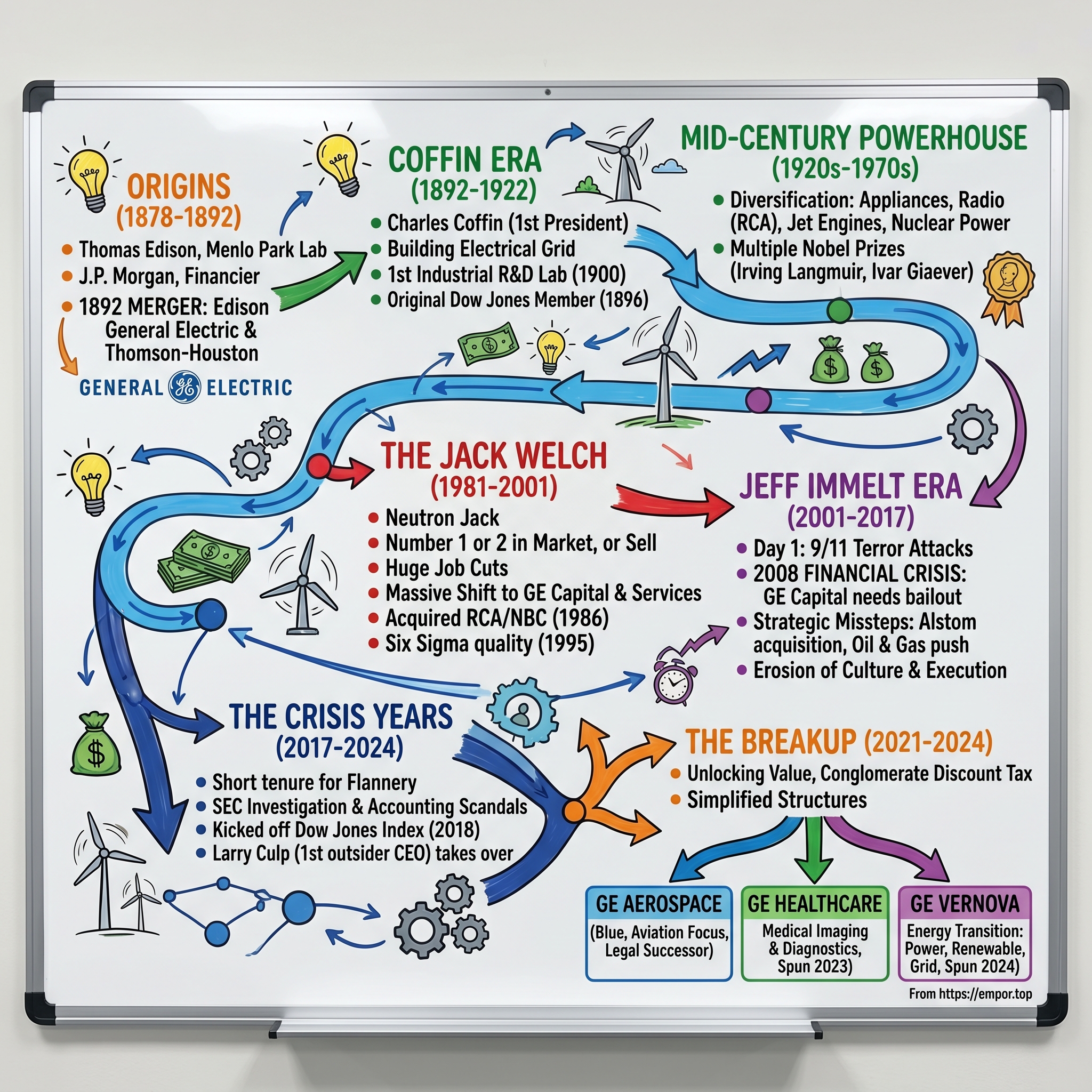

General Electric: The Rise and Fall of an American Icon

I. Introduction & Episode Roadmap

Picture this: It's April 2, 2024, and the trading floor at the New York Stock Exchange is buzzing with an unusual energy. After 132 years, General Electric—the company that literally illuminated America—is conducting its final act as a unified entity. The conglomerate that once employed over 300,000 people, powered cities, built jet engines, and even owned NBC, is splitting into three separate companies. The iconic GE monogram, virtually unchanged since 1892, would now represent only an aerospace company.

How did we get here? How did a company that was synonymous with American industrial might, that survived two world wars, the Great Depression, and countless economic cycles, ultimately decide its best path forward was to cease existing as we knew it?

The paradox of General Electric is striking: while its cursive logo remained almost untouched for over a century—a beacon of stability and trust—everything else about the company underwent radical transformation. From Thomas Edison's light bulbs to nuclear reactors, from television networks to subprime mortgages, GE's journey is really the story of American capitalism itself.

At its peak under Jack Welch in 2000, GE was worth over $600 billion, making it the most valuable company in the world. By 2018, it had lost 90% of that value. The company that had been one of the original twelve members of the Dow Jones Industrial Average in 1896—and the last remaining original member—was unceremoniously kicked out of the index.

This is a story of brilliant innovation and catastrophic miscalculation, of visionary leadership and destructive hubris. It's about how a company can be simultaneously too big to fail and too complex to succeed. Most importantly, it's about what happens when financial engineering replaces actual engineering, when quarterly earnings trump long-term value creation, and when a culture of excellence gives way to a culture of denial.

The breakup into GE Aerospace, GE HealthCare, and GE Vernova wasn't just a corporate restructuring—it was an admission that the conglomerate model that defined American business for much of the 20th century no longer worked in the 21st. Each piece of the old GE now trades separately, collectively worth more apart than they ever were together in recent years. The conglomerate discount had become a conglomerate tax.

As we trace GE's arc from Edison's workshop to today's three separate companies, we'll see how each era of leadership reflected the business zeitgeist of its time: Coffin's infrastructure building, Welch's financialization, Immelt's digital ambitions, and finally Culp's surgical dismantling. It's a masterclass in how competitive advantages erode, how complexity becomes a liability, and why even the mightiest institutions must eventually adapt or die.

What makes GE's story particularly compelling for investors is that it challenges our most basic assumptions about business success. If operational excellence (Six Sigma), visionary leadership (multiple "CEO of the Century" winners), massive scale, and technological innovation aren't enough to sustain a company, what is? The answer to that question might just redefine how we think about building enduring businesses in the modern era.

II. Origins: Edison, Thomson-Houston, and the Birth of GE (1878-1892)

The story begins not in a boardroom but in a laboratory thick with chemical fumes and littered with failed experiments. In the fall of 1878, Thomas Edison stood in his Menlo Park workshop, holding yet another burnt-out filament. He'd been at this for months—testing platinum, carbon, even human hair—searching for a material that could sustain an electric current long enough to create practical indoor lighting. Gas lamps flickered on the walls, a ironic reminder of what he was trying to replace.

Edison wasn't just inventing a light bulb; he was architecting an entire industry. At 31, he'd already revolutionized Wall Street with his improved stock ticker, earning enough credibility to attract serious capital. His friend Grosvenor Lowry, a well-connected lawyer, helped him establish the Edison Electric Light Company with $300,000 in backing from J.P. Morgan, the Vanderbilts, and other Gilded Age titans. This wasn't venture capital—this was the 1878 equivalent of Elon Musk getting backed by Warren Buffett and Bill Gates.

But here's what most people miss about the early electricity industry: Edison's direct current (DC) system was actually the wrong bet. While Edison was perfecting his incandescent bulb and building DC power stations that could only transmit electricity about a mile, a rival company in Lynn, Massachusetts was quietly developing something far more scalable.

The Thomson-Houston Electric Company, founded by Elihu Thomson and Edwin Houston, had focused on arc lighting—those brilliant, harsh lights that illuminated city streets. More importantly, they were working with alternating current (AC), which could transmit power over vast distances. Thomson, a former high school teacher, was the technical genius; Charles Coffin, a former shoe manufacturer from Lynn, was the business mind who understood that patents and scale, not just innovation, would determine the winner. The patent wars of the 1880s were vicious. By 1888, there were nearly 600 electric companies in America, all fighting over fundamental patents—from light bulb filaments to generator designs. Edison's team spent as much time in courtrooms as laboratories. Patent conflicts were stymieing the growth of both companies and the idea of saving on some 60 ongoing lawsuits was becoming a strategic imperative.

The financial pressure was immense. The market was in a general downturn causing cash shortages for all the companies concerned, and both Edison General Electric and Thomson-Houston were selling generating equipment below cost just to undercut each other. It was mutually assured destruction, 19th-century style.

Edison was becoming marginalized in his own company having lost majority control in the 1889 merger that formed Edison General Electric. The inventor who had started it all was increasingly sidelined as financiers took control. Henry Villard, Edison's main backer, thought he could dictate merger terms from a position of strength. He was wrong.

Enter J.P. Morgan, the ultimate power broker. In early 1892, Morgan's committee of financiers worked on what they saw as an inevitable consolidation. As a committee of financiers, which included J.P. Morgan, worked on the deal in early 1892, things went against Villard. In Morgan's view, Thomson-Houston looked on the books to be the stronger of the two companies and engineered a behind the scenes deal announced on April 15, 1892, that put the management of Thomson-Houston in control of the new company, now called General Electric (dropping Edison's name).

The cruelest detail? Thomas Edison was not aware of the deal until the day before it happened. The man whose name had been synonymous with electric light learned about the merger that would erase his name from the company masthead with less than 24 hours' notice. Edison put on a brave face publicly, noting how his stock had gained value, but privately he was devastated.

In 1892, Thomson-Houston was merged with the Edison General Electric Company of Schenectady, New York (arranged by John Pierpoint Morgan), to form the General Electric Company. The new entity instantly controlled three-quarters of America's electrical business. The fifteen electric companies that existed five years before had merged down to two: General Electric and Westinghouse.

Charles A. Coffin, the former shoe manufacturer who had led Thomson-Houston, became GE's first president. This was no accident—Coffin led the company and organized its finances, marketing, and sales operations, and by 1892, Thomson-Houston had grown to $10 million in sales with 4,000 employees. Coffin understood something Edison never fully grasped: in the industrial age, operational excellence and financial discipline mattered more than pure innovation.

Edison's relationship with his namesake company effectively ended here. He was appointed to the board but attended only one meeting. By 1894, he had sold all his shares, though he continued collecting royalties on his patents and occasionally consulted. The wizard of Menlo Park had been transformed from entrepreneur to employee to shareholder to, finally, just another vendor.

The merger created more than just a company—it established a template for American industrial consolidation that would define the next century. Scale, patents, and financial engineering would trump innovation. The age of the inventor-entrepreneur was ending; the age of the professional manager was beginning.

III. The Coffin Era: Building America's Electrical Infrastructure (1892-1922)

Charles Coffin didn't look like a titan of industry. Short, unassuming, with a neat mustache and the demeanor of a small-town banker, he had started his career making shoes in Lynn, Massachusetts. But when he walked into GE's boardroom in 1892, he brought something more valuable than Edison's genius or Morgan's money: he understood how to build an institution.

"The genius of Mr. Coffin," one contemporary observed, "was that he never tried to be a genius." Instead, he created systems that turned genius into products, products into profits, and profits into market dominance. Under his leadership from 1892 to 1922, GE would transform from a collection of feuding patents into the backbone of American electrification.

General Electric was formed through the 1892 merger of Edison General Electric Company and Thomson-Houston Electric Company with the support of Drexel, Morgan & Co. But a merger on paper was one thing; creating a unified company was another. Coffin's first masterstroke was keeping the talent. Rather than purging Edison's team, he convinced brilliant engineers like Charles Steinmetz—a hunchbacked German socialist who chain-smoked cigars and kept alligators as pets—to stay and innovate.

By 1900, GE wasn't just making light bulbs. The company manufactured the entire electrical ecosystem: massive generators for power plants, transmission equipment to carry electricity across states, industrial motors that powered factories, electric locomotives that moved freight, and yes, the bulbs that lit American homes. It was vertical integration before business schools had a term for it. But Coffin's most prescient decision came in 1900. General Electric Research Laboratory was the first industrial research facility in the United States. Established in 1900, the lab was home to the early technological breakthroughs of General Electric and created a research and development environment that set the standard for industrial innovation for years to come. Up to that point, research had been carried out in universities or in private laboratories similar to Edison's Menlo Park workshop. Coffin created something entirely new: corporate R&D.

Founded in 1900 by Thomas Edison, Willis R. Whitney, and Charles Steinmetz, this lab defined industrial research for years to come. The laboratory began in the most humble of circumstances—Carriage House in rear of 233 Liberty Street, Schenectady, which was used by Steinmetz as a laboratory. Steinmetz lived at 233 Liberty Street from 1897-1901. The carriage barn was used as the first home of the General Electric Research Laboratory from 1900 until 1901, when it burned. Yes, America's first industrial research lab started in a barn and promptly burned down. Silicon Valley's garage startup mythology had nothing on GE.

The real genius of the research lab wasn't just the science—it was the business model. The lab grew from 8 people to 102 people by 1906, which included scientifically trained researchers that made up 40% of the staff. Whitney believed in exploratory scientific research, with the goal of creating new commercial products. This dual focus on pure research and commercial application would become the template for every corporate R&D center that followed.

Meanwhile, GE was quietly building a monopoly through something more powerful than innovation: patent pooling. This merger of the Edison company, along with its lighting patents, and the Thomson-Houston, with its AC patents, created a company that controlled three quarters of the US electrical business. In 1896, GE and its only real competitor, Westinghouse Electric, entered into a patent pool agreement. Rather than continue their destructive competition, they agreed to share fundamental patents. It was collusion dressed up as cooperation.

The numbers tell the story of Coffin's success. When he took over in 1892, the combined companies had revenues of about $12 million. By 1900, revenues had grown to $28 million. By 1910, they exceeded $80 million. In 1886, the year of GE's establishment in Schenectady, approximately 13,000 people lived in the city. By 1900 the population had more than doubled to 30,000. "GE transformed Schenectady from a largely agricultural area to a top industrial manufacturer in the world."

GE also became a founding member of American capitalism's most exclusive club. The company was one of the original 12 companies listed on the newly created Dow Jones Industrial Average in 1896. Of those original dozen—which included companies like American Tobacco, Chicago Gas, and National Lead—GE would be the last survivor, maintaining its position for 122 years until its ignominious removal in 2018.

Under Coffin, GE didn't just manufacture products; it manufactured the future. The company built the generators for Niagara Falls, the world's first large-scale hydroelectric project. It electrified the New York Central Railroad. It lit the Panama Canal. Every major infrastructure project in America's rise to industrial supremacy had GE's fingerprints on it.

The research lab paid immediate dividends. In 1908, engineer and new head researcher William Coolidge invented the ductile tungsten light bulb filament, providing a more durable and long-lasting light filament than the existing technology. "The invention secured GE's technological leadership in the market and epitomized the role of the GE research lab — bringing innovation to the marketplace."

But perhaps Coffin's greatest achievement was cultural. He created what became known as the "GE Way"—a management philosophy that emphasized long-term thinking, employee development, and systematic innovation. He established profit-sharing plans, employee training programs, and a culture of promoting from within. When he stepped down as president in 1913 (remaining chairman until 1922), he had built not just a company but an institution.

The Coffin era proved that in the industrial age, the spoils went not to the inventor but to the organizer, not to the innovator but to the integrator. Edison had the vision, but Coffin built the machine. And that machine would dominate American industry for the next century.

IV. The Mid-Century Powerhouse: Innovation & Expansion (1920s-1970s)

On a foggy morning in November 1922, something extraordinary happened at WGY, GE's experimental radio station in Schenectady. An engineer flipped a switch, and for the first time in history, a dramatic program—"The Wolf," performed by actors in the studio—was broadcast to radios across the Northeast. GE had just invented the radio drama, and with it, the blueprint for electronic mass media.

This wasn't supposed to be GE's business. The company made turbines and transformers, not entertainment. But in the 1920s, GE's leadership saw something others missed: electricity wasn't just about power generation—it was about what that power enabled. Radio, and later television, would need transmitters, receivers, vacuum tubes, and countless other components. Why let someone else capture that value?

The formation of RCA (Radio Corporation of America) in 1919 showcased GE's evolving playbook. Rather than compete directly in consumer products, GE became the arms dealer, owning 30% of RCA and supplying its technology. When RCA's David Sarnoff pitched the idea of television in 1928, it was GE's labs that developed the iconoscope—the first practical TV camera tube. By controlling the intellectual property and manufacturing capability, GE could profit from every aspect of the electronic revolution without the messy business of selling to consumers. The scientific breakthroughs came in waves. Irving Langmuir was awarded the Nobel Prize in Chemistry in 1932 for his work in surface chemistry, becoming the first industrial scientist to win the prize. While at General Electric from 1909 to 1950, Langmuir advanced several fields of physics and chemistry, inventing the gas-filled incandescent lamp and the hydrogen welding technique. His gas-filled bulb revolutionized lighting—by 1928, GE held 96% of incandescent light sales in America.

Four decades later, history repeated itself. Ivar Giaever, a Norwegian-American physicist who shared the 1973 Nobel Prize in Physics with Leo Esaki and Brian Josephson. One half of the prize was awarded jointly to Giaever and Esaki "for their experimental discoveries regarding tunneling phenomena in semiconductors and superconductors, respectively". The work that led to Giaever's Nobel Prize was performed at General Electric in 1960. The story of how Giaever won his Nobel perfectly captures GE's culture: October 23, 1973 was a big day at the General Electric Research Laboratory in Niskayuna. Everyone and everything was ready to help celebrate the 100th birthday of physicist William D. Coolidge, the man who vastly improved the efficiency of X-ray machines and light bulbs... at 6 a.m. that morning, GE supervisor Milan Fiske got a phone call from a friend in Stockholm, Sweden, with some great news: The Nobel Prizes had just been announced and Ivar Giaever, a native of Norway and a GE employee for the previous two decades, had just been named the Nobel winner in physics. The Coolidge celebration had just been trumped.

But the real transformation of GE came during World War II. The company became America's arsenal of innovation. GE built the superchargers that allowed B-17 bombers to fly at high altitude. It developed radar systems that could spot U-boats in the Atlantic. Most significantly, it created America's first jet engine, reverse-engineering Frank Whittle's British design and improving it. By war's end, GE had established itself as indispensable to national defense—a position that would guarantee government contracts for decades. The nuclear age represented GE's ultimate bet on the future. In 1949, GE began designing and building nuclear reactors, with its pioneering reactor project leading to the first commercial nuclear power plant in the United States in 1958. GE's involvement in nuclear energy was part of a broader effort to diversify its product lines and capitalize on the growing demand for electricity, marking a significant milestone in the company's history.

While Westinghouse built the famous Shippingport reactor that opened in 1957, GE wasn't far behind. In 1955, the Atomic Power Equipment Department was established by GE. Two years later, in 1957, GE's first privately financed nuclear power reactor provided electricity for commercial use in Vallecitos, California. Additionally, in 1960, GE made and contributed to the Dresden Nuclear Power Station in Chicago. GE had bet on boiling water reactors (BWRs) rather than pressurized water reactors (PWRs), a technological choice that would define its nuclear business for decades.

The medical technology breakthrough came almost by accident. General Electric revolutionized the medical field in 1962 by introducing one of the first Computed Tomography (CT) scanners. This innovation provided a new, non-invasive way for doctors to see inside the human body, transforming diagnostic medicine. The CT scanner, developed by GE's medical systems division, became a critical tool in detecting and diagnosing diseases, showcasing GE's legacy of innovation in health technology.

By the 1970s, GE had become something unprecedented: a corporation that could credibly claim to touch every aspect of American life. Your alarm clock? GE. The power that ran it? Generated by GE turbines. The light you turned on? GE bulb. The TV you watched? Possibly made by RCA, owned by GE, and certainly using GE components. The jet that flew you to work? GE engines. The medical equipment that diagnosed your illness? GE scanners.

This wasn't just vertical integration or horizontal expansion—it was three-dimensional dominance. GE had positioned itself at every critical node of the industrial economy. The company employed over 400,000 people globally and had become, in many ways, more powerful than some governments. Its research lab had grown to employ thousands of scientists and had spun off entire new industries.

But beneath this success lay the seeds of future problems. The company had become so complex that no single person could understand all its businesses. The corporate structure that had once enabled efficient capital allocation was becoming a bureaucratic maze. And most dangerously, GE was beginning to believe its own mythology—that it could manage any business, enter any market, solve any problem through the sheer application of management science.

The stage was set for the Jack Welch era, when GE would transform from an industrial company that happened to have a finance arm into something far more dangerous: a financial company that happened to make things.

V. The Jack Welch Revolution: "Neutron Jack" Transforms GE (1981-2001)

The boardroom at GE's Fairfield, Connecticut headquarters was dead silent on December 19, 1980. Reg Jones, the outgoing CEO, had just announced his successor: Jack Welch, the youngest and most controversial of the three internal candidates. Several board members exchanged worried glances. Welch was brilliant, no doubt, but he was also volcanic, profane, and had once blown up a factory (literally—a plastics plant explosion early in his career). The chemical engineer from Salem, Massachusetts, with the thick Boston accent and no Ivy League pedigree, was about to take the helm of America's most prestigious corporation.

John Francis "Jack" Welch Jr. (born November 19, 1935) was chairman and CEO of General Electric between 1981 and 2001. In 1980, the year before Welch became CEO, GE recorded revenues of roughly $26.8 billion and in 2000, the year before he left, they were nearly $130 billion. During his tenure at GE, the company's value rose 4,000%.

Within months, Welch earned his nickname: "Neutron Jack"—like a neutron bomb, he eliminated people while leaving buildings standing. His first major speech to Wall Street analysts in December 1981 at the Pierre Hotel in New York set the tone: every GE business would be number one or number two in its market, or it would be fixed, sold, or closed. No exceptions. The era of sentimental attachment to underperforming businesses was over.

The carnage was swift and shocking. In his first five years, Welch eliminated 118,000 jobs—one in four GE employees. He sold off $10 billion in assets, including the housewares division that made GE toasters and irons, the very products that had made GE a household name. He shuttered 73 plants and facilities. Wall Street loved it; the communities that had depended on GE for generations were devastated. Schenectady, the company's birthplace, saw employment drop from 30,000 to 8,000.

But Welch wasn't just destroying—he was rebuilding GE in a radically different image. His insight, controversial then and even more so now, was that manufacturing was becoming commoditized. The real money was in services and finance. Why make a jet engine for a one-time profit when you could lease it and service it for thirty years? Why sell a CT scanner when you could finance it and make money on both the equipment and the loan?

GE Capital, which had been a small division helping customers finance GE equipment purchases, became Welch's weapon of choice. Under his leadership, it morphed into something unprecedented: an industrial company's finance arm that grew so large it essentially became a bank, eventually contributing up to 50% of GE's profits. GE Capital leveraged GE's AAA credit rating to borrow money cheaply and lend it out at higher rates. It moved into commercial real estate, credit cards, insurance—anything that could generate financial returns. The acquisition strategy was equally transformative. In 1986, General Electric acquired RCA Corporation for $6.4 billion, marking one of the largest mergers of its time. This acquisition not only brought RCA's NBC television network under GE's umbrella but also expanded GE's reach in the consumer electronics market. The merger allowed GE to integrate synergies from RCA's technological assets and brand, strengthening its position in media and broadcasting industries. Suddenly, GE wasn't just making the equipment that transmitted television signals—it was creating the content too.

But it wasn't until 1995 that Welch made his most controversial and influential decision: embracing Six Sigma. Many attribute Welch's success to the go-go business atmosphere of the 1980s, but it wasn't until 1995 that he embraced Six Sigma. After seeing the success he had in implementing Six Sigma quality controls, many companies followed General Electric's lead. The story of how this happened is pure Welch: he heard that AlliedSignal's Larry Bossidy, his former protégé, was getting incredible results with this Motorola-developed quality program. Welch's competitive instincts kicked in—if Bossidy could do it, GE could do it better.

It was in 1995 when General Electric's implementation of Six Sigma began. In 1995, CEO Jack Welch made a goal for GE to become a Six Sigma company within five years by adopting the "Six Sigma Quality" as a part of the company's culture. Welch adopted Motorola's Six Sigma quality program in late 1995.

The Six Sigma implementation at GE was unprecedented in its scope and intensity. GE required almost all employees to take a two week, 100-hour Six Sigma Training Program. Afterward, employees were asked to complete a project implementing those methodologies. This wasn't optional—Welch also asked for a commitment to their Six Sigma goals from both executives and the GE workforce, linking promotions and bonuses to improvement in quality. A Green Belt certification became a minimum requirement for promotion at GE and almost half of each area of bonuses depended on the successful implementation of Six Sigma projects.

The financial results were staggering. When Six Sigma was officially implemented at GE in 1996, there wasn't any money saved: the company invested $200 million, and only saw a cost savings of $170 million. This would change in 1997, when CEO Jack Welch made the choice to tie in leadership bonuses to Six Sigma results. It proved to work: that year, $400 million was invested in Six Sigma, with an overall savings incurred of $700 million. After five years of implementing Six Sigma, General Electric reported savings of $12 billion.

The cultural transformation was equally profound. Full-time, Master Black Belt Six Sigma professionals were required to train and mentor employees whose jobs were integral to key processes. After those employees were trained and mentored to become Black Belts as well, GE Black Belt teams carried out different Six Sigma projects within the company. The language of business at GE changed—suddenly everyone was talking about "defects per million opportunities" and "process variation."

Welch's leadership style was as distinctive as his strategies. He instituted "Work-Out" sessions—town hall meetings where employees could confront bosses about bureaucratic obstacles. He created the famous "vitality curve," ranking employees and firing the bottom 10% every year. He preached the gospel of "boundarylessness"—eliminating barriers between departments, between GE and its customers, between GE and its suppliers.

His management philosophy could be brutal. "Control your destiny, or someone else will"; "Be candid with everyone"; "Bureaucrats must be ridiculed and removed"; and "If we wait for the perfect answer, the world will pass us by." These weren't just slogans; they were marching orders that reshaped how 300,000 employees thought about their work.

By 2000, Welch's final full year as CEO, GE seemed invincible. The company's market capitalization reached $600 billion, making it the most valuable company in the world. GE Capital alone would have been one of America's largest financial institutions. The company was generating $130 billion in revenue and $12.7 billion in profit. Fortune magazine named Welch "Manager of the Century."

But beneath the triumph, fault lines were forming. GE Capital had grown so large that it represented nearly 50% of GE's profits, making the industrial giant increasingly dependent on financial markets. The focus on quarterly earnings had led to increasingly aggressive accounting practices—though always just within the letter of the law. The constant pressure to hit numbers led managers to engage in "earnings management," smoothing results to meet Wall Street expectations.

More fundamentally, Welch had transformed GE from a company that made things into a company that made money. The finance tail was wagging the industrial dog. When Welch retired in 2001 with a $420 million severance package—the largest in corporate history at the time—he left behind a company that looked invincible but was actually incredibly vulnerable. The next crisis would expose just how fragile the house that Jack built really was.

VI. The Jeff Immelt Era: Crisis, Transformation, and Decline (2001-2017)

Jeff Immelt's first day as CEO should have been a celebration. September 7, 2001, marked the beginning of a new era for GE. The handpicked successor to Jack Welch, Immelt was a 6'4" former Dartmouth football player with an easy smile and an engineer's mind. He'd run GE Medical Systems brilliantly, growing it from $3 billion to $12 billion in revenue. The board loved him. Welch had endorsed him. The future looked bright.

Four days later, two planes hit the World Trade Center.

He took the helm on Sept. 7, 2001, four days before 9/11. The impact of the terrorist attacks battered several of GE's businesses, causing shares to plunge 20%. GE's insurance business faced massive claims. Its aircraft leasing arm, GE Capital Aviation Services, watched in horror as global air travel collapsed. NBC's advertising revenue evaporated. Within weeks, GE's stock had fallen 30%. Immelt hadn't even unpacked his office, and he was already in crisis mode.

But 9/11 was just the appetizer for the feast of disasters that would define Immelt's tenure. The real catastrophe came seven years later. In 2008, as Lehman Brothers collapsed and credit markets froze, GE Capital—the crown jewel of the Welch era—nearly destroyed the entire company.

The numbers were terrifying. GE Capital rose to as much as 50% of earnings by 2007. When the financial crisis hit, At the height of the 2008 crisis, literally no one would lend to it in the overnight markets. GE Capital was only saved by an emergency injection of $12 billion from Warren Buffet and other investors.

The government bailout details were even more shocking. Ultimately, GE Capital got a whopping $139 billion bailout from the federal government. For a company that had prided itself on financial engineering excellence, this was the ultimate humiliation. 15, 2008, the day Lehman Brothers declared bankruptcy, Paulson says he was "startled" when Immelt came to his office and told him GE was finding it "very difficult" to sell short-term debt "for any term longer than overnight".

The dividend cut was perhaps the most painful moment. So for the first time in its history, GE had to slash its dividend payments, from 30 cents to 10 cents a share; a massive two-thirds reduction. In terms of total dollars going to shareholders, it was the biggest single dividend cut by an American company ever. For millions of retirees who had counted on GE's dividend as safe as a government bond, it was devastating. Immelt tried to pivot GE towards what he saw as the future: industrial internet, digital transformation, and clean energy. He created GE Digital, hired thousands of software engineers, and declared that GE would become a "top 10 software company." The reality was more sobering—GE was trying to compete with Silicon Valley while carrying the baggage of a 120-year-old industrial company.

The strategic missteps multiplied. The biggest came with the Alstom acquisition for $17 billion (approximately €12.4 billion) in 2015. At a price of $10.6 billion, this was GE's most expensive industrial acquisition ever. Immelt participated actively in mergers and acquisitions, purchasing Amersham PLC for $9.5 billion in 2004 and Alstom's power business for approximately €12.4 billion in 2015.

The timing couldn't have been worse. GE was doubling down on fossil fuel power generation just as renewable energy was taking off and natural gas prices were collapsing. "The completion of the Alstom power and grid acquisition is another significant step in GE's transformation," said Jeff Immelt, chairman and CEO, GE. Within two years, the power market had collapsed, and Alstom became an albatross. CEO John Flannery—who was intimately involved with the purchase as head of business development at the time—admitted as much in a CNBC interview, saying: We were looking at a high teens return. I'd say we're in a single-digit return. It's not an acceptable deal from a financial framework right now.

The oil and gas investments were equally disastrous. GE had spent billions building up its oil and gas business, only to be caught flat-footed by the 2014 oil price collapse. The company was forced to merge the business with Baker Hughes in a complex deal that essentially admitted defeat.

Perhaps most damaging was the erosion of GE's execution culture. Under Immelt, the company developed a reputation for missing earnings targets, something that would have been unthinkable under Welch. "Jeff assumed early on that this company is phenomenal at operational execution and will continue no matter what," says one executive who worked with him. The result was a company that couldn't deliver on its promises.

The financial engineering that had worked so well under Welch became increasingly desperate under Immelt. He spent $93 billion buying back stock, which isn't necessarily a bad idea, but he had an unfortunate knack for buying at high prices. GE spent only $7 billion of that $93 billion from 2008 through 2011, when the stock price was mostly in the teens; the company spent almost $80 billion buying back shares at prices over $30.

By the end of Immelt's tenure in 2017, the damage was catastrophic. During Immelt's tenure, GE's stock fell about 30%, wiping out over $150 billion in market value, which many analysts, investors and even fellow CEOs blame on Immelt's missteps. Yet GE was the worst-performing stock in the Dow during Immelt's 16-year reign.

The irony was cruel: Immelt had tried to transform GE from an industrial conglomerate dependent on finance into a focused industrial company. Instead, he left behind a company that was neither—too complex to manage, too indebted to invest, too damaged to inspire confidence. The man who wanted to be remembered as a transformational leader would instead be remembered as the CEO who broke General Electric.

VII. The Crisis Years: Flannery, Culp, and the Dismantling (2017-2024)

John Flannery lasted exactly 424 days as CEO of General Electric—the shortest tenure in the company's history. A 30-year GE veteran who had run GE Healthcare successfully, Flannery took the helm in August 2017 with a mandate to fix what Immelt had broken. His first investor meeting in November 2017 was supposed to reassure Wall Street. Instead, it triggered panic.

Standing before analysts at the New York Stock Exchange, Flannery delivered a presentation that was part confession, part autopsy. He admitted GE Power was in "deep declines." He acknowledged the company had been "paying a dividend in excess of our free cash flow for a number of years." He revealed $23 billion in losses that had been hidden in insurance contracts written decades earlier. Most shocking: he announced GE would cut its sacred dividend from 24 cents to 12 cents per share—only the second cut since the Great Depression.

The stock crashed 7% that day. Within months, it would lose another 50% of its value.

Immelt's successor, John Flannery, lasted just 14 months as chief executive before he too was pushed out. The board had lost confidence. In desperation, they turned to an outsider for the first time in GE's history: Larry Culp.

Culp, a former chief executive of Danaher Corp., replaced him more than two years ago at Boston-based GE. His arrival in October 2018 marked a watershed moment. For 126 years, GE had promoted from within, believing that only someone steeped in the GE way could run the company. Now they were admitting that the GE way was part of the problem.

The new CEO inherited a nightmare. GE's market value had fallen to $63 billion—roughly 10% of its peak under Welch. The company was burning through cash, its credit rating was in jeopardy, and its accounting was under investigation by the SEC and Department of Justice. The accounting scandals were perhaps the most damaging blow to GE's reputation. GE agreed Wednesday evening to pay a $200 million penalty to settle the regulatory agency's investigations, which began about three years ago. These "disclosure failures" between 2015 and 2017 meant investors were blindsided when those businesses eventually stumbled badly, regulators said. The SEC found that GE misled investors by describing its GE Power profits without explaining that one-quarter of profits in 2016 and nearly half in the first three quarters of 2017 stemmed from reductions in its prior cost estimates.

The symbolic nadir came on June 26, 2018. On June 26, 2018, General Electric was removed from the Dow Jones Industrial Average after being one of the original members for over a century. This decision reflected GE's diminished influence in the American industrial landscape as the company struggled with declining revenues and restructuring challenges. The removal marked a symbolic shift in the U.S. economy towards tech-driven companies and underscored the difficulties GE faced in adapting to new market dynamics.

The company that had been a founding member of the Dow in 1896, that had survived the Great Depression and two world wars, was now deemed too insignificant to remain in America's most famous stock index. It was replaced by Walgreens, a drugstore chain.

Culp's approach was radical by GE standards: complete transparency about the problems, no sugar-coating, no promises he couldn't keep. He discovered that GE's problems went even deeper than anyone realized. The Power business was hemorrhaging cash. The insurance liabilities were worse than disclosed. The culture was broken—layers of bureaucracy, no accountability, and a pervasive belief that someone else would fix the problems.

His solution was equally radical: break up the company. On November 9, 2021, General Electric announced its plan to split into three distinct companies, focusing on aviation, healthcare, and energy. This strategic move aimed to simplify GE's structure and allocate resources more efficiently, allowing each segment to focus on its industry-specific growth opportunities. The split was part of a broader effort to revive GE's fortunes and enhance shareholder value following years of financial difficulties and strategic missteps.

The logic was compelling. Each business faced different challenges, served different customers, and required different strategies. Aviation was strong but held back by association with Power's problems. Healthcare was growing but couldn't get the investment it needed because cash was being diverted to prop up struggling divisions. The conglomerate structure that had once been GE's greatest strength had become its greatest weakness.

But executing the breakup was extraordinarily complex. GE had to untangle shared services, separate IT systems, divide pension obligations, and allocate debt. Each new company needed its own management team, board of directors, and corporate infrastructure. The process would take years and cost billions.

The dismantling of General Electric wasn't just a corporate restructuring—it was an admission that the entire premise of the industrial conglomerate, the idea that had defined American business for a century, no longer worked in the modern economy.

VIII. The Three-Way Split: GE Aerospace, GE HealthCare, GE Vernova

The boardroom at GE's Boston headquarters was silent as Larry Culp laid out the final details on November 9, 2021. After 129 years as one company, General Electric would cease to exist. The board members, some of whom had served for decades, understood they were presiding over the end of an era. One director later described it as "like attending your own funeral."

The math was brutally simple: GE's stock was trading at a conglomerate discount of roughly 30-40%. The three businesses inside GE were worth substantially more apart than together. Wall Street no longer believed that the synergies of a conglomerate outweighed the complexity. The "GE Store"—the vaunted system of sharing technology and best practices across divisions—had become the "GE Tax."

The first spin-off of GE HealthCare was finalized on January 4, 2023; GE continues to hold 10.24% of shares and intends to sell the remaining over time. The healthcare business, with $18 billion in revenue, emerged as a standalone company focused on medical imaging, ultrasound, patient monitoring, and diagnostics. Free from the drag of GE's other problems, it could now compete directly with Siemens Healthineers and Philips without the stigma of association with GE Power's failures.

This was followed by the spin-off of GE's portfolio of energy businesses, which became GE Vernova on April 2, 2024. Vernova—a portmanteau of "verde" (green) and "nova" (new)—combined GE's renewable energy, power generation, and grid businesses. With approximately $33 billion in revenue, it instantly became one of the world's largest energy companies, though it inherited significant challenges, particularly in offshore wind where GE had lost billions.

Following these transactions, GE became an aviation-focused company; GE Aerospace is the legal successor of the original GE. This was perhaps the most telling decision. Of all GE's businesses, aviation was the crown jewel—high margins, strong competitive position, decades-long customer relationships. The fact that this was the business GE chose to keep, to BE, said everything about where the value really lay. The market's verdict on the breakup has been decisive. Since the split was completed, the three companies have collectively outperformed the old GE by a significant margin. GE Aerospace, benefiting from the aerospace boom and its dominant position in jet engines, has seen its stock surge. GE HealthCare has found its footing as a pure-play medical technology company. GE Vernova, despite inheriting the troubled power business, has positioned itself for the energy transition.

Each company now operates with clarity of purpose that was impossible under the conglomerate structure. GE Aerospace can focus exclusively on the aviation market, where it holds a duopoly with Rolls-Royce in wide-body engines and partners with Safran in the hugely successful CFM joint venture. The LEAP engine program alone has a backlog worth hundreds of billions of dollars.

GE HealthCare, freed from the capital constraints of the conglomerate, can invest in AI-powered diagnostics and precision medicine without competing for resources with turbines and jet engines. The company is positioning itself to compete directly with Siemens Healthineers and Philips in the rapidly evolving healthcare technology market.

GE Vernova faces the biggest challenges but also perhaps the greatest opportunities. As the world transitions to renewable energy, Vernova's combination of traditional power generation, renewable energy, and grid technology positions it uniquely. The company is betting heavily on offshore wind despite current losses, believing the market will eventually turn profitable.

The financial engineering required to execute the split was staggering. GE had to allocate $70 billion in debt among the three companies, divide pension obligations of over $40 billion, separate IT systems that had been integrated for decades, and create three distinct corporate cultures from one. Each company needed its own board, management team, and strategic direction.

For shareholders, the split has been complex but generally positive. Holders of GE common stock were entitled to receive one share of GE Vernova common stock for every four shares of GE common stock held. The distribution was structured to be tax-efficient for U.S. shareholders. Early results suggest the market values the focused companies more highly than the conglomerate.

The leadership of each company reflects their distinct challenges. Larry Culp remains CEO of GE Aerospace, leveraging his operational expertise in the company's strongest business. Peter Arduini, formerly of Integra LifeSciences, leads GE HealthCare with a mandate to accelerate innovation. Scott Strazik, a GE veteran who ran the combined energy businesses, leads Vernova through the energy transition.

But perhaps the most telling aspect of the breakup is what it says about the evolution of business strategy. The conglomerate model that defined American capitalism for much of the 20th century—the idea that good management could run any business, that diversification reduced risk, that scale always won—has been thoroughly discredited. In its place: focus, agility, and specialization.

The three companies that emerged from GE's breakup are, in many ways, a rejection of everything the old GE represented. They are smaller, simpler, and more focused. They can no longer cross-subsidize struggling divisions with profits from strong ones. They must succeed or fail on their own merits. In breaking apart, they may have found the freedom to succeed that eluded them as parts of a dying giant.

IX. Playbook: Business & Investing Lessons

The Dangers of Financialization and Complexity

GE's transformation from industrial powerhouse to financial engineering firm offers a masterclass in how financialization can destroy even the strongest companies. Under Jack Welch, GE Capital grew to contribute 50% of the company's profits by 2007. This wasn't just diversification—it was a fundamental identity shift. GE had discovered it was easier to make money lending money than making things.

The seduction was understandable. Manufacturing jet engines required billions in R&D, decades of development, and enormous capital investment for single-digit margins. GE Capital could borrow at 2%, lend at 6%, and generate 20% returns on equity with a few keystrokes. Why build when you could bankroll?

But this financial engineering created fatal vulnerabilities. When credit markets froze in 2008, GE Capital nearly destroyed the entire company. The business that had seemed like free money became an existential threat. Warren Buffett's emergency investment came with a 10% dividend—loan shark rates for a company that had once been America's most valuable.

The complexity that grew from this financialization was equally destructive. By 2017, GE's 10-K filing ran over 200 pages, and even sophisticated investors couldn't understand how the company really made money. The infamous "GE Store"—the idea that divisions shared technology and best practices—became a euphemism for opaque internal transactions that obscured individual business performance.

Conglomerate Discount vs. Focused Excellence

The market's judgment on conglomerates has been brutal and consistent: they trade at a discount to the sum of their parts. GE's breakup unlocked immediate value—the three separate companies are worth substantially more than the unified entity. This isn't just about GE; it's a broader repudiation of the conglomerate model.

The theoretical benefits of conglomerates—diversification, capital allocation efficiency, shared resources—have been overwhelmed by their drawbacks. Investors can diversify more efficiently themselves. Capital markets can allocate resources better than corporate headquarters. And the supposed synergies rarely materialize while the complexity costs are immediate and real.

Focused companies win because they can move faster, think clearer, and execute better. GE Aerospace doesn't have to explain why it's investing in next-generation engines while GE Power is laying off thousands. Each business can have its own strategy, culture, and capital structure optimized for its specific market.

The Importance of Timing and Market Cycles

GE's history is littered with brilliant strategies executed at exactly the wrong time. The Alstom acquisition in 2015—buying fossil fuel power generation assets just as renewable energy was taking off. The expansion of GE Capital in the 2000s—just before the financial crisis. The push into oil and gas—right before the 2014 price collapse.

These weren't necessarily bad ideas, but timing in business isn't just important—it's everything. The difference between genius and folly often comes down to when you act, not what you do. Immelt's digital industrial vision might have been right, but executing it while managing a crisis-ridden conglomerate was impossible.

Culture as Competitive Advantage

The deterioration of GE's culture from Welch to Immelt to the crisis years shows how culture, once broken, is nearly impossible to repair. Under Welch, despite his brutal methods, there was clarity: perform or perish. Under Immelt, the culture became one of happy talk and missed numbers. By the Flannery era, it was every division for itself.

Culture isn't soft stuff—it's what determines whether people tell the truth about problems, whether they take ownership of failures, whether they push for excellence or settle for good enough. GE's culture of "success theater"—where everyone pretended things were fine while the company burned—was more destructive than any competitive threat.

Capital Allocation: The CEO's Most Important Job

Warren Buffett says capital allocation is a CEO's most important job, and GE proves it. The company spent $93 billion on buybacks, mostly at peak prices. It paid dividends it couldn't afford, borrowing money to maintain the illusion of stability. It made acquisitions at the top of cycles and sold assets at the bottom.

Good capital allocation isn't about complex financial engineering—it's about discipline, patience, and understanding value. It's about saying no to bad deals even when everyone else is saying yes. It's about returning cash to shareholders when you don't have better uses for it, and keeping it when you do.

Why "Management Quality" Isn't Enough

GE had some of the most celebrated managers in business history. Jack Welch was literally named "Manager of the Century." Jeff Immelt was on every CEO council and advisory board. These were smart, dedicated, hardworking executives. And they still destroyed enormous value.

Management quality matters, but it's not sufficient. You need the right strategy, the right structure, and the right market conditions. The best captain in the world can't save a ship that's fundamentally unseaworthy. GE's structure—a massive conglomerate with a huge finance arm—was obsolete regardless of who ran it.

The Innovator's Dilemma at Massive Scale

GE faced the innovator's dilemma not in one business but across dozens simultaneously. In power generation, renewable energy was disrupting gas turbines. In medical imaging, AI was changing diagnostics. In aviation, new materials were revolutionizing engine design. How do you disrupt yourself when you're defending multiple franchises?

The answer, ultimately, was that you can't. The antibodies in a large organization are too strong. The existing businesses have too much political power. The quarterly earnings pressure is too intense. Innovation requires focus, and focus requires choice, and choice was what the conglomerate structure made impossible.

Lessons from Six Sigma: When Operational Excellence Isn't Enough

GE's Six Sigma implementation was legendary—$12 billion in savings, a complete transformation of how the company operated. But it also created a culture of incremental improvement when what was needed was radical change. You can't Six Sigma your way out of a structurally declining business.

Operational excellence is necessary but not sufficient. It can make you better at what you do, but it can't tell you what you should be doing. GE became incredibly efficient at running businesses that shouldn't have existed in their current form. They optimized the wrong things.

The playbook, then, is clear: Focus beats diversification. Simplicity beats complexity. Strategy beats operational excellence. Culture beats process. And timing beats everything. These aren't new lessons, but GE's spectacular rise and fall provides perhaps the most expensive validation of these principles in business history.

X. Analysis & Bear vs. Bull Case

What Really Killed GE: Structural Issues vs. Management Failures

The autopsy of General Electric reveals multiple causes of death, but the primary culprit was structural obsolescence, not management incompetence. The conglomerate model that had been GE's greatest strength became an inoperable cancer. No amount of management brilliance could have saved a structure that the market had decided was fundamentally flawed.

The evidence is compelling: every major conglomerate has either broken up (ITT, AT&T), dramatically simplified (United Technologies becoming Raytheon), or struggled with similar issues (Siemens trading at persistent discounts). The market's verdict is unanimous: in an age of specialization and transparency, conglomerates destroy value.

That said, management failures accelerated the decline. Immelt's expansion of GE Capital before the financial crisis, the Alstom acquisition at the peak of the fossil fuel era, the attempt to build a digital industrial platform while the core businesses were struggling—these were unforced errors. Better timing, better capital allocation, and more honest communication might have bought time for a more orderly restructuring.

But ultimately, GE was trying to solve a 21st-century problem with a 19th-century structure. The company was organized for an era of scarce capital, limited information, and stable markets. In a world of abundant capital, instant information, and constant disruption, the conglomerate model was as obsolete as the steam engines GE once built.

Could the Conglomerate Model Have Survived?

The contrarian case for conglomerates still has adherents. Berkshire Hathaway, after all, is essentially a conglomerate and has created enormous value. The difference is that Berkshire is a capital allocator first and an operator second. It buys good businesses and leaves them alone. GE tried to actively manage dozens of complex industrial businesses from corporate headquarters.

A different path was theoretically possible. GE could have become a holding company, giving each business true independence while providing patient capital. It could have focused on a narrower set of related businesses where real synergies existed. It could have spun off GE Capital earlier, avoiding the near-death experience of 2008.

But these counterfactuals ignore market reality. Investors in 2024 want pure plays. They want to choose their own diversification. They want transparency and simplicity. Even if GE had executed perfectly, it would still trade at a discount to focused competitors. The model itself, not just the execution, was the problem.

Comparison to Other Industrial Giants

Looking at GE's peers provides crucial context. Siemens, the closest European equivalent, has faced similar pressures and is undergoing its own simplification, spinning off Siemens Energy and Siemens Healthineers. The German giant trades at a significant discount to its sum-of-parts value despite better execution than GE.

United Technologies chose radical surgery, merging with Raytheon to create a focused aerospace and defense company while spinning off Otis (elevators) and Carrier (HVAC). The result: all three companies have outperformed the former conglomerate.

Honeywell, still maintaining a semi-conglomerate structure, trades at a discount despite strong operational performance. Activist investors continuously pressure it to break up, arguing the pieces would be worth more separately.

The lesson is clear: the market has decided conglomerates are obsolete. Companies can fight this reality or accept it. GE fought it for too long, destroying enormous value in the process.

The Future of American Manufacturing

GE's breakup represents more than just one company's restructuring—it signals the end of an era in American manufacturing. The idea that scale and scope were sustainable competitive advantages has been thoroughly debunked. In its place: focus, innovation, and agility.

The future belongs to companies that do one thing exceptionally well, not many things adequately. Tesla doesn't make washing machines. Apple doesn't run a finance company. Amazon Web Services doesn't build jet engines (though Amazon does seemingly everything else). The winners are ruthlessly focused on their core competencies.

This has profound implications for American competitiveness. The U.S. can't compete with China on scale or cost in traditional manufacturing. But it can win through innovation, specialization, and higher-value products. GE Aerospace's dominance in jet engines shows this model works. The question is whether enough American manufacturers can make this transition.

Each Successor Company's Competitive Position

GE Aerospace enters independence in the strongest position. It has a duopoly in wide-body engines, a massive installed base generating recurring service revenue, and decades-long customer relationships. The aerospace cycle is in a strong upturn, with record order backlogs. The main risk is execution—can they ramp production to meet demand while maintaining quality?

GE HealthCare faces intense competition but has strong positions in medical imaging and diagnostics. The shift to value-based care and AI-powered diagnostics plays to its strengths. The challenge is innovation speed—competing with both traditional rivals like Siemens and new entrants using AI and software to disrupt traditional hardware businesses.

GE Vernova has the toughest road. The power generation business faces structural decline as utilities shift to renewables. The renewable energy business, particularly offshore wind, is currently losing money. But the energy transition represents a massive opportunity if Vernova can position itself correctly. The company is betting that its combination of traditional and renewable energy assets will be valuable during the decades-long transition.

Was the Breakup Value-Creating or Value-Destroying?

The market's verdict is clear: the breakup created significant value. The three separate companies are worth approximately 50% more than the pre-breakup GE, even accounting for the costs of separation. This isn't just multiple expansion—it's a recognition that focused companies can create more value than conglomerates.

But there's a deeper question: could this value have been created earlier with less destruction along the way? If GE had broken up in 2010, or 2000, or even 1995, how much value could have been preserved? The hundreds of billions lost during the decline weren't inevitable—they were the cost of clinging to an obsolete model.

The Bear Case

The pessimistic view is that GE's breakup is simply rearranging deck chairs. The fundamental challenges facing each business—aerospace's cyclicality, healthcare's reimbursement pressures, power's structural decline—remain unchanged. Separate companies might make these challenges more visible, but they don't solve them.

Moreover, the three companies lose whatever synergies actually existed. GE Research's innovations won't flow as freely between companies. Procurement scale advantages disappear. The ability to offset weak businesses with strong ones is gone. Each company now faces the market alone, without the cushion of diversification.

The timing could hardly be worse. We're potentially heading into a global recession, aerospace may be peaking, healthcare faces regulatory pressure, and the energy transition is proving more difficult and expensive than expected. The three companies might have been stronger together facing these headwinds.

The Bull Case

The optimistic view is that focus and accountability will drive performance improvement that was impossible under the conglomerate structure. Each management team can now make decisions optimized for their specific business without corporate interference or capital competition.

The market clearly prefers pure plays, and each company can now access capital markets on its own merits. GE Aerospace can command aerospace multiples. GE HealthCare can be valued like a medical technology company. GE Vernova can attract ESG-focused investors interested in the energy transition.

Most importantly, the breakup enables cultural transformation. Each company can build its own identity, attract talent suited to its industry, and create incentives aligned with its specific goals. The deadweight of corporate bureaucracy is gone. The confusion of competing priorities is resolved. For the first time in decades, everyone knows what business they're in and what success looks like.

The bull case, ultimately, is that the breakup didn't destroy a great company—it liberated three good companies from a failed structure. The value was always there; it was just trapped in a conglomerate that no longer made sense.

XI. Epilogue & Reflections

Standing in the Museum of Innovation and Science in Schenectady, you can still see it: the original GE logo from 1892, its graceful cursive letters virtually identical to the mark that adorns GE Aerospace planes today. In a glass case nearby sits one of Edison's original light bulbs, its filament still intact after more than a century. These artifacts feel less like museum pieces and more like archaeological evidence of a lost civilization.

General Electric's story is, in many ways, the story of American capitalism's evolution. Born in the age of robber barons and trusts, it thrived through the era of professional management, dominated during the age of conglomerates, and finally succumbed to the age of disruption. Each transformation of GE reflected a broader transformation in how Americans thought about business, value, and success.

The shift from building infrastructure to financial engineering wasn't unique to GE—it happened across corporate America. In 1950, finance represented 10% of U.S. corporate profits; by 2008, it was 40%. GE just took this trend to its logical extreme, becoming a hedge fund that happened to make jet engines. When the music stopped in 2008, GE was left without a chair.

What would Edison think of what became of his company? The inventor who famously said "genius is 1% inspiration and 99% perspiration" might be puzzled by a company that tried to finesse its way to greatness through financial engineering. Edison was famously litigious and aggressive about patents, but he was ultimately a builder, not a banker. He wanted to light the world, not leverage it.

Yet in another sense, the breakup represents a return to Edison's vision. Each of the three companies is now focused on solving specific problems: GE Aerospace on safer, more efficient flight; GE HealthCare on better medical outcomes; GE Vernova on the energy transition. They're back to building things that matter, freed from the distraction of managing a financial empire.

The end of the conglomerate era isn't just about GE—it's about a fundamental shift in how value is created in the modern economy. The industrial age rewarded scale and scope. The information age rewards focus and innovation. The companies that will define the next century won't be vast, all-encompassing enterprises but focused specialists that do one thing better than anyone else.

There's a temptation to see GE's story as a tragedy, and in human terms, it was. Hundreds of thousands of jobs lost, communities devastated, retirements destroyed. The city of Schenectady, once "the city that lights the world," is now struggling to reinvent itself after GE's departure. These costs can't be minimized or forgotten.

But there's also something liberating about GE's breakup. For decades, the company was trapped by its own history, unable to change because of what it had been. Every decision was weighted with 130 years of precedent. Every strategy had to account for dozens of different businesses. The complexity had become crushing.

Now, freed from that burden, each company can write its own story. GE Aerospace doesn't have to apologize for power turbine failures. GE HealthCare doesn't have to subsidize renewable energy losses. GE Vernova doesn't have to meet quarterly targets designed for industrial businesses. They can each be what they are, not what history demands they should be.

The most profound lesson from GE's rise and fall might be about the danger of mistaking the permanent for the temporary. GE seemed permanent—it had survived everything America could throw at it for 130 years. But nothing is permanent in business. Not business models, not competitive advantages, not even the most successful companies.

Jeff Immelt once said, "Every job looks easy when you're not the one doing it." The same might be said of running a conglomerate in the 21st century. It looked easy when Jack Welch was generating 20% annual returns. It looked manageable when the economy was growing and credit was flowing. But when the tide went out, we discovered GE had been swimming naked.

The final irony is that in breaking up, GE might have saved itself. Not the corporate entity—that's gone forever. But the businesses, the innovations, the capabilities that made GE matter—these survive in the three new companies. The patients who get better diagnoses from GE HealthCare scanners don't care about conglomerate structures. The passengers who fly safely on GE Aerospace engines don't think about corporate history. The communities powered by GE Vernova turbines just want the lights to stay on.

Perhaps that's the real legacy of General Electric: not the corporate structure or the management theories or the financial engineering, but the actual things the company built that improved human life. Edison wanted to light the world, and he did. That his company couldn't sustain itself as a unified entity doesn't diminish that achievement.

In the end, GE's story is a reminder that in business, as in life, nothing lasts forever—and that's okay. Companies, like organisms, are born, grow, mature, and eventually transform into something else. The three companies that emerged from GE's chrysalis might accomplish things the conglomerate never could have. Sometimes, breaking apart is the only way forward.

The GE monogram will live on at GE Aerospace, still recognizable as the logo Edison approved over a century ago. But it now represents something different: not an empire but an enterprise, not a conglomerate but a company, not the past but the future. And maybe, after all the financial engineering and corporate drama, getting back to building things that matter is exactly where GE needed to end up.

RSS Feed

RSS Feed Spotify

Spotify Apple Podcasts

Apple Podcasts Amazon Music

Amazon Music Audible

Audible YouTube

YouTube