Erie Indemnity: The Reciprocal Empire Built on Service

I. Introduction & Hook

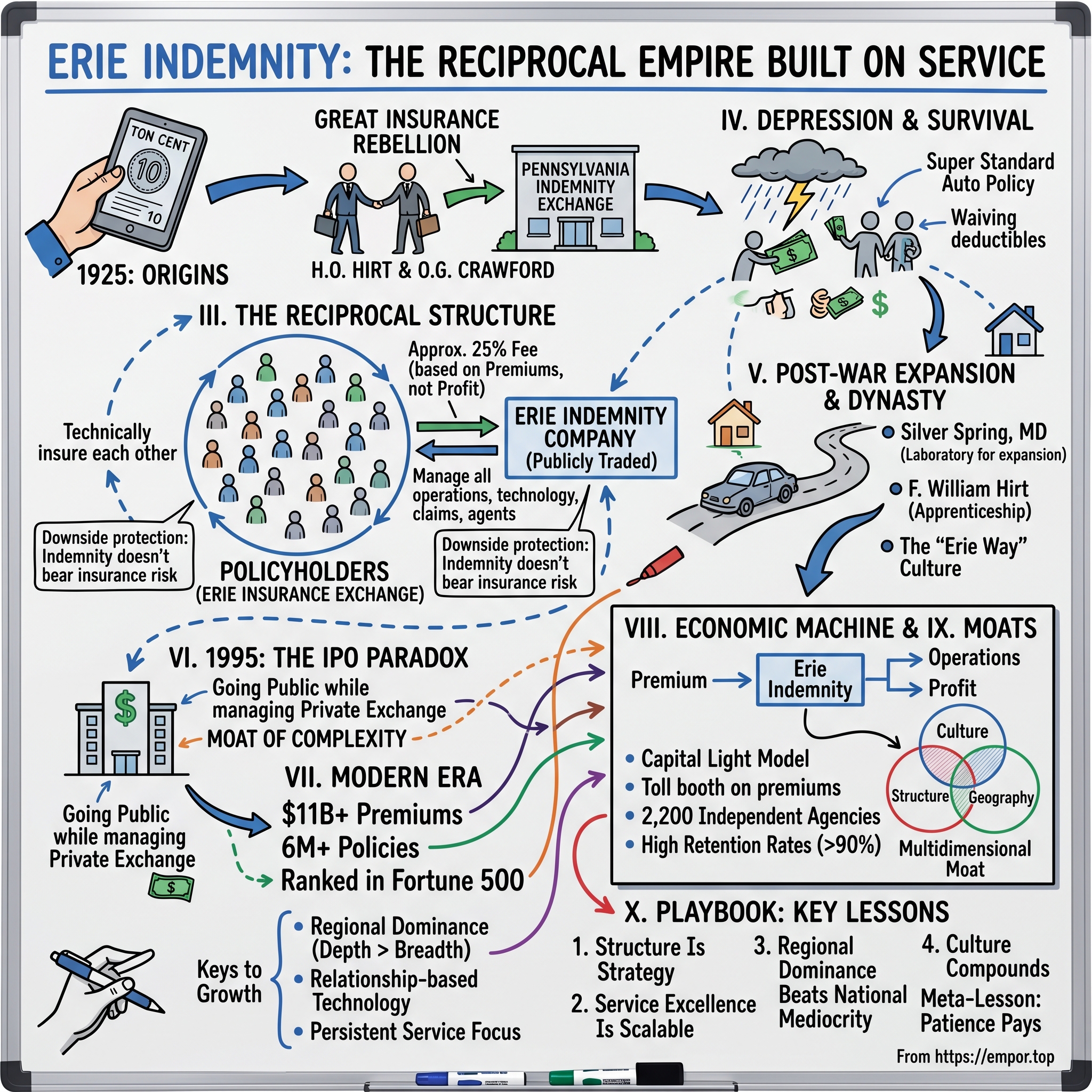

Picture this: Erie, Pennsylvania, 1925. Two insurance salesmen sit hunched over a ten-cent tablet in a dimly lit office, penciling out calculations that would reshape American insurance. H.O. Hirt and O.G. Crawford weren't tech entrepreneurs or Wall Street financiers—they were local guys who'd just quit their jobs at Pennsylvania Indemnity Exchange, convinced they could build something better. Their former employer was so confident these two wouldn't amount to much that they hired six salesmen to replace them. Six for two. That ratio would prove to be one of the great miscalculations in insurance history.

What Hirt and Crawford sketched on that tablet wasn't just another insurance company. It was a reciprocal exchange—a structure so unusual that even today, nearly a century later, Wall Street analysts struggle to categorize it. The publicly-traded Erie Indemnity Company (NASDAQ: ERIE) doesn't actually insure anyone. Instead, it manages a private reciprocal exchange where policyholders technically insure each other, like a massive, sophisticated version of neighbors helping neighbors rebuild after a barn fire.

This peculiar structure has created one of America's most enduring insurance empires. From those pencil scratches in 1925, Erie has grown to manage over 6 million policies across 12 states and Washington D.C., ranking 323rd on the 2025 Fortune 500. The company that started with $31,000 scraped together from 90 local investors now oversees billions in premiums. Yet most investors have never heard of it, and those who have often can't explain how it actually makes money.

The Erie story isn't just about insurance—it's about the power of aligned incentives, the value of stubbornness (Hirt's favorite word), and how a company can thrive for a century by focusing relentlessly on service over scale. It's about building a Fortune 500 company while maintaining the soul of a regional mutual aid society. And it's about a business model so counterintuitive that it's hidden in plain sight on public markets, generating consistent returns while competitors chase the latest InsurTech trends.

This is the story of how two salesmen with a dime-store tablet built an insurance empire by convincing people to insure each other—and somehow figured out how to take that model public while keeping it private. It's a structure that shouldn't work, in an industry that's supposedly commoditized, in a region that's supposedly past its prime. Yet here we are, a century later, and Erie keeps compounding.

II. Origins: The Great Insurance Rebellion (1920s)

The rebellion began not with manifestos or protests, but with a resignation letter. In 1924, H.O. Hirt and O.G. Crawford walked away from secure positions at Pennsylvania Indemnity Exchange, one of the region's established insurance players. They weren't leaving for better offers or bigger salaries—they were leaving to build their own vision of what insurance could be. PIE's management must have chuckled when they heard the news. These were just two salesmen, after all. To replace them, the company hired six new agents, figuring they'd more than covered their bases.

But Hirt and Crawford weren't just salesmen—they were students of the insurance game who'd identified a fundamental flaw in how it was played. Traditional insurance companies operated like fortresses, with shareholders on one side, policyholders on the other, and profits extracted from the friction between them. The reciprocal exchange model they envisioned would collapse this adversarial structure. Policyholders would own the exchange, insuring each other through a pool of shared risk, while a separate management company would handle operations for a transparent fee.

The fundraising campaign that followed reads like a Depression-era startup hustle. Armed with their ten-cent tablet full of projections and a compelling pitch about neighbors protecting neighbors, Hirt and Crawford knocked on doors across Erie County. They needed capital not for the exchange itself—that would be funded by policyholder premiums—but for the management company that would run it. Over four grueling months in early 1925, they convinced 90 local investors to put up $31,000. These weren't venture capitalists or institutional investors; they were local business owners, professionals, and even some farmers who believed in the vision of community-based insurance.

On April 20, 1925, the papers were signed. Erie Insurance Exchange was officially formed as a reciprocal, with Erie Indemnity Company established as its attorney-in-fact—the legal term for the entity managing a reciprocal exchange. The structure was intentionally complex, almost byzantine, but Hirt insisted this complexity served a purpose. It aligned everyone's interests: policyholders owned the risk pool, the management company earned fees only when it served those policyholders well, and local agents built long-term relationships rather than chasing quick commissions.

The company's first motto, created by the founders themselves, revealed their philosophy: "Above all in sERvIcE"—with the capitalized ERIE cleverly embedded in the word service. This wasn't just marketing copy; it was a operating principle that would guide every major decision for the next century. While competitors focused on financial engineering and scale, Erie would win through superior claims handling, local relationships, and an almost obsessive focus on policyholder satisfaction.

By 1928, just three years after formation, Erie had expanded from its namesake city to Pittsburgh, Pennsylvania's industrial powerhouse. This wasn't a random expansion—Pittsburgh's growing middle class needed auto insurance, and Erie's model of transparent, service-first coverage resonated with steel workers and shop owners who'd been burned by traditional insurers. The expansion required hiring local agents who understood their communities, building claims offices that could respond quickly to accidents, and most importantly, maintaining the service standards that were already becoming Erie's signature.

The genius of Hirt and Crawford's rebellion wasn't in inventing the reciprocal structure—those had existed since the 1800s. It was in recognizing that insurance, at its core, is about trust. And trust, they believed, was best built through alignment, transparency, and relentless focus on service. While their former employer needed six people to replace them, Hirt and Crawford were building something that would eventually employ thousands and serve millions. The tablet might have cost a dime, but the idea sketched on it would prove priceless.

III. The Reciprocal Structure: A Business Model Unlike Any Other

To understand Erie's empire, you must first untangle one of American capitalism's most elegant puzzles: how do you create a public company that manages a private entity where the customers own the business but have no say in running it? If this sounds like a riddle wrapped in a paradox, welcome to the reciprocal exchange structure—a 19th-century mutual aid concept that Erie transformed into a 21st-century profit machine.

Here's how it works: When you buy an Erie insurance policy, you're not actually buying insurance from Erie Indemnity, the public company. Instead, you're joining Erie Insurance Exchange, an unincorporated association where thousands of policyholders agree to insure one another. Think of it as a massive risk-sharing cooperative, except instead of barn-raisings and potluck dinners, there are actuarial tables and claims adjusters. Each policyholder is technically both an insurer (sharing in the risk of others) and an insured (having their own risk covered by others).

But here's where it gets interesting: while policyholders own the Exchange's surplus and share in its risks, they have essentially no decision-making power. They can't vote on management, can't demand dividends, can't even see detailed financials beyond regulatory filings. This isn't a bug in the system—it's the central feature. The Exchange needs an "attorney-in-fact" to handle everything from selling policies to investing premiums to settling claims. Enter Erie Indemnity Company, the publicly-traded management company that runs the entire operation.

The economics are beautifully simple: Erie Indemnity charges the Exchange a management fee of approximately 25% of all premiums written. Not profits, not investment returns—premiums. In 2023, that meant roughly $2.8 billion in management fees on $11.2 billion in premiums. This fee covers everything: agent commissions, underwriting expenses, claims processing, technology, marketing, and corporate overhead. Whatever's left after expenses is Erie Indemnity's profit, which flows to its public shareholders.

This creates an unusual dynamic. Erie Indemnity's revenue is essentially guaranteed as long as the Exchange writes policies. The company doesn't bear insurance risk—if a hurricane devastates Pennsylvania, the Exchange pays claims from its surplus, not Erie Indemnity. The management company's only risk is operational: can it provide services efficiently enough to earn a profit on that 25% fee? This transforms a volatile insurance business into a predictable fee-generating machine, more akin to an asset manager than a traditional insurer.

The 25% cap isn't arbitrary—it's a carefully calibrated number that threads multiple needles. It's high enough to cover Erie Indemnity's costs and generate attractive returns for shareholders, but low enough that the Exchange remains competitive on pricing. It's transparent enough to satisfy regulators who scrutinize related-party transactions, but opaque enough that competitors can't easily replicate the model. Most importantly, it's been remarkably stable: the fee has remained around 25% for decades, through hard and soft insurance markets, through catastrophes and calm periods.

Why does this structure matter for investors? First, it creates tremendous operating leverage. When premiums grow—whether through rate increases, new policies, or geographic expansion—Erie Indemnity's revenue grows proportionally, but its costs don't necessarily scale linearly. Second, it provides downside protection: even if the Exchange has a terrible underwriting year, Erie Indemnity still collects its fees. Third, it aligns long-term incentives: Erie Indemnity only thrives if the Exchange thrives, creating a genuine partnership rather than an adversarial relationship.

The structure also explains some of Erie's quirks. The company's legendary focus on service isn't just cultural—it's structural. Since Erie Indemnity doesn't benefit from denying claims or shortchanging policyholders (that would just hurt the Exchange's surplus), it can focus purely on efficiency and satisfaction. The company's conservative expansion strategy makes sense too: each new state requires building local agent networks and claims capabilities, costs that Erie Indemnity bears upfront but only recoups through long-term fee generation.

Critics argue this structure creates conflicts of interest—how can Erie Indemnity negotiate fairly with the Exchange when it controls both sides of the table? The answer lies in governance: independent trustees oversee the Exchange, state regulators scrutinize the fee arrangement, and ultimately, market forces prevail. If the Exchange becomes uncompetitive due to excessive fees, policies decline, and Erie Indemnity's revenue evaporates. It's a delicate balance that's worked for nearly a century, creating value for both public shareholders and private policyholders—a feat that shouldn't be possible in efficient markets, yet here we are.

IV. Depression, War, and Survival (1930s-1940s)

The Great Depression arrived in Erie like a late winter storm—sudden, brutal, and seemingly endless. By 1933, a quarter of Pennsylvania's workforce was unemployed. Steel mills shut down, factories closed, and families who'd scraped together enough money for a Model T suddenly couldn't afford gas, let alone insurance. For a young company barely eight years old, built on the premise of neighbors protecting neighbors, this was the ultimate test: what happens when your neighbors can't protect themselves?

H.O. Hirt's response revealed the strategic genius hidden beneath his folksy demeanor. While competitors slashed coverage and raised deductibles—figuring desperate customers would accept anything—Hirt went the opposite direction. In 1934, Erie introduced the "Super Standard Auto Policy," a product that sounds like marketing fluff but was actually revolutionary. The policy included "Drive Other Car" coverage (protecting policyholders when driving borrowed vehicles) and, most remarkably, waived deductibles for accidents between Erie-insured vehicles.

Think about that last provision for a moment. In Depression-era Pennsylvania, where extended families shared cars and neighbors helped each other with transportation, the chances of two Erie-insured vehicles colliding were surprisingly high. By waiving deductibles in these cases, Erie eliminated the awkwardness and financial strain of neighbors having to collect from each other. It was a masterstroke of community-focused product design, turning a potential source of conflict into a demonstration of mutual aid.

The math behind this generosity was counterintuitive but brilliant. Since both vehicles were Erie-insured, the Exchange was paying claims regardless. By waiving deductibles, Erie reduced administrative costs (no need to collect small amounts from struggling policyholders) and dramatically improved customer satisfaction. The cost was minimal, but the loyalty it generated was priceless. Word spread through Pennsylvania's tight-knit communities: Erie didn't just talk about being different—they proved it when times were toughest.

Hirt's philosophy during this period became company legend, encapsulated in his favorite word: "stubbornness." At a 1935 agent meeting, with many insurers failing and others retrenching, he declared: "I recommend stubbornness. Others may quit, others may fail, but we will not. We are not competing against other companies—we are the competition." This wasn't empty rhetoric. While competitors laid off agents, Erie maintained its force. While others delayed claims, Erie accelerated them, understanding that a quick settlement might mean the difference between a family keeping their home or losing it.

The Exchange's reciprocal structure proved its worth during these dark years. Traditional insurance companies, pressured by shareholders demanding dividends despite losses, had to choose between service and solvency. Erie Insurance Exchange, owned by its policyholders, could prioritize long-term survival over short-term profits. The management company, Erie Indemnity, tightened its belt but continued investing in agent training and claims processing, betting that superior service during the crisis would pay dividends during the recovery.

World War II brought different challenges and unexpected opportunities. Gas rationing meant fewer miles driven and fewer accidents, improving loss ratios across the industry. But it also meant families holding onto cars longer, increasing the importance of comprehensive coverage beyond just collision. Erie adapted its products to cover these aging vehicles, understanding that a 1935 Plymouth might be a family's most valuable asset in 1943.

The war years also demonstrated Erie's operational resilience. With young men deployed overseas, the company promoted women to roles previously reserved for men—claims adjusters, underwriters, even agency managers. This wasn't progressive politics; it was practical necessity. But it revealed something important about Erie's culture: competence mattered more than convention. Many of these women remained with the company after the war, creating a more diverse workforce decades before it became fashionable.

By 1945, as soldiers returned home and the economy began its post-war boom, Erie had not just survived—it had built an unshakeable foundation. The company that entered the Depression with operations in two Pennsylvania cities now had agents across the state, a reputation for unmatched service, and most importantly, the trust of communities that had witnessed its character during the darkest times. The stubborn refusal to compromise on service when it would have been easy—even logical—to do so had created something more valuable than surplus: a brand that meant something to people who'd lived through times when meaning was scarce.

The lesson from this era wasn't just about weathering storms—it was about using crisis to reveal and reinforce core values. Every company claims to prioritize customers and service. Erie proved it when proof mattered most, turning the Depression from an existential threat into a competitive moat that would protect the company for generations.

V. Post-War Expansion & Family Dynasty (1950s-1980s)

The 1950s dawned with America in motion—literally. Eisenhower's Interstate Highway System was turning the country into a vast network of asphalt arteries, suburbs were sprouting like mushrooms after rain, and the two-car garage was becoming as American as apple pie. For Erie, perched in its Pennsylvania stronghold, the question wasn't whether to expand, but how to do it without losing the soul that made the company special.

The answer came in 1953 with the opening of Erie's Maryland branch in Silver Spring, a suburb of Washington D.C. that epitomized the new American dream. This wasn't random expansion—it was surgical. Silver Spring sat just across the Pennsylvania border, allowing Erie to leverage its existing agent relationships while tapping into the federal government's growing workforce of middle-class professionals who needed reliable auto insurance. The branch became Erie's laboratory for expansion: could the company's high-touch, service-first model work outside its home state?

The Maryland experiment revealed a crucial insight: Erie's competitive advantage wasn't just service—it was the ability to build and maintain long-term agent relationships. While national insurers treated agents as interchangeable distribution points, Erie invested in making agents true partners. The company provided extensive training, generous commissions, and most importantly, local autonomy to serve their communities. An Erie agent in Silver Spring could make decisions that an Allstate agent would need three levels of approval to consider.

This period also marked the transformation of Erie from a startup into a dynasty. F. William Hirt, H.O.'s son, joined the company in the early 1950s, not as heir apparent but as a ground-level employee who had to prove himself. The younger Hirt worked his way through various departments—claims, underwriting, agency management—learning the business from the inside out. This wasn't nepotism; it was apprenticeship. By the time he assumed leadership roles, F. William understood Erie's operations better than any MBA consultant ever could.

The family's influence deepened in 1980 when Susan Hirt Hagan, H.O.'s granddaughter, was elected to the board—one of the first women to serve on a major insurance company board. Her appointment wasn't ceremonial. Hagan brought fresh perspectives on technology and customer service, pushing Erie to modernize while maintaining its traditional values. The Hirt family's continued involvement created something rare in American business: multi-generational strategic thinking. While public companies obsessed over quarterly earnings, Erie could plan in decades.

The agency network that emerged during these years became Erie's secret weapon. By 1980, the company had over 1,000 independent agencies, each deeply embedded in their local communities. These weren't just sales offices—they were relationship hubs. An Erie agent might insure three generations of the same family, attend their weddings and funerals, sponsor their Little League teams. This created switching costs that had nothing to do with price and everything to do with trust.

The economics of this model were compelling. While direct insurers like GEICO spent fortunes on advertising to acquire customers one at a time, Erie's agents brought in entire families and kept them for decades. Customer acquisition costs were higher upfront—agents earned substantial commissions—but lifetime value was extraordinary. Erie's retention rates consistently exceeded 90%, meaning the company spent less on marketing and more on service, creating a virtuous cycle that competitors struggled to break.

The culture that crystallized during these decades—"The Erie Way," as employees called it—blended Pennsylvania pragmatism with genuine care for policyholders. Claims adjusters were encouraged to look for ways to approve claims, not deny them. Underwriters were trained to understand individual circumstances, not just apply rigid formulas. This sounds like expensive idealism, but it was actually hardheaded business logic: happy customers don't switch insurers, and they tell their friends.

Geographic expansion continued methodically through the 1970s—West Virginia in 1972, Virginia in 1975, North Carolina in 1979. Each new state followed the same playbook: identify strong local agents, invest in claims infrastructure, and slowly build density. Erie refused to chase growth for growth's sake. The company would rather be dominant in 10 states than marginal in 50, understanding that insurance is ultimately a local business, even in an increasingly national economy.

By 1980, Erie had transformed from a regional insurgent into an established power, managing over $500 million in premiums. But more importantly, it had solved a puzzle that confounded the industry: how to scale a relationship business without losing relationships. The answer lay not in technology or financial engineering, but in structure and culture—the reciprocal model that aligned interests, the family leadership that thought long-term, and the agent network that turned insurance from a transaction into a relationship.

The company that H.O. Hirt built on stubbornness had evolved into something more sophisticated but no less stubborn. It still refused to compromise on service, refused to chase fads, refused to prioritize shareholders over policyholders. This stubbornness, once a survival mechanism, had become a competitive advantage. While the insurance industry consolidated into mega-corporations and direct-to-consumer startups, Erie occupied a unique position: big enough to matter, small enough to care, structured to align everyone's interests for the long haul.

VI. Going Public: The IPO Paradox (1995)

October 2, 1995, should have been impossible. That morning, Erie Indemnity Company began trading on the NASDAQ under the ticker "ERIE," marking one of the most paradoxical IPOs in market history. Here was a company going public that didn't actually insure anyone, managing an exchange that would remain private, with a business model so unusual that the SEC had to create special disclosure categories just to describe it. The road shows must have been surreal—imagine explaining to Wall Street that you're buying shares in a company whose only customer is an entity you can never invest in.

The decision to go public had been percolating since the early 1990s, driven by a collision of practical needs and strategic opportunities. The Hirt family and early investors, some holding shares for seven decades, needed liquidity. Erie Indemnity needed capital to fund technology investments as the insurance industry digitized. But perhaps most importantly, the company's leadership recognized that public markets could provide something more valuable than money: discipline and transparency that would benefit both shareholders and policyholders.

The IPO prospectus was a masterpiece of explaining the inexplicable. How do you value a company whose revenue is capped at 25% of another entity's premiums? How do you analyze growth prospects when expansion depends on regulatory approval in each new state? How do you assess risk when the company doesn't actually bear insurance risk but is entirely dependent on a single customer? The bankers at Alex. Brown & Sons (later acquired by Deutsche Bank) earned their fees threading this needle.

Wall Street's initial reaction ranged from confusion to skepticism to intrigue. Some analysts couldn't get past the structural complexity—one famously called it "a solution in search of a problem." Others dismissed it as a sleepy regional insurer dressed up in financial engineering. But a few sophisticated investors recognized what Erie really was: a toll booth on a growing stream of insurance premiums, with built-in inflation protection and minimal capital requirements.

The IPO raised $92 million at $17.50 per share, valuing the company at roughly $900 million. By Wall Street standards, this was a modest debut. No hockey-stick growth projections, no promises to "disrupt" insurance, no charismatic founder doing CNBC interviews. Just a 70-year-old company with a peculiar structure and a promise to keep doing what it had always done: collect fees for managing insurance operations exceptionally well.

The early trading revealed the market's schizophrenia about Erie. The stock would spike when investors focused on the predictable fee income and high returns on equity. It would slump when they worried about the Exchange's underwriting results or Erie's geographic limitations. This volatility masked a deeper truth: the market didn't know how to price a business model that had no true comparables.

The formal listing on December 16, 1995, after the quiet period ended, brought more scrutiny and more confusion. Sell-side analysts struggled to categorize Erie. Was it a property-casualty insurer? Not really, since it didn't bear insurance risk. A specialty finance company? Perhaps, but it didn't make loans or manage traditional assets. A business services firm? Closer, but that missed the integrated nature of the insurance ecosystem. This categorization challenge would persist for decades, contributing to what many believed was chronic undervaluation.

The governance structure post-IPO added another layer of complexity. Public shareholders owned Erie Indemnity but had no direct say in the Exchange's operations. The Exchange's trustees, appointed through a Byzantine process involving policyholders and state regulators, made key decisions about underwriting standards and geographic expansion. Erie Indemnity's board could influence but not dictate strategy. This separation of ownership and control violated every principle taught in business schools, yet somehow it worked.

For employees and agents, the IPO marked a cultural watershed. Erie had always prided itself on being different—a mutual-aid society scaled up, a company where relationships mattered more than ratios. Now it had ticker symbols and quarterly earnings calls. Some worried that public market pressure would erode Erie's famous service standards. Would claims adjusters start denying borderline cases to boost quarterly profits? Would agents push unnecessary coverage to increase premiums and thus management fees?

The answer, remarkably, was no. The IPO actually reinforced Erie's unique culture by making its unusual model transparent. Every quarter, analysts could see that Erie Indemnity only prospered when the Exchange did well. Every annual report demonstrated that short-term profit maximization would ultimately destroy long-term value. The public market discipline, rather than corrupting Erie's model, validated it.

By the end of 1996, a year after going public, Erie's stock had climbed 40%, outperforming most insurance stocks despite—or perhaps because of—its unusual structure. Early investors who'd puzzled through the complexity were being rewarded. The company that shouldn't exist as a public entity was proving that sometimes the best investments are the ones that require a lengthy explanation.

The IPO paradox—taking public a company that manages a private entity where customers own everything but control nothing—became Erie's greatest strength. It created a moat of complexity that kept out short-term speculators while attracting patient capital. It forced transparency that benefited all stakeholders. Most importantly, it proved that you could access public markets without sacrificing the mutual-aid principles that made Erie special. The market might not fully understand Erie, but it was beginning to appreciate it.

VII. Modern Era: From Regional Player to Fortune 500 (1996-Present)

Stephen Milne's appointment as CEO in 1996 could have been a changing of the guard. After all, the company was now public, the founding family was transitioning to board roles, and the insurance industry was consolidating at breakneck speed. Instead, Milne—who'd worked alongside H.O. Hirt since 1973—orchestrated something more subtle and powerful: an evolution that preserved Erie's DNA while adapting it for the 21st century.

Milne understood something his Wall Street critics didn't: Erie's regional limitation wasn't a weakness to be fixed but a strength to be leveraged. While competitors spread themselves thin trying to achieve national scale, Erie would dominate its chosen territories. The strategy was almost military in its precision—achieve 10% market share in existing states before considering new ones, build density corridor by corridor, never enter a state unless you can provide the same level of service that made you successful in Pennsylvania.

The true test of this philosophy came in September 1999 when Hurricane Floyd devastated North Carolina, dumping 20 inches of rain and causing billions in damage. Erie had only been in the state for two decades, still building its presence. The easy response would have been to process claims slowly, challenge coverage, preserve capital. Instead, Erie deployed what became a legendary response: within 48 hours, nearly every affected policyholder had met face-to-face with a claims representative. Not a phone call, not an app—an actual human being with a checkbook and authority to settle claims on the spot.

The Floyd response cost millions more than actuarially necessary, but it cemented Erie's reputation in North Carolina for the next generation. Local agents reported families switching from carriers who'd made them wait weeks for adjusters. The story spread through communities like wildfire: when disaster strikes, Erie shows up. This wasn't charity—it was long-term value creation disguised as exceptional service.

The year 2003 marked a symbolic milestone when Erie debuted on the Fortune 500 list at number 492. For a company that had never operated in more than a dozen states, this was remarkable. The listing validated Erie's strategy of depth over breadth—you didn't need to be everywhere to be significant. By 2021, Erie had climbed to 347th, and by 2025, reached 323rd, managing over 6 million policies with $11 billion in premiums.

The digital transformation that swept through insurance in the 2010s posed an existential question: how does a company built on personal relationships compete in an age of algorithms and apps? Erie's answer was characteristically thoughtful—embrace technology to enhance relationships, not replace them. The company invested hundreds of millions in digital capabilities, but always in service of the agent-policyholder relationship. Mobile apps for claims photos, yes. But the photos went to local adjusters who knew the community, not to an AI in a data center.

This hybrid approach proved prescient during the COVID-19 pandemic. While purely digital insurers struggled with complex claims that required human judgment, and traditional insurers scrambled to enable remote operations, Erie seamlessly shifted to a model where technology handled routine tasks while humans managed relationships and complex decisions. Claims satisfaction scores actually increased during the pandemic, a testament to the model's resilience.

The numbers tell the modern Erie story: consistent combined ratios in the mid-90s (meaning the Exchange remains profitable on underwriting, not just investments), customer retention above 90%, and returns on equity for Erie Indemnity consistently above 15%. But the numbers don't capture the full picture. In an era when insurance has become increasingly commoditized, Erie has somehow maintained pricing power. Customers willingly pay 5-10% more for Erie policies, a premium for something intangible but real—the confidence that when disaster strikes, Erie will be there.

Geographic expansion continued methodically into the 21st century—Tennessee in 2003, Kentucky in 2007, reaching a footprint of 12 states plus D.C. by 2025. Each expansion followed the same playbook developed decades earlier, proof that in insurance, execution matters more than innovation. While InsurTech startups burned billions trying to "disrupt" insurance, Erie quietly grew by doing the basics exceptionally well.

The modern Erie operates at a scale that would astonish H.O. Hirt—2,200 agencies, 13,000 licensed agents, 6,000 employees—yet maintains the feel of a regional mutual aid society. Agents still know their customers' names. Claims adjusters still have authority to make judgment calls. The company still prioritizes policyholder satisfaction over quarterly earnings. This shouldn't work in an age of algorithmic efficiency and ruthless optimization, yet Erie's returns suggest otherwise.

The transformation from regional player to Fortune 500 stalwart wasn't about changing what Erie was—it was about proving that what Erie had always been could scale. The reciprocal structure that seemed antiquated in 1995 now looks prescient, aligning stakeholder interests in ways that traditional corporate structures struggle to achieve. The focus on relationships over transactions, dismissed as quaint by digital disruptors, has created switching costs that no app can overcome. The geographic concentration, criticized as lack of ambition, has generated returns that nationally diversified insurers envy.

As Erie approaches its centennial, it occupies a unique position in American business—big enough to matter in any market it enters, focused enough to dominate those markets, and structured in a way that makes the usual corporate pathologies nearly impossible. It's a Fortune 500 company that acts like a family business, a public company serving a private exchange, a 21st-century success story built on 19th-century principles. The modern era hasn't changed Erie so much as revealed that Erie's model was modern all along.

VIII. The Economics Machine: How Erie Makes Money

Let's dispense with the suspense: Erie Indemnity's business model is one of the most elegant money-making machines in American capitalism. It's a toll booth on insurance premiums, a royalty on risk, a fee extractor that would make medieval tax collectors jealous—except it's completely legal, totally transparent, and somehow beneficial to all parties involved. Understanding how this machine works requires peeling back layers of structure to reveal the beautiful simplicity beneath.

Start with the basics: Erie Indemnity collects approximately 25% of all premiums written by the Erie Insurance Exchange. In 2024, that translated to roughly $3 billion in revenue on $12 billion in premiums. This isn't a percentage of profits or a share of investment income—it's a cut of gross premiums, paid whether the Exchange has a good year or a terrible one. It's as if McDonald's franchisees paid corporate 25% of every dollar that came through the door, not just a slice of profits.

But here's where it gets interesting: that 25% fee must cover everything. Agent commissions, which run about 69% of policy issuance expenses. Underwriting costs. Claims processing. Technology infrastructure. Marketing. Corporate overhead. Executive compensation. The Christmas party. Everything. What's left after all these expenses is Erie Indemnity's profit, which has consistently generated returns on equity north of 15% for decades.

The genius of this model lies in its operating leverage. When premiums grow 10%, Erie Indemnity's revenue grows 10%, but its costs might only grow 5-6%. Why? Because much of the infrastructure—technology systems, corporate functions, regional offices—represents fixed or semi-fixed costs. You don't need twice as many accountants to process twice as many premiums. This leverage means that premium growth drops almost directly to the bottom line after covering marginal costs.

Consider the unit economics of a single auto policy. Let's say the annual premium is $1,500. Erie Indemnity immediately collects $375 (25%). From this, it pays the agent roughly $150 in first-year commission (dropping to maybe $75 in renewal years). Underwriting and policy issuance might cost $50. Claims handling allocation could be $40. Technology and overhead might add another $60. That leaves $75 in profit on a new policy, $160 on a renewal. With retention rates above 90%, the lifetime value of that customer relationship could exceed $1,000 in profits to Erie Indemnity—all without bearing any insurance risk.

The capital efficiency of this model borders on absurd. Traditional insurers need massive balance sheets to support their underwriting. They must hold capital against potential losses, maintain liquidity for claims, and manage complex investment portfolios. Erie Indemnity needs almost none of this. Its capital requirements are minimal—just enough to fund operations and maintain regulatory compliance. This means returns on invested capital that make software companies envious.

The fee structure creates fascinating incentive alignments. Erie Indemnity wants the Exchange to write more premiums, but not bad premiums that would impair the Exchange's surplus and threaten long-term growth. It wants to settle claims quickly and fairly—not because it bears the cost (the Exchange does) but because satisfied customers renew policies and refer friends. It wants to invest in technology and service—not to boost short-term profits but to maintain the competitive position that enables premium growth.

The management fee cap at 25% acts as both ceiling and floor. It's high enough to generate attractive returns but low enough to keep the Exchange competitive. More subtly, it forces Erie Indemnity to become ever more efficient. Since the company can't raise its percentage take, the only way to grow profits faster than premiums is to reduce unit costs. This has driven decades of operational improvements, from digitizing applications to automating routine claims, all while maintaining service quality.

Investment income adds another layer to the economics. While Erie Indemnity doesn't bear insurance risk, it does hold substantial investments—both its own capital and float from premiums collected but not yet remitted to the Exchange. In a normal interest rate environment, this generates meaningful additional income. During the zero-interest-rate decade after 2008, this income evaporated, yet Erie Indemnity remained highly profitable, proving the resilience of the core fee model.

The geographic concentration strategy makes economic sense through this lens. Entering a new state requires upfront investment in agents, claims infrastructure, and regulatory compliance—costs Erie Indemnity bears immediately but only recoups through years of fee collection. Better to dominate existing markets, where the infrastructure is paid for and marginal policies are highly profitable, than to spread thin across new territories. This patient approach to expansion has generated returns that growth-at-any-cost strategies rarely achieve.

What about competitive threats to this golden goose? The Exchange can't realistically switch management companies—Erie Indemnity's operations are too embedded, its knowledge too specialized. Regulators monitor the fee arrangement but have blessed it for decades. Policyholders could theoretically revolt, but with satisfaction scores in the 90s, why would they? The model has achieved a rare equilibrium where all parties benefit from the status quo.

The ultimate test of any business model is its performance through cycles, and Erie's has proven remarkably resilient. During hard insurance markets when premiums rise, Erie Indemnity's revenue automatically increases. During soft markets, the company's efficient operations and high retention rates provide stability. During catastrophes, the Exchange bears the losses while Erie Indemnity keeps collecting fees. During economic downturns, people still need insurance, and Erie's customer base of middle-class families and small businesses proves surprisingly stable.

This economics machine—elegant in design, powerful in operation, resilient through cycles—has generated billions in profits from what amounts to a service contract. It's a business model that shouldn't exist in efficient markets, yet has thrived for nearly a century. The beauty isn't just in the returns it generates, but in how those returns align everyone's interests: Erie Indemnity prospers when the Exchange does well, agents succeed when customers are satisfied, and policyholders benefit from excellent service at fair prices. It's capitalism at its most symbiotic, proof that sometimes the best business models are the ones that make everyone a winner.

IX. Competitive Analysis & Moats

Warren Buffett once said he looks for businesses with moats so wide you could float the Queen Mary through them. Erie's moat isn't just wide—it's multidimensional, creating barriers that protect the company from threats both expected and unimaginable. Understanding these competitive advantages requires looking beyond the usual metrics to see how structure, culture, and geography combine to create something nearly impossible to replicate.

Start with the agent network: 2,200 independent agencies with over 13,000 licensed agents, built over a century of careful cultivation. These aren't employees—they're independent business owners who've staked their livelihoods on Erie's success. While State Farm and Allstate operate captive agent models (agents can only sell their products), and GEICO sells direct to consumers, Erie occupies a sweet spot: independent agents who predominantly sell Erie products because they want to, not because they have to.

The economics of replicating this network border on prohibitive. Training a new agent costs tens of thousands of dollars. Building an agency to profitability takes years. Achieving the density Erie has in Pennsylvania or Maryland would require billions in investment with no guarantee of success. When Progressive or GEICO wants to enter a new market, they buy advertising. When they want to grow, they spend more on advertising. Erie's growth comes from agents who've spent decades building relationships. Which would you rather own?

The A+ (Superior) rating from A.M. Best isn't just a badge—it's a competitive weapon. This rating, maintained consistently for decades, allows Erie to compete for commercial lines and high-net-worth individuals who won't consider insurers with lower ratings. More importantly, it provides comfort to agents and policyholders that claims will be paid, even after catastrophic events. In insurance, trust is the product, and ratings are trust quantified.

Geographic concentration, often cited by analysts as Erie's weakness, is actually its strength. In Pennsylvania, Erie holds roughly 8% market share in auto insurance—third behind State Farm and Allstate but ahead of GEICO and Progressive. This density creates economies that dispersed nationals can't match. Claims adjusters can handle more claims per day because they're not driving across three states. Agents know their markets intimately. Brand recognition means lower customer acquisition costs. It's the insurance equivalent of Walmart's hub-and-spoke dominance in rural America.

The reciprocal structure creates a moat that's nearly impossible to cross. A competitor can't just decide to become a reciprocal—it requires creating an entirely new entity, convincing regulators, and most impossibly, convincing customers to join an unproven exchange. The structure also makes Erie uninvestable for many institutions—you can buy Erie Indemnity stock, but you can't buy the Exchange that generates the premiums. This complexity keeps out momentum traders and attracts patient capital, creating a shareholder base that understands and values the model.

Technology presents both threat and opportunity. InsurTech startups like Lemonade and Root promised to revolutionize insurance through AI and behavioral analytics. Five years and billions of dollars later, they're struggling to achieve profitability while Erie quietly generates 15% returns on equity. Why? Because Erie uses technology to enhance its model, not replace it. Digital applications speed up agents, not eliminate them. AI helps adjusters assess damage, not replace human judgment. The company spends hundreds of millions on technology, but always in service of relationships.

The cultural moat might be the widest of all. Erie's service obsession isn't a marketing slogan—it's embedded in every process, metric, and incentive. Claims adjusters are measured on satisfaction, not just efficiency. Agents are rewarded for retention, not just new sales. Executives visit agencies and talk to customers, not just analyze spreadsheets. This culture, built over a century, can't be replicated with consultants or mission statements. It must be lived, practiced, and reinforced through thousands of daily decisions.

Competition with the nationals—State Farm, Allstate, GEICO, Progressive—plays out on multiple dimensions. On price, Erie is rarely the cheapest, typically charging 5-10% premiums over direct insurers. On coverage, Erie often provides more comprehensive protection, including unique features like the deductible waiver between Erie-insured vehicles. On service, Erie consistently outranks nationals in satisfaction surveys. On claims, Erie's local adjusters provide a personal touch that call centers can't match.

The regional competitors—Cincinnati Financial in Ohio, Auto-Owners in Michigan—present a different challenge. They understand Erie's model because they operate similar ones. But geographic overlap is limited, and these companies often end up competing more with nationals than with each other. It's like local restaurants in different neighborhoods—they might serve similar food, but they're not really fighting for the same customers.

Climate change looms as the industry's existential challenge, but here too Erie's model provides protection. The company's geographic footprint avoids the most catastrophe-prone areas—no Florida hurricanes, no California earthquakes, minimal tornado alley exposure. When disasters do strike, Erie's concentrated operations enable faster, more coordinated responses than nationals managing claims across fifty states. The Exchange structure also means catastrophe losses don't directly impact Erie Indemnity's profitability.

The ultimate test of Erie's moats is pricing power, and here the evidence is compelling. Despite operating in a supposedly commoditized industry, Erie maintains margins that suggest anything but commodity economics. Customers pay more for Erie policies and stay longer, generating lifetime values that justify higher acquisition costs. Agents choose to sell Erie despite having other options, creating a distribution advantage that compounds over time.

These moats—structural, operational, cultural, geographic—don't just protect Erie's current position. They create optionality for the future. The company could expand geographically, leveraging its model into new states. It could move up-market, using its service reputation to capture more commercial and high-net-worth business. It could even license its operating model to reciprocals in non-competing geographies. The moats that protect today's business enable tomorrow's opportunities.

X. Playbook: Lessons for Founders & Investors

Every business story teaches lessons, but Erie's century-long journey offers a masterclass in contrarian thinking that actually works. While Silicon Valley preaches "move fast and break things," Erie moved deliberately and fixed things. While Wall Street demands growth at any cost, Erie chose profitable growth at sustainable cost. While consultants push digital transformation, Erie pursued digital enhancement. The lessons aren't just about insurance—they're about building enduring value in any industry.

Lesson 1: Structure Is Strategy The reciprocal structure wasn't an accident or anachronism—it was a strategic masterstroke that aligned interests before "stakeholder capitalism" became fashionable. By separating ownership (the Exchange) from operations (Erie Indemnity), the founders created a system where the management company only prospers when policyholders do well. This isn't just good governance—it's a competitive advantage that compounds over time. Founders taking note: sometimes the best moat isn't technology or brand, but a structure that makes everyone root for your success.

Lesson 2: Service Excellence Is Scalable Conventional wisdom says service doesn't scale—that's why most companies abandon it as they grow. Erie proved the opposite: service excellence, properly systematized, actually becomes more powerful at scale. The key is embedding service into structure (agents compensated for retention), process (claims adjusters empowered to make decisions), and culture (hiring for empathy, not just efficiency). The lesson for founders: don't accept the false choice between scale and service. Design for both from day one.

Lesson 3: Boring Is Beautiful Erie never pivoted, never disrupted, never transformed. It sold auto insurance in 1925 and sells auto insurance in 2025. This boring consistency allowed compound improvements that flashier competitors never achieve. While others chased the next big thing, Erie perfected the current thing. For investors, this teaches patience. The best returns often come from companies doing mundane things exceptionally well, not exceptional things moderately well.

Lesson 4: Regional Dominance Beats National Mediocrity Erie could have gone national decades ago. Instead, it chose to dominate selected markets, achieving density that creates operational advantages and customer intimacy that builds switching costs. This geographic discipline requires saying no to growth opportunities that would dilute focus. The playbook: own your backyard before eyeing the neighborhood. Market share in focused geographies beats market presence across dispersed ones.

Lesson 5: Capital Allocation Is Everything The reciprocal structure created a capital-light model that generates high returns on invested capital. But Erie's leadership had to resist the temptation to lever up, make acquisitions, or chase growth that would require capital intensity. They understood that in insurance, the best risk is the one you don't take. For investors, this highlights the importance of business models that generate cash without consuming it. For founders, it emphasizes discipline over deployment.

Lesson 6: Culture Compounds Erie's culture wasn't built through offsites and consultants—it evolved through decades of consistent actions. Paying claims quickly during the Depression. Promoting women during World War II. Showing up within 48 hours after Hurricane Floyd. These actions, repeated and reinforced, created a culture that becomes self-perpetuating. New employees join because of the culture, then strengthen it through their actions. This cultural compounding is impossible to replicate quickly, making it a sustainable competitive advantage.

Lesson 7: Complexity Can Be a Moat Most businesses strive for simplicity, but Erie's byzantine structure—a public company managing a private reciprocal where customers own but don't control the entity—creates a complexity moat that protects against both competition and unwanted attention. The structure is too complicated for momentum traders, too unusual for index funds, too specialized for private equity. This complexity attracts patient capital that understands the model, creating a stable shareholder base that enables long-term thinking.

Lesson 8: The Power of Permanent Capital The Exchange structure creates essentially permanent capital—policyholders can't withdraw their surplus, can't demand dividends, can't force liquidation. This permanence allows for long-term thinking that public companies struggle to achieve. Combined with the fee model that generates predictable cash flow, Erie operates with a time horizon measured in decades, not quarters. The lesson: structure your capital to match your strategy timeline.

Lesson 9: Technology Should Enhance, Not Replace While InsurTech startups tried to eliminate agents and automate underwriting, Erie used technology to make agents more effective and underwriters more accurate. The company understood that in relationship businesses, technology should reduce friction, not replace relationships. This enhancement approach requires more nuance than disruption—you need to understand what to automate and what to preserve. But it creates sustainable advantages that pure technology plays struggle to achieve.

Lesson 10: Succession Planning Is Strategic Planning The Hirt family's multi-generational involvement wasn't nepotism—it was strategic continuity. By grooming successors through operations rather than appointing them to leadership, Erie ensured that leaders understood the business intimately. This created strategic consistency that allowed for long-term planning and cultural preservation. The lesson: succession isn't just about picking the next CEO—it's about ensuring strategic continuity across generations.

The Meta-Lesson: Patience Pays Perhaps the most important lesson from Erie's story is that patience—strategic, operational, and financial—creates value that impatience destroys. Erie waited decades to enter new states. It spent years training agents before they became profitable. It maintained service standards during recessions when cutting them would have boosted short-term profits. This patience, often mistaken for lack of ambition, created compound advantages that aggressive competitors couldn't match.

For founders, Erie's playbook suggests that the best businesses aren't always the fastest growing or most innovative. Sometimes they're the ones that pick a model, perfect it over decades, and resist the temptation to chase every opportunity. For investors, Erie demonstrates that the best returns often come from companies that seem boring on the surface but possess structural advantages that compound over time. The playbook isn't complicated—it just requires the discipline to execute it consistently for longer than anyone else is willing to wait.

XI. Bear vs. Bull Case

The Bull Case: A Perpetual Compounding Machine

The bulls see Erie as Warren Buffett's dream hiding in plain sight—a capital-light, fee-generating machine with competitive advantages that strengthen over time. Start with the economics: Erie Indemnity essentially clips a 25% coupon on a growing stream of insurance premiums without bearing insurance risk. It's like owning a toll road where traffic grows with inflation and population, except the toll rate is fixed by contract and the maintenance costs are minimal.

The reciprocal structure, far from being an archaic complexity, is actually a modern marvel of aligned incentives. No activist investor can force short-term profit maximization that hurts long-term value. No private equity firm can load it with debt and strip its assets. The structure is essentially takeover-proof, allowing management to focus on decades-long value creation rather than quarterly earnings management. This permanent capital advantage, combined with the fee model, creates predictability that investors should pay a premium for, not discount.

Geographic expansion represents a massive untapped opportunity. Erie operates in just 12 states plus D.C., leaving 38 states of virgin territory. If the company can achieve even half its current market share in these new markets, premiums could triple over the next two decades. The playbook is proven—enter a state, build agent relationships, achieve density, generate superior returns. There's no reason this can't work in Iowa or Texas or Colorado. At a 25% management fee, geographic expansion drops almost directly to Erie Indemnity's bottom line.

The digital transformation story is even more compelling. While InsurTech startups burn cash trying to rebuild insurance from scratch, Erie can selectively adopt proven technologies that enhance its existing advantages. Digital applications reduce agent paperwork. AI speeds claims processing. Telematics enables better risk pricing. Each innovation improves margins while maintaining the relationship-based model that creates switching costs. Erie gets the benefits of technology without the risks of disruption.

Climate change, paradoxically, could strengthen Erie's position. As catastrophes make insurance more expensive and complex, customers will value Erie's service excellence even more. The company's geographic footprint avoids the most dangerous zones while its concentrated operations enable superior disaster response. As marginal insurers exit catastrophe-prone markets, Erie can cherry-pick the best risks at premium prices. The Exchange structure means catastrophe losses don't directly impact Erie Indemnity, while higher premiums from increased risk directly boost management fees.

The competitive dynamics increasingly favor Erie's model. Pure digital players are struggling to achieve profitability, proving that insurance requires more than algorithms. National insurers face pressure to cut costs, reducing service quality and creating opportunities for Erie to capture dissatisfied customers. Regional players lack Erie's scale and operational excellence. The company occupies a sweet spot—big enough to invest in technology and operations, small enough to maintain service excellence, structured to align everyone's interests.

Valuation remains compelling despite the stock's strong performance. At current multiples, the market is pricing Erie like a traditional insurer despite its superior business model. The company generates returns on equity above 15% with minimal capital requirements, yet trades at valuations similar to capital-intensive insurers generating single-digit returns. As more investors understand the model, multiple expansion could drive significant returns beyond the underlying business growth.

The Bear Case: Structural Constraints and Existential Threats

The bears see a company trapped by its own structure, facing existential threats it's ill-equipped to handle. Start with the elephant in the room: Erie Indemnity has exactly one customer—the Erie Insurance Exchange. If anything happens to the Exchange, Erie Indemnity becomes worthless overnight. This isn't diversifiable risk—it's complete concentration, the kind that should terrify any rational investor.

The 25% management fee cap isn't just a ceiling—it's a straightjacket. While revenues can grow with premiums, Erie Indemnity can never capture more value, no matter how well it performs. In a world where successful companies expand margins over time, Erie is permanently capped. Worse, if regulatory scrutiny increases or the Exchange's trustees decide 25% is too high, the fee could be reduced, devastating Erie Indemnity's economics with no recourse.

Geographic expansion, touted by bulls as opportunity, is actually a trap. The states where Erie doesn't operate aren't virgin territory—they're competitive battlegrounds where entrenched players have spent decades building advantages. California has unique regulatory requirements and catastrophe exposures. Texas is dominated by State Farm and Allstate. Florida is a regulatory nightmare with hurricane risk. The easy markets were entered long ago; what's left requires massive investment for uncertain returns.

The agent model is increasingly obsolete. Millennials and Gen Z consumers don't want to visit insurance offices or develop relationships with agents—they want to buy insurance on their phones in five minutes. Every dollar Erie spends maintaining its agent network is a dollar not spent on digital capabilities. The company is essentially doubling down on a distribution model that's dying, like Blockbuster investing in better stores while Netflix was mailing DVDs.

InsurTech isn't failing—it's learning. Companies like Lemonade and Root may be struggling now, but they're gathering data, refining algorithms, and building digital-native brands that will eventually crack the code. When they do, Erie's relationship-based model will seem as quaint as travel agents booking flights. The company's measured technology adoption isn't prudent—it's falling behind in a race where winner-takes-all dynamics could emerge.

Climate change poses existential risks the bulls underestimate. While Erie avoids coastal hurricanes, it's exposed to inland flooding, severe thunderstorms, and winter storms that are becoming more frequent and severe. The Exchange bears these losses, but repeated catastrophes could impair its surplus, forcing premium increases that make Erie uncompetitive. If the Exchange shrinks, Erie Indemnity's fees shrink proportionally, with no ability to offset the decline.

The reciprocal structure, rather than providing protection, could become a liability. Regulators increasingly scrutinize complex structures that separate ownership from control. The Exchange's policyholders, who technically own the surplus but have no say in its management, could eventually demand change. A class action lawsuit challenging the fee arrangement or governance structure could unravel the entire model. The complexity that protected Erie for decades could become the weapon that destroys it.

Management succession presents unaddressed risks. The Hirt family's influence is waning, and professional managers may lack the long-term orientation that made Erie special. Without family stakes creating alignment, future executives might pursue strategies that boost short-term metrics but erode long-term value. The culture that took a century to build could dissipate in a decade under wrong leadership.

The valuation assumes perfection that reality won't deliver. The market is pricing Erie for continued growth and margin stability, but both face pressure. Premium growth requires either geographic expansion (difficult and expensive) or price increases (limited by competition). Margin improvement is capped by the fee structure. The stock's outperformance has created expectations that the business model simply can't satisfy.

XII. Epilogue: What Would You Do?

Standing at Erie's helm today, you face the strategic question that has defined the company for a century: how do you balance growth with the discipline that made growth possible? The temptation to go national must be overwhelming. Thirty-eight states await, each representing billions in potential premiums and hundreds of millions in management fees. Wall Street analysts constantly ask why you're not in California or Texas. The playbook seems obvious—just replicate what worked in Pennsylvania across America.

But then you remember H.O. Hirt's favorite word: stubbornness. Not stubbornness as obstinacy, but as commitment to principles even when abandoning them seems profitable. The question isn't whether Erie could go national, but whether it should. Would the company that enters California still be Erie, or just another national insurer that happens to have started in Pennsylvania?

The technology investment question looms equally large. Should Erie build its own InsurTech platform, competing directly with digital natives? The company certainly has the capital, and the reciprocal structure provides patient shareholders who could tolerate years of losses. Or should Erie double down on the agent model, betting that relationships will matter even more in an algorithmic world? The middle path—digital enhancement of the existing model—seems safe but might be the riskiest choice if it satisfies neither digital natives nor relationship seekers.

The reciprocal model itself faces existential questions. In a world of stakeholder capitalism and ESG investing, does a structure where policyholders own but don't control make sense? Should Erie proactively reform governance to give policyholders more voice, even if it complicates operations? Or should the company defend the current structure as a feature, not a bug—a model that enables long-term thinking precisely because it insulates management from short-term pressures?

Succession planning beyond the founding family requires delicate navigation. Should Erie seek leaders from within who understand the culture but might lack fresh perspectives? Or recruit outsiders who bring new ideas but might not appreciate what makes Erie special? The company's history suggests internal promotion, but the industry's transformation might demand external expertise. Getting this wrong could unravel a century of culture in a single CEO cycle.

The climate change response can't be delayed much longer. Should Erie use its strong balance sheet to enter catastrophe-prone markets when others retreat, capturing premium refugees from carriers abandoning Florida or California? Or should it maintain geographic discipline, accepting slower growth to avoid existential risks? The Exchange structure provides some protection, but repeated catastrophes could still impair growth for decades.

Perhaps the most profound question is whether Erie's model—built on relationships, service, and geographic concentration—can survive in a world moving toward transactions, automation, and global scale. Is Erie a relic of 20th-century American capitalism, living on borrowed time until digital disruption finally arrives? Or is it exactly what 21st-century consumers will crave—authentic, local, and human in an increasingly artificial world?

The answer might lie not in choosing between these paths but in recognizing that Erie's greatest strength has always been its ability to evolve while appearing unchanged. The company that started with hand-written policies now processes claims through mobile apps. The firm that began in one Pennsylvania city now spans a dozen states. The business that H.O. Hirt sketched on a ten-cent tablet now ranks among America's 500 largest companies.

What would you do? Perhaps the same thing Erie's leaders have done for nearly a century: move deliberately, maintain principles, serve customers exceptionally, and trust that a business model built on aligning everyone's interests will find a way forward. The specifics might change—new states entered, new technologies adopted, new products offered—but the core would remain: a reciprocal exchange where neighbors protect neighbors, managed by a company that profits only when policyholders prosper.

The Erie story isn't finished. The next chapter will be written by leaders facing choices H.O. Hirt couldn't have imagined—artificial intelligence, climate catastrophe, demographic transformation. But the principles Hirt established—stubbornness in service, alignment of interests, long-term thinking—remain as relevant as ever. In a world of quarterly capitalism and digital disruption, Erie's century-long experiment in reciprocal insurance might not just survive but thrive, proving that sometimes the oldest ideas, properly executed, are the most revolutionary of all.

The real question isn't what you would do if you ran Erie. It's whether any other model—venture-backed InsurTech, private equity rollup, or traditional public company—could have created what Erie built: a Fortune 500 company that still feels like a community institution, a public entity serving a private exchange, a 21st-century success story written in 19th-century principles. The answer, stubborn as it might seem, is probably not.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube