PI Industries: From Edible Oil to India's Agrochemical Champion

I. Introduction & Setting the Stage

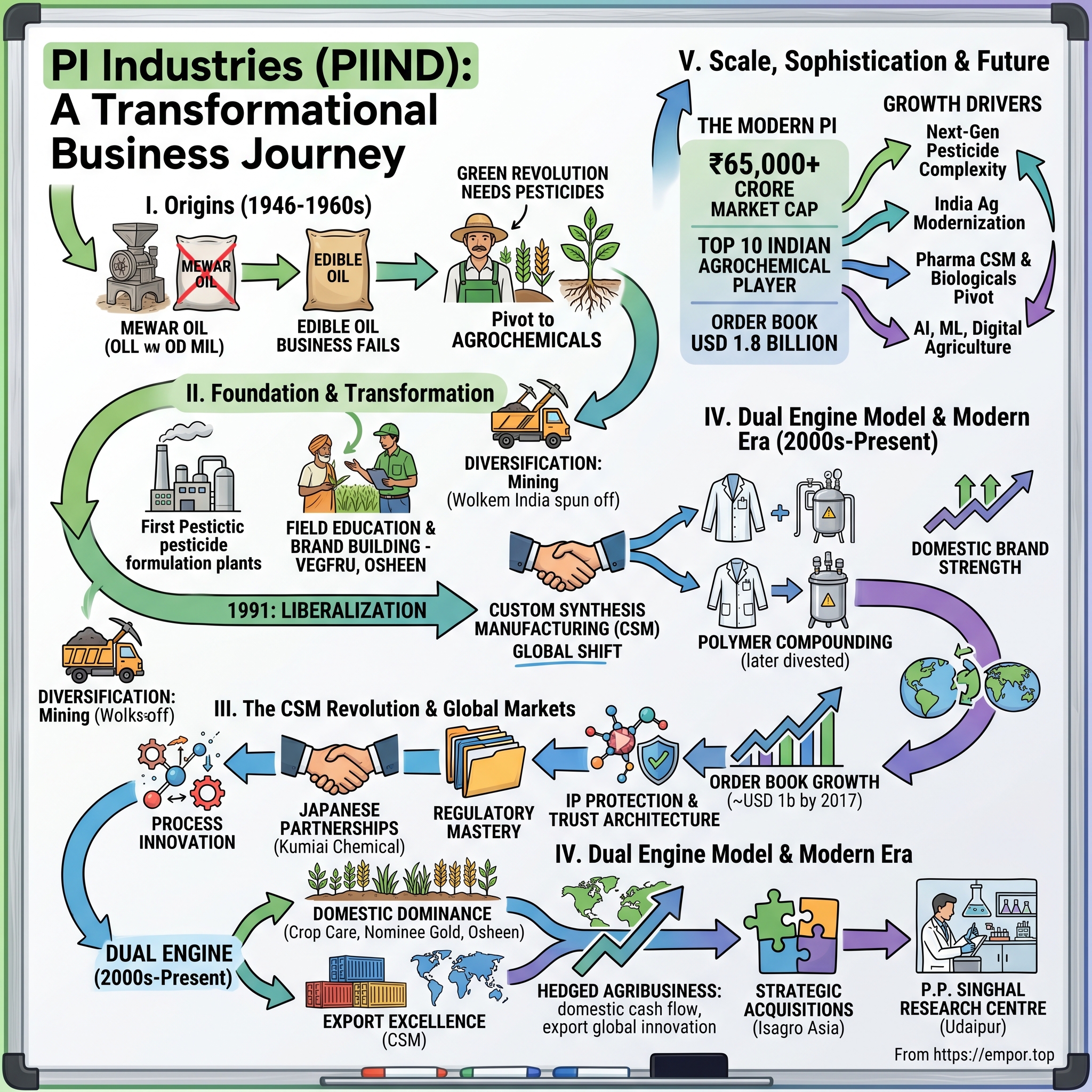

Picture this: December 31, 1946. The last day of a tumultuous year. India stands on the cusp of independence, mere months away from Partition's chaos. In the princely state of Mewar, in a modest office in Udaipur, a chemistry graduate named P.P. Singhal signs the incorporation papers for Mewar Oil & General Mills Limited. He dreams of processing edible oils, feeding a nascent nation.

He couldn't possibly imagine that his failed oil venture would transform into one of India's most sophisticated chemical companies—a ₹65,000+ crore market cap giant that today manufactures molecules so complex that global agricultural titans like Bayer and BASF entrust their most precious intellectual property to its laboratories.

This is the paradox of PI Industries: how a company that couldn't crack the edible oil business in post-independence India became the country's second-largest agrochemical player by market capitalization, with a $1.8 billion order book stretching years into the future.

Today's PI Industries operates a twin-engine model that would baffle its founder: one engine serves Indian farmers with crop protection chemicals under brands like Nominee Gold and Osheen, weathering monsoons and commodity cycles. The other engine—far more powerful—manufactures custom synthesis molecules for global innovators, operating in the rarefied world of high-pressure chemistry and multi-step synthesis where a single campaign can be worth hundreds of millions.

Why does this story matter? Because PI Industries represents something larger than quarterly earnings or market multiples. It's the story of how Indian companies learned to compete not on cost alone, but on trust, complexity, and technical sophistication. It's about how a Rajasthan-based family business cracked the code that eludes most emerging market manufacturers: becoming indispensable to the world's most demanding customers.

In an era when "China Plus One" dominates boardroom discussions and supply chain resilience has become national security, PI's journey from Udaipur's dusty lanes to Panoli's gleaming reactors offers lessons that transcend industries. This is a company that bet its future on process chemistry when product innovation seemed sexier, that chose to be the arms dealer rather than the warrior in the global agrochemical wars.

The numbers tell one story: 70+ years of evolution, 150 researchers focused exclusively on process innovation, 25.59% operating margins. But the real story lies in the decisions made in moments of crisis—when the oil business failed, when China entered the CSM market, when patents expired and opportunities emerged.

As we'll see, PI Industries isn't just about chemicals. It's about how three generations of the Singhal family navigated India's economic transformation, from License Raj to liberalization to globalization. It's about building trust so deep that companies hand over molecules worth billions in future revenues. And it's about the peculiar alchemy of turning other people's innovations into your own competitive advantage.

II. Origins: The Mewar Oil Story (1946-1960s)

The last hours of 1946 ticked away as P.P. Singhal, a 26-year-old with a master's degree in chemistry from Allahabad University, founded Mewar Oil & General Mills Limited in Udaipur. The timing wasn't coincidental—young Indians everywhere were seizing the moment, sensing that independence would create opportunities the British Raj never allowed.

Singhal chose edible oils for practical reasons. Post-war India faced chronic shortages of cooking oils. The traditional ghani mills were inefficient, and modern solvent extraction was still rare. Here was a chemist who understood both the science and the market need. The business plan seemed bulletproof.

It wasn't.

By the late 1950s, Mewar Oil was struggling. The edible oil business proved more challenging than anticipated—volatile commodity prices, intense local competition, and the peculiar dynamics of Indian food distribution networks. While giants like Hindustan Lever (now Unilever) could leverage scale and distribution, smaller players like Mewar Oil found themselves squeezed.

But P.P. Singhal possessed something rarer than business acumen: the ability to recognize failure early and pivot decisively. As the 1960s dawned, India was changing. The Green Revolution was gathering momentum. American agricultural scientist Norman Borlaug's high-yielding variety seeds were arriving in Indian fields. These miracle seeds came with a catch—they needed protection from pests and diseases that traditional varieties had naturally resisted.

Singhal saw the opportunity with a chemist's clarity. India would need pesticides—lots of them. Not the crude formulations of DDT and BHC that dominated the market, but sophisticated molecules that could protect crops without poisoning farmers. In 1960, he made the decision that would define his company's next six decades: exit edible oils, enter agrochemicals.

The company was renamed, first to Pesticides India, then simply PI Industries—a name vague enough to accommodate future pivots, specific enough to signal industrial ambition. Singhal began setting up India's first private sector pesticide formulation plants. While multinationals imported finished products and government factories produced basic chemicals, PI carved out a middle ground: formulating imported technical-grade pesticides for Indian conditions.

The context matters here. This was Nehruvian India, where the commanding heights of the economy belonged to the state. Private enterprise operated in the shadows of the License Raj, where producing an extra kilogram beyond your licensed capacity could land you in jail. Yet within these constraints, Singhal navigated brilliantly. He secured licenses, built relationships with state agriculture departments, and most importantly, began understanding the peculiar chemistry of Indian agriculture.

By the mid-1960s, PI was manufacturing its first pesticide formulations. The products were basic—organophosphates and organochlorines that would later be banned—but they worked. More importantly, Singhal insisted on something revolutionary for the time: teaching farmers how to use them safely. PI's early field officers didn't just sell pesticides; they conducted demonstrations, explained dilution ratios, and emphasized protective equipment.

This wasn't corporate social responsibility—that term didn't exist yet. It was pragmatic brand-building. Every farmer who used PI products successfully became a walking advertisement. Every village where PI's pesticides saved a crop became a loyal market.

The Green Revolution accelerated through the 1960s, and PI rode the wave. High-yielding varieties of wheat and rice spread across Punjab, Haryana, and western Uttar Pradesh. Each hectare of these new varieties needed chemical protection. The Indian pesticide market grew from virtually nothing to hundreds of crores in revenue. PI was perfectly positioned—not the largest player, but among the most technically competent.

As the 1960s ended, P.P. Singhal had successfully transformed his failed oil mill into a thriving agrochemical business. But this was just the foundation. The real transformation—from a domestic formulator to a global manufacturing partner—still lay ahead. The company had learned to walk in India's protected markets. Soon, it would need to run in the global arena.

III. Building the Foundation: Early Growth & Transformation (1960s-1990s)

The infrastructure of Indian agriculture in the 1970s was a patchwork of bullock carts and imported tractors, traditional knowledge and modern chemistry. Into this landscape, PI Industries began laying down what would become one of India's most extensive agrochemical distribution networks. But first, tragedy struck.

In 1979, P.P. Singhal died at just 59. His son Salil, trained as an engineer, suddenly found himself leading a company at a crossroads. India's pesticide market was exploding, but so was competition. Multinationals like Bayer and Ciba-Geigy (later Novartis) were entering India. Domestic players were proliferating. The easy growth of the Green Revolution's early years was ending.

Salil Singhal made a decision that would define PI's trajectory: instead of competing on price in commoditized pesticides, the company would focus on technical sophistication and brand building. The first major move was establishing India's first private-sector agrochemical technical manufacturing plant. While others imported technical-grade pesticides and simply formulated them, PI would synthesize the molecules themselves.

The distinction matters enormously. Formulation is mixing—combining active ingredients with solvents, surfactants, and stabilizers. Synthesis is chemistry—building complex molecules from simpler precursors through multi-step reactions. The technical challenges are exponentially greater, but so are the margins and competitive advantages.

Through the 1980s, PI built capabilities that seem mundane today but were revolutionary then. The company installed high-pressure reactors capable of handling dangerous chemistry. It developed analytical capabilities to ensure product purity. Most importantly, it began accumulating the tacit knowledge—the tricks of temperature control, the art of crystallization, the intuition about reaction kinetics—that separates competent manufacturers from exceptional ones.

The brand strategy proceeded in parallel. PI launched VEGFRU, targeting vegetable and fruit farmers who needed specialized pesticides. The name itself was clever marketing—easy to pronounce in Indian languages, clearly indicating its purpose. But the real innovation was the go-to-market strategy. PI's field officers didn't just visit large farmers; they conducted village-level demonstrations, creating visible proof of efficacy.

A fascinating diversification emerged during this period: mining. PI entered the business of mining and processing specialty minerals, particularly bentonite and attapulgite clays. The logic was sound—these minerals were used in pesticide formulations as carriers and stabilizers. Vertical integration would reduce costs and ensure quality. This mining division would later be spun off as Wolkem India, now a separate listed company worth thousands of crores—a reminder that not all diversifications fail.

The 1980s also saw PI's first tentative steps into international markets. The company began exporting formulated pesticides to Southeast Asia and Africa. These weren't sophisticated markets—they wanted cheap, effective products for tropical agriculture. But the export experience taught PI crucial lessons about documentation, quality standards, and the higher expectations of international customers.

Then came 1991—the year that changed everything.

India's economic liberalization didn't happen overnight on July 24, 1991, when Manmohan Singh presented his historic budget. For companies like PI, the writing had been on the wall since the balance of payments crisis began in 1990. Salil Singhal and his team spent months preparing for a new reality: foreign competition would intensify, but so would opportunities.

The company made three strategic bets that would define its next phase. First, it would enter custom synthesis manufacturing (CSM) for global agrochemical companies. Second, it would diversify into related technical fields like polymer compounding. Third, it would maintain and strengthen its domestic branded business as a hedge against global market volatility.

The CSM decision was particularly bold. In the early 1990s, global agrochemical companies did almost all their manufacturing in-house. Outsourcing critical chemistry to a third party—especially in India—seemed unthinkable. But Salil Singhal sensed a shift coming. Patent cliffs were approaching for major pesticides. Environmental regulations in developed countries were making chemical manufacturing expensive. Global companies needed partners, not just vendors.

PI's entry into CSM started modestly. The company approached Japanese firms first—they were more open to outsourcing than Western companies, and Japan's stringent quality requirements would force PI to upgrade capabilities. The early projects were simple: single-step reactions, non-critical intermediates, small volumes. But each successful delivery built trust. Each quality audit passed opened doors to more complex work.

By the mid-1990s, PI had established something unprecedented: an Indian company that global innovators trusted with their intellectual property. The Panoli facility in Gujarat became the centerpiece of this strategy—located in a well-developed chemical zone with access to raw materials and waste treatment, it signaled PI's seriousness about meeting international standards.

The polymer compounding diversification, started in the same period, seems like a distraction in hindsight. PI entered the business of creating specialized plastic compounds for automotive and electrical applications. The technology overlap with pesticides was minimal, but the quality systems and customer relationships proved valuable. This business would eventually be divested in the 2000s, but not before teaching PI important lessons about serving demanding industrial customers.

As the 1990s ended, PI Industries had transformed from a regional pesticide company into something far more complex: a domestic brand leader, an emerging custom manufacturer, and a company comfortable operating across the value chain from raw material extraction to finished product marketing. The foundation was complete. The global expansion could begin.

IV. The CSM Revolution: Entering Global Markets (Mid-1990s-2000s)

The conference room at Kumiai Chemical's Tokyo headquarters was austere—white walls, a long table, no unnecessary decoration. Across from the PI Industries delegation sat Japanese executives who had spent their careers believing that critical chemistry stayed in Japan. It was 1996, and Salil Singhal was trying to convince them otherwise.

The molecule under discussion was a rice herbicide going off-patent. Kumiai needed to cut manufacturing costs to compete with generic producers, but they couldn't compromise on quality—Japanese farmers were unforgiving about consistency. Singhal didn't pitch price. Instead, he pulled out analytical data from PI's Panoli plant showing particle size distribution, impurity profiles, and stability studies that matched Japanese specifications exactly.

"We don't want to be your vendor," Singhal said, according to executives present. "We want to be your chemistry department in India."

This framing—partnership over transaction—would become PI's CSM philosophy. While Chinese manufacturers competed aggressively on price and Western companies emphasized regulatory compliance, PI positioned itself as something different: a company that thought like an innovator but manufactured like an engineer.

The CSM business that PI entered in the mid-1990s was fundamentally different from selling pesticides to farmers. When Bayer or BASF develops a new agrochemical, they spend $250-300 million and 10-12 years bringing it to market. The molecule is their crown jewel, protected by patents and manufacturing secrets. Outsourcing production requires extraordinary trust.

PI built that trust methodically. The company established what was then rare in India: a process research center focused not on discovering new molecules but on finding better ways to make existing ones. The distinction is crucial. Product innovation asks, "What molecule will kill this pest?" Process innovation asks, "How can we make this molecule with fewer steps, higher yield, and lower environmental impact?"

By 2000, PI employed 150 researchers focused exclusively on process research. They weren't trying to out-innovate Syngenta or DuPont. They were trying to out-engineer them. A typical project would start with a customer providing a target molecule and a reference process—say, a seven-step synthesis with 40% overall yield. PI's chemists would dissect each step, looking for improvements. Could they telescope reactions, eliminating intermediate isolations? Could they replace expensive catalysts with cheaper alternatives? Could they develop crystallization conditions that avoided chromatography?

The results spoke for themselves. In one landmark project, PI reduced a nine-step synthesis to five steps, doubled the overall yield, and eliminated two chlorinated solvents that were becoming regulatory nightmares in Europe. The customer—a major European agrochemical company—shifted the entire global production to PI's Panoli facility.

But technical capability alone doesn't explain PI's CSM success. The company developed three complementary strengths that created a formidable moat.

First was regulatory mastery. As environmental regulations tightened globally, chemical manufacturing became as much about paperwork as chemistry. PI built teams that could navigate the EPA, REACH, and Japanese chemical regulations simultaneously. They maintained audit-ready documentation that satisfied the most demanding inspectors. When a customer needed rapid regulatory approval for a manufacturing site change, PI could deliver the required dossiers in weeks, not months.

Second was manufacturing flexibility. Unlike Chinese plants often designed for single products at massive scale, PI built multi-product plants (MPPs) capable of handling diverse chemistry. The same reactor train could run a Grignard reaction on Monday, a hydrogenation on Wednesday, and a diazotization on Friday. This flexibility meant customers could start with small volumes for market testing and scale up seamlessly as demand grew.

Third was intellectual property protection. In an industry paranoid about technology theft, PI developed physical and procedural safeguards that gave customers confidence. Critical process information was compartmentalized—no single employee knew the entire synthesis route. Key intermediates were code-named. Customer visits were strictly controlled. PI even developed IT systems that prevented unauthorized data transfer while allowing legitimate technical communication. The results were tangible. PI's order book rose to ~USD1b (8-9 molecules) by 2017, but the foundations were laid much earlier. By 2005, the CSM business was generating substantial revenues, though still dwarfed by the domestic operations.

The 2000-2005 period saw PI make crucial infrastructure investments. The company expanded its R&D center in Udaipur, creating dedicated synthesis laboratories where customer molecules could be developed in isolation. During the period 2005-2012, PI Industries commissioned a new manufacturing site at Jambusar, Gujarat, adding critical capacity for the growing CSM business.

One executive from this period recalled the intensity of customer audits. "A Japanese client once spent three days examining our effluent treatment plant. Not the reactors, not the quality control lab—the waste treatment. They wanted to ensure we wouldn't create an environmental incident that could damage their reputation." PI passed that audit and won a multi-year contract worth tens of millions.

The CSM business also drove a cultural transformation within PI. The domestic pesticide business operated on Indian timelines—seasonal demand, relationship-based sales, flexible deadlines. CSM clients operated on global pharmaceutical standards—batch failures meant lawsuits, delayed shipments meant plant shutdowns, quality deviations meant relationship termination.

PI adapted by creating parallel organizations. The CSM division had its own quality assurance teams trained in international standards. It had dedicated project managers who communicated in the precise, technical English that global clients expected. Most importantly, it had a zero-tolerance approach to deviations that would have seemed excessive in the domestic market but was table stakes for global competition.

By 2005, PI was manufacturing molecules so complex that even describing them required specialized notation. One product required handling phosgene, a chemical weapon from World War I that's also a critical building block for many pesticides. Another involved a Suzuki coupling, a Nobel Prize-winning reaction that requires inert atmosphere and palladium catalysts. This wasn't the simple formulation business P.P. Singhal had started—it was sophisticated chemistry that few companies globally could execute safely and economically.

The financial model of CSM was equally sophisticated. Unlike the domestic business where PI took inventory risk and seasonal variation, CSM operated on long-term contracts with take-or-pay clauses. Customers committed to minimum volumes years in advance. Pricing was formula-based, passing through raw material costs while protecting margins. Most importantly, customers often funded capacity expansion, reducing PI's capital requirements.

This model created remarkable visibility. While competitors struggled with monsoon predictions and commodity cycles, PI could forecast revenues years into the future. The order book position for the year stood at ~$1.5 billion by FY21, providing a cushion that few Indian chemical companies enjoyed.

As the 2000s progressed, PI's CSM business began attracting attention from larger players. Bayer, BASF, and DuPont—companies that had never outsourced critical chemistry to India—began exploring partnerships. Each success created a virtuous cycle: better clients meant more complex molecules, which meant higher margins, which funded better capabilities, which attracted better clients.

The transformation was complete. What had started as an opportunistic diversification in the mid-1990s had become PI's growth engine. The domestic business provided stability and cash flow. But CSM provided the future—access to global innovation, protection from local volatility, and margins that reflected genuine value addition rather than commodity trading. The student had become the master, and PI was ready to scale heights that its founder could never have imagined.

V. Dual Engine Model: Domestic Dominance & Export Excellence (2000s-2015)

The monsoon of 2009 failed spectacularly. India's rainfall deficit reached 23%, the worst in four decades. Agriculture Minister Sharad Pawar declared it a "drought-like situation." For most agrochemical companies, this spelled disaster—farmers don't buy pesticides for crops they don't plant.

At PI Industries' headquarters, executives watched their domestic revenues crater. But in the same quarter, the CSM division posted record growth. A new molecule for a European client had entered commercial production, generating margins that offset the entire domestic decline. The dual-engine model wasn't just theory—it was salvation.

This period crystallized PI's unique position in global agrochemicals: neither purely domestic nor purely export-focused, but something more sophisticated—an integrated model where capabilities, relationships, and cash flows reinforced each other across businesses.

The domestic business, far from being a legacy burden, had evolved into a sophisticated operation. The CSM business accounted for 82 per cent of the company's Q3FY23 revenue, but this statistic obscures the domestic division's strategic importance. It provided three critical advantages that pure CSM players lacked.

First, it generated stable cash flows during CSM investment cycles. Building a multi-product plant could take 18-24 months with no revenue. The domestic business funded these investments without diluting equity or taking excessive debt.

Second, it provided real-world testing grounds for process improvements. When PI developed a new crystallization technique for a CSM client, they could validate it on domestic products first. Failures were learning opportunities, not client relationship disasters.

Third, and most subtly, it gave PI credibility with global innovators. A company that successfully marketed pesticides to millions of Indian farmers understood agriculture in ways that pure contract manufacturers never could. When Bayer or BASF discussed market strategy, PI could contribute insights, not just manufacturing capacity.

The domestic portfolio reflected this sophistication. Nominee Gold, a herbicide for rice, became a blockbuster by solving a specific problem: controlling weeds in direct-seeded rice, a water-saving technique gaining popularity as groundwater depleted. The product wasn't just chemistry—it was agricultural insight translated into molecular form. Indeed, in the last five years, two of the company's products - the herbicide Nominee Gold, and the insecticide Osheen, both of them for paddy - have proved blockbusters, making, as analysts estimate, at least Rs 100 crore in revenue. These weren't just products; they were precision tools for Indian agriculture's evolving needs.

Osheen, an insecticide for brown planthopper in rice, succeeded through timing as much as chemistry. PI launched it just as pest resistance to older insecticides was becoming critical. But the real innovation was the formulation—a suspension concentrate that mixed easily in water and adhered to rice leaves even after rain. Farmers noticed the difference. Word spread through WhatsApp groups and village meetings faster than any advertising campaign.

The domestic business operated through a distribution architecture that took decades to build. PI didn't just sell to dealers; it created a three-tier system. At the top were distributors who managed inventory and credit. Below them were dealers who knew local cropping patterns. At the ground level were PI's own field officers who conducted demonstrations and gathered market intelligence.

This network became a competitive moat. When a new pest outbreak occurred, PI's field officers reported it within days. When farmers complained about product performance, the feedback reached R&D within weeks. This real-time market sensing allowed PI to adjust formulations, launch targeted products, and build trust that advertising couldn't buy.

Meanwhile, the CSM business was scaling dramatically. The company, with revenue of Rs 2,137 crore and profit after tax of Rs 243 crore in 2014/15, has two distinct product streams: first, a range of plant protectors and plant nutrients, including pesticides, for the domestic market, and second, custom synthesis and manufacturing (CSM) of agri-chemicals for specific global companies, all overseas. The CSM business made up 55% of revenue in 2014/15 with $650 million order book, providing an enduring cushion against monsoon vagaries.

The CSM client list read like a who's who of global agrochemicals. Bayer AG entrusted PI with manufacturing a next-generation insecticide that required handling hydrogen cyanide. BASF SE partnered for a fungicide involving multiple chiral centers—molecular handedness that made synthesis exponentially complex. DuPont (later Corteva) outsourced production of a herbicide safener, a molecule that protects crops from herbicide damage.

But the deepest relationships were with Japanese companies. Kumiai Chemical Industry didn't just give PI manufacturing contracts; they created joint ventures. Ihara Chemical Industry shared not just molecules but process knowledge. These partnerships reflected Japanese business philosophy—long-term relationships over transactional efficiency.

The economics of these relationships were compelling. A typical CSM contract might run for 5-7 years with minimum volume commitments. Pricing formulas passed through 60-70% of raw material cost changes, protecting margins while sharing commodity risk. Most importantly, once PI began manufacturing a molecule, switching costs for the client were enormous—requalifying a new manufacturer could take years and millions in regulatory costs.

This stickiness created extraordinary revenue visibility. While domestic competitors scrambled to predict next season's demand, PI could forecast CSM revenues years ahead. The order book became a buffer, smoothing earnings through agricultural cycles.

The integration between domestic and export businesses went beyond financial hedging. When PI developed a new reaction for a CSM client—say, a selective bromination technique—the knowledge enhanced domestic manufacturing. When domestic R&D created a novel formulation technology, it became a selling point for CSM clients considering PI for new projects.

On 9 May 2017, PI Industries and BASF announced a strategic partnership to offer farmers in India a broader portfolio of crop protection solutions. This wasn't just distribution—it was co-creation. PI would market BASF's innovative fungicide technologies while contributing local market knowledge to optimize formulations.

The joint venture with Kumiai Chemical on 22 June 2017 went even further. The companies established a manufacturing facility specifically for Bispyribac Sodium, the active ingredient in Nominee Gold. This vertical integration secured supply while giving Kumiai access to Indian markets through PI's distribution network.

By 2015, PI Industries had achieved something remarkable: a business model that was both hedged and leveraged. Hedged against local volatility through global revenues. Leveraged through capabilities that reinforced across businesses. The dual engines weren't just running in parallel—they were powering each other, creating momentum that neither could achieve alone.

VI. Scale & Sophistication: The Modern Era (2015-Present)

The boardroom at PI Industries' Mumbai office buzzed with nervous energy in early 2017. Across the table sat executives from Kumiai Chemical, and the stakes couldn't be higher. They weren't discussing another supply contract or technology transfer. They were negotiating a joint venture that would fundamentally alter PI's position in the global agrochemical value chain.

"We don't want to be your manufacturer," Mayank Singhal, who had taken over day-to-day operations from his father Salil, reportedly said. "We want to be your partner in creating the future of Indian agriculture."

The joint venture, announced on June 22, 2017, established a dedicated facility to manufacture Bispyribac Sodium. But this was more than backward integration. It signaled PI's evolution from contract manufacturer to strategic partner, from order-taker to value co-creator. The Isagro Asia acquisition, completed in December 2019, exemplified this new strategic posture. PI executed an offer with Isagro S.p.A for acquisition of the business of Isagro Asia through acquisition of 100% shareholding for a consideration of Rs 345 crore. The transaction value was estimated Rs 345 crore net of cash and debt subject to closing adjustments. The total transaction value of acquisition was Rs 4432 million and Isagro Asia had a 30 Acre manufacturing site including production plants for agrochemical technical and formulations adjacent to Company's existing manufacturing unit in Panoli (Gujarat).

This wasn't just capacity addition. Isagro brought proprietary molecules, established customer relationships, and most importantly, a manufacturing site adjacent to PI's existing Panoli facility. The synergies were immediate—shared utilities, combined effluent treatment, coordinated logistics. But the strategic value ran deeper. PI could now offer global clients an integrated manufacturing campus capable of handling everything from early-stage development to commercial production at massive scale.

The integration proceeded with surgical precision. The process for eventual structuring and integration of the acquired entity was underway, the leadership roles and organization structures were clearly defined and a global consulting firm was already on board to support the integration process. PI retained Isagro's technical talent while implementing its own quality systems. Customer contracts were honored while being gradually integrated into PI's broader portfolio. Within months, the combined entity was operating more efficiently than either had individually.

Meanwhile, the CSM business was reaching unprecedented scale. The order book position for the year stood at ~$1.5 billion in FY21. By Q1FY24, this had grown further to USD 1.8 billion, providing multi-year revenue visibility that few chemical companies globally could match.

The nature of CSM projects was evolving too. Early contracts involved straightforward chemistry—esterifications, chlorinations, basic heterocycle formation. By 2020, PI was handling molecules that pushed the boundaries of synthetic chemistry. One project required enzymatic resolution to separate mirror-image molecules. Another involved photochemistry, using light to drive reactions impossible through conventional heating. A third required handling organolithium reagents at -78°C, chemistry so sensitive that moisture from breath could cause explosions.

This technical sophistication enabled PI to move up the value chain. Instead of competing for commodity intermediates where Chinese manufacturers dominated, PI focused on late-stage intermediates and active ingredients where quality, reliability, and intellectual property protection mattered more than price.

The digital transformation accelerated during this period. PI implemented SAP across operations, creating real-time visibility from raw material procurement to finished product delivery. But the real innovation was in process control. The company installed distributed control systems (DCS) in new plants, allowing operators to monitor and adjust hundreds of parameters simultaneously. Reactions that once required round-the-clock manual monitoring could now run with minimal supervision, improving both safety and consistency.

The domestic business, far from being neglected, underwent its own transformation. In 2017-18, PI Industries simultaneously launched 5 new generation products for the first time. These weren't me-too generics but differentiated formulations addressing specific Indian agricultural challenges.

The company also entered mechanized spray machines in 2017, recognizing that labor shortage was becoming critical in Indian agriculture. These weren't just imported machines but solutions adapted for Indian conditions—smaller turning radius for fragmented fields, higher ground clearance for flooded paddy, simplified controls for operators with limited technical training. The partnership ecosystem expanded strategically. PI Industries and Mitsui Chemicals Agro Inc (MCAG) jointly announced to have entered into an agreement to establish a joint venture company in India. The JV, to be named Solinnos Agro Sciences Pvt Ltd, will provide registration services for Mitsui Chemicals Agro's proprietary agrochemicals. Mitsui Chemicals Agro held 51 percent stake in Solinnos Agro Sciences (headquartered at Gurgaon (Haryana), while remaining stake was held by PI Industries.

This wasn't just about registration—it was about creating a pipeline of next-generation molecules for Indian agriculture. Each partner brought complementary strengths: PI's regulatory expertise and distribution network, Mitsui's innovative chemistry and global perspective.

The capital markets took notice. In July 2020, PI raised Rs 20,000 million through a Qualified Institutional Placement (QIP) of equity shares, issuing 13,605,442 equity shares at Rs 1,470 per share. The raise was oversubscribed multiple times, with global investors recognizing PI's unique positioning in the CSM value chain.

The funds enabled aggressive expansion. PI commissioned MPP 11, established PI Enzachem Private Limited and PI Fermachem Private Limited as new subsidiaries, and most significantly, founded the P.P. Singhal Research Centre in Udaipur—a state-of-the-art facility focused on next-generation process chemistry.

FY24 performance reflected this transformation: Sales of ₹7,666 crores from ₹6,492 crores in FY23, net profit of ₹1,682 crores. But more importantly, operating margins at 25.59% in FY24 demonstrated that PI had successfully moved up the value chain. These weren't commodity chemical margins—they were innovation premiums.

The company's approach to sustainability evolved from compliance to competitive advantage. PI began tracking Eco Scale scores for all processes, quantifying environmental impact alongside economic returns. Solar installations across facilities contributed 6.60% of total energy use. Water recycling systems achieved near-zero liquid discharge. These weren't just CSR initiatives—they were customer requirements, particularly from European clients facing stringent environmental regulations.

Digital transformation accelerated with SAP HANA implementation, creating end-to-end visibility across the value chain. But the real innovation was in process analytics. PI began using machine learning to optimize reaction conditions, analyzing thousands of variables to identify patterns human chemists might miss. One algorithm identified a correlation between trace impurities and catalyst deactivation, extending catalyst life by 40% and saving millions in operational costs.

The modern PI Industries operates at a scale and sophistication unimaginable when P.P. Singhal founded Mewar Oil. The company maintains relationships with virtually every major agrochemical innovator globally. Its order book provides visibility years into the future. Its technical capabilities rival any global CSM player. Yet at its core, PI remains what it has always been—a company that transforms other people's innovations into commercial reality, creating value through execution excellence rather than invention alone.

VII. The CSM Moat: Chemistry, Trust & Complexity

In the pristine cleanroom of PI's analytical laboratory in Panoli, a young chemist peers at an HPLC chromatogram showing peaks separated by mere seconds. She's analyzing an intermediate for a molecule so new it doesn't yet have a common name—just an alphanumeric code known to fewer than fifty people globally. The purity requirement is 99.95%. She achieves 99.97%.

This scene—repeated hundreds of times daily across PI's facilities—illustrates the true moat in CSM: not the ability to make molecules, but the ability to make them consistently, safely, and with a level of quality that satisfies the world's most demanding customers.

The global CSM market, valued at $271.33 billion in 2022 and expected to reach $474.94 billion by 2028, attracts hundreds of players. Chinese companies offer rock-bottom prices. Western firms provide regulatory expertise. Indian competitors tout cost advantages. Yet PI has carved out a unique position through three interlocking advantages that create a moat wider than any single capability.

First is technical complexity. PI specializes in molecules that make other manufacturers pause. Multi-step syntheses involving hazardous chemistry—organometallics, high-pressure hydrogenations, reactions with toxic gases. The company's comprehensive CSM solutions include process R&D, analytical method development, synthesis of reference standards, impurity synthesis, scale-up studies, safety data generation, process engineering, and commercial production.

Consider a recent project: synthesizing an insecticide intermediate requiring a Friedel-Crafts acylation followed by a Wolff-Kishner reduction, then a diazotization, and finally a Sandmeyer reaction. Each step has multiple failure modes. The Friedel-Crafts can polymerize. The Wolff-Kishner requires temperatures that decompose the product. The diazotization creates explosive intermediates. The Sandmeyer needs precise temperature control or yields plummet.

PI's process chemists didn't just execute this synthesis—they redesigned it. They developed a telescoped process eliminating two isolations, replaced the Wolff-Kishner with a safer catalytic hydrogenation, and optimized the Sandmeyer to run at ambient temperature. The result: 70% overall yield versus 35% for the reference process, two fewer unit operations, and elimination of hydrazine, a suspected carcinogen.

This technical sophistication creates switching costs that lock in customers. Once a process is validated and filed with regulators, changing manufacturers requires extensive requalification—new impurity profiles, stability studies, bioequivalence testing. For a blockbuster pesticide, this could cost $10-20 million and delay market entry by years.

The second moat is trust architecture. In CSM, clients share their most valuable assets—molecules representing hundreds of millions in R&D investment. A security breach or intellectual property theft could destroy competitive advantage overnight.

PI has built trust through radical transparency combined with bulletproof security. Clients can audit any aspect of operations with 48 hours notice. Real-time dashboards show production status, quality metrics, and inventory levels. Yet simultaneously, the company maintains compartmentalization that would impress intelligence agencies. Project teams sign additional NDAs. Key intermediates use code names. Customer zones in R&D require biometric access. Even senior management doesn't know all customer projects.

One Japanese client tested this system by deliberately leaving confidential documents in a conference room. When a PI employee found them, they were immediately sealed, logged, and returned unopened—exactly following protocol. That client later awarded PI their largest ever CSM contract.

The third moat is manufacturing flexibility that seems paradoxical—plants designed for everything, optimized for nothing, yet more efficient than specialized facilities. PI's multi-product plants (MPPs) can switch between products in days, not weeks. The same reactor that runs an atmospheric pressure esterification on Monday handles a high-pressure hydrogenation on Thursday.

This flexibility requires sophisticated engineering. Reactors use glass-lining to handle both acids and bases. Piping systems allow multiple configuration without cross-contamination. Automation systems can implement entirely different control strategies at the push of a button. The capital cost is higher than single-product plants, but utilization rates approach 90% versus industry averages of 60-70%.

The de-risked business model provides healthy revenue visibility and stable profitability that few chemical companies achieve. Long-term contracts with take-or-pay clauses ensure minimum utilization. Quarterly price adjustments pass through raw material volatility. Most importantly, PI typically doesn't compete on price—clients choose them for reliability, quality, and speed to market.

The trust equation in CSM is beautifully complex. Global innovators like Bayer or Syngenta spend $250-300 million developing a new pesticide. By the time they approach PI for manufacturing, they've invested too much to risk failure. They need a partner who can deliver exactly what's promised, when promised, at the quality promised. No excuses, no delays, no surprises.

PI delivers this through what they call "customer intimacy"—understanding not just the chemistry but the business context. When a client needs accelerated delivery for a product launch, PI runs 24/7 operations. When regulatory requirements change, PI's teams work alongside client's regulatory affairs to update dossiers. When a competitor's patent challenge threatens market position, PI develops non-infringing processes.

This intimacy extends to innovation. PI's process researchers don't just optimize existing routes—they propose alternatives. For one fungicide, PI suggested replacing a palladium-catalyzed coupling with a copper-catalyzed version, reducing catalyst cost by 95%. For an herbicide, they developed a biocatalytic step replacing three chemical transformations. These innovations become joint intellectual property, aligning incentives for long-term partnership.

The regulatory mastery adds another layer to the moat. PI maintains teams specialized in different regulatory regimes—EPA for the US, REACH for Europe, PMDA for Japan, CIBRC for India. They understand not just current requirements but anticipated changes. When the EU proposed restrictions on certain solvents, PI proactively developed alternative processes for affected products, ensuring uninterrupted supply while competitors scrambled to comply.

Risk mitigation through diversification prevents single points of failure. No single customer represents more than 15% of CSM revenue. No single product exceeds 10%. The portfolio spans insecticides, herbicides, fungicides, and plant growth regulators. If one segment faces pressure, others compensate.

The financial implications are compelling. CSM generates returns on capital employed exceeding 25%, far above the chemical industry average of 10-12%. The order book provides 3-4 years of revenue visibility, enabling confident capacity planning. Most remarkably, PI achieves these returns while maintaining net cash positions—growth funded through operations, not leverage.

As one industry executive noted, "Anyone can build reactors. Many can handle complex chemistry. Some can meet regulatory requirements. Very few can do all three while maintaining the trust of companies betting billions on their molecules. That's PI's real moat—not any single capability, but the integration of all of them into something irreplaceable."

VIII. Business Model Analysis & Unit Economics

The conference call in Q2 FY2023 began with an analyst's pointed question: "Your CSM margins have expanded 300 basis points year-over-year while raw material costs increased. How is this possible?" Mayank Singhal's response revealed the economic engine that powers PI Industries: "We don't sell chemicals. We sell certainty."

This distinction—between commodity manufacturing and value creation—defines PI's unit economics. While competitors focus on cost-plus pricing, PI has built a business model that captures value far exceeding production costs.

The revenue architecture tells the story. The CSM business accounted for 82 per cent of the company's Q3FY23 revenue. Even as overall revenue saw a growth of 19 per cent, the CSM business, or the export segment, grew by a strong 23 per cent over the year-ago period. But the real insight lies in the composition of that revenue.

A typical CSM contract with PI follows a predictable lifecycle. Year 1-2: Process development, where PI invests R&D resources to optimize the client's route. The client pays milestone payments covering costs but generating minimal profit. Year 3-4: Validation batches and regulatory filing, where margins begin expanding as PI's process improvements reduce manufacturing costs. Year 5+: Commercial production, where margins peak as volumes scale and processes are fully optimized.

This lifecycle creates a compounding effect. At any given time, PI has projects across all stages. New projects consume R&D resources but promise future returns. Validation projects generate moderate margins while de-risking commercial production. Mature projects throw off cash that funds new investments. The portfolio effect smooths earnings while continuously improving margins.

The capital allocation framework reflects sophisticated financial engineering. PI typically invests 4-5% of revenue in R&D, but the returns are asymmetric. A successful process optimization might reduce manufacturing costs by 30-40%, savings shared with clients but improving PI's margins by 500-1000 basis points on that product.

Manufacturing capacity investments follow a different logic. When clients commit to long-term contracts, they often provide advance payments or equipment financing. PI might invest ₹100 crores in a new MPP, but ₹30-40 crores comes from client advances, reducing PI's capital at risk. The plant generates returns on the full investment, but PI only funds 60-70% of it.

Working capital management in CSM differs fundamentally from typical chemical operations. Raw materials are often procured on back-to-back arrangements with clients—PI doesn't take commodity risk. Finished goods inventory is minimal since production follows confirmed orders. The cash conversion cycle in CSM averages 60-70 days versus 120+ days in domestic agrochemicals.

The high points of recent times for PI Industries have been the setting up of two new plants in September and December 2015, both at Jambusar, Gujarat, demonstrating the company's capital deployment discipline. These weren't speculative investments but capacity expansions backed by confirmed order books.

The domestic business operates on entirely different economics but provides crucial portfolio benefits. The company, with revenue of Rs 2,137 crore and profit after tax of Rs 243 crore in 2014/15, has two distinct product streams: first, a range of plant protectors and plant nutrients, including pesticides, for the domestic market, and second, custom synthesis and manufacturing (CSM) of agri-chemicals for specific global companies, all overseas.

Domestic agrochemicals generate gross margins of 40-45% but require significant distribution costs. The net margins of 15-18% seem pedestrian compared to CSM. However, the domestic business provides three economic advantages that pure-play CSM companies lack:

First, cash flow timing. Domestic sales generate cash year-round, while CSM revenues can be lumpy based on campaign schedules. This smooths working capital requirements and reduces reliance on external financing.

Second, operating leverage. Fixed costs like corporate overhead, regulatory compliance, and senior management are spread across a larger revenue base. This improves overall margins by 200-300 basis points.

Third, risk mitigation. When global agrochemical demand softened in 2015-2016, PI's domestic business provided stability. Indeed, in the last five years, two of the company's products - the herbicide Nominee Gold, and the insecticide Osheen, both of them for paddy - have proved blockbusters, making, as analysts estimate, at least Rs 100 crore in revenue.

The integrated model creates synergies beyond financial metrics. When PI develops a cost-effective synthesis route for a CSM client, the knowledge often applies to domestic products. When domestic R&D creates a novel formulation technology, it becomes a selling point for CSM customers. This knowledge spillover is impossible to quantify but clearly valuable.

Partnership economics deserve special attention. Unlike typical vendor relationships where price is continuously negotiated, PI's partnerships often span 5-10 years with predetermined pricing formulas. A typical formula might be: Manufacturing Cost + 25% margin + 50% of any cost savings achieved. This aligns incentives—PI profits from efficiency improvements while clients benefit from lower costs.

The in-licensing model for domestic products follows similar logic. PI licenses molecules from global innovators for Indian markets, paying royalties on sales. But PI handles all regulatory approval, manufacturing, and distribution. The innovator gets market access without infrastructure investment. PI gets proven products without R&D risk. Both parties win.

Risk mitigation through diversification shows up in the numbers. Customer concentration is manageable—the top 10 clients represent less than 60% of CSM revenue. Product diversification is even better—no single molecule exceeds 8% of total revenue. Geographic diversification provides another buffer—exports span 30+ countries across regulatory regimes.

The financial metrics validate the model. Company has delivered good profit growth of 29.5% CAGR over last 5 years Operating margins consistently exceed 20%, reaching 25.59% in FY24. Return on equity hovers around 25-30%, exceptional for a manufacturing business. Most impressively, PI achieves these returns while maintaining conservative leverage—debt-to-equity rarely exceeds 0.3x.

The reinvestment economics are particularly attractive. Unlike industries requiring constant capital expenditure just to maintain position, PI's investments directly drive growth. Each new MPP enables ₹200-300 crores in incremental revenue at 25%+ margins. Each R&D project that succeeds generates returns for 5-10 years. This creates a compounding machine where today's profits fund tomorrow's growth.

The unit economics tell a simple story: PI has structured its business to capture value at every stage of the agrochemical value chain. From process development through commercial manufacturing, from domestic distribution through global partnerships, each activity reinforces others while generating attractive standalone returns. It's not just a business model—it's an economic ecosystem where the whole consistently exceeds the sum of its parts.

IX. Competitive Landscape & Market Position

The global agrochemical CSM industry resembles a chess match where players compete on multiple boards simultaneously. Chinese manufacturers dominate volume. Western companies control innovation. Indian players navigate between them, seeking profitable niches. In this complex game, PI Industries has achieved something remarkable: competing effectively against all three groups while avoiding direct confrontation with any.

Market Cap ₹ 58,524 Cr. places PI as India's second-largest agrochemical company by market capitalization, but this understates its unique position. Unlike UPL, which grew through global acquisitions, or Rallis, which leverages Tata Group backing, PI built its position through organic growth and technical excellence.

The domestic competitive landscape reveals PI's strategic positioning. UPL, with revenues exceeding ₹50,000 crores, operates at a different scale—a global giant competing with Bayer and Syngenta. But UPL's size comes with complexity—integrating acquisitions, managing debt, navigating diverse markets. PI's focused approach generates superior returns on capital despite smaller absolute scale.

Rallis India, backed by Tata Chemicals, represents a different competitive threat. With similar revenues to PI but lower margins, Rallis competes aggressively on price in commodity segments. PI sidesteps this competition by focusing on differentiated products and technical segments where price isn't the primary decision factor.

Dhanuka Agritech and Insecticides India represent the broader domestic industry—hundreds of players competing in generic formulations. These companies operate on 10-12% margins, rely heavily on monsoons, and face constant price pressure. PI's branded products compete in this market but from a position of technical superiority, not cost leadership.

The real competition comes from global CSM players, particularly Chinese manufacturers. Companies like Shandong Weifang Rainbow and Nantong Jiangshan Agrochemical operate at massive scale with cost advantages PI can't match. A synthesis requiring 10 steps might cost 30% less in China due to cheaper raw materials and less stringent environmental compliance.

PI doesn't try to match Chinese pricing. Instead, it competes on dimensions where China struggles. Intellectual property protection remains problematic in China despite improvements. Regulatory compliance, particularly for European and American markets, requires documentation and transparency that many Chinese firms can't provide. Most importantly, the geopolitical tensions accelerated by COVID-19 have made many Western companies eager to diversify away from China.

PI has positioned itself as the primary beneficiary of "China Plus One" strategies. When Bayer or BASF wants to reduce Chinese exposure, PI offers a compelling alternative—costs higher than China but lower than the West, quality matching global standards, IP protection rivaling developed markets, and regulatory expertise spanning multiple jurisdictions.

The competitive advantages compound. PI Industries is still well behind market leader United Phosphorus Ltd (UPL) in revenues, but that does not bother Singhal. "Competing on top line is not my approach," he says. "Excellence is what I care about." He notes that PI Industries' price-earnings ratio and operating profit are comparable to those of the top players in the industry and indeed surpass some of them.

Process expertise stands as the first major advantage. While competitors might execute a client's process as provided, PI reimagines it. This isn't just optimization—it's fundamental redesign using different chemistry, alternative raw materials, or novel techniques. When successful, these innovations create switching costs that lock in relationships for decades.

Regulatory knowledge provides another edge. PI maintains regulatory teams that understand not just current requirements but regulatory trends. When the EU began restricting endocrine disruptors, PI preemptively identified affected molecules and developed compliance strategies. Competitors reacted; PI anticipated.

Client relationships, built over decades, create perhaps the strongest advantage. Trust in CSM isn't earned through presentations or proposals—it's built through years of consistent delivery. When a Japanese client has worked with PI for 20 years without a single major quality deviation, switching to save 10% makes no sense.

The market dynamics favor PI's positioning. The global CSM market expected to grow at CAGR of approximately 10% during 2023-2028 reflects multiple tailwinds. Patent cliffs create opportunities as originators seek cost reduction. Regulatory pressures in developed markets drive outsourcing. Increasing molecular complexity favors technically sophisticated manufacturers.

PI's market position as one of top 10 domestic players understates its global relevance. In the specialized world of agrochemical CSM, PI ranks among the top 5 globally by number of innovator relationships. More importantly, PI is often the primary or sole manufacturer for critical molecules, giving it influence far exceeding its market share.

The competitive threats are real but manageable. Chinese players will continue offering lower prices, but PI doesn't compete on price. Indian competitors might copy PI's model, but building technical capabilities and client trust takes decades. Western companies could in-source manufacturing, but the economics no longer work with their cost structures.

New threats emerge from unexpected directions. CDMOs (Contract Development and Manufacturing Organizations) from pharma are entering agrochemicals, attracted by similar chemistry and better margins. Technology companies propose AI-driven process optimization that could commoditize PI's expertise. Sustainability requirements might favor bio-based pesticides over synthetic chemistry.

PI's response reveals strategic sophistication. The company partners with potential disruptors rather than competing. It collaborates with AI companies to enhance its own process development. It invests in biological pesticides while maintaining chemical expertise. It turns threats into opportunities through adaptation rather than resistance.

The competitive moat continues widening. Each successful project adds to PI's reputation. Each client relationship deepens switching costs. Each process innovation extends technical leadership. Each regulatory approval raises entry barriers. The competitive landscape isn't static—it's a dynamic system where PI's advantages compound over time.

Market position ultimately reflects more than market share or revenue rankings. It's about strategic positioning in value chains, relationship depth with key stakeholders, and ability to capture value from industry transitions. By these measures, PI Industries hasn't just achieved strong market position—it's created a unique strategic space where it faces limited direct competition while maintaining multiple growth vectors.

X. Growth Drivers & Future Trajectory

Standing in PI's newly commissioned MPP-11 facility in Jambusar, you can almost hear the future humming through the gleaming reactors. This isn't just another manufacturing plant—it's a physical manifestation of where PI Industries is heading: larger scale, greater complexity, deeper integration with global innovation cycles.

The company targets 18% to 20% revenue growth, but the real story isn't the growth rate—it's the multiple engines driving it. Each growth vector reinforces others, creating momentum that transcends individual market cycles.

The CSM market tailwinds are hurricane-force. The order book position for the year stood at ~$1.5 billion. Patent cliffs approaching for major pesticides worth $15+ billion in annual sales create immediate opportunities. As these molecules lose patent protection, originators need cost-competitive manufacturing to compete with generics. PI's established relationships position it as the natural partner for these transitions.

But the real CSM opportunity lies in complexity escalation. Next-generation pesticides aren't just molecules—they're molecular systems. Binary mixtures where components must be manufactured in precise ratios. Controlled-release formulations requiring specialized encapsulation. Biological-chemical hybrids combining synthetic molecules with microbial agents. Each innovation increases manufacturing complexity, widening the moat between sophisticated players like PI and commodity manufacturers.

The outsourcing megatrend accelerates regardless of economic cycles. Global agrochemical companies face a stark reality: maintaining chemical manufacturing infrastructure in developed markets is economically unviable. Environmental compliance costs escalate annually. Chemical engineering talent gravitates toward tech and pharma. Communities resist chemical plants. The choice isn't whether to outsource, but to whom.

PI's positioning for this transition is nearly perfect. Unlike pure-play CDMOs that might optimize for any given client, PI understands agriculture. When a client discusses formulation challenges in tropical climates, PI contributes insights from decades of serving Indian farmers. This domain expertise plus manufacturing excellence creates value beyond simple cost arbitrage.

Domestic growth vectors operate on different dynamics but equal promise. India's agricultural transformation—from subsistence to commercial, from traditional to scientific, from volume to value—creates continuous opportunities. As farmers shift from flooding fields with cheap pesticides to precise application of sophisticated molecules, PI's premium positioning pays dividends.

Product launches accelerate. In 2024, Company launched six new products namely Eketsu, Claret, Aminogrow, Kadett, PB Knot, PIILIN. It commercialized 6 new molecules during the year, including Electronic and Performance Chemicals. Each launch isn't just a new SKU—it's a solution to specific agricultural challenges. Eketsu strengthens PI's rice herbicide portfolio. Claret addresses emerging pest resistance. These targeted innovations command premium pricing while building farmer loyalty.

Market penetration remains nascent despite PI's 70-year history. India uses 0.6 kg of pesticides per hectare versus 13 kg in China and 5 kg in Brazil. This isn't about flooding fields with chemicals—it's about scientific application of appropriate products. As Indian agriculture modernizes, pesticide intensity will increase, but toward sophisticated, targeted products where PI excels.

The premiumization trend favors PI's positioning. Farmers increasingly understand that spending ₹200 more per acre on better pesticides can increase yields worth ₹2,000. This value-over-volume shift plays to PI's strengths—technical superiority, brand trust, and solution-oriented approach.

New ventures expand the growth horizon. PI's entry into pharma CSM leverages similar chemistry with different applications. The pharma opportunity is massive—the global pharma CDMO market exceeds $150 billion, dwarfing agrochemical CSM. PI won't become a pharma giant overnight, but capturing even 0.1% market share would double current revenues.

The biological pesticides pivot represents another growth frontier. As regulatory pressures mount and consumer preferences shift, biological alternatives gain traction. PI's approach is pragmatic—not abandoning chemical expertise but augmenting it with biological capabilities. The future might be integrated pest management combining chemicals, biologicals, and digital monitoring.

Technology integration multiplies growth potential. AI/ML in molecule discovery isn't science fiction—it's happening now. PI collaborates with computational chemistry companies to identify promising molecules faster than traditional screening. Digital agriculture creates new business models—subscription services for pest prediction, precision application protocols, outcome-based pricing.

ESG considerations transform from compliance burden to competitive advantage. European customers increasingly demand suppliers with verified sustainability credentials. PI's investments in renewable energy, water recycling, and green chemistry position it as a preferred partner for ESG-conscious clients.

Geographic expansion offers untapped potential. While PI exports globally, direct presence remains limited to India. Establishing manufacturing in other emerging markets—Vietnam, Brazil, Turkey—could replicate the India success story. Each geography offers unique opportunities while diversifying regulatory and market risks.

The capital allocation framework supports aggressive growth. With minimal debt and strong cash generation, PI can fund expansion without diluting returns. The company invests 15-18% of revenue in capex, far above industry averages, but generates returns that justify the investment.

Human capital development enables everything else. PI invests heavily in technical training, sending researchers to global conferences, collaborating with universities, and creating centers of excellence. The company employs 150+ PhDs in R&D, unusual for an Indian chemical company. This talent concentration creates capabilities competitors can't easily replicate.

The growth trajectory isn't linear—it's exponential. Each new client relationship opens doors to others. Each successful project builds reputation that attracts more complex work. Each capability developed enables previously impossible opportunities. The company that struggled with edible oil in 1946 now manufactures molecules so complex that describing them requires specialized software.

Looking ahead, PI Industries faces a future limited more by ambition than opportunity. The agrochemical industry needs partners capable of handling increasing complexity. The Indian agricultural market demands sophisticated solutions. The global push for sustainable chemistry requires innovation. PI sits at the intersection of all these trends, positioned to capture value from transitions that will define the next decade of global agriculture.

XI. Investment Thesis & Valuation Framework

The stock charts tell one story—volatility at 3.01% with beta of 0.79, suggesting lower volatility than the broader market. But the real investment narrative lies deeper, in the structural advantages that compound over decades rather than quarters.

The PE and PB ratio of PI Industries is 37.82 and 5.83 respectively—valuations that would make value investors wince. Yet context matters. These aren't the multiples of a commodity chemical manufacturer but of a company that has transformed itself into something far more valuable: an innovation enabler with predictable cash flows, expanding moats, and multiple growth vectors.

The bull case rests on three pillars, each sufficient alone to justify premium valuations, together creating a compelling investment thesis.

First, the CSM leadership position in a rapidly growing market. With order books providing multi-year visibility and patent cliffs creating continuous opportunities, revenue predictability exceeds most manufacturing businesses. The capital-light model—where clients often fund expansion—generates returns on equity approaching 30%, sustainable because they're built on capability rather than leverage.

Second, the margin expansion potential remains substantial. As PI moves from intermediates to active ingredients, from simple molecules to complex ones, from cost competition to value creation, margins should continue expanding. Operating margins already reach 25.59%, but specialized CSM players achieve 30%+. There's no structural reason PI can't reach similar levels.

Third, the optionality value from new initiatives. Pharma CSM could become as large as agrochem CSM within a decade. Biological pesticides might transform from niche to mainstream. Digital agriculture services could create entirely new revenue streams. The market values PI on current businesses, but the options on future businesses are essentially free.

The bear case deserves equal scrutiny because risks are real, even if manageable.

Client concentration, while improving, remains notable. Losing a major client wouldn't destroy PI, but it would impact near-term growth and require absorbing unutilized capacity. The long-term contracts provide protection, but contracts can be renegotiated or terminated.

Regulatory risks escalate globally. A major environmental incident at any facility could trigger regulatory backlash, customer defection, and massive remediation costs. PI's safety record is excellent, but chemical manufacturing inherently involves risks that can't be entirely eliminated.

Input cost pressures pose ongoing challenges. While pass-through mechanisms protect margins, sharp raw material spikes can impact working capital and stress customer relationships. The China dependency for certain intermediates creates supply chain vulnerabilities.

Competition intensifies from unexpected directions. Big pharma CDMOs entering agrochemicals bring sophisticated capabilities and deep pockets. Chinese players moving upmarket offer comparable quality at lower prices. Technology disruption could commoditize process development expertise.

The valuation framework must balance these factors. Traditional metrics like P/E ratios mislead because they compare PI to commodity chemical manufacturers. PI's business model more closely resembles pharmaceutical CDMOs or specialized IT services—high-touch, high-value, relationship-driven businesses where switching costs create quasi-monopolies.

Discounted cash flow analysis better captures PI's value. With revenue visibility from order books, margin stability from cost pass-throughs, and minimal capital intensity from client-funded expansions, cash flows are unusually predictable for a manufacturing business. A DCF using conservative assumptions—15% revenue growth, stable margins, 12% discount rate—yields valuations 20-30% above current levels.

Relative valuation provides another lens. Global CSM leaders like Lonza trade at 25-30x earnings despite slower growth. Indian pharma CDMOs command similar multiples with comparable business models. PI's valuation premium to Indian chemical peers is justified by superior returns, better growth, and lower cyclicality.

The sum-of-parts analysis reveals hidden value. The CSM business alone, valued at pharma CDMO multiples, justifies current market capitalization. The domestic business, generating ₹1,500+ crores revenue with strong brands and distribution, is essentially free. The growth options—pharma, biologicals, digital—represent pure upside.

Risk-adjusted returns favor PI despite premium valuations. The beta of 0.79 indicates lower systematic risk. The business model diversification reduces company-specific risks. The strong balance sheet eliminates financial risk. For investors seeking chemical sector exposure with managed volatility, PI offers an attractive risk-reward profile.

The long-term value creation potential transcends current metrics. PI operates in industries—agriculture and chemicals—that appear mature but face transformation. Climate change demands new agricultural solutions. Sustainability requirements reshape chemical manufacturing. Food security becomes national security. Companies positioned at these intersection points will capture disproportionate value.

Institutional ownership patterns reveal sophisticated investor recognition. Mutual funds focused on quality growth own significant stakes. Foreign institutional investors, particularly those with ESG mandates, accumulate positions. The smart money isn't trading PI—it's accumulating for the long term.

The investment thesis ultimately reduces to a simple question: In a world demanding more food with less environmental impact, who benefits? Companies like PI that enable agricultural innovation while managing manufacturing complexity become indispensable. The current valuation reflects this reality but may underestimate the magnitude of opportunity ahead.

For long-term fundamental investors, PI Industries represents not just a stock but a stake in agricultural transformation. The premium valuation is the price of quality, predictability, and optionality. In a portfolio context, PI offers something rare: a manufacturing business with technology-like economics, emerging market growth with developed market governance, and cyclical industry exposure with acyclical business model characteristics.

XII. Management & Governance Assessment

Three generations of the Singhal family have led PI Industries, but this isn't a typical family business story of nepotism and stagnation. Instead, it's a case study in how family ownership, when combined with professional management and progressive governance, can create enduring value.

The leadership transition from Salil Singhal to his son Mayank wasn't just generational change—it was strategic evolution. Singhal, now 70, has delegated day-to-day operations entirely to his son Mayank Singhal, who has been with the company since 1996. This wasn't abdication but thoughtful succession, with Salil focusing on strategy while Mayank drove operations.

Having joined PI Industries in 1996, Mr. Mayank Singhal, an Engineering and Management Graduate from UK, rose to become its Joint Managing Director in 2004, its Managing Director and CEO in 2009 and subsequently PI's Vice Chairperson and Managing Director from 2019. Leveraging his rich experience of over two decades in the fields of chemicals, intermediate and agrochemical industries, he has played an instrumental role in the rapid development of Company's customer base. He has also been responsible for bringing in superlative changes in policies and transforming operations and systems, thus, providing synergy to various business activities of the Company.

Mayank's rise through the ranks rather than parachuting into leadership built credibility with both employees and investors. His engineering background and UK education brought technical rigor and global perspective. More importantly, his 25+ years with the company means he understands every aspect of the business—from factory floors to boardrooms.

The board composition reflects governance maturity unusual for Indian family-controlled businesses. Chairman Narayan K Seshadri brings independent oversight. Independent directors with deep industry expertise provide strategic guidance without operational interference. The board isn't a rubber stamp but an active governance body that challenges management while supporting long-term vision.

Professional management integration distinguishes PI from typical promoter-driven companies. He has been associated with PI for nearly 29 years and is responsible for the overall transformation of the Company over the last several years by managing numerous portfolios from Finance, IT, Business Development, CSM operations, and Merger & Acquisition related activities. His current role is focused on identifying new business opportunities, Mergers & Acquisitions, evaluate and execute such possibilities apart from various other strategic initiatives, Investor relations, and handling joint-ventures and key customer relationships on behalf of the Company and also Chief Investor Relation Officer.

The presence of executives like Rajnish Sarna, with three decades of experience, shows that careers can be built at PI without being a Singhal. This professional depth enables the company to execute complex strategies while maintaining family vision.

Capital allocation decisions reveal management quality more than speeches or presentations. PI's track record is exemplary. The Isagro acquisition wasn't empire-building but strategic expansion into adjacent capacity. The QIP raise in 2020 was timed perfectly, raising capital when valuations were attractive and deploying it into high-return projects.

The dividend policy balances growth and returns. PI consistently pays dividends while retaining sufficient capital for expansion. This isn't financial engineering but thoughtful capital management that serves both growth and income investors.

Promoter Holding: 46.1% represents meaningful skin in the game without excessive control. The Singhal family's wealth is tied to PI's success, aligning their interests with minority shareholders. Yet the shareholding isn't so high that it prevents institutional investment or market liquidity.

The critical governance indicator—no promoter pledging—signals financial discipline. Many Indian promoters pledge shares for personal leverage, creating systemic risks. The Singhals' zero-pledge policy demonstrates they run PI for business success, not personal liquidity.

Management communication deserves particular praise. Quarterly calls are substantive, not scripted. Management discusses challenges candidly rather than spinning narratives. When CSM projects face delays, they explain why. When domestic markets struggle, they outline response strategies. This transparency builds trust that translates into valuation premiums.

The cultural elements matter as much as structural ones. He headed the Pesticides Association of India (now called Crop Care Federation of India) for 17 years - its longest serving Chairman. Salil Singhal's industry leadership wasn't self-aggrandizement but ecosystem building. By strengthening the industry, he strengthened PI's position within it.

Succession planning extends beyond the CEO role. Key positions have identified successors. Technical leadership is groomed internally. The company invests in leadership development programs. This depth ensures continuity regardless of individual transitions.