant and controversial—a public company with the control dynamics of a private one.

The dual-class structure works like this: The public owns 25.8% of the economic interest through Class A shares, which trade on NASDAQ. But IBG Holdings LLC owns all the Class B shares, which carry enhanced voting rights. Since Peterffy controls 91% of IBG Holdings, he effectively controls Interactive Brokers despite owning less than a quarter of the economic interest directly.

This isn't corporate governance by committee—it's enlightened dictatorship. Peterffy can make decade-long bets without worrying about quarterly earnings calls. He can maintain unprofitable products that might become important later. He can ignore Wall Street fashion and focus on engineering excellence.

The Succession Question

The appointment of Milan Galik as CEO in 2019 was telling. Not a Wall Street star, not a Silicon Valley visionary, but a company lifer who started in operations. Galik joined in 1990 as employee #95, working his way through clearing, risk management, and operations. He knows every system, every process, every quirk of the platform.

This wasn't succession planning—it was cultural preservation. Galik represents continuity, not change. His mandate is clear: keep building the machine Peterffy designed, just faster and bigger.

But the real succession question isn't about the CEO—it's about control. When Peterffy eventually exits (he's now 80), what happens to his 91% stake in IBG Holdings? The structure suggests a gradual transition: Peterffy has been slowly selling shares through Rule 10b5-1 plans, typically 10-20 million shares at a time. But at this pace, it would take decades to meaningfully dilute his control.

The Cultural DNA

Interactive Brokers' culture is engineering culture, not Wall Street culture. No expensive offices, no executive dining rooms, no company jets. The Greenwich headquarters looks more like a server farm than a financial institution. Employees are engineers and operators, not rainmakers and relationship managers.

Compensation reflects this: modest salaries, minimal bonuses, but significant equity participation. Peterffy himself took only $800,000 in salary as CEO—less than a first-year investment banker at Goldman Sachs. The message is clear: build long-term value, not short-term commissions.

This culture creates remarkable alignment. When every employee thinks like an owner, automation isn't threatening—it's liberating. Instead of protecting their jobs, employees automate them away and move on to harder problems. It's creative destruction as organizational principle.

The Governance Paradox

By traditional governance standards, Interactive Brokers is a disaster. One man controls everything. The board is largely ceremonial. Minority shareholders have essentially no say. It's the antithesis of modern corporate governance.

Yet it works. The company has created more value for minority shareholders than almost any financial firm over the past two decades. The stock has risen from $30 at IPO to over $150, a 400% return not including dividends. Customer assets have grown from $15 billion to $568 billion.

The paradox is that autocratic control has enabled long-term thinking that democratic governance often prevents. While public companies optimize for quarterly earnings, Interactive Brokers optimizes for decades. While competitors chase trends, Interactive Brokers builds infrastructure.

The Hidden Alignments

The structure creates subtle but powerful alignments:

Customer-Owner Alignment: Peterffy's wealth is tied to the stock price, which depends on sustainable growth, not fee extraction. Screwing customers for short-term profit would destroy his net worth.

Employee-Owner Alignment: With significant insider ownership, employees aren't just workers—they're co-owners. Every efficiency gain, every new customer, every basis point of margin improvement benefits them directly.

Long-term-Short-term Alignment: The controlling structure means Interactive Brokers can ignore short-term market pressures. They can invest in projects with 10-year payoffs, knowing control won't change.

This isn't corporate governance theory—it's practical engineering applied to corporate structure. Like everything at Interactive Brokers, it's unconventional, slightly uncomfortable, and remarkably effective.

X. Playbook: What We Can Learn

Automation as Competitive Advantage: Being 10x Better, Not 10% Better

The Interactive Brokers story isn't about marginal improvements—it's about order-of-magnitude advantages. When Peterffy built his first handheld computer, it didn't price options 10% faster than paper sheets; it priced them instantly versus hourly updates. When SmartRouting launched, it didn't find slightly better prices; it found prices invisible to human traders.

This is the critical lesson: in technology-driven industries, incremental improvement is a path to irrelevance. You need capabilities your competitors can't match, not just lower prices or better service. Interactive Brokers' automation wasn't just cost-cutting—it was capability-building. They could do things (trade globally, route intelligently, manage risk in real-time) that others simply couldn't.

The playbook: identify processes your competitors treat as fixed costs and turn them into competitive advantages through radical automation. Don't automate to save money—automate to do the impossible.

The Power of Saying No

Interactive Brokers might be the most successful company built on rejection. No branches. No advisors. No hand-holding. No research. No relationship banking. No free trades (until forced). No payment for order flow (for Pro accounts). No social features. No gamification.

Each "no" was a conscious choice to focus resources on what mattered: execution quality, global access, and low costs. While competitors added features to attract customers, Interactive Brokers removed friction for the customers they wanted.

This selective focus created a powerful filter. Customers who needed hand-holding went elsewhere. Those who remained were sophisticated, profitable, and loyal. By saying no to most customers, Interactive Brokers attracted the best customers.

Global from Day One

Most companies expand internationally after dominating domestically. Interactive Brokers went global from inception. The first Timber Hill offices were in New York, London, and Zug simultaneously. The trading systems were built for multiple currencies, time zones, and regulations from the start.

This wasn't ambitious—it was necessary. Options markets are global by nature. A mispricing in Tokyo affects prices in London. Building for one market would have been building for failure.

The lesson: if your business has natural global dynamics, build global infrastructure from the beginning. The cost of retrofitting domestic systems for international markets is often higher than building globally from scratch.

Technology Moats in Financial Services

Interactive Brokers proves that technology moats in financial services are possible but require three elements:

1. Continuous Innovation: The moat isn't the technology you built yesterday but your ability to build new technology tomorrow. Interactive Brokers' advantage isn't their current systems but their capacity to build new ones.

2. Scale Economics: Technology advantages compound with scale. Every additional customer makes the platform more valuable, the data better, the economics stronger.

3. Switching Costs: Once traders learn Trader Workstation, connect their algorithms via API, and build strategies around Interactive Brokers' capabilities, switching becomes painful. The moat isn't just technology—it's expertise.

Early But Not Too Early

Peterffy's timing was exquisite. He automated trading just as computers became powerful enough but before they became commoditized. He built electronic brokerages just as the internet emerged but before it became saturated. He went international just as markets globalized but before nationalism returned.

Being early means building infrastructure before demand materializes. Being too early means dying before demand arrives. The key is to identify inevitable trends and position yourself just ahead of the adoption curve—close enough to survive, far enough to dominate.

Interactive Brokers survived by serving niche markets (options traders, international investors) while waiting for mainstream adoption. They didn't try to educate the market—they served the educated and waited for the market to catch up.

The Patience to Compound

Perhaps the most underappreciated aspect of Interactive Brokers' success is time. Forty-five years of consistent execution, continuous improvement, and compound growth. No pivots, no radical strategy changes, no transformational acquisitions. Just relentless, patient, methodical improvement.

This patience enabled strategies unavailable to others: - Spending decades building global infrastructure - Accepting lower margins to gain scale - Investing in automation with 10-year paybacks - Ignoring profitable trends that didn't fit the model

The modern startup ecosystem celebrates speed, pivots, and disruption. Interactive Brokers represents a different model: pick the right direction, build sustainable advantages, and compound them over decades. It's not exciting, but it works.

XI. Bear & Bull Case Analysis

The Bear Case: Why Interactive Brokers Could Stumble

Commoditization of Brokerage Services: The race to zero has a logical endpoint—zero. With commissions already free at most brokers, Interactive Brokers' traditional advantage is eroding. If execution quality becomes table stakes and everyone offers similar products, what differentiates them? The risk is becoming a utility—essential but undifferentiated.

Regulatory Risks and Compliance Costs: Interactive Brokers operates in 36 countries, each with evolving regulations. MiFID III in Europe, evolving crypto regulations globally, potential transaction taxes—each new rule adds complexity and cost. Unlike pure technology companies, Interactive Brokers can't just ignore unfavorable jurisdictions. Their global model requires global compliance, and that's getting exponentially more complex.

Competition from Neo-Brokers and Big Tech: Robinhood proved that user experience beats functionality for many traders. Cash App added stocks. PayPal is expanding into investing. If Apple or Google decided to offer trading, they could leverage their ecosystems to rapidly gain share. Interactive Brokers' utilitarian interface and complex products might be strengths for professionals but weaknesses against consumer-focused competitors.

Succession Risk: Peterffy is 80. While Galik is competent, he's an operator, not a visionary. When Peterffy exits, Interactive Brokers loses its founder-prophet—the person who can make decade-long bets because he built the company. The dual-class structure that enabled long-term thinking might become a liability if control passes to less capable hands.

Market Volatility Dependency: Interactive Brokers thrives on trading volume, which spikes during volatility. But sustainable businesses shouldn't depend on chaos. If markets enter a prolonged period of low volatility—like 2017's record-low VIX—revenues could stagnate. The company is essentially short market stability.

Interest Rate Sensitivity: With 62% of revenue from net interest income, Interactive Brokers is effectively a leveraged bet on interest rates. Every 25 basis point cut reduces annual income by $64 million. If rates return to zero—as they did post-2008—the business model breaks. They'd need to triple trading volumes just to maintain current profitability.

The Bull Case: Why Interactive Brokers Could Dominate

Massive International Opportunity: Interactive Brokers has 3.3 million customers. Charles Schwab has 35 million. The global addressable market is perhaps 500 million potential investors. As wealth grows in Asia, Latin America, and Africa, demand for sophisticated trading tools will explode. Interactive Brokers is the only platform positioned to capture this demand.

Operating Leverage Still Improving: At 75% profit margins, you'd think efficiency gains would be exhausted. You'd be wrong. Every new customer adds essentially zero marginal cost. Every basis point of market share gained drops straight to the bottom line. If Interactive Brokers doubles customers to 6 million—entirely feasible—profits might triple.

Prime Brokerage for Everyone: The Universal Account isn't just a brokerage account—it's a complete financial operating system. Trade any asset, in any currency, with portfolio margining and securities lending. This was once available only to institutions. As wealth inequality grows and sophisticated investors proliferate, demand for these tools will soar.

API and B2B2C Expansion: Thousands of fintechs need execution and clearing. Interactive Brokers provides the infrastructure, invisible to end users but essential to operations. This B2B2C model has unlimited scaling potential—why build trading infrastructure when you can rent Interactive Brokers'?

Regulatory Moat Strengthening: Each new regulation raises the bar for new entrants. Interactive Brokers has spent decades building compliance infrastructure. A startup trying to replicate their global reach would need hundreds of millions just for regulatory approvals. Paradoxically, the regulatory burden that bears fear actually protects Interactive Brokers' position.

AI and Algorithmic Trading Explosion: As AI democratizes quantitative trading, demand for professional-grade execution will explode. Every GitHub coder with a trading algorithm needs market access. Interactive Brokers' APIs and execution quality make them the default choice. They're selling picks and shovels for the AI gold rush.

The Verdict: Asymmetric Upside

The bear case is real but manageable. Commoditization is a risk, but execution quality still matters for active traders. Regulatory costs are rising, but so are barriers to entry. Succession is uncertain, but the culture and systems survive founders.

The bull case is compelling and accelerating. International expansion, operating leverage, and the democratization of sophisticated trading all play to Interactive Brokers' strengths. They've built infrastructure for a world that's just arriving—one where everyone is a trader, algorithms make decisions, and markets never close.

The asymmetry is this: the downside is becoming a profitable utility with steady cash flows. The upside is becoming the operating system for global finance. For long-term investors, that's a bet worth making.

XII. Grading & Final Thoughts

Execution: A+

Consistent innovation over 45+ years

From handheld computers in 1983 to cryptocurrency trading in 2021, Interactive Brokers has consistently executed on its vision of automated, global, electronic trading. They didn't just adapt to change—they drove it. The typing robot at NASDAQ, the SmartRouting algorithm, the Universal Account—each innovation was perfectly executed and years ahead of competitors. More remarkably, they've maintained this execution excellence across decades and leadership changes. This isn't just good execution; it's generational excellence.

Timing: A

Multiple first-mover advantages

Peterffy's timing has been uncanny. Electronic trading in the 1980s, just as computers became powerful enough. Internet brokerage in the 1990s, just as connectivity became reliable. International expansion in the 2000s, just as markets globalized. Commission-free trading in 2019, just as the market tipped. Each move captured a massive secular trend at exactly the right moment. The only minor deduction is for being occasionally too early—the market needed time to appreciate what they built.

Market Selection: A-

Chose the right market, but niche focus

Choosing electronic trading and global brokerage was brilliant—these markets had massive tailwinds and winner-take-all dynamics. But Interactive Brokers' focus on sophisticated traders, while profitable, limited their total addressable market. They chose depth over breadth, which created a defensible position but capped their growth potential. Robinhood, serving a worse market with worse economics, achieved a higher valuation by serving more customers.

Business Model: A

75% margins speak for themselves

The combination of commission revenue, net interest income, and minimal marginal costs creates a financial perpetual motion machine. Customer metrics showed robust growth, with the number of accounts rising by 30 per cent in the last three months of 2024 to 3.34 million. The profit margin stood at 75 per cent. These aren't software margins—they're better, because the regulatory moat prevents new competition. The model is antifragile: volatility increases revenues, stability reduces costs, growth improves unit economics.

Culture & Team: B+

Engineering excellence, but succession questions

The engineering-first culture is Interactive Brokers' greatest asset. Every employee thinks like an owner, automating rather than protecting their position. But this culture was shaped by Peterffy's singular vision. Can it survive without him? Galik is competent but not visionary. The next generation of leadership isn't obvious. The culture is strong but untested without its founder.

Overall Grade: A

Interactive Brokers is what every technology company claims to be but few achieve: a fundamental reinvention of an established industry through systematic application of technology. They didn't disrupt finance—they rebuilt it from first principles.

The Biggest Lessons for Entrepreneurs

1. Compound Advantages: Small edges, consistently maintained and improved over decades, become insurmountable moats. Interactive Brokers' advantages seem modest individually but are overwhelming collectively.

2. Serve the Sophisticated: While competitors chased mass market retail investors, Interactive Brokers focused on the most demanding customers. These customers are harder to acquire but more valuable to retain.

3. Build Infrastructure, Not Products: Products can be copied; infrastructure can't. Interactive Brokers built the pipes that others flow through. This is harder but creates permanent competitive advantage.

4. Ignore the Noise: For 45 years, Interactive Brokers ignored trends, fads, and fashion. They built what they thought was right, not what the market said it wanted. This requires conviction that few possess.

5. Time Arbitrage: In a world obsessed with quarters, thinking in decades is a superpower. Interactive Brokers made investments with 10-year paybacks while competitors worried about next quarter's earnings.

The Ultimate Assessment

Interactive Brokers is the greatest business story nobody knows. While Tesla and Amazon capture headlines, Interactive Brokers quietly built one of the most profitable, defensible, and scalable businesses in finance. They turned trading—a relationship business based on trust and tradition—into an engineering problem solved through automation.

The story isn't over. At $568 billion in customer assets, Interactive Brokers is still tiny compared to Schwab ($7.6 trillion) or Fidelity ($11.8 trillion). If they can maintain their growth rate and expand beyond sophisticated traders, they could become the default platform for global investing.

But even if they don't—even if they remain a niche player serving professional traders—they've already won. They've proven that an immigrant with $100,000 and an engineering mindset can rebuild Wall Street from scratch. They've shown that automation beats relationships, that global beats local, that patience beats speed.

Most importantly, they've demonstrated that in business, as in engineering, the elegant solution isn't the most complex or the most popular—it's the one that works. Interactive Brokers works. After 45 years, millions of trades, and endless innovation, it just works.

That's the highest praise an engineer can give.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube