HP Inc.: The Original Silicon Valley Story

I. Introduction & Episode Roadmap

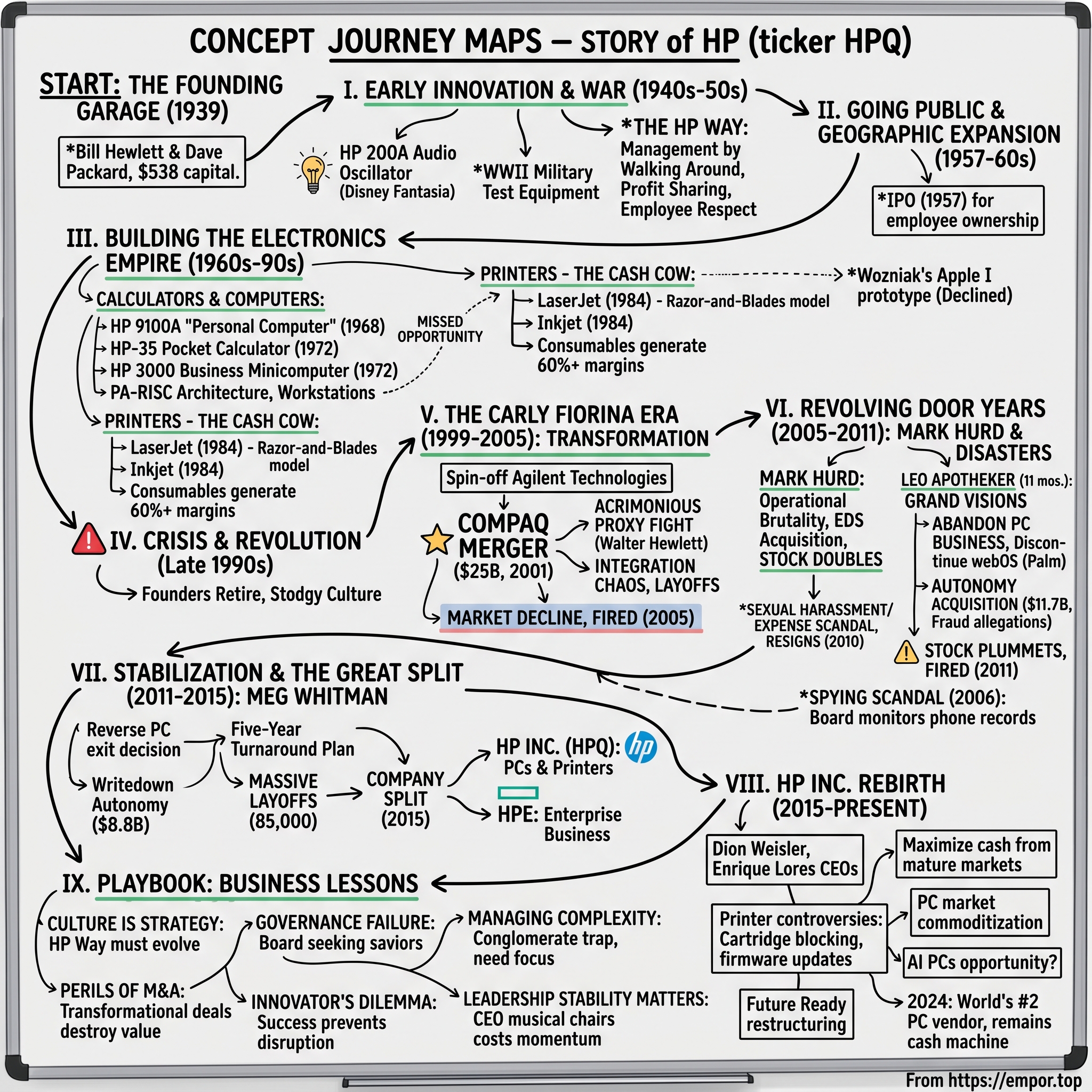

Picture this: A one-car garage in Palo Alto, California, 1939. Two Stanford graduates, Bill Hewlett and David Packard, are tinkering with electronic equipment, their total capital a mere $538. The Great Depression still casts its shadow over America, yet these two engineers are about to launch what would become the foundational company of Silicon Valley. That garage at 367 Addison Avenue would later be designated "the Birthplace of Silicon Valley" by the state of California—not hyperbole, but historical fact.

Fast forward to 2015: The company they built is being cleaved in two. HP Inc., keeper of the personal computer and printer businesses, would retain the original stock ticker HPQ and claim direct lineage to that garage startup. Its sibling, Hewlett Packard Enterprise, would take the enterprise computing business and forge a separate path. The split wasn't just corporate restructuring—it was an admission that the sprawling technology conglomerate had become too complex, too conflicted, too broken to continue as one entity.

How did the company that literally invented the Silicon Valley way of doing business—open workspaces, stock options for all employees, management by walking around—become a cautionary tale of corporate dysfunction? How did HP go from being the gold standard of American technology companies to cycling through five CEOs in six years, writing off billions in failed acquisitions, and becoming better known for printer cartridge controversies than innovation?

The answer lies in a series of pivotal decisions, cultural shifts, and market forces that transformed HP from a maker of audio oscillators for Disney's Fantasia into a $53 billion technology giant that today battles for relevance in mature markets. This is a story of breathtaking innovation and crushing strategic mistakes, of a company that created an entire industry's culture and then lost its own soul, of boards that went from visionary to vindictive.

At its core, this is about a fundamental question every technology company must face: Can you maintain the innovative spirit of a startup while operating at the scale of a multinational corporation? HP's journey suggests the answer is far more complex than Silicon Valley's mythology would have us believe. The company that taught the world about "the HP Way"—a management philosophy emphasizing respect for individuals, contribution to communities, and uncompromising integrity—would eventually spy on its own board members, force out CEOs with nine-figure severance packages, and pursue acquisitions that destroyed more value than most companies ever create.

Yet HP endures. As of 2024, it remains the world's second-largest PC vendor, generates billions in free cash flow from its printer business, and continues to employ over 50,000 people globally. The company that began in a garage selling oscillators to Walt Disney now sells everything from $300 laptops to $100,000 3D printers. It's a testament to both the durability of great businesses and the difficulty of killing a technology giant, no matter how hard its leadership might try.

What follows is the complete story of HP—from its Depression-era founding through its current struggles and opportunities. We'll explore how two Stanford engineers created not just a company but an entire ecosystem, how their successors built one of technology's great franchises, and how a series of CEOs and board members nearly destroyed it all. Along the way, we'll uncover lessons about corporate governance, the challenges of technological disruption, and what happens when a company loses sight of its founding principles.

This isn't just corporate history—it's a blueprint for understanding how technology companies rise, fall, and sometimes rise again. Because if HP, the original Silicon Valley success story, could lose its way so dramatically, what does that mean for today's technology giants? And if it can find redemption after such spectacular failures, what does that tell us about corporate resilience and the possibility of reinvention?

II. The Garage: Founding Story & Early Years (1939-1960s)

The story begins not in the garage, but in a Stanford University classroom in 1930. Frederick Terman, a young professor of electrical engineering, is teaching a course on radio engineering. Among his students are two undergraduates who've become fast friends: William Redington Hewlett, son of a medical doctor who died when Bill was twelve, and David Packard, a tall, athletic Coloradan whose father was a lawyer. They bonded over a shared love of the outdoors—camping and fishing in the Sierra Nevada—and a fascination with electronics that went beyond academic requirements.

Terman wasn't just any professor. He had a vision for what would later be called technology transfer—moving innovations from university laboratories into commercial enterprises. While the rest of America struggled through the Depression, Terman encouraged his brightest students to start companies rather than flee to the established electronics firms of the East Coast. "Why go to New York?" he'd ask. "Build your companies here." It was radical advice in 1934, when Silicon Valley was still called the Valley of Heart's Delight, known more for its apricot orchards than its oscilloscopes. After graduation, both men went their separate ways initially. Packard took a job at General Electric in Schenectady, New York, while Hewlett pursued graduate work at MIT and Stanford. But Terman kept pulling them back, urging them to start something together. In 1938 David and Lucile Packard got married and rented the first floor of the house at 367 Addison Avenue in Palo Alto. The simple one car garage became the HP workshop and the little shack out back became Bill Hewlett's home. The eureka moment came from a master's thesis. Bill Hewlett had been working on a new type of audio oscillator that used a simple light bulb as a temperature-dependent resistor to stabilize the circuit—an elegant solution that delivered sine waves with less than 1% distortion. His professors thought it was clever but impractical. Packard disagreed. He saw commercial potential where others saw academic curiosity.

The two friends formalized their partnership in 1939, deciding the company name with a coin toss. They tossed a coin to decide whether the company they founded would be called Hewlett-Packard (HP) or Packard-Hewlett. Hewlett won, though Packard would joke for decades that he suspected Bill used a two-headed coin.

Their first product, the HP 200A audio oscillator, was deliberately numbered to suggest they'd been in business for years—startup fake-it-till-you-make-it culture existed even in 1939. They priced it at $54.40, a fraction of the $200-600 competitors charged for inferior equipment. The price point wasn't random; They originally chose a price of $54.40 based on a historical slogan. When they later found that their closest competitor was a General Radio product that sold for $400, they decided to change the price to a still comparatively modest $71.50.

Then came the Disney moment. Hewlett brought his new oscillator to a regional meeting of the Institute of Radio Engineers held in Portland, Oregon, where an engineer from Walt Disney Studios also attended. The Disney engineer recognized the product was just what they needed for their revolutionary Fantasound system—the world's first multichannel stereo sound system for motion pictures. Disney needed oscillators that could handle frequencies down to 20 Hz for their groundbreaking animated film Fantasia. With a few component changes, the 200B was born, and Disney purchased eight of the new oscillators for $54.40 each

The Disney sale proved pivotal beyond its modest $435.20 in revenue. It demonstrated that two engineers in a garage could outperform established East Coast manufacturers on both price and quality. Word spread through the engineering community. Orders trickled in from other film studios, universities, and government contractors. By the end of 1939, HP had generated $5,369 in revenue and $1,563 in profits—a 29% margin that would make today's hardware companies weep with envy.

World War II transformed HP from garage startup to serious business. The U.S. government needed electronic testing equipment, and HP's oscillators, signal generators, and pulse generators were suddenly essential to the war effort. Revenue exploded from $34,000 in 1940 to $750,000 by 1943. The company moved from the garage to a proper facility, hired its first employees beyond the founders, and began developing the management practices that would define Silicon Valley culture for generations.

The war years also crystallized what would become known as "the HP Way." Faced with rapid growth and the need to maintain quality while scaling production, Hewlett and Packard developed their management philosophy organically. They instituted profit-sharing in 1940, making every employee a stakeholder in the company's success. They created an open floor plan where engineers and executives worked side by side—no corner offices, no executive dining rooms. When materials were scarce, they encouraged employees to experiment and innovate rather than wait for perfect conditions. Post-war, the company incorporated on August 18, 1947, with Packard as president and Hewlett as vice president. Sales had reached $5.5 million by 1951, driven by electronic instrumentation that became essential for the emerging aerospace and defense industries. The Korean War brought another surge of government contracts, pushing revenue to $20 million by 1956.

Then came the decision to go public. On November 6, 1957, HP offered 300,000 shares at $16 each, valuing the company at $49 million based on 3 million total shares outstanding. The IPO was issued for two reasons: to help with estate planning for its founders and to enable employees to share in the company. This wasn't just about raising capital—it was about democratizing ownership in a way that aligned with the HP Way philosophy.

The 1960s brought geographic and product expansion. HP went global, establishing a marketing organization in Geneva and a manufacturing plant in Boeblingen, Germany. HP entered the Asian market by forming its first joint venture, Yokogawa-Hewlett-Packard (YHP) in Tokyo. The company's reputation for quality and innovation spread internationally, with European and Asian customers particularly valuing HP's precision instrumentation.

But perhaps the most significant development of this era was the codification of the HP Way. In 1957, the same year as the IPO, Hewlett and Packard articulated their management philosophy in a set of corporate objectives that would influence business culture far beyond HP's walls. These weren't just platitudes—they were operational principles:

First, profit wasn't the goal but the means to achieve other objectives. HP existed to make technical contributions to the advancement and welfare of humanity. Second, employees should share in the company's success through profit-sharing and stock ownership. Third, job security was paramount—HP committed to avoiding layoffs through careful planning and controlled growth. Fourth, the company would grow only as fast as it could finance growth from profits, avoiding excessive debt.

The HP Way extended to the physical workspace. In 1958, HP moved to the Stanford Industrial Park (now Stanford Research Park), becoming one of the first tenants in what would become the geographic heart of Silicon Valley. The new facilities featured open floor plans, no reserved parking spaces, and coffee stations where engineers and executives would naturally interact. Friday afternoon beer busts became legendary—not as forced corporate fun but as genuine celebrations of the week's achievements.

Management by walking around, later popularized by Tom Peters in "In Search of Excellence," originated here. Hewlett and Packard spent hours on the factory floor and in the labs, not inspecting but listening. Engineers were encouraged to spend 10% of their time on personal projects. Flexible working hours, unheard of in 1960s corporate America, became standard at HP. The company even instituted the nine-day fortnight during the 1970 recession rather than laying off employees—everyone took a 10% pay cut but kept their jobs.

This cultural foundation would prove both HP's greatest strength and, eventually, a source of vulnerability. The HP Way worked brilliantly when the company was small enough for personal relationships to matter, when the founders were present to embody the values, and when the technology industry rewarded patient, methodical innovation. Whether it could survive rapid growth, global competition, and the founders' eventual absence would become the central question of HP's next chapter.

III. Building the Electronics Empire (1960s-1990s)

The transformation from instrument maker to computer company began not with a grand strategic vision but with necessity. In 1966, HP engineers were frustrated. They needed a controller for their growing line of test instruments—something more flexible than hard-wired logic but more reliable than the minicomputers available from Digital Equipment Corporation or IBM. So they built their own. HP's first computer, the HP 2116A, was developed in 1966 specifically to manage the company's test and measurement devices.

The 2116A wasn't meant to compete with mainframes or even minicomputers initially. It was an instrument controller that happened to be a computer. But customers started asking if they could buy it for other purposes. HP had accidentally entered the computer business, a pattern that would repeat throughout its history—following customer needs rather than grand strategic plans.

The next breakthrough came from an unexpected source: a calculator that thought it was a computer. In 1968, HP introduced the 9100A, a desk-sized device that could perform complex mathematical operations, store programs on magnetic cards, and display results on a small CRT screen. HP's marketing department made a fateful decision: they called it a "personal computer" in their advertising. While it cost $4,900 (about $40,000 in today's dollars), making it personal only for well-funded engineers and scientists, HP had coined a term that would define an industry.

In 1972, using advanced integrated-circuit technology, Hewlett-Packard unveiled the first pocket-sized calculator, the HP-35. Bill Hewlett had challenged his engineers to build a scientific calculator that would fit in his shirt pocket, replacing the slide rules that engineers carried everywhere. The HP-35 could perform trigonometric and logarithmic functions with ten-digit precision. Priced at $395, HP expected to sell 10,000 units in the first year. They sold 100,000. Every engineering student wanted one; slide rule manufacturers went out of business virtually overnight.

The calculator success taught HP crucial lessons about consumer electronics: miniaturization mattered, battery life was critical, and engineers would pay premium prices for professional tools. These lessons would inform their entry into personal computers, though not always successfully. In 1972 the company released the HP 3000 general-purpose minicomputer—a product line that remains in use today—for use in business.

Then came one of Silicon Valley's great what-if moments. In 1976 an engineering intern at the company, Stephen G. Wozniak, built a prototype for the first personal computer and offered it to the company. Hewlett-Packard declined and gave Wozniak all rights to his idea; later he joined with Steven P. Jobs to create Apple Computer, Inc. HP's decision made sense within their framework—the Apple I didn't fit their target market of business and technical professionals. But it revealed a blind spot that would haunt HP: they understood engineers and businesses but struggled to see consumer opportunities.

Hewlett-Packard introduced its first desktop computer, the HP-85, in 1980. Because it was incompatible with the IBM PC, which became the industry standard, it was a failure. This pattern would repeat: HP would create technically superior products that failed to achieve market standards. Their computers were elegant, their calculators unmatched, their instruments precise—but in the emerging PC world, compatibility mattered more than capability.

The solution came from an unexpected direction: printers. In 1984, HP introduced the LaserJet, based on Canon's laser printing engine but with HP's own formatter and software. The original LaserJet printed eight pages per minute at 300 dots per inch resolution, cost $3,495, and transformed office printing. Within two years, HP had sold over 500,000 units. By 1988, printer revenues exceeded those from computers and instruments combined.

The LaserJet's success wasn't just about technology—it was about business model innovation. HP realized that printers were platforms for selling consumables. A LaserJet might generate $3,000 in initial revenue but $10,000 or more in toner sales over its lifetime. This razor-and-blades model would eventually generate tens of billions in high-margin revenue, funding HP's expansion into other markets and covering for numerous strategic mistakes.

Meanwhile, HP was building a powerhouse in technical workstations. The company's PA-RISC architecture, introduced in 1986, powered Unix workstations that competed with Sun Microsystems and Silicon Graphics for the lucrative computer-aided design and engineering markets. When internal development wasn't fast enough, HP turned to acquisition. In 1989, they purchased Apollo Computer for $476 million, briefly becoming the largest workstation vendor.

The 1980s also saw HP's first serious attempts at the PC market that actually acknowledged IBM compatibility. The HP-150, an IBM PC-compatible system that had a touch screen, was technically interesting but failed in the marketplace. HP kept trying, introducing the Vectra line of IBM-compatible PCs in 1985. These machines were well-built and reliable but expensive. HP couldn't compete with Compaq on performance or with clone makers on price.

By 1990, HP had grown to $13 billion in revenue and 90,000 employees. The company that started with two engineers and $538 was now a global technology conglomerate. It dominated scientific instruments, led in printers, held strong positions in minicomputers and workstations, and struggled in PCs. The HP Way still governed corporate culture, though managing by walking around was harder when your employees were spread across 120 countries.

David Packard stepped down as chairman in 1993, though he remained involved until his death in 1996. Bill Hewlett had already reduced his role, retiring as vice chairman in 1987. The founders' departure marked the end of an era. They left behind a $25 billion company that was the pride of Silicon Valley, profitable and growing, with dominant positions in several markets.

But storm clouds were gathering. The workstation market was consolidating around Sun Microsystems. The printer business, while hugely profitable, faced challenges from inkjet technology that HP itself had developed. The PC market was becoming increasingly commoditized. And most ominously, HP's consensus-driven, employee-friendly culture was increasingly seen as too slow for the internet age. The company needed new leadership for new challenges. What it got was a revolution that nearly destroyed it.

IV. The Carly Fiorina Era: Transformation & Controversy (1999-2005)

On July 19, 1999, HP made history. The board named Carly Fiorina as CEO, making her the first woman to lead a Dow 30 company. She came from Lucent Technologies, where she'd orchestrated that company's spin-off from AT&T and driven aggressive sales growth. HP's board, concerned that the company was falling behind in the internet age, wanted a change agent. They got more than they bargained for.

Fiorina inherited a company that was profitable but pedestrian. HP's stock had underperformed the S&P 500 for years. Revenue growth was anemic. The company was organized into 83 autonomous product divisions—a structure that preserved entrepreneurial spirit but created massive redundancy and prevented coordinated strategy. Engineers still ruled the culture, but the market increasingly rewarded marketing and speed over technical perfection.

Her first major move was bold and necessary. In 1999, HP spun off Agilent Technologies, separating the original test and measurement business from the computer and printer operations. Agilent's IPO was the largest in Silicon Valley history to date, raising $2.1 billion. The spin-off made strategic sense—the slow-growing instrumentation business had little synergy with computers and printers. But symbolically, it was earthshaking. HP was literally spinning off the business that Bill and Dave had started in the garage.

Fiorina then launched a massive reorganization, collapsing the 83 divisions into four groups: Enterprise Systems, Services, Imaging and Printing, and Personal Systems. She centralized sales and marketing, eliminated redundant research projects, and laid off 6,000 employees. The HP Way's promise of job security was officially dead. The old-timers were horrified, but Wall Street initially approved—the stock rose 65% in her first year.

Then came September 3, 2001. Fiorina announced HP would acquire Compaq Computer for $25 billion, creating a technology behemoth with $87 billion in combined revenues. The logic seemed compelling: achieve massive scale in PCs and servers, eliminate redundant costs, and compete more effectively with IBM and Dell. Compaq brought the profitable ProLiant server line, a strong services business, and the legendary Digital Equipment Corporation technology it had previously acquired.

The merger triggered Silicon Valley's most bitter proxy fight. Walter Hewlett, son of co-founder Bill Hewlett and an HP board member, led the opposition. He argued the deal would dilute HP's profitable printer business with low-margin PCs, create massive integration challenges, and destroy shareholder value. David Packard's children and foundations joined the opposition. The battle turned personal and ugly, with both sides spending millions on advertisements and proxy solicitors.

The numbers were staggering. HP promised $2.5 billion in annual cost savings but admitted this required laying off 15,000 employees. The combined company would have 145,000 employees and operate in 160 countries. HP shareholders would own 64% of the merged company, with Compaq shareholders receiving 0.6325 HP shares for each Compaq share. The deal valued Compaq at a 19% premium to its pre-announcement price.

The proxy vote on March 19, 2002, was extraordinarily close—50.95% in favor, 49.05% against. Walter Hewlett challenged the results, alleging HP had improperly influenced Deutsche Bank's vote, but a Delaware judge upheld the merger. On May 3, 2002, the deal closed. HP changed its stock ticker from HWP to HPQ, another symbolic break from the past.

Integration proved even harder than critics predicted. Combining two companies with different cultures, overlapping products, and conflicting strategies created chaos. Customer defections accelerated as sales teams were reorganized. Key executives from both companies departed. The promised cost savings required not 15,000 but eventually 30,000 layoffs. Meanwhile, Dell was eating HP's lunch in PCs and servers with its direct sales model and lean operations.

Fiorina made other strategic moves that ranged from questionable to disastrous. In January 2004, HP announced a partnership with Apple to sell HP-branded iPods. The deal made HP a reseller of Apple's wildly successful music player, but with minimal margins and no control over the product. Apple got distribution through HP's retail channels while giving up almost nothing. When Steve Jobs later terminated the partnership, HP was left with nothing to show for it except the humiliation of having been played by a master strategist.

The financial results told the story. During Fiorina's tenure, HP's stock price fell by 50% while the NASDAQ rose 16%. Revenue grew primarily through acquisition, not organic growth. The company's debt rating was downgraded. Market share gains in PCs came at the cost of profitability. The printer business, HP's cash cow, saw margins decline as Fiorina pushed for market share over profits.

By late 2004, the board had lost confidence. Fiorina's imperious management style—she insisted on a corporate jet, hired her own security detail, and centralized decision-making—clashed with HP's collaborative culture. Sales execution problems mounted. The stock languished. On February 9, 2005, the board asked for her resignation. She negotiated a $21 million severance package and departed, leaving behind a company that was larger but weaker, with a damaged culture and uncertain strategy.

The Fiorina era's legacy remains debated. Supporters argue she modernized a stodgy company and that the Compaq merger, while painful, was necessary for HP to achieve scale in commodity businesses. Critics contend she destroyed HP's culture, pursued growth over profitability, and executed a merger that destroyed tens of billions in shareholder value.

What's undeniable is that Fiorina transformed HP from a decentralized confederation of entrepreneurs into a centralized corporation. Whether that transformation was necessary or destructive would be tested by her successors, who faced the challenge of managing the sprawling entity she'd created while trying to restore profitability and purpose to a company that had lost its way.

V. The Revolving Door Years: Hurd, Apotheker & Crisis (2005-2011)

Mark Hurd arrived at HP in March 2005 like a turnaround specialist entering a trauma ward. The former NCR CEO was everything Fiorina wasn't—low-key, operations-focused, and obsessed with execution rather than vision. Where Fiorina held elaborate presentations about transforming HP into the "leading technology company," Hurd pulled out spreadsheets and asked why gross margins were declining.

His prescription was brutal but effective. Hurd launched the largest restructuring in HP's history, eventually eliminating 48,000 jobs—nearly one in six employees. He consolidated data centers from 85 to 6, reduced the number of software applications from 6,000 to 1,500, and outsourced manufacturing and support functions. Every business unit faced new profitability targets. Sacred cows were slaughtered—even the HP Labs budget was cut by 20%.

In 2008, HP completed a $12.6 billion acquisition of Electronic Data Systems under Hurd, bringing 140,000 employees and establishing HP as a major player in IT services. Unlike the Compaq merger, the EDS integration was methodical and successful. Hurd also acquired Palm for $1.2 billion in 2010, hoping to compete in smartphones and tablets against Apple's iPhone and iPad.

The results were impressive. HP's stock price doubled during Hurd's tenure. Revenue grew to $126 billion by 2010, making HP the world's largest technology company by revenue. Operating margins expanded from 4% to 9%. HP briefly overtook Dell as the world's largest PC maker. Wall Street loved Hurd's discipline and execution. Then, on August 6, 2010, it all came crashing down. Hurd resigned following a sexual harassment claim against him and the company. The scandal began when HP received a letter from a lawyer representing a marketing contractor employed by the company on June 30. While HP's investigation found Hurd didn't violate its sexual harassment policy, it uncovered something else: He repeatedly filed inaccurate expense account reports in a bid to keep the relationship secret.

The amounts were trivial—about $20,000 according to reports—pocket change for a company with over $100 billion in revenue. But the principle was devastating. The CEO who'd preached operational excellence and ethical conduct had falsified expense reports to hide a personal relationship with contractor Jodie Fisher. Oracle CEO Larry Ellison reportedly wrote "The HP board just made the worst personnel decision since the idiots on the Apple board fired Steve Jobs many years ago".

The market agreed with Ellison. On the day of the announcement, HP's market value fell by $10 billion, close to a 10 per cent decline. Hurd was provided a severance payment of approximately $12 million, adding insult to injury for shareholders who'd just lost billions in value.

The board moved quickly to contain the damage, appointing CFO Cathie Lesjak as interim CEO. But finding a permanent replacement proved challenging. HP needed someone with the gravitas to lead a $126 billion company, the operational skills to manage its complexity, and the strategic vision to navigate rapidly changing technology markets. After a two-month search, they made a choice that would prove catastrophic.

Leo Apotheker's appointment as CEO on September 30, 2010, puzzled Silicon Valley. The former SAP CEO had been forced out after barely a year, with SAP's stock falling 28% during his tenure. He had no experience in consumer electronics, limited knowledge of HP's core businesses, and a reputation for grand visions disconnected from operational reality. The board, perhaps overcorrecting from Hurd's tactical focus, wanted a strategist. They got a disaster.

Apotheker's strategy, unveiled in March 2011, was breathtaking in its ambition and naivety. HP would transform from a hardware company into an enterprise software and services giant, essentially becoming IBM. To execute this vision, he announced three massive moves: First, HP would spin off or sell its Personal Systems Group, exiting the PC business where it was the global leader. Second, HP would discontinue webOS devices and operations, effectively abandoning the mobile market just months after the Palm acquisition. Third, HP would acquire UK software company Autonomy for $11.7 billion, a 79% premium to its market value.

The market reaction was swift and brutal. On August 19, 2011, the day these plans were announced, HP's stock fell 20%. It fell another 5% the next day. In total, HP lost $20 billion in market value in 48 hours. The strategic logic was questionable at best—why would HP pay a massive premium for Autonomy while simultaneously telling the world it was desperate to transform? Why exit profitable businesses to enter markets where HP had no competitive advantage?

The Autonomy acquisition would prove even worse than critics imagined. Within a year, HP would write down $8.8 billion of Autonomy's value, alleging accounting fraud. Lawsuits would drag on for years, with HP eventually winning a fraud case against Autonomy's founder Mike Lynch, though recovering only a fraction of the losses.

Apotheker's tenure lasted just 11 months. On September 22, 2011, the board fired him, making him the third CEO to leave HP in six years. His severance package totaled $13.2 million, bringing HP's CEO severance payments to over $83 million since 2005. The board had managed to destroy billions in shareholder value while enriching failed executives.

The revolving door of CEOs wasn't HP's only governance disaster. In 2006, the company had been embroiled in a spying scandal when chairwoman Patricia Dunn authorized private investigators to obtain phone records of board members and journalists to identify the source of boardroom leaks. The investigation used "pretexting"—essentially lying to phone companies to obtain records illegally. Dunn was forced to resign, four people were charged with crimes, and HP's reputation for ethical behavior was shattered.

The board that had once included Silicon Valley luminaries now seemed incapable of basic governance. They'd hired CEOs without proper vetting, approved strategies without rigorous analysis, and created a culture of crisis and confusion. Each new CEO arrived promising transformation, only to leave in disgrace or failure. Each transition destroyed value and demoralized employees. The HP Way wasn't just forgotten—it was systematically dismantled.

VI. The Meg Whitman Stabilization (2011-2015)

On September 22, HP's board of directors appointed Meg Whitman as president and chief executive officer. The former eBay CEO represented a return to operational stability after the chaos of the Apotheker era. Unlike her predecessor, Whitman understood technology, had successfully run a large company, and commanded respect in Silicon Valley. She also had the political skills to navigate HP's dysfunctional board, having served as a director since January 2011.

Whitman inherited a company in crisis. Employee morale was shattered after years of layoffs and strategic whiplash. Customers were confused about HP's direction. The stock had fallen 75% from its 2010 highs. The Autonomy disaster was still unfolding. And despite Apotheker's grandiose announcements, HP was still fundamentally a PC and printer company that needed to figure out its future.

Her first move was to reverse Apotheker's most damaging decision. In October 2011, just weeks after taking charge, Whitman announced HP would keep its PC division. The message was clear: HP would not abandon its core businesses in pursuit of transformation fantasies. "HP is committed to the PC," she declared, trying to reassure customers and partners who'd been planning for a post-HP world.

But stabilizing HP required more than strategic reversals. The company was bloated, inefficient, and struggling to compete. Whitman launched a massive restructuring, eventually eliminating 85,000 jobs—nearly a third of HP's workforce. These weren't just cost cuts but a fundamental reorganization. Entire layers of management were eliminated. Redundant operations were consolidated. Non-core assets were sold.

The human cost was staggering. Engineers who'd spent decades at HP were let go. Entire divisions were shuttered. The Palo Alto headquarters, once buzzing with innovation, became increasingly empty. But Whitman argued the cuts were necessary for survival. HP's costs were simply too high to compete with Asian manufacturers in PCs or focused competitors in enterprise computing.

Whitman also had to clean up the Autonomy mess. In November 2012, HP announced the $8.8 billion writedown and accused Autonomy's leadership of accounting fraud. The allegations triggered investigations by the SEC and the UK's Serious Fraud Office. Lawsuits flew in all directions. The legal battle would consume millions in fees and management attention for years.

Despite the challenges, Whitman brought stability HP desperately needed. She committed to a five-year turnaround plan and stuck to it. She rebuilt relationships with customers and partners. She invested in new areas like 3D printing and security while maintaining HP's core businesses. Most importantly, she gave HP time to breathe after years of crisis.

By 2014, it was clear HP's fundamental problem wasn't execution but structure. The company was trying to serve everyone from consumers buying $300 laptops to enterprises spending millions on data centers. The synergies between selling printers to consumers and servers to corporations were minimal. The different businesses required different strategies, investment levels, and corporate cultures.

The solution was radical but necessary: split HP in two. On October 6, 2014, Whitman announced that HP would separate into two independent public companies. HP Inc. would take the PC and printer businesses, focusing on consumers and commercial printing. Hewlett Packard Enterprise would take the servers, storage, networking, and services businesses, focusing on corporate customers.

The split was complex, involving separating 300,000 employees, thousands of contracts, and operations in 170 countries. But Whitman executed it methodically. Each company would be large enough to compete but focused enough to succeed. HP Inc. would generate about $55 billion in annual revenue, HPE about $50 billion. Both would be Fortune 100 companies.

Hewlett Packard Enterprise would comprise HP's enterprise technology infrastructure, software and services businesses, while HP Inc. would contain HP's personal systems and printing businesses and retain the current logo. Importantly, The split was structured so that Hewlett-Packard changed its name to HP Inc. and spun off Hewlett Packard Enterprise as a new publicly traded company. HP Inc. retains Hewlett-Packard's pre-2015 stock price history and its former stock ticker symbol, HPQ, while Hewlett Packard Enterprise trades under its own symbol, HPE.

Whitman's tenure wasn't without controversy. The massive layoffs devastated communities where HP had been a major employer. The company's innovation engine, HP Labs, was gutted. R&D spending was cut to fund restructuring. Critics argued Whitman was managing decline rather than driving growth.

But she'd accomplished something important: she'd saved HP from collapse. When she stepped down as CEO of HP Inc. after the split, the company was smaller but stable. It had a clear strategy, improving financials, and a path forward. After years of chaos, that counted as success.

VII. The Great Split & HP Inc. Rebirth (2015-Present)

On November 1, 2015, Hewlett-Packard was split into two companies. Its personal computer and printer businesses became HP Inc., while its enterprise business became Hewlett Packard Enterprise. The split was more than corporate restructuring—it was an acknowledgment that the conglomerate model no longer worked in technology.

HP Inc. emerged as the legal successor to the original company, inheriting not just the PC and printer businesses but also the cultural legacy and historic responsibility of being "the real HP." With roughly $50 billion in annual revenue and 50,000 employees, it was still massive but now manageable. Dion Weisler, who'd run the printing business, became CEO with a clear mandate: maximize cash flow from the mature businesses while finding new growth opportunities.

The printer business remained HP Inc.'s cash cow, but it was increasingly controversial. HP had perfected the razor-and-blades model, selling printers at low margins or even losses while generating enormous profits from ink and toner. A cartridge that cost $3 to manufacture might sell for $30 or more. HP's margins on supplies exceeded 60%, generating billions in profit annually.

But this model created perverse incentives. HP began using firmware updates to block third-party and refilled cartridges, forcing customers to buy expensive HP-branded supplies. When customers found workarounds, HP pushed updates that disabled their printers. The Electronic Frontier Foundation called these practices "deceptive" and "anti-competitive." Class-action lawsuits proliferated. In 2024, a French association called Halte à l'Obsolescence Programmée filed a complaint against HP, accusing it of planned obsolescence practices. The complaint alleges that HP artificially blocks printers when it detects a cartridge as empty, even if there is ink remaining.

The PC business faced different challenges. HP Inc. was the world's second-largest personal computer vendor by unit sales after Lenovo and ahead of Dell as of 2024, but the market was mature and commoditized. Margins were thin, competition fierce, and differentiation difficult. HP tried various strategies—gaming PCs under the Omen brand, premium laptops competing with Apple, hybrid devices for business users—but struggled to escape the commodity trap.

Innovation efforts yielded mixed results. HP invested heavily in 3D printing, acquiring several companies and developing new technologies. The market potential was enormous, with 3D printing potentially disrupting traditional manufacturing. But commercialization proved slower than expected. Industrial customers were cautious about new technology. Consumer 3D printing remained niche. Revenues grew but from a tiny base. Financially, HP Inc. had mixed results. Fiscal 2024 first quarter net revenue of $13.2 billion, down 4.4% from the prior-year period. However, the company remained profitable and cash-generative. HP generated $3.7 billion in net cash provided by operating activities and $3.3 billion of free cash flow in fiscal 2024. HP returned 96% of its free cash flow to shareholders in fiscal 2024 through dividends and share buybacks.

Leadership changes continued, though with less drama than before. Dion Weisler stepped down as CEO in 2019, replaced by Enrique Lores, a 30-year HP veteran who'd run the printing business. Lores brought stability and focus, launching a restructuring plan called "Future Ready" aimed at simplifying operations and reducing costs. The company continued to shrink, with headcount falling below 50,000 by 2024.

The COVID-19 pandemic initially boosted HP's business as remote work drove PC and printer demand. But the surge proved temporary. As workers returned to offices and PC refresh cycles lengthened, demand normalized. HP faced the same challenge it had for years: how to grow in mature, commoditized markets.

By 2024, HP Inc. remained the world's second-largest personal computer vendor by unit sales after Lenovo and ahead of Dell. In the 2023 Fortune 500 list, HP is ranked 63rd-largest United States corporation by total revenue. The company is listed on the New York Stock Exchange and is a constituent of the S&P 500 Index.

The company operates through three segments: Personal Systems, Printing, and Corporate Investments. But controversy continued to dog the printer business. Beyond the cartridge blocking issues, HP faced criticism for its environmental impact. The company's business model encouraged waste—printers designed to fail, cartridges that couldn't be refilled, firmware that prevented repairs. Environmental groups targeted HP as a symbol of planned obsolescence and electronic waste.

VIII. Playbook: Business & Management Lessons

The HP story offers a masterclass in both building and destroying corporate value. The lessons are particularly relevant for technology companies navigating rapid change, but apply broadly to any organization facing disruption.

The HP Way: Lost but Not Forgotten

The original HP Way wasn't just management philosophy—it was competitive advantage. By treating employees as partners rather than costs, HP attracted and retained exceptional talent. The profit-sharing, job security, and collaborative culture created an environment where innovation flourished. Engineers took risks because failure didn't mean termination. The lesson: culture is strategy, especially in knowledge industries where human capital is the primary asset.

But the HP Way had limitations. It worked brilliantly in a growing company with patient competition and long product cycles. It struggled when markets demanded speed, when competitors operated with different values, and when scale made personal relationships impossible. The deeper lesson: even the best culture must evolve with circumstances. HP's mistake wasn't abandoning the HP Way but doing so without replacing it with something equally powerful.

Governance Failures: The Board as Destroyer

HP's board dysfunction offers a cautionary tale about corporate governance. The board that included technology luminaries in the 1990s devolved into a group that spied on its own members, hired CEOs without proper vetting, and approved strategies without rigorous analysis. The Autonomy acquisition alone destroyed more value than most companies ever create.

The pattern was consistent: faced with strategic challenges, the board sought saviors rather than solutions. Each new CEO was hired to fix the problems created by their predecessor, leading to strategic whiplash. Fiorina centralized what Hewlett and Packard had decentralized. Hurd cut what Fiorina had built. Apotheker tried to exit businesses Hurd had optimized. Whitman split what Fiorina had merged.

The lesson is that boards must provide strategic continuity, not just CEO selection. They need industry expertise, not just general business experience. And they must resist the temptation to solve strategic problems with leadership changes. HP's board failed on all counts, destroying billions in value through poor governance.

The Perils of Transformational M&A

HP's acquisition history reads like a textbook on how not to do M&A. The Compaq merger, the largest technology merger of its time, destroyed enormous value. The Autonomy acquisition was even worse—not just expensive but fraudulent. Even smaller deals like Palm failed to deliver strategic value.

The pattern reveals several mistakes. First, HP consistently overpaid, especially when desperate for transformation. Second, integration was always harder than expected—cultures clashed, systems didn't mesh, key people left. Third, HP bought companies to enter new markets rather than strengthen existing positions, a strategy that rarely works in technology.

The successful acquisitions were different—small, focused, and complementary. The LaserJet business was built through acquiring Canon's technology and improving it. The early test equipment acquisitions added products to existing channels. The lesson: in technology, organic innovation beats transformational M&A almost every time.

Managing Complexity: The Conglomerate Trap

HP's evolution from focused instrument maker to sprawling conglomerate illustrates the challenges of managing complexity. Each new business made sense individually—computers to control instruments, printers to output computer data, services to support hardware. But collectively, they created an unmanageable entity.

The different businesses had different economics, customers, and competitive dynamics. Printers generated huge margins but faced disruption from digital documents. PCs had scale but commodity economics. Enterprise systems required long sales cycles and deep technical support. Services demanded different skills than hardware manufacturing.

The 2015 split was recognition that conglomerate structures don't work in technology. Unlike industrial companies that can share manufacturing and distribution, technology businesses require focus. The lesson: growth through adjacency has limits. At some point, complexity costs exceed diversification benefits.

The Innovator's Dilemma Played Out

Clayton Christensen could have written "The Innovator's Dilemma" about HP. The company consistently failed to see disruptions that threatened its core businesses. It dismissed the Apple I because it didn't meet professional standards. It ignored inkjet technology initially because laser printing was more profitable. It missed the mobile revolution entirely despite acquiring Palm.

The pattern was always the same: HP's existing customers didn't want the new technology, so HP didn't pursue it. By the time customers changed their minds, competitors had established dominant positions. HP was always playing catch-up, buying companies like Palm or Autonomy to enter markets it should have pioneered.

The lesson is that successful companies must disrupt themselves. They need separate organizations to pursue emerging opportunities, different metrics for evaluating new businesses, and willingness to cannibalize existing products. HP occasionally tried—creating separate divisions for new businesses—but never committed fully. The antibodies of the existing business always won.

Culture vs. Strategy: The False Choice

HP's decline is often framed as choosing strategy over culture—abandoning the HP Way for financial performance. But this misses the point. The real failure was believing they were separate. The HP Way wasn't soft management—it was a strategy for attracting talent, encouraging innovation, and building sustainable advantage.

When HP abandoned its culture without replacing it, it lost its strategic differentiation. Every CEO tried to import their own culture—Fiorina's celebrity centralization, Hurd's operational brutality, Apotheker's strategic grandiosity. None stuck because culture can't be imposed from above. It must be built over time, reinforced by actions, and embodied by leadership.

The lesson is that culture and strategy are inseparable in knowledge businesses. Culture determines what strategies are possible—collaborative cultures can't execute command-and-control strategies, aggressive cultures can't sustain patient innovation. HP's tragedy wasn't choosing wrong strategies but destroying the culture that made any strategy possible.

The Cost of CEO Musical Chairs

HP's CEO revolving door cost more than the $83 million in severance payments. Each transition destroyed momentum, confused employees, and delayed decisions. Projects started under one CEO were cancelled by the next. Strategies announced with fanfare were quietly abandoned. Customers and partners didn't know what HP stood for or where it was heading.

The hidden costs were even greater. Talented executives left rather than endure another transition. Innovation stalled as engineers waited to see if their projects would survive. The best people avoided HP, not wanting to join a company in perpetual crisis. The company that once attracted Stanford's brightest became a place ambitious people avoided.

The lesson extends beyond HP: leadership stability matters more than leadership perfection. A decent CEO who stays for a decade creates more value than brilliant CEOs who last two years. Strategies need time to work, relationships need time to build, cultures need time to develop. HP's board never learned this lesson, always seeking the next savior rather than supporting the current leader.

IX. Power Analysis & Bear vs. Bull Case

Current Competitive Position

HP Inc. in 2024 occupies a peculiar position—dominant in declining markets, profitable but not growing, cash-rich but strategically constrained. The company generates billions in free cash flow but struggles to find growth investments. It returns most cash to shareholders through dividends and buybacks, essentially managing decline rather than driving growth.

In PCs, HP maintains the second-largest global market share but faces structural headwinds. PC refresh cycles are lengthening as devices become more durable. Cloud computing reduces the need for powerful local machines. Tablets and smartphones handle tasks that once required PCs. The market isn't dying but it's mature, with competition focused on price rather than innovation.

The printer business presents a different challenge. HP dominates the market but faces existential questions. Digital documents reduce printing needs. Environmental concerns discourage paper use. Work-from-home reduces office printing. HP's response—blocking third-party cartridges, firmware restrictions, subscription services—generates cash but destroys goodwill. It's a strategy that maximizes short-term profits while accelerating long-term decline.

Bear Case: The Declining Empire

The bear case for HP is straightforward: it's a melting ice cube, generating cash while slowly shrinking. Both core businesses face structural decline that no amount of operational excellence can offset.

In PCs, HP competes against Lenovo's scale advantages and Dell's direct model efficiency. Chinese manufacturers like Xiaomi and Huawei are entering Western markets with competitive products at lower prices. Component standardization means differentiation is nearly impossible. HP is trapped in a commodity business where only scale matters, and it lacks the scale to win.

The printer business is even more challenged. HP's aggressive monetization tactics—blocking third-party ink, forcing subscription services, preventing repairs—suggest a company extracting maximum value before the end. Younger consumers don't own printers. Businesses are going paperless. The installed base is aging and shrinking. HP is optimizing a dying business rather than building a new one.

Innovation efforts have consistently disappointed. 3D printing remains niche despite years of investment. Gaming PCs compete in a crowded market dominated by specialists. Commercial PCs and workstations face competition from cloud services. HP spends billions on R&D but produces little breakthrough innovation.

The financial engineering can't continue forever. Share buybacks boost EPS but don't create value. Dividends satisfy income investors but signal lack of growth opportunities. Cost cutting has limits—HP has already eliminated tens of thousands of jobs. Eventually, the cash generation will decline, and financial engineering won't hide operational challenges.

Corporate governance remains problematic. While less dysfunctional than the 2000s, HP's board lacks technology visionaries. Management is competent but not transformational. The company culture, once its greatest asset, is a shadow of its former self. HP feels like a company managing decline rather than building the future.

Bull Case: The Cash Machine

The bull case rests on HP's remarkable cash generation and potential for operational improvement. The company generates over $3 billion in annual free cash flow with minimal capital requirements. This cash funds generous shareholder returns while leaving room for strategic investments.

The printer business, despite challenges, remains a cash cow. HP's installed base of hundreds of millions of printers creates recurring revenue streams. Supplies generate 60%+ gross margins. Commercial printing remains strong. Even with secular decline, the business could generate cash for decades. Smart management could extend the runway through new services, managed print solutions, and commercial applications.

PCs aren't the growth business they once were, but they're not disappearing either. Remote work created permanent demand increase. Gaming PCs are growing. Commercial refresh cycles, while longer, still exist. HP's brand, distribution, and service capabilities create competitive advantages. Market share gains are possible as smaller competitors exit.

New opportunities exist despite past failures. 3D printing could eventually reach inflection point. AI PCs might drive refresh cycle. Subscription services could stabilize revenues. Digital manufacturing creates new printing applications. HP has the resources to invest in these opportunities while returning cash to shareholders.

Valuation provides margin of safety. HP trades at single-digit P/E ratios, reflecting extreme pessimism. The dividend yield exceeds 3%. Share buybacks reduce share count by 5-7% annually. Even modest operational improvement could drive significant multiple expansion. The market is pricing HP for extinction when gradual decline is more likely.

Management is finally realistic about challenges. Unlike previous CEOs who promised transformation, current leadership focuses on execution and cash generation. They're not wasting money on moonshots or transformational acquisitions. This pragmatism might not excite growth investors but it protects value for shareholders.

Power Dynamics and Competitive Advantages

Despite its challenges, HP retains some competitive advantages. Brand recognition remains strong, particularly in commercial markets. Distribution relationships span decades. Service and support infrastructure is extensive. These aren't revolutionary advantages but they create barriers to entry and switching costs.

HP's scale, while not industry-leading, still matters. The company can negotiate component prices, invest in R&D, and maintain global operations. Smaller competitors can't match HP's reach or resources. In mature markets, these advantages matter more than innovation.

The installed base creates lock-in effects. Businesses with thousands of HP PCs and printers face switching costs. IT departments know HP products. Procurement processes favor incumbents. These factors slow share loss even when competitors offer better value.

X. Epilogue: Lessons from Silicon Valley's First Child

HP's journey from garage startup to global giant to troubled incumbent spans the entire history of Silicon Valley. The company that invented the Silicon Valley way of doing business—stock options, open offices, casual culture—also demonstrated how that model could fail. The lessons extend far beyond HP to every technology company grappling with growth, scale, and disruption.

The Technology Company Lifecycle

HP's evolution reveals a consistent pattern in technology companies. They begin with breakthrough innovation, driven by founders with technical vision. Early success comes from product superiority and cultural differentiation. Growth brings professional management, public markets, and pressure for quarterly results. Scale creates complexity, bureaucracy, and distance from customers. Eventually, the company becomes what it once disrupted—slow, political, and defensive.

This lifecycle isn't inevitable but it's common. Apple avoided it through Steve Jobs' return and ruthless focus. Microsoft escaped it by embracing cloud computing under Satya Nadella. Amazon perpetuates Day 1 thinking through mechanisms and culture. But these are exceptions. Most technology giants follow HP's path from innovation to optimization to decline.

The pattern suggests structural forces at work. Public markets demand predictable growth. Scale requires process over intuition. Success creates conservatism. Employees who joined for stock options stay for stability. The very mechanisms that enable growth—professional management, systematic processes, risk management—destroy the capabilities that created growth.

The Importance of Succession Planning

HP's founder transition was remarkably smooth. Bill Hewlett and David Packard groomed successors, stayed involved as advisors, and maintained cultural continuity. The company thrived for decades after they stepped back. But when that generation retired, succession planning collapsed.

Each CEO was chosen to fix their predecessor's mistakes rather than build on their successes. The board looked outside for saviors rather than developing internal talent. Cultural continuity was sacrificed for strategic pivots. The result was expensive failure—billions in severance, destroyed value, and organizational chaos.

The lesson is that succession planning must be continuous and cultural. Companies need deep benches of leaders who understand the business and embody its values. Boards must resist the temptation to hire outsiders promising transformation. Strategic evolution beats revolution almost every time.

How Culture Gets Lost

HP didn't lose its culture overnight. It eroded through thousands of small decisions—a layoff here, a process there, a compromise everywhere. Each decision made sense individually but collectively transformed the company. The HP Way became a slogan rather than lived experience.

The mechanics of cultural decay are predictable. Growth dilutes founding culture as new employees outnumber old. Geographic distribution makes informal coordination impossible. Professional managers import "best practices" that conflict with existing norms. Financial pressure forces short-term thinking. Eventually, the company has the same culture as every other large corporation.

Preserving culture requires intentional effort. Amazon's leadership principles aren't just words but hiring criteria and promotion requirements. Netflix documents its culture explicitly and enforces it ruthlessly. Google's 20% time institutionalizes innovation. These mechanisms feel artificial compared to organic culture but they're necessary at scale.

Parallels to Today's Giants

HP's story offers warnings for today's technology leaders. Google faces similar challenges—dominant in search but struggling to find new growth, criticized for abandoning "Don't be evil" culture, cycling through messaging apps and social networks without success. Meta confronts questions about its core business while betting billions on unproven metaverse visions. Even Apple, seemingly invincible, depends heavily on iPhone revenues in a mature smartphone market.

The parallels are striking. Like HP with printers, these companies have cash-cow businesses funding speculation. Like HP's board in the 2000s, some face governance challenges and regulatory scrutiny. Like HP's failed transformations, their moonshots often disappoint. The question isn't whether they'll face HP's challenges but how they'll respond.

Some lessons from HP's failure seem obvious. Don't abandon core culture for quarterly earnings. Don't pursue transformational M&A from positions of weakness. Don't cycle through CEOs seeking silver bullets. Don't optimize dying businesses at the expense of customer relationships. But knowing lessons and applying them are different things.

Can Legacy Tech Companies Reinvent Themselves?

HP's struggles raise fundamental questions about corporate reinvention. Can a company successful in one era transform for another? Can culture evolve without dying? Can public companies make long-term bets against short-term pressure?

The evidence is mixed. IBM successfully transformed from mainframes to services to AI, though at great cost. Microsoft reinvented itself under new leadership. Intel is attempting similar transformation today. But for every success, there are multiple failures—Sun Microsystems, Digital Equipment Corporation, Compaq, and arguably HP itself.

The challenge is that transformation requires capabilities that success destroys. Innovation needs risk-taking that mature companies avoid. Speed requires autonomy that scale prevents. Culture change needs crisis that success prevents until too late. By the time transformation is obviously necessary, it's often impossible.

HP's split represents one answer—when transformation proves impossible, division might work. HP Inc. and HPE are both more focused and manageable than the combined entity. Neither will recapture the glory days but both might survive and even thrive in their niches. Sometimes accepting limitations beats pursuing transformation.

Final Assessment

HP's place in technology history is secure but complicated. It created Silicon Valley's culture, pioneered management practices now considered essential, and built multiple breakthrough businesses. But it also squandered advantages, destroyed value, and lost its way so completely that splitting up became the only option.

The company that exists today—HP Inc.—is profitable but uninspiring, successful but not triumphant. It generates cash, serves customers, and employs thousands. But it doesn't change the world, inspire entrepreneurs, or define the future. It's a perfectly acceptable Fortune 500 company, which is perhaps the saddest epitaph for the organization that invented Silicon Valley.

Yet HP endures. The company founded in 1939 still operates in 2024, having survived wars, recessions, technological disruptions, and self-inflicted disasters. That resilience counts for something. In an industry where companies rise and fall in decades, HP's 85-year run is remarkable. The garage startup became a global giant, stumbled badly, but continues forward.

The ultimate lesson from HP's journey might be about corporate mortality. Companies, like people, have lifecycles. They're born, grow, mature, and eventually decline. The goal isn't immortality but meaningful contribution during existence. By that measure, HP succeeded spectacularly. It created an industry, employed millions, generated trillions in economic value, and showed the world how technology companies could operate.

That legacy survives even as the company struggles. Every Silicon Valley startup that offers stock options, every technology company with open offices, every CEO who manages by walking around owes something to HP. The company that Bill Hewlett and David Packard started in a garage didn't just build products—it built an ecosystem that transformed the world.

XI. Recent News & Market Dynamics

As of late 2024 and early 2025, HP Inc. continues navigating a challenging environment with both headwinds and opportunities emerging. The company's latest financial results and strategic announcements provide insight into its current trajectory and future prospects.

HP announced fiscal 2025 first quarter net revenue of $13.5 billion, up 2.4% from the prior-year period, marking the third consecutive quarter of revenue growth after several quarters of decline. This modest growth suggests stabilization in HP's core markets, though hardly the dramatic transformation some investors hope for.

The company is adapting to new geopolitical realities. HP's outlook reflects the added cost driven by the current U.S. tariff increases on China, and by the end of fiscal year 2025, expects more than 90 percent of HP products sold in North America will be built outside of China. This supply chain diversification represents both a challenge and an opportunity—higher short-term costs but reduced long-term geopolitical risk.

Leadership continues emphasizing operational excellence over transformation. CEO Enrique Lores focuses on "bringing terrific innovation to our customers while driving disciplined execution across every facet of the business." This pragmatic approach lacks the excitement of previous CEOs' grand visions but has delivered more consistent results.

The controversy around HP's printing practices continues to escalate. Environmental groups and consumer advocates increasingly challenge HP's business model, with potential regulatory implications. The European Union is considering right-to-repair legislation that could force HP to allow third-party cartridges and repairs. Such changes would significantly impact HP's most profitable business.

AI represents both opportunity and threat. HP is positioning itself in the "AI PC" market, arguing that local AI processing will drive a refresh cycle. But cloud-based AI services might reduce the need for powerful local hardware. HP's ability to capitalize on AI remains uncertain, especially given its historical struggles with emerging technologies.

The competitive landscape continues evolving. Chinese manufacturers are becoming more sophisticated, moving beyond price competition to innovation. Cloud computing continues reducing demand for traditional PCs and printers. Younger consumers have different technology preferences than HP's traditional customers. These trends suggest HP's challenges will intensify rather than diminish.

XII. Conclusion: The Price of Lost Purpose

HP's story is ultimately about purpose—having it, losing it, and struggling to find it again. Hewlett and Packard didn't start their company to maximize shareholder value or achieve market dominance. They wanted to make useful things with people they respected. That simple purpose created one of history's great technology companies.

When HP lost that purpose—through growth, pressure, and leadership changes—it lost its way. Each CEO tried to give HP new purpose: Fiorina's transformation, Hurd's optimization, Apotheker's reinvention, Whitman's stabilization. But purpose can't be imposed from above or changed with strategy. It must emerge from identity and values.

Today's HP Inc. has a purpose of sorts—generating cash for shareholders while serving customers in declining markets. It's not inspiring but it's honest. The company no longer pretends to be changing the world or defining the future. It makes PCs and printers, returns cash to shareholders, and employs thousands of people. There are worse purposes for a corporation.

But the contrast with HP's origins is stark. The company that invented Silicon Valley's culture now embodies corporate America's challenges. The organization that pioneered management innovation now struggles with basic governance. The firm that created entire industries now optimizes declining businesses.

This transformation wasn't inevitable. Different decisions at crucial moments might have preserved more of HP's original character. But path dependence is powerful. Each compromise made the next easier. Each quarter's pressure justified further drift. Eventually, HP became what its founders would have barely recognized—a normal corporation struggling with normal corporate problems.

The lesson for today's technology companies is clear: purpose matters more than strategy, culture more than capability, values more than value. These soft factors are easy to dismiss when growth is strong and competition is weak. But when markets mature and disruption threatens, they determine survival.

HP's endurance, despite everything, offers hope. The company survived terrible leadership, failed strategies, and massive disruption. It's smaller and less dynamic than at its peak, but it continues. Sometimes survival is success enough. Sometimes endurance is its own form of victory.

The garage at 367 Addison Avenue is now a museum, carefully preserved to look exactly as it did in 1939. Tourists come to see where Silicon Valley began, to understand how two engineers with $538 created a global industry. The garage is empty now, holding memories rather than making products. It's a perfect metaphor for HP itself—historically important, carefully maintained, but no longer creating the future.

Yet even empty garages serve purposes. They remind us where we came from. They teach us what's possible. They warn us what can be lost. HP's journey from that garage to global giant to troubled incumbent isn't just corporate history. It's Silicon Valley's creation myth, cautionary tale, and ongoing experiment in whether technology companies can endure across generations.

The answer remains uncertain. HP Inc. might gradually decline, becoming less relevant each year until it's acquired or liquidated. It might find new growth in unexpected areas, reinventing itself once more. It might continue as is—profitable but uninspiring, successful but not triumphant.

Whatever happens, HP's legacy is secure. The company changed how businesses operate, how technology develops, and how we think about corporate culture. It created immense value even while destroying shareholder wealth. It employed millions even while laying off thousands. It defined an industry even while losing its way.

That's the paradox of HP—simultaneously one of technology's great successes and failures. The company that showed the world how to build technology businesses also showed how to destroy them. The organization that created Silicon Valley's culture also demonstrated its limitations. The firm that Bill Hewlett and David Packard started in a garage became everything they opposed, yet somehow still embodies their spirit.

In the end, HP's story isn't about technology or business strategy or financial engineering. It's about the human challenge of maintaining purpose and values while adapting to change. It's about the tension between preservation and transformation, between honoring the past and embracing the future. It's about what happens when companies outlive their founders, their missions, and sometimes their markets.

These challenges aren't unique to HP. Every successful company eventually faces them. Every organization that survives long enough must navigate the transition from startup to giant, from innovation to optimization, from purpose to profit. HP just did it first, most publicly, and with the most dramatic consequences.

The company that invented the rules of Silicon Valley also broke them all. The organization that defined technology management also demonstrated its failures. The firm that began in a garage with infinite possibilities now manages decline in glass towers. It's a tragedy, a cautionary tale, and oddly, still an inspiration.

Because despite everything—the failed mergers, the fired CEOs, the lost culture, the strategic confusion—HP endures. The company that began in 1939 continues in 2024. It's not what it was, might never be what it could have been, but it's still here. In Silicon Valley, where companies rise and fall in years, that's no small achievement.

The garage startup became a global giant, lost its way, split itself apart, and continues forward. It's not the ending Bill Hewlett and David Packard imagined, but it's not an ending at all. It's just another chapter in the ongoing story of American business, Silicon Valley culture, and the eternal challenge of maintaining purpose while managing change.

HP's story continues, less dramatic than before but still unfolding. Every quarter brings new results, every year new challenges, every decade new questions about relevance and survival. The company that invented Silicon Valley might not define its future, but it remains part of its present. That's more than most garage startups achieve. That's more than most giants sustain. That's HP—diminished but not defeated, struggling but not surrendering, forever linked to both Silicon Valley's greatest triumphs and its most sobering lessons.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube