Finolex Cables: The Story of India's Wire & Cable Pioneer

Introduction: The Origins of India's Cable Empire

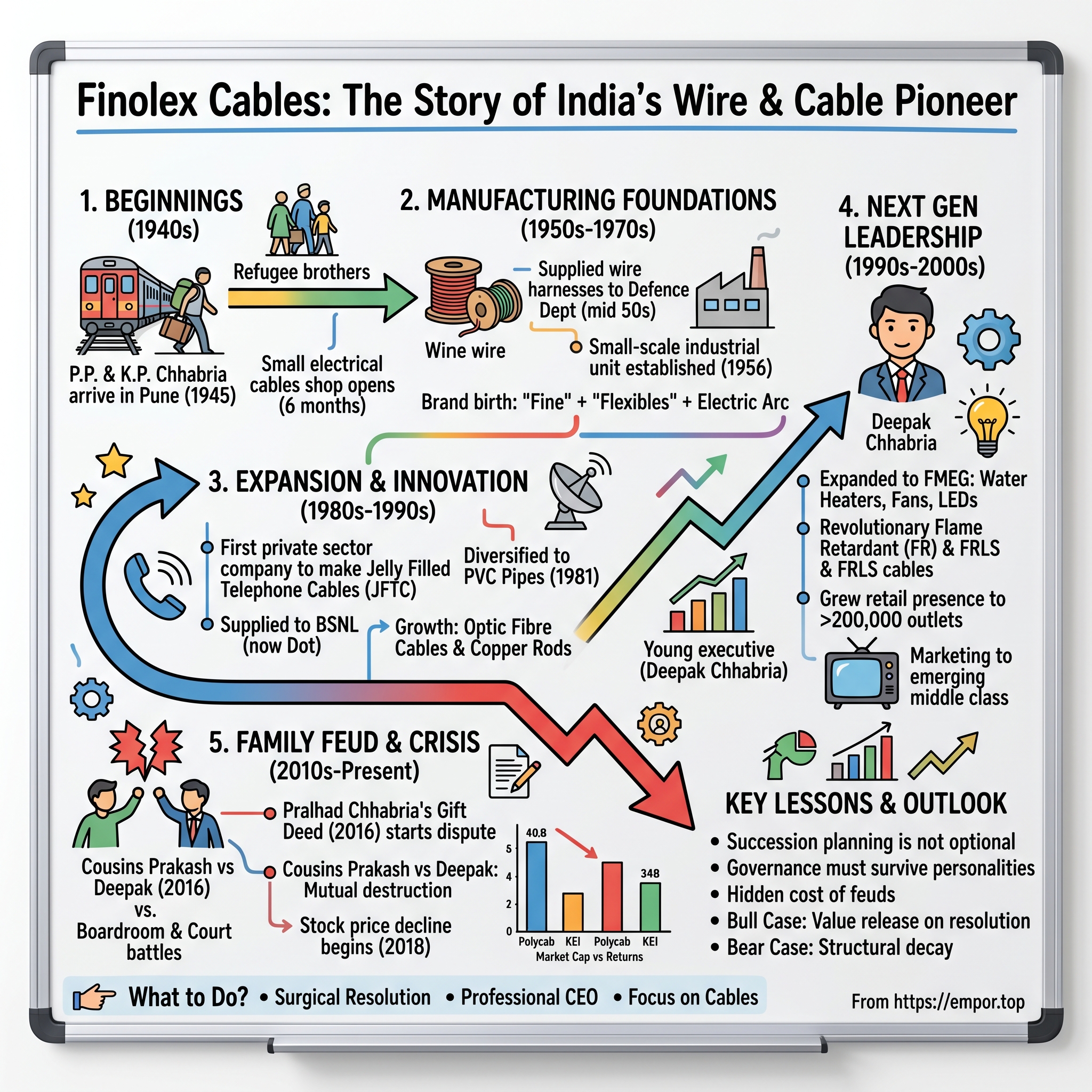

Picture this: a sweltering day in the late 1940s, just after the chaos of Partition. Two young brothers, carrying little more than determination and dreams, step off a train in Pune. They've left everything behind in Karachi—their home, their networks, their certainties. P.P. Chhabria and K.P. Chhabria arrived in July 1945, seeking a new livelihood. Within six months, they'd scraped together enough to open a small electrical cables shop. They couldn't have imagined that this modest beginning would spawn one of India's most storied cable empires—or that seven decades later, their grandsons would tear it apart in corporate India's most bitter family feud.

The question haunts every investor who's watched Finolex Cables Limited crater in recent years: How did the refugees who built India's cable infrastructure giant become the family that destroyed billions in shareholder value? The market cap stands at ₹12,434 crores, down a staggering 43.9% in just one year. While competitor stocks soar, Finolex languishes, trapped not by market forces but by a Shakespearean tragedy playing out in boardrooms and courtrooms across India.

This is more than a business story—it's a parable about what happens when family businesses fail to plan succession, when cousins turn combatants, and when ego trumps enterprise. It's about two branches of a family tree that grew so far apart they forgot they shared the same roots. The decline in the cable manufacturer's stock price began in 2018 when the fight between Deepak and Prakash Chhabria became public.

Today, we'll journey from those first desperate days in post-Partition Pune to the gleaming corporate offices where Deepak Chhabria and Prakash Chhabria—sons of the original founders—now wage war as chairmen of the group's flagship companies. We'll explore how a company that pioneered everything from PVC cables to fiber optics, that built the backbone of India's telecom revolution, now finds itself hamstrung by the very family that created it. Along the way, we'll uncover the business lessons hidden in this cautionary tale: about governance, about succession, about the unique challenges of family enterprises in emerging markets.

Because ultimately, this isn't just the story of Finolex. It's the story of Indian capitalism itself—its promise, its perils, and the price of putting family before fiduciary duty.

The Partition Refugees Who Built an Empire

The monsoon of 1945 brought two brothers, P.P. and K.P. Chhabria, to Pune from Karachi. Like millions displaced by Partition, they arrived with nothing but determination. Within six months, they established a small electrical cables shop, marking the beginning of their journey to reshape India's industrial landscape.

Picture the scene: a cramped shop in Pune's bustling market, the brothers haggling over prices, learning the local language, building trust one customer at a time. The retail business became quite successful. But success in post-independence India meant something different—it meant nation-building, it meant creating what the country desperately needed but couldn't import.

The turning point came with an order that would have intimidated established manufacturers. A sizeable order in the mid 1950's from the Defence Department for wire harnesses for trucks and tanks bolstered their confidence and they decided to manufacture Cables, themselves. Think about that audacity—two refugees with a retail shop deciding to supply the Indian military. This wasn't just business expansion; it was a leap of faith in a nation still finding its feet.

Starting as a small-scale industrial unit in 1956, they manufactured PVC insulated cables for the automobile industry. The timing was perfect. India's first Five Year Plan was in full swing, Nehru's vision of industrial self-reliance was taking shape, and here were two brothers ready to answer the call.

The brand name itself told their story. Finolex brand was born from "Fine" & "Flexibles" and "O" with an electric arc across it - signifying the electrical cable business the company was in. Simple, memorable, and distinctly Indian—a brand that would outlive its founders and their feuding descendants.

What set the Chhabrias apart wasn't just their business acumen but their immigrant's hunger. They knew what it meant to lose everything and start over. This wasn't inherited wealth or colonial connections—this was pure, relentless hustle. They worked eighteen-hour days, reinvested every rupee, and slowly built relationships that would span decades.

The brothers complemented each other perfectly. Pralhad (P.P.) was the visionary, always looking at the bigger picture, while Kishandas (K.P.) was the operations wizard, ensuring quality and efficiency. Together, they navigated the treacherous waters of India's License Raj, where a single permit could make or break a business.

By the late 1960s, Finolex wasn't just surviving—it was thriving. The company had become a trusted supplier to India's growing automotive industry, and the brothers were eyeing bigger opportunities. They understood a fundamental truth: in a developing economy, infrastructure is destiny. And India needed cables—millions of kilometers of them—to electrify villages, connect cities, and power industries.

Their relentless search for growth and doughty perseverance saw them through some difficult times and in 1972 the enterprise turned into a limited company. This transformation from partnership to corporation marked their arrival as serious players in Indian industry. No longer just refugees making good, they were now industrialists shaping India's future.

From Small Shop to Manufacturing Pioneer (1956-1972)

The transformation from refugee-run workshop to industrial powerhouse happened not through luck but through an almost obsessive focus on quality and timing. In 1958, the brothers formally incorporated their venture, marking the birth of what would become India's cable giant. But the real story of this period wasn't in the paperwork—it was in the factory floors where innovation met necessity.

Imagine walking into their first proper manufacturing facility in 1960s Pune. The smell of hot PVC, the rhythmic hum of extrusion machines imported at great expense, workers meticulously testing each meter of cable. The Chhabrias weren't just manufacturing products; they were building a reputation. Every cable that left their factory carried with it the promise that Indian manufacturing could match international standards.

The License Raj era of the 1960s and early 1970s should have strangled a company like Finolex. Getting permits to import machinery required months of applications, bribes were expected at every turn, and established players with political connections dominated the market. But the brothers had learned survival in the crucible of Partition. They knew how to wait, when to push, and most importantly, how to build relationships that transcended mere transactions.

Their masterstroke came in understanding that India's industrial policy, despite its flaws, created protected markets for those who could navigate the system. While foreign competition was kept at bay, domestic demand was exploding. Every new factory needed cables, every housing colony required wiring, every government office demanded electrical infrastructure. The Chhabrias positioned themselves not as suppliers but as partners in nation-building.

By 1970, Finolex had become synonymous with reliability in industrial circles. Their cables powered textile mills in Coimbatore, automobile factories in Chennai, and engineering workshops across the industrial belt. But the brothers knew that remaining a partnership firm would limit their ambitions. India was changing, and they needed to change with it.

Their relentless search for growth and doughty perseverance saw them through some difficult times and in 1972 the enterprise turned into a limited company. This wasn't just a legal formality—it was a declaration of intent. The transformation marked their evolution from traders to industrialists, from survivors to builders.

The timing couldn't have been better. India's economy was about to undergo seismic shifts. The oil crisis of 1973 would test every manufacturer's resilience, but it would also create opportunities for those with the foresight to adapt. The Chhabrias had built more than a company—they had built a fortress of financial prudence and operational excellence that could weather any storm.

Since then, there has been no looking back and following a public offering in July 1983, Finolex Cables Limited embarked on a continuous process of expansion and modernisation. The IPO wasn't just about raising capital—it was about democratizing ownership, bringing in professional management, and preparing for the next phase of growth that would transform Finolex from a regional player to a national champion.

The Telecommunications Revolution & Diversification (1980s-1990s)

The late 1980s marked a watershed moment in Finolex's journey. While most Indian companies were content serving domestic markets, the Chhabria brothers saw something transformative on the horizon—India's telecommunications revolution. In the late 80s, the unfolding possibilities in the telecommunications sector led the management to put in place strong growth drivers and Finolex Cables became the first private sector company in India to manufacture Jelly Filled Telephone Cables (JFTC), technology that would become the backbone of India's landline network.

Consider the audacity of this move. The Department of Telecommunications (DoT, later BSNL) was a monolithic government entity with its own preferences, procedures, and prejudices against private suppliers. Breaking into this market required not just technical capability but diplomatic finesse. The Company successfully supplied to National Telecom Provider DoT (now BSNL), becoming one of the few private players trusted with building India's communication infrastructure.

The JFTC technology wasn't just about cables filled with petroleum jelly to prevent moisture ingress—it represented India's first serious attempt at telecommunication self-reliance. Every kilometer of JFTC cable laid meant villages getting connected, businesses establishing networks, and families staying in touch across the vast subcontinent. In fact, every year Bharat Sanchar Nigam Ltd. (BSNL) (erstwhile DoT) has been purchasing JFTC at a growth of approximately 20%.

Meanwhile, the brothers weren't content with single-product dominance. Their relentless quest for growth saw the brothers establishing Finolex Industries Limited (FIL) in 1981. The company sought to manufacture Rigid PVC Pipes and Fittings, targeting India's agricultural sector. This wasn't diversification for its own sake—it was strategic vertical integration. By controlling their PVC supply chain, they could ensure quality and manage costs in their cable business while opening entirely new revenue streams.

The 1990s brought both triumph and disruption. The early nineties saw the Finolex Group expanding into new business domains to manufacture Optic Fibre Cables and Copper Rods. The fiber optic venture was particularly prescient. While copper cables still dominated, the Chhabrias understood that data, not just voice, would drive future communication needs.

But then came the disruption nobody saw coming. The late 1990s witnessed the advent of mobile phones, which fundamentally challenged the landline-centric telecom infrastructure Finolex had mastered. Suddenly, those kilometers of JFTC cables seemed less essential. Villages that had waited decades for landline connections leapfrogged directly to mobile technology. It was India's own version of technological disruption—brutal, swift, and transformative.

Yet Finolex's response revealed the company's resilience. Rather than retreat, they doubled down on diversification. Having mastered this technology, Finolex has been exporting JFTC and in the last two years having recorded a growth of more than 200% in exports. While India moved to mobile, developing nations in Africa and Southeast Asia still needed copper infrastructure. The company that had built India's telecom backbone was now exporting that expertise globally.

The telecommunications revolution taught Finolex a crucial lesson: in technology markets, today's breakthrough is tomorrow's obsolescence. The company that had pioneered JFTC cables in India now had to reinvent itself for the digital age. This ability to adapt, to see disruption not as threat but opportunity, would define Finolex's next chapter—and set the stage for both its greatest triumphs and most bitter conflicts.

Next Generation Leadership: The Deepak Chhabria Era

The year 1986 marked more than a generational transition—it heralded a fundamental reimagining of what Finolex could become. In 1986, Mr. K.P. Chhabria's son, Mr. Deepak Chhabria, joined the company after completing his studies in the USA. Picture a young man, trained at the University of Evansville in engineering management, returning to a company still operating like a traditional Indian family business. The contrast must have been stark—American MBA theories meeting Indian market realities.

What Deepak saw wasn't just a cable company but a sleeping giant. Transforming Finolex from a one-product, one-client company, he diversified the product portfolio and expanded the customer base. This wasn't mere tinkering at the margins. Within a decade, he had orchestrated one of Indian industry's most dramatic transformations.

The numbers tell only part of the story. As of FY24, they have 24.9% market share in the organized wire industry—a testament to three decades of relentless expansion and innovation. But the real revolution happened in the factories and R&D labs where Deepak pushed boundaries that his father's generation wouldn't have imagined possible.

Take the innovation in safety products. The standard multi-strand wire, for instance, remains a revolutionary concept, now a recognised compliance norm sought by BIS across the country. The company also spearheaded advancements in safety with the development of newer innovative products such as Flame Retardant (FR) cables, fire-resistant low-smoke (FRLS) cables. These weren't incremental improvements—they were paradigm shifts that saved lives in high-rise fires and industrial accidents.

The FR and FRLS cables story deserves special attention. As India's cities grew vertically in the 1990s and 2000s, fire safety became a critical concern. Traditional PVC cables would emit toxic fumes when burned, turning fires into death traps. Deepak's team developed cables that not only resisted flame but produced minimal smoke—crucial for evacuation in emergencies. Today, these cables are mandatory in hospitals, schools, and high-rises across India.

But perhaps Deepak's greatest achievement was transforming Finolex's distribution network. When he took charge, Finolex was essentially a B2B company selling to large buyers. Under his leadership, it has expanded its retail presence to over 200,000 outlets. Think about that scale—from Ladakh to Kanyakumari, from metropolitan showrooms to village hardware stores, Finolex products became ubiquitous.

The cultural transformation was equally profound. When I took control in the 90s, the decade was marked by the internet, digital and cable revolution. With AT&T, world leaders in communication technology, selecting us as a joint venture partner, we were empowered to meet emerging requirements of the information age. After break-up of AT&T in various divisions, the cable business was named Lucent and thus the JV became Lucent-Finolex. Lucent was later acquired by a Japanese company and Finolex retained the plant in lieu of its shares. These international partnerships brought global best practices to Pune's industrial corridors.

Deepak also understood that brand building in commoditized markets required more than quality—it needed aspiration. The company that once sold cables to government departments now marketed lifestyle products to India's emerging middle class. The tagline evolved from functional descriptions to emotional connections. Marketing moved from trade journals to primetime television.

His management style blended American professionalism with Indian relationship-building. I believe in 6 days hard work, spending Saturday night with friends and full Sunday with family, he once said, capturing his philosophy of intense work balanced with human connections. This wasn't the old patriarch model of management—it was collaborative, data-driven, yet deeply personal.

Under Deepak's leadership, Finolex didn't just grow—it transformed into a modern corporation while retaining its entrepreneurial spirit. The company that started in a Pune shop now competed with multinationals, exported to dozens of countries, and set industry standards. Yet this very success would sow the seeds of future conflict, as growth created complexity and complexity bred disagreement about the path forward.

The FMEG Expansion: From B2B to B2C (2010s-Present)

The pivot from industrial supplier to consumer brand represents one of Indian industry's most ambitious transformations—and perhaps its most challenging. Besides manufacturing a wide variety of wires and cables, Finolex has also forayed into the manufacturing of Fast-Moving Electrical Goods (FMEG) and home appliances. This wasn't just product diversification; it was a complete reimagining of what Finolex could be.

The FMEG market presented a tantalizing opportunity—₹50,000 crores and growing. But for a company that had spent six decades selling to electricians and contractors, reaching the end consumer required a cultural revolution. In its never-ending quest of providing total electrical solutions to its consumers, the company has expanded its portfolio to include a wide spectrum of products such as Electric Water Heaters, Fans, LED lights, Switches, Switchgear etc.

The challenge was formidable. Our market share is hardly 2 to 3 pc as of now in this category and we want to be in the top three in all the product categories in the coming three to four years. In fans, they competed with Orient and Crompton. In water heaters, with Bajaj and Racold. In switches, with Havells and Anchor. These weren't startups—they were entrenched players with decades of consumer relationships.

The marketing transformation was dramatic. Gone were the technical specifications and B2B catalogs. Enter Bollywood. Finolex Cables Limited, India's leading manufacturer of electrical and telecommunication cables, introduced Bollywood superstar Kartik Aaryan and Kiara Advani as brand ambassadors. The choice was deliberate—young, aspirational, and crucially, appealing to the urban millennial homeowner who had never heard of Finolex's industrial legacy.

The 'No Stress. Finolex' campaign captured more than a product promise—it reflected a generational shift in Indian consumption. The stressed-out urban professional didn't want to think about electrical fittings; they wanted solutions that just worked. There is a rising awareness among the new age consumers about safe, smart and stress-free home solutions.

The distribution strategy leveraged Finolex's greatest asset—its massive network. it has expanded its retail presence to over 200,000 outlets. But reaching retailers was one thing; convincing them to stock and push FMEG products from a wire company was another. The solution was ingenious—bundle products, leverage electrician relationships, and create pull through consumer advertising.

The company also recognized that rural markets, where Finolex had strong brand recognition from decades of cable sales, could be the backdoor to FMEG success. Farmers know Finolex very well because they are using our cables in their submersible pumps in their fields since ages. A farmer who trusted Finolex cables for his irrigation pump might trust their fans for his home.

Product innovation focused on bridging the organized-unorganized divide. The cost of an immersion rod is Rs.300 to 400—affordable enough to compete with local manufacturers but backed by Finolex's quality promise. Smart switches that worked with Alexa targeted urban professionals; basic immersion rods targeted rural households. It was portfolio management at its most sophisticated.

The digital transformation was equally ambitious. Virtual showrooms where customers could visualize products in their homes, apps for electricians to track rewards, IoT-enabled fans controlled by voice—Finolex was attempting to leapfrog established players through technology. That product range includes smart fans or lights which can be controlled with voice assistants like Alexa and Google Home.

Yet the execution challenges were immense. Building consumer brand equity takes years, even decades. Changing perception from "cable company" to "lifestyle electrical brand" required not just advertising but fundamental changes in product design, packaging, and customer service. The sales force, trained to sell by the kilometer, now had to sell aesthetics and convenience.

Financial results reflected both promise and struggle. New products within the FMEG sector grew by around 44% in value in the last quarter, impressive growth but from a tiny base. The company that dominated industrial cables with 25% market share was a minnow in consumer electricals with less than 3%.

The FMEG expansion represented more than business diversification—it was Deepak Chhabria's vision of Finolex's future, a consumer-facing conglomerate built on industrial foundations. But as the company stretched into new territories, internal tensions that had simmered for years would finally boil over into open warfare.

The Family Feud: When Cousins Collide

March 28, 2016. Remember that date—it's when the Finolex empire began its slow-motion implosion. On that day, patriarch Pralhad Chhabria, ailing and approaching death, signed a document that would tear his family apart. The deed transferred 70.4 per cent out of the 82.07 per cent of the holding company Orbit's shares, which made Prakash the majority owner in Orbit and thereby also the largest shareholder in FCL.

To understand the devastation this caused, you need to grasp the intricate web of cross-holdings the founders had created. The dispute began when their fathers, who jointly started the company, created a shareholding structure whereby Orbit held 31 percent shares in FCL and 19 percent in FIL. In turn, the two listed companies had cross-holdings, with FCL owning 32 percent of FIL, and FIL owning 15 percent of FCL. It was corporate structure as family compromise—everyone owned a piece of everything, forcing cooperation.

But that gift deed shattered the delicate balance. Deepak Chhabria, who had spent three decades building Finolex Cables into a consumer brand, suddenly found his cousin Prakash—who ran the pipes business—controlling his company through the holding structure. The Gift Deed, which was executed on 28.03.2016 in an extremely hasty manner, without any knowledge or information to the other branch of the family, is itself doubtful and under cloud of suspicion, Deepak's lawyers would later argue.

The human drama behind the legal battles is heartbreaking. "Pralhad and Kishan may have argued but actually sat together and ate their office lunch together for almost three decades," said a Finolex executive. The brothers had built an empire on trust and shared sacrifice. Now their sons were destroying it through mistrust and legal warfare.

The accusations flew thick and fast. Prakash Chhabria is moving to dismiss Deepak Chhabria, accusing him of destabilizing the equilibrium of the group and tarnishing the brand via multiple lawsuits. Meanwhile, Deepak claimed the gift deed was forged, that his uncle was too ill to understand what he was signing, that there had been previous documents—trust deeds, wills—that showed different intentions.

The corporate consequences were immediate and brutal. Two major corporate shareholders namely: Orbit Electricals Private Limited holding 30.7 per cent and Finolex Industries Limited holding 14.5 per cent aggregating to 45.2 per cent of the paid up share capital of the company voted against each of the resolutions for reappointments at board meetings. Suddenly, routine governance became warfare.

The September 29, 2023, Annual General Meeting became the Waterloo. Finolex Cables conducted its annual general meeting (AGM) on 29 September 2023 and one of the items on the agenda for voting by the shareholders was for the reappointment of Deepak Chhabria as a whole-time director designated as an 'executive chairman'. The consolidated scrutinizer's report reflected that 72.34 per cent of votes were against resolution Number 4. After decades of building the company, Deepak was voted out of his own firm.

The legal battles reached absurd heights. The Supreme Court initiated contempt proceedings against NCLAT members when they defied orders about voting results. Judges resigned, fines of crores were imposed, and corporate India watched in horror as one of its most respected business families tore itself apart in public.

What makes this tragedy particularly poignant is that both cousins are competent businessmen. Prakash successfully runs Finolex Industries, Deepak transformed Finolex Cables. In any rational world, they would collaborate, leveraging their different strengths. Instead, they're locked in mutually assured destruction.

The founder even wrote in his letters that "his relationship with his brother was unassailable". One wonders what Pralhad and Kishan Chhabria would think, watching from whatever afterlife entrepreneurs inhabit, as their life's work becomes a cautionary tale about succession planning. Maybe, despite his wisdom, Pralhad Chhabria realized that keeping peace amongst the next generations would be a challenge.

The dispute has created a governance nightmare. Independent directors resign rather than navigate the family minefield. Strategic decisions are paralyzed by shareholder conflicts. Management spends more time in courtrooms than boardrooms. And through it all, the stock price—that brutal arbiter of corporate value—continues its relentless decline.

Current State & Competitive Landscape

The numbers tell a story of squandered potential. Revenue: 5,484 Cr · Profit: 619 Cr might seem respectable in isolation, but context reveals the tragedy. While Finolex Industries stock has doubled over the previous five years, Finolex Cables has given its shareholders a meagre 10 per cent return over the same period. The low return partly is the result of Finolex Cables' slow sales growth, which compounded at 3 per cent over the last five years.

The competitive landscape has shifted dramatically while Finolex fought itself. Polycab reported a revenue of Rs. 14,108 Cr in FY23 which increased from Rs. 12,203 in FY22, scaling its revenue by 16% that year. Meanwhile, KEI Industries during the year increased its revenue by 40% from Rs. 5727 Cr in FY22 to Rs. 6912 Cr in FY23. These aren't just numbers—they represent market share bleeding away, customer relationships lost, opportunities forsaken.

The valuation disconnect is particularly painful. In terms of valuations, Finolex Cables trades at 14 times earnings while Polycab trades at 42 times earnings. The market has rendered its verdict: a company torn by internal strife is worth less than half its focused competitors, even with similar fundamentals.

Company is almost debt free. Company has a low return on equity of 13.2% over last 3 years. This paradox—financial strength coupled with poor returns—epitomizes Finolex's current state. It's like owning a Ferrari but being stuck in perpetual gridlock. The resources exist, but governance paralysis prevents their deployment.

The market share story is equally sobering. As of FY24, they have 24.9% market share in the organized wire industry—still formidable, but eroding. Competitors smell blood. Polycab is an undisputed leader when it comes to the Indian wiring & Cables segment with an approximate 22%-24% market share in the organized market. The gap is closing, and not in Finolex's favor.

Innovation has stalled while competitors surge ahead. The three key players in India's cables and wires segment reported a more than 25% YoY jump in quarterly revenue for the March quarter. Polycab India's total revenue grew by 25% YoY to ₹6,948 crore, KEI Industries saw a growth of 25.1% to ₹2,915 crore, and RR Kabel posted a 26% YoY jump in revenue at ₹2,217 crore. Finolex's growth? A fraction of these figures.

The operational metrics reveal deeper dysfunction. Working capital days have increased from 138 days to 225 days—cash tied up while competitors run lean. Management attention focused on courtrooms rather than customers. Strategic decisions deferred pending family settlements.

Even in segments where Finolex should dominate, it's losing ground. The company that pioneered telecom cables in India now watches as nimbler competitors capture 5G infrastructure contracts. The firm that introduced FR cables sees others winning safety-conscious contracts. Legacy without leadership is merely nostalgia.

The international comparison is damning. While Indian infrastructure booms, while Make in India creates unprecedented opportunities, while global supply chains reorganize post-pandemic, Finolex remains paralyzed. The wires and cables industry is experiencing significant growth, with a yearly increase of approximately 13% from FY 2019 to FY 2024. As demand rises across residential, commercial, infrastructure, and industrial sectors, there is a growing opportunity. Finolex watches this feast from outside, nose pressed against the window.

The tragedy isn't that Finolex is failing—it's that it's failing despite having everything needed to succeed. Brand recognition, distribution network, manufacturing capability, financial resources, technical expertise—all present. What's missing is the ability to deploy these assets coherently, strategically, aggressively. The family feud hasn't just damaged relationships; it's destroyed value creation capacity.

Playbook: Business & Investing Lessons

The Finolex saga offers a masterclass in how family businesses can self-destruct, but more importantly, it illuminates timeless principles about governance, succession, and value creation. Let's extract the lessons that transcend this specific tragedy.

Lesson 1: Succession Planning is Not Optional The founders' failure to clearly delineate ownership and control created a ticking time bomb. Cross-holdings and informal understandings work until they don't. The gift deed controversy could have been avoided with transparent, legally bulletproof succession planning executed while the patriarch was healthy. Every family business should have ironclad agreements about ownership transfer, voting rights, and management succession—signed, sealed, and communicated while founders are alive and competent.

Lesson 2: Governance Structures Must Survive Personalities Finolex's governance collapsed because it depended on family relationships rather than institutional structures. Independent directors became pawns, board meetings became battlegrounds. Strong companies build governance frameworks that function regardless of personal animosities. This means truly independent boards, clear escalation mechanisms, and decision-making processes that don't require family consensus.

Lesson 3: The Hidden Cost of Family Feuds The market cap destruction—down 43.9% while competitors soar—represents only the visible cost. The invisible costs are deadlier: talent exodus, customer defection, supplier nervousness, banker wariness. When leadership fights itself, the entire ecosystem loses confidence. The reputational damage takes decades to repair, if ever.

Lesson 4: Distribution as Moat, Innovation as Bridge Finolex's 200,000+ outlet network remains its greatest asset, but distribution without innovation is a wasting asset. Competitors can build distribution; they can't easily replicate decades of innovation culture. But when innovation stops—as it has during the feud—distribution becomes mere inertia, slowly eroding as hungrier competitors offer retailers better products, margins, and support.

Lesson 5: B2B to B2C Transformation Requires Total Commitment The FMEG expansion revealed a profound truth: you can't be half-pregnant with consumer businesses. Finolex's 2-3% market share in FMEG despite massive distribution shows that B2C success requires different DNA—marketing creativity, consumer insight, rapid iteration. Industrial companies venturing into consumer markets must be willing to fundamentally rewire their organizations, not just add product lines.

Lesson 6: Capital Allocation in Uncertainty Being debt-free sounds virtuous, but Finolex's low ROE despite zero leverage reveals capital allocation paralysis. In boom markets, conservative balance sheets mean missed opportunities. The company sits on cash while competitors leverage up to capture market share. Sometimes the biggest risk is taking no risk.

Lesson 7: The Compound Effect of Slow Growth Finolex's 3% revenue CAGR versus competitors' 15-40% growth rates demonstrates how quickly leaders become laggards. In rapidly growing markets, standing still means going backward. Market share loss compounds—lost customers become competitor references, missed contracts become competitor credentials, departing talent becomes competitor advantage.

Lesson 8: Valuation Reflects Governance Quality The PE multiple discount—14x versus Polycab's 42x—isn't about current earnings but future uncertainty. Markets ruthlessly punish governance dysfunction because it creates unquantifiable risk. No amount of cheap valuation compensates for the possibility that family disputes could escalate, paralyzing the company further or forcing value-destructive settlements.

Lesson 9: Industrial Brands Can Become Consumer Brands, But Rarely Finolex's struggle in FMEG highlights how difficult it is for industrial brands to gain consumer mindshare. Havells succeeded through decades of patient brand-building and acquisition. Most industrial companies are better off acquiring consumer brands than trying to build them. The skills, culture, and timelines are fundamentally different.

Lesson 10: The Agency Problem in Family Firms When family members prioritize personal battles over shareholder value, minority investors suffer most. The Finolex feud exemplifies the agency problem—managers (the family) pursuing objectives that destroy shareholder wealth. This is why many institutional investors simply avoid family-controlled businesses with unclear succession or visible conflicts.

Analysis & Bear vs. Bull Case

Bull Case: The Coiled Spring Thesis

The optimist sees Finolex as a compressed spring, ready to explode upward once the family feud resolves. The fundamentals remain intact—₹5,484 crores in revenue, debt-free balance sheet, 24.9% market share in organized wires, 200,000+ retail outlets. This is not a dying business but a constrained one.

Resolution of the promoter dispute could catalyze immediate re-rating. If the cousins settle, or if one buys out the other, governance concerns evaporate overnight. The stock could double simply on clarity, before any operational improvements. At 14x earnings versus peers at 40x+, the valuation gap offers massive upside potential.

The infrastructure supercycle is just beginning. India's ₹111 lakh crore infrastructure pipeline, housing boom, and industrial expansion will drive unprecedented cable demand. Finolex's established brand and distribution position it perfectly to capture this growth—if management can focus on business instead of battles.

The FMEG opportunity remains nascent. Despite current struggles, Finolex has barely scratched the surface of the ₹50,000 crore FMEG market. With focused execution, the company could achieve its stated goal of ₹500 crore revenue per category, adding ₹2,500 crores in high-margin revenue.

Technical expertise and manufacturing excellence haven't disappeared. The company's ability to produce everything from basic wires to sophisticated fiber optic cables remains intact. The innovation DNA that created FR and FRLS cables still exists in R&D labs and factory floors. It just needs leadership unity to unleash it.

Bear Case: The Slow Bleed Thesis

The pessimist sees structural decay that no settlement can reverse. Family feuds don't end with handshakes—they leave scars, create factions, poison cultures. Even if the cousins formally settle, the organization remains divided, dysfunctional, demoralized.

Competitive gaps are widening irreversibly. While Finolex stagnated, Polycab built international operations, KEI captured infrastructure projects, new players like RR Kabel went public with growth capital. These competitors have momentum, management bandwidth, and market confidence. Catching up requires more than peace—it requires excellence.

The FMEG expansion is a costly distraction. Competing with Havells, Bajaj, and Orient in consumer electricals while fighting internal battles is delusional. The 2-3% market share after years of effort suggests fundamental unsuitability for B2C markets. Every rupee invested in FMEG is a rupee not strengthening the core wire business.

Talent exodus and cultural damage may be permanent. The best managers don't wait around for family disputes to resolve. Key talent has likely migrated to competitors or startups. The employees who remain are those without options—hardly the foundation for a turnaround. Rebuilding human capital takes years, assuming it's even possible.

Commodity supercycles cut both ways. Rising copper prices, supply chain disruptions, and competitive intensity could squeeze margins even if volumes grow. The organized sector's growth attracts new entrants, including Chinese players and well-funded startups. Market share gains become harder and more expensive.

The valuation discount may be permanent. Some family-controlled companies trade at perpetual discounts due to governance concerns. Even if the current feud ends, investors will remember. The next succession crisis, the next family disagreement, the next governance failure—the market will price in these risks forever.

The Verdict

The truth, as always, lies between extremes. Finolex isn't dying, but neither is it poised for miraculous resurrection. It's a wounded giant, bleeding slowly while more agile competitors feast on its markets. The bull case requires not just family peace but exceptional execution in increasingly competitive markets. The bear case may be too pessimistic about the power of Finolex's inherited assets—brand, distribution, manufacturing.

For investors, Finolex represents a complex bet on human nature as much as business fundamentals. Can cousins who've spent years in bitter litigation suddenly collaborate? Can an organization traumatized by family warfare suddenly innovate? Can a company that's lost its growth muscle suddenly sprint?

The risk-reward depends entirely on your view of these human factors. If you believe in redemption, reconciliation, and renewal, Finolex offers asymmetric upside. If you believe that family feuds leave permanent damage, that competitive advantages erode irreversibly, that corporate cultures once broken stay broken, then Finolex is a value trap, not a value investment.

Epilogue & "What Would We Do?"

If we were parachuted into Finolex tomorrow with a mandate to maximize value, the playbook would be radical but necessary.

Priority 1: Surgical Resolution The family dispute must end, not with compromise but with clarity. One branch should buy out the other at a fair value determined by independent bankers. Yes, it's expensive. Yes, someone must swallow pride. But the cost of continuation far exceeds the cost of resolution. Every day of dispute destroys value multiples of what a settlement would cost.

Priority 2: Professional Management Post-settlement, the winning family branch should step back from operational management. Hire a CEO from outside—someone with no baggage, no loyalties, no history. Give them a five-year contract with aggressive performance incentives. Let professionals run the business while the family remains on the board for strategic oversight.

Priority 3: Portfolio Rationalization Exit FMEG within 18 months. Sell the business to Havells or Bajaj, who can actually extract value from it. Use proceeds to strengthen the core wire and cable business. Focus is not about doing less—it's about doing what you do better than anyone else. Finolex should dominate cables, not dabble in consumer electricals.

Priority 4: Innovation Acceleration Establish a ₹500 crore innovation fund focused on next-generation cable technologies—EV charging cables, renewable energy transmission, smart grid solutions, fire-resistant materials. Partner with IITs, collaborate with global leaders, acqui-hire startups. Reclaim the innovation leadership that built Finolex.

Priority 5: Distribution Transformation Convert the 200,000 outlet network from a passive asset to an active advantage. Implement digital ordering systems, provide credit solutions, offer training programs, create loyalty rewards. Make it irresistibly profitable for retailers to push Finolex products. Distribution without engagement is just geography.

Priority 6: Cultural Revolution Launch a massive cultural transformation program. Acknowledge the past, apologize for the disruption, articulate a compelling future vision. Implement performance-based promotions, profit-sharing programs, stock options for key employees. Make Finolex the employer of choice in the electrical industry again.

Priority 7: M&A Offense Use the debt-free balance sheet aggressively. Acquire regional cable companies for geographic expansion. Buy specialized cable technologies for capability enhancement. Consider international acquisitions for market access. Growth through acquisition can be faster than organic expansion, especially when starting from behind.

Priority 8: Capital Market Reset Once operational momentum returns, conduct a qualified institutional placement (QIP) to bring in marque institutional investors. Their presence would improve governance perception and provide external pressure for performance. Consider stock buybacks at current depressed valuations to signal confidence and reward patient shareholders.

Priority 9: Sustainability Leadership Launch India's first comprehensive cable recycling program. Commit to carbon neutrality by 2030. Develop bio-based cable insulation materials. Sustainability isn't just ethics—it's a competitive advantage in government contracts and corporate procurement.

Priority 10: Digital Transformation Build direct-to-consumer capabilities for premium products. Create an contractor super-app for ordering, training, and rewards. Implement AI-based demand forecasting to optimize inventory. Use IoT sensors in manufacturing for predictive maintenance. Digital isn't just efficiency—it's survival.

This playbook isn't fantasy—it's what any competent private equity firm would implement post-acquisition. The tragedy of Finolex isn't that it can't be fixed, but that the fix is so obvious yet so impossible given current dynamics.

The larger lesson for Indian capitalism is stark: family businesses that fail to professionalize don't just stagnate—they destroy value for all stakeholders. As India's economy matures, as capital markets deepen, as governance standards rise, the Finolex model—brilliant founders, feuding heirs, paralyzed companies—must become extinct.

For Finolex itself, the clock is ticking. Every quarter of underperformance makes recovery harder. Every lost customer becomes harder to win back. Every departed talent becomes impossible to replace. The company that once epitomized Indian entrepreneurial success now exemplifies its potential failures.

The story isn't over. Redemption remains possible. But it requires something harder than strategy or capital—it requires the Chhabria family to choose legacy over ego, shareholders over self, future over past. Whether they can make that choice will determine not just Finolex's fate, but serve as a beacon or warning for every family business in India.

The wires that once connected India now entangle their creators. The question is whether anyone has the courage to cut through them and set the company free.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube